Embed Size (px)

DESCRIPTION

not sure of the info

Citation preview

Corporate Presentation December 2014

Forward-Looking Information In the interest of providing investors with information regarding Inter Pipeline, including management’s current expectations, estimates and projections about the future, certain statements and

graphs throughout this presentation contain forward-looking statements or information (collectively referred to as "forward-looking statements") within the meaning of applicable securities

legislation. When used in this presentation, the words "may", "would", "should", "could", "will", "intend", "plan", "anticipate", "believe", "estimate", "expect", "continue", "project", "forecast", "target"

and similar expressions, as they relate to Inter Pipeline or its management are intended to identify forward-looking statements. Forward-looking statements contained in this presentation relate to,

among other things, statements regarding business strategy, plans and other expectations, beliefs, goals, objectives, information and statements about possible future events. Specific forward-

looking statements that may be contained in this presentation include statements regarding the ability of Inter Pipeline to maintain its current level of dividends; changes in legislation relating to

Inter Pipeline and its structure, including income tax considerations and the treatment of security holders under tax laws; and the composition of the management and Board of Directors of Inter

Pipeline; in addition, this presentation may contain forward-looking statements attributed to third-party industry sources. Readers are cautioned not to place undue reliance on such forward-looking

statements. Such statements reflect the current views of Inter Pipeline with respect to future events and are subject to certain risks, uncertainties and assumptions that could cause the results of

Inter Pipeline to differ materially from those expressed in the forward-looking statements. Factors that could cause actual results to vary from forward-looking information or may affect the

operations, performance, development and results of Inter Pipeline's businesses include, among other things: risks and assumptions associated with operations, such as Inter Pipeline's ability to

successfully implement its strategic initiatives and achieve expected benefits, including the further development of its oil sands pipeline systems; assumptions concerning operational reliability; the

availability and price of labour and construction materials; the status, credit risk and continued existence of customers having contracts with Inter Pipeline and their respective affiliates; availability

of energy commodities; volatility of and assumptions regarding prices of energy commodities; competitive factors, pricing pressures and supply and demand in the natural gas and oil

transportation, ethane transportation and natural gas liquids (NGL) extraction and storage industries; assumptions based upon Inter Pipeline's current financial and operational guidance;

fluctuations in currency and interest rates; inflation; the ability to access sufficient capital from internal and external sources; risks and uncertainties associated with the ability to maintain Inter

Pipeline's current level of cash dividends; risks inherent in Inter Pipeline's Canadian and foreign operations; risks of war, hostilities, civil insurrection, instability and political and economic

conditions in or affecting countries in which Inter Pipeline and its affiliates operate; severe weather conditions; terrorist threats; risks associated with technology; Inter Pipeline's ability to generate

sufficient cash flow from operations to meet its current and future obligations; Inter Pipeline's ability to access external sources of debt and equity capital; general economic and business

conditions; the potential delays of and costs of overruns on construction projects, including, but not limited to Inter Pipeline's current oil sands projects and future expansions of Inter Pipeline's oil

sands pipeline systems; risks associated with the failure to finalize formal agreements with counterparties in circumstances where letters of intent or similar agreements have been executed and

announced by Inter Pipeline; Inter Pipeline's ability to make capital investments and the amounts of capital investments; changes in laws and regulations, including environmental, regulatory and

taxation laws, and the interpretation of such changes to laws and regulations; the risks associated with existing and potential future lawsuits and regulatory actions against Inter Pipeline and its

affiliates; increases in maintenance, operating or financing costs; availability of adequate levels of insurance; difficulty in obtaining necessary regulatory approvals and maintenance of support of

such approvals; the inability to meet or continue to meet listing requirements of the TSX; and such other risks and uncertainties described from time to time in Inter Pipeline's reports and filings with

the Canadian securities regulatory authorities. The impact of any one assumption, risk, uncertainty or other factor on a particular forward-looking statement is not determinable with certainty, as

these are interdependent and Inter Pipeline's future course of action depends on management's assessment of all information available at the relevant time. See "Risk Factors" in the

management's discussion and analysis of Inter Pipeline's operating results for the years ended December 31, 2013 and 2012 and other reports and filings available at www.sedar.com. Although

the forward-looking statements contained in this presentation are based upon what management believes to be reasonable assumptions, there can be no assurance that actual results will be

consistent with these forward-looking statements. The forward-looking statements contained, or incorporated by reference, herein are expressly qualified in their entirety by this cautionary

statement. The forward-looking statements included, or incorporated by reference, in this presentation are made as of the date hereof and Inter Pipeline undertakes no obligation to publicly update

such forward-looking statements to reflect new information, subsequent events or otherwise, except as required by applicable securities laws. You are further cautioned that the preparation of

financial statements in accordance with GAAP requires management to make certain judgments and estimates that affect the reported amounts of assets, liabilities, revenues and expenses. These

estimates may change, having either a negative or positive effect on net earnings as further information becomes available and as the economic environment changes. GAAP and Non-GAAP

Measures – In addition to providing measures prepared in accordance with GAAP this presentation may contain references to non-GAAP measures as identified herein. These measures do not

have any standardized meaning prescribed by GAAP and therefore may not be comparable to similar measures presented by other entities. Investors are cautioned that non-GAAP and additional

GAAP financial measures should not be construed as alternatives to other measures of financial performance calculated in accordance with GAAP. References to the term “EBITDA” used in this

presentation may include EBITDA or adjusted EBITDA. The most closely related GAAP and non-GAAP measures are defined in Inter Pipelines’ most recent Management Discussion and

Analysis available at www.interpipeline.com. Industry Data - Certain market, independent third party and industry data contained in this presentation is based upon information from government or

other independent industry publications and reports or based on estimates derived from such publications and reports. Government and industry publications and reports generally indicate that

they have obtained their information from sources believed to be reliable, but do not guarantee the accuracy or completeness of their information. This presentation also includes certain data,

including information on export and refining capacity, supply and demand for certain commodity types and total remaining established oil ands reserves, and other operational results, derived from

public filings made by independent third parties. While Inter Pipeline believes this data to be reliable, market and industry data is subject to variations and cannot be verified with complete certainty

due to limits on the availability and reliability of raw data, the voluntary nature of the data gathering process and other limitations and uncertainties inherent in any statistical survey. Inter Pipeline

has not independently verified any of the data from independent third party sources referred to in this presentation or ascertained the underlying assumptions relied upon by such sources.

Market Information

1

Market Capitalization

Enterprise Value

Annualized Dividend

Yield

$10.7 billion

$15.1 billion

$1.47/share

4.5%

Information as at close of markets on December 3, 2014

2

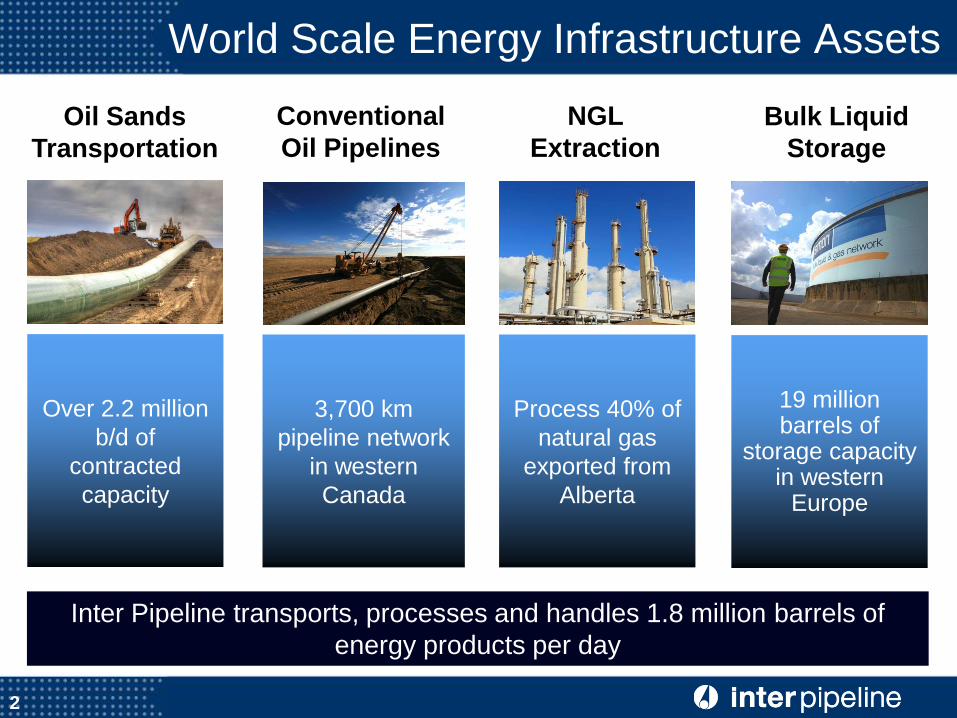

World Scale Energy Infrastructure Assets

Oil Sands

Transportation

NGL

Extraction

Conventional

Oil Pipelines

Bulk Liquid

Storage

Over 2.2 million

b/d of

contracted

capacity

3,700 km

pipeline network

in western

Canada

Process 40% of

natural gas

exported from

Alberta

19 million barrels of

storage capacity in western

Europe

Inter Pipeline transports, processes and handles 1.8 million barrels of

energy products per day

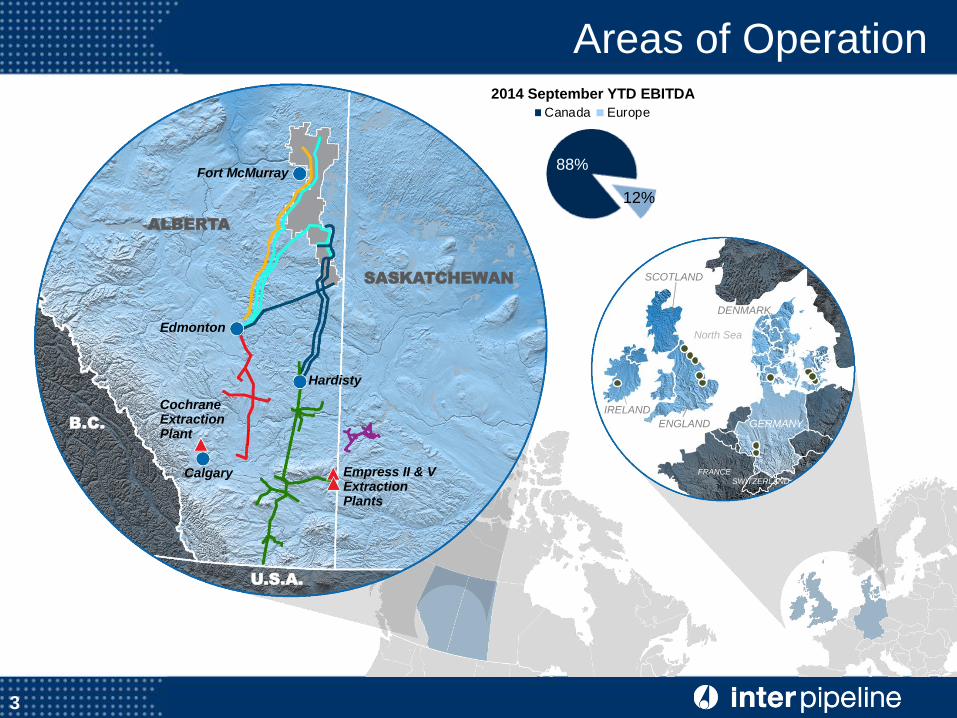

Areas of Operation

Fort McMurray

Edmonton

ALBERTA

SASKATCHEWAN

Hardisty

Calgary

Cochrane Extraction Plant

B.C.

U.S.A.

Empress II & V Extraction Plants

GERMANY

DENMARK

SCOTLAND

ENGLAND

IRELAND

FRANCE

SWITZERLAND

North Sea

2014 September YTD EBITDA

3

88%

12%

Canada Europe

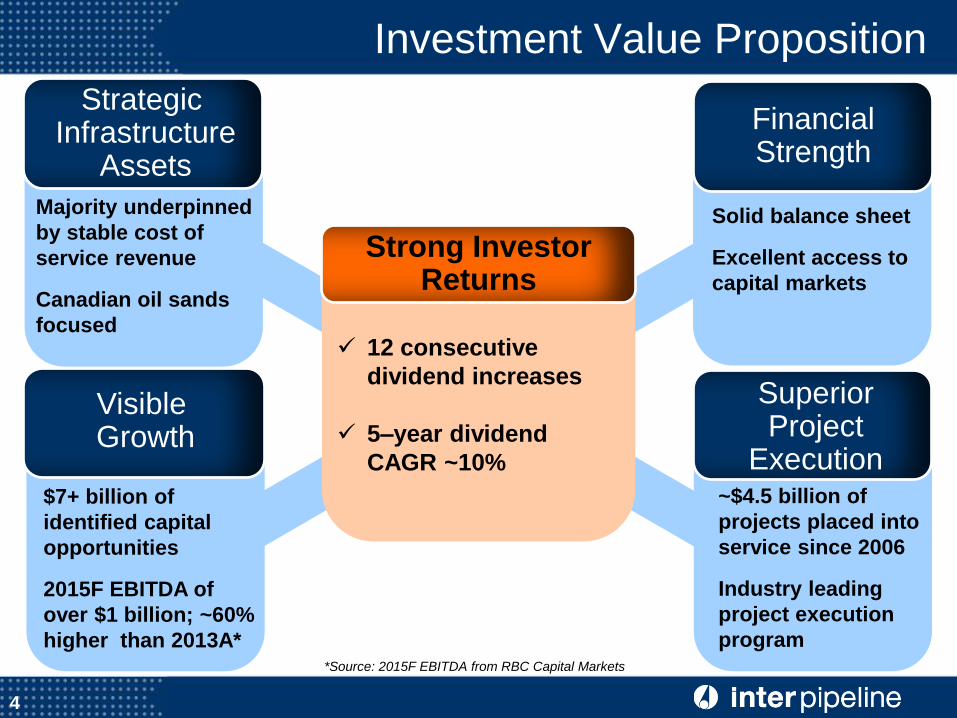

Strategic Infrastructure

Assets

Financial Strength

Investment Value Proposition

Majority underpinned

by stable cost of

service revenue

Canadian oil sands

focused

Solid balance sheet

Excellent access to

capital markets

*Source: 2015F EBITDA from RBC Capital Markets

Financial Strength

$7+ billion of

identified capital

opportunities

2015F EBITDA of

over $1 billion; ~60%

higher than 2013A*

Visible Growth

Superior Project

Execution ~$4.5 billion of

projects placed into

service since 2006

Industry leading

project execution

program

4

Strong Investor Returns

12 consecutive

dividend increases

5–year dividend

CAGR ~10%

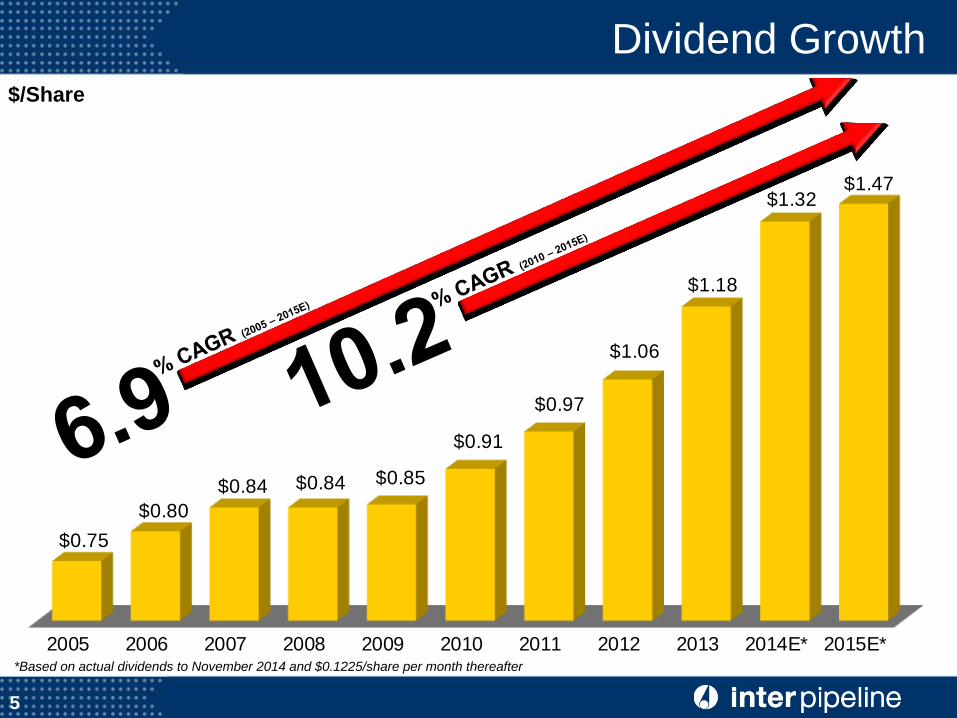

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014E* 2015E*

$0.75

$0.80

$0.84 $0.84 $0.85

$0.91

$0.97

$1.06

$1.18

$1.32$1.47

Dividend Growth $/Share

*Based on actual dividends to November 2014 and $0.1225/share per month thereafter

5

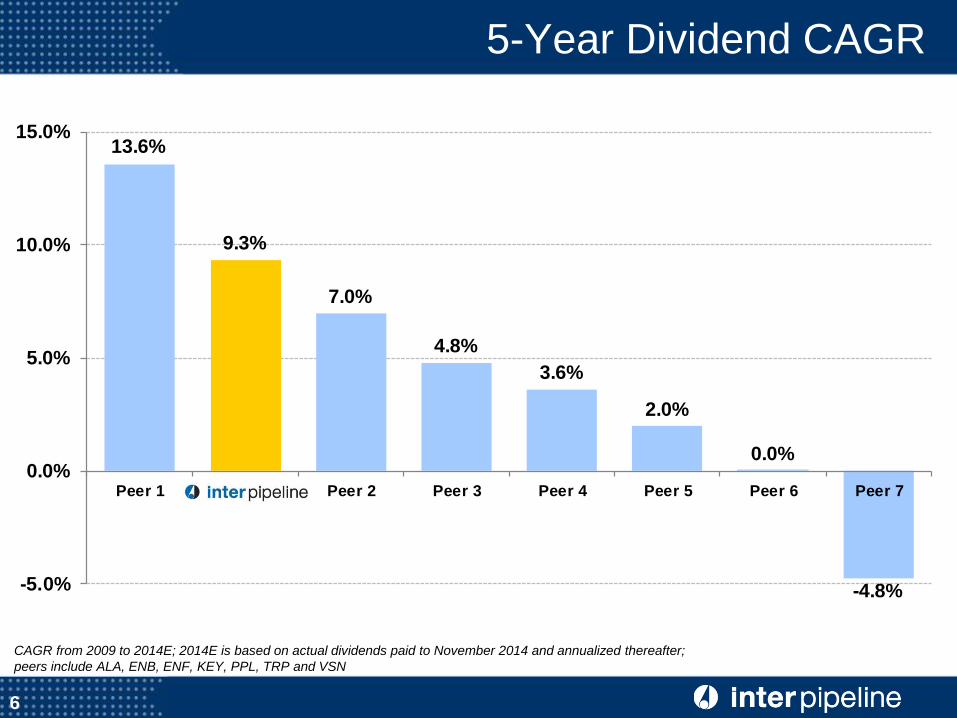

13.6%

9.3%

7.0%

4.8%

3.6%

2.0%

0.0%

-4.8%-5.0%

0.0%

5.0%

10.0%

15.0%

Peer 1 Inter Pipeline Peer 2 Peer 3 Peer 4 Peer 5 Peer 6 Peer 7

5-Year Dividend CAGR

CAGR from 2009 to 2014E; 2014E is based on actual dividends paid to November 2014 and annualized thereafter;

peers include ALA, ENB, ENF, KEY, PPL, TRP and VSN

6

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

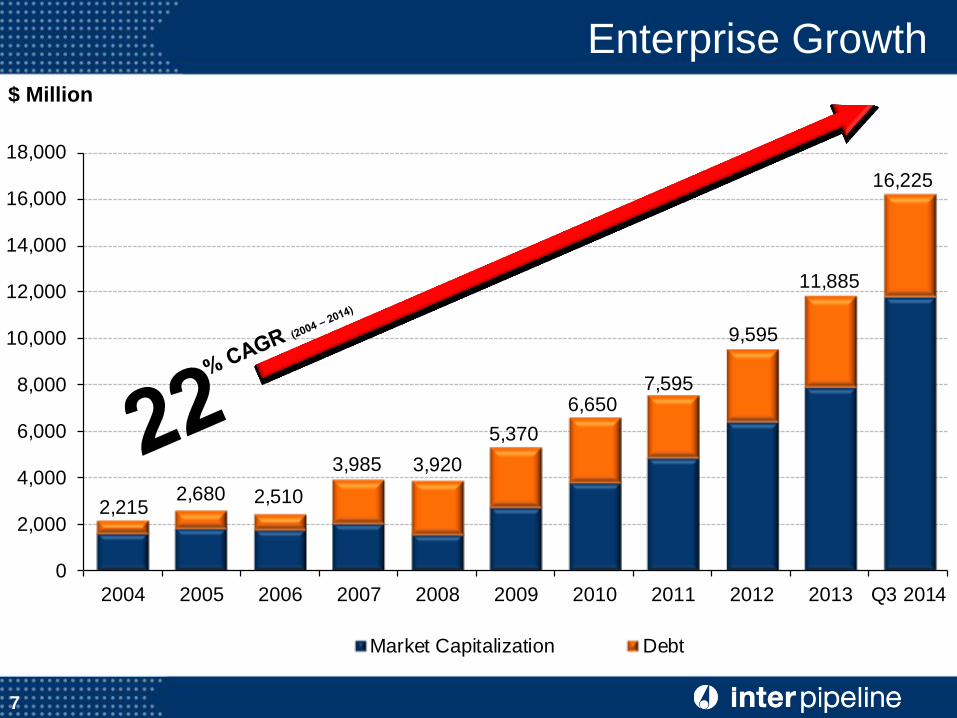

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 Q3 2014

Market Capitalization Debt

2,2152,680 2,510

3,985 3,920

5,370

7,595

9,595

11,885

6,650

16,225

Enterprise Growth $ Million

7

Recent Developments

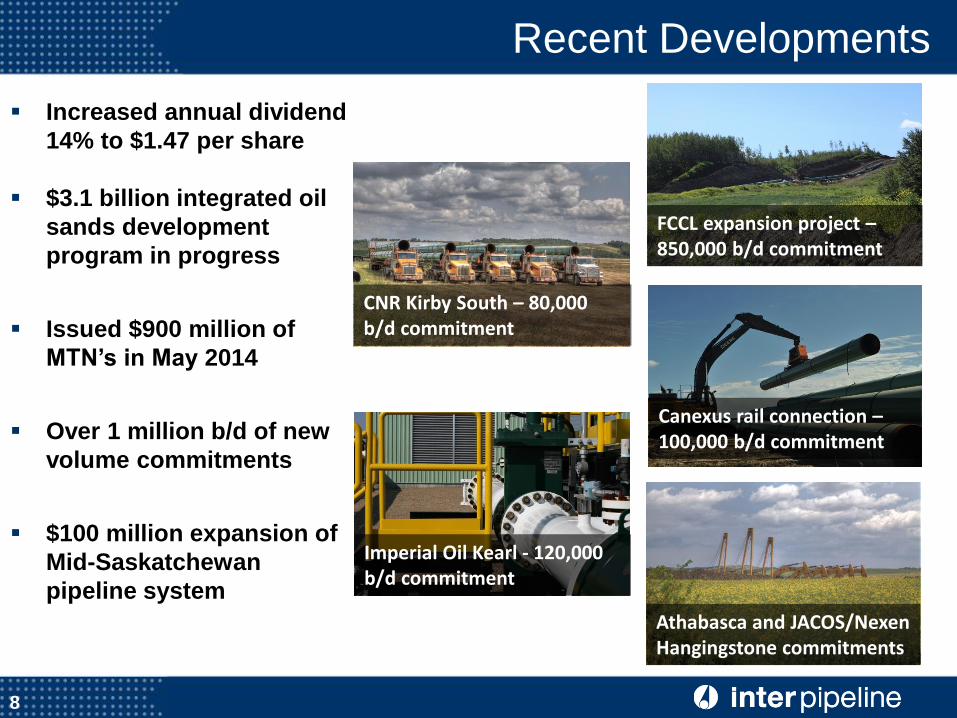

Increased annual dividend

14% to $1.47 per share

$3.1 billion integrated oil

sands development

program in progress

Issued $900 million of

MTN’s in May 2014

Over 1 million b/d of new

volume commitments

$100 million expansion of

Mid-Saskatchewan

pipeline system

FCCL expansion project – 850,000 b/d commitment

CNR Kirby South – 80,000 b/d commitment

Canexus rail connection – 100,000 b/d commitment

Imperial Oil Kearl - 120,000 b/d commitment

8

Athabasca and JACOS/Nexen Hangingstone commitments

2014 September YTD EBITDA

9

44%

FCCL Christina Lake

Husky Sunrise

Imperial Kearl

Suncor

AOC Hangingstone

CNR Kirby South

Hardisty

Edmonton

Jacos/Nexen Hangingstone

Polaris Extension

Blend Line Expansion

FCCL Foster Creek

Fort McMurray

FCCL Narrows Lake

Canexus Facility

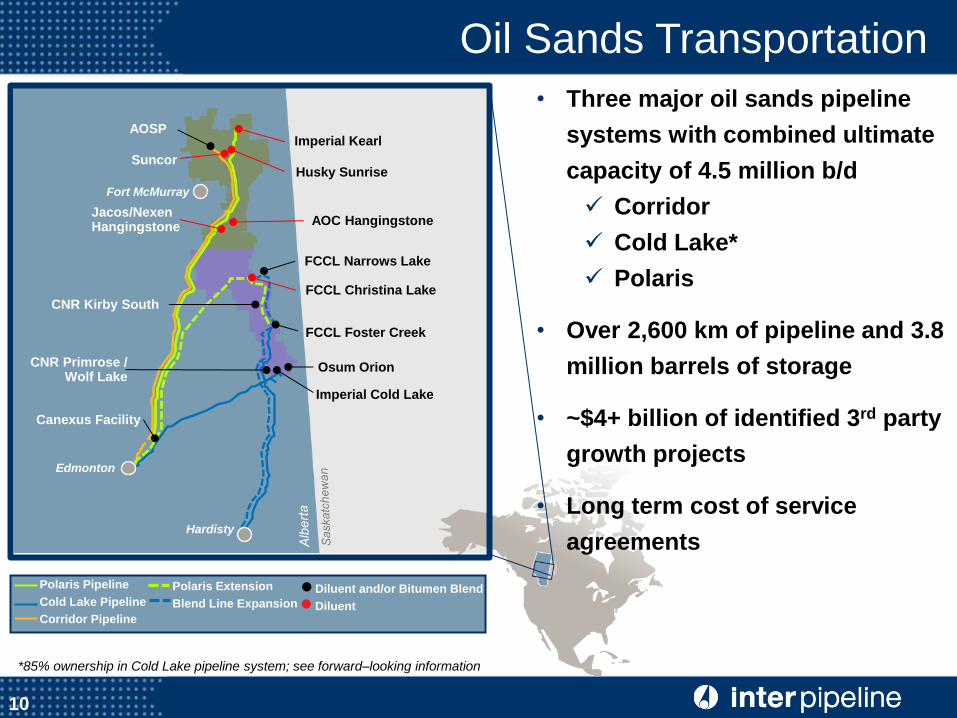

Oil Sands Transportation

• Three major oil sands pipeline

systems with combined ultimate

capacity of 4.5 million b/d

Corridor

Cold Lake*

Polaris

• Over 2,600 km of pipeline and 3.8

million barrels of storage

• ~$4+ billion of identified 3rd party

growth projects

• Long term cost of service

agreements

Polaris Extension

Blend Line Expansion

Polaris Pipeline

Cold Lake Pipeline

Corridor Pipeline

Diluent and/or Bitumen Blend

Diluent

10

AOSP

CNR Primrose / Wolf Lake

Imperial Cold Lake

Osum Orion

*85% ownership in Cold Lake pipeline system; see forward–looking information

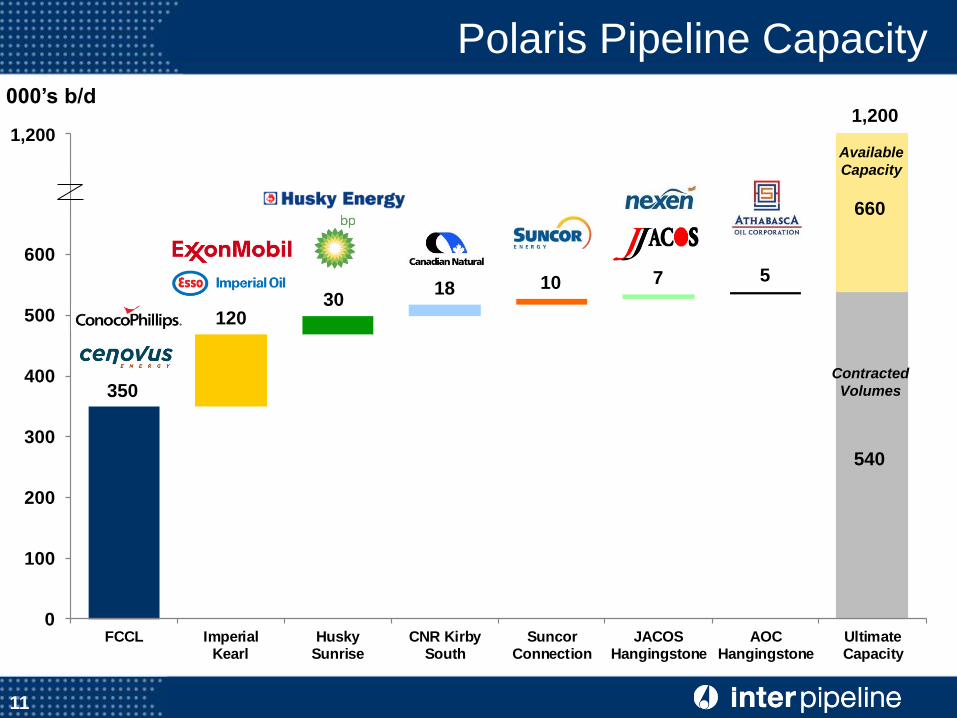

0

100

200

300

400

500

600

700

800

FCCL ImperialKearl

HuskySunrise

CNR KirbySouth

SuncorConnection

JACOSHangingstone

AOCHangingstone

UltimateCapacity

000’s b/d

1,200

350

120 30

18 10 7 5

1,200

540

660

Contracted

Volumes

Available

Capacity

11

Polaris Pipeline Capacity

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

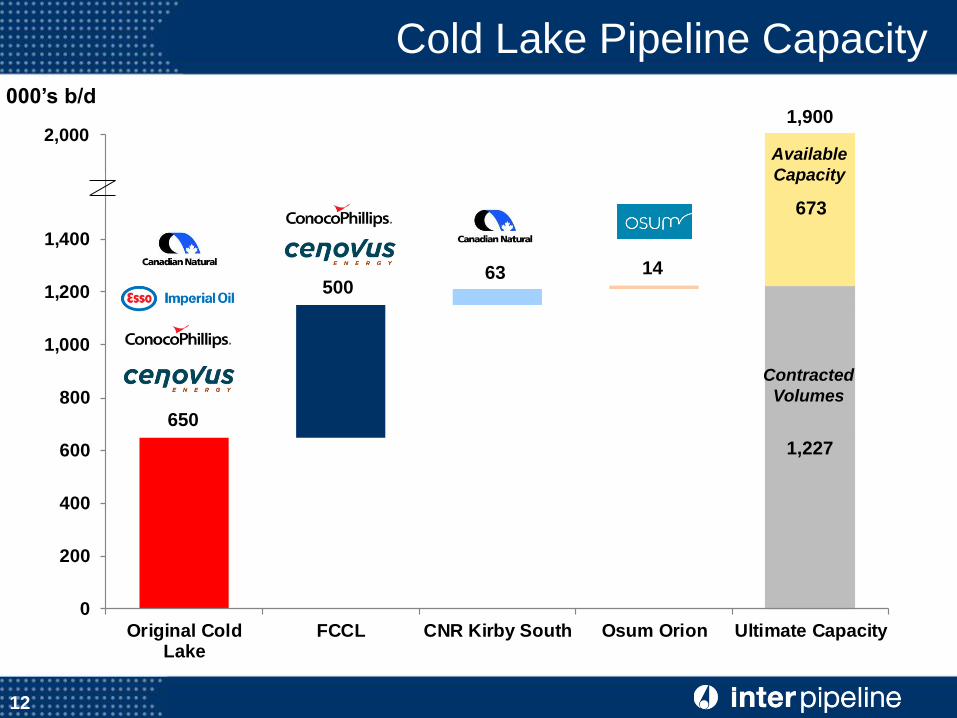

Original ColdLake

FCCL CNR Kirby South Osum Orion Ultimate Capacity

000’s b/d

2,000

650

500 63 14

1,900

Contracted

Volumes

Available

Capacity

1,227

673

12

Cold Lake Pipeline Capacity

0

200

400

600

800

1,000

1,200

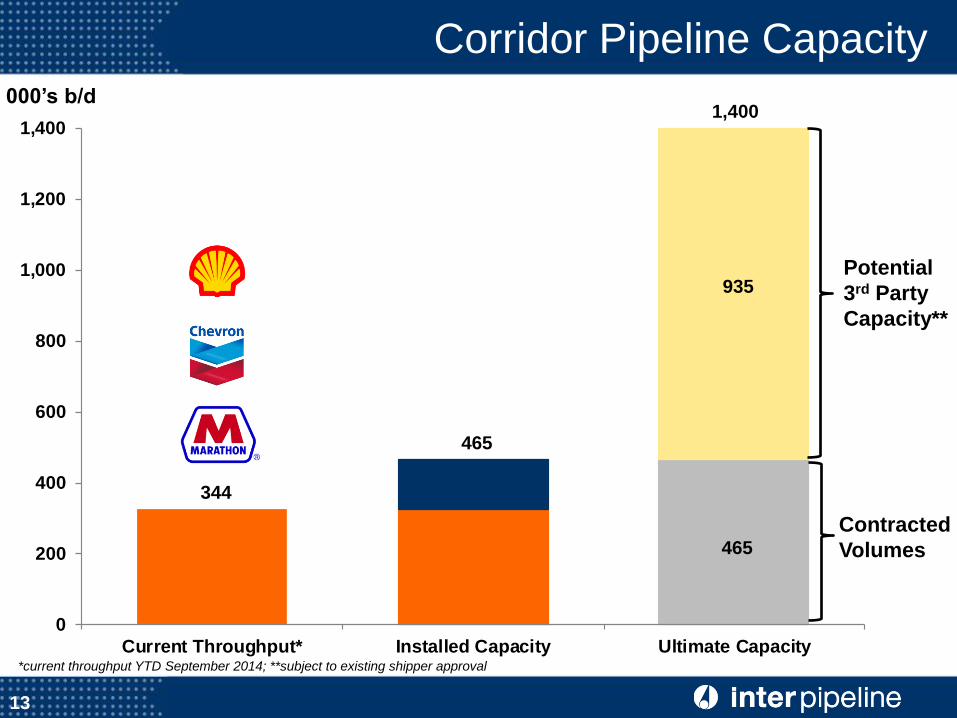

1,400

Current Throughput* Installed Capacity Ultimate Capacity

000’s b/d

344

465

1,400

*current throughput YTD September 2014; **subject to existing shipper approval

935

465

Potential

3rd Party

Capacity**

Contracted

Volumes

13

Corridor Pipeline Capacity

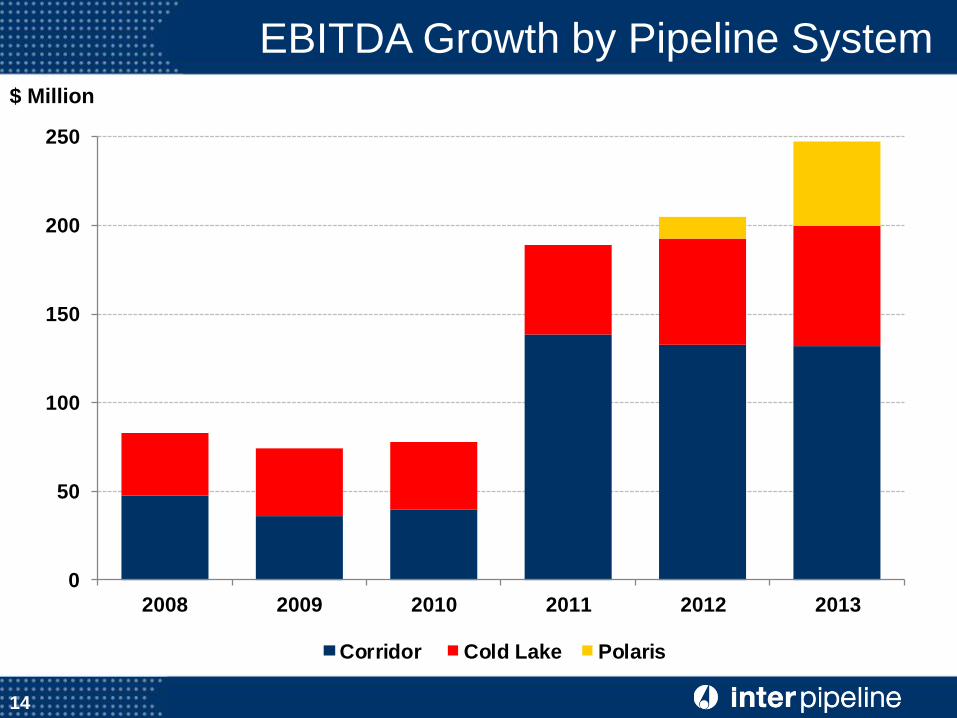

EBITDA Growth by Pipeline System

$ Million

0

50

100

150

200

250

2008 2009 2010 2011 2012 2013

Corridor Cold Lake Polaris

14

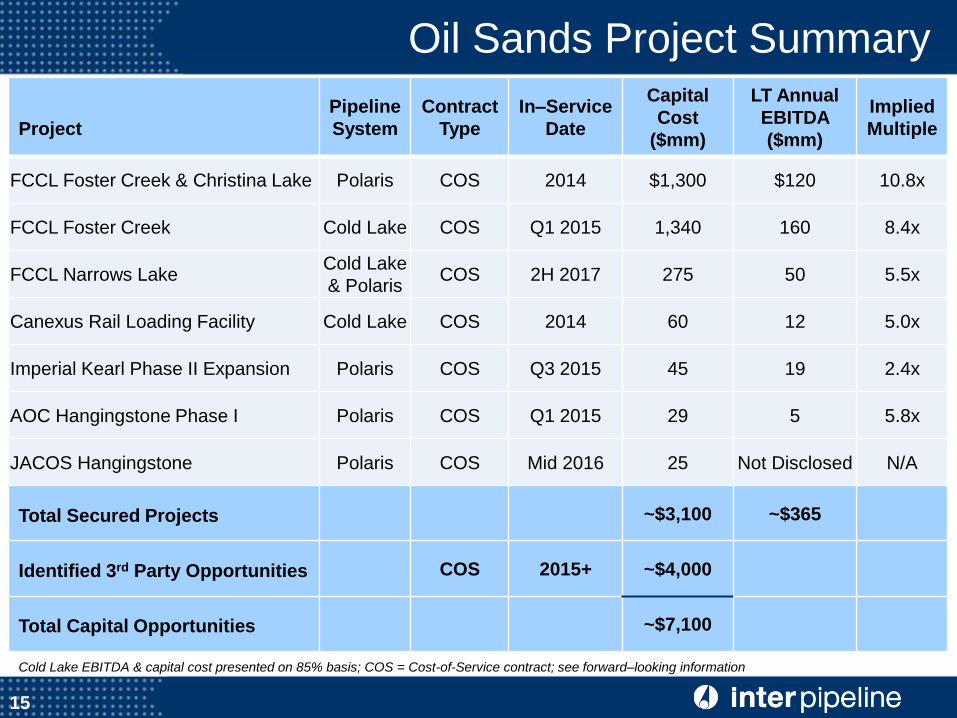

Oil Sands Project Summary

Project

Pipeline

System

Contract

Type

In–Service

Date

Capital

Cost

($mm)

LT Annual

EBITDA

($mm)

Implied

Multiple

FCCL Foster Creek & Christina Lake Polaris COS 2014 $1,300 $120 10.8x

FCCL Foster Creek Cold Lake COS Q1 2015 1,340 160 8.4x

FCCL Narrows Lake Cold Lake

& Polaris COS 2H 2017 275 50 5.5x

Canexus Rail Loading Facility Cold Lake COS 2014 60 12 5.0x

Imperial Kearl Phase II Expansion Polaris COS Q3 2015 45 19 2.4x

AOC Hangingstone Phase I Polaris COS Q1 2015 29 5 5.8x

JACOS Hangingstone Polaris COS Mid 2016 25 Not Disclosed N/A

Total Secured Projects ~$3,100 ~$365

Identified 3rd Party Opportunities COS 2015+ ~$4,000

Total Capital Opportunities ~$7,100

Cold Lake EBITDA & capital cost presented on 85% basis; COS = Cost-of-Service contract; see forward–looking information

15

$0

$50

$100

$150

$200

$250

$300

$350

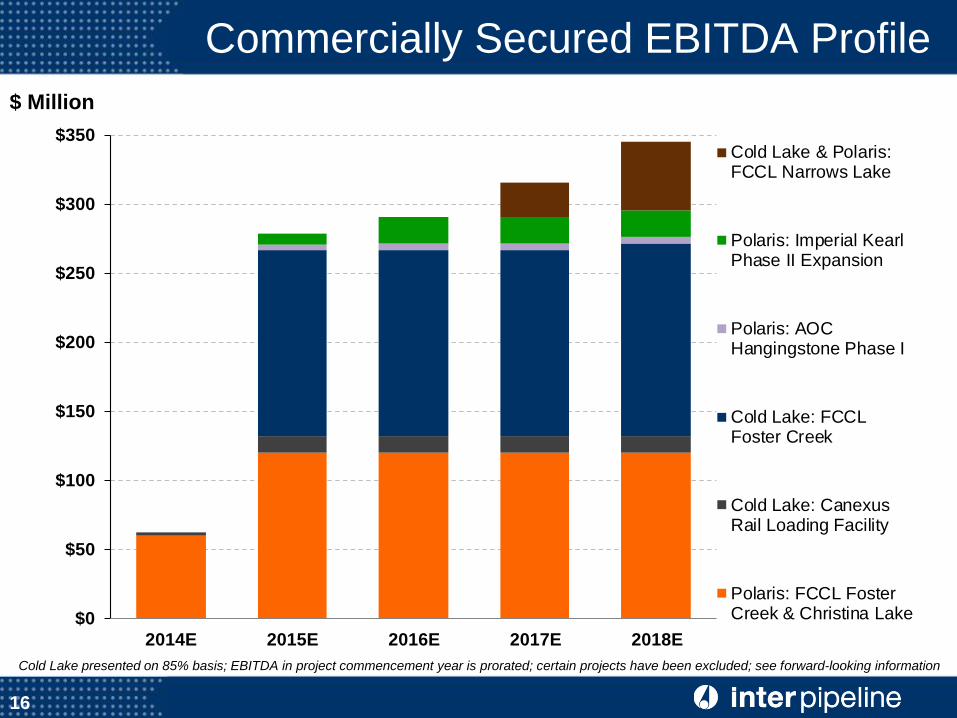

2014E 2015E 2016E 2017E 2018E

Cold Lake & Polaris:FCCL Narrows Lake

Polaris: Imperial KearlPhase II Expansion

Polaris: AOCHangingstone Phase I

Cold Lake: FCCLFoster Creek

Cold Lake: CanexusRail Loading Facility

Polaris: FCCL FosterCreek & Christina Lake

Commercially Secured EBITDA Profile

Cold Lake presented on 85% basis; EBITDA in project commencement year is prorated; certain projects have been excluded; see forward-looking information

$ Million

16

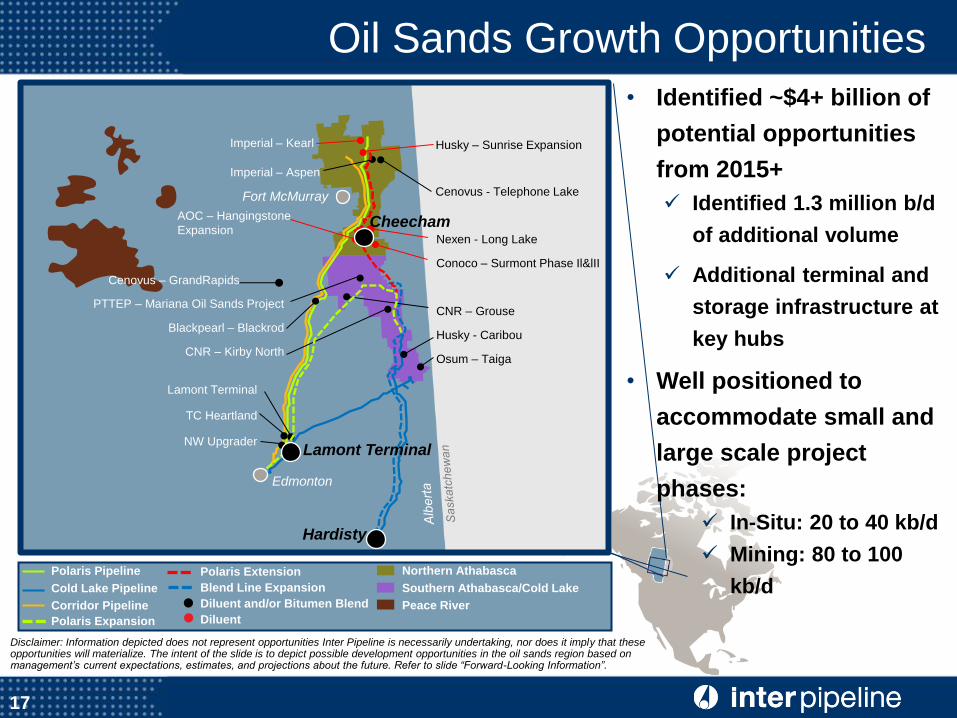

Oil Sands Growth Opportunities

Disclaimer: Information depicted does not represent opportunities Inter Pipeline is necessarily undertaking, nor does it imply that these opportunities will materialize. The intent of the slide is to depict possible development opportunities in the oil sands region based on management’s current expectations, estimates, and projections about the future. Refer to slide “Forward-Looking Information”.

Edmonton

Hardisty

Fort McMurray

• Identified ~$4+ billion of

potential opportunities

from 2015+

Identified 1.3 million b/d

of additional volume

Additional terminal and

storage infrastructure at

key hubs

• Well positioned to

accommodate small and

large scale project

phases:

In-Situ: 20 to 40 kb/d

Mining: 80 to 100

kb/d

Nexen - Long Lake

Conoco – Surmont Phase Il&lII

CNR – Grouse

Husky - Caribou

Osum – Taiga

AOC – Hangingstone

Expansion

PTTEP – Mariana Oil Sands Project

Blackpearl – Blackrod

CNR – Kirby North

Imperial – Kearl

Imperial – Aspen

Husky – Sunrise Expansion

Cenovus – GrandRapids

Lamont Terminal

TC Heartland

NW Upgrader Lamont Terminal

Cheecham

17

Cenovus - Telephone Lake

Polaris Pipeline

Cold Lake Pipeline

Corridor Pipeline

Polaris Expansion

Northern Athabasca

Southern Athabasca/Cold Lake

Peace River

Polaris Extension

Blend Line Expansion

Diluent and/or Bitumen Blend

Diluent

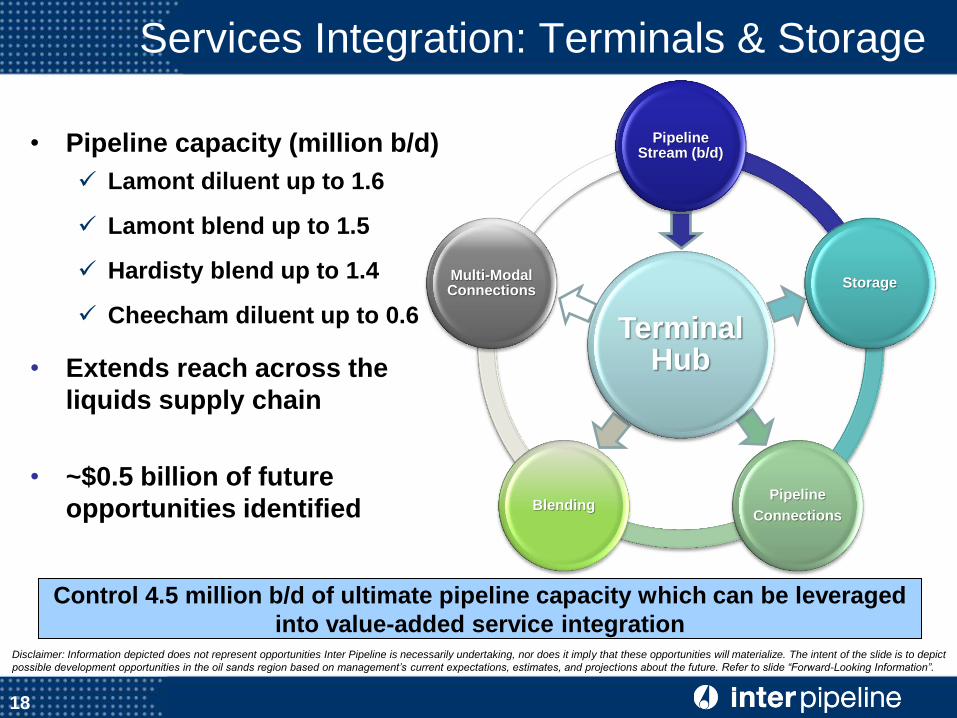

• Pipeline capacity (million b/d)

Lamont diluent up to 1.6

Lamont blend up to 1.5

Hardisty blend up to 1.4

Cheecham diluent up to 0.6

• Extends reach across the

liquids supply chain

• ~$0.5 billion of future

opportunities identified

18

/

Control 4.5 million b/d of ultimate pipeline capacity which can be leveraged

into value-added service integration

Services Integration: Terminals & Storage

Disclaimer: Information depicted does not represent opportunities Inter Pipeline is necessarily undertaking, nor does it imply that these opportunities will materialize. The intent of the slide is to depict

possible development opportunities in the oil sands region based on management’s current expectations, estimates, and project ions about the future. Refer to slide “Forward-Looking Information”.

Terminal Hub

Pipeline Stream (b/d)

Storage

Pipeline

Connections Blending

Multi-Modal Connections

0

300

600

900

1,200

1,500

0

1,000

2,000

3,000

4,000

5,000

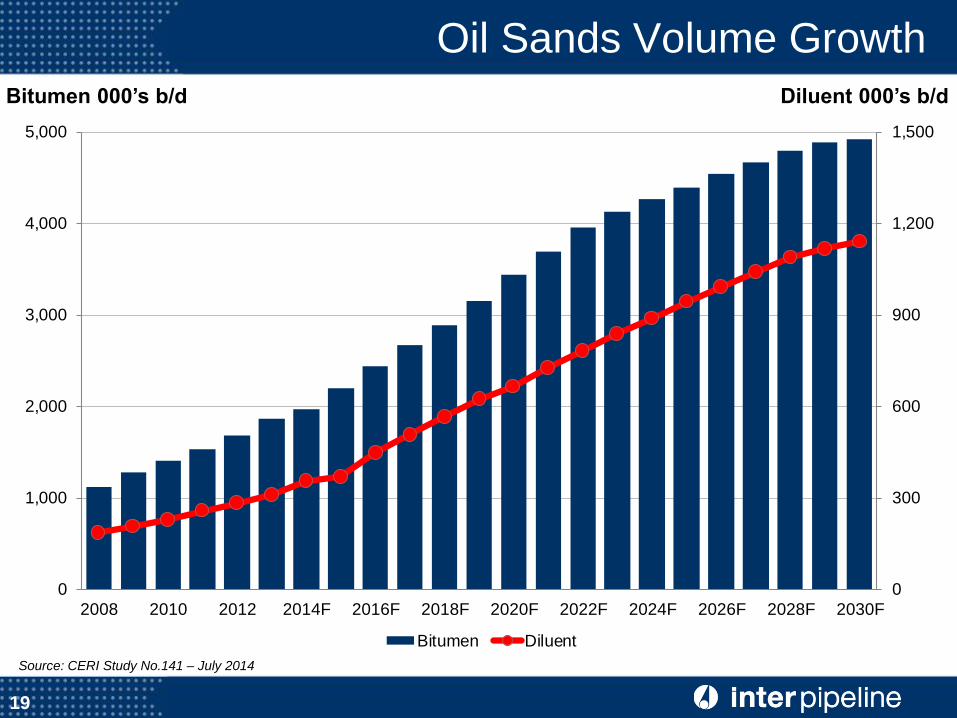

2008 2010 2012 2014F 2016F 2018F 2020F 2022F 2024F 2026F 2028F 2030F

Bitumen Diluent

Oil Sands Volume Growth

Bitumen 000’s b/d

19

Source: CERI Study No.141 – July 2014

Diluent 000’s b/d

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

2010 2015 2020 2025 2030

Pro

du

cti

on

/ C

ap

ac

ity

Refining Express

Enbridge ML East

Alberta Clipper

Keystone

Rail (Current)

Alberta Clipper Expansion

Rail (Expansion)

Keystone XL

TMPL Expansion

Northern Gateway

TCPL Energy East

20

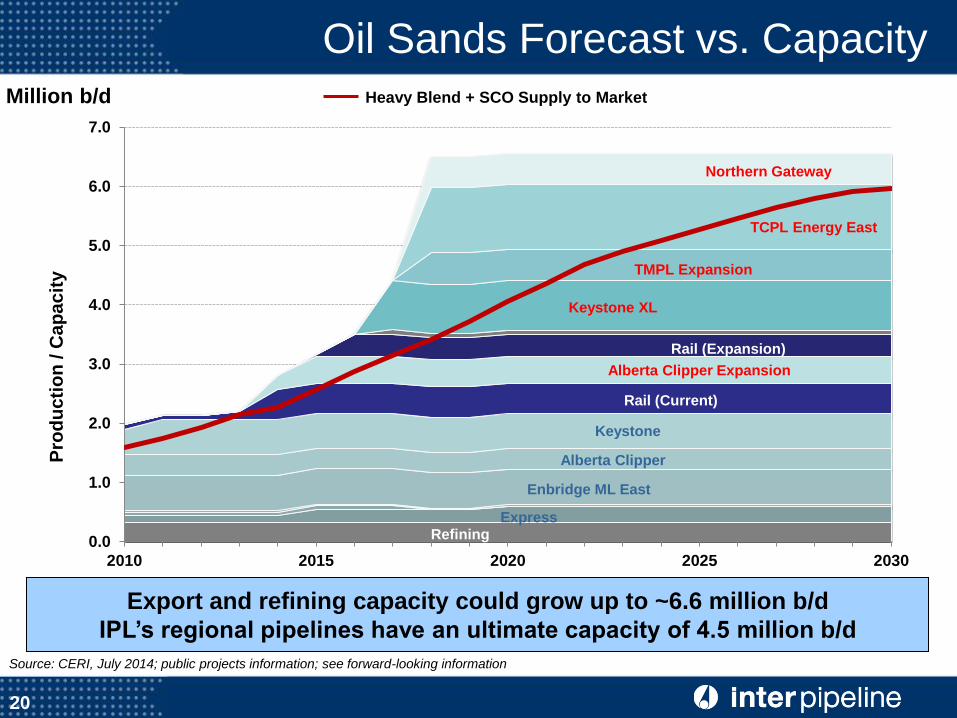

Oil Sands Forecast vs. Capacity Heavy Blend + SCO Supply to Market

Source: CERI, July 2014; public projects information; see forward-looking information

Million b/d

Export and refining capacity could grow up to ~6.6 million b/d

IPL’s regional pipelines have an ultimate capacity of 4.5 million b/d

21

24%

2014 September YTD EBITDA

Calgary

ALBERTA

Edmonton

U.S.A.

Hardisty

Kerrobert

Milk River

SASK.

22

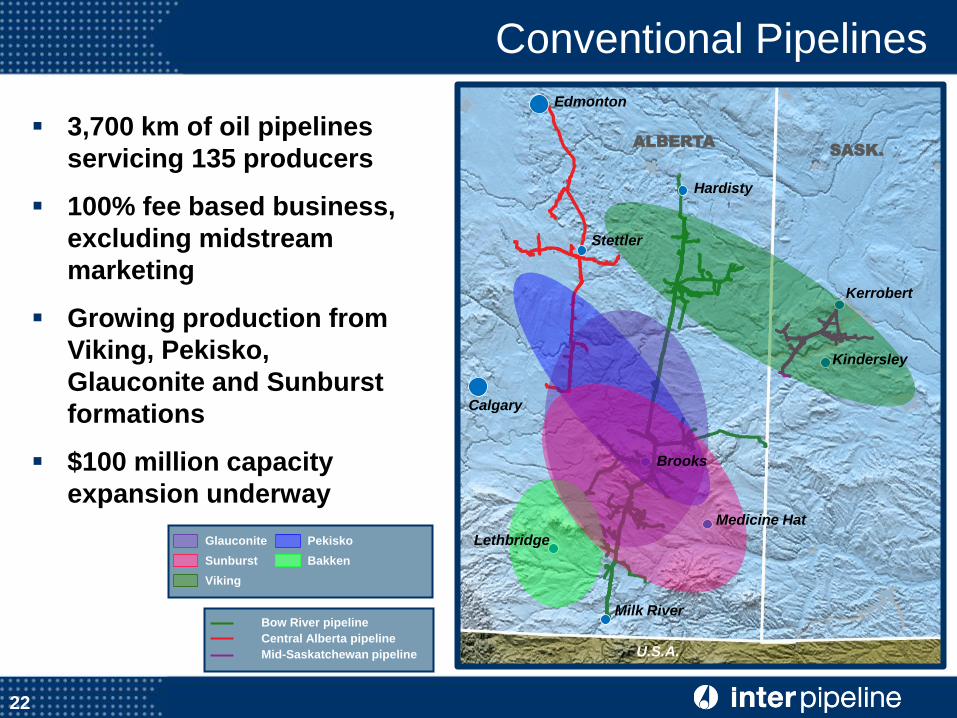

Conventional Pipelines

Bow River pipeline

Central Alberta pipeline

Mid-Saskatchewan pipeline

3,700 km of oil pipelines

servicing 135 producers

100% fee based business,

excluding midstream

marketing

Growing production from

Viking, Pekisko,

Glauconite and Sunburst

formations

$100 million capacity

expansion underway

Glauconite Pekisko

Sunburst Bakken

Viking

Brooks

Lethbridge

Medicine Hat

Kindersley

Stettler

0

20

40

60

80

100

120

140

160

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Oil Gathering Hardisty Midstream Marketing

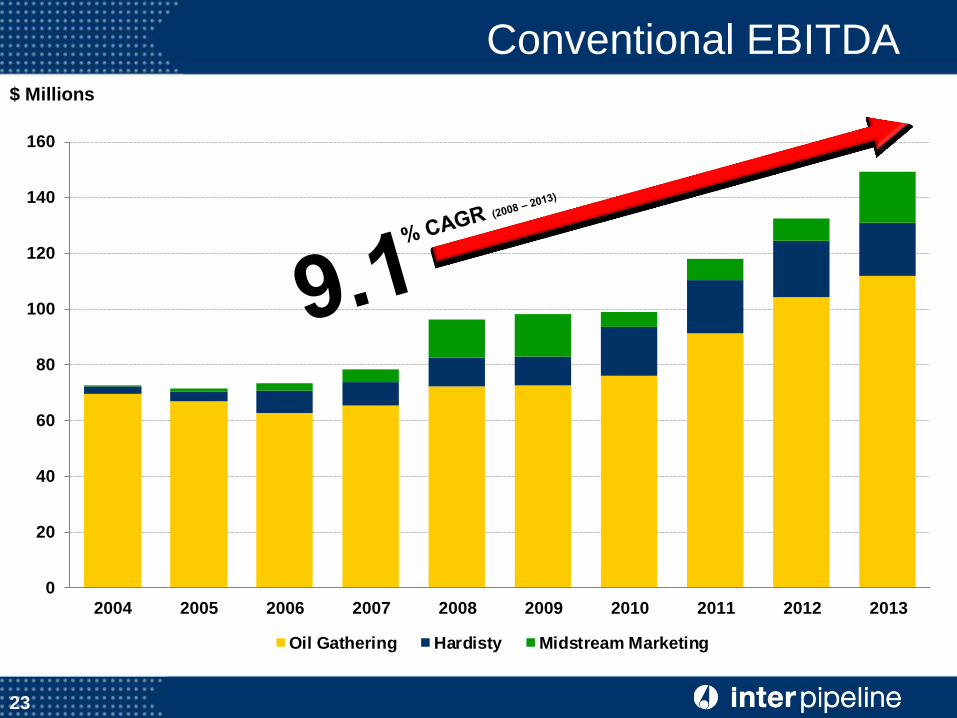

Conventional EBITDA $ Millions

23

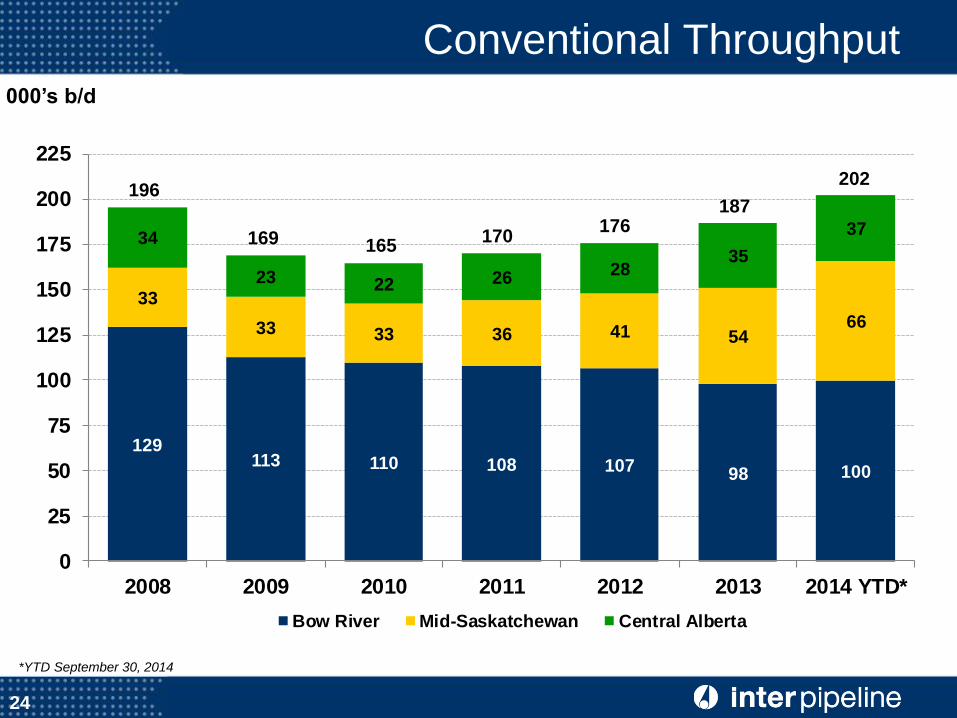

129113 110 108 107 98 100

33

33 33 36 41 5466

34

23 22 2628

35

37

0

25

50

75

100

125

150

175

200

225

2008 2009 2010 2011 2012 2013 2014 YTD*

Bow River Mid-Saskatchewan Central Alberta

Conventional Throughput

24

000’s b/d

*YTD September 30, 2014

202

187 176

170 165 169

196

Calgary

Medicine Hat

Lethbridge

ALBERTA

Edmonton

U.S.A.

Hardisty

Milk River

Stettler

SASK.

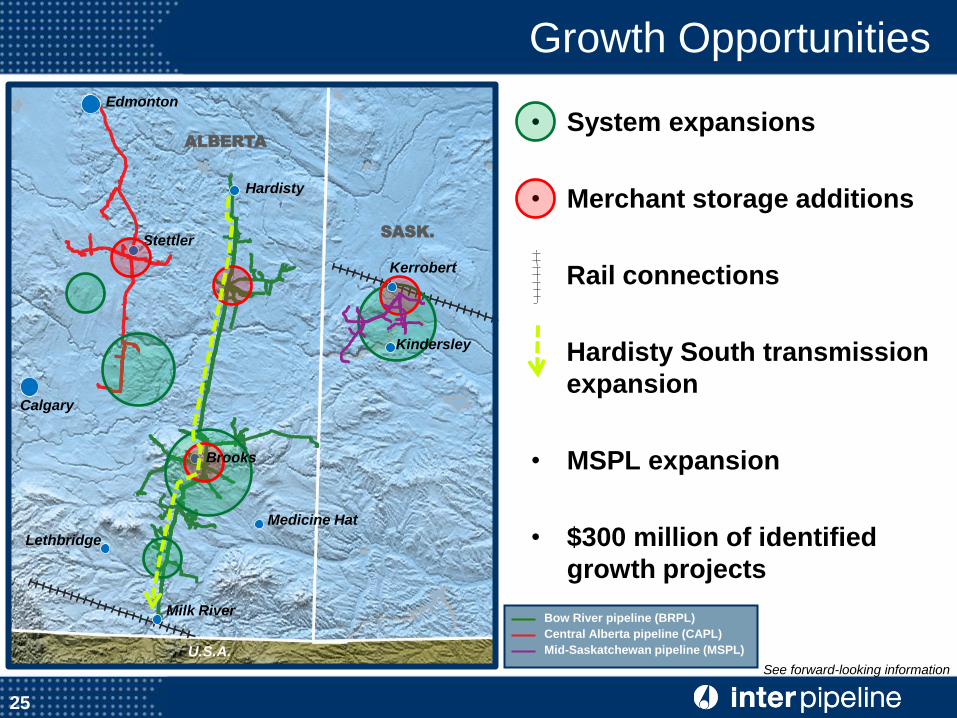

Growth Opportunities

• System expansions

• Merchant storage additions

Rail connections

Hardisty South transmission

expansion

• MSPL expansion

• $300 million of identified

growth projects

Kerrobert

Kindersley

25

Bow River pipeline (BRPL)

Central Alberta pipeline (CAPL)

Mid-Saskatchewan pipeline (MSPL)

See forward-looking information

Brooks

0

10,000

20,000

30,000

40,000

50,000

60,000

0

200

400

600

800

1,000

1,200

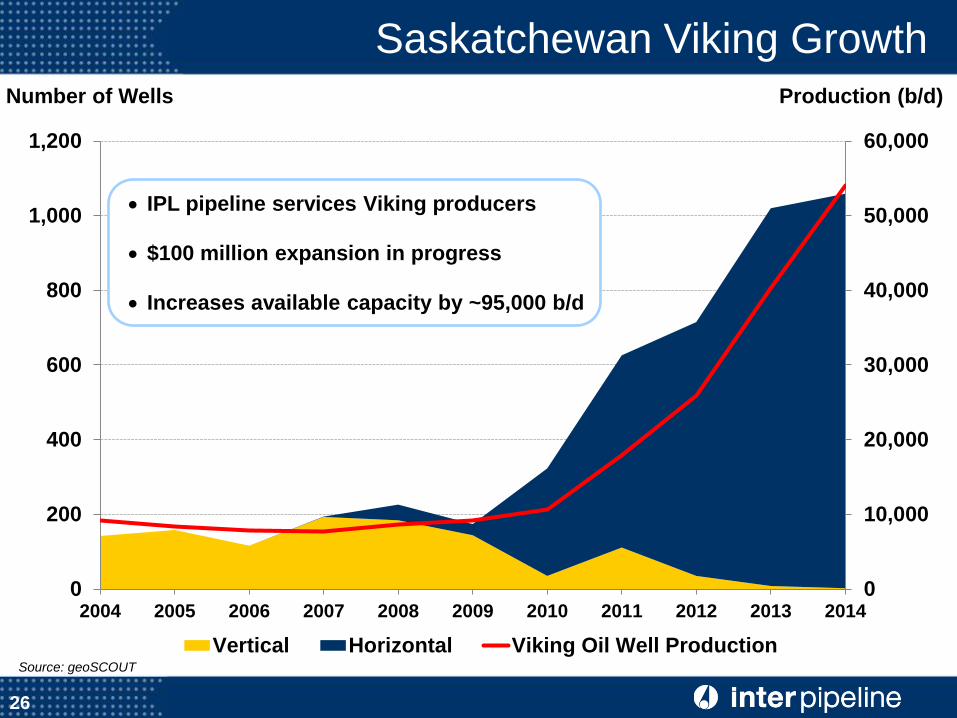

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Vertical Horizontal Viking Oil Well Production

26

Saskatchewan Viking Growth

Number of Wells Production (b/d)

Source: geoSCOUT

IPL pipeline services Viking producers

$100 million expansion in progress

Increases available capacity by ~95,000 b/d

27

2014 September YTD EBITDA

20%

SASKATCHEWAN

Edmonton ALBERTA

U.S.A.

B.C.

Calgary

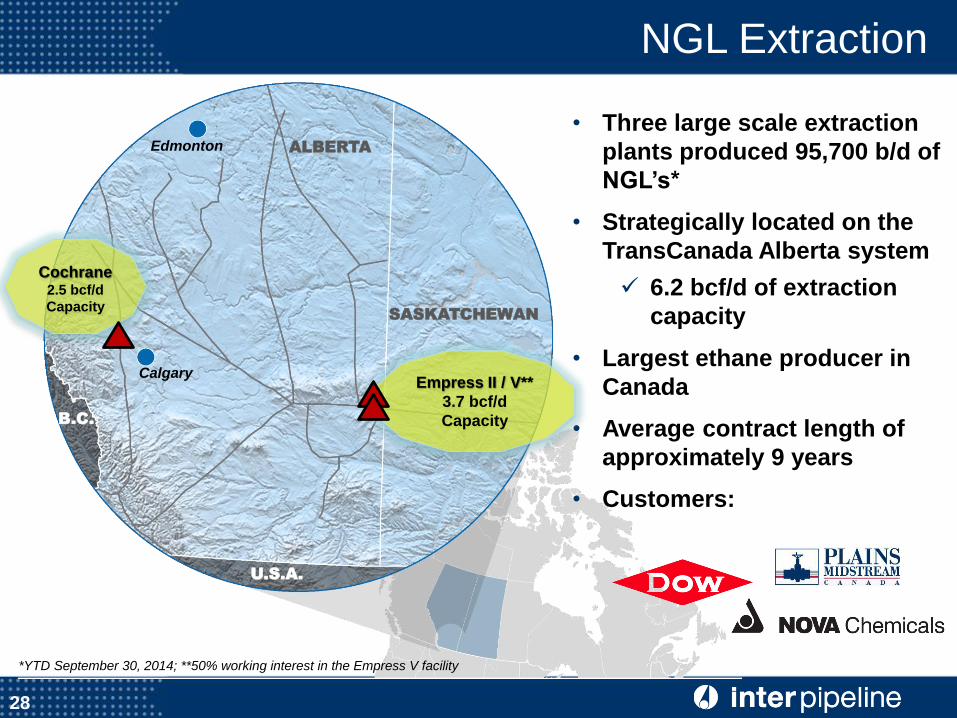

• Three large scale extraction

plants produced 95,700 b/d of

NGL’s*

• Strategically located on the

TransCanada Alberta system

6.2 bcf/d of extraction

capacity

• Largest ethane producer in

Canada

• Average contract length of

approximately 9 years

• Customers:

28

Cochrane 2.5 bcf/d

Capacity

Empress II / V**

3.7 bcf/d

Capacity

NGL Extraction

*YTD September 30, 2014; **50% working interest in the Empress V facility

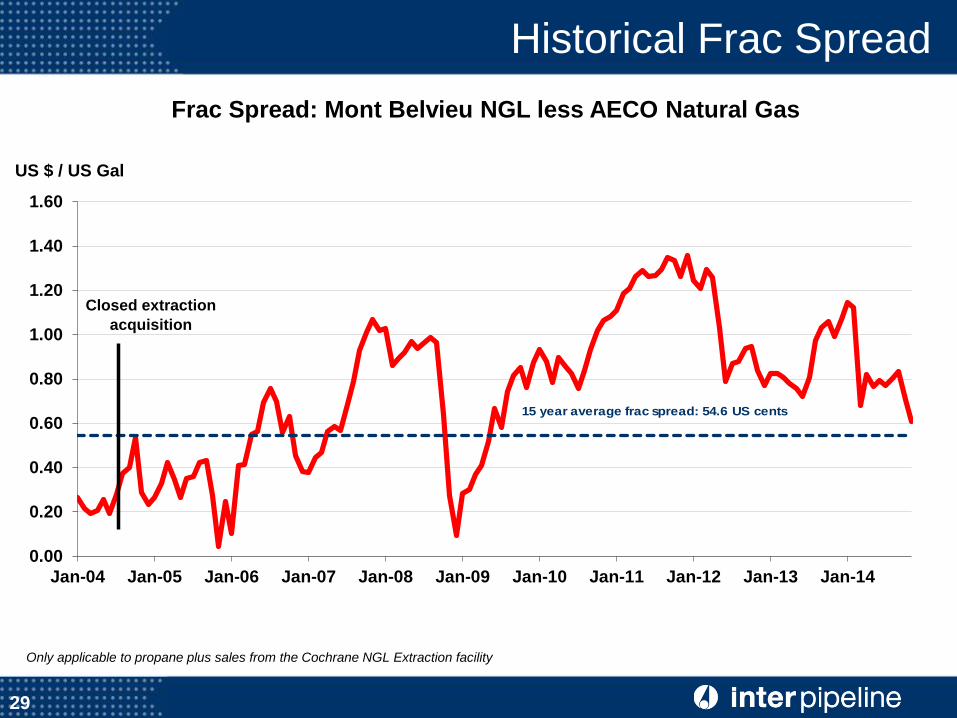

Historical Frac Spread

Frac Spread: Mont Belvieu NGL less AECO Natural Gas

Only applicable to propane plus sales from the Cochrane NGL Extraction facility

29

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14

US $ / US Gal

Closed extraction

acquisition

15 year average frac spread: 54.6 US cents

Future Opportunities

30

Calgary

SASK. ALBERTA

Edmonton

U.S.A.

B.C. Empress II & V Extraction Plants*

Cochrane Extraction Plant

DUVERNAY

• New developments require

additional infrastructure

• Leverage IPL’s strengths in:

Pipelines

Plant operations

Terminals

Major project

development

• Opportunities to pursue

large scale and strategic

partnerships

MONTNEY

*50% working interest in the Empress V facility; see forward looking-information

31

2014 September YTD EBITDA

12%

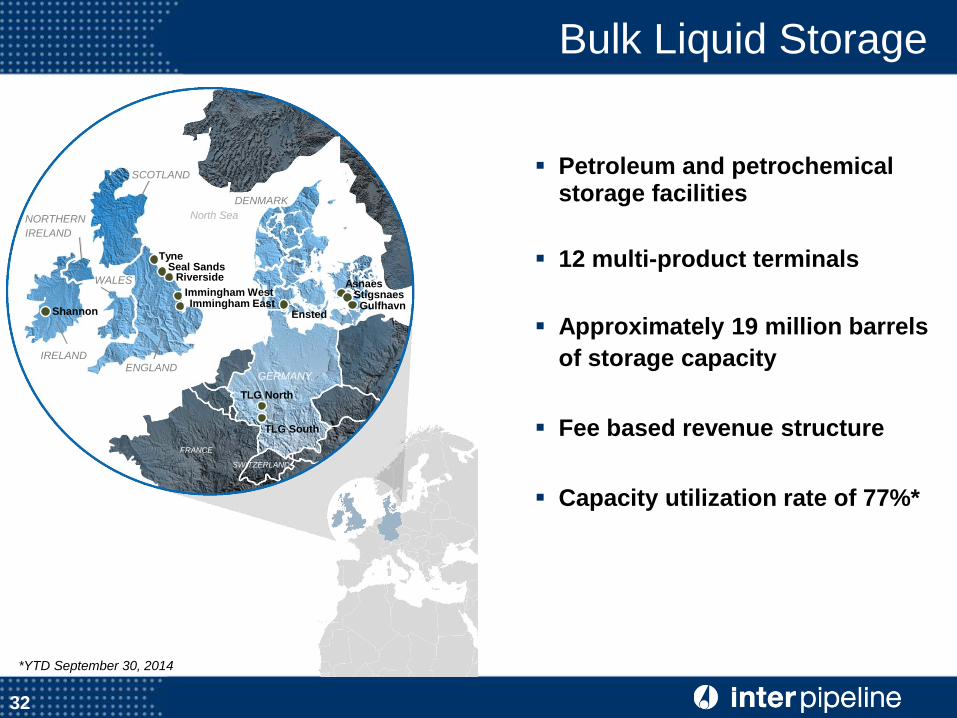

Bulk Liquid Storage

Petroleum and petrochemical storage facilities

12 multi-product terminals

Approximately 19 million barrels

of storage capacity

Fee based revenue structure

Capacity utilization rate of 77%*

32

ENGLAND

NORTHERN

IRELAND

SCOTLAND

IRELAND

WALES

GERMANY

Shannon

Immingham West

Tyne Seal Sands

Riverside

Immingham East

TLG North

TLG South

North Sea

FRANCE

SWITZERLAND

DENMARK

Ensted

Asnaes Stigsnaes Gulfhavn

*YTD September 30, 2014

Strategic Drivers

Long-life infrastructure assets

Strong organic investment potential

Geographic diversification, mature markets

Stable political and regulatory environments

Fee-based cash flow

Experienced operations and management teams

Attractive acquisition multiples

33

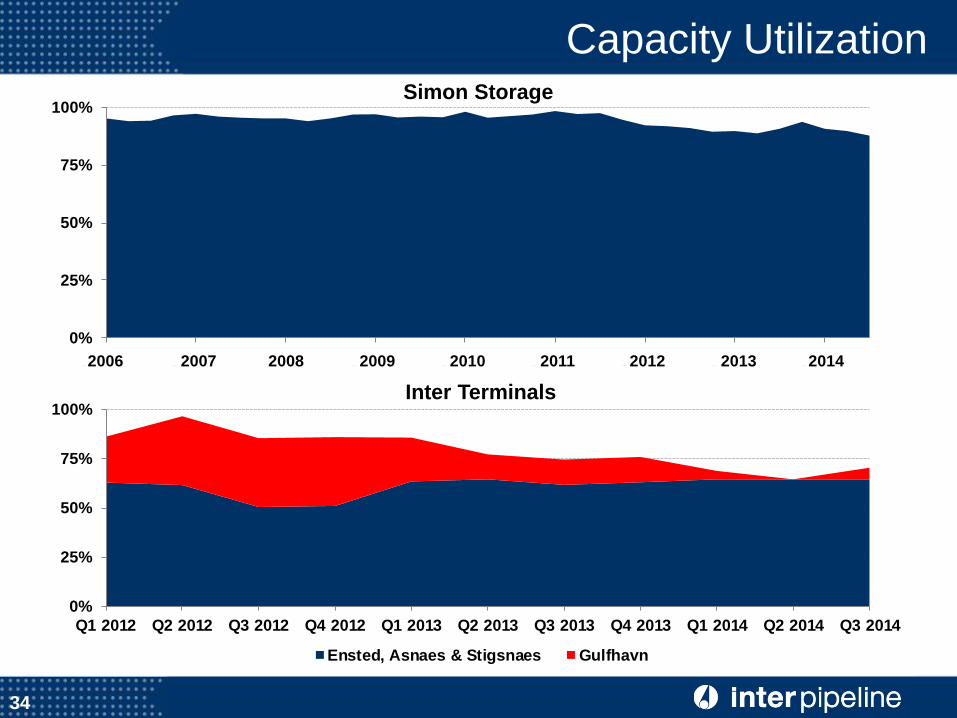

0%

25%

50%

75%

100%

Q1 2012 Q2 2012 Q3 2012 Q4 2012 Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014

Ensted, Asnaes & Stigsnaes Gulfhavn

0%

25%

50%

75%

100%

Q1 2006 Q1 2007 Q1 2008 Q1 2009 Q1 2010 Q1 2011 Q1 2012 Q1 2013 Q1 2014

Capacity Utilization Simon Storage

Inter Terminals

2006 2007 2008 2009 2010 2011 2012 2013 2014

34

Aquisition opportunities in NW Europe:

• Conversion of refinery tank storage

to regional import terminals

• Opportunities to acquire oil

distribution terminals as major oil

companies focus upstream

• Acquisition of tank storage

terminals from existing players

• Opportunities to acquire terminals

for Government backed strategic

storage contracts

35

Acquisition Growth Opportunities

IPL is a sophisticated and reputable operator,

a quality desired by sellers

Inter Pipeline’s historical acquisition

multiples:

Inter Terminals (2012) 9.3x EBITDA

Simon Storage (2005) 8.6x EBITDA

See forward-looking information

• 57,000 bbl new stainless steel

chemical tanks under construction in

Germany

• Assessing demand for additional

chemical tankage at Seal Sands and

Tyne

• Tank upgrades to provide storage for

a broader product mix

• Opportunities to convert existing

tanks for government backed

strategic storage contracts

36

Existing asset base provides numerous organic growth opportunities

Organic Growth Opportunities

See forward-looking information

37

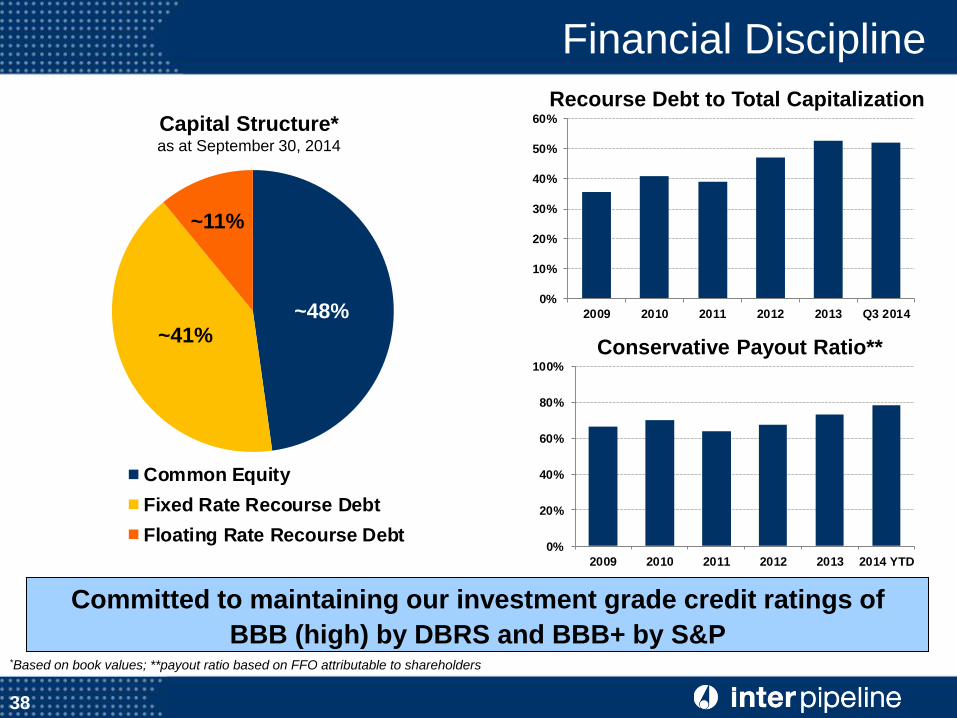

Common Equity

Fixed Rate Recourse Debt

Floating Rate Recourse Debt0%

20%

40%

60%

80%

100%

2009 2010 2011 2012 2013 2014 YTD

0%

10%

20%

30%

40%

50%

60%

2009 2010 2011 2012 2013 Q3 2014

*Based on book values; **payout ratio based on FFO attributable to shareholders

Capital Structure* as at September 30, 2014

~48% ~41%

Committed to maintaining our investment grade credit ratings of

BBB (high) by DBRS and BBB+ by S&P

Conservative Payout Ratio**

Recourse Debt to Total Capitalization

~11%

Financial Discipline

38

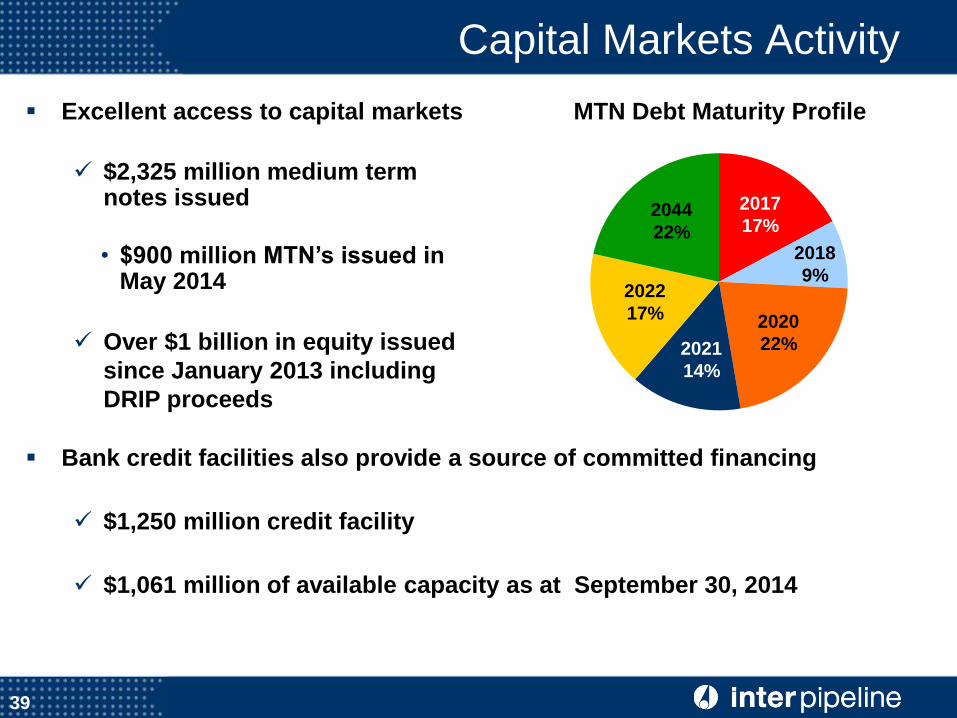

Capital Markets Activity

Excellent access to capital markets

$2,325 million medium term notes issued

• $900 million MTN’s issued in May 2014

Over $1 billion in equity issued

since January 2013 including

DRIP proceeds

39

Bank credit facilities also provide a source of committed financing

$1,250 million credit facility

$1,061 million of available capacity as at September 30, 2014

MTN Debt Maturity Profile

2044

22% 2018

9%

2017

17%

2021

14%

2020

22%

2022

17%

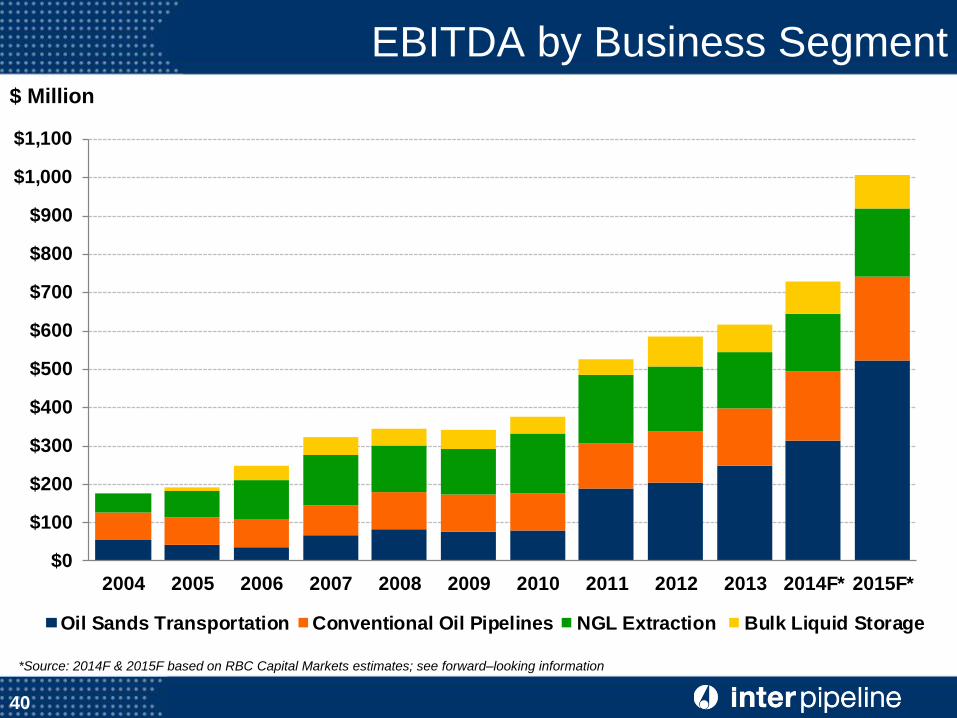

EBITDA by Business Segment $ Million

40

*Source: 2014F & 2015F based on RBC Capital Markets estimates; see forward–looking information

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

$1,000

$1,100

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014F* 2015F*

Oil Sands Transportation Conventional Oil Pipelines NGL Extraction Bulk Liquid Storage

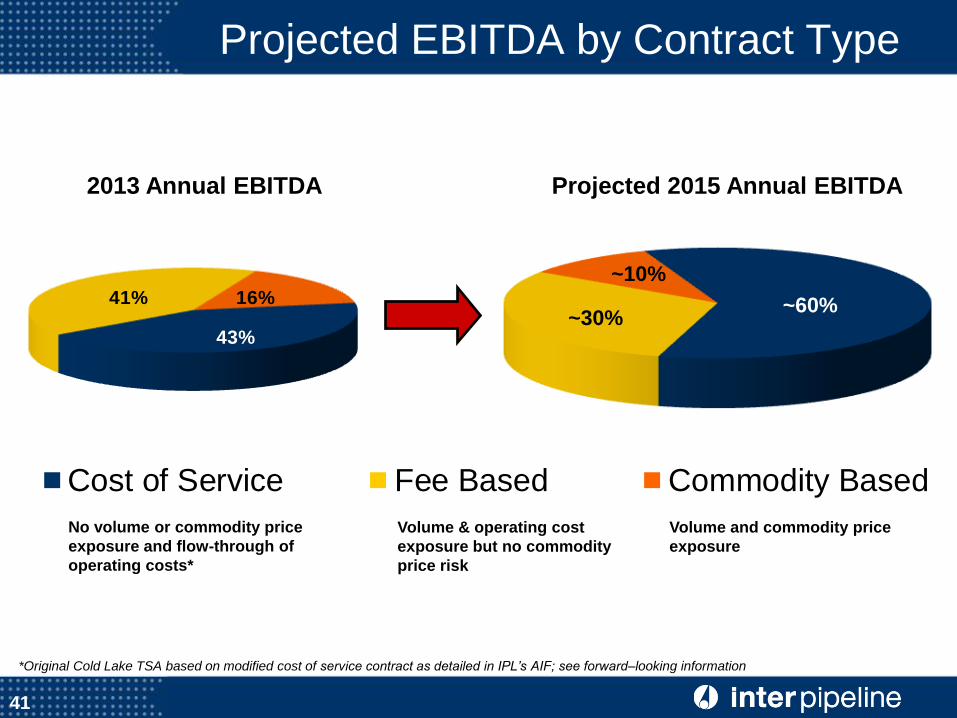

Projected EBITDA by Contract Type

Projected 2015 Annual EBITDA

37%

~10%

~60% 41%

~30%

41

43%

41% 16%

Cost of Service Fee Based Commodity Based

*Original Cold Lake TSA based on modified cost of service contract as detailed in IPL’s AIF; see forward–looking information

Cost of Service Fee Based Commodity Based

Volume and commodity price

exposure

Volume & operating cost

exposure but no commodity

price risk

No volume or commodity price

exposure and flow-through of

operating costs*

2013 Annual EBITDA

Inter Pipeline

2015F EBITDA

Mid Cap Peers

2015F EBITDA*

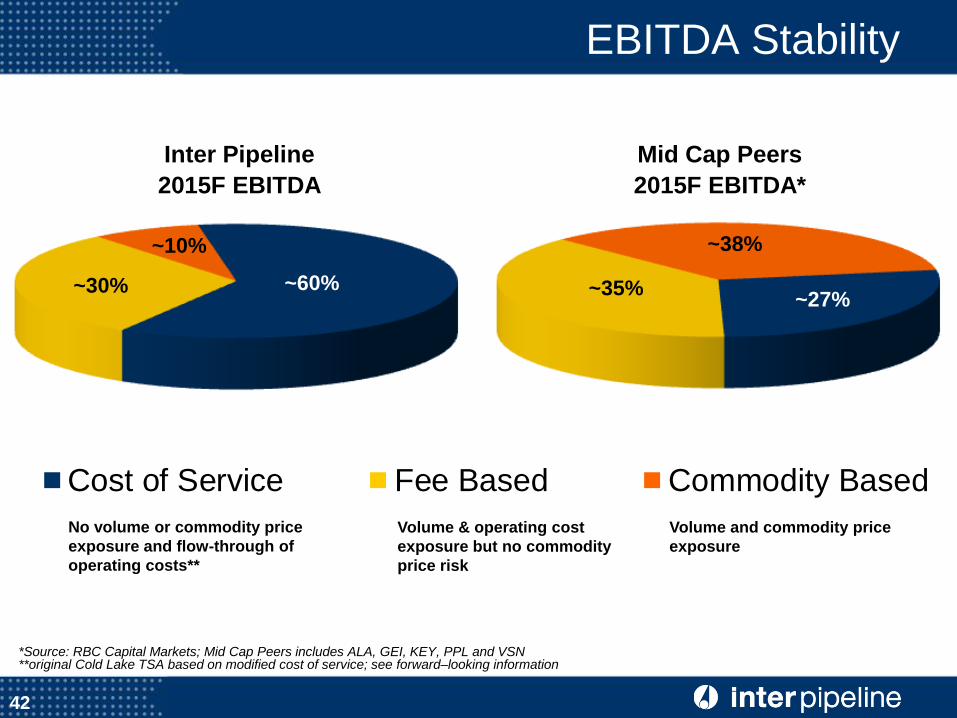

~27%

~10%

~60% ~30%

42

EBITDA Stability

~38%

~35%

Cost of Service Fee Based Commodity Based

*Source: RBC Capital Markets; Mid Cap Peers includes ALA, GEI, KEY, PPL and VSN **original Cold Lake TSA based on modified cost of service; see forward–looking information

No volume or commodity price

exposure and flow-through of

operating costs**

Volume & operating cost

exposure but no commodity

price risk

Volume and commodity price

exposure

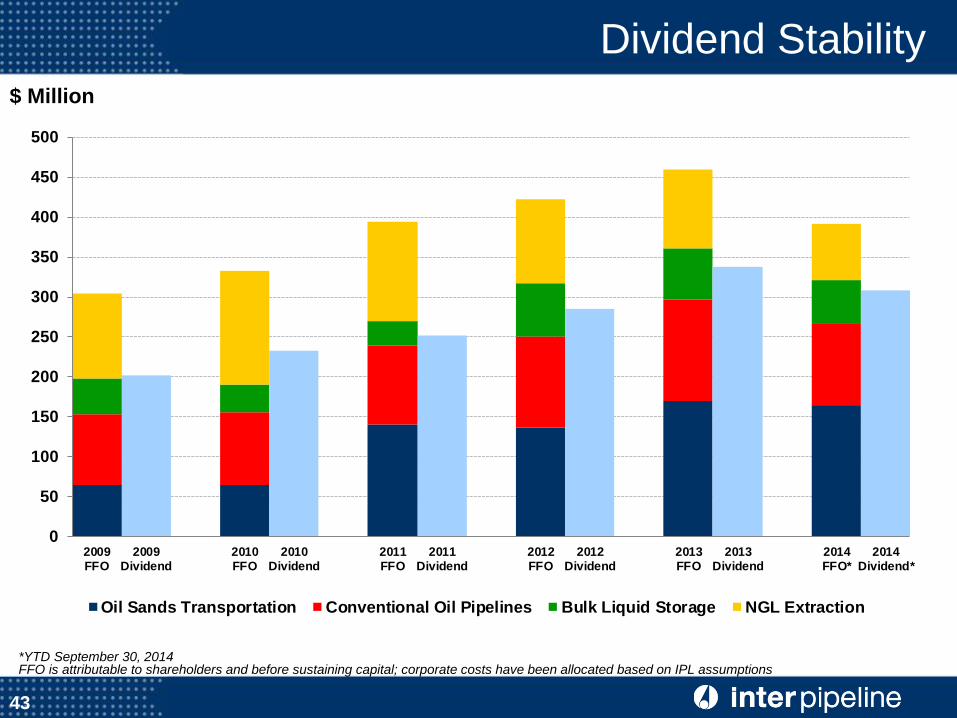

$ Million

Dividend Stability

43

*YTD September 30, 2014 FFO is attributable to shareholders and before sustaining capital; corporate costs have been allocated based on IPL assumptions

0

50

100

150

200

250

300

350

400

450

500

2009FFO

2009Dividend

2010FFO

2010Dividend

2011FFO

2011Dividend

2012FFO

2012Dividend

2013FFO

2013Dividend

2014FFO*

2014Dividend*

Oil Sands Transportation Conventional Oil Pipelines Bulk Liquid Storage NGL Extraction

Looking Forward

Experienced management team with a solid

track record of increasing shareholder value

Continued focus on developing over $7 billion

of major oil sands growth opportunities

Long-term contracts expected to generate

~60% of consolidated EBITDA by 2015

Fee-based and cost of service cash flow alone

should support future dividends

Well positioned to extend track record of

dividend growth

44

Contact Information

45

Christian Bayle

President & CEO

Brent Heagy

Chief Financial Officer

Jeremy Roberge

Vice President, Capital Markets

Inter Pipeline Ltd.

Suite 2600, 237 – 4th Avenue SW

Calgary, Alberta T2P 4K3

Phone: 1 866 716 7473

Phone: (403) 290 6000

Fax: (403) 290 6090

Web: www.interpipeline.com