Embed Size (px)

Citation preview

Communicating Quantitative Information

Excel HomeworkSocial Security, Pensions

Stocks and BondsLife expectancy

Homework: Postings. Homework due after Thanksgiving. Find on-line retirement planner. Compute prediction for

yourself (or for a parent) or John/Jane doe or someone made up. Make posting on experience (do not show results)

Retirement problem

What will I have in the future starting with pv and with the system of payments described by the rest of the parameters.

• FV is future value=fv(rate, nper, pmt, pv, type)– Rate is 4%, – pv is -4000, – pmt = -2000– nper = 20– For type, try both 0 and 1. This indicates paying at the

end of the period versus paying at the beginning

Retirement

• Take it one year at a time:

Retirement

Compare after 4 years: 13,172.36 vs 12000

Retirement answers:

• Adding the 2000 to savings – at the end of the year:

=fv(.04,20,-2000,-4000,0) $68,320.65

– at the start of the year:=fv(.04,20,-2000,-4000,1) $70,702.90

– Putting the money away, no interest: 4000 + 2000*20 $44,000

Purchase TV problemWhat is the better thing to do, comparing what you are

paying in terms of the value of money today. This assumes a cost of money

• You are comparing – the cost paying $2500 nowwith– the cost of making annual payments over the next 4 years – Assumption: you have or will have the money. You can invest

money today to have in the future (put away less now to produce/grow to something later).

• Use pv for present value

• =pv(rate,nper,pmt,fv,type)– For rate, use 10% for what you need for capital– nper is 4. pmt is -750.– Set fv as 0. Try both values of type. The answer is different!

TV problem: answers• You don't pay anything for a whole year:

=pv(.10,4,-750,0,0) $2,377.40– Note: the first 0 indicates no extra last

paymentIf you can get this deal AND you can invest money to ear 10% interest, take it!

• You pay $750 at the start of each of the 4 years=pv(.10,4,-750,0,1) $2,615.14You are better off paying the whole thing up front!

Go to Excel Help and read [more] examples.

PV and FV (and PMT)• Need to be careful on time unit, e.g., month vs.

year. I avoided this in the 2 problems.• Why is present value of something in the future

less now?– Think about what you need to put away to reach that

value, assuming earnings and compounding

• Need to be careful with signs– Solution: use HELP in Excel!!!

• Need to be careful with default values

Alternate tools

• Get google mail (gmail) account and use Google Documents – Word processing and Spreadsheet

– Has advantage that you can access your projects anywhere

– Has advantage that you can share access to work

– Disadvantage: requires fast web connection.

Social Security• Not intended as investment/retirement plan• Transfer plan:

– Tax current workers to pay entitled workers (retirees, disabled, families) a guaranteed percentage of prior wages

• Full amount at 65 going to 67. You can start at 62 for reduced benefits (reduction stays in place). You can wait up to 70 for increased benefits (8%/year).

• If you don't fully retire, some reduction in benefits up until 70.

• Benefits can be taxed as income if total income large enough.

– Original goals:• Encouraged retirements, helping new workers get jobs• Put money into circulation: help economy• Keep elderly out of poverty • Minimal administration costs

– Success

Social Security taxes

• Part of what is called 'payroll taxes'– along with Medicare (1.45), withholding taxes US and

State (taxes taken away for income tax: exact amount owed determined when your file returns)

• 6.2% from employee, matched by 6.2% from employer– Responsibility of employer to collect– Up to a cap, which has moved up over the years:

currently set at $102,000 – Self-employed pay: 12.4%, also up to cap.

Social Security Situation• System currently takes in more than it pays out.

– No 'lock box', but treasury bonds• Estimates are that system will start paying out

more than it takes in in 2017– Based on population ("baby boomers" retiring) and

economy• Estimates are that in 2041, the funds will be

depleted and the money coming in will only cover 70%

Estimates are considered conservative: situation could be better, for example, if economy is good with more people earning money and paying taxes.

These estimates are from 2 years ago. Extra Credit to find current estimate.

Is this a crisis?

• Government generally runs a deficit– Surplus in latter part of Clinton administration– Deficits in Bush administration due to

• fall in taxes because of economy• wars in Afghanistan and Iraq• substantial tax cuts (mostly benefiting people in

upper upper-range of income)

• Changes now (earlier rather than later) will make a significant difference.

Alternative view: see next• Real crisis is growth in Medicare entitlements

– Entitlement: class of people entitled by law to benefits

• Recent addition of drug benefits– Criticized from the right for being yet another

entitlement– Criticized from the left for forbidding negotiations with

drug companies to lower costs AND for not covering more expenses (the doughnut)

• This is independent of issues of the uninsured, underinsured, benefits tied to employment, etc.

• This is related to general issue of costs of medical care going up.

New Health Care legislation• Provide more efficient (cheaper) care

– Require [almost] everyone to buy insurance– Encourage/require all but smallest businesses to provide health

insurance– Support preventative/wellness care to Medicare clients

• Provide plans in exchanges• Cut down on Medicare Advantage • Monitor (reward or punish) hospitals for better care• Close drug donut hole (negotiation with drug companies.• Other programs that may over time move towards pay for care

versus pay for procedures.

Congressional Budget office says this will reduce growth of costs

Personal Retirement Accounts• Divert portion of individual Social Security taxes to

personal account. Details not complete, but may be:– 2% to 4%: (2% of salary to PRA, 4.2% to Social

Security)– Go into managed account of index funds and bonds

(see later)– Claim (hope) that this will grow faster than

government securities– Upon retirement, use money to buy annuity– Anything left over available to individual and family

• This is what is called: privatization of Social Security• With financial crisis, fall in stocks, election of Obama,

this will not be pushed.– But some candidates did suggest it again.

Suggested fixes for Social Security• Pop the cap: raise from $102,000 ($106,000 in 2009)• Raise retirement age (for full benefits)• Raise tax rate on everyone. Raise tax rate on some.• Lower benefits (other than by age)

– make raises based on wages not prices– decrease standard to cover less than 40% of prior

income• Personal Retirement accounts would take money out of the

system. – Significant transition problem: money taken out of system when it is

needed– Advocates claim (hope) that investments make up for

decreases in benefits. Give people sense of ownership.– Many (most?) economists are skeptical. Note also that

the system would require fees to investment companies as well as increased administrative costs.

Panel: http://www.nytimes.com/2010/11/11/us/politics/11fiscal.html?hp

• Findings leaked out. May still change.

• Do raise (pop?) the cap on Social Security payroll taxes

• Change benefits (means-testing): lower for some, higher for others.

• Change tax code including– Remove mortgage interest deduction– Subject health care benefit, other benefits to

taxes– Lower rates

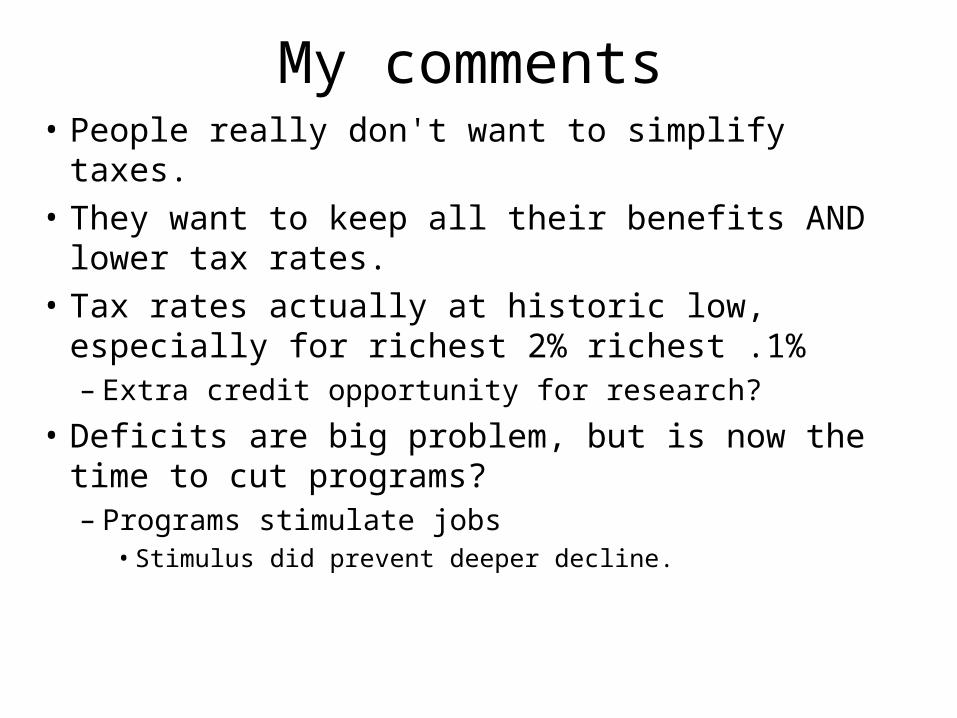

My comments• People really don't want to simplify taxes.

• They want to keep all their benefits AND lower tax rates.

• Tax rates actually at historic low, especially for richest 2% richest .1%– Extra credit opportunity for research?

• Deficits are big problem, but is now the time to cut programs?– Programs stimulate jobs

• Stimulus did prevent deeper decline.

Pensions, etc.• Employers may offer

– defined benefit plans: employee received a set amount (based on salary and years of service) upon retirement. This is the traditional way, being replaced in many places by:

– defined contribution plans: Employee contributes and employer matches/over-matches. Amount is invested.

• Example: SUNY: 3 % with 8% match• May be choices. Enron and other examples led to rules to

widen investments choices, but…• Too many choices tends to decrease participation• Recent legal change made enrollment the default. New

employee needs to ‘opt out’.– Why would anyone opt out?

Independent of employer

• Tax encouraged plans. Person saves into special account– IRA: tax deferred– Roth IRA: tax sheltered

• NOTE: under-utilized

• Limits to how much

• Limits to who can do it

Investment options• Individual company stocks• Mutual funds: buy shares. Manager buys & sells various things

according to a strategy. Management fees.• Index funds: stocks of each of some set of companies, say S&P

500 industrials. Fees are less.NOTE: all of the above often called equities.

• Municipal Bonds: individual bonds of government agencies. Get stated interest usually twice a year plus principle back when 'bond matures'

NOTE: many of these did fall in value in financial crisis, due to supply of hedge funds selling. Face value still good.

• Company bonds: same from companies• Money market, CDs, savings: offered by banks: defined

interest, maturity date.• Treasury bonds: most secure, lower interest

Investment options

• Global (outside of USA or mixture) funds, bonds, stock

• Gold, other commodities

• Real Estate Investment Trusts

• Futures: puts and calls

• Other???

Treasury Bills• … are bonds sold by U.S. government.• Purchased by U.S. residents AND others• Many are purchased by people,

organizations, banks in China– The comment that 'we are borrowing money

from China to pay for the war' comes from this.

– Note: China (Chinese companies, people, government) also sell U.S. residents goods.

Federal reserve

• Acts to prevent (control) inflation and

• Help economy

• Interest rates already very low.

• Recent effort: buying treasuries is intended to encourage borrowing.

Zero-coupon bond

• Buy at specific discount from 'face' value.

• Do not get periodic interest.

• At end of agreed upon time, get full value.

• Graduation gift???

Jargon• Market: place to buy and sale• Liquidity: how easy it is to sell something, that is,

convert item to cash• Credit market: places to get money (that is, take

out loans) or sell loans (like selling an IOU)– Credit market is said to be frozen now.

• Recession: officially is two months of declines in Gross Domestic Product (total of goods and services)– Extra credit: get different definitions of GDP and

compare

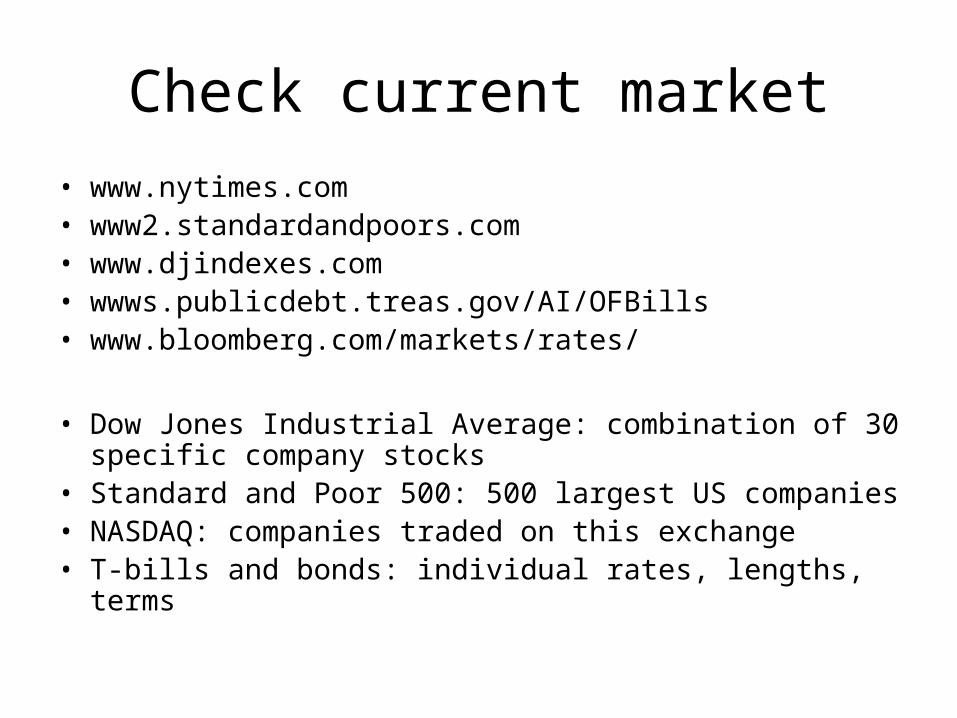

Check current market

• www.nytimes.com• www2.standardandpoors.com• www.djindexes.com• wwws.publicdebt.treas.gov/AI/OFBills• www.bloomberg.com/markets/rates/

• Dow Jones Industrial Average: combination of 30 specific company stocks

• Standard and Poor 500: 500 largest US companies• NASDAQ: companies traded on this exchange• T-bills and bonds: individual rates, lengths, terms

Trends

• Overall, in long [long] term, stocks (mutual funds, even with fees) have done better than T-Bills though– Periods when that has not been true

• Some evidence that stocks are over-valued now.• The phrase ‘Stock market up’ or "Stock market

is down' generally refers to the DOW: 30 specific large companies– Extra credit opportunity: first person who posts the list

of companies– There also is S&P 500, NASDAQ, others???

Life Expectancy

www.cdc.gov/nchs/fastats/lifexpec.htm• Life expectancy at birth is different than at a

late[r] age– If you make it to an advanced age, the expectation is

that you will live even longer

• If you live until your 60s, how many [more] years of life?

65 in Wh. male Wh. female B. male B. female

2002 16.6 19.5 14.6 18

Life expectancy

• World

http://www.worldpolicy.org/globalrights/econrights/maps-life.html

NOTE: this data represented is life expectancy at birth: infant mortality is significant factor.

Life expectancy

• http://www.ac.wwu.edu/~stephan/Animation/expectancy.html\

(unofficial source, but appealing presentation)

What is the significance of what parts change and what parts don't?

gapminder

• UN statistics• www.gapminder.org

– Gapminder World 2006 (first application) Go To Graph

– Dimensions shown:• Country / Region / Size• Income (log scale, 'International Dollars'

vs • Life Expectancy• Time (dynamic)

Extra credit / Project II

• Use Gapminder to pick 2 or 3 countries with different trajectories

• Consult 2 or 3 other sources

• Offer explanations (theories) for differences

Project II: Tentative• If you didn't present before, you should to present

now (see me).• You may work in teams (from more, more is

expected)• Propose topic. I will suggest some.

– Including maps, charts, diagrams– Analysis of feature(s) of election okay– Local relevance always a plus

• Focus on definitions, denominator, difference (contexts), dimension, distribution, … critical features of quantitative topic in the news

Do you have enough for retirement• How much do you need

– often stated as percentage of current income– how many years do you expect to live

• Sources (some/all of which may grow)– Social Security– Defined benefit plan(s)– Defined contribution plan(s)

• IRA, Roth IRA, 401K, other

– Savings not in retirement accounts

• What is expected growth of investments (in retirement plans and other)?

• What is expected inflation?• Some plans ask about spouse• Some retirement estimators ask if you want to leave an

estate

Homework: over Thanksgiving• Find a retirement calculator and do the

calculation for yourself and/or a parent.– http://www.asec.org/ballpark/– http://www.raymondjames.com/retire_calc.htm– http://cgi.money.cnn.com/tools/retirementplanner/

retirementplanner.jsp– http://sites.stockpoint.com/aarp_rc/wm/Retirement/

Retirement.asp?act=LOGIN– other (maybe ones associated with parent's work or

investments)• Find sources and make comments, backed by data, on

Social Security, pensions, savings, etc.

NO PERSONAL DATA

John/Jane DoeIf you do this option, write about your choices.• Decide on age and do research to find life expectancy• Decide on age for retirement• Has estimated Social Security $1100/month if retiring at

67• Current salary $45,000. You decide on estimated raises

(bet. 1 to 3 %)• Company retirement: do both or only 1 (3 ways)

– Has guaranteed defined benefit retirement of 25% of average of highest 5 years

– Has 401k of $30,000. Contributing 3%, matched by company.– Can add something from previous job

• Savings: $27,000 ?? (median in http://www.forbes.com/2005/05/04/cx_da_0504topnews.html OR see http://www.bls.gov/opub/cwc/cm20050114ar01p1.htm

• Has house with outstanding mortgage??• Has credit card debt???

![Proposals to Extend Healthy Life Expectancy in Shizuoka ...€¦ · [Gap between life expectancy and healthy life expectancy in Shizuoka Prefecture] Healthy life expectancy *Source:](https://img.pdfslide.us/doc/110x75/5f427921a09c2479a15262fb/proposals-to-extend-healthy-life-expectancy-in-shizuoka-gap-between-life-expectancy.jpg)