Embed Size (px)

Citation preview

PS4-3.1

CONCEPT AND TECHNIQUES FOR GRASSROOTSLNG PLANT COST OPTIMIZATION

LA CONCEPCION ET LES TECHNIQUES POUR L’OPTIMISATIONDES COUTS DANS LES USINES DE GNL

Yoga P. SupraptoEngineering Manager -Tangguh LNG Project

PERTAMINA

ABSTRACT

• How Grassroots LNG Plant Can Compete With Expansion Project Cost

• Screening of LNG Liquefaction Process Technology

• Contract Management of Front End Engineering Work for Multiple TechnologyCompetition

• Case Discussion for Tangguh LNG Project

As the Asia Pacific LNG market experiences a sluggish demand in the last 5 years,the competition to find a niche market between LNG projects are getting tighter andtighter. The new grassroots LNG projects are facing their biggest challenge for survivalunless they can compete head to head with the expansion project, something that is noteasily achieved due to the significant difference in the project scope.

The changing supply demand balance of the Asia Pacific LNG forced the LNGproducer revisited the basic concept the way a LNG project is being developed. Thispaper describes and analyzes the critical change drivers of the business in order toappropriately address the best strategy to compete.

In the next section, this paper discuss how to put the cost optimization merits to worksin the real world in a grassroots LNG project, which include the implementation ofMultiple technology Front End Engineering Design competition.

Further discussion focus on the implementation of Multiple FEED execution,technology screening, and risk management and project coordination. Then, a detaileddiscussion on the execution procedures follows, how a Multiple FEED procedures andevaluation criteria should be properly designed to maintain fair and equal competitionbetween FEED Contractors. As an example, the Tangguh LNG project Multiple FEEDexecution is used as the basis of case discussion.

A grassroots LNG project does have some inherent cost optimization merits, which anexpansion project does not always have. This paper analyzes the project cost factors andidentifies which are the cost optimization merits for a grassroots LNG project.

RESUME

• Comment une unite de GNL “grassroots” peut elle etre competitive avec un projetd’extension.

• Revue des technologies de procedes de liquefaction de GNL.

PS4-3.2

• Comment specifier des conceptions competitives, niveau de detail et criteresd’evaluation des offres pour optimiser le cout du projet.

• Discussion sur le projet GNL Tangguh.

A un moment ou le marche du GNL en Asie-Pacifique fait face y une demandelethargique depuis cinq ans, la competition pour trouver une niche de marche entre lesprojets de GNL est de plus en plus serree. Les nouveaux projets “grassroot” de GNL fontface y leur plus grand defi pour survivre, excepte s’ils peuvent etre competitifs avec lesprojets d’extension, ce n’est pas facile y realiser compte tenu de la difference significativedes cahiers des charges.

Le changement de la balance de la production et de la demande de GNL en Asie-Pacifique force les producteurs de GNL au revoir le concept de base et la maniere dont leprojet de GNL est developpe. Ce papier decrit et analyse les moteurs de changementcritique de l‘industrie pour adresser correctement la meilleure strategie pour etrecompetitif.

La section suivante de ce papier discute les merites d’optimisation des couts d’unprojet de GNL en “grassroot”, qui inclut la mise en ouvre d’etudes preliminaires quimettent en compétition plusieurs technologies et conceptions. (Multiple technology FrontEnd Engineering Design competition).

La suite de la discussion vise la realisation de plusieurs etudes preliminaires(Multiple FEED), comparaison technologique, analyse des risques et coordination duprojet. En suite il y aura une discussion sur les procedures d’execution, dans le cas d’un“Mutiple FEED”, quelles procedures et criteres d’evaluation doivent etre elabores pourmaintenir une juste et egale competition entre les contracteurs pour un “FEED”. Commeexemple de “Mutiple FEED execution” le projet de GNL Tangguh est utilise comme basede discussion.

Un projet de GNL “grassroot” contient des zones d’optimisation de cout qu’un projetd’extension n’a pas toujours. Ce papier analyse les facteurs de cout du projet et identifieles avantages d’optimisation des couts d’un projet de GNL “grassroot”.

PS4-3.3

CONCEPT AND TECHNIQUES FOR GRASSROOTSLNG PLANT COST OPTIMIZATION

INTRODUCTION

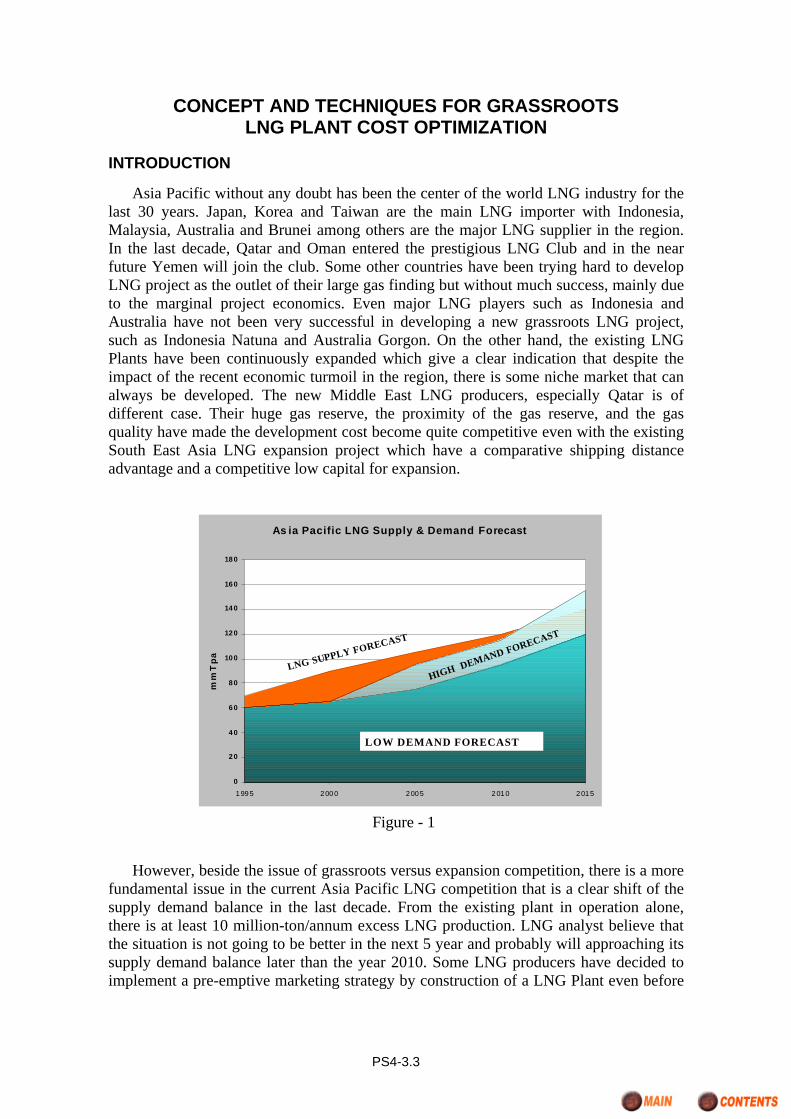

Asia Pacific without any doubt has been the center of the world LNG industry for thelast 30 years. Japan, Korea and Taiwan are the main LNG importer with Indonesia,Malaysia, Australia and Brunei among others are the major LNG supplier in the region.In the last decade, Qatar and Oman entered the prestigious LNG Club and in the nearfuture Yemen will join the club. Some other countries have been trying hard to developLNG project as the outlet of their large gas finding but without much success, mainly dueto the marginal project economics. Even major LNG players such as Indonesia andAustralia have not been very successful in developing a new grassroots LNG project,such as Indonesia Natuna and Australia Gorgon. On the other hand, the existing LNGPlants have been continuously expanded which give a clear indication that despite theimpact of the recent economic turmoil in the region, there is some niche market that canalways be developed. The new Middle East LNG producers, especially Qatar is ofdifferent case. Their huge gas reserve, the proximity of the gas reserve, and the gasquality have made the development cost become quite competitive even with the existingSouth East Asia LNG expansion project which have a comparative shipping distanceadvantage and a competitive low capital for expansion.

However, beside the issue of grassroots versus expansion competition, there is a morefundamental issue in the current Asia Pacific LNG competition that is a clear shift of thesupply demand balance in the last decade. From the existing plant in operation alone,there is at least 10 million-ton/annum excess LNG production. LNG analyst believe thatthe situation is not going to be better in the next 5 year and probably will approaching itssupply demand balance later than the year 2010. Some LNG producers have decided toimplement a pre-emptive marketing strategy by construction of a LNG Plant even before

As ia Pacific LNG Supply & Demand Forecast

0

20

40

60

80

100

120

140

160

180

1995 2000 2005 2010 2015

mm

Tp

a

LOW DEMAND FORECAST

HIGH DEMAND FORECAST

LNG SUPPLY FORECAST

Figure - 1

PS4-3.4

all of the design capacity is committed. A new project financing strategy is required forthis kind of marketing scheme.

The fierce competition between LNG producing countries, or between projects in aproducing country, have forced Seller and the Buyer parties constantly revisited the termand condition of a LNG Sales Agreement. A shorter LNG commitment is not a new issueanymore, and some LNG producers offer a full business chain development up to thepower plant gate. China and India enter the LNG importer club at this favorable time forLNG Buyers, with additional advantage of not being severely impacted by the Asianeconomic crisis. While Indian LNG market is more or less confined to the Middle EastLNG producers, China LNG market is more open for competition.

Notwithstanding with the importance of competitive LNG Sales contract terms andcomparative advantage of shipping distance, the question that is very intriguing to beexplored is: why some LNG producing countries still pursuing a grassroots LNG projectfor a market before the year 2010? Will a 1-train grassroots LNG plant be competitivewith an expansion project? How to manage the project cost competition while satisfyingBuyer and Project Financier investment risk. The Indonesia’s Tangguh LNG Project willbe used as a case study for this discussion of optimization of grassroots LNG Plant cost.

It is worth to note that the whatever strategy a LNG producer is taking, the finalobjective of a LNG project is to secure LNG Sales Agreement and the Project FinancingAgreement therefore LNG Buyers and Project Financier interest and concern mustbecome the underlying framework in every strategy discussion.

CHANGE DRIVERS OF ASIA-PACIFIC LNG INDUSTRY

No LNG project are alike, uniqueness of each business chain contribute to a complexfactors of a LNG Project cost structure. Benchmarking of LNG Project Cost must be donecautiously and sometime has misled Project Owner or their Audit Team. However, at theend of the day what really matters to the LNG Buyer and Project Financier is the Cost ofService of the LNG as received by the Buyers at their gate or unloading flange. The costof service gives a simplified indication of LNG Project strength to return a capitalinvestment. Low cost of service is a warranty that a project is not only economicallyattractive but also more importantly it will make the project more resilient to anyfluctuation in any of the economics parameter. A very important issue for a long term‘take or pay’ LNG Sales Contract. However, higher cost of service does not necessarilymeans the LNG Buyers or Project Financiers will not select that particular LNG project.If the LNG producer is willing to absorb or share the impact of economics fluctuationfrom their revenue then a LNG project with higher cost of service may still bematerialized.

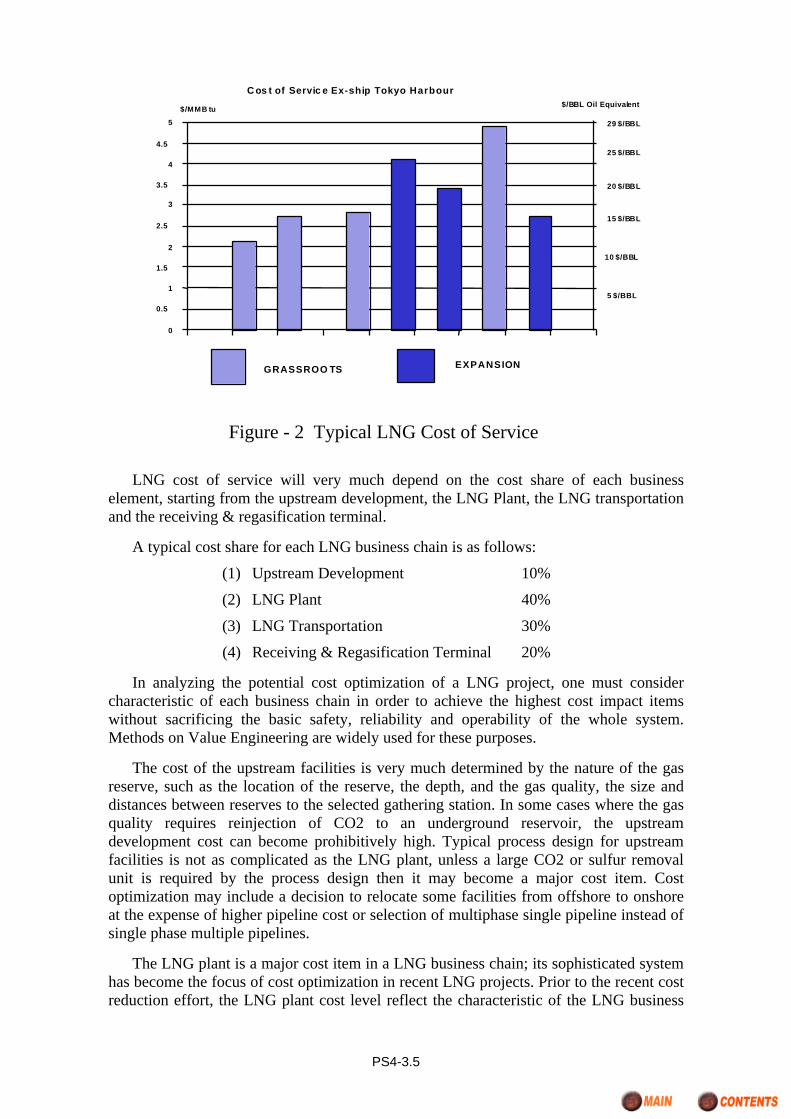

The graph below showed a typical variation of cost of service of LNG in the AsiaPacific region.

PS4-3.5

LNG cost of service will very much depend on the cost share of each businesselement, starting from the upstream development, the LNG Plant, the LNG transportationand the receiving & regasification terminal.

A typical cost share for each LNG business chain is as follows:

(1) Upstream Development 10%

(2) LNG Plant 40%

(3) LNG Transportation 30%

(4) Receiving & Regasification Terminal 20%

In analyzing the potential cost optimization of a LNG project, one must considercharacteristic of each business chain in order to achieve the highest cost impact itemswithout sacrificing the basic safety, reliability and operability of the whole system.Methods on Value Engineering are widely used for these purposes.

The cost of the upstream facilities is very much determined by the nature of the gasreserve, such as the location of the reserve, the depth, and the gas quality, the size anddistances between reserves to the selected gathering station. In some cases where the gasquality requires reinjection of CO2 to an underground reservoir, the upstreamdevelopment cost can become prohibitively high. Typical process design for upstreamfacilities is not as complicated as the LNG plant, unless a large CO2 or sulfur removalunit is required by the process design then it may become a major cost item. Costoptimization may include a decision to relocate some facilities from offshore to onshoreat the expense of higher pipeline cost or selection of multiphase single pipeline instead ofsingle phase multiple pipelines.

The LNG plant is a major cost item in a LNG business chain; its sophisticated systemhas become the focus of cost optimization in recent LNG projects. Prior to the recent costreduction effort, the LNG plant cost level reflect the characteristic of the LNG business

C os t of Servic e Ex-ship Tokyo Harbour

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

5

$/MMB tu$/BBL Oil Equivalent

29 $/BBL

25 $/BBL

20 $/BBL

15 $/BBL

10 $/BBL

5 $/BBL

GRASSROO TS EXPANSION

Figure - 2 Typical LNG Cost of Service

PS4-3.6

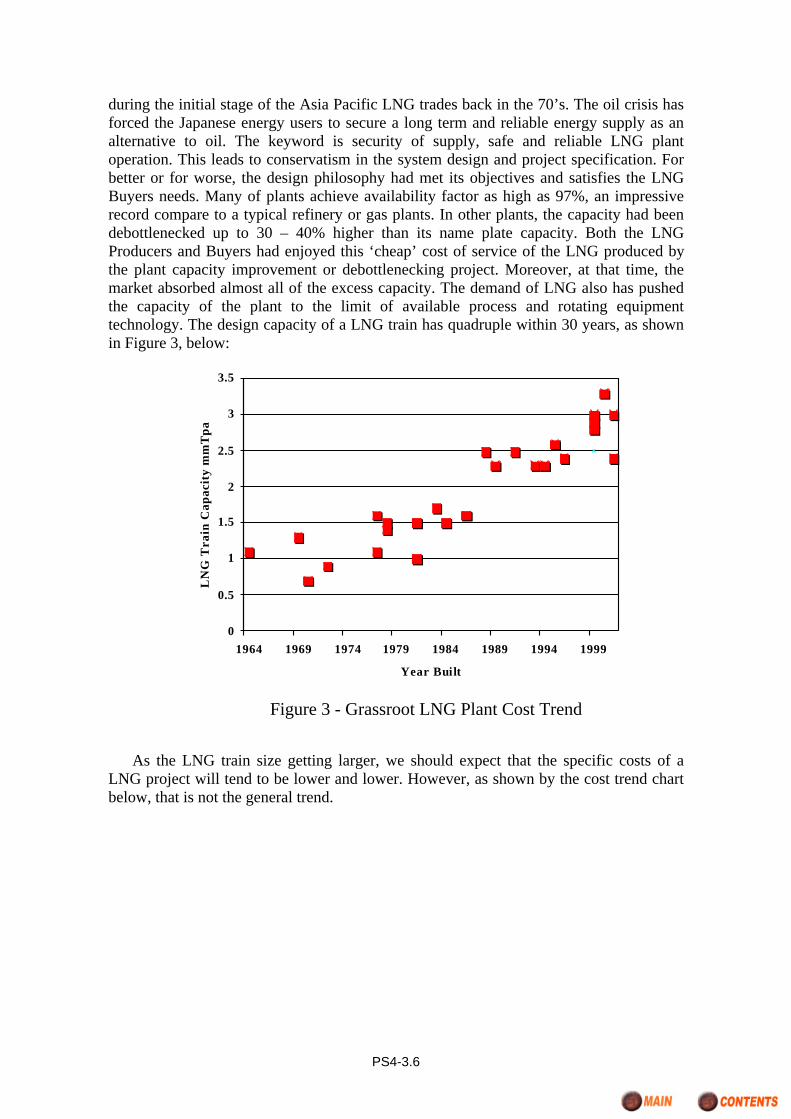

during the initial stage of the Asia Pacific LNG trades back in the 70’s. The oil crisis hasforced the Japanese energy users to secure a long term and reliable energy supply as analternative to oil. The keyword is security of supply, safe and reliable LNG plantoperation. This leads to conservatism in the system design and project specification. Forbetter or for worse, the design philosophy had met its objectives and satisfies the LNGBuyers needs. Many of plants achieve availability factor as high as 97%, an impressiverecord compare to a typical refinery or gas plants. In other plants, the capacity had beendebottlenecked up to 30 – 40% higher than its name plate capacity. Both the LNGProducers and Buyers had enjoyed this ‘cheap’ cost of service of the LNG produced bythe plant capacity improvement or debottlenecking project. Moreover, at that time, themarket absorbed almost all of the excess capacity. The demand of LNG also has pushedthe capacity of the plant to the limit of available process and rotating equipmenttechnology. The design capacity of a LNG train has quadruple within 30 years, as shownin Figure 3, below:

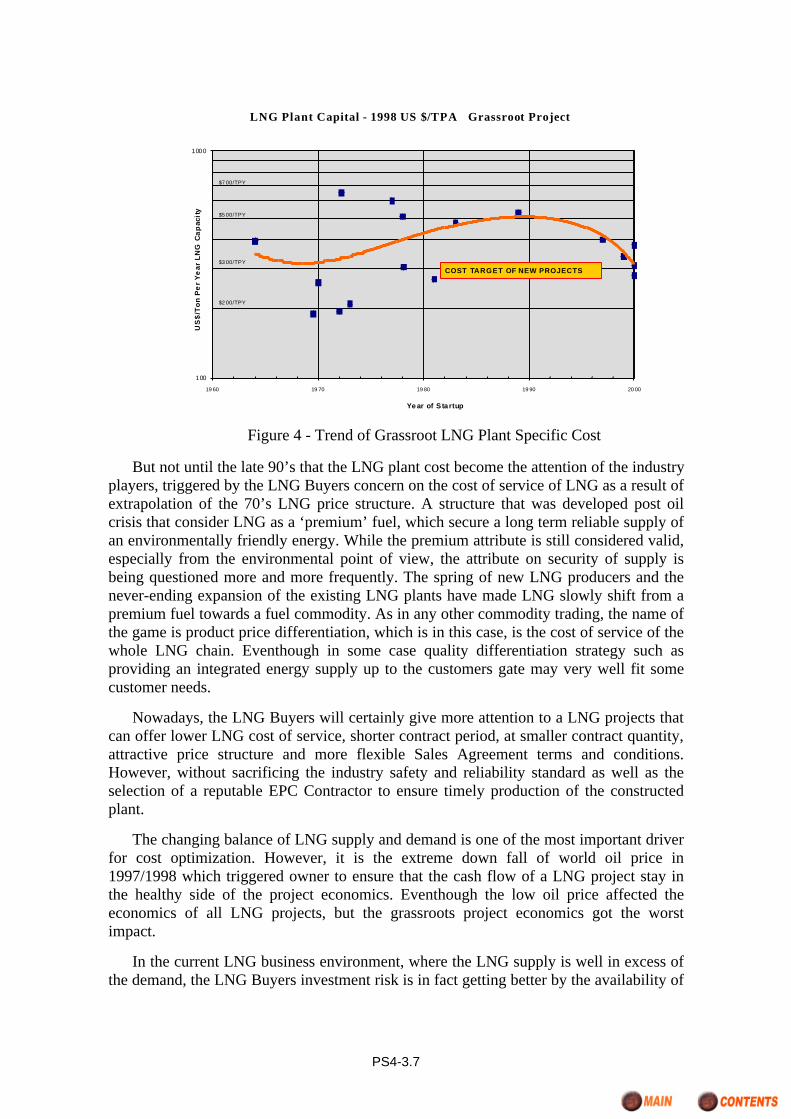

As the LNG train size getting larger, we should expect that the specific costs of aLNG project will tend to be lower and lower. However, as shown by the cost trend chartbelow, that is not the general trend.

0

0.5

1

1.5

2

2.5

3

3.5

1964 1969 1974 1979 1984 1989 1994 1999

Year Built

LN

G T

rain

Cap

acit

y m

mT

pa

Figure 3 - Grassroot LNG Plant Cost Trend

PS4-3.7

But not until the late 90’s that the LNG plant cost become the attention of the industryplayers, triggered by the LNG Buyers concern on the cost of service of LNG as a result ofextrapolation of the 70’s LNG price structure. A structure that was developed post oilcrisis that consider LNG as a ‘premium’ fuel, which secure a long term reliable supply ofan environmentally friendly energy. While the premium attribute is still considered valid,especially from the environmental point of view, the attribute on security of supply isbeing questioned more and more frequently. The spring of new LNG producers and thenever-ending expansion of the existing LNG plants have made LNG slowly shift from apremium fuel towards a fuel commodity. As in any other commodity trading, the name ofthe game is product price differentiation, which is in this case, is the cost of service of thewhole LNG chain. Eventhough in some case quality differentiation strategy such asproviding an integrated energy supply up to the customers gate may very well fit somecustomer needs.

Nowadays, the LNG Buyers will certainly give more attention to a LNG projects thatcan offer lower LNG cost of service, shorter contract period, at smaller contract quantity,attractive price structure and more flexible Sales Agreement terms and conditions.However, without sacrificing the industry safety and reliability standard as well as theselection of a reputable EPC Contractor to ensure timely production of the constructedplant.

The changing balance of LNG supply and demand is one of the most important driverfor cost optimization. However, it is the extreme down fall of world oil price in1997/1998 which triggered owner to ensure that the cash flow of a LNG project stay inthe healthy side of the project economics. Eventhough the low oil price affected theeconomics of all LNG projects, but the grassroots project economics got the worstimpact.

In the current LNG business environment, where the LNG supply is well in excess ofthe demand, the LNG Buyers investment risk is in fact getting better by the availability of

LNG Plant Capital - 1998 US $/TPA Grassroot Project

Ye ar of S tartup

100

1000

19 60 19 70 19 80 19 90 20 00

US

$/T

on

Pe

r Y

ea

r L

NG

Ca

pac

ity

$2 00/TPY

$3 00/TPY

$5 00/TPY

$7 00/TPY

COST TARGET OF NEW PROJECTS

Figure 4 - Trend of Grassroot LNG Plant Specific Cost

PS4-3.8

alternate sources. More spot LNG sales is a clear indication that alternative LNG isavailable in the open market.

Therefore, from the project economics perspective, the LNG project financiers willface higher investment risk than ever before. Especially if the major portion of the projectis funded through non-recourse project financing. On the other hand, in the case of equityfinancing, the burden shift to the Owner sides. Shorter contract period at a smallercontract quantity work against the project economics, above it all relaxation of the ‘takeor pay’ clause is a killer for the project economics.

All this will make the project financiers execute a more stringent due diligent on theproject economics, the feasibility of the design and the technology used, the EPCContractor performance (technical and financial), political stability in the producingcountry as well as the financial capability of the LNG Buyers. At the end of the day, theproject financier’s assessment will be reflected in financing cost of the project.

All of the above change drivers set a perfect framework for the LNG industry that aLNG project cost optimization is mandatory for the survival of many LNG projects andthe grassroots project has the highest priority to do so.

COST OPTIMIZATION MERITS IN A GRASSROOTS AND EXPANSION LNGPROJECTS

Why a grassroots project? Some owners or producing countries have an option eitherto build a grassroots plant or to expand the existing LNG plant. Beside the projecteconomics there are other consideration that a project owner, a producing country or insome cases the LNG Buyers and the project financier will promote a grassroots LNGproject instead of an expansion project.

In a country like Indonesia where the state oil company are the single LNG Seller andwhere the substantial gas findings are in distance apart, the development of multiple LNGcenter will add strength to the security and reliability of supply aspect. Any productionand shipping problem can be conveniently covered by the other LNG center, whichensure reliable supply to the Buyers and predictable revenue to the Seller.

For the project financier multiple LNG center of a single Seller will dissipate the riskof the investment as well as reducing the risk impact on the existing LNG plantinvestment if portion of the existing plant is financed by different investor.

The next question will be can a grassroots LNG plant project compete with expansionprojects. There are several factors to be considered before we can appropriately addressthis issue. It is generally accepted that a grassroots plant will never be able to competewith an expansion project. However, since the LNG cost of service and the LNG salesprice are two different things, it is possible that a project Owner offer a competitive LNGsales price even if the cost of service is higher, such as for a grassroots plant. In this case,the project Owner is accepting less revenue margin.

From a technical point of view, several factors may work in favor of a grassrootsLNG plant. The nature of the gas reserve may become the significant advantage for agrassroots LNG plant, such as the proximity of the gas reserve, access to deep sea waters,the depth of the reserve as well as the quality of the gas itself.

PS4-3.9

The existing LNG plant also impose an inherent disadvantage for the costoptimization of the expansion project. Because of its modular train concept, safety,operability and maintainability consideration, cause the expansion project usually a mereduplicate of the existing trains. While this will reduce the design and operating cost, aduplicate design will limit the possibility of other potential cost optimization for anexpansion project as follows:

• Duplicate capacity causes an expansion train could not enjoy the economic ofscale advantage of a larger train design.

• For an expansion project done long after the first train, duplicate design mayfind that some equipment or spare parts has become obsolete and costly.

• Duplicate design will limit the EPC Contractor opportunity for a competitivebidding of each equipment and therefore reduce the possibility for anoptimized project cost.

• Duplicate design will limit the opportunity for cost optimization through latesttechnology development such as in advanced process control; computer aidedproduction as well as the newest application of higher efficiency equipmentand material.

• Duplicate design may require a design retrofit to comply with the latestenvironmental specification, which will be more efficiently done in agrassroots design.

On the other hand, an expansion project does not require a new set of full-scaleinfrastructures, LNG harbor and utilities, which is a major cost item for a project.

An expansion project with a duplicate design also could not easily enjoy theopportunity of multiple technology competitive bidding as in a grassroots project. All ofthe existing LNG plants have selected the same LNG liquefaction technology for theirexpansion project. However, this concept is currently being questioned by severalOwners and a multiple technology trains in a single plant is not an impossible concept toimplement.

Also, a grassroots plant enjoy the possibility for a ‘fit for purpose’ design with a pre-set cost objective which can be determined to meet or exceed the cost advantage of anexpansion project. The following chart shows an estimated project cost comparison ofgrassroots and expansion LNG projects.

PS4-3.10

Therefore, competitiveness of a grassroots plant versus an expansion project shouldbe analyzed on a case by case basis and could not be simplistically generalized. In fact, arecent grassroots LNG plant had successfully prove that a grassroots plant can beconstructed at a competitive cost compare to a typical expansion project.

MAKING COMPETITION AT WORK FOR A GRASSROOTS LNG PROJECTCOST OPTIMIZATION

For many years, the practice in the LNG industry has been a competition in the EPC(Construction) work. Project Owner pre-selected the main technology, which include theLNG Liquefaction technology and the Process Driver technology. Those are thetechnologies not much dependent on the feed gas composition or other site-specificcondition. In the Asia-Pacific region, the Propane Pre-cooled Mixed Refrigerant LNGLiquefaction technology has led the market share. It has a proven track record on safetyand reliability, which was and is still the main consideration of the Asia Pacific LNGBuyers. One LNG plant employs a Cascade Refrigeration LNG Liquefaction technology,which has equal safety and reliability records.

In line with the rapid growth of LNG market in Asia-Pacific in the 70’s and 80’s,larger and larger plant capacity becoming a necessity to fulfill the economic of scale. Theprocess efficiency and the manufacturing flexibility of the main equipment to match thehigher plant capacity, makes the Propane Pre-cooled MR the technology of choice in thatbooming LNG era. The demand for a larger LNG plant also matched by the developmentof larger gas turbine technology, which makes the gas turbine the technology of choicefor the process system driver. Despite the booming of the LNG market, it is quitesurprising that the other LNG Liquefaction technology developer did not make significantattempt to advance their technology for the large capacity LNG plant.

Not until recently that the other LNG Liquefaction, technology developer start torealize that the LNG market seem to offer enough rooms for more than one player. As hasbeen described earlier, the key issue in the year 2000 era is a low cost LNG plant,something that the previous LNG project which happen to apply the Propane Pre-cooled

Optimization Oportunity - Grassroots & Expansion LNG Project, 1 Train, 3 mmTpa

Grassroots -Ba se Gra ssroots - Optim ized Expa nsion - Ba se Expa nsion - Optim ize d

Pro

ject

Cos

t

Liquefaction Utilities

S & L Marine

Infrastructure EP C

Figure 5 - Optimization Opportunity of Grassroot & Expansion Project

PS4-3.11

MR, seem fail to address. Even for a larger capacity, which could have improved theeconomic of scale, as shown in Figure 4?

LNG analysts have different assessment as to whether it is the LNG Liquefactiontechnology or the other aspect of the plant design is the main factor for the high LNGcost.

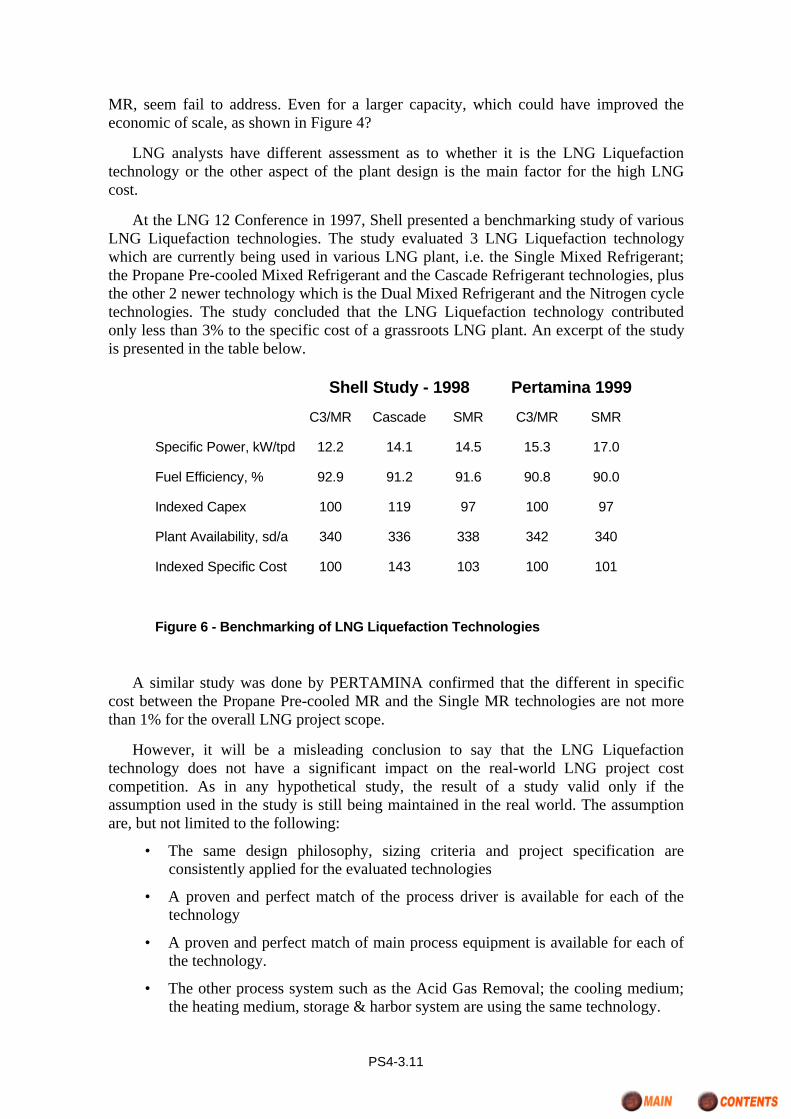

At the LNG 12 Conference in 1997, Shell presented a benchmarking study of variousLNG Liquefaction technologies. The study evaluated 3 LNG Liquefaction technologywhich are currently being used in various LNG plant, i.e. the Single Mixed Refrigerant;the Propane Pre-cooled Mixed Refrigerant and the Cascade Refrigerant technologies, plusthe other 2 newer technology which is the Dual Mixed Refrigerant and the Nitrogen cycletechnologies. The study concluded that the LNG Liquefaction technology contributedonly less than 3% to the specific cost of a grassroots LNG plant. An excerpt of the studyis presented in the table below.

C3/MR Cascade SMR C3/MR SMR

Specific Power, kW/tpd 12.2 14.1 14.5 15.3 17.0

Fuel Efficiency, % 92.9 91.2 91.6 90.8 90.0

Indexed Capex 100 119 97 100 97

Plant Availability, sd/a 340 336 338 342 340

Indexed Specific Cost 100 143 103 100 101

Figure 6 - Benchmarking of LNG Liquefaction Technologies

Shell Study - 1998 Pertamina 1999

A similar study was done by PERTAMINA confirmed that the different in specificcost between the Propane Pre-cooled MR and the Single MR technologies are not morethan 1% for the overall LNG project scope.

However, it will be a misleading conclusion to say that the LNG Liquefactiontechnology does not have a significant impact on the real-world LNG project costcompetition. As in any hypothetical study, the result of a study valid only if theassumption used in the study is still being maintained in the real world. The assumptionare, but not limited to the following:

• The same design philosophy, sizing criteria and project specification areconsistently applied for the evaluated technologies

• A proven and perfect match of the process driver is available for each of thetechnology

• A proven and perfect match of main process equipment is available for each ofthe technology.

• The other process system such as the Acid Gas Removal; the cooling medium;the heating medium, storage & harbor system are using the same technology.

PS4-3.12

• No consideration for the additional cost required to compensate discrepancieson operational and maintenance features of each technology, such as control orsafety system complication

• No consideration for the EPC competitiveness impact on cost such asprocurement efficiency and construction efficiency

• No consideration or the EPC Contractor bidding strategy impact on cost

Therefore, in the evaluation of the real world LNG project cost competition, it is moreimportant to put attention on assumptions and what is not considered in a hypotheticalstudies than the hard number conclusion of the studies itself.

The only way to verify the assumption is by executing a Multiple technology FrontEnd Engineering Design. However, multiple FEED is not cheap and simple to manage,requires not only technically competent Owner’s project team but also require a uniqueproject management plan and control.

It is therefore very important that the selection of the LNG technology to be involvedin a Multiple FEED competition shall be put under the frame work of the final projectobjective, that is to secure LNG Sales Contract and Financing Agreement.

As has been discussed in the earlier section, with shorter contract term and smallerquantity commitment the risk of a new LNG project lies more on the project financierrather than on the LNG Buyers side. Therefore, unless a technology has a clear technicaland cost competitiveness that can be justified later in front of the project financier andBuyer it would not be wise to carry out a Multiple FEED.

However, the problem is, the clear technical and cost competitiveness of a technologycan only be verified after the FEED. Unfortunately, even a FEED cannot be used toverify the cost impact of EPC Contractor’s procurement and construction efficiency,and/or bidding strategy which will only be known after the EPC work bids.

Requesting project financier and/or Buyer opinion prior to execution of MultipleFEED is not a common practice since what their concern is not how a project Ownerimplement the FEED but what is the outcome of the FEED work for the proposed projectand proposed financial plan. In the current LNG producer competition, a project financieror a LNG Buyer will not have a difficulty to find alternative LNG project, which fit theirrequirement or risk criteria.

Justification to include a technology in a Multiple FEED remains in the projectowner’s hand, and can be addressed by one of the following strategy:

• Include only the technology which have been well accepted by the LNG projectfinancier or Buyers in the region

• Include as many viable technology as the FEED cost can be justified and makedecision after the EPC bids is received, evaluated and offered to the LNG market.

Execution of a Multiple FEED is indeed a unique and challenging undertaking, theLNG industry is yet to learn the whole process, the constraint and the complication ofdoing a Multiple FEED work. However, the potential benefit is so promising for agrassroots LNG project to simply ignore the concept. For them, it is more a survival kitsrather than great looking outfit.

PS4-3.13

LNG LIQUEFACTION TECHNOLOGY, IS IT THE REAL AND THE ONLYISSUE ON PROJECT COST COMPETITION?

As has been discussed briefly in the earlier section, the technology per se is not asignificant factor for the project cost optimization. This means, in theory the optimizationobjective could still be achieved with design competition implemented around a pre-selected LNG technology.

However, execution of a Multiple technology competition is still one of the bestpractical ways to promote cost optimized LNG plant design:

• Technology competition open the possibility for a performance based designrather than a specification based design

• Technology competition breaks the latent paradigm of outdated projectphilosophies and promote design innovation

• More Contractors and technology licensors involved, promote higher level ofcompetition

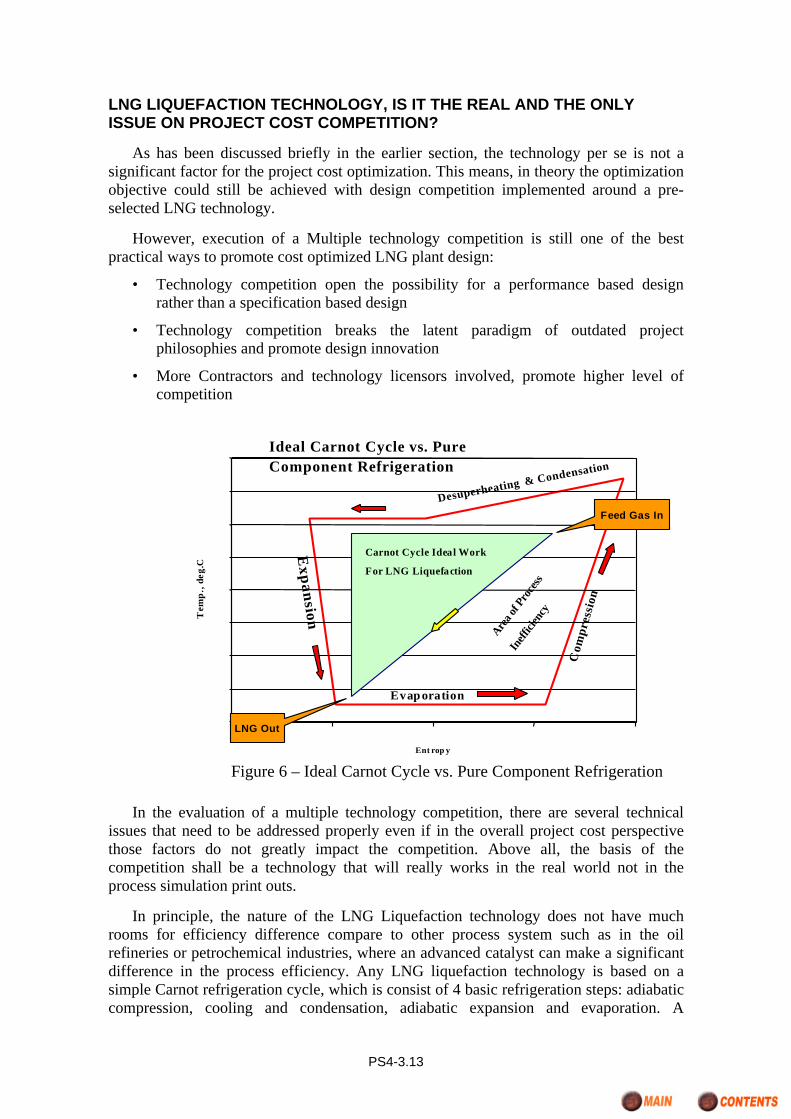

In the evaluation of a multiple technology competition, there are several technicalissues that need to be addressed properly even if in the overall project cost perspectivethose factors do not greatly impact the competition. Above all, the basis of thecompetition shall be a technology that will really works in the real world not in theprocess simulation print outs.

In principle, the nature of the LNG Liquefaction technology does not have muchrooms for efficiency difference compare to other process system such as in the oilrefineries or petrochemical industries, where an advanced catalyst can make a significantdifference in the process efficiency. Any LNG liquefaction technology is based on asimple Carnot refrigeration cycle, which is consist of 4 basic refrigeration steps: adiabaticcompression, cooling and condensation, adiabatic expansion and evaporation. A

Ent rop y

Tem

p.,

deg.

C

Feed Gas In

LNG Out

Carnot Cycle Ideal Work

For LNG Liquefaction

Area o

f Pro

cess

Ineff

icien

cy

Ideal Carnot Cycle vs. PureComponent Refrigeration

Com

pres

sion

Desuperheating & Condensation

Evap oration

Expansion

Figure 6 – Ideal Carnot Cycle vs. Pure Component Refrigeration

PS4-3.14

refrigeration cycle is a process of transferring heat from the process side into a heat sink(air, seawater or a cooling tower system).

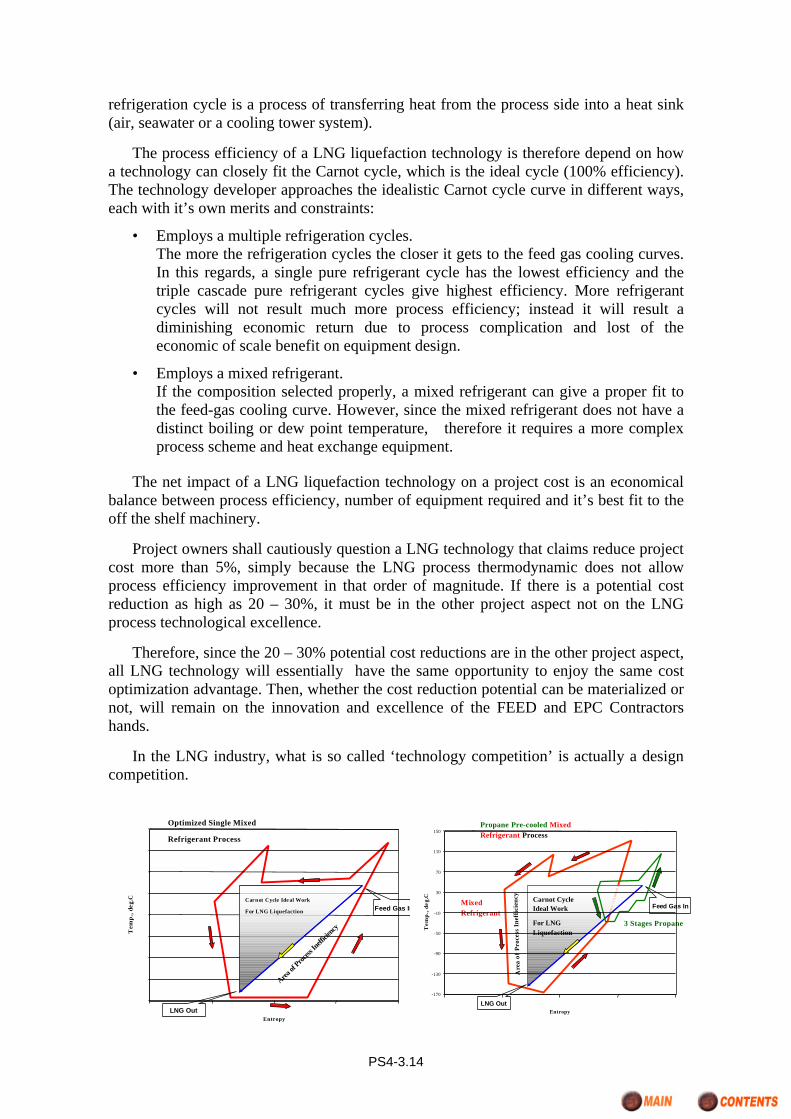

The process efficiency of a LNG liquefaction technology is therefore depend on howa technology can closely fit the Carnot cycle, which is the ideal cycle (100% efficiency).The technology developer approaches the idealistic Carnot cycle curve in different ways,each with it’s own merits and constraints:

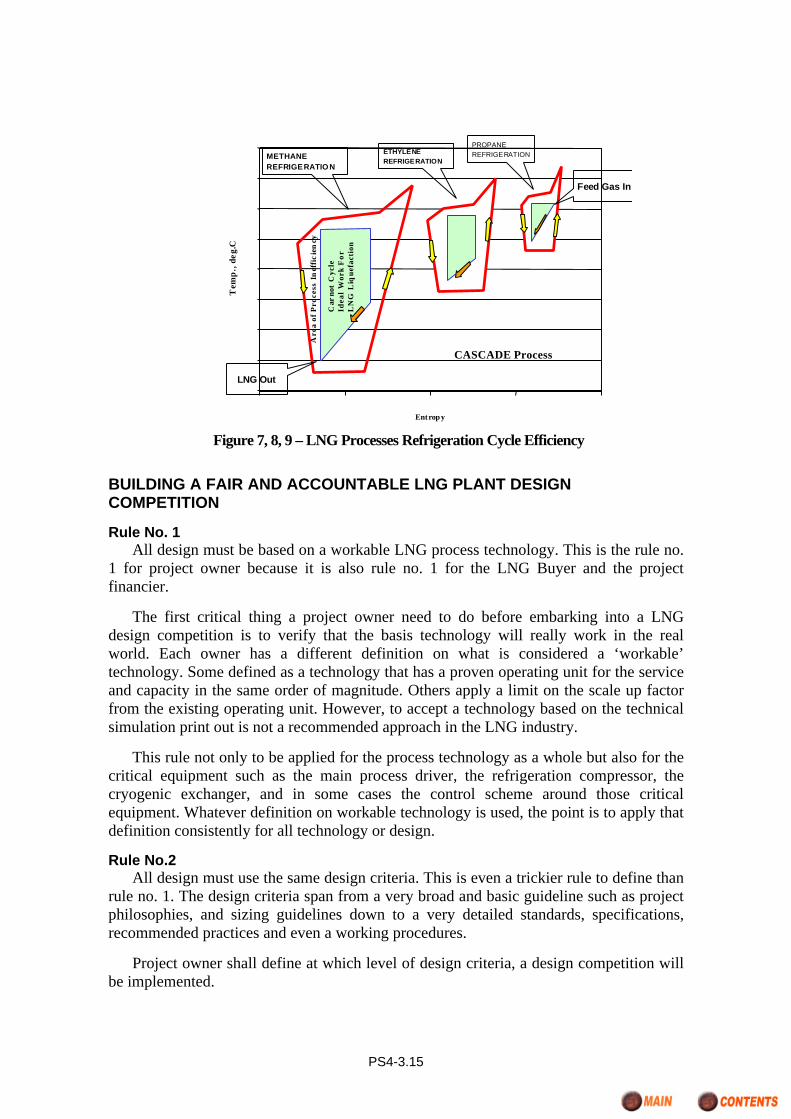

• Employs a multiple refrigeration cycles.The more the refrigeration cycles the closer it gets to the feed gas cooling curves.In this regards, a single pure refrigerant cycle has the lowest efficiency and thetriple cascade pure refrigerant cycles give highest efficiency. More refrigerantcycles will not result much more process efficiency; instead it will result adiminishing economic return due to process complication and lost of theeconomic of scale benefit on equipment design.

• Employs a mixed refrigerant.If the composition selected properly, a mixed refrigerant can give a proper fit tothe feed-gas cooling curve. However, since the mixed refrigerant does not have adistinct boiling or dew point temperature, therefore it requires a more complexprocess scheme and heat exchange equipment.

The net impact of a LNG liquefaction technology on a project cost is an economicalbalance between process efficiency, number of equipment required and it’s best fit to theoff the shelf machinery.

Project owners shall cautiously question a LNG technology that claims reduce projectcost more than 5%, simply because the LNG process thermodynamic does not allowprocess efficiency improvement in that order of magnitude. If there is a potential costreduction as high as 20 – 30%, it must be in the other project aspect not on the LNGprocess technological excellence.

Therefore, since the 20 – 30% potential cost reductions are in the other project aspect,all LNG technology will essentially have the same opportunity to enjoy the same costoptimization advantage. Then, whether the cost reduction potential can be materialized ornot, will remain on the innovation and excellence of the FEED and EPC Contractorshands.

In the LNG industry, what is so called ‘technology competition’ is actually a designcompetition.

Entropy

Tem

p.,

deg.

C

Feed Gas In

LNG Out

Carnot Cycle Ide al Work

For LNG Liquefaction

Area of

Process

Ineff

icien

cy

Optimized Single Mixed

Refrigerant Process

Feed Gas InCarnot CycleIdeal Work

For LNGLiquefaction

Are

a of

Pro

cess

Ine

ffic

ienc

y

Propane Pre-cooled MixedRefrigerant Process

3 Stages Propane

MixedRefrigerant

-170

-130

-90

-50

-10

30

70

110

150

Entropy

Tem

p.,

deg.

C

LNG Out

PS4-3.15

BUILDING A FAIR AND ACCOUNTABLE LNG PLANT DESIGNCOMPETITION

Rule No. 1All design must be based on a workable LNG process technology. This is the rule no.

1 for project owner because it is also rule no. 1 for the LNG Buyer and the projectfinancier.

The first critical thing a project owner need to do before embarking into a LNGdesign competition is to verify that the basis technology will really work in the realworld. Each owner has a different definition on what is considered a ‘workable’technology. Some defined as a technology that has a proven operating unit for the serviceand capacity in the same order of magnitude. Others apply a limit on the scale up factorfrom the existing operating unit. However, to accept a technology based on the technicalsimulation print out is not a recommended approach in the LNG industry.

This rule not only to be applied for the process technology as a whole but also for thecritical equipment such as the main process driver, the refrigeration compressor, thecryogenic exchanger, and in some cases the control scheme around those criticalequipment. Whatever definition on workable technology is used, the point is to apply thatdefinition consistently for all technology or design.

Rule No.2All design must use the same design criteria. This is even a trickier rule to define than

rule no. 1. The design criteria span from a very broad and basic guideline such as projectphilosophies, and sizing guidelines down to a very detailed standards, specifications,recommended practices and even a working procedures.

Project owner shall define at which level of design criteria, a design competition willbe implemented.

CASCADE Process

Entrop y

Tem

p.,

deg.

C

METHANE REFRIGERATIO N

ETHYLENE REFRIGERATION

PROPANE REFRIGERATION

Are

a of

Pro

cess

In

effi

cie

ncy

Car

not

Cyc

leId

eal

Wor

k F

or

LN

G L

ique

fact

ion

Feed Gas In

LNG Out

Figure 7, 8, 9 – LNG Processes Refrigeration Cycle Efficiency

PS4-3.16

On a performance based design competition, the Contractors use the same projectphilosophies and sizing guidelines. Owner only defines the main characteristic of theproject such the plant capacity, product quality and the plant availability factor, then therest of the design would be up to each Contractor. In this case, owner must prepare toreceive a design, which will not be ‘apple to apple’ from the equipment design point ofview. In a performance-based design competition, a cost reduction up to 20 –30% is notuncommon target to achieve, regardless the technology selected as the basis of the designcompetition.

In a specification based design competition, the outcome of the design will looksmore ‘apple to apple’, but since the Contractors do not have too much degree of freedomto design, Owner shall be prepared to accept a cost reduction in the order of 10 – 15%only. In the LNG industry, it is advisable that owner at least define the safety andreliability specifications at a detailed enough level to maintain the current proven trackrecord of the LNG industry.

Those two basic rules set the cost optimization objective in a fair and accountableLNG plant design competition. Furthermore, owner require to define and describe to theContractor the EPC bid evaluation criteria in order to maintain a fair and accountabledesign competition:

• If owner pre-selected the process driver and its available power, will owner allowthe Contractors to utilize the available power beyond the plant capacity specifiedby owner and receive a merit score in the EPC bid evaluation

• In the case the EPC bid evaluation is done on a ‘life cycle cost’ basis, owner todefine how the fuel or feed gas saving will be valued.

• A ‘life cycle cost’ EPC bid evaluation will also require owner to define the valueused for imported fuel, chemicals and refrigerant.

• Owner is also require to define Net Discount Rate as well as the Break EvenCapex $ for every $ of Opex saving.

A clear definition of EPC bid evaluation criteria will not only ensure that the ownerwill receive an EPC Bid Proposal which met the owner project objectives, but also enableContractor concentrate on the design competition and feel comfortable that the EPC bidevaluation will be done fairly according to the prescribed criteria known to the EPCBidders and the public.

REAL WORLD DILEMMA IN LNG PLANT MULTIPLE FEED COMPETITION

Real World Factors in LNG Technology Competitiveness:

1. Specified LNG Plant Capacity

2. Specified Driver Type and Configuration

3. Allowed Supplemental Driver Power

4. Value of Potential Excess LNG Capacity

5. Value of Fuel Gas

6. Feed Gas Composition

PS4-3.17

In the concept of multiple FEED competition for LNG plant cost optimizationdescribed above, it is concluded that the LNG technology does not really have asignificant impact to the overall project cost. However, since every concept is developedbased on idealistic approach, its real world application may lead to a completely differentconclusion. One of the important factor which cause a LNG technology may has anoticeable merit in a project cost reduction is the specified plant capacity. Most recentLNG projects were designed based on the gas turbine drivers fixed off the shelf availablepower, this constraint will cause certain technology will enjoy an optimum driver powerutilization. All available power is used and match will Owner requirement for thespecified plant capacity. For a more fair competition, it is recommended to allowContractor select from several approved type of gas turbine drivers. Other way is to allowContractor to utilize starter/helper driver (motor or steam turbine) supplement in the gasturbine trains.

Plant capacity specification and the limitation of approved gas turbine type to be usedfor the design may also impose a particular LNG technology must apply refrigerationcompressor size beyond what is considered ‘proven’ by the LNG industry. This constraintwill certainly lower the technical confidence of those particular technology and iftechnical confidence in this critical part of the plant had a significant weight factor on theoverall technical evaluation, a particular technology may not become attractive tocompete.

Other impact of the specified plant capacity to the competitiveness of a LNGtechnology is how Owner valued the ‘excess’ LNG production or limitation on theallowed supplemental power from the helper driver. Excess LNG capacity has no valuedif the plant is under utilized. However, many LNG producers have been successfullymarket their excess capacity. Some LNG plants even enjoyed a repetitive debottleneckingprojects. On the other hand, if the potential excess capacity is valued too high, Contractormay design a high capacity plant, which may not be actually marketable, when the plantis in operation.

The gas composition may also has considerable advantage to a particular technology.A rich feed gas or a feed gas with adequate heavier components content will advantage aLNG technology using all refrigerants from the available feed gas component, whileother LNG technology may need to import the refrigerants which will require additionalinvestment for the receiving and storage facilities.

While some factors such as feed gas composition are beyond Owner control, otherfactors can be devised to promote maximum competition on LNG technology.

Factors on LNG Plant Design Competition:

1. Contractor competition within a particular technology

2. Definition of ‘Fit For Purpose’ design

3. Level of details of design deliverables

4. Limitation on bid documents deviations, exceptions and alternativesproposal.

5. Bidding Processes

As has been discussed earlier in the concept of fair and equal LNG Plant designcompetition, it is of utmost important to apply the same principle and criteria for all

PS4-3.18

competing LNG technology and competing EPC Contractors. In other words, ideallywhat left for the competition are: (a) the intrinsic characteristic of the technology, (b)Contractors innovation in facilities design, (c) Contractor efficiency in procurement and(d) Contractor efficiency in the construction of the facilities.

However, strict application of the same design principle and criteria will greatlyreduced Contractors flexibility in the interpretation of the principle and criteria, matchthem with their past experiences, best practices, company policy and procedures andworking environment. Each of which is unique for every Contractor and may contributeto considerable potential cost reduction of project cost if applied properly.

One case in point is how a process licensor market their LNG technology to the EPCContractors. Many of the process licensor make their technology available for anyinterested Contractor, some has a closer relationship and preferences to a particularContractor and a process licensor may decide to have an exclusive alliance with only oneContractor to improve their competitiveness in the LNG industry. Exclusive alliance of aprocess licensor to a particular Contractor is not a new concept in other industry such asin the oil refinery, petrochemicals and fertilizer industries. In fact, in those industriesexclusive alliance may become a necessary business strategy to protect the intellectualproperty rights of the technology. Exclusive alliance of a process licensor and aContractor is not a common concept in the LNG industry, until recently. LNG technologyis more a physical processes and apply very similar refrigeration principles. However, anexclusive alliance or any close relationship of a process licensor to a Contractor may havea considerable advantage in project cost reduction due to the potential improvement in theworking efficiency and will foster design innovations.

Alliance or not to alliance, both have their own merit and disadvantage. Exclusivealliance will not work for single FEED concept where Owner pre-selected a LNGtechnology. The best way for Owner is to leave this business decision to the processlicensor and the EPC Contractors community. In a multiple FEED competition, all partieshave the same opportunity to win the competition and therefore benefit Owner objectivefor project cost reduction. However, Owner must be very careful in accessing the impactof exclusive alliance for the project expansion case. In a multi trains LNG project, anytechnology or contractor successfully won the initial train development will have a clearadvantage over other competing technology or contractor for the expansion project evenif the expansion project is opened for different technologies.

The EPC of a LNG project consist of approximately 10 – 15% detail engineering cost.The contractor who won the contract for the initial project facilities will enjoy a minimumcost for the design of the expansion project. This factor need to be considered orincorporated in the evaluation criteria for the expansion project to ensure that the bidprocesses and environment for the expansion project will still be attractive for competingcontractors and promote project cost reduction.

PS4-3.19

The other three factors in the design competition, (a) definition of the ‘fit for purpose’design, (b) level of details of the design deliverables, and (c) limitation on the alloweddesign deviation, exception or alternative proposal are interlinked.

It is not very simple to define and agree on what is considered a ‘fit for purposes’design. Figure – 10 below illustrate the basic components of a LNG plant design. It iswell understood that a project shall has a consistent project philosophies applied in allproject design basis, specification and data sheets. In the development of project designbasis, specification and data sheets, requirement for a very detail design deliverables is anassurance of what will be purchased, built and constructed. Detail project description alsomakes the bid evaluation much easier and accountable. On the other hand, detaildescription means the qualified manufacturers, supplier or vendor list are gettingnarrower which will certainly limit contractor leverage with the sub-contractor orvendors. The cost of the project may become adversely impacted.

Therefore, the key of the issue is to find an acceptable balance between the level ofdetails of the design deliverables to ensure a clear main contractor commitment to theproject owner, but not to details as to limit the subsequent competition in the sub-contractor and vendor level.

Another dilemma is how owner will evaluate or treat a non compliance bids. A nearperfect bid documents shall lead to a minimum number of clarified items, none orminimum number of bid exception, deviation or alternative proposal. However, the EPCcontractor community does not have as high concern as the owner side to fully complywith a bid requirement. For the contractor, an alternative proposal may be the only wayto win a bid. Therefore, it will be very naïve to expect that all contractors will fullycomply with the bid requirement. On the other hand, if a project description andspecification is to broad and give so much freedom for an interpretation and alternatives,

Project Strategy(Mission Statement, Project Economics, Execution Plan,

Marketing, Contracting, Organization)

Project Philosophy(Commitment statement, RFP, Basis of Design, Corporate EHS Policy, TIICS, Preinvestment)

Technology & System Industrial Standard Design Margin Life Cycle Cost

Licensor Technology,Process Scheme

API, ASME, NFPA, etc.EPC Contractor Margin

Licensor MarginOwner Margin

Capital Cost vs Operating Cost

Exis

ting

LNG

Pla

ntPr

actic

es

Oth

er L

NG

Pla

nt

Oth

er I

ndus

try

New

Dev

elop

ed

INNOVATION

EPC BID Alternative

OVERALL “FIT FOR PURPOSE” MATRIX

“Must and Shall” for LNG Plant

Must have for general Industry

“Should” (Optional)

EHS Aspect

EPC BID Alternative

Maintenance &Operational Aspects

Capital Cost

Operating Cost

Expected EPCCost from FEEDContractor

Figure 10

PS4-3.20

the bid evaluation may become the second FEED work. Before defining what is expected,allowed or not allowed, owner may want to explore each potential bidders intention andinterpretation of the bid documents.

Due to the complication of the multiple FEED bid processes and evaluation, it isalmost impossible to execute a multiple FEED bid processes in a single bid proposalsubmittal system. Separate submittal of technical bid, followed by clarification andrevision is likely to be more manageable and ensure that all bidders meet ownerexpectation on technical requirement. Submission of the commercial proposal and theLumpsum fixed price is then be done only if all technical matters have been clarified. Thedownside of this separate submittal of technical and commercial bid is the longer timerequired to reach a bid winner decision. Here again, the key is to find a balance betweenthe available time for bid evaluation and a consistent ‘apple to apple’ technical bidevaluation.

CONTRACTING STRATEGY FOR A LNG PROJECT COST COMPETITION

Beside a consistent design and bid evaluation criteria, a well defined contractingstrategy is another essential factor for a fair and accountable LNG plant designcompetition. The contracting strategy for a Multiple technology design competition canbe either:

• An integrated bidding process of FEED work and EPC work.In this case, the pre-qualification process is intended to qualify Contractors forthe EPC bid. The qualified EPC Bidders are also the qualified FEED Bidders.The integrated bid process is intended to shorten the whole bid process byeliminating the pre-qualification phase in the EPC bid process. Owner mayalso apply a so-called ‘drip FEED’, in which the Contractors not winning theFEED contract will receive the FEED deliverables, as they are available fromthe Contractor executing the FEED work. By doing so, the time to prepare theEPC bid proposal can be reduce by 50%. While this contracting strategy doeshave a merit to speed up the project schedule, it is a complex process andtherefore requires a careful planning, proper technical quality assurance aswell as adequate project control and administration.

• A separate FEED work and EPC work bidding process.This is the conventional way of executing the FEED and EPC bid and can bedone only if the time is available. In this case, the qualified FEED bidder doesnot necessarily become a qualified EPC bidder. Another pre-qualificationusing different criteria will be done for the EPC bid phase.

PS4-3.21

In the multiple FEED design competition with ‘drip FEED’, owner must pay adequateattention to the quality of the FEED work. There is a possibility that due to the need to becompetitive in the EPC bid the FEED contractor will not completely disclosed all of theirdesign innovation to their ‘would be competitors’. If the FEED work is done properly,there should not be much exception; clarification or alternative bid items in the EPC bidproposal.

COST OPTIMIZATION OF INDONESIA’S TANGGUH LNG PROJECT

The Tangguh LNG is developed to be the third LNG center in Indonesia. Located inthe eastern part of Indonesia, it enjoys the proximity to China, Japan, Korea and TaiwanLNG market. For PERTAMINA, Tangguh LNG is the next grassroots plant almost 30years after the grassroots facilities were built in Arun and Bontang LNG Plants.

However, the LNG business environment today is completely different from thebusiness set-up back in the 70’s. The future is no longer a linear extrapolation of ourexperiences.

Bontang LNG plant still hold the world record for the shortest time required for thefirst LNG shipment counted from the first gas well discovery. Both Arun and Bontanggrassroots LNG Plants were built as a fast track project on reimbursable fee EPCcontract.

On the contrary, Tangguh LNG project is being developed in a fierce LNG marketcompetition, as a grassroots plant that has to compete with many LNG expansionprojects. Therefore, Tangguh LNG project must do things differently in order to survivethe competition.

The Tangguh LNG Project was originally planned for a two trains launch, withOwner pre-selected the Acid Gas Removal technology and the LNG Liquefactiontechnology on a single FEED contract strategy. The project economics started to

INTEGRATED FEED & EPC BID

B D EV E LO P F E E D

- T E CH NO LOG Y X

F EED BID DERS:

A, B, C

B

EPC BID DERS :

A, B, C

E D EV E LO P F E E D

- TE C H N O L O G Y Y

F EED BID DERS:

D, E, F

E

EPC BID DERS :

D, E, F

G D EV E LO P FE E D

- TE C H N O L O G Y Z

FEED BID DER:

G

G

EPC BID DER:

G

EPC

Contract

Winner

D

X -

EPC BIDPACKA GE

Y -

EPC BIDPACKA GE

Z -EPC BID

PACKA GE

Multiple FEED

FEED BID DERS:

A, B, C, D,E, F, G

Figure 10 – Contracting Strategy for Multiple Technology Competition

PS4-3.22

deteriorate when the industry experience a record low on crude oil price in 1998,amplified by the difficulties to find prospective Buyers for a 2 trains production quantity.Since then, the project economics was thoroughly re-evaluated, crude oil priceassumption revised, and the launch quantity revised to one train. It was concluded that theonly way to achieve such a massive cost reduction was by executing a multipletechnology competition on an integrated FEED and EPC bidding processes. Lesson waslearned from the Trinidad LNG Project, in which British Gas is also one of the partner inthe project.

FEED/EPC Bidders pre-qualification completed in August 1999, and the FEED bidprocess completed in February 2000. The FEED work started in April 2000 for a 12months schedule . The FEED applies a ‘drip FEED’ concept, in which the FEEDContractor will drip the deliverables to the EPC Bidders participant.

The Multiple FEED strategy had been implemented in Atlantic LNG (Trinidad &Tobago), and had achieved a very significant project cost reduction. The plant has beencommissioned and operated successfully. The ‘drip FEED’ had been implemented inOman LNG Project and has reduced the project cycle time significantly. Tangguh LNGProject will implement both concept, a Multiple and ‘drip’ FEED. To the best of ourknowledge, no other LNG project has ever embarked into such kind of integrated projectmanagement concept.

PERTAMINA had executed two grassroots LNG projects in the 70’s, since thenPERTAMINA had successfully managed 7 (seven) LNG Expansion Projects. The lastproject was completed in 1999. No other oil majors have similar experiences. Despite theprevious project were managed in a ’conventional’ way, our commitment to executeTangguh LNG project in a different way prove PERTAMINA ability to meet thechanging LNG industry demand, business practices and competition.

CONCLUSION

The world LNG industry is changing but the Asia Pacific LNG industry is facing evenmore business pressure to change. With the sluggish LNG demand forecast and moreplayers entering the LNG industry, LNG will become more a commodity rather thanpremium energy alternative.

Eventhough analysts forecasted that the supply demand gap would disappear past theyear 2010, but that forecast itself is a signal that more LNG project will be developed toanticipate the narrowing gap. Competition for the LNG market will not going to be easierin he future. Consequently, the LNG producers started to accept the need to restructurethe business, the contract term and condition, the project management and the project-financing scheme.

Any grassroots LNG project has obvious cost disadvantage compare to an expansionproject, owing to larger scope and complexity. However, a grassroots project has its ownmerit of higher opportunity for cost optimization since it does not limited by the existingdesign, specification or contracting strategies. If managed properly a grassroots LNGproject would be able to compete head to head with any expansion project, even at asmaller LNG sales quantity.

The need and the opportunity to do things differently in a grassroots LNG project hasgenerated a numbers of project management concept, design philosophies and contracting

PS4-3.23

strategies. Multiple FEED and ‘drip’ FEED emerges as a promising concept to achievethe specified target cost.

Execution of Multiple and ‘drip’ FEED requires Owner to clearly pre-scribe thecompetition boundary and the evaluation criteria. Level of detail on design competitionshould be appropriately set to meet Owner project cost objective. All of the competitionaspect, including bid procedure should be planned thoroughly to achieve a fair andaccountable design competition.

The LNG industry has a varied understanding on what is called a LNG Liquefactiontechnology competition. Many studies revealed that the LNG Liquefaction technology isnot a significant contributor to the project cost optimization. Recent PERTAMINA studyalso confirmed the previous study finding. Other aspect such as design innovation, projectspecification and contracting strategy contribute more than the feature of the technologyitself. The so called ‘technology competition’ is more appropriately called as ‘designcompetition’.

PERTAMINA considers a design competition is a necessary tool for a survival of agrassroots project like the Tangguh LNG Project. In the future, it would not be impossibleto expand the concept for an expansion project.

In doing any effort to optimize project cost, Owner must always remember that theend result of any LNG project competition is to secure LNG Sales Purchase Agreementand Project Financing Agreement. Buyer requirement to meet safety and reliabilitystandards shall not be overlooked or relaxed by the need to reduce cost.

The trend to have a smaller contract quantity, for a shorter period and at a less rigidcontract term and condition has put a LNG project as a higher investment risk for ProjectFinancier. Owner should consider this aspect by designing countermeasures in the projectcost optimization effort. FEED/EPC Bidders must be pre-qualified and selected not onlybased on their technical performance but also the financial strength.

The LNG industry will continue to change. The players that will survive in the longrun is the one that can adjust to and anticipate new demand and situation.

REFERENCES CITED

1. “Asia Pacific LNG Demand and Supply Forecast”, Gas Matters, April 1998

2. “LNG Project Cost Benchmarking, Multi Client Study”, Poten & Partner, InternalReport to ARCO, April 1999

3. R. N. DiNapoli, C. C. Yost III, “LNG Plant Costs: Present and Future Trends”, 12th

International Conference on Liquefied Natural Gas, Perth, May 1998

4. K. J. Vink, R. K. Neigelvoort, “Comparison of Baseload Liquefaction Processes”,12th International Conference on Liquefied Natural Gas, Perth, May 1998

5. PERTAMINA, “LNG Processes Evaluation Report”, PKP, Processing DirectorateInternal Study, November 1999

6. “Liquefied Natural Gas (LNG) Fact Sheet”, U.S. Energy Information Administration,October 1998

7. Institute of Gas Technology, “Delay Seen For New Projects”, LNG Observer Vol. IXNo.6, November – December 1998