Embed Size (px)

Citation preview

`

Copyright

by

John DeCiucis Adamo

2018

`

The Thesis Committee for John DeCiucis Adamo

Certifies that this is the approved version of the following thesis:

On the Sustainability of Liquefied Natural Gas (LNG) as a Marine Fuel

in a Post-International Maritime Organization (IMO) 0.5% Sulfur Cap

Environment

APPROVED BY

SUPERVISING COMMITTEE:

Fred C. Beach, Supervisor

John C. Butler, Co-Supervisor

Richard J. Chuchla

`

On the Sustainability of Liquefied Natural Gas (LNG) as a Marine Fuel

in a Post-International Maritime Organization (IMO) 0.5% Sulfur Cap

Environment

by

John DeCiucis Adamo

Thesis

Presented to the Faculty of the Graduate School of

The University of Texas at Austin

in Partial Fulfillment

of the Requirements

for the Degrees of

Master of Science in Energy and Earth Resources

And

Master of Business Administration

The University of Texas at Austin

May 2018

iv

Acknowledgements

I would like to acknowledge my Thesis Committee, Dr. Fred Beach, Dr. John Butler,

and Mr. Richard Chuchla, for their enthusiasm and support during the research, analysis, and

writing phases of this thesis. I would like to thank my professors and peers in the McCombs

School of Business Full-Time MBA Program and the Jackson School of Geosciences Energy

and Earth Resources Program who have pushed me to become a better leader and energy

professional. I would like to thank all industry professionals in the shipping and LNG

communities who helped me understand the incredible opportunity for LNG to reduce long-

run operational costs and environmental impacts in the maritime industry. Lastly, I would like

to thank my incredible wife for her patience and encouragement not only during the writing

of this thesis but throughout the entire journey of graduate school.

v

Abstract

On the Sustainability of Liquefied Natural Gas (LNG) as a Marine Fuel

in a Post-International Maritime Organization (IMO) 0.5% Sulfur Cap

Environment

John DeCiucis Adamo, MSEER; MBA

The University of Texas at Austin, 2018

Supervisors: Fred C. Beach and John C. Butler

The International Maritime Organization (IMO), the leading regulatory body for the shipping

industry, recently finalized its decision to decrease the global sulfur cap for marine bunker

fuels from 3.5% to 0.5% effective January 2020 to reduce the shipping community’s

environmental impact. This decision will have significant impacts on shipowners, forcing

them to choose among a suite of options to comply with the new emissions limit, options with

substantial capital expenditure (CAPEX) or operational expenditure (OPEX) implications.

Among these options is using liquefied natural gas (LNG) as an alternative to low-sulfur fuel

oil or distillates and exhaust gas cleaning systems (EGCS). While LNG has been used in a

limited capacity as a marine fuel, mostly in passenger vessels (ferries) and LNG carriers from

the boil-off gas (BOG) in storage tanks, there are currently only 119 LNG-capable ships

operating globally (out of a merchant fleet of over 50,000). LNG fuel can effectively eliminate

nearly 100% of sulfur oxide (SOx) and particulate matter (PM) emissions, while reducing

nitrogen oxide (NOx) emissions up to 80% and greenhouse gas (GHG) emissions by up to

30%. LNG is also price competitive with other bunker fuel, making it an attractive alternative

both environmentally and economically.

vi

This thesis examines the business case for LNG-capable ships as a viable option to

meet the IMO’s sulfur cap. Specifically, the thesis compares the choice to invest in an LNG-

capable ship to investing in EGCS (enabling continued use of high-sulfur fuel oil) or using

compliant low-sulfur fuel oil or distillates (which still requires selective catalytic reduction

(SCR) or exhaust gas recirculation (EGR) systems to comply with NOx limits). The thesis

analyzes eight different vessel types across the three investment options and considers three

different fuel price scenarios, accounting for variation in CAPEX, OPEX, engine types, ship

utilization, and charter rates, for a total of 96 scenarios. Each scenario uses a discounted cash

flow (DCF) model to yield unique NPV, IRR, and payback for the investment. The thesis

demonstrates that LNG-capable vessels are competitive investments and, in some cases,

outperform other options to achieve compliance with SOx and NOx emissions limits.

vii

Table of Contents

List of Tables ....................................................................................................................................... ix List of Figures ....................................................................................................................................... x Chapter 1 – Introduction .................................................................................................................... 1

The LNG Industry .................................................................................................................... 1 What is Liquefied Natural Gas? ..................................................................................... 1

LNG Roles In Shipping ............................................................................................................ 1 IMO Emissions Rulings ............................................................................................................ 1 Thesis Statement ........................................................................................................................ 6

Chapter 2 – State of the LNG Industry ............................................................................................ 7 Macro-Level Supply & Demand Analysis .............................................................................. 7 Liquefaction And Regasification Capacity – Current & Projected ..................................... 9 LNG Prices ............................................................................................................................... 19

LNG Contract Structures ............................................................................................. 19 Effects of Liquidity on LNG Contracts and Pricing Structures ............................. 20 LNG Bunker Prices ....................................................................................................... 23

LNG Use As A Marine Fuel .................................................................................................. 23 Dual-Fuel and Gas Engine Technology Development............................................ 23 LNG Fuel Systems and Storage .................................................................................. 26 Environmental Benefits of LNG Fuel ....................................................................... 28

Chapter 3 – The Role of LNG as a Marine Fuel ........................................................................... 32 LNG-Fueled Ships – Current & Projected .......................................................................... 32

Examples of Company-Level Pursuit of LNG-Capable Ships ............................... 35 Financing Structures for LNG-Capable Ships and Other Emissions

Reductions Measures .......................................................................................... 39 Types Of Marine Fuels – Historical And Forecasted Volumes & Prices ........................ 41 The Chicken or The Egg – LNG Bunkering Networks .................................................... 47

Status of LNG Bunkering Networks .......................................................................... 48 Types of LNG Bunkering Solutions ........................................................................... 49 Regulatory and Safety Considerations for LNG Bunkering .................................... 52

Methods To Achieve IMO Sulfur Cap Compliance ........................................................... 55 Chapter 4 – The Business Case for LNG-Capable Ships ............................................................ 61

Methodology And Assumptions ............................................................................................ 61 Methodology .................................................................................................................. 61 Key Assumptions ........................................................................................................... 63

Results ........................................................................................................................................ 71 Base Case ........................................................................................................................ 73 EIA Case ......................................................................................................................... 73 Dynamic Case ................................................................................................................. 73

Sensitivity Analysis ................................................................................................................... 74 Base Case ........................................................................................................................ 76 EIA Case ......................................................................................................................... 76

viii

Dynamic Case ................................................................................................................. 76 Alternative Methodology ........................................................................................................ 78

Base Case ........................................................................................................................ 80 EIA Case ......................................................................................................................... 80 Dynamic Case ................................................................................................................. 80

Sensitivity Analysis ................................................................................................................... 80 Base Case ........................................................................................................................ 82 EIA Case ......................................................................................................................... 82 Dynamic Case ................................................................................................................. 82

Non-Compliance Considerations .......................................................................................... 84 Chapter 5 – Conclusion .................................................................................................................... 88

Summary Of Results ................................................................................................................ 88 Note on Assumptions, Shortfalls, & Areas Of Further Research .................................... 88

Appendices .......................................................................................................................................... 90 Appendix 1 – Assumptions and Model Control Page ........................................................ 90 Appendix 2 – Cost of Capital Analysis ................................................................................. 91 Appendix 3 – Price Decks ...................................................................................................... 93 Appendix 4 – Price Regression Analysis .............................................................................. 94 Appendix 5 – Business Case Analysis DCF ......................................................................... 95 Appendix 6 – Calorific Values & Conversion Factors ....................................................... 96 Appendix 7 – Fuel Cost Savings Methodology ................................................................... 97 Appendix 8 – @Risk Output Summary for Business Case Analysis DCF ..................... 98 Appendix 9 - @Risk Output Summary for Fuel Cost Savings and Net Payback to

LS Fuel Analysis ........................................................................................................... 101 Glossary ............................................................................................................................................. 103 References ......................................................................................................................................... 105

ix

List of Tables

Table 1: Summary of LNG Import and Export Terminal Capacity in North America (in

MTPA) ......................................................................................................................... 16 Table 2: Global Average LNG Netback Pricing Analysis .......................................................... 22 Table 3: LNG Bunker Pricing Estimate Based on Henry Hub ................................................. 23 Table 4: Otto and Diesel Cycle Features ....................................................................................... 24 Table 5: Gas Engine Technologies ................................................................................................. 24 Table 6: LNG Fuel Tanks Pros and Cons ..................................................................................... 27 Table 7: Environmental Benefits of LNG Fuel ........................................................................... 29 Table 8: GHG Emissions Profiles of Different Marine Fuels ................................................... 31 Table 9: LNG-Capable Newbuilds (Thousands of Gross Tons)............................................... 33 Table 10: Types of Marine Fuels .................................................................................................... 44 Table 11: Average Annual CO2-e Savings between 2018-2030 from Ship Speed Reduction 57 Table 12: Newbuild Prices for Multiple Configurations, $ in millions ..................................... 64 Table 13: Operational Expenses for Multiple Configurations, $ in millions ........................... 65 Table 14: Illustrative Utilization Factor Calculations .................................................................. 66 Table 15: Engine Type and Fuel Consumption Data .................................................................. 67 Table 16: 1-Year Time Charter Rate Equivalents by Vessel Type – 5-year Historical Average,

$/day ............................................................................................................................ 68 Table 17: Adjusted 1-Year Time Charter Rate Equivalents by Vessel Type, $/day ............... 68 Table 18: Illustrative Financing Structure and Cost of Capital Summary ................................ 69 Table 19: End of Useful Life Salvage Value, based on $/ldt ..................................................... 71

x

List of Figures

Figure 1: IMO Projections of CO2 Emissions from Maritime Transportation ......................... 2 Figure 2: Existing and Proposed Emissions Control Areas (ECA) for SOx, NOx, or Both .... 3 Figure 3: IMO Implementation of Fuel Oil Sulfur Limits ............................................................ 4 Figure 4: IMO Implementation of NOx Limits .............................................................................. 5 Figure 5: LNG Supply Forecast by Current Status ........................................................................ 7 Figure 6: LNG Export Capacity by Region 2005-2040 ................................................................. 8 Figure 7: LNG Import Capacity by Region 2005-2040................................................................. 9 Figure 8: Global Liquefaction Capacity and Utilization .............................................................. 10 Figure 9: Global Nominal Liquefaction Capacity as of January 2017 ....................................... 11 Figure 10: Types of Liquefaction Technologies ........................................................................... 12 Figure 11: North American Existing LNG Import/Export Terminals .................................... 13 Figure 12: North American Approved LNG Import/Export Terminals ................................ 14 Figure 13: North American Proposed LNG Export Terminals ................................................ 15 Figure 14: Major LNG Flows in 2016 ........................................................................................... 17 Figure 15: Global Receiving Terminal (Regasification) Capacity ............................................... 18 Figure 16: Regasification Terminal Import Capacity and Utilization Rate in 2016 and 2022 19 Figure 17: Duration of Sales and Purchase Agreements (SPAs) for LNG .............................. 20 Figure 18: LNG Landed Prices on a Netback Basis, January 2018, $/MMBtu ....................... 22 Figure 19: Number of World Merchant Fleet Ships .................................................................... 32 Figure 20: Number of Contracts and % LNG Newbuilds ......................................................... 34 Figure 21: LNG-capable ships by vessel type ............................................................................... 35 Figure 22: Marine Fuel Consumption, 2012 (MTPA) ................................................................. 41 Figure 23: Marine Fuel Consumption by Ship Type, 2012 ......................................................... 42 Figure 24: Merchant Fleet Vessel Types and Fuel Consumption, 2016 ................................... 43 Figure 25: LNG Bunker Fuel Demand at 2020 ............................................................................ 45 Figure 26: Historical Fuel Oil Prices against Oil and Natural Gas Hub Prices, $/MMBtu ... 46 Figure 27: LNG Bunkering Ports, Existing and Planned ........................................................... 48 Figure 28: LNG Supply Locations: In Operation, Decided, Under Discussion .................... 49 Figure 29: LNG Bunkering Solutions ............................................................................................ 50 Figure 30: Types of LNG Bunker Solutions ................................................................................. 52 Figure 31: CO2 Emissions Reduction Pathway 2015-2025 ......................................................... 58 Figure 32: Most Likely Pathways to Meet SOx (and NOx) Emissions Requirements ............. 59 Figure 33: Comparison of Scrubber and LNG Investments ...................................................... 60 Figure 34: Illustrative Business Case Analysis Framework w/ Key Assumptions .................. 62 Figure 35: Business Case Analysis Results for All Vessel Types and Price Scenarios ............ 72 Figure 36: Business Case Analysis Results at 50% ECA Time................................................... 75 Figure 37: Business Case Analysis Results at 100% ECA Time ................................................ 77 Figure 38: Investment Costs Results for All Vessel Types and Price Decks ........................... 79 Figure 39: Investment Costs Results at 50% ECA Time ............................................................ 81 Figure 40: Investment Costs Results at 100% ECA Time .......................................................... 83 Figure 41: Effect of Non-Compliance Penalty of $25,000/day and 100% ECA Time ......... 85

xi

Figure 42: Effect of Non-Compliance Penalty of $5,000/day and 100% ECA time ............. 87

1

Chapter 1 – Introduction

THE LNG INDUSTRY

What is Liquefied Natural Gas?

Liquefied Natural Gas (LNG) is natural gas in liquid form. To achieve this phase change,

natural gas must be cooled to -161°C (or approximately -260°F), resulting in a volume change

of approximately 600x. This allows natural gas to be more easily transported, typically by truck

or ship, to an import terminal where it is re-gasified and released into the pipeline network for

distribution. LNG is colorless and odorless and is only flammable when it reaches

concentrations between 4.5% and 16.5% in air; auto-ignition is extraordinarily rare, as a

temperature of 537°C is needed for that to occur (Foss 2012). In short, LNG is really a

competitor to the compressed natural gas (CNG) distributed through overland pipeline

networks.

LNG ROLES IN SHIPPING

LNG fuel historically has had a limited role in the shipping community. LNG carriers (the

vessels that transport LNG) have used LNG to power their propulsion systems, either fully

or in part though boil off gas (BOG). Non-LNG carriers have been slow to adopt LNG as a

fuel due to the technical challenges and additional cost of a dual-fuel ship with LNG capability

as well as the limited LNG bunkering networks (i.e. the storage and distribution systems of

the actual LNG bunker, or fuel) that currently exist. However, this is rapidly changing as the

maritime industry seeks less polluting alternatives to fuel oil.

IMO EMISSIONS RULINGS

The International Maritime Organization (IMO) is the leading regulatory body for the shipping

industry. It is responsible for setting standards related to ship design, safety, efficiency, and

environmental impacts. Just as the power sector has come under increasingly stringent

emissions standards, particularly related to sulfur oxides (SOx) and nitrogen oxides (NOx) but

2

also more recently with greenhouse gas emissions (GHG), the shipping industry is also

experiencing increasing attention on emissions. Figure 1 shows the projections of carbon

(CO2) emissions in multiple scenarios.

Figure 1: IMO Projections of CO2 Emissions from Maritime Transportation

(Source: Cames et al. 2015, p. 23)

Notwithstanding the projected increase of shipping-related carbon dioxide emissions, an

important greenhouse gas, from approximately 2.8% to over 10% of global CO2 emissions by

2050 (Wiseman 2016), the focus of the shipping community has been on reduction of SOx

and NOx in emission control areas (ECAs) to reduce pollution. As shown in in Figures 2 and

3, the IMO has instituted increasingly strict emissions standards on sulfur at a global scale

prompting the need for continual reduction in the sulfur content of fuel oils or increased

3

access to alternative fuels such as LNG to meet the new deadline of less than 0.5% sulfur by

2020 (MARPOL Annex VI Regulation 14).

Figure 2: Existing and Proposed Emissions Control Areas (ECA) for SOx, NOx, or Both

(Source: World Ocean Review 2015)

Even China is considering implementing ECAs in certain port areas in Pearl River Delta

(Hong Kong/Shenzhen and surrounding areas), the Yangtze River Delta (Shanghai and

surrounding areas) and Bohai Bay (Tianjin and surrounding areas). These ECAs are designated

by Chinese law only and are not part of the IMO’s MARPOL1 Annex VI designated areas. By

January 2019, all vessels operating within an ECA must use a fuel with a maximum sulfur

content of 0.5% (in alignment with the IMO). However, after 2020, Chinese authorities will

evaluate both the size of the ECAs and the potential benefits of 0.1% sulfur fuel or other

emissions reductions initiatives (NEPIA 2016).

1 MARPOL is the International Convention for the Prevention of Pollution from Ships

4

Figure 3: IMO Implementation of Fuel Oil Sulfur Limits

(Source: Lloyd’s Marine Register 2015, p. 6)

The IMO has also passed increasingly strict limitations on NOx emissions (MARPOL Annex

VI Regulation 13). As shown in Figure 4, Tier I and II limits apply globally and became

effective in 2000 and 2011, respectively, while Tier III limits apply only to vessels built after

January 1, 2016 and operate within North America and the Caribbean ECAs (Lloyd’s Marine

Register, April 2015, p. 8). Europe’s North Sea and Baltic Sea regions could also see

application of the Tier III limits by 2021 (DNV GL November 2017b, p. 4).

5

Figure 4: IMO Implementation of NOx Limits

(Source: DieselNet 2016)

The IMO recently finalized its decision to implement a global sulfur cap of 0.5% on all fuel

oils effective January 1, 2020, down from the 2012 level of 3.5%. The impact of this decision

is far-reaching: not only will low-sulfur distillates likely command an even greater premium

than fuel oil but also the growth of LNG availability could allow LNG capable newbuild ships

to compete. Even retrofitting current ships with exhaust gas cleaning systems (EGCS), which

comes with a significant price tag, is risky as some areas within ECAs neither allow the use of

fuel oil nor make it available in port (and can carry a significant fine if used). Thus, for the

shipowner, the investment in a dual-fuel vessel that is LNG-capable, or at a minimum LNG-

ready, is becoming more attractive.

6

THESIS STATEMENT

LNG as a marine fuel offers the shipowner community a sustainable fueling option that is

both cost effective and environmentally friendly. Given the projected supply of LNG and the

growing bunkering network worldwide, LNG fuel is a promising alternative for the global

shipping community that offers longer-term reduction in operational costs and superior

environmental performance. The following analysis will first review the macro-level trends in

LNG supply and demand, LNG-capable ship development, LNG bunkering solutions, and

marine fuel options; and, then evaluate the business case for using LNG-capable ships versus

other options to comply with emissions regulations. The goal is to determine if LNG-

capability is an attractive investment option, by how much LNG-capable ships could penetrate

the overall merchant fleet, and other factors that might limit larger-scale adoption.

7

Chapter 2 – State of the LNG Industry

MACRO-LEVEL SUPPLY & DEMAND ANALYSIS

At the end of 2016, 267 MTPA (million tonnes per annum) of LNG was traded globally. By

the end of 2017, global LNG supply trade increased to 294 MTPA, an annual growth of just

over 10% (which is faster than this century’s first decade) (IHS Markit December 2017, p. 4).

Further, liquefaction capacity could grow between 200 and 430 MTPA by 2040, to levels

between 470 and 720 MTPA depending on how the demand for natural gas develops (IHS

Markit August 2017, p. 34). As shown in Figure 5, liquefaction capacity is expected to plateau

in the early 2020’s, providing enough supply to meet current demand. However, by 2025, the

spread between supply and demand grows upwards of 250 MTPA by 2040, prompting another

wave of liquefaction projects needed to reach final investment decision (FID) in order to meet

demand in the latter half of the 2020s and into the 2030s.

Figure 5: LNG Supply Forecast by Current Status

(Source: IHS Markit August 2017, p. 53)

8

Another global LNG outlook study by Nexant has similar projections. As shown in Figure 6,

global LNG export capacity will reach about 900 billion standard cubic meters (Bscm), or

approximately 615 MTPA, at roughly 90% utilization to match demand for LNG imports. As

shown in Figure 7, on the import side, LNG regasification capacity could reach 800 Bscm (or

615 MTPA).

Figure 6: LNG Export Capacity by Region 2005-2040

(Source: Nexant 2017, p. 25)

9

Figure 7: LNG Import Capacity by Region 2005-2040

(Source: Nexant 2017, p. 24)

LIQUEFACTION AND REGASIFICATION CAPACITY – CURRENT & PROJECTED

According to Figure 8, nominal liquefaction capacity reached just under 340 MTPA in January

2017, with utilizations remaining well above 80%. Another 115 MTPA is under construction,

with most of that in the United States (57.6 MTPA) and Australia (31.1 MTPA). Liquefaction

capacity is expected to grow 35% by 2022 (IGU World LNG Report 2017).

10

Figure 8: Global Liquefaction Capacity and Utilization

(Source: IGU World LNG Report 2017, p. 20)

As shown in Figure 9, the two dominant LNG exporters are Qatar and Australia by significant

margins, with Algeria, Nigeria, Indonesia, and Malaysia in the next bracket of exporters. Russia

and the United States are currently marginal LNG exporters, but both plan to bring online

significant LNG export capacity. Russia will still deliver natural gas predominantly by pipeline,

but given competition from US and African LNG, it will leverage recent projects like Yamal

LNG to continue to put downward price pressure to compete with non-Russian LNG

imports. The United States is poised to bring on substantial capacity by the early 2020s, and,

as described in subsequent paragraphs, there could be up to four LNG export terminals in

operation in the US by the end of 2018. By 2020, the US will join Qatar and Australia as the

three dominant LNG exporters.

11

Figure 9: Global Nominal Liquefaction Capacity as of January 2017

(Source: IGU World LNG Report 2017, p. 21)

While the details of the liquefaction process are not the focus of this thesis, it is worth

mentioning the main technologies used to liquefy natural gas. As shown in Figure 10, there

are essentially two dominant technologies. First, Air Products C3MR, X, and C3MR/Split

MR processes account for nearly 80% of current liquefaction plants and 60% of the 115

MTPA under construction. Second, ConocoPhillips (CP) Optimized Cascade process

accounts for roughly 20% of current liquefaction plants but could see that market share grow

to about 30% (IGU World LNG Report 2017, p. 23). The AP C3MR process pre-cools natural

gas using propane and mixed refrigerants (MR) then utilizes a proprietary heat exchanger

technology in combination with other system components, which maximizes cooling

efficiency and offers economies of scale for large-scale liquefaction plants. On the other hand,

CP’s Cascade Process utilizes a proprietary step-down cooling process with a pure refrigerant

and compressors. This process is generally less capital intensive but not as efficient; it also

can have additional maintenance or other OPEX increases associated with the step-down

cooling components (Tusiani and Shearer 2016, pp. 320-324).

12

Figure 10: Types of Liquefaction Technologies

(Source: IGU World LNG Report 2017, p. 22)

North America, but particularly US, liquefaction capacity is projected to substantially increase

by the middle of next decade. As shown is Figure 11, there are currently 12 LNG import

terminals in the US (total of 18.835 billion cubic feet per day (Bcfd) or approximately 150

MTPA), 1 in Canada (1.0 Bcfd or approximately 8 MTPA), and 3 in Mexico (2.2 Bcfd or 17.5

MTPA). As of January 2018, there are 2 LNG export terminals operational with a total

capacity of 3 Bcfd (or approximately 24 MTPA).

13

Figure 11: North American Existing LNG Import/Export Terminals

(Source: FERC 2018)

There are also several approved import and export projects in the queue in North America.

As shown in Figure 12, there are 4 approved import terminals with a total capacity of 3.4 Bcfd

(or approximately 27 MTPA). In the US, there are 10 export terminals that have been

approved – 6 under construction with a total capacity of 8.95 Bcfd (or approximately 71.6

MTPA) and 4 not yet under construction with a total capacity of 6.79 Bcfd (or approximately

54.32 MTPA). Canada also has 4 approved export terminals not yet under construction with

a total capacity of 6.76 Bcfd (or approximately 54.08 MTPA).

14

Figure 12: North American Approved LNG Import/Export Terminals

(Source: FERC 2018)

Finally, as shown in Figure 13, there are 15 proposed LNG export terminals in the US, with

12 pending applications with FERC with a total capacity 21.782 Bcfd (or approximately 174.3

MTPA), 3 projects in pre-filing with FERC with a total capacity of 3.69 Bcfd (or approximately

29.5 MTPA), and 1 project proposed to the US Coast Guard (USCG)/US Department of

Transportation Maritime Administration (MARAD) with a total capacity of 1.8 Bcfd (or 14.4

MTPA). In western Canada, there are 2 proposed export terminals with a total capacity of

1.51 Bcfd (or approximately 12 MTPA).

15

Figure 13: North American Proposed LNG Export Terminals

(Source: FERC 2018)

The US is clearly trying to capitalize on the shale revolution by finding new markets for its

abundant gas resources, becoming a net exporter of natural gas and joining Australia and Qatar

as the top three players in the global LNG market. See Table 1 for a summary of North

American existing, approved, and proposed LNG facilities. To put US LNG export/import

capacity in the context of global gas markets, even if all this capacity was built it would

represent just a fraction of US and global natural gas demand. In 2016, global gas demand

was approximately 123,820 Bcf, or 339.23 Bcfd (IHS Markit August 2017, p. 25), with the US

at 74.22 Bcfd (EIA March 2018). Even if all the approved export facilities were brought

online, US LNG export nominal capacity would only amount to approximately 18.74 Bcfd,

with less than 10 Bcfd actually exported based on current utilization rates of 50%. With global

16

gas demand projected to increase to nearly 200,000 Bcf by 2040 (IHS Markit August 2017, p.

25), US LNG exports still represent a small fraction of overall gas demand.

Country Existing

Approved Proposed

Total Under

Construction

Not Under

Construction

FERC -

Pending

FERC

Pre-Filing

USCG /

MARAD

United

States

Import 150 3.2 24 -- -- -- 177.2

Export 24 71.6 54.32 174.3 29.5 14.4 368.12

Canada

Import 8 -- -- -- -- -- 8

Export -- -- 54.08 12 -- -- 66.08

Mexico

Import 17.5 -- -- -- -- -- 17.5

Export -- -- -- -- -- -- --

Total

Import 175.5 3.2 24 -- -- -- 202.7

Export 24 71.6 108.4 186.3 29.5 14.4 434.2

Table 1: Summary of LNG Import and Export Terminal Capacity in North America (in

MTPA)

(Source: FERC 2018)

The US is still in its infancy of exporting LNG, with Cheniere Energy’s Sabine Pass the only

operational exporter as of the end of 2017. As shown in Figure 14, much of global LNG trade

flows from Australia and Qatar, with Indonesia, Malaysia, and Russia distant seconds. Most

LNG is imported by China, India, Japan, and Korea, as well as Taiwan and the UK, countries

that either have poorly developed or no indigenous natural gas resources.

17

Figure 14: Major LNG Flows in 2016

(Source: GIIGNL 2017, p. 4)

As shown in Figure 15, global regasification capacity reached nearly 800 MTPA in January

2017; however, given that less 300 MTPA of LNG traded in 2017, receiving terminal

utilization remains under 40% as LNG continues to compete with pipeline gas. In addition,

although 82% of regasification facilities are currently located onshore, floating LNG (FLNG)

and floating storage and regasification units (FSRU) are becoming more attractive options to

18

receive LNG, as they have lower CAPEX and more flexibility to receive, reposition, and

distribute gas when needed (IGU World LNG Report 2017, pp. 46-52).

Figure 15: Global Receiving Terminal (Regasification) Capacity

(Source: IGU World LNG Report 2017, p. 46)

As shown in Figure 16, the two largest importers of natural gas are Japan and Korea, with

nearly 200 and 100 MTPA of regasification capacity, respectively, as of January 2017. This

capacity is not expected to be fully utilized, remaining in the 30% to 40% range, unless both

countries experience demand growth for natural gas that is not offset by growth in other

energy sources such as renewables, storage, or nuclear (for Japan). US import capacity will

likely stay somewhat steady, as the country expects to remain a net exporter of natural gas into

the mid-2020s. China and India will nearly double and triple regasification capacity,

respectively, as they look to source cleaner burning natural gas as a replacement for coal-fired

generation plants. These two countries also have higher regasification utilization rates, likely

19

to meet continuously the power demands of the two most populous nations. Lastly, Spain

and the UK will remain around 50 MTPA of capacity through mid-2020s.

Figure 16: Regasification Terminal Import Capacity and Utilization Rate in 2016 and 2022

(Source: IGU World LNG Report 2017, p. 48)

LNG PRICES

LNG Contract Structures

LNG delivered (or landed) prices are derived from a variety of methods, more commonly

based on either an oil-linked or natural gas hub-linked structure. If the former, the price is

based on a percentage of oil price plus the cost of liquefaction and transportation. If the latter,

the price is based on percentage of natural gas hub price plus the cost of liquefaction and

transportation. Some LNG contracts do have a hybrid structure (combining both oil and

natural gas-linked prices), but as natural gas markets, and hence LNG markets, become more

liquid, many contracts are using regional natural gas hub pricing as their basis. Hub-linked

contracts could reach over one-third of all LNG contracts by 2040 (IHS Markit August 2017,

p. 32).

20

Effects of Liquidity on LNG Contracts and Pricing Structures

As the LNG market matures and experiences a potential shift from regional trade activity to

more global trade activity, LNG contracts and pricing structures could change significantly.

For example, most LNG contracts have been on a long-term basis (upwards of 20 years) with

pricing typically reflecting either an oil-linked basis or a regional hub-linked basis. However,

as demonstrated in Figure 17, over the last five years contract duration has shifted to short

and medium-term contracts, with 20 of 30 contracts in 2017 below 5 years in length and an

average contract length of about 7 years. If this trend continues, the market could see short-

term, hub-based-contracts become the norm, particularly if oil prices rise faster than natural

gas prices.

Figure 17: Duration of Sales and Purchase Agreements (SPAs) for LNG

(Source: Poten & Partners January 2018)

21

One of the challenges with hub-based prices is the significant variation across geographies (see

Figure 18 for LNG landed prices on a netback basis2 as of January 2018). While North

America’s Henry Hub (HH), the UK’s National Balancing Point (NBP) and Europe’s Title

Transfer Facility (TTF), and Asia’s Japan-Korea Marker (JKM) are the most prominent

reference points for hub-based pricing, typically on a regional basis, the growing liquidity of

the LNG spot market could potentially create a more global pricing basis. Just as Singapore’s

IFO 380 or IFO 180 act as a global benchmark for fuel oil, the Singapore Exchange (SGX)

LNG benchmark could become a global benchmark for LNG prices. Another option could

be to take a “basket,” or weighted average, of hub prices to determine a global LNG price. A

global benchmark price for LNG likely will not happen until the market reaches a sufficient

level of liquidity, but even then, pricing LNG bunker will likely still be closely related to

regional LNG costs.

2 Netback Basis is defined as the natural gas price at market destinations less the costs of pipeline transportation,

regasification, transportation (shipping) and liquefaction.

22

Figure 18: LNG Landed Prices on a Netback Basis, January 2018, $/MMBtu

(Source: FERC 2018)

As shown in Table 2, since 2012 LNG netbacks have fallen significantly due to a glut in the

LNG market but started to recover in 2017 and are continuing to rise into 2018, a positive

trend for exporters seeking an arbitrage opportunity.

Table 2: Global Average LNG Netback Pricing Analysis

(Source: Bloomberg Intelligence 2018)

23

LNG Bunker Prices

LNG bunker price is a function of several costs associated with the full supply chain, from

natural gas production and procurement, through liquefaction and delivery to the bunkering

source, whether that be a truck, vessel, or storage tank in or near a berthing area. The most

practical way to price LNG bunker is to base it off natural gas hub prices and layer on

subsequent supply chain costs. Table 3 represents a baseline scenario for North American

(and other regions if Henry Hub basis is used) LNG bunker.

LNG Bunker Pricing Estimate (Henry Hub-based), Units in $/MMBtu

Henry Hub Price $3.00

Procurement Charge 15% of Hub ($0.45)

Liquefaction $3.00

Storage / Transport $1.00

Total pre-Delivery $7.45

Bunkering (Shore/Truck/Vessel) $3.00

Total at-Delivery $10.45

Table 3: LNG Bunker Pricing Estimate Based on Henry Hub

(Source: Harsema-Mensonides 2018)

Similar LNG bunker price build-outs could be done using the above format for different

regions. For the business case analysis discussed in a subsequent section, a Henry Hub basis

for LNG bunker is assumed.

LNG USE AS A MARINE FUEL

Dual-Fuel and Gas Engine Technology Development

Engine types suitable for LNG use include either gas only or dual-fuel engines. Gas only and

dual-fuel engines have only become commonplace in the last decade or so (particularly for

non-LNG Carrier vessels) as more shipowners want flexibility in fuel options as environmental

24

regulations became stricter. Pure gas engines run on the Otto cycle while dual-fuel run on

Diesel and Otto cycles when operating in those respective modes. The main manufacturers

of these engine types include Wärtsilä, MAN, Winterthur (WinGD), and Caterpillar (MAK).

Whether the engine is gas only or dual fuel, those that operate on four-stroke Otto cycle meet

IGF-Code requirements for the ‘inherently safe’ engine room (as it operates under low

pressure). However, two-stroke engines are more common and are available for both fuel

scenarios (DNV GL October 2015a). Tables 4 and 5 provide a summary of the Diesel and

Otto Cycle features as well as gas turbine and dual fuel engine technologies.

Cycle Fuel Injection Ignition

Otto Gas-air mix admitted to the

cylinder before the compression starts Typically, an electric spark or

injection of pilot oil

Diesel Fuel admitted to the cylinder first at the

end of the compression stroke Self-ignition of the fuel (compression ignition)

CC DF Gas mode – Otto cycle process

Diesel mode – Diesel cycle process

Gas mode – injection of pilot fuel oil into the compressed mixture of air/natural gas Diesel Mode – compression ignition

Diesel Cycle DF

Gas and diesel modes – fuel admitted to the cylinder first at the end of the

compression stroke

Gas mode – pilot fuel is injected and self-ignites; gas is then injected into the flame

from the pilot oil

Table 4: Otto and Diesel Cycle Features

(Source: Adapted from IMO 2016, p. 75)

Feature Pure Gas Turbine DF 2-Stroke DF 4-Stroke

Cycle Otto Otto/Diesel Otto

Gas Supply Low Pressure Low/High Pressure Low Pressure

Ignition Source Spark Plug Liquid Pilot Fuel Liquid Pilot Fuel

Table 5: Gas Engine Technologies

(Source: Adapted from IMO 2016, p. 75)

Wärtsilä. Wärtsilä is one of the leading manufacturers of 4-stroke dual-fuel (DF) engines. Its

engines provide maximum fuel flexibility with the ability to burn natural gas, marine diesel oil

(MDO), and heavy fuel oil (HFO), seamlessly switching between fuels without any loss of

25

power. Originally designed for use on LNG carriers, its DF engines are now being used on

cruise ships, Roll-on/Roll-off and Roll-on/Passenger (RoRo/RoPax) vessels, offshore

support vessels (OSVs), and ferries (most notably Viking Line). The DF engine family has

been operating for nearly 20 years, with over 1,300 engines at more than 12 million hours of

run time and are NOx Tier III compliant (thus no additional need for selective catalytic

reduction (SCR) or exhaust gas recirculation (EGR) systems – systems discussed in a later

section). The company also provides full ship designs for LNG-capable containerships,

oil/chemical tankers (up to Aframax or 111k-deadweight tonne (dwt) size), and LNG bunker

vessels and tugs (Wärtsilä 2018).

MAN. German marine engine manufacturer, MAN, also is a leading technology solutions

provider in the dual fuel specification. The company has both a two-stroke, low-speed, high-

pressure gas injection (ME-GI) version and a 4-stroke, medium speed dual-fuel engine. The

two-stroke engine builds upon the successful Tier II NOx compliant diesel engine platform by

adding a gas-injection capability that meets Tier III NOx standards in gas mode with the

addition of either a SCR or EGR. The 4-stroke engine configurations – the 35/44DF and

51/60DF – offer ultimate fuel flexibility with the ability to burn HFO, MDO, MGO, and

natural gas. In liquid fuel mode, the engine is Tier II NOx compliant, and in gas mode the

engine is fully Tier III NOx compliant. These engines are best suited for ferries, Roll-on/Roll-

off (RoRo), cruise ships, and OSVs (MAN 2018).

Winterthur G&D. Swiss marine engine manufacturer, WinGD, also provides LNG-capable

dual fuel engines to support cleaner engine options for shipowners. As mentioned above,

there are essentially two technology options for low-speed engines: either a ‘lean burn’ dual-

fuel (DF) gas engine at low-pressure utilizing the Otto cycle, or a gas-diesel engine at high-

pressure utilizing the diesel cycle. WinGD is a leading manufacturer in low-speed, low-

pressure DF Otto-cycle engines; its X-DF line, ranging from 4.775 to 63.840 MW, currently

has 43 orders for a range of vessel types, including four 15,000-dwt product tankers. WinGD

decided to pursue these engine types due to the reduced CAPEX, OPEX, and efficiencies of

26

a two-stroke, low-speed engine, as well as the elimination of the need for an SCR or EGR to

meet IMO Tier III NOx limits while operation in gas-mode (Tier II limits would be met only

in diesel mode, hence, the need for an SCR/EGR). CAPEX reductions are due to the

elimination of the need for high-pressure compressors plus an adequate supply base for parts.

Its X-DF line achieves efficiencies from three key components: the gas admission, pilot fuel,

and automation and control systems. Of note is the hydraulically actuated gas admission

valves (GAVs), which increases overall fuel delivery performance and functionality. The X-

DF engine has been tested for over 3000 hours in almost exclusively gas-mode on the MT

Ternsund (a 15,000-dwt chemical tanker), meeting or exceeding commercial expectations (Ott

2017).

Caterpillar (MAK). Lastly, MAK also provides DF technology for shipowners. Its M34DF

and M46DF engines offer Tier II and Tier III compliance in diesel and gas modes, respectively,

and can burn HFO, MDO, MGO, and LNG, eliminating the need for scrubber use in ECA

areas. The engines offer superior energy efficiency design index (EEDI) performance (this

concept is described in a later section) and an overall lower OPEX (Caterpillar 2018).

LNG Fuel Systems and Storage

There are three types of LNG tanks for marine use: Type A/membrane; Type B/spherical;

and Type C/cylindrical. Type A and B tanks are generally prismatic in shape and can more

easily be fitted to a ship’s hull. LNG carriers typically use membrane tanks or Type B tanks

(the spherical Moss Rosenberg design); however, both A and B tanks need a secondary barrier

to prevent release of LNG in the event of tank failure. Type C tanks do not require this

secondary barrier. In addition, Type C tanks can function under much higher pressures,

managing BOG issues more effectively than A or B tanks (World Ports Climate Initiative,

N.D.). Table 6 provides a summary of the three types of LNG tanks.

27

Tank Description Pressure Pros Cons

A

Prismatic tank, adjustable to hull

shape; full secondary barrier

<0.7 bar g

Space-efficient Boil-off gas handling

More complex fuel system High costs

B

Prismatic tank, adjustable to hull

shape; partial secondary barrier

<0.7 bar g

Space-efficient Boil-off gas handling

More complex fuel system High costs

Spherical tank; partial secondary barrier

Reliably proven in LNG carriers

Boil-off gas handling. More complex fuel system

C Pressure vessel,

cylindrical with dished ends

>2 bar g

Allows pressure increase Simple fuel system Little maintenance Easy installation

Lower costs

On board space requirements

Table 6: LNG Fuel Tanks Pros and Cons

(Source: Adapted from World Ports Climate Initiative, N.D.)

The most common LNG fuel tank aboard ships and for small-scale storage is the Type-C

LNG tank. These tanks are low cost, easy to scale, and can withstand pressures of up to 10

bar (roughly 10 atm). According to IGF Code, Type C tanks must have a minimum holding

time for BOG of 15 days, 21 days as per USCG rules (IMO 2016, p. 73). However, their

cylindrical shape makes it harder to accommodate in valuable ship space; add to that insulation

and the space requirement becomes even greater. In addition, since LNG has about 1.6 times

less energy than fuel oil per unit of volume, tanks need to be larger to accommodate this energy

density difference. Therefore, incorporating LNG fuel storage into retrofits or newbuilds

often results in a space requirement of 3-4 times what would be needed for fuel oil or marine

diesel (Harsema-Mensonides 2017).

Insulation is critical for the performance of Type C tanks and must combat against the effects

of conduction (minimize touch points), convection (maximize vacuum environment), and,

most importantly, radiation (ensure excellent insulation). Type C tanks have a choice of three

insulation materials. Polyurethane foam has the highest conductivity, so it needs to be quite

28

thick (~800mm) to achieve maximum insulation effects. Perlite (a bulk filler) is cheap but it

is notorious for settling because of its weight, creating voids in insulation. It also requires

about 250mm of thickness around the tank. Multilayer insulation (MLI) has become the

choice for mobile platforms, requiring only about 10-15mm thickness. MLI has the effect of

reducing total additional insulation weight by up to 25 tonnes per tank. Incorporation of

effective insulation is critical in LNG-capable newbuild design (Kogan 2017).

On the fuel delivery system side, several companies offer turnkey and customized solutions.

MAK offers fully integrated DF engines, fuel delivery, storage, and regasification systems.

MAN also offers LNG fuel delivery systems.

ACD USA – High-Pressure Fuel Delivery System. ACD is a leading provider of centrifugal and

reciprocating cryogenic fuel pump systems for LNG-fueled ships as part of its clean energy

solutions initiative. ACD’s pumps can support both low-pressure and high-pressure engine

types, as well as fuel delivery systems on LNG bunker vessels (ACD 2018).

TGE Marine Gas Engineering. TGE Marine is a leading provider of LNG fuel delivery systems.

It provides integrated solutions utilizing Type C storage tanks, and fuel gas systems for both

2-stroke and 4-stroke main engines including the four companies listed above. Vessel types

include tankers, containerships, very large ore carriers (VLOC), and RoRo/RoPax/ConRo

configurations. TGE also successfully completed the retrofitting of the Wes Amelie, a 1,000

twenty-foot equivalent unit (TEU) container feeder vessel that operates in the North and

Baltic Seas. This was one of the first successful conversions of a ship to LNG-capability, with

TGE providing components for the LNG fuel gas plant, storage tanks, and control and safety

systems (TGE Marine 2018).

Environmental Benefits of LNG Fuel

LNG fuel is one the cleanest burning fuels across the emission spectrum. As shown in Table

7, LNG emits virtually no SOx or particulate matter (PM), reduces NOx by up to 85% with a

29

low-pressure engine (meeting Tier III requirements) and up to 40% with a high-pressure

engine, and reduces CO2 emissions by up to 30%. While some LNG-capable engine

configurations will require NOx reduction technology, such as a selective catalytic reduction

(SCR) or an exhaust gas recirculation (EGR) system, there are 4-stroke (low-pressure) engines

that can meet Tier III NOx limits without other technology. However, low pressure, 2-stroke

engines are likely the way forward as larger ships integrate dual-fuel LNG capable technology.

Table 7: Environmental Benefits of LNG Fuel

(Source: DNV GL October 2015a, p. 33)

While the primary focus of this thesis is focused on technology options to reduce SOx, it is

worth mentioning some NOx reduction technologies as they are often complementary to SOx

emissions reduction solutions. As mentioned above, the two main NOx reduction

technologies are SCR and EGR. SCR technology works by injecting urea into the stack where

it reacts with exhaust on the surface of a catalyst (typically titanium or vanadium oxides). Since

the exhaust reacts external to the combustion process, engine efficiency is not compromised

but operational costs increase. EGR technology works primarily with two-stroke engines and

recirculates exhaust back through the combustion chamber, lowering the overall combustion

temperature, which reduces NOx by 70-80%. However, these systems do not address SOx and

PM directly, but rather with a water treatment process in addition to the scrubber, adding to

total operational costs. SCR technology is the most likely solution for reaching Tier III

compliance with 4-stroke engines, while SCR or EGR can apply to 2-stroke engines that burn

fuel oil or low sulfur distillates. However, LNG offers a Tier III solution without the need

for an SCR or EGR (Nishifuji 2017).

30

To meet SOx emissions targets, low sulfur distillates such as marine gasoil (MGO) will be the

likely options. However, this fuel type has several issues operating in existing engines such as

lower viscosity, poorer lubrication, lower flash and volatility points, and increased sediment

buildup in the cylinder. While there are several remedies to these issues, the use of exhaust

gas cleaning systems (EGCS), or scrubbers, has become the solution of choice for shipowners.

While they do have relatively high capital costs (+/- $5 million), scrubbers can reduce sulfur

content of emissions to the equivalent of using 0.1% sulfur fuel oil, which is consistent with

the ECA limit, while simultaneously reducing PM by 70-80%. Scrubbers are divided into two

categories – wet and dry. Wet scrubbers use treated water to clean exhaust gas and come in

open, closed, and hybrid loop systems, whereas dry scrubbers use a reactant like sodium or

calcium hydroxide to remove SOx. Wet scrubbers are more available but both types add

significant CAPEX and OPEX to a shipowner, especially in handling and disposal of waste.

Overall, scrubbers might be the most economical choice in a low fuel oil price and high

distillate price environment. However, as LNG-capable engines, fuel systems, and bunkering

networks develop, LNG fuel could gain greater market share because of its price

competitiveness and environmental benefits (Nishifuji 2017).

As shown in Table 8, LNG-capable vessels are also much more competitive in reducing GHG

emissions. LNG fuel can lower CO2-e emissions by up to 25-30%. However, one of the

critical issues facing dual-fuel engines is ‘methane slip,’ which is an imperfection in the Otto

cycle that allows methane to escape through the exhaust system unburned. Since methane has

a higher global warming potential than CO2, unmitigated methane slip can offset the GHG

reduction benefits of LNG-capable vessels. Engine manufacturers like Wärtsilä have achieved

significant improvements in its DF engine designs, minimizing methane slip to less than

6g/kWh, the level considered as competitive as other fuels (Ship and Bunker 2016).

31

Table 8: GHG Emissions Profiles of Different Marine Fuels

(Source: DNV GL October 2015a, p. 33)

32

Chapter 3 – The Role of LNG as a Marine Fuel

LNG-FUELED SHIPS – CURRENT & PROJECTED

In the current world merchant fleet, there are approximately 50,000 vessels in operation. As

shown in Figure 19, the overwhelming majority of vessels are cargo ships, followed by tankers

and containerships. A smaller percentage of vessels are Roll-on/Roll-off (Ro-Ro), which

include car carriers and ferries, and passenger ships like cruiseliners. LNG carriers, while

massive, represent a fraction of total number of ships but are instrumental in sustaining the

global LNG trade.

Figure 19: Number of World Merchant Fleet Ships

(Source: Statista 2017, p. 12)

In May 2015, DNV GL reported that there were 63 LNG-fueled ships in operation with 76

newbuilds on order (DNV GL October 2015a, pp. 40-43). At the end of 2016, there were 88

LNG-fueled ships operating with 98 newbuilds on order, with an additional 70 ships

33

designated as LNG-conversion ready. Most of these ships will operate in Northern European

and North American zones, where ECAs are very strict. However, 4 of the currently operating

ships and 22 newbuilds will operate globally. Industry experts estimate that by 2020 there

could be as many as 400 to 600 LNG-capable ships fully operational (Wold 2017)

In 2017, there were a total of 325 LNG-capable vessels, of which 229 were LNG carriers, with

the remaining hundred split among offshore service and cargo vessels, passenger vessels, and

other types of vessels. 110 LNG-capable newbuilds were on order (UNCTAD/RMT/2017,

p. 39). As shown in Table 9, LNG-capable ships are becoming increasingly attractive,

capturing more than 13% of the total orderbook in 2018 and beyond:

Table 9: LNG-Capable Newbuilds (Thousands of Gross Tons)

(Source: UNCTAD/RMT/2017, p. 38)

34

LNG procurement company Titan LNG also has predicted a surge in LNG newbuild orders

as LNG pricing becomes more competitive with other fuel types. As shown in Figure 20, in

2017, 11% of newbuild orders were for LNG-capable ships (Wainwright 2018).

Figure 20: Number of Contracts and % LNG Newbuilds

(Source: Titan LNG 2017)

The most recent numbers are even more positive. As shown in Figure 21, as of January 1,

2018, 119 LNG fueled ship were operating globally (excluding LNG carriers and inland

waterway vessels), with another 125 confirmed LNG-capable newbuilds and 114 LNG-ready

ships (i.e. ships that could be easily converted to LNG-capable). Car/passenger ferries and

oil/chemical tankers are the most prevalent LNG-fueled ships, with containerships, platform

supply vessels (PSVs), and cruise ships also becoming an attractive target for LNG capability,

primarily with dual-fuel engine configuration (DNV GL January 2018).

35

Figure 21: LNG-capable ships by vessel type

(Source: Adapted from DNV GL January 2018, p. 14)

Examples of Company-Level Pursuit of LNG-Capable Ships

At the international level, LNG-capable ships are becoming a more attractive option and major

shipowners are integrating this capability into their newbuild orders. For example, Sovcomflot

(SCF Group), a Russian company, has increased its LNG-capable newbuilding orders for

Aframax tankers to six. Each vessel is approximately 114,000 dwt priced at about $60 million

each, and are they are the first Aframax tankers to use LNG. Further, SCF has allegedly

considered transitioning most of its 60 Aframax vessels to LNG-capable by 2022 (Hine

November 23, 2017).

BP has stated it is pursuing two LNG-capable Very Large Crude Carriers (VLCCs) on 3-year

time charter with two one-year options. However, the LNG capability comes at a cost for

these unique vessels, with approximately a 25% premium above the typical newbuild cost of

$77 to $83 million. BP has considered retrofitting the vessels with open-loop exhaust gas

2 2

33

3

18

4 19

21

4 3 5 4103 2

14

21

152

1

364

2

9 115

0

10

20

30

40

50

LNG-Capable Ships by Vessel Type

Ships in Operation Ships on Order

36

cleaning systems (EGCS), or scrubbers, at a cost of $2.5 million per ship but uncertainty over

the potential significant premium of low sulfur fuel oil could erode its estimated one-year

payback (Hine November 16, 2017).

On the bulker vessel side, ESL Shipping will be receiving two 26,000-dwt newbuilds, which

will also be the world’s largest LNG-capable vessels in this class. ESL noted that it did not

consider scrubbers for these vessels as heavy fuel oil (HFO) is not allowed in Scandinavia due

to stringent ECA policies (Craig November 9, 2017).

Shipping giant CMA CGM, which recently has ordered up to eight 14,000 twenty-foot

equivalent units (TEU) container ships worth $850 million, is considering LNG capability for

these ships. On these ships, the premium for this capability is about 15 to 20%. However,

given that the company opted for LNG-capability on its new generation of nine ultra large

container vessels (ULCV) of 22,000 TEU, the smaller container ships may very well likely

follow suit (Ang and Hine, January 11, 2018). These ships, also known as the PERFECt

(Piston Engine Room Free Efficient Containership), intend to use a combined gas and steam

turbine engine for ship power and propulsion (Wold 2017).

Cruise ships have also been a target of opportunity for LNG fuel. As of early January 2017,

there were 11 LNG-capable cruise ships on order. These ships typically use between 30,000

to 50,000 tons per year of LNG, representing an estimated .3 to .5 MTPA of LNG each year,

a significant percentage of total marine fuel use from just a dozen or so ships (Wold 2017).

One of the largest cruise ship operators in North America, Carnival has seven LNG-capable

cruise ships on order for delivery between this year and 2022. This is a critical step for Carnival

as it diversifies its fleet away from using scrubbers (70 ships) or low-sulfur fuel (33 ships).

Carnival estimates its LNG ships will emit essentially zero SOx, reduce particulate matter (PM)

by 95 to 100%, reduce NOx by 85%, and lower CO2 by 25-28%. The two North American

operating LNG vessels are both 180,000 gt and will be fueled by a new LNG bunker barge

supplied by Shell (Hine and Juliano November 8, 2017). Further, Carnival’s Mediterranean

37

affiliate AIDA Cruises will also provide LNG fuel to two of its ships, the AIDAperla and

AIDAprima, utilizing truck to ship while in port and barge to ship while at sea from Shell

(Juliano November 27, 2017).

There are also two companies that are completely rethinking ship design for LNG capability.

First, Arista Shipping’s Forward LNG Project intends to be the largest and cleanest Bulk

Carrier. The ship is designed with Wärtsilä engines and GTT membrane tanks with a capacity

of 2500 m3, giving the ship a voyage endurance of 40 days and/or 14,000 nautical miles. The

ship can run completely on LNG and does not need any additional emissions reduction

equipment like scrubbers (for SOx) or SCR (for NOx) (Forward LNG 2017). Second, DNV

GL’s Piston Engine Room Free Efficient Containership (PERFECt) is designed in

conjunction with GTT and CMA CGM to support future Ultra Large Container Vessels

(ULCV) with 20,000+ TEU capacities. The design uses a combined cycle gas and steam

turbine (COGAS) electric propulsion engine that burns cleaner LNG and has greater

efficiencies than marine diesel engines (greater than 60% compared to 52%). The ship has

two 11,000 m3 membrane storage tanks, and despite being twice the size of conventional fuel

oil tanks, allows for the addition of 300 TEU spaces since no additional engine room is needed.

The CAPEX premium for this ship is between 20 and 25%; however, significant OPEX cost

reductions could be achieved by elimination of other emissions controls and cheaper LNG

fuel costs. In fact, the vessel achieves comparable paybacks to using scrubbers and SCRs

(DNV GL October 2015b).

Domestically, several Jones Act Vessel companies have already made or plan to make the

switch to LNG-capable vessels. Tote Maritime was one of the first-movers in this space with

its Marlin-class vessels. Delivered in late 2015 and early 2016, these container ships run almost

exclusively on LNG for their Jones Act Vessel trade between the US and Puerto Rico. The

ships are 100% American-made and are supported by LNG bunkering solutions out of

Jacksonville, FL (Tote N.D.).

38

Crowley Maritime Corporation has also been a leader in this space with two newbuild orders

of Commitment (C) Class LNG-capable combination container Roll-On/Roll-Off (ConRo)

ships. At a value of approximately $350 million, these ships transport containers and vehicles

between the US and Puerto Rico, and have a capacity of 2,400 TEU with space to

accommodate 300 refrigerated units and 400 vehicles, all while maintaining a max cruising

speed of 22 knots. At 26,500 dwt, the ships are expected to garner the CLEAN notation and

Green Passport issued by ship certification company DNV GL (Ship Technology December

2017)

SEA-Vista LLC has been a leader on the product tanker side. In March of 2017, General

Dynamics shipbuilding arm NASSCO delivered the last of three product carriers, the Liberty,

that are LNG-conversion ready and are sized at 50,000 dwt, 610-ft long, and with a capacity

of 330,000 bbls. The other two ships, the Independence and Constitution, are already operating in

Jones Act vessel trade (NASSCO 2017).

Hawaii-based Jones Act vessel company Pasha has ordered two LNG-capable containerships

at an estimated value of over $400 million to be built by Keppel AmFELS and delivered in

2020. The vessels are rated at 2,525 TEU, with the ability to carry 500 45 ft containers, 400

reefer units, and 300 forty-foot equivalent units (FEU) while maintaining a cruising speed of

23 knots. The ships will run nearly exclusively on LNG (LNG Industry, September 2017, p.

8).

Finally, Matson, a leading shipping company in the Pacific and competitor to Pasha, also began

production on two ConRo vessels for its Hawaii fleet that are expected for delivery in late

2019 and early 2020. These two “Kanaloa Class” vessels are LNG-ready should Matson decide

to operate them more frequently on LNG. The vessels are 3,500 TEU, designed to run at a

service speed of 23 kts, and employ the latest eco-friendly designs to maximize efficiency and

reduce environmental impacts (Matson 2017).

39

Financing Structures for LNG-Capable Ships and Other Emissions Reductions

Measures

The focus on making more environmentally friendly ships has created challenges for

shipowners due to the additional capex and/or premiums of options. Therefore, financing

mechanisms exist to provide shipowners with lower cost capital as they pursue different

options for meeting more stringent emissions standards. In the US, the Department of

Transportation’s Maritime Administration (MARAD) runs the Federal Ship Financing

Program (FSFP) for Jones Act vessels, which is a generous program that allows up to 87.5%

of guaranteed debt financing over a term of 25 years, with interest rates typically matched to

a treasury note of the same tenor as the debt, and nominal program fees. To date, both Tote

and Crowley have leveraged the FSFP for their LNG-capable newbuilds, with total loan values

of $324.6 million and $362.7 million, respectively. It should be noted that these loan values

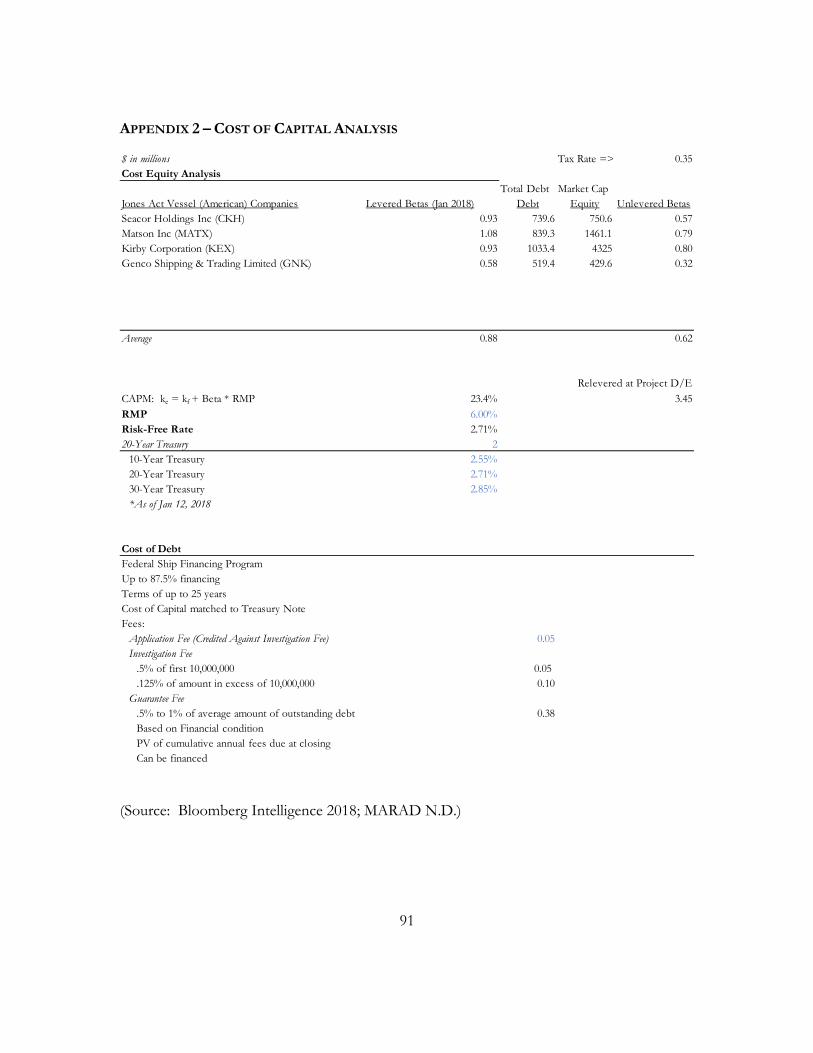

represent the maximum level of guaranteed debt financing (MARAD N.D.).

Internationally, particularly in Europe, financing programs have been established to green the

fleet. The European Investment Bank (EIB) has created two facilities to assist shipowners

finance either retrofits or newbuilds that address environmental quality constraints. First, the

European Fund for Strategic Initiatives (EFSI) Green Shipping Loan Program is a €250

million loan program targeting Atlantic and Mediterranean-based EU shipowners for

newbuild contracts. The program covers up to 50% of the investment cost and is expected

to assist a total investment portfolio of €500 million. The debt takes a senior secured structure.

Second, the Connecting Europe Facility (CEF), a new financial instrument designed to

support green shipping initiatives, is attempting to reverse the reluctance of lenders to finance

environmentally focused investments. Similar to the US FSFP, the CEF is a guarantee

program that can cover up to 100% of retrofit investments or up to 50% of newbuild

investments. The program has a value of €750 million and is expected to support up to €3

billion of investments at a senior or subordinated structure (Gaudet 2016).

40

Both financing programs represent critical government-sponsored support for the next era of

ships designed to address significant environmental issues. The business case analyses

discussed in subsequent chapters will utilize these programs to understand their impact on the

overall financial feasibility of different environmentally-based investment decisions.

In addition to traditional project finance structures and state-sponsored financing programs

like the Federal Ship Financing Program and the EIB Green Shipping Programme, there are

some alternative financing options for shipowners to assist in meeting increasingly strict

emissions regulations. One such alternative is called the Emissions Compliance Service

Agreement (ECSA), offered by an infrastructure development group called Clean Marine

Energy (CME). The ECSA brings third-party financing to a shipowner to eliminate the

upfront capital costs associated with installing scrubbers or even retrofitting a vessel to burn

cleaner fuels like LNG. CME recoups its investment by sharing a portion of the OPEX

savings, mostly from the perceived savings (the differential between high sulfur fuel oil and

low sulfur fuel oil/distillates) from continued use of non-compliant fuel oil in the case of a

scrubber installation until a required rate of return is met. At that point, all OPEX savings

would revert to the shipowner who would continue to benefit from those savings for the

remainder of ship life (Clean Marine Energy 2018).

Lastly, while no research indicates that this structure has been used, tax equity investments

might also be a way to help facilitate investments in “clean shipping.” Tax equity investments

have been used to finance utility scale solar and wind generation projects, offering an incentive

for a corporation with a large tax burden to monetize the investment tax credit (ITC) for solar

or production tax credit (PTC) for wind. While these tax credits are beginning to sunset for

power generation projects since costs are nearly at parity or in some cases cheaper than other

generation sources, a similar structure could be used in ship financing to help alleviate the

premium for emissions reductions investments, whether that be emissions controls for SOx

and NOx or a completely new ship that is LNG-capable. Subsidies for alternative energy

sources have come under increasing scrutiny the last few years so this approach would likely

41

require significant championing in government, financial institutions, and the shipowner

community.

TYPES OF MARINE FUELS – HISTORICAL AND FORECASTED VOLUMES & PRICES

In 2012, the global shipping community used approximately 300 million tonnes per year of

bunker fuel across several variants (See Figures 22 and 23). The most common types of

bunker fuel include heavy fuel oil (HFO), intermediate fuel oil (IFO), marine diesel oil (MDO),

marine gasoil (MGO), and low-sulfur variants of all three. Low sulfur distillates either have

1.0% sulfur or 0.1% sulfur; these fuels were made for compliance with stringent emission

control area (ECA) limits on the amount of allowable sulfur.

Figure 22: Marine Fuel Consumption, 2012 (MTPA)

(Source: Adapted from Concawe 2016, p. 4)

228

64

8

0

50

100

150

200

250

300

350

Marine Fuels

Marine Fuel Consumption, 2012

HFO MDO LNG

42

Figure 23: Marine Fuel Consumption by Ship Type, 2012

(Source: Adapted from Concawe 2016, p. 3)

A recent DNV GL study puts total marine fuel consumption for 2016 at roughly 233 to 256

million tonnes. As shown in Figure 24, containerships, bulkers, and tankers account for most

of the fuel use. This decrease from 2012 levels is likely due to several factors but could be

attributed to increased energy efficiency in ship design as well as decisions to reduce cruising

speeds to reduce fuel use and, in turn, emissions. In addition, since the price of oil plummeted

in 2014/2015, demand for shipping services decreased dramatically, causing an oversupply in

the market and decimating charter rates, which also likely contributed to an overall reduction

in total fuel use (DNV GL May 2017).

All other ships8%

Vehicle3% Offshore

3%

Cruise4%

LNG Carrier5%

Fishing5%

Chemical Tanker6%

RoRo and RoPax6%General Cargo

7%

Oil Tanker13%

Bulk Carrier18%

Containership22%

Marine Fuel Consumption (2012): 300 Mt (Global)

43

Figure 24: Merchant Fleet Vessel Types and Fuel Consumption, 2016

(Sources: Adapted from DNV GL November 2017a, p. 23; Statista 2017)

As noted above, there are essentially three major fuel types: fuel oil, marine gasoil (MGO),

and marine diesel oil (MDO). Within the fuel oil group, there are heavier and lighter variations,

with intermediate fuel oil (IFO) 380 and 180 (representing centistokes, or the unit of viscosity)

being the most common. IFO 380 is a blend of heavy fuel oil (HFO) and elements of light

oil, that creates a “cleaner” burning fuel. IFO 180 utilizes more marine gas oil, diesel oil, or

light cycle gas-oil blends to create a less viscous fuel oil. On the distillate side, MDO has a

lower cetane index than marine gasoil but a higher density, and usually contains a higher

amount of light cycle gasoil. Marine gas oil (MGO) is very similar to MDO but contains

negligible or no light cycle gasoil (Vermeire 2012, pp. 5-6). See Table 10 for a summary of

non-gaseous marine fuel types.

11,844

6,532 5,383

19,824

8,600

23%

16%

26%24%

11%

0%

5%

10%

15%

20%

25%

30%

0

5,000

10,000

15,000

20,000

25,000

Bulkers Tankers Containerships Other CargoVessels

All OtherVessels

% T

ota

l F

uel

Consu

mpti

on

Nu

mb

er o

f V

esse

lsMerchant Fleet Vessel Types and Fuel Consumption, 2016

Number of Vessels % Fuel Consumption

44

Industrial Name ISO Name Composition

Intermediate Fuel Oil 380 (IFO 380) MRG35 98% Residual Oil 2% Distillate Oil

Intermediate Fuel Oil 180 (IFO 180) RME 25 88% Residual Oil 12% Distillate Oil

Marine Diesel Oil DMB Distillate oil with trace of residual oil

Marine Gas Oil DMA 100% Distillate Oil

Table 10: Types of Marine Fuels

(Source: Adapted from EIA 2015, p. 9)

In 2016, the IMO proposed a plan to require all vessels larger than 5,000-gross tonnes to

report their annual fuel consumption to their flag state, which would then report this data to

the IMO Ship Fuel Consumption Database. The fuel reporting requirement may become

effective in 2018 and is intended to capture more accurately total fuel use by type across all

vessel classes to verify if efficiency and emissions reductions improvements are occurring

(Wiseman 2016). These classes of ships account for more than 85% of the merchant fleet’s