Embed Size (px)

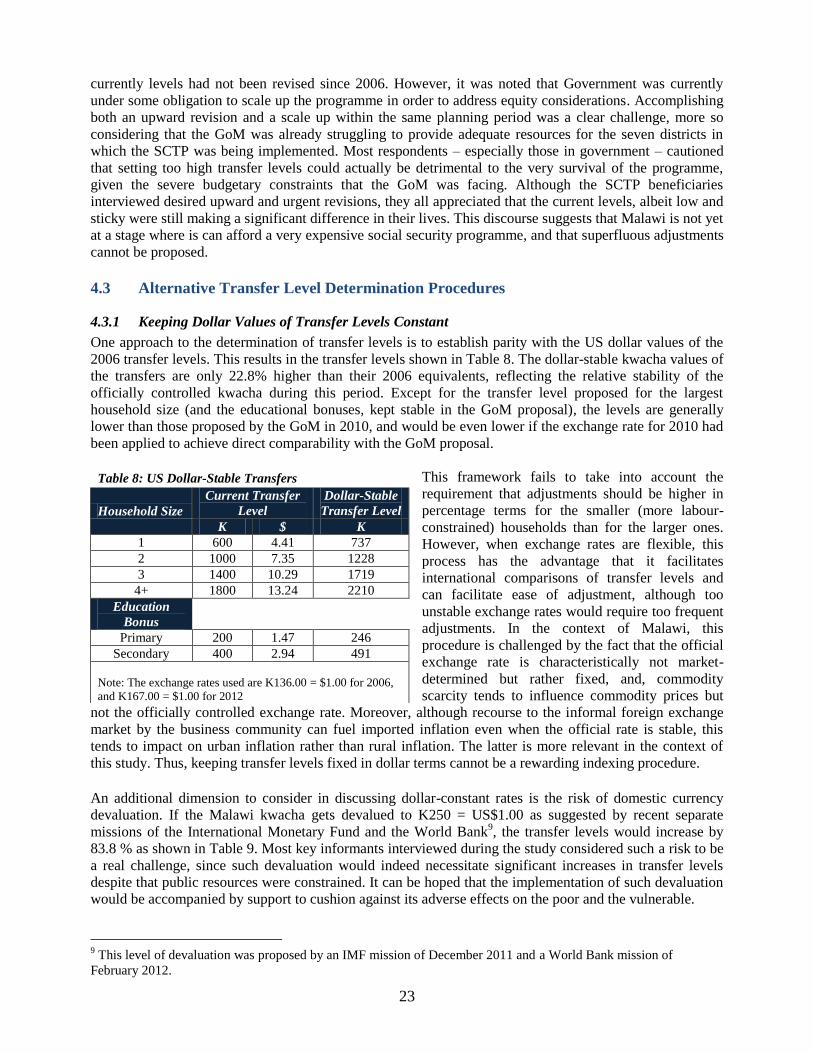

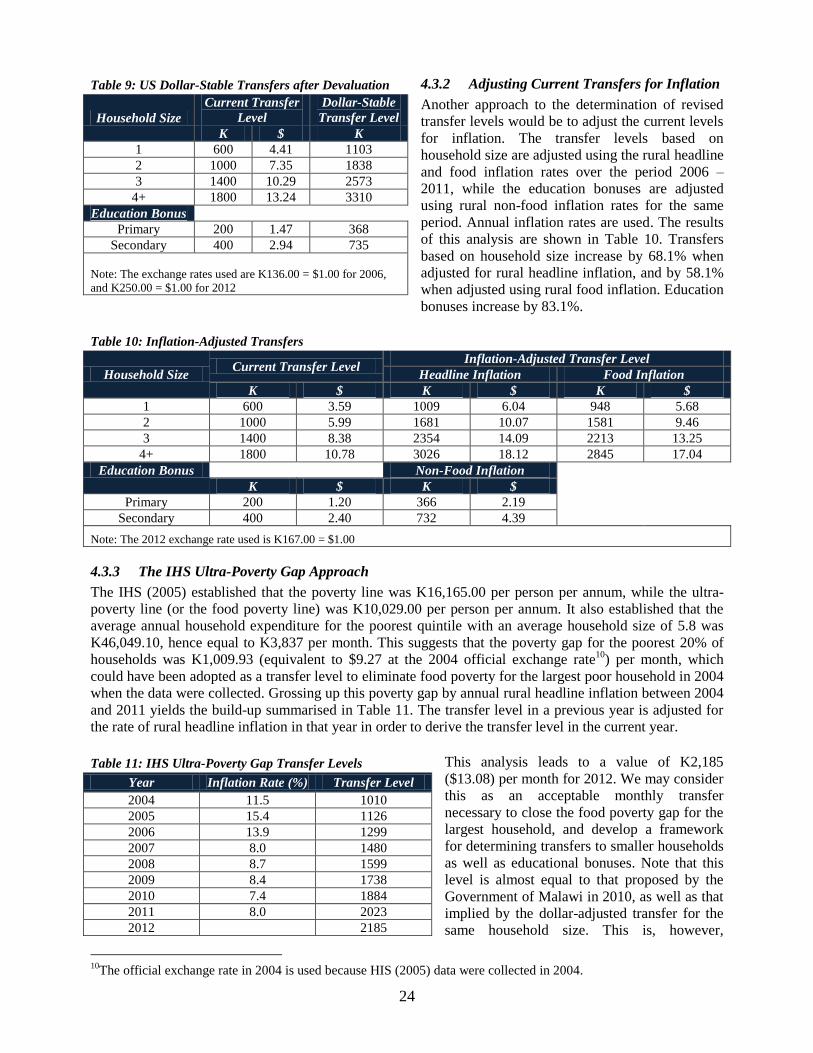

Citation preview

`

Costing and Analysis of Transfer Levels for

The Malawi Social Cash Transfer Programme

Ronald Mangani

Robert White

April 2012

Acknowledgements

This study was conducted for the Government of Malawi with financial support from UNICEF Malawi.

The authors sincerely appreciate the close guidance and support provided by Harry Mwamlima (Director,

Division of Poverty Reduction and Social Protection, in the Ministry of Economic Planning and

Development) and Maki Kato, Chief of Social Police at UNICEF Malawi. The technical guidance provided

by staff of the Division (especially Tom Mtenje and Imran Nedi) as well as staff at UNICEF Malawi

(especially Sophie Shawa and Tayllor Renee Spadafora) is gratefully acknowledged.

The authors would like to extend their thanks to all individuals and organisations consulted during the

course of the study. A full list of the people consulted is provided in Annexes to the report.

The views expressed in this report are those of the authors and do not necessarily represent the views of the

Government of Malawi or UNICEF Malawi

1

Acronyms and Abbreviations

AIDS - Acquired Immuno Deficiency Syndrome

CCT - Conditional Cash Transfers

CRC - Convention on the Rights of the Child

CSSC - Community Social Support Committee

EU - European Union

FGD - Focus Group Discussions

FISP - Farm Input Subsidy Programme

GDP - Gross Domestic Product

GMI - Guaranteed Minimum Income

GoM - Government of Malawi

HIV - Human Immune Virus

IHS - Integrated Household Survey

K - Malawi kwacha

KII - Key Informant Interviews

KfW - Kreditanstalt für Wiederaufbau (Reconstruction Credit Institute of Germany)

MASAF - Malawi Social Action Fund

MDG - Millennium Development Goals

MGDS - Malawi Growth and Development Strategy

MK - Malawi Kwacha

MPVA - Malawi Poverty and Vulnerability Assessment

NAC - National AIDS Commission

NSNP - National Safety Net Programme

NSSP - National Social Support Programme

PN - Perceived Needs

PPP - Purchasing Power Parity

PRSP - Poverty Reduction Strategy Paper

PWP - Public Works Programme

SB - Subsistence Basket

SCT - Social Cash Transfer

SCTP - Social Cash Transfer Programme

$ - United States dollar

UNICEF - United Nations Children Education Fund

USD - United States Dollars

WFP - World Food Programme

WMS - Welfare Monitoring Survey

2

Contents

Acknowledgements ..............................................................................................................................

Acronyms and Abbreviations ............................................................................................................. 1

Contents .............................................................................................................................................. 2

Executive Summary ........................................................................................................................... 4

1. Introduction ................................................................................................................................ 7

1.1 Background ...................................................................................................................... 7

1.2 Purpose and Scope of the Study....................................................................................... 8

1.3 Methodologies.................................................................................................................. 8

1.4 Study Limitations ............................................................................................................. 9

1.5 Organisation of the Report ............................................................................................... 9

2. A Contextual Background of the Malawi SCTP ...................................................................... 10

2.1 Poverty and Vulnerabilities in Malawi .......................................................................... 10

2.2 Consequences and Impacts of Poverty .......................................................................... 11

2.3 Interventions and Intervention Linkages ....................................................................... 11

2.4 The Policy and Regulatory Environment ....................................................................... 12

3. National Poverty Profile and SCTP Beneficiary Targeting ..................................................... 14

3.1 Measures of Poverty in Malawi ..................................................................................... 14

3.2 Beneficiary Targeting in the SCTP ................................................................................ 15

3.3 Determination of Target Beneficiary Households ......................................................... 16

4. Determination of Cash Transfer Levels ................................................................................... 19

4.1 The Literature................................................................................................................. 19

4.2 Appraisal of the determination of the current SCTP transfer levels .............................. 20

4.3 Alternative Transfer Level Determination Procedures .................................................. 23

4.4 Comparisons and Propositions ....................................................................................... 27

4.5 Revision of Transfer Levels ........................................................................................... 30

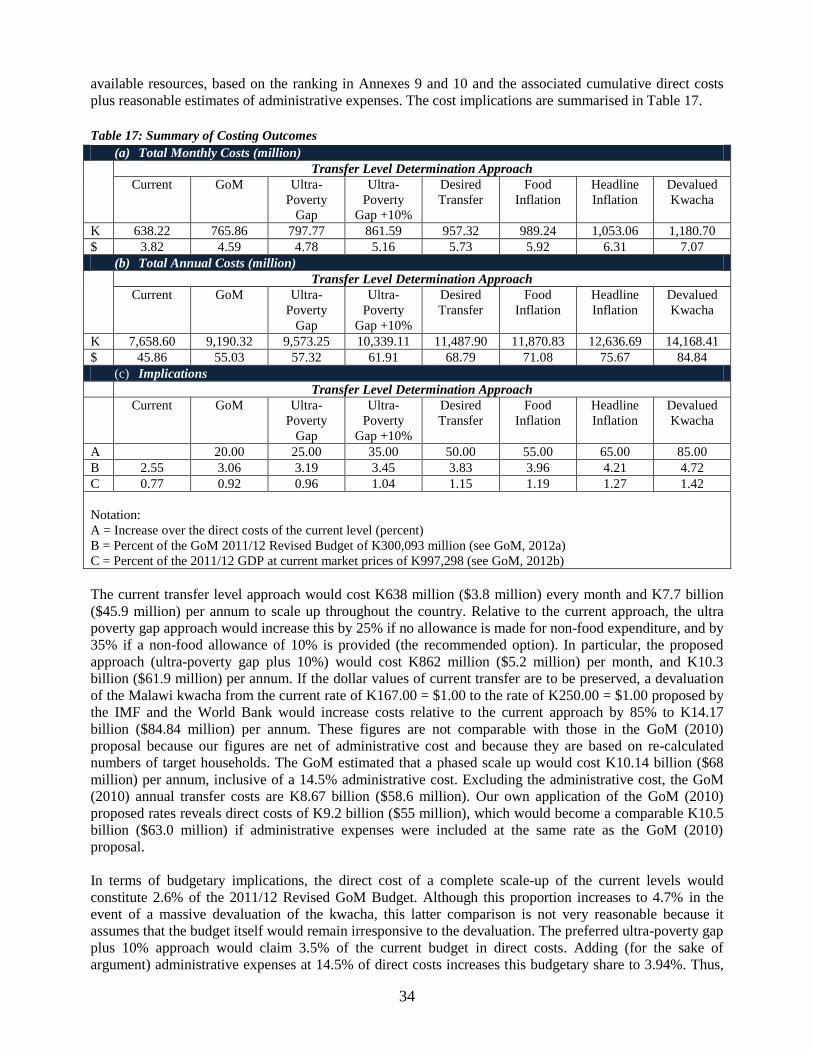

5. Cost Implications...................................................................................................................... 32

5.1 Introduction .................................................................................................................... 32

5.2 Assumptions ................................................................................................................... 33

5.3 Costing Outcomes .......................................................................................................... 33

5. Conclusion ................................................................................................................................ 35

3

Tables

Table 1: SCTP Beneficiary Chart – August 2011 8

Table 2: Gender Categories for Key Informants 9

Table 3: Age Categories of the Beneficiary Key Informants 9

Table 4: Incidence of Poverty in Malawi (2004 – 2009) 15

Table 5: Estimates of Beneficiary Households Per District 18

Table 6: Calculating Malawi SCTP Generosity in Terms of the Ultra-Poverty Line 20

Table 7: Transfers Levels Proposed by the GoM (2010) 22

Table 8: US Dollar-Stable Transfers 23

Table 9: US Dollar-Stable Transfers after Devaluation 24

Table 10: Inflation-Adjusted Transfers 24

Table 11: IHS Ultra-Poverty Gap Transfer Levels 24

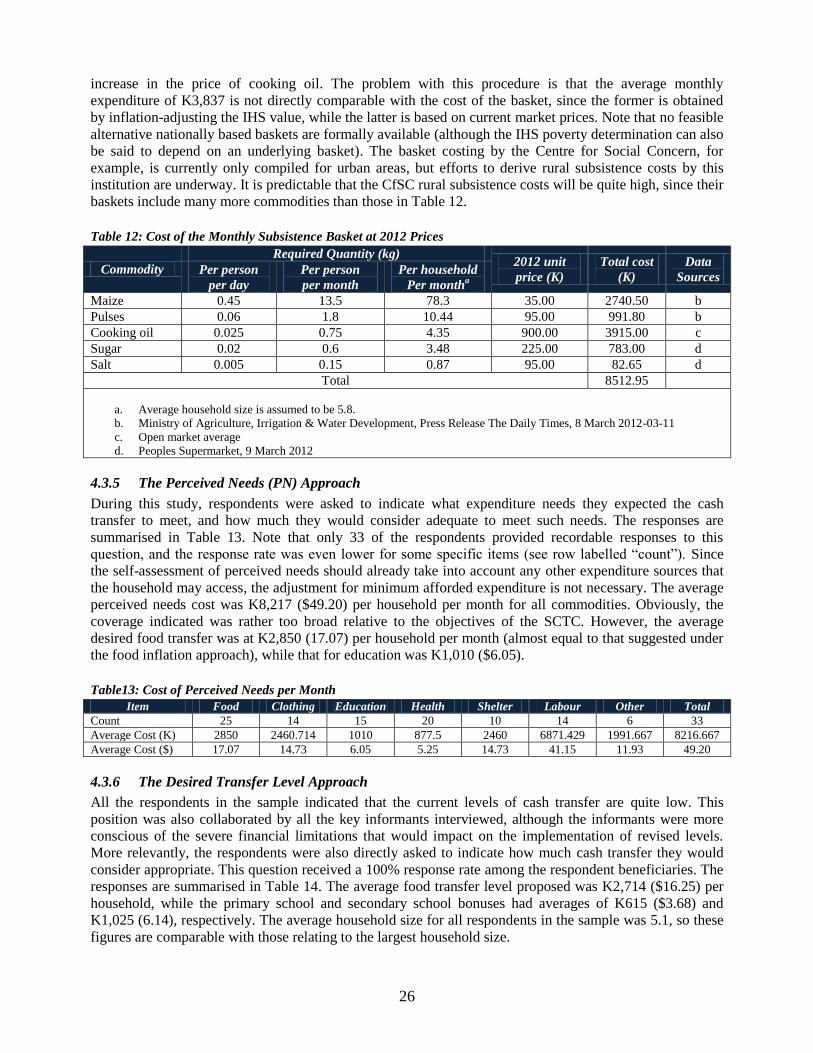

Table 12: Cost of the Monthly Subsistence Basket at 2012 Prices 26

Table13: Cost of Perceived Needs per Month 26

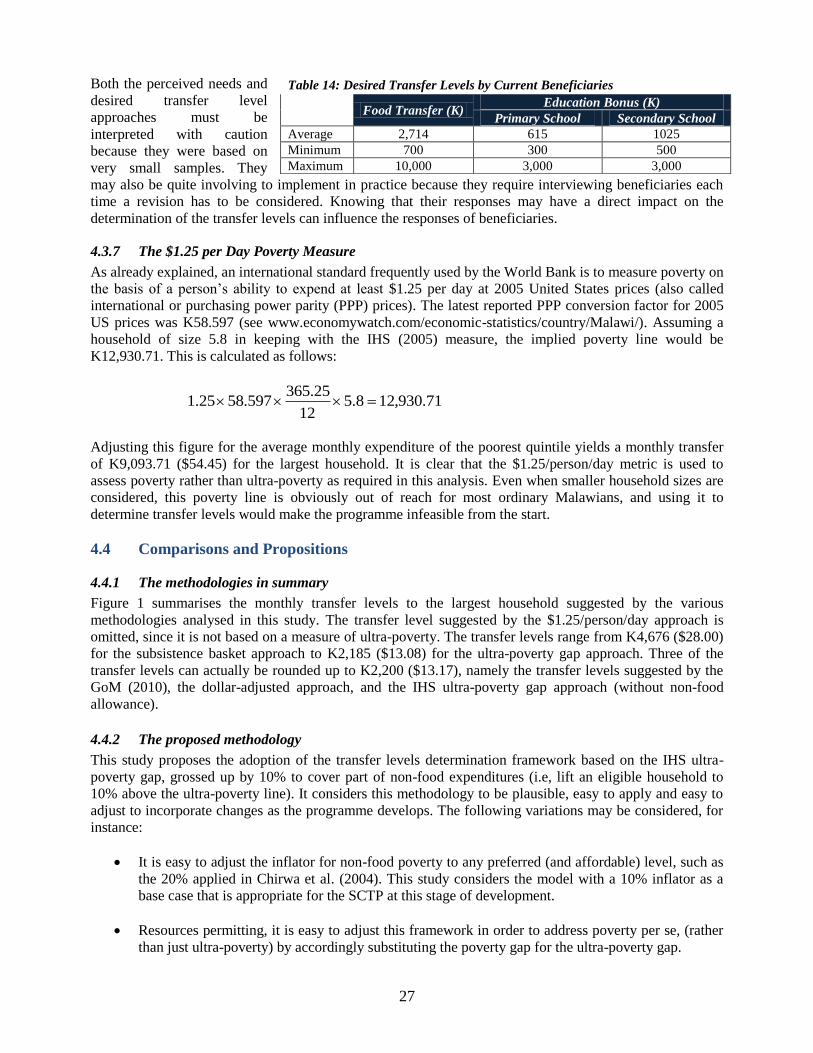

Table 14: Desired Transfer Levels by Current Beneficiaries 27

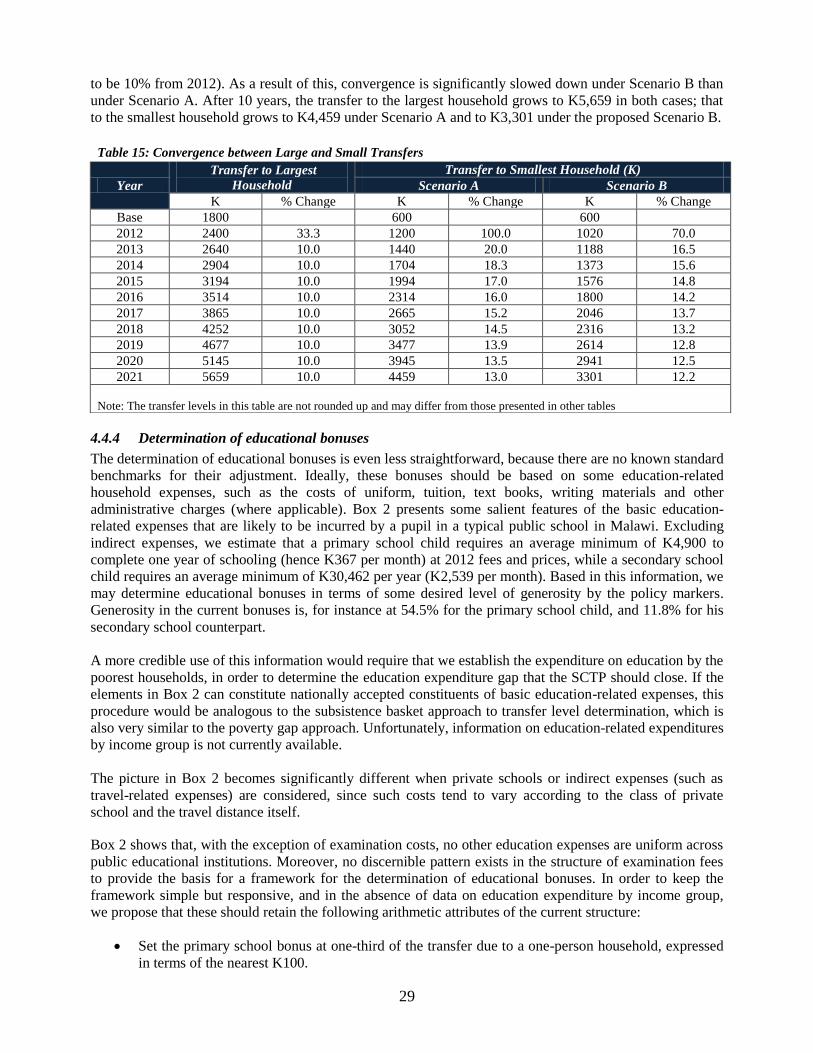

Table 15: Convergence between Large and Small Transfers 29

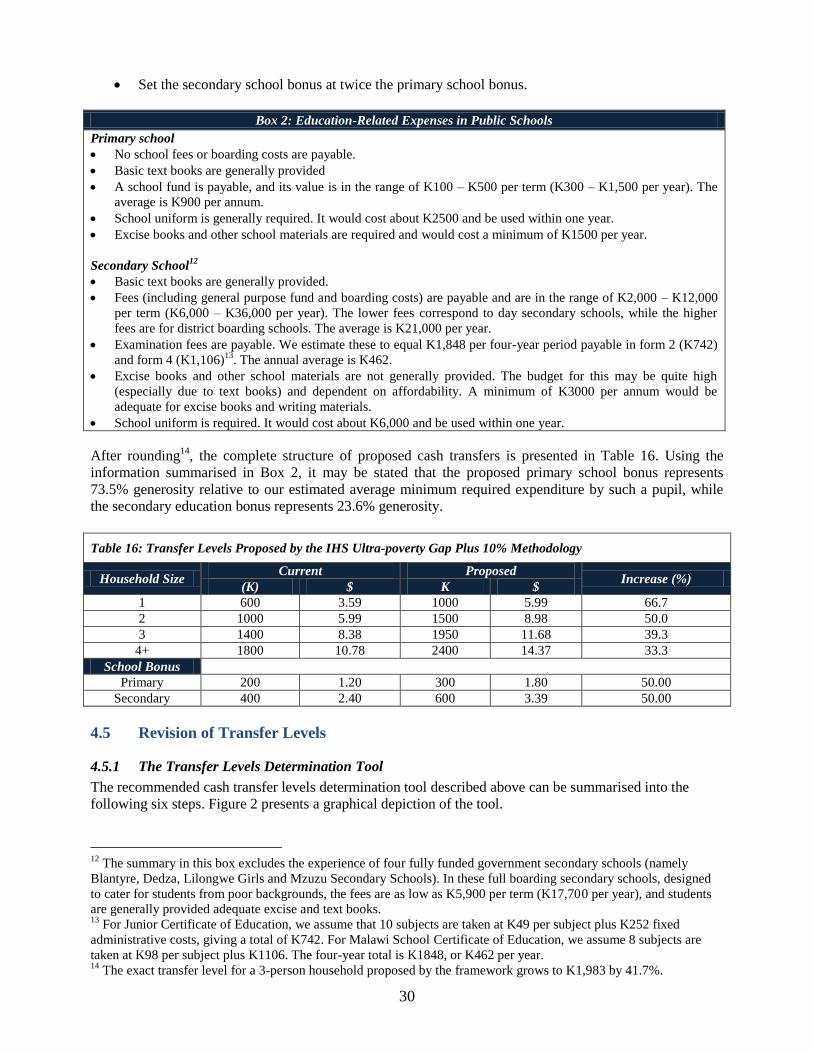

Table 16: Transfer Levels Proposed by the IHS Ultra-poverty Gap Plus 10% Methodology 30

Table 17: Summary of Costing Outcomes 34

Figures

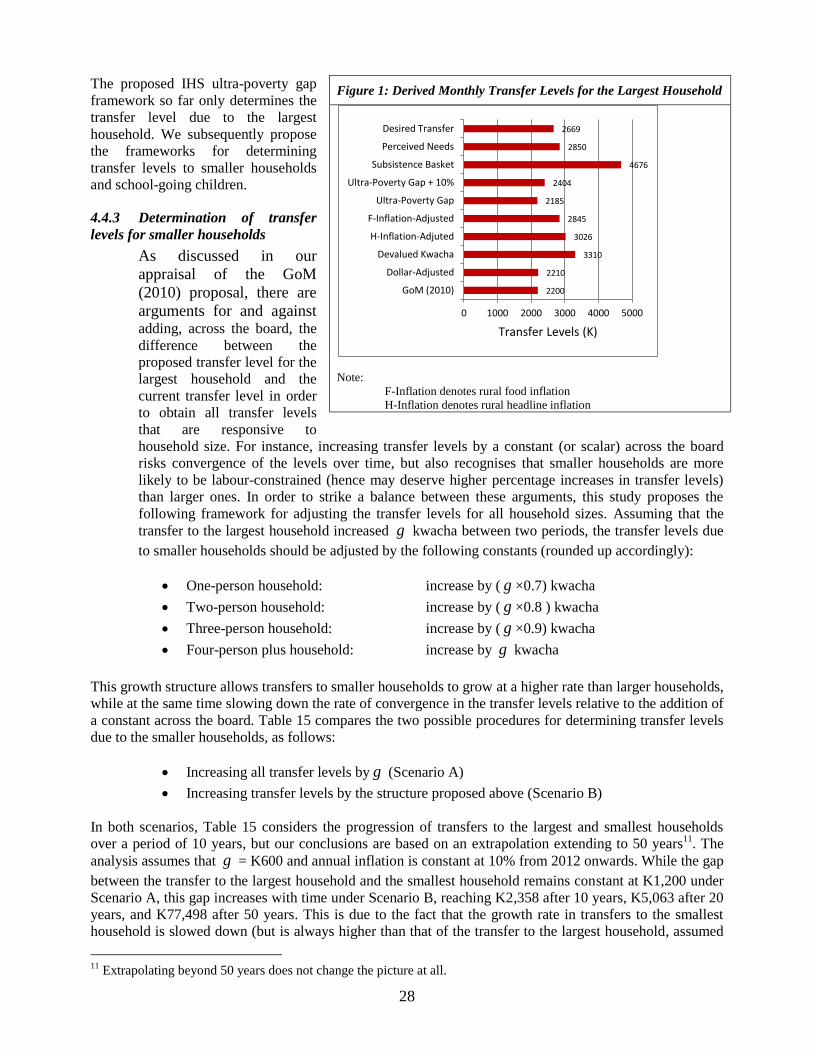

Figure 1: Derived Monthly Transfer Levels for the Largest Household 28

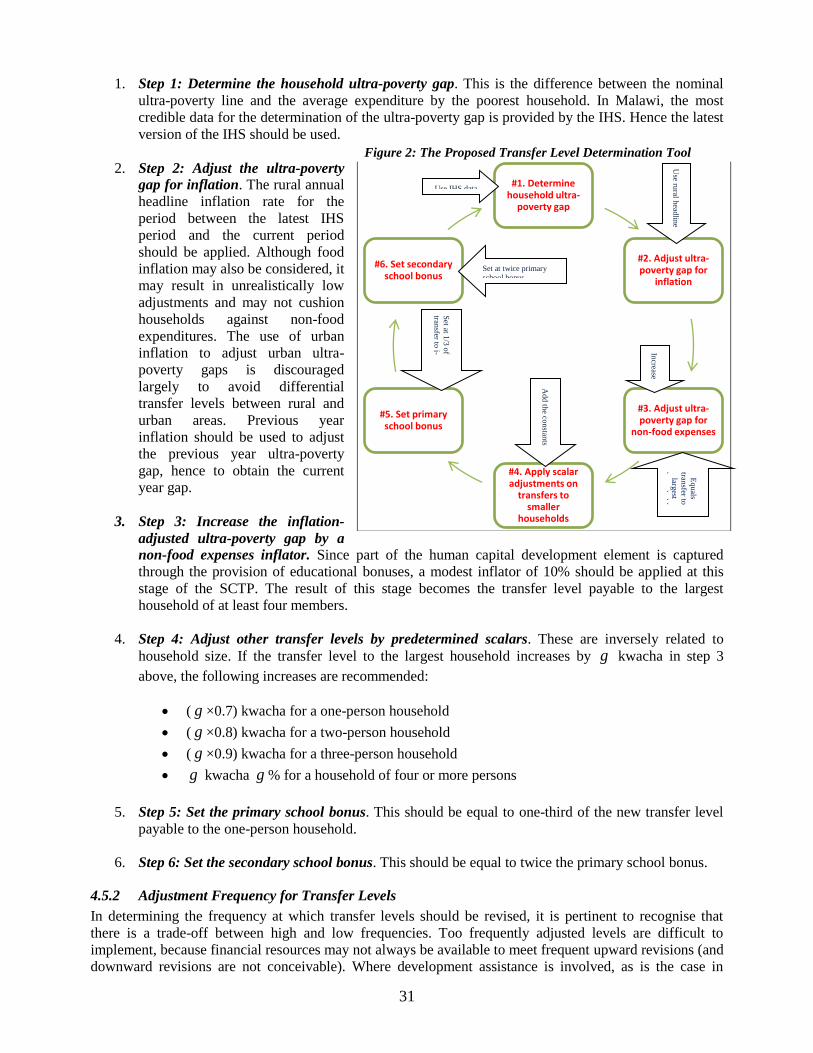

Figure 2: The Proposed Transfer Level Determination Tool 31

Figure 3: Cash Transfer Costs in 12 Countries 35

Boxes

Box 1: Data Improvements and SCTP Beneficiary Targeting 18

Box 2: Education-Related Expenses in Public Schools 30

Annexes

Annex 1: References 37

Annex 2: List of National Level Key Informants 39

Annex 3: List of Key Informants at District Level 40

Annex 4: List of FGD Participants 41

Annex 5: Guiding Questions for National Level Consultations 42

Annex 6: Questionnaire for Beneficiaries – Field Work 44

Annex 7: Guiding Questions for FGD 47

Annex 8: Incidence of Poverty by District (% of population) 49

Annex 9: Targeting Methods 50

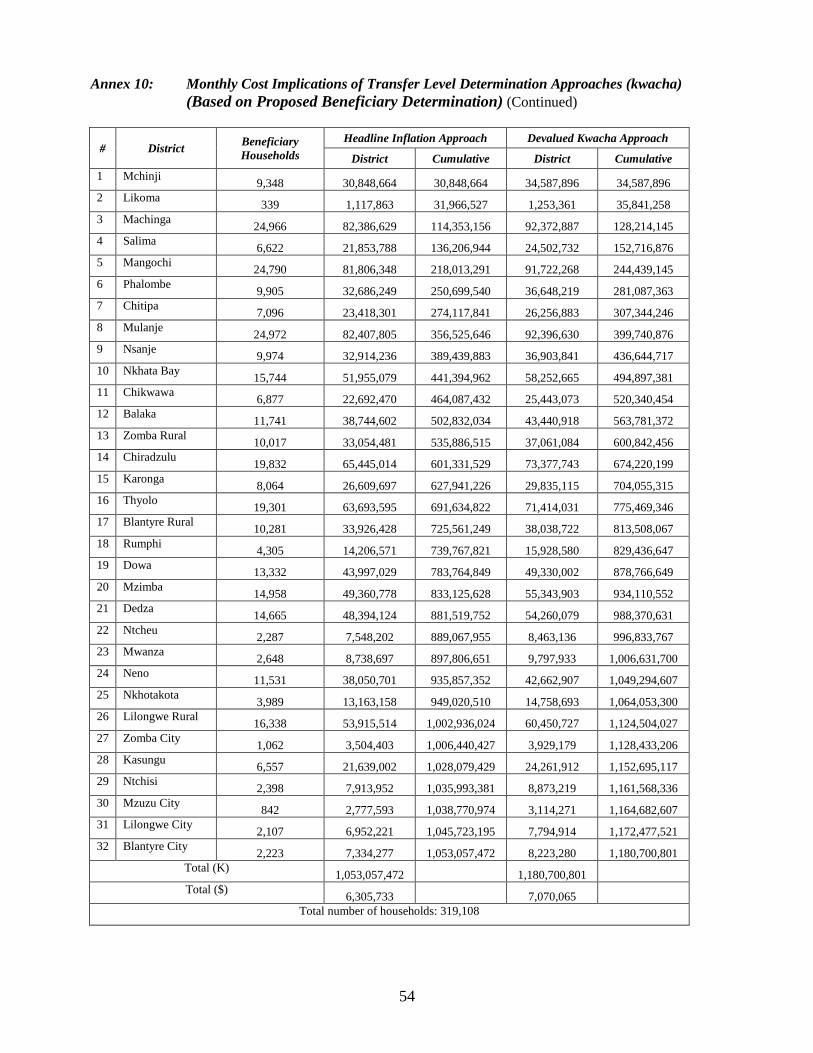

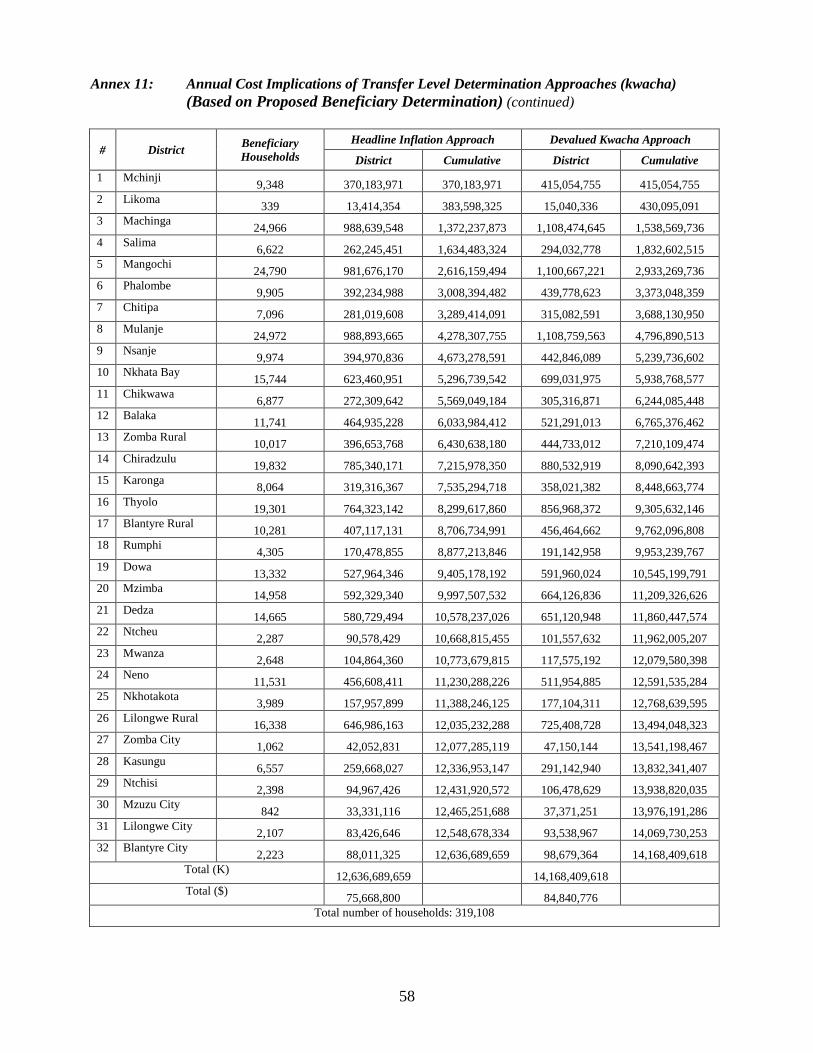

Annex 10: Monthly Cost Implications of Transfer Level Determination Approaches (kwacha) 51

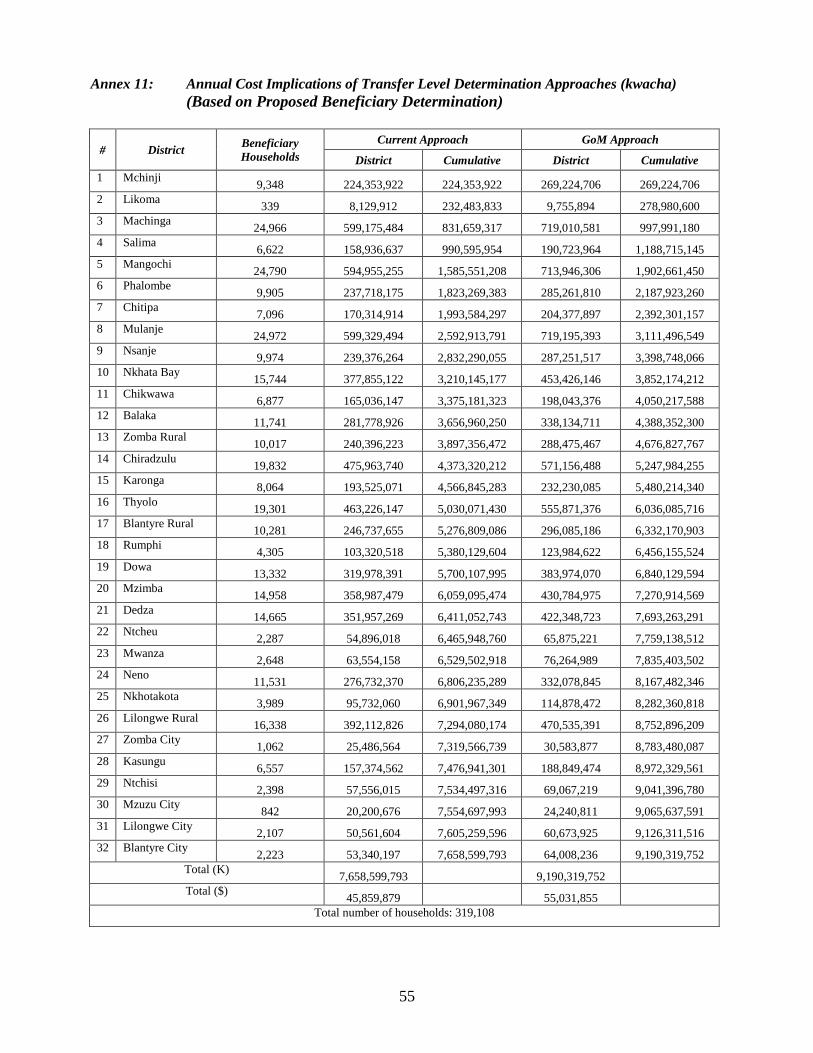

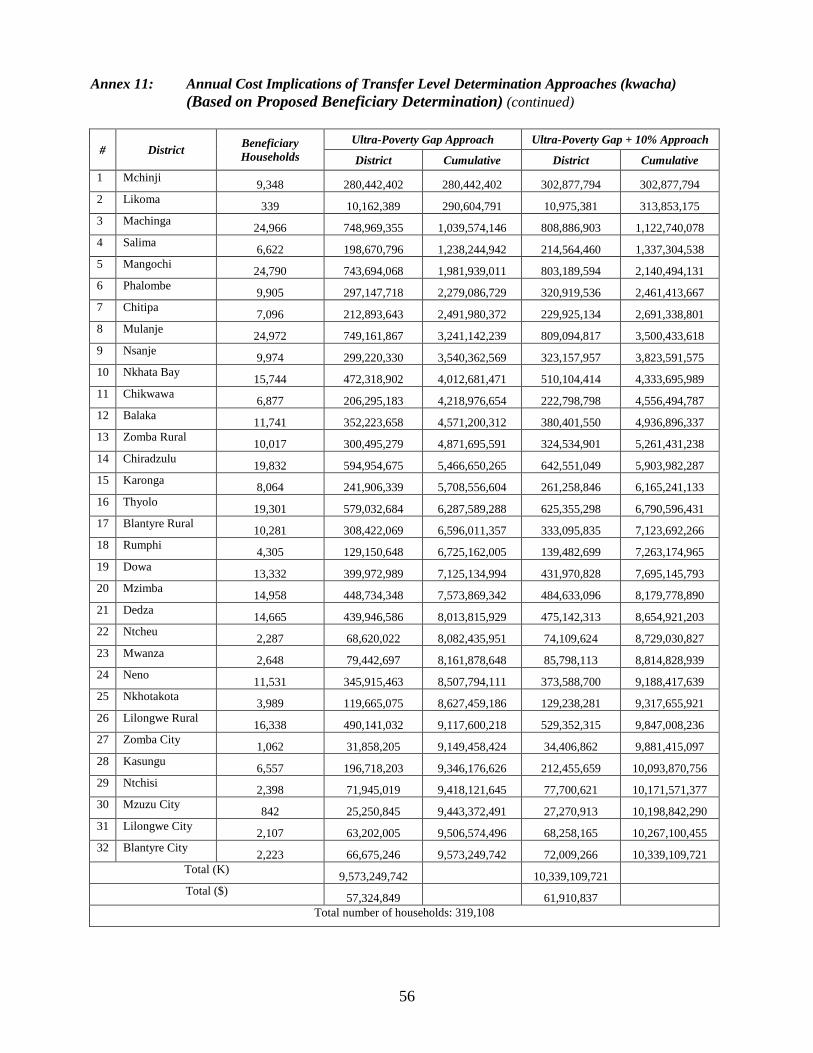

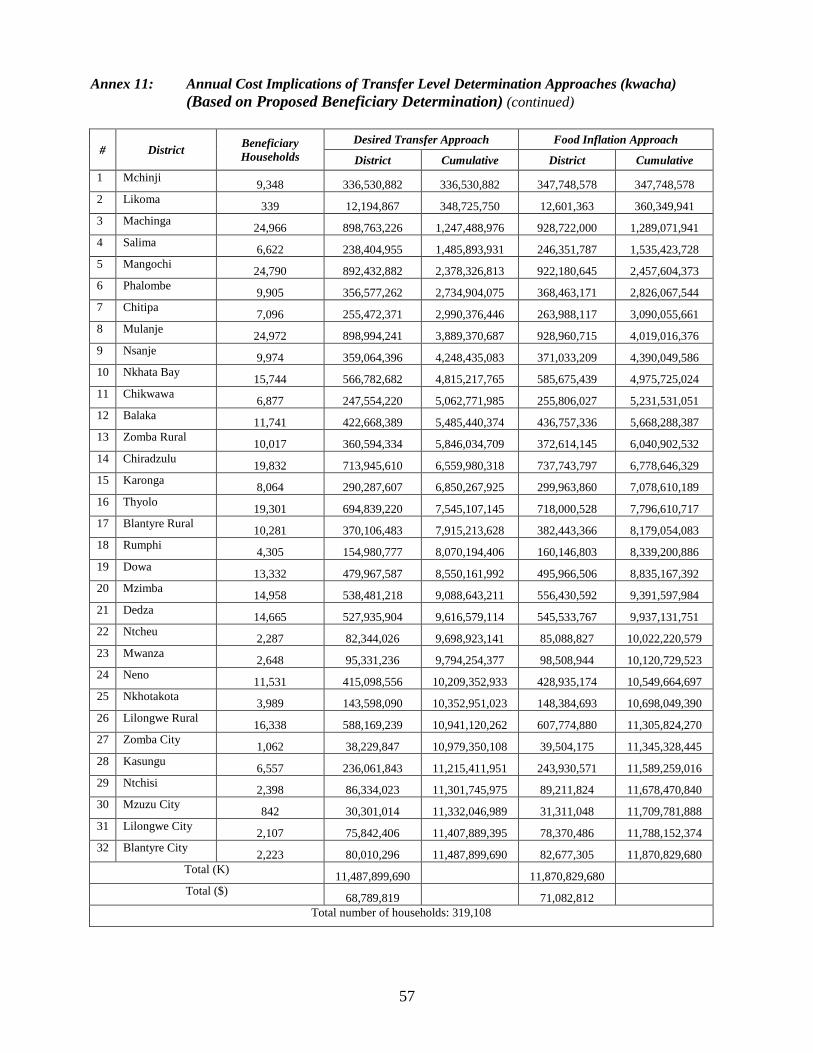

Annex 11: Annual Cost Implications of Transfer Level Determination Approaches (kwacha) 55

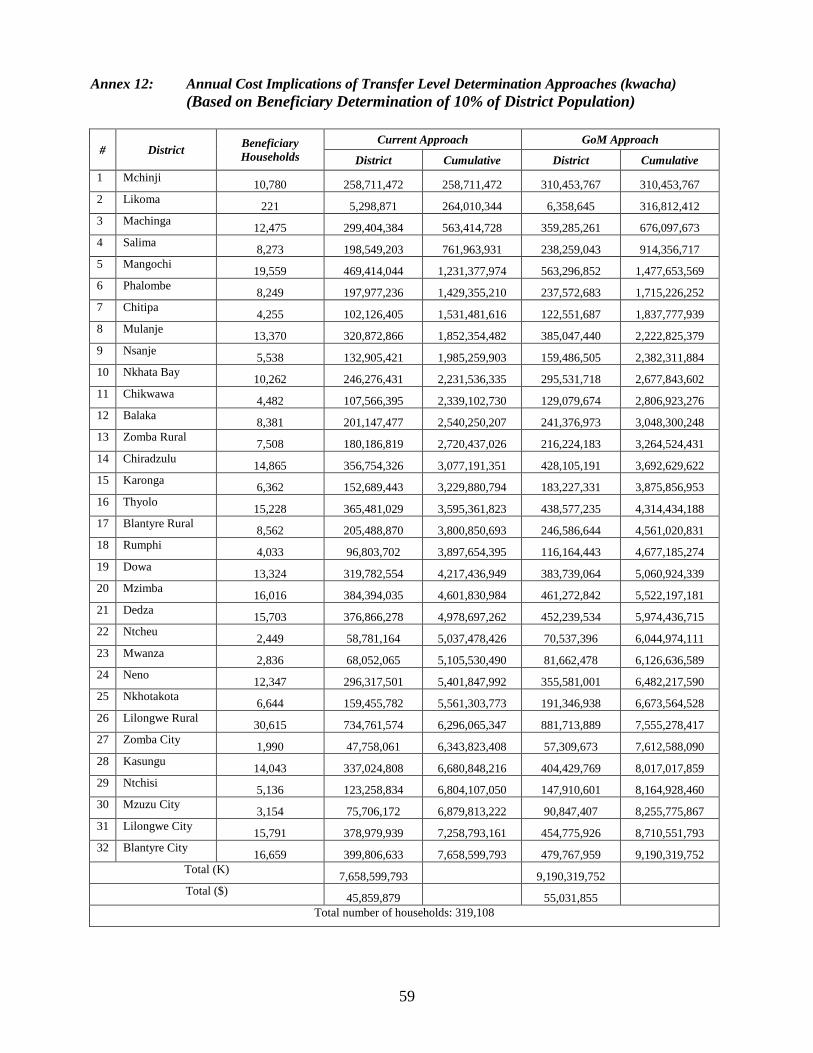

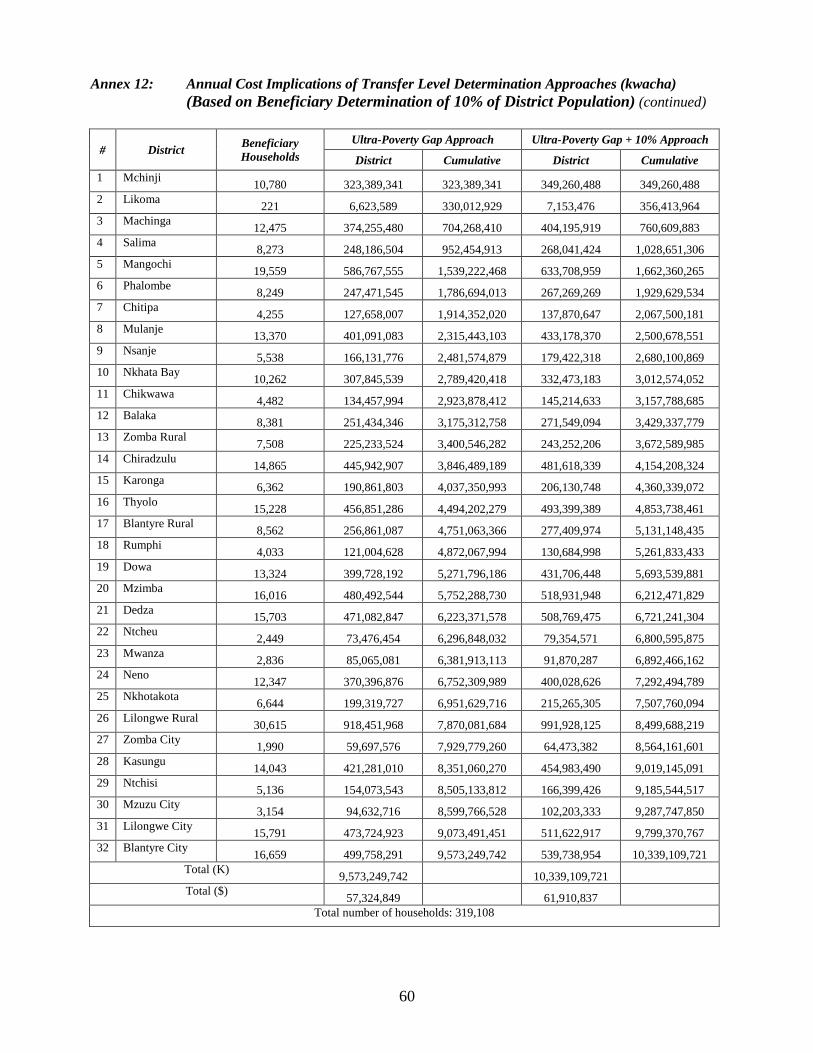

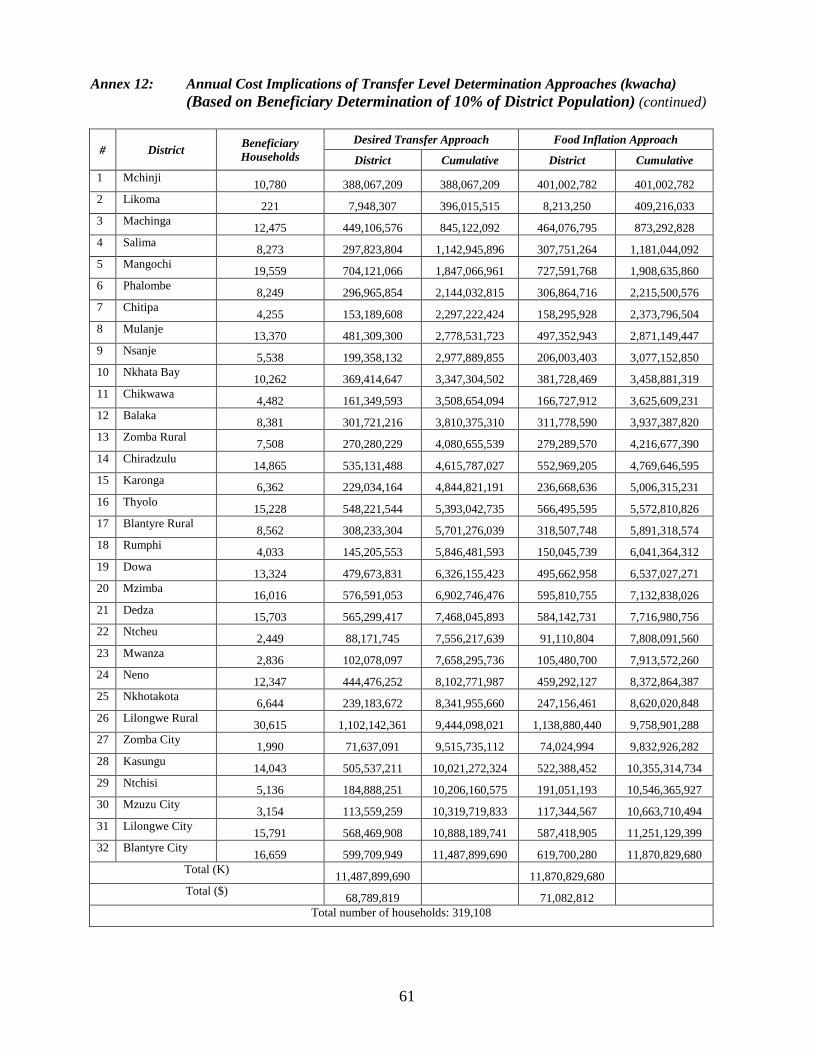

Annex 12: Annual Cost Implications of Transfer Level Determination Approaches (kwacha) 60

4

Executive Summary

This study on the costing and analysis of transfer levels for the Malawi Social Cash Transfer Programme

(SCTP) was commissioned by UNICEF Malawi on behalf of the Government of Malawi. The study

accomplishes three main things summarised in this report, as follows. First, it formalises the framework for

determining the target number of beneficiary household of the SCTP, and presents such estimated for 2012.

Second, it explores and appraises the various methodologies for determining transfer levels, and

recommends an appropriate tool for revising the transfer levels in the programme which is easy, flexible

and relatively prudent in terms of its demand on public resources. Finally, the study estimates the monthly

and annual direct costs implied by the various transfer level determination frameworks.

The main recommendations and implications of this analysis are as follows:

I. The determination of target beneficiary households in each district should be based on the following

general procedure:

a. Calculate the intercensal (1998 – 2008) annual growth rate in the number of households for each

district by iteratively solving for r in:

10

9808 1 rPP

where P08 = number of households in the district in 2008

P98 = number of households in the district in 1998.

b. Compound the total number of households per district in 2008 at the rate of r, to obtain an estimate

of the number of households per district in 2012.

c. Sum up the numbers of households per district to obtain the estimated total number of households

in Malawi in 2012.

d. Calculate the estimated total number of beneficiary households in 2012 as 10% of the estimated

total number of households in Malawi in 2012, in line with the SCTP design.

e. Calculate the number of ultra-poor households per district by multiplying each district‟s ultra-

poverty headcount ratio by the estimated number of households in the district.

f. Sum up the numbers of ultra-poor households in all districts to obtain the total number of ultra-poor

households in Malawi.

g. Obtain each district‟s share of ultra-poor households by dividing each district‟s number of ultra-

poor households by the national number of ultra-poor households.

h. Obtain the number of beneficiary households per district by multiplying each district‟s share of

ultra-poor households by the total number of beneficiaries in Malawi.

In order to improve the framework for determining beneficiary households, it is recommended that the

National Statistical Office should readily supply the following data in standard reports:

a. intercensal growth in the numbers of households per district,

b. ultra-poverty headcount ratios per district per annum, and

c. labour-constrained and non-labour-constrained ultra-poor households per district per annum.

5

II. The revision of cash transfer levels should be based on the IHS ultra-poverty gap approach. The

following transfer level determination tool should be used:

a. Step 1: Determine the ultra-poverty gap. This is the difference between the nominal ultra-poverty

line for the poorest household of a given size, and the average expenditure by the poorest segment

of the population.

b. Step 2: Adjust the ultra-poverty gap for inflation. The rural annual headline inflation rates for the

period between the latest IHS period and the current period should be applied. Previous year

inflation should be used to adjust the previous year ultra-poverty gap to obtain the current year‟s

ultra-poverty gap.

c. Step 3: Increase the inflation-adjusted ultra-poverty gap by a basic non-food expenditures inflator

of 10%. The result obtained at this stage becomes the transfer level payable to the largest household

of at least four members.

d. Step 4: Adjust other transfer levels based on household size by pre-determined growth rates:

Assuming that the transfer to the largest household increased g kwacha between two periods, adjust

transfer levels due to smaller households by the following constants (rounded up accordingly):

One-person household: increase by (g×0.7) kwacha

Two-person household: increase by (g×0.8 ) kwacha

Three-person household: increase by (g×0.9) kwacha

Four-person plus household: increase by g kwacha

e. Step 5: Set the primary school bonus. This should be equal to one-third of the new transfer level

payable to the one-person household.

f. Step 6: Set the secondary school bonus. This should be equal to double the primary school bonus.

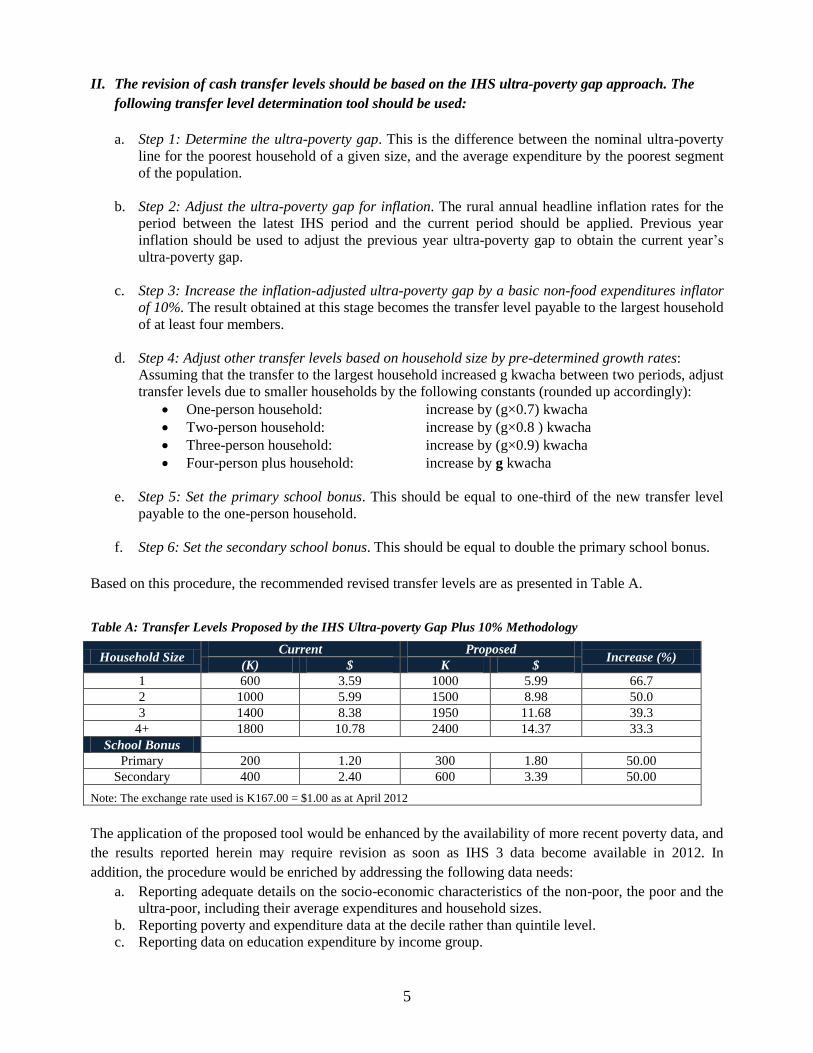

Based on this procedure, the recommended revised transfer levels are as presented in Table A.

Table A: Transfer Levels Proposed by the IHS Ultra-poverty Gap Plus 10% Methodology

Household Size Current Proposed

Increase (%) (K) $ K $

1 600 3.59 1000 5.99 66.7

2 1000 5.99 1500 8.98 50.0

3 1400 8.38 1950 11.68 39.3

4+ 1800 10.78 2400 14.37 33.3

School Bonus

Primary 200 1.20 300 1.80 50.00

Secondary 400 2.40 600 3.39 50.00

Note: The exchange rate used is K167.00 = $1.00 as at April 2012

The application of the proposed tool would be enhanced by the availability of more recent poverty data, and

the results reported herein may require revision as soon as IHS 3 data become available in 2012. In

addition, the procedure would be enriched by addressing the following data needs:

a. Reporting adequate details on the socio-economic characteristics of the non-poor, the poor and the

ultra-poor, including their average expenditures and household sizes.

b. Reporting poverty and expenditure data at the decile rather than quintile level.

c. Reporting data on education expenditure by income group.

6

III. Conduct annual reviews of transfer levels.

Apart from ensuring responsiveness to changes, annual reviews have the advantage that costs are likely

to adjust slowly from year to year, especially when rural inflation remains low.

If the application of the adjustment tool in a given review period results in an adjustment of less than

5% to the prevailing transfer due the largest household, it is our view that the transfer levels need not be

revised in that period.

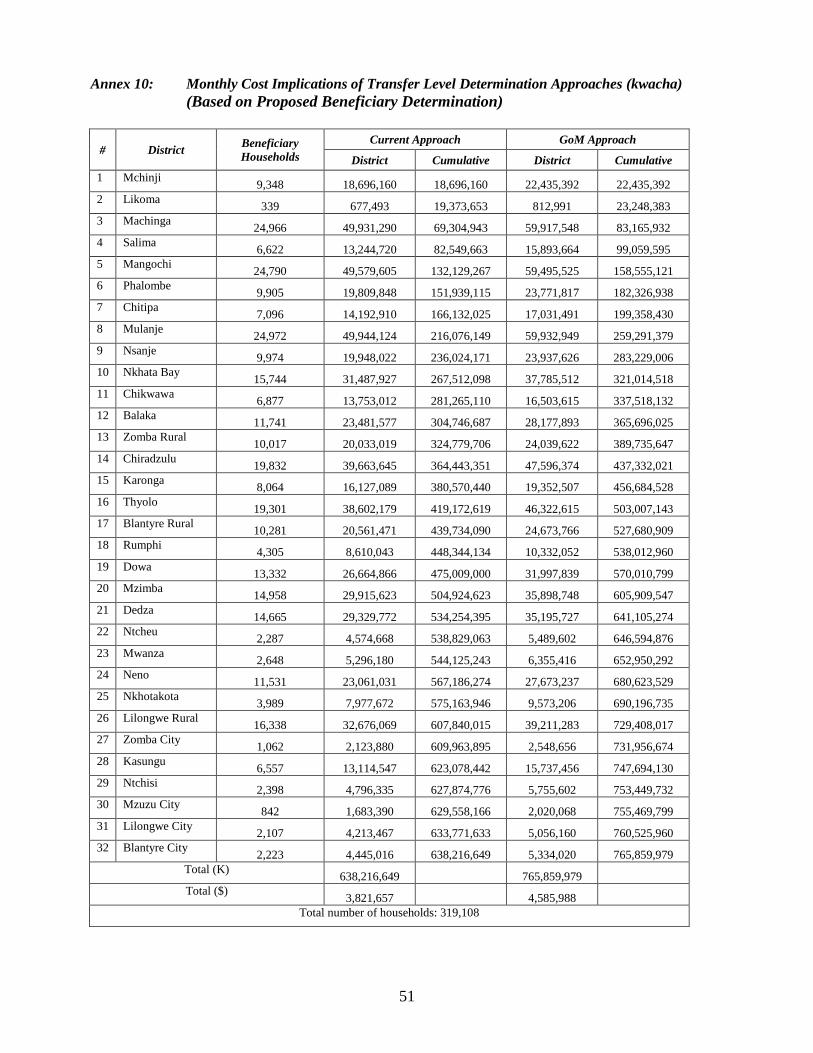

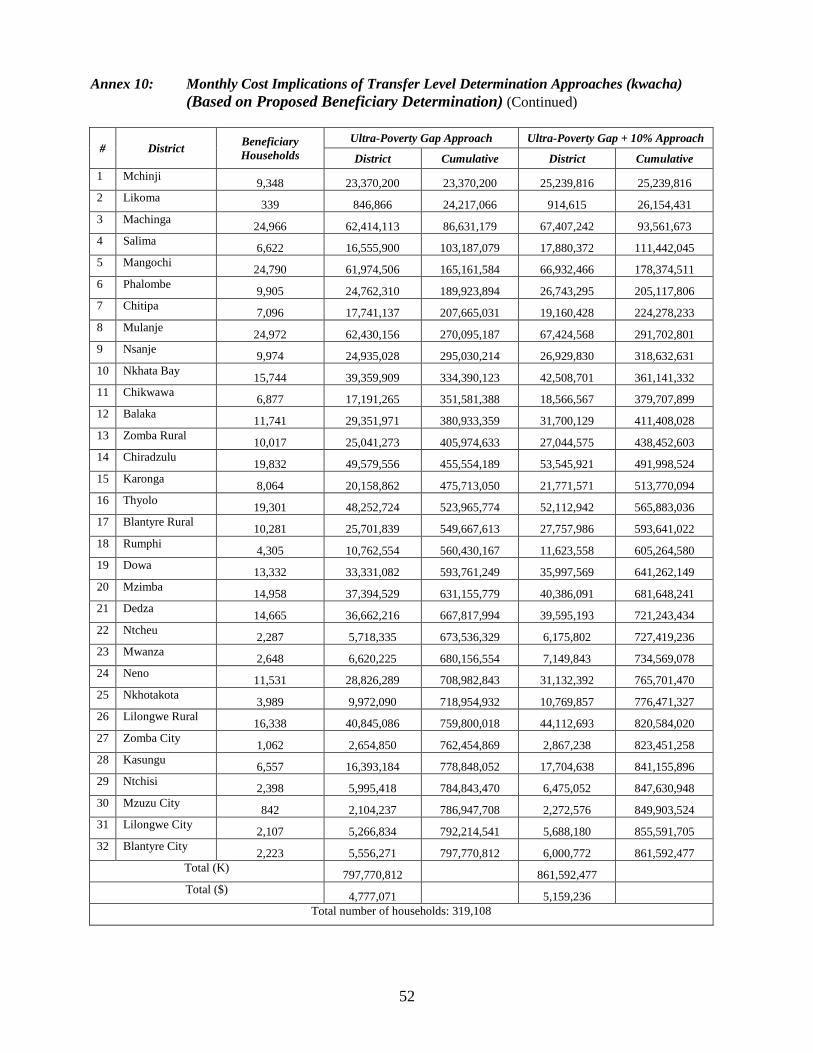

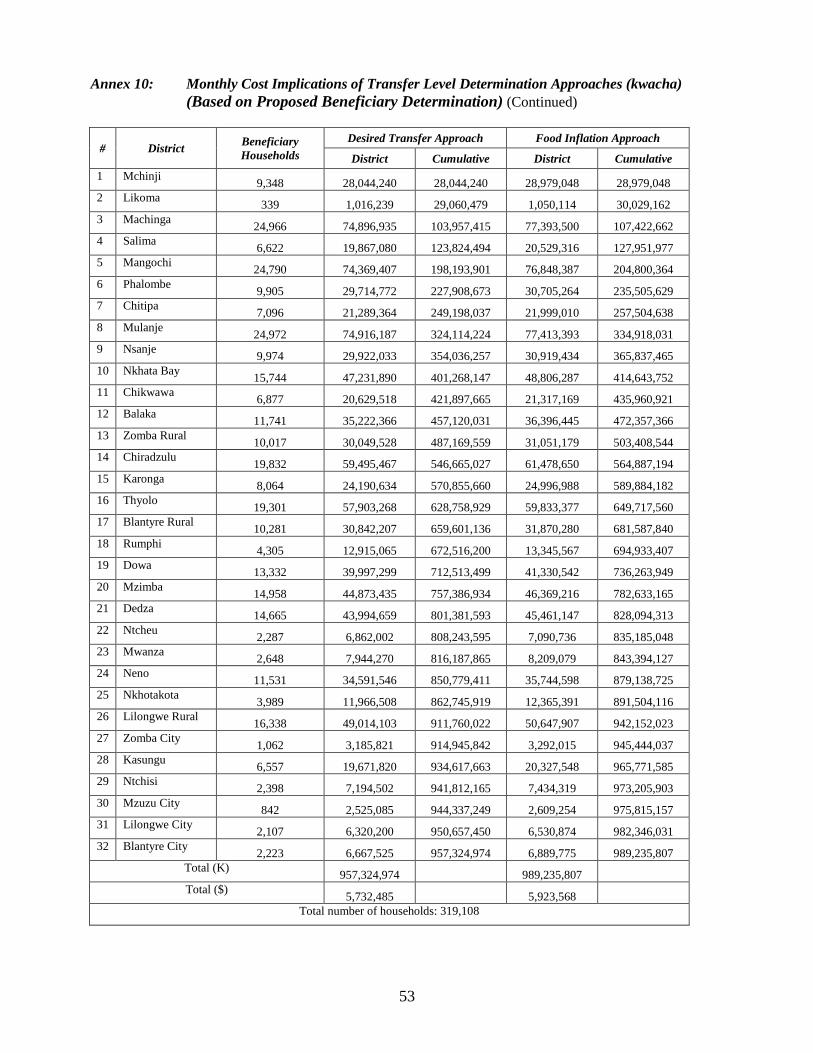

IV. The direct cost implications of these recommendations as at April 2012 are as follows:

a. A national programme roll-out based on the current transfer levels would cost K638.22 million

($3.82 million) per month, or K7.66 billion ($45.9 million) per annum in direct costs.

b. A national programme roll-out based on the proposed ultra-poverty gap plus 10% approach would

cost K861.59 million ($5.16 million) per month, and K10.34 billion ($61.91 million) per annum in

direct costs.

c. Therefore, implementation of the proposed transfer level determination tool would cost 35% more

than the current framework at today‟s prices. Given the objectives and design of the SCTP, this is

appears to be the most cost-effective of the procedures explored in the study.

d. Additionally, the direct costs due to the proposed approach would be 3.45% of the current Malawi

Government Budget, and 1.04% of GDP. These are lower than figures reported for other

developing countries, notwithstanding that the SCTP is only one of several other public social

security programmes being implemented in Malawi.

7

1. Introduction

1.1 Background

The Malawi Social Cash Transfer Programme (SCTP) was initiated with the objectives of reducing poverty,

hunger and starvation and increasing child school enrolment, health and nutrition among vulnerable

households. The programme was piloted in Mchinji District from 2006, and is currently being implemented

in 7 districts of the country reaching about 25,000 ultra-poor and labour-constrained households as of

August, 2011 (Table 1). The total number of beneficiary households was estimated at 29,925 in November

2011. The programme is implemented for the Government of Malawi (GoM) by the SCTP Secretariat of

the Ministry of Gender, Children and Community Development, while policy direction is provided by the

GoM‟s Division of Poverty Reduction and Social Protection in the Ministry of Economic Planning and

Development. Until end 2011, transfer funding has been largely provided by the Global Fund to Fight

Malaria, AIDS and Tuberculosis through the National AIDS Commission (NAC). Additional transfer

funding has also been provided by Irish Aid. From, January 2012 funding amounting to €13 million will be

provided by the German Government through Kreditanstalt für Wiederaufbau (KfW). The United Nations

Children Fund (UNICEF) Malawi provides technical assistance and capacity strengthening to the

programme.

The SCTP targets ultra-poor and labour-constrained households in Malawi. These are defined as follows:1:

Ultra poor households: A household is ultra poor if it is in the lowest expenditure quintile and

under the national ultra poverty line (only able to afford one meal per day; not able to purchase

essential non-food items such as soap, clothing, school material; are begging; and have no valuable

assets)

Labour constrained households: A household is considered labour constrained if it has no able-

bodied adult fit for work or a dependency ratio of more than 3. These households are not able to

access or benefit sufficiently from labour based interventions such as public works or casual labour

(ganyu).

The Government of Malawi has developed the following criteria for labour constrained households:

A household with high dependency ratio, identified as one whose household head is between the

ages of 19-59 who may or may not be fit for work, but must care for more than 3 dependants.

A person who is not fit for work, including a child who is under the age of 18; a person who is

elderly (above 60 years of old); a person who is between the ages of 19-59, but is chronically ill or

disabled; or a school going person, up to the age of 25.

The SCTP monthly cash transfer levels vary according to family size as follows:2

K600 ($3.60) for a one-person household

K1000 ($6.00) for a two-person household

K1,400 ($8.40) for a three-person household

K1,800 ($10.75) for a household of four or more members.

1see http://www.unicef.org/malawi/MLW_resources_qasocialcashpilot.pdf

2 Unless otherwise stated, United States dollar ($) values are obtained using the exchange rate of K167.00 = $1.00.

8

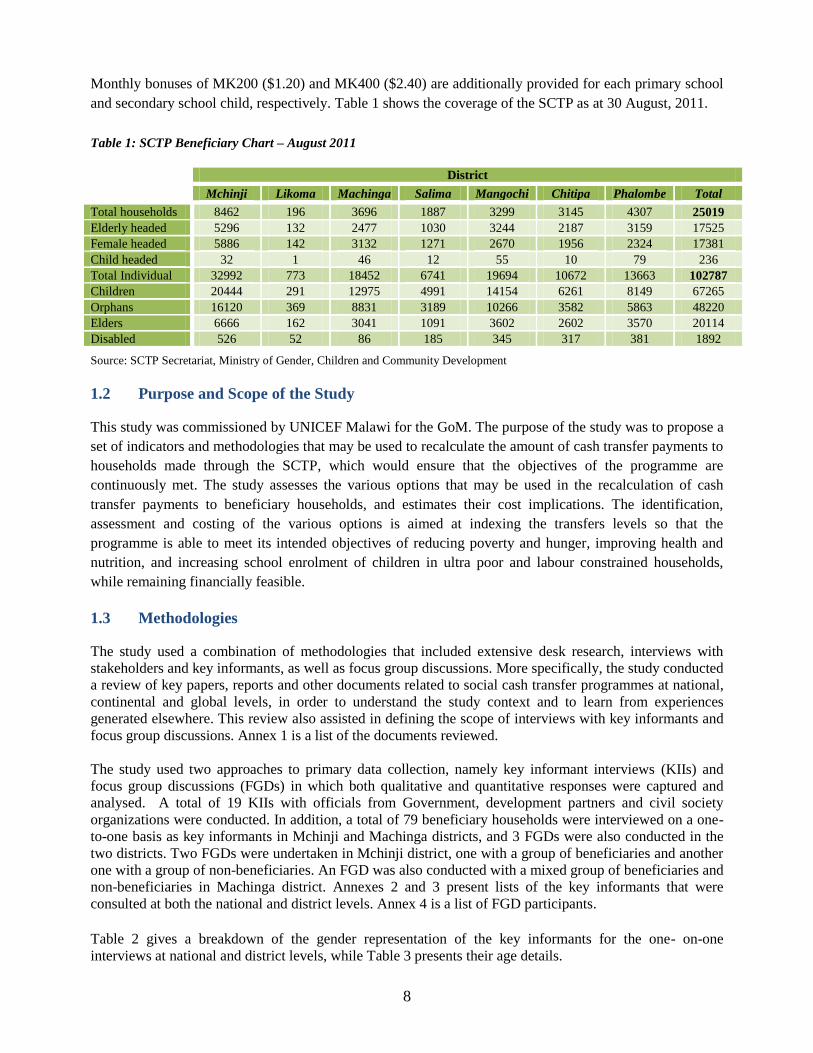

Monthly bonuses of MK200 ($1.20) and MK400 ($2.40) are additionally provided for each primary school

and secondary school child, respectively. Table 1 shows the coverage of the SCTP as at 30 August, 2011.

Table 1: SCTP Beneficiary Chart – August 2011

District

Mchinji Likoma Machinga Salima Mangochi Chitipa Phalombe Total

Total households 8462 196 3696 1887 3299 3145 4307 25019

Elderly headed 5296 132 2477 1030 3244 2187 3159 17525

Female headed 5886 142 3132 1271 2670 1956 2324 17381

Child headed 32 1 46 12 55 10 79 236

Total Individual 32992 773 18452 6741 19694 10672 13663 102787

Children 20444 291 12975 4991 14154 6261 8149 67265

Orphans 16120 369 8831 3189 10266 3582 5863 48220

Elders 6666 162 3041 1091 3602 2602 3570 20114

Disabled 526 52 86 185 345 317 381 1892

Source: SCTP Secretariat, Ministry of Gender, Children and Community Development

1.2 Purpose and Scope of the Study

This study was commissioned by UNICEF Malawi for the GoM. The purpose of the study was to propose a

set of indicators and methodologies that may be used to recalculate the amount of cash transfer payments to

households made through the SCTP, which would ensure that the objectives of the programme are

continuously met. The study assesses the various options that may be used in the recalculation of cash

transfer payments to beneficiary households, and estimates their cost implications. The identification,

assessment and costing of the various options is aimed at indexing the transfers levels so that the

programme is able to meet its intended objectives of reducing poverty and hunger, improving health and

nutrition, and increasing school enrolment of children in ultra poor and labour constrained households,

while remaining financially feasible.

1.3 Methodologies

The study used a combination of methodologies that included extensive desk research, interviews with

stakeholders and key informants, as well as focus group discussions. More specifically, the study conducted

a review of key papers, reports and other documents related to social cash transfer programmes at national,

continental and global levels, in order to understand the study context and to learn from experiences

generated elsewhere. This review also assisted in defining the scope of interviews with key informants and

focus group discussions. Annex 1 is a list of the documents reviewed.

The study used two approaches to primary data collection, namely key informant interviews (KIIs) and

focus group discussions (FGDs) in which both qualitative and quantitative responses were captured and

analysed. A total of 19 KIIs with officials from Government, development partners and civil society

organizations were conducted. In addition, a total of 79 beneficiary households were interviewed on a one-

to-one basis as key informants in Mchinji and Machinga districts, and 3 FGDs were also conducted in the

two districts. Two FGDs were undertaken in Mchinji district, one with a group of beneficiaries and another

one with a group of non-beneficiaries. An FGD was also conducted with a mixed group of beneficiaries and

non-beneficiaries in Machinga district. Annexes 2 and 3 present lists of the key informants that were

consulted at both the national and district levels. Annex 4 is a list of FGD participants.

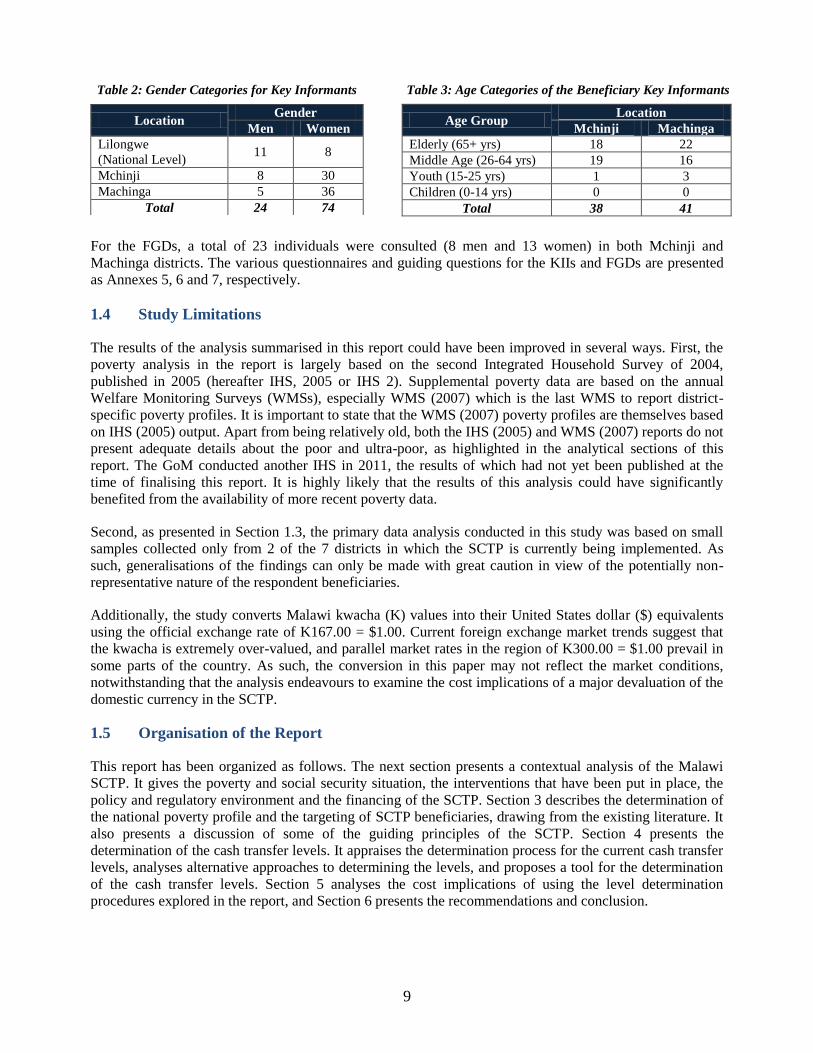

Table 2 gives a breakdown of the gender representation of the key informants for the one- on-one

interviews at national and district levels, while Table 3 presents their age details.

9

Table 2: Gender Categories for Key Informants

Table 3: Age Categories of the Beneficiary Key Informants

Location Gender

Men Women

Lilongwe

(National Level) 11 8

Mchinji 8 30

Machinga 5 36

Total 24 74

Age Group

Location

Mchinji Machinga

Elderly (65+ yrs) 18 22

Middle Age (26-64 yrs) 19 16

Youth (15-25 yrs) 1 3

Children (0-14 yrs) 0 0

Total 38 41

For the FGDs, a total of 23 individuals were consulted (8 men and 13 women) in both Mchinji and

Machinga districts. The various questionnaires and guiding questions for the KIIs and FGDs are presented

as Annexes 5, 6 and 7, respectively.

1.4 Study Limitations

The results of the analysis summarised in this report could have been improved in several ways. First, the

poverty analysis in the report is largely based on the second Integrated Household Survey of 2004,

published in 2005 (hereafter IHS, 2005 or IHS 2). Supplemental poverty data are based on the annual

Welfare Monitoring Surveys (WMSs), especially WMS (2007) which is the last WMS to report district-

specific poverty profiles. It is important to state that the WMS (2007) poverty profiles are themselves based

on IHS (2005) output. Apart from being relatively old, both the IHS (2005) and WMS (2007) reports do not

present adequate details about the poor and ultra-poor, as highlighted in the analytical sections of this

report. The GoM conducted another IHS in 2011, the results of which had not yet been published at the

time of finalising this report. It is highly likely that the results of this analysis could have significantly

benefited from the availability of more recent poverty data.

Second, as presented in Section 1.3, the primary data analysis conducted in this study was based on small

samples collected only from 2 of the 7 districts in which the SCTP is currently being implemented. As

such, generalisations of the findings can only be made with great caution in view of the potentially non-

representative nature of the respondent beneficiaries.

Additionally, the study converts Malawi kwacha (K) values into their United States dollar ($) equivalents

using the official exchange rate of K167.00 = $1.00. Current foreign exchange market trends suggest that

the kwacha is extremely over-valued, and parallel market rates in the region of K300.00 = $1.00 prevail in

some parts of the country. As such, the conversion in this paper may not reflect the market conditions,

notwithstanding that the analysis endeavours to examine the cost implications of a major devaluation of the

domestic currency in the SCTP.

1.5 Organisation of the Report

This report has been organized as follows. The next section presents a contextual analysis of the Malawi

SCTP. It gives the poverty and social security situation, the interventions that have been put in place, the

policy and regulatory environment and the financing of the SCTP. Section 3 describes the determination of

the national poverty profile and the targeting of SCTP beneficiaries, drawing from the existing literature. It

also presents a discussion of some of the guiding principles of the SCTP. Section 4 presents the

determination of the cash transfer levels. It appraises the determination process for the current cash transfer

levels, analyses alternative approaches to determining the levels, and proposes a tool for the determination

of the cash transfer levels. Section 5 analyses the cost implications of using the level determination

procedures explored in the report, and Section 6 presents the recommendations and conclusion.

10

2. A Contextual Background of the Malawi SCTP

2.1 Poverty and Vulnerabilities in Malawi

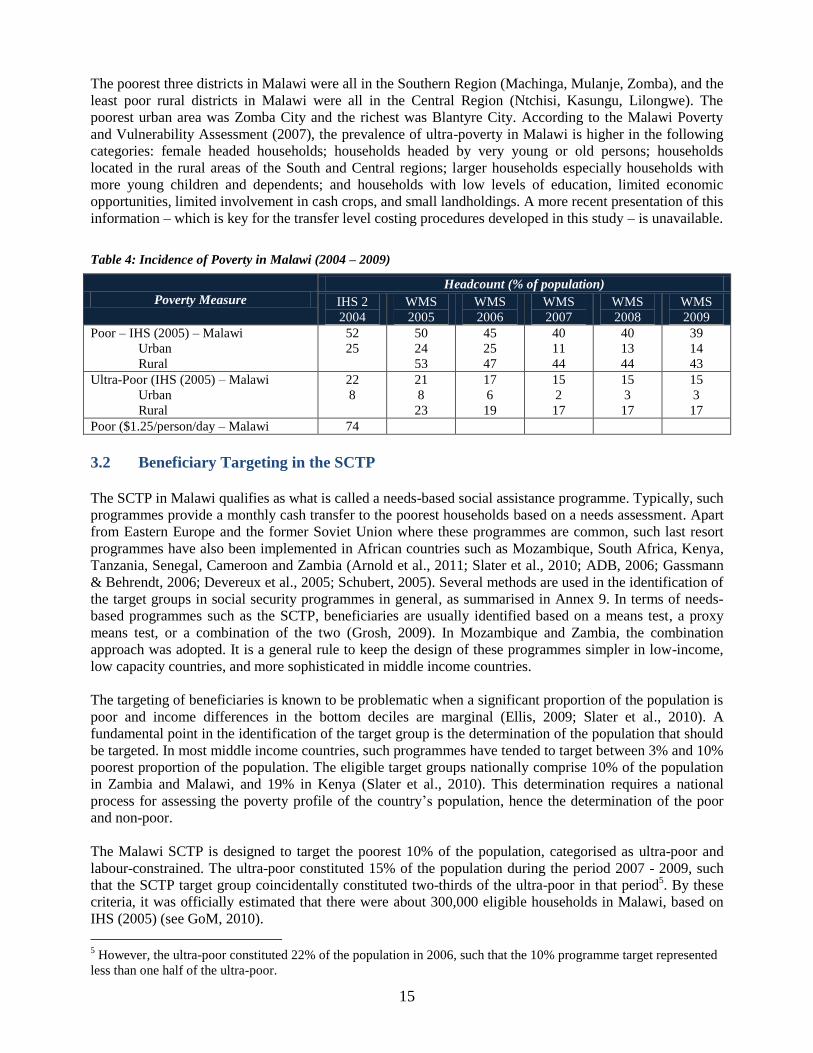

The WMS (2009), the Malawi Poverty and Vulnerability Assessment (2007) and the IHS (2005) are the

most recent sources of information on the poverty levels in the country. The WMS and the IHS define a

household as poor if its annual per capita consumption expenditure is below a threshold or a poverty line.

The poverty line is a subsistence minimum expressed in Malawi kwacha based on a cost of basic needs

methodology which has two parts: (a) minimum food expenditure based on the food requirements of an

individual, and (b) critical non-food consumption. Individuals or households whose consumption is lower

than the total poverty line are defined as poor, while those whose total expenditure falls short of that

necessary to meet the minimum food requirements are categorized as ultra-poor. This process provides an

absolute measure of poverty where the poverty and ultra-poverty lines were respectively established as

K16,165 and K10,029 per person per year in 2004 (IHS, 2005).

According to the WMS (2009), the proportion of the population living below the poverty line in Malawi

fell from 52.4% in 2004 (IHS, 2005) to about 39% in 2009. The ultra-poor and moderately poor proportions

were estimated at 15% and 25% respectively in 2009. The proportion of the ultra-poor in Malawi declined

in the period 2004 - 2009 from 22% (IHS, 2005) to 15% (WMS, 2009).

Poverty is dynamic, with individuals and households shifting frequently from one category to another. This

could be due to a harvest shock which can tip large numbers of the non-poor into poverty. In order to

understand poverty in Malawi, it is also important to understand how vulnerability has contributed to the

poverty dynamics. Vulnerability is defined as the inability of households to deal with shocks to their

livelihoods. The following are the key vulnerabilities affecting Malawians at national level:

1. Agricultural vulnerabilities that are caused by erratic rainfall, shortage of land for agricultural

production, limited access to farm inputs and credit, and lack of livestock as assets.

2. Economic shocks and processes resulting from undiversified livelihoods, weak markets, interaction

between transitory shocks and chronic poverty.

3. Demographic vulnerabilities due to high population growth, increasing number of households

headed by women, children and the elderly.

4. Health and nutrition risks including HIV and AIDS

According to the GoM (2011), there are two main causes of poverty in Malawi, namely:

Limited livelihood sources where most households earn their livelihood only from their household

farm and fishing. However, the average household farm sizes are declining with population

increase and with declining agricultural productivity caused by deteriorating soil fertility, among

other factors. In addition, over-fishing is causing declining catches and affecting the earnings from

the fish. Seasonality in time use is another factor that is contributing to poor livelihood because of

the substantial underemployment of the people for most of the year. Poor infrastructure is another

factor that is adversely affecting access to centres of economic activities such as markets hence

leading to limited livelihood sources.

Pervasive risks and high vulnerability to shocks which include rainfall and food price variability

and volatility in space and time, illnesses and deaths. Frequent and widespread existence of shocks

results into large movements into and out of poverty in Malawi. Most households have limited ex

ante strategies to mitigate risks due to lack of access to financial services and poorly functioning

food markets which place a premium on staple production. Households are therefore forced to

11

resort to ex-post coping mechanisms which often deplete household assets and entail permanent

damage to the household‟s ability to engage in productive activities.

In addition to the above two factors, overdependence on rain fed agriculture and limited access to farm

inputs and produce markets have compounded the poverty situation in the country. The Malawi Poverty

and Vulnerability Assessment (GoM/World Bank, 2007) reported that poverty in Malawi manifests itself

through the following: high mortality rates; low life expectancy; and malnutrition. Low school attainment

and poor health and nutritional status during childhood are other major causes of poverty in Malawi.

Although poverty is widespread in Malawi, it is more concentrated in the rural areas and in the southern

region of the country.

2.2 Consequences and Impacts of Poverty

Individuals and households caught up in poverty often face a multitude of problems which have dire

consequences on their livelihoods. Often times the consequences of poverty are pervasive and mutually

reinforcing in that the many effects of poverty lead into its persistence. In Malawi, the poor lack and have

limited access to social and economic services such as health, education, water and sanitation, and food

security. They face high disease burden due to common illnesses such as malaria, diarrhoea, as well as HIV

and AIDS related illnesses. This leads to loss of wellbeing due to loss of productivity from the illnesses

and/or from taking care of the sick. The resultant deaths cause loss of human capital. Children from poor

households tend to have no or limited access to education, which affects their future development and the

earning potential of the households, leading to a vicious cycle of intergenerational poverty.

The level of poverty influences the nutritional status of individuals and households. Extremely poor

households are more likely to suffer from chronic and acute malnutrition due to constant exposure to

hunger and food insecurity. Malnutrition leads to reduced immunity, resulting into increased risk of

morbidity and mortality. Malnutrition also leads to reduced mental and physical development of children,

resulting in poor performance in schools and, therefore, low academic and professional achievements. It is

estimated that productivity losses due to disease, death and reduced earnings potential caused by low

academic achievement will cost Malawi about $446 million between 2006 and 2015 (GoM, 2011).

In Malawi, most poor households earn their livelihoods from on-farm employment. However, with limited

access to land, declining productivity of the land, effects of climate change and environmental degradation,

as well as depressed crop prices and substantial underemployment due to seasonality of the agricultural

sector, there is a substantial proportion of the population which still remains cut off from major economic

activity and livelihood opportunities. From desperation and lack of viable sources of livelihoods, people

that are trapped in poverty engage in coping strategies that are further destructive and harmful to their

livelihoods and the external environment such as selling productive assets, violent crime, prostitution,

burning charcoal, brewing illicit alcoholic beverages and child labour - strategies that exacerbate poverty

in the long term.

2.3 Interventions and Intervention Linkages

Social protection in Malawi is defined in the context of social support which includes all public and private

initiatives that provide income or consumption transfers to the poor, protect the vulnerable against

livelihood risks, and enhance social status and rights of the marginalized. The overall objective is to reduce

ultra-poverty as well as the economic and social vulnerability of poor and marginalized groups (GoM,

2009). The social protection instruments in Malawi are categorized into the following: direct welfare

instruments, productivity enhancing instruments, market interventions and transformative policy changes

(Chirwa, 2010). These can be looked at as a package that is used to target the poor and ultra poor

individuals and households, in order to address their livelihood needs.

12

2.3.1 Direct Welfare Programmes

Direct welfare instruments in Malawi include both conditional and unconditional cash transfers,

supplementary feeding programmes and food aid. There are currently two direct welfare schemes in

Malawi at various levels, as follows:

The SCTP implemented by the GoM at local council levels as described in Section 1 of this report.

The Supplementary Feeding Programmes, particularly the school feeding programmes

implemented in various districts of the country by the Ministry of Education with support from the

World Food Programme (WFP), Mary Meals, Millennium Village Project Zomba and Land O‟

Lakes. These are aimed at improving school enrolment, attendance, retention and the nutrition

status of children of school going age. The WFP‟s School Meals Programme started in 1999 as a

pilot in one district and is currently being implemented in thirteen districts in the southern and

central regions of the country. Mary Meals School Feeding Programme started in 2000 and it

targets districts that are not targeted by the WFP‟s School Feeding Programme.

2.3.2 Productivity Enhancing Programmes

These are Public Works Programmes (PWPs) and Agricultural Subsidy Programmes implemented by the

GoM with support from development partners. Examples of the Productivity Enhancing Programmes in

Malawi include the following:

Public Works Programmes where individuals and households with labor are engaged in various

public works initiatives, and earn income for their labor. An example is the Local Development

Fund Public Works programme (formerly known as MASAF PWP) implemented through local

councils with support from the World Bank. This is a safety net for poor households as a cash

transfer strategy through labor intensive public works that create employment. The main activities

include rehabilitation and construction of economic infrastructures. Another example is the Income

Generating Public Works Programme supported by the European Union, whose main aim is to

achieve durable poverty alleviation and food security by improving the overall socio-economic

status of households through such initiatives as addressing lack of accessibility to rural areas;

developing sustainable fuel wood and timber supplies; improving dry season gardening and

providing an alternative to the distribution of food to needy communities and to replace these food

handouts with projects and activities that enable communities to achieve longer term food security

(Chirwa, 2010).

Farm Input Subsidy Programme (FISP) which aims at promoting access to and use of farm inputs

(mostly fertilizers and improved seed) among smallholder farmers, in order to increase agricultural

productivity. The FISP is largely financed by the GoM with support from development partners

especially through the purchase of improved seed, and the main objective of FISP is to achieve

household food self sufficiency and increased income through increased food and cash crop

production.

2.4 The Policy and Regulatory Environment

The GoM, with support from development partners, developed the National Safety Net Strategy in 2000

and the National Safety Nets Programme (NSNP) in 2001 within the context of the Vision 2020 and the

Poverty Reduction Strategy Paper (PRSP) developed in 2002 to address chronic poverty and vulnerability.

The key objective of the NSNP was to reduce poverty and vulnerability of the poor and most vulnerable

sections of the Malawi society, and it comprised the following sub programmes: Public Works Programme,

Targeted Nutrition Programme, Targeted Inputs Programme, and Direct Welfare Transfer Programme

(GoM, 2011). Implementation of the NSNP faced a number of challenges including poor coordination,

13

inadequate funding, programme design and capacity limitations, and lack of policy guidelines for

implementation of interventions.

Given these challenges, the GoM, in consultation with stakeholders, shifted focus from addressing poverty

and vulnerabilities through safety nets to the social support approach. This change culminated into the

inclusion of the Social Protection and Disaster Risk Reduction theme into the first Malawi Growth and

Development Strategy (MGDS I), a second generation PRSP which was formulated for the period 2006 -

2011. The GoM is also in the process of finalizing the National Social Support Policy whose aim is to

facilitate the implementation of public and private programmes that will provide income or consumption

transfers, protect against vulnerability and enhance the social status and rights of the ultra-poor and the

moderately poor. The policy is yet to be adopted for implementation by Cabinet. In order to support the

implementation of the National Social Protection Policy, the GoM developed the National Social Support

Programme 2011 – 2016 (NSSP) in 2011. The NSSP has the purpose of guiding all social support

stakeholders, including Government, civil society and faith based organizations, the private sector as well

as development partners in championing government priorities on social support. Specifically, the NSSP is

aimed at achieving the following:

Defining key strategies to improve the socio-economic status of the poor and vulnerable.

Providing reference guidelines to all stakeholders in the design, implementation and monitoring of

social support programmes.

Providing guidelines for cost effective, predictable and sustainable interventions to the benefit of

beneficiaries, implementers and financiers.

Establishing an institutional framework with the mandate to initiate, coordinate, implement,

monitor and evaluate social support programmes.

The development and envisaged implementation of the NSSP has strong linkages with other national

economic and social policies and with disaster risk reduction strategies, including the following: the revised

National HIV and AIDS Policy; The National Youth Policy; the Agriculture and Food Security Policy; The

National Gender Policy; the National Policy on Orphans and Vulnerable Children; the Sexual and

Reproductive Health Policy; Early Childhood Care and Development Policy; the National Environment

Policy; the National Land Policy; the Equalisation of Opportunities (Disability) Policy; the Decentralization

Policy; the National Nutrition Policy and Strategy; and other relevant programmes in agriculture, education,

health and labour. It is expected that through synergies with these policies, the NSSP will contribute to

asset creation and protection, income generation; strengthen human capital and stimulate economic

activities; promote social empowerment, reduce income inequality and break intergenerational cycle of

poverty; and ensure social and political stability and fulfilment of human rights and freedoms (GoM, 2011).

The NSSP also recognises the existence of global and regional development frameworks such as the

Millennium Development Goals (MDGs), the Universal Declaration on Human Rights, the Convention on

the Rights of the Child (CRC), and the Convention on the Elimination of all forms of Discrimination

against Women.

In the MGDS II which succeeded the MGDS I, Government has also included a theme on Social Support

and Disaster Risk Management. The interventions on poverty and vulnerabilities in the MGDS are closely

related to the interventions under other themes, especially on Sustainable Economic Growth, Social

Development and cross cutting issues.

There is concern among stakeholders, however, that extended delays in the adoption of the National Social

Protection Policy reflect the GoM‟s lack of commitment to social protection. It is speculated that the

adoption of the policy could unlock resources into social protection.

14

3. National Poverty Profile and SCTP Beneficiary Targeting

3.1 Measures of Poverty in Malawi

Malawi principally uses a national measure of poverty and equality that compares the income measure of an

individual‟s consumption-related expenditure with a cost-of-basic-needs threshold. This is a common

procedure adopted by the World Bank for developing countries. In practice, this poverty assessment

procedure uses a household welfare indicator defined as the total annual per capita consumption

expenditure (including implicit expenditure of own production) reported by a household. This is expressed

in Malawi kwacha, deflated to February/March 2004 prices3. Second, a threshold level of welfare that

distinguishes between poor and non-poor households is established, and defines the poverty line. The

poverty line is technically a subsistence minimum based on the cost-of-basic-needs methodology, and

comprises two parts as already described in Section 2.1 above: (a) minimum food expenditure based on the

food requirements of an individual, tied to the recommended daily calorie requirement - which defines the

ultra-poverty line; and (b) critical non-food consumption, estimated based on the expenditure patterns of

households whose total expenditure is close the minimum food expenditure. The sum of the minimum food

and non-food expenditures define the poverty line. Individuals or households whose consumption is lower

than the poverty line are poor, while those whose total expenditure falls short of that necessary to meet the

minimum food requirements are ultra-poor. This process provides an absolute measure of poverty. The

poverty and ultra-poverty lines were established as K16,165 and K10,029 per person per year in 2004 (IHS,

2005). The poverty gap4 in Malawi was estimated at 17.8% overall and 5.3% among the ultra poor. This

meant that the poor on average were subsisting on 17.8% less than the poverty line, and the ultra poor on

average survived on 5.3% less than the ultra-poverty line. The poverty line of K16,165 was equal to K44.3

or US$0.5 per person per day, and the ultra-poor were subsisting on less than K26.40 per person per day.

As an alternative, the World Bank commonly measures national poverty in terms of the ability of a person

to live on at least the local currency equivalent of $1.25 per day at 2005 international prices (i.e., adjusted

for purchasing power parity (PPP) at the dollar value in 2005). Using the latest available PPP conversion

factor of K58.597 = $1.00, the implied poverty line for Malawi is K19,468 per person per annum. It is clear

that this measure is in respect of poverty per se, and cannot be compared with the ultra-poverty measure

that is most relevant in the context of the SCTP.

A poverty headcount ratio measures the proportion of the population that lives below the defined poverty

line. Based on IHS (2005) computations and subsequent data annually generated through the WMSs, the

National Statistical Office releases poverty headcount ratios for Malawi. The available headcount ratio

based on the $1.25/day measure is for 2004. The ratios based on IHS and WMS are also available by region

and rural-urban split up to 2009, and by district up to 2007. Table 4 shows the available published ratios for

Malawi. Significant progress was made in reducing poverty between 2004 and 2006, but this slowed down

thereafter. Most of the poor live in rural areas, but a possible increase in urban poverty is discernible. Since

the poverty line based on the $1.25/person/day measure is generally higher, this measure tends to report

higher poverty incidence than the national measure. Moreover, because the post-2004 poverty statistics are

based on IHS (2005), their reliability tends to decline over time. It is anticipated that the latest IHS

conducted in 2011, whose outcomes have not yet been published, will provide a better picture of the status

of poverty in Malawi.

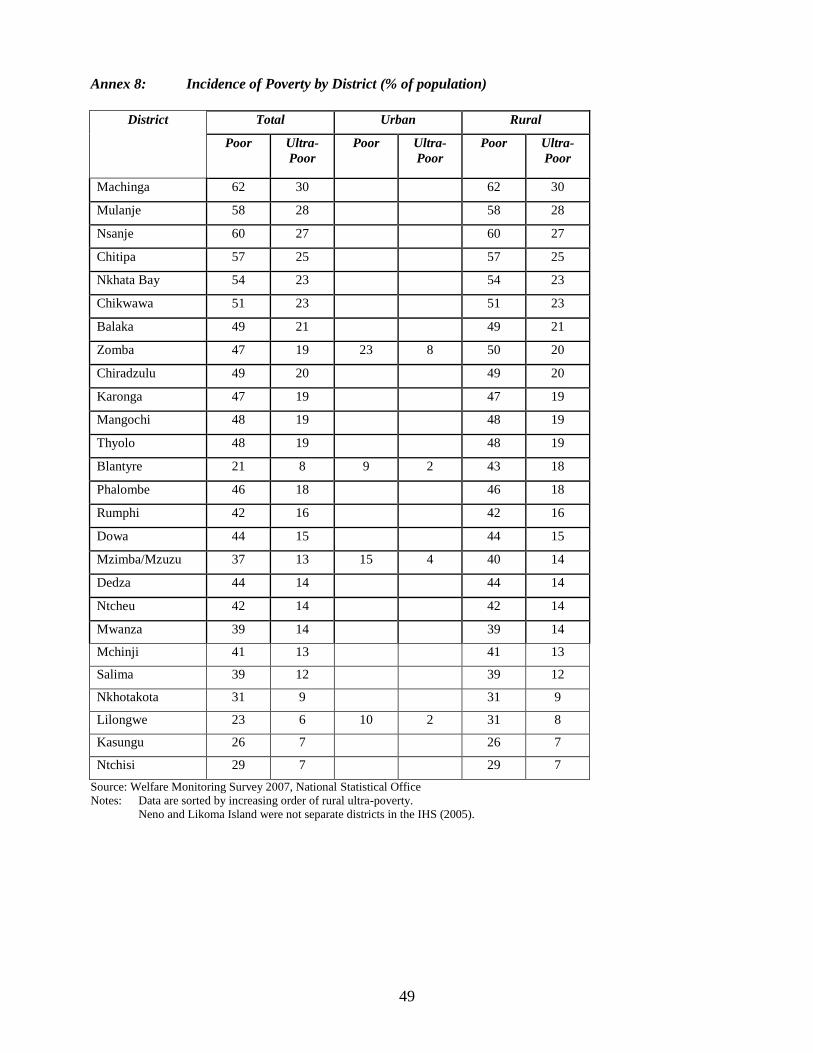

Table 4 also shows that the incidence of poverty has a geographical perspective in Malawi. More

specifically, Annex 8 shows the poverty incidence by district in 2007. The southern region has a greater

share of the poor with poverty and ultra-poverty incidences being higher than anywhere else in the country.

3The IHS (2005) upon which the calculations are based was conducted in this period.

4 The poverty gap is defined in terms of how far below the poverty line households are found, on average, expressed

as a percentage of the poverty line. Those households that are close to the poverty line could be improved out of

poverty with less effort than those that are far below the line

15

The poorest three districts in Malawi were all in the Southern Region (Machinga, Mulanje, Zomba), and the

least poor rural districts in Malawi were all in the Central Region (Ntchisi, Kasungu, Lilongwe). The

poorest urban area was Zomba City and the richest was Blantyre City. According to the Malawi Poverty

and Vulnerability Assessment (2007), the prevalence of ultra-poverty in Malawi is higher in the following

categories: female headed households; households headed by very young or old persons; households

located in the rural areas of the South and Central regions; larger households especially households with

more young children and dependents; and households with low levels of education, limited economic

opportunities, limited involvement in cash crops, and small landholdings. A more recent presentation of this

information – which is key for the transfer level costing procedures developed in this study – is unavailable.

Table 4: Incidence of Poverty in Malawi (2004 – 2009)

Poverty Measure

Headcount (% of population)

IHS 2

2004

WMS

2005

WMS

2006

WMS

2007

WMS

2008

WMS

2009

Poor – IHS (2005) – Malawi

Urban

Rural

52

25

50

24

53

45

25

47

40

11

44

40

13

44

39

14

43

Ultra-Poor (IHS (2005) – Malawi

Urban

Rural

22

8

21

8

23

17

6

19

15

2

17

15

3

17

15

3

17

Poor ($1.25/person/day – Malawi 74

3.2 Beneficiary Targeting in the SCTP

The SCTP in Malawi qualifies as what is called a needs-based social assistance programme. Typically, such

programmes provide a monthly cash transfer to the poorest households based on a needs assessment. Apart

from Eastern Europe and the former Soviet Union where these programmes are common, such last resort

programmes have also been implemented in African countries such as Mozambique, South Africa, Kenya,

Tanzania, Senegal, Cameroon and Zambia (Arnold et al., 2011; Slater et al., 2010; ADB, 2006; Gassmann

& Behrendt, 2006; Devereux et al., 2005; Schubert, 2005). Several methods are used in the identification of

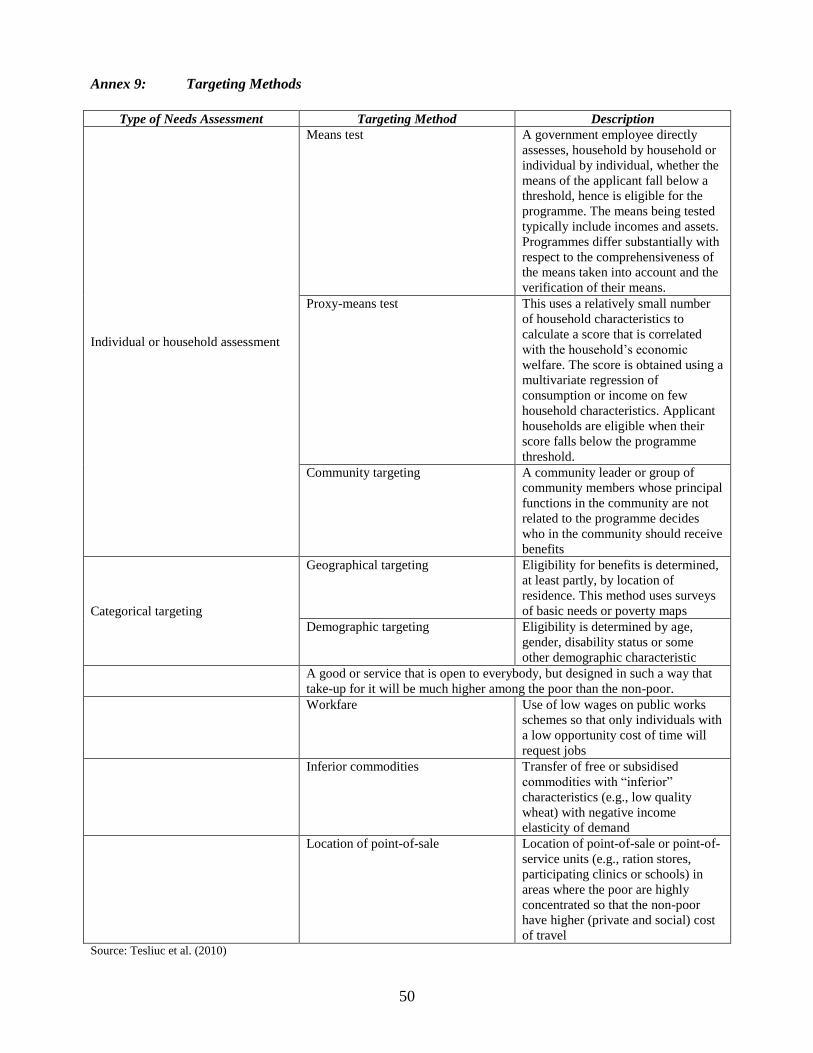

the target groups in social security programmes in general, as summarised in Annex 9. In terms of needs-

based programmes such as the SCTP, beneficiaries are usually identified based on a means test, a proxy

means test, or a combination of the two (Grosh, 2009). In Mozambique and Zambia, the combination

approach was adopted. It is a general rule to keep the design of these programmes simpler in low-income,

low capacity countries, and more sophisticated in middle income countries.

The targeting of beneficiaries is known to be problematic when a significant proportion of the population is

poor and income differences in the bottom deciles are marginal (Ellis, 2009; Slater et al., 2010). A

fundamental point in the identification of the target group is the determination of the population that should

be targeted. In most middle income countries, such programmes have tended to target between 3% and 10%

poorest proportion of the population. The eligible target groups nationally comprise 10% of the population

in Zambia and Malawi, and 19% in Kenya (Slater et al., 2010). This determination requires a national

process for assessing the poverty profile of the country‟s population, hence the determination of the poor

and non-poor.

The Malawi SCTP is designed to target the poorest 10% of the population, categorised as ultra-poor and

labour-constrained. The ultra-poor constituted 15% of the population during the period 2007 - 2009, such

that the SCTP target group coincidentally constituted two-thirds of the ultra-poor in that period5. By these

criteria, it was officially estimated that there were about 300,000 eligible households in Malawi, based on

IHS (2005) (see GoM, 2010).

5 However, the ultra-poor constituted 22% of the population in 2006, such that the 10% programme target represented

less than one half of the ultra-poor.

16

As reported by Miller et al. (2008), the SCTP in Malawi uses a community based, multi-stage participatory

targeting process. Community volunteers determine the eligible households in their villages, guided by the

programme‟s Manual of Operations which provides “proxies” of poverty for community members to

consider (e.g., the poorest households eat only one meal per day). The procedure involves household

interviews conducted by the Community Social Support Committee (CSSC) trained by the district SCT

secretariat; verification of the interview results by a community meeting at which eligible households are

identified; verification of the eligibility of households by extension workers; and consideration and

approval of the proposed list of eligible households by a district-level Social Support Committee. Ideally,

this process aims at selecting the neediest households up to a cut-off point, which currently ought to be two-

thirds of the ultra-poverty incidence for the district in order to ensure that the poorest and labour-

constrained 10% of the population is targeted. Miller (2009) notes that proxy means testing is somewhat

used in the Malawi SCTP, but there is need to ensure that the proxy is appropriate, well-understood, easy to

identify and field-tested. The GoM (2010) also proposes that the targeting process should be formally

verified by a proper proxy means test, in order to increase objectivity.

Evidence on the ground suggests that the Malawi SCTP targeting process simply seeks to identify the

poorest 10% of the population in each district, without regard for the district‟s poverty profile in relation to

other districts in the country. This suggests that the programme may not be targeting the poorest households

when the national picture is considered. Additionally, while the normal procedure is to start with

programme implementation among the poorest individuals, households and geographical areas (Arnold,

2011, Samson et al., 2006), it is the case that the project was initially piloted in Mchinji which had only the

ninth highest incidence of ultra-poverty in 2004 and the sixth lowest incidence in 2007. Apart from

Machinga (highest incidence in 2007), the inclusion of the ultra-poorest districts in the piloting phase has

not been high. It is understood that, among other considerations, Mchinji was chosen in order to facilitate

the administration of the piloting phase, because it was then the poorest among districts that are close to

Lilongwe.

3.3 Determination of Target Beneficiary Households

This study estimates the total number of eligible beneficiary households for 2012 using the following

procedure. Let i denote a specific district and t denote the current period (year). Recognise that, currently,

the published census data do not report the annual intercensal growth rates in the number of households per

district, and that these are inherently different from the annual intercensal growth rates in the „population‟

per district. Then:

a. The annual growth rate in the number of households for each district i is calculated by iteratively

solving for the district-specific compound rate ( ir ) in the compounding formula:

10

98,08, 1 iii rPP

where ir = annual intercensal growth rate in the number of households for district i

08,iP = number of households in district i in 2008

98,iP = number of households in district i in 1998

National Census data are used to obtain 08,iP and 98,iP

b. The total number of households per district in 2008 obtained from the 2008 Population and

Housing Census is compounded at the rate of ir as calculated above, to obtain an estimate of the

number of households per district in 2012, say 12,ihh . For Neno, Balaka and the four cities, where

necessary, data splitting is accomplished in relation to Mwanza, Machinga and the corresponding

host districts for the cities respectively, by assuming constant population proportions.

17

c. The estimated number of households per district is summed up to obtain the estimated total number

of households in Malawi in 2012, say 12HH . The available data yield:

083,191,312,12 i

ihhHH

d. We take 10% of 12HH as the SCTP national target number of beneficiary households in 2012

(denoted 12T ), in line with the SCTP design. The available data yield:

108,3191.0 1212 HHT

e. Let u

ih be the ultra-poverty headcount ratio for each district i . The number of ultra-poor

households per district in 2012 (say u

ihh 12, ) is calculated by multiplying the number of households

per district obtained in (b) above by the ultra-poverty headcount ratio for the district. That is,

12,12, i

u

i

u

i hhhhh . Since u

ih are not reported annually for each district, the latest available ultra-

poverty headcount ratios established in the WMS (2007) are used.6 For Likoma and Neno, the

respective percentages applied relate to Nkhata Bay and Mwanza7.

f. We sum up the numbers of ultra-poor households across districts to obtain the total number of

ultra-poor households in Malawi in 2012 (say uHH12 ). The available data yield:

370,47812,12 i

u

i

u hhHH .

g. Since data on labour-constrained ultra-poor households is not reported (see Box 1), we propose that

the national target number of beneficiary households should be distributed across districts on the

basis of ultra-poverty headcount ratios. Therefore, we calculate each district‟s share (proportion) of

ultra-poor households in Malawi in 2012 as:

u

u

iu

iHH

hhp

12

12,

12, .

h. Determine the number of STCS target beneficiary households per district in 2012 (say 12,it ) as

being equal to 1212,12, Tpt u

ii , such that the sum of these district households equals the total

national target number of beneficiary households. Thus:

i

i Tt 108.3191212,

The procedure described above can improve with the availability of data as described in Box 1. It is

recommended that the National Statistical Office should consider addressing these data requirements.

6Just as the growth rate in population does not necessarily correspond with the growth rate in the number of

households, the poverty incidences may differ between population and households. We do not have adequate data to

calculate the ultra-poverty incidence at the household level in 2012. This discrepancy may, however, be very minimal. 7While this is a reasonable assumption in relation to Neno, it may not be equally reasonable for Likoma whose socio-

economic profile is typically different from that of Nkhata Bay.

18

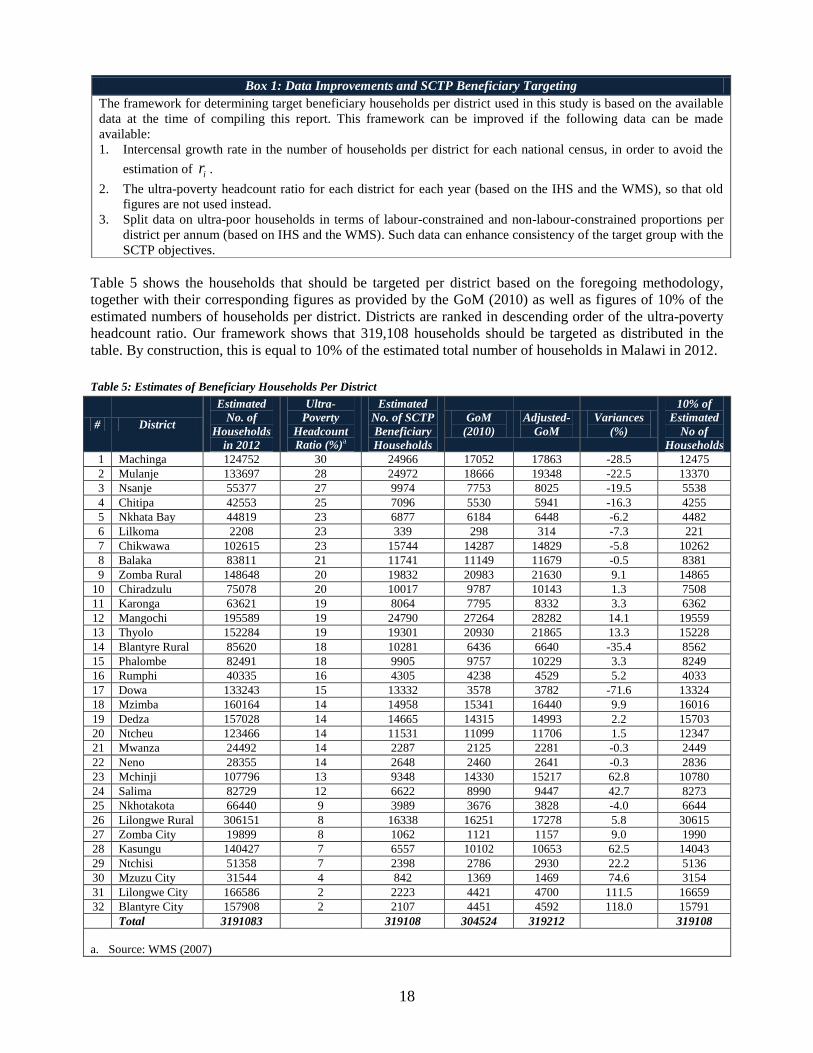

Table 5 shows the households that should be targeted per district based on the foregoing methodology,

together with their corresponding figures as provided by the GoM (2010) as well as figures of 10% of the

estimated numbers of households per district. Districts are ranked in descending order of the ultra-poverty

headcount ratio. Our framework shows that 319,108 households should be targeted as distributed in the

table. By construction, this is equal to 10% of the estimated total number of households in Malawi in 2012.

Table 5: Estimates of Beneficiary Households Per District

# District

Estimated

No. of

Households

in 2012

Ultra-

Poverty

Headcount

Ratio (%)a

Estimated

No. of SCTP

Beneficiary

Households

GoM

(2010)

Adjusted-

GoM

Variances

(%)

10% of

Estimated

No of

Households

1 Machinga 124752 30 24966 17052 17863 -28.5 12475

2 Mulanje 133697 28 24972 18666 19348 -22.5 13370

3 Nsanje 55377 27 9974 7753 8025 -19.5 5538

4 Chitipa 42553 25 7096 5530 5941 -16.3 4255

5 Nkhata Bay 44819 23 6877 6184 6448 -6.2 4482

6 Lilkoma 2208 23 339 298 314 -7.3 221

7 Chikwawa 102615 23 15744 14287 14829 -5.8 10262

8 Balaka 83811 21 11741 11149 11679 -0.5 8381

9 Zomba Rural 148648 20 19832 20983 21630 9.1 14865

10 Chiradzulu 75078 20 10017 9787 10143 1.3 7508

11 Karonga 63621 19 8064 7795 8332 3.3 6362

12 Mangochi 195589 19 24790 27264 28282 14.1 19559

13 Thyolo 152284 19 19301 20930 21865 13.3 15228

14 Blantyre Rural 85620 18 10281 6436 6640 -35.4 8562

15 Phalombe 82491 18 9905 9757 10229 3.3 8249

16 Rumphi 40335 16 4305 4238 4529 5.2 4033

17 Dowa 133243 15 13332 3578 3782 -71.6 13324

18 Mzimba 160164 14 14958 15341 16440 9.9 16016

19 Dedza 157028 14 14665 14315 14993 2.2 15703

20 Ntcheu 123466 14 11531 11099 11706 1.5 12347

21 Mwanza 24492 14 2287 2125 2281 -0.3 2449

22 Neno 28355 14 2648 2460 2641 -0.3 2836

23 Mchinji 107796 13 9348 14330 15217 62.8 10780

24 Salima 82729 12 6622 8990 9447 42.7 8273

25 Nkhotakota 66440 9 3989 3676 3828 -4.0 6644

26 Lilongwe Rural 306151 8 16338 16251 17278 5.8 30615

27 Zomba City 19899 8 1062 1121 1157 9.0 1990

28 Kasungu 140427 7 6557 10102 10653 62.5 14043

29 Ntchisi 51358 7 2398 2786 2930 22.2 5136

30 Mzuzu City 31544 4 842 1369 1469 74.6 3154

31 Lilongwe City 166586 2 2223 4421 4700 111.5 16659

32 Blantyre City 157908 2 2107 4451 4592 118.0 15791

Total 3191083 319108 304524 319212 319108

a. Source: WMS (2007)

Box 1: Data Improvements and SCTP Beneficiary Targeting

The framework for determining target beneficiary households per district used in this study is based on the available

data at the time of compiling this report. This framework can be improved if the following data can be made

available:

1. Intercensal growth rate in the number of households per district for each national census, in order to avoid the

estimation of ir .

2. The ultra-poverty headcount ratio for each district for each year (based on the IHS and the WMS), so that old

figures are not used instead.

3. Split data on ultra-poor households in terms of labour-constrained and non-labour-constrained proportions per

district per annum (based on IHS and the WMS). Such data can enhance consistency of the target group with the

SCTP objectives.

19

Although our estimate of eligible households is slightly higher than that of 304,524 reported by the GoM

(2010), the GoM figure becomes a close 319,212 when the district target numbers of households are

compounded for two years at the intercensal household growth rates derived in this study, to obtain the

Adjusted-GoM estimates reported in the table. However, there are discernible variations in terms of target

beneficiaries in specific districts when our estimates are compared with the Adjusted-GoM estimates.

Relative to our framework, the Adjusted-GoM framework proposes significantly more households to be

targeted in the cities of Blantyre, Lilongwe and Mzuzu as well as the relatively well-off districts of Mchinji

and Salima. On the other hand, the Adjusted-GoM framework includes much fewer target households in the

poorer districts of Machinga, Mulanje, Nsanje, and Chitipa, but lower quotas are also suggested for Dowa

and Blantyre Rural. Reconciling these deviations can be a matter of necessity in order to enhance targeting

objectivity.

Currently, the SCTP targets 10% of each district‟s population regardless of district-specific poverty

profiles. The current procedure advantages districts with low poverty ultra-incidences and disadvantages

the poorest (hence most eligible) districts. Foe example, our procedure suggests that 24,966 households

should be targeted in Machinga (about twice as many as those suggested by the flat 10% rule), while only

2,107 households should benefit in Blantyre City (compared with 15,791 households by the current

practice). Clearly, the proposed procedure would enhance objectivity in the identification of beneficiaries.

4. Determination of Cash Transfer Levels

4.1 The Literature

No clear answer exists in the literature regarding what the appropriate transfer level should be (or how

generous the programme should be to the target group). Teslius et al. (2010) notes that, ultimately, the

transfer level becomes one of the products of designing the programme in the sense that the level should fit

within the programme‟s budgetary, administrative and political constraints, while also maximising

outcomes on its intended objectives. In general, last resort programmes such as the SCTP aim to reduce

poverty, such that the benefit level is typically set as a fraction of the income (or poverty) gap of expected

beneficiaries. Variations exist to this general rule. For instance, in low income countries, it is common to

set benefits relative to the cost of an “adequate” food basket or the food poverty line. The cash transfer

programme for Kalomo in Zambia pays $10 per month to a beneficiary household, equivalent to the cost of

a 50 kilogram bag of maize. Some guaranteed minimum income (GMI) programmes in Europe and Central

Asia provide a transfer equivalent to the difference between the eligibility threshold and the income of each

family. Procedures that compensate beneficiaries for one element of expenditure – called gap formulas –

are also used for family allowances that cover a portion of the cost of such expenditure, such as the cost of

raising or educating a child, or food stamps that cover the food poverty gap. Conditional cash transfer

(CCT) programmes encourage poor beneficiaries to invest in children‟s human capital by conditioning the

benefit on the use of school, nutrition and/or health services. Thus, the level of benefits in CCT

programmes reflects two objectives: reducing beneficiaries‟ poverty (as in last resort programmes) and

providing incentives for human capital accumulation (typically through education, nutrition or health

grants). In the Family Allowance Programme in Honduras and the Social Protection Network in Nicaragua,

supply grants were offered to the service providers – schools and health facilities (Teslius et al., 2010).

The programme‟s overall budget constraint is the key second consideration in setting the transfer level.

Once information on the number of „deserving‟ beneficiaries and their corresponding income gaps is

obtained, policy makers can estimate the overall resource deficit among the poor, and determine whether or

not covering such a deficit is affordable. The initial estimate of the financial effort required to eliminate

poverty is usually larger that the available resources. This imbalance is typically dealt with through an

iterative process where the generosity and/or the coverage of the programme is typically restricted to the

poorest and most destitute (Teslius et al., 2010 p15). The ultimate programme design also has to consider

the need to balance between finding a transfer level that is neither too high to generate dependency, nor too

20

low to lack impact. Too generous a transfer level may have adverse consequences, such as reducing work

incentives or crowding out private transfers. Too low a benefit would prevent the programme from

achieving its intended objectives. As an illustration, a transfer value limited to 10% to 30% of the ultra-

poverty line has become an accepted practice in several programmes in Africa, irrespective of national or

local poverty profiles or income levels. However, limiting the transfer in this way, while making it

affordable, carries the risk that it may not have a significant impact on poverty, and may undermine the

purpose of the programme (Slater et al., 2010).

Comprehensive SCT programmes can be quite expensive. In 2009, South Africa invested over 3% of its

national income and more than 10% of government spending on its comprehensive social grants system.

However, there is evidence that adequate political will is key to the affordability of SCT programmes, and

that these programmes can be made affordable in many low income countries when there is such will

(Samson, 2009).

Other considerations in the determination of benefit formulas include whether these should be tailor-made

to the characteristics of beneficiaries. Benefit formulas may be flat (i.e. giving the same benefit to all

beneficiaries) or they may vary according to beneficiary characteristics. Benefits may vary by several

criteria, including household size, age of household members, gender, time of year, geographical area,

longevity in the programme, and promotion of preferred behavioural changes (Teslius et al., 2010 p16).

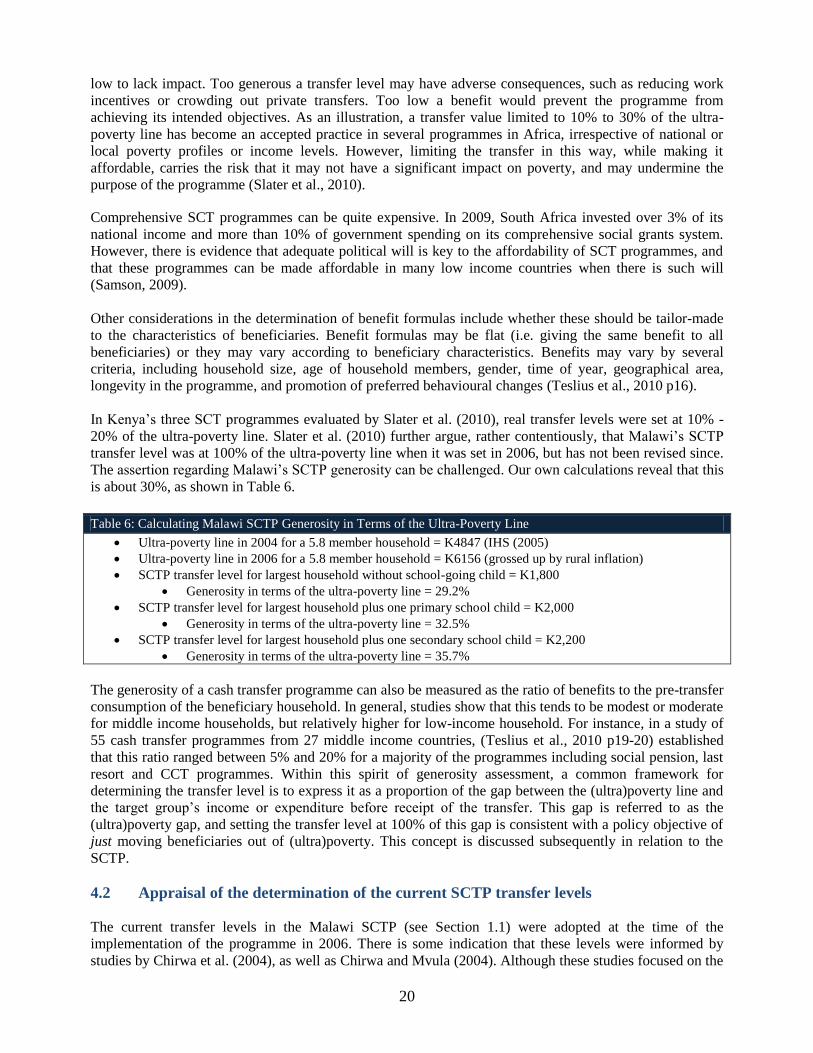

In Kenya‟s three SCT programmes evaluated by Slater et al. (2010), real transfer levels were set at 10% -

20% of the ultra-poverty line. Slater et al. (2010) further argue, rather contentiously, that Malawi‟s SCTP

transfer level was at 100% of the ultra-poverty line when it was set in 2006, but has not been revised since.

The assertion regarding Malawi‟s SCTP generosity can be challenged. Our own calculations reveal that this

is about 30%, as shown in Table 6.

Table 6: Calculating Malawi SCTP Generosity in Terms of the Ultra-Poverty Line

Ultra-poverty line in 2004 for a 5.8 member household = K4847 (IHS (2005)

Ultra-poverty line in 2006 for a 5.8 member household = K6156 (grossed up by rural inflation)

SCTP transfer level for largest household without school-going child = K1,800

Generosity in terms of the ultra-poverty line = 29.2%

SCTP transfer level for largest household plus one primary school child = K2,000

Generosity in terms of the ultra-poverty line = 32.5%

SCTP transfer level for largest household plus one secondary school child = K2,200

Generosity in terms of the ultra-poverty line = 35.7%

The generosity of a cash transfer programme can also be measured as the ratio of benefits to the pre-transfer

consumption of the beneficiary household. In general, studies show that this tends to be modest or moderate

for middle income households, but relatively higher for low-income household. For instance, in a study of

55 cash transfer programmes from 27 middle income countries, (Teslius et al., 2010 p19-20) established

that this ratio ranged between 5% and 20% for a majority of the programmes including social pension, last

resort and CCT programmes. Within this spirit of generosity assessment, a common framework for

determining the transfer level is to express it as a proportion of the gap between the (ultra)poverty line and

the target group‟s income or expenditure before receipt of the transfer. This gap is referred to as the

(ultra)poverty gap, and setting the transfer level at 100% of this gap is consistent with a policy objective of

just moving beneficiaries out of (ultra)poverty. This concept is discussed subsequently in relation to the

SCTP.

4.2 Appraisal of the determination of the current SCTP transfer levels

The current transfer levels in the Malawi SCTP (see Section 1.1) were adopted at the time of the

implementation of the programme in 2006. There is some indication that these levels were informed by

studies by Chirwa et al. (2004), as well as Chirwa and Mvula (2004). Although these studies focused on the

21

determination of the minimum wage for PWPs, their wage determination procedure recognised that the

PWPs implemented in Malawi have explicit poverty reduction and livelihoods objectives. As such, the

studies used a poverty line analysis, which derived the following outcomes at 2004 prices:

The IHS poverty line: Grossing up the IHS (1998) poverty line with rural inflation, the monthly

household food poverty line was K4,099, and increased to K5,465 when non-food costs (estimated

at 20%) were included.

The subsistence basket poverty line: Basing on the cost of purchasing a basket of subsistence

consumption food items that would provide a household with 2,100 calories per person per day as

required by WFP, a monthly household subsistence basket (SB) poverty line of K2,917 was

obtained, which increased to K3,501 when non-food costs were added at 20%.

The perceived needs poverty line: Using information on the cost of a bundle of goods considered

necessary for subsistence obtained from workers in a sample PWP implemented by the Malawi

Social Action Fund (MASAF), a perceived needs (PN) poverty line of K2,125 per six-member

household per month for food only was derived, which increased to K2,745 when non-food cost

were added.

The foregoing studies also considered other sources of household income as well as own production in the

determination of the PWP wage rate. The respective monthly wages required to meet subsistence needs

after adjusting for other income sources in the three scenarios (IHS, SB, and PN poverty lines) were

K2,900, K2,075 and K1,500 when food costs only were considered. These increased to K4,275, K2,675 and

K2,100 when non-food costs were added, respectively. Ultimately, the study based its recommendations on

the outcome of the perceived needs analysis, with the implication that the PWP daily wage rate should be

between K83 and K107 at 2004 prices.

The link between this framework and the determination of the transfer levels adopted by the SCTP remains

unclear, but can possibly be constructed. For instance, a household of at least 4 members with one primary

school child and one secondary school child would earn K2,400 in the SCTP, which falls within the

monthly wage range of K2,075 - K2,675 proposed under the PN poverty line approach.

However, in Miller et al. (2008) and during interviews in the context of this study, it was established that

the average transfer to a household was K2,000, which is at the lower end of the monthly wage range

suggested by the perceived needs approach. Moreover, since the SCTP targets the ultra-poor and labour-

constrained, it is also clear that the adjustment for additional sources of income and own production was

necessary in the context of the PWP, but not the SCTP. Instead, the monthly wages implied by these

procedures should have been adjusted for the average monthly household expenditures of the relevant target

group.

There are indications, substantiated during this study, that the actual determination of the SCTP transfer

levels may have been guided by the reasoning that it should afford a six-member household the equivalent

of some 2 bags of maize weighing 50 kilograms each. The cost of such a bag was around K900 during

2006, which establishes the maximum value of the transfer level based on the household size (i.e., K1,800).

To determine the transfer level for a one-person household, moral consideration was made that such a

transfer should be lower than the lowest pension paid to a retired public servant, then estimated at K700 per

month. In 2011-2012, the minimum cost of a 50 kilogram bag of maize was K1,500, while the lowest

pension paid was in the region of K1,400. These statistics would suggest a 2012 transfer level of, say,

K1,300 for a one-person household and K3,000 for the largest household. These are 116.7% and 66.7%

higher than the current levels.

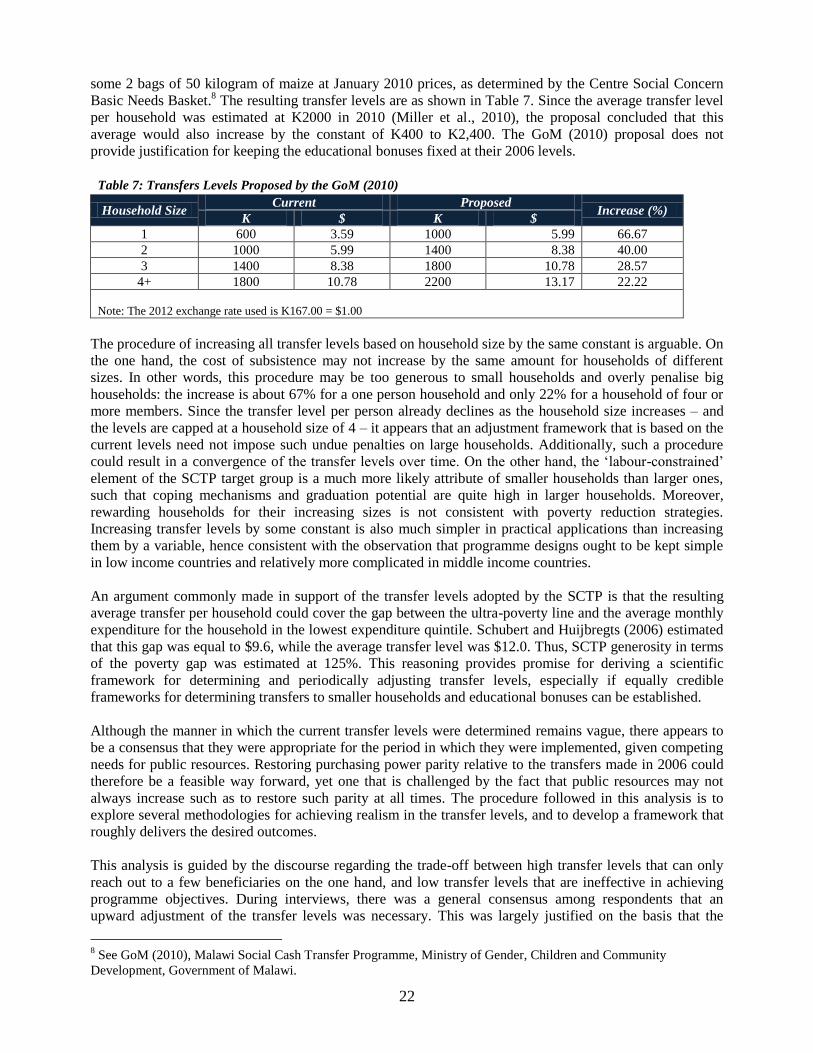

In 2010, the GoM proposed that all the transfer levels based on household size should be increased by

K400, guided by requirement that the transfer to a six-member household should afford such a household

22

some 2 bags of 50 kilogram of maize at January 2010 prices, as determined by the Centre Social Concern

Basic Needs Basket.8 The resulting transfer levels are as shown in Table 7. Since the average transfer level

per household was estimated at K2000 in 2010 (Miller et al., 2010), the proposal concluded that this

average would also increase by the constant of K400 to K2,400. The GoM (2010) proposal does not

provide justification for keeping the educational bonuses fixed at their 2006 levels.

Table 7: Transfers Levels Proposed by the GoM (2010)

Household Size Current Proposed

Increase (%) K $ K $

1 600 3.59 1000 5.99 66.67

2 1000 5.99 1400 8.38 40.00

3 1400 8.38 1800 10.78 28.57

4+ 1800 10.78 2200 13.17 22.22

Note: The 2012 exchange rate used is K167.00 = $1.00

The procedure of increasing all transfer levels based on household size by the same constant is arguable. On

the one hand, the cost of subsistence may not increase by the same amount for households of different

sizes. In other words, this procedure may be too generous to small households and overly penalise big

households: the increase is about 67% for a one person household and only 22% for a household of four or

more members. Since the transfer level per person already declines as the household size increases – and

the levels are capped at a household size of 4 – it appears that an adjustment framework that is based on the

current levels need not impose such undue penalties on large households. Additionally, such a procedure

could result in a convergence of the transfer levels over time. On the other hand, the „labour-constrained‟

element of the SCTP target group is a much more likely attribute of smaller households than larger ones,

such that coping mechanisms and graduation potential are quite high in larger households. Moreover,

rewarding households for their increasing sizes is not consistent with poverty reduction strategies.