Embed Size (px)

Citation preview

Franke Aviation & Transportation ConsultingFranke Aviation & Transportation Consulting

DE/EN

COPYRIGHT 2010 WWW.FRANKE-AVIATION.COM

FORWARDING & LOGISTICS RAIL POSTAL & EXPRESS DELIVERY OEMs, SUPPLIERS, SERVICE PROVIDERSAVIATION

Contribution of Network Carriers and Low Cost Carriersto the development of (regional) air transport services

Dr. Markus Franke, Founder and Owner of FATC

1st Cracow Aviation Conference: „Managing Regional Airports in Competitive Environment“

Cracow, March 10, 2011

Presentation Cracow Aviation Conference, 03/2011Page 1

Franke Aviation & Transportation Consulting

COPYRIGHT 2010 WWW.FRANKE-AVIATION.COM

Main topics of today‘s presentation

What are the prospects for Poland‘s aviation sector, and what arethe shares of relevant business segments?

Which are feasible objectives for regional airports, and how willWAW / CAP interfere with them?

How can Network Carriers and Low Cost Carriers contribute to asustainable development of Polish regional airports?

What are critical success factors of Network Carriers and Low CostCarriers in Poland, and which actions can be taken to foster them?

1

2

3

4

Presentation Cracow Aviation Conference, 03/2011Page 2

Franke Aviation & Transportation Consulting

COPYRIGHT 2010 WWW.FRANKE-AVIATION.COM

Poland‘s air traffic is emerging – however, there is still a gapbetween overall wealth trajectory and propensity to fly

1

Source: Eurostat, www.finanzwirtschafter.de, Statistics of International Monetary Funds, www.skyscrapercity.com

40,00030,00020,00010,000

UK

Germany

Poland

CzechRepublic

Portugal

Spain

Italy France

Romania

Slovenia

0

Outboundflightsper capita(log, 2009)

0.01

0.1

1.0

10

GDP per capita (USD, 2009, Purchase power parity)

Propensity to fly in selected (European) countries (2009)

Empiricrange

Hungary

Mid-term gap:10…12 Mn pax p.a.

Passenger growth:+13 % p.a. 2002-2010

Presentation Cracow Aviation Conference, 03/2011Page 3

Franke Aviation & Transportation Consulting

COPYRIGHT 2010 WWW.FRANKE-AVIATION.COM

Poland‘s air traffic is emerging – however, there is still a gapbetween overall wealth trajectory and propensity to fly

1

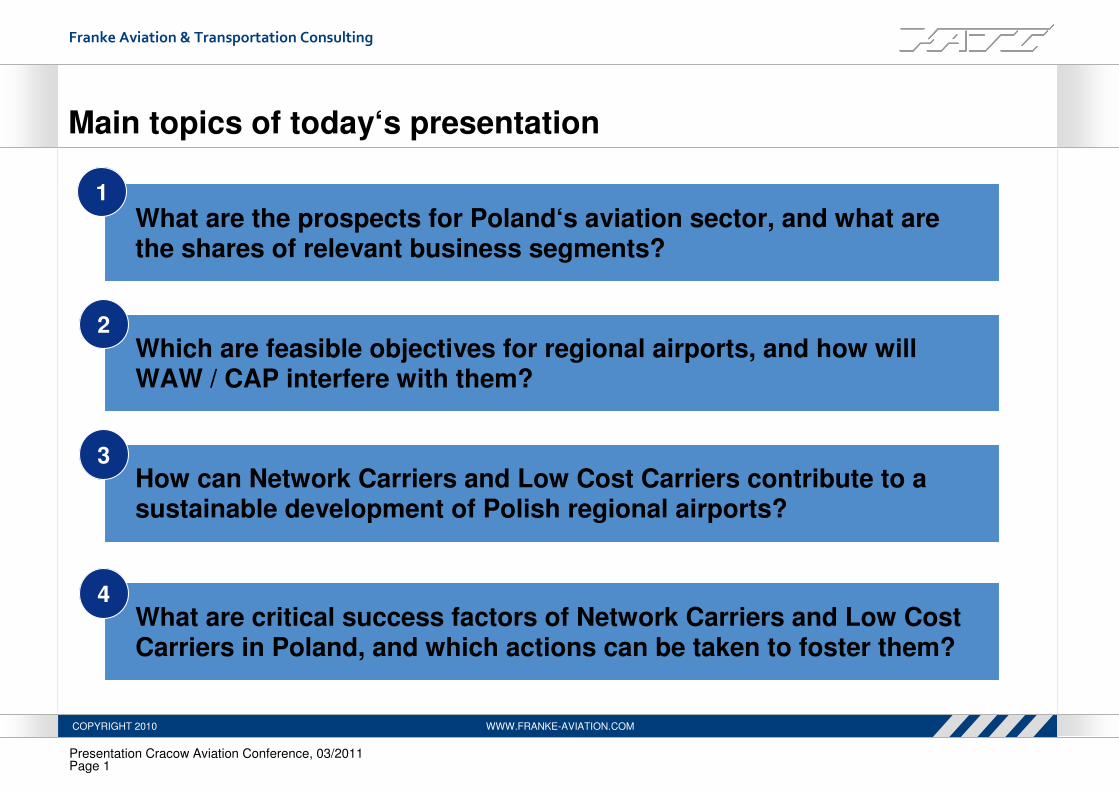

● Poland‘s economy is continuously growing, even throughout the 2008/2009 financial crisis

- GDP (2002 – 2010) + 42 % (+ 18 % price-adjusted)

- CAGR (GDP 2002 – 2010) = 4.5 % (+2 % price-adjusted)

- CAGR (GDP per capity 2002 – 2010) > 2 % (price-adjusted)

● Air traffic has grown even more

- CAGR of passenger numbers (2005 – 2010) = +13% (11.3 Mn � 20.7 Mn)

● However, affinity to fly of Polish citizens is still disproportionately low relative to mature

European economies (e.g., Germany):

- Poland has 47% in terms of inhabitants compared to Germany

- Poland‘s GDP per capita is around 46% of the German number (adjusted by purchase power parity)

- However, Poland‘s airports reported in 2010 only 12% of overall passengers

compared to Germany (20.6 Mn : 167 Mn)

- With the same travel / buying behaviour like in Germany, Polish citizens would create

36 Mn departures (wealth-level-adjusted)

Consequently, there is a gap of > 15 Mn passengers or +74% to be tackled in the future

Source: Eurostat, www.finanzwirtschafter.de, Statistics of International Monetary Funds, www.skyscrapercity.com

BACKUP

Presentation Cracow Aviation Conference, 03/2011Page 4

Franke Aviation & Transportation Consulting

COPYRIGHT 2010 WWW.FRANKE-AVIATION.COM

Although Polish air traffic sector is highly concentrated on top 8 airports, regional airports account for 55% of total passengers

Poznan

Gdansk

Wroclaw

Katowice

LodzZielonaGora

SzczecinSzczytno

Bydogszcz

Rzeszow

Warsaw /CAP

Concentration of passengers at polish airports(2008 in % of total PAX)

0%

20%

40%

60%

80%

100%

Wars

awKra

kow

Katow

ice

Gda

nsk

Wro

claw

Pozna

n

Lodz

Jasi

onka

Gol

enio

wByd

ogsz

czZie

lona

Oth

ers

Top 4 airports~81%

Top 8 airports~97%

Total PAX: 20.7 mn

Source: CAP Project of Polish Ministry of Infrastructure, Oliver Wyman, PwC, DFS, MKmetric

1

Top 6 airports~94%

WAW(45%)

RegionalAirports

(55%)

Krakow

Presentation Cracow Aviation Conference, 03/2011Page 5

Franke Aviation & Transportation Consulting

COPYRIGHT 2010 WWW.FRANKE-AVIATION.COM

Growth of household incomes has boosted charters, which nowgenerate substantial traffic for most airports

1

Source: ULC, Instytut Turystyki ; analyses FATC and Dr. Roman Gurbiel

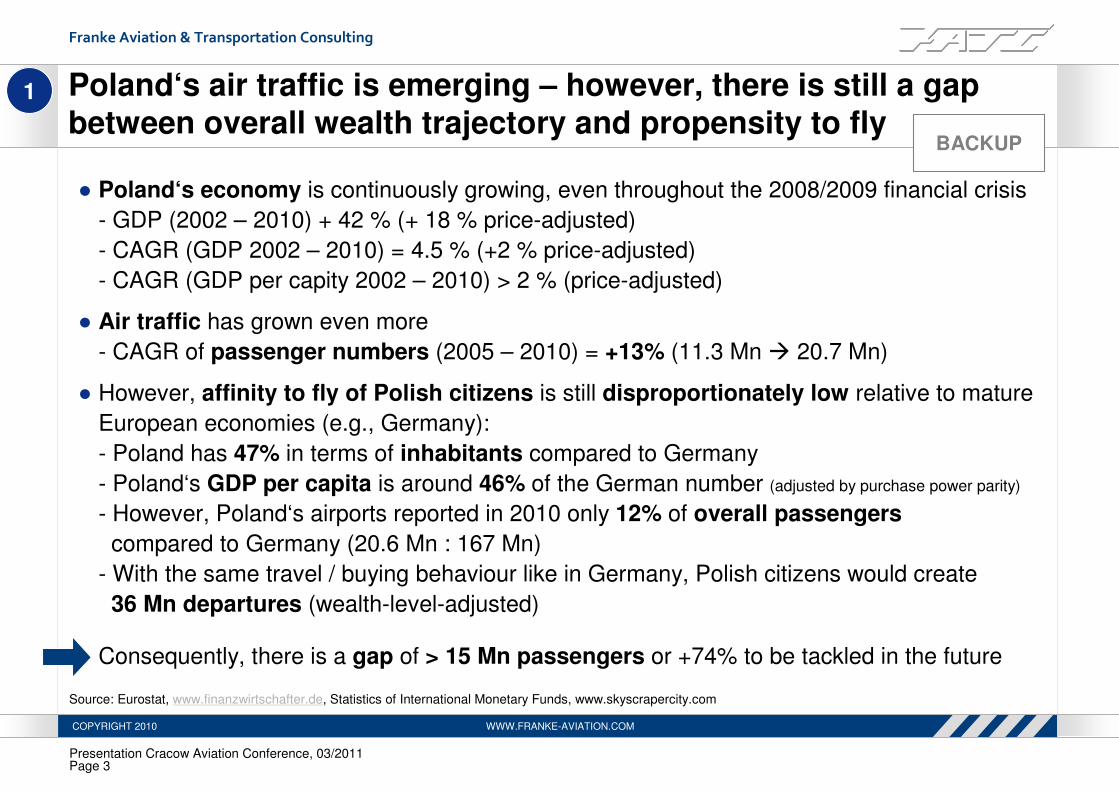

● Regional airports have provided Polish people with easy access to attractive tourism destinations

● Share of Polish charters has grown rapidly from 11% to 16% in 2005-2009

● This trend is expected to continue due to rising incomes and large Poles’s appetite to travel

● Warsaw is the largest charter hub (44% share in 2009), leveraging the region’s wealth and tour operators preferences

● Katowice has emerged as the second strongest charter hub in Poland

8%

8%

24%

14%

35%

22%

6%

8%

8%

11%

16%

7%

26%

16%

27%

16%

8%

22%

9%

8%

16%

0% 10% 20% 30% 40%

Warszawa

Kraków

Katowice

Wrocław

Poznań

Łódź

Gdańsk

Szczecin

Bydgoszcz

Rzeszów

Total Poland

2005 2009

Share of charter traffic

in total traffic (PAX, %)

44%

7%

19%

7%

12%

2%

5%

2%

1%

1%

Share of Polishcharter market (2009)

100%

Presentation Cracow Aviation Conference, 03/2011Page 6

Franke Aviation & Transportation Consulting

COPYRIGHT 2010 WWW.FRANKE-AVIATION.COM

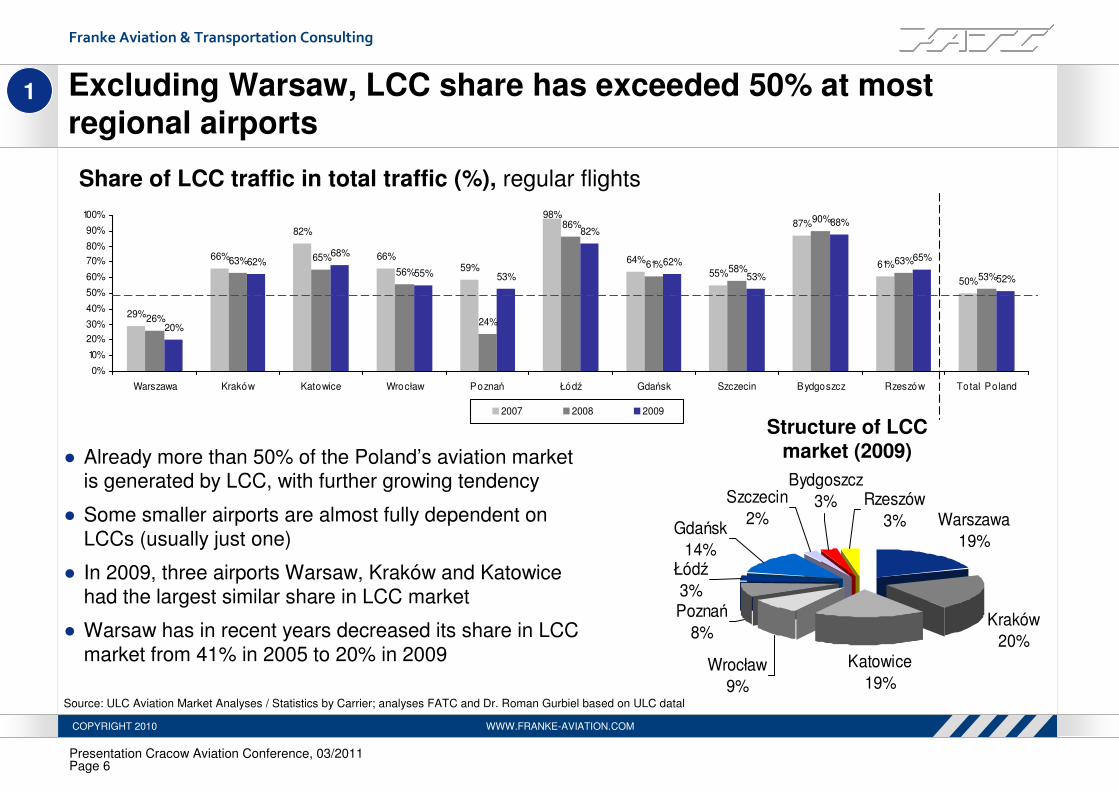

● Already more than 50% of the Poland’s aviation marketis generated by LCC, with further growing tendency

● Some smaller airports are almost fully dependent onLCCs (usually just one)

● In 2009, three airports Warsaw, Kraków and Katowice had the largest similar share in LCC market

● Warsaw has in recent years decreased its share in LCC market from 41% in 2005 to 20% in 2009

29%

66%

82%

66%59%

98%

64%

55%

87%

61%

50%

26%

63% 65%

56%

24%

86%

61% 58%

90%

63%

53%

20%

62%68%

55% 53%

82%

62%

53%

88%

65%

52%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Warszawa Kraków Katowice Wrocław Poznań Łódź Gdańsk Szczecin Bydgoszcz Rzeszów Total Poland

2007 2008 2009

Share of LCC traffic in total traffic (%), regular flights

Warszawa

19%

Kraków

20%Katowice

19%

Łódź

3%

Rzeszów

3%Gdańsk

14%

Bydgoszcz

3%Szczecin

2%

Poznań

8%

Wrocław

9%

Structure of LCCmarket (2009)

Excluding Warsaw, LCC share has exceeded 50% at mostregional airports

1

Source: ULC Aviation Market Analyses / Statistics by Carrier; analyses FATC and Dr. Roman Gurbiel based on ULC datal

Presentation Cracow Aviation Conference, 03/2011Page 7

Franke Aviation & Transportation Consulting

COPYRIGHT 2010 WWW.FRANKE-AVIATION.COM

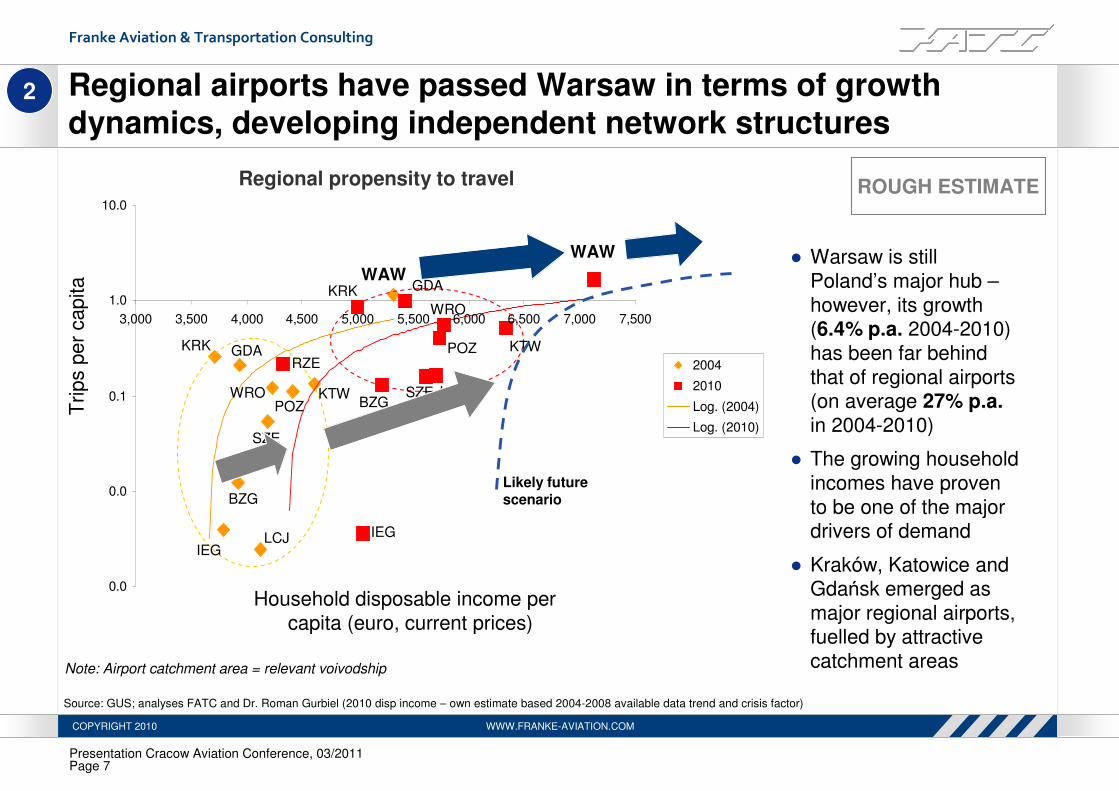

Regional airports have passed Warsaw in terms of growth dynamics, developing independent network structures

2

● Warsaw is still Poland’s major hub –however, its growth (6.4% p.a. 2004-2010) has been far behind that of regional airports(on average 27% p.a.in 2004-2010)

● The growing household incomes have provento be one of the majordrivers of demand

● Kraków, Katowice and Gdańsk emerged as major regional airports, fuelled by attractive catchment areas

Source: GUS; analyses FATC and Dr. Roman Gurbiel (2010 disp income – own estimate based 2004-2008 available data trend and crisis factor)

Note: Airport catchment area = relevant voivodship

ROUGH ESTIMATE

0.0

0.0

0.1

1.0

10.0

3,000 3,500 4,000 4,500 5,000 5,500 6,000 6,500 7,000 7,500

2004

2010

Log. (2004)

Log. (2010)

Household disposable income per capita (euro, current prices)

Trips p

er

capita WAW

WAW

IEG

IEGLCJ

LCJ

KTW

WRO

POZ

KRK GDA

SZEBZG

RZE

KRK GDA

BZG

SZE

WROPOZ

KTW

Likely future scenario

Regional propensity to travel

Presentation Cracow Aviation Conference, 03/2011Page 8

Franke Aviation & Transportation Consulting

COPYRIGHT 2010 WWW.FRANKE-AVIATION.COM

Even if LOT boosts its transfer share in WAW / CAP, the growth dynamics of regional airports will be untapped

2

Source: CAP Project of Polish Ministry of Infrastructure, Oliver Wyman, PwC, DFS, MKmetric

2010 2035

2010 2035

Scenario 1: LOT‘s (low) transfer share remainsconstant (<8%)

Scenario 2: LOT boosts ist transfer share (30%)

20 Mn Pax

20 Mn Pax

+4% p.a.

+4% p.a.

53 Mn Pax

53 Mn Pax

LOT: 7 Mn

(of which

transfer PAX

≈ 600 thsd.)

LOT: 18.6 Mn

(of which

transfer PAX

≈ 1.5 Mn)

LOT: 22.7 Mn(of which

transfer PAX

≈ 5.6 Mn)

● Regional airports had 11…12

Mn passengers in 2010

● LOT is very focused on WAW and contributes only a minor

share to regional airports’ paxnumber

● At 4% annual growth and a

constant transfer share of LOT, regional airports would see

additional 20 Mn pax in 2035

● Assuming that LOT could win additional passengers through

boosting its transfer share in WAW / CAP to 30%, some

passengers could be lost for regional airports

● Even if they would lose all

transfer passengers, they would still see additional 16 Mn pax in 2035 (+ 3.4% p.a.)

ROUGH ESTIMATE

Presentation Cracow Aviation Conference, 03/2011Page 9

Franke Aviation & Transportation Consulting

COPYRIGHT 2010 WWW.FRANKE-AVIATION.COM

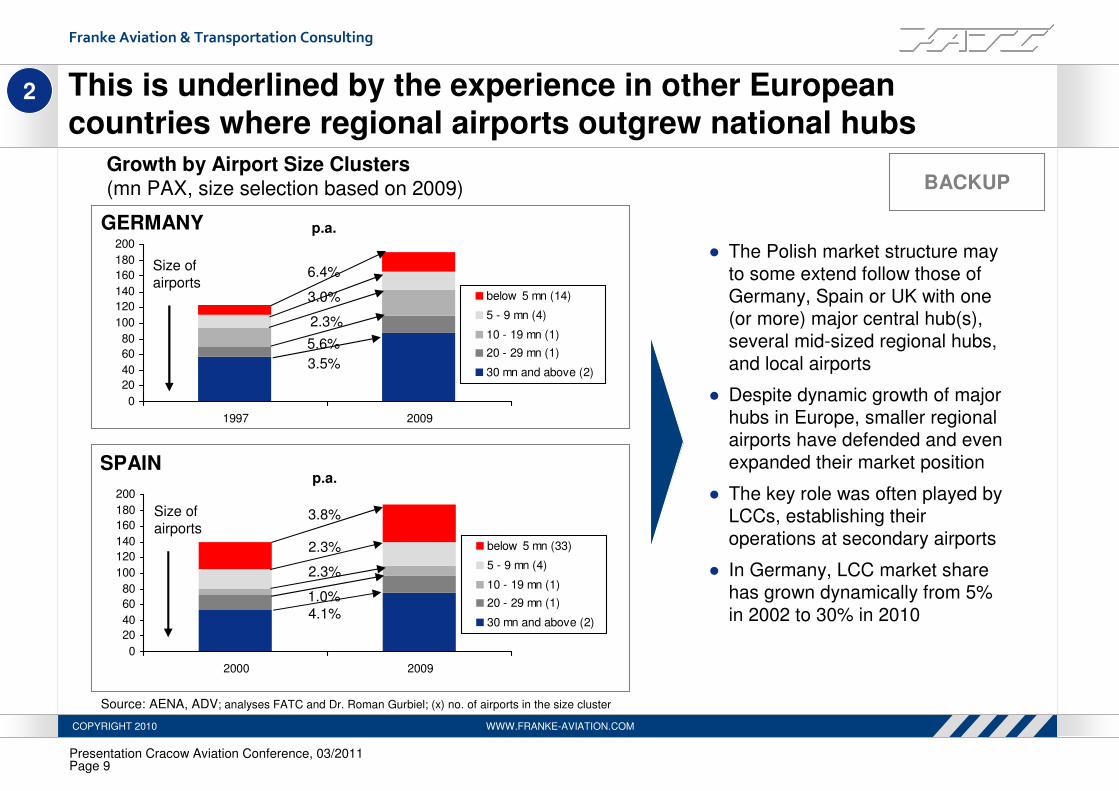

This is underlined by the experience in other European countries where regional airports outgrew national hubs

2

Source: AENA, ADV; analyses FATC and Dr. Roman Gurbiel; (x) no. of airports in the size cluster

GERMANY

SPAIN

● The Polish market structure may to some extend follow those of

Germany, Spain or UK with one(or more) major central hub(s),

several mid-sized regional hubs,

and local airports

● Despite dynamic growth of major

hubs in Europe, smaller regional airports have defended and even

expanded their market position

● The key role was often played by LCCs, establishing their

operations at secondary airports

● In Germany, LCC market share has grown dynamically from 5%

in 2002 to 30% in 2010

0

20

40

60

80

100

120

140

160

180

200

2000 2009

below 5 mn (33)

5 - 9 mn (4)

10 - 19 mn (1)

20 - 29 mn (1)

30 mn and above (2)

p.a.

3.8%

2.3%

2.3%

1.0%

4.1%

0

20

40

60

80

100

120

140

160

180

200

1997 2009

below 5 mn (14)

5 - 9 mn (4)

10 - 19 mn (1)

20 - 29 mn (1)

30 mn and above (2)

p.a.

6.4%

3.0%

2.3%

5.6%

3.5%

Growth by Airport Size Clusters(mn PAX, size selection based on 2009) BACKUP

Size of

airports

Size of

airports

Presentation Cracow Aviation Conference, 03/2011Page 10

Franke Aviation & Transportation Consulting

COPYRIGHT 2010 WWW.FRANKE-AVIATION.COM

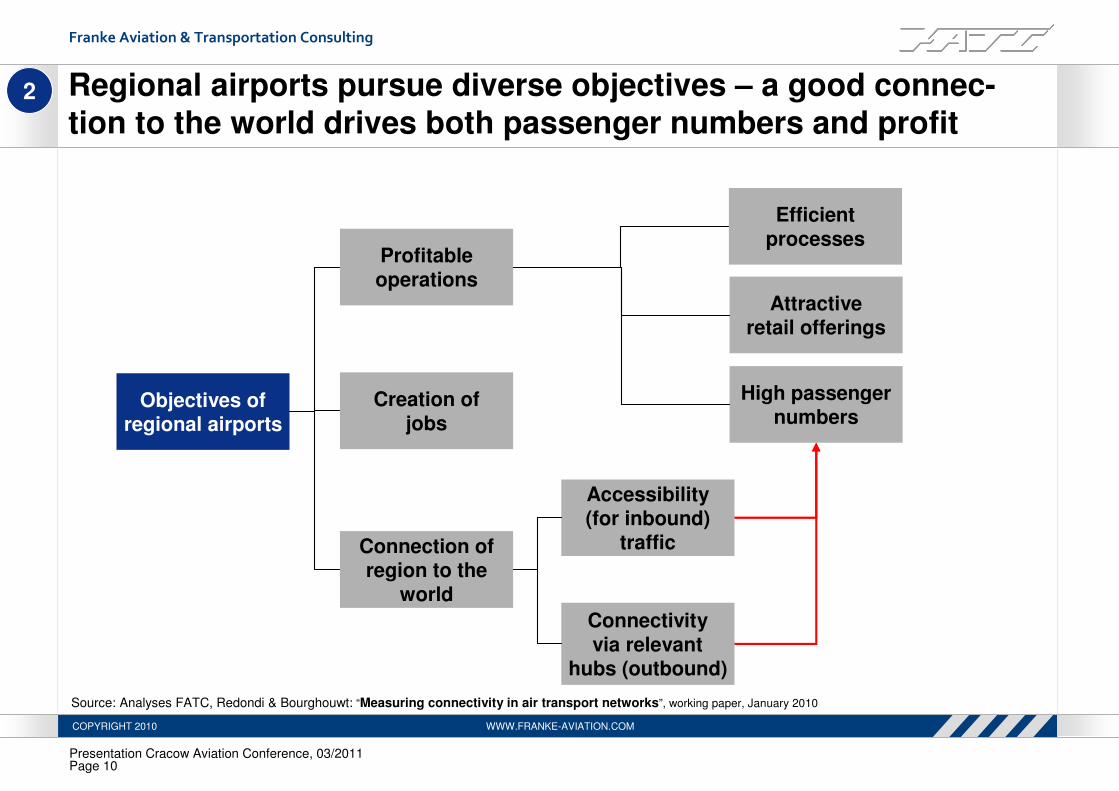

Regional airports pursue diverse objectives – a good connec-tion to the world drives both passenger numbers and profit

2

Objectives ofregional airports

Profitableoperations

Creation ofjobs

Connection ofregion to the

world

High passengernumbers

Attractiveretail offerings

Connectivityvia relevant

hubs (outbound)

Accessibility(for inbound)

traffic

Efficientprocesses

Source: Analyses FATC, Redondi & Bourghouwt: “Measuring connectivity in air transport networks”, working paper, January 2010

Presentation Cracow Aviation Conference, 03/2011Page 11

Franke Aviation & Transportation Consulting

COPYRIGHT 2010 WWW.FRANKE-AVIATION.COM

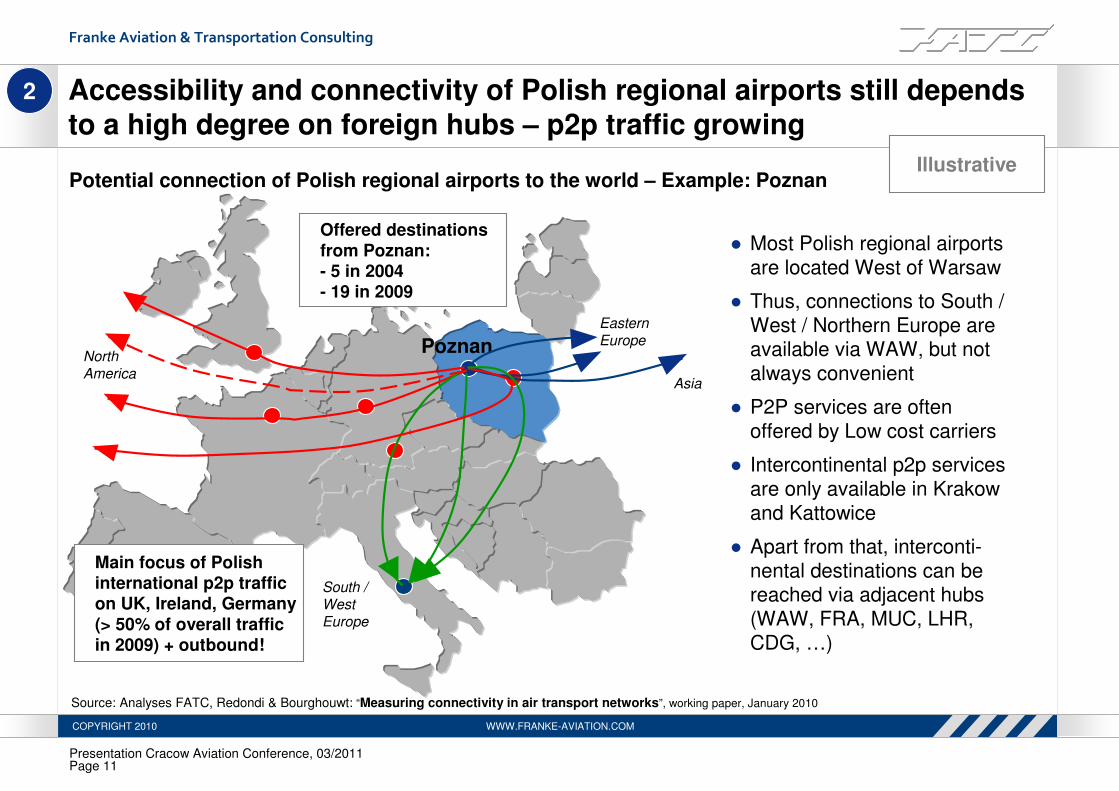

Accessibility and connectivity of Polish regional airports still dependsto a high degree on foreign hubs – p2p traffic growing

Poznan

Asia

Eastern

EuropeNorth

America

South /

West

Europe

IllustrativePotential connection of Polish regional airports to the world – Example: Poznan

● Most Polish regional airportsare located West of Warsaw

● Thus, connections to South / West / Northern Europe areavailable via WAW, but notalways convenient

● P2P services are oftenoffered by Low cost carriers

● Intercontinental p2p servicesare only available in Krakow and Kattowice

● Apart from that, interconti-nental destinations can bereached via adjacent hubs(WAW, FRA, MUC, LHR, CDG, …)

Source: Analyses FATC, Redondi & Bourghouwt: “Measuring connectivity in air transport networks”, working paper, January 2010

2

Offered destinationsfrom Poznan:- 5 in 2004- 19 in 2009

Main focus of Polishinternational p2p trafficon UK, Ireland, Germany(> 50% of overall trafficin 2009) + outbound!

Presentation Cracow Aviation Conference, 03/2011Page 12

Franke Aviation & Transportation Consulting

COPYRIGHT 2010 WWW.FRANKE-AVIATION.COM

Further growth of wealth level and air traffic demand in Poland will in any case foster expansion of regional airports

2

● Total number of offered destinations from regional airports has increased from

34 to 135 (2004-2009)

(summer season; winterseason: from 12 to 132)

● Connection to the worldand growth of passengernumbers go hand in hand

● Even an increase of transfer

traffic via adjacent hubs(WAW / CAP, BBI, FRA, …)

should not harm O&D demand

● O&D network development

will however strongly depend on the local demand

32

913

4 5 2 1

68

30 30

21 19 18

5 5 4 3

0

10

20

30

40

50

60

70

80

Warszawa Kraków Katowice Gdańsk Poznań Wrocław Bydgoszcz Rzeszów Łódź Szczecin

Summer 2004 Summer 2009

Offered Destinations (regular flights, summer season, 2004 vs. 2009)

WAW 2004

level

Likely future scenario

Major

Poland’s hub;

increasing

role of transfer

and intercont

traffic

Stand-alone

O&D spoke,

potential for

some transfer

traffic in future

Medium O&D

operations,

hub-feeding

Niche O&D

operations,

hub-feeding

Source: ULC; analyses FATC and Dr. Roman Gurbiel

BACKUP

Presentation Cracow Aviation Conference, 03/2011Page 13

Franke Aviation & Transportation Consulting

COPYRIGHT 2010 WWW.FRANKE-AVIATION.COM

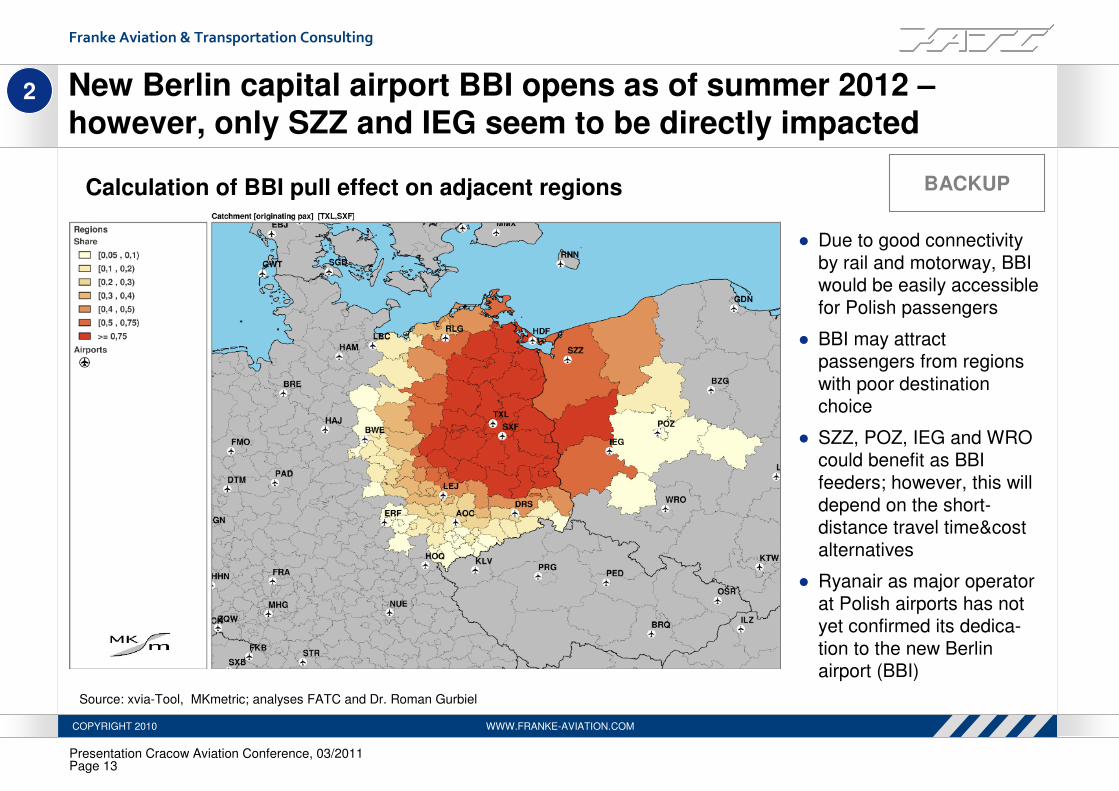

New Berlin capital airport BBI opens as of summer 2012 –however, only SZZ and IEG seem to be directly impacted

2

Source: xvia-Tool, MKmetric; analyses FATC and Dr. Roman Gurbiel

BACKUP

● Due to good connectivity

by rail and motorway, BBI would be easily accessible

for Polish passengers

● BBI may attractpassengers from regions

with poor destination choice

● SZZ, POZ, IEG and WRO could benefit as BBI

feeders; however, this will

depend on the short-distance travel time&cost

alternatives

● Ryanair as major operator

at Polish airports has notyet confirmed its dedica-

tion to the new Berlin airport (BBI)

Calculation of BBI pull effect on adjacent regions

Presentation Cracow Aviation Conference, 03/2011Page 14

Franke Aviation & Transportation Consulting

COPYRIGHT 2010 WWW.FRANKE-AVIATION.COM

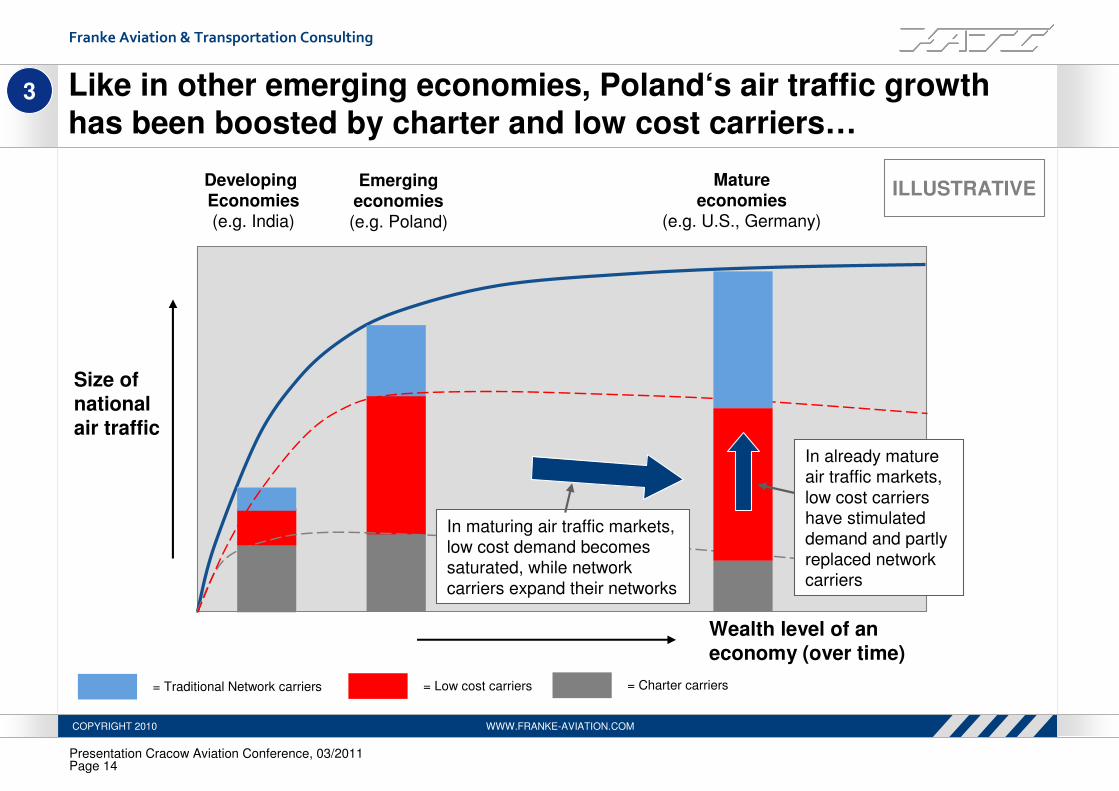

Like in other emerging economies, Poland‘s air traffic growth has been boosted by charter and low cost carriers…

= Traditional Network carriers = Low cost carriers = Charter carriers

3

Matureeconomies

(e.g. U.S., Germany)

Size ofnationalair traffic

Wealth level of aneconomy (over time)

Emergingeconomies(e.g. Poland)

In maturing air traffic markets, low cost demand becomessaturated, while network

carriers expand their networks

In already matureair traffic markets,

low cost carriershave stimulateddemand and partly

replaced networkcarriers

ILLUSTRATIVEDevelopingEconomies(e.g. India)

Presentation Cracow Aviation Conference, 03/2011Page 15

Franke Aviation & Transportation Consulting

COPYRIGHT 2010 WWW.FRANKE-AVIATION.COM

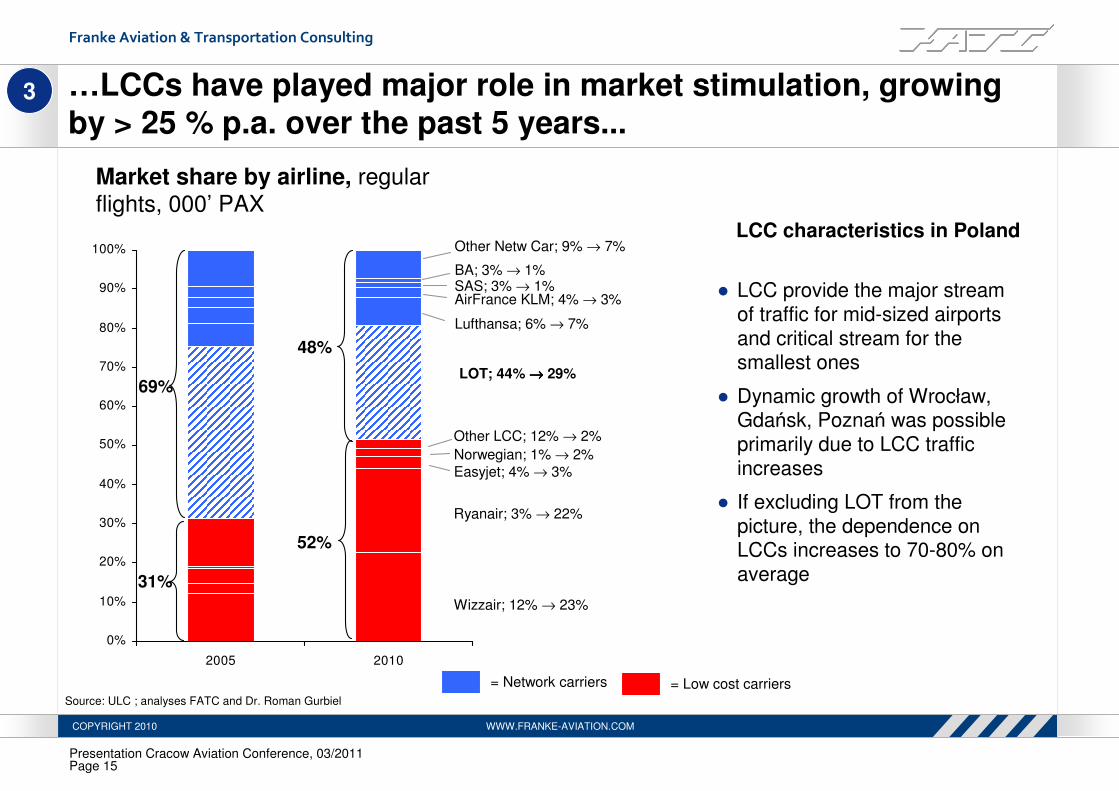

…LCCs have played major role in market stimulation, growingby > 25 % p.a. over the past 5 years...

3

Market share by airline, regular flights, 000’ PAX

Source: ULC ; analyses FATC and Dr. Roman Gurbiel

LCC characteristics in Poland

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2005 2010

Other LCC; 12% → 2%

Norwegian; 1% → 2%

Easyjet; 4% → 3%

Ryanair; 3% → 22%

Wizzair; 12% → 23%

BA; 3% → 1%SAS; 3% → 1%AirFrance KLM; 4% → 3%

Lufthansa; 6% → 7%

LOT; 44% →→→→ 29%

Other Netw Car; 9% → 7%

69%

31%

52%

48%

= Network carriers = Low cost carriers

● LCC provide the major stream of traffic for mid-sized airports and critical stream for the smallest ones

● Dynamic growth of Wrocław, Gdańsk, Poznań was possible primarily due to LCC traffic increases

● If excluding LOT from the picture, the dependence on LCCs increases to 70-80% on average

Presentation Cracow Aviation Conference, 03/2011Page 16

Franke Aviation & Transportation Consulting

COPYRIGHT 2010 WWW.FRANKE-AVIATION.COM

…however, Poland‘s flag carrier LOT has still considerablegrowth prospects

3

Source: ULC ; analyses FATC and Dr. Roman Gurbiel

Growth prospects for LOT (and other network carriers)

• LOT‘s national market share has steadily decreased

• Up to now, Polish people are still reluctant – despite increasing wealth level

– to pay premium fares for air travel � they love Low cost carriers

• Thus, LOT focuses on few international markets with limited intercontinentaluplift, supported by domestic network

• With an expected further growth of wealth level, Polish citizens are likely to demand more air travel capacities, both nationally and internationally

• Network carriers like LOT are suited to satisfy this growing demand, particularly in the premium and intercontinental segment

Presentation Cracow Aviation Conference, 03/2011Page 17

Franke Aviation & Transportation Consulting

COPYRIGHT 2010 WWW.FRANKE-AVIATION.COM

There are no “good” or “bad” airlines – both Low cost and Network carriers can contribute to the development of regional airports

3

Low cost carriers Network carriers

Wizz Air, easyJet, Ryanair,Germanwings, …

LOT, Lufthansa, Air France /KLM, British Airways, …

Examples in Poland

• Presence: strong (> 60% market share)

• Commitment: mediocre (most

stations – except Wizz Air) are abroad

• Presence: poor (some hub feed;

international flights only in KRK + KTW)

• Commitment: medium (some local

planes and jobs)

Presence in / commit-ment to regional airports(local station � jobs)

• Domestic: most major city pairs• Continental: numerous routes

• Intercontinental: None

• Domestic: some city pairs + feedertraffic to WAW

• Continental: some routes P2P,more via WAW, FRA, MUC, CDG

Intercontinental: a few routes viaWAW, FRA, MUC, CDG, …

Destination portfolio(connection to the world)

• Medium (additional bases in Poland

+ European city pairs)

• High (stimulation of additional – premium –

demand for P2P and transfer traffic, esp.

Internationally)

Passenger potential(growth options)

• Airport fees: poor (LCCs are very tough

bargainers)

• Retail: limited (bargainer passengers)

• Airport fees: good• Retail: good (� esp. International

passengers, inbound)

Economic potential(fees and revenues)

Characteristics of Low cost & Network carriers from the perspective of regional airports

Presentation Cracow Aviation Conference, 03/2011Page 18

Franke Aviation & Transportation Consulting

COPYRIGHT 2010 WWW.FRANKE-AVIATION.COM

Example LCC: Ryanair uses a uniform approach to develop itsnetwork in Poland, leveraging e.g. large commuter flows

3

Kraków

Wrocław

Gdańsk

Poznań

Rzeszów

Szczecin

Bydgoszcz

Katowice

Łódź

Thin network is the result of strong Wizzair position

Source: Ryanair (as of March 2011)

BACKUP

Presentation Cracow Aviation Conference, 03/2011Page 19

Franke Aviation & Transportation Consulting

COPYRIGHT 2010 WWW.FRANKE-AVIATION.COM

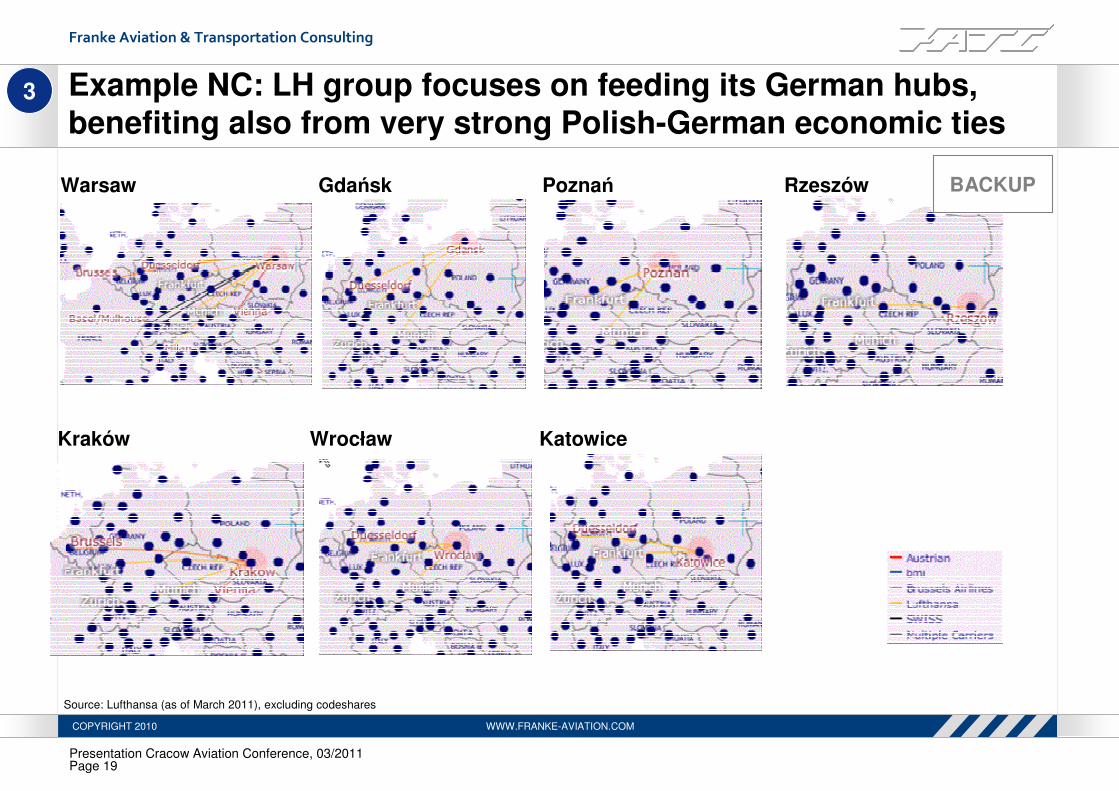

Example NC: LH group focuses on feeding its German hubs, benefiting also from very strong Polish-German economic ties

3

Warsaw

Wrocław

Gdańsk Poznań Rzeszów

KatowiceKraków

Source: Lufthansa (as of March 2011), excluding codeshares

BACKUP

Presentation Cracow Aviation Conference, 03/2011Page 20

Franke Aviation & Transportation Consulting

COPYRIGHT 2010 WWW.FRANKE-AVIATION.COM

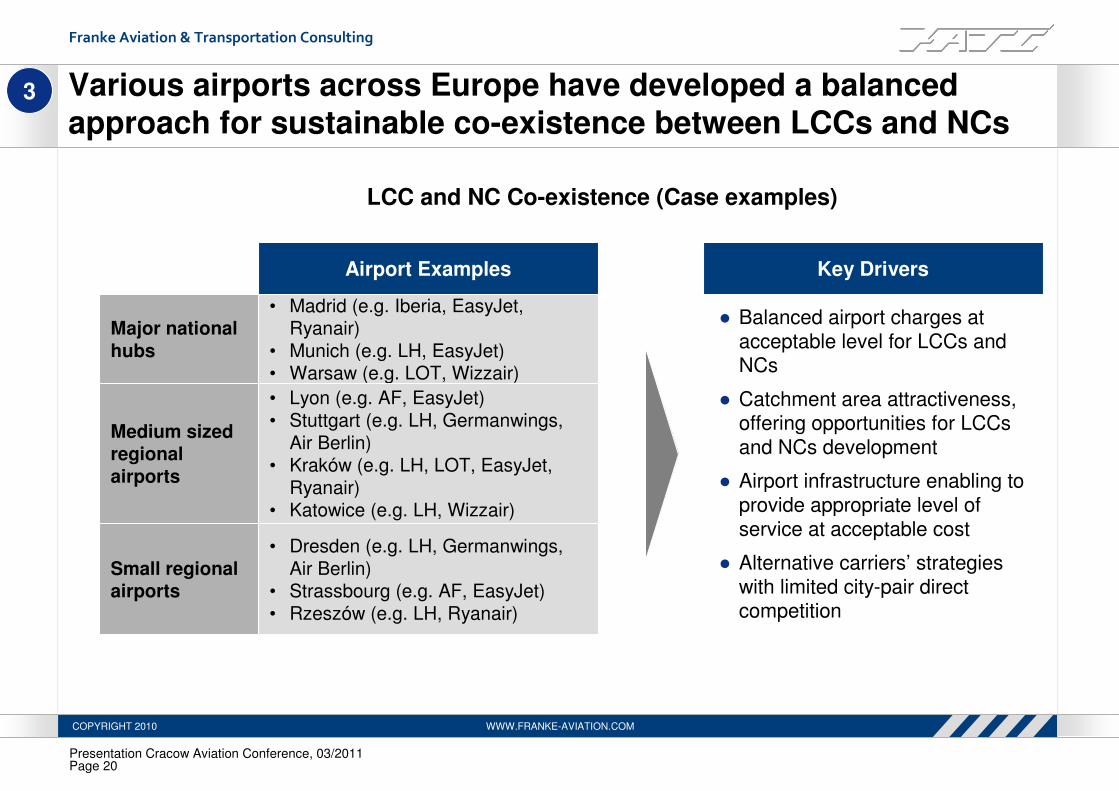

Various airports across Europe have developed a balancedapproach for sustainable co-existence between LCCs and NCs

3

Airport Examples

• Madrid (e.g. Iberia, EasyJet, Ryanair)

• Munich (e.g. LH, EasyJet)• Warsaw (e.g. LOT, Wizzair)

Major national hubs

• Lyon (e.g. AF, EasyJet)

• Stuttgart (e.g. LH, Germanwings,

Air Berlin)• Kraków (e.g. LH, LOT, EasyJet,

Ryanair)• Katowice (e.g. LH, Wizzair)

Medium sized regional airports

• Dresden (e.g. LH, Germanwings,

Air Berlin)• Strassbourg (e.g. AF, EasyJet)

• Rzeszów (e.g. LH, Ryanair)

Small regional airports

LCC and NC Co-existence (Case examples)

● Balanced airport charges at acceptable level for LCCs and NCs

● Catchment area attractiveness, offering opportunities for LCCs and NCs development

● Airport infrastructure enabling to provide appropriate level of service at acceptable cost

● Alternative carriers’ strategies with limited city-pair direct competition

Key Drivers

Presentation Cracow Aviation Conference, 03/2011Page 21

Franke Aviation & Transportation Consulting

COPYRIGHT 2010 WWW.FRANKE-AVIATION.COM

Assuming that both LCCs and NCs will further prosper in Poland, regional airports should pursue a phased approach

4

Further expansion of domesticand European P2P traffic

Development of high-yielddemand and respective

service offerings

Build-up of intercontinentalconnections (via WAW / CAP or

other hubs)

Build-up of intercontinentalp2p services

Step 1

Step 2

Step 3

Step 4

Contribution of…

LCCs Network carriers

Four steps towards further growth

• Strongcontribution

• Poor (outsidetraditional LCC strike zone)

• Feed to networkcarriers withintercontinentalservices?

• Today: none(future: long-haulLCC models?)

• Medium (opportunisticdevelopment)

• Considerablecontribution

• Considerablecontribution (in the course of O&D growth)

• Opportunisticdevelopment(depends onO&D demand)

Presentation Cracow Aviation Conference, 03/2011Page 22

Franke Aviation & Transportation Consulting

COPYRIGHT 2010 WWW.FRANKE-AVIATION.COM

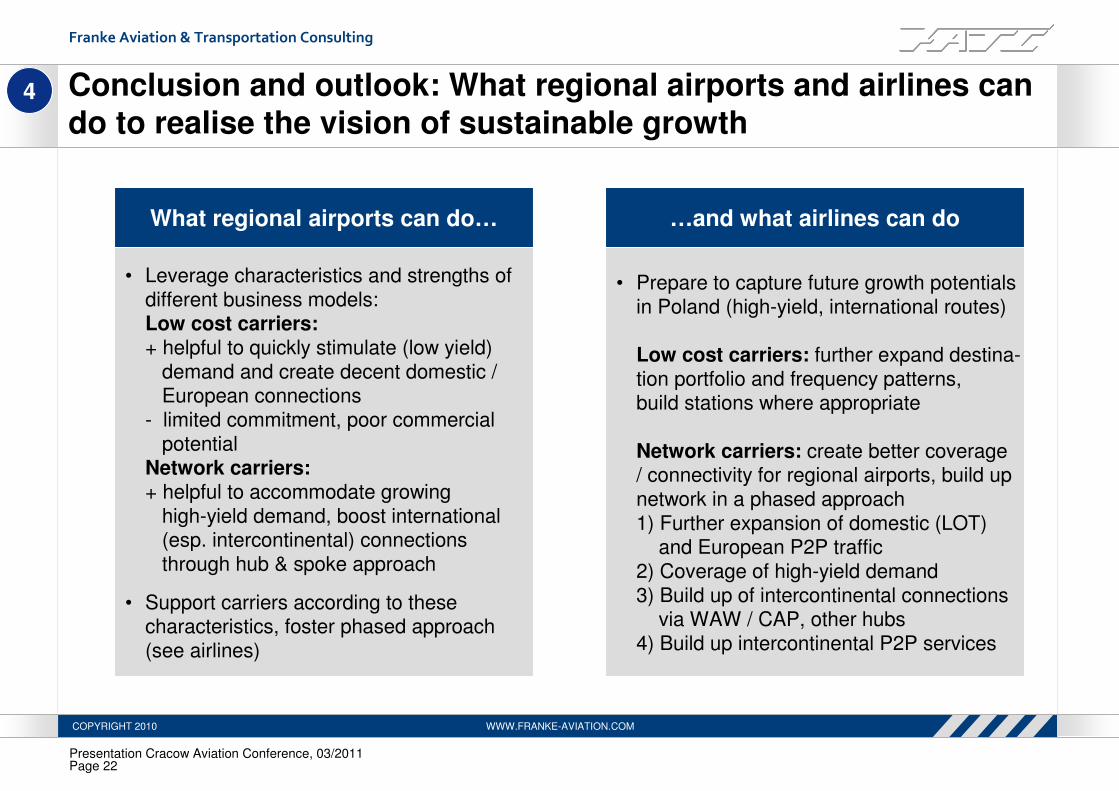

Conclusion and outlook: What regional airports and airlines cando to realise the vision of sustainable growth

4

What regional airports can do… …and what airlines can do

• Leverage characteristics and strengths ofdifferent business models:Low cost carriers:+ helpful to quickly stimulate (low yield)

demand and create decent domestic /European connections

- limited commitment, poor commercialpotential

Network carriers:+ helpful to accommodate growing

high-yield demand, boost international(esp. intercontinental) connectionsthrough hub & spoke approach

• Support carriers according to thesecharacteristics, foster phased approach(see airlines)

• Prepare to capture future growth potentialsin Poland (high-yield, international routes)

Low cost carriers: further expand destina-tion portfolio and frequency patterns,build stations where appropriate

Network carriers: create better coverage/ connectivity for regional airports, build upnetwork in a phased approach1) Further expansion of domestic (LOT)

and European P2P traffic2) Coverage of high-yield demand3) Build up of intercontinental connections

via WAW / CAP, other hubs4) Build up intercontinental P2P services

Presentation Cracow Aviation Conference, 03/2011Page 23

Franke Aviation & Transportation Consulting

COPYRIGHT 2010 WWW.FRANKE-AVIATION.COM

…THANK YOU VERY MUCH FOR YOUR ATTENTION!!!

Dr. Markus FrankeOwner, Senior Advisor

Franke Aviation &

Transportation Consulting

Von-Stauffenberg-Str. 10

D-41352 Korschenbroich

+49 175 2905004 (mob.)[email protected]

www.franke-aviation.com

Selected aviation clients of FATC / Dr Franke