Embed Size (px)

Citation preview

Accounting Analysis of Ameren Gas Rate Case Docket No. 13-0192

January 28, 2014

Mary Selvaggio, Accounting Department, Manager

Financial Analysis Division Public Utilities Bureau

Illinois Commerce Commission

1

Overview

• Accounting Controls – Compliance with Uniform System of Accounts (USOA) – Submission of Annual Reports

• Accounting Review of Rate Case – Required Utility Documentation – Test Year – Rate Base – Operating Expenses

• Determination of Revenue Requirement – Ameren Gas – Rate Zone III, Docket No. 13-0192

2

Accounting Controls: Compliance with Uniform Systems of Accounts (USOA)

• There is a specific USOA for each of the utility industries -- gas, electric, water, and sewer.

• Each USOA consists of definitions and instructions for each account.

Benefit: Uniformity of accounting records among public utilities.

• ICC adopts as its USOA for each industry a USOA

maintained by either the FERC (gas and electric) or NARUC (water and sewer). ICC modifies the national USOA to reflect Illinois regulatory policy and adopts it as part of its rules in the 83 Illinois Administrative Code.

• Available at http://www.icc.illinois.gov/publicutility/usoa.aspx

3

Accounting Controls: Submission of Annual Reports • The ICC prescribes the information to be submitted annually to the

Commission and to be available publicly pursuant to Section 5-109 of the Public Utilities Act.

– Form 21 ILCC – Gas and Electric at

http://www.icc.illinois.gov/forms/results.aspx?st=2&t=4 – Form 22 ILCC – Water and Sewer at

http://www.icc.illinois.gov/forms/results.aspx?st=9&t=19

4

Additional Accounting Controls

• Utility financial statements should be audited by an independent public accountant.

• Commission can order the submission of reports summarizing an internal audit of specific costs or programs performed by the utility’s internal audit staff.

• Commission can order the utility to hire an outside firm to conduct an audit of specific costs or programs.

• Commission can hire an outside firm to conduct an audit of specific costs or programs, supervise the audit, and require the utility to pay for the audit.

5

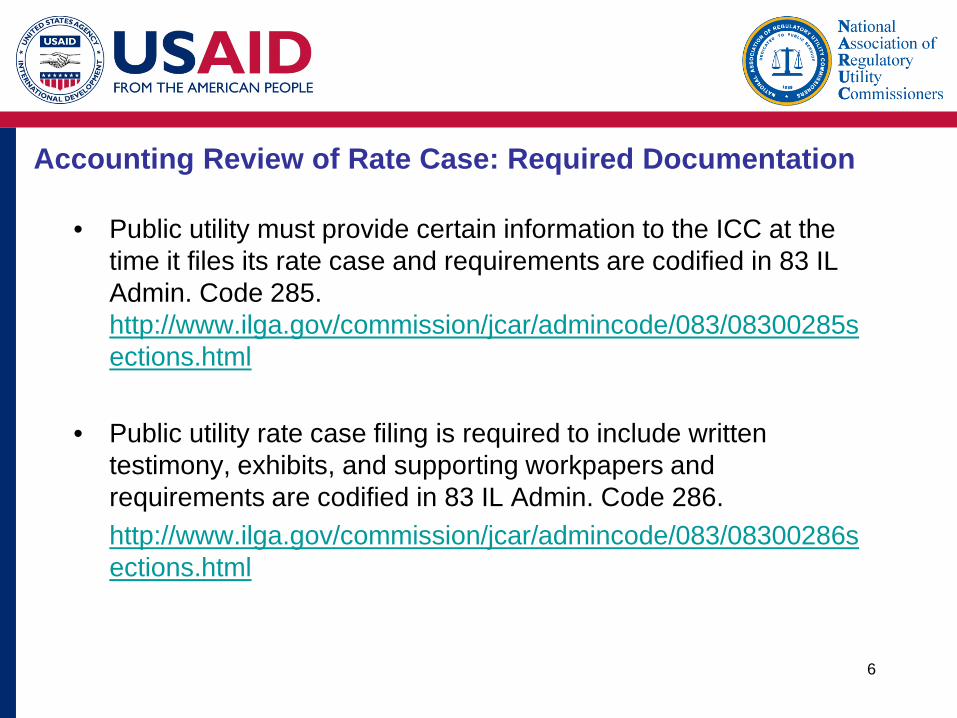

Accounting Review of Rate Case: Required Documentation

• Public utility must provide certain information to the ICC at the time it files its rate case and requirements are codified in 83 IL Admin. Code 285. http://www.ilga.gov/commission/jcar/admincode/083/08300285sections.html

• Public utility rate case filing is required to include written

testimony, exhibits, and supporting workpapers and requirements are codified in 83 IL Admin. Code 286.

http://www.ilga.gov/commission/jcar/admincode/083/08300286sections.html

6

Accounting Review of Rate Case

• The revenue requirement established in a rate case should reflect the just and reasonable costs of operating a public utility in a safe, adequate, and reliable manner. • Proper measurement of these two main components of the revenue requirement is an accounting function: – Rate Base – Operating Expenses

• Proper measurement begins with identification of a test year that reflects just and reasonable costs of operating a public utility.

7

Test Year

• Time period used for data underlying a requested rate increase. Purpose : To develop representative costs for the first year in which

rates being set will be in effect.

• The rules for a rate case test year are codified in 83 IL Admin. Code 287. http://www.ilga.gov/commission/jcar/admincode/083/08300287sections.html

• Two types of test year that an Illinois utility can select: 1. Historical Test Year

2. Future Test Year

8

Historical Test Year Any consecutive 12 month period, beginning no more than 24 months prior to the date of the utility's filing, for which actual data are available at the time of filing new tariffs. (83 Ill. Adm. 287.20(a)) Rate Case Filing on 1/25/13

• Historical Test Year could have been any consecutive 12 month period between 1/25/2011 & 1/24/2013 for which actual data would have been available on 1/25/2013. • The only calendar year that could have been used would have been 2012.

Allows pro forma adjustments to the historical data for known and measurable changes

9

Future Test Year Any consecutive 12 month period of forecasted data beginning no earlier than the date new tariffs are filed and ending no later than 24 months after the date new tariffs are filed. (83 Ill. Adm. Code 287.20(b)) Ameren Rate Case Filing on 1/25/13 was a Future Test Year ending December 31, 2014.

• Future Test year could have been any 12 month period between 1/25/2013 and 1/24/2015. • The only calendar year could have been 2014.

Anticipated changes are included in the test year.

10

11 11

Rate Base Accounting & others

Rate of Return Finance

Required Operating Income

X =

=

Expenses Accounting & others

+ Revenue Requirement

Customer Rates Rates Dept.

Rate Base reflects the net investment in the public utility on which utilities are allowed an opportunity to earn a fair rate of return.

Accounting Review of Rate Case: Rate Base

Accounting Review of Rate Case: Rate Base

Gross Utility Plant In Service Less: Accumulated Depreciation

= Net Plant Plus: (Working Capital) Cash Working Capital Materials & Supplies Inventory Less: (Cost-Free, Non-Investor Supplied Capital) Accumulated Deferred Income Taxes Customer Advances for Construction Customer Deposits Budget Payment Plan Balances

= Rate Base

12

• The following is how a utility’s rate base is typically calculated:

• This formula ensures the value of utility property on which a rate of return is allowed reflects only what was supplied by utility investors.

Accounting Review of Rate Case: Rate Base Critical Concepts

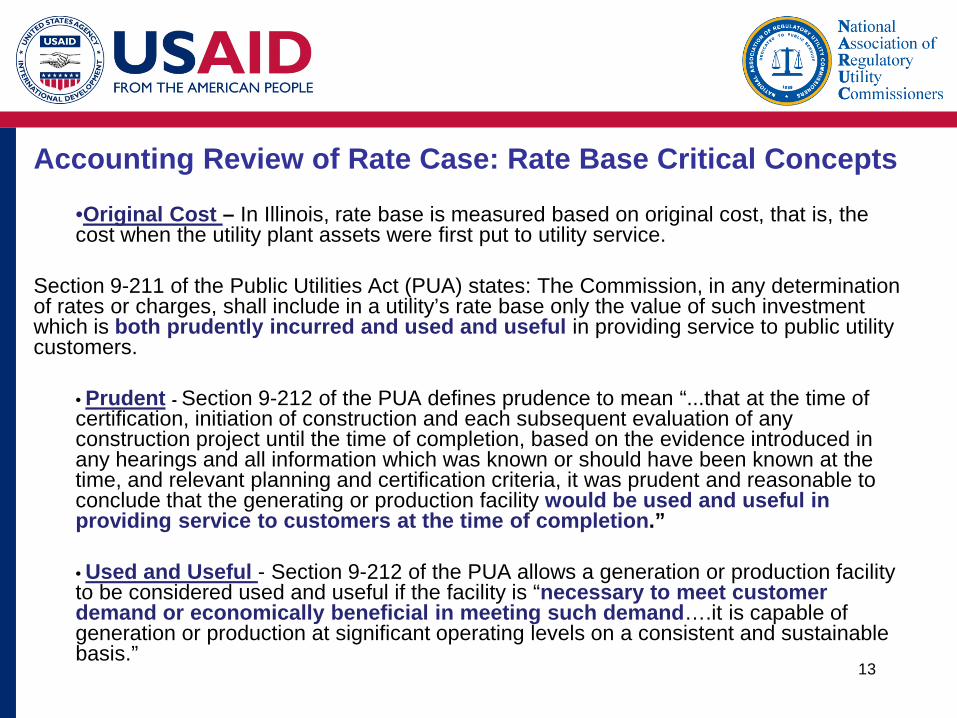

•Original Cost – In Illinois, rate base is measured based on original cost, that is, the cost when the utility plant assets were first put to utility service.

Section 9-211 of the Public Utilities Act (PUA) states: The Commission, in any determination of rates or charges, shall include in a utility’s rate base only the value of such investment which is both prudently incurred and used and useful in providing service to public utility customers.

• Prudent - Section 9-212 of the PUA defines prudence to mean “...that at the time of certification, initiation of construction and each subsequent evaluation of any construction project until the time of completion, based on the evidence introduced in any hearings and all information which was known or should have been known at the time, and relevant planning and certification criteria, it was prudent and reasonable to conclude that the generating or production facility would be used and useful in providing service to customers at the time of completion.”

• Used and Useful - Section 9-212 of the PUA allows a generation or production facility to be considered used and useful if the facility is “necessary to meet customer demand or economically beneficial in meeting such demand….it is capable of generation or production at significant operating levels on a consistent and sustainable basis.”

13

Rate Base Additions to Net Plant: Working Capital

In determining rate base, the following working capital items are added to utility plant investments (such as gas distribution mains, utility cars and trucks, utility office building, etc.):

• Materials and Supplies

Examples: Small tools, spare parts, nuts, bolts, screws, etc. that are not directly assignable to specific plant accounts.

• Cash Working Capital Amount needed to bridge the gap between the time expenditures are required to provide utility service and the time collections are received for such service. Determined through either of two methods: • Lead-lag Study - usually performed by larger companies. • Formula Method (calculated as1/8 of operating expenses which equals

approximately 45 days) – usually performed by smaller companies.

14

Rate Base Deductions to Net Plant: Cost-Free, Non-Investor Supplied Capital

• Deferred Income Taxes –A utility uses straight-line depreciation on its books and for ratemaking purposes. –A utility uses accelerated depreciation for income tax purposes. –Thus, the difference in income tax expense is Deferred Income Taxes. (A lower tax obligation results

in earlier years as taxes were deferred to later years.) –Deduction because it represents a cost-free “loan” from the IRS that is “paid back” over the life of the

asset as the tax-timing differences reverse.

• Customer Deposits –Paid by customers to a utility to initiate service and refunded at cessation of utility service. –Deduction because it represents funds furnished by customers.

• Customer Advances

–Paid to a utility to extend service from utility’s present facilities to new facilities (e.g., new subdivision). Includes new mains and service lines. These are refunded over time to the applicant for service.

– Deduction because it represents funds not provided by the utility.

• Budget Payment Plan Balances

The total of balances from the Budget Payment Plan. Utilities offer customers the option to pay a fixed amount each month regardless of the amount of the monthly utility bill. At the end of the budget payment plan period, the amount is trued-up. At any point in time, the total balance of all customers could be an overpayment or an underpayment. – Depending on whether the balance is positive or negative, this is a deduction or an addition.

15

Rate Base Measurement Period

16

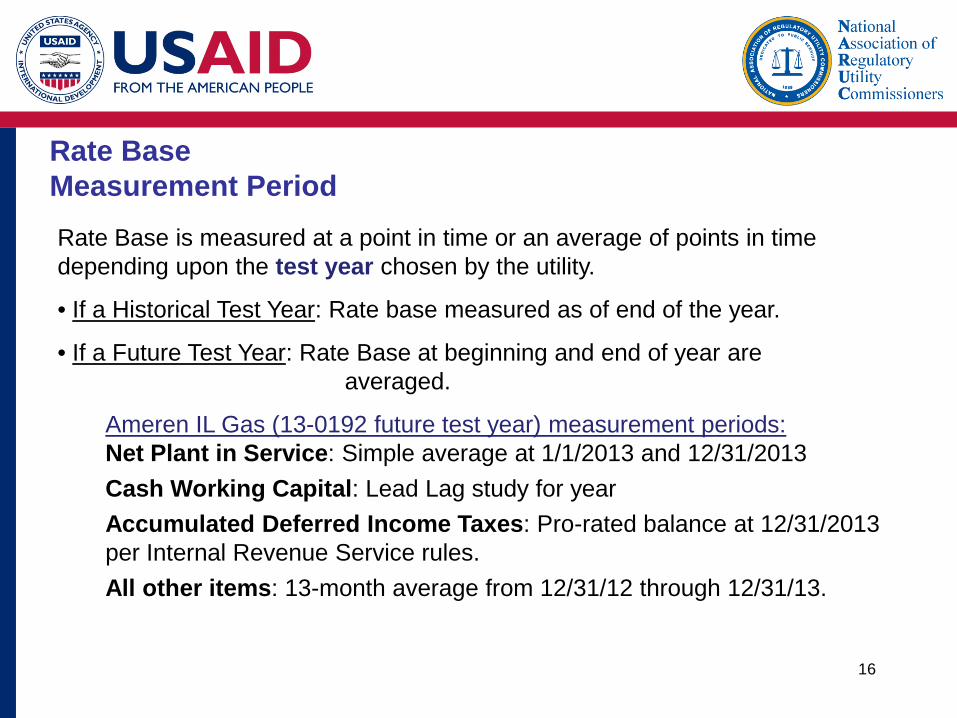

Rate Base is measured at a point in time or an average of points in time depending upon the test year chosen by the utility.

• If a Historical Test Year: Rate base measured as of end of the year.

• If a Future Test Year: Rate Base at beginning and end of year are averaged.

Ameren IL Gas (13-0192 future test year) measurement periods: Net Plant in Service: Simple average at 1/1/2013 and 12/31/2013 Cash Working Capital: Lead Lag study for year Accumulated Deferred Income Taxes: Pro-rated balance at 12/31/2013 per Internal Revenue Service rules. All other items: 13-month average from 12/31/12 through 12/31/13.

17

Accounting Review of Rate Case: Operating Expenses

Rate Base Accounting & others

Rate of Return Finance

Required Operating Income

X =

=

Expenses Accounting & others

+ Revenue Requirement

Customer Rates Rates Dept.

A utility’s Operating Expenses reflects the just and reasonable costs to operate and maintain the public utility so that it can provide safe, adequate and reliable service. It also includes taxes and annual depreciation costs.

Accounting Review of Rate Case: Operating Expenses • The utility’s “operating income statement” summarizes the financial results of its utility operations. It contains data used to determine the revenue requirement.

18

3 Operating Expense4 Purchased Gas 2,400 5 Operations and Maintenance 900 6 Depreciation and Amortization 450 7 Income Taxes 200 8 Revenue Taxes 30 9 Other Taxes 20 10 Total Operating Expenses 4,000 1112 Operating Income (Line 1 minus 10) $1,8001314 Total Other Income (Deductions) 10015 Interest Expense 25016 Dividends Paid on Preferred Stock 1201718 Net Income Available for Common Stock $1,330

The “line”

• Only revenues and expenses recorded “Above the Line” are used in calculating the revenue requirement.

Accounting Review of Rate Case: Operating Expenses Regulatory Accounting Adjustments

The ICC adjusts the utility’s operating expenses to reflect Illinois regulatory policy as determined by any of the following:

• State law • State rules (83 Illinois Administrative Code) • Prior Commission Orders • Commission practice

Examples • Disallowance of political and lobbying expenses (Section 9-224) • Disallowance of promotional advertising (Section 9-225)

19

To determine the costs that are representative of what the utility will incur in the year after rates are set, adjustments some times need to be made to the operating expenses:

• Normalization Adjustments -Smoothes the impact of unusual levels of revenues or expense. -Essentially restates specific test year data to reflect normal conditions. Example: Abnormal level of chemical expense appears in the test year. Restate expense as an average of an appropriately determined prior number of years.

• Out-of-Period Adjustments -An adjustment for an expense occurring outside the test year. Example: There are 13-months of lease expense included in the test year. Allow only 12 months of expense in the test year.

• Known and Measurable” Adjustments – Applies only to historical test years. If a known & measurable change occurs during or after the historical test year, the impact of the change may be reflected as if the change had been in effect for the entire test year. Example: Wage increase occurred during the test year: annualize the increase so it applies to the whole test year. Wage increase occurred after the test year: restate wage expense as if the wage increase had been effect for the whole test year.

20

Accounting Review of Rate Case: Operating Expenses

Examples of Adjustments to Ameren IL Gas Operating Expenses Docket No. 13-0192

• Bad Debts Expense: Based on three-year average of net write-offs. • Salaries Expense: Removed salaries of employees responsible for lobbying. • Industry Dues: Removed that which was unrelated to the provision of gas service or

was related to lobbying efforts. • Pension Expense: Revised to reflect an actuarial valuation as of 12/31/2012. • Charitable Contributions: Commission adopted a 3-year average escalated by 2%

inflation for 2013 and 2014. • Increase in Non-Union Wages: Commission adjustment reflect increase in non-union

wages based on the most recent actual data available in 2013 rather than a forecast. • Advertising: Commission adopted a 4-year average adjusted by inflation. • Miscellaneous Costs Charged on Company Credit Card (Flowers, Snacks,

Decorations, New Employee Gifts, Flat Screen TVs, etc.): Removed as charges are excessive and inappropriate for recovery. ICC recommended Ameren institute reasonable controls over credit card use.

21

Determination of Revenue Requirement

• Every Commission Rate Order contains a detailed appendix that shows the approved revenue requirement per the Order.

• The appendix shows the amounts requested and the adjustments (increases or decreases) ordered by the Commission to rate base and the operating expense items. Example: 13-0192 Ameren gas rate case Order

22

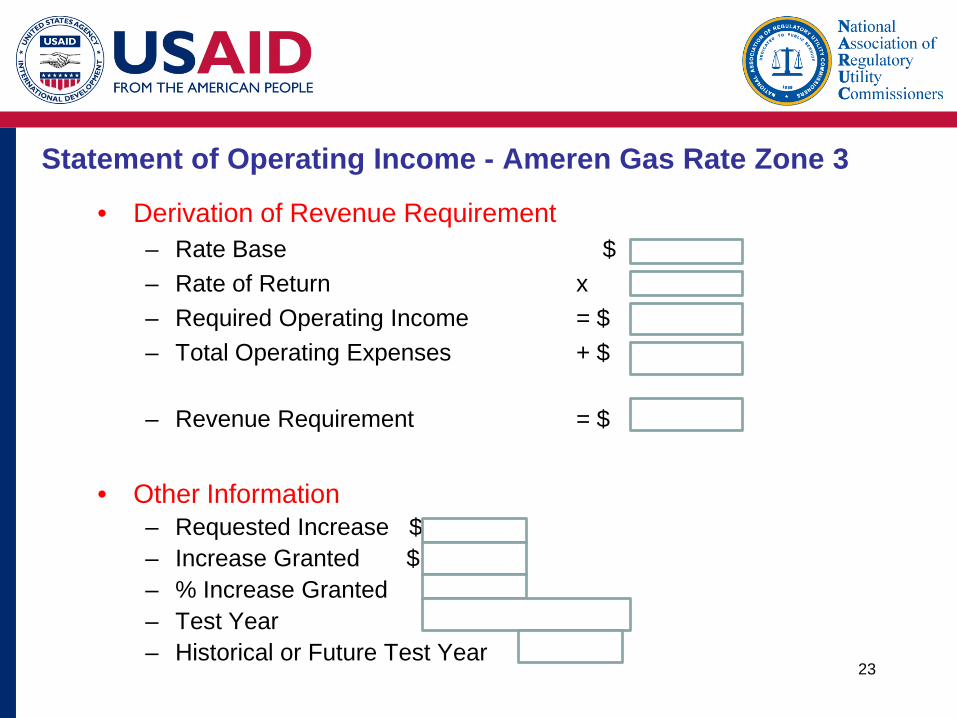

Statement of Operating Income - Ameren Gas Rate Zone 3

• Derivation of Revenue Requirement – Rate Base $ 564,128 – Rate of Return x 7.75% – Required Operating Income = $ 43,739 – Total Operating Expenses + $ 140,029

– Revenue Requirement = $ 183,768

• Other Information – Requested Increase $ 20,021 – Increase Granted $ 11,453 – % Increase Granted 6.64% – Test Year Forecasted 2014 – Historical or Future Test Year Future

23

Costs Not Recovered Through Base Rates (Distribution)

• Utilities have various automatic adjustment clauses (“Riders”) approved by the Commission to provide automatic and full recovery of specific costs without the need of filing for a rate case. Example: Purchased Gas Adjustment Clause provides

distribution utility full recovery of gas commodity costs. • Controls

– Regular utility filings to ICC that provide support for any changes in the rate charged through a rider.

– Annual reconciliation proceedings for riders to ensure any over-collections or under-collections are refunded or charged to ratepayers, respectively.

24