Embed Size (px)

Citation preview

COP21: 10 THINGS THE NEGOTIATORS NEED TO KNOW

23 November 2015

1

WHAT THE COP21 NEGOTIATORS NEED TO KNOW…

COP21: 10 Things the Negotiators Need to Know – 23 November 2015

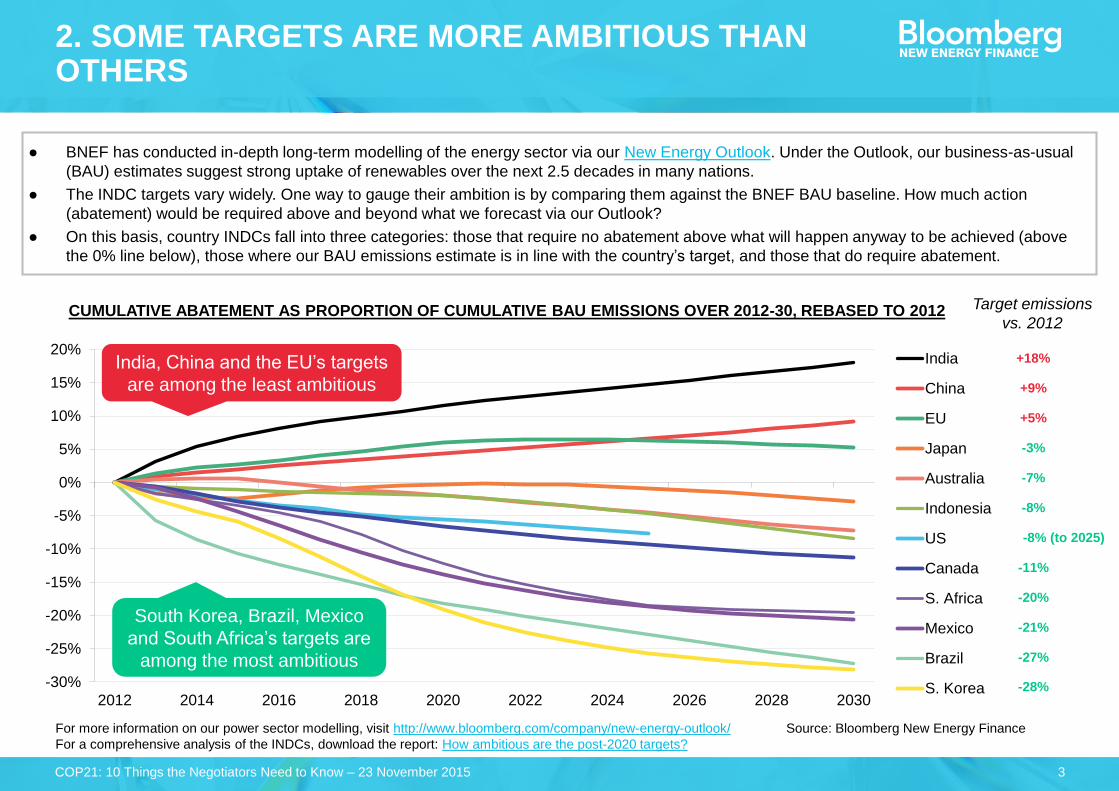

2. SOME TARGETS ARE MORE AMBITIOUS THAN OTHERS

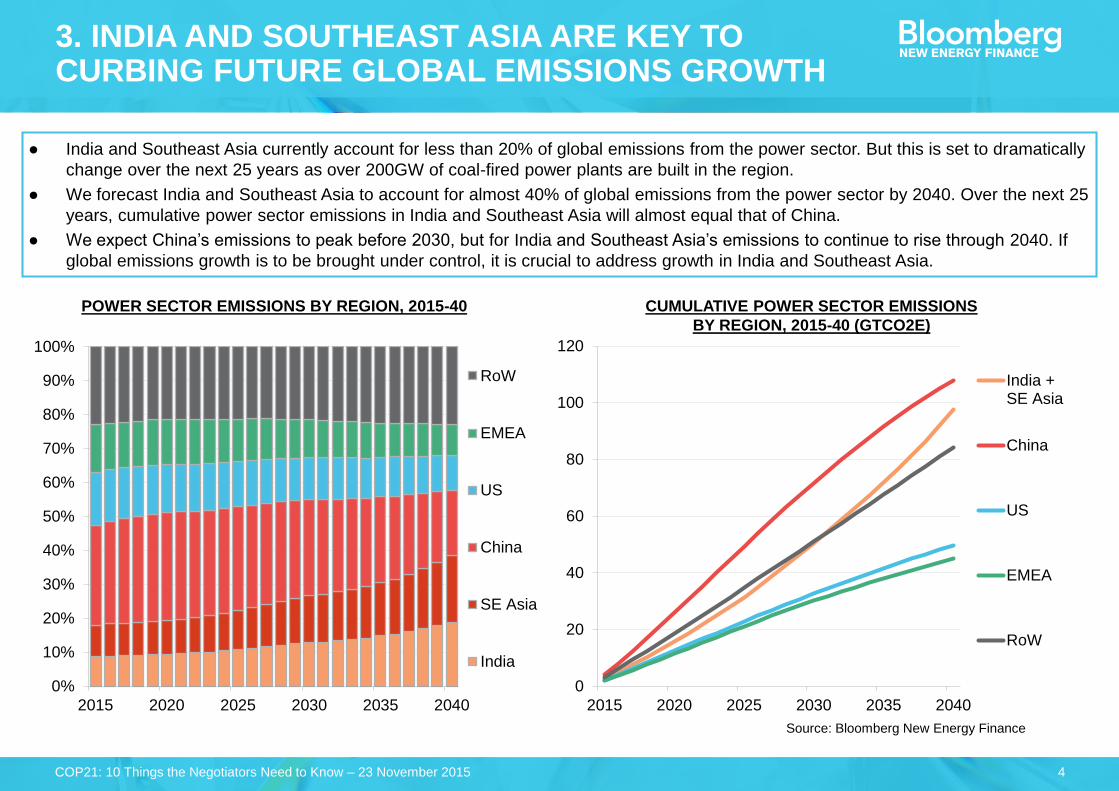

3. INDIA AND SOUTHEAST ASIA ARE KEY TO CURBING FUTURE

GLOBAL EMISSIONS GROWTH

4. RENEWABLE ENERGY IS GETTING CHEAPER

6. CLEAN ENERGY INVESTMENT HAS LEVELLED AT ~$300BN/YR

SINCE 2011

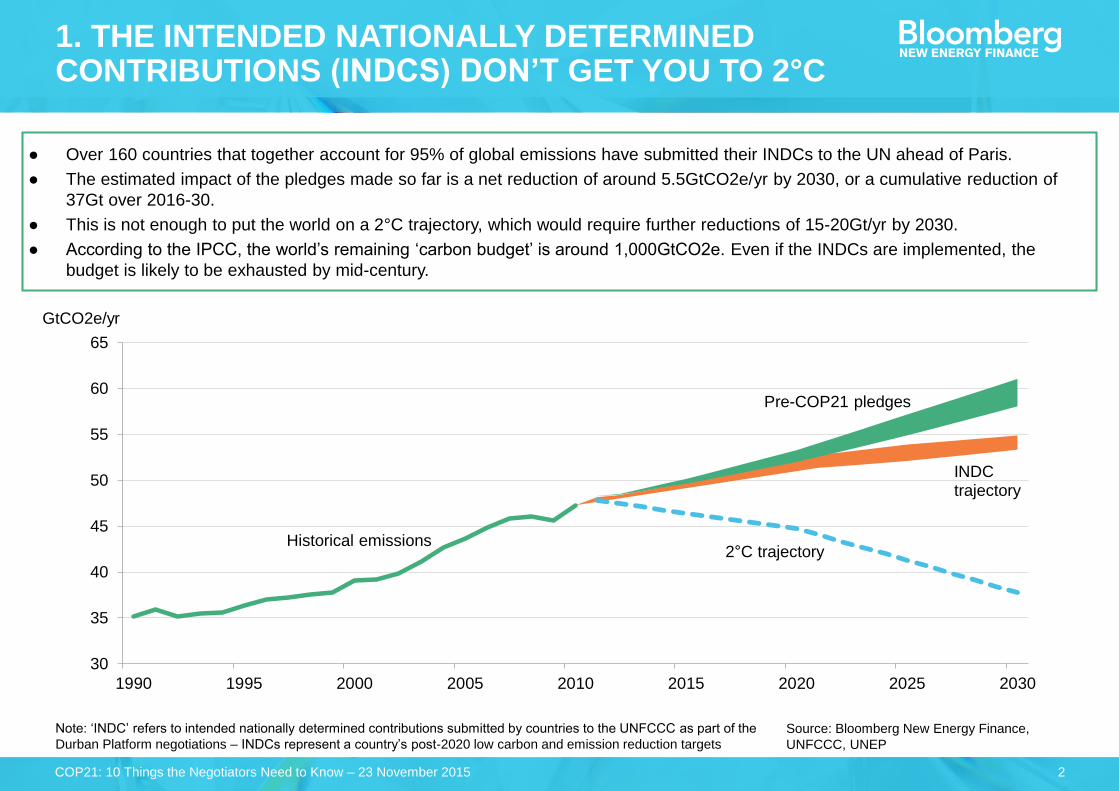

1. THE INTENDED NATIONALLY DETERMINED CONTRIBUTIONS

(INDCS) SUBMITTED DON’T GET YOU TO 2°C

When UNFCCC delegates meet at COP21 in Paris, it is crucial that the negotiations are well informed with independent opinion and

analysis.

This report is not intended to be a comprehensive guide to the COP21 talks, nor does it try to touch on all of the issues that will be on

the agenda in Paris. Instead it takes aim at a select number of issues that are often the subject of misinformation and contention

within the climate negotiations. Each section of this report presents objective data and charts that we hope will serve to better inform the

negotiations towards a new global climate deal.

Bloomberg New Energy Finance is a leading independent provider of news, research and analysis on clean energy and the

low-carbon transition. For more information visit about.bnef.com

8. CLEAN ENERGY INVESTMENT FROM WEALTHY TO LOWER

INCOME NATIONS HAS GROWN BUT IS STILL ONLY $10-15BN/YR

9. FOSSIL FUELS WILL BE A CASUALTY OF THE LOW-CARBON

ENERGY EVOLUTION, REGARDLESS OF PARIS

10. ECONOMICS ALONE WILL TRANSFORM THE ENERGY SECTOR,

BUT MUCH GREATER ACTION WILL BE NEEDED TO REACH 2°C

7. THE MAJORITY OF CLEAN ENERGY INVESTMENT IS NOW

OUTSIDE OF THE OECD – BUT LEAST DEVELOPED NATIONS

LAG FAR BEHIND CHINA, BRAZIL, INDIA AND S. AFRICA.

5. WIND AND SOLAR ARE ALREADY CHEAPER THAN COAL- AND

GAS-FIRED POWER PLANTS IN MANY COUNTRIES

2

30

35

40

45

50

55

60

65

1990 1995 2000 2005 2010 2015 2020 2025 2030

Historical emissions2 C trajectory

INDC trajectory

Pre-COP21 pledges

GtCO2e/yr

1. THE INTENDED NATIONALLY DETERMINED CONTRIBUTIONS (INDCS) DON’T GET YOU TO 2°C

● Over 160 countries that together account for 95% of global emissions have submitted their INDCs to the UN ahead of Paris.

● The estimated impact of the pledges made so far is a net reduction of around 5.5GtCO2e/yr by 2030, or a cumulative reduction of

37Gt over 2016-30.

● This is not enough to put the world on a 2°C trajectory, which would require further reductions of 15-20Gt/yr by 2030.

● According to the IPCC, the world’s remaining ‘carbon budget’ is around 1,000GtCO2e. Even if the INDCs are implemented, the

budget is likely to be exhausted by mid-century.

Source: Bloomberg New Energy Finance,

UNFCCC, UNEP

Note: ‘INDC’ refers to intended nationally determined contributions submitted by countries to the UNFCCC as part of the

Durban Platform negotiations – INDCs represent a country’s post-2020 low carbon and emission reduction targets

COP21: 10 Things the Negotiators Need to Know – 23 November 2015

3

2. SOME TARGETS ARE MORE AMBITIOUS THAN OTHERS

● BNEF has conducted in-depth long-term modelling of the energy sector via our New Energy Outlook. Under the Outlook, our business-as-usual

(BAU) estimates suggest strong uptake of renewables over the next 2.5 decades in many nations.

● The INDC targets vary widely. One way to gauge their ambition is by comparing them against the BNEF BAU baseline. How much action

(abatement) would be required above and beyond what we forecast via our Outlook?

● On this basis, country INDCs fall into three categories: those that require no abatement above what will happen anyway to be achieved (above

the 0% line below), those where our BAU emissions estimate is in line with the country’s target, and those that do require abatement.

-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

2012 2014 2016 2018 2020 2022 2024 2026 2028 2030

India

China

EU

Japan

Australia

Indonesia

US

Canada

S. Africa

Mexico

Brazil

S. Korea

+9%

-8%

-8% (to 2025)

-20%

+5%

-3%

-11%

-7%

-21%

-27%

-28%

+18%

CUMULATIVE ABATEMENT AS PROPORTION OF CUMULATIVE BAU EMISSIONS OVER 2012-30, REBASED TO 2012 Target emissions

vs. 2012

For more information on our power sector modelling, visit http://www.bloomberg.com/company/new-energy-outlook/

For a comprehensive analysis of the INDCs, download the report: How ambitious are the post-2020 targets?

Source: Bloomberg New Energy Finance

South Korea, Brazil, Mexico

and South Africa’s targets are

among the most ambitious

India, China and the EU’s targets

are among the least ambitious

COP21: 10 Things the Negotiators Need to Know – 23 November 2015

4

3. INDIA AND SOUTHEAST ASIA ARE KEY TO CURBING FUTURE GLOBAL EMISSIONS GROWTH

● India and Southeast Asia currently account for less than 20% of global emissions from the power sector. But this is set to dramatically

change over the next 25 years as over 200GW of coal-fired power plants are built in the region.

● We forecast India and Southeast Asia to account for almost 40% of global emissions from the power sector by 2040. Over the next 25

years, cumulative power sector emissions in India and Southeast Asia will almost equal that of China.

● We expect China’s emissions to peak before 2030, but for India and Southeast Asia’s emissions to continue to rise through 2040. If

global emissions growth is to be brought under control, it is crucial to address growth in India and Southeast Asia.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2015 2020 2025 2030 2035 2040

RoW

EMEA

US

China

SE Asia

India

0

20

40

60

80

100

120

2015 2020 2025 2030 2035 2040

India +SE Asia

China

US

EMEA

RoW

Source: Bloomberg New Energy Finance

POWER SECTOR EMISSIONS BY REGION, 2015-40 CUMULATIVE POWER SECTOR EMISSIONS

BY REGION, 2015-40 (GTCO2E)

COP21: 10 Things the Negotiators Need to Know – 23 November 2015

5

0.1

1

10

100

1 10 100 1,000 10,000 100,000 1,000,000

Experience curve Historic prices (Maycock) Chinese c-Si module prices (BNEF)

1976

1985

2003

2012

Cumulative capacity (MW)

2015

Source: Bloomberg New Energy Finance, Paul MaycockSource: Bloomberg New Energy Finance, Lawrence Berkeley National

Laboratory, ExTool study (Neij et al, 2003), Vestas annual reports

Note: data is inflation corrected to 2014 prices

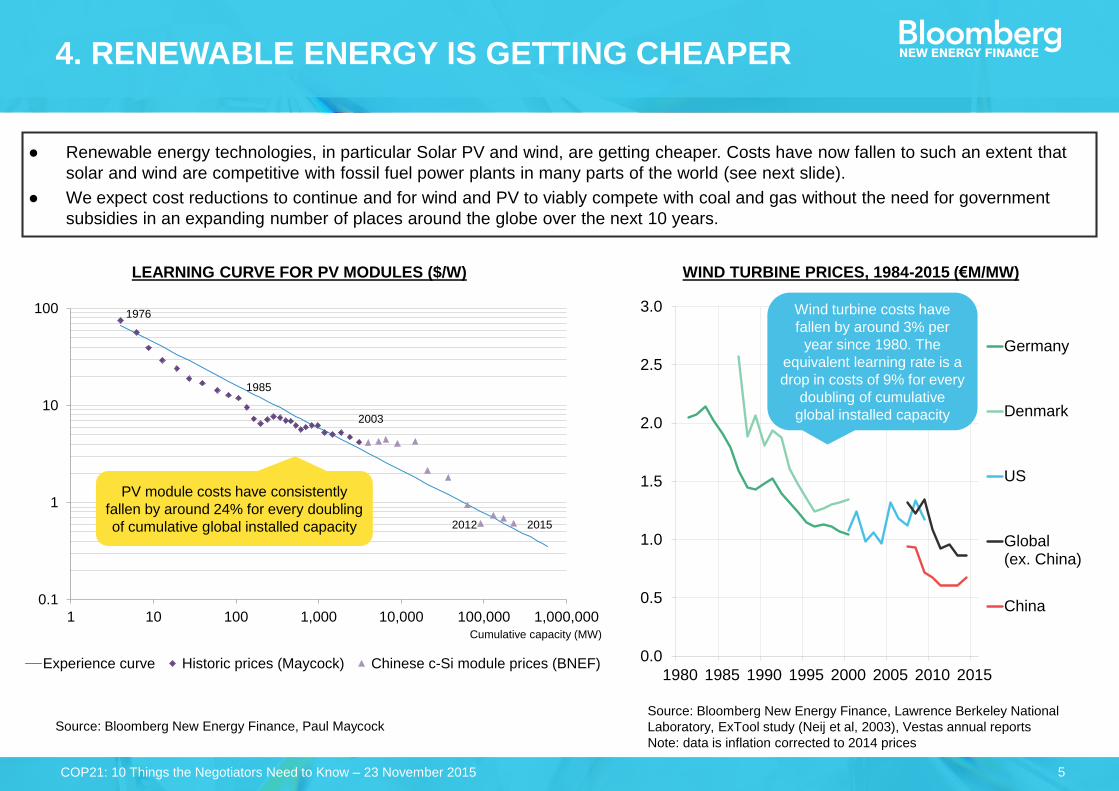

4. RENEWABLE ENERGY IS GETTING CHEAPER

● Renewable energy technologies, in particular Solar PV and wind, are getting cheaper. Costs have now fallen to such an extent that

solar and wind are competitive with fossil fuel power plants in many parts of the world (see next slide).

● We expect cost reductions to continue and for wind and PV to viably compete with coal and gas without the need for government

subsidies in an expanding number of places around the globe over the next 10 years.

0.0

0.5

1.0

1.5

2.0

2.5

3.0

1980 1985 1990 1995 2000 2005 2010 2015

Germany

Denmark

US

Global(ex. China)

China

LEARNING CURVE FOR PV MODULES ($/W) WIND TURBINE PRICES, 1984-2015 (€M/MW)

PV module costs have consistently

fallen by around 24% for every doubling

of cumulative global installed capacity

Wind turbine costs have

fallen by around 3% per

year since 1980. The

equivalent learning rate is a

drop in costs of 9% for every

doubling of cumulative

global installed capacity

COP21: 10 Things the Negotiators Need to Know – 23 November 2015

6

Source: Bloomberg New Energy Finance

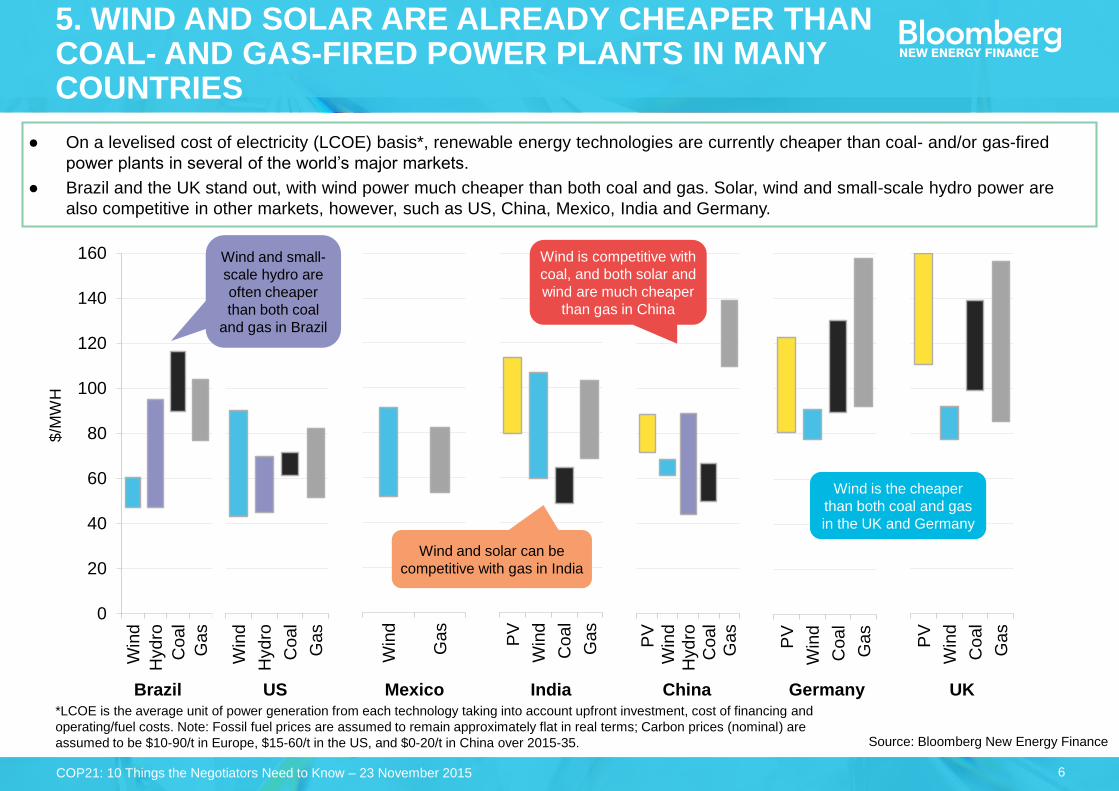

5. WIND AND SOLAR ARE ALREADY CHEAPER THAN COAL- AND GAS-FIRED POWER PLANTS IN MANY COUNTRIES

● On a levelised cost of electricity (LCOE) basis*, renewable energy technologies are currently cheaper than coal- and/or gas-fired

power plants in several of the world’s major markets.

● Brazil and the UK stand out, with wind power much cheaper than both coal and gas. Solar, wind and small-scale hydro power are

also competitive in other markets, however, such as US, China, Mexico, India and Germany.

*LCOE is the average unit of power generation from each technology taking into account upfront investment, cost of financing and

operating/fuel costs. Note: Fossil fuel prices are assumed to remain approximately flat in real terms; Carbon prices (nominal) are

assumed to be $10-90/t in Europe, $15-60/t in the US, and $0-20/t in China over 2015-35.

0

20

40

60

80

100

120

140

160

Win

d

Hydro

Coal

Gas

Brazil

PV

Win

d

Hydro

Coal

Gas

China

PV

Win

d

Coal

Gas

Germany

PV

Win

d

Coal

Gas

India

Win

d

Gas

Mexico

PV

Win

d

Coal

Gas

UK

Win

d

Hydro

Coal

Gas

US

$/M

WH

Wind and small-

scale hydro are

often cheaper

than both coal

and gas in Brazil

Wind and solar can be

competitive with gas in India

Wind is competitive with

coal, and both solar and

wind are much cheaper

than gas in China

Wind is the cheaper

than both coal and gas

in the UK and Germany

COP21: 10 Things the Negotiators Need to Know – 23 November 2015

7

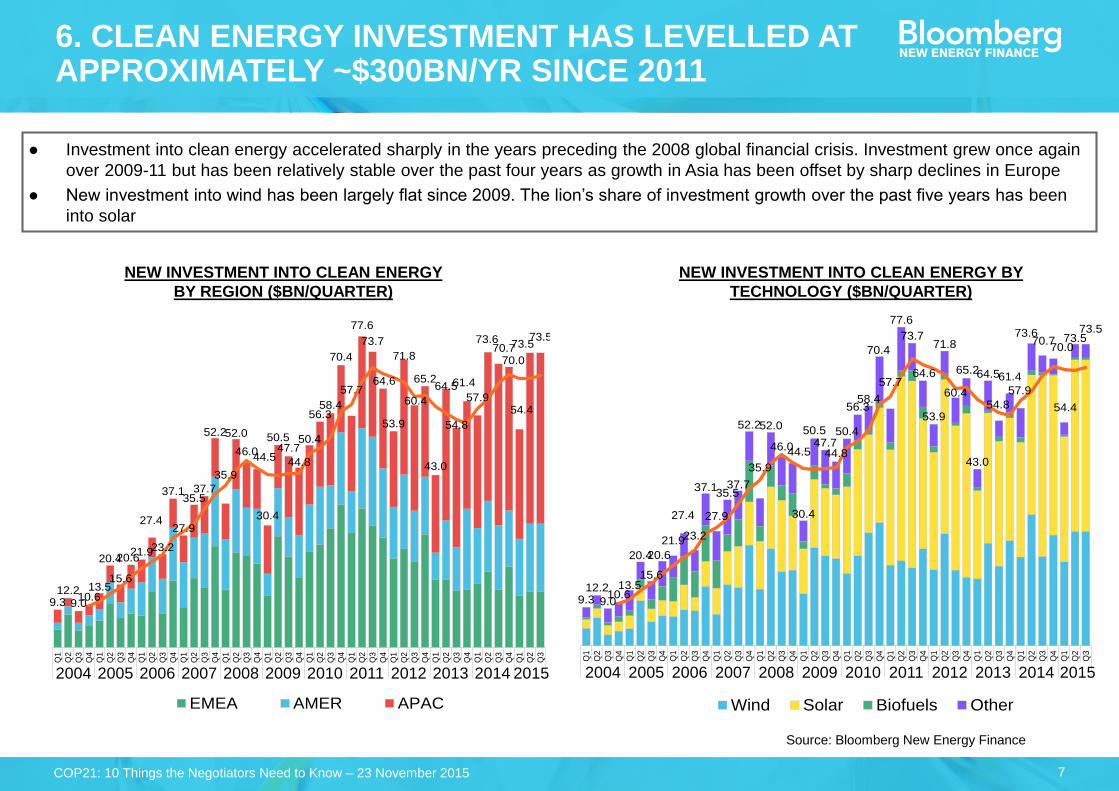

6. CLEAN ENERGY INVESTMENT HAS LEVELLED AT APPROXIMATELY ~$300BN/YR SINCE 2011

● Investment into clean energy accelerated sharply in the years preceding the 2008 global financial crisis. Investment grew once again

over 2009-11 but has been relatively stable over the past four years as growth in Asia has been offset by sharp declines in Europe

● New investment into wind has been largely flat since 2009. The lion’s share of investment growth over the past five years has been

into solar

9.312.2

9.010.6

13.5

20.4

15.6

20.621.9

27.4

23.2

37.1

27.9

35.537.7

52.2

35.9

52.0

46.044.5

30.4

50.547.7

44.8

50.4

56.358.4

70.4

57.7

77.6

73.7

64.6

53.9

71.8

60.4

65.2

43.0

64.5

54.8

61.4

57.9

73.670.7

70.0

54.4

73.573.5

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

EMEA AMER APAC

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

9.312.2

9.010.6

13.5

20.4

15.6

20.6

21.9

27.4

23.2

37.1

27.9

35.537.7

52.2

35.9

52.0

46.044.5

30.4

50.547.7

44.8

50.4

56.358.4

70.4

57.7

77.6

73.7

64.6

53.9

71.8

60.4

65.2

43.0

64.5

54.8

61.4

57.9

73.670.7

70.0

54.4

73.573.5

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Wind Solar Biofuels Other

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

NEW INVESTMENT INTO CLEAN ENERGY

BY REGION ($BN/QUARTER)

NEW INVESTMENT INTO CLEAN ENERGY BY

TECHNOLOGY ($BN/QUARTER)

Source: Bloomberg New Energy Finance

COP21: 10 Things the Negotiators Need to Know – 23 November 2015

8

Source: Bloomberg New Energy Finance

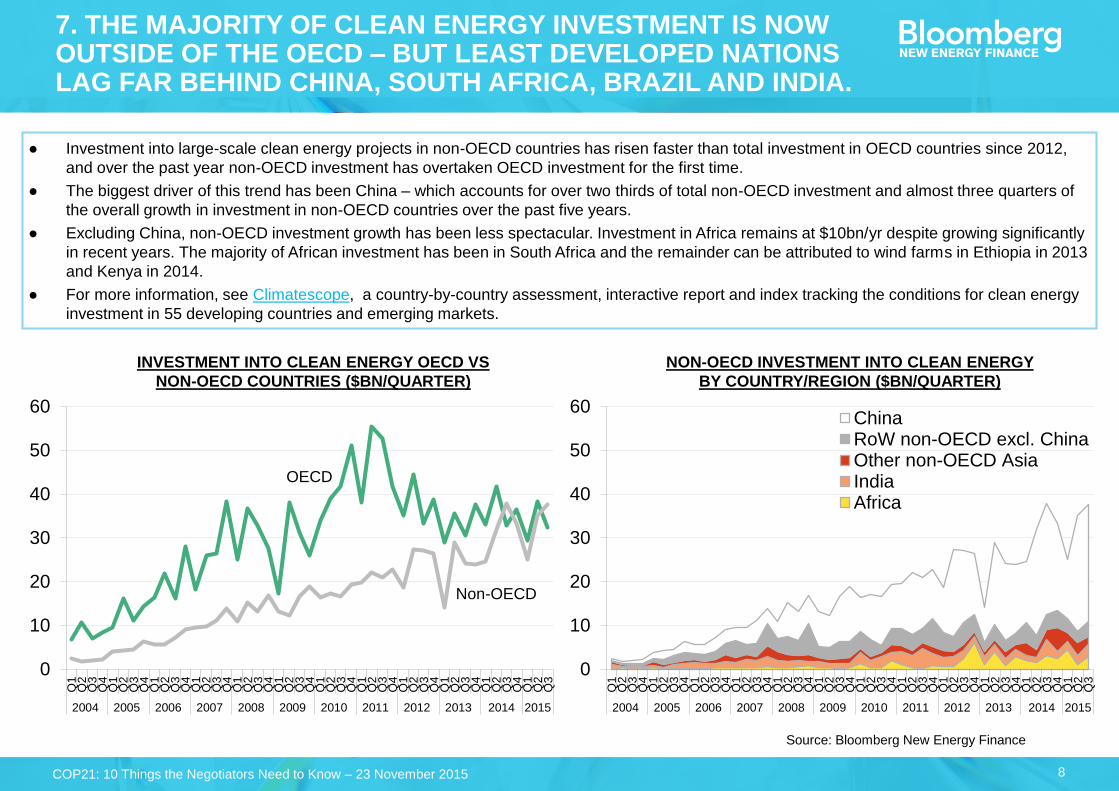

7. THE MAJORITY OF CLEAN ENERGY INVESTMENT IS NOW OUTSIDE OF THE OECD – BUT LEAST DEVELOPED NATIONS LAG FAR BEHIND CHINA, SOUTH AFRICA, BRAZIL AND INDIA.

● Investment into large-scale clean energy projects in non-OECD countries has risen faster than total investment in OECD countries since 2012,

and over the past year non-OECD investment has overtaken OECD investment for the first time.

● The biggest driver of this trend has been China – which accounts for over two thirds of total non-OECD investment and almost three quarters of

the overall growth in investment in non-OECD countries over the past five years.

● Excluding China, non-OECD investment growth has been less spectacular. Investment in Africa remains at $10bn/yr despite growing significantly

in recent years. The majority of African investment has been in South Africa and the remainder can be attributed to wind farms in Ethiopia in 2013

and Kenya in 2014.

● For more information, see Climatescope, a country-by-country assessment, interactive report and index tracking the conditions for clean energy

investment in 55 developing countries and emerging markets.

INVESTMENT INTO CLEAN ENERGY OECD VS

NON-OECD COUNTRIES ($BN/QUARTER)

NON-OECD INVESTMENT INTO CLEAN ENERGY

BY COUNTRY/REGION ($BN/QUARTER)

0

10

20

30

40

50

60

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

0

10

20

30

40

50

60

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

ChinaRoW non-OECD excl. ChinaOther non-OECD AsiaIndiaAfrica

OECD

Non-OECD

COP21: 10 Things the Negotiators Need to Know – 23 November 2015

9

0

10

20

30

40

50

60

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

South-South

North-South

North-North

0

10

20

30

40

50

60

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

0

10

20

30

40

50

60

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Source: Bloomberg New Energy Finance

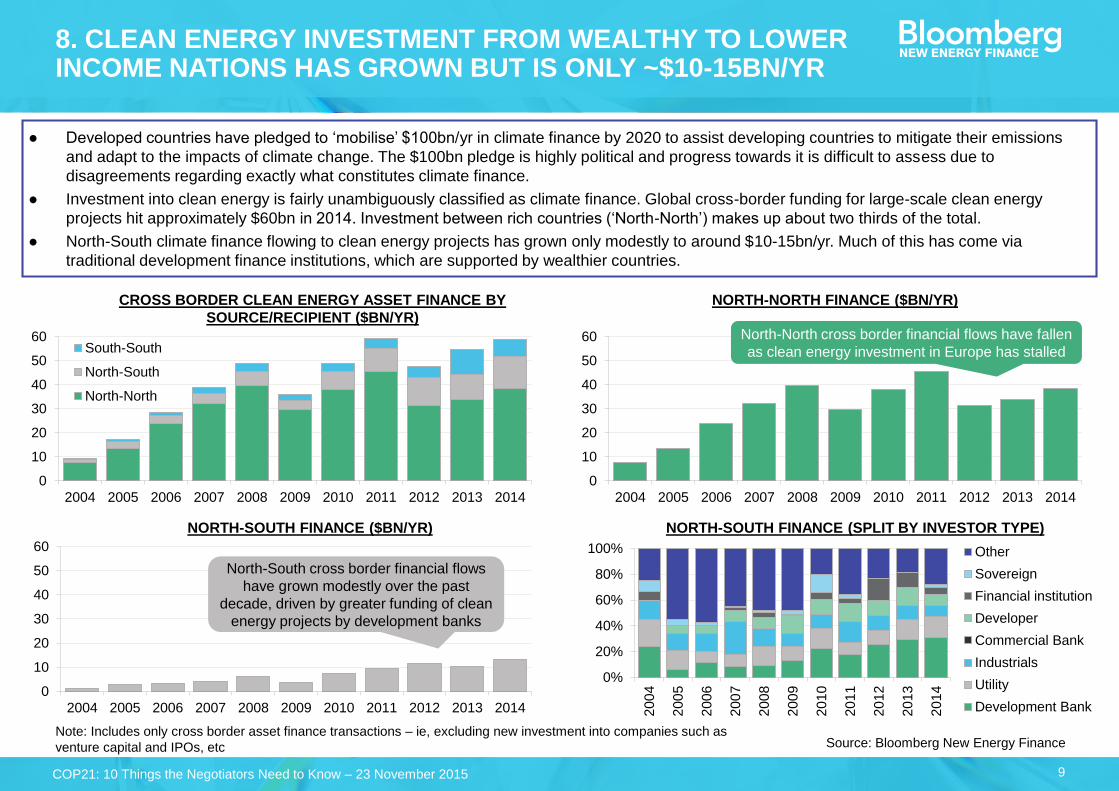

8. CLEAN ENERGY INVESTMENT FROM WEALTHY TO LOWER INCOME NATIONS HAS GROWN BUT IS ONLY ~$10-15BN/YR

● Developed countries have pledged to ‘mobilise’ $100bn/yr in climate finance by 2020 to assist developing countries to mitigate their emissions

and adapt to the impacts of climate change. The $100bn pledge is highly political and progress towards it is difficult to assess due to

disagreements regarding exactly what constitutes climate finance.

● Investment into clean energy is fairly unambiguously classified as climate finance. Global cross-border funding for large-scale clean energy

projects hit approximately $60bn in 2014. Investment between rich countries (‘North-North’) makes up about two thirds of the total.

● North-South climate finance flowing to clean energy projects has grown only modestly to around $10-15bn/yr. Much of this has come via

traditional development finance institutions, which are supported by wealthier countries.

Note: Includes only cross border asset finance transactions – ie, excluding new investment into companies such as

venture capital and IPOs, etc

CROSS BORDER CLEAN ENERGY ASSET FINANCE BY

SOURCE/RECIPIENT ($BN/YR)

NORTH-NORTH FINANCE ($BN/YR)

NORTH-SOUTH FINANCE ($BN/YR) NORTH-SOUTH FINANCE (SPLIT BY INVESTOR TYPE)

COP21: 10 Things the Negotiators Need to Know – 23 November 2015

North-North cross border financial flows have fallen

as clean energy investment in Europe has stalled

North-South cross border financial flows

have grown modestly over the past

decade, driven by greater funding of clean

energy projects by development banks

0%

20%

40%

60%

80%

100%

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

Other

Sovereign

Financial institution

Developer

Commercial Bank

Industrials

Utility

Development Bank

10

50%

100%

150%

200%

250%

2015 2020 2025 2030 2035 2040

50%

100%

150%

200%

250%

2015 2020 2025 2030 2035 2040

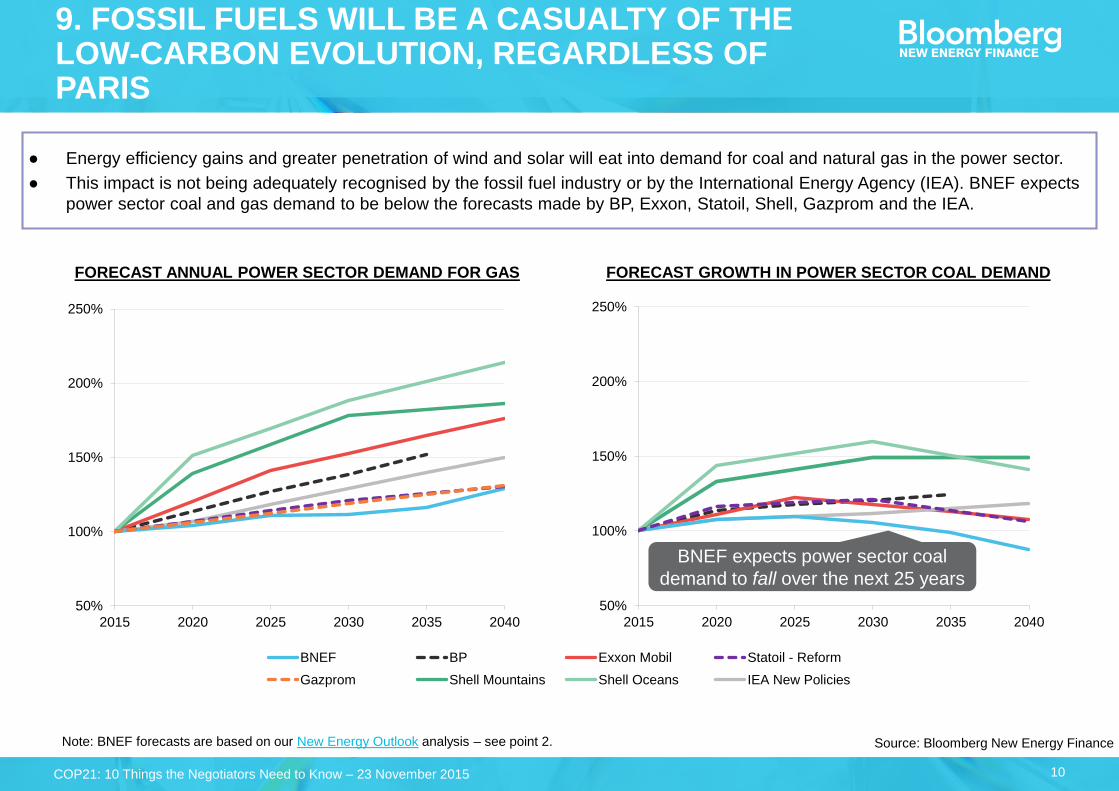

9. FOSSIL FUELS WILL BE A CASUALTY OF THE LOW-CARBON EVOLUTION, REGARDLESS OF PARIS

● Energy efficiency gains and greater penetration of wind and solar will eat into demand for coal and natural gas in the power sector.

● This impact is not being adequately recognised by the fossil fuel industry or by the International Energy Agency (IEA). BNEF expects

power sector coal and gas demand to be below the forecasts made by BP, Exxon, Statoil, Shell, Gazprom and the IEA.

Source: Bloomberg New Energy Finance

FORECAST ANNUAL POWER SECTOR DEMAND FOR GAS FORECAST GROWTH IN POWER SECTOR COAL DEMAND

BNEF expects power sector coal

demand to fall over the next 25 years

Note: BNEF forecasts are based on our New Energy Outlook analysis – see point 2.

0%50%100%150%200%250%

2015 2020 2025 2030 2035 2040

BNEF BP Exxon Mobil Statoil - Reform

Gazprom Shell Mountains Shell Oceans IEA New Policies

COP21: 10 Things the Negotiators Need to Know – 23 November 2015

11

Source: Bloomberg New Energy Finance

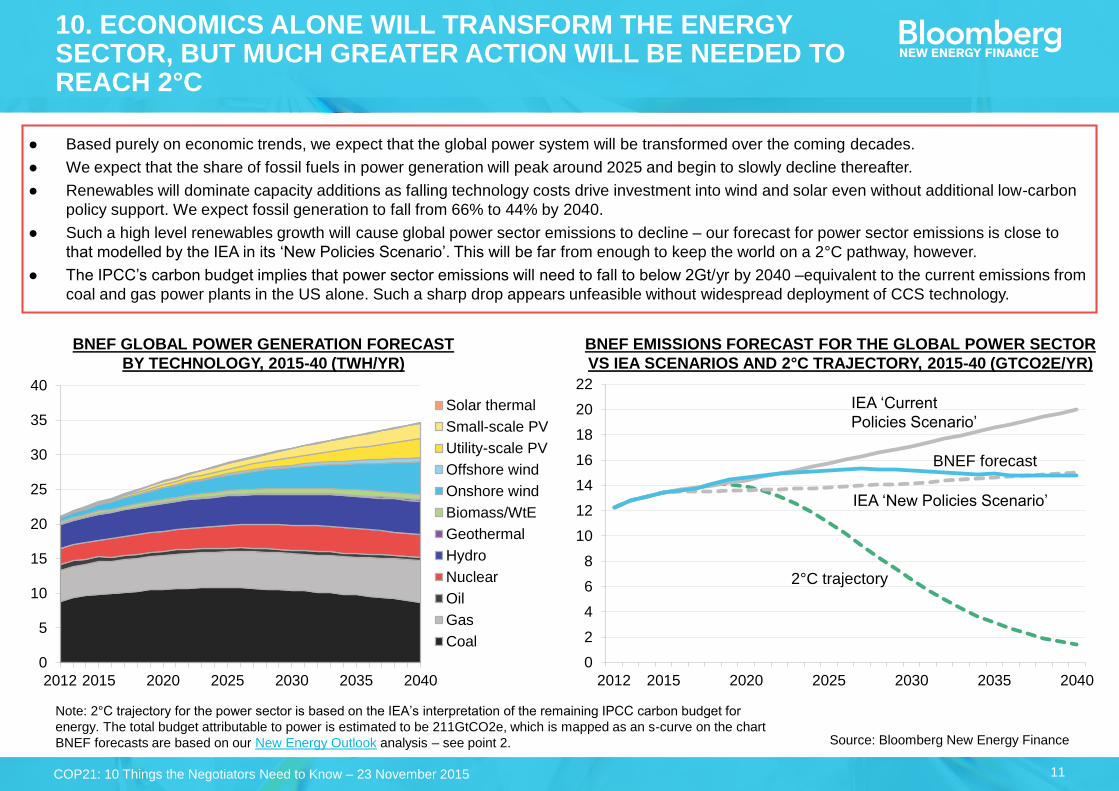

10. ECONOMICS ALONE WILL TRANSFORM THE ENERGY SECTOR, BUT MUCH GREATER ACTION WILL BE NEEDED TO REACH 2°C

● Based purely on economic trends, we expect that the global power system will be transformed over the coming decades.

● We expect that the share of fossil fuels in power generation will peak around 2025 and begin to slowly decline thereafter.

● Renewables will dominate capacity additions as falling technology costs drive investment into wind and solar even without additional low-carbon

policy support. We expect fossil generation to fall from 66% to 44% by 2040.

● Such a high level renewables growth will cause global power sector emissions to decline – our forecast for power sector emissions is close to

that modelled by the IEA in its ‘New Policies Scenario’. This will be far from enough to keep the world on a 2°C pathway, however.

● The IPCC’s carbon budget implies that power sector emissions will need to fall to below 2Gt/yr by 2040 –equivalent to the current emissions from

coal and gas power plants in the US alone. Such a sharp drop appears unfeasible without widespread deployment of CCS technology.

Note: 2°C trajectory for the power sector is based on the IEA’s interpretation of the remaining IPCC carbon budget for

energy. The total budget attributable to power is estimated to be 211GtCO2e, which is mapped as an s-curve on the chart

BNEF forecasts are based on our New Energy Outlook analysis – see point 2.

0

5

10

15

20

25

30

35

40

2012 2015 2020 2025 2030 2035 2040

Solar thermal

Small-scale PV

Utility-scale PV

Offshore wind

Onshore wind

Biomass/WtE

Geothermal

Hydro

Nuclear

Oil

Gas

Coal

BNEF GLOBAL POWER GENERATION FORECAST

BY TECHNOLOGY, 2015-40 (TWH/YR)

BNEF EMISSIONS FORECAST FOR THE GLOBAL POWER SECTOR

VS IEA SCENARIOS AND 2°C TRAJECTORY, 2015-40 (GTCO2E/YR)

0

2

4

6

8

10

12

14

16

18

20

22

2012 2015 2020 2025 2030 2035 2040

BNEF forecast

IEA ‘Current

Policies Scenario’

2°C trajectory

IEA ‘New Policies Scenario’

COP21: 10 Things the Negotiators Need to Know – 23 November 2015

12

This publication is the copyright of Bloomberg New Energy Finance. No portion of this document may be photocopied,

reproduced, scanned into an electronic system or transmitted, forwarded or distributed in any way without prior consent of

Bloomberg New Energy Finance.

The information contained in this publication is derived from carefully selected sources we believe are reasonable. We do

not guarantee its accuracy or completeness and nothing in this document shall be construed to be a representation of such

a guarantee. Any opinions expressed reflect the current judgment of the author of the relevant article or features, and does

not necessarily reflect the opinion of Bloomberg New Energy Finance, Bloomberg Finance L.P., Bloomberg L.P. or any of

their affiliates ("Bloomberg"). The opinions presented are subject to change without notice. Bloomberg accepts no

responsibility for any liability arising from use of this document or its contents. Nothing herein shall constitute or be

construed as an offering of financial instruments, or as investment advice or recommendations by Bloomberg of an

investment strategy or whether or not to "buy," "sell" or "hold" an investment.

COPYRIGHT AND DISCLAIMER

Unique analysis, tools and data for decision-makers

driving change in the energy system

MARKETS Renewable Energy

Energy Smart Technologies

Advanced Transport

Gas

Carbon and RECs

SERVICESAmericas Service

Asia Pacific Service

EMEA Service

Applied Research

Events and Workshops

Richard Chatterton, CFA