Embed Size (px)

Citation preview

Company Presentation 22 May 2006

Initial Public OfferingJasmine Telecom Systems Public Company Limited

2

Company Background

Jasmine Telecom Systems and its wholly owned subsidiary (Siam Teltech Computer) engage as a system integrator in telecommunications and information technology which categorised into four areas;

Telecom system integration

Computer system integration

Payphones lease

Test equipment distribution

3

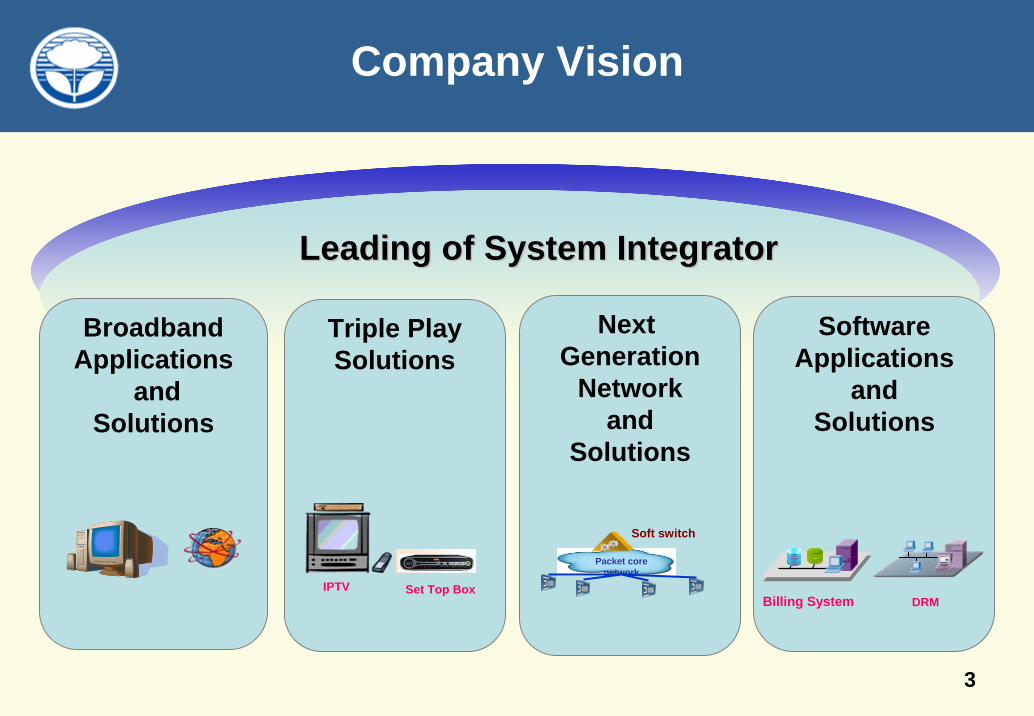

Company Vision

Leading of System IntegratorLeading of System Integrator

Triple PlaySolutions

Next Generation

Networkand

Solutions

BroadbandApplications

andSolutions

SoftwareApplications

andSolutions

Packet core network

Soft switch

IPTV Set Top BoxBilling System DRM

4

Jasmine Telecom Systems Plc.

Section 1 Company Profile

Section 2 Industry Overview

Section 3 Company Business

Section 4 Financial Highlights

Section 5 Investment Highlights

5

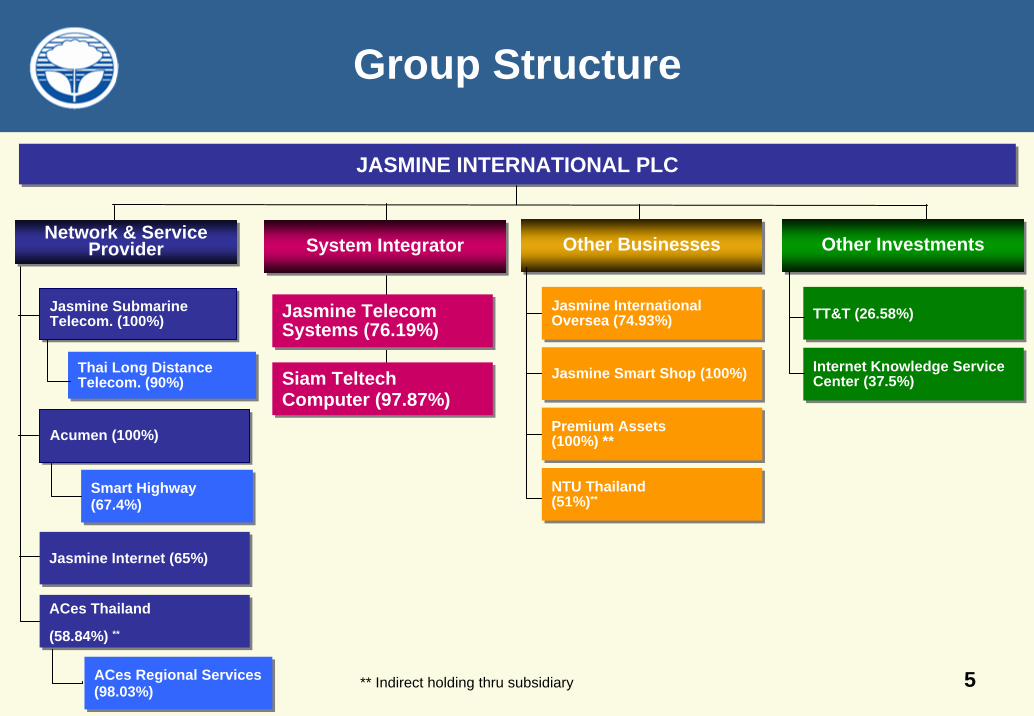

Group Structure

JASMINE INTERNATIONAL PLCJASMINE INTERNATIONAL PLC

Jasmine Submarine Telecom. (100%)Jasmine Submarine Telecom. (100%)

Thai Long Distance Telecom. (90%)Thai Long Distance Telecom. (90%)

Smart Highway (67.4%)Smart Highway (67.4%)

ACes Thailand

(58.84%) **

ACes Thailand

(58.84%) **

Jasmine Internet (65%)Jasmine Internet (65%)

Acumen (100%)Acumen (100%)

Jasmine Telecom Systems (76.19%)Jasmine Telecom Systems (76.19%)

Siam Teltech Computer (97.87%)Siam Teltech Computer (97.87%)

System IntegratorSystem IntegratorNetwork & Service Provider

Network & Service Provider Other BusinessesOther Businesses

Jasmine International Oversea (74.93%)Jasmine International Oversea (74.93%)

Jasmine Smart Shop (100%)Jasmine Smart Shop (100%)

Premium Assets(100%) **Premium Assets(100%) **

Other InvestmentsOther Investments

TT&T (26.58%)TT&T (26.58%)

Internet Knowledge Service Center (37.5%)Internet Knowledge Service Center (37.5%)

NTU Thailand(51%)**NTU Thailand(51%)**

ACes Regional Services (98.03%)ACes Regional Services (98.03%) ** Indirect holding thru subsidiary

6

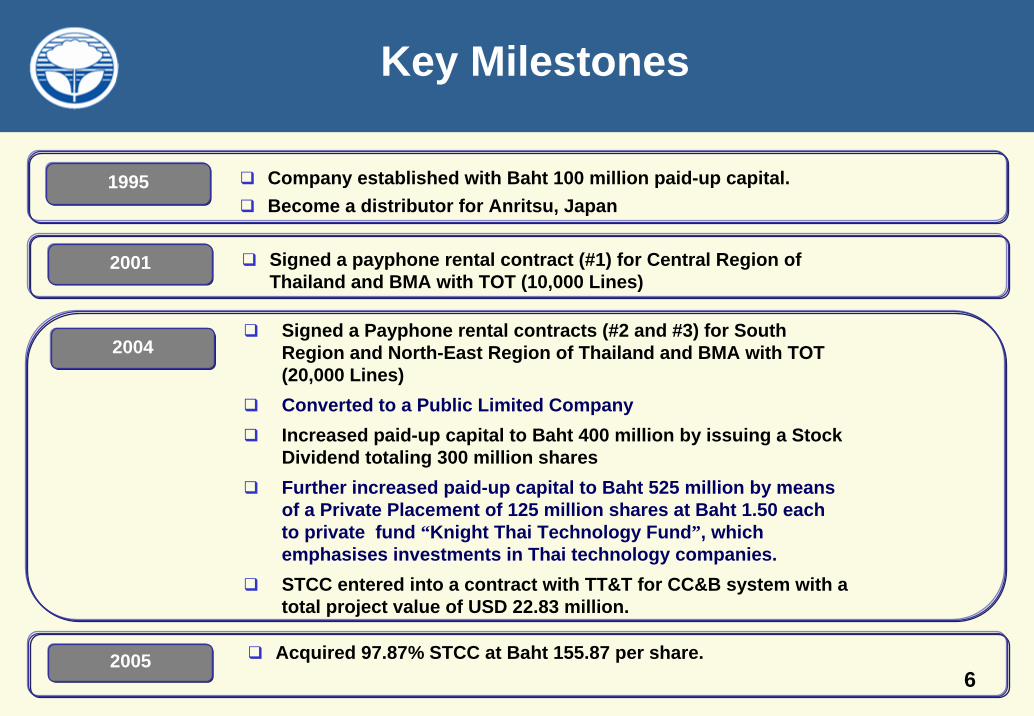

Key Milestones

Company established with Baht 100 million paid-up capital.Become a distributor for Anritsu, Japan

1995

Signed a payphone rental contract (#1) for Central Region of Thailand and BMA with TOT (10,000 Lines)

2001

Acquired 97.87% STCC at Baht 155.87 per share.2005

Signed a Payphone rental contracts (#2 and #3) for South Region and North-East Region of Thailand and BMA with TOT(20,000 Lines)Converted to a Public Limited CompanyIncreased paid-up capital to Baht 400 million by issuing a Stock Dividend totaling 300 million sharesFurther increased paid-up capital to Baht 525 million by meansof a Private Placement of 125 million shares at Baht 1.50 eachto private fund “Knight Thai Technology Fund”, which emphasises investments in Thai technology companies.STCC entered into a contract with TT&T for CC&B system with a total project value of USD 22.83 million.

2004

7

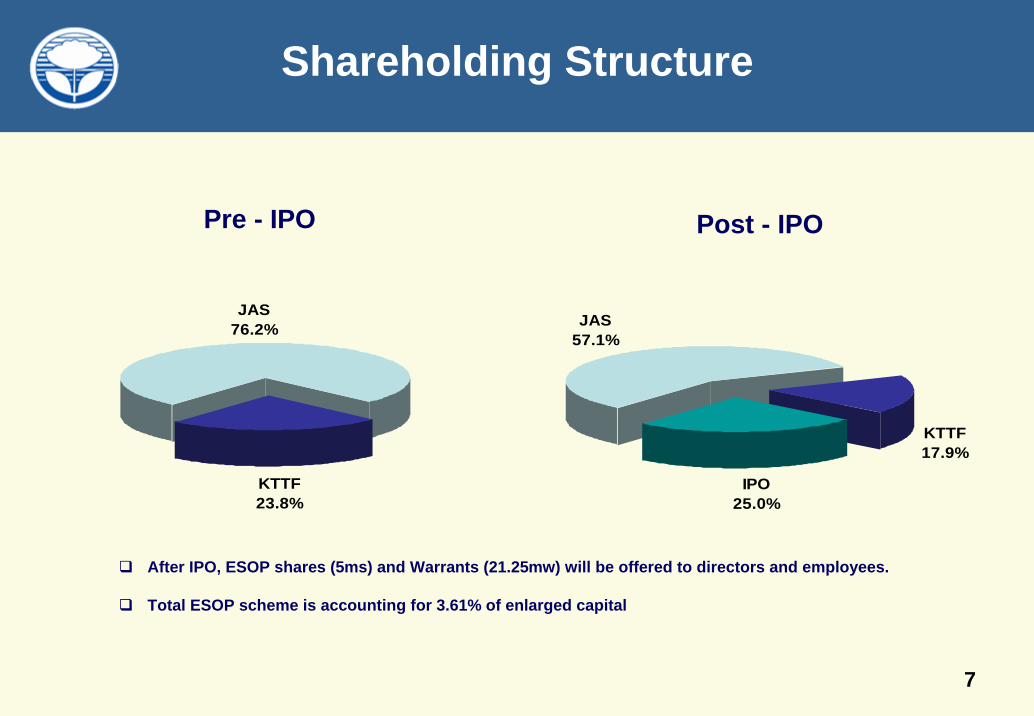

Shareholding Structure

JAS76.2%

KTTF23.8%

JAS57.1%

IPO25.0%

KTTF17.9%

After IPO, ESOP shares (5ms) and Warrants (21.25mw) will be offered to directors and employees.

Total ESOP scheme is accounting for 3.61% of enlarged capital

Pre - IPO Post - IPO

8

Terms and conditions of ESOP

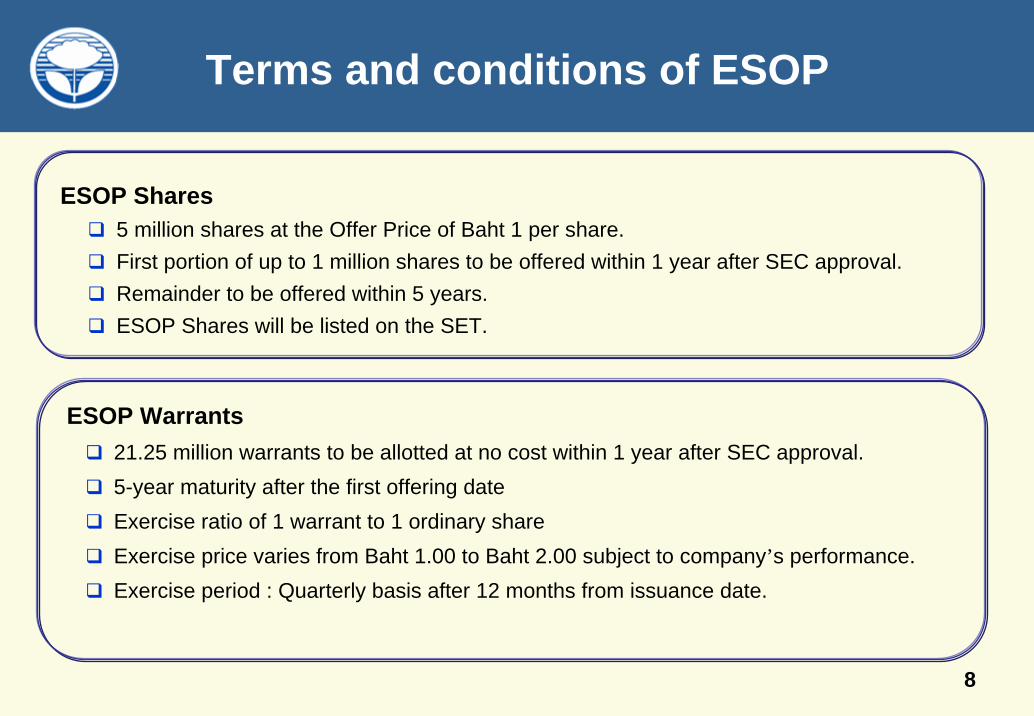

ESOP Shares5 million shares at the Offer Price of Baht 1 per share.First portion of up to 1 million shares to be offered within 1 year after SEC approval.Remainder to be offered within 5 years.ESOP Shares will be listed on the SET.

ESOP Warrants21.25 million warrants to be allotted at no cost within 1 year after SEC approval.5-year maturity after the first offering dateExercise ratio of 1 warrant to 1 ordinary share Exercise price varies from Baht 1.00 to Baht 2.00 subject to company’s performance. Exercise period : Quarterly basis after 12 months from issuance date.

9

Jasmine Telecom Systems Plc.

Section 1 Company Profile

Section 2 Industry Overview

Section 3 Company Business

Section 4 Financial Highlights

Section 5 Investment Highlights

10

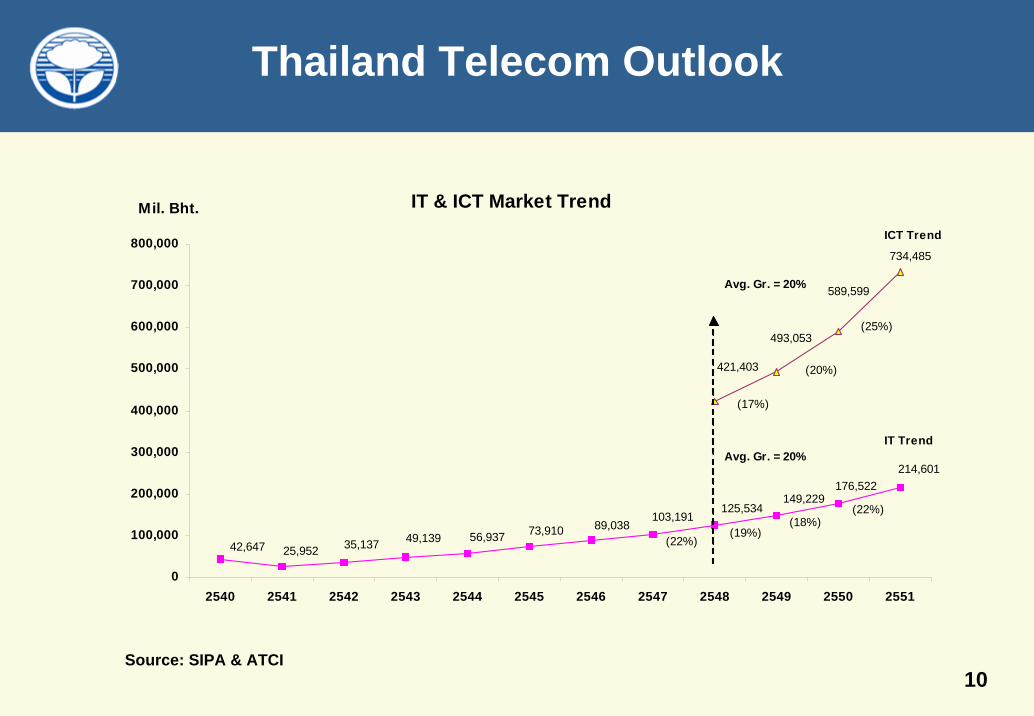

Thailand Telecom Outlook

Source: SIPA & ATCI

IT & ICT Market Trend

214,601176,522

149,229125,534

103,19189,03873,91056,93749,13935,13725,95242,647

734,485

589,599

493,053

421,403

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

2540 2541 2542 2543 2544 2545 2546 2547 2548 2549 2550 2551

Mil. Bht.

(22%)(19%)

(18%)(22%)

(17%)

(20%)

(25%)

ICT Trend

IT Trend

Avg. Gr. = 20%

Avg. Gr. = 20%

11

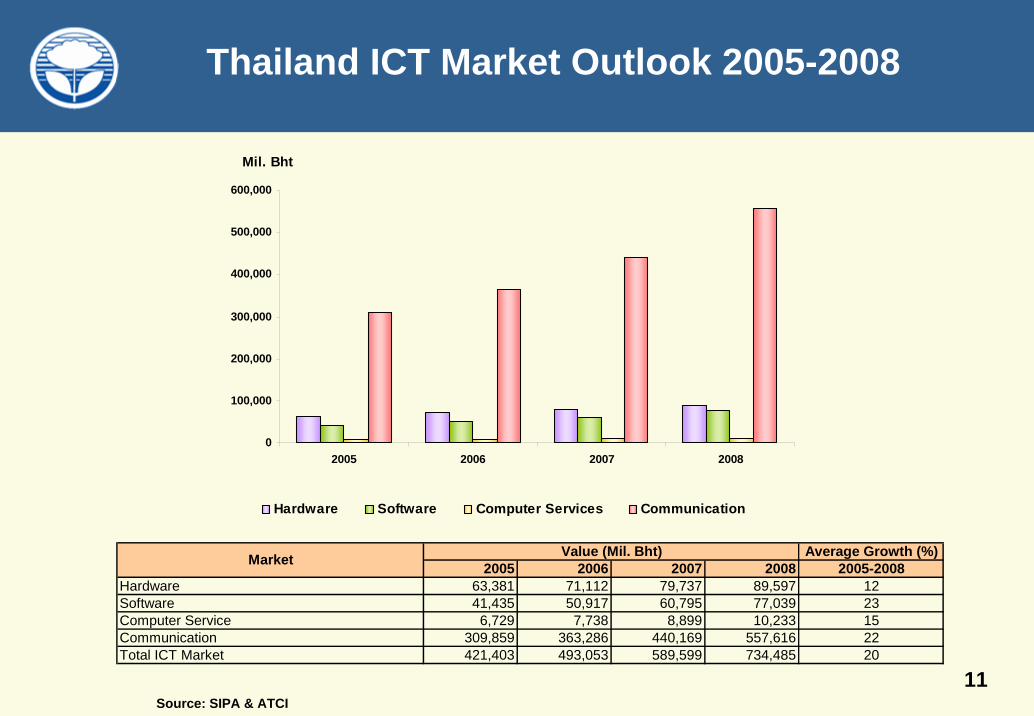

Thailand ICT Market Outlook 2005-2008

Source: SIPA & ATCI

0

100,000

200,000

300,000

400,000

500,000

600,000

2005 2006 2007 2008

Mil. Bht

Hardware Software Computer Services Communication

2005 2006 2007 2008Hardware 63,381 71,112 79,737 89,597Software 41,435 50,917 60,795 77,039Computer Service 6,729 7,738 8,899 10,233Communication 309,859 363,286 440,169 557,616Total ICT Market 421,403 493,053 589,599 734,485 20

12231522

Value (Mil. Bht)Market Average Growth (%)2005-2008

12

0

500

1,000

1,500

2,000

2,500

3,000

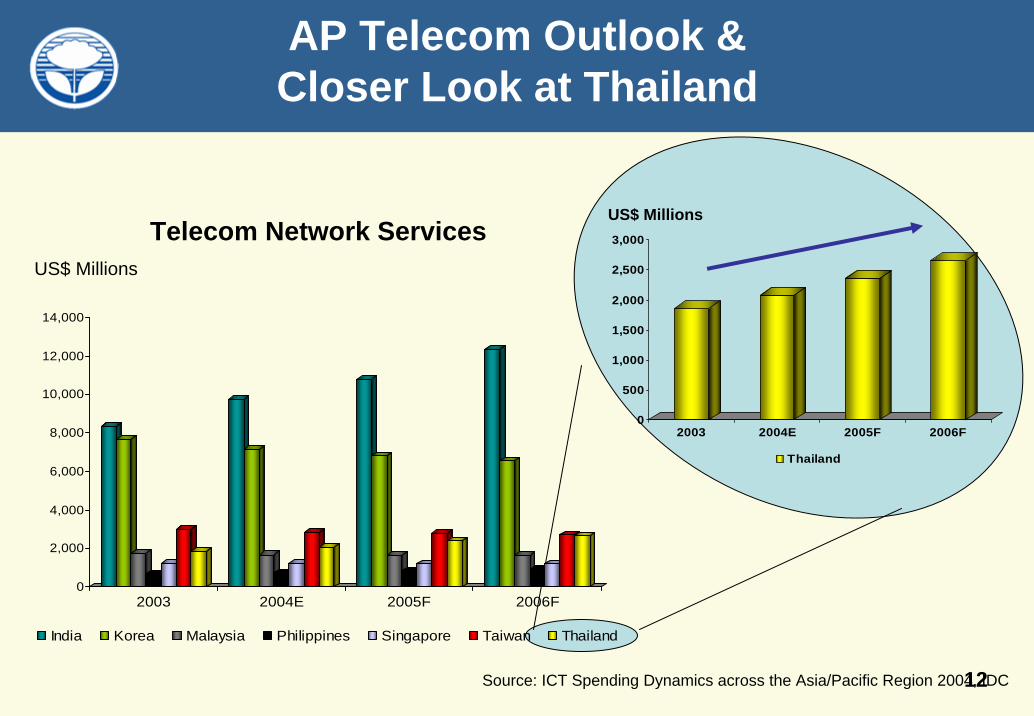

2003 2004E 2005F 2006F

Thailand

US$ Millions

Source: ICT Spending Dynamics across the Asia/Pacific Region 2004, IDC

AP Telecom Outlook & Closer Look at Thailand

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

2003 2004E 2005F 2006F

India Korea Malaysia Philippines Singapore Taiwan Thailand

Telecom Network ServicesUS$ Millions

13

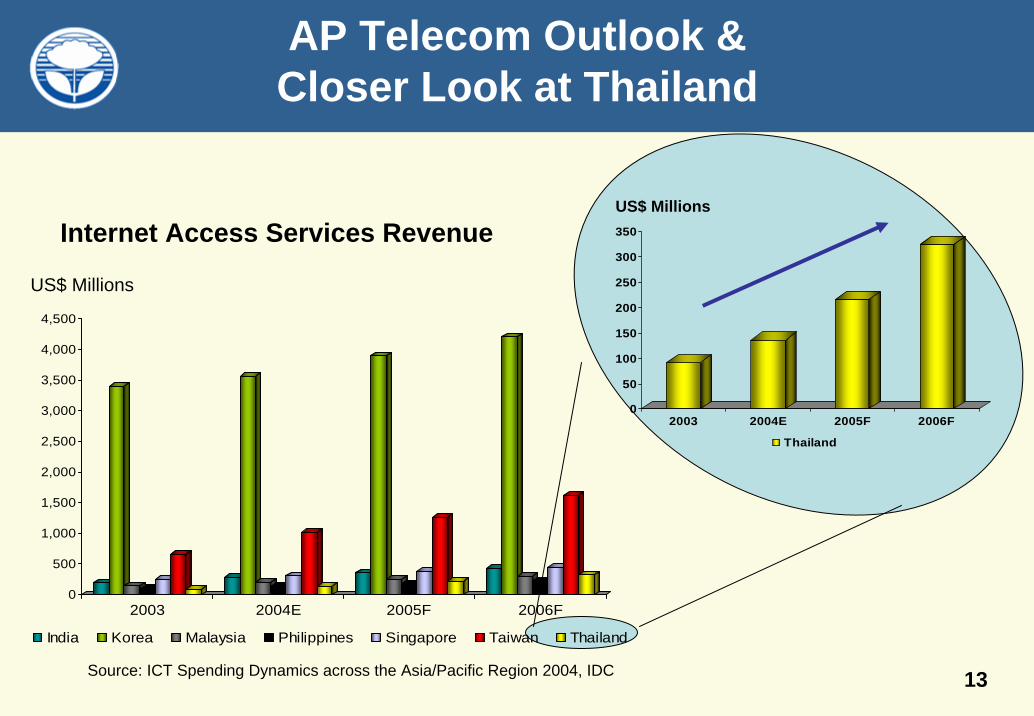

US$ Millions

0

50

100

150

200

250

300

350

2003 2004E 2005F 2006F

Thailand

Source: ICT Spending Dynamics across the Asia/Pacific Region 2004, IDC

Internet Access Services Revenue

US$ Millions

AP Telecom Outlook & Closer Look at Thailand

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

2003 2004E 2005F 2006F

India Korea Malaysia Philippines Singapore Taiwan Thailand

14

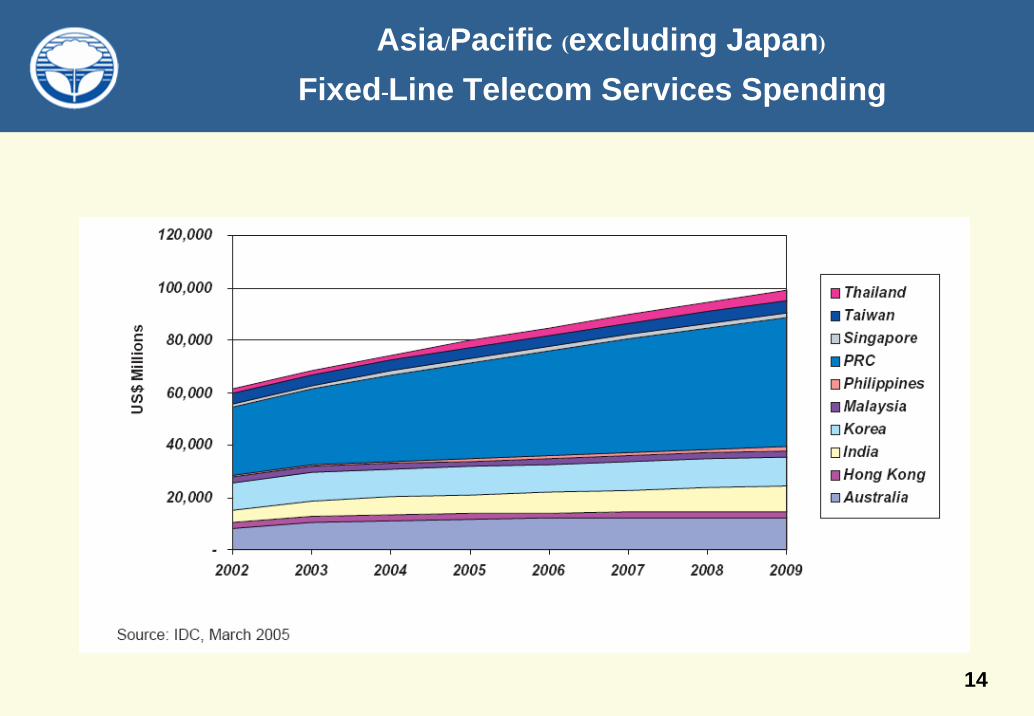

Asia/Pacific (excluding Japan)Fixed-Line Telecom Services Spending

15

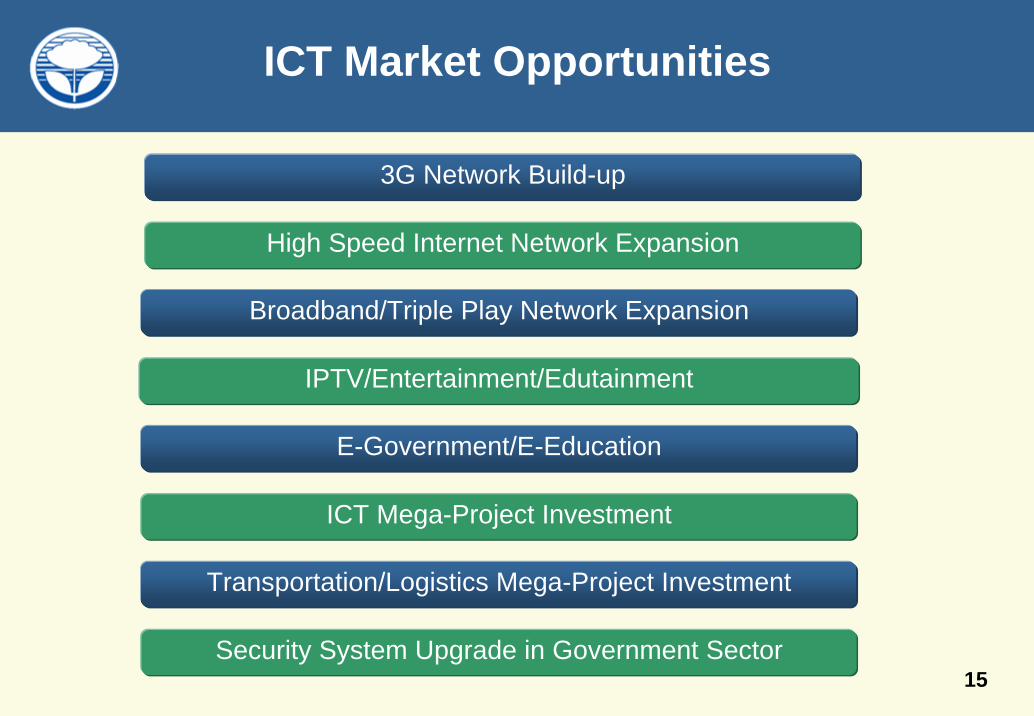

ICT Market Opportunities

3G Network Build-up

High Speed Internet Network Expansion

Broadband/Triple Play Network Expansion

IPTV/Entertainment/Edutainment

E-Government/E-Education

ICT Mega-Project Investment

Transportation/Logistics Mega-Project Investment

Security System Upgrade in Government Sector

16

Jasmine Telecom Systems Plc.

Section 1 Company Profile

Section 2 Industry Overview

Section 3 Company Business

Section 4 Financial Highlights

Section 5 Investment Highlights

17

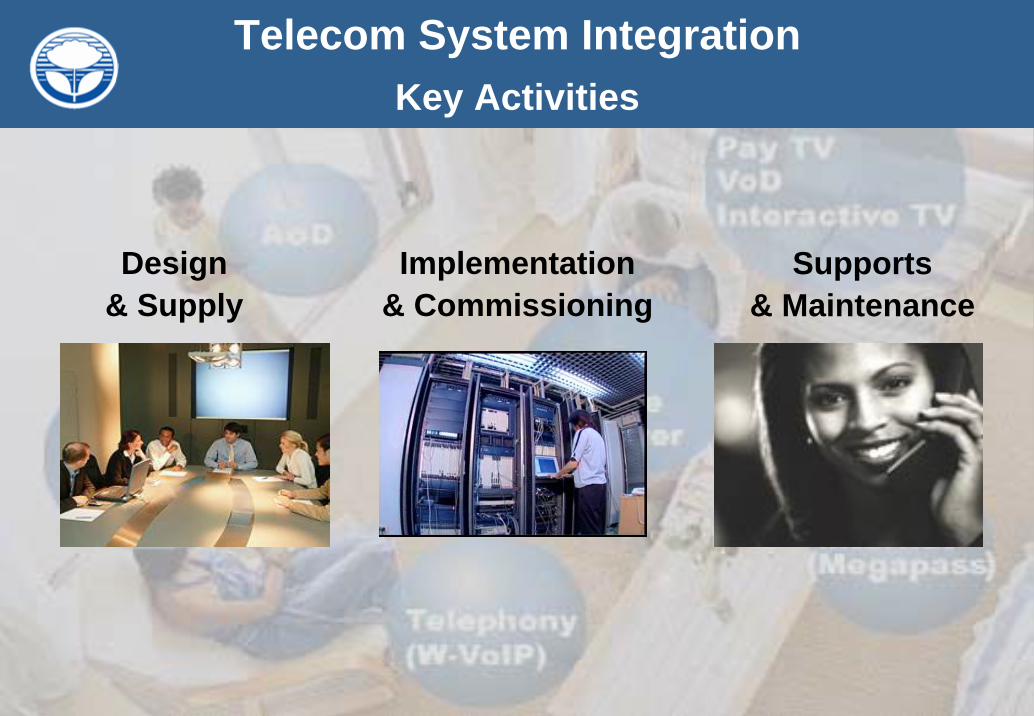

Telecom System IntegrationKey Activities

Design& Supply

Implementation& Commissioning

Supports& Maintenance

18

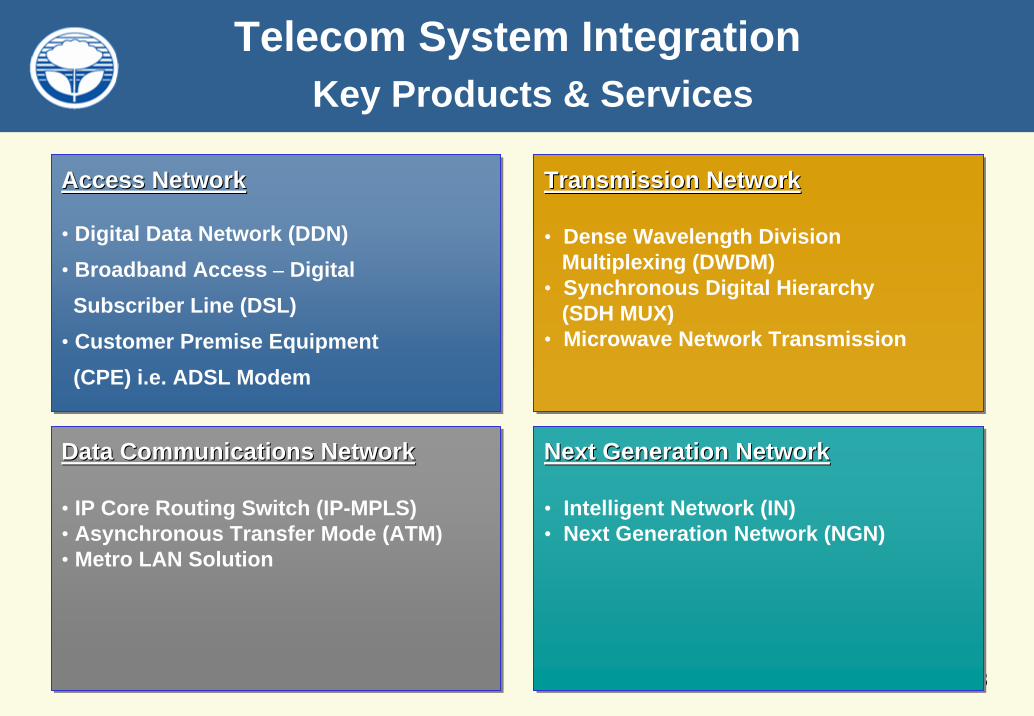

Next Generation Network

• Intelligent Network (IN)• Next Generation Network (NGN)

Next Generation NetworkNext Generation Network

• Intelligent Network (IN)• Next Generation Network (NGN)

Transmission Network

• Dense Wavelength Division Multiplexing (DWDM)

• Synchronous Digital Hierarchy (SDH MUX)

• Microwave Network Transmission

Transmission NetworkTransmission Network

• Dense Wavelength Division Multiplexing (DWDM)

• Synchronous Digital Hierarchy (SDH MUX)

• Microwave Network Transmission

Access Network

• Digital Data Network (DDN)• Broadband Access – Digital

Subscriber Line (DSL)• Customer Premise Equipment

(CPE) i.e. ADSL Modem

Access NetworkAccess Network

• Digital Data Network (DDN)• Broadband Access – Digital

Subscriber Line (DSL)• Customer Premise Equipment

(CPE) i.e. ADSL Modem

Data Communications Network

• IP Core Routing Switch (IP-MPLS)• Asynchronous Transfer Mode (ATM)• Metro LAN Solution

Data Communications NetworkData Communications Network

• IP Core Routing Switch (IP-MPLS)• Asynchronous Transfer Mode (ATM)• Metro LAN Solution

Telecom System Integration Key Products & Services

19

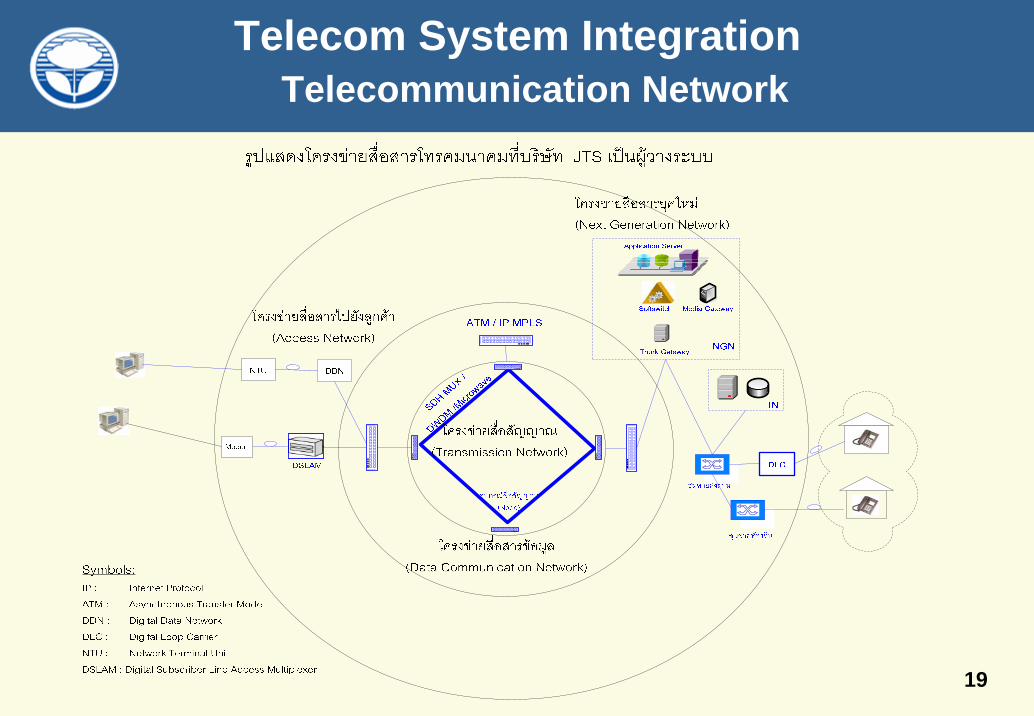

Telecom System Integration Telecommunication Network

21

Telecom System IntegrationKey Customers

Telecom Operators Utilities Transportations

PEA

EGAT

22

Payphone BusinessKey Activities

Supply Installation Supervision Maintenance

23

Payphone BusinessKey Partners

Pragai Siam Lump Sum

Suppliers

Subcontractors

24

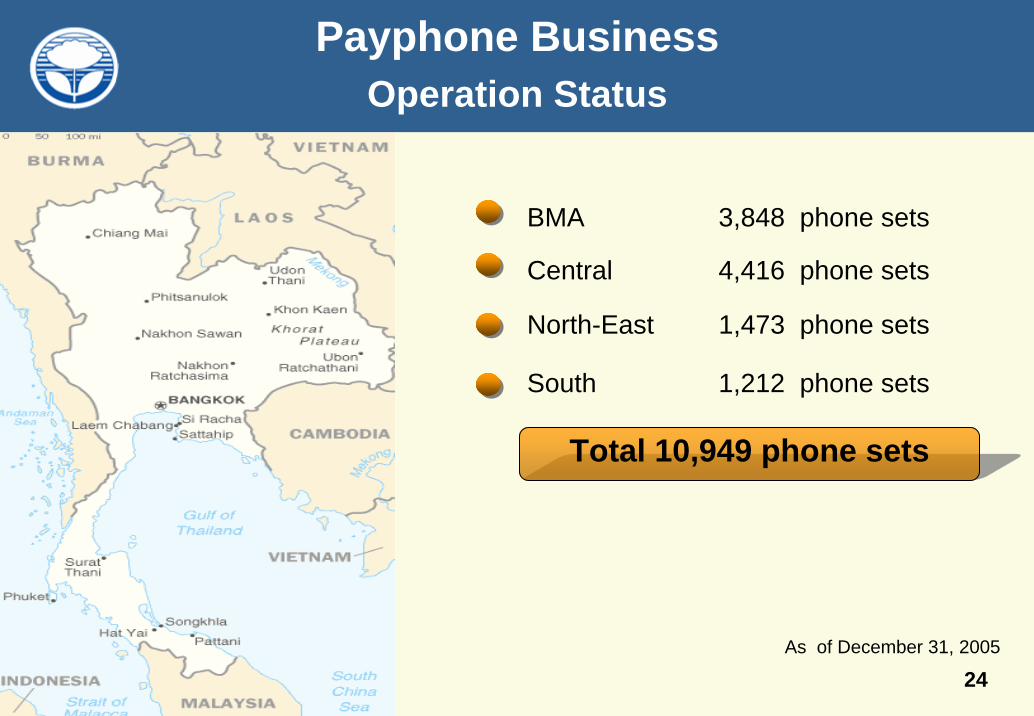

Payphone BusinessOperation Status

As of December 31, 2005

Total 10,949 phone sets

Central 4,416 phone sets

BMA 3,848 phone sets

North-East 1,473 phone sets

South 1,212 phone sets

25

Test Equipment BusinessKey Activities

Marketing & Sales Customer Service Training & Education

26

Test Equipment BusinessKey Partner

The Exclusive Distributor of Anritsu Since 1995The Exclusive Distributor of Anritsu Since 1995

World Class Telecom Test Solutions

27

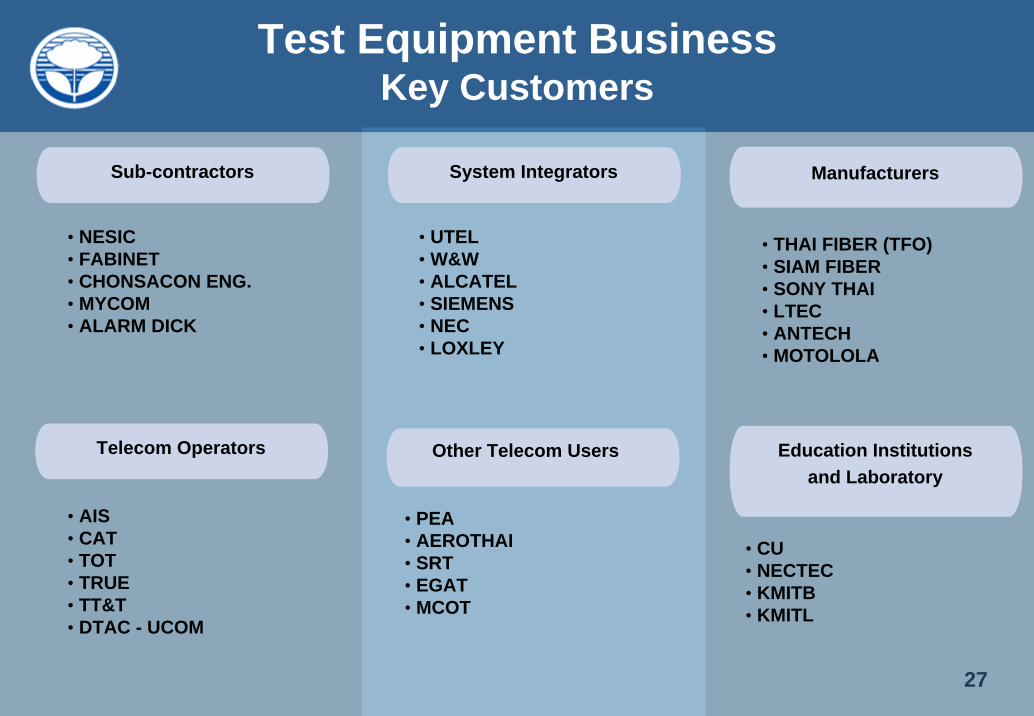

Test Equipment BusinessKey Customers

Sub-contractors

Telecom Operators

• NESIC• FABINET• CHONSACON ENG.• MYCOM• ALARM DICK

• AIS• CAT• TOT• TRUE• TT&T• DTAC - UCOM

Education Institutionsand Laboratory

Other Telecom Users

System Integrators

• UTEL• W&W• ALCATEL• SIEMENS• NEC• LOXLEY

Manufacturers

• THAI FIBER (TFO)• SIAM FIBER• SONY THAI• LTEC• ANTECH• MOTOLOLA

• PEA• AEROTHAI• SRT• EGAT• MCOT

• CU• NECTEC• KMITB• KMITL

28

Computer System IntegrationKey Activities

Design &Supply

Software Development & Customization

Support & Maintenance

Implementation& Commissioning

29

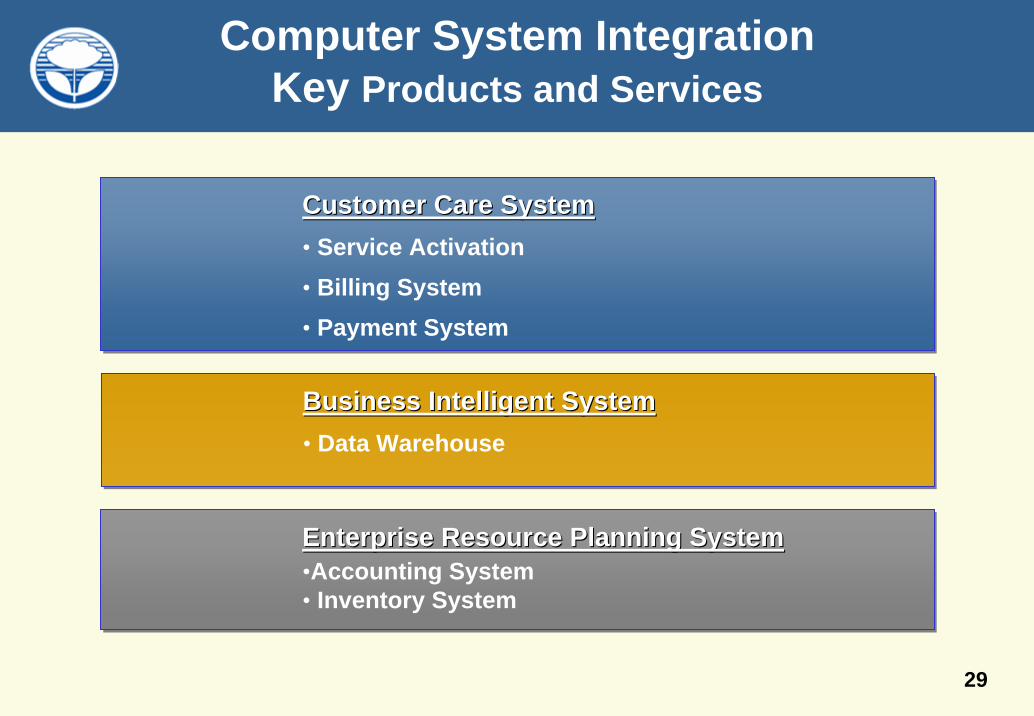

Computer System IntegrationKey Products and Services

Business Intelligent System• Data Warehouse

Business Intelligent SystemBusiness Intelligent System• Data Warehouse

Customer Care System• Service Activation• Billing System• Payment System

Customer Care SystemCustomer Care System• Service Activation• Billing System• Payment System

Enterprise Resource Planning System•Accounting System• Inventory System

Enterprise Resource Planning SystemEnterprise Resource Planning System•Accounting System• Inventory System

30

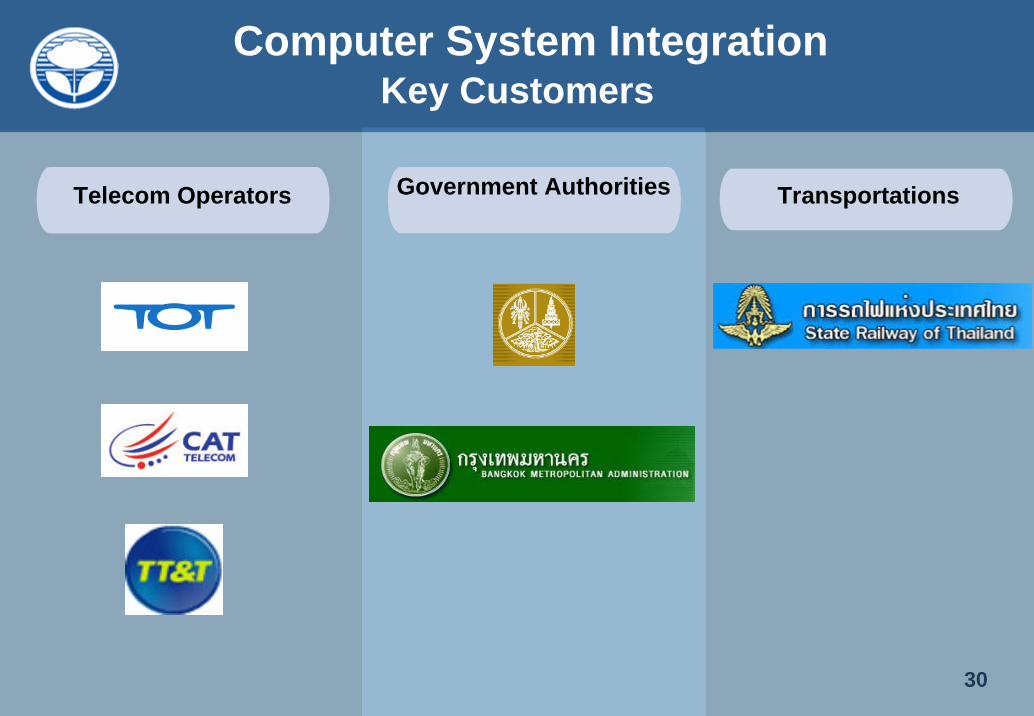

Computer System IntegrationKey Customers

Telecom Operators Government Authorities Transportations

31

Jasmine Telecom Systems Plc.

Section 1 Company Profile

Section 2 Industry Overview

Section 3 Company Business

Section 4 Financial Highlights

Section 5 Investment Highlights

32

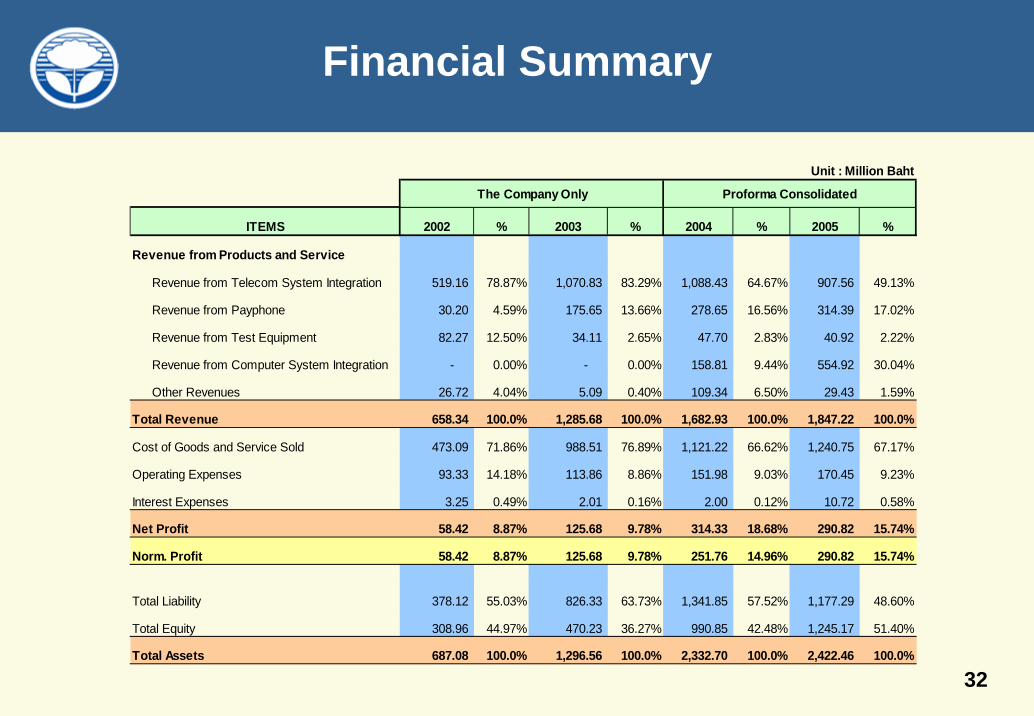

Financial Summary

Unit : Million Baht

The Company Only Proforma Consolidated

ITEMS 2002 % 2003 % 2004 % 2005 %

Revenue from Products and Service

Revenue from Telecom System Integration 519.16 78.87% 1,070.83 83.29% 1,088.43 64.67% 907.56 49.13%

Revenue from Payphone 30.20 4.59% 175.65 13.66% 278.65 16.56% 314.39 17.02%

Revenue from Test Equipment 82.27 12.50% 34.11 2.65% 47.70 2.83% 40.92 2.22%

Revenue from Computer System Integration - 0.00% - 0.00% 158.81 9.44% 554.92 30.04%

Other Revenues 26.72 4.04% 5.09 0.40% 109.34 6.50% 29.43 1.59%

Total Revenue 658.34 100.0% 1,285.68 100.0% 1,682.93 100.0% 1,847.22 100.0%

Cost of Goods and Service Sold 473.09 71.86% 988.51 76.89% 1,121.22 66.62% 1,240.75 67.17%

Operating Expenses 93.33 14.18% 113.86 8.86% 151.98 9.03% 170.45 9.23%

Interest Expenses 3.25 0.49% 2.01 0.16% 2.00 0.12% 10.72 0.58%

Net Profit 58.42 8.87% 125.68 9.78% 314.33 18.68% 290.82 15.74%

Norm. Profit 58.42 8.87% 125.68 9.78% 251.76 14.96% 290.82 15.74%

Total Liability 378.12 55.03% 826.33 63.73% 1,341.85 57.52% 1,177.29 48.60%

Total Equity 308.96 44.97% 470.23 36.27% 990.85 42.48% 1,245.17 51.40%

Total Assets 687.08 100.0% 1,296.56 100.0% 2,332.70 100.0% 2,422.46 100.0%

33

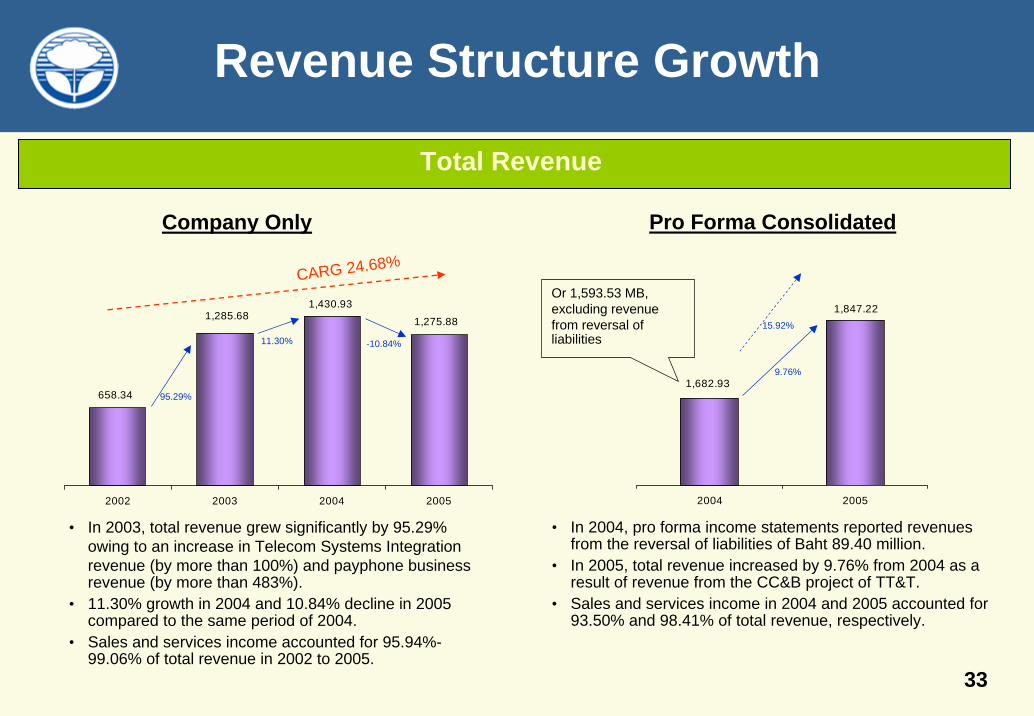

Revenue Structure Growth

1,275.88

1,430.931,285.68

658.34

2002 2003 2004 2005

Total Revenue

Company Only Pro Forma Consolidated

1,847.22

1,682.93

2004 2005

Or 1,593.53 MB, excluding revenue from reversal of liabilities

• In 2004, pro forma income statements reported revenues from the reversal of liabilities of Baht 89.40 million.

• In 2005, total revenue increased by 9.76% from 2004 as a result of revenue from the CC&B project of TT&T.

• Sales and services income in 2004 and 2005 accounted for 93.50% and 98.41% of total revenue, respectively.

• In 2003, total revenue grew significantly by 95.29% owing to an increase in Telecom Systems Integration revenue (by more than 100%) and payphone business revenue (by more than 483%).

• 11.30% growth in 2004 and 10.84% decline in 2005 compared to the same period of 2004.

• Sales and services income accounted for 95.94%-99.06% of total revenue in 2002 to 2005.

CARG 24.68%

95.29%

11.30% -10.84%

9.76%

15.92%

34

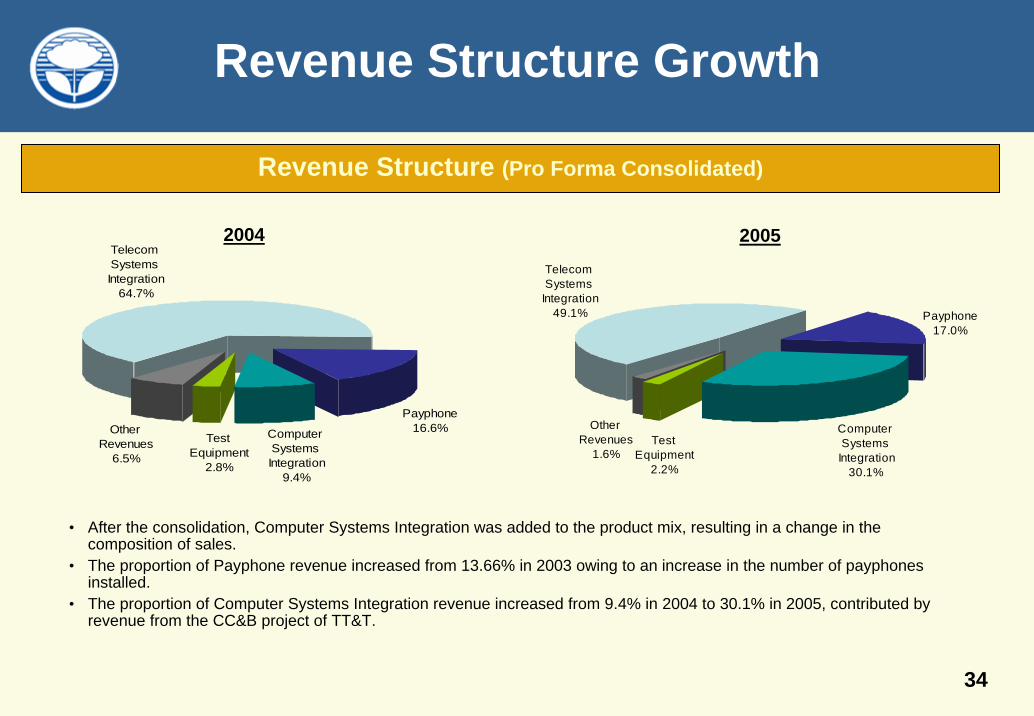

Revenue Structure Growth

Telecom Systems Integration

64.7%

Computer Systems Integration

9.4%

Other Revenues

6.5%

Test Equipment

2.8%

Payphone16.6%

Revenue Structure (Pro Forma Consolidated)

• After the consolidation, Computer Systems Integration was added to the product mix, resulting in a change in the composition of sales.

• The proportion of Payphone revenue increased from 13.66% in 2003 owing to an increase in the number of payphones installed.

• The proportion of Computer Systems Integration revenue increased from 9.4% in 2004 to 30.1% in 2005, contributed by revenue from the CC&B project of TT&T.

Telecom Systems Integration

49.1%

Computer Systems Integration

30.1%

Other Revenues

1.6%Test

Equipment2.2%

Payphone17.0%

2004 2005

35

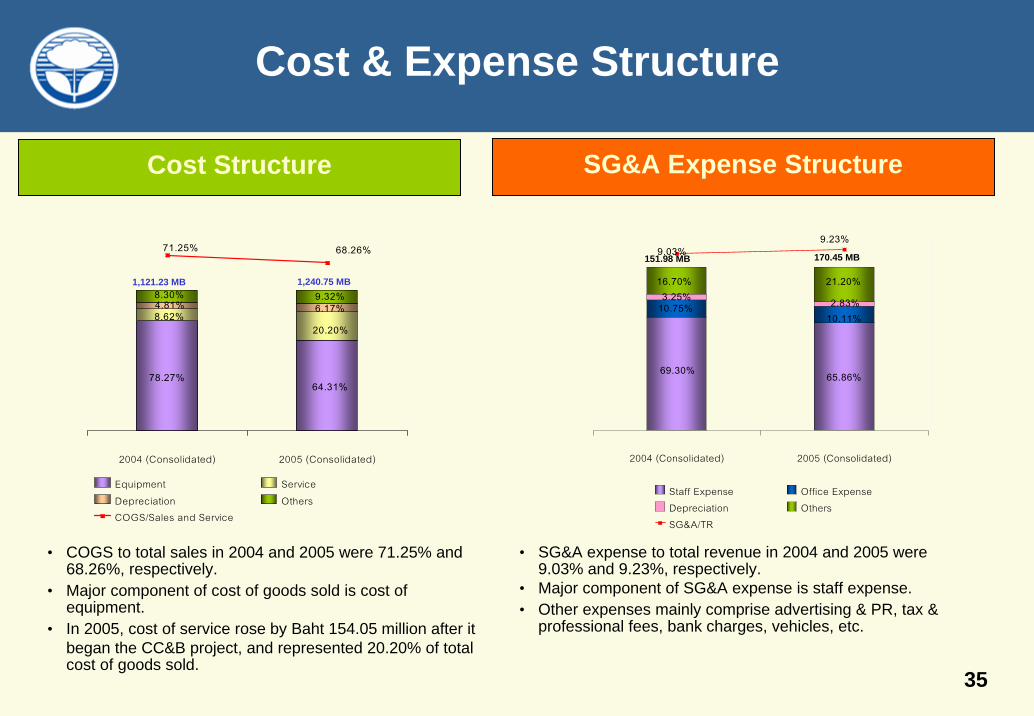

Cost & Expense Structure

Cost Structure

78.27%64.31%

20.20%8.62%

6.17%4.81%8.30% 9.32%

68.26%71.25%

2004 (Consolidated) 2005 (Consolidated)

Equipment ServiceDepreciation OthersCOGS/Sales and Service

1,121.23 MB 1,240.75 MB

• COGS to total sales in 2004 and 2005 were 71.25% and 68.26%, respectively.

• Major component of cost of goods sold is cost of equipment.

• In 2005, cost of service rose by Baht 154.05 million after it began the CC&B project, and represented 20.20% of total cost of goods sold.

SG&A Expense Structure

65.86%69.30%

10.75%10.11%

3.25% 2.83%

21.20%16.70%

9.23%9.03%

2004 (Consolidated) 2005 (Consolidated)

Staff Expense Office ExpenseDepreciation OthersSG&A/TR

151.98 MB 170.45 MB

• SG&A expense to total revenue in 2004 and 2005 were 9.03% and 9.23%, respectively.

• Major component of SG&A expense is staff expense. • Other expenses mainly comprise advertising & PR, tax &

professional fees, bank charges, vehicles, etc.

36

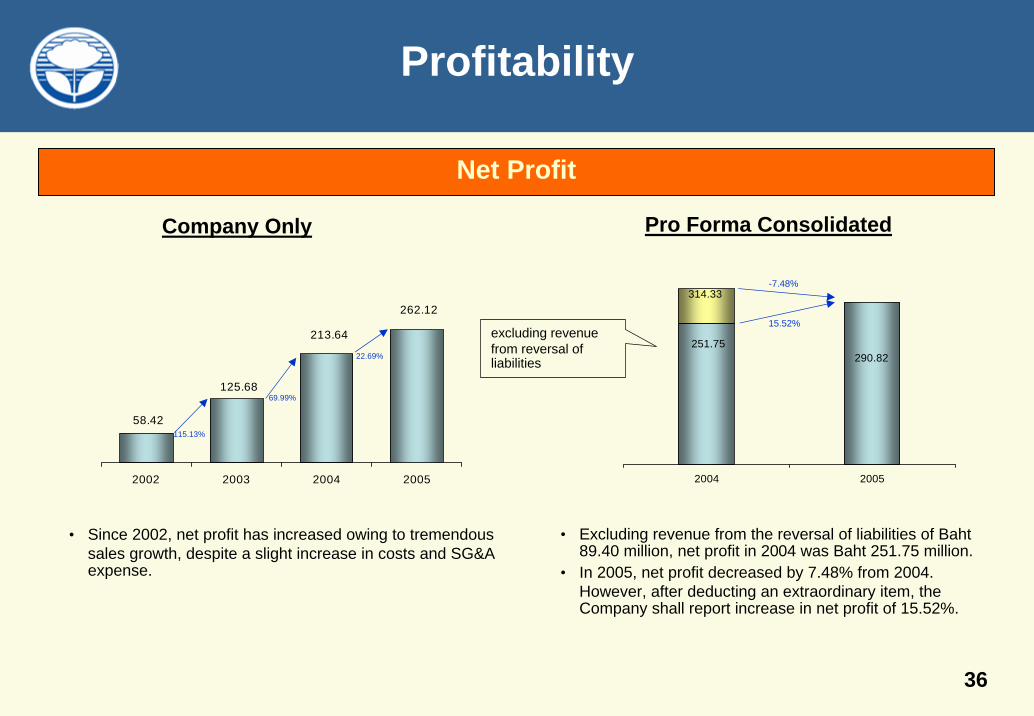

Profitability

251.75290.82

314.33

2004 2005

Net Profit

Company Only Pro Forma Consolidated

• Since 2002, net profit has increased owing to tremendous sales growth, despite a slight increase in costs and SG&A expense.

excluding revenue from reversal of liabilities

• Excluding revenue from the reversal of liabilities of Baht 89.40 million, net profit in 2004 was Baht 251.75 million.

• In 2005, net profit decreased by 7.48% from 2004. However, after deducting an extraordinary item, the Company shall report increase in net profit of 15.52%.

262.12

213.64

58.42

125.68

2002 2003 2004 2005

15.52%

-7.48%

115.13%

69.99%

22.69%

37

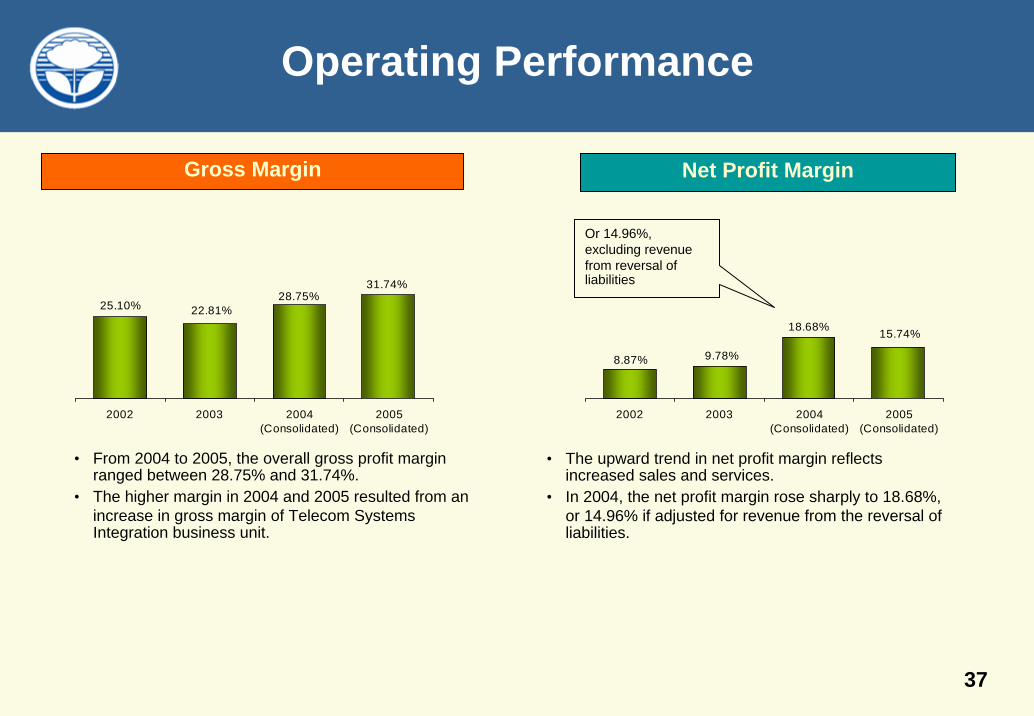

Operating Performance

15.74%18.68%

8.87% 9.78%

2002 2003 2004(Consolidated)

2005(Consolidated)

Net Profit MarginGross Margin

• The upward trend in net profit margin reflects increased sales and services.

• In 2004, the net profit margin rose sharply to 18.68%, or 14.96% if adjusted for revenue from the reversal of liabilities.

Or 14.96%, excluding revenue from reversal of liabilities

• From 2004 to 2005, the overall gross profit margin ranged between 28.75% and 31.74%.

• The higher margin in 2004 and 2005 resulted from an increase in gross margin of Telecom Systems Integration business unit.

31.74%28.75%

25.10% 22.81%

2002 2003 2004(Consolidated)

2005(Consolidated)

38

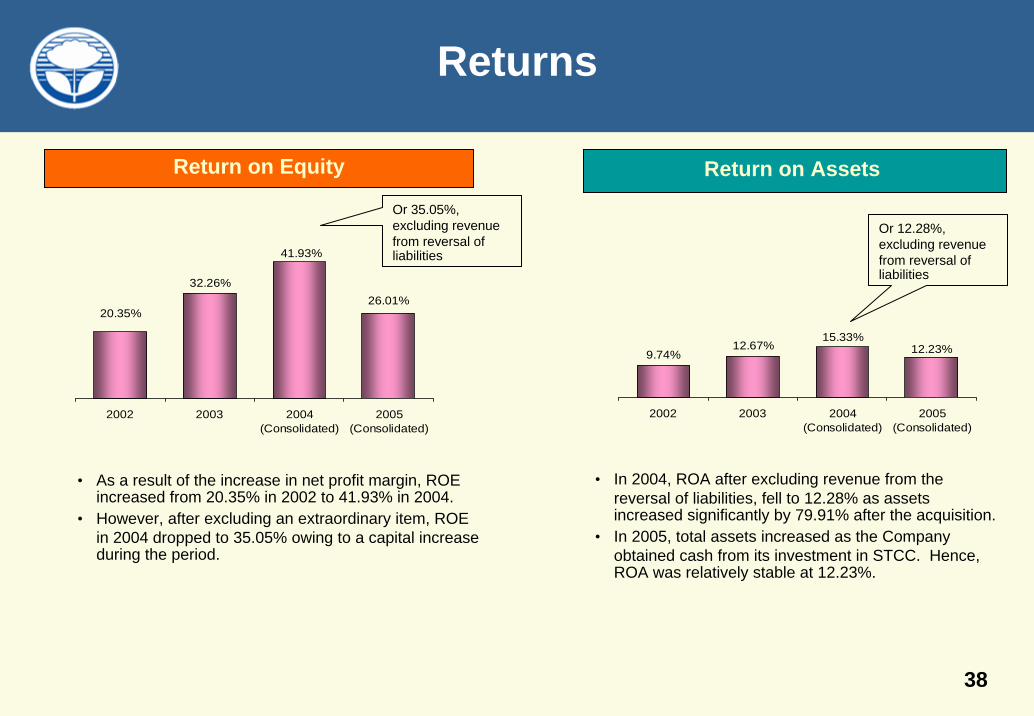

Returns

26.01%

41.93%

20.35%

32.26%

2002 2003 2004(Consolidated)

2005(Consolidated)

Return on AssetsReturn on Equity

• As a result of the increase in net profit margin, ROE increased from 20.35% in 2002 to 41.93% in 2004.

• However, after excluding an extraordinary item, ROE in 2004 dropped to 35.05% owing to a capital increase during the period.

Or 35.05%, excluding revenue from reversal of liabilities

Or 12.28%, excluding revenue from reversal of liabilities

• In 2004, ROA after excluding revenue from the reversal of liabilities, fell to 12.28% as assets increased significantly by 79.91% after the acquisition.

• In 2005, total assets increased as the Company obtained cash from its investment in STCC. Hence, ROA was relatively stable at 12.23%.

12.23%15.33%

9.74%12.67%

2002 2003 2004(Consolidated)

2005(Consolidated)

39

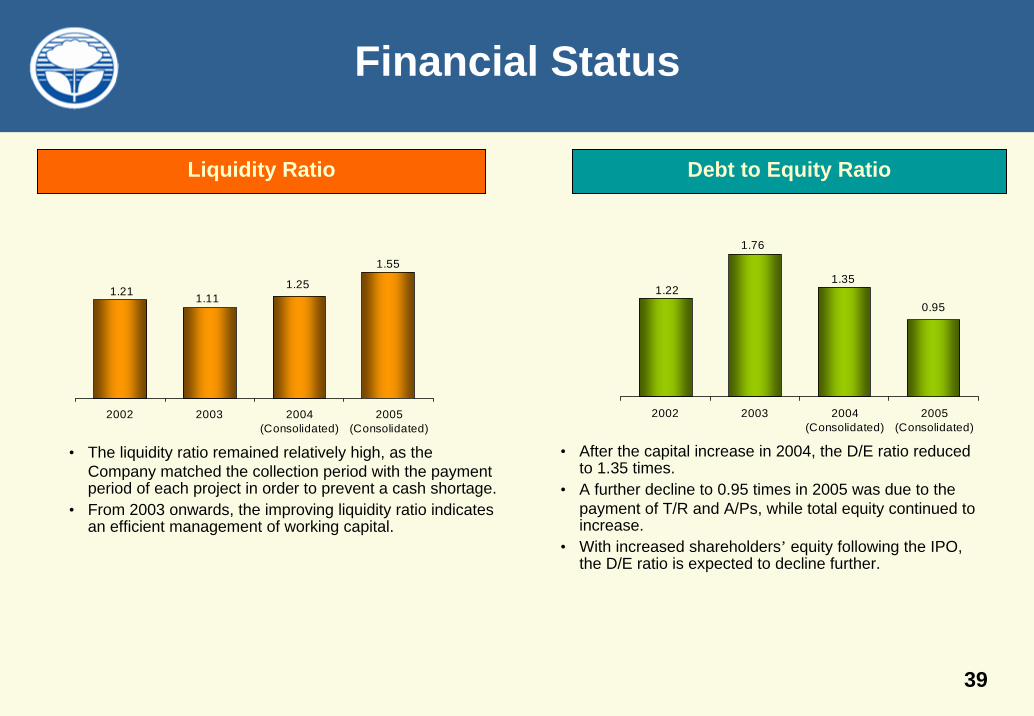

Financial Status

1.55

1.251.21 1.11

2002 2003 2004(Consolidated)

2005(Consolidated)

Debt to Equity RatioLiquidity Ratio

• The liquidity ratio remained relatively high, as the Company matched the collection period with the payment period of each project in order to prevent a cash shortage.

• From 2003 onwards, the improving liquidity ratio indicates an efficient management of working capital.

• After the capital increase in 2004, the D/E ratio reduced to 1.35 times.

• A further decline to 0.95 times in 2005 was due to the payment of T/R and A/Ps, while total equity continued to increase.

• With increased shareholders’ equity following the IPO, the D/E ratio is expected to decline further.

0.95

1.351.22

1.76

2002 2003 2004(Consolidated)

2005(Consolidated)

40

Jasmine Telecom Systems Plc.

Section 1 Company Profile

Section 2 Industry Overview

Section 3 Company Business

Section 4 Financial Highlights

Section 5 Investment Highlights

41

Investment Highlights

One of Market leader in ICT systems integration business

Expertise in implementation and management of large-scale turnkey Telecom and Computer projectsBusiness partnership with world-class suppliersMajor supplier of rented payphones for TOTExclusive distributor of Anritsu test equipment in ThailandBusiness with strong market position and highly attractive fundamentals

Sustainable growing ICT market CAGR 20% 2005 to 2008F – large market/high volume

Low debt/high cash position, proceeds of IPO directly to expand its business and large projects; stable dividend payable policyDiversified risk through several business

42

Offering Summary

Paid-up capital Baht 700 million after IPOPaid-up capital Baht 700 million after IPO

IPO Shares 175 million shares - 87.5 ms for Institutional investors (50%)- 52.5 ms for retail investors (30%)- 35 ms for Sponsor (20%)

IPO Shares 175 million shares - 87.5 ms for Institutional investors (50%)- 52.5 ms for retail investors (30%)- 35 ms for Sponsor (20%)

Secondary Market The Stock Exchange of ThailandSecondary Market The Stock Exchange of Thailand

Sector Technology / Communication sectorSector Technology / Communication sector

43

Tentative Timetables

Last day of Book Build 25 May 2006Last day of Book Build 25 May 2006

Road show 4 to 16 May 2006 Road show 4 to 16 May 2006

Final price determined 26 May 2006Final price determined 26 May 2006

IPO period 5 to 7 June 2006IPO period 5 to 7 June 2006

Listing date W 3 of June 2006Listing date W 3 of June 2006

Thank you Jasmine Telecom Systems Plc.