Embed Size (px)

Citation preview

SHARING KNOWLEDGE. GROWING IMPACT.

cfinsights.org

© CF Insights 2015

Community Foundation

Business Models

Prepared for:

FAOG Conference 2015

October 12, 2015

the IDEA BEHIND

IS SIMPLE

What if EACH community

foundation could know what

ALL community foundations

collectively know?

“Strengthen the social sector by

advancing knowledge about

philanthropy in the U.S. and around

the world.”

Reflecting On Over 10 Years

2006-2010 2004-2006

Center for

Financial

Insights

IMAGINE

&

FUND

at

2015-

MOVE

&

EXPAND

2010-2014

LAUNCH

&

BUILD

EVOLVE

&

ENHANCE

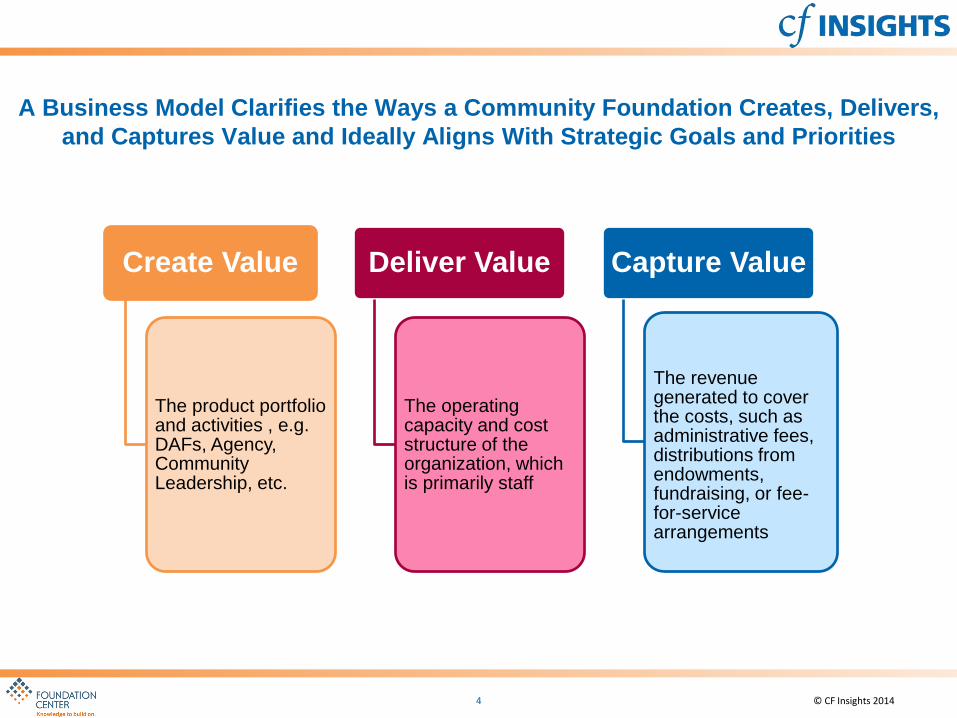

A Business Model Clarifies the Ways a Community Foundation Creates, Delivers,

and Captures Value and Ideally Aligns With Strategic Goals and Priorities

© CF Insights 2014 4

Create Value

The product portfolio and activities , e.g. DAFs, Agency, Community Leadership, etc.

Deliver Value

The operating capacity and cost structure of the organization, which is primarily staff

Capture Value

The revenue generated to cover the costs, such as administrative fees, distributions from endowments, fundraising, or fee-for-service arrangements

We are the community’s

philanthropic

institution, our value is

inherently clear.

We can rely on our

endowment/discretionary

funds to cover operations

and leadership funding

needs.

We’ve been in this

business for a

long time. We

know what works.

We don’t have the

time or capacity to

evaluate our

business model. As part of the Social

Sector we should

be mission-driven

not profit and

revenue driven.

Yet Reluctance to Define, Analyze, and Evolve Community Foundation

Business Models Persists Among Both Staff and Boards

Given our unique circumstances,

what works at other foundations

won’t apply to us.

For example:

• How to be thoughtful about future areas of growth and investment, particularly in areas with

challenging business model implications or less alignment with mission

- Product growth and focus should be intentional and aligned with mission and strategy

- Similarly, investments in products and activities should be the result of intentional decisions

rather than a lack of information

• How to consider opportunities to enhance programmatic and leadership possibilities in order

to grow impact and relationships in the community

- Clarify the foundation’s leadership role in the community

- Determine new terms for accepting new relationships or projects

A Review of the Business Model Will Generate Insights about

Key Strategic Questions and Potential Changes to Consider

© CF Insights 2013 7

A Series of Shifts in Community Foundation Operating Models Will Occur

Over the Next Several Years

The

Institution

The

Community • Every service and product community foundations offer is

now available from other sources, or soon will be • Community foundations must move beyond the important

emphasis on operational efficiency of the last decade to a second order of change

Managing

Financial Assets Long-term

Leadership • Community foundations must begin to see their endowments as a means to service, not the end in itself

• Foundations can only differentiate themselves from other service providers through taking a visible leadership role in the community

• Success on the ground in communities and successful competition for donors will require a fundamental shift from a mindset of independent value to one of coordinated impact

• Just as foundations increasingly expect nonprofits to collaborate to solve social problems, foundations, too, must be willing to partner with others in the field

Competitive

Independence Coordinated

Impact

Source: “On the Brink of New Promise: The Future of U.S. Community Foundations” from Blueprint Research & Design and the Monitor Institute, Giving USA,

United Way of America, Fidelity Charitable Gift Fund

Established

Institution

• Older community

foundation, typically

located in large Northeast

or Midwest city

• High percent of assets in

endowed & discretionary/

field of interest funds

• Known and respected by

donors as area’s core

philanthropic institution

• Relatively high percent of

deceased and aging

donors

• Offers a wide array of

products, with emphasis

on building endowment

• Several supporting/

affiliate organizations

• Deeply rooted in

community, invests

discretionary resources in

leadership activities

• Serves as convener, key

stakeholder, and initiator

in leadership efforts

Change Catalyst

• Emphasizes a few key

products, but focuses

largest share of capacity

on initiatives and

leadership

• Seeks to create buy-in

and support by proactively

asking donors to learn

about and fund initiatives

• Manages products to

cover costs and develops

revenue streams

specifically to fund

leadership efforts (e.g.,

Civic Leadership Fund)

• Clearly articulated agenda

for community leadership

and initiatives

• Leads the way &

encourage donors, non-

profits, and other partners

to become engaged

Product/

Service

Emphasis

Defining

Factors

Leadership

Approach

Statewide/

Rural Regional

• Develops charitable

resources and addresses

multiple communities’

needs across the entire

state/region

• Serves a diverse donor

base – different

interests/needs, financial

capacities, community

affiliations

• Offers a wide array of

products, subsidizing

some because they are

the only entity offering

that product in the

region/state

• Involved in a range of

initiatives (often small

scale/grassroots) in

multiple communities

Donor-Focused

• Lean business model –

little room to subsidize

products or fund

leadership

• Assets & revenues almost

entirely in donor-driven

products, little to no

discretionary funds

• Emphasis on developing

and serving ultra high net

worth, savvy donors

• Strong relationships with

donor advisors

• Tiered service levels

• Heavily concentrated in

donor-advised, corporate

funds, & fee-for-service

• Deemphasize products

that do not cover costs

• Servant leadership -

support and inform donors

in their self-identified

leadership efforts

Donor

Relationships

We’ll Use Four Example Business Model Types to Illustrate the Variation

Across the Field and Discuss Some Key Trends

4.3% 1.9% 9.7%

12.9%

21.1%

2.3%

4.6%

30.5%

85.3%

34.1% 18.1%

33.4%

22.7%

19.9%

0.7% 1.1%

2.1%

9.8%

5.4% 1.4%

1.5% 6.5%

4.4% 5.7%

12.7%

26.8%

2.0%

17.1%

1.1%

0%

20%

40%

60%

80%

100%

EstablishedInstitution

Donor-Focused Change Catalyst Statewide/RuralRegional

Other

CommunityLeadership/Initiatives

Fee-for-Service

Supporting Organizations

Scholarships

Geographic Affiliates

Deferred Gifts

Discretionary/FOI

Donor Advised

Designated

Agency / NonprofitEndowment

The Asset Mix For Each Foundation Type Is Distinctly Different

% of Total Assets by Product

5.3% 1.3% 1.3% 6.6%

10.1%

4.4%

3.4%

25.7%

62.3%

15.0%

19.5%

24.6%

0.9%

15.8%

16.3%

6.9% 0.5%

2.4%

3.1%

8.2%

3.0% 6.6%

4.6%

9.0%

8.3% 2.7%

4.4%

7.0%

14.7%

3.0%

16.2%

6.6%

50.0%

18.1%

3.6% 8.8%

0%

20%

40%

60%

80%

100%

EstablishedInstitution

Donor-Focused Change Catalyst Statewide/RuralRegional

Other

CommunityLeadership/Initiatives

Fee-for-Service

Supporting Organizations

Scholarships

Geographic Affiliates

Deferred Gifts

Discretionary/FOI

Donor Advised

Designated

Agency / NonprofitEndowment

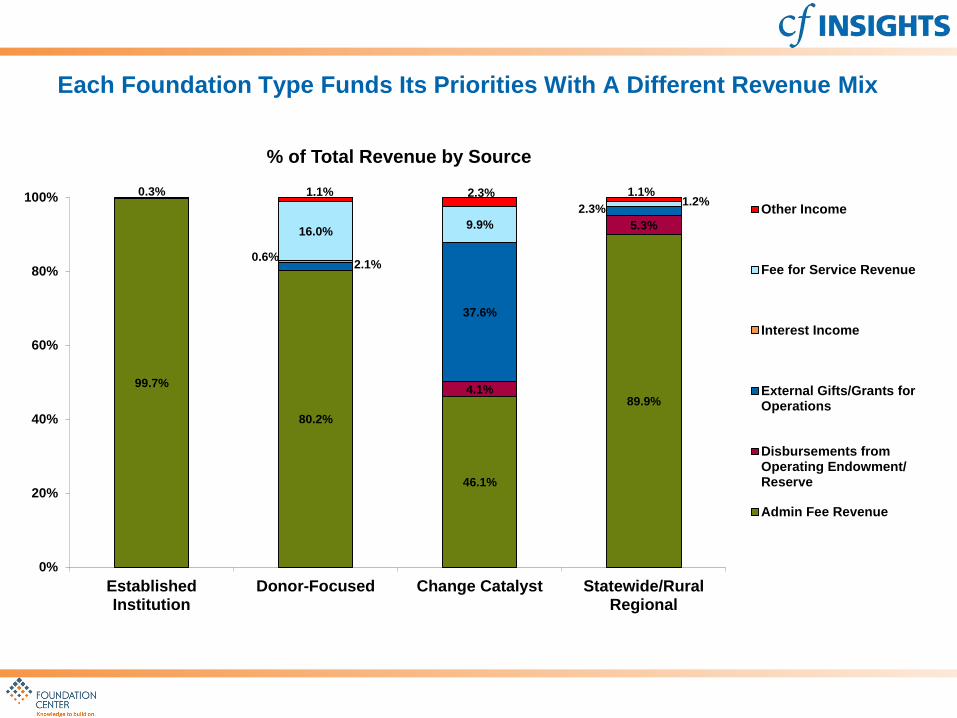

Capacity Dedicated to Products and Activities Reflects Differing Priorities

% of Total Costs by Product

99.7%

80.2%

46.1%

89.9% 4.1%

5.3%

2.1%

37.6%

2.3%

0.6%

16.0% 9.9%

1.2% 0.3% 1.1% 2.3% 1.1%

0%

20%

40%

60%

80%

100%

EstablishedInstitution

Donor-Focused Change Catalyst Statewide/RuralRegional

Other Income

Fee for Service Revenue

Interest Income

External Gifts/Grants forOperations

Disbursements fromOperating Endowment/Reserve

Admin Fee Revenue

Each Foundation Type Funds Its Priorities With A Different Revenue Mix

% of Total Revenue by Source

Established Institution

Changing donor bases and expectations require new approaches to development and donor relations

Increased competition and challenges to endowed philanthropy threaten the traditional role of community

foundations

Shift from role as funder and convener to collaborator

Donor-Focused

Need to differentiate from commercial DAF providers

Lack of endowment or discretionary funds requires creativity and efficiency in managing funds

Make strategic decisions about where to invest

Change Catalyst

Grow sustainable funding source(s) for leadership and initiatives

Easy to become over-extended

Avoid straying too far from community foundation roots

Statewide/Rural Regional

Being “everything to everyone” is unsustainable

Working with lots of small donors and small communities with limited resources is time intensive

Can be challenging to align leadership priorities across multiple communities

With Each Foundation Type Comes A Unique Set of

Business Model Challenges and Considerations

There Are Many Tools Available to Help Community Foundations

Understand Their Business Model and Adapt to Meet Changing Needs

Let’s look at two that work well together . . .

Business Model Canvas Activity-Based Costing

The Canvas Helps a Foundation Visualize and Articulate

Each Component of Its Business Model

Through An Iterative Process, the Canvas Helps Create an Adaptive, Concise

Model That Reflects Current Conditions and Future Aspirations

https://canvanizer.com/new/business-model-canvas

16

Activity-Based Costing Enables a Foundation To Better Understand

the True Cost of Products and Services

• Activity-Based Costing (ABC) allows organizations to determine the fully-loaded cost associated with

each product or service

• Rather than considering volume alone (i.e., number of donor advised funds) ABC takes into account

non-volume related characteristics such allocations of administrative overhead

• First activities are identified and defined, then cost data is gathered and traced to activities, finally

costs are allocated to products or services based on their utilization of activities

Expense 1 Expense 3 Expense 4 Expense 2

Activity 1 Activity 2 Activity 3

Product 1 Product 2

Costs are

assigned

to activities…

…then allocated

based on utilization

of activities

© CF Insights 2014

17

100% of the Foundation’s Staff Time, Cost and Other Expenses Are

Assigned to a Matrix of Activities and Products

Cost Matrix Agency Designated Donor Advised FOI Scholarships Planned

Giving

Fee for

Service Initiatives Leadership …

Acquiring or

Establishing a

New Fund or

Gift

$Y $Y $Y $Y $Y $Y $Y $Y $Y $Y

Maintaining

Funds $Y $Y $Y $Y $Y $Y $Y $Y $Y $Y

Making

Grants $Y $Y $Y $Y $Y $Y $Y $Y $Y $Y

Providing

Non-Grant

Services to

the

Community

$Y $Y $Y $Y $Y $Y $Y $Y $Y $Y

Other Staff

Activities $Y $Y $Y $Y $Y $Y $Y $Y $Y $Y

Products Defined by Community Foundation

>1

00

A

cti

vit

ies

Staff costs are assigned to activities and products based on reported time, weighted by

individual salaries and including taxes and benefits

© CF Insights 2014

18

Once Staff Costs Have Been Assigned, Direct and Indirect Foundation

Costs Are Allocated Across the Matrix of Activities and Products

The complete matrix of products and activities includes

staff, direct and indirect costs for each activity and product

Staff

Activity

Survey

Product

1

Product

2

Product

3

Product

4

Product

5

Product

6

Product

7

Product

8

Activity A $Y $Y $Y $Y $Y $Y $Y $Y

Activity B $Y $Y $Y $Y $Y $Y $Y $Y

Activity C $Y $Y $Y $Y $Y $Y $Y $Y

Activity D $Y $Y $Y $Y $Y $Y $Y $Y

Activity E $Y $Y $Y $Y $Y $Y $Y $Y

Activity F $Y $Y $Y $Y $Y $Y $Y $Y

Activity G $Y $Y $Y $Y $Y $Y $Y $Y

Activity H $Y $Y $Y $Y $Y $Y $Y $Y

Activity I $Y $Y $Y $Y $Y $Y $Y $Y

Total $Y $Y $Y $Y $Y $Y $Y $Y

Allocate Indirect

Costs such as

occupancy and

office expenses to

activities and

products based on

the distribution of

staff time

Allocate Direct Costs

such as events,

publications, or

investment

management

consultants to

activities and

products based on

specific allocation

rules

© CF Insights 2014

19

The Analysis Includes an Assessment of the Overall Business Model

Example: Subsidy vs. Contribution by Product

$254K $209K

$91K $65K

$34K ($7)K ($22)K ($40)K ($43)K ($106)K ($588)K

Desig

na

ted

Unre

str

icte

d &

FO

I

DA

F -

End

ow

me

nt

Scho

lars

hip

s -

Bo

ard

Fee f

or

Se

rvic

e

Defe

rred

Veh

icle

s

Geo

gra

ph

ic A

ffili

ate

s

Org

an

ization

Fund

Ra

isin

g F

und

s

DA

F -

No

n E

nd

ow

ed

Com

mu

nity L

ead

ers

hip

Fee-Based Products Leadership Activities

Surplus Subsidy Investment

© CF Insights 2014

20

The Analysis Also Includes Product-Level Details the Community

Foundation Is Most Interested in Exploring

Example: A Closer Look at DAFs

© CF Insights 2014

$0K

$50K

$100K

$150K

$200K

$250K

$300K

$350K

$400K

1 2 3 4 5 6 7 8 9 10111213141516171819202122232425262728293031323334353637383940414243444546474849505152535455565758596061

Non-Permanent, Non-Invested Non-Permanent, Invested Permanent

DAFs managed by Foundation as of 12/31/2013

Ass

et

Size

($

k)

Dotted lines represent breakeven fund sizes

$140k

$79k

$64k

Average Fund Size: $42k $64k $142k

21

Comparisons to Appropriate Peers Provide Context

CF 1 CF 2 CF 3 CF 4 CF 5 CF 6

Total Revenue

Total Cost

Total CommunityLeadership Surplus orSubsidy

Tota

l Co

mm

un

ity

Lead

ersh

ip

Co

sts

and

Rev

enu

es

COMMUNITY LEADERSHIP COSTS AS % OF TOTAL ADMINISTRATIVE COSTS

42% 23% 30% 32% 15% 25%

Example: Community Leadership Revenues and Costs

© CF Insights 2014

SHARING KNOWLEDGE. GROWING IMPACT.

cfinsights.org

Aaron Schill, Director

(212) 807-2538

David Rosado, Member Services Manager

(212) 807-2430

The CF Insights Team