Embed Size (px)

Citation preview

Confronting Tough Questions About Carriers of Last Resort

NARUC February 2008

Bob RoweSenior Partner

Balhoff, Rowe & Williams, LLC

Slide Slide 22

OverviewOverview

What is COLR? Examples of state policies Comparison to energy restructuring Traditional (relatively closed) model Disruptive (increasingly open) model –

making life and regulation interesting COLR issues in current High Cost Fund Framework for policy reform The COLR challenge About BR&W

What is COLR?

Slide Slide 44

What is COLR?What is COLR? Broadly – requirement to serve all

within a set geographic area.May be express or implicit from other

requirementsContrast with common carriage (non-

discrimination) Working financial definition

Network investment In specific regions that are costly to serveThat cannot support carrier services In exchange for support received

Examples of State Policies

Slide Slide 66

Typical state policiesTypical state policies May be express reference to “COLR” or may be

stated as specific requirements without mentioning “COLR”

Permission to begin service Permission to discontinue service Requirement to stand ready to serve Service quality requirements Offer specific services Rate setting Implicit supports

“Value based pricing” Vertical > basic Urban > rural LD > local Bus > res

Slide Slide 77

State Regulations OverviewState Regulations OverviewFrom 30,000 feetFrom 30,000 feet

State Express COLR Requirements? Technical COLR Requirements? Approval to discontinue?

Arkansas COLR obligations on all ETCs.Required to furnish “basic local exchange services”

Permits use of CMRS.“Single party service w/ no mileage/zone charges”“Safe, adequate, reliable”

Carrier may w/draw if at least 1 other ETC.PSC likely review discontinuation of service.

California ILECs = COLR in service territory until another carrier designated COLR.Monopoly provider obliged to provide service.

All LECs must offer defined “basic service”.Any alter. Tech. would likely have to satisfy all 17 “basic service” elements.

Carrier cannot w/draw a service w/out PUC approval.Can apply to w/draw; auction if no other provider willing to be COLR.

Illinois No express COLR obligation. Must provide “suitable facilities and services” LEC must get ICC approval before abandoning.

Indiana No express COLR requirement.IRUC indicates ETCs may have COLR-like obligation

“Reasonably adequate service & facilities”. Approval required to sell.Approval may not be necess. for partial w/drawal.

Kansas LECs have COLR obligation in their exchanges; shall “remain” COLRs.

KCC approval required to discontinue service.

Michigan No express COLR obligations; some precedent for required service.

Must provide “basic local exchange service”; “2-way interactive voice or data”.

LEC needs PSC auth. To discontinue service; can’t unless 1 or more alter. furnishing same service.

Missouri ILECs are COLRs for “essential telecommunications services”.

Must provide “essential telecommunications services” & “basic local exch. service”CMRS not a replacement.

PSC must approve abandonment or discontinuance.

Nevada Provision of basic service & intrastate interexchange toll services.

Must provide “basic service”. PUC approval to discontinue, modify or restrict service.

Ohio No express obligation; implied in ILEC territory on customer request.

All local service providers must offer “basic local exch. service”.

Must file a certif. to abandon, approved by PUCO pre-abandon.

Oklahoma LECs designated as COLRs; oblig. to build facilities to customers w/in ¼ mi. of existing facilities.

All LECs must meet min. service standards.Can’t regulate broadband.

Notice req’d to customers & OCC prior to curtail. or discontinuance.

Texas Must offer all basic local telecom service to ea. customer.Regardless of whether more than one certified provider in the area.

Must provide “basic telecommunications services”.

Prior approval from PUC to w/draw a tariffed service.

Wisconsin No express COLR rule. PSC defines set of “essential telecom services” for ETCs & can require advanced services.

File notice of discontinuance w/ PSC; approval required prior to withdrawal or discontinue of service.

Slide Slide 88

State InitiativesState Initiatives New York Competition III and follow-on Florida

Universal service “an evolving level of access . . . just, reasonable and affordable rates . . . including to rural, economically disadvantaged and high cost areas.”

Recognizes potential for erosion of revenue streams that contribute to universal service

Process for automatic and “good cause shown” waiver of COLR Generally concerns project developers

Texas Creation and subsequent review of state USF “Customers in all regions of this state, including low-income customers

and customers in rural and high-cost areas, [shall] have access to telecommunications and information . . . that are reasonably comparable to those services provided in urban areas and that are available at prices that are reasonably comparable to prices charged for similar services in urban areas.” PURA § 51.001(g).

Wisconsin Investigation into the Level of Regulation “Open a dialogue” concerning “guiding principles,” specific questions and relevant proposals.

Comparison to Energy Restructuring

Have we seen this movie before?

Slide Slide 1010

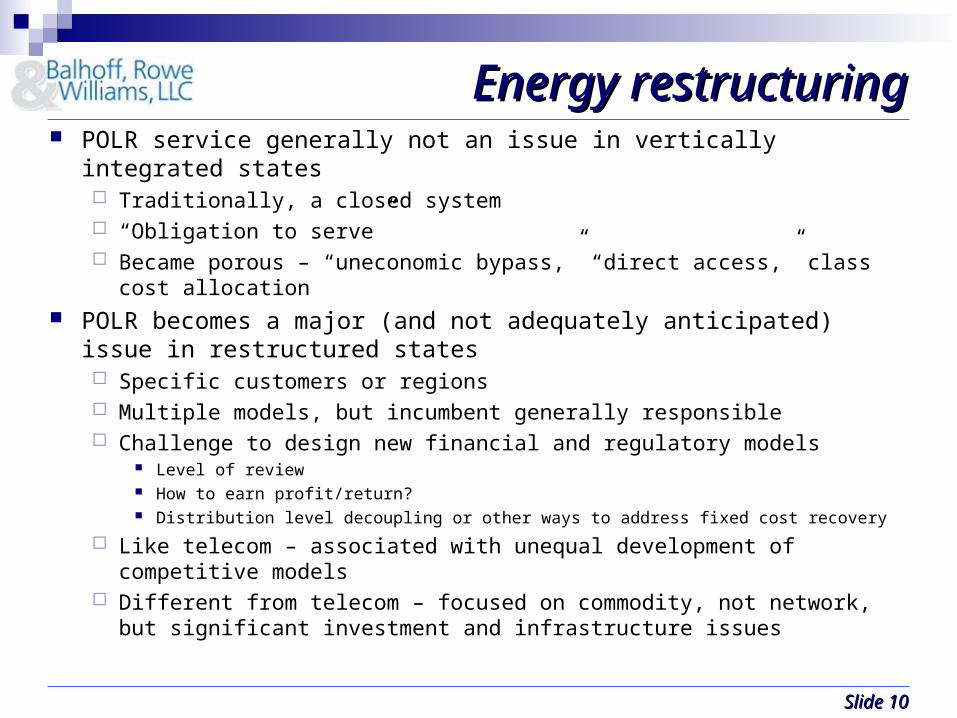

Energy restructuringEnergy restructuring POLR service generally not an issue in vertically integrated

states Traditionally, a closed system “Obligation to serve” Became porous – “uneconomic bypass,” “direct access,” class

cost allocation POLR becomes a major (and not adequately anticipated)

issue in restructured states Specific customers or regions Multiple models, but incumbent generally responsible Challenge to design new financial and regulatory models

Level of review How to earn profit/return? Distribution level decoupling or other ways to address fixed cost recovery

Like telecom – associated with unequal development of competitive models

Different from telecom – focused on commodity, not network, but significant investment and infrastructure issues

Traditional (Relatively Closed) Model

Slide Slide 1212

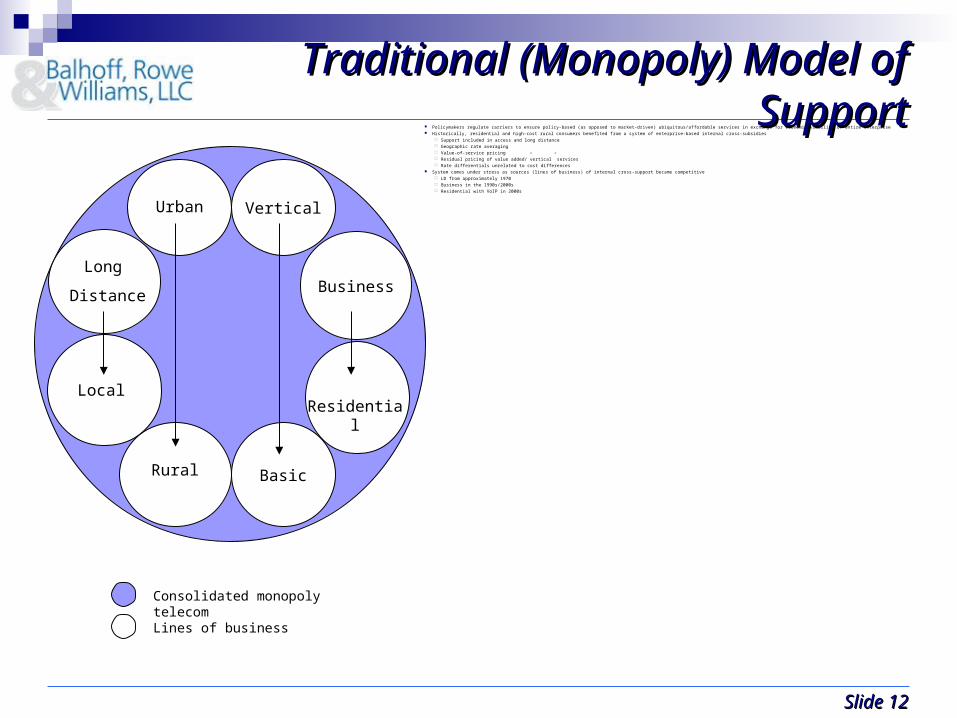

Traditional (Monopoly) Model of SupportTraditional (Monopoly) Model of Support Policymakers regulate carriers to ensure policy-based (as opposed to market-driven) ubiquitous/affordable services in exchange for economic viability of entire enterprise Historically, residential and high-cost rural consumers benefited from a system of enterprise-based internal cross-subsidies

Support included in access and long distance Geographic rate averaging Value-of-service pricing Residual pricing of value added/”vertical” services Rate differentials unrelated to cost differences

System comes under stress as sources (lines of business) of internal cross-support became competitive LD from approximately 1970 Business in the 1990s/2000s Residential with VoIP in 2000s

Long

Distance

Urban

Rural

Local

Business

Residential

Consolidated monopoly telecomLines of business

Vertical

Basic

Slide Slide 1313

Stages, Policy and Financial Perspectives Stages, Policy and Financial Perspectives on universal service goalson universal service goals

From Universal Service Funding, Balhoff, Rowe & Williams, LLC (2007)

Disruptive (Increasingly Open) Model

Slide Slide 1515

Competitive disruption and disparityCompetitive disruption and disparity

Disparate competition By customer type By geography

Disparate policy Obligations Regulation Jurisdiction

Disparate approaches among states CETC and ETC practices Reform of current obligations

Piecemeal or systematic

Slide Slide 1616

Rural Financial ProblemRural Financial ProblemFrom BR&W Texas StudyFrom BR&W Texas Study

Competitive line losses are concentrated in townships, not outside Companies/BR&W note findings are consistent with data in other

states BR&WR Texas study focused on cost patterns and competitive

activity Methodology involving financial data study based on . . .

“Supported services” only (revenues, costs, investment) Actual revenues received for provision of these services Forward-looking costs (12 kft loops – no costs for broadband-capable plant)

Data set Over 100 Texas wire centers Approximately 375,000 lines Approximately $250 million in revenue (including USF receipts) ~$850 million in gross loop investment (~$450 million net R1/B1 investment)

Analyzed financial characteristics/performance of wire centers in data set Segmented into ROI groups (negative, 0%-10%, >10%) Sub-wire center analyses of financial performance

Using geo-coded information, studied the geographic coverage of the cable operators (only in towns) & characteristics of service areas

NOTE: “Supported services” revenue streams included in analysis consist of Basic Area Local Revenue, End User Common Line (excluding USF surcharges), Carrier Common Line, Switched Access (including CALLS support), IntraLATA Toll, and High Cost USF where indicated. Costs and investment reflect what is required to provide R1/B1 services (including Loop, Transport & Switching), with returns calculated based on net investment (after accumulated depreciation).

Slide Slide 1717

Central Office Switch

Remote switches

Town Center vs. Outside of TownTown Center vs. Outside of Town Fundamental goal – better

understand challenges in serving rural customers based on sub-wire center financial & competitive factors

Studied “Town Center” regions, close enough to the CO (less than 12,000 feet) to be served directly, versus “Outside of Town” areas CO typically placed in population

centers Higher density, lower cost areas

Sub-wire center data are key to understanding . . . Economics of serving differing

geographic regions (in terms of density, costs, investment, etc.)

Why and where wireline competition is occurring, and where it is not

Role of explicit support mechanisms

Future pressures on mechanisms

Typical Wire Center Service Area

“Town Center”

Served directly by Central Office (CO)

switch“Outside of Town”

Distance from CO too great to be served

directly (more sparsely populated and longer

loops)

Slide Slide 1818

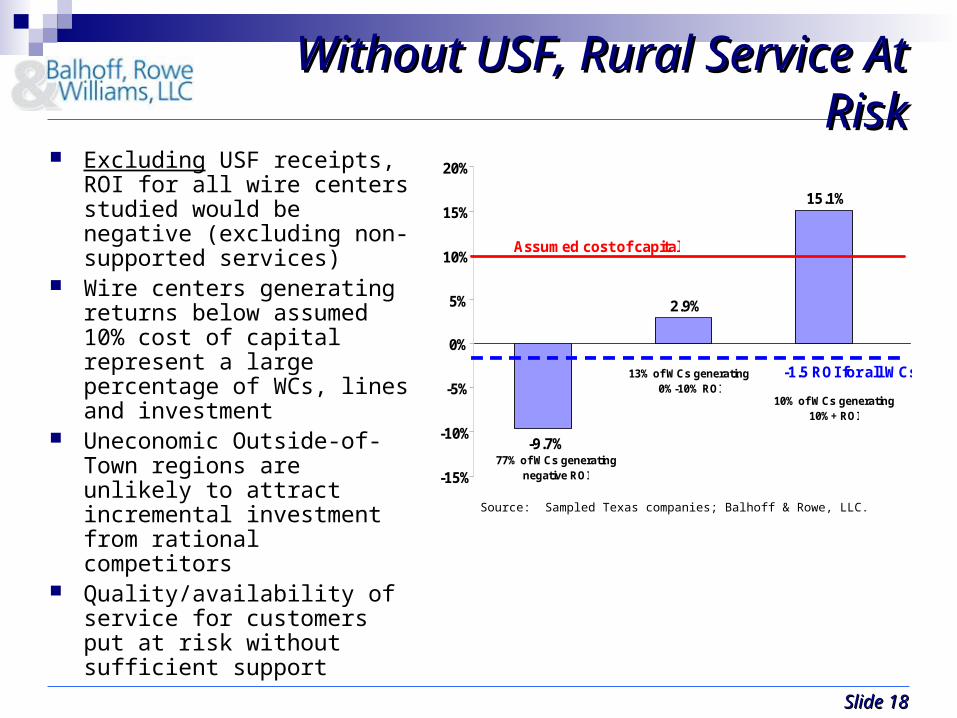

Without USF, Rural Service At RiskWithout USF, Rural Service At Risk Excluding USF receipts, ROI

for all wire centers studied would be negative (excluding non-supported services)

Wire centers generating returns below assumed10% cost of capital represent a large percentage of WCs, lines and investment

Uneconomic Outside-of-Town regions are unlikely to attract incremental investment from rational competitors

Quality/availability of service for customers put at risk without sufficient support

-1.5 ROI for all WCs

-9.7%

2.9%

15.1%

-15%

-10%

-5%

0%

5%

10%

15%

20%

77% of WCs generating negative ROI

13% of WCs generating 0%-10% ROI

10% of WCs generating 10%+ ROI

Assumed cost of capital

Source: Sampled Texas companies; Balhoff & Rowe, LLC.

Slide Slide 1919

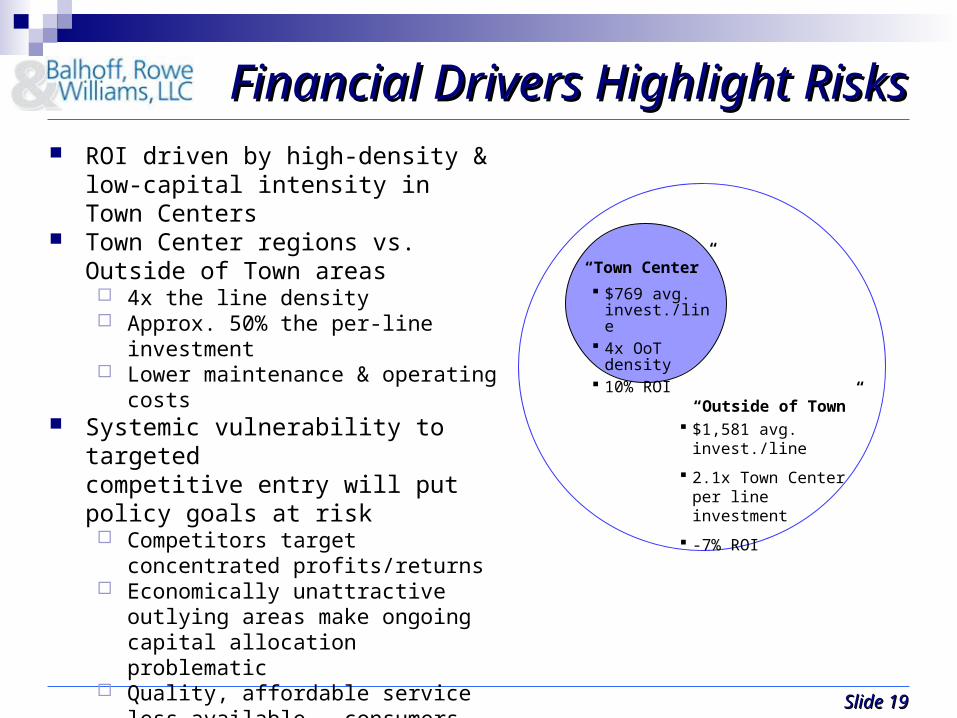

ROI driven by high-density & low-capital intensity in Town Centers

Town Center regions vs. Outside of Town areas 4x the line density Approx. 50% the per-line

investment Lower maintenance & operating

costs Systemic vulnerability to targeted

competitive entry will put policy goals at risk Competitors target concentrated

profits/returns Economically unattractive outlying

areas make ongoing capital allocation problematic

Quality, affordable service less available – consumers lose

$769 avg. invest./line

4x OoT density

10% ROI

“Outside of Town”

“Town Center”

$1,581 avg. invest./line

2.1x Town Center per line investment

-7% ROI

Financial Drivers Highlight RisksFinancial Drivers Highlight Risks

Slide Slide 2020

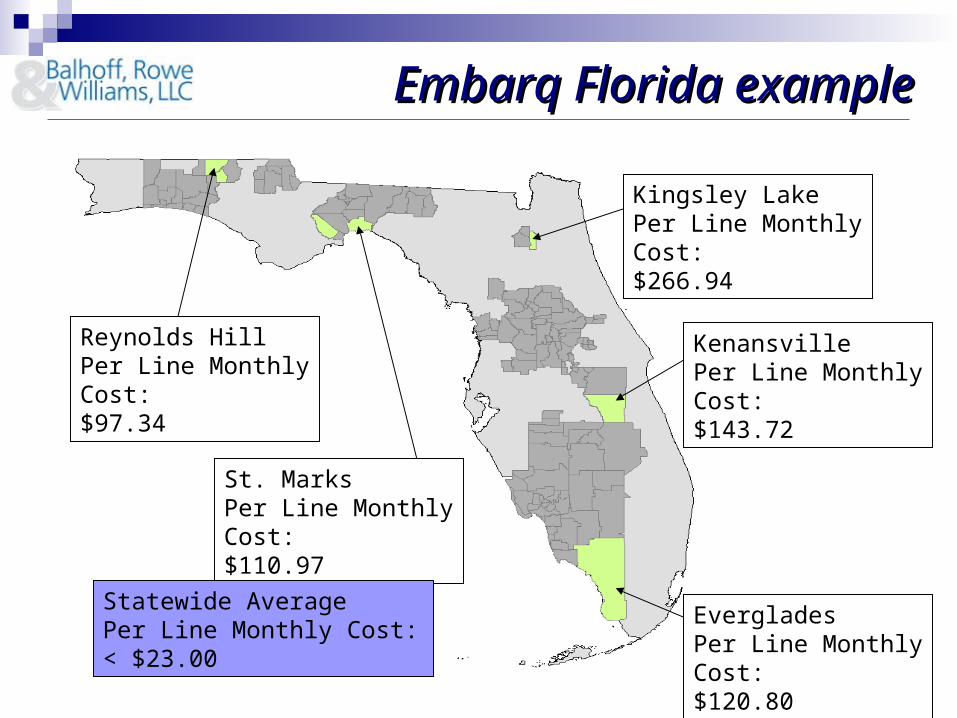

Reynolds HillPer Line Monthly Cost:$97.34

St. MarksPer Line Monthly Cost:$110.97

Kingsley LakePer Line Monthly Cost:$266.94

KenansvillePer Line Monthly Cost:$143.72

EvergladesPer Line Monthly Cost:$120.80

Statewide AveragePer Line Monthly Cost:< $23.00

Embarq Florida exampleEmbarq Florida example

Slide Slide 2121

Embarq Florida exampleEmbarq Florida example

Forward looking cost based on Hybrid Cost Proxy Model

1.77M lines in Florida Average Florida R1 rate is about $15

Price cap regulated Embarq receives no high cost loop or local

switching support in Florida. Embarq does receive about $17M a year in

CALLS money (access replacement).

COLR Issues in Current High Cost Fund

Slide Slide 2323

1996 Telecom Act1996 Telecom Act

Quality services at just, reasonable, and affordable rates

Access to advanced services in all regions

Reasonable comparability of rural and urban rates and services

Certification of ETCs and CETCs Subsequent growth of fund and shifts in

support patterns

Slide Slide 2424

Total USF is growingTotal USF is growingFederal Universal Service Fund Elements

1,697 1,7302,233 2,622 2,942 3,154 3,122 3,186 3,096

333639 1,083

464 480

519589

676716 763

804803

1,338

1,6921,524

1,7011,455 1,393

1,8621,924

1314720

1

811

21 24 24

2646

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

1998 1999 2000 2001 2002 2003 2004 2005 2006

Rural Health Care

Schools & Libraries

Low Income

CETCs

ILECs

High Cost Fund

$mils.

Source: USAC FCC filings: Balhoff & Rowe, LLC.

Policy/political problem with USF generally identified as persistent “growth”

Growth tied to other questions

Should multiple carriers receive funding?

What is the basis for funding?

Contribution problems—who should contribute and on what basis?

To understand and address the “growth problem” one must correctly identify sources of growth, and craft solutions that address those specific sources

One-time program changes, such as creation of Schools & Libraries (1999) Shift from intercarrier access payments to explicit support mechanisms (2000-

2002) Emphasis on support for wireless Competitive Eligible Telecommunications

Carriers (CETCs) (ongoing)

Slide Slide 2525

Composition of CETC funding growthComposition of CETC funding growth

Funds to CETCs exploding 96% CAGR 2002-2006 Approximately 61% growth

2005-2006 Access replacement is

approximately 46% of CETC total receipts in 2006 (composed of Interstate Common Line Support, Interstate Access Support &, pre-2005, Long-term Support) Wireless CETCs did not

receive access payments prior to reforms

CETC Annual Funding by Fund Element

$

$100

$200

$300

$400

$500

$600

$700

$800

$900

2001 2002 2003 2004 2005 2006

$m

illi

on

s

Access replacement

Other

Local switching support

High cost model

High Cost Loop

96% compound annual growth rate 2002-2006 (238% CAGR 2001-2002)

Source: Universal Service Administrative Company Quarterly appendices HC01 (only eligible and ETC-approved funding); Balhoff & Rowe, LLC.

Slide Slide 2626

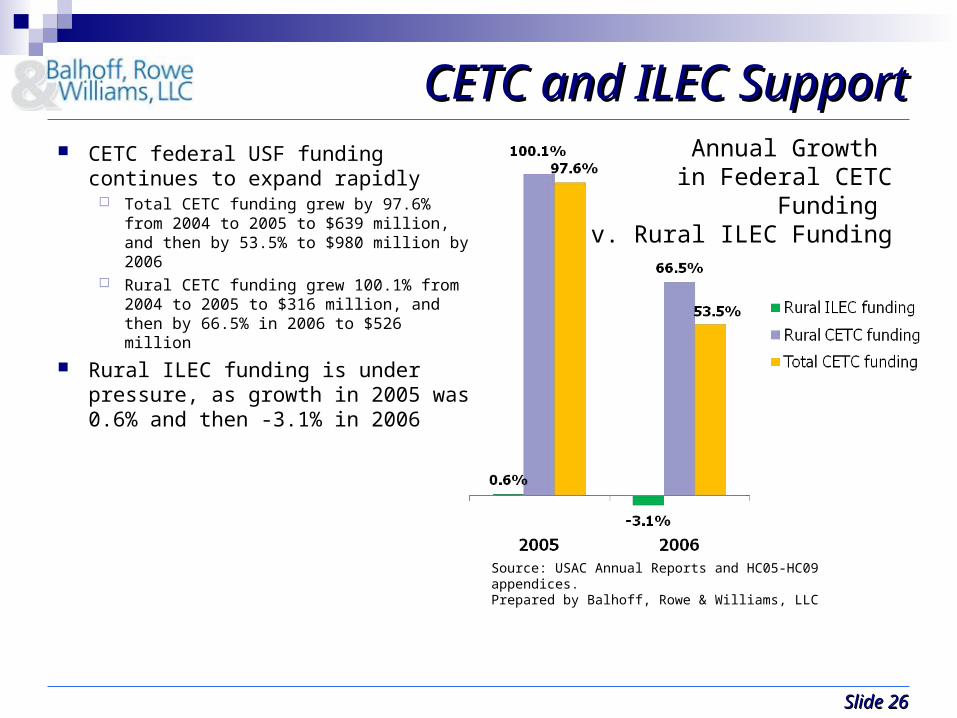

CETC and ILEC SupportCETC and ILEC Support CETC federal USF funding

continues to expand rapidly Total CETC funding grew by 97.6%

from 2004 to 2005 to $639 million, and then by 53.5% to $980 million by 2006

Rural CETC funding grew 100.1% from 2004 to 2005 to $316 million, and then by 66.5% in 2006 to $526 million

Rural ILEC funding is under pressure, as growth in 2005 was 0.6% and then -3.1% in 2006

Annual Growth in Federal CETC Funding

v. Rural ILEC Funding

Source: USAC Annual Reports and HC05-HC09 appendices.Prepared by Balhoff, Rowe & Williams, LLC

Slide Slide 2727

USF Contraction for Large RLECsUSF Contraction for Large RLECs

Largest rural carriers are reporting significant contraction in federal USF receipts

Among explanations . . . Increased efficiencies at rural companies Unanticipated effects of Rural Growth Factor as investment continues but the

number of access lines contract

Growth and Decline in Funding, December 20, 2007Growth and Decline in Funding, December 20, 2007

2004-2006 “Growth” In Large Rural

Company Federal USF Funding

Slide Slide 2828

Joint Board 11-20-07 RDJoint Board 11-20-07 RD POLR the core of current High Cost Fund program Move to separate broadband, mobility and POLR programs

within USF POLR recommendations

The Commission should focus on developing a unified POLR mechanism, rather than separate mechanisms dependent on the nature of the carrier.

As part of this, the FCC should address the transfer of exchange or “parent trap” rules.

The current mechanism recognizes loop costs, and to an extent switching costs, but not transport costs, which can be significant.

The mechanism may need to be modernized to account for factors such as targeted competition, competitive line losses, non-regulated revenues, and reduced support under the ILEC cap, despite costs that have remained relatively constant.

Slide Slide 2929

Joint Board 11-20-07 RDJoint Board 11-20-07 RD

“New entrants often compete only in densely populated areas that have relatively low costs. This makes it much more difficult for incumbent LECs to charge the same rates in both their low-cost densely populated areas and their higher cost, more remote areas. None of the existing support mechanisms adequately recognizes this phenomenon, which generally occurs on a smaller scale than the typical telephone exchange.”

Recommended Decision, Para. 22.

Slide Slide 3030

ImplementationImplementation Following Joint Board’s recommendation, in

context of FCC proceeding, stakeholders should Further develop facts Clarify goals Sharpen (realistic) expectations In order to

Provide investor clarity Better match support with costs Produce customer/community benefits

It is very doable for stakeholders from multiple perspectives to come together based on facts, in a structured process, to craft approaches that will allow all of them to invest in services for customers

Framework for Policy Reform

Slide Slide 3232

Competitive Paradigm ShiftCompetitive Paradigm Shift Explicit support mechanisms

intended to eliminate internal cross-subsidies Access systems Federal/state USF programs Access reforms

Competition targets most profitable business lines, eroding profitability & making cross-subsidies unsustainable LD market example

Lines of business must be economically justifiable (COLR) Allow competition to govern

competitive markets Uneconomic regions receive

increasingly explicit support Policy support matches policy

duties

Long Distance

Urban

Rural (incl. business)

Local

Business

Residential

Explicit Support (USF)

Balhoff, Rowe & Williams, USF Funding:Realities of Serving Telecom Customers in High Cost Regions (2007)

Slide Slide 3333

Reforms must be achievableReforms must be achievable Policy goals should be clearly stated Focus on solutions that are …

Based on accurate analysis & proper issue definition Adoptable (i.e. politically feasible) Achievable

Reasonably likely to result in desired goals Minimize risk of bad outcomes

Sustainable – remain effective as conditions change Consistent with the point at which reforms are commencing

Policy path dependency – “it’s costly & dangerous to switch from driving on the left side to driving on the right side”

Incorporate feedback mechanisms to adjust & improve based on time & experience

See, Barbara Cherry, “The Telecommunications Economy and Regulation as Coevolving Complex Adaptive Systems: Implications for Federalism” (delivered to TRP); Barbara Cherry and Johannes Bauer, “Adaptive Regulation: Contours of a Policy Model for the Internet Economy” (September 2004), presented at the International Telecommunications Society 15th Biennial Conference, Berlin Germany.

Slide Slide 3434

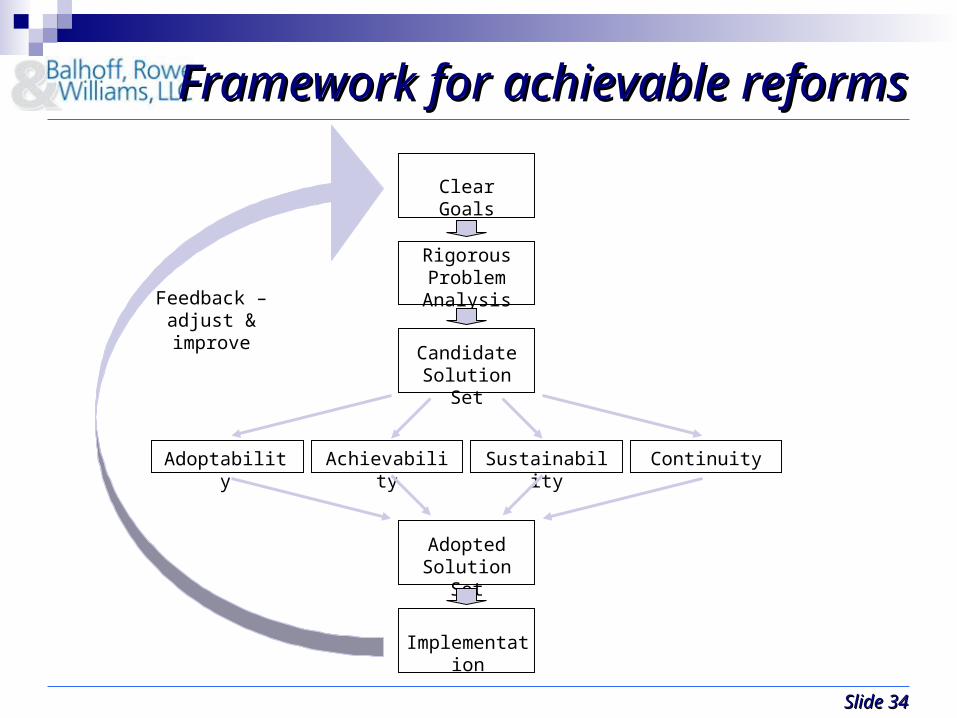

Framework for achievable reformsFramework for achievable reforms

Clear Goals

Rigorous Problem Analysis

Candidate Solution Set

Adoptability Achievability Sustainability Continuity

Adopted Solution Set

Implementation

Feedback – adjust & improve

Slide Slide 3535

HCF goalsHCF goals

Clear Goals

Rigorous Problem Analysis

Candidate Solution

Set

Adoptability Achievability

Sustainability

Continuity

Adopted Solution

Set

Implementation

Feedback – adjust & improve

Network focus Support investment to better serve customers

Customer focus Benefit from service availability & affordability Comparable services Limit exposure to harm from high risk “solutions”

Carrier of last resort Support service uneconomic to provide but required by policy goals

Broadband platform “No barriers to deployment” of advanced services (Rural Task Force)

The COLR Challenge

Slide Slide 3737

The ChallengeThe Challenge Work together to

Understand competitive and financial issues Address stresses on current model Sharpen focus on clearly-defined goals Develop clear, sustainable means to achieve them

Consider NARUC workgroup

Value in surveying current state practices and reform efforts

Ongoing financial analysis Broad state inquiries (e.g. new Wisconsin docket)

Slide Slide 3838

Questions to considerQuestions to consider

What are current express and implicit state policies?

What could or should COLR include? What are the costs associated with

providing COLR? How should those costs be covered in

current and future telecom markets? When and how should COLR be

modified or terminated?

Slide Slide 3939

The Last WordThe Last Word

“Competition is a reality today not only in our urban centers, but also increasingly in the small towns, villages and rural communities which are the population cores of rural areas across the country. It is essential that POLR support be matched as closely as possible to the high cost exurban (“truly rural”) areas. This requires adoption of improved analytical and modeling techniques to examine those costs at a far more granular level than has been heretofore been possible. Failure to align support with costs as closely as possible could put rural service at risk as surely as the unmanaged ballooning of the high cost program.”

Statement of Comm. Landis

About BR&W

Slide Slide 4141

PrincipalsPrincipalsMichael J. Balhoff, CFA, Managing Partner

Michael J. Balhoff, CFA, is managing partner at Balhoff, Rowe & Williams. Previously, Mr. Balhoff headed for 16 years the Telecommunications Equity Research Group at Legg Mason, which advised investors about equities in media, cable, wireless, telephony, communications equipment and regulation. Prior to joining Legg Mason in 1989, Mr. Balhoff taught at both the graduate and undergraduate levels. He has a doctorate in Canon Law and four master’s degrees, including an M.B.A., concentration in finance, from the University of Maryland. A Chartered Financial Analyst and a member of the Baltimore Security Analysts Society, Mr. Balhoff has been named on six occasions as a Wall Street Journal All-Star Analyst for his telecommunications recommendations. His coverage of telecom was named by Institutional Investor as the top telecommunications boutique in the country in 2003. He has also testified multiple times before congressional committees, is regularly a featured speaker at conferences for investors and policymakers, and is widely quoted in the media, including television, newspapers as well as communications and business journals.

Robert C. Rowe, Esq., Senior PartnerRobert C. Rowe, Esq., is a senior partner at Balhoff, Rowe & Williams. Previously, Mr. Rowe served as the Chairman of the Montana Public Service Commission which was responsible for regulating telecommunications, electricity, natural gas, water, and some transportation services. Mr. Rowe also served as President of the National Association of Regulatory Utility Commissioners, Chairman of the NARUC Telecommunications Committee, member and state chair of the Federal-State Joint Board on Universal Service, member of the Federal-State Joint Conference on Advanced Services, chairman of the thirteen state Operations Support Systems Collaborative working with Qwest and its competitors to achieve compliance with Section 271 of the 1996 Federal Telecommunications Act, and member of various advisory boards for university-affiliated programs.

Bradley P. Williams, Esq., PartnerBradley P. Williams joined the firm in 2005 and became a partner at Balhoff, Rowe & Williams in October, 2007. Previously, Mr. Williams was a member of the Strategic Planning & Business Development group at Lowe’s Companies Inc., the Fortune 50 home improvement retailer. Prior to joining Lowe’s, Mr. Williams worked with Mr. Balhoff in the award-winning Telecommunications Equity Research Group at Legg Mason, focusing on incumbent and rural local exchange carriers. Prior to joining Legg Mason, Mr. Williams was a co-founder of eSprocket / Beachfire, a venture-backed company that evolved into one of the pioneers in mediation technology solutions for the financial services sector. Previously, he served as a financial executive for Iron Road Railways Incorporated, a Washington, D.C.-based holding company that integrated, through acquisitions, a significant regional freight rail network serving northern New England and eastern Canada. Mr. Williams began his career as an investment banker in First Union’s Capital Markets Group. He has a BA in Economics from the University of North Carolina and a JD from the University of North Carolina School of Law.

Slide Slide 4242

Clients and ServicesClients and Services

Financial advisoryFairPoint and several other confidential discussions

MTA strategic acquisition

Facilitation and coordination of acquisition of NW

Investment analysis of wireless and wireline telecom

Advocacy/representationCongress (Phantom Traffic / USF for rural carriers

Senate Finance Committee concerning USF)

FCC (issues regarding access, USF, Phantom Traffic)

State commissions (acquisitions, rural exemptions, predatory pricing, financial strength, USF, etc.)

Consulting and analysisStrategic facilitation for CEOs/COOs of five carriers

Study of divestitures of rural properties

USF analysis for RBOCs; study of USF and access for rural telecom carriers

Study of municipal broadband

Representative assignments