Embed Size (px)

Citation preview

Cost Accounting Horngreen, Datar, Foster

Cost terms and Purposes revisited

1

Cost Accounting Horngreen, Datar, Foster

Cost and Cost Terminology

Cost is a resource sacrificed or forgone to achieve a specific objective.It is usually measured as the monetary amount that must be paid to acquire goods and services.An actual cost is the cost incurred (a historical cost) as distinguished from budgeted costs. A cost object is anything for which a separate measurement of costs is desired.

2

Cost Accounting Horngreen, Datar, Foster

Cost and Cost Terminology

There are two basic stages of accounting for costs:1 Cost accumulation2 Cost assignment to various cost objects

CostAccumulation

Cost Object

Cost Object

Cost Object

Cost Assignment

3

Cost Accounting Horngreen, Datar, Foster

Cost and Cost Terminology

Cost accumulation is the collection of cost data in some organized way by means of an accounting system.Cost assignment is a general term that encompasses...– tracing accumulated costs to a cost object, and– allocating accumulated costs to a cost object.

4

Cost Accounting Horngreen, Datar, Foster

Direct Costs

Direct costs of a cost object are those that are related to a given cost object (product, department, etc.) and that can be traced to it in an economically feasible way.Cost-Tracing describes the assignment of direct costs to the particular cost object.

5

Cost Accounting Horngreen, Datar, Foster

Indirect Costs...

– are related to the particular cost object but cannot be traced to it in an economically feasible way.

6

Cost Accounting Horngreen, Datar, Foster

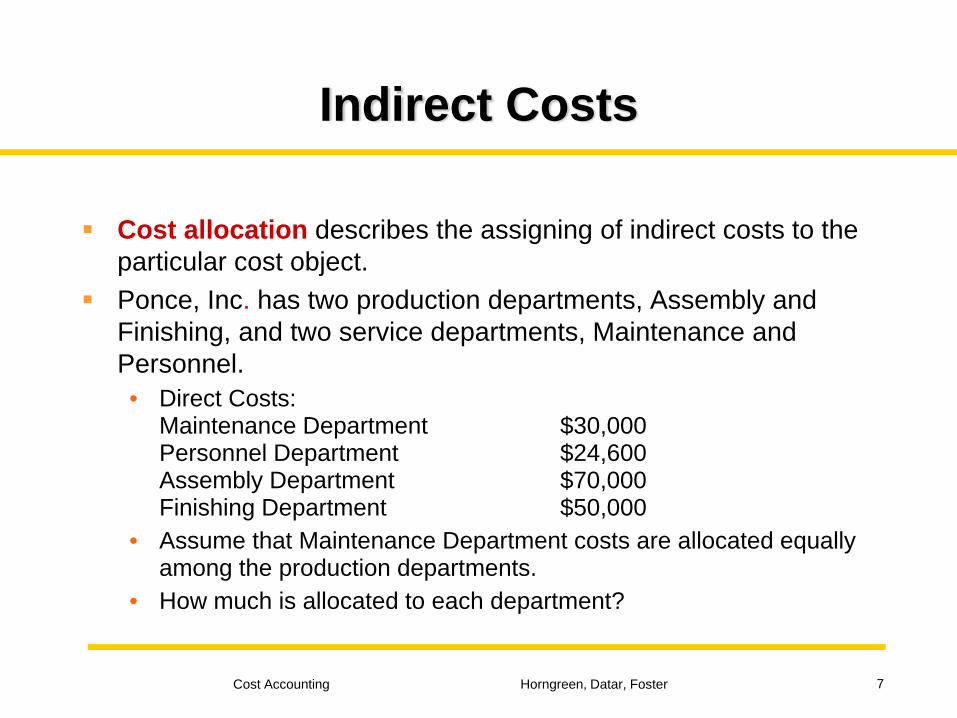

Indirect Costs

Cost allocation describes the assigning of indirect costs to the particular cost object.Ponce, Inc. has two production departments, Assembly and Finishing, and two service departments, Maintenance and Personnel.• Direct Costs:

Maintenance Department $30,000 Personnel Department $24,600 Assembly Department $70,000 Finishing Department $50,000

• Assume that Maintenance Department costs are allocated equally among the production departments.

• How much is allocated to each department?

7

Cost Accounting Horngreen, Datar, Foster

Direct and Indirect Costs

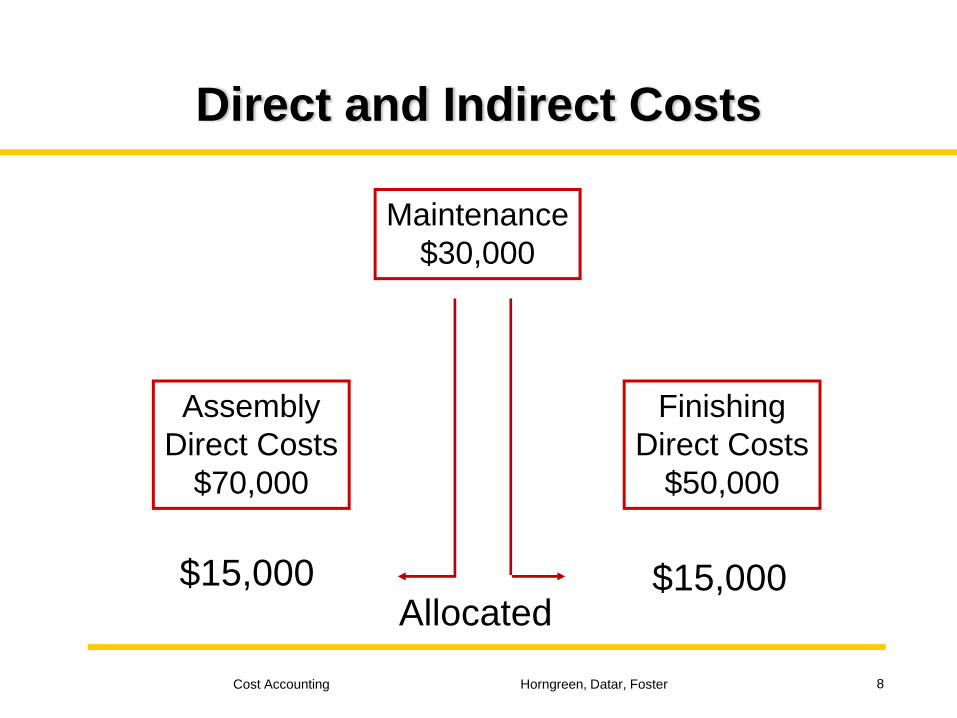

Allocated$15,000 $15,000

Maintenance$30,000

AssemblyDirect Costs

$70,000

FinishingDirect Costs

$50,000

8

Cost Accounting Horngreen, Datar, Foster

Direct and Indirect Costs

Several factors affect the classification of a cost as direct or indirect:– The materiality of the cost in question– Available information-gathering technology– Design of operations– Contractual arrangements

The direct/indirect classification depends on the choice of the cost object.

9

Cost Accounting Horngreen, Datar, Foster

Cost Behavior Patterns

Variable costs change in total in proportion to changes in the related level of total activity or volume.Fixed costs do not change in total for a given time period despite wide changes in the related level of total activity or volume.Assume that Metairie Bicycles buys a handlebar at $52 for each of its bicycles.Total handlebar cost is an example of a cost that changes in total in proportion to changes in the number of bicycles assembled (variable cost).What is the total handlebar cost when 1,000 bicycles are assembled?

10

Cost Accounting Horngreen, Datar, Foster

Cost Behavior Patterns

1,000 units x $52 = $52,000What is the total handlebar cost when 3,500 bicycles are assembled?3,500 units x $52 = $182,000

11

Cost Accounting Horngreen, Datar, Foster

Cost Behavior Patterns

Total costs ($000)

$182

$52

0 1,000 3,500 Units

12

Cost Accounting Horngreen, Datar, Foster

Cost Behavior Patterns

Assume that Metairie Bicycles incurred $94,500 in a given year for the leasing of its plant.This is an example of fixed costs with respect to the number of bicycles assembled. These costs are unchanged in total over a designated range of the number of bicycles assembled during a given time span.• What is the leasing (fixed) cost per bicycle when Metairie assembles

1,000 bicycles? • $94,500 ÷ 1,000 = $94.50• What is the leasing (fixed) cost per bicycle when Metairie assembles

3,500 bicycles?• $94,500 ÷ 3,500 = $27

13

Cost Accounting Horngreen, Datar, Foster

Cost Drivers

A cost driver is a factor, such as the level of activity or volume, that causally affects costs (over a given time span).The cost driver of variable costs is the level of activity or volume whose change causes the (variable) costs to change proportionately.The number of bicycles assembled is a cost driver of the cost of handlebars.

14

Cost Accounting Horngreen, Datar, Foster

Relevant Range...

is the band of the level of activity or volume in which a specific relationship between the level of activity or volume and the cost in question is valid.Assume that fixed (leasing) costs are $94,500 for a year and that they remain the same for a certain volume range (1,000 to 5,000 bicycles).1,000 to 5,000 bicycles is the relevant range.If annual demand for Metairie’s bicycles increases, and the company needs to assemble more than 5,000 bicycles, it would need to lease additional space which would increase its fixed costs.

15

Cost Accounting Horngreen, Datar, Foster

Relevant Range

Total fixed costs ($000)

Relevant range

0 1,000 5,000 Volume

$ 94.5

16

Cost Accounting Horngreen, Datar, Foster

Is it that easy?

Measuring cost requires to make decisions:Some costs are known, others are notThe firm does not know its cost functionWhich cost driver reflects change in costs best?What is the relevant range?Are all variable costs linear?

What accountants typically use is linear approximation and aggregation

17

Cost Accounting Horngreen, Datar, Foster

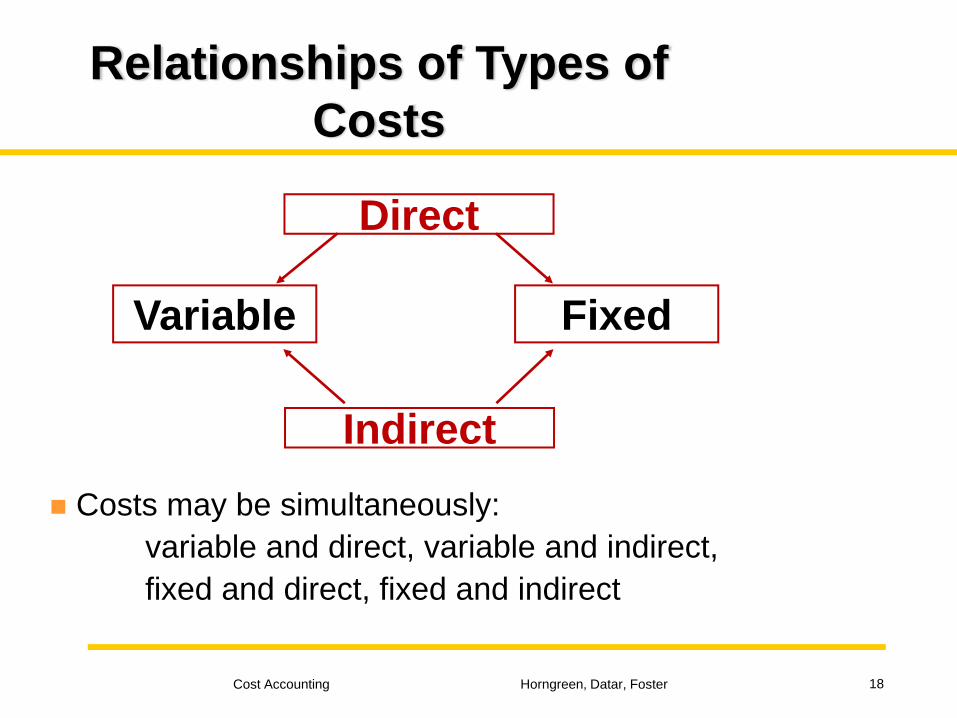

Relationships of Types of Costs

Direct

Indirect

Variable Fixed

Costs may be simultaneously: variable and direct, variable and indirect, fixed and direct, fixed and indirect

18

Cost Accounting Horngreen, Datar, Foster

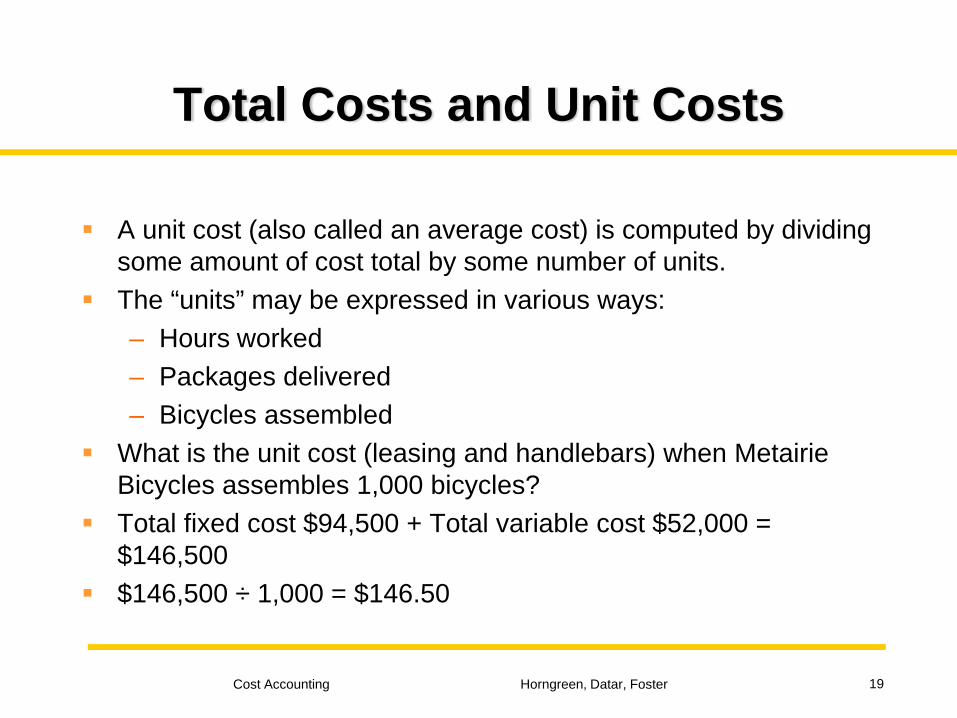

Total Costs and Unit Costs

A unit cost (also called an average cost) is computed by dividing some amount of cost total by some number of units.The “units” may be expressed in various ways:– Hours worked– Packages delivered– Bicycles assembled

What is the unit cost (leasing and handlebars) when Metairie Bicycles assembles 1,000 bicycles?Total fixed cost $94,500 + Total variable cost $52,000 = $146,500$146,500 ÷ 1,000 = $146.50

19

Cost Accounting Horngreen, Datar, Foster

Total Costs and Unit Costs

Total costs ($000)

0 1,000 Volume

$146.5

$ 94.5

20

Cost Accounting Horngreen, Datar, Foster

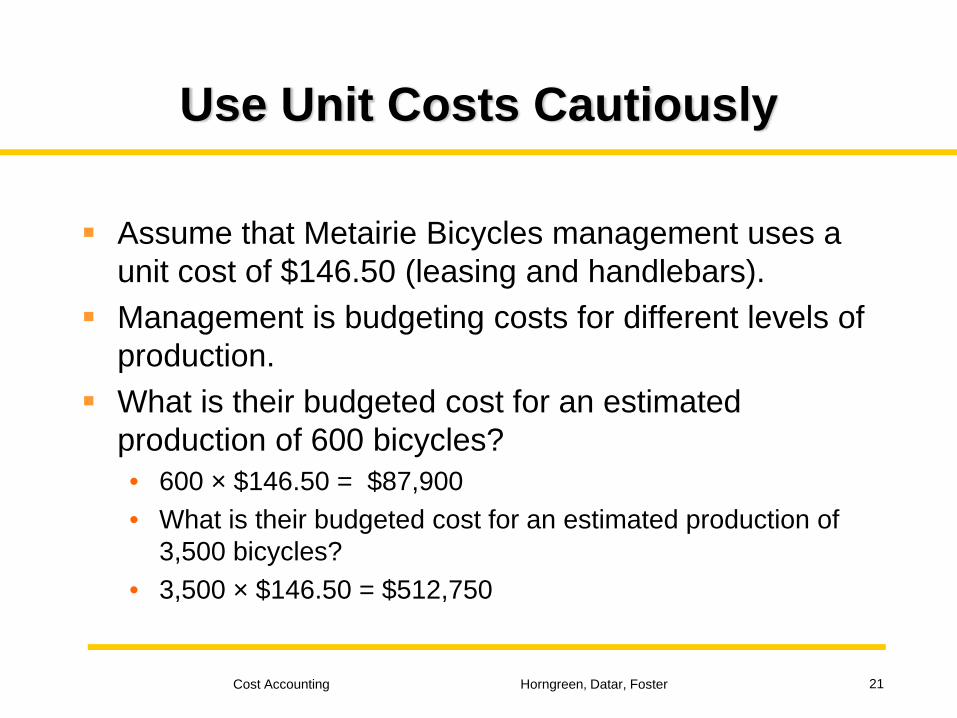

Use Unit Costs Cautiously

Assume that Metairie Bicycles management uses a unit cost of $146.50 (leasing and handlebars).Management is budgeting costs for different levels of production.What is their budgeted cost for an estimated production of 600 bicycles?• 600 × $146.50 = $87,900• What is their budgeted cost for an estimated production of

3,500 bicycles?• 3,500 × $146.50 = $512,750

21

Cost Accounting Horngreen, Datar, Foster

Use Unit Costs Cautiously

What should the budgeted cost be for an estimated production of 600 bicycles?Total fixed cost $ 94,500 Total variable cost ($52 × 600) = 31,200 Total

$125,700$125,700 ÷ 600 = $209.50

Using a cost of $146.50 per unit would underestimate actual total costs if output is below 1,000 units.

22

Cost Accounting Horngreen, Datar, Foster

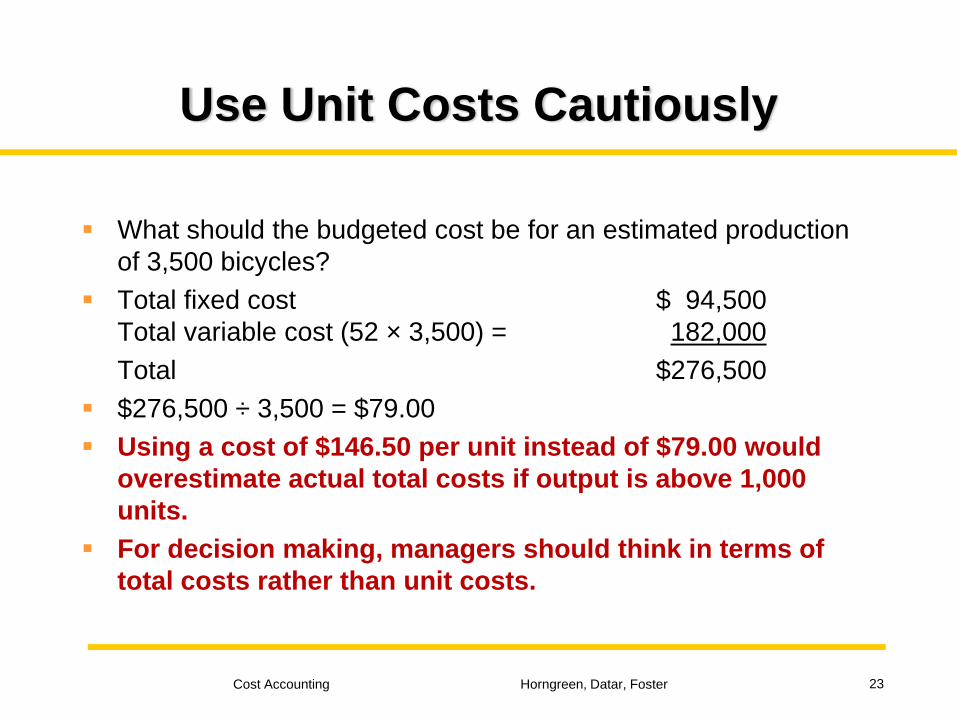

Use Unit Costs Cautiously

What should the budgeted cost be for an estimated production of 3,500 bicycles?Total fixed cost $ 94,500 Total variable cost (52 × 3,500) = 182,000Total $276,500$276,500 ÷ 3,500 = $79.00Using a cost of $146.50 per unit instead of $79.00 would overestimate actual total costs if output is above 1,000 units.For decision making, managers should think in terms of total costs rather than unit costs.

23

Cost Accounting Horngreen, Datar, Foster

Manufacturing

Manufacturing-sector companies purchase materials and components and convert them into finished goods. A manufacturing company must also develop, design, market, and distribute its products.

24

Cost Accounting Horngreen, Datar, Foster

Merchandising

Merchandising-sector companies purchase and then sell tangible products without changing their basic form.

25

Cost Accounting Horngreen, Datar, Foster

Service Companies...

– provide services or intangible products to their customers.• Labor is the most significant cost category.

26

Cost Accounting Horngreen, Datar, Foster

Types of Inventory

Manufacturing-sector companies typically have one or more of the following three types of inventories:• Direct materials inventory

• direct materials in stock and awaiting use in the manufacturing process

• Work-in-process inventory (work in progress)• goods partially worked on but not yet fully completed.

• Finished goods inventory• goods fully completed but not sold.

27

Cost Accounting Horngreen, Datar, Foster

Types of Inventory

Merchandising-sector companies hold only one type of inventory – the product in its original purchased form.Service-sector companies usually do not hold inventories of tangible products.

28

Cost Accounting Horngreen, Datar, Foster

Classification of Manufacturing Costs

Direct materials costs• Direct materials costs are the acquisition costs of all

materials that eventually become part of the cost object.

• Direct materials costs can be traced economically.• Acquisition costs include freight-in (inward delivery)

charges, sales taxes, and customs duties.

29

Cost Accounting Horngreen, Datar, Foster

Classification of Manufacturing Costs

Direct materials costsDirect manufacturing labor costs

• Direct manufacturing labor costs include the compensation of all manufacturing labor that can be traced to the cost object in an economically feasible way.

• Wages and fringe benefits paid to:– Machine operators– Assembly-line workers

30

Cost Accounting Horngreen, Datar, Foster

Classification of Manufacturing Costs

Direct materials costsDirect manufacturing labor costsIndirect manufacturing costs

• Indirect manufacturing costs are all manufacturing costs that are considered to be part of the cost object, but that cannot be traced to that cost object in an economically feasible way.

• Other terms for this cost category include manufacturing overhead costs and factory overhead costs.

31

Cost Accounting Horngreen, Datar, Foster

Inventoriable CostsInventoriable costs are all costs of a product that are regarded as an asset when they are incurred and then become cost of goods sold when the product is sold.• For manufacturing-sector companies, almost all manufacturing costs

are inventoriable costs.• Inventoriable costs (direct materials, direct labor and indirect

manufacturing costs) are included in work-in-process and finished goods inventory.

• For merchandising-sector companies, inventoriable costs are the costs of purchasing the goods which are resold in their same form.

• For service-sector companies, the absence of inventories means there are no inventoriable costs.

32

Cost Accounting Horngreen, Datar, Foster

Period Costs

Period costs are all costs in the income statement other than cost of goods sold.Period costs are recorded as expenses of the accounting period in which they are incurred.

– For manufacturing-sector companies, period costs include all non-manufacturing costs (research and development, distribution, etc.).

– For merchandising-sector companies, period costs include all costs not related to the cost of goods purchased for resale.

– For service-sector companies, all of their costs are period costs.

33

Cost Accounting Horngreen, Datar, Foster

Categories of Inventory

The three categories of inventory found in many manufacturing companies depict stages in the conversion process:• materials

• Direct materials inventory costs are used to compute the cost of materials used.

• Beginning direct materials inventory + Purchases of direct materials − Ending direct materials inventory = Direct materials used

34

Cost Accounting Horngreen, Datar, Foster

Categories of Inventory

The three categories of inventory found in many manufacturing companies depict stages in the conversion process:• materials

• work-in-process• Work-in-process inventory costs are used to compute the cost of

goods manufactured.• Beginning work-in-process inventory

+ Manufacturing costs incurred during the period− Ending work-in-process inventory = Cost of goods manufactured

35

Cost Accounting Horngreen, Datar, Foster

Categories of InventoryThe three categories of inventory found in many manufacturing companies depict stages in the conversion process:• materials• work-in-process

• finished goods• Finished goods inventory costs are used to compute the cost of

goods sold.• Beginning finished goods inventory

+ Cost of goods manufactured − Ending finished goods inventory = Cost of goods sold

36

Cost Accounting Horngreen, Datar, Foster

Measuring Costs Requires Judgment

Judgment is frequently required when measuring costs.Differences can exist in the way accounting terms are defined.

37

Cost Accounting Horngreen, Datar, Foster

Measuring Costs Requires Judgment

Manufacturing labor-cost classifications vary among companies.The following distinctions are generally found:• Direct manufacturing labor• Manufacturing overhead

• Indirect labor• Managers’ salaries• Payroll fringe costs

38

Cost Accounting Horngreen, Datar, Foster

Measuring Costs Requires Judgment

Overtime premium consists of the wages paid to all workers (for both direct labor and indirect labor) in excess of their straight-time wage rates.• Overtime premium is usually considered part of overhead.• Why is overtime premium of direct labor usually considered an

indirect rather than a direct cost?• Because it does not “penalize” (add to) the cost of a particular

batch of work solely because it happened to be worked on during the overtime hours.

• Sometimes overtime is not random; for instance a rush job may clearly be the sole source of the overtime.

• In this case the overtime premium is regarded as a direct cost of the services on that job.

39

Cost Accounting Horngreen, Datar, Foster

Many Meanings of Product Cost

A product cost is the sum of the costs assigned to a product for a specific purpose.1 Pricing and product emphasis decisions2 Contracting with government agencies3 Preparing financial statements for external

reporting under generally accepted accounting principles

40

Cost Accounting Horngreen, Datar, Foster

Many Meanings of Product Cost

For pricing and product mix decisions, the costs included are all areas of the value chain.When contracting with government agencies, companies must follow the guidelines provided on the allowable and non allowable items in a product-cost amount.

41

Cost Accounting Horngreen, Datar, Foster

Many Meanings of Product Cost

When preparing financial statements for external reporting, the focus is on inventoriable costs. Usually under generally accepted accounting principles, only manufacturing costs are assigned to inventories in the financial statements.

42

Cost Accounting Horngreen, Datar, Foster

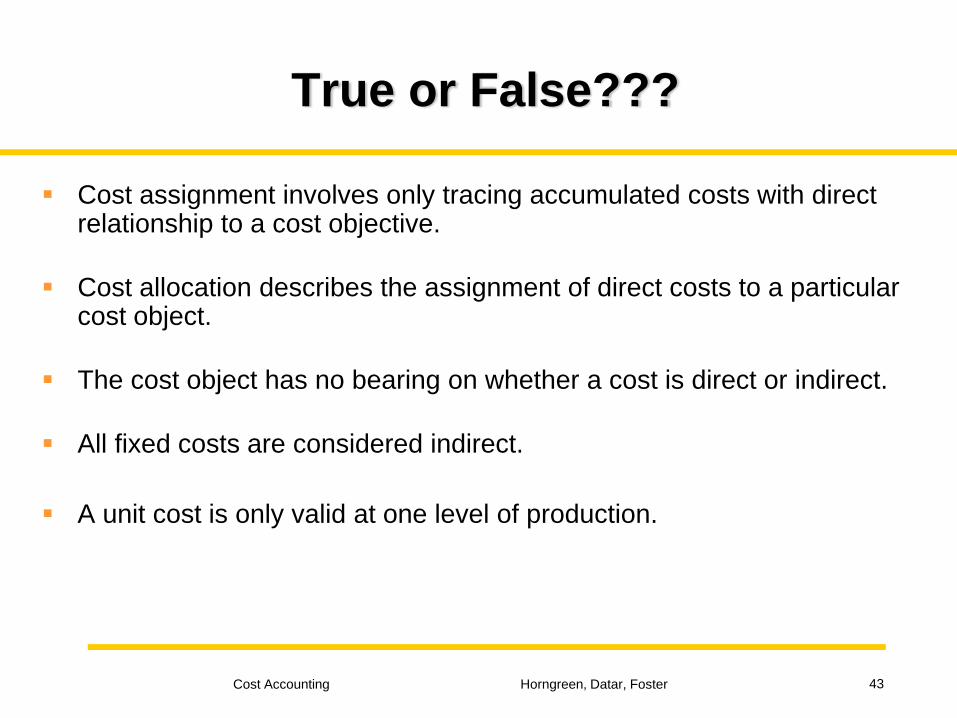

True or False???

Cost assignment involves only tracing accumulated costs with direct relationship to a cost objective.

Cost allocation describes the assignment of direct costs to a particular cost object.

The cost object has no bearing on whether a cost is direct or indirect.

All fixed costs are considered indirect.

A unit cost is only valid at one level of production.

43

Cost Accounting Horngreen, Datar, Foster

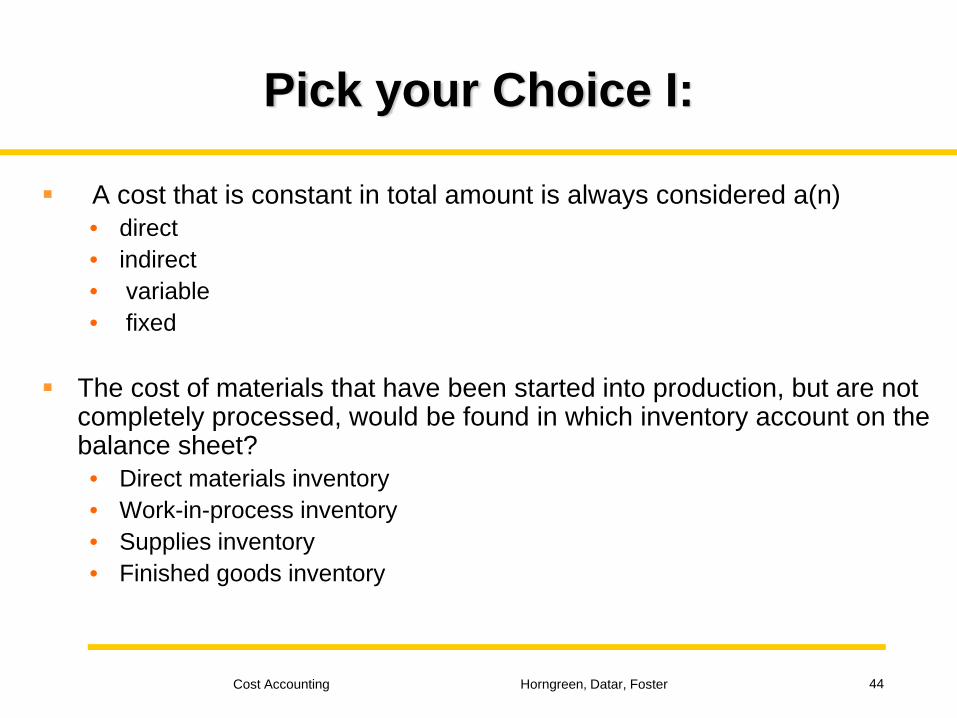

Pick your Choice I:

A cost that is constant in total amount is always considered a(n) • direct• indirect• variable• fixed

The cost of materials that have been started into production, but are not completely processed, would be found in which inventory account on the balance sheet? • Direct materials inventory• Work-in-process inventory• Supplies inventory• Finished goods inventory

44

Cost Accounting Horngreen, Datar, Foster

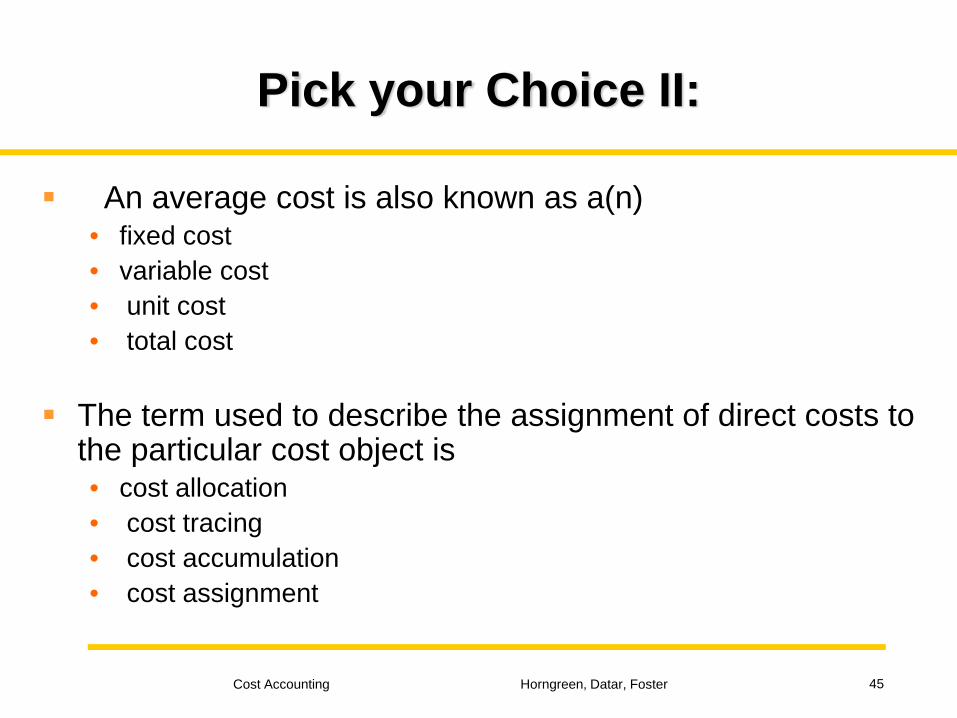

Pick your Choice II:

An average cost is also known as a(n) • fixed cost• variable cost• unit cost• total cost

The term used to describe the assignment of direct costs to the particular cost object is • cost allocation• cost tracing• cost accumulation• cost assignment

45

![IntegrationofFPGAsinDatabaseManagementSystems ......Bala Gurumurthy bala.gurumurthy@ovgu.de more for data-processing contexts. Prominent examples are Microsoft’s Catapult [38], Baidu’s](https://img.pdfslide.us/doc/110x75/613d6c32e1ef621e9f2db6c0/integrationoffpgasindatabasemanagementsystems-bala-gurumurthy-balagurumurthyovgude.jpg)

![Seminar II [Schreibgeschützt]II_neu.pdf · Dipl.-Ing. Andreas Jörke1 Tutorial Chemical Reaction Engineering: 2. Stoichiometry 1Institute of Process Engineering, G25-217, andreas.joerke@ovgu.de](https://img.pdfslide.us/doc/110x75/5f1047537e708231d448520b/seminar-ii-schreibgeschtzt-iineupdf-dipl-ing-andreas-jrke1-tutorial.jpg)