Embed Size (px)

Citation preview

Corporate FinanceCorporate Finance

Lecture 4Lecture 4

Topics coveredTopics covered

Inflation in capital budgetingInflation in capital budgeting– Interest rate and inflation rateInterest rate and inflation rate– Discounting with inflationDiscounting with inflation

Investment with unequal livesInvestment with unequal lives

Inflation and capital Inflation and capital budgetingbudgeting Interest rates and inflationInterest rates and inflation

– The effect of inflation: The time value The effect of inflation: The time value of money is deflated by inflation. of money is deflated by inflation.

– Real interest rate vs. nominal interest Real interest rate vs. nominal interest raterate

1 real interest rate = 1+nominal interest rate1+inflation rate

InflationInflation

Be consistent in how you handle Be consistent in how you handle inflation!inflation!– Use nominal interest rates to Use nominal interest rates to

discount nominal cash flows.discount nominal cash flows.– Use real interest rates to discount Use real interest rates to discount

real cash flows.real cash flows.– Notice the treatment of depreciations in Notice the treatment of depreciations in

the two approaches: Dthe two approaches: Depreciation is a epreciation is a nominalnominal number! number!

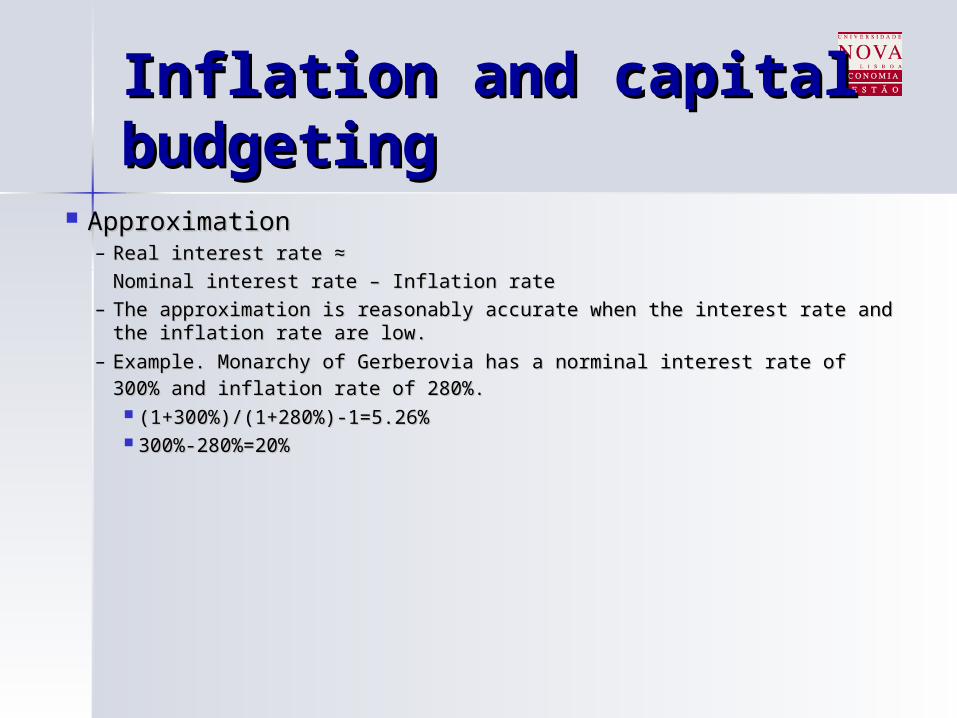

Inflation and capital Inflation and capital budgetingbudgeting

ApproximationApproximation– Real interest rate ≈ Real interest rate ≈

Nominal interest rate – Inflation rateNominal interest rate – Inflation rate– The approximation is reasonably accurate when the interest rate and the The approximation is reasonably accurate when the interest rate and the

inflation rate are low.inflation rate are low.– Example. Monarchy of Gerberovia has a norminal interest rate of 300% and Example. Monarchy of Gerberovia has a norminal interest rate of 300% and

inflation rate of 280%.inflation rate of 280%. (1+300%)/(1+280%)-1=5.26%(1+300%)/(1+280%)-1=5.26% 300%-280%=20%300%-280%=20%

InflationInflation

ExampleExample

You own a lease that will cost You own a lease that will cost you $8,000 this year, you $8,000 this year, increasing at 3% a year (the increasing at 3% a year (the forecasted inflation rate) for 3 forecasted inflation rate) for 3 additional years (4 years additional years (4 years total). If discount rates are total). If discount rates are 10% what is the present value 10% what is the present value cost of the lease?cost of the lease?

InflationInflation

Example - nominal Example - nominal figuresfigures

8,741.82=8000x1.033

20.487,8=8000x1.032

8,240=8000x1.031

80000

FlowCash Year

3

2

$29,072.98

6,567.86

7,014.22

91.490,7

00.000,8

10% @ PV

3

2

10.182.8741

10.120.8487

10.18240

InflationInflation

Example - real figuresExample - real figures

8,0003

8,0002

8,0001

8,0000

FlowCash Year

29,072.98

6,567.86

7,014.22

7,490.91

8,000

3

2

068.1

8,000068.1

8,000068.1

8,000

= $

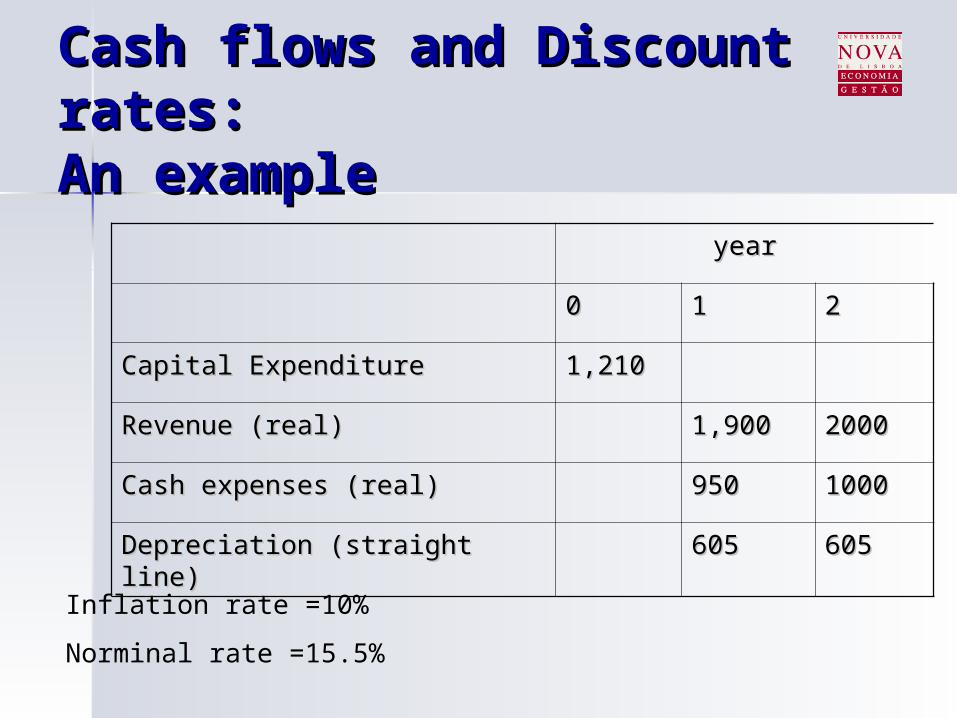

Cash flows and Discount Cash flows and Discount rates: rates: An exampleAn example

yearyear

00 11 22

Capital ExpenditureCapital Expenditure 1,2101,210

Revenue (real)Revenue (real) 1,9001,900 20002000

Cash expenses (real)Cash expenses (real) 950950 10001000

Depreciation (straight line)Depreciation (straight line) 605605 605605

Inflation rate =10%

Norminal rate =15.5%

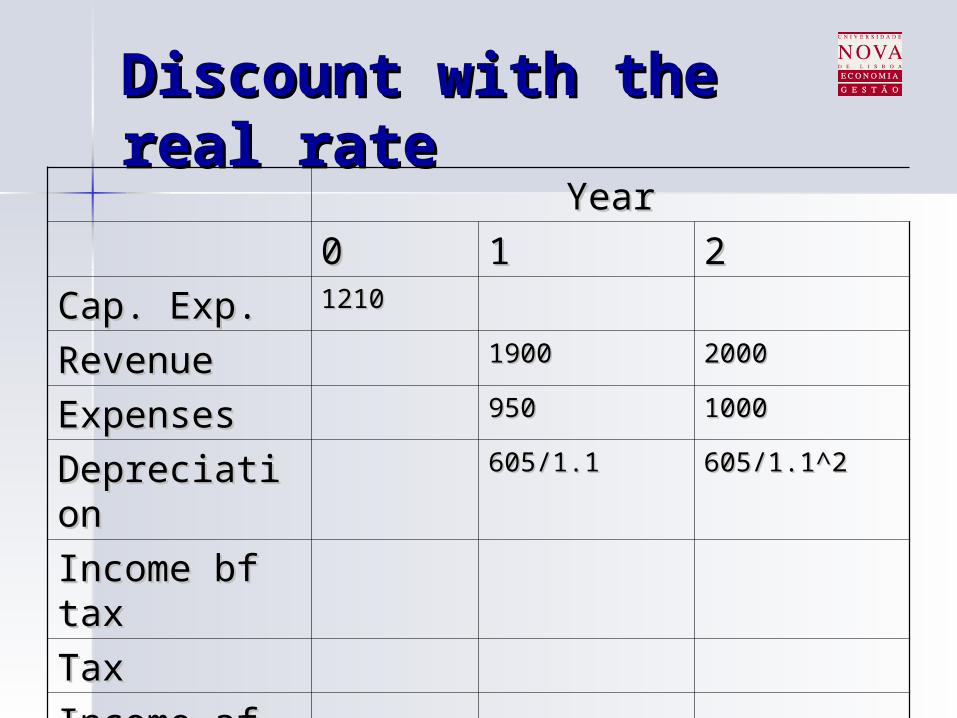

Discount with the real Discount with the real raterate

YearYear

00 11 22

Cap. Exp.Cap. Exp. 12101210

RevenueRevenue 19001900 20002000

ExpensesExpenses 950950 10001000

DepreciationDepreciation

Income bf Income bf taxtax

TaxTax

Income af Income af taxtax

NCFNCF

Discount with the real Discount with the real raterate

YearYear

00 11 22

Cap. Exp.Cap. Exp. 12101210

RevenueRevenue 19001900 20002000

ExpensesExpenses 950950 10001000

DepreciationDepreciation 605/1.1605/1.1 605/1.1^2605/1.1^2

Income bf Income bf taxtax

TaxTax

Income af Income af taxtax

NCFNCF

Discount with the real Discount with the real raterate

YearYear

00 11 22

Cap. Exp.Cap. Exp. 12101210

RevenueRevenue 19001900 20002000

ExpensesExpenses 950950 10001000

DepreciationDepreciation 605/1.1605/1.1 605/1.1^2605/1.1^2

Income bf Income bf taxtax

400400 500500

TaxTax

Income af Income af taxtax

NCFNCF

Discount with the real Discount with the real raterate

YearYear

00 11 22

Cap. Exp.Cap. Exp. 12101210

RevenueRevenue 19001900 20002000

ExpensesExpenses 950950 10001000

DepreciationDepreciation 605/1.1605/1.1 605/1.1^2605/1.1^2

Income bf Income bf taxtax

400400 500500

TaxTax 400*40%400*40% 500*40%500*40%

Income af Income af taxtax

NCFNCF

Discount with the real Discount with the real raterate

YearYear

00 11 22

Cap. Exp.Cap. Exp. 12101210

RevenueRevenue 19001900 20002000

ExpensesExpenses 950950 10001000

DepreciationDepreciation 605/1.1605/1.1 605/1.1^2605/1.1^2

Income bf Income bf taxtax

400400 500500

TaxTax 400*40%400*40% 500*40%500*40%

Income af Income af taxtax

240240 300300

NCFNCF

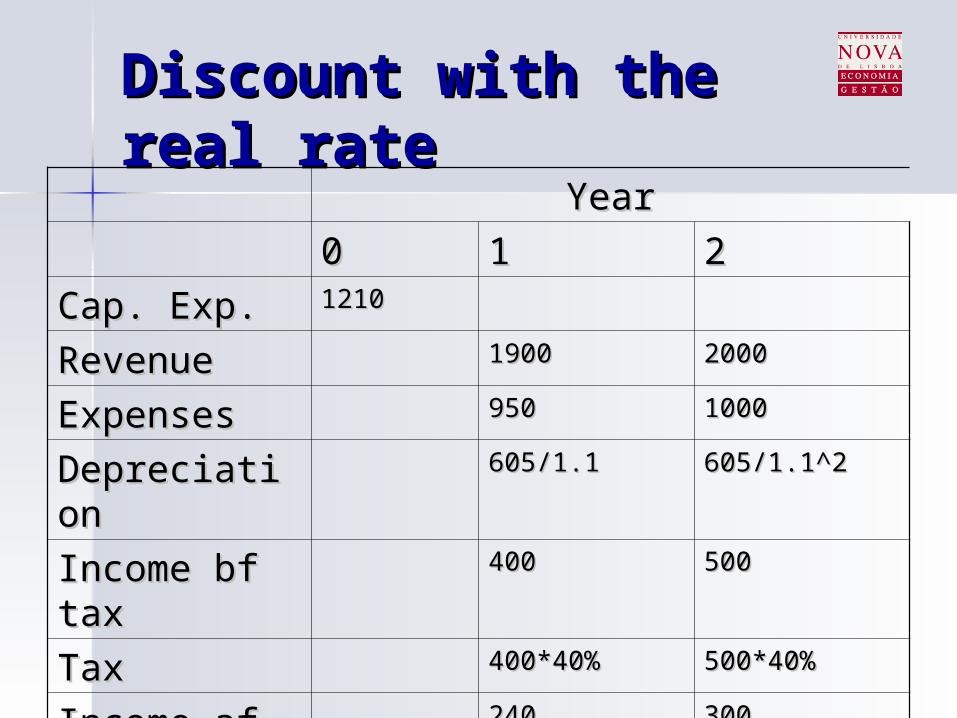

Discount with the real Discount with the real raterate

YearYear

00 11 22

Cap. Exp.Cap. Exp. 12101210

RevenueRevenue 19001900 20002000

ExpensesExpenses 950950 10001000

DepreciationDepreciation 605/1.1605/1.1 605/1.1^2605/1.1^2

Income bf Income bf taxtax

400400 500500

TaxTax 400*40%400*40% 500*40%500*40%

Income af Income af taxtax

240240 300300

NCFNCF -1210-1210 790790 800800

Real rate=(1+15.5%)/(1+1.10)-1=5%

Discount with the real Discount with the real raterate

YearYear

00 11 22

Cap. Exp.Cap. Exp. 12101210

RevenueRevenue 19001900 20002000

ExpensesExpenses 950950 10001000

DepreciationDepreciation 605/1.1605/1.1 605/1.1^2605/1.1^2

Income bf Income bf taxtax

400400 500500

TaxTax 400*40%400*40% 500*40%500*40%

Income af Income af taxtax

240240 300300

NCFNCF -1210-1210 790790 800800

NPVNPV -1210-1210 790/1.05790/1.05 800/1.05^2800/1.05^2

Discount with the real Discount with the real raterate

YearYear

00 11 22

Cap. Exp.Cap. Exp. 12101210

RevenueRevenue 19001900 20002000

ExpensesExpenses 950950 10001000

DepreciationDepreciation 605/1.1605/1.1 605/1.1^2605/1.1^2

Income bf taxIncome bf tax 400400 500500

TaxTax 400*40%400*40% 500*40%500*40%

Income af taxIncome af tax 240240 300300

NCFNCF -1210-1210 790790 800800

NPVNPV -1210-1210 790/1.05790/1.05 800/1.05^2800/1.05^2

NPV=268NPV=268

Discount with the Discount with the nominal ratenominal rate

YearYear

00 11 22

Cap. Exp.Cap. Exp. 12101210

RevenueRevenue 1900*1.11900*1.1 2000*1.1^22000*1.1^2

ExpensesExpenses 950*1.1950*1.1 1000*1.1^21000*1.1^2

DepreciationDepreciation

Income bf Income bf taxtax

TaxTax

Income af Income af taxtax

NCFNCF

Discount with the Discount with the nominal ratenominal rate

YearYear

00 11 22

Cap. Exp.Cap. Exp. 12101210

RevenueRevenue 1900*1.11900*1.1 2000*1.1^22000*1.1^2

ExpensesExpenses 950*1.1950*1.1 1000*1.1^21000*1.1^2

DepreciationDepreciation 605605 605605

Income bf Income bf taxtax

TaxTax

Income af Income af taxtax

NCFNCF

Discount with the Discount with the nominal ratenominal rate

YearYear

00 11 22

Cap. Exp.Cap. Exp. 12101210

RevenueRevenue 1900*1.11900*1.1 2000*1.1^22000*1.1^2

ExpensesExpenses 950*1.1950*1.1 1000*1.1^21000*1.1^2

DepreciationDepreciation 605605 605605

Income bf Income bf taxtax

440440 605605

TaxTax

Income af Income af taxtax

NCFNCF

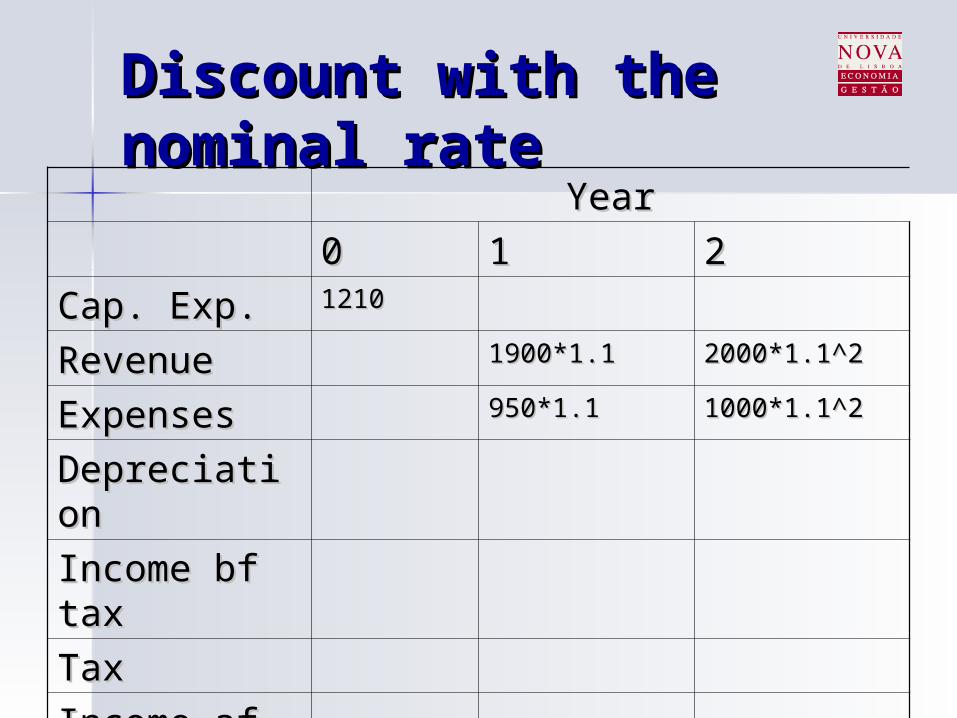

Discount with the Discount with the nominal ratenominal rate

YearYear

00 11 22

Cap. Exp.Cap. Exp. 12101210

RevenueRevenue 1900*1.11900*1.1 2000*1.1^22000*1.1^2

ExpensesExpenses 950*1.1950*1.1 1000*1.1^21000*1.1^2

DepreciationDepreciation 605605 605605

Income bf Income bf taxtax

440440 605605

TaxTax 440*40%440*40% 605*40%605*40%

Income af Income af taxtax

NCFNCF

Discount with the Discount with the nominal ratenominal rate

YearYear

00 11 22

Cap. Exp.Cap. Exp. 12101210

RevenueRevenue 1900*1.11900*1.1 2000*1.1^22000*1.1^2

ExpensesExpenses 950*1.1950*1.1 1000*1.1^21000*1.1^2

DepreciationDepreciation 605605 605605

Income bf Income bf taxtax

440440 605605

TaxTax 440*40%440*40% 605*40%605*40%

Income af Income af taxtax

264264 363363

NCFNCF

Discount with the Discount with the nominal ratenominal rate

YearYear

00 11 22

Cap. Exp.Cap. Exp. 12101210

RevenueRevenue 1900*1.11900*1.1 2000*1.1^22000*1.1^2

ExpensesExpenses 950*1.1950*1.1 1000*1.1^21000*1.1^2

DepreciationDepreciation 605605 605605

Income bf Income bf taxtax

440440 605605

TaxTax 440*40%440*40% 605*40%605*40%

Income af Income af taxtax

264264 363363

NCFNCF -1210-1210 869869 968968

Discount with the Discount with the nominal ratenominal rate

YearYear

00 11 22

Cap. Exp.Cap. Exp. 12101210

RevenueRevenue 1900*1.11900*1.1 2000*1.1^22000*1.1^2

ExpensesExpenses 950*1.1950*1.1 1000*1.1^21000*1.1^2

DepreciationDepreciation 605605 605605

Income bf Income bf taxtax

440440 605605

TaxTax 440*40%440*40% 605*40%605*40%

Income af Income af taxtax

264264 363363

NCFNCF -1210-1210 869869 968968

NPVNPV -1210-1210 869/1.155869/1.155 968/1.155^2968/1.155^2

Discount with the Discount with the nominal ratenominal rate

YearYear

00 11 22Cap. Exp.Cap. Exp. 12101210

RevenueRevenue 1900*1.11900*1.1 2000*1.1^22000*1.1^2

ExpensesExpenses 950*1.1950*1.1 1000*1.1^21000*1.1^2

DepreciationDepreciation 605605 605605

Income bf taxIncome bf tax 440440 605605

TaxTax 440*40%440*40% 605*40%605*40%

Income af taxIncome af tax 264264 363363

NCFNCF -1210-1210 869869 968968

NPVNPV -1210-1210 869/1.155869/1.155 968/1.155^2968/1.155^2

NPV=268NPV=268

Investments of Investments of unequal livesunequal lives So far, the NPV rule has been our So far, the NPV rule has been our

rule-of-thumb.rule-of-thumb. However, there are situations However, there are situations

when the NPV rule is not when the NPV rule is not sufficient. sufficient.

E.g. when investments under E.g. when investments under decision have different lengths of decision have different lengths of life.life.

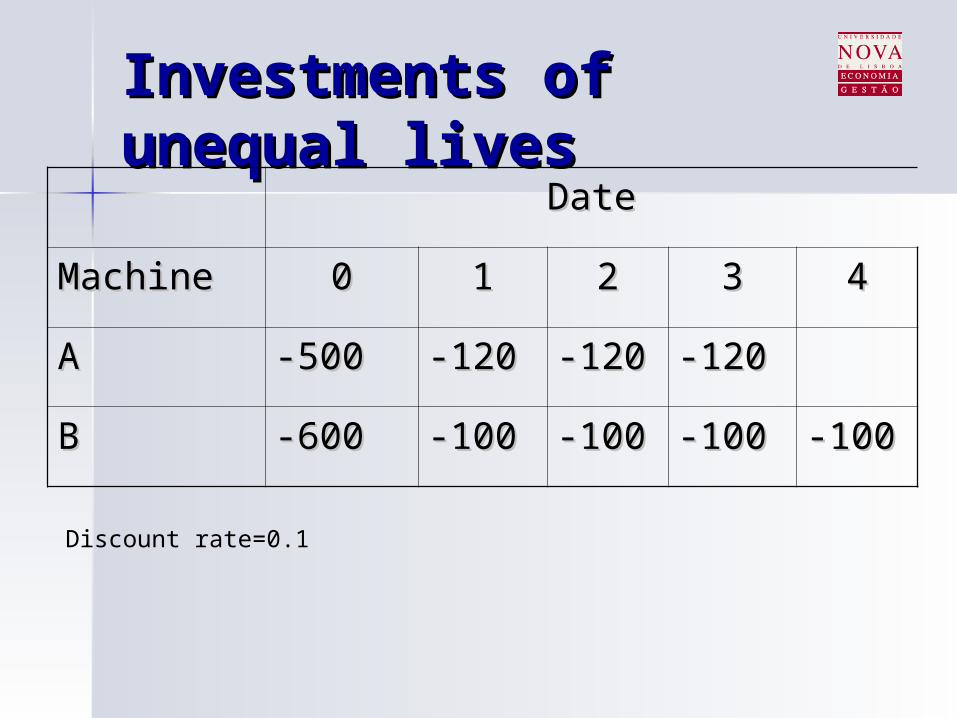

Investments of Investments of unequal livesunequal lives

DateDate

MachineMachine 00 11 22 33 44

AA -500-500 -120-120 -120-120 -120-120

BB -600-600 -100-100 -100-100 -100-100 -100-100

Discount rate=0.1

Investments of Investments of unequal livesunequal lives

DateDate

MachinMachinee

00 11 22 33 44

AA --500500

-120-120 -120-120 -120-120

NPV ANPV A

BB --600600

-100-100 -100-100 -100-100 -100-100

NPV BNPV B

Investments of Investments of unequal livesunequal lives

DateDate

MachinMachinee

00 11 22 33 44

AA --500500

-120-120 -120-120 -120-120

NPV ANPV A -500-500 --120/1.1120/1.1

--120/1.1^2120/1.1^2

--120/1.1^3120/1.1^3

BB --600600

-100-100 -100-100 -100-100 -100-100

NPV BNPV B

Investments of Investments of unequal livesunequal lives

DateDate

MachinMachinee

00 11 22 33 44

AA -500-500 -120-120 -120-120 -120-120

NPV ANPV A -500-500 --120/1.1120/1.1

--120/1.1^2120/1.1^2

--120/1.1^3120/1.1^3

NPV ANPV A --798.42798.42

BB -600-600 -100-100 -100-100 -100-100 -100-100

NPV BNPV B

Investments of Investments of unequal livesunequal lives

DateDate

MachinMachinee

00 11 22 33 44

AA -500-500 -120-120 -120-120 -120-120

NPV ANPV A -500-500 --120/1.1120/1.1

--120/1.1^2120/1.1^2

--120/1.1^3120/1.1^3

NPV ANPV A --798.42798.42

BB -600-600 -100-100 -100-100 -100-100 -100-100

NPV BNPV B -600-600 --100/1.1100/1.1

--100/1.1^2100/1.1^2

--100/1.1^3100/1.1^3

--100/1.1^4100/1.1^4

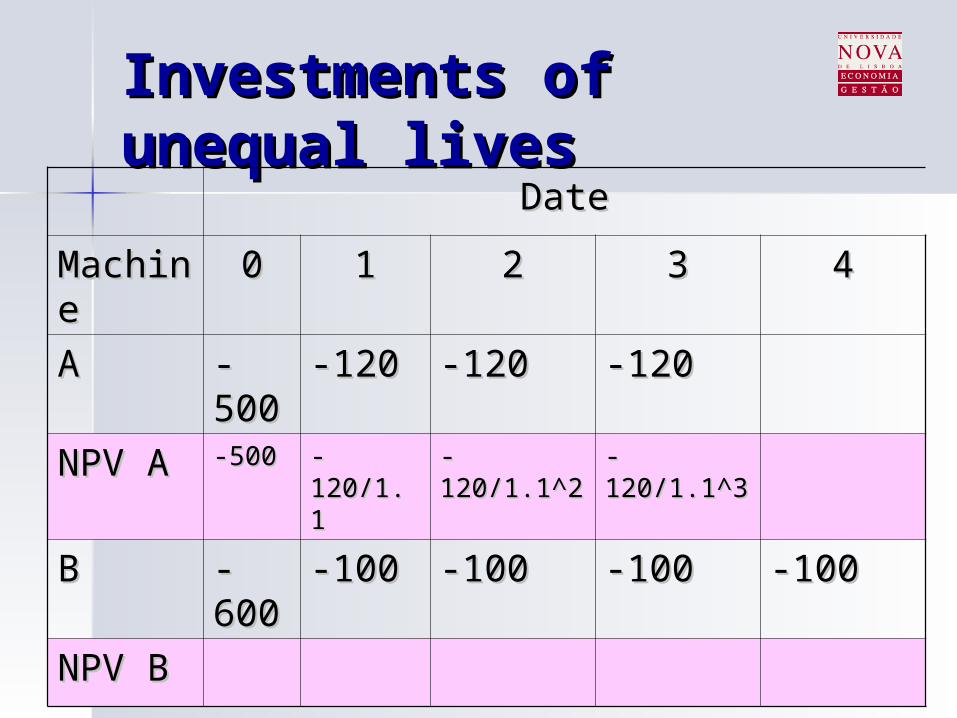

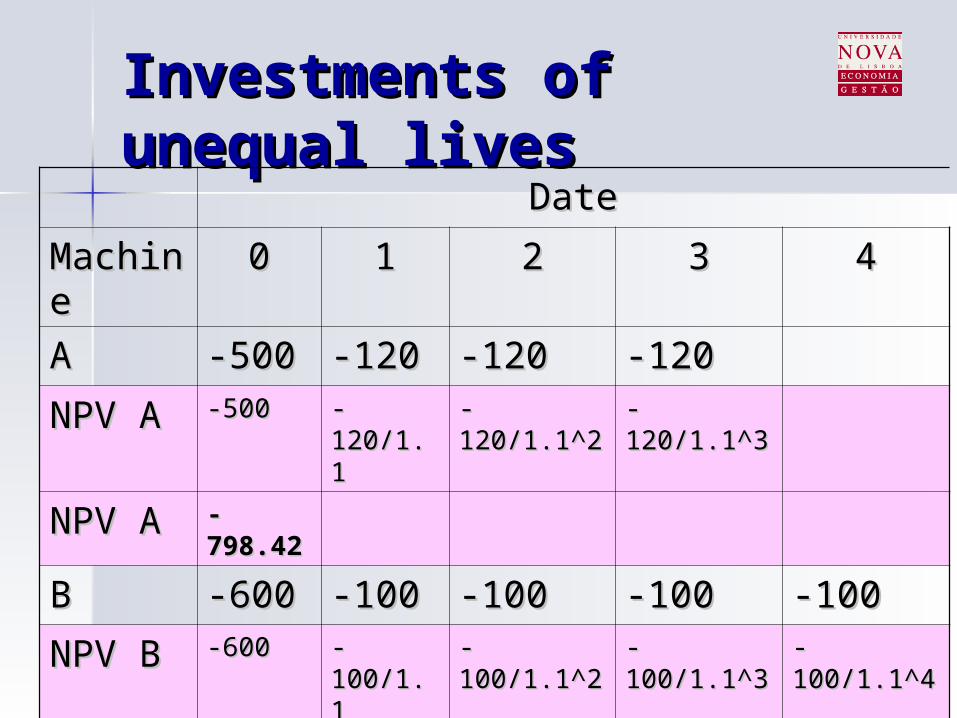

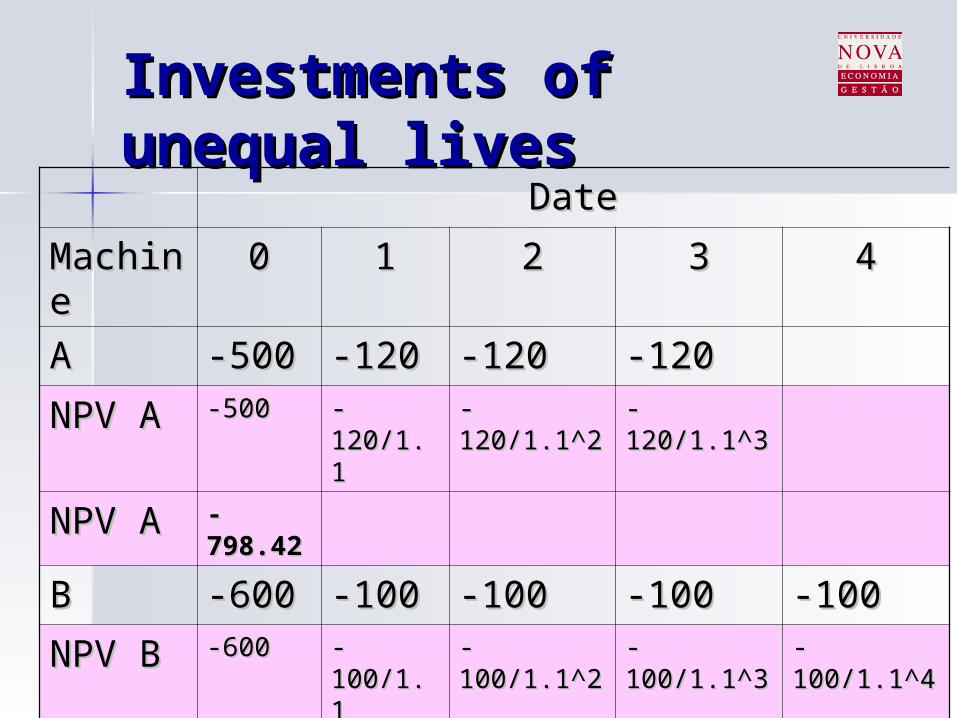

Investments of Investments of unequal livesunequal lives

DateDate

MachinMachinee

00 11 22 33 44

AA -500-500 -120-120 -120-120 -120-120

NPV ANPV A -500-500 --120/1.1120/1.1

--120/1.1^2120/1.1^2

--120/1.1^3120/1.1^3

NPV ANPV A --798.42798.42

BB -600-600 -100-100 -100-100 -100-100 -100-100

NPV BNPV B -600-600 --100/1.1100/1.1

--100/1.1^2100/1.1^2

--100/1.1^3100/1.1^3

--100/1.1^4100/1.1^4

NPV BNPV B --916.99916.99

Investments of Investments of unequal livesunequal lives

DateDate

MachiMachinene

00 11 22 33 44

AA -500-500 -120-120 -120-120 -120-120

NPV ANPV A -500-500 --120/1.1120/1.1

--120/1.1^2120/1.1^2

--120/1.1^3120/1.1^3

NPV ANPV A --798.42798.42

BB -600-600 -100-100 -100-100 -100-100 -100-100

NPV BNPV B -600-600 --100/1.1100/1.1

--100/1.1^2100/1.1^2

--100/1.1^3100/1.1^3

--100/1.1^4100/1.1^4

NPV BNPV B --916.99916.99

NPV rule will suggest Machine A because it has a lower NPV of costs……But, is this correct?

Investments of Investments of unequal livesunequal lives The NPV rule does not consider the The NPV rule does not consider the

time that each machine will last. time that each machine will last. – Machine A is cheaper but only last for Machine A is cheaper but only last for

three years.three years.– Machine B is more costly but last for Machine B is more costly but last for

one more year. one more year. Therefore, it is necessary to Therefore, it is necessary to

compare the cost on a compare the cost on a per yearper year basis.basis.

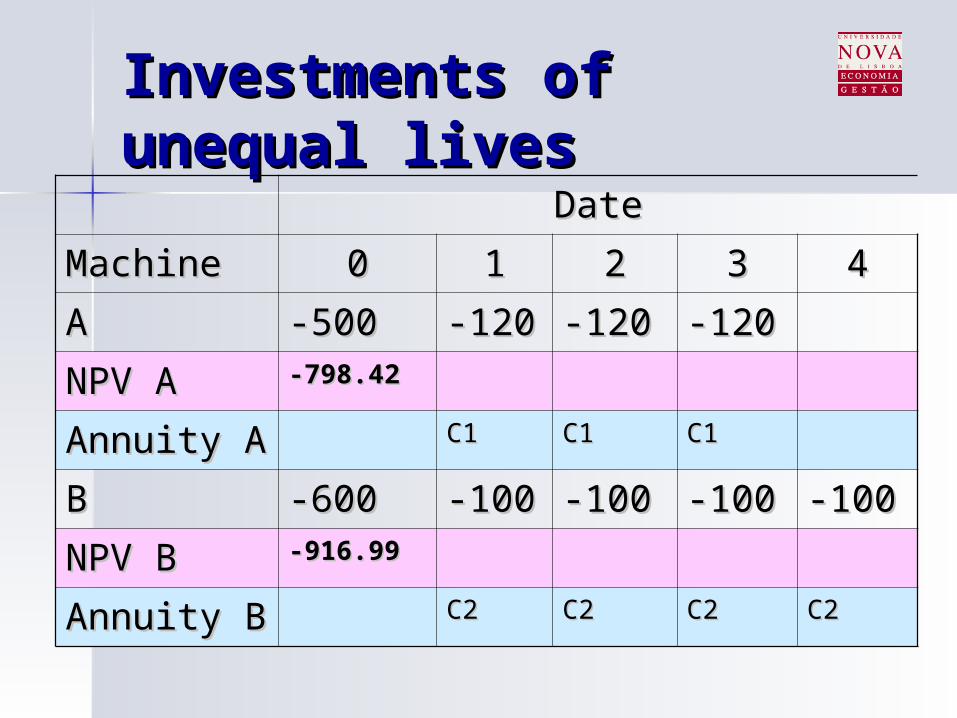

Investments of Investments of unequal livesunequal lives

DateDate

MachineMachine 00 11 22 33 44

AA -500-500 -120-120 -120-120 -120-120

NPV ANPV A -798.42-798.42

Annuity AAnnuity A C1C1 C1C1 C1C1

BB -600-600 -100-100 -100-100 -100-100 -100-100

NPV BNPV B -916.99-916.99

Annuity BAnnuity B C2C2 C2C2 C2C2 C2C2

Investments of Investments of unequal livesunequal lives Annuity Annuity A: A: 798.42=C1*798.42=C1*

C1=798/2.4869=321.05C1=798/2.4869=321.05

B: 916.99=C2*B: 916.99=C2*

C2=916.99/3.1699=289.28C2=916.99/3.1699=289.28

C1>C2, it is cheaper to buy machine C1>C2, it is cheaper to buy machine BB

410.0A

310.0A