Embed Size (px)

Citation preview

Communicating a Smarter FutureKeynote at Network 20124th annual distribution network strategy conference

16 February 2012

Sandy SheardDeputy Director for Future Electricity Networks, DECC

Agenda

• Context

• Smarter systems and customer engagement

• Government action

• Conclusions

2

DECC’s low carbon and security of supply objectives will lead to major changes in future generation and demand.

Today’s electricity generation can easily be flexed to meet changes in demand, and is largely located onshore.

To 2020 and beyond we will see:• increased electricity demand

with different load patterns• intermittent and inflexible

supply• More generation in new

locations, two-way flows• A greater role for non-

generation flexible solutions like demand side response (DSR), storage and interconnection 3

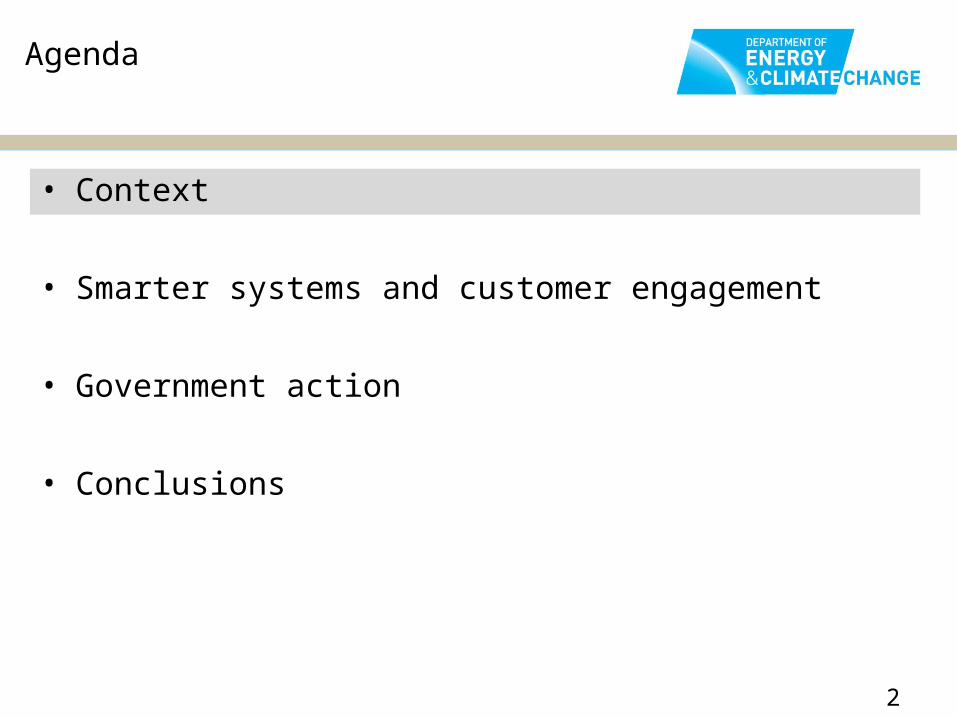

Two key challenges for the system: levels of investment and system balancing

Generation: £75bn could be needed by 2020

Transmission networks: Up to £24bn could be needed onshore in the period 2013-21 and in the order of £7bn could be needed offshore by 2020

Distribution networks: around £28bn could be needed in the period 2015 to 2023; a further £60-80bn could be needed in the period 2020-2050

Investment System Balancing

0

20

40

60

80

100

120

140

160

Day 1 Day 2 Day 3 Day 4 Day 5 Day 6 Day 7

GWLOW WIND - 7 days in January 2050 - no DSR

Peaking output

Spilled output

Intermittent output

Baseoutput

Demand pre DSR

*Actual wind data from 2006

0

20

40

60

80

100

120

140

160

Day 1 Day 2 Day 3 Day 4 Day 5 Day 6 Day 7

GW

BASE GENERATION - 7 days in January 2010

Margin

Unabated Coal

Unabated Gas

Intermittent

European

Nuclear

0

20

40

60

80

100

120

140

160

Day 1 Day 2 Day 3 Day 4 Day 5 Day 6 Day 7

GW

BASE DEMAND - 7 days in January 2010

Resistive 2010

Domestic 2010

Commercial 2010

Industrial 2010

Demand over even days in January 2010

Demand over seven days in January 2050*

Increased intermittency & inflexibility

Smarter systems can help us address these challenges4

Agenda

• Context

• Smarter systems and customer engagement

• Government action

• Conclusions

5

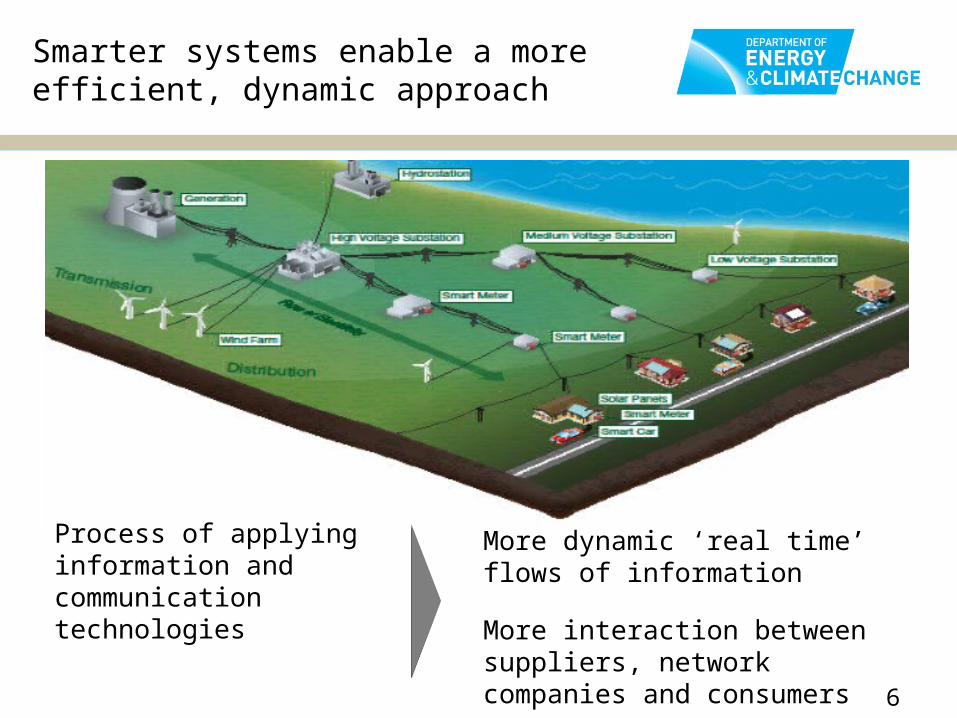

Smarter systems enable a more efficient, dynamic approach

Process of applying information and communication technologies

More dynamic ‘real time’ flows of information More interaction between suppliers, network companies and consumers

6

Smarter systems will help us meet future challenges by making the right investment choices and increasing system flexibility

• maximise use of networks (headroom)• factor in and make best use of

distributed generation sources• build less peaking plant • maximise use of intermittent sources • reduce / shift demand (DSR)• use the right ‘tool’ for the job (storage

vs. generation vs. wires)

Use system assets more efficiently

• use non-generation sources and local generation sources to flex ‘supply’ (EVs & heat pumps as storage, distributed generation)

• manage 2-way electricity flows • reduce / shift peak demand through

DSR (user control & remote control)

Use tools & technology innovatively

At the networks level, the main change needs to come from distribution networks.

More active management of the networks including greater interaction with customers.

7

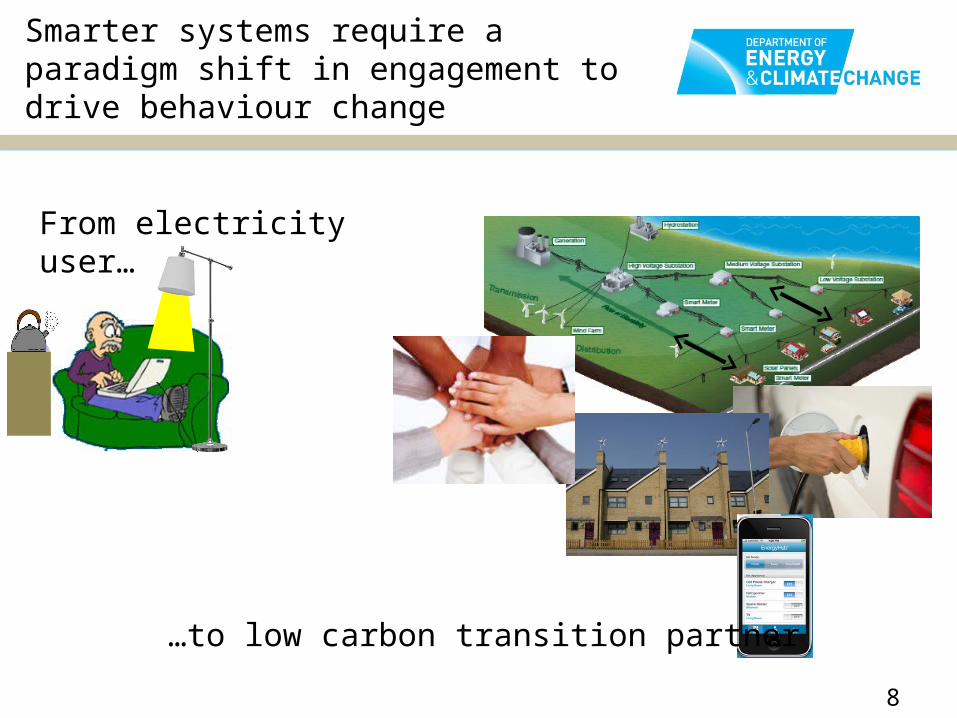

…to low carbon transition partner

From electricity user…

Smarter systems require a paradigm shift in engagement to drive behaviour change

8

Agenda

• Context

• Smarter systems and customer engagement

• Government action

• Conclusions

9

Government is already taking action on smarter systems

1 Leadership on network investment

2

3 Enabling a smarter grid

4 Longer term thinking on future challenges

Changing customer behaviour

10

Leadership on network investment, working with Ofgem

11

Smart Grid Forum brings together thinking from DECC, Ofgem and

industry

Informing Ofgem’s “RIIO” price control framework for distribution companies

1

Changing customer behaviour2

Behavioural Change and Energy Use’ paper written jointly with Cabinet Office Behavioural Insight team – including five trials.

Green Deal: Running trials to understand behaviour and incentives

Smart meters: Using behavioural theory and trials to inform customer

engagement strategy

Smart meters programme and the Green Deal are giving customers choice and the opportunity to take an active role in energy efficiency and demand side management.

12

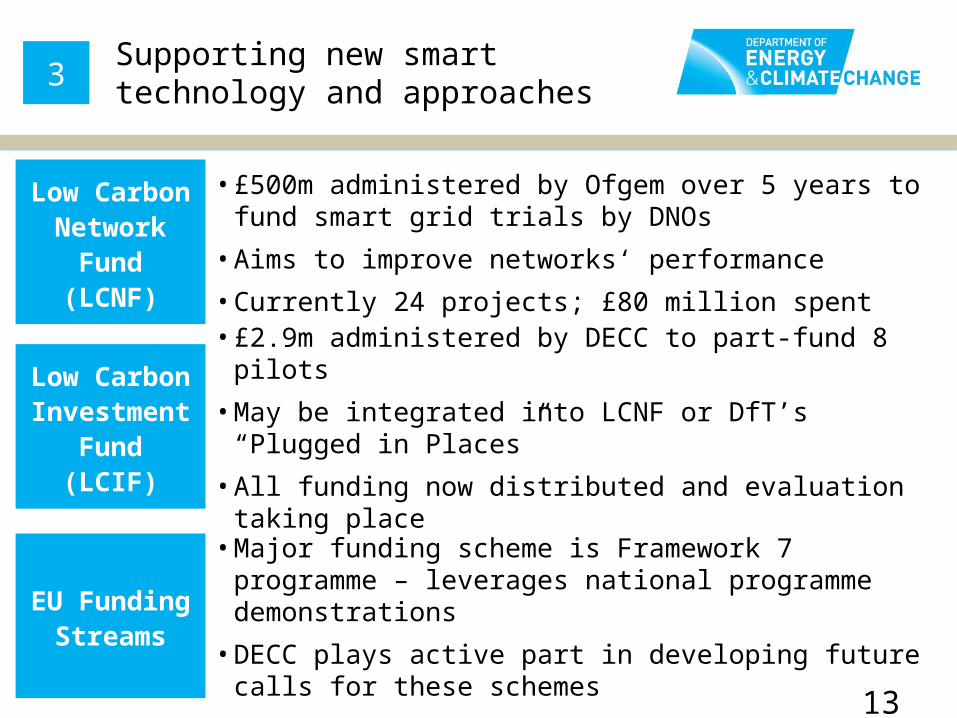

Supporting new smart technology and approaches3

Low Carbon Network Fund

(LCNF)

Low Carbon Investment Fund (LCIF)

EU Funding Streams

• £500m administered by Ofgem over 5 years to fund smart grid trials by DNOs

• Aims to improve networks‘ performance

• Currently 24 projects; £80 million spent

• £2.9m administered by DECC to part-fund 8 pilots

• May be integrated into LCNF or DfT’s “Plugged in Places”

• All funding now distributed and evaluation taking place

• Major funding scheme is Framework 7 programme – leverages national programme demonstrations

• DECC plays active part in developing future calls for these schemes

13

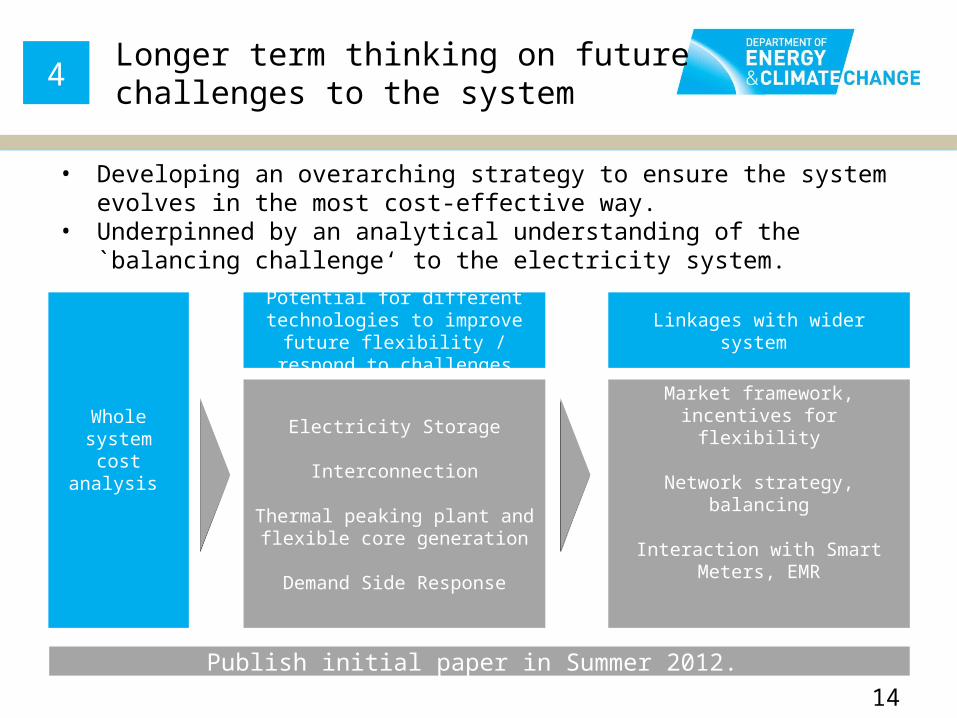

Longer term thinking on future challenges to the system4

Electricity Storage

Interconnection

Thermal peaking plant and flexible core generation

Demand Side Response

Publish initial paper in Summer 2012.

Whole system cost analysis

Potential for different technologies to improve future

flexibility / respond to challengesLinkages with wider system

Market framework, incentives for flexibility

Network strategy, balancing

Interaction with Smart Meters, EMR

• Developing an overarching strategy to ensure the system evolves in the most cost-effective way.

• Underpinned by an analytical understanding of the `balancing challenge‘ to the electricity system.

14

Agenda

• Context

• Smarter systems and customer engagement

• Government action

• Conclusions

15

Conclusions

•Smarter systems, with the grid at their heart, will be a key enabler to deliver the transition to low carbon.

•Smarter systems will need industry to work in partnership with customers requiring a paradigm shift in engagement.

•Industry, consumers, government and the regulator need to work together, today, to deliver the smart systems of tomorrow.

16