Embed Size (px)

Citation preview

CORPORATE GOVERNANCE IN

ISLAMIC BANKS (IBs)

Tariqullah Khan

IRTI/IDB

Disclaimer: Views expressed are those of the presenter and do not necessarily reflect those of IDB/IRTI or any other entity quoted.

GDLN IRTI Distance Learning Lecture, April 22, 2008

Lecture Outline

Part 1: Corporate Governance – General Background

Part 2: Corporate Governance in Islamic Banks – Current State and Special Issues

Part 3: Corporate Governance in Islamic Banks – Looking Ahead

PART 1: CORPORATE GOVERNANCE: GENERAL BACKGROUND

Background

The new firm—Corporation; separation of ownership and control; asymmetric information problem and conflict of interest

Fundamental Problems of Corporate Governance: US—dispersed shareholders: “alleviate the conflict of

interest between dispersed small shareholders and powerful controlling managers”

Europe—one dominant shareholder: “align the interests of controlling and minority shareholders”

Corporate Governance refers to a set of formerly defined relationships between a company’s Management, its Board of Directors, its Shareholders and other Stakeholders

These set of relationships provide the corporate structure as well as culture through which:

the objectives of the company are set; and the means of attaining those objectives and

monitoring performance are determined.

What Is Corporate Governance?

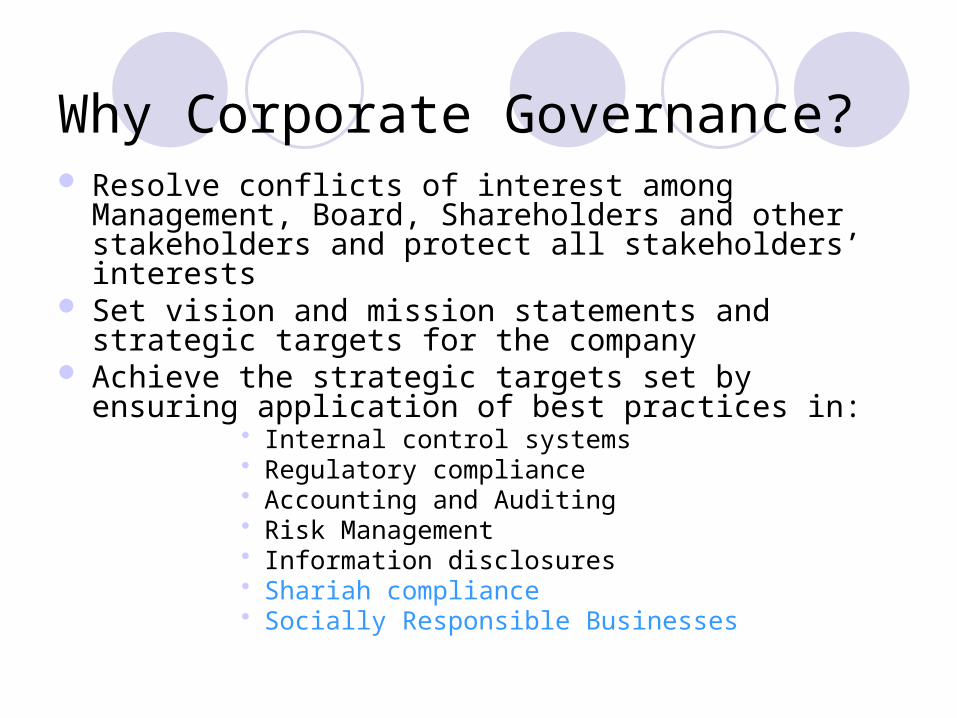

Why Corporate Governance? Resolve conflicts of interest among Management, Board,

Shareholders and other stakeholders and protect all stakeholders’ interests

Set vision and mission statements and strategic targets for the company

Achieve the strategic targets set by ensuring application of best practices in:

Internal control systems Regulatory compliance Accounting and Auditing Risk Management Information disclosures Shariah compliance Socially Responsible Businesses

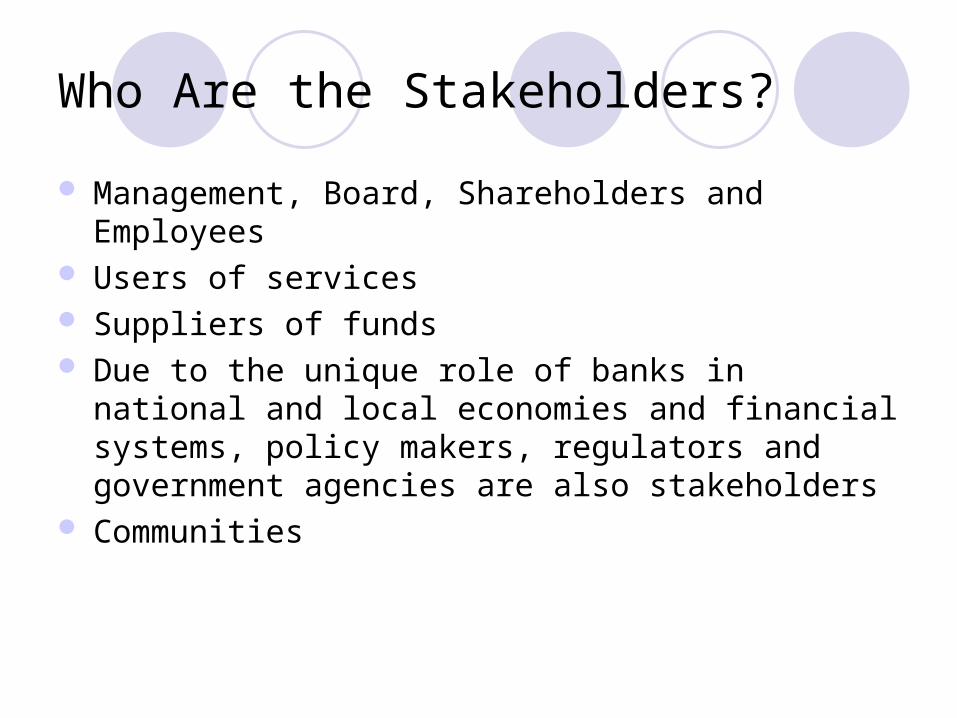

Who Are the Stakeholders?

Management, Board, Shareholders and Employees Users of services Suppliers of funds Due to the unique role of banks in national and local

economies and financial systems, policy makers, regulators and government agencies are also stakeholders

Communities

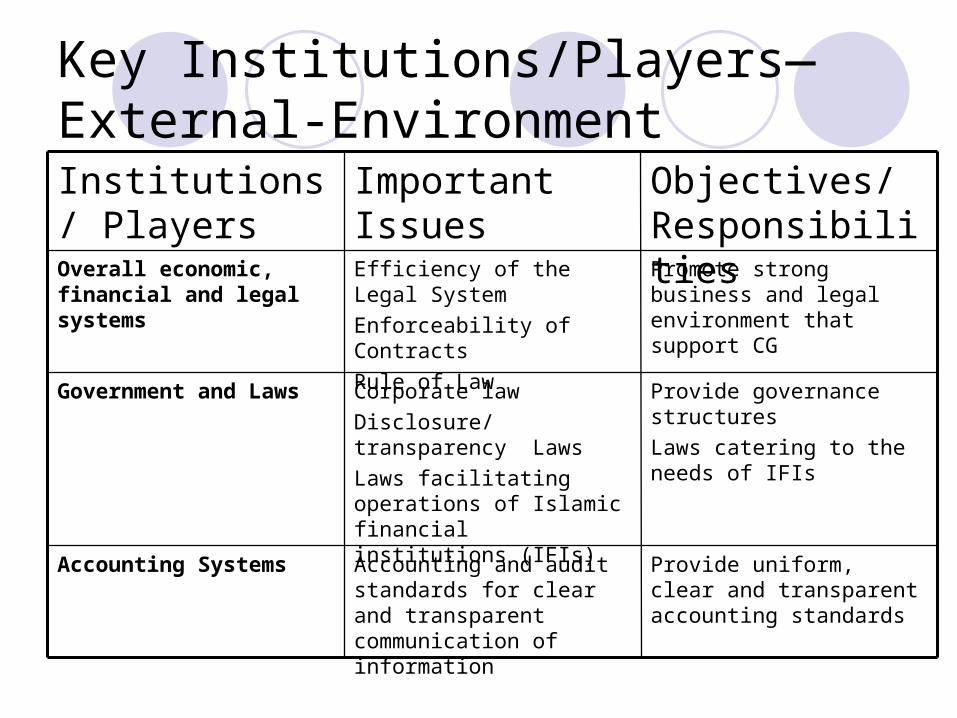

Key Institutions/Players—External-Environment

Provide uniform, clear and transparent accounting standards

Accounting and audit standards for clear and transparent communication of information

Accounting Systems

Provide governance structures

Laws catering to the needs of IFIs

Corporate law

Disclosure/transparency Laws

Laws facilitating operations of Islamic financial institutions (IFIs)

Government and Laws

Promote strong business and legal environment that support CG

Efficiency of the Legal System

Enforceability of Contracts

Rule of Law

Overall economic, financial and legal systems

Objectives/ Responsibilities

Important IssuesInstitutions/ Players

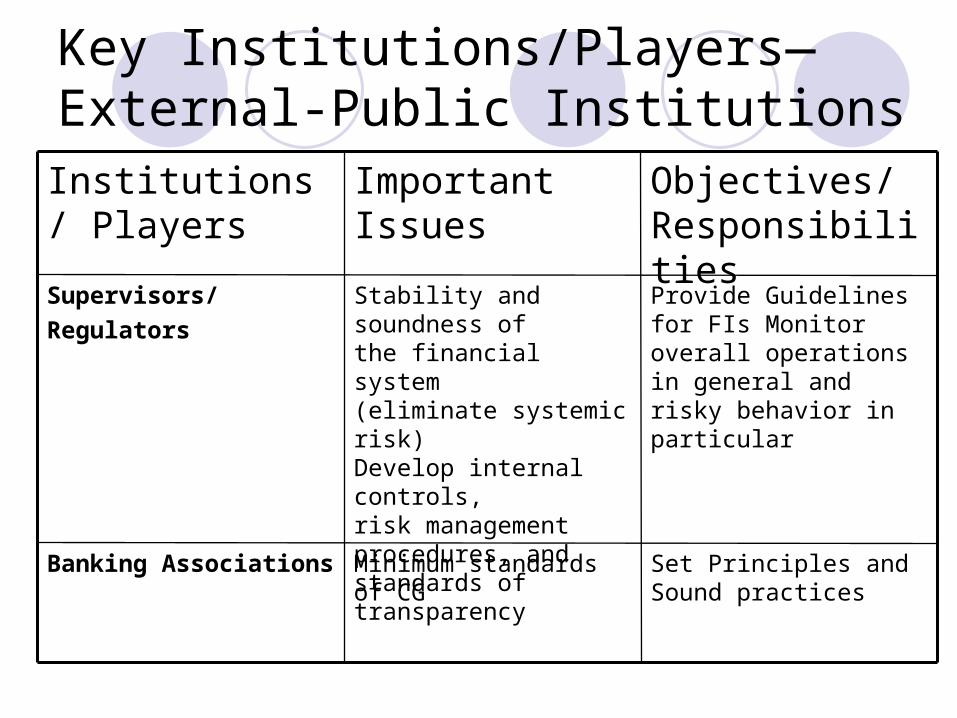

Key Institutions/Players—External-Public Institutions

Set Principles and Sound practices

Minimum standards of CGBanking Associations

Provide Guidelines for FIs Monitor overall operations in general and risky behavior in particular

Stability and soundness ofthe financial system(eliminate systemic risk)Develop internal controls,risk management procedures, and standards oftransparency

Supervisors/

Regulators

Objectives/ Responsibilities

Important IssuesInstitutions/ Players

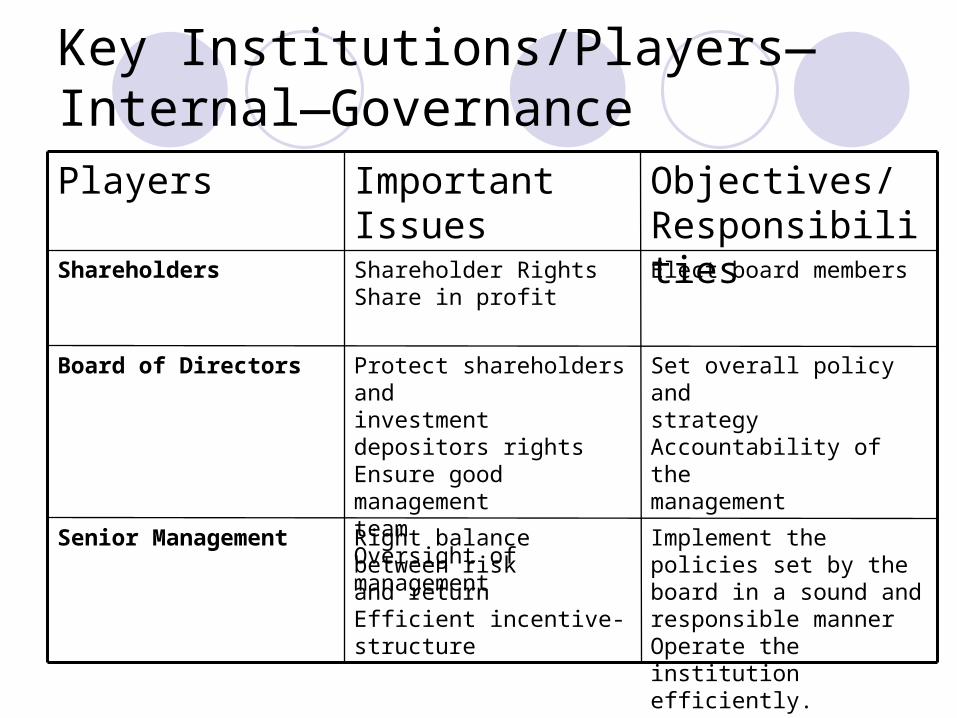

Key Institutions/Players—Internal—Governance

Implement the policies set by the board in a sound and responsible mannerOperate the institutionefficiently.

Right balance between riskand returnEfficient incentive-structure

Senior Management

Set overall policy and strategy Accountability of themanagement

Protect shareholders andinvestment depositors rightsEnsure good managementteamOversight of management

Board of Directors

Elect board members Shareholder RightsShare in profit

Shareholders

Objectives/ Responsibilities

Important IssuesPlayers

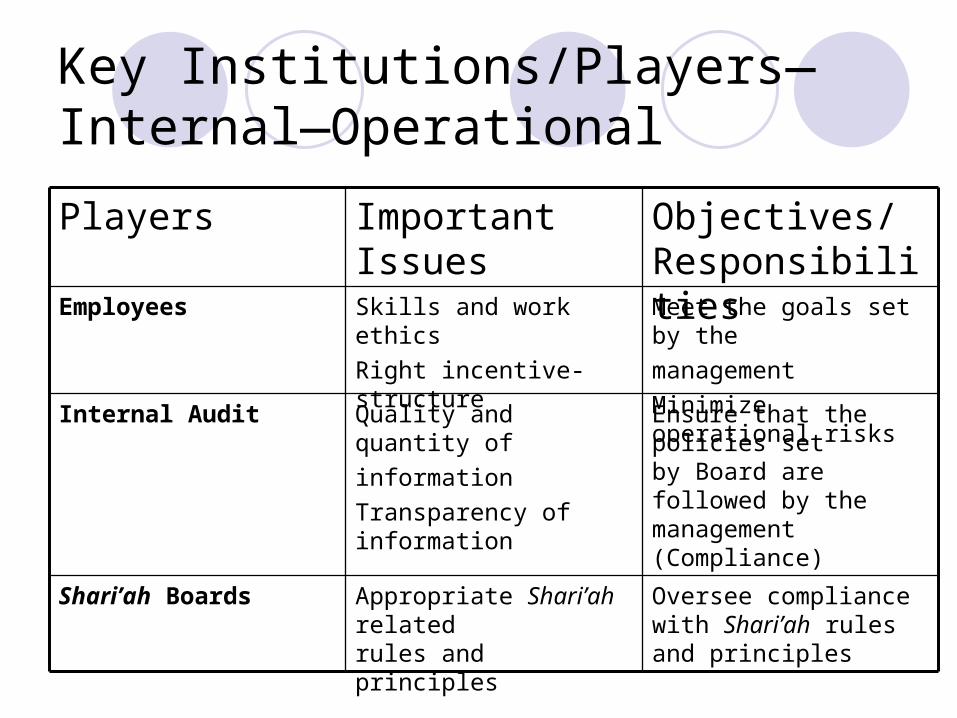

Key Institutions/Players—Internal—Operational

Oversee compliance with Shari’ah rules and principles

Appropriate Shari’ah relatedrules and principles

Shari’ah Boards

Ensure that the policies setby Board are followed by themanagement (Compliance)

Quality and quantity of

information

Transparency of information

Internal Audit

Meet the goals set by the

management

Minimize operational risks

Skills and work ethics

Right incentive-structure

Employees

Objectives/ Responsibilities

Important IssuesPlayers

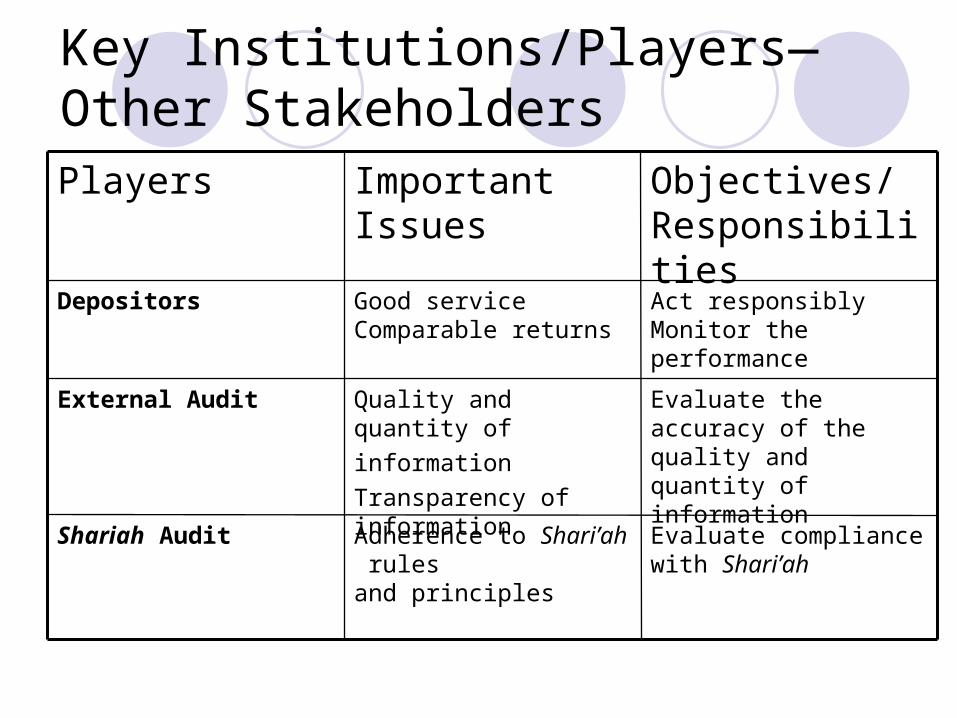

Key Institutions/Players—Other Stakeholders

Evaluate compliance with Shari’ah

Adherence to Shari’ah rulesand principles

Shariah Audit

Evaluate the accuracy of thequality and quantity ofinformation

Quality and quantity of

information

Transparency of information

External Audit

Act responsiblyMonitor the performance

Good serviceComparable returns

Depositors

Objectives/ Responsibilities

Important IssuesPlayers

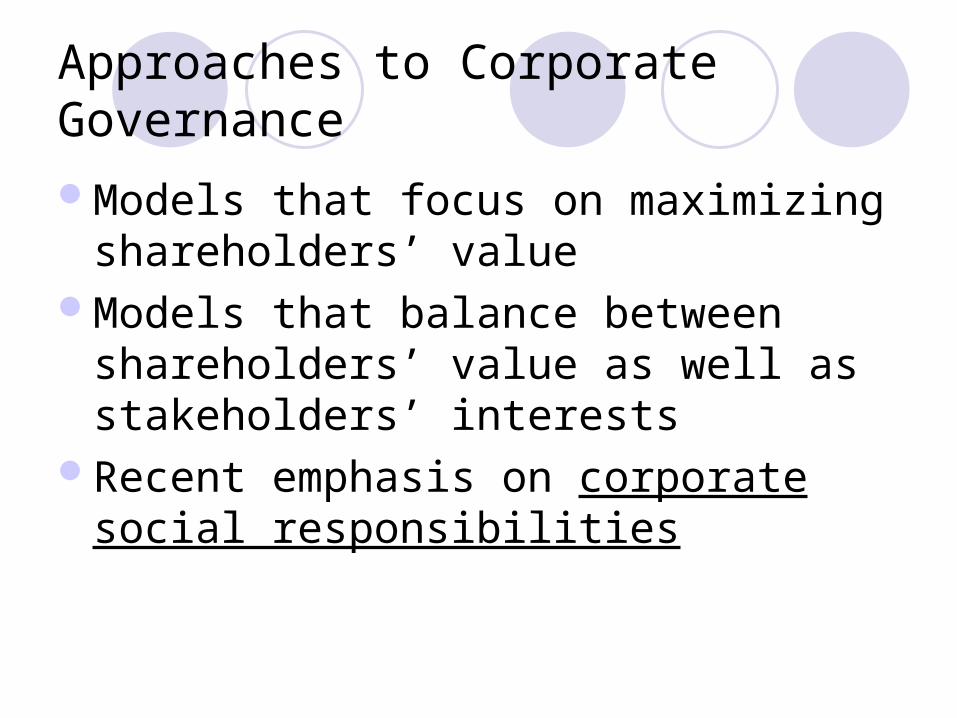

Approaches to Corporate Governance

Models that focus on maximizing shareholders’ value

Models that balance between shareholders’ value as well as stakeholders’ interests

Recent emphasis on corporate social responsibilities

How to Protect the Interests of Stakeholders?

Apply best practice standards and effective systems of accountability and incentives

Unambiguous contracts and documented rights and responsibilities of parties

Information disclosure and market discipline Institutional checks and balances Regulation and supervision Moral suasion Enabling environment

PART 2: CORPORATE GOVERNANCE IN ISLAMIC BANKS: CURRENT STATE AND SPECIAL ISSUES

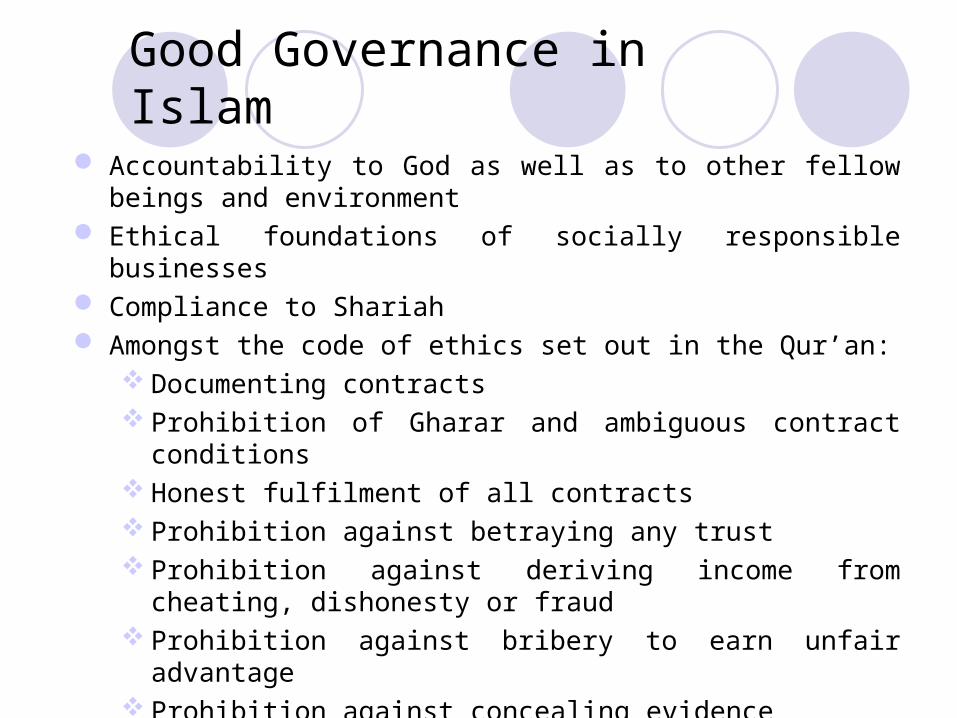

Good Governance in Islam

Accountability to God as well as to other fellow beings and environment

Ethical foundations of socially responsible businesses Compliance to Shariah Amongst the code of ethics set out in the Qur’an:

Documenting contracts Prohibition of Gharar and ambiguous contract conditions Honest fulfilment of all contracts Prohibition against betraying any trust Prohibition against deriving income from cheating, dishonesty

or fraud Prohibition against bribery to earn unfair advantage Prohibition against concealing evidence

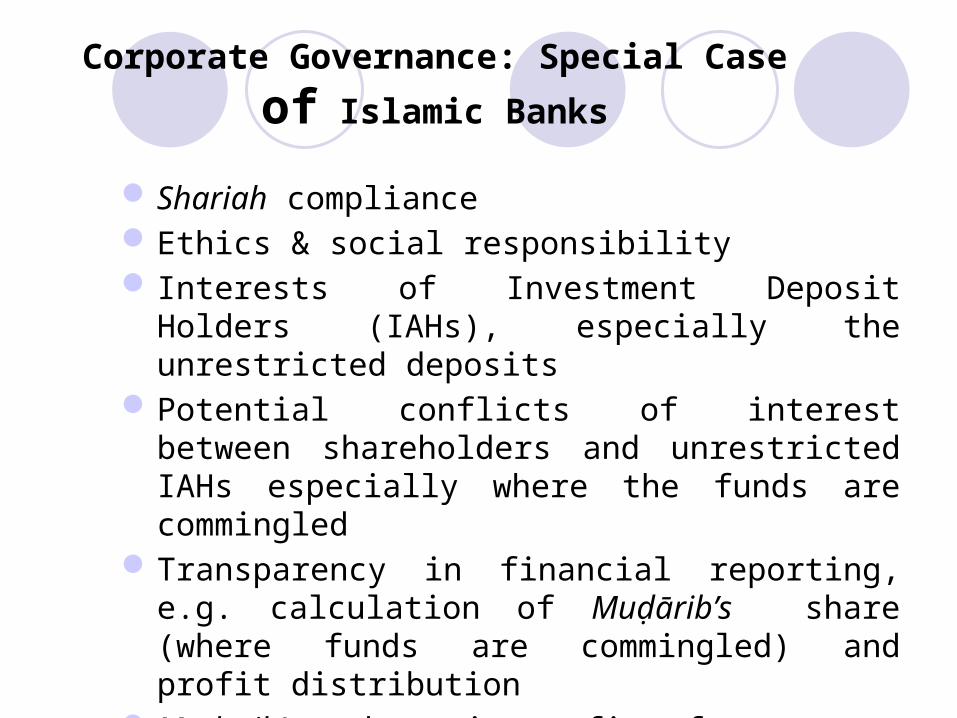

Corporate Governance: Special Case of Islamic Banks

Shariah compliance Ethics & social responsibility Interests of Investment Deposit Holders (IAHs),

especially the unrestricted deposits Potential conflicts of interest between shareholders

and unrestricted IAHs especially where the funds are commingled

Transparency in financial reporting, e.g. calculation of Muḍārib’s share (where funds are commingled) and profit distribution

Muḍārib’s share in profits from assets financed by current accounts

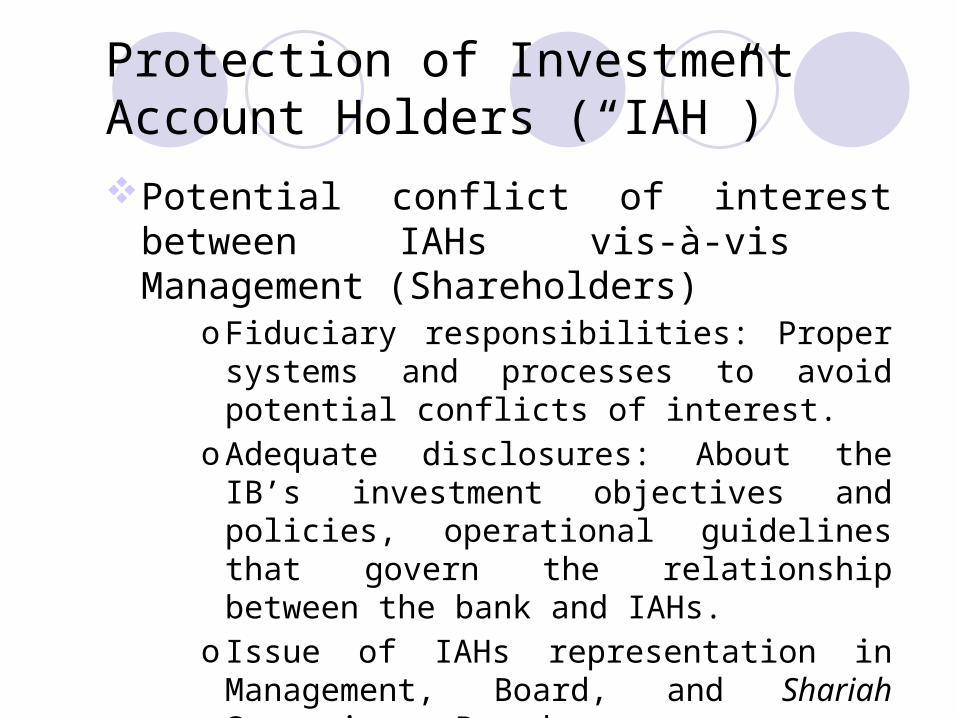

Potential conflict of interest between IAHs vis-à-vis Management (Shareholders)

o Fiduciary responsibilities: Proper systems and processes to avoid potential conflicts of interest.

o Adequate disclosures: About the IB’s investment objectives and policies, operational guidelines that govern the relationship between the bank and IAHs.

o Issue of IAHs representation in Management, Board, and Shariah Supervisory Board

Protection of Investment Account Holders (“IAH”)

SSB is a specific organ of governance. It should be concerned with monitoring Shariah compliance and not just issuing fatwas.

Since SSB members may lack monitoring skills, auditors and audit committee should act in concert to assist SSB.

Sharī`ah Supervisory Board (“SSB”)

Transparency in Financial Reporting

The current financial reporting practices of IBs do not provide adequate information to their IAH regarding the revenues and expenses accruing to their particular investment fund

IAH is rightfully entitled to transparency, e.g. calculation of Muḍārib share and profit allocation

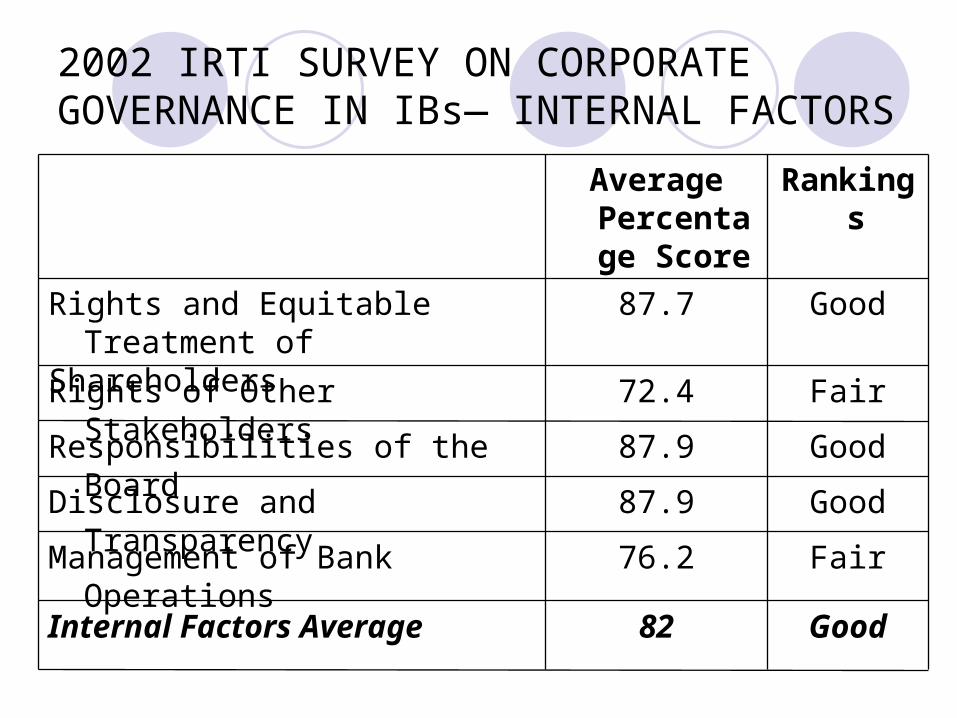

2002 IRTI SURVEY ON CORPORATE GOVERNANCE IN IBs— INTERNAL FACTORS

Good82Internal Factors Average

Fair76.2Management of Bank Operations

Good87.9Disclosure and Transparency

Good87.9Responsibilities of the Board

Fair72.4Rights of Other Stakeholders

Good87.7Rights and Equitable Treatment of Shareholders

Rankings Average Percentage

Score

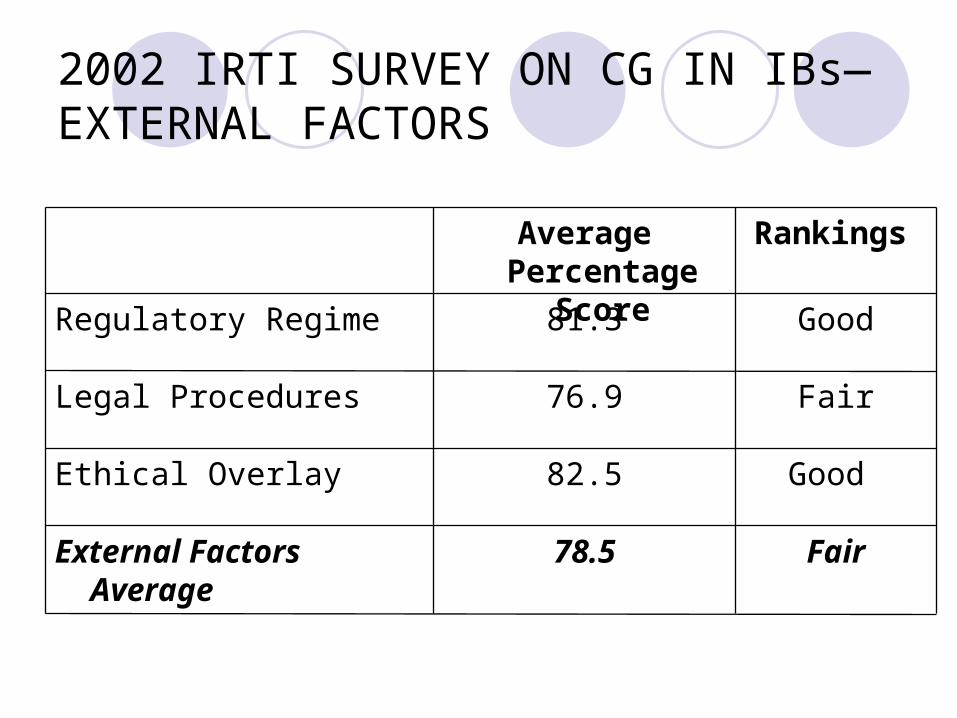

Fair78.5External Factors Average

Good 82.5Ethical Overlay

Fair76.9Legal Procedures

Good81.3Regulatory Regime

Rankings Average Percentage Score

2002 IRTI SURVEY ON CG IN IBs— EXTERNAL FACTORS

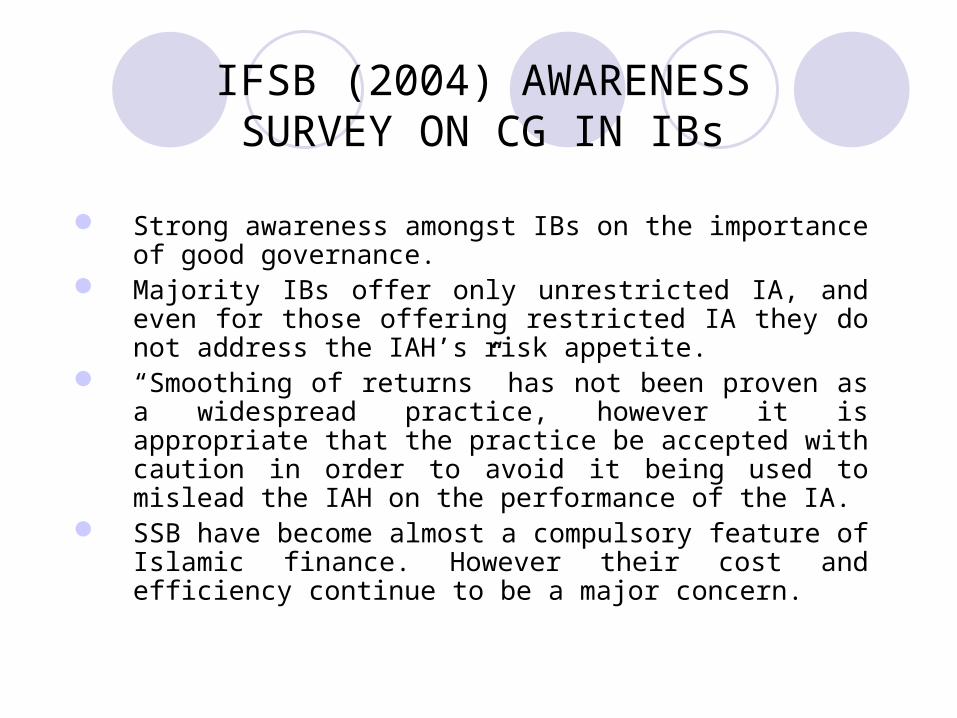

Strong awareness amongst IBs on the importance of good governance.

Majority IBs offer only unrestricted IA, and even for those offering restricted IA they do not address the IAH’s risk appetite.

“Smoothing of returns” has not been proven as a widespread practice, however it is appropriate that the practice be accepted with caution in order to avoid it being used to mislead the IAH on the performance of the IA.

SSB have become almost a compulsory feature of Islamic finance. However their cost and efficiency continue to be a major concern.

IFSB (2004) AWARENESS SURVEY ON CG IN IBs

PART 3: CORPORATE GOVERNANCE IN ISLAMIC BANKS – LOOKING AHEAD

Islamic Financial Services Board (IFSB), “Guiding Principles on Corporate Governance of Institutions Offering Islamic Financial Services (IIFS)”: Scope and Related Issues

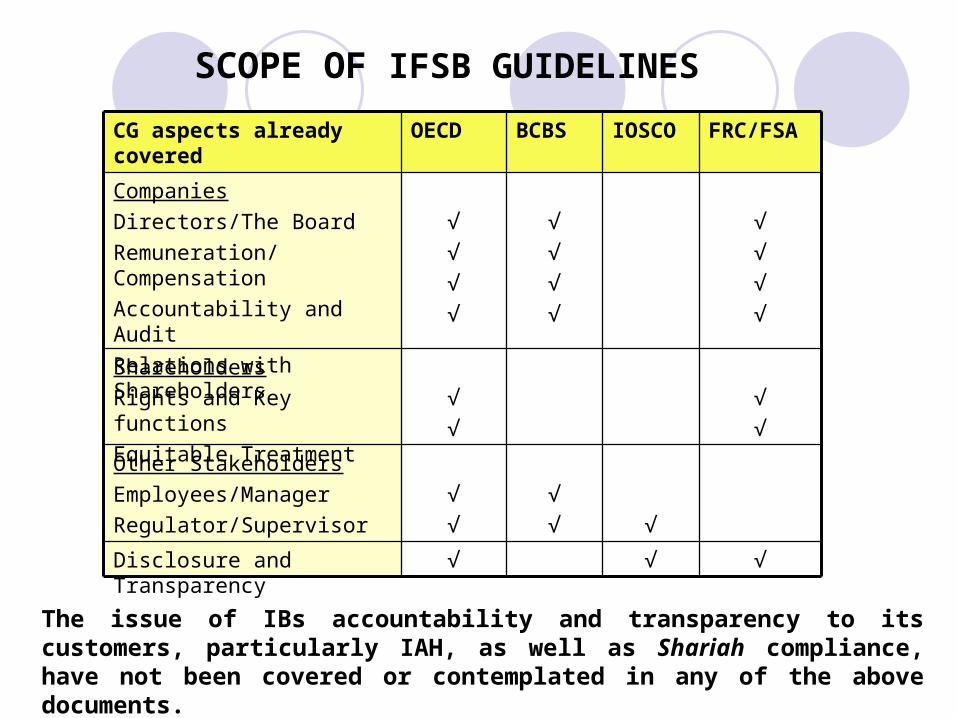

SCOPE OF IFSB GUIDELINES

√

√

√

√

√

√

√

FRC/FSA

√

√

IOSCO

√Disclosure and Transparency

√

√

√

√

Other Stakeholders

Employees/Manager

Regulator/Supervisor

√

√

Shareholders

Rights and Key functions

Equitable Treatment

√

√

√

√

√

√

√

√

Companies

Directors/The Board

Remuneration/Compensation

Accountability and Audit

Relations with Shareholders

BCBSOECDCG aspects already covered

The issue of IBs accountability and transparency to its customers, particularly IAH, as well as Shariah compliance, have not been covered or contemplated in any of the above documents.

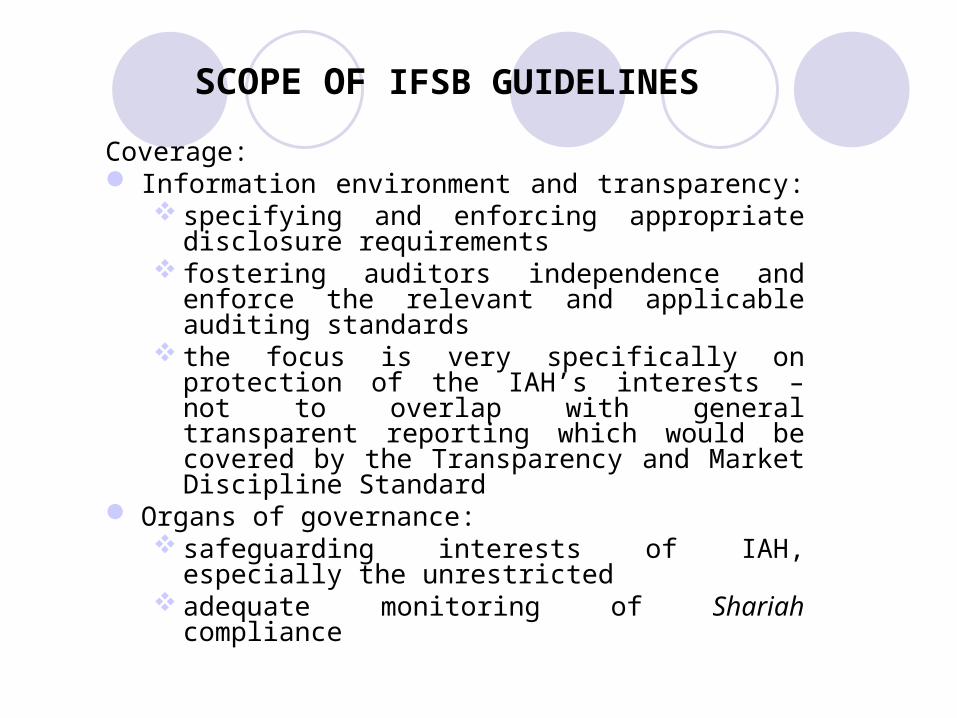

Coverage: Information environment and transparency:

specifying and enforcing appropriate disclosure requirements

fostering auditors independence and enforce the relevant and applicable auditing standards

the focus is very specifically on protection of the IAH’s interests – not to overlap with general transparent reporting which would be covered by the Transparency and Market Discipline Standard

Organs of governance: safeguarding interests of IAH, especially the

unrestricted adequate monitoring of Shariah compliance

SCOPE OF IFSB GUIDELINES

IFSB PRINCIPLES OF CORPORATE GOVERNANCE

Principle 1.1

IBs shall establish a comprehensive governance policy framework which sets out the strategic roles and functions of each organs of governance and mechanisms for balancing their accountabilities to various stakeholders.

Principle 1.2

IBs shall ensure that the reporting of their financial and non-financial information meets the requirements of internationally recognised accounting standards which are in compliance with Shariah rules and principles and are applicable to the Islamic financial services industry as recognised by the supervisory authorities.

IFSB PRINCIPLES OF CORPORATE GOVERNANCE

Principle 2.1

IBs shall acknowledge the IAH’s rights to monitor the performance of their investments and the associated risks, and put into place adequate means to ensure that these rights are observed and exercised.

IFSB PRINCIPLES OF CORPORATE GOVERNANCE

Principle 2.2

IBs shall adopt a sound investment strategy which is appropriately aligned to the risk and return expectations of IAH (bearing in mind the distinction between restricted and unrestricted IAH), and be transparent in smoothing any returns.

IFSB PRINCIPLES OF CORPORATE GOVERNANCE

Principle 3.1

IBs shall have in place an appropriate mechanism for obtaining Shariah rulings, application of fatwas and monitoring of Shariah compliance in all aspects of their products and operations.

IFSB PRINCIPLES OF CORPORATE GOVERNANCE

Principle 3.2

IBs shall comply with the Shariah rules and principles as expressed in the rulings of the IBs Shariah scholars. The IBs shall make these rules and principles available to the public.

IFSB PRINCIPLES OF CORPORATE GOVERNANCE

Principle 4.1

IBs shall make adequate and timely disclosure to IAH and the public, of material and relevant information on the investment accounts that they manage.

IFSB PRINCIPLES OF CORPORATE GOVERNANCE

The IFSB understands that: Adoption of OECD and BCBS recommendations will improve

IBs’ Board and Directors’ and Management’s awareness of the importance of good governance

Due recognition of IAH’s rights and risks as residual claimants will lead to appropriate protection of IAH

More professional approach for Shariah compliance will mitigate compliance and reputational risks of IBs

Increased transparency in financial and non-financial reporting by IBs will inculcate better risk management structure and discipline culture amongst IBs

Looking Ahead

Looking Ahead – Need to Strengthen CG Architecture for IBs Credit-rating agencies Centralized Shariah boards Shariah Courts and Banking tribunals AAOIFI and other Audit organizations Training in Islamic banking Islamic financial market IFSB, Islamic Financial Services Board IIFM, International Islamic Financial Market CIBAFI and Corporate Social Responsibility of IBs Lender of Last Resort Reform of the Stock Market

Acknowledgments and References

Ahmed, Habib (2007), presentation on “Corporate Governance in Islamic Banks”

Hussain, Madzlan Mohamad (2006) Presentation on IFSB Guidelines on Corporate Governance in IIFS

Chapra, M. U and Habib Ahmed (2002) Corporate Governance in Islamic Financial Institutions, Jeddah IRTI

IFSB (2007) “Guiding Principles on corporate Governance of Institutions Offering Islamic Financial Services (IIFS)”