Embed Size (px)

Citation preview

HEADQUARTERSMAPEI SpA Via Cafiero, 22 - 20158 MilanTel. +39-02-37673.1 Fax +39-02-37673.214Internet: www.mapei.comE-mail: [email protected]

CO

NSOL

IDAT

ED F

INAN

CIAL

STA

TEM

ENTS

DEC

EMBE

R 31

st 2

012

DECEMBER 31st

2012CONSOLIDATEDFINANCIALSTATEMENTS

ADHESIVES • SEALANTS • CHEMICAL PRODUCTS FOR BUILDING

The 75th anniversary of the founding of the Company was the perfect occasion to

present the new corporate image that Mapei wishes to project for the future.

The Milanese illustrator Carlo Stanga designed “Mapei World”, a place that seems

suspended yet, at the same time, very real, in which the main characters of the life

and autonomy of the image are the Mapei products present in each single place

within this fantasy city. Mapei World is a world of projects, all created and executed

thanks to the important contribution of the Company’s solutions and products,

always innovative and always cutting edge. At the heart of this world is man who,

through his actions and thoughts, sees the fulfilment of his destiny in the world within

the complexity of a city under constant transformation.

Illust

ratio

n by

Car

lo S

tang

a

I I

DECEMBER 31st

2012CONSOLIDATEDFINANCIALSTATEMENTS

I I I

I N D I C E

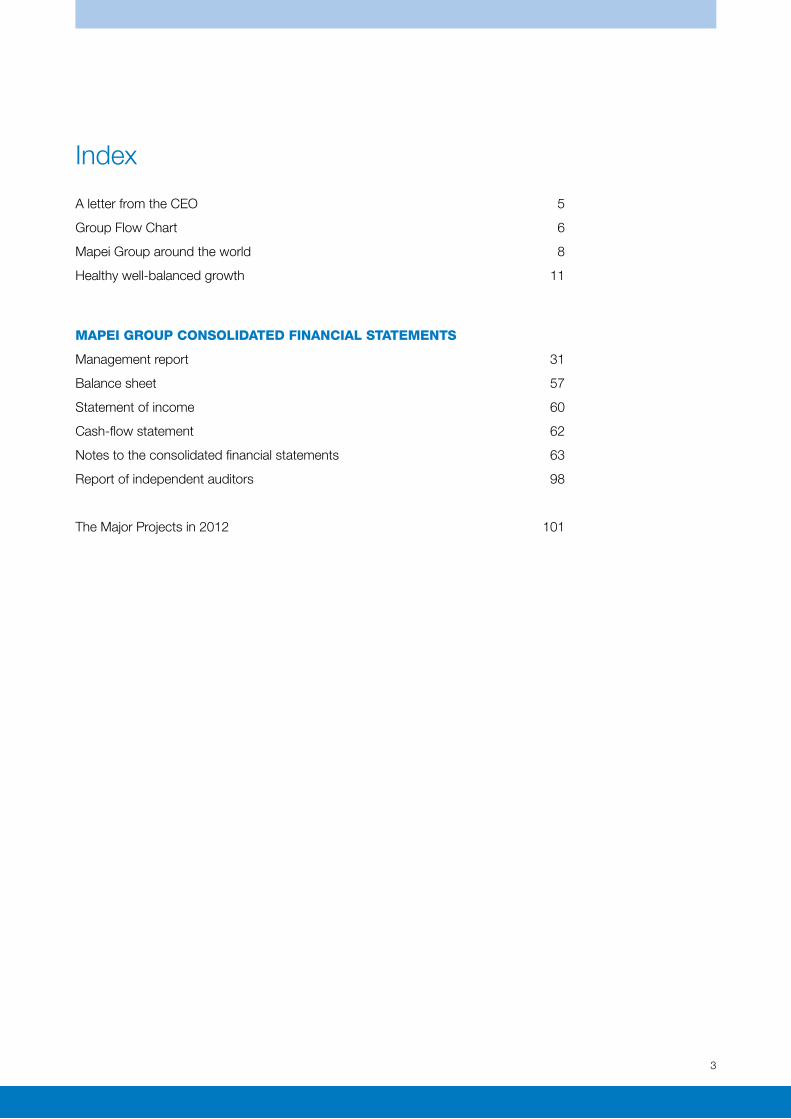

3

Index

A letter from the CEO 5

Group Flow Chart 6

Mapei Group around the world 8

Healthy well-balanced growth 11

MAPEI GROUP CONSOLIDATED FINANCIAL STATEMENTS

Management report 31

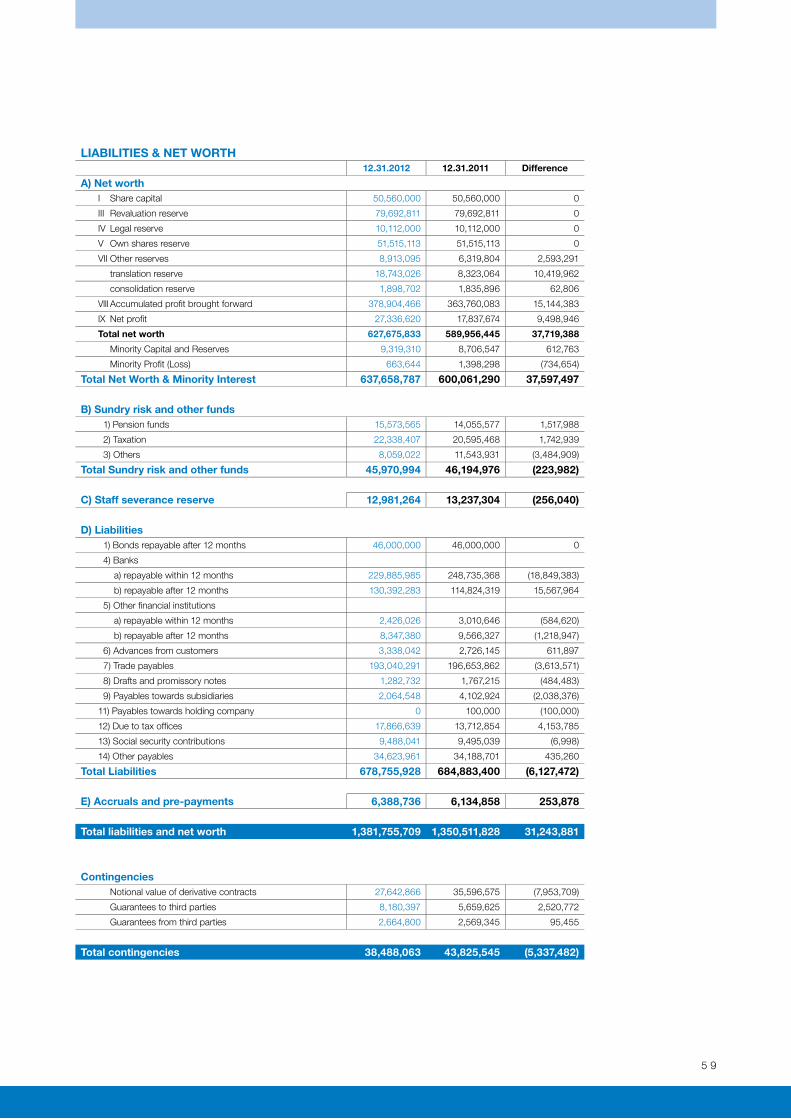

Balance sheet 57

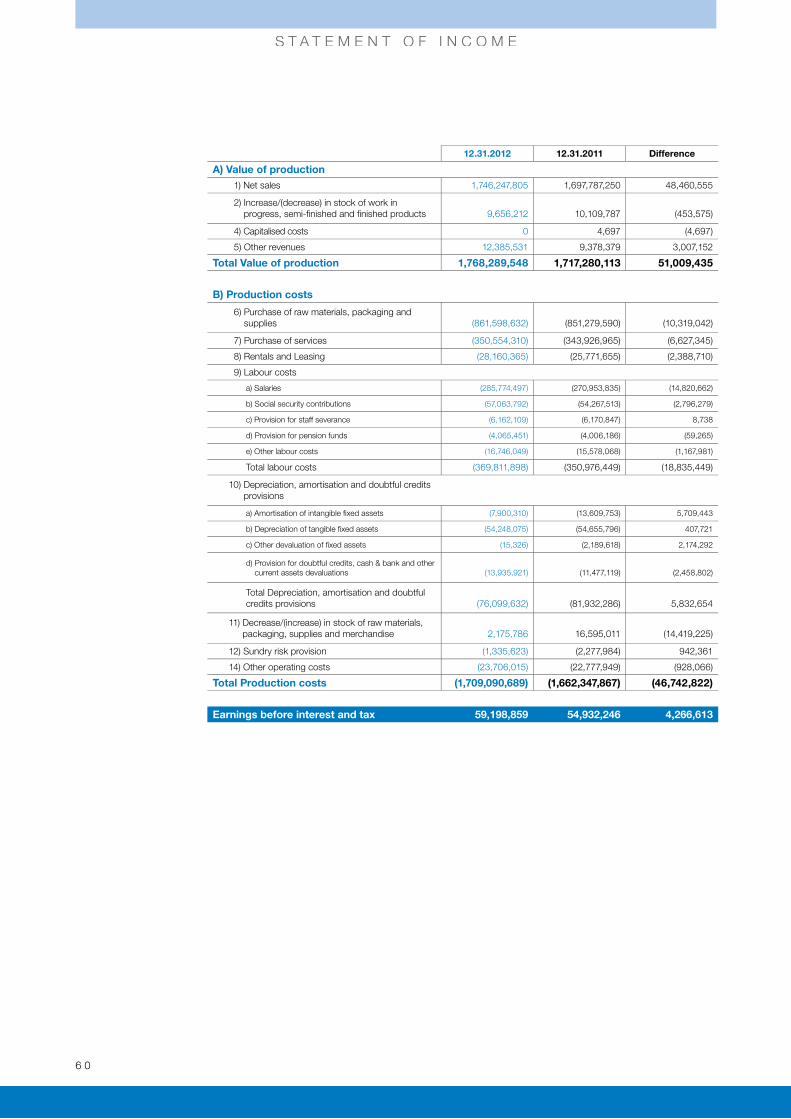

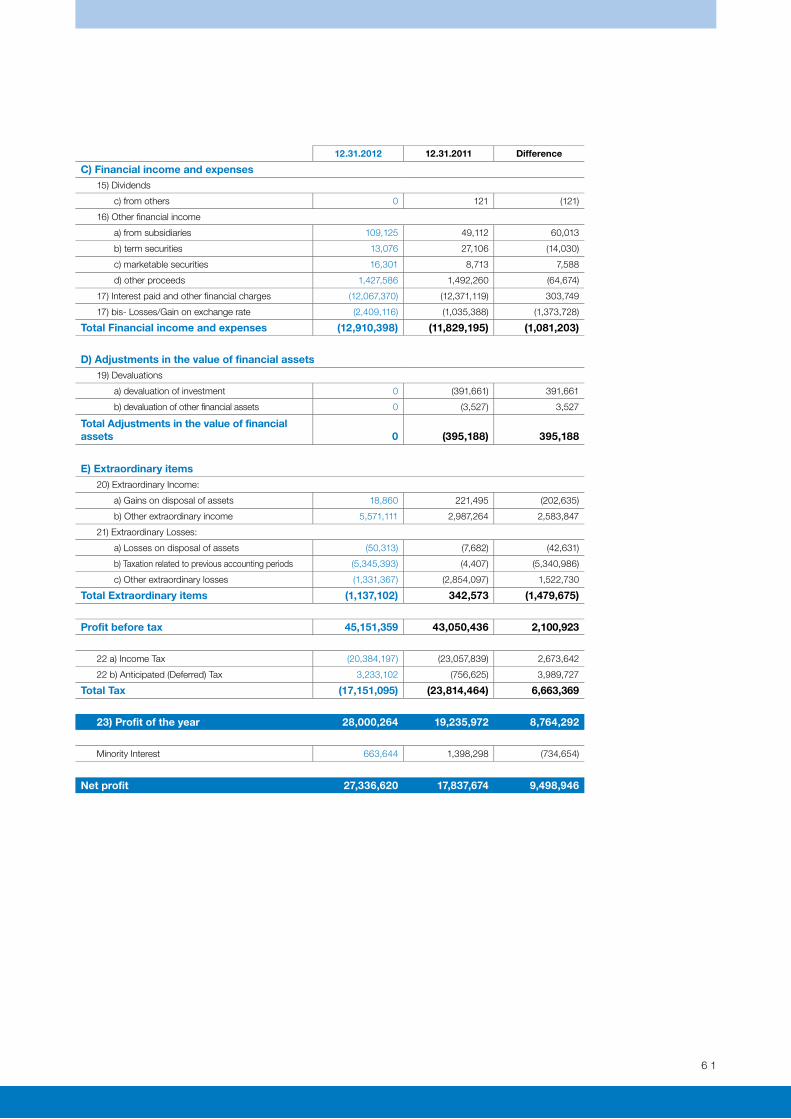

Statement of income 60

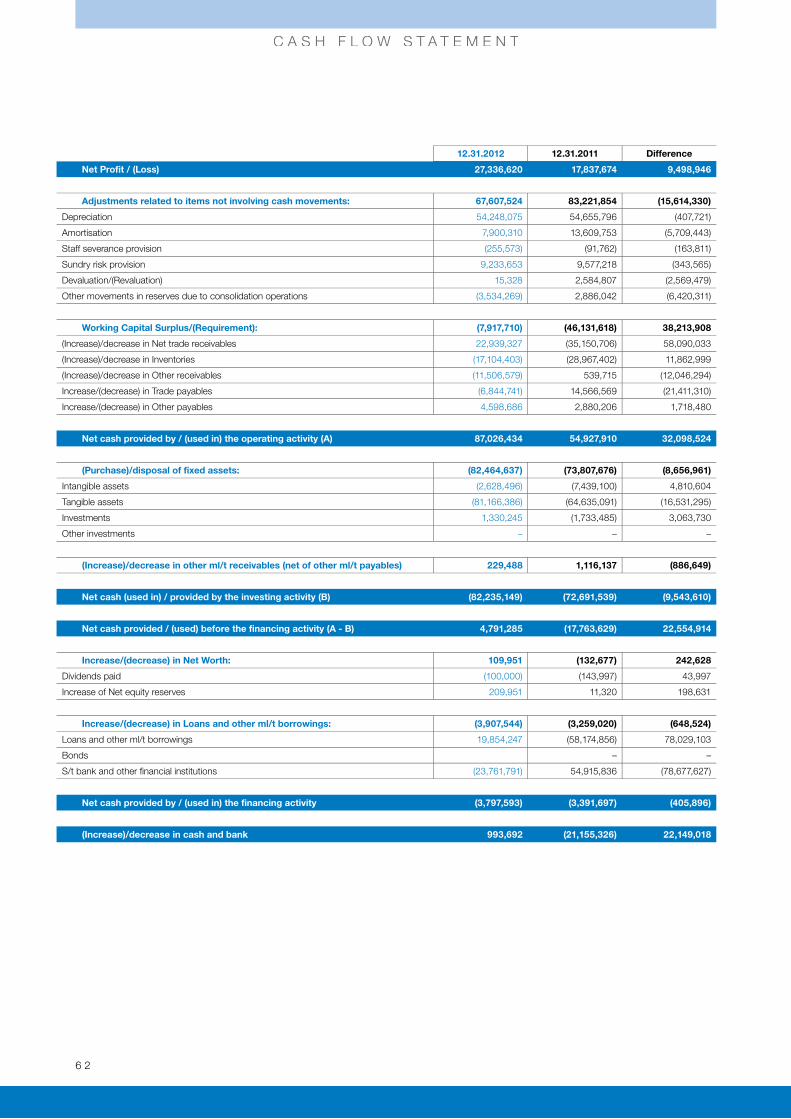

Cash-flow statement 62

Notes to the consolidated financial statements 63

Report of independent auditors 98

The Major Projects in 2012 101

4

T E S T A T I N A

4

5

In 2012 Mapei celebrated its first 75 years of business. What

started o� as a small family concern has grown over the years

to become a world-leading company in adhesives and chemical

products for the building industry, with a consolidated presence

over five continents.

In the last 75 years Italy, just like every other country in the world,

has grown and witnessed radical transformation. A period of

modernisation with Mapei amongst the key players, a company

that, through its products and technology, has made a significant

contribution to the execution of major building projects and the

renovation and conservative restoration of Italy’s cultural and

artistic heritage. Mapei’s growth has been global and continues

because its roots are embedded firmly in the past, and in values that have the merit of always being

topical: specialisation in the building world, internationalisation with a special focus on local market

needs, research and development into increasingly technologically-advanced products, tailor-made

service and support for our clientèle, teamwork, sustainable development of all our activities, concern

for the health and safety of all those who apply and use our products and the constant care taken by

our Human Resources department.

Without ever overlooking the fact that we are a chemicals company, Mapei knows only too well that

sustainability and technological innovation are the levers to guarantee constant improvement in the

level of wellbeing for the entire planet. Seventy five years after being founded, this constant process of

innovation is the elixir of life for Mapei. A winning recipe to continue looking to the future with confidence

and to look back at the past with well-deserved pride.

Confirmation comes from the latest figures, and further proof is the increase in the number of new,

highly-evolved products capable of satisfying all the requirements of experts from the building

industry all over the world. With the exception of Italy, the growth of Mapei Group has continued in

all geographical areas, with particularly significant peaks in Asia (+36.9%), Oceania (+23.7%) and the

Americas (+15.2%). Without overlooking the growth in Western Europe (+6.5%), Africa (+4.1%) and

Eastern Europe (+2.9%). The Group’s profit margin has also started to grow again; from a net profit of

19.2 million Euros in 2011 to 28.0 million Euros in 2012, an excellent increase of 45.6%.

Confirmation that the “desire for growth” is the real driving force of Mapei. A constant growth that, with

the objective of o�ering solutions in line with local needs and keeping costs under control at all times,

confirms how Mapei’s destiny really is that of being a global force.

This is why looking to the future with confidence is not simply a wish; it is a stimulus to work even more

intensely, at all levels, to be the best at what we do and o�er the most satisfying products that the

international building market could ask for. It is on these foundations that we base our knowledge of

never being far from the expectations of our stakeholders, be they clients, suppliers, collaborators or

shareholders. Giorgio Squinzi CEO

An anniversary to encourage growth

6

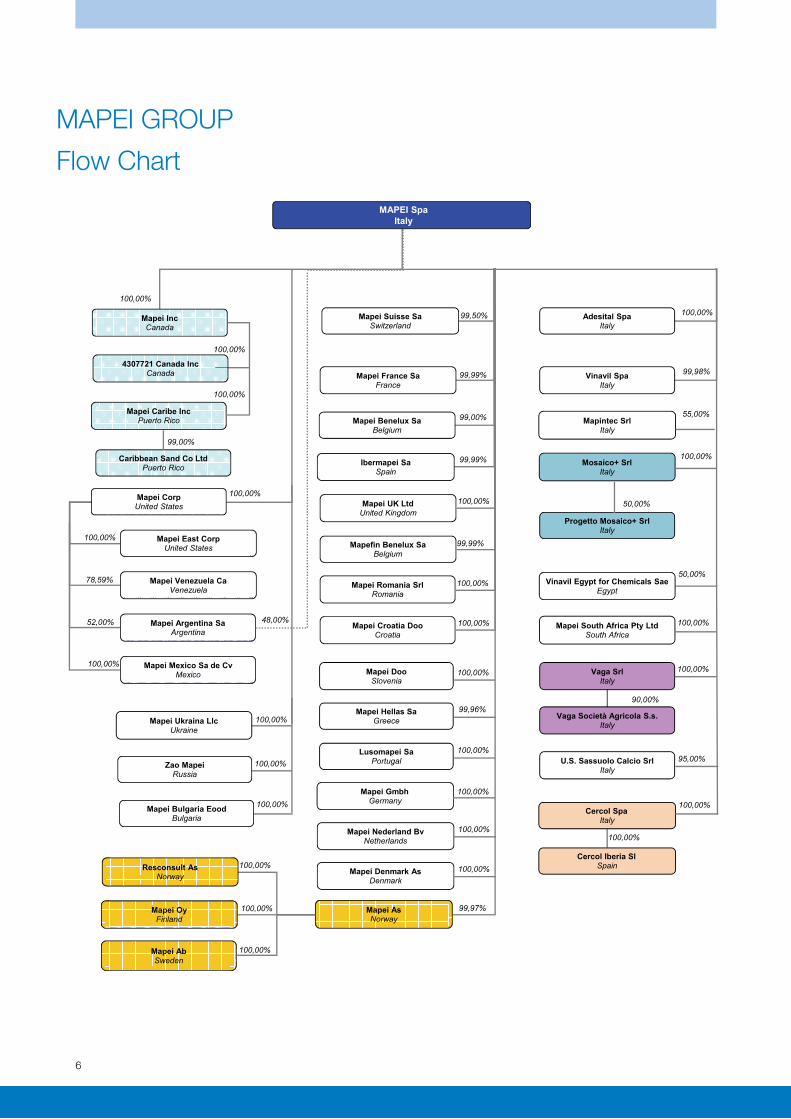

Mapei Inc

Canada

Mapei Corp

United States

Mapei East Corp

United States

Mapei Argentina Sa

Argentina

Mapei Venezuela Ca

Venezuela

Ibermapei Sa

Spain

Mapei France Sa

France

Mapei Benelux Sa

Belgium

Mapei Suisse Sa

Switzerland

99,99%

99,99%

99,00%

99,50%

100,00%

100,00%

100,00%

78,59%

Mapefin Benelux Sa

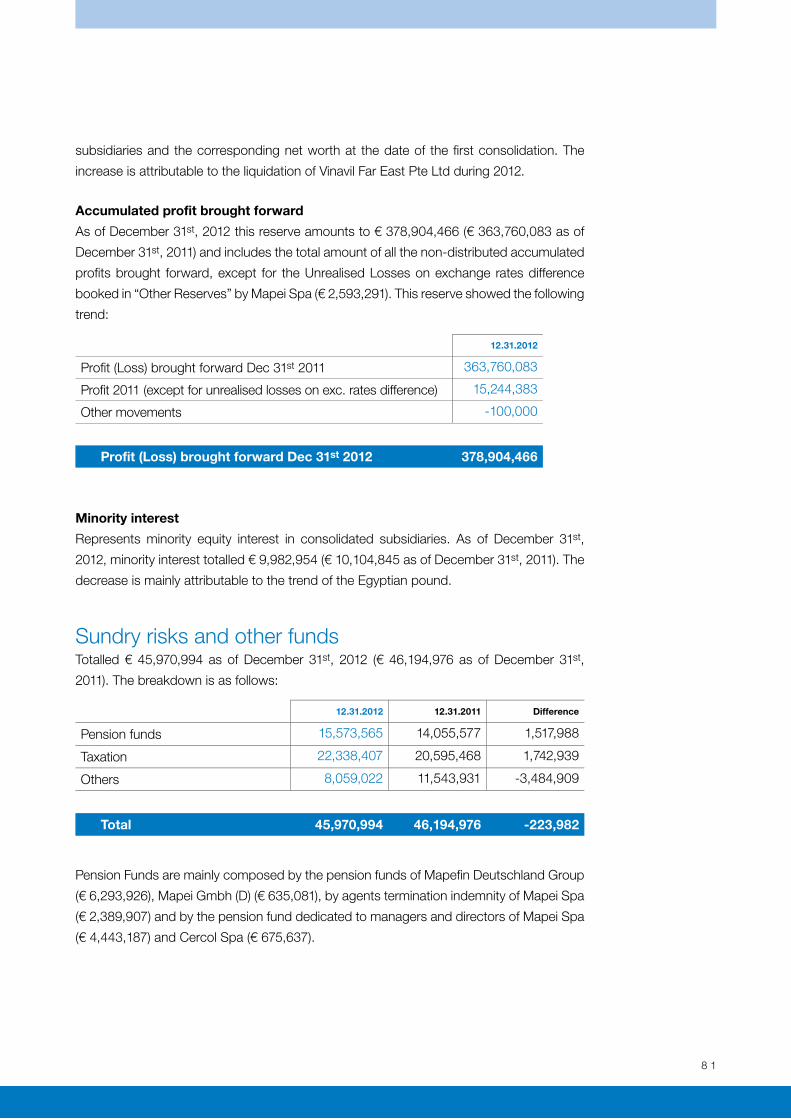

Belgium

Mapei UK Ltd

United Kingdom

99,99%

Mapei As

Norway

Mapei Ab

Sweden

Mapei Oy

Finland100,00%

100,00%Vaga Srl

Italy

Vinavil Spa

Italy

99,98%

Adesital Spa

Italy100,00%

100,00%

Vinavil Egypt for Chemicals Sae

Egypt

50,00%

Mapei Gmbh

Germany

Zao Mapei

Russia

Mapei Doo

Slovenia

Mapei Hellas Sa

Greece

Lusomapei Sa

Portugal

99,96%

100,00%

52,00%

100,00%

Mapei Caribe Inc

Puerto Rico

100,00%

Cercol Spa

Italy

SpainCercol Iberia Sl

100,00%

100,00%

Mapei Romania Srl

Romania100,00%

100,00%

Mapei Croatia Doo

Croatia100,00%

UkraineMapei Ukraina Llc

Mosaico+ Srl

Italy

Mapintec Srl

Italy

55,00%

100,00%

Mapei Bulgaria Eood

Bulgaria

100,00%

Mapei Nederland Bv

Netherlands

100,00%

100,00%

100,00%

100,00%

100,00%

Caribbean Sand Co Ltd

Puerto Rico

99,00%

Mapei South Africa Pty Ltd

South Africa100,00%

Mapei Mexico Sa de Cv

Mexico100,00%

Mapei Denmark As

Denmark100,00%100,00%

Resconsult As

Norway

Progetto Mosaico+ Srl

Italy

50,00%

99,97%

90,00%

48,00%

Vaga Società Agricola S.s.

Italy

4307721 Canada Inc

Canada

U.S. Sassuolo Calcio Srl

Italy95,00%

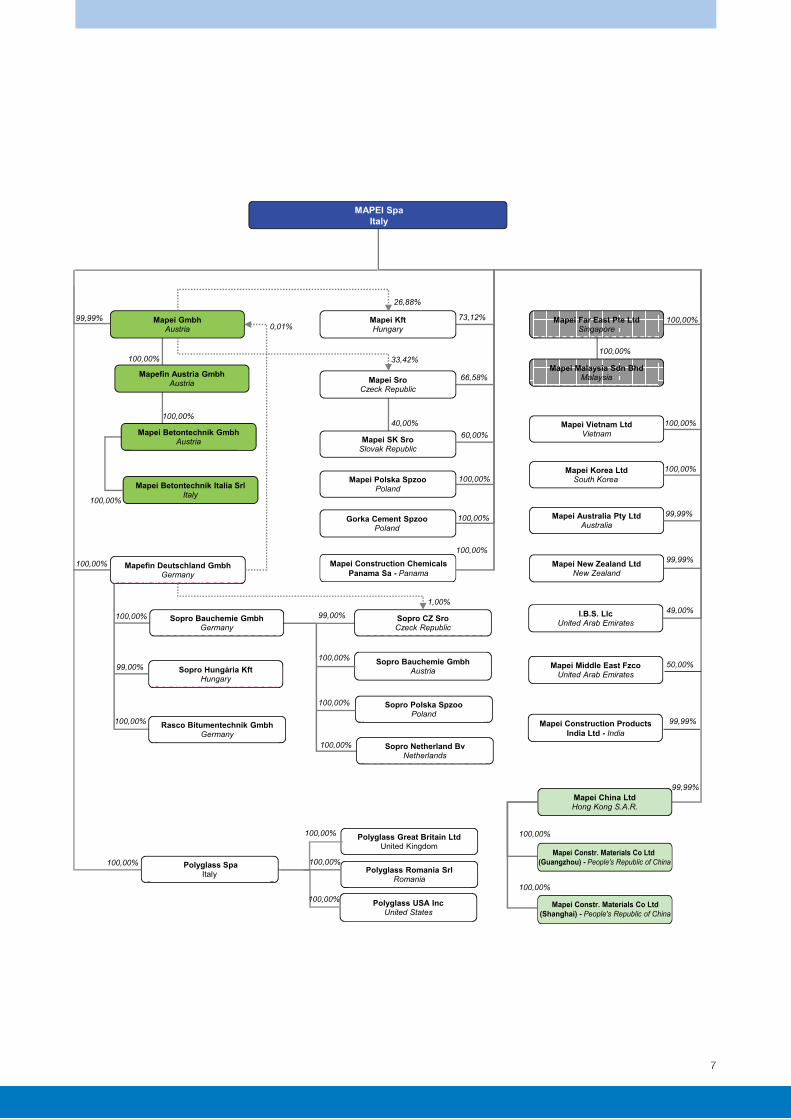

MAPEI Spa

Italy

MAPEI GROUP

Flow Chart

7

Mapei Far East Pte Ltd

Singapore

Mapefin Deutschland Gmbh

Germany100,00%

Sopro CZ Sro

Czeck Republic

Sopro Bauchemie Gmbh

Austria

Sopro Polska Spzoo

Poland

100,00%

1,00%

Sopro Netherland Bv

Netherlands

Mapei Gmbh

Austria

100,00%

99,99%

100,00%

100,00%

Gorka Cement Spzoo

Poland

Mapei Kft

Hungary

Mapei Sro

Czeck Republic

73,12%

66,58%

33,42%

26,88%

Mapei SK Sro

Slovak Republic

40,00%

Mapei Polska Spzoo

Poland

Mapei Malaysia Sdn Bhd

Malaysia

Mapei Vietnam Ltd

Vietnam

Mapei Australia Pty Ltd

Australia

100,00%

100,00%

100,00%

Mapei New Zealand Ltd

New Zealand

Mapei China Ltd

Hong Kong S.A.R.

99,99%

99,99%

100,00%

99,00%

100,00%

99,99%

Germany100,00%

100,00%

100,00%

I.B.S. Llc

United Arab Emirates49,00%

Mapei Middle East Fzco

United Arab Emirates50,00%

Polyglass USA Inc

United States

Polyglass Romania Srl

Romania

Polyglass Great Britain Ltd

United Kingdom

100,00%

100,00%

100,00%100,00%

Mapei Betontechnik Gmbh

Austria

Mapei Betontechnik Italia Srl

Italy100,00%

60,00%

Mapefin Austria Gmbh

Austria

Polyglass Spa

Italy

Mapei Korea Ltd

100,00%South Korea

99,99%

100,00%

0,01%

Mapei Construction Chemicals

Panama Sa - Panama

Mapei Construction Products

India Ltd - India

Mapei Constr. Materials Co Ltd

(Guangzhou) - People's Republic of China

Mapei Constr. Materials Co Ltd

(Shanghai) - People's Republic of China

Sopro Hungária Kft

Hungary99,00%

100,00%

Rasco Bitumentechnik Gmbh

100,00%

MAPEI Spa

Italy

Sopro Bauchemie Gmbh

Germany

8

* Operational companies as of 31/12/2012

HeadquartersHeadquarters

Mapei S.p.A.Milan - Italy

Mapei main o�ces with factories

Mapei commercial branch o�ces

Main o�ces with factories of other companies

Commercial branch o�ces of other companies

R&D centres

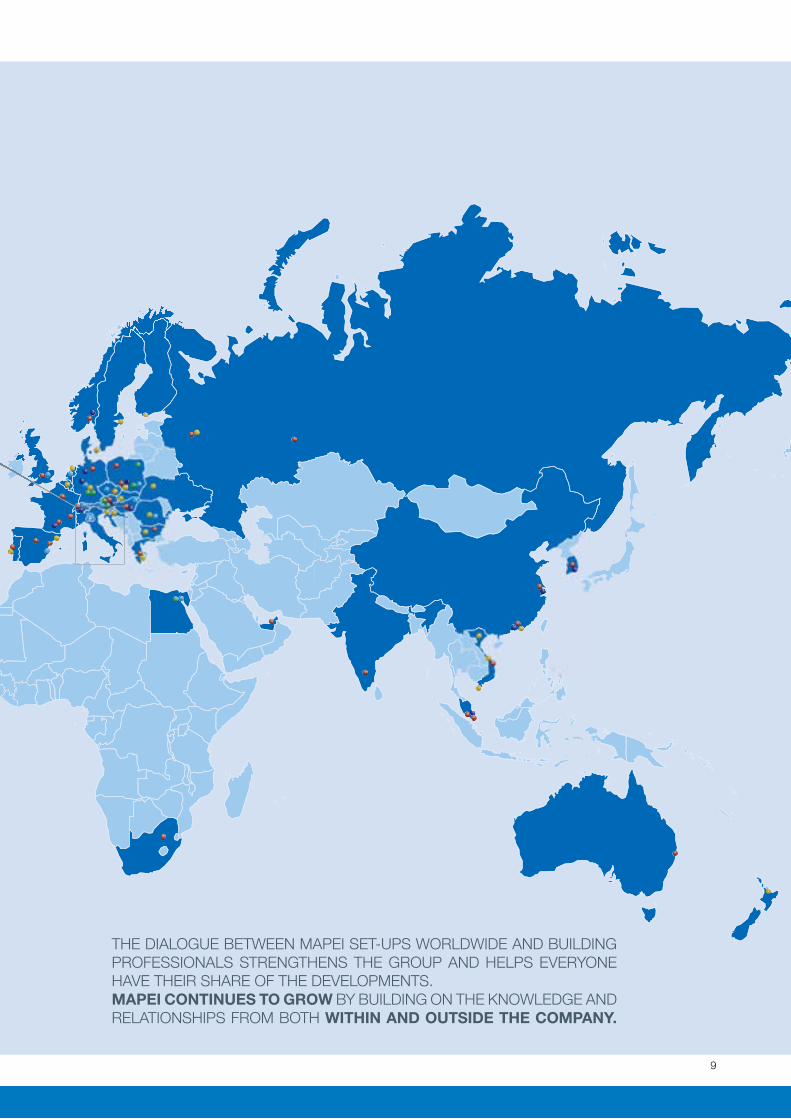

62 PLANTS AND75 SUBSIDIARIES*,SYNERGY TO CREATE ADDED VALUE.

9

THE DIALOGUE BETWEEN MAPEI SET-UPS WORLDWIDE AND BUILDING PROFESSIONALS STRENGTHENS THE GROUP AND HELPS EVERYONE HAVE THEIR SHARE OF THE DEVELOPMENTS.MAPEI CONTINUES TO GROW BY BUILDING ON THE KNOWLEDGE AND RELATIONSHIPS FROM BOTH WITHIN AND OUTSIDE THE COMPANY.

Illustration by Carlo Stanga

1 1

Growth is at the centre of Mapei Group’s corporate philosophy: a growth that must

be healthy and well-balanced in which investments are used to increase the presence

of the Group in the local area.

Our growth strategy is based on the premise that Mapei is a global actor managed

along the lines of a family business, with the support of a strong management team for

all the research, finance and sales activities within the business, and with an outlook

projected over a medium to long-term period. Mapei wishes to maximise growth

and e¨ciency, not only profits, by concentrating on a mix that includes products,

production capacity and people.

It wishes to achieve all this while being fully aware that the strength of the Group is

measured not only by its new acquisitions in strategic areas of the global market, or

by its economic and financial growth, but also by the level of trust shown by all those

who choose our Company. The need to become global through internationalisation is

tightly connected to an increase in production capacity by having production facilities

in the major market areas, supplying solutions in line with local needs and keeping

costs under control to remain constantly competitive.

Human resources are a central element to this approach. Our people have to be

proactive in the development of local growth strategies and, in order to have the best

understanding of the needs of each geographical area, it is fundamental to have an

e¨cient local management team. Headhunting the most talented people from all over

the world is another constant commitment of the Company.

Healthy well-balanced growth

1 2

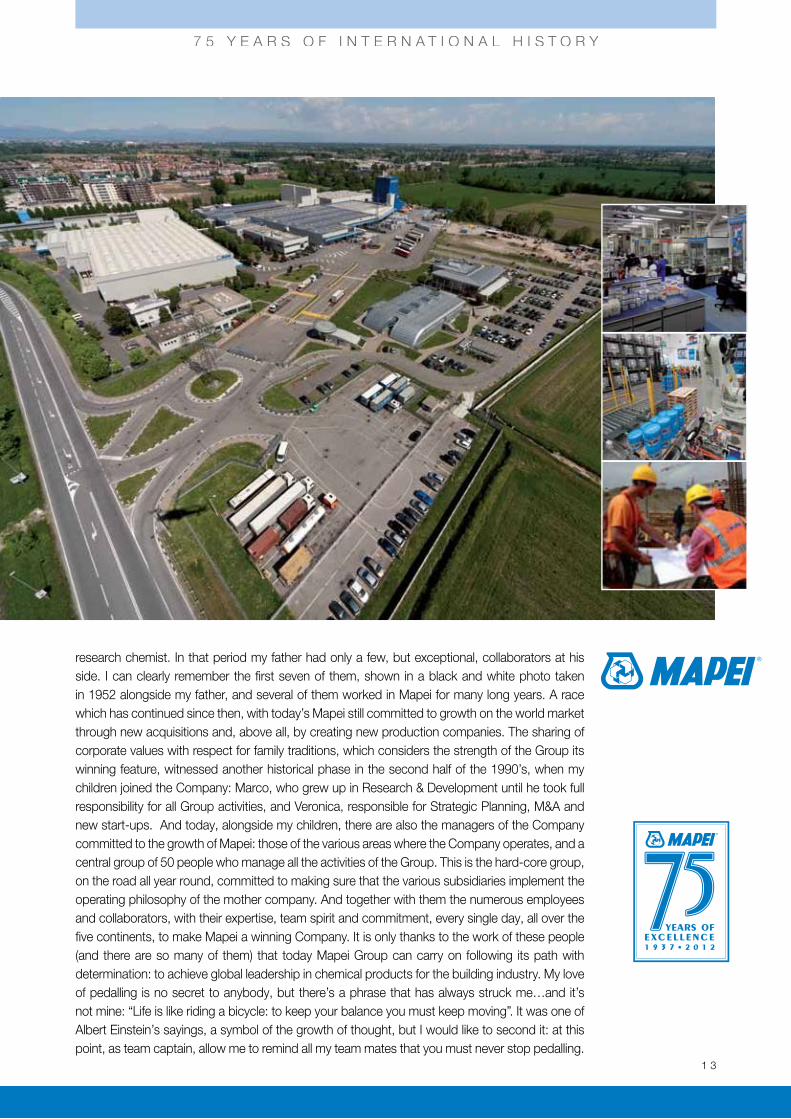

A stage race with challenging climbs and exciting sprint finishes, but above all so many exhilarating successes and exceptional team members. This metaphor of cycling - the sport I love most - is the best one to summarise the growth of Mapei and my memories tied to its story. 75 years from its foundation is the right occasion to celebrate, but also to look back over the most significant moments which have determined its development. As I said, in stages. Not a detailed commentary, but just a mention of the main turning points which have characterised its life until now. A growth which continues because it is based precisely on the solid roots of the past, and on values which have the beauty of always being valid, even today. And so, if I look back, I can see Mapei, and then Mapei again. It may seem rhetorical or over the top, but that’s the way it is: firstly for reasons of age - I was born just a few years after the Company was founded - but also because the story and growth of the Company inevitably blends in with my own personal story and that of my family. And if I wish to associate a face with Mapei that represents the entire being of the Company, this can be one person and one person only, my father Rodolfo, founder of the Company. A man who had the gift of creativity and an extraordinarily open mind, a unique role model who for me is still a source of inspiration. I inherited from him my enormous love of cycling and the opera, and the conviction that there cannot be work without art. As a child I would walk with him from our home, in Via Imbriani, Milan, towards the first headquarters of the Company in Via Cafiero, the same place which is today home of the Group’s most important Research & Development Centre. And in those few hundred metres, by my father’s side, I started to cultivate my dream: to become a

75 years of historyNever stop pedalling, by Giorgio Squinzi

7 5 Y E A R S O F I N T E R N A T I O N A L H I S T O R Y

1 3

research chemist. In that period my father had only a few, but exceptional, collaborators at his side. I can clearly remember the first seven of them, shown in a black and white photo taken in 1952 alongside my father, and several of them worked in Mapei for many long years. A race which has continued since then, with today’s Mapei still committed to growth on the world market through new acquisitions and, above all, by creating new production companies. The sharing of corporate values with respect for family traditions, which considers the strength of the Group its winning feature, witnessed another historical phase in the second half of the 1990’s, when my children joined the Company: Marco, who grew up in Research & Development until he took full responsibility for all Group activities, and Veronica, responsible for Strategic Planning, M&A and new start-ups. And today, alongside my children, there are also the managers of the Company committed to the growth of Mapei: those of the various areas where the Company operates, and a central group of 50 people who manage all the activities of the Group. This is the hard-core group, on the road all year round, committed to making sure that the various subsidiaries implement the operating philosophy of the mother company. And together with them the numerous employees and collaborators, with their expertise, team spirit and commitment, every single day, all over the five continents, to make Mapei a winning Company. It is only thanks to the work of these people (and there are so many of them) that today Mapei Group can carry on following its path with determination: to achieve global leadership in chemical products for the building industry. My love of pedalling is no secret to anybody, but there’s a phrase that has always struck me…and it’s not mine: “Life is like riding a bicycle: to keep your balance you must keep moving”. It was one of Albert Einstein’s sayings, a symbol of the growth of thought, but I would like to second it: at this point, as team captain, allow me to remind all my team mates that you must never stop pedalling.

7 5 Y E A R S O F I N T E R N A T I O N A L H I S T O R Y

1 4

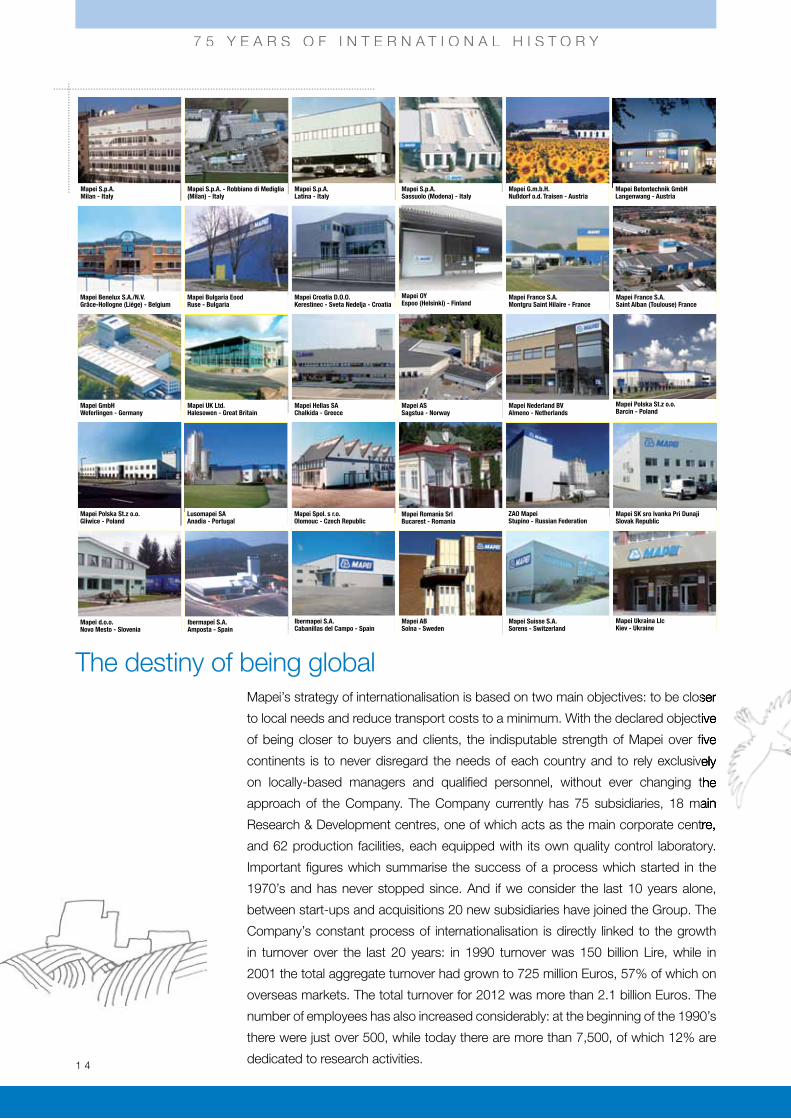

Mapei’s strategy of internationalisation is based on two main objectives: to be closer

to local needs and reduce transport costs to a minimum. With the declared objective

of being closer to buyers and clients, the indisputable strength of Mapei over five

continents is to never disregard the needs of each country and to rely exclusively

on locally-based managers and qualified personnel, without ever changing the

approach of the Company. The Company currently has 75 subsidiaries, 18 main

Research & Development centres, one of which acts as the main corporate centre,

and 62 production facilities, each equipped with its own quality control laboratory.

Important figures which summarise the success of a process which started in the

1970’s and has never stopped since. And if we consider the last 10 years alone,

between start-ups and acquisitions 20 new subsidiaries have joined the Group. The

Company’s constant process of internationalisation is directly linked to the growth

in turnover over the last 20 years: in 1990 turnover was 150 billion Lire, while in

2001 the total aggregate turnover had grown to 725 million Euros, 57% of which on

overseas markets. The total turnover for 2012 was more than 2.1 billion Euros. The

number of employees has also increased considerably: at the beginning of the 1990’s

there were just over 500, while today there are more than 7,500, of which 12% are

dedicated to research activities.

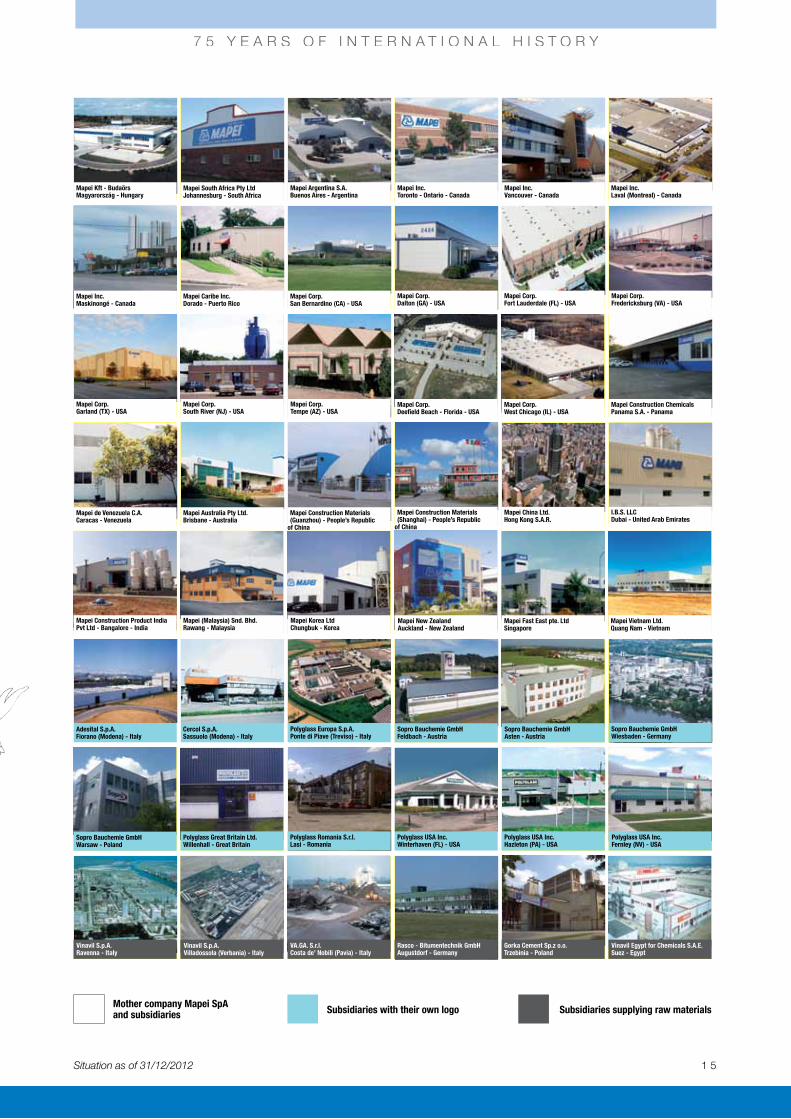

The destiny of being global

7 5 Y E A R S O F I N T E R N A T I O N A L H I S T O R Y

Mapei’s strategy of internationalisation is based on two main objectives: to be closer

to local needs and reduce transport costs to a minimum. With the declared objective

of being closer to buyers and clients, the indisputable strength of Mapei over five

continents is to never disregard the needs of each country and to rely exclusively

on locally-based managers and qualified personnel, without ever changing the

approach of the Company. The Company currently has 75 subsidiaries, 18 main

evelopment centres, one of which acts as the main corporate centre,

Ibermapei S.A.Cabanillas del Campo - Spain

Mapei AB Solna - Sweden

Mapei Suisse S.A. Sorens - Switzerland

Mapei Polska St.z o.o. Gliwice - Poland

Lusomapei SA Anadia - Portugal

Mapei Hellas SA Chalkida - Greece

Mapei AS Sagstua - Norway

Mapei Nederland BV Almeno - Netherlands

Mapei UK Ltd.Halesowen - Great Britain

Mapei S.p.A. - Robbiano di Mediglia(Milan) - Italy

Mapei S.p.A. Latina - Italy

Mapei S.p.A. Sassuolo (Modena) - Italy

Mapei G.m.b.H. Nußdorf o.d. Traisen - Austria

Mapei Betontechnik GmbHLangenwang - Austria

Mapei S.p.A. Milan - Italy

Mapei Spol. s r.o. Olomouc - Czech Republic

Mapei Romania Srl Bucarest - Romania

ZAO Mapei Stupino - Russian Federation

Mapei SK sro Ivanka Pri DunajiSlovak Republic

Mapei d.o.o. Novo Mesto - Slovenia

Ibermapei S.A.Amposta - Spain

Mapei France S.A. Montgru Saint Hilaire - France

Mapei France S.A. Saint Alban (Toulouse) France

Mapei GmbH Weferlingen - Germany

Mapei Bulgaria Eood Ruse - Bulgaria

Mapei Croatia D.O.O. Kerestinec - Sveta Nedelja - Croatia

Mapei Benelux S.A./N.V. Grâce-Hollogne (Liège) - Belgium

Mapei OYEspoo (Helsinki) - Finland

Mapei Polska St.z o.o.Barcin - Poland

Mapei Ukraina LlcKiev - Ukraine

1 5

7 5 Y E A R S O F I N T E R N A T I O N A L H I S T O R Y

Situation as of 31/12/2012

Subsidiaries with their own logoMother company Mapei SpAand subsidiaries Subsidiaries supplying raw materials

Mapei Corp. Dalton (GA) - USA

Mapei Corp. Fort Lauderdale (FL) - USA

Mapei Corp. Fredericksburg (VA) - USA

Mapei Corp. Garland (TX) - USA

Mapei Corp. South River (NJ) - USA

Mapei Corp. Tempe (AZ) - USA

Mapei Kft - Budaörs Magyarország - Hungary

Mapei South Africa Pty LtdJohannesburg - South Africa

Mapei Argentina S.A. Buenos Aires - Argentina

Mapei China Ltd. Hong Kong S.A.R.

Mapei Construction Materials (Shanghai) - People’s Republic

of China

I.B.S. LLC Dubai - United Arab Emirates

Mapei Construction Product India Pvt Ltd - Bangalore - India

Mapei (Malaysia) Snd. Bhd. Rawang - Malaysia

Mapei Korea Ltd Chungbuk - Korea

Mapei Corp. Deefield Beach - Florida - USA

Mapei Corp. West Chicago (IL) - USA

Mapei Construction ChemicalsPanama S.A. - Panama

Mapei de Venezuela C.A. Caracas - Venezuela

Mapei Australia Pty Ltd. Brisbane - Australia

Mapei Construction Materials (Guanzhou) - People’s Republic

of China

Mapei Inc. Toronto - Ontario - Canada

Mapei Inc. Vancouver - Canada

Mapei Inc. Laval (Montreal) - Canada

Mapei Inc. Maskinongé - Canada

Mapei Caribe Inc. Dorado - Puerto Rico

Mapei Corp. San Bernardino (CA) - USA

Sopro Bauchemie GmbHWiesbaden - Germany

Polyglass Great Britain Ltd.Willenhall - Great Britain

Polyglass Romania S.r.l.Lasi - Romania

Polyglass USA Inc.Winterhaven (FL) - USA

Polyglass USA Inc.Hazleton (PA) - USA

Polyglass USA Inc.Fernley (NV) - USA

Mapei New Zealand Auckland - New Zealand

Mapei Fast East pte. Ltd Singapore

Mapei Vietnam Ltd. Quang Nam - Vietnam

Adesital S.p.A.Fiorano (Modena) - Italy

Cercol S.p.A.Sassuolo (Modena) - Italy

Polyglass Europa S.p.A.Ponte di Piave (Treviso) - Italy

Vinavil S.p.A.Villadossola (Verbania) - Italy

VA.GA. S.r.l.Costa de’ Nobili (Pavia) - Italy

Rasco - Bitumentechnik GmbHAugustdorf - Germany

Gorka Cement Sp.z o.o. Trzebinia - Poland

Vinavil Egypt for Chemicals S.A.E.Suez - Egypt

Vinavil S.p.A.Ravenna - Italy

Sopro Bauchemie GmbHFeldbach - Austria

Sopro Bauchemie GmbHAsten - Austria

Sopro Bauchemie GmbHWarsaw - Poland

1 6

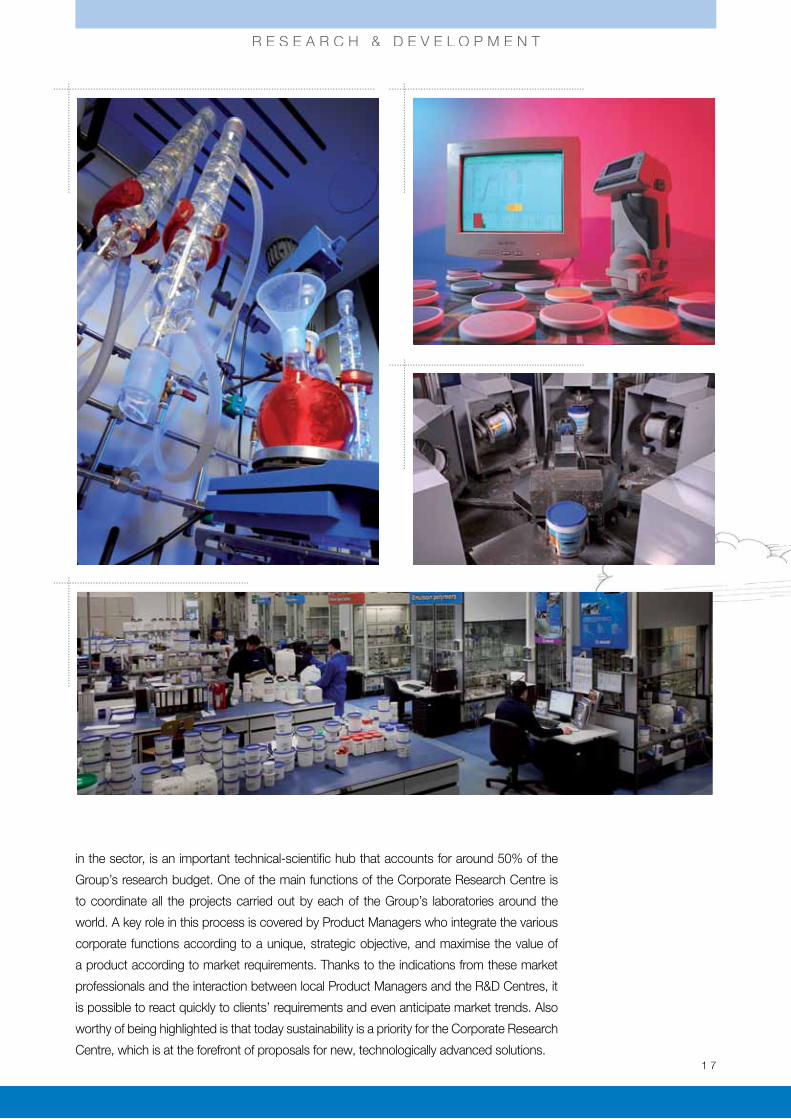

R&D: continuous innovation for growthSpecialisation, Internationalisation, Research & Development. These are the three main

pillars that support the growth and development of Mapei Group. Thanks to “specialisation”

Mapei currently o�ers 15 product lines and, as concrete proof of its “internationalisation”,

the Group has 75 subsidiaries and 62 production facilities in 30 countries over 5 continents.

Worth underlining is the increase in the number of Mapei R&D centres in the world, with

1 Corporate Research Centre and 17 Research laboratories (2 in Italy, 2 in Germany, 1 in

France, 1 in Norway, 1 in Canada, 3 in the United States, 1 in Austria, 1 in Switzerland, 1 in

Poland, 1 in Singapore, 2 in China and 1 in South Korea). It is a well known fact that intense

scientific research work is at the base of all Mapei products; the Corporate Research

centre in Milan, widely recognised at a worldwide level as one of the best laboratories 1 6

R&D: continuous innovation for growth

R E S E A R C H & D E V E L O P M E N T

1 7

in the sector, is an important technical-scientific hub that accounts for around 50% of the

Group’s research budget. One of the main functions of the Corporate Research Centre is

to coordinate all the projects carried out by each of the Group’s laboratories around the

world. A key role in this process is covered by Product Managers who integrate the various

corporate functions according to a unique, strategic objective, and maximise the value of

a product according to market requirements. Thanks to the indications from these market

professionals and the interaction between local Product Managers and the R&D Centres, it

is possible to react quickly to clients’ requirements and even anticipate market trends. Also

worthy of being highlighted is that today sustainability is a priority for the Corporate Research

Centre, which is at the forefront of proposals for new, technologically advanced solutions.

R E S E A R C H & D E V E L O P M E N T

1 81 8

The most innovative products for the building industry come from the Group’s 62

plants. Eco-compatible production to meet the needs of more than 55,000 clients all

around the world. There are more than 1,400 products that make up the complete

Mapei range. Production, through highly-automated processes, is another strong

point of Mapei, which has created facilities all over the world to optimise logistics

costs and to be closer to our clients. Technological development is one of the main

characteristics of Mapei production plants. Most of the Group’s production facilities

are equipped with innovative energy saving systems as well as particularly e¨cient

systems that control the level of emissions into the ground and air and systems that

maintain a safe working environment during the various production processes.

Cutting-edge production system

P R O D U C T I O N

1 9

There were numerous new products introduced in 2012. The family of lightweight

products welcomed two new rapid, high-performance, lightweight adhesives, ideal

for installing all types of ceramic tiles, thin porcelain tiles and stone: the rapid versions

of ULTRALITE S1 and ULTRALITE S2. The spotlight also fell on MAPEWRAP EQ

SYSTEM, the innovative passive strengthening system for buildings to counteract

the e�ects of seismic activity. Another innovative product is RE-CON ZERO which is

used for the sustainable recovery of returned concrete: it does not produce any waste

material, it is added directly to the mixing drum of cement trucks and no treatment

plant is required. For the wall coatings range DURSILITE MATT and ELASTOCOLOR

TONACHINO PLUS and, for resin playing surfaces, MAPECOAT TNS URBAN.

P R O D U C T I O N

New products

Ret

urne

d C

oncr

ete

with

Zer

o Im

pact

Ret

urne

d C

oncr

ete

with

Zer

o Im

pact

Ret

urne

d C

oncr

ete

with

Zer

o Im

pact

2 0

72 73

Carpet’s best friend is... an eco-compatible adhesive

72 73

Products for resilient and textile

floors and walls

78 79

Systems for laying heated floors and soundproofing against the noise of footsteps

78 79

Products for wooden

flooring

84 85

Systems for high performance flooring

84 85

Products for cementitious

and resin flooring

88 89

The joy of silence, experience the true meaning of wellbeing

88 89

Products for acoustic insulation

92 93

Work of art products

92 93

Products for building

98 99

Structural strengthening systems for concrete and masonry

98 99

Products for structural strengthening

58 59

When the going gets thinMapei technology gets going

58 59

Products for ceramics and stone materials

68 69

Colours that seal

68 69

Elastic Sealants and

Adhesives

Mapei products contribute to the quality of life by modifying and improving

aesthetics, comfort and safety in the environments in which we live. More than 1,400

technologically-advanced products which meet all the requirements of designers,

professionals and end users, supplying solutions which start from the foundations

and reach right up to the roof top. Mapei is synonymous with innovation and

constantly creates complete product systems as an answer to any type of request.

This is the real reason why Mapei is world leader in the market of adhesives, sealants

and chemical products for the building industry.

15 product lines:Certified quality and commitment to the environment

M A R K E T I N G A N D C O M M U N I C A T I O N S

2 0

2 1

102 103

Mape-Antique LineThe difference between being and wellbeing: from historical buildings to new construction

102 103

Products for the repair of masonry buildings

106 107

Harmony born from a solid bond, resistant to the rigours of life

106

106 107

Products for thermal insulation

110 111

Colours to light up the environment we live in with passion

110 111

Wall protective and decorative

coatings

122 123

Concrete admixtures for large sites

122 123

Admixturesfor

concrete

116 117

A splash of fun, without a sea of trouble

116 117

Products for

waterproofing

126 127

Everything you need for underground construction work

126 127

Products for underground constructions

130 131

Technology for high performance cement

130 131

Grinding aids

for cement

M A R K E T I N G A N D C O M M U N I C A T I O N S

Mapei is committed to research programmes targeted at developing solvent-free

products with very low emissions of volatile organic compounds (VOC), all with the

aim of improving the wellbeing of those who use the buildings where they are applied.

For Mapei, environmental responsibility is a priority. The Group has developed, and

carries on developing, the widest range of innovative products which not only respect

the most severe regulations, but also help designers and contractors create innovative

LEED-certified projects, “The Leadership in Energy and Environmental Design”, in

compliance with the U.S. Green Building Council.

MAPEI GmbHWerk Weferlingen

Ultrabond Eco S955 1K

ZulassungsnummerZ-155.10-55

EmissionsgeprüftesBauprodukt nachDIBt-Grundsätzen

A+ A B C

ÉMISSIONS DANS L’AIR INTÉRIEUR*

A+

2 2

M A R K E T I N G A N D C O M M U N I C A T I O N S

Global marketingINSTRUMENTS AND STRATEGIES TO BE KNOWN AND TO GROW

Even though our corporate philosophy aims at encouraging growth with respect

for every single local variation, Mapei follows a particularly precise marketing policy.

Marketing tools and operations are specially designed to be used alongside specific

strategies according to product range, target market and type of client.

Targeted advertising campaigns through press releases and television spots and

sponsorships for high-impact projects. All this without forgetting sales outlets and

sales points dedicated to Mapei products at authorised dealers.

A key tool is the Mapei portal which allows you to connect with all the Mapei

subsidiaries around the world.

2 3

M A R K E T I N G A N D C O M M U N I C A T I O N S

As in previous years, in 2012 Mapei didn’t miss any of the appointments with the

most important international trade fairs: Cersaie in Bologna for the ceramics sector,

Domotex in Hannover for resilients and MADE expo in Milan for the vast building

sector. All this without overlooking the numerous national and macro-regional trade

fairs organised all around the world. Alongside specially-designed interactive, multi-

media systems and video presentations, Mapei also chose to present its products

using demonstration panels where you could see for yourself how items are made

using various product systems, and live demonstration areas where you could actually

view and check the real advantages that can be achieved by using the products

correctly.

Trade fairs in Italy and around the world

MADE EXPO - MILAN - ITALY CERSAIE / SAIE - BOLOGNA - ITALY

DOMOTEX - HANNOVER - GERMANY SURFACES - LAS VEGAS - NEVADA

MOSBUILD - MOSCOW - RUSSIA TEKTONIKA - LISBON - PORTUGAL

2 4

Realtà Mapei, a “Bi-monthly magazine of current a�airs, technical news and culture”,

is an international magazine. 146,000 copies of each edition are printed and posted

to around 132,000 subscribers from our updated database all over Italy and abroad.

It is an important means of communication between the Company and the world of

building, and anyone who needs to know and use Mapei products.

Realtà Mapei: the voice of Mapei around the world

C O M M U N I C A T I O N S

Year

XIII

- N.

39

- Ju

ly 20

12

Rea

ltà

MA

PE

I ln

tern

atio

nal

N. 3

9

INTERNATIONAL IssuE 39[ ][ ][ ]Realtà[ ][ ]RealtàRealtà[Realtà[Realtà]Realtà]MAPEIA Company at the top building into future.

For 75 years, Mapei has been at the top with their quality chemical products for the buildingIndustry, products for a better job on both large and small sites. Their commitment became reality with 60 production facilities in the 5 continents, 18 main Research & Development centres with more than 900 researchers, a range of more than 1,400 products and more than 200 new products every year. These are the “figures” which make Mapei the leading international Group of chemical products for the building industry. Discover the world of Mapei: www.mapei.com

000_cover_RM_INT_dottore.indd 1 05/07/12 09.23

Year

XIII

- N

. 40

- Se

ptem

ber 2

012

Rea

ltà

MA

PE

I ln

tern

atio

nal

N. 4

0

INTERNATIONAL ISSUE 40[ ][ ][ ]Realtà[ ][ ]RealtàRealtà[Realtà[Realtà]Realtà]MAPEI

Ready-to-use liquid waterproofing membrane, with high solar reflectance and thermal emissivity, with a solar reflectance index (SRI) of 105.

Aquaflex Roof HR

/mapeispa

Discover the world of Mapei: www.mapei.com

• Reduces the surface temperature of roofs by more than 50% compared with a dark coloured covering;• 83% solar reflectance;• Solar reflectance index (SRI): 105;• Resistant to all atmospheric agents and UV rays;• Easy and pratical to apply;

• Elastic, with high crack-bridging capacity;• Resistant to light foot traffic.

Couldn’t be easier!

APPLYING THE MEMBRANE

SRI105

ADHESIVES • SEALANTS • CHEMICAL PRODUCTS FOR BUILDING

For 75 years we’ve been helping to build large and small dreams.

Year

XIII

- N

. 41

- De

cem

ber 2

012

Rea

ltà

MA

PE

I ln

tern

atio

nal

N. 4

1

INTERNATIONAL ISSUE 41[ ][ ][ ]Realtà[ ][ ]RealtàRealtà[Realtà[Realtà]Realtà]MAPEI

Year

XIII

- N.

38

- Fe

brua

ry 2

012

Rea

ltà

MA

PE

I ln

tern

atio

nal

N. 3

8

projectsSpecial Feature INTERNATIONAL IssuE 38[ ][ ][ ]Realtà[ ][ ]RealtàRealtà[Realtà[Realtà]Realtà]MAPEI

INTERNATIONALIssuE 38

[] RealtàMAPEI

Realtá MAPEI®

Americas

ISSUE

16

What’s InsidePlaniprep™

Advancing concrete repairs with FRP technology

Tisk

anic

a, p

ošta

rina

plać

ena

u po

štan

skom

ure

du 1

0431

Sve

ta N

edel

ja

[ ][ ][ ]Sv et[ ][ ]Sv etSv et[Sv et[Sv et]Sv et]MAPEI

Godi

na V

III –

bro

j 23

– st

uden

i 201

2 - n

ovos

ti, te

hnič

ka rj

ešen

ja, k

ultu

ra

TitelthemaEine starke Marke

ArchitektenmarketingPlanungshandbuch jetzt auch als E-Book

75 Jahre MapeiGiorgio Squinzis Meinung

Deutsches Handwerk hilftPeter Maffay

Der neue Mikrofaserklebstoff

für höchste Maßstabilität

Realtà MapeiAKTUELLES AUS DEUTSCHLAND UND ÖSTERREICH

12

Aus

gab

e N

r. 12

– M

ai 2

012

Rok

IX -

Nr 1

6 - S

ierp

ień

2012

Nr 16[ ][ ][ ]KronikaKronikaKronikaKronikaMAPEI

Sierpień 2012

Októ

ber 2

012

[ ]RealitaMAPEI

11Godi

na V

I – b

roj 1

0 –

dece

mba

r 201

2 –

novo

sti,

tehn

ička

reše

nja,

kul

tura

[ ][ ][ ]Svet[ ][ ]SvetSvet[Svet[Svet]Svet]MAPEI

Pošt

nina

pla

čana

pri

pošt

i 110

2 Lj

ublja

na

TIS

KOVI

NA

[ ][ ][ ]Svet[ ][ ]SvetSvet[Svet[Svet]Svet]MAPEI

Leto

VIII

– š

tevil

ka 2

3 –

nove

mbe

r 201

2 - n

ovos

ti, te

hnič

ne re

šitv

e, k

ultu

ra

Realtà Mapei Schweiz / Suisse - Ausgabe / édition 03/2012 1

S C H W E I ZS U I S S E 0 9 2 0 1 2

03Real

tà M

apei

Sch

wei

z / S

uiss

e - A

usga

be /

éditi

on 0

3/20

12

[ ]N Ú M E RO 1 0P U B L I C A C I Ó NT RI M E S T RA L[ ][ ]Reali d ad[ ][ ]MAPEI

Año

7 -

nº 1

0 - d

icie

mbr

e 20

12

MA

PE

I K

rónik

a 3

5.

szám

– 2

01

2 o

któ

ber

35

IVANKA FLASTER burkolólapokRagasztásukhoz az IVANKA Stúdió

a KERAFLEX ragasztót ajánlja

[ ][ ][ ]Krónika[ ][ ]KrónikaKrónika[Krónika[Krónika]Krónika]MAPEIépítőipari információs lap

Several introductory pages of Mapei’s corporate magazine Realtà Mapeiprinted in Italian and English in 2012

Anno

22

- N.

110

- G

enna

io -

Feb

brai

o 2

012

- co

ntie

ne I.

P. -

Bim

estra

le d

i attu

alità

, tec

nica

e c

ultu

ra

ROSE

RIO

CMP

][ ][ ][Realtà][ ][MAPEI

110110

Anno

22

- N.

111

- M

arzo

- A

prile

201

2 -

cont

iene

I.P.

- Bi

mes

trale

di a

ttual

ità, t

ecni

ca e

cul

tura

ROSE

RIO

CMP

][ ][ ][Realtà][ ][MAPEI

111111

S i l e n z i o . . .

INIZIA LA NOSTRA FESTA

Anno

22

- N.

112

- M

aggi

o -

Giug

no 2

012

- co

ntie

ne I.

P. -

Bim

estra

le d

i attu

alità

, tec

nica

e c

ultu

ra

ROSE

RIO

CMP

][ ][ ][Realtà][ ][RealtàRealtà]Realtà]Realtà[Realtà[MAPEI

112112

Anno

22

- N.

113

- L

uglio

- A

gost

o 2

012

- co

ntie

ne I.

P. -

Bim

estra

le d

i attu

alità

, tec

nica

e c

ultu

ra

ROSE

RIO

CMP

][ ][ ][Realtà][ ][MAPEI

113113

Anno

22

- N.

114

- S

ette

mbr

e -

Otto

bre

201

2 -

cont

iene

I.P.

- Bi

mes

trale

di a

ttual

ità, t

ecni

ca e

cul

tura

ROSE

RIO

CMP

][ ][ ][Realtà][ ][MAPEI

114114

ROSE

RIO

CMP

115115

Anno

22

- N.

115

- N

ovem

bre

- Di

cem

bre

201

2 -

cont

iene

I.P.

- Bi

mes

trale

di a

ttual

ità, t

ecni

ca e

cul

tura

Realtà Mapei has also been published in 16 dierent languages!

2 5

C O M M I T M E N T T O S P O R T

The Mapei Sport Research Centre, founded in 1996 to o�er rationalised scientific support with a precise ethical approach to athletes from all sporting disciplines, is today a renowned international centre. 2012 was the 15th anniversary of the Centre and this important event was celebrated with a convention and the presentation of a research grant to honour the memory of Professor Aldo Sassi, former Director of the Centre and, along with Giorgio Squinzi, its co-founder.Now at its eighth event, Mapei Day 2012 was also the icing on the cake for the celebrations to mark the seventy fifth anniversary of the founding of Mapei and the number 75 was used on the Santini cycling jerseys.

Mapei Sport Research Centre and Mapei Day 2012

and this important event was celebrated with a convention and the presentation of a irector of the

prog

ram

ma

program

ma

2° Convegno Centro Ricerche MAPEI Sport

Presentazione 1° assegno di ricerca “Aldo Sassi”

per Laureati in scienze motorie

Sabato 25 febbraio 2012 - ore 9,00 - 13,00

Auditorium MAPEI - Viale Jenner, 4 - Milano

Sport Service MAPEI - Via Don Minzoni, 34 - 21053 Castellanza (VA)

Mapei Sport e Ricerca: storia e prospettive future

ASSEGNO DI RICERCA “ALDO SASSI”

promosso da Mapei Sport in collaborazione con Fondazione MAI Confindustria.

Pubblicazione bando 01/02/2012 - Chiusura bando 31/03/2012.

Assegnazione ufficiale assegno 15/04/2012.

Informazioni utili

Possono accedere alla selezione i Laureati in scienze motorie da non più di 18 mesi alla data

di pubblicazione del bando presentando domanda sul sito www.fondazionemai.it nell’apposita

area dedicata entro il 31 marzo 2012.

Per scaricare il bando completo visitare il sito www.fondazionemai.it oppure www.mapeisport.it

Per ulteriori informazioni [email protected] oppure telefono 0331-575757.

Sport Service MAPEI - Via Don Minzoni, 34 - 21053 Castellanza (VA)

e con Fondazione MAI Confindustria.

ti in scienze motorie da non più di 18 mesi alla data

nell’apposita

www.mapeisport.it

www.mapeisport.it

www.mapeisport.it

www.mapeisport.it

[email protected] oppure telefono 0331-575757.

L’iscrizione al convegno è obbligatoria

inviando i propri dati all’indirizzo

e-mail: [email protected]

ore 8,30

Registrazione

ore 9,00

15 anni di attività del

Centro Ricerche Mapei Sport

Claudio Pecci

Centro Ricerche MAPEI Sport,

Castellanza (VA)

Mapei e Ricerca:

un binomio inscindibile

Giorgio Squinzi

Mapei SpA, Milano

Investire in ricerca per offrire

un futuro ai giovani

Diana Bracco

Presidente Fondazione MAI Confindustria

Ricerca e sport, importanti strumenti

della comunicazione aziendale

Adriana Spazzoli

Mapei SpA, Milano

ore 10,00

La ricerca come supporto

per l’evoluzione dello sport

Impellizzeri Franco

Dipartimento Ricerca e Sviluppo,

Schulthess Clinic,

Centro di Eccellenza FIFA,

Zurich, Svizzera

CeRiSM, Università degli Studi di Verona

ore 10,30

La ricerca come

risorsa per lo sport,

allenare su basi scientifiche

Luca Guercilena

Team RadioShack - Leopard,

Lussemburgo

ore 11,00

L’innovazione

tecnologica e la sua

applicazione nella ricerca e

nello sport

Andrea Morelli

Centro Ricerche MAPEI Sport, Castellanza (VA)

Coffee break

ore 11,45

Presentazione

1° assegno di ricerca “ALDO SASSI”

Fondazione MAI

Claudio Pecci

Centro Ricerche MAPEI Sport, Castellanza (VA),

ore 12,00

La BMX nuova disciplina olimpica:

il primo progetto di ricerca

Ermanno Rampinini

Centro Ricerche MAPEI Sport, Castellanza (VA)

ore 12,15

Specialità ciclistiche emergenti e

mondializzazione: necessità di una

ricerca applicata

Mario Zorzoli

Unione Ciclistica Internazionale, Aigle, Svizzera

ore 12,30

Nuove frontiere del ciclismo

Claudio Gregori

RCS La Gazzetta dello Sport, Milano

ore 13,00 - Brunch

2 6

C O M M I T M E N T T O S P O R T

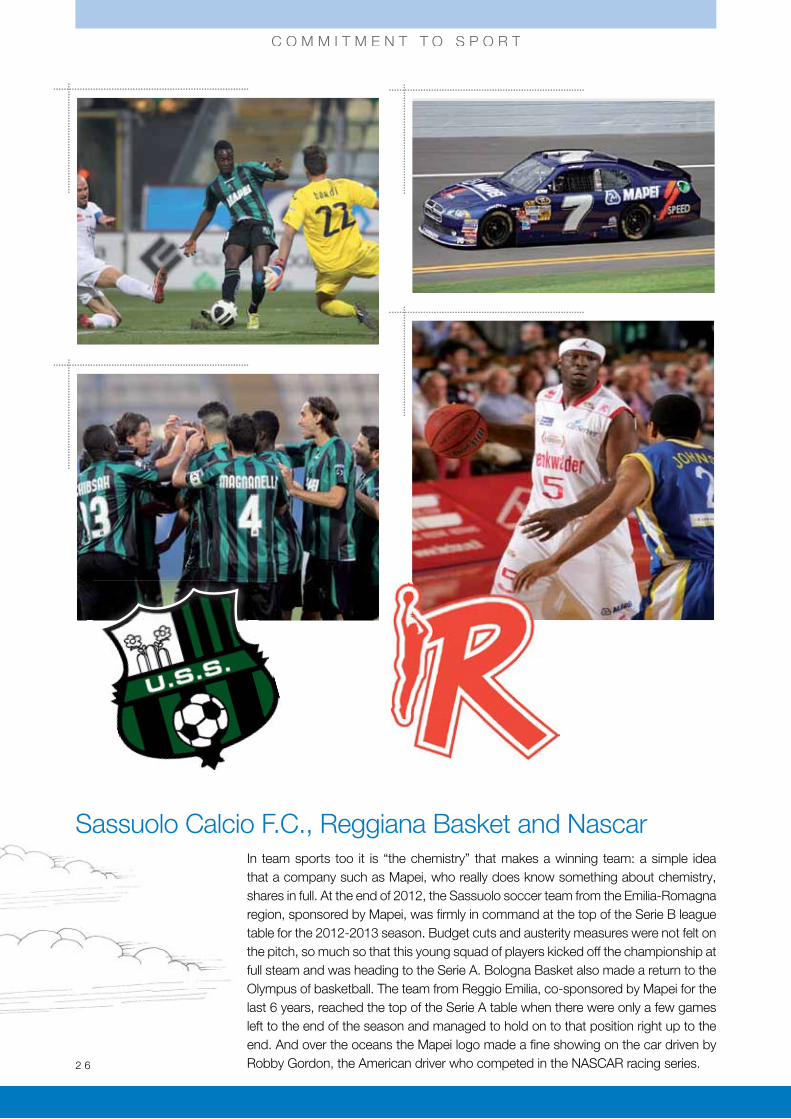

In team sports too it is “the chemistry” that makes a winning team: a simple idea that a company such as Mapei, who really does know something about chemistry, shares in full. At the end of 2012, the Sassuolo soccer team from the Emilia-Romagna region, sponsored by Mapei, was firmly in command at the top of the Serie B league table for the 2012-2013 season. Budget cuts and austerity measures were not felt on the pitch, so much so that this young squad of players kicked o� the championship at full steam and was heading to the Serie A. Bologna Basket also made a return to the Olympus of basketball. The team from Reggio Emilia, co-sponsored by Mapei for the last 6 years, reached the top of the Serie A table when there were only a few games left to the end of the season and managed to hold on to that position right up to the end. And over the oceans the Mapei logo made a fine showing on the car driven by Robby Gordon, the American driver who competed in the NASCAR racing series.

Sassuolo Calcio F.C., Reggiana Basket and Nascar

2 7

C O M M I T M E N T T O S P O R T

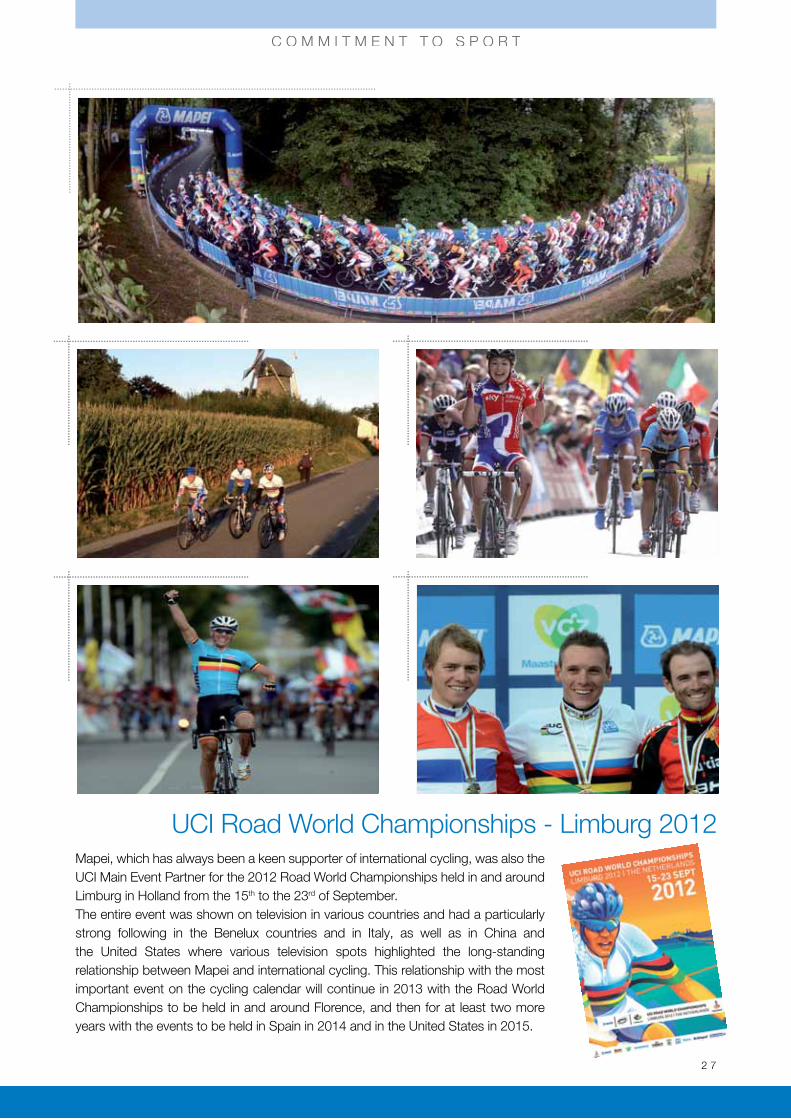

Mapei, which has always been a keen supporter of international cycling, was also the UCI Main Event Partner for the 2012 Road World Championships held in and around Limburg in Holland from the 15th to the 23rd of September.The entire event was shown on television in various countries and had a particularly strong following in the Benelux countries and in Italy, as well as in China and the United States where various television spots highlighted the long-standing relationship between Mapei and international cycling. This relationship with the most important event on the cycling calendar will continue in 2013 with the Road World Championships to be held in and around Florence, and then for at least two more years with the events to be held in Spain in 2014 and in the United States in 2015.

UCI Road World Championships - Limburg 2012

2 8

C O M M I T M E N T T O C U L T U R E

Mapei invites all its friends, clients and collaborators to enjoy great music, such as the occasion to celebrate its 75th anniversary, with the presentation of a memorable Aida at the La Scala Theatre in Milan on the 19th and 21st of April. On the 30th of October, a concert in support of Vidas marked the return to the La Scala stage of Maestro Claudio Abbado. Another magnificent event sponsored by Mapei was held on the 2nd of December at the New Opera House Theatre in Florence: Turandot by Giacomo Puccini, conducted by Zubin Mehta and directed by Zhang Yimou. And an unforgettable concert sponsored by Mapei was held in Rome on the 13th of December at the Santa Cecilia National Academy. The stars were two great orchestra conductors: Daniel Barenboim, Musical Director of the Berlin State Opera House and the La Scala Theatre in Milan, and Antonio Pappano, conductor of the Santa Cecilia National Academy Orchestra.

Two memorable concerts and two great operas

AIDA - LA SCALA THEATRE, MILAN - 19TH and 21ST of February

CONCERT CONDUCTED BY ANTONIO PAPPANO - DANIEL BARENBOIM AT THE PIANOSANTA CECILIA NATIONAL ACADEMY, ROME - 13TH of December

TURANDOT CONDUCTED BY ZUBIN MEHTANEW OPERA HOUSE THEATRE, FLORENCE - 2ND of December

CONCERT CONDUCTED BY CLAUDIO ABBADOLA SCALA THEATRE, MILAN - 30TH of October

2 9

Mapei GroupConsolidated financial statements year endedDecember 31st 2012

3 0

3 1

MANAGEMENT REPORT

Report to sole shareholder year ended December 31st, 2012

Dear Sole Shareholder,

The consolidated financial accounts of the Mapei Group at December 31st, 2012, which we

hereby submit for your approval, show a consolidated net profit of € 28.0 million (€ 19.2 m

in 2011) after depreciations and devaluations of € 76.1 million (€ 81.9 m in 2011) and after

income tax accruals of € 17.2 million (€ 23.8 m in 2011).

The net profit pertaining to the Group after minority interest is € 27.3 million (€ 17.8m in

2011).

Global economic trends The world GDP recorded in 2012 an increase of 3.3%, leading to a slowdown compared

to 2011. The previous year (2011) showed an increase of 3.9%. In 2012 the GDP grew

by 1.3% in the developed countries while in the emerging nations the growth was 5.3%.

It has to be mentioned that 2012 showed an economic downturn in EU area as in 2011,

in particular in the Southern Europe Area. France and Germany, the most advanced

economies, had a slowdown too. Among the developed countries Japan, heavily hit by

the earthquake in 2011, recorded a GDP increase of 2.2%. In 2012 US GDP increased by

2.2%, showing an improvement compared to 2011 (+1.8%). Among the emerging nations

the economic trend has been heterogeneous; the GDP increased by 7.8% in China, by

4.9% in India, by 1.5% in Brazil, by 2.0% in Eastern Europe and by 5.3% in Middle East

and North Africa. In 2012 the economic development related to these countries declined,

because of the reduction of the export to the developed nations. In 2012 the world building

market recorded a growth of 3.5%; the five continents had a different impact on this result.

An analysis by the seven macro regions where our Group operates will follow, with a focus

on the construction sector trend and the position of our subsidiaries in the market.

3 2

M A N A G E M E N T R E P O R T

Group economic trends The Mapei Group, within the outlined macro-economic picture, recorded a good sales

trend in the various geographical areas, showing the best results in Asia, Oceania and

Americas (double digit growth). Negative results have been showed only by the Italian

market.

The Mapei Group consolidated turnover exceeded € 1,746.2 million against € 1,697.8

million in the previous period. The increase in net sales in our Group has been equal to

€ 48.4 million, which represents a growth of 2.9%, lower than the years before. These

performances have to be evaluated as a positive result due to the situation of the world

building market.

The increase in turnover is explained by an internal growth. The contribution given by the

company incorporated for the first fiscal year (Mapei Construction Chemicals Panama Sa)

is around € 7 million only.

After the decrease recorded in 2011, net profit had a significant increase of 45.6%, moving

from € 19.2 million to € 28 million, despite the results of some start-up companies.

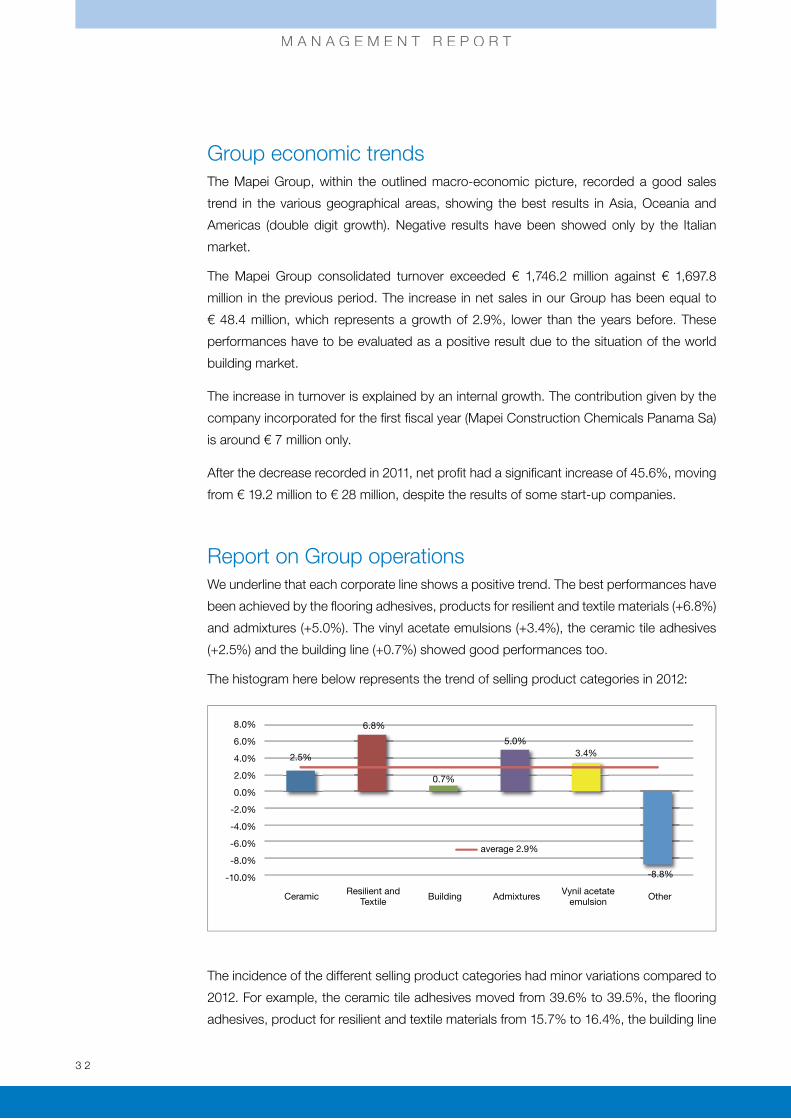

Report on Group operationsWe underline that each corporate line shows a positive trend. The best performances have

been achieved by the flooring adhesives, products for resilient and textile materials (+6.8%)

and admixtures (+5.0%). The vinyl acetate emulsions (+3.4%), the ceramic tile adhesives

(+2.5%) and the building line (+0.7%) showed good performances too.

The histogram here below represents the trend of selling product categories in 2012:

The incidence of the different selling product categories had minor variations compared to

2012. For example, the ceramic tile adhesives moved from 39.6% to 39.5%, the flooring

adhesives, product for resilient and textile materials from 15.7% to 16.4%, the building line

Ceramic Resilient and Textile Building Admixtures Vynil acetate

emulsion Other

8.0%

6.0%

4.0%

2.0%

0.0%

-2.0%

-4.0%

-6.0%

-8.0%

-10.0%

average 2.9%

2.5%

6.8%

0.7%

5.0%3.4%

-8.8%

3 3

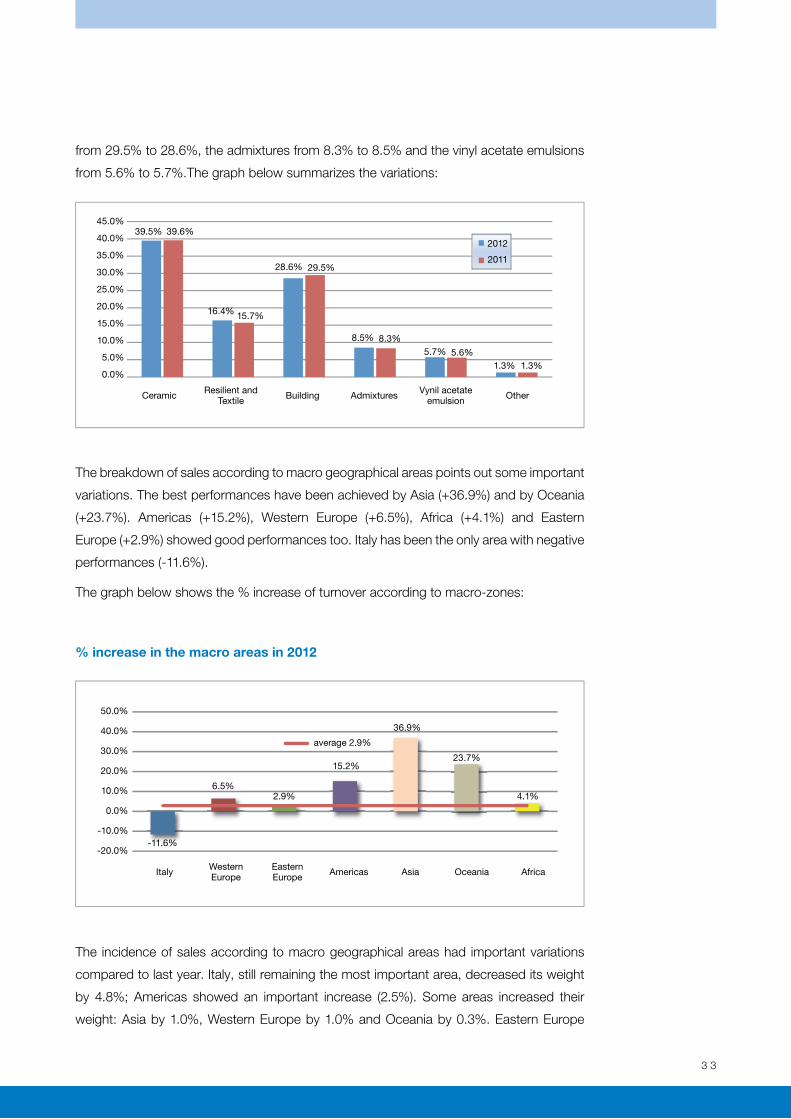

from 29.5% to 28.6%, the admixtures from 8.3% to 8.5% and the vinyl acetate emulsions

from 5.6% to 5.7%.The graph below summarizes the variations:

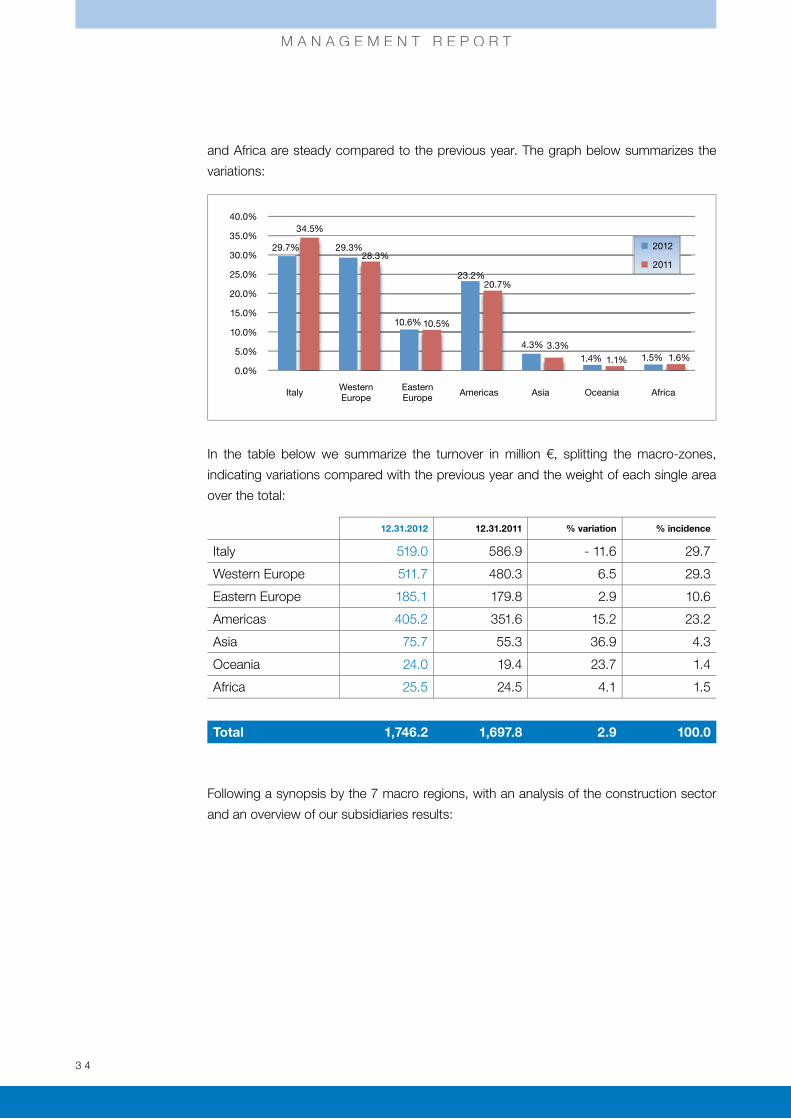

The breakdown of sales according to macro geographical areas points out some important

variations. The best performances have been achieved by Asia (+36.9%) and by Oceania

(+23.7%). Americas (+15.2%), Western Europe (+6.5%), Africa (+4.1%) and Eastern

Europe (+2.9%) showed good performances too. Italy has been the only area with negative

performances (-11.6%).

The graph below shows the % increase of turnover according to macro-zones:

% increase in the macro areas in 2012

The incidence of sales according to macro geographical areas had important variations

compared to last year. Italy, still remaining the most important area, decreased its weight

by 4.8%; Americas showed an important increase (2.5%). Some areas increased their

weight: Asia by 1.0%, Western Europe by 1.0% and Oceania by 0.3%. Eastern Europe

Ceramic Resilient and Textile Building Admixtures Vynil acetate

emulsion Other

45.0%

40.0%

35.0%

30.0%

25.0%

20.0%

15.0%

10.0%

5.0%

0.0%

39.5% 39.6%

16.4%

28.6%

2012

2011

15.7%

29.5%

8.5% 8.3%5.7% 5.6%

1.3% 1.3%

Italy Western Europe

Eastern Europe Americas Asia Oceania Africa

50.0%

40.0%

30.0%

20.0%

10.0%

0.0%

-10.0%

-20.0%

average 2.9%

6.5%

-11.6%

2.9%

15.2%

36.9%

23.7%

4.1%

3 4

M A N A G E M E N T R E P O R T

and Africa are steady compared to the previous year. The graph below summarizes the

variations:

In the table below we summarize the turnover in million €, splitting the macro-zones,

indicating variations compared with the previous year and the weight of each single area

over the total:

12.31.2012 12.31.2011 % variation % incidence

Italy 519.0 586.9 - 11.6 29.7

Western Europe 511.7 480.3 6.5 29.3

Eastern Europe 185.1 179.8 2.9 10.6

Americas 405.2 351.6 15.2 23.2

Asia 75.7 55.3 36.9 4.3

Oceania 24.0 19.4 23.7 1.4

Africa 25.5 24.5 4.1 1.5

Total 1,746.2 1,697.8 2.9 100.0

Following a synopsis by the 7 macro regions, with an analysis of the construction sector

and an overview of our subsidiaries results:

40.0%

35.0%

30.0%

25.0%

20.0%

15.0%

10.0%

5.0%

0.0%

29.7%

34.5%

29.3%

10.6%

2012

201128.3%

10.5%

23.2%20.7%

4.3% 3.3%1.5% 1.6%

Italy Western Europe

Eastern Europe Americas Asia Oceania Africa

1.4% 1.1%

3 5

ItalyIn 2012 Italian GDP had a strong slowdown

of 2.4%. The national economy was strongly

affected by the fiscal measures taken over by

the Italian Government, by the credit crunch

and by the uncertain scenario produced by the

financial situation in the EU Area.

The construction market went through an

economic downturn as in the previous four

years (2011, 2010, 2009, 2008). According to

the statistics of Ance institute the slowdown

in investments was more than 7.0%. Even

last year the construction market, where our

Group operates, had worse performances than

the rest of the economy. The housing market

showed a heavy downturn (-17%), only partially

counterbalanced by the renovation segment.

The building market showed a downturn too

(-8%). The begin of this slowdown is even older

than the one related the housing market. The

macro-economic scenario described above

discouraged also the public works; the slowdown in investments in the construction

market was more than 10%.

In the macro-economic picture described above, the performances of the Italian companies

have been negatively affected. The volume generated moved from € 586.9 million to € 519.0

million (-11.6%). Italy decreased its weight by 4.8% considering the total turnover; anyway

this area still represents the 30% of the total sales. We are present in the country with 7

production companies and 9 plants, 3 research centres and 9 quality control laboratories

and 3 service companies. During 2012 Mapefin Srl has been merged with Mapei Spa.

In 2012, obviously, also the result of the area was negatively influenced by the scenario

described above. At the beginning of 2013 some measures have been taken in order to

reach better performances already starting from the next year.

The only company with good results in sales was Vinavil Spa (+0.8%).

Companies of the Group:

Adesital Spa

Cercol Spa

Mapei Betontechnik Italia Srl

Mapei Spa

Mapintec Srl

Mosaico+ Srl

Polyglass Spa

Progetto Mosaico+ Srl

Vaga Srl

Vinavil Spa

3 6

M A N A G E M E N T R E P O R T

Western EuropeThe Western Europe countries showed different

trends in 2012. The Northern and Central Europe

nations recorded a moderate GDP growth while the

Southern ones had a heavy recession.

Germany recorded a GDP rise of 0.9% compared

to a GDP rise of 3.1% in 2011. France had a lower

GDP growth (0.1%) compared to the year before

(+1.7%). UK had a slowdown (-0.4%). Spain showed

a further recession; GDP showed a decrease of

1.5%.

The construction market went through an economic

downturn as in the previous four years; the drop

has been estimated around 2%. EU area showed

the lowest investments in this industry on a world-

wide level. It has to be considered that Portugal,

Greece and Ireland showed a heavy recession as

well as Spain.

Among the most important markets, Spain had a

further drop in the building industry. The value of

the investments in 2012 showed a decrease of

11%. The housing market had the strongest fall. In

Spain during 2007 have been realized 685,000 new

houses, while in 2012 only 110,000. France targeted

a moderate growth in the housing market of 1%. UK

had a positive trend too after the slowdown in 2011.

The construction market showed better results

than the rest of the economy.

The construction market in Germany, best

performer in 2011, has recorded this year a steady

performance. Despite a good development of the

housing market, the industrial building sector and the public works showed a decline.

Mapei Group achieved a growth in terms of volumes in this area (€ 31.4 million), with an

increase of 6.5% compared to 2011. Turnover for 2012 was equal to € 511.7 million.

Mapei Group operates in Western Europe with 13 production companies, 16 plants,

6 research centres, 16 quality control laboratories, 8 trading companies and 4 service

companies.

The EBITDA had a rise compared to 2011 and it remains the first one in the Group.

In terms of sales, the companies with the best performances were Polyglass GB Ltd

(+21.0%), Mapei Uk Ltd (+19.6%) and Mapei Benelux Sa (+14.2%).

Companies of the Group:

Cercol Iberia SlIbermapei SaLusomapei SaMapefin Austria GmbhMapefin Benelux SaMapefin Deutschland GmbhMapei AbMapei AsMapei Benelux SaMapei Betontechnik GmbhMapei Denmark As Mapei France SaMapei Gmbh (A) Mapei Gmbh (D)Mapei Hellas SaMapei Nederland Bv Mapei OyMapei Suisse SaMapei UK LtdPolyglass GB LtdRasco Bitumentecknik GmbhResconsult AsSopro Bauchemie Gmbh (A) Sopro Bauchemie Gmbh (D) Sopro Nederland Bv

3 7

Eastern EuropeIn 2012, the economic growth of Eastern European

Countries had a slowdown; GDP experienced a

rise of 2%, while 2011 showed a strong growth

(5%). The Eastern Europe Nations had different

economic trends. GDP had an important rise in

Russia (4%), in particular thanks to the energy

industry. Good performances in term of growth

were realized by Ukraine (3.0%) and Turkey (3.0%)

even if the rise has been lower than the two years

before. Poland had a good trend as in the last

decade, with a GDP rise of 2.4%. Bulgaria and

Romania had a lower GDP growth, while Hungary

and Czech Republic showed a recession (-1.0%).

In 2012 the construction market showed a GDP

rise of 3.3%; the result is better than the rest of

the economy. Russia has been the country with

the best performances in the building industry

(7.6%). A growth has been recorded by Poland

and Turkey too but at a lower level compared

to the years before. Bulgaria and Romania

experienced a moderate growth in line with the

rest of the economy. Hungary and Czech Republic

experienced a slowdown and an upturn is not

foreseen also for 2013.

Mapei Group operates in Eastern Europe with 6

production companies, 7 plants, 7 quality control

laboratories, 1 research centre and 9 trading

companies. The turnover in the area in 2012 was

€ 185.1 million against € 179.8 million of last year,

with an increase of 2.9%. EBITDA in this area had

a small increase compare to last year and it is the

third one in the Group.

The companies with the best performances in

sales have been Mapei Croatia Doo (+58.7%), Zao

Mapei (+23.8%) and Mapei Ukraina Llc (+20.8%).

Companies of the Group:

Gòrka Cement Spzoo

Mapei Bulgaria Eood

Mapei Croatia Doo

Mapei Doo

Mapei Kft

Mapei Polska Spzoo

Mapei Romania Srl

Mapei Sk Sro

Mapei Sro

Mapei Ukraina Llc

Polyglass Romania Srl

Sopro Cz Sro

Sopro Hungaria Kft

Sopro Polska Spzoo

Zao Mapei

3 8

M A N A G E M E N T R E P O R T

AmericasIn 2012 United States had a moderate GDP growth

of 2.2% compared to 1.8% recorded in 2011. The

rise was driven by the improvement of the labor

market and by the reduction of the private sector

bank debt. Canadian GDP showed a rise of 1.9%,

compared to 2.5% recorded in 2011.

The housing market in the US showed a rise of 10%

and it has been the locomotive for the whole building

industry. According to the statistics the growth of the

construction sector was equal to 6%. The building

industry experienced a more regular trend in Canada

where the recession took place only in 2009. In 2012

the Canadian investments increased by 3.4%, the

indicators showed solidity in the building market but

the housing market and the public works had good

performances too.

Mexico had a GDP rise of 3.8%. The

construction market experienced the

same trend also thanks to the upturn

of the US economy. Panama had an

important GDP growth of 8.5% compared

to 10.6% recorded in 2011.

South America showed a growth with

a GDP rise of 3.2% compared to 4.5%

in 2011. In the countries where we are

present the economy had a different

trend. Argentina experienced a rise of

2.6%, recording an important drop compared to 2011 where the growth was equal to

8.9%. Venezuela had a growth of 5.7%, even better than 2011 (4.2%).

In South America the construction market has many potentialities and in 2012 the

investments increased by 3%, in line with the rest of the economy. The development was

partly affected by the delay in public works happened in Brazil and by the slowdown

recorded in Argentina. Venezuela had a different trend; the construction market performed

better in 2012 than in 2011.

Mapei is present in the region with 8 production companies, 20 plants, 4 research centres,

20 quality control laboratories, 2 trade companies and 2 service companies. The turnover

in this area in 2012 was € 405.2 million against € 351.6 million in 2011, with an increase of

15.2%. The weight of this area on consolidated turnover increased from 20.7% to 23.2%.The

profitability had an important increase (+25.6%) and remains one of the best in the Group.

The companies with the best performances in sales have been Mapei Mexico Sa de Cv

(+69.8%), Mapei Venezuela Ca (+52.4%) and Mapei Corp (+15.9%).

Companies of the Group:

4307721 Canada IncCaribbean Sand Co. LtdMapei Argentina Sa Mapei Caribe IncMapei Contruction Chemicals Panama SaMapei CorpMapei East CorpMapei IncMapei Mexico Sa de Cv Mapei Venezuela CaPolyglass Usa IncVinavil Americas Inc

3 9

AsiaThe Asian continent has been the driving force

of the world economy as in the previous years.

The growth was attributable to the emerging

countries, showing an average GDP rise of

6.7% (7.8% in 2011). It has to be mentioned the

positive trend of China 7.8% and India 4.9%.

Among the developed countries South Korea

had a GDP rise of 2.7%, while

Japan, strongly affected in 2011

by tragic events, recorded a rise

equal to 2.2%.

In the Middle East Area Saudi

Arabia, the most dynamic

market of the region, showed

a strong GDP growth

(6.0%). United Arab Emirates

experienced a rise in GDP of

4%, after the growth recorded

in 2011 of 5%.

In 2012 the growth of the construction market was sustained by the emerging countries.

The best performance in term of growth was realized by China (7%). The extreme dynamism

of this industry forced the Chinese Government to adopt more conservative measures, in

order to lead the economic growth towards sustainable levels. The Indian construction

market had a GDP growth equal to 5%, recording a small drop compared to the year

before. The gentrification is the driving force of the development in the building industry, in

particular in the housing market. Also in 2012 in the Middle East area positive results were

reached by Saudi Arabia; the growth is estimated around 5%. The good performances

of the oil market sustained the investments plan in housing and infrastructure segments.

Mapei Group is present in Asia with 8 production companies, 8 plants, 4 research centres,

8 quality control laboratories and 1 trading company. The turnover generated in Asia in

2012 was equal to € 75.7 million against € 55.3 million in the previous year, with an increase

of 36.9%. The new organizational development put in place generated a positive Ebitda

for the first time.

We underline the rise in sales of Mapei China Ltd (+88.8%), Mapei Malaysia Sdn Bhd

(+61.1%) and Mapei Construction Materials Co Ltd Guangzhou (+25.7%).

Companies of the Group:

Innovative Building Solution Llc

Mapei China Ltd

Mapei Construction Materials Company Ltd (Guangzhou)

Mapei Construction Materials Company Ltd (Shanghai)

Mapei Construction Products India Ltd

Mapei Far East Pte Ltd

Mapei Korea Ltd

Mapei Malaysia Sdn Bhd

Mapei Vietnam Ltd

4 0

M A N A G E M E N T R E P O R T

OceaniaIn Australia, the most important economy of the

area, GDP had a rise of 3.3%, driven by the mining

sector. This is a country with an enviable position

among the most developed nations; Australia was

only partly affected by the world crisis thanks to

the growing integration with the emerging Asian

countries. The 2012 GDP rise has been the best

in the last five years.

New Zealand, the second most important

economy of the area, experienced a GDP rise

of 2.2%. The result has been an important

improvement compared to the year before (1.2%)

when the country was strongly affected by the

earthquakes.

In Australia the building market recorded lower performances than the rest of the

economy, in particular in housing market and in public works. In New Zealand the

building market experienced a better trend compared to Australia. The good results

were attributable to the housing market and the public works necessary after the 2011

earthquakes.

Mapei Group is present in Oceania with 1 production company, 1 plant, 1 quality control

laboratory in Australia and 1 trading company in New Zealand. The turnover generated in

the region was over € 24.0 million, against € 19.4 million of last year, with an increase of

23.7%. The EBITDA was very good as in the previous year.

Our companies in the area registered good results in terms of sales: Mapei Australia

Pty Ltd increased its volume by 26.2% while Mapei New Zealand Ltd showed a rise of

10.7%.

Companies of the Group:

Mapei Australia Pty Ltd

Mapei New Zealand Ltd

4 1

AfricaIn Africa the GDP had a consistent rise in 2012.

GDP of Sub Saharan Africa grew by 5.0%,

thanks to the export towards the emerging Asian

economies. The result is in line with the year 2011.

South Africa, the most important economy of the

Area, recorded a lower GDP growth (2.6%) and

suffered the high unemployment rate, estimated

around 25%. Moreover this country, having many

connections with Europe, was negative influenced

by the recession started in the EU area.

In North Africa, the economy was strongly

affected by the uncertain political scenarios. The

averaged GDP growth has been equal to 2.5%.

Egypt showed a moderate growth of 2.0%, Morocco of 2.9%, Tunisia of 2.7% and Algeria

of 2.6%. Libya had a better GDP trend after the end of the war happened in 2011.

The construction market in Sub Saharan Africa had a good trend. The growth was

driven by public works and in particular by Chinese and European investments in road

infrastructures, communications industry and energy segment. The building industry in

North Africa had an important rise too. The development was attributable both to the

housing market and to the public works.

We are present in Egypt with a joint venture, Vinavil Egypt for Chemicals Sae, located in

Suez Industrial Zone. The company has 1 production plant in Suez industrial zone with 1

quality control laboratory. The second company, Mapei South Africa Pty Ltd, is a production

company selling mainly admixtures in the South African Market and neighbouring countries.

The growth generated in Africa by our Group in 2012 was moderate (+4.1%) with a turnover

equal to € 25.5 million. We are strongly convinced that Mapei Group will be able to reach

good results in this area.

The EBITDA showed a positive result but the performances were lower than 2011.

Vinavil Egypt for Chemicals Sae turnover increased by 3.5%, while Mapei South Africa Pty

Ltd has recorded an increase of 6.7%.

Companies of the Group:

Mapei South Africa Pty Ltd

Vinavil Egypt for Chemicals Sae

4 2

M A N A G E M E N T R E P O R T

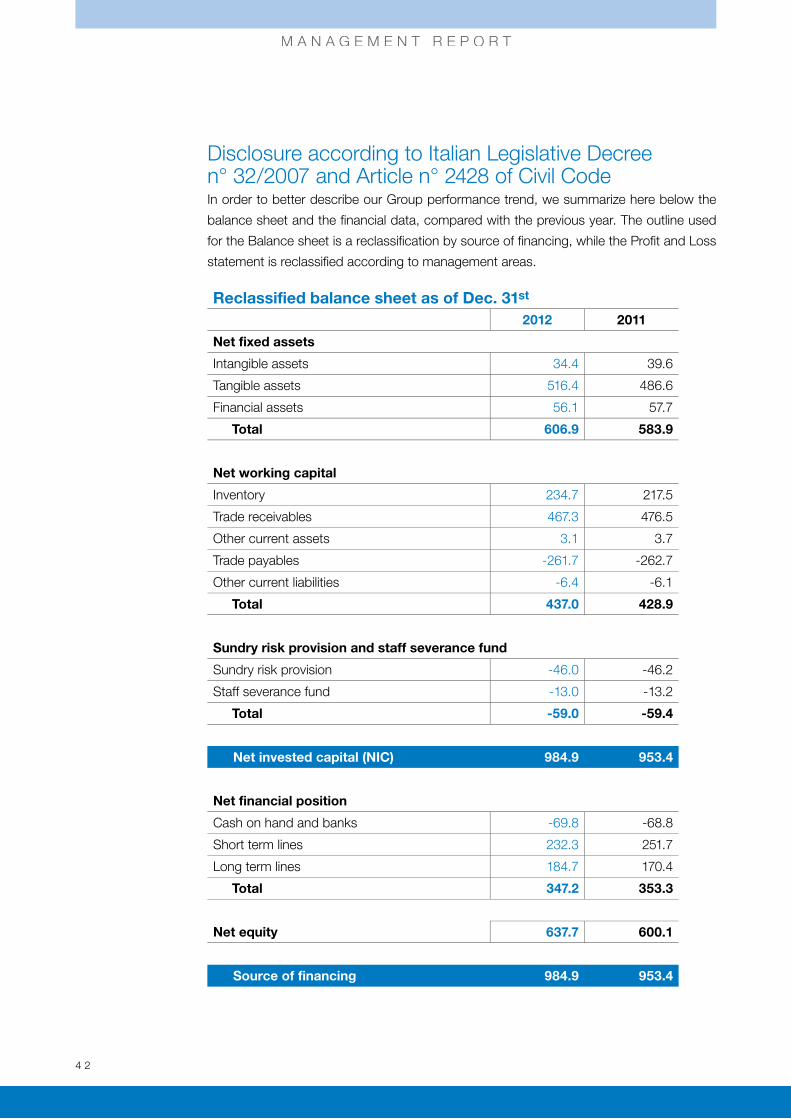

Disclosure according to Italian Legislative Decree n° 32/2007 and Article n° 2428 of Civil Code In order to better describe our Group performance trend, we summarize here below the

balance sheet and the financial data, compared with the previous year. The outline used

for the Balance sheet is a reclassification by source of financing, while the Profit and Loss

statement is reclassified according to management areas.

Reclassified balance sheet as of Dec. 31st

2012 2011

Net fixed assets

Intangible assets 34.4 39.6

Tangible assets 516.4 486.6

Financial assets 56.1 57.7

Total 606.9 583.9

Net working capital

Inventory 234.7 217.5

Trade receivables 467.3 476.5

Other current assets 3.1 3.7

Trade payables -261.7 -262.7

Other current liabilities -6.4 -6.1

Total 437.0 428.9

Sundry risk provision and staff severance fund

Sundry risk provision -46.0 -46.2

Staff severance fund -13.0 -13.2

Total -59.0 -59.4

Net invested capital (NIC) 984.9 953.4

Net financial position

Cash on hand and banks -69.8 -68.8

Short term lines 232.3 251.7

Long term lines 184.7 170.4

Total 347.2 353.3

Net equity 637.7 600.1

Source of financing 984.9 953.4

4 3

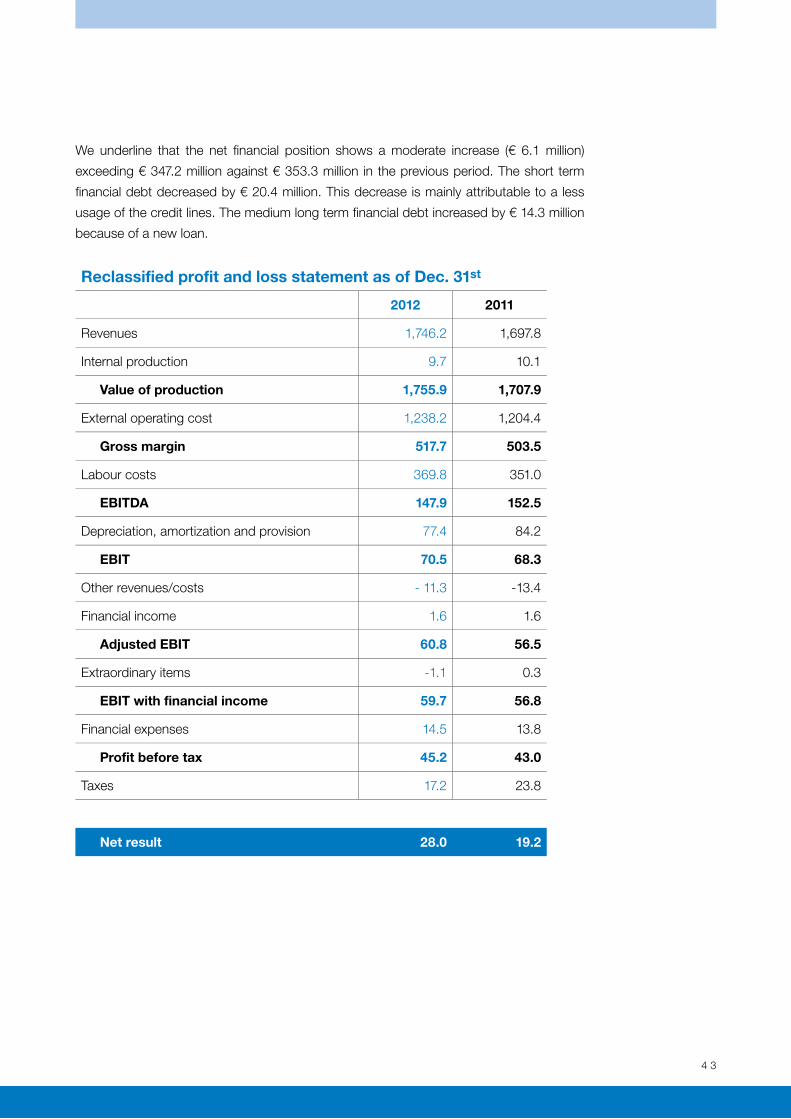

We underline that the net financial position shows a moderate increase (€ 6.1 million)

exceeding € 347.2 million against € 353.3 million in the previous period. The short term

financial debt decreased by € 20.4 million. This decrease is mainly attributable to a less

usage of the credit lines. The medium long term financial debt increased by € 14.3 million

because of a new loan.

Reclassified profit and loss statement as of Dec. 31st

2012 2011

Revenues 1,746.2 1,697.8

Internal production 9.7 10.1

Value of production 1,755.9 1,707.9

External operating cost 1,238.2 1,204.4

Gross margin 517.7 503.5

Labour costs 369.8 351.0

EBITDA 147.9 152.5

Depreciation, amortization and provision 77.4 84.2

EBIT 70.5 68.3

Other revenues/costs - 11.3 -13.4

Financial income 1.6 1.6

Adjusted EBIT 60.8 56.5

Extraordinary items -1.1 0.3

EBIT with financial income 59.7 56.8

Financial expenses 14.5 13.8

Profit before tax 45.2 43.0

Taxes 17.2 23.8

Net result 28.0 19.2

4 4

M A N A G E M E N T R E P O R T

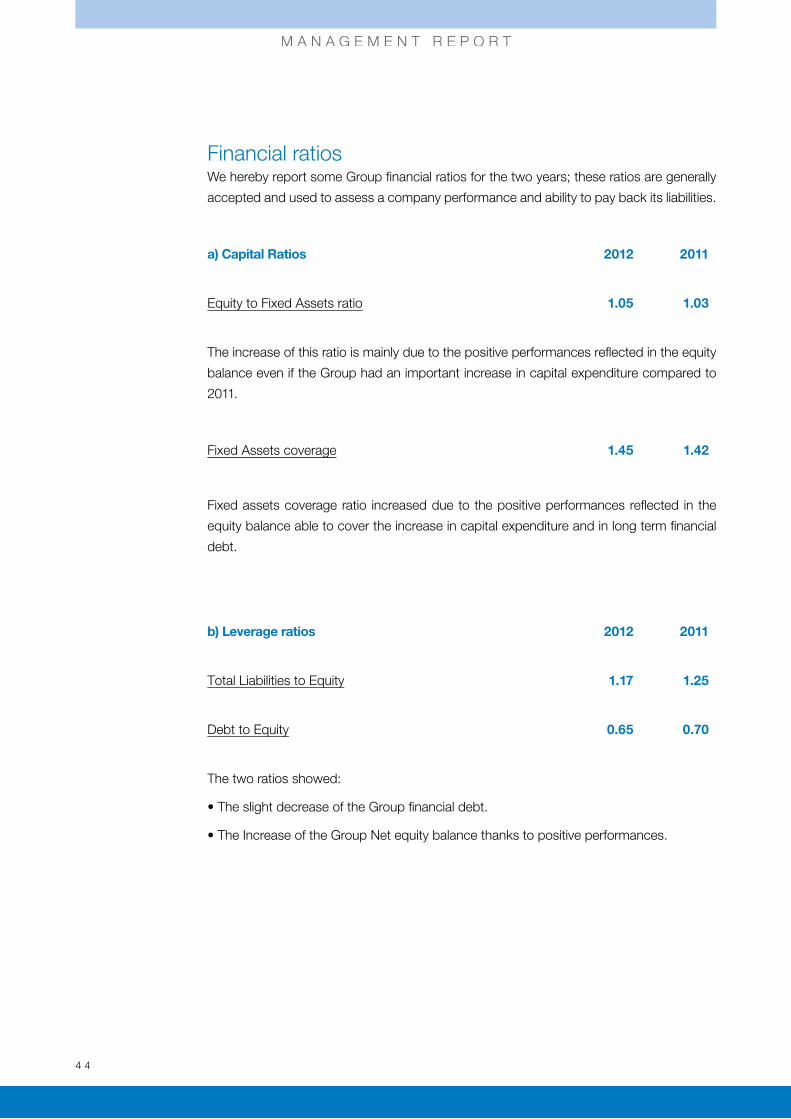

Financial ratiosWe hereby report some Group financial ratios for the two years; these ratios are generally

accepted and used to assess a company performance and ability to pay back its liabilities.

a) Capital Ratios 2012 2011

Equity to Fixed Assets ratio 1.05 1.03

The increase of this ratio is mainly due to the positive performances reflected in the equity

balance even if the Group had an important increase in capital expenditure compared to

2011.

Fixed Assets coverage 1.45 1.42

Fixed assets coverage ratio increased due to the positive performances reflected in the

equity balance able to cover the increase in capital expenditure and in long term financial

debt.

b) Leverage ratios 2012 2011

Total Liabilities to Equity 1.17 1.25

Debt to Equity 0.65 0.70

The two ratios showed:

• The slight decrease of the Group financial debt.

• The Increase of the Group Net equity balance thanks to positive performances.

4 5

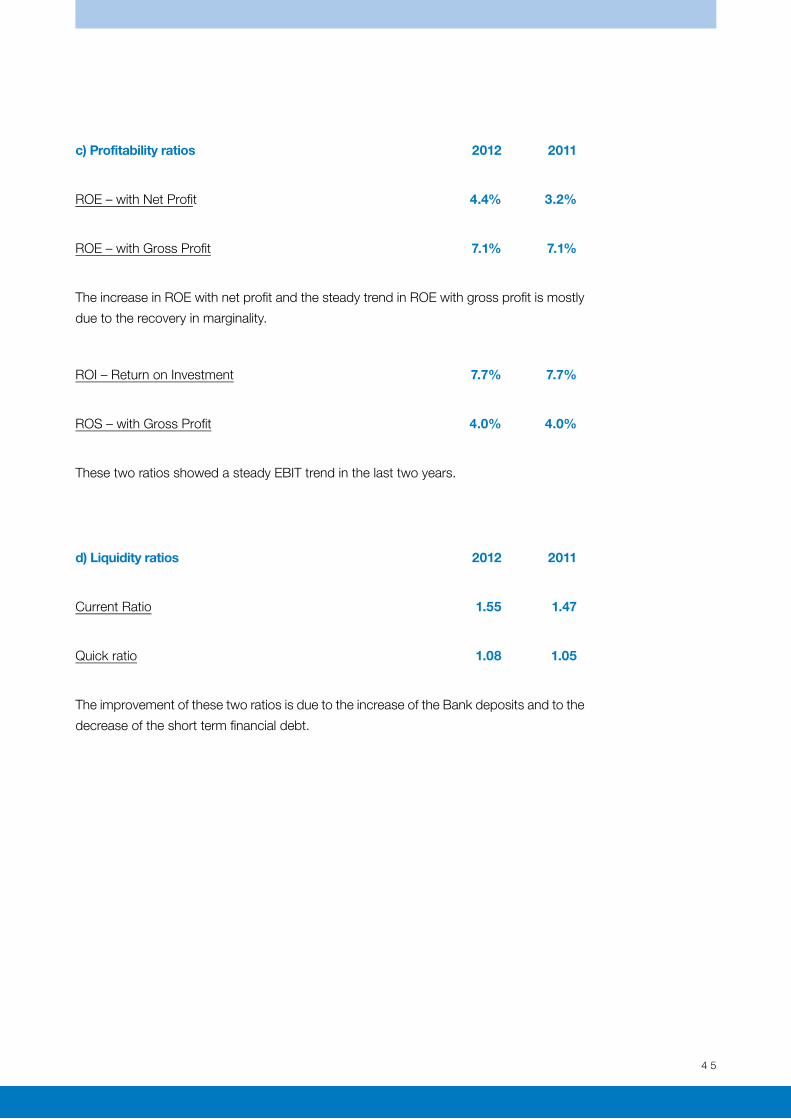

c) Profitability ratios 2012 2011

ROE – with Net Profit 4.4% 3.2%

ROE – with Gross Profit 7.1% 7.1%

The increase in ROE with net profit and the steady trend in ROE with gross profit is mostly

due to the recovery in marginality.

ROI – Return on Investment 7.7% 7.7%

ROS – with Gross Profit 4.0% 4.0%

These two ratios showed a steady EBIT trend in the last two years.

d) Liquidity ratios 2012 2011

Current Ratio 1.55 1.47

Quick ratio 1.08 1.05

The improvement of these two ratios is due to the increase of the Bank deposits and to the

decrease of the short term financial debt.

4 6

M A N A G E M E N T R E P O R T

Capital expenditureIn 2012, the Mapei Group capital expenditure has been approximately € 82.1 million and

is mainly related to manufacturing assets; please find here below the main investments by

macro-region.

Italy

• Mapei Spa invested € 15.7 million mainly related to a new land next to the production site

in Mediglia and to complete some plants in Mediglia and Latina sites.

• Investments of approximately € 7.0 million were made by Vinavil Spa, mostly referred to

the new Dynamon reactor, to the installation of the Rotoform machinery in Ravenna and

to the start-up of the new beads plant in Villadossola.

• Polyglass Spa had investments for an amount of € 1.1 million, mainly to complete the line

number four related to the bituminous membranes, after the fire of 2010.

• Minor investments were made by Cercol Spa (€ 0.6 million), Adesital Spa (€ 0.8 million)

and Vaga Srl (€ 0.7 million).

Western Europe

• Mapei France Sa invested € 10.2 million to complete the new production site in Lyon

area. Including this new site Mapei France has now three plants located in the areas of

Paris, Lyon and Toulouse.

• Mapei Gmbh (D) invested approximately € 2.3 million for the extension of the warehouse

in Weferlingen.

Eastern Europe

• Mapei Polska Spzoo made investments for € 7.8 million for the new production site in

Barcin Area and for the new admixtures plant in Gliwice.

• Investments for € 4.0 million in Gorka Cement Spzoo for the renewal and maintenance

of the plant in Trzebinia.

4 7

Americas

• Mapei Corp invested € 9.4 million, mainly related to a new land and a new building in New

Jersey. Moreover the Company made investments for a new land and building in West

Chicago in order to extend the current production site.

• In Mapei Inc € 9.2 million have been spent for the renewal and maintenance of the plant/

machinery/building in the production area of Toronto.

• The incorporation of Mapei Construction Chemicals Panama Sa on a line by line basis for

the first fiscal year showed tangible assets for a value equal to € 0.7 million.

Asia

• Mapei Malaysia Sdn Bhd invested approximately € 2.7 million in the new plant in Kuala

Lumpur area.

The decrease in fixed assets refers to the category Plants and Machinery, Industrial and

Commercial Equipment and Other Intangible Assets (cars, computers and office equipment

fallen into disuse) for € 7.1 million.

The impact of exchange rate is remarkable (€ 4.4 million) and it is attributable to the

revaluation of Polish Zloty and, with minor relevance, of Norwegian Crown, Hungarian

Florin and Russian Rouble.

4 8

M A N A G E M E N T R E P O R T

Research and developmentIn order to grow in the global market a Group has to be competitive. In order to be

competitive a Group has to invest in Research and Development. In order to invest in

an effective way a Group has to be connected to the leading industrial and scientific

research institutes and major universities around the world. This approach belongs to

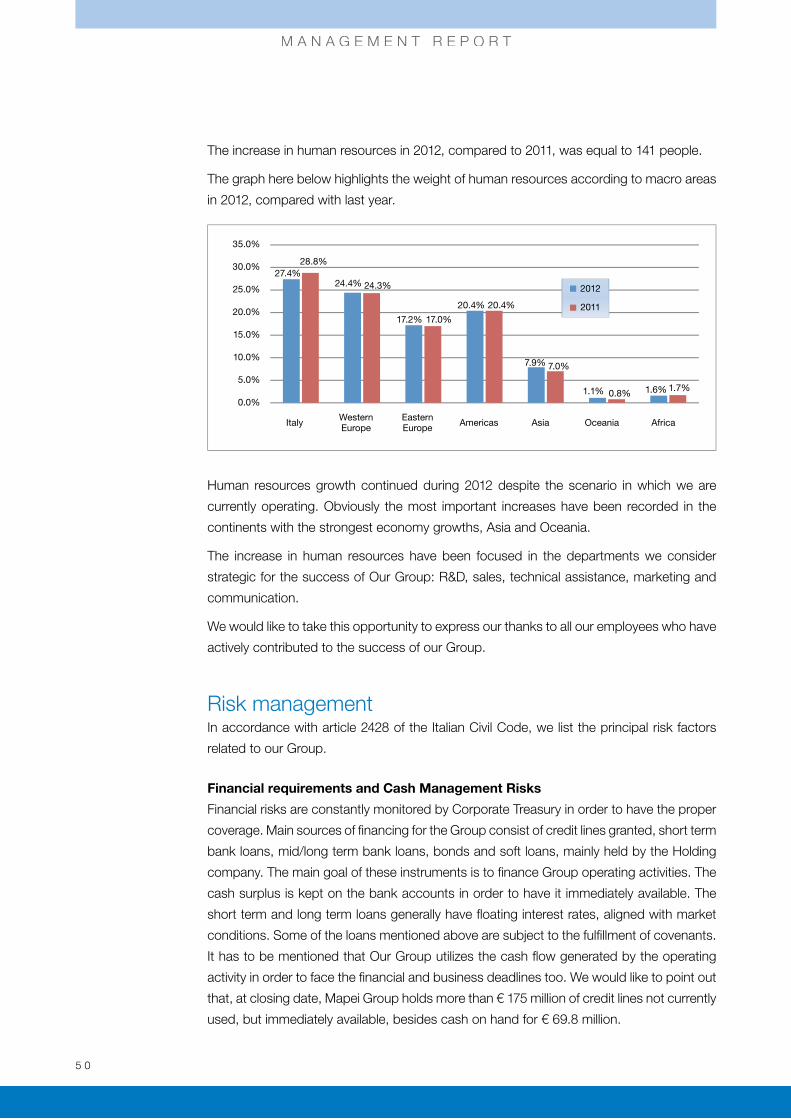

Mapei DNA.