Embed Size (px)

Citation preview

8/4/2019 Cost Optimization & Diagonstic

http://slidepdf.com/reader/full/cost-optimization-diagonstic 1/70

Conducting Company Diagnostic &Cost Rohit Anand

Optimization Strategy 10BSP1025

Page 1

A

Conducting Company Diagnostic and

to develop Cost Optimization Strategy

for XYZ Company

Final Report

10th May, 2011

Rohit Anand, 10BSP1025

Interim Report submitted in partial fulfilments of requirement of PGPM Program of ICFAI Business School

8/4/2019 Cost Optimization & Diagonstic

http://slidepdf.com/reader/full/cost-optimization-diagonstic 2/70

Conducting Company Diagnostic &Cost Rohit Anand

Optimization Strategy 10BSP1025

Page 2

A

REPORT

ON

CONDUCTING COMPANY DIAGNOSTIC AND TO

DEVELOP COST OPTIMIZATION STRATEGY FOR XYZ

COMPANY

BY:

ROHIT ANAND

10BSP1025

FOR:

X.Y.Z. LIMITED

ON BEHALF OF

FINTEQ INDIA LIMITED.

A REPORT SUBMITTED ON PARTIAL FULFILLMENT OF THEREQUIREMENTS OF P.G.P.M. PROGRAM OF IBS KOLKATA

DISTRIBUTUION LIST:

SUBMITTTED TO:

Mr. ANUJ JAIN (FACULTY GUIDE);

Mr. SUMANTO GHOSH (COMPANY GUIDE)

DATE OF SUBMISSION: 10th

May 2011

8/4/2019 Cost Optimization & Diagonstic

http://slidepdf.com/reader/full/cost-optimization-diagonstic 3/70

Conducting Company Diagnostic &Cost Rohit Anand

Optimization Strategy 10BSP1025

Page 3

ACKNOWLEDGEMENT

To acknowledge all the persons who had helped for the fulfilment of the project is notpossible for any researcher but in spite of all that it becomes the foremost responsibility of the researcher and also the part of research ethics to acknowledge those who had playeda great role for the completion of the project.

I would also like to express my deepest gratitude to MR.JAYANTA CHATTERJEE, Chairman-

FINTEQ ENTERPRISE PVT. LTD, and my company guide MR. SUMANTO GHOSH , who

stood by me as a beacon of light, guiding me and believing in my convictions and calibre

and providing me a platform to learn and experience the real market challenges and the

corporate environment along with enhancing my financial knowledge and Interpersonal

skills.

I also express my special gratitude to ICFAI Business School, Kolkata (IBS, Kolkata) for

excellent facilities provided by the institute in the form of library and computer lab.

This project report and the learning process behind it would not have been possible

without the guidance of my faculty guide, Prof. Anuj Jain. He was able to impart me with

the right approach that my training required for its successful practical implication. I was

involved with FINTEQ ENTERPRISE PVT. LTD for three months and I came across a lot of

people who put in their time and effort towards acclimatizing me to the workings of the

organization. This Summer Internship Program was of utmost importance for me as this

program added value towards my path of knowledge.

Last but not the least, I would like to thank all my colleagues and friends who have directly

or indirectly contributed in my endeavour and helped me complete this project. Thanks a

lot.

So in the same sequence at very first, I would like to acknowledge my parents because of whom I got the existence in the world for the inception and the conception of this project.Rest all those people who helped me are not only matter of acknowledgment but alsoauthorized for sharing my success.

Rohit Anand

10BSP1025

IBS KOLKATA

8/4/2019 Cost Optimization & Diagonstic

http://slidepdf.com/reader/full/cost-optimization-diagonstic 4/70

Conducting Company Diagnostic &Cost Rohit Anand

Optimization Strategy 10BSP1025

Page 4

AUTHORISATION

This is to certify that an Final report titled ―‖Conducting Company Diagnostic and Cost

Optimization Strategy for X.Y.Z‖ ―

--- is being submitted as a component in the evaluationof Summer Internship Program for the requirement of PGPM program of ICFAI Business

School, Kolkata.

8/4/2019 Cost Optimization & Diagonstic

http://slidepdf.com/reader/full/cost-optimization-diagonstic 5/70

Conducting Company Diagnostic &Cost Rohit Anand

Optimization Strategy 10BSP1025

Page 5

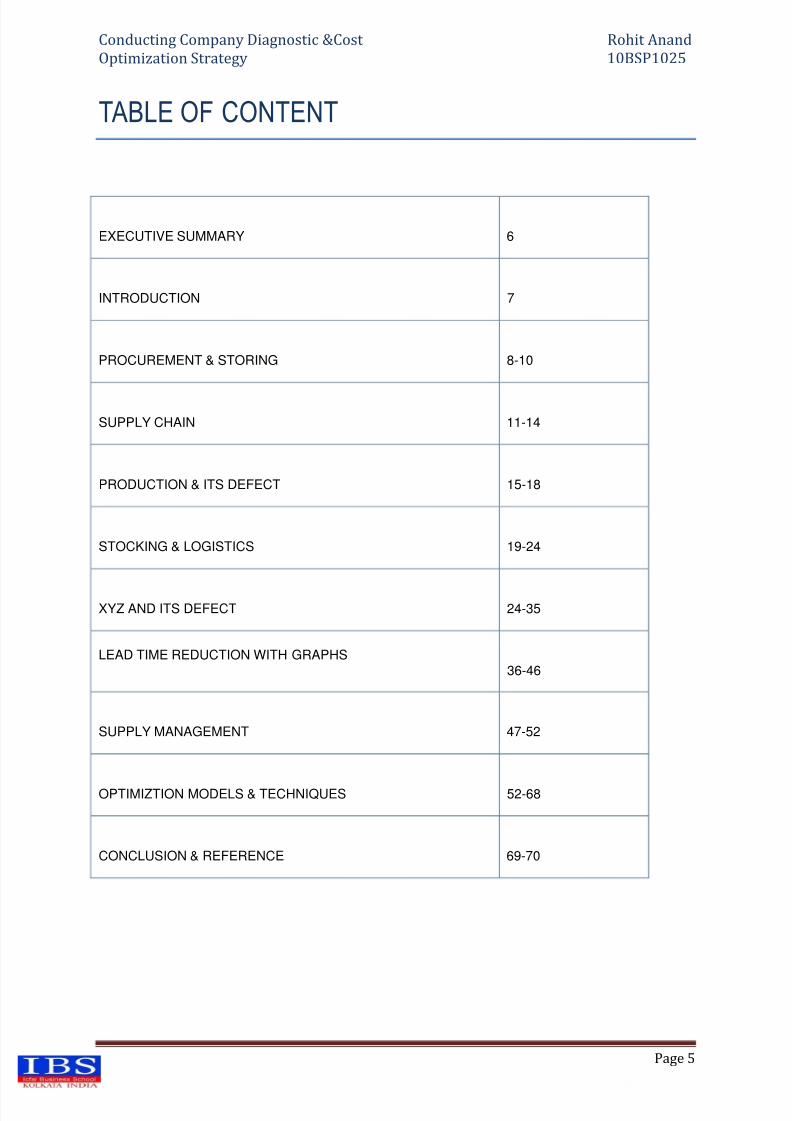

TABLE OF CONTENT

EXECUTIVE SUMMARY 6

INTRODUCTION 7

PROCUREMENT & STORING 8-10

SUPPLY CHAIN 11-14

PRODUCTION & ITS DEFECT 15-18

STOCKING & LOGISTICS 19-24

XYZ AND ITS DEFECT 24-35

LEAD TIME REDUCTION WITH GRAPHS36-46

SUPPLY MANAGEMENT 47-52

OPTIMIZTION MODELS & TECHNIQUES 52-68

CONCLUSION & REFERENCE 69-70

8/4/2019 Cost Optimization & Diagonstic

http://slidepdf.com/reader/full/cost-optimization-diagonstic 6/70

Conducting Company Diagnostic &Cost Rohit Anand

Optimization Strategy 10BSP1025

Page 6

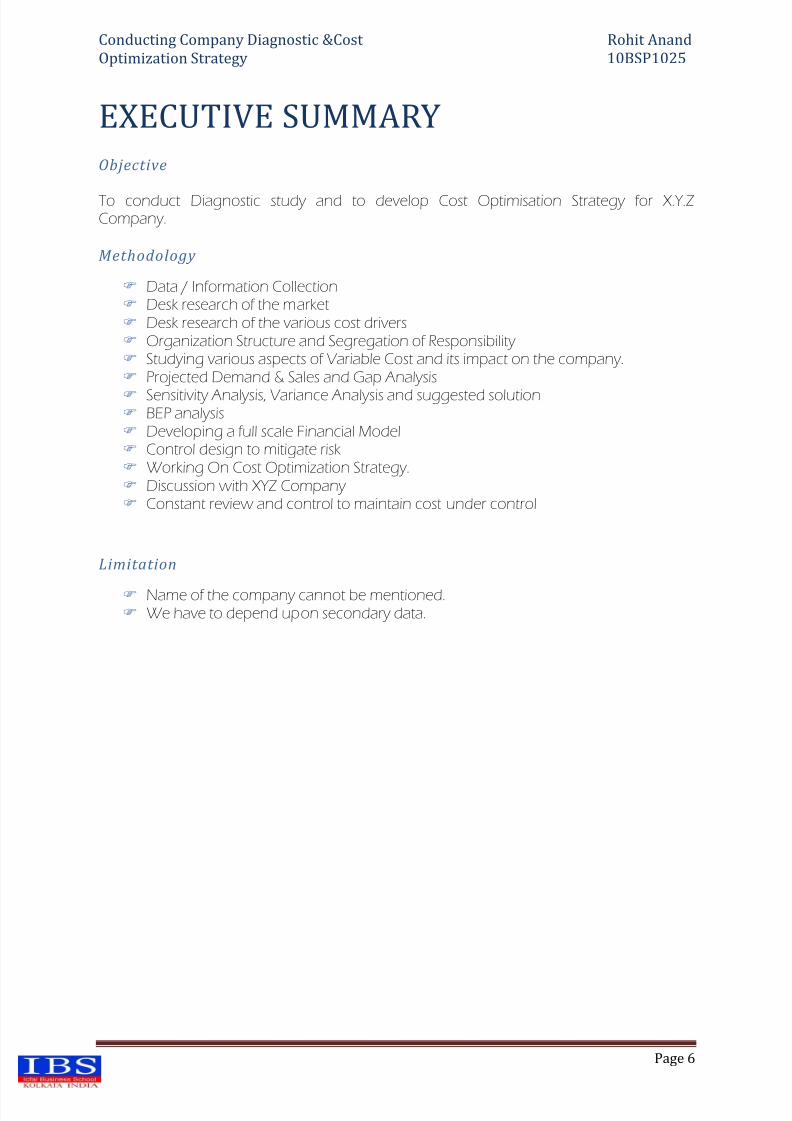

EXECUTIVE SUMMARY

Objective

To conduct Diagnostic study and to develop Cost Optimisation Strategy for X.Y.ZCompany.

Methodology

Data / Information Collection Desk research of the market Desk research of the various cost drivers Organization Structure and Segregation of Responsibility Studying various aspects of Variable Cost and its impact on the company. Projected Demand & Sales and Gap Analysis

Sensitivity Analysis, Variance Analysis and suggested solution BEP analysis Developing a full scale Financial Model Control design to mitigate risk Working On Cost Optimization Strategy. Discussion with XYZ Company Constant review and control to maintain cost under control

Limitation

Name of the company cannot be mentioned. We have to depend upon secondary data.

8/4/2019 Cost Optimization & Diagonstic

http://slidepdf.com/reader/full/cost-optimization-diagonstic 7/70

Conducting Company Diagnostic &Cost Rohit Anand

Optimization Strategy 10BSP1025

Page 7

Introduction

Your ultimate goal is to increase company profitability —either making unprofitable

customers profitable, or making profitable customers more profitable! If you don’t know anaccurate Cost-to-Serve for current customers and products, you can’t even get startedimproving profitability.

There are multiple methods and disciplines to achieve this, and the distinctions betweenthem are not always clear. The terms ―Activity -based Costing‖ (ABC) and ―Costto -Serve

Analysis‖ (CTSA) are used to describe two different cost modeling approaches, both of which require allocating indirect costs to cost drivers in a process or supply chain model.Further, Supply Chain Network Design and Cost-to-Serve Optimization are both supply chain optimization disciplines that can identify and reduce costs and increase profitability.

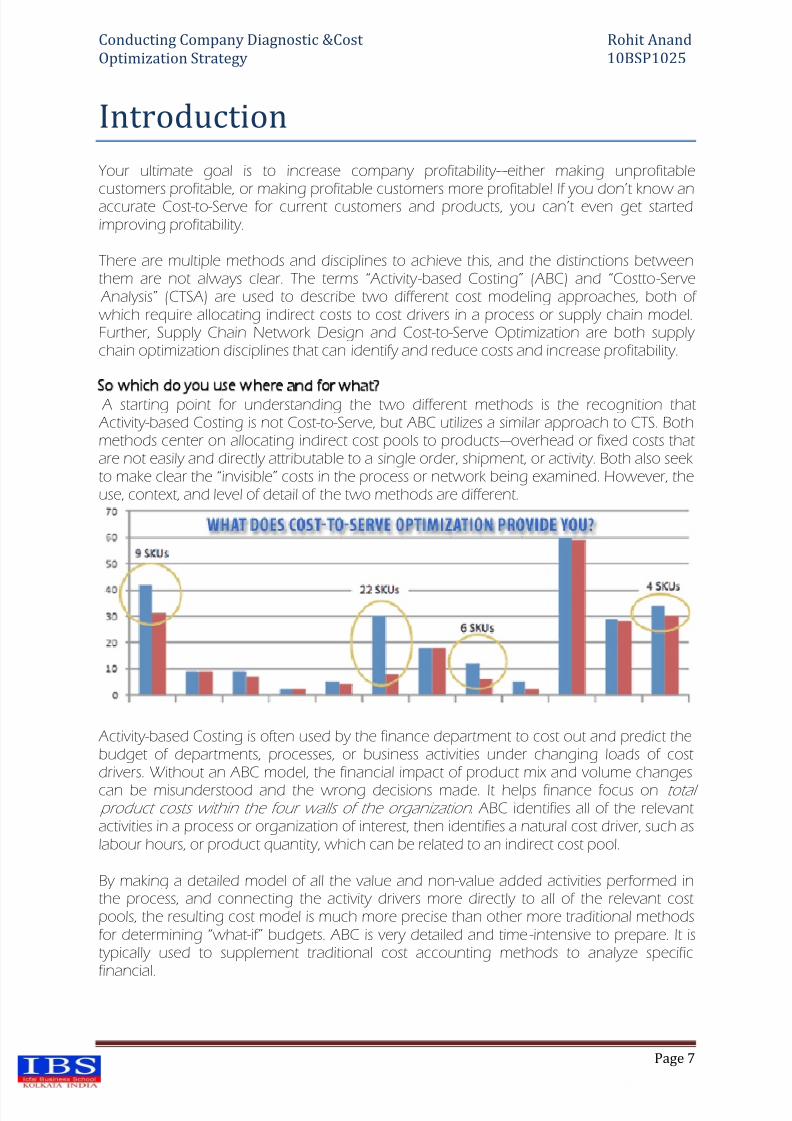

So which do you use where and for what? A starting point for understanding the two different methods is the recognition that Activity-based Costing is not Cost-to-Serve, but ABC utilizes a similar approach to CTS. Bothmethods center on allocating indirect cost pools to products —overhead or fixed costs thatare not easily and directly attributable to a single order, shipment, or activity. Both also seekto make clear the ―invisible‖ costs in the process or network being examined. However, theuse, context, and level of detail of the two methods are different.

Activity-based Costing is often used by the finance department to cost out and predict thebudget of departments, processes, or business activities under changing loads of costdrivers. Without an ABC model, the financial impact of product mix and volume changes

can be misunderstood and the wrong decisions made. It helps finance focus on total product costs within the four walls of the organization . ABC identifies all of the relevantactivities in a process or organization of interest, then identifies a natural cost driver, such aslabour hours, or product quantity, which can be related to an indirect cost pool.

By making a detailed model of all the value and non-value added activities performed inthe process, and connecting the activity drivers more directly to all of the relevant costpools, the resulting cost model is much more precise than other more traditional methodsfor determining ―what -if‖ budgets. ABC is very detailed and time -intensive to prepare. It istypically used to supplement traditional cost accounting methods to analyze specificfinancial.

8/4/2019 Cost Optimization & Diagonstic

http://slidepdf.com/reader/full/cost-optimization-diagonstic 8/70

Conducting Company Diagnostic &Cost Rohit Anand

Optimization Strategy 10BSP1025

Page 8

Task Assigned

Conducting Company Diagnostic and to develop Cost optimization Strategy for XYZ Company in termof following field:

Procurement & Storing. Production. Storage & Logistics.

Procurement & Storing

METHOD FOR RAW MATERIAL PROCUREMENT :

The budgeting process commences in June/July each year with the Head of the Supply Chain Department drawing up estimates of costs of significant raw materials and other

items/services to be procured during the next budgeting cycle. This estimate is based on

the production planned for each product line during the next cycle, historical price trends

for items/services to be purchased and likely price movements during the next cycle. This

estimate is then sent to the Chief Financial Officer who finalizes and approves the budget

in consultation with the Chief Executive Officer of the Company. The budget figures would

be quantified in terms of value as also the cost per unit of product. During the budgeting

exercise, due attention shall be paid to securing economy in the cost of purchases without

sacrificing quality and service considerations.

The purchase budget on approval is then broken up into quarterly budgets by the

Purchase Department taking into account the seasonal variations in production.

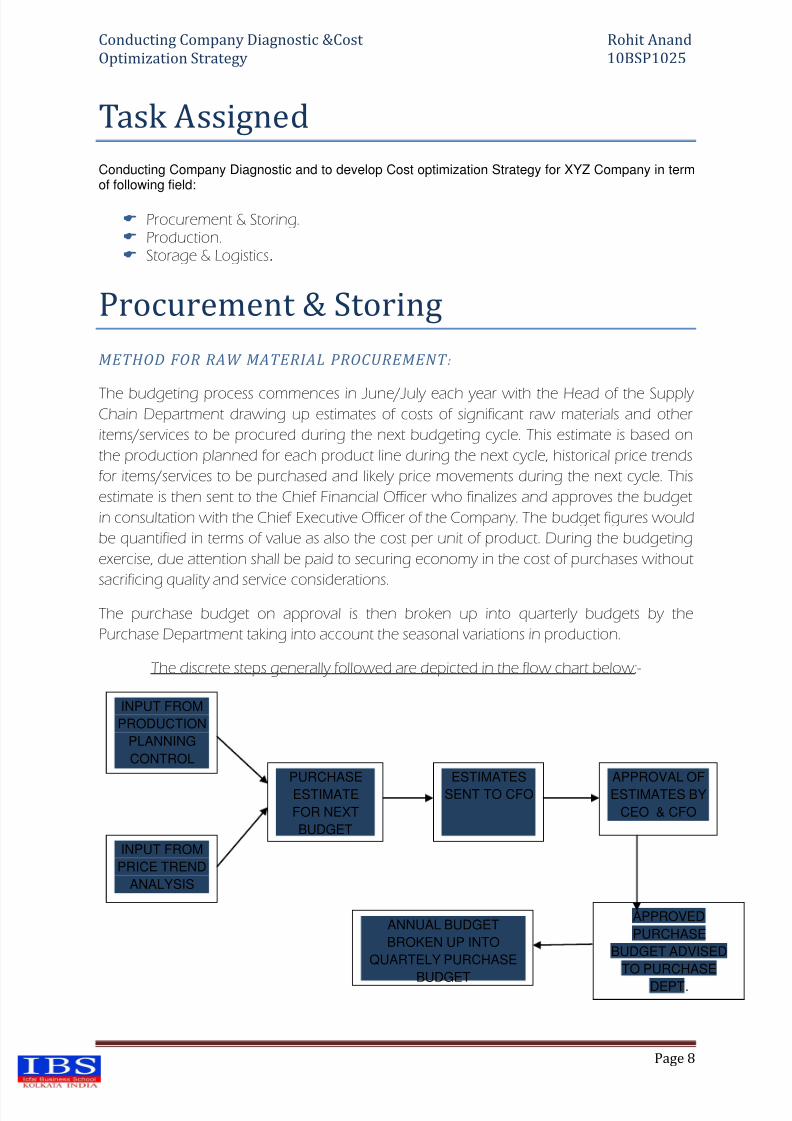

The discrete steps generally followed are depicted in the flow chart below:-

INPUT FROM

PRODUCTION

PLANNING

CONTROL

INPUT FROM

PRICE TREND

ANALYSIS

PURCHASE

ESTIMATE

FOR NEXT

BUDGET

ESTIMATES

SENT TO CFO

APPROVAL OF

ESTIMATES BY

CEO & CFO

APPROVED

PURCHASE

BUDGET ADVISED

TO PURCHASE

DEPT.

ANNUAL BUDGET

BROKEN UP INTO

QUARTELY PURCHASE

BUDGET

8/4/2019 Cost Optimization & Diagonstic

http://slidepdf.com/reader/full/cost-optimization-diagonstic 9/70

Conducting Company Diagnostic &Cost Rohit Anand

Optimization Strategy 10BSP1025

Page 9

Types of Purchase Contracts

Purchase Contracts or Purchase orders issued for purchase of goods or services are of two kinds:

One time purchase contracts or purchase orders

Where delivery of the goods and services purchased are to be completed in entirety at one time

or within a short time span.

Scheduled Agreements or purchase orders

where goods or services to be purchased are against the requirements of the Company over an

extended time period or for annual requirements. Deliveries against these contracts or orders

are to be staggered over the time period of the contract. Unit Prices of goods or services may

vary over the supply period depending on price movements. Quantities delivered under the

contract at various points of time may vary depending on requirements of the Company .

Enquiry/ Quotations/ Negotiations

Most of the RM/PM required and Initiating Systems are available only from a limited

number of vendors. This is due to the nature of these materials and also since the

manufacture of Capacitors maintaining quality of the finished product.

Accordingly the procurement system is essentially based on obtaining quotations

from the limited number of pre-qualified vendors who are capable of supplying

materials in conformity with prescribed standards.

Enquiries for quotations are floated to the approved vendors by email or fax, and

responses obtained. The company has an approved list of vendors with respect to

each RM/PM. Procurement department feels the necessity of inclusion of new

vendor or deleting any then it should follow the company’s vendor evaluation

process and seek approval as per the authority level of XYZ.

On receipt of quotations the supply officer negotiates with the vendors and selects

the final vendor considering their respective production capacities, delivery history

and other factors into account.

Strategies Adopted

Given are few ideas which can result in savings:

Opportunity BuyingMost of the commodities and raw material has seasonal cycle of prices as they peak and fall in intervals .Hence we can book maximum amount of ourrequirement when prices are low .

Local Vendors

8/4/2019 Cost Optimization & Diagonstic

http://slidepdf.com/reader/full/cost-optimization-diagonstic 10/70

Conducting Company Diagnostic &Cost Rohit Anand

Optimization Strategy 10BSP1025

Page 10

Vendors should be located in close vicinity of company which helps in keepinglow inventory as well as low freight cost.

Partnerships With Major VendorsIt is highly recommended to have partnership with vendors in either havingequity or technical collaboration so as to pass on savings to the customer. Which

results in cost reduction in manufacturing cost? Most of the Automobiles Majorshas this kind of arrangement with their vendors .Vendors is assured of business.

E ProcurementPutting up tenders and requirement on Internet and setting up auction forrequirement on web which helps in reaching out more numbers of vendorbases. This also helps in cutting cost when we opt for conventional way of askingtender /quotation. Most popular way of procurement strategy is reverse auction,where the lowest price bidder takes away the order.

Buying Material From Tax Exempted Area.In several countries the federal/ State govts provide tax heavens formanufactures for certain period say 10- 15 years .Hence buying from these area s

helps in cutting cost .In common parlance it is called TAX HOLIDAYS . Look outfor such places prior to placing orders.

Alternate MaterialSelect high cost items and replace it by some low cost material. eg ; steel by plastic/aluminium .

Try Merge In TransitThe concept of in-transit product merging —where, for example, two things areshipped from different locations and then married in transit so that they reach thecustomer as a single shipment —can be seen as a technique for reducinginventory if the need for the customer to simultaneously receive multiple SKUs is agiven. To some extent, merge-in-transit represents an extension of postponement

beyond the distribution centre walls. Vendor Managed Inventory (Vmi)

With the appropriate incentives, allowing suppliers to assume the responsibility for replenishment of your inventory, because of their visibility into both their owninventory and production schedule and your demand data can almost alwaysreduce your inventory.

Vendor Stocking Program (Vsp) Used primarily for maintenance inventories but applicable to all, VSPs require asupplier to commit to an extremely high service level for delivery of specific SKUswithin a fixed time at a predefined mark-up. VSPs can reduce or eliminateinventories for slow-moving products. There are numerous ways to take better

control of inventory and decrease its associated costs. The key to managinginventory successfully is to continuously measure your performance and look fornew ways to improve. These 25 strategies should get your organization thinkingabout what it can do to lower inventory costs.

8/4/2019 Cost Optimization & Diagonstic

http://slidepdf.com/reader/full/cost-optimization-diagonstic 11/70

Conducting Company Diagnostic &Cost Rohit Anand

Optimization Strategy 10BSP1025

Page 11

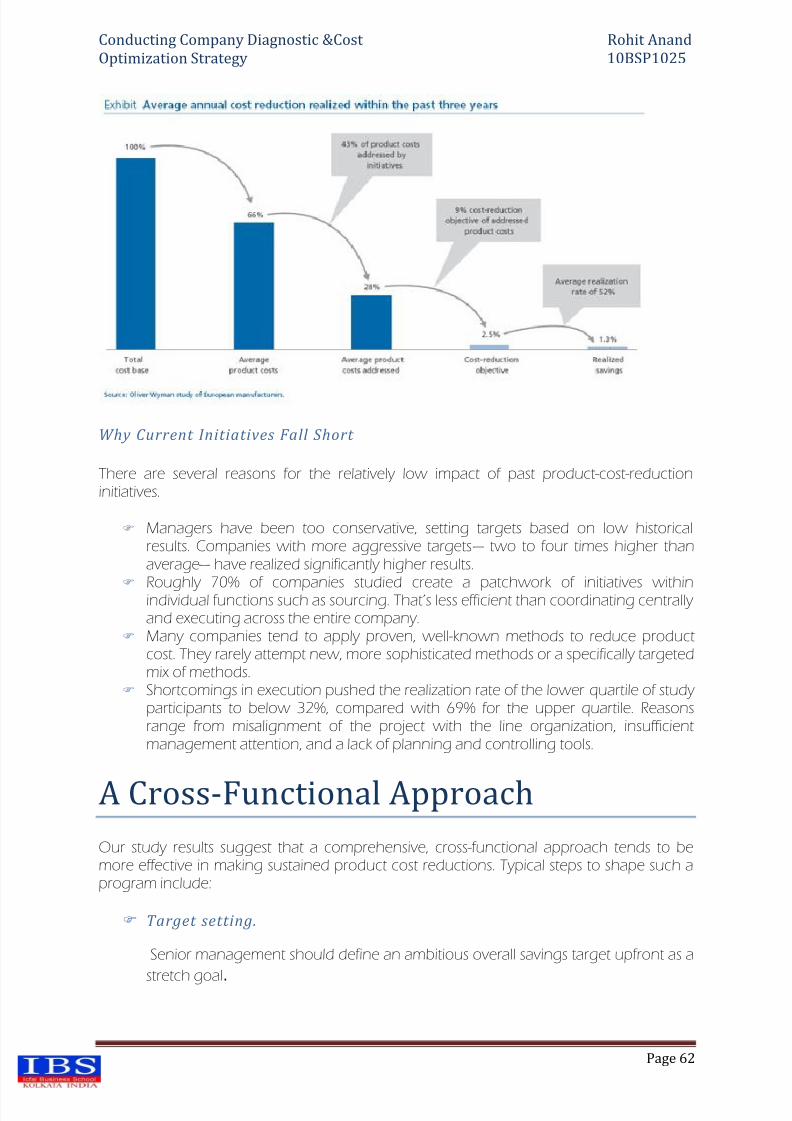

Three Ways to Trim Costs in the Supply Chain:

Eliminate Redundancies In The Supply ChainFor all supply chain partners, create a flow chart of all activities involved in theprocurement, set up, production, inspection, storage, and transportation of all

materials and components that go into the final product. You will likely find activitiesthat are repeated by different supply chain partners (e.g., outgoing inspection by one supply chain partner immediately followed by incoming inspection by another). If you can work with your supply chain partners to eliminate suchredundancies, you can reduce their costs and, as a result, your price.

Shift Tasks to the Most Efficient Supply Chain Partner. Sometimes the capabilities of supply chain partners overlap. Let's consider acustomer's purchase of engraved plaques. The customer's immediate supplier may do direct marketing, fulfilment, and engraving. That supplier's supplier may dodesign, manufacturing, and engraving. In this case, who should do the engraving?

The most efficient supply chain partner should, assuming that either can meetquality, delivery, and service standards. But this means that you have to question"the way we've always done it" so that you can do it the best way.

Leverage The Supply Chain's Buying Power. Often, the products and services purchased by second tier suppliers are alsopurchased by a first-tier supplier. Many times, that first-tier supplier gets a betterprice than the second-tier suppliers. In cases like these, the first-tier supplier cannegotiate to add second-tier suppliers' volume onto its agreements, thereby gettingeven deeper discounts for itself and reducing total cost throughout the supply chain.

Cost Reduction Ideas–

Procurement

Removing Intermediaries Wherever possible buy directly from manufacturers /authorised dealers /OEMnot from any agent /dealer or commission agent. Lesser the intermediarieslower the rate.

Non - Branded ItemsLook out for non branded items for non - critical areas as branded items has

premium attached to it .Sometimes you can get good items which are non -branded just in case of garments.

Recycling And Reuse All items come into some form of secondary packaging and out of which someof the items can be reused or recycled .Ask vendors to reuse /recycle packingitems. Eg cans, sacks, bottles, cores trays and pallets etc.

ConversionsBuying primary material then giving it to processor instead of buyingdirectly from the converter , it helps in two ways as we can avail modvat

exemption on the raw material and can eliminate the premium on conversionegKraft paper for cbbs .

8/4/2019 Cost Optimization & Diagonstic

http://slidepdf.com/reader/full/cost-optimization-diagonstic 12/70

Conducting Company Diagnostic &Cost Rohit Anand

Optimization Strategy 10BSP1025

Page 12

Make And Buy DecisionsFew items can be made in house rather getting it from outside eg groundedsugar, cashew nuts etc.

Negotiations

The price should always be negotiated with all information available. Prices arewhen you are informed and aware of options available .Always check priceswith alternate sources.

Economical Order Quantity ( Eoq) This is the maximum qty of item which you can place to a vendor taking intoaccount the frequency of items used.

InspectionBy eliminating inspection at factory and asking vendors to provide materials asper standards and completing inspections at their end we can eliminate delays

and manpower used in these kinds of activities.

Scrap ManagementSegregation of scrap generated in a manufacturing unit is important .It hasbeen observed that all scrap are sold as lot to scrap merchant who in turnsegregates it in different categories and sells it in at higher rates .

Achievements:

To Increase Further Utilization of SAP for the Supply Chain Management

A general comment was that the SAP system is either not fully customized or proper

utilization was not being made of the system. Also too much paperwork and manual effort

was being used. The following are worth mentioning:

The Company does not use SAP for processing its material requirement plans. The

production planning and the bill of materials required for each product line is

processed manually. Decisions on the quantity of order to be placed judgmental and

are done manually based on historical consumption patterns. MRP plan module can

be made operational on the SAP system

Requisition of all RM/PM and engineering items and services are not made out of the

SAP system. It is only after placing the Purchase Orders/service orders that relevantdata is entered into the SAP system.

Engineering spares are not entered into stores records until inspection is completed.

There are entered into Stores records only after inspection. This needs to be changed

and goods received pending inspection to be recorded as goods under inspection.

(For RM/PM this is not the case and goods under inspection are recorded as such).

Transportation services are not directly through the SAP system. A way about route is

taken using SAP. As such no Purchase orders are generated for transportation

services. The information like batch details therefore cannot be linked with the

transport orders. This may cause difficulties for excise refunds in case of rejections.

8/4/2019 Cost Optimization & Diagonstic

http://slidepdf.com/reader/full/cost-optimization-diagonstic 13/70

Conducting Company Diagnostic &Cost Rohit Anand

Optimization Strategy 10BSP1025

Page 13

Also information required by PESO of the CCE can be linked with the SAP system if

the transportation services module can be properly used.

The Company should utilize the full range of SAP facilities to reduce manual inputs to the

extent possible. Training of staff to utilize the SAP process can be made on periodic

intervals and suggestions from users can be sought periodically.

Procurement Planning Process

Production plans are generated over a 15 day time horizon and the procurement plans

are for one month only. Procurement plans are also done manually through BOM Excel

spreadsheet and is not generated by SAP. Company indicated that demand forecasting is

of limited use since the factory operates at close to 100% capacity and material

procurement is more production driven rather than demand driven.

No demand forecasting and as a follow on production planning is done over a 6 monthhorizon. Some procurement planning is done over a 3 month period.

The suggested approach is: The Annual procurement plan should be derived from the annual Production plan.

Since production department is the custodian of the recipes and BOM, dependingupon the annual Production plan of each finished item, the Material requirementplan is to be derived and provided to the procurement department. The productionshould provide the monthly breakdown of material required to the procurementdepartment at the start of the financial year..

The Procurement department based on the Stock levels, seasonality, criticality and

economic purchase decisions base their monthly Purchase Plan of each material forthe whole year.

When Procurement department receives the actual production plan for thefollowing month from the Production department, it shall only make adjustments totheir monthly procurement plans depending on the change of actual productionplan vis-à-vis the Budgeted monthly plans.

For engineering items coded, the procurement department can base itsassumptions based on inputs from various departments and past history.

For Project items the annual procurement plan can be based on the projectedCapex proposals.

Purchase Order Conditions

The General terms and conditions provided in the Purchase order in some items were

contradictory and do not cover many general issues.

A suggested format is proposed in Annexure 1 for review of the company and

implementation.

The issue of Performance guarantees to be incorporated in the General terms and

conditions for RM/ PM may not be practicable as the basic nature of RM/PM is to undergo

change in form and substance after use in a production process and therefore non

performance or under performance of that particular RM/PM is difficult to substantiate.

What can be introduced for certain RM/PM is the minimum shelf life period warranty from

8/4/2019 Cost Optimization & Diagonstic

http://slidepdf.com/reader/full/cost-optimization-diagonstic 14/70

Conducting Company Diagnostic &Cost Rohit Anand

Optimization Strategy 10BSP1025

Page 14

the vendors subject to certain storage conditions. A review of and tightening of the

specification conditions for each such RM/PM can be made to create better control of

input RM/PM. For which RM/PM such shelf life warranty can be introduced is a technical

question and the company’s R & QA department can decide with the Production

department.

However for certain engineering items, spares such performance guarantee can be

introduced. This again shall be judgment of the technical departments.

In case such shelf life conditions for RM/PM and performance guarantees for certain

engineering items be introduced it should be in the face of the Purchase order as Special

conditions and not as General terms and conditions.

Production

Productivity measures the efficiency with which resources such as labour or capital are

employed in the production process. There are two widely used productivity measures;

labour productivity.

Labour productivity is measured as real output per hour worked. Multifactor productivity, a

broader measure of efficiency, is measured as real output per unit of combined inputs

(capital, labour, etc).In essence, this is the efficiency of all or your factors of production.

A business wishing to improve its profitability must undertake certain steps that can

guarantee to provide the desired results. One of the things that the management staff

must give important notice is the production and productivity of the business as a whole.

As has been known, to increase the profitability of an enterprise, certain things must be

improved in the workplace.

Activity can be identified with production and consumption. Production is a process of

combining various immaterial and material inputs of production so as to produce tools for

consumption. The methods of combining the inputs of production in the process of

making output are called technology. Technology can be depicted mathematically by the

production function which describes the function between input and output. The

production function depicts production performance and productivity is the metric for it.Measures may be applied with, for example, different technology to improve productivity

and to raise production output.

Seven Wastes in a Production Line

Kaizen principles has have highlighted seven wastes in production line where companieslooses out time , money and productivity .Manufacturers have to eliminate these deadly wastes with modification ,low cost automation and asking question whether customerwould pay for the activity involved at shop floors.

8/4/2019 Cost Optimization & Diagonstic

http://slidepdf.com/reader/full/cost-optimization-diagonstic 15/70

Conducting Company Diagnostic &Cost Rohit Anand

Optimization Strategy 10BSP1025

Page 15

Here are the seven wastes in any manufacturing unit:

Over-production Waiting Transporting

Inappropriate Processing Unnecessary Inventory Unnecessary/Excess Motion Defects.

OVER PRODUCTION

Normally most of the manufacturers adopt these principles which works in pushsystem rather than pull system where production is plan in batch and items areproduced in excess to be kept as inventory .Reasons for Over production could be

non- availability of machines , wrong sales forecast stock out of certain raw material ,high change over time .Over production results in waste of money which could havebeen used for other useful activity. Stocks get deterioted if kept for longer time.Few Examples are Producing more than the customer needs right now Producing product to stock based on sales forecasts Producing more to avoid set-upsBatch process resulting in extra output Forecasting Long set-ups Solution could bePull system scheduling,Heijunka – level loading, Set-up reduction

WAITING:

Now this could be a finished product waiting for dispatch , items waiting for the next

phase on the production line or raw material procured in advance for any reason.Thus blocking companies money .Few Examples for waiting areIdle time created when material, information, people, or equipment is not ready

Waiting for partsWaiting for printsWaiting for inspectionWaiting for machinesWaiting for informationWaiting for machine repair

Solution could be Takt time production, In-process gauging,Jidoka,Office Kaizen,TPM

TRANSPORTING

This is due to wrong layout of the production flow as objects are kept at distancewhich has to be moved to production shop floor resulting in waste ( time , labour andcost ) . Care should be taken such that the time spent on transporting items to or fromwarehouse is minimum. Better examples are work stations in any automobile company where every thing is delivered at work station. Low automation on loading,unloading and transporting can save good amount of money.

8/4/2019 Cost Optimization & Diagonstic

http://slidepdf.com/reader/full/cost-optimization-diagonstic 16/70

Conducting Company Diagnostic &Cost Rohit Anand

Optimization Strategy 10BSP1025

Page 16

Few Examples Movement of product that does not add valueMoving parts in and out of storage. Moving material from one workstation to anotherBatch production Solution could be Pull system, Value Stream organizations.

INAPPROPRIATE PROCESSING

In appropriate processing comes into picture when manufacturers go for advance hi-tech machinery for normal job which could have done by conventional machine.These highly automated machines if not handled carefully tends to over produce .Thisalso includes items sourced from a wrong supplier.Few ExamplesOne-piece pullOffice Kaizen3PLean DesignSolution One-piece pull, Office Kaizen, 3P, Lean Design

UNNECESSARY INVENTORY

This happens due to faulty production planning, long lead times also contributes oninventory, long set up time .,Overproduction of finished goods ,WIP .This also happensdue lack of proper ordering procedure based on EOQ .Solution Supplier development, One-piece flow lines, Set-up reduction, Internal kanbanand External kanban

UNECESSARY/EXCESS MOTION:

Normally it is about ergonomics the worker s posture which results in unnecessary motion or few jobs which are done repetitively without adding any value to the job.Few examplesSearching for parts, tools, prints, etc.Sorting through materialsReaching for toolsLifting boxes of partsWorkplace disorganizationMissing itemsPoor workstation designUnsafe work area

5SSolution could be Point of Use Storage, Water Spider, One-piece flow, Workstationdesign

Defects

Defects are shear waste and has to minimised to zero as these are cost to company defective products consumes raw material fuel labour .Cost is incurred on rework on thesedefectives. .Few Examples

8/4/2019 Cost Optimization & Diagonstic

http://slidepdf.com/reader/full/cost-optimization-diagonstic 17/70

Conducting Company Diagnostic &Cost Rohit Anand

Optimization Strategy 10BSP1025

Page 17

VariationMissing partsProcess failureMis-loaded partBatch process

Inspect-in quality Incapable machines

Solution GembaSigma,Pokayoke,One-piece pull, Built-in quality,3P,Jidoka

Ways to Minimize Production :

Reducing waste should be on any manufacturer's list of priorities. There are three basictypes of waste produced by the manufacturing process. The first type, process wastes, isthose that result from transforming lower-value feed materials into higher-value products.

The second type, utility wastes, is those that result from the utility systems that are neededto power the manufacturing process. A third type results from start-ups and shutdowns,maintenance and other offhand operations.

Process wastes are the most costly of the three types and therefore should be the first typethat manufacturers attempt to reduce. By minimizing process wastes, manufacturers canlower the cost of making a certain product and also reduce their investment in treating thewastes that manufacturing the product creates. Furthermore, utility wastes, which can takethe form of released steam, an inefficient boiler, or air and nitrogen leaks, has a directcorrelation with how much process waste is produced.

The DuPont methodology analyzes each waste stream in four steps. The first step is to listall of the waste stream's components. Secondly, the components triggering the concernshould be identified, including hazardous air pollutants and carcinogenic compounds.Third, the highest volume materials (which are often diluents such as air, water, a carriergas or a solvent) must be identified. These materials often control the investment andoperating costs associated with end-treatment of the waste streams. The source of thesediluents within the process must be determined and then waste minimization options mustbe developed to reduce or eliminate them entirely. The fourth step is to identify the nextset of components that has an impact on the investment and operating costs of the end-treatment.

The ultimate goal of the methodology is to guide the manufacturer to a state of efficiency in which all of the materials that are added to or removed from a process are valuable. Inorder to do this, the raw materials that the manufacturer uses, the intermediates, or theproducts themselves, must perform the functions previously performed by input streamssuch as air, water and other catalysts. To come closer to achieving this ideal, themanufacturer needs to undertake a process analysis. The first step in this process analysis isto list all salable products, all raw materials reacting to salable products and any intermediates. The second step of the process analysis is to enumerate all of the othermaterials created in the process, such as non-saleable by-products (waste), on a second list.Third, for each compound in the second list, the process engineer should ask, "how canwe use a material from the first list to do the same function?" or "how can we modify the

process to eliminate the need for this material?" Finally, in considering the materials in thesecond list that result from producing non-saleable products, the process engineer should

8/4/2019 Cost Optimization & Diagonstic

http://slidepdf.com/reader/full/cost-optimization-diagonstic 18/70

Conducting Company Diagnostic &Cost Rohit Anand

Optimization Strategy 10BSP1025

Page 18

ask, "how can we modify the chemistry or process to minimize or eliminate these wastes?"This method of analysis, when correctly used in collaboration with the application of fundamental engineering and chemical practices, can help in developing a technology plan for achieving a manufacturing state that generates the minimum amount of waste.

The beauty of the DuPont methodology is that it uses a minimum amount of time andmoney to define process improvements and to conduct baseline analysis. In addition, ituses existing process information to define process improvement opportunities andprocess characteristics. And, last but not least, it has been proven to work.

Downtime

Downtime is the time from the first equipment breakdown to full running production.Clearly any time production is not producing quality product profits are being lost. That

alone is good reason to address the issues that cause downtime and it's not difficult to do.Simply exposing downtime when it occurs is a great start. The following strategies will help you get a grip on downtime:

• Expose Downtime and Set Goals for Reducing It • Reduce Downtime through Team Awareness • Find Out With OEE

The strategies below depict a few of the many problems our customers ask us to solve andthe solutions we provide. Always feel free to call us if you'd like to discuss a specificproblem or idea. We encourage you to use our application experience to help you reduce

your downtime.

Lean Manufacturing

Lean Manufacturing-- Every organisation is trying to imbibe concept of leanmanufacturing so as to reduce cost and optimum productivity.Basic principles of lean manufacturing are:

Cellular cell: Work places are divided into cells which are then placed in systematic way tohelp smooth flow of process.

5s : Proper management of work place

Kanban system: Pull system when orders move only when demand is present

Six sigma: Eliminating waste and defective through datas and scientific methods

Jit : removing waste from system and reducing inventories

8/4/2019 Cost Optimization & Diagonstic

http://slidepdf.com/reader/full/cost-optimization-diagonstic 19/70

Conducting Company Diagnostic &Cost Rohit Anand

Optimization Strategy 10BSP1025

Page 19

Storage

Receipt of Goods/ Inspection

The vendor shall deliver the goods or services to the desired location in terms of the

delivery instructions provided in the Purchase Order. Delivery not in accordance with

these delivery instructions shall render the vendor liable to non-acceptance of the

delivery. In such a case the vendor shall make arrangements to deliver the goods or

services to the appropriate location and within the time limits as specified in the

Purchase Order at without the Company being liable for any additional expenses that

may be incurred in this connection by the vendor. Also in all cases of deviations from

the delivery instructions provided, the Purchase Department should be informed and

their approval taken in advance.

All deliveries shall be accompanied by all the necessary documentation as mentioned

in the Purchase Order and the security pass shall be obtained at the factory gate. A

Pre inspection GRN is issued through the SAP system.

In the case of outbound logistics the vendor shall arrange for delivery to the relevant

sites and the means of transportation shall comply with all requirements laid down by

the Company in its Purchase Orders and in strict compliance with the norms laid

down by the CCE and other statutory requirements.

The Company carries out inspection testing of incoming materials only at its QA

facilities. No inspection or checks are normally undertaken at other locations or at the

vendors’ facilities and if such inspection and testing is to be carried out, vendorswould be suitably informed in advance or mentioned in the purchase order.

The Company usually insists that a test certificate be provided by the vendor from an

independent agency, or if this is not possible they should at least provide a

certification from their in-house testing facility. On the material being received at the

Stores, the materials are first tagged as under testing. Samples are drawn from the

material and specifications are checked at the QA laboratories. This inspection and

testing should be completed before the expiry of thirty days from the receipt of

materials at Stores.

Based on an inspection of a valid sample, XYZ may reject the goods or services in

whole or in part. If goods delivered or services performed by Vendor are found to be

defective, IEL shall have the right to require the correction thereof by Vendor. XYZ

may charge Vendor the cost of inspecting or re-inspecting rejected goods and/or

services.

Rejected goods will be returned to Vendor, with transportation charges being

collected from the vendor, or held by XYZ for disposition at Vendor's risk and expense.

Vendor shall have to arrange to take back the rejected goods within 90 days of

intimation of rejection by the XYZ and after arranging for all the necessary

documents/permission from statutory authorities. All rejected goods or part thereof

not lifted within 90 days shall be disposed off automatically by the XYZ as scrap andthe vendor will have no claim on them thereafter.

8/4/2019 Cost Optimization & Diagonstic

http://slidepdf.com/reader/full/cost-optimization-diagonstic 20/70

Conducting Company Diagnostic &Cost Rohit Anand

Optimization Strategy 10BSP1025

Page 20

Stocking/Issue

Goods qualifying QA certification is entered into the SAP system as unrestricted stock

and the GRN number is issued.

The total stock in stores can at any time be reviewed from SAP as the sum of QA Pre-

inspection stock, Blocked stock and unrestricted stock. Stocks are released to the

production based on the daily requisition slips from the Production department.

The total stock in stores cannot be fully assessed at any point of time from SAP as under

-inspection stock is not recorded in SAP. The unrestricted stock can be obtained from

the SAP system and the procurement department finds out physically the under-

inspection stocks and adds them to get the total stock. Stores issues engineering spares and consumables against requisition from the user

Departments.

Stocks of coded engineering spares and consumables are maintained separately for

each product group i.e, for Bulk explosives, Packaged Explosives and Initiating systems

and are also maintained separately for routine maintenance.

GRN numbers of items are issued after qualifying inspection but not recorded into the

SAP system.

The User departments are the custodian of these stock items whether it is temporarily

kept in the company’s stores or issued to User departments.

Storage are the godowns for keeping and storing of raw materials , components semi -finished goods , tools, maintenance , repairing and operating equipments and operatingequipments related to production functions. Storage warehouse may be located at any point but usually have strong relationship with production facilities .Operations of storageare all closely related to problems of demand and supply. Storages are most frequently used by firms to meet seasonal demands and supply patterns to level out productionactivities.

Warehouse

Warehouses are the god owns for keeping and storing finished goods facilitating to themarketing and distribution functions of firms.In logistics and supply chain perspective ,ware house performs the storing function ,wheregoods are stored in bulk quantities and from there a new and different small assortmentof goods is selected and moved forward to be dispersed to the next level . Hence,

ware house are generally located near the market for smooth and quick flow of finishedgoods to the customers.

Distribution Centres

The distribution centre is a new idea in supply chain management ,referring to dynamic ,

full service warehouse primarily related to the market .It emphasis on the movement of goods rather than their storage .The emphasis of distribution centres is on quick

8/4/2019 Cost Optimization & Diagonstic

http://slidepdf.com/reader/full/cost-optimization-diagonstic 21/70

Conducting Company Diagnostic &Cost Rohit Anand

Optimization Strategy 10BSP1025

Page 21

movement of goods as per customer requirement along with other logistical supportincluding documentation ,assortment , information sharing ,intact delivery of goods , creditfacility and located near to the market. Warehouse Strategy

Options for any firm for warehousing are

Centralised warehousing Decentralised warehousing

Factors for Selection of Number and Location of Warehouse:

Number of geographical locations of market targeted by the firm. Location of production centres

Transportation infrastructure facilities Nature, quality and quantity of goods stored.

Availability of financial resources Elements of Warehousing Costs: Cost of procurement/rental of space Handling and transfer cost Administrative cost Cost incurred in direct and direct physical facilities Taxes Insurances for risk coverage’s Pilferage , deterioration and obsolescence

Cross docking

This concepts have been used by all major retailers eg care four ,wal-mart, reliance fresh

etc.It requires good to transferred to vehicles scheduled for dispatch to customer s

immediately from goods received from manufacturer immediately .In other words goods

are moved from a receiving dock to a shipping dock without intermediate storage or

the most products are stationed for very Short Span.

Achievement

Stock Levels

Success of the procurement process is interlinked with the success of the storesmanagement. The company should review its Inventory Policies and Procedures to ensuregaps to be filled in this area. Some of the points identified are:

Bin cards are not maintained in the engineering items store

8/4/2019 Cost Optimization & Diagonstic

http://slidepdf.com/reader/full/cost-optimization-diagonstic 22/70

Conducting Company Diagnostic &Cost Rohit Anand

Optimization Strategy 10BSP1025

Page 22

Reorder levels, minimum and maximum levels of stocks are not regularly updated.In some cases such levels are not maintained.

Non coded engineering spares are not are not the responsibility of Stores though

they are received into Stores and are not part of store records. They are the

responsibility of user Departments.

The company should review the Inventory policies and Procedures.

Logistical Services- Outbound/Inbound

Selection of Vendor/Approved List

For selection of vendor the company employs an assessment procedure, through an

assessment form which assesses a number of factors including its valid explosives license

from the Chief Controller of Explosives (for Vans), number of tankers/vans/trucks it hasunder its own fleet all licensed, SHE capability and commitment as per Orica standards,

experience, history of default, capability of handling etc. The Assessment form is available

with the Supply chain department and is amended from time to time.

An approved list of such selected and approved vendors is maintained by the Supply chain

department and the Deputy Manager, is responsible to keep and update such records of

assessment. In most cases the tankers/Vans /Trucks are allotted with the type of material

they shall deliver.

Inclusion of any new vendor or deletion of any vendor from the approved list and any

change of the type of items that any specific vendor shall carry, will be on approval of the

Procurement manager and the Supply chain manager. The changeovers shall be done ina controlled way and the respective tankers/vans/trucks etc shall be re-inspected before

usage.

Agreement

Inbound and outbound logistical services Vendors are usually contracted for on an

annual basis by the Supply Chain Department. The annual agreements are approved

legally by the company’s legal cell or from legal consultants.

Routine assessment

All Tankers/Vans/trucks etc. for all vendors shall be assessed routinely at least once in a

year. An audit checklist is framed by the procurement department to undertake the said

audit procedure and on the basis of the Audit Report the Supply officer decides either to

continue or withdraw the services of the transporter or provide time and deadlines for

appropriate action by the transporter. For all such assessments Safety, Health and

environmental issues and delivery performance shall not be compromised.

In case a transporter or any of its tankers/vans/trucks are withdrawn temporarily or

permanently, the supply chain department shall forthwith inform all the different sites anddepartments and remove the vendor from the list of vendors.

8/4/2019 Cost Optimization & Diagonstic

http://slidepdf.com/reader/full/cost-optimization-diagonstic 23/70

Conducting Company Diagnostic &Cost Rohit Anand

Optimization Strategy 10BSP1025

Page 23

In case the vendor completes its corrective actions the supply chain department shall

undertake fresh assessment and compliance audit as if is a new vendor and if complied

shall re-introduce the vendor in the approved list.

Requisitions

For Outbound logistics, requisitions are usually planned by the Supply chain department

on the basis of the current production plan over a period of a fortnight in advance, and

any changes in actual production as advised by production departments are taken into

account while planning logistical needs.

Transport Orders

Transport orders are generated from SAP which contains the name and address of the

vendor, Order number, date, items to be transported, terms of variable charges, payment

terms, time of delivery, insurance, escalation clauses and specific standard clauses that thevendor should follow for the particular consignment. Besides a General terms and

conditions applicable to all vendors are also attached. The transport orders are usually

issued by the Assistant manager Purchase. For any change in terms and condition or for

transport orders in excess of budget approval is required from the Procurement manager/

supply chain manager.

For each single destination outbound transport order, an Entry sheet is created which

provides for the items/materials to be delivered, place and time of delivery, with estimated

distances in KM. For each such entry sheet a specific entry sheet number is generated in

the SAP system. Rate masters are available in the SAP master with respect to each

destination with respect to each vendor.For Multi destination transport orders similar entry sheets are prepared against an entry

sheet number. The only difference being in case of multi destination transfers in most cases

the estimated costs of the order may change depending on situations. For this additional

Entry sheets need to be generated for the excess budgeted amounts. For this approval of

the Procurement manager/supply chain manager is essential.

For in bound transportation the contracts are usually on a Per Unit of quantity basis. The

rate masters are entered in SAP vendor wise.

Delivery/Payment

Outbound transportation are either to client premises or stock transfer to inter units of the

company. For outbound delivery the company has a 29 point checklist at the security gate

of company premises. After necessary checks if found OK van is allowed to come inside the

factory to take load The van reports to magazine with the Loading Advice and accordingly

the van is loaded as per the product mentioned maintaining FIFO system of the magazine.

The van after completion of loading returns back to Logistics office with the batch details

for further generation of Invoice. The van is checked at the main gate by the security officer

and is released from the factory gate. The final documents are handed over to the driver

after getting endorsement on RE 12.

8/4/2019 Cost Optimization & Diagonstic

http://slidepdf.com/reader/full/cost-optimization-diagonstic 24/70

Conducting Company Diagnostic &Cost Rohit Anand

Optimization Strategy 10BSP1025

Page 24

For inbound delivery the company has a security inspection procedure at gate of

company premises. The security signs the inward challan after checking. The Stores

department checks the quantity after quality and specification checks are made by the QA

department. The transporter submits the Invoice along with the Receipted challan. The

procurement department submits the same along with the printed GRN to the Accounts

department for payment.

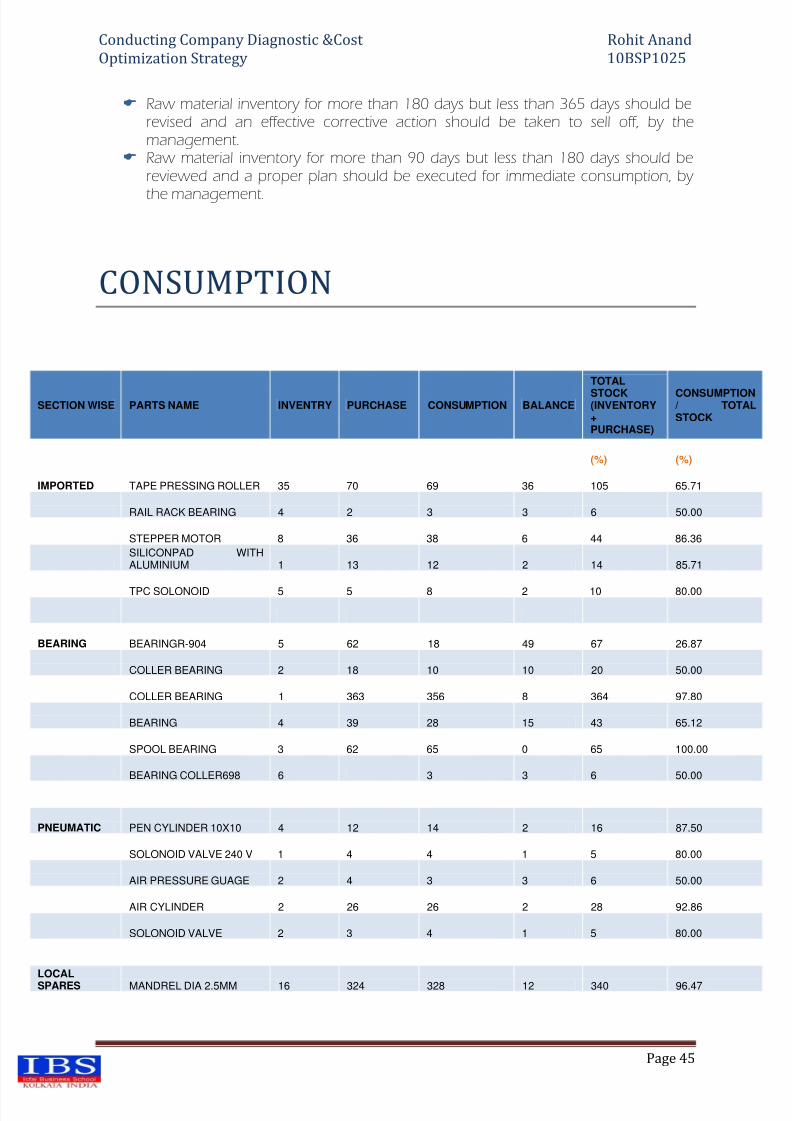

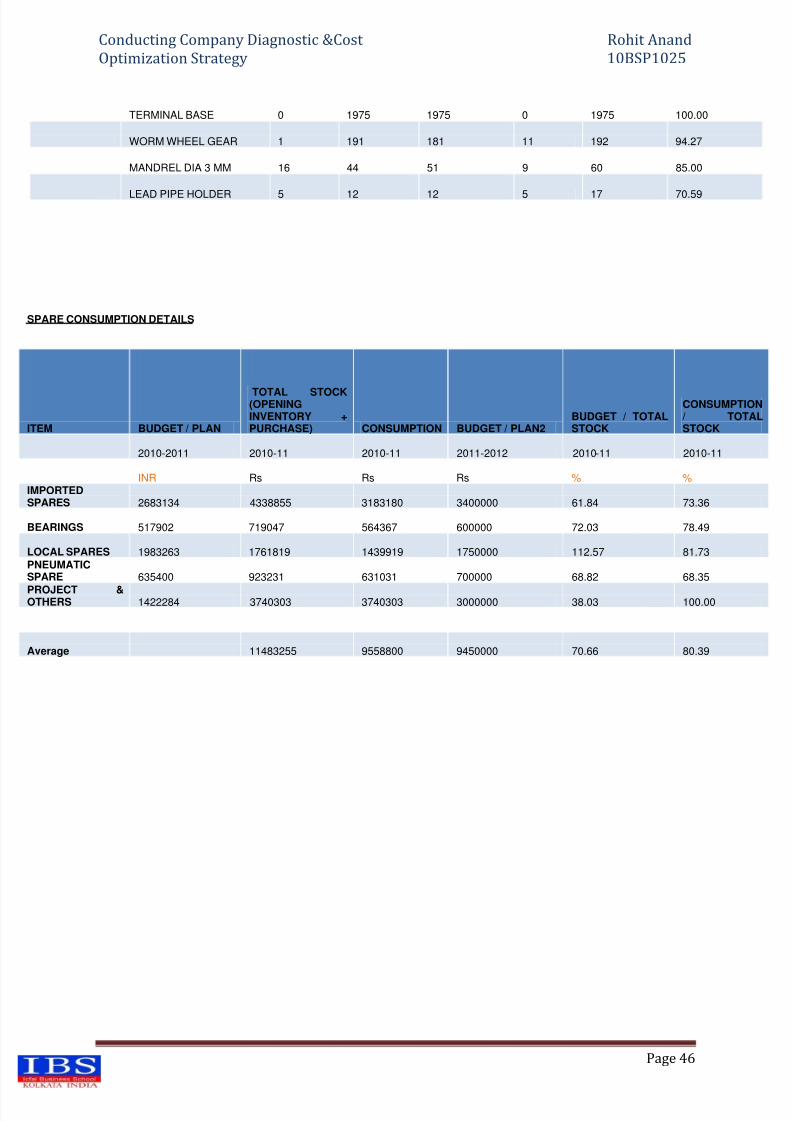

XYZ Defects & Its Remedies:

OBJECTIVE

1. Review of Process-wise Yield and Scrap generation for Mpet.

2. Scrap Generation Flow Diagram for MYLER.

FINDING

8/4/2019 Cost Optimization & Diagonstic

http://slidepdf.com/reader/full/cost-optimization-diagonstic 25/70

Conducting Company Diagnostic &Cost Rohit Anand

Optimization Strategy 10BSP1025

Page 25

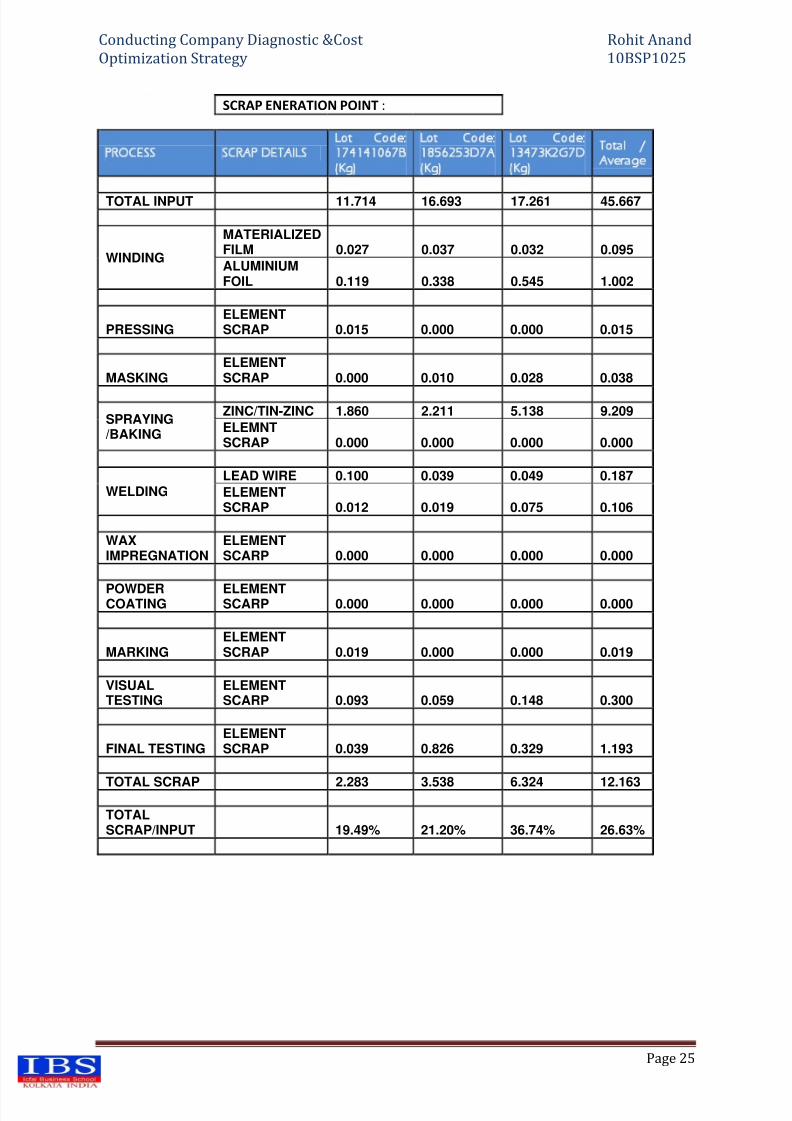

SCRAP ENERATION POINT :

PROCESS SCRAP DETAILSLot Code:174141067B(Kg)

Lot Code:1856253D7A(Kg)

Lot Code:13473K2G7D(Kg)

Total /Average

TOTAL INPUT 11.714 16.693 17.261 45.667

WINDING

MATERIALIZEDFILM 0.027 0.037 0.032 0.095

ALUMINIUMFOIL 0.119 0.338 0.545 1.002

PRESSINGELEMENTSCRAP 0.015 0.000 0.000 0.015

MASKINGELEMENTSCRAP 0.000 0.010 0.028 0.038

SPRAYING/BAKING

ZINC/TIN-ZINC 1.860 2.211 5.138 9.209

ELEMNTSCRAP 0.000 0.000 0.000 0.000

WELDINGLEAD WIRE 0.100 0.039 0.049 0.187

ELEMENTSCRAP 0.012 0.019 0.075 0.106

WAXIMPREGNATION

ELEMENTSCARP 0.000 0.000 0.000 0.000

POWDERCOATING

ELEMENTSCARP 0.000 0.000 0.000 0.000

MARKINGELEMENTSCRAP 0.019 0.000 0.000 0.019

VISUALTESTING

ELEMENTSCARP 0.093 0.059 0.148 0.300

FINAL TESTINGELEMENTSCRAP 0.039 0.826 0.329 1.193

TOTAL SCRAP 2.283 3.538 6.324 12.163

TOTALSCRAP/INPUT 19.49% 21.20% 36.74% 26.63%

8/4/2019 Cost Optimization & Diagonstic

http://slidepdf.com/reader/full/cost-optimization-diagonstic 26/70

Conducting Company Diagnostic &Cost Rohit Anand

Optimization Strategy 10BSP1025

Page 26

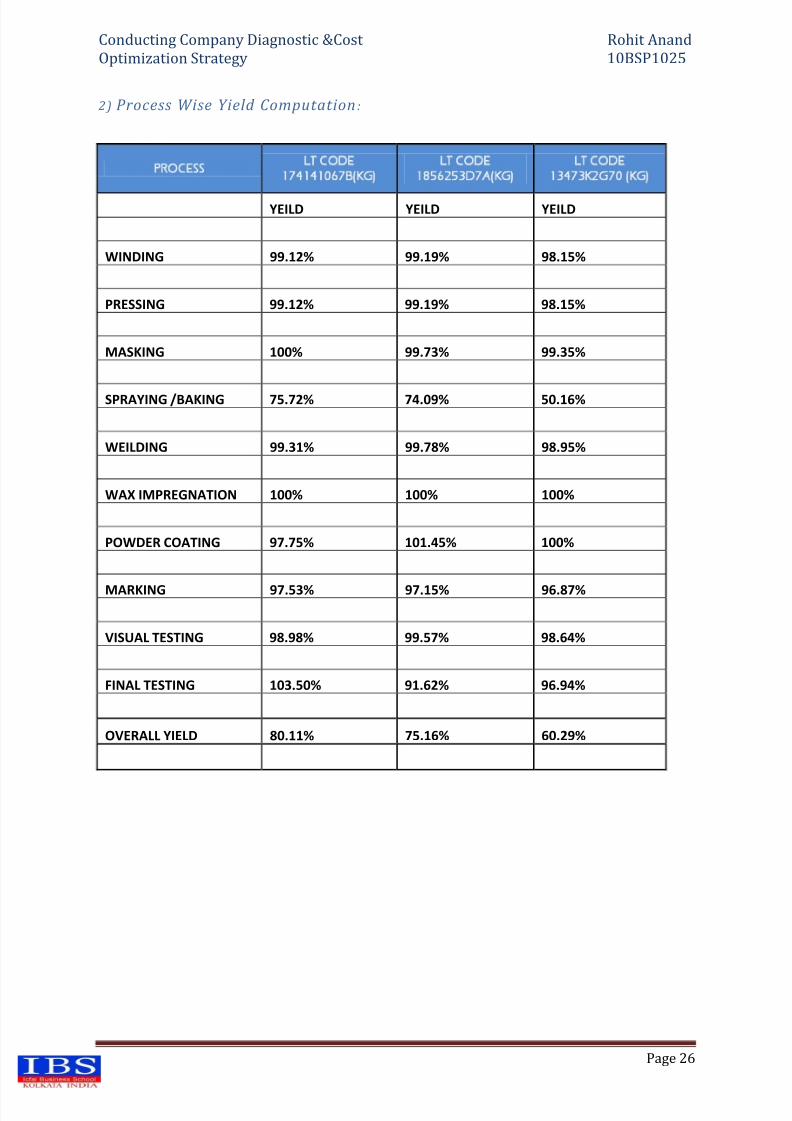

2) Process Wise Yield Computation :

PROCESSLT CODE

174141067B(KG)LT CODE

1856253D7A(KG)LT CODE

13473K2G70 (KG)

YEILD YEILD YEILD

WINDING 99.12% 99.19% 98.15%

PRESSING 99.12% 99.19% 98.15%

MASKING 100% 99.73% 99.35%

SPRAYING /BAKING 75.72% 74.09% 50.16%

WEILDING 99.31% 99.78% 98.95%

WAX IMPREGNATION 100% 100% 100%

POWDER COATING 97.75% 101.45% 100%

MARKING 97.53% 97.15% 96.87%

VISUAL TESTING 98.98% 99.57% 98.64%

FINAL TESTING 103.50% 91.62% 96.94%

OVERALL YIELD 80.11% 75.16% 60.29%

8/4/2019 Cost Optimization & Diagonstic

http://slidepdf.com/reader/full/cost-optimization-diagonstic 27/70

Conducting Company Diagnostic &Cost Rohit Anand

Optimization Strategy 10BSP1025

Page 27

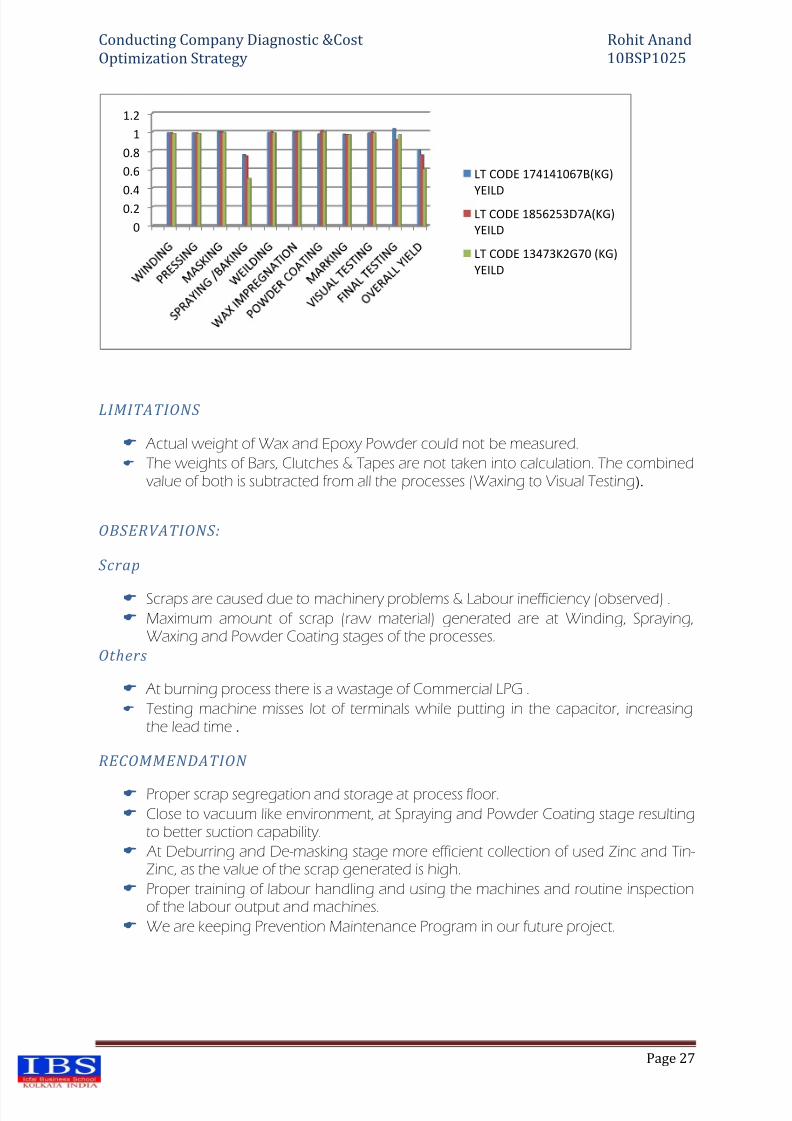

LIMITATIONS

Actual weight of Wax and Epoxy Powder could not be measured.

The weights of Bars, Clutches & Tapes are not taken into calculation. The combinedvalue of both is subtracted from all the processes (Waxing to Visual Testing).

OBSERVATIONS:

Scrap

Scraps are caused due to machinery problems & Labour inefficiency (observed) .

Maximum amount of scrap (raw material) generated are at Winding, Spraying,Waxing and Powder Coating stages of the processes.

Others

At burning process there is a wastage of Commercial LPG .

Testing machine misses lot of terminals while putting in the capacitor, increasingthe lead time .

RECOMMENDATION

Proper scrap segregation and storage at process floor.

Close to vacuum like environment, at Spraying and Powder Coating stage resultingto better suction capability.

At Deburring and De-masking stage more efficient collection of used Zinc and Tin-Zinc, as the value of the scrap generated is high.

Proper training of labour handling and using the machines and routine inspectionof the labour output and machines.

We are keeping Prevention Maintenance Program in our future project.

0

0.20.4

0.6

0.8

1

1.2

LT CODE 174141067B(KG)

YEILDLT CODE 1856253D7A(KG)

YEILD

LT CODE 13473K2G70 (KG)

YEILD

8/4/2019 Cost Optimization & Diagonstic

http://slidepdf.com/reader/full/cost-optimization-diagonstic 28/70

Conducting Company Diagnostic &Cost Rohit Anand

Optimization Strategy 10BSP1025

Page 28

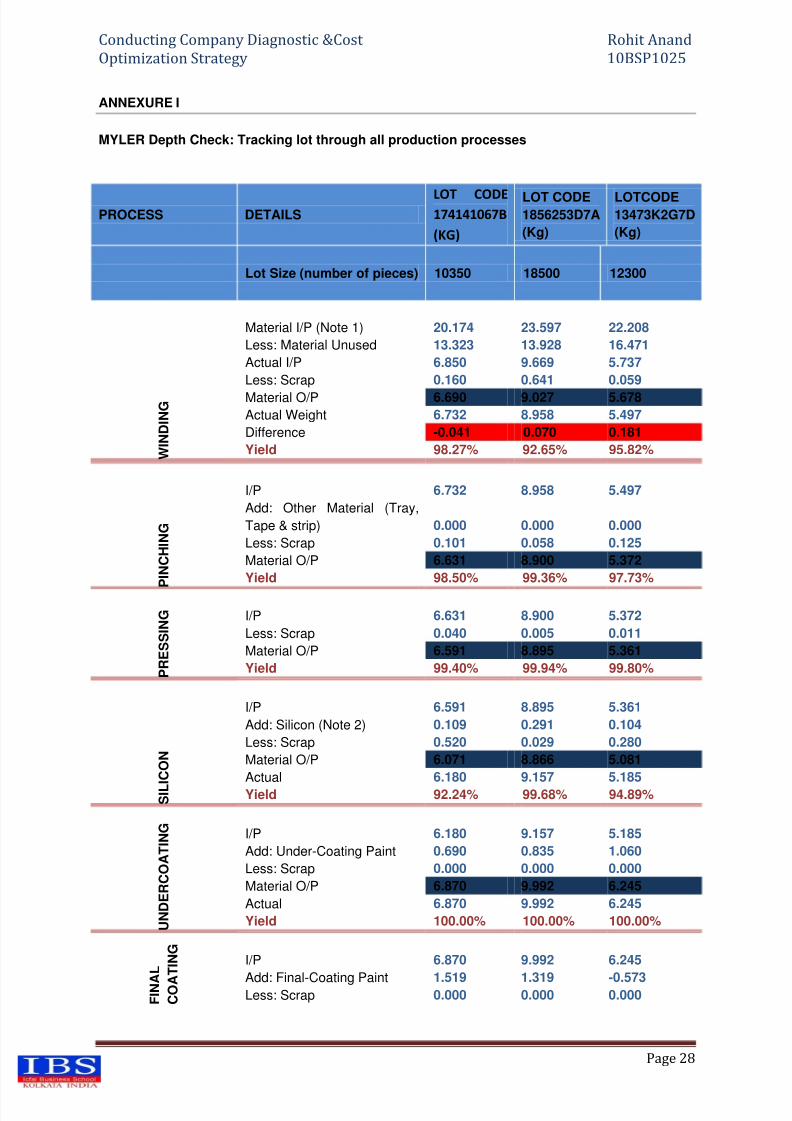

ANNEXURE I

MYLER Depth Check: Tracking lot through all production processes

PROCESS DETAILSLOT CODE174141067B

(KG)

LOT CODE1856253D7A

(Kg)

LOTCODE13473K2G7D

(Kg)

Lot Size (number of pieces) 10350 18500 12300

W I N D I N G

Material I/P (Note 1) 20.174 23.597 22.208

Less: Material Unused 13.323 13.928 16.471

Actual I/P 6.850 9.669 5.737

Less: Scrap 0.160 0.641 0.059

Material O/P 6.690 9.027 5.678

Actual Weight 6.732 8.958 5.497

Difference -0.041 0.070 0.181

Yield 98.27% 92.65% 95.82%

P I N C H I N G

I/P 6.732 8.958 5.497

Add: Other Material (Tray,

Tape & strip) 0.000 0.000 0.000

Less: Scrap 0.101 0.058 0.125

Material O/P 6.631 8.900 5.372

Yield 98.50% 99.36% 97.73%

P R E S S I N G

I/P 6.631 8.900 5.372

Less: Scrap 0.040 0.005 0.011

Material O/P 6.591 8.895 5.361

Yield 99.40% 99.94% 99.80%

S I L I C O N

I/P 6.591 8.895 5.361

Add: Silicon (Note 2) 0.109 0.291 0.104

Less: Scrap 0.520 0.029 0.280

Material O/P 6.071 8.866 5.081

Actual 6.180 9.157 5.185

Yield 92.24% 99.68% 94.89%

U N D E R C O A T I N G

I/P 6.180 9.157 5.185

Add: Under-Coating Paint 0.690 0.835 1.060

Less: Scrap 0.000 0.000 0.000

Material O/P 6.870 9.992 6.245

Actual 6.870 9.992 6.245

Yield 100.00% 100.00% 100.00%

F I N A

L

C O A

T I N G

I/P 6.870 9.992 6.245

Add: Final-Coating Paint 1.519 1.319 -0.573Less: Scrap 0.000 0.000 0.000

8/4/2019 Cost Optimization & Diagonstic

http://slidepdf.com/reader/full/cost-optimization-diagonstic 29/70

Conducting Company Diagnostic &Cost Rohit Anand

Optimization Strategy 10BSP1025

Page 29

Actual 8.389 11.311 5.672

Yield

100.00% 100.00% 100.00%

V I S U A L T E S T I N G

I/P 8.389 11.311 5.672

Less: Scrap 0.912 0.331 0.002

Material O/P 7.477 10.980 5.670

Yield

89.13% 97.07% 99.96%

F I N A L T

E S T I N G

I/P 7.477 10.980 5.670

Less: Scrap 0.028 0.014 0.052

Final O/P 7.449 10.966 5.619

Actual 7.397 10.963 5.554Difference 0.053 0.003 0.064

Yield 98.92% 99.84% 97.95%

Total Input 9.168 12.114 6.328

Total Output 7.397 10.963 5.554

Total Scrap 1.760 1.078 0.529

Output + Scrap 9.157 12.040 6.083

Material Balance Differential {I/P - (O/P + Scrap)} 0.011 0.073 0.245

Overall Yield 80.68% 90.50% 87.77%

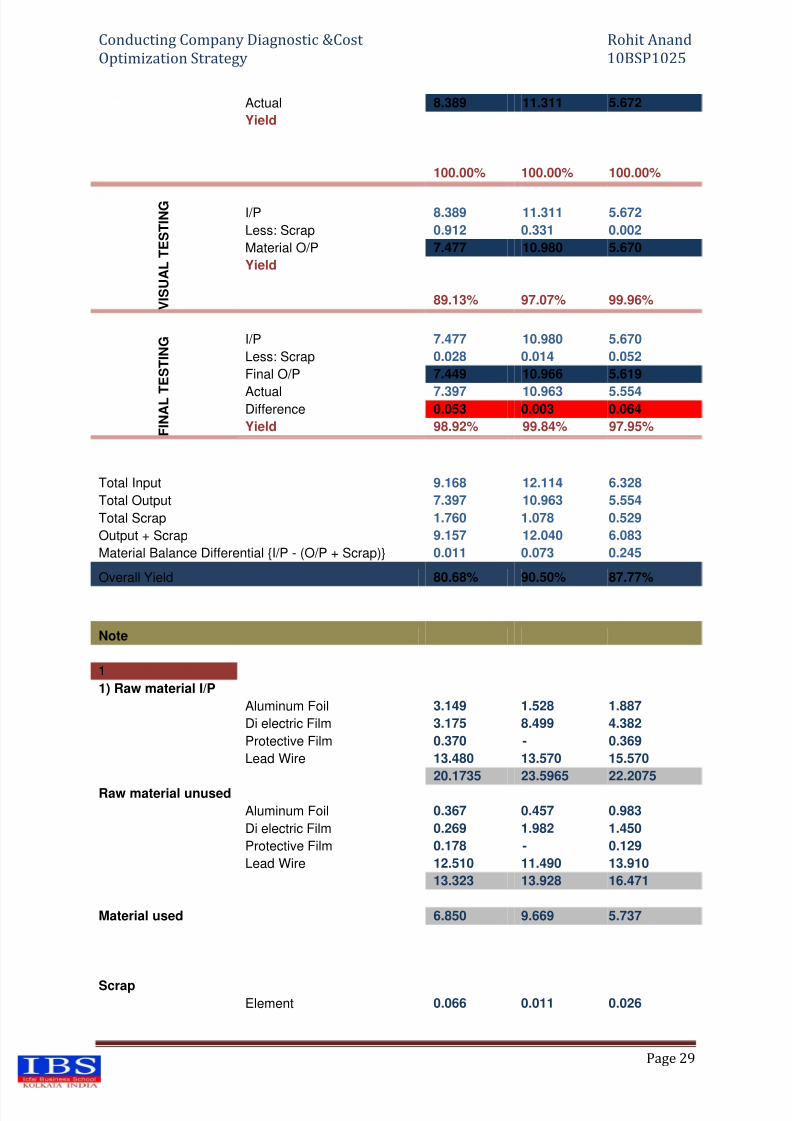

Note

1

1) Raw material I/P

Aluminum Foil 3.149 1.528 1.887

Di electric Film 3.175 8.499 4.382

Protective Film 0.370 - 0.369

Lead Wire 13.480 13.570 15.570

20.1735 23.5965 22.2075

Raw material unused

Aluminum Foil 0.367 0.457 0.983

Di electric Film 0.269 1.982 1.450

Protective Film 0.178 - 0.129

Lead Wire 12.510 11.490 13.910

13.323 13.928 16.471

Material used 6.850 9.669 5.737

ScrapElement 0.066 0.011 0.026

8/4/2019 Cost Optimization & Diagonstic

http://slidepdf.com/reader/full/cost-optimization-diagonstic 30/70

Conducting Company Diagnostic &Cost Rohit Anand

Optimization Strategy 10BSP1025

Page 30

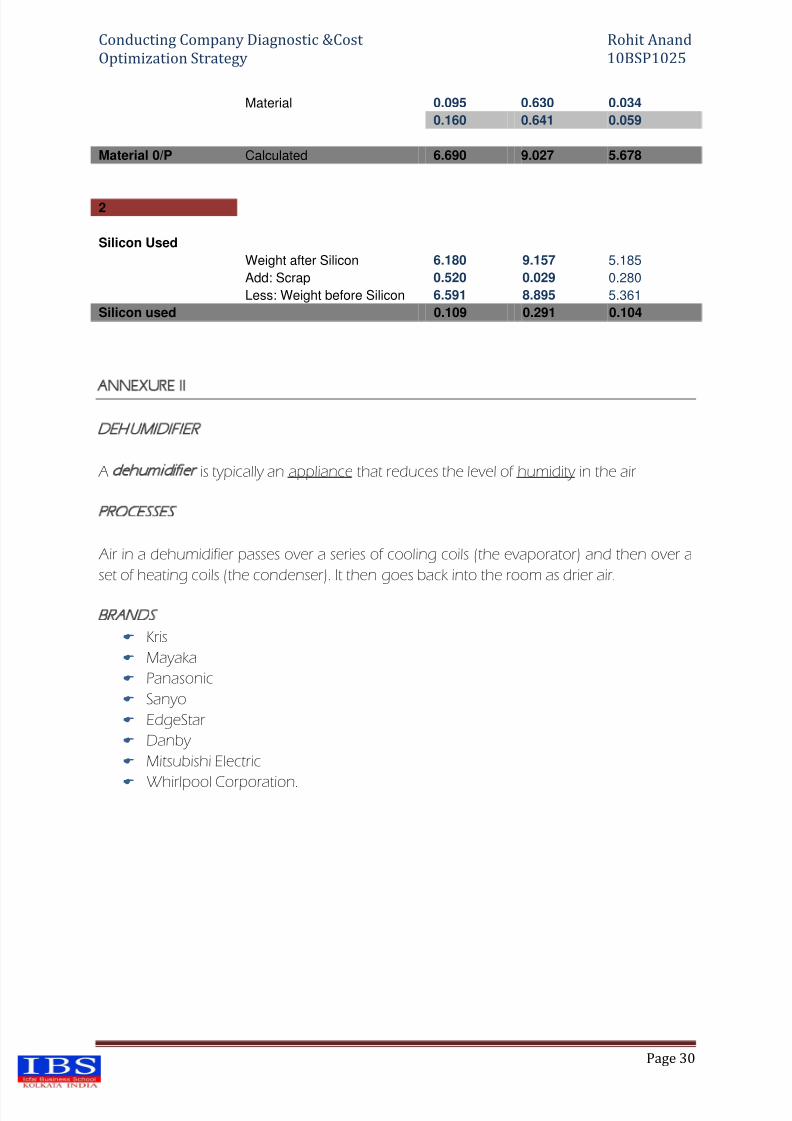

Material 0.095 0.630 0.034

0.160 0.641 0.059

Material 0/P Calculated 6.690 9.027 5.678

2

Silicon Used

Weight after Silicon 6.180 9.157 5.185

Add: Scrap 0.520 0.029 0.280

Less: Weight before Silicon 6.591 8.895 5.361

Silicon used 0.109 0.291 0.104

ANNEXURE II

DEHUMIDIFIER

A dehumidifier is typically an appliance that reduces the level of humidity in the air

PROCESSES

Air in a dehumidifier passes over a series of cooling coils (the evaporator) and then over a

set of heating coils (the condenser). It then goes back into the room as drier air.

BRANDS

Kris

Mayaka

Panasonic

Sanyo

EdgeStar

Danby

Mitsubishi Electric

Whirlpool Corporation.

8/4/2019 Cost Optimization & Diagonstic

http://slidepdf.com/reader/full/cost-optimization-diagonstic 31/70

Conducting Company Diagnostic &Cost Rohit Anand

Optimization Strategy 10BSP1025

Page 31

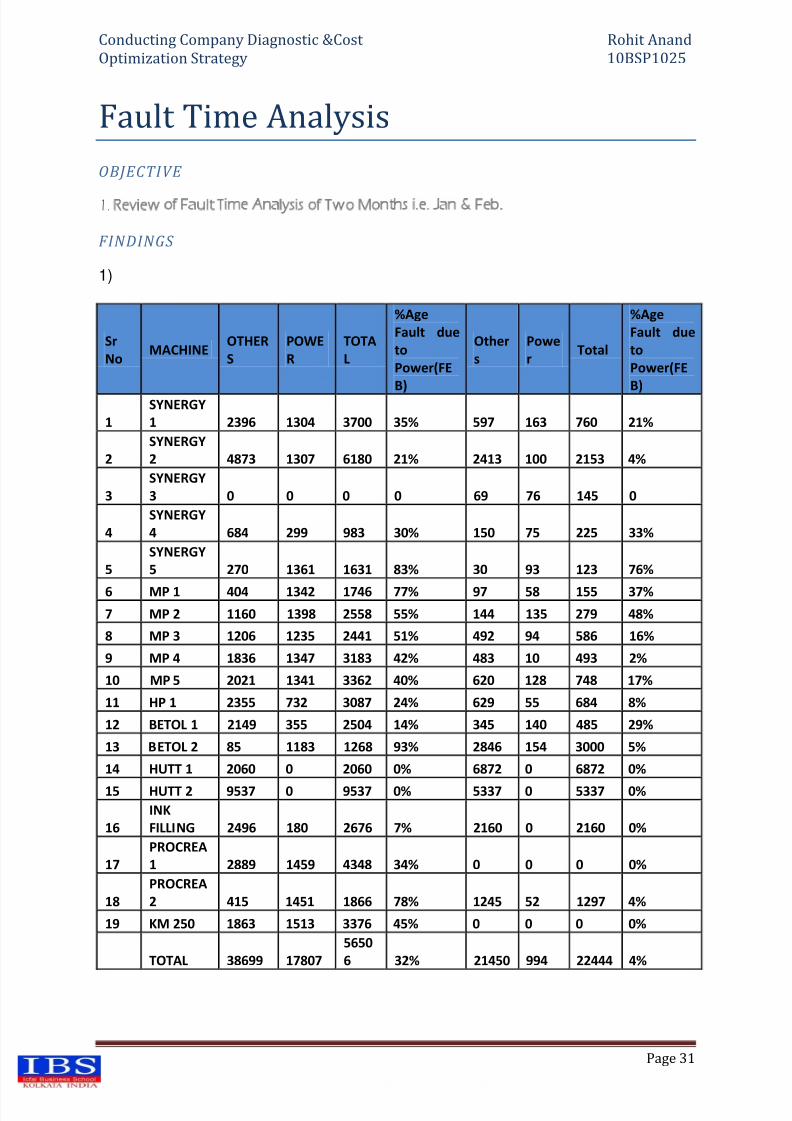

Fault Time Analysis

OBJECTIVE

1. Review of Fault Time Analysis of Two Months i.e. Jan & Feb.

FINDINGS

1)

Sr

NoMACHINE

OTHER

S

POWE

R

TOTA

L

%Age

Fault due

to

Power(FE

B)

Other

s

Powe

rTotal

%Age

Fault due

to

Power(FE

B)

1

SYNERGY

1 2396 1304 3700 35% 597 163 760 21%

2

SYNERGY

2 4873 1307 6180 21% 2413 100 2153 4%

3

SYNERGY

3 0 0 0 0 69 76 145 0

4

SYNERGY

4 684 299 983 30% 150 75 225 33%

5

SYNERGY

5 270 1361 1631 83% 30 93 123 76%

6 MP 1 404 1342 1746 77% 97 58 155 37%

7 MP 2 1160 1398 2558 55% 144 135 279 48%

8 MP 3 1206 1235 2441 51% 492 94 586 16%

9 MP 4 1836 1347 3183 42% 483 10 493 2%

10 MP 5 2021 1341 3362 40% 620 128 748 17%

11 HP 1 2355 732 3087 24% 629 55 684 8%

12 BETOL 1 2149 355 2504 14% 345 140 485 29%

13 BETOL 2 85 1183 1268 93% 2846 154 3000 5%

14 HUTT 1 2060 0 2060 0% 6872 0 6872 0%

15 HUTT 2 9537 0 9537 0% 5337 0 5337 0%

16

INK

FILLING 2496 180 2676 7% 2160 0 2160 0%

17

PROCREA

1 2889 1459 4348 34% 0 0 0 0%

18

PROCREA

2 415 1451 1866 78% 1245 52 1297 4%

19 KM 250 1863 1513 3376 45% 0 0 0 0%

TOTAL 38699 17807

5650

6 32% 21450 994 22444 4%

8/4/2019 Cost Optimization & Diagonstic

http://slidepdf.com/reader/full/cost-optimization-diagonstic 32/70

Conducting Company Diagnostic &Cost Rohit Anand

Optimization Strategy 10BSP1025

Page 32

2) FINDINGS FROM DATA

WE FIND THAT % FAULT DUE TO POWER IS MORE IN FEBURARY WHICH IS 32%

COMPARED TO THAT IN JANURARY WHICH IS 4% WHICH MIGHT BE DUE TO STOCK

OUT OF RAW MATERIAL IN MONTH OF FEBURARY 2011 WHICH CAN BE SEEN MARKEDRED IN COLOUR FOR CONVENIENCE FROM ABOVE TABLE .WE HAVE PLOTTED THE

CONSUMPTION (=ISSUE) VS STOCKING PATTERN TO ELABORATE THIS POINT .

3) RECOMMENDATION

Proper training of labour handling and using the machines and routineinspection of the labour output and machines.

We are keeping Prevention Maintenance Program in our future project.

Proper Maintenance of required Raw Material to avoid Stock out Of Raw

material. Ensuring suitable supply of Power to make proper use of Machine.

8/4/2019 Cost Optimization & Diagonstic

http://slidepdf.com/reader/full/cost-optimization-diagonstic 33/70

Conducting Company Diagnostic &Cost Rohit Anand

Optimization Strategy 10BSP1025

Page 33

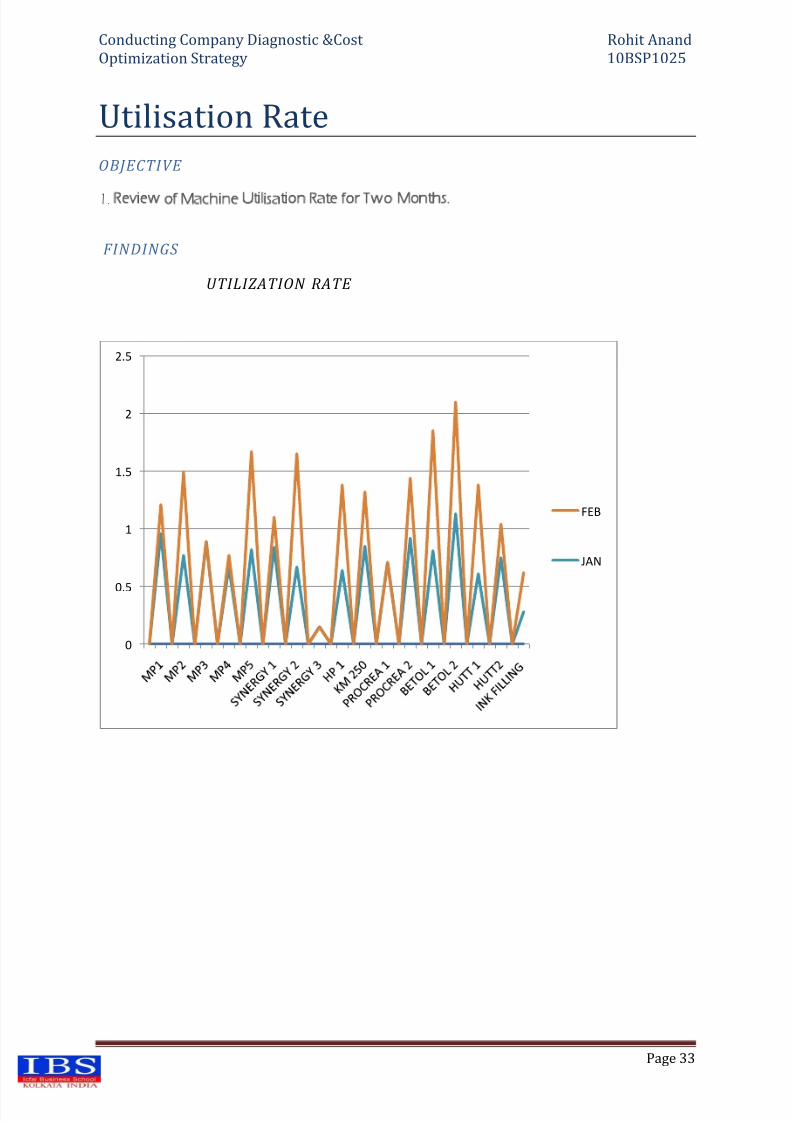

Utilisation Rate

OBJECTIVE

1. Review of Machine Utilisation Rate for Two Months.

FINDINGS

UTILIZATION RATE

0

0.5

1

1.5

2

2.5

FEB

JAN

8/4/2019 Cost Optimization & Diagonstic

http://slidepdf.com/reader/full/cost-optimization-diagonstic 34/70

Conducting Company Diagnostic &Cost Rohit Anand

Optimization Strategy 10BSP1025

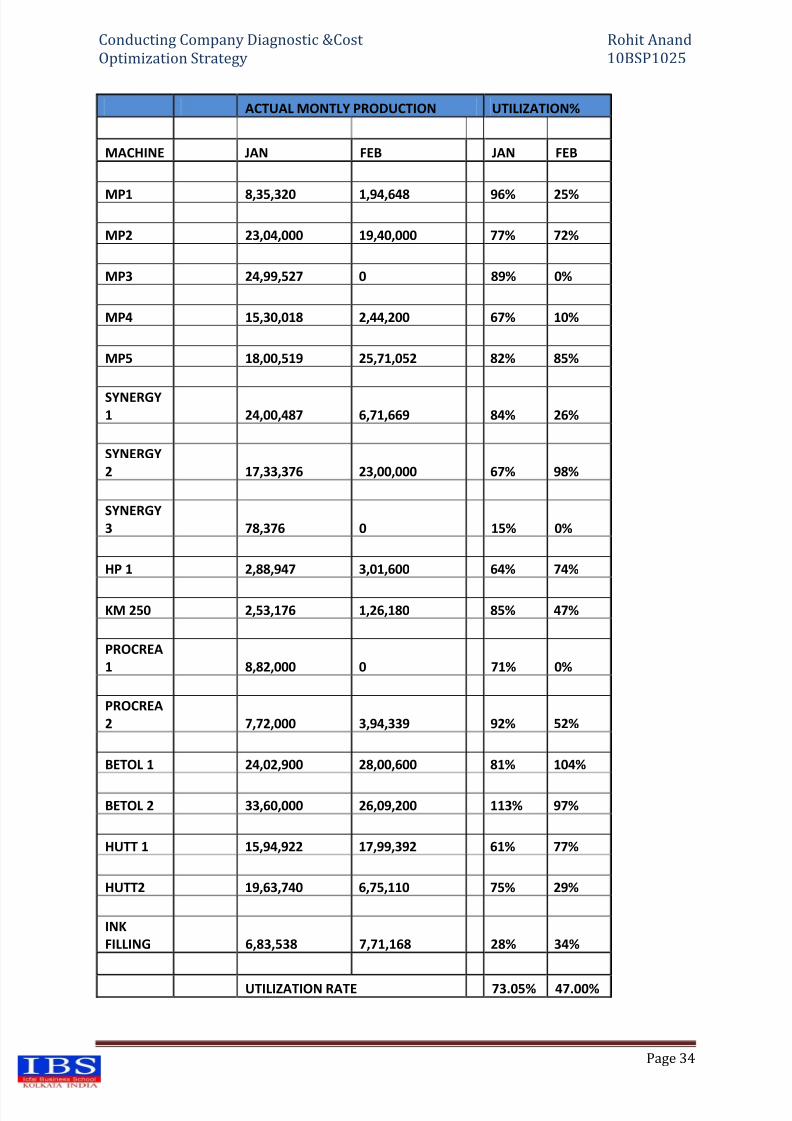

Page 34

ACTUAL MONTLY PRODUCTION UTILIZATION%

MACHINE JAN FEB JAN FEB

MP1 8,35,320 1,94,648 96% 25%

MP2 23,04,000 19,40,000 77% 72%

MP3 24,99,527 0 89% 0%

MP4 15,30,018 2,44,200 67% 10%

MP5 18,00,519 25,71,052 82% 85%

SYNERGY1 24,00,487 6,71,669 84% 26%

SYNERGY

2 17,33,376 23,00,000 67% 98%

SYNERGY

3 78,376 0 15% 0%

HP 1 2,88,947 3,01,600 64% 74%

KM 250 2,53,176 1,26,180 85% 47%

PROCREA

1 8,82,000 0 71% 0%

PROCREA

2 7,72,000 3,94,339 92% 52%

BETOL 1 24,02,900 28,00,600 81% 104%

BETOL 2 33,60,000 26,09,200 113% 97%

HUTT 1 15,94,922 17,99,392 61% 77%

HUTT2 19,63,740 6,75,110 75% 29%

INK

FILLING 6,83,538 7,71,168 28% 34%

UTILIZATION RATE 73.05% 47.00%

8/4/2019 Cost Optimization & Diagonstic

http://slidepdf.com/reader/full/cost-optimization-diagonstic 35/70

Conducting Company Diagnostic &Cost Rohit Anand

Optimization Strategy 10BSP1025

Page 35

FINDINGS FROM FOLLOWING TABLES

WE FIND THAT FROM ABOVE DATA THAT MACHINE UTILISATION RATE IS BETTER IN

JANURARY WHICH IS AROUND-73.05% WHICH IS FAR BETTER THAN THAT OF

FEBURARY WHICH IS ABOUT 47%, FALL IN UTILISATION RATE MIGHT BE DUE TO

MACHINE MAINTENACE, POWER FAILURE, RAW MATERIAL SHORTAGE AND LACK OF

LABOUR OR DEMAND FOR THAT PARTICULAR PRODUCT .

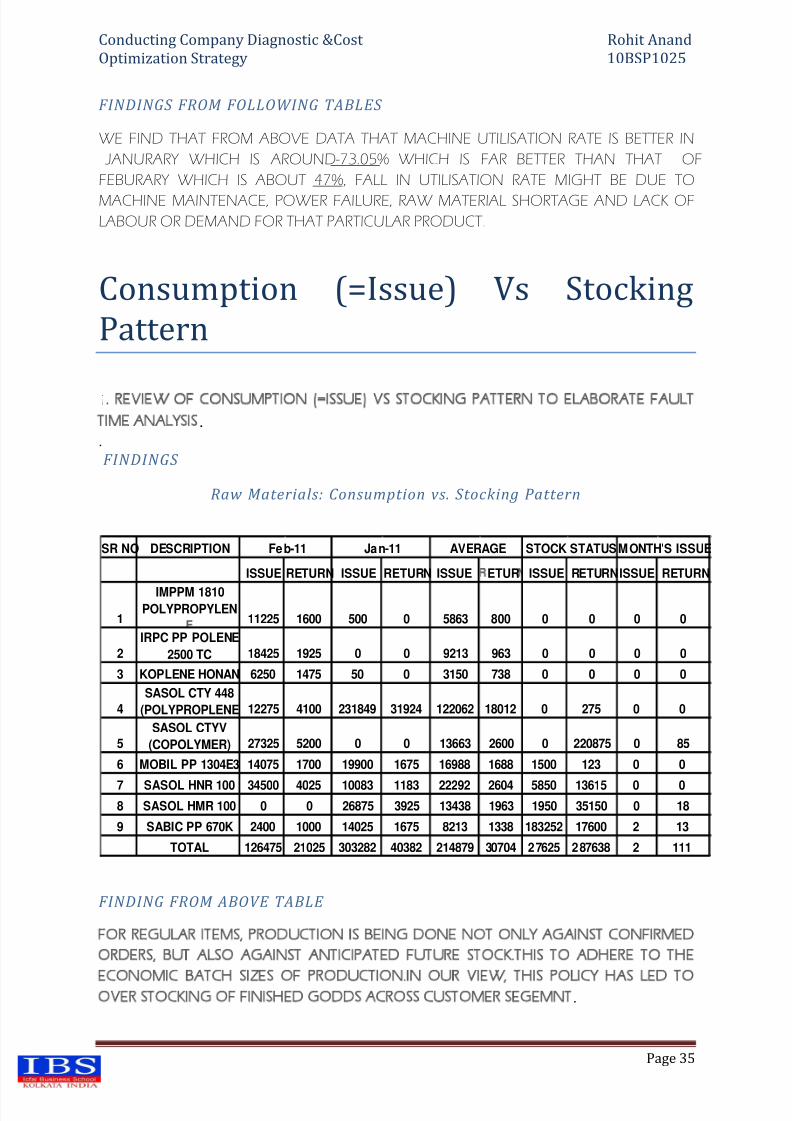

Consumption (=Issue) Vs Stocking

Pattern

1. REVIEW OF CONSUMPTION (=ISSUE) VS STOCKING PATTERN TO ELABORATE FAULT

TIME ANALYSIS. .

FINDINGS

Raw Materials: Consumption vs. Stocking Pattern

FINDING FROM ABOVE TABLE

FOR REGULAR ITEMS, PRODUCTION IS BEING DONE NOT ONLY AGAINST CONFIRMED

ORDERS, BUT ALSO AGAINST ANTICIPATED FUTURE STOCK.THIS TO ADHERE TO THE

ECONOMIC BATCH SIZES OF PRODUCTION.IN OUR VIEW, THIS POLICY HAS LED TOOVER STOCKING OF FINISHED GODDS ACROSS CUSTOMER SEGEMNT.

SR NO DESCRIPTION

ISSUE RETURN ISSUE RETURN ISSUE ETUR ISSUE RETURNISSUE RETURN

1

IMPPM 1810POLYPROPYLEN

11225 1600 500 0 5863 800 0 0 0 0

2

IRPC PP POLENE

2500 TC 18425 1925 0 0 9213 963 0 0 0 0

3 KOPLENE HONAN 6250 1475 50 0 3150 738 0 0 0 0

4

SASOL CTY 448

(POLYPROPLENE 12275 4100 231849 31924 122062 18012 0 275 0 0

5

SASOL CTYV

(COPOLYMER) 27325 5200 0 0 13663 2600 0 220875 0 85

6 MOBIL PP 1304E3 14075 1700 19900 1675 16988 1688 1500 123 0 0

7 SASOL HNR 100 34500 4025 10083 1183 22292 2604 5850 13615 0 08 SASOL HMR 100 0 0 26875 3925 13438 1963 1950 35150 0 18

9 SABIC PP 670K 2400 1000 14025 1675 8213 1338 183252 17600 2 13

TOTAL 126475 21025 303282 40382 214879 30704 27625 287638 2 111

Feb-11 Jan-11 AVERAGE STOCK STATUSMONTH'S ISSUE

8/4/2019 Cost Optimization & Diagonstic

http://slidepdf.com/reader/full/cost-optimization-diagonstic 36/70

Conducting Company Diagnostic &Cost Rohit Anand

Optimization Strategy 10BSP1025

Page 36

Havells Capacitors a Step Further In

Energy Conservation

Today's world is dependent on electricity. For economic prosperity and securing the futureit is necessary that everyone should contribute to prevent themselves and environmentfrom the losses occurring due to distribution.

The prime concern of today's world is energy conservation in the most effective way,catering to this need of the society, in most modern world our dependency on thecapacitor is increasing day by day. Capacitors are designed to improve the power factor.These capacitors improve "Active Power" and reduce "Reactive Power" that helps in savingenergy.

Power saving is a vital issue today. An acute shortage of electrical power has been felt andmore importantly it has been very well accepted that the resources are limited. Therefore,energy saving need to be looked upon as one of the key initiative to mitigate the problemin near future.

Normal practice is to consider the parameter of actual amount of money spent on usageof electrical energy is considered and direct expenditure incurred on power becomes thepoint of focus and all the effort are taken to improve upon that. Normal efforts are alwaysoriented towards saving in Active Energy, i.e., kWh unless it is made mandatory by Electricity Board to control Power Factor.

In this process, the user is mostly unaware of problems that arise in the society. The adverseaffect of quality of power on saving and in generating electrical pollution are generally unknown to the industrial user. In their pursuit of energy saving, little attention is paid tothe issue of power quality.

The indirect effect of power quality poses problem not only to user but also on distributionand generation. Every day, we witness losses due to power failure, load shedding andgeneration, cascade failure of turbine in a grid, blowing up of transformers, sustain low voltage, etc. At the root of these problems is increasing pollution of electrical power causedby poor power factor, high harmonics content and high crest factor. This causestremendous strain on our power resources; therefore optimum use of power must be

exercised. Power saving in real sense cannot be achieved unless all these aspects areconsidered, studied and rectified.

Society needs to be cautious of all these factors, while using electricity in whichever form.Therefore, the perspective should not only from the point of direct saving but also asindirect and additional savings through power conservation.

Voltage and Current are two most important parameters on which quality of power canbe examined. While voltage is within the control of the power generation and distributionagency, current is under total control of the user. Maximum synchronisation of these twoparameters would achieve a goal of "saving" in totality and would ensure the best quality of power. These two parameters must go hand in hand and any shift between themwould lead to introduction of ineffective use of power and would results in monetary

8/4/2019 Cost Optimization & Diagonstic

http://slidepdf.com/reader/full/cost-optimization-diagonstic 37/70

Conducting Company Diagnostic &Cost Rohit Anand

Optimization Strategy 10BSP1025

Page 37

losses. In power saving and quality of power, Power Factor improvement is the mostimportant area, which needs to be focused on priority.

However, most of the electricity boards/distribution companies have made it compulsory to improve the Power Factor to a level of 0.90 minimum. This level varies for different states.

Power capacitor plays a vital role not only in power saving but also in improving the quality of power. The ordinary capacitor normally available in the Indian market is mainly in therange of 1 to 25 KVAr as single unit, which can be increased to any rating by the way of parallel connecting these capacitors. There are different technologies existing in thecapacitor like MPP, APP, mixed dielectric, etc.

The latest state-of-the-art technology is the metallised polypropylene capacitor, which ishaving self-healing property. It gets self-healed even in case of any puncture in thedielectric due to over voltage or over current. It has the lowest losses in the capacitor incomparison to other technologies of capacitor.

Now with these advances, MPP type capacitor is the best option for not only improvingpower quality but also act as a major component in optimum utilisation of electricalenergy. The entire range of MPP capacitors is meticulously made to provide consumers thebest and consistent performance.

In today's state, it has become very important to increase the use of MPP capacitors andimprove the power factor in all the areas, which will save energy at local level as well asnational level. This in turn will give us less load shedding and improved level of powersupply without disturbance with less price.

Low watt loss, less heating gives extra edge to life For a consistent and reliable product it isrequired to adopt the best practices, which requires following conditions in control:

Machinery Raw Material Control Process Control Environment

At Havells we have taken care of all the above mentioned parameters.

Winding Machine: Today the company has the worlds latest generation windingmachines. These machines are imported from Switzerland and are of very high speed.These machines are very useful from the customer point of view as these do not allow thecapacitor manufacturer to use low grade of polypropylene film in the capacitor, which waspossible with the earlier machines of same make. Thanks to the latest technologicaladvances, these machines even do automatic staggering and provide consistent outputquality. However, the earlier machines were also automatic in terms of winding, filmfeeding, core feeding, etc., but the staggering was required to be done manually so thechances of human error were possible.

Raw Material: The base film, i.e., polypropylene, which is the main part of any capacitorshould be of best quality. Thanks to world latest machines Havells customers can be restassured that lower grade MPP cannot be used. Presently the company is using films fromTreofan - Germany and Oji - Japan, which also have a very good break down voltage.

8/4/2019 Cost Optimization & Diagonstic

http://slidepdf.com/reader/full/cost-optimization-diagonstic 38/70

Conducting Company Diagnostic &Cost Rohit Anand

Optimization Strategy 10BSP1025

Page 38

Control Process: To have a control output quality, process needs to be controlled. AtHavells even the small process to make the notch mechanism is also fully automatic. Otherprocesses, which include testing, self clearing, spray painting all is fully automatic, wherethe function of the operator is only to load the job. Especially the zinc spray, which isanother very important process after winding, is fully automatic and spray process on both

the sides is completed in single operation.

Control Environment: Since moisture and dust are very much detrimental for the capacitor,it is very important that winding should be done in the controlled environment. Windingroom at Havells covers all the important factors, which include:

Air on the work area is controlled for its flow, temperature, humidity and dust. Winding room is equipped with air handle unit with risers, filters, pre-filters and

fresh air source. AHU is designed for 1000 Class Accuracy (300 particles/ft3 of 0.3 mm size and 100

particles/ft3 of 0.5 mm size).

The winding room is provided with air showers (1000 Class) that blast dust fromclothes. Also act as airlocks to prevent contaminants.

Entry into winding room only with air showers, aprons, hair caps and shoe covers.

With all the above controls, the company is able to achieve the lowest watt loss in theindustry. Where Industry norms are 0.5 watt/kVAr even the best of manufacturers couldnot be able to go beyond 0.35 Watt/kVAr, the per kVAr watt loss of Havells capacitor is tothe tune of 0.06 Watt/kVAr to 0.25 Watt/kVAr.

Thus, Havells has tried to do the basics right and the product output is consistent andcontrolled.

8/4/2019 Cost Optimization & Diagonstic

http://slidepdf.com/reader/full/cost-optimization-diagonstic 39/70

Conducting Company Diagnostic &Cost Rohit Anand

Optimization Strategy 10BSP1025

Page 39

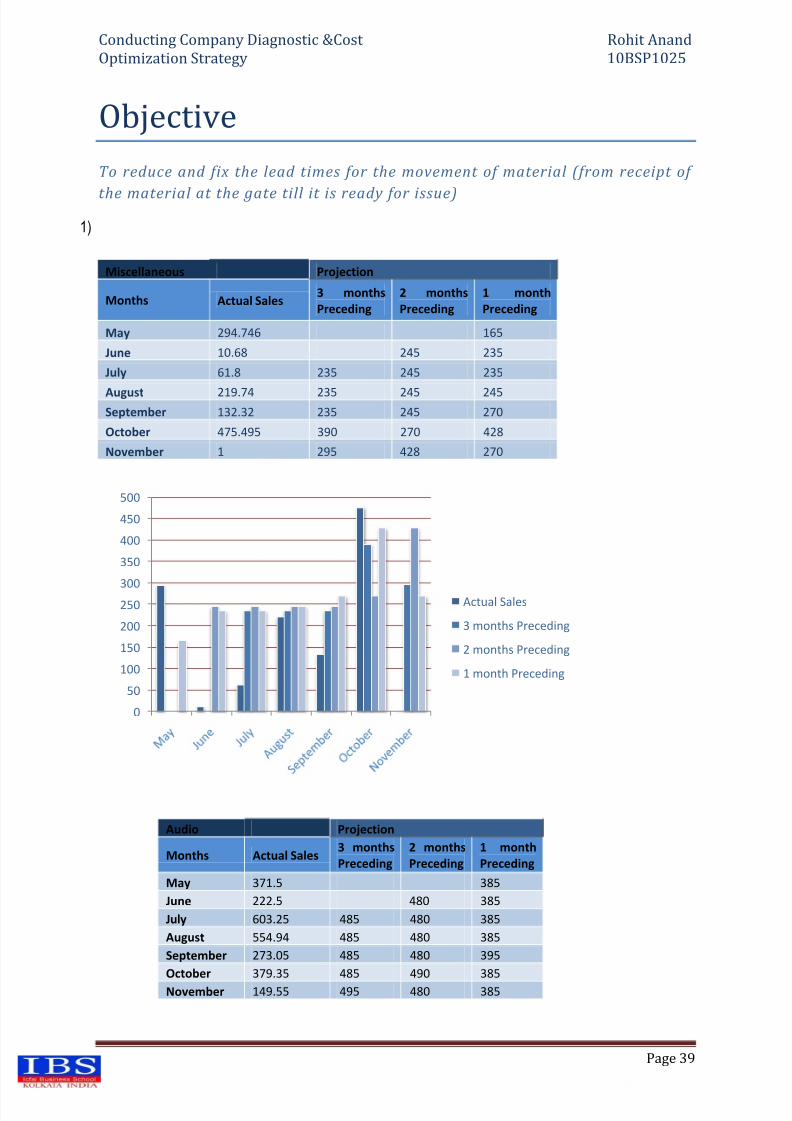

Objective

To reduce and fix the lead times for the movement of material (from receipt of

the material at the gate till it is ready for issue)

1)

Miscellaneous Projection

Months Actual Sales3 months

Preceding

2 months

Preceding

1 month

Preceding

May 294.746 165

June 10.68 245 235

July 61.8 235 245 235

August 219.74 235 245 245September 132.32 235 245 270

October 475.495 390 270 428

November 1 295 428 270

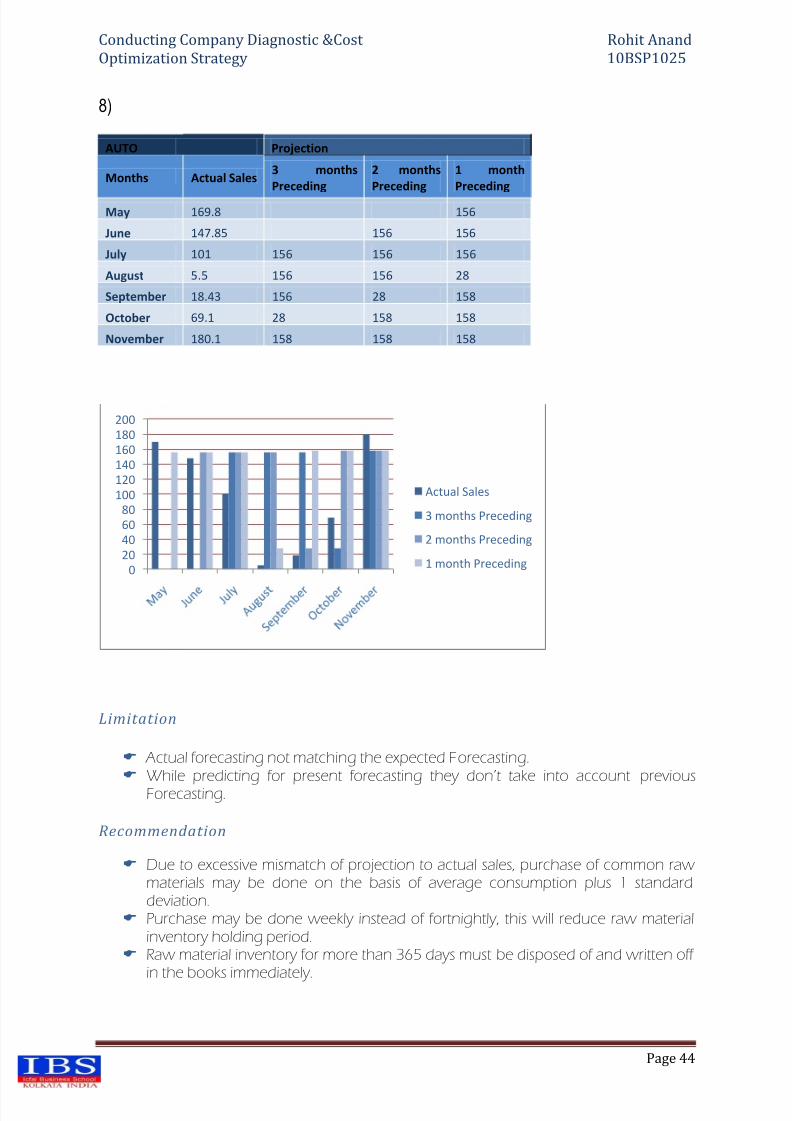

Audio Projection

Months Actual Sales3 months

Preceding

2 months

Preceding

1 month

Preceding

May 371.5 385

June 222.5 480 385

July 603.25 485 480 385

August 554.94 485 480 385

September 273.05 485 480 395

October 379.35 485 490 385

November 149.55 495 480 385

0

50

100

150

200

250300

350

400

450

500

Actual Sales

3 months Preceding

2 months Preceding

1 month Preceding

8/4/2019 Cost Optimization & Diagonstic

http://slidepdf.com/reader/full/cost-optimization-diagonstic 40/70

Conducting Company Diagnostic &Cost Rohit Anand

Optimization Strategy 10BSP1025

Page 40

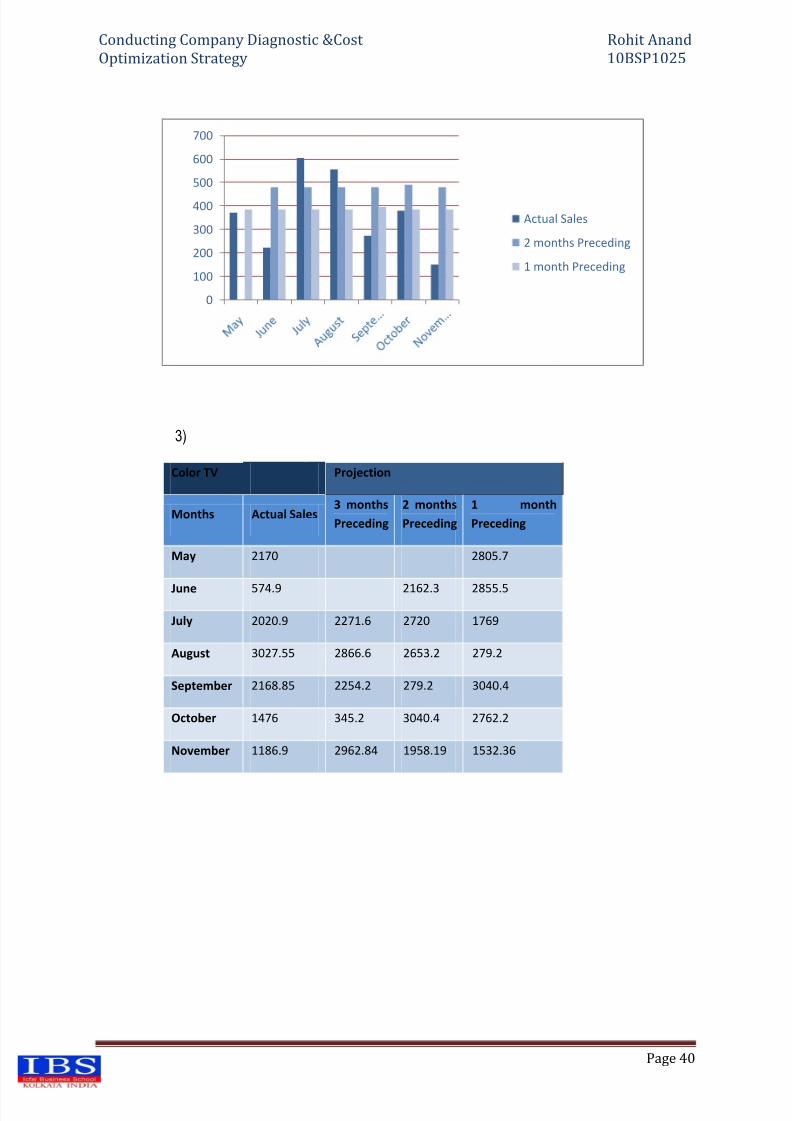

3)

Color TV Projection

Months Actual Sales3 months

Preceding

2 months

Preceding

1 month

Preceding

May 2170 2805.7

June 574.9 2162.3 2855.5

July 2020.9 2271.6 2720 1769

August 3027.55 2866.6 2653.2 279.2

September 2168.85 2254.2 279.2 3040.4

October 1476 345.2 3040.4 2762.2

November 1186.9 2962.84 1958.19 1532.36

0

100

200

300

400

500

600

700

Actual Sales

2 months Preceding

1 month Preceding

8/4/2019 Cost Optimization & Diagonstic

http://slidepdf.com/reader/full/cost-optimization-diagonstic 41/70

Conducting Company Diagnostic &Cost Rohit Anand

Optimization Strategy 10BSP1025

Page 41

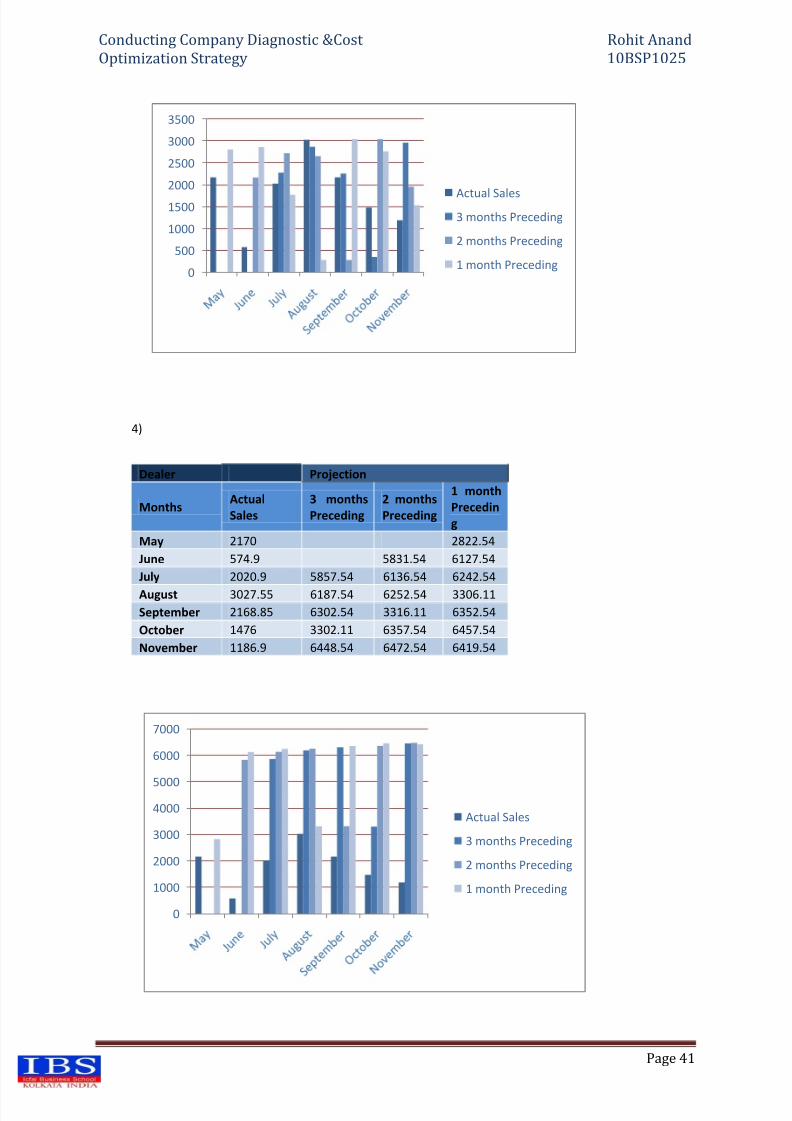

4)

Dealer Projection

MonthsActual

Sales

3 months

Preceding

2 months

Preceding

1 month

Precedin

g

May 2170 2822.54

June 574.9 5831.54 6127.54

July 2020.9 5857.54 6136.54 6242.54

August 3027.55 6187.54 6252.54 3306.11

September 2168.85 6302.54 3316.11 6352.54

October 1476 3302.11 6357.54 6457.54

November 1186.9 6448.54 6472.54 6419.54

0

500

1000

1500

2000

2500

3000

3500

Actual Sales

3 months Preceding

2 months Preceding

1 month Preceding

0

1000

2000

3000

4000

5000

6000

7000

Actual Sales

3 months Preceding

2 months Preceding

1 month Preceding

8/4/2019 Cost Optimization & Diagonstic

http://slidepdf.com/reader/full/cost-optimization-diagonstic 42/70

Conducting Company Diagnostic &Cost Rohit Anand

Optimization Strategy 10BSP1025

Page 42

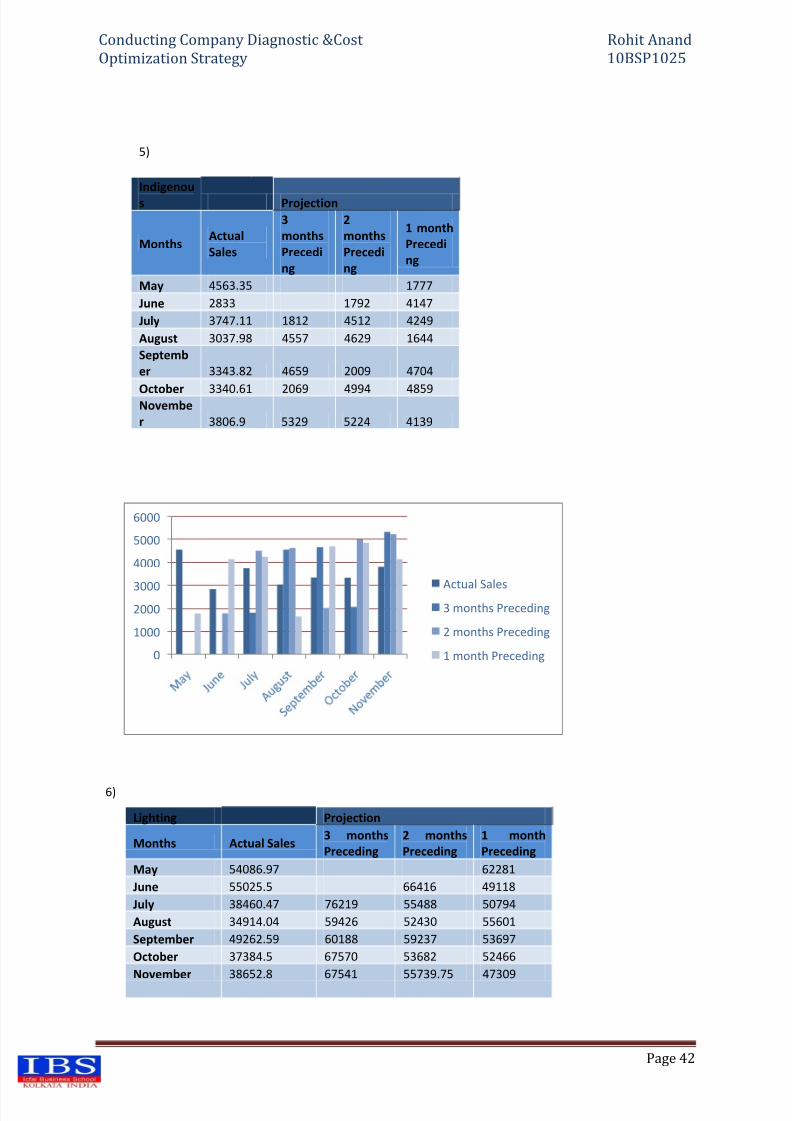

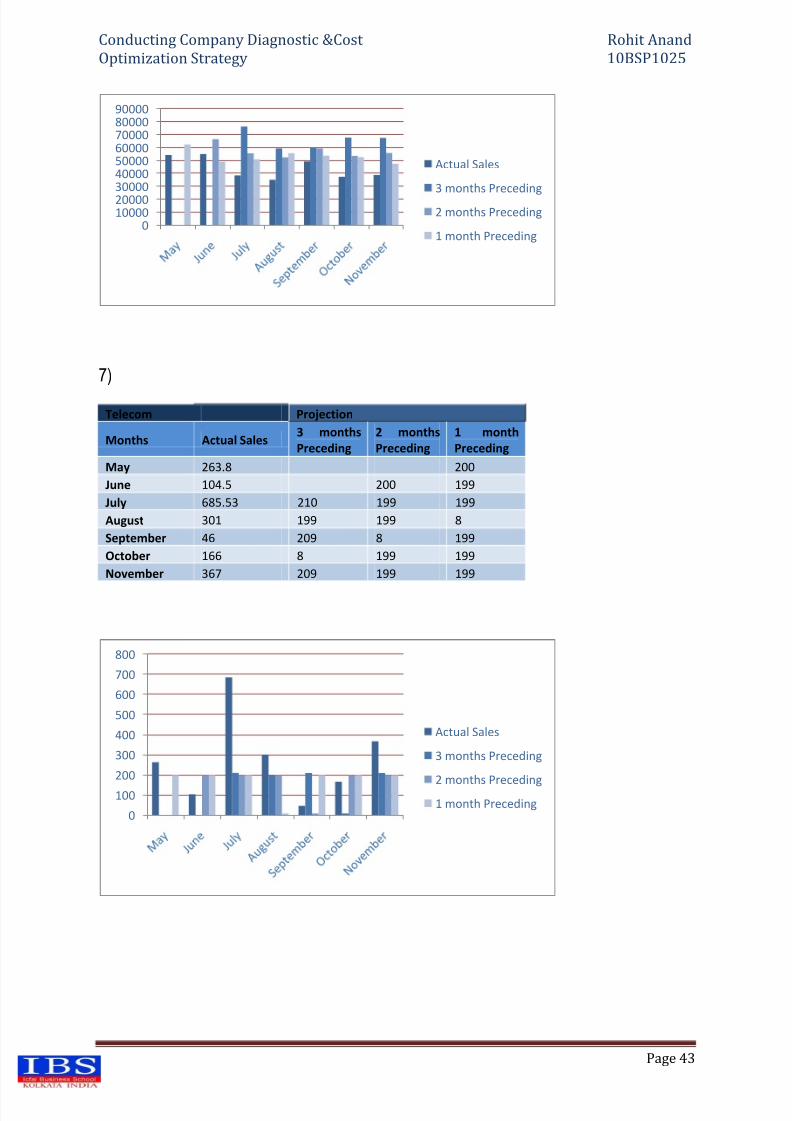

5)

Indigenou

s Projection

MonthsActual

Sales

3

months

Precedi

ng

2

months

Precedi

ng

1 month

Precedi

ng

May 4563.35 1777

June 2833 1792 4147

July 3747.11 1812 4512 4249