Embed Size (px)

Citation preview

Compounding of Contraventions & Transfer Pricing Developments

Prof.(Dr.) Alok Pandey, Professor (Finance) & Member Academic Advisory Body

Lal Bahadur Shastri Institute of Management, Delhi

Overview of Presentation

• Section 1: FEMA- A brief overview• Section 2: Compounding of Contraventions• Section 3: Transfer Pricing & Recent

Developments

FEMA: A Brief Overview

Section 1

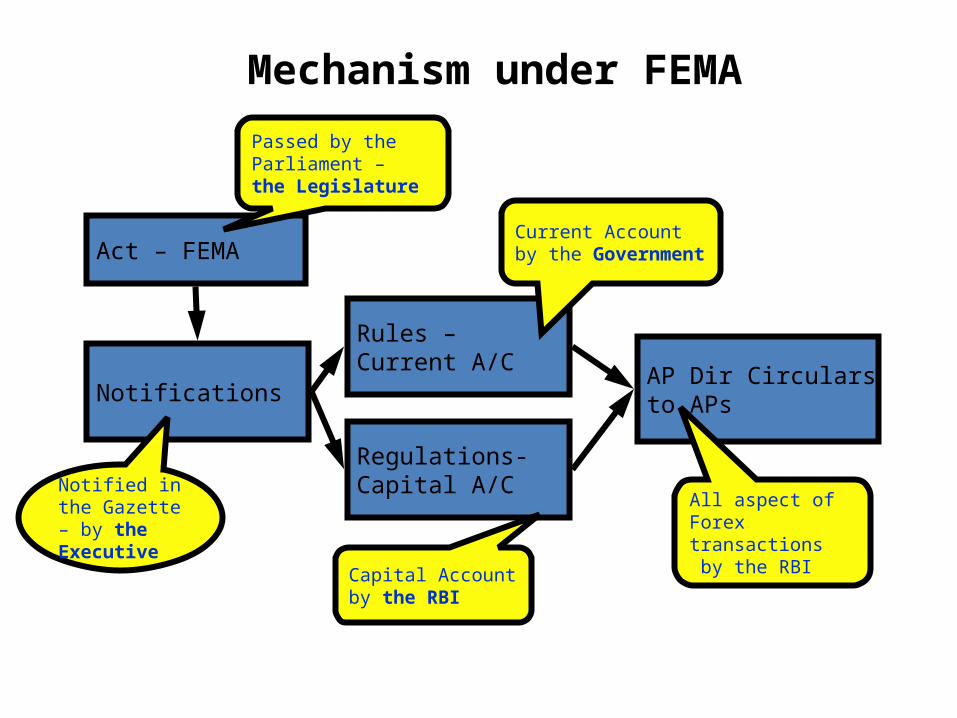

Mechanism under FEMA

Act – FEMA

Notifications

Rules – Current A/C

Regulations- Capital A/C

AP Dir Circulars to APs

Passed by the Parliament – the Legislature

Notified in the Gazette – by the Executive

Current Account by the Government

Capital Account by the RBI

All aspect of Forex transactions by the RBI

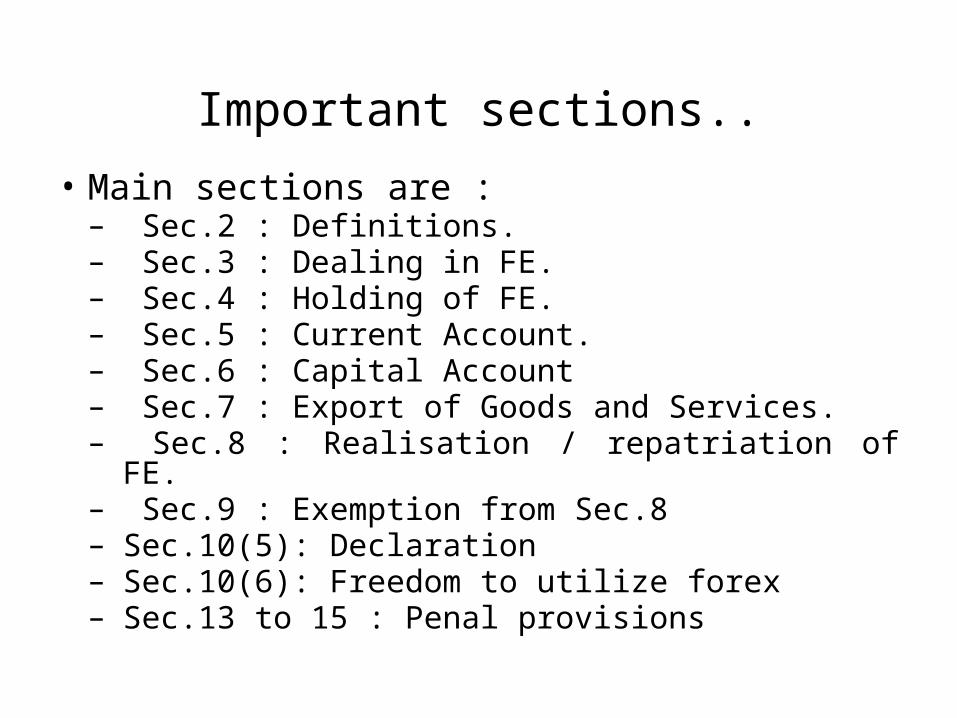

Important sections..• Main sections are :

– Sec.2 : Definitions.– Sec.3 : Dealing in FE.– Sec.4 : Holding of FE.– Sec.5 : Current Account.– Sec.6 : Capital Account– Sec.7 : Export of Goods and Services.– Sec.8 : Realisation / repatriation of FE.– Sec.9 : Exemption from Sec.8– Sec.10(5): Declaration– Sec.10(6): Freedom to utilize forex– Sec.13 to 15 : Penal provisions

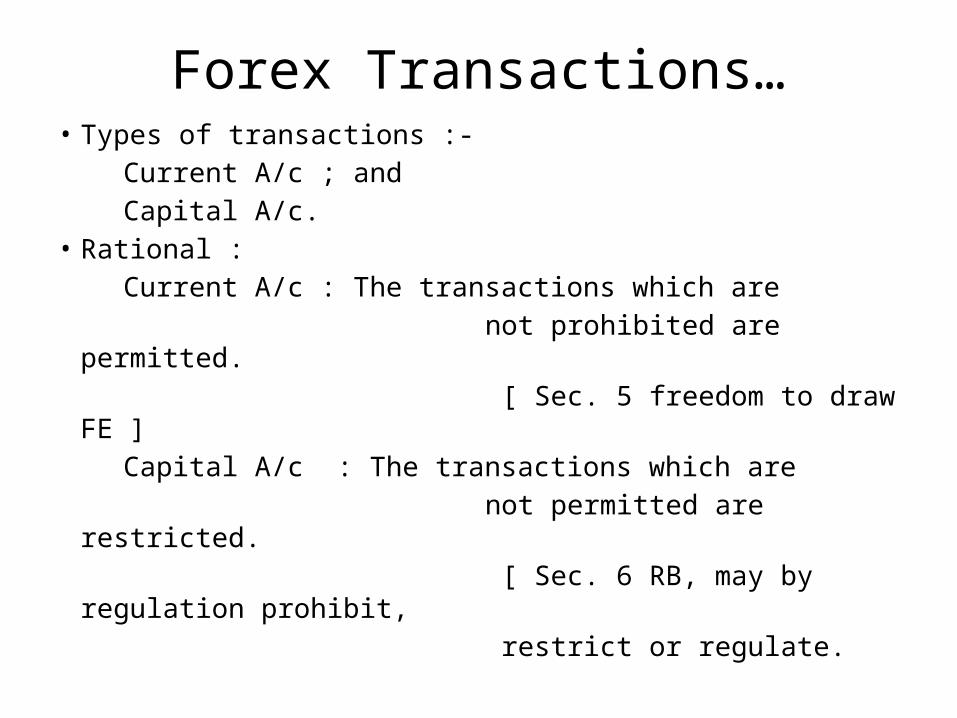

Forex Transactions…• Types of transactions :- Current A/c ; and Capital A/c.• Rational : Current A/c : The transactions which are not prohibited are permitted. [ Sec. 5 freedom to draw FE ] Capital A/c : The transactions which are not permitted are restricted. [ Sec. 6 RB, may by regulation prohibit, restrict or regulate.

Cross Border Investments

• Foreign Direct Investments in India• Overseas Direct Investment by Indians Abroad

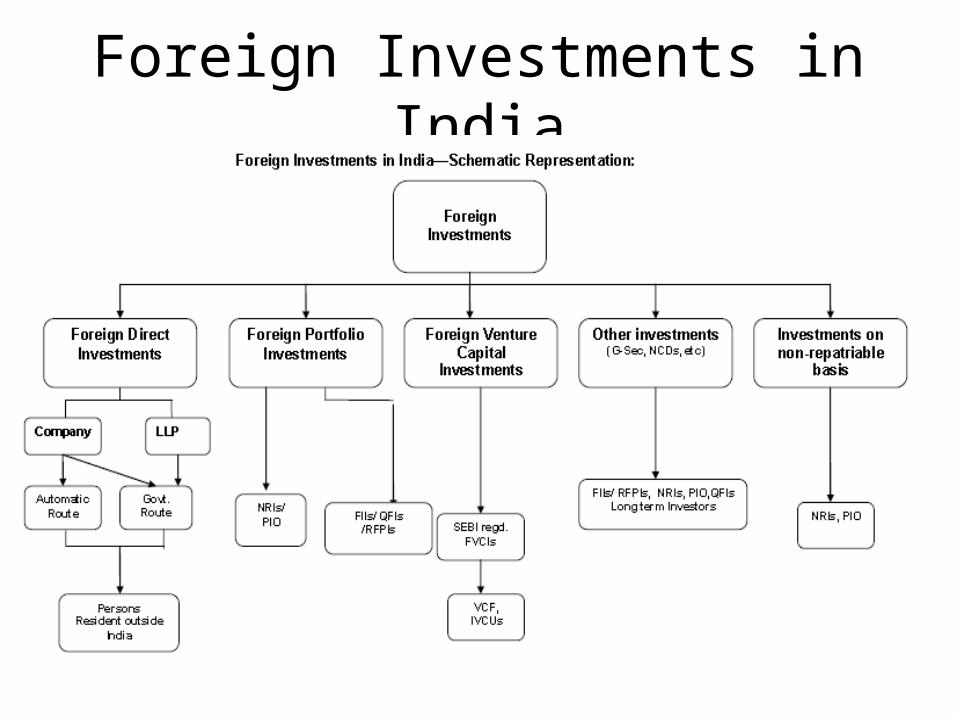

Foreign Investments in India

Compounding of Contraventions

Section II

Contraventions under FEMA

• Contravention is a breach of the provisions of the Foreign Exchange Management Act (FEMA), 1999 and rules/ regulations/ notification/ orders/ directions/ circulars issued there under by RBI.

Compounding of contraventions under FEMA

• Compounding refers to the process of voluntarily admitting the contravention, pleading guilty and seeking redressal.

• The Reserve Bank is empowered to compound any contraventions as defined under section 13 of FEMA, 1999 except the contravention under section 3(a), for a specified sum after offering an opportunity of personal hearing to the contravener.

Compounding of Contraventions under FEMA

• It is a voluntary process in which an individual or a corporate seeks compounding of an admitted contravention.

• It provides comfort to any person who contravenes any provisions of FEMA, 1999 [except section 3(a) of the Act] by minimizing transaction costs.

• Willful, malafide and fraudulent transactions are, however, viewed seriously, which will not be compounded by the Reserve Bank.

Eligibility for applying for Compounding

• Any person who contravenes any provision of the FEMA, 1999 [except section 3(a)] or contravenes any rule, regulation, notification, direction or order issued in exercise of the powers under this Act or contravenes any condition subject to which an authorization is issued by the Reserve Bank, can apply for compounding to the Reserve Bank.

• Applications seeking compounding of contraventions under section 3(a) of FEMA, 1999 may be submitted to the Directorate of Enforcement.

When to apply for Compounding

• When a person is made aware of the contravention of the provisions of FEMA, 1999 by the Reserve Bank or the Foreign Investment Promotion Board (FIPB) or any other statutory authority or the auditors or by any other means, she/he may apply for compounding.

• One can also make an application for compounding, suo moto, on becoming aware of the contravention.

Where to apply?

• The powers to compound contraventions have been vested with the Regional Offices of Foreign Exchange Department(FED), Reserve Bank.

Procedure

• The form given in the annexuret o the A.P.(DIR Series) Circular No. 56 dated June 28, 2010 issued by the Reserve Bank of India, can be used for applying for compounding.

• The same can also be downloaded from the Reserve Bank’s website.

• Further the documents as mentioned in A.P.(DIR) circular nos. 57 and 20 dated December 13, 2011 and August 12, 2013 respectively should also be submitted along with the application.

Fee for Compounding

• The application in the prescribed format along with necessary documents and a demand draft for Rs. 5000/- (Rupees five thousand only) drawn in favour of the “Reserve Bank of India” should be sent to the Reserve Bank of India while sending the request for compounding.

What RBI does with the Application?

• The Reserve Bank makes a scrutiny of the application to verify whether the required details and documents furnished by the applicant are prima-facie in order.

• Applications with incomplete details or where the contravention is not admitted will be returned to the applicant.

• On the admission of applications, the Reserve Bank will examine and decide if the contravention is technical, material or sensitive in nature.

Types of Contraventions

• Technical.• Material. • Sensitive.

What are Sensitive Contraventions?

• The contraventions, prima facie, involving money laundering, national and security concerns involving serious infringement of the regulatory framework, etc., are sensitive contraventions.

• When the issues involved are sensitive / serious in nature they need to be referred to the Directorate of Enforcement (DOE/DRI).

What are Technical Contraventions?

• Whenever a contravention is identified by the Reserve Bank or brought to its notice by the entity involved in contravention by way of a reference other than through the prescribed application for compounding, the Bank will decide if a contravention is technical and/or minor in nature and, as such, can be dealt with by way of an administrative/ cautionary advice.

What are Material Contraventions?

• Material contraventions are those which are required to be compounded for which the necessary compounding procedure has to be followed.

RBI decides on Nature of Contravention

• Whether contravention under the Foreign Exchange Management Act (FEMA) is to be treated as technical and/ or minor or serious would be decided by the Reserve Bank on the merits of the case. The application will be disposed of keeping in view the procedure notified in this regard.

• Persons who have contravened the provisions of FEMA should not take upon themselves suo moto, or on the basis of external advice to decide whether a particular contravention is technical or minor in nature and, hence, no compounding application need be submitted to the Reserve Bank.

Apply to avoid getting penalised

• If such applications for compounding are not made, the person concerned shall expose himself/herself to such action under the provisions of FEMA as the authorities may deem appropriate.

• The persons concerned should, therefore, in their own interest submit their applications for compounding of contravention under FEMA to the Reserve Bank at the earliest opportunity.

The Hearing by RBI

• Personal appearance is not mandatory and the applicant may inform his preference of appearing/not appearing in writing to Compounding Authority (CA).

• Another person may be authorised by the applicant to attend the personal hearing on his behalf but only with proper written authority.

Qualifications of person appearing on behalf of Applicant

• It has to be ensured that the person appearing on behalf of the applicant is conversant with the nature of contravention and the related matters.

• The Reserve Bank encourages the applicant to appear directly for the personal hearing rather than being represented/ accompanied by legal experts/consultants, etc. as the compounding is only for admitted contraventions.

Conclusion of Compounding

• The Compounding Authority passes an order indicating details of the contravention and the provisions of FEMA, 1999 that have been contravened.

• The sum payable for compounding the contravention is indicated in the compounding order.

• The contravention is compounded by payment of the penalty imposed.

Payment of Compounding Charges

• The amount should be paid within 15 days from the date of the order by way of a demand draft drawn on "Reserve Bank of India" and payable at the Regional office which has issued the compounding order and at Mumbai if the order is issued by CEFA (Cell for Effective Implementation of FEMA) , Mumbai.

Completion of Process

• On realization of the sum for which contravention is compounded, a certificate shall be issued by the Reserve Bank indicating that the applicant has complied with the order passed by the Compounding Authority.

Completion of Process

• There cannot be a second adjudication by any authority on the contravention compounded. In terms of FEMA, 1999, where a contravention has been compounded, no proceeding or further proceeding, as the case may be, can be initiated or continued, as the case may be, against the person committing such contravention under that section, in respect of the contravention compounded.

Non Payment of Compounding Charges

• In case of non-payment of the amount indicated in the compounding order within 15 days of the order, it will be treated as if the applicant has not made any compounding application to the Reserve Bank and the other provisions of FEMA, 1999 regarding contraventions will apply. Such cases will be referred to the Directorate of Enforcement for necessary action

Appeal against the order of the Compounding Authority

• As compounding is based on voluntary admissions and disclosures, there is no provision under the Compounding Rules for an appeal against the order of the Compounding Authority or for a request for reduction of amount compounded or extension of period for payment of penalty.

Timeframe for completing the compounding process

• The compounding process is normally completed within 180 days from the date of receipt of the application complete in all aspects, by the Reserve Bank.

Penalties

• Penalty up to thrice the sum involved in such contravention where such amount is quantifiable, or

• Up to two lakh rupees where the amount is not quantifiable, and where such contravention is a continuing one, further penalty which may extend to five thousand rupees for every day after the first day during which the contravention continues.

Penalties

• Any currency, security or any other money or property in respect of which the contravention has taken place shall be confiscated to the Central Government and further direct that the foreign exchange holdings, if any, of the persons committing the contraventions or any part thereof, shall be brought back into India or shall be retained outside India in accordance with the directions made in this behalf.

Transfer Pricing: Recent Developments

Section III

Transfer PricingRegulations

Transfer Pricing

• Transfer pricing is one of the most important issues in international tax.

• Transfer pricing happens whenever two companies that are part of the same multinational group trade with each other: when a India-based subidiary of Coca-Cola, for example, buys something from a French-based subsidiary of Coca-Cola.

• When the parties establish a price for the transaction, this is transfer pricing.

The Arm’s Length principle: Unrelated Parties

• If two unrelated companies trade with each other, a market price for the transaction will generally result.

• This is known as “arms-length” trading, because it is the product of genuine negotiation in a market.

• This arm’s length price is usually considered to be acceptable for tax purposes.

Arm’s Length Principle: Related Parties

• But when two related companies trade with each other, they may wish to artificially distort the price at which the trade is recorded, to minimise the overall tax bill.

• This might, for example, help it record as much of its profit as possible in a tax haven with low or zero taxes.

Case

• A company called India MNC Ltd., which produces a type of food product in India, then processes it and sells the finished product in the United States.

• India MNC Ltd. does this via three subsidiaries: India MNC Ltd. (in India), Haven Inc. (in a tax haven, with zero taxes) and America Inc. (in the United States).

Case

• Now Inc. sells the produce to Haven Inc. at an artificially low price, resulting in India MNC Ltd. having artificially low profits – and consequently an artificially low tax bill in India.

• Then Haven Inc. sells the product to America Inc. at a very high price – almost as high as the final retail price at which America Inc. sells the processed product.

Case

• As a result, America Inc. also has artificially low profitability, and an artificially low tax bill in America.

• By contrast, however, Haven Inc. has bought at a very low price, and sold at a very high price, artificially creating very high profits. However, it is located in a tax haven – so it pays no taxes on those profits.

International Transaction

• Transaction between two or more associated companies situated in different countries in terms of a property that is tangible or intangible, a service offered by the company, or any form of lending of money, etc.

• It is compulsory that at least one of the participants involved in the transaction is a non-resident of India.

Transaction between NRIs

• However, a transaction that has been carried out by two non-resident Indians, where one of them possesses a permanent setup in India and whose income is taxable from India, such a type of transaction is also considered as ‘International Transaction.’

Authorized Person

• Any person who has involved in an international transaction in the previous year shall submit the report in Form 3CEB through a Chartered Accountant, duly verified and certified by him, on or before the date ( i.e. 30th September ( of every year) ) prescribed by the authority, furnishing all the required details .

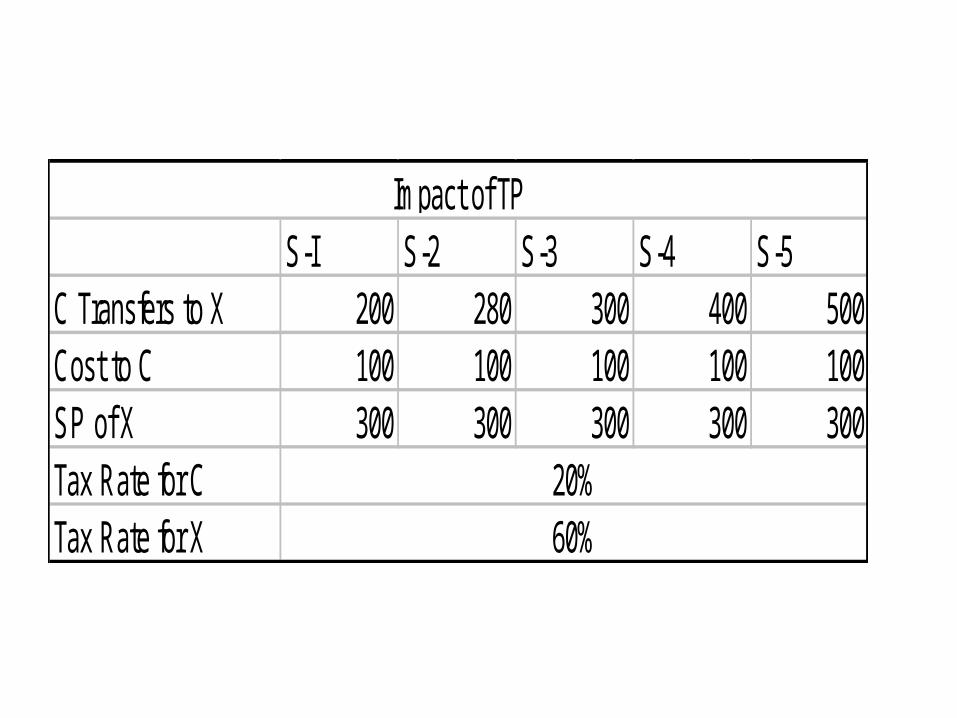

S-I S-2 S-3 S-4 S-5C Transfers to X 200 280 300 400 500Cost to C 100 100 100 100 100SP of X 300 300 300 300 300Tax Rate for CTax Rate for X

Impact of TP

20%60%

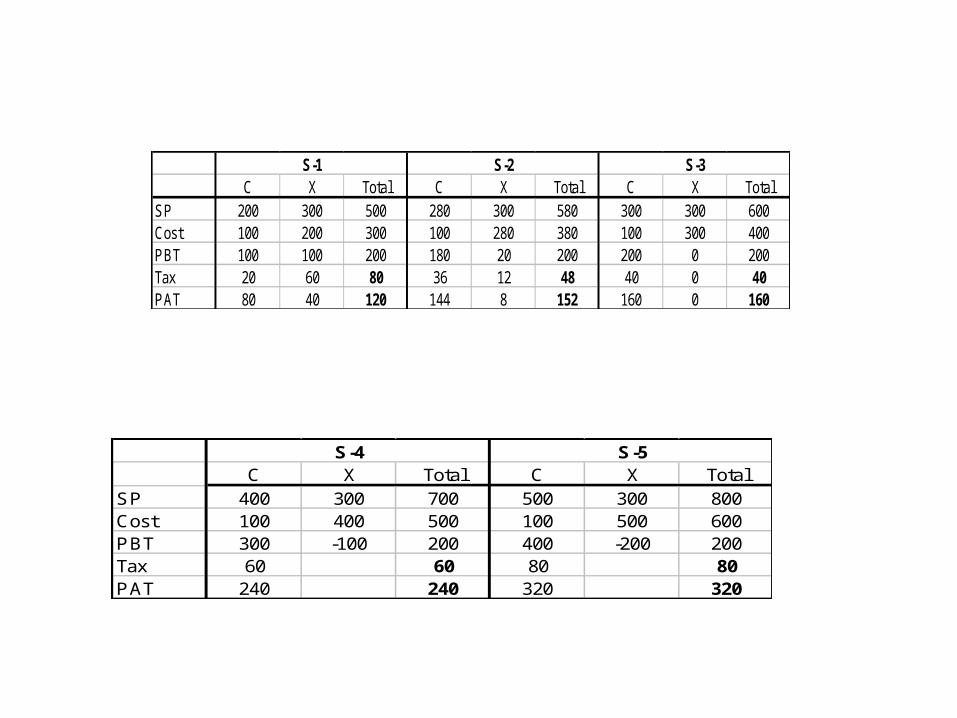

C X Total C X Total C X TotalSP 200 300 500 280 300 580 300 300 600Cost 100 200 300 100 280 380 100 300 400PBT 100 100 200 180 20 200 200 0 200Tax 20 60 80 36 12 48 40 0 40PAT 80 40 120 144 8 152 160 0 160

S-3S-1 S-2

C X Total C X TotalSP 400 300 700 500 300 800Cost 100 400 500 100 500 600PBT 300 -100 200 400 -200 200Tax 60 60 80 80PAT 240 240 320 320

S-4 S-5

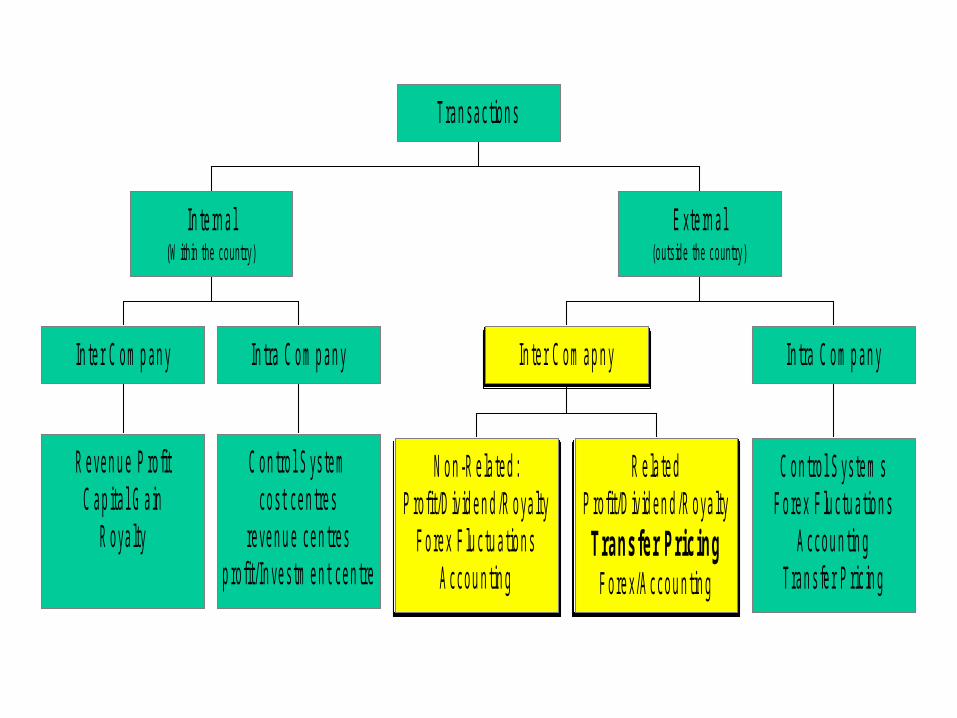

R even u e P ro fitC ap ita l G a in

R oya lty

In te r C om p an y

C on tro l S ys temcos t cen tres

reven u e cen tresp ro fit/ In ves tm en t cen tre

In tra C om p an y

In te rn a l(W ithin the country )

N on -R e la ted :P ro fit/D ivid en d /R oya lty

F orex F lu c tu a tion sA ccou n tin g

R e la tedP ro fit/D ivid en d /R oya lty

T rans fe r Pr ic ingF orex/A ccou n tin g

In te r C om ap n y

C on tro l S ys tem sF orex F lu c tu a tion s

A ccou n tin gTran s fe r P ric in g

In tra C om p an y

E xte rn a l(outs ide the country )

Tran sac tion s

Transfer Price: What and Why?

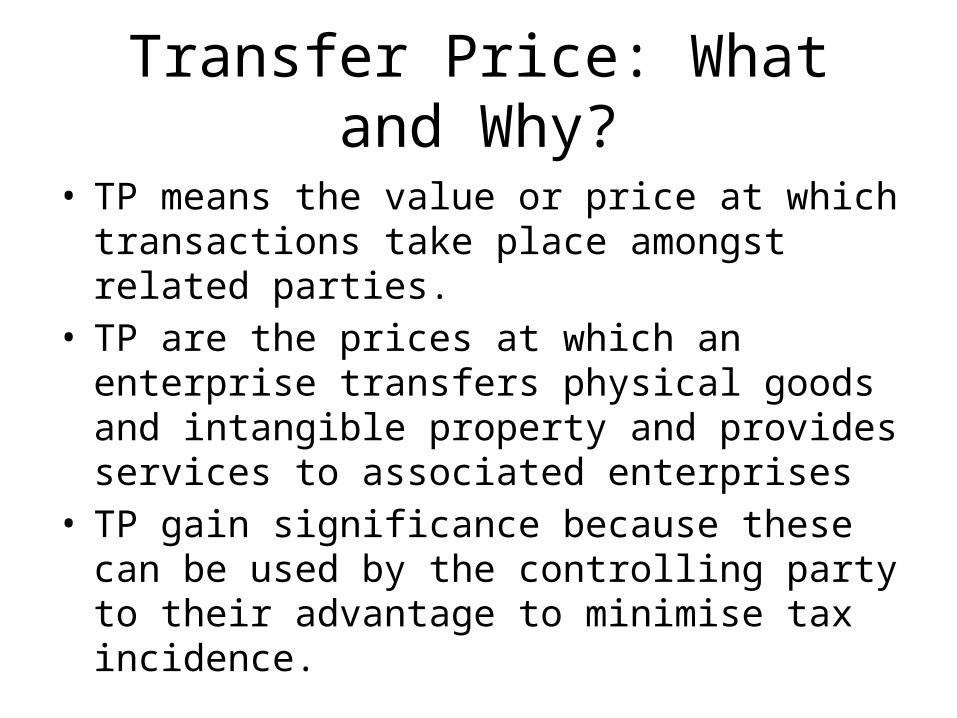

• TP means the value or price at which transactions take place amongst related parties.

• TP are the prices at which an enterprise transfers physical goods and intangible property and provides services to associated enterprises

• TP gain significance because these can be used by the controlling party to their advantage to minimise tax incidence.

Transfer Price: What and Why?

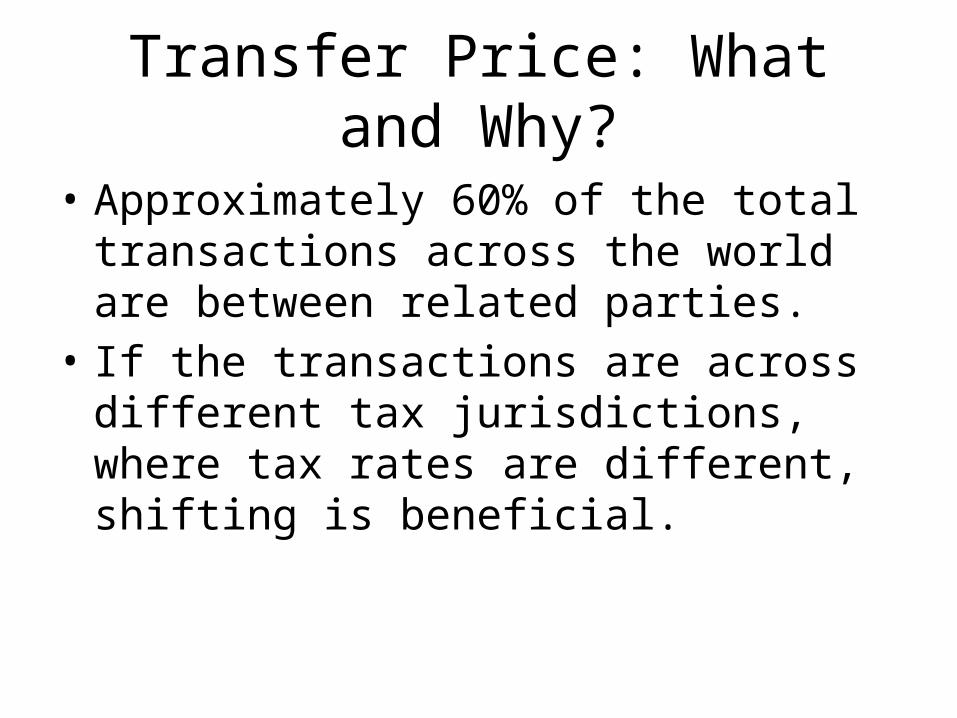

• Approximately 60% of the total transactions across the world are between related parties.

• If the transactions are across different tax jurisdictions, where tax rates are different, shifting is beneficial.

Factors Affecting Transfer Pricing

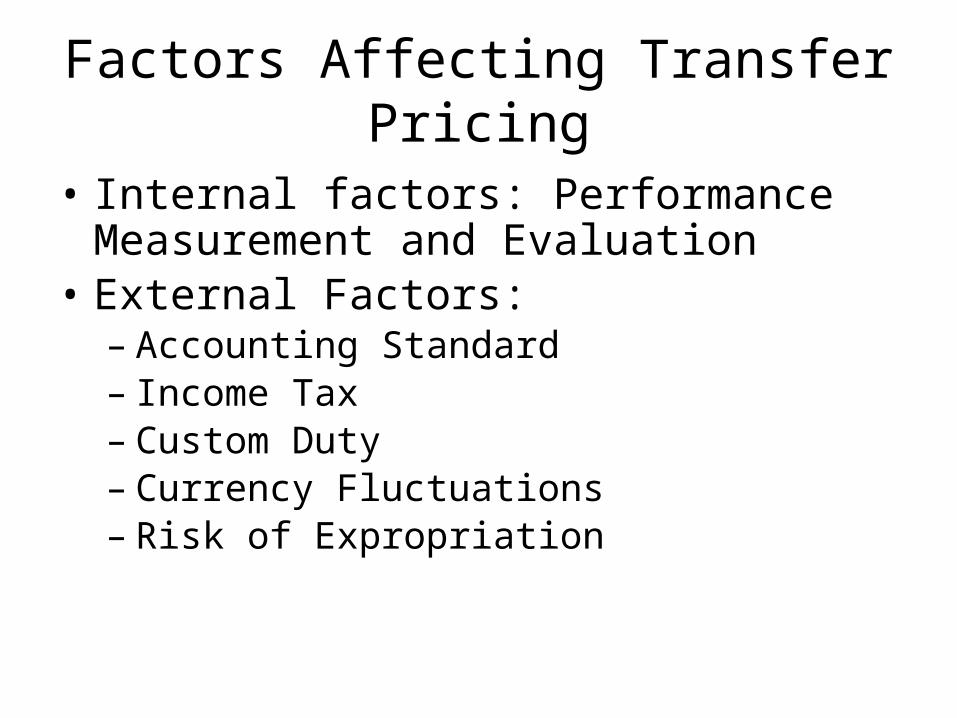

• Internal factors: Performance Measurement and Evaluation

• External Factors:– Accounting Standard– Income Tax – Custom Duty– Currency Fluctuations – Risk of Expropriation

Transfer Price Regulations

International• OECD formulated “Guidelines on transfer

pricing”. They serve as generally accepted practices by the tax authorities

India• The Finance Act 2001 introduced the detailed

TPR w.e.f. 1st April 2001• The Income Tax Act• AS-18• Other Relevant Acts

Accounting Standard 18

Requires disclosure of ‘any elements of the related party transactions necessary for an understanding of the financial statements’.

Related Parties

• Control by ownership– 50% of the voting right

• Control over composition of board of directors– Power to appoint or remove the directors

• Control of substantial interest– 20% or more interest in the voting power

AS-18 and Transactions

• Purchase and sale of goods;• Rendering or receiving services;• Agency arrangements;• Leasing arrangements;• Transfer of research and development;• Licence aggrements;• Finance• Guarantees and collaterals;• Management contracts.

Income Tax Act and TP

• Finance Act 2001 substituted the old section of 92 of the ITA by sections 92,92A to 92 F.

• These sections are the backbone of Indian TPR.

• These sections define the meaning of related parties, international transactions, pricing methodologies etc.

TPR: Some Important Concepts

• Income/Expenses/Cost arising from an international transaction shall be computed having regard to arm’s length price (ALP).

• ALP provisions can be applied if it leads to decrease in taxable income or increase in losses.

Associate Enterprise: 92A

• Direct Control/Control through intermediary• Holding 26% of voting power• Advance of not less than 51% of the total assets of

borrowing company.• Guarantees not less than 10% on behalf of borrower• Appointment of more than 50% of the BoD• Dependence for 90% or more of the total raw

material or other consumables

International Transactions: 92B

• Transaction between two or more AE of which either both or anyone is a non-resident.

• Transactions:– Purchase/Sale/Lease– Provision of service– Lending or borrowing

Arm’s Length Price

• Price which two independent firms would agree on.

• Price which is generally charged in a transaction between persons other than associated enterprises.

Arm’s Length Price: 92C

• Comparable uncontrolled price method• Resale price method• Cost plus method• Profit split method

Comparable uncontrolled price method

• CUP method compares the price transferred in a controlled transaction to the price charged in a comparable un-controlled transaction.

• CUP method is the most direct and reliable way to apply the arm’s length principle.

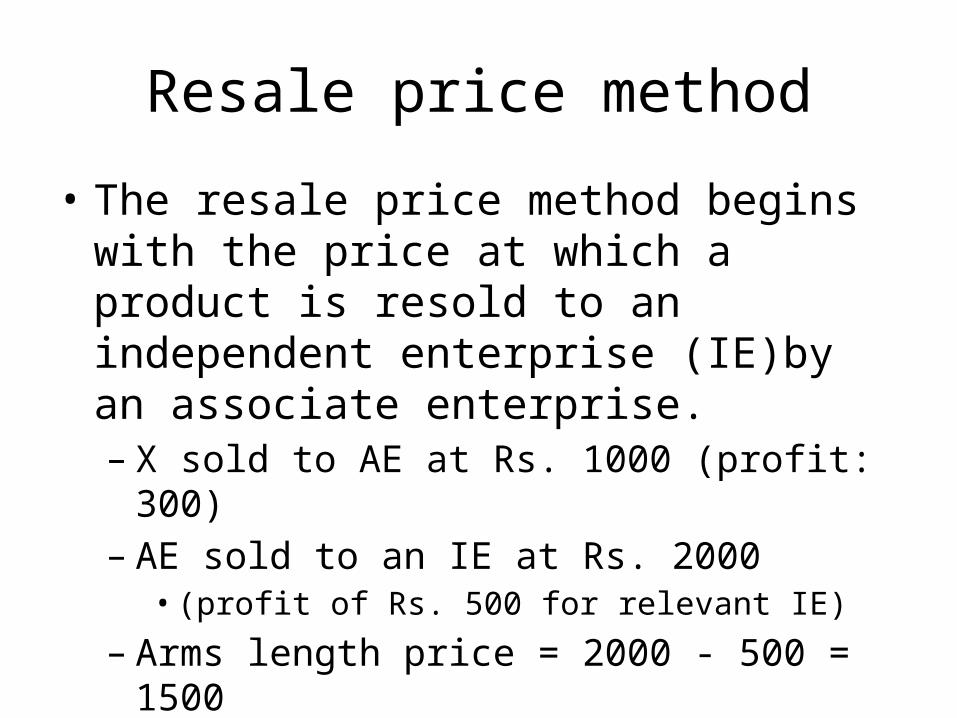

Resale price method

• The resale price method begins with the price at which a product is resold to an independent enterprise (IE)by an associate enterprise.– X sold to AE at Rs. 1000 (profit: 300)– AE sold to an IE at Rs. 2000

• (profit of Rs. 500 for relevant IE)

– Arms length price = 2000 - 500 = 1500

Profit Split Method

• PSM is used when transactions are inter-related and is not possible to evaluate separately.

• PSM first identifies the profit to be split for the AE. The profit so determined is split between the AE on the basis of the functions performed/assets/CE

Cost Plus Method

• In CP method, first the cost incurred is determined. An appropriate cost plus mark-up is then added to the cost to arrive at an appropriate profit. The resultant figure is the arm’s length price.

Some Transactions subject to ALP

• Purchase at little or no cost.

• Payment for services never rendered.

• Sales below MP/ Purchase above MP

• Interest free borrowings

• Exchanging property• Selling of real estate at

a price different from MP

• Use of trade names or patents at exorbitant rates even after their expiry.

Some Cases

• Kinetic Honda Motors– Collaborator: Honda Motor Co. Ltd Japan and

their Subsidiary Honda Trading Corpn. Japan

• Hero Honda Motors Ltd.– Parent: Honda Motor Co. Ltd Japan and their

Subsidiary Honda Trading Corpn. Japan

Some Cases

• Peico Electronics & Electricals Ltd.– Parent: Phillips Netherlands and its subsidiaries

• Asea Brown Boveri– Parent: ABB Switzerland and its subsidiaries

• Videocon Group– Collaborators: Toshiba Co., Mitsubishi Co

Latest Developments in Transfer Pricing

APA Introduced in India

• The concept of Advance Pricing Agreement (APA) has been introduced in India

• The Central Board of Direct Taxes has recently notified advance pricing agreements scheme.

• Given the numerous transfer pricing cases in dispute, introduction of APAs is expected to considerably alleviate the uncertainty regarding arm’s length pricing of international transactions.

APA

• Advance Pricing Agreement (APA) provisions were introduced in the Income-tax Act, 1961 (Act) w.e.f. 1 July 2012.

• The rules in respect of the APA scheme have been notified by the Central Board of Direct Taxes (CBDT) by way of insertion of Rule 10F to Rule 10T and Rule 44GA in the Income-tax Rules, 1962 (Rules).

APA Explained

• Agreement between a tax payer and tax authority determining the transfer pricing methodology for pricing the tax payer’s international transactions for future years.

• The methodology is to be applied for a certain period of time based on the fulfillment of certain terms and conditions (called critical assumptions).

Types of APAs

• Unilateral APA• Bilateral APA (BAPA)• Multilateral APA (MAPA)

Unilateral APA

• Involves only the tax payer and the tax uthority of the country where the tax payer is located.

Bilateral APA

• Involves the tax payer, associated enterprise (AE) of the tax payer in the foreign country, tax authority of the country where the tax payer is located, and the foreign tax authority.

Multilateral APA

• Involves the tax payer, two or more AEs of the tax payer in different foreign countries, tax authority of the country where the tax payer is located, and the tax authorities of AEs.

What is Mutual Agreement Procedure

• MAP is a mechanism laid down in tax treaties to ensure that taxation is in accordance with the tax treaty.

• This can also be invoked when a tax payer suffers or is likely to suffer an adverse action during transfer pricing audit to avoid economic double taxation.

How is APA different?

• APA can be entered into for prospective years. • Tax payers with litigation history may opt to

file MAP in respect of pending disputes and also opt for APA for the same transactions for the future years as an effective dispute resolution/avoidance strategy.

Eligibility for APA

• Any tax payer who has undertaken an international transaction or is contemplating to undertake an international transaction is eligible to file for an APA.

• Any type of international transaction can be covered in an APA.

Advantages of APA

• Removal of an audit threat (minimize rigours of audit), and deliverance of a particular tax outcome based on the terms of the agreement.

• Certainty with respect to tax outcome of the tax payer’s international transactions, by agreeing in advance the arm’s length pricing or pricing methodology (ies) to be applied to the tax payer’s international transactions covered by the APA

Advantages of APA

• Substantial reduction of compliance costs over the term of the APA; and

• APA also reduces cost of administration and also frees scarce resources.

Scope of APA

• All International transactions covered;• Agreed transfer pricing policy;• Determination of arm’s length price including

the transfer pricing methodology to be applied;

• Definition of any relevant term; and Critical assumptions and the conditions, if any, other than that provided in the Act or the Rules.

Methodology

• Pre filing Consultation (even on no name basis)

• Fee to be deposited• Negotiations to be done with CBDT • Finalized APAs to not to be in public domain.• Other provisions of Transfer Pricing Act to

remain operational.

Methodology

• Tax payer will have to comply with all the• provisions including maintenance of transfer

pricing documentation and filing of Form 3CEB.

• Tax authorities will continue with the audit as per the provisions of the Act even while the APA is under negotiation.

Methodology

• On conclusion of APA, tax payer has to revise its return of income for the past years, covered under APA, within three months from the conclusion of APA.

• Tax authorities will complete/amend the audit of revised returns in accordance with the terms of the APA

Further

• In a move to clear ambiguities related to retrospective amendments on transfer pricing, the Finance Minister Arun Jaitley has proposed to set up high level Central Board of Direct Taxes (CBDT) committee to decide on fresh cases arising out of the 2012 amendment of Income Tax (I-T) Act.

More Developments

• Three measures have been introduced on transfer pricing in the Budget — “roll back” provision in advance pricing agreements (APAs), range concept for determining arm’s length price and allowing multiple-year data for comparable analysis.

‘Roll Back’

• Means, If a company and IT Dept. sign an APA agreement right now, its (share pricing) methodology can be applied for solving pending cases upto last four years.

‘Range concept for Arm’s length price’

• A transfer pricing report usually produces a list of companies proposed as comparables.

• The results are often summarised as an interquartile range.• An interquartile range discards the results of the bottom quarter

and top quarter of the results. • The median is the mid-point of the interquartile range. The median

will generally produce a different result to the average of the range being considered.

• In a case where all the comparables being used are more or less equally valid, and there is no reason why the tested company is any better performance wise than those comparables companies, then there is probably nothing wrong with using the interquartile range.

OECD’s Base Erosion & Profit Sharing Action Points

ACTION 1:Address the tax challenges of the digital economy

ACTION 2:Neutralise the effects of hybrid mismatch arrangements

ACTION 3:Strengthen CFC rulesACTION 4:Limit base erosion via interest

deductions and other financial payments

ACTION 5:Counter harmful tax practices more effectively, taking into account transparency and substance

ACTION 6:Prevent treaty abuseACTION 7:Prevent the artificial avoidance of PE

statusACTIONS 8, 9, 10:Assure that transfer pricing

outcomes are in line with value creation