Embed Size (px)

Citation preview

Copyright © 2003 South-Western/Thomson Learning All rights reserved.

Chapter 2

The Creation of

Financial Assets

Copyright © 2003 South-Western/Thomson Learning. All rights reserved.

The Transfer of Funds from Savers to Business

• Income that is saved is subsequently invested

• The process of investing creates financial claims

• Financial claims are either–debt–equity

Copyright © 2003 South-Western/Thomson Learning. All rights reserved.

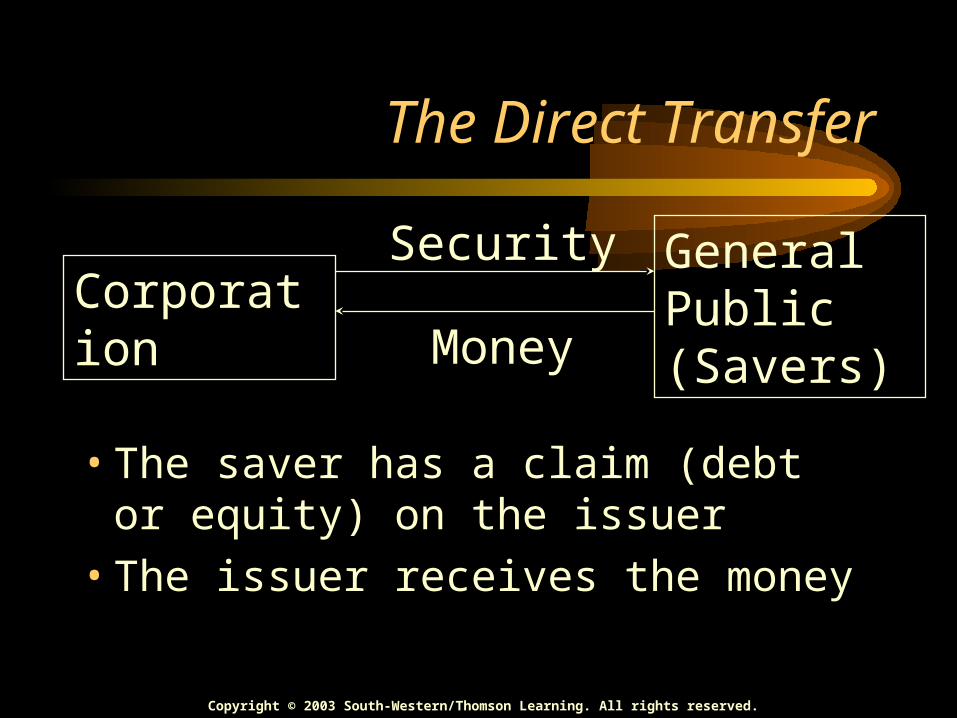

The Direct Transfer

• The saver has a claim (debt or equity) on the issuer

• The issuer receives the money

CorporationGeneral Public(Savers)

Security

Money

Copyright © 2003 South-Western/Thomson Learning. All rights reserved.

The Indirect Transfer through a Financial Intermediary

• The saver has a claim on the financial intermediary

• The financial intermediary has a claim on the ultimate user of the funds

Financial Intermediary

General Public(Savers)

Account

Money

Copyright © 2003 South-Western/Thomson Learning. All rights reserved.

The Private Placement

• Direct sale of securities

• Eliminates selling costs

• Features can be tailor made for both parties

Copyright © 2003 South-Western/Thomson Learning. All rights reserved.

The Sale of New Securities to the General Public

• Initial public offerings (IPOs)

• The role of investment bankers

Copyright © 2003 South-Western/Thomson Learning. All rights reserved.

The Sale of New Securities To the General Public

• The mechanics of security underwriting

–the originating house or managing underwriter

–the guaranteed sale - firm commitment

–underwriter bears the risk

–the syndicate

Copyright © 2003 South-Western/Thomson Learning. All rights reserved.

The Sale of New Securities To the General Public

• The mechanics of security underwriting

–underwriting discount

–prospectus

• Best effort agreements

–issuing firm bears the risk

Copyright © 2003 South-Western/Thomson Learning. All rights reserved.

Pricing an IPO

• Underpricing leads to windfall gains to initial buyers

• Overpricing inflicts losses on initial buyers and the investment bankers

• Tendency to underprice to assure a successful sale

Copyright © 2003 South-Western/Thomson Learning. All rights reserved.

The Price Volatility of IPOs

• Prices can rise dramatically

• Many firms eventually fail

• Few investors get to participate in an IPO

Copyright © 2003 South-Western/Thomson Learning. All rights reserved.

Regulation of Initial Public Offerings

• Registration of new securities

• The prospectus

• Securities and Exchange Commission (SEC)

• The shelf-registration

• The lock-up

Copyright © 2003 South-Western/Thomson Learning. All rights reserved.

Financial Intermediaries and Investment Bankers Differ

• Financial intermediaries create claims on themselves

• Investment bankers

–facilitate the sale of new securities

–do not create claims on themselves

Copyright © 2003 South-Western/Thomson Learning. All rights reserved.

The Variety of Financial Intermediaries

•Commercial banks

•Savings and loan associations

•Mutual savings banks

•Credit unions

•Life insurance companies

Copyright © 2003 South-Western/Thomson Learning. All rights reserved.

The Variety of Financial Intermediaries

• Pension plans

• Money market mutual funds

Copyright © 2003 South-Western/Thomson Learning. All rights reserved.

Financial Intermediaries

• Each financial intermediary creates claims on itself and transfers funds from savers to

–firms

–governments

–people who need funds

Copyright © 2003 South-Western/Thomson Learning. All rights reserved.

Depository Financial Institutions

• The Depository Institutions Deregulation and Monetary Control Act of 1980

• Subject to the regulation of the Federal Reserve

Copyright © 2003 South-Western/Thomson Learning. All rights reserved.

Regulation Covers

• Types of deposits each intermediary may issue

• Amounts that must be held in reserve against deposits

Copyright © 2003 South-Western/Thomson Learning. All rights reserved.

Federal Deposit Insurance Corporation (FDIC)

• Insures accounts up to specified limit

• Another source of regulation

Copyright © 2003 South-Western/Thomson Learning. All rights reserved.

Regulatory Trends

• The consolidation of regulation through the Federal Reserve

• The increased ability to issue various types of accounts

• Reduced or blurred the distinctions among the different types of depository institutions

Copyright © 2003 South-Western/Thomson Learning. All rights reserved.

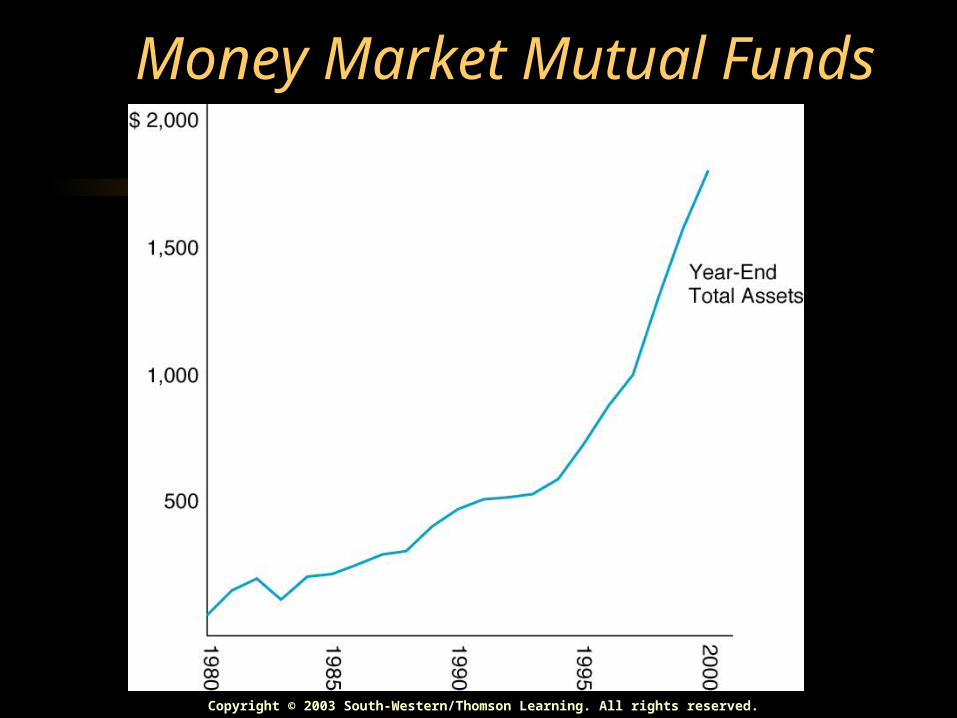

Money Market Mutual Funds

• A specialized investment company

• Makes only short-term investments

• Acquires money market instruments

• Shares in money funds have become popular investments

Copyright © 2003 South-Western/Thomson Learning. All rights reserved.

Money Market Mutual Funds

Copyright © 2003 South-Western/Thomson Learning. All rights reserved.

The Money Market Instruments

•Certificates of deposit (CDs)

•Negotiable CDs

•Eurodollar CDs

•U.S. Treasury bills

Copyright © 2003 South-Western/Thomson Learning. All rights reserved.

The Money Market Instruments

• Commercial Paper

• Repurchase agreements (repos)

• Bankers' acceptances

• Tax (or revenue) anticipation notes

Copyright © 2003 South-Western/Thomson Learning. All rights reserved.

The Money Market Instruments

• These instruments are

–safe

–liquid

• Offer competitive short-term rates