Embed Size (px)

Citation preview

7/24/2019 Commodity Research Report 29 February 2016 Ways2Capital

http://slidepdf.com/reader/full/commodity-research-report-29-february-2016-ways2capital 1/9

7/24/2019 Commodity Research Report 29 February 2016 Ways2Capital

http://slidepdf.com/reader/full/commodity-research-report-29-february-2016-ways2capital 2/9

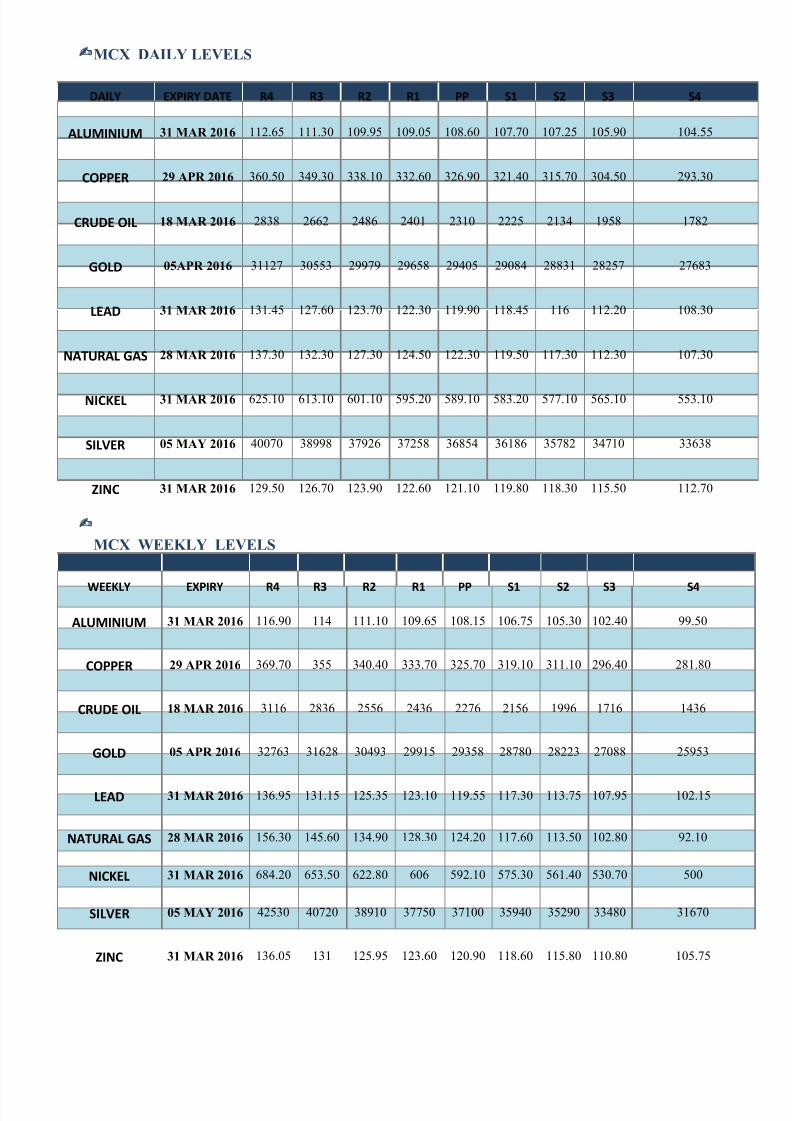

MCX DAILY LEVELS

DAILY EXPIRY DATE R4 R3 R2 R1 PP S1 S2 S3 S4

ALUMINIUM 31 MAR 2016 112.65 111.30 109.95 109.05 108.60 107.70 107.25 105.90 104.55

COPPER 29 APR 2016 360.50 349.30 338.10 332.60 326.90 321.40 315.70 304.50 293.30

CRUDE OIL 18 MAR 2016 2838 2662 2486 2401 2310 2225 2134 1958 1782

GOLD 05APR 2016 31127 30553 29979 29658 29405 29084 28831 28257 27683

LEAD 31 MAR 2016 131.45 127.60 123.70 122.30 119.90 118.45 116 112.20 108.30

NATURAL GAS 28 MAR 2016 137.30 132.30 127.30 124.50 122.30 119.50 117.30 112.30 107.30

NICKEL 31 MAR 2016 625.10 613.10 601.10 595.20 589.10 583.20 577.10 565.10 553.10

SILVER 05 MAY 2016 40070 38998 37926 37258 36854 36186 35782 34710 33638

ZINC 31 MAR 2016 129.50 126.70 123.90 122.60 121.10 119.80 118.30 115.50 112.70

MCX WEEKLY LEVELS

WEEKLY EXPIRY R4 R3 R2 R1 PP S1 S2 S3 S4

ALUMINIUM 31 MAR 2016 116.90 114 111.10 109.65 108.15 106.75 105.30 102.40 99.50

COPPER 29 APR 2016 369.70 355 340.40 333.70 325.70 319.10 311.10 296.40 281.80

CRUDE OIL 18 MAR 2016 3116 2836 2556 2436 2276 2156 1996 1716 1436

GOLD 05 APR 2016 32763 31628 30493 29915 29358 28780 28223 27088 25953

LEAD 31 MAR 2016 136.95 131.15 125.35 123.10 119.55 117.30 113.75 107.95 102.15

NATURAL GAS 28 MAR 2016 156.30 145.60 134.90 128.30 124.20 117.60 113.50 102.80 92.10

NICKEL 31 MAR 2016 684.20 653.50 622.80 606 592.10 575.30 561.40 530.70 500

SILVER 05 MAY 2016 42530 40720 38910 37750 37100 35940 35290 33480 31670

ZINC 31 MAR 2016 136.05 131 125.95 123.60 120.90 118.60 115.80 110.80 105.75

7/24/2019 Commodity Research Report 29 February 2016 Ways2Capital

http://slidepdf.com/reader/full/commodity-research-report-29-february-2016-ways2capital 3/9

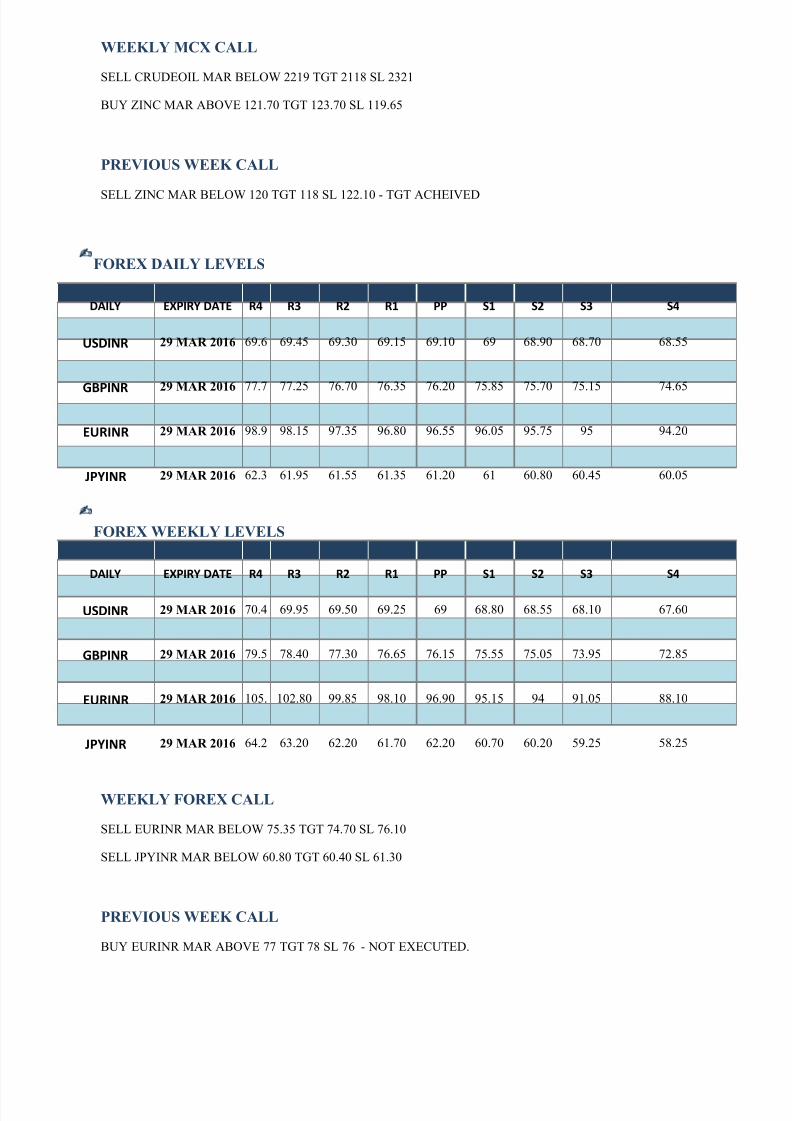

WEEKLY MCX CALL

SELL CRUDEOIL MAR BELOW 2219 TGT 2118 SL 2321

BUY ZINC MAR ABOVE 121.70 TGT 123.70 SL 119.65

PREVIOUS WEEK CALL

SELL ZINC MAR BELOW 120 TGT 118 SL 122.10 - TGT ACHEIVED

FOREX DAILY LEVELS

DAILY EXPIRY DATE R4 R3 R2 R1 PP S1 S2 S3 S4

USDINR 29 MAR 2016 69.6

69.45 69.30 69.15 69.10 69 68.90 68.70 68.55

GBPINR29 MAR 2016

77.7

77.25

76.70

76.35

76.20

75.85

75.70

75.15

74.65

EURINR 29 MAR 2016 98.9

98.15 97.35 96.80 96.55 96.05 95.75 95 94.20

JPYINR 29 MAR 2016 62.3

61.95 61.55 61.35 61.20 61 60.80 60.45 60.05

FOREX WEEKLY LEVELS

DAILY EXPIRY DATE R4 R3 R2 R1 PP S1 S2 S3 S4

USDINR 29 MAR 2016 70.4

69.95 69.50 69.25 69 68.80 68.55 68.10 67.60

GBPINR 29 MAR 2016 79.5

78.40 77.30 76.65 76.15 75.55 75.05 73.95 72.85

EURINR 29 MAR 2016 105.

102.80 99.85 98.10 96.90 95.15 94 91.05 88.10

JPYINR 29 MAR 2016 64.2

63.20 62.20 61.70 62.20 60.70 60.20 59.25 58.25

WEEKLY FOREX CALL

SELL EURINR MAR BELOW 75.35 TGT 74.70 SL 76.10

SELL JPYINR MAR BELOW 60.80 TGT 60.40 SL 61.30

PREVIOUS WEEK CALL

BUY EURINR MAR ABOVE 77 TGT 78 SL 76 - NOT EXECUTED.

7/24/2019 Commodity Research Report 29 February 2016 Ways2Capital

http://slidepdf.com/reader/full/commodity-research-report-29-february-2016-ways2capital 4/9

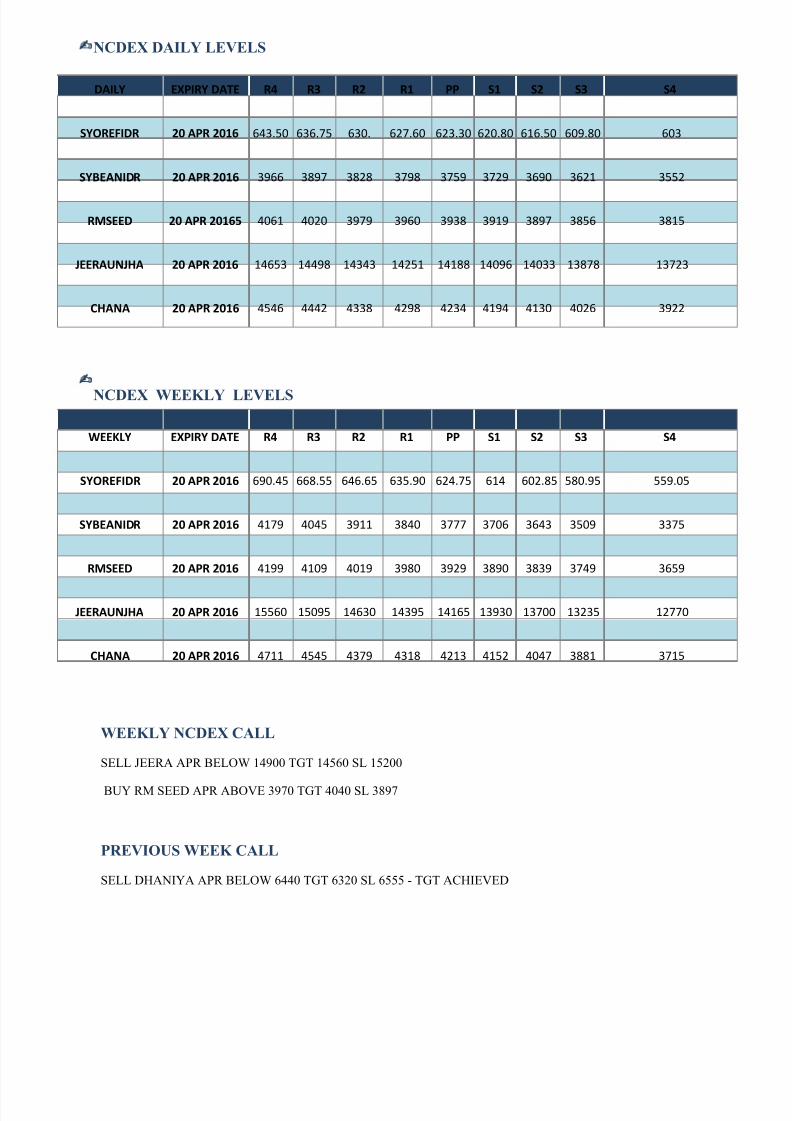

NCDEX DAILY LEVELS

DAILY EXPIRY DATE R4 R3 R2 R1 PP S1 S2 S3 S4

SYOREFIDR 20 APR 2016 643.50 636.75 630. 627.60 623.30 620.80 616.50 609.80 603

SYBEANIDR 20 APR 2016 3966 3897 3828 3798 3759 3729 3690 3621 3552

RMSEED 20 APR 20165 4061 4020 3979 3960 3938 3919 3897 3856 3815

JEERAUNJHA 20 APR 2016 14653 14498 14343 14251 14188 14096 14033 13878 13723

CHANA 20 APR 2016 4546 4442 4338 4298 4234 4194 4130 4026 3922

NCDEX WEEKLY LEVELS

WEEKLY EXPIRY DATE R4 R3 R2 R1 PP S1 S2 S3 S4

SYOREFIDR 20 APR 2016 690.45 668.55 646.65 635.90 624.75 614 602.85 580.95 559.05

SYBEANIDR 20 APR 2016 4179 4045 3911 3840 3777 3706 3643 3509 3375

RMSEED 20 APR 2016 4199 4109 4019 3980 3929 3890 3839 3749 3659

JEERAUNJHA 20 APR 2016 15560 15095 14630 14395 14165 13930 13700 13235 12770

CHANA 20 APR 2016 4711 4545 4379 4318 4213 4152 4047 3881 3715

WEEKLY NCDEX CALL

SELL JEERA APR BELOW 14900 TGT 14560 SL 15200

BUY RM SEED APR ABOVE 3970 TGT 4040 SL 3897

PREVIOUS WEEK CALL

SELL DHANIYA APR BELOW 6440 TGT 6320 SL 6555 - TGT ACHIEVED

7/24/2019 Commodity Research Report 29 February 2016 Ways2Capital

http://slidepdf.com/reader/full/commodity-research-report-29-february-2016-ways2capital 5/9

MCX - WEEKLY NEWS LETTERS

INTERNATIONAL NEWS

Bullion

Gold fell more than 1 percent on Friday, as the dollar and global shares rose, but fund buying persisted a

investors expected a G20 summit would produce little in the way of a coordinated stimulus program. Financia

leaders from G20 nations gathered in Shanghai against a backdrop of worsening economic conditions and

lack of wider consensus on how to fix the problems. Concerns that a slowing global economy could eventually

push the United States into recession eased as data showed U.S. economic growth slowed less than expected i

the fourth quarter. Despite Friday's losses, gold has rediscovered its role as a shelter for risk averse investors

Assets of SPDR Gold Trust, the top bullion exchange traded fund, held steady on Thursday, after rising to thei

highest since March 2015 on Wednesday. Economists had expected fourth quarter GDP growth to be revise

down to 0.4%. The positive surprise underpinned the dollar and sent gold prices sharply lower. Hedge fund

and money managers raised their bullish stances in COMEX gold to a one-year high in the week to Feb. 23

U.S. Commodity Futures Trading Commission data showed on Friday. SPDR Gold Trust, the world's larges

gold-backed exchange traded fund, said its holdings rose 0.27 percent to 762.41 tonnes on Friday, the highesin about a year. With US economy staying on the sweet spot the possibilities of further interest rate hikes in

this year have rose significantly from the beginning of this month, which has started to put pressure on gol

prices . Domestically we have a big day as the government is going to present the general budget for the yea

2016-2017, where it is expected to announce a policy to curb the gold imports which is putting burden on th

current account deficit of the nation. Amidst the big economic event the markets can turn volatile as the price

on MCX are already trading at a discount in comparison to the COMEX prices in anticipation of a possibl

import duty cut .For the day we recommend a range based trade in gold.

Energy

MCX crude oil prices on Friday gained more than 5%, registering at Rs.2316/bbl for March month contract.On

weekly basis, WTI and Brent crude oil for April month contract gained around 3.20% and 6.30% respectively

whereas MCX crude oil for March month contract gained around 5%.Crude oil prices last week showed som

relief as the market witnessed products side inventory levels moving down. Rest other than the products sid

inventories, crude stocks and stocks at Cushing was most negative. Cushing stocks moved more than 6

million barrels and are near to its threshold levels.Overall crude stockpiles as per last week crossed 507 millio

barrels, which is all time high levels. Apart from this, if we see the fall in Baker Hughes rig count data, it’

quite supportive for crude prices in long term. 10 continuous weekly fall in active crude oil rigs have left jus400 operational rigs in the US region. Average levels as shown on right hand side have gone down from

couple of months. International agencies are predicting the same to continue its downtrend till 2017, which i

actually good for crude oil prices. Apart from this, refinery maintenance shutdown period is going on in the U

region, during which they will produce less products and thus inventory withdrawals can be seen and also

gasoline demand will surge.

U.S. natural gas futures slid Friday on steady forecasts for two more weeks o

warmer-than-normal weather, a day after the prior front month contract expired at its lowest level since 1999

Heating demand since the start of the industry's November-March winter season was running about 12 percen

below normal in the lower 48 U.S. states due to the warming effect of the El Nino weather pattern

Meteorologists predict that warmth will continue into March, with heating demand expected to be 26 percen

7/24/2019 Commodity Research Report 29 February 2016 Ways2Capital

http://slidepdf.com/reader/full/commodity-research-report-29-february-2016-ways2capital 6/9

below normal, according to Thomson Reuters Analytic. Despite the lack of heating demand, however

consumers have used about 1 percent more gas than usual so far this winter as the power sector burns record

levels of the fuel due to its low price compared with coal, which carries higher transport and environmenta

costs.

Base Metal

Copper prices surged on Friday to their highest level in more than three months as investors hoped for a

recovery in metals demand following stronger than expected U.S. economic data and a G20 policymakermeeting. Industrial metals joined rallies in oil and share markets as investors put fears about a struggling globa

economy on the back burner. U.S. consumer spending rose solidly in January while fourth quarter economi

growth was revised up to 1 percent, higher than expected. Some analysts were wary, however, due to concer

about growth in top metals consumer China. Copper demand growth in China slowed last year to about 2

percent and is not expected to improve significantly this year. China accounts for about half of global deman

estimated at around 22 million tonnes. The metals market appeared to shrug off a firmer U.S. currency, whic

makes dollar-denominated commodities more expensive for non-U.S. firms, while oil rose as traders reverse

bets on lower prices. Stock markets rose as G20 policymakers meeting in Shanghai sought common ground o

how to reboot a struggling global economy in the face of renewed financial and political risks. Setting the tonefor the Shanghai meeting of the Group of 20, China's central bank chief, Zhou Xiaochuan, said Beijing still ha

the room and tools to support the world's second largest economy

Industrial prices surged on Friday to their highest level in more than

three months as investors hoped for a recovery in metals demand following stronger than expected U.S

economic data and a G20 policymakers meeting. The Baltic Exchange confirmed on Friday it had received

number of "exploratory approaches" after the Singapore Exchange Ltd revealed it was seeking to buy th

business which has been the hub of the global shipping market for centuries.

The zinc price has pushed above its sister metal lead for the first time since November and is likely to remain

ascendant in coming months as speculators step up zinc buying on forecasts of shortages while l

NCDEX - WEEKLY NEWS LETTERS

Agri Sector Eye on Budget 2016

The Budget needs to outline measures to restore the health of the rural economy without increasing

unproductive subsidy spend. Rating firm CRISIL highlight six broad areas that require innovative polic

solutions:

1. Expand irrigation cover: In India, poor irrigation cover exposes agriculture to shocks from uneven rainfal

patterns. At the all-India level, irrigation covers only 46.9% of the total cropped area, exposing the rest t

monsoon shocks. Around 84% of pulses, 80% of horticulture, 72% of oil seeds, 64% of cotton and 42% o

cereals are cultivated in unirrigated conditions. The combined spending of Center and states on irrigation ha

been a mere 2% per year of their total spending in the last five years.

2. Extend direct benefits transfer (DBT) scheme to food and fertiliser subsidy: A critical step to funnellinresources into agriculture will require plugging leakages in the existing public distribution system (PDS). A

7/24/2019 Commodity Research Report 29 February 2016 Ways2Capital

http://slidepdf.com/reader/full/commodity-research-report-29-february-2016-ways2capital 7/9

per a 2015 study by Gulati and Saini3, 46.7% of the off-taken grain is leaked from PDS. This is the ga

between the grains off-taken by each state and consumption by the targeted consumer for the year 2011-12

Extending the DBT scheme to include food subsidy in addition to LPG transfers will help curb losses due to

leakages and result in significant savings for the government.

3. Farm investment versus farm subsidy: After coming to power, the National Democratic Alliance (NDA

government promised a technology-driven second Green Revolution in India.

Encourage production by making agriculture profitable: Profitability at the farm is low and declining as cost o

inputs continues to soar. And if that weren’t enough, input and output cost dynamics have been turning

unfavorable year af ter year, reducing the farmer’s profit margin.

4. Big push to crop insurance: One way to mitigate the pain from crop losses due to weather shocks i

through crop insurance. But in India, coverage remains low. For example, the Universal National Cro

Insurance Scheme, which merges all existing schemes, only covers 25% of all farmers and 20% of the area.An

AssochamSkymet survey (April 2015) found that crop insurance is not a natural choice for farmers. Only 19%

of respondents have their crops insured, exposing the rest to the vagaries of monsoon. Of the uninsured, 46%

were aware but not interested, 24% said the facility was not available to them, while the rest (11%) could no

afford to pay the insurance premium.

India to deliver 8,500 MT imported Pulses shortly:

India has released total 116334.85 MT of pulses seized as pert of the de-hoarding operations, in the market a

on February 23, 2016, Ram Vilas Paswan, Food Minister, informed Rajyasabha in a written reply on Friday

The Minister added that import of pulses is being made by Government through MMTC. Delivery of 8,50

MT pulses is expected shortly.

ndia has been under severe pressure owing to the shortfall in pulses production and subsequent rise in prices

The rise in the prices of pulses is due to several factors leading to demand & supply mismatch. Hoarding is on

such factor. De-hoarding operations are carried out by the State Governments under the Essential Commoditie

Act, 1955. All the States have been requested to enforce the Act effectively, the Minister said.As per 2nd

Advance Estimates for 2015-16, India expects total pulses production of 17.33 million tonnes during 2015-1

is marginally higher than the previous year’s production of 17.15 million tonnes. India imports pulses from

countries like Canada. India is Canada's biggest export market for pulses. India is the largest importer o

Canadian lentils so far this year. Analysts from Canada expects India will continue to be the strongest importe

for the rest of 2016 as well as next year.

Chana

During Friday’s trading session NCDEX Chana April opened negative but later it traded upside during mos

part of the day and ended the session positive only. NCDEX Chana April futures ended the day at Rs 4258 pe

quintal which is 1.8% up against the previous day. Economic survey 2015 – 20 showed that in India most o

the land dedicated to growing pulses in each state is unirrigated and the national output of pulses come

predominantly from un-irrigated land. According to government sources, 116334.85 tonnes of pulses hav

been disposed off in the market out of 126758.59 tonnes seized from hoarders. In Maharashtra, 78,232.3

tonnes of pulses have been offloaded out of 80,167.44 tonnes seized from hoarders, while in Karnataka

7/24/2019 Commodity Research Report 29 February 2016 Ways2Capital

http://slidepdf.com/reader/full/commodity-research-report-29-february-2016-ways2capital 8/9

23,708.34 tonnes have been disposed out of 25,545.83 tonnes. Pulses output is expected to increase marginally

to 17.33 million tonnes in 2015-16 crop year from last year's 17.15 million tonnes though it's still not sufficien

to meet domestic demand. Every year around 4-5 million tonnes of pulses is getting imported in the country

According to the Canadian Grain Commission Canadian pea and lentil exports are slowing down, with only

10,200 tonnes of peas and 600 tonnes of lentils moved during the week ended February 21.

Turmeric

Turmeric futures extended their bearish trade on back of negative sentiments prevailing in the market. Mosactive contract opened lower; however traded in both directions for major parts of previous trade. Turmeri

April futures closed the trade at Rs. 8710 per quintal, with a loss of 0.6% w.r.t previous close. During previou

trade at Nizamabad, turmeric traded at Rs. 4025-931 for Finger variety and 4011-8279 for Bulb and arrival

were reported at 702.9 tonnes. Turmeric Erode finger and Bulb traded steady in range of Rs. 9300-9500 and

Rs.9000-9200 per quintal respectively. Stock positions at the NCDEX accredited warehouses are 279 tons a

on 26th Feb 2016.

Jeera

Jeera futures resumed down during Friday’s trading session after the two days of recovery. Long liquidation b

the investors along with improved supplies of fresh crops in the spot markets pulled down the prices from

higher levels. Therefore, jeera future prices traded and settled the day on at Rs.14130 per quintal with 0.4%

losses. On spot market front, Unjha spot market in Gujarat, prices hovered in the range of Rs.13700- 17000 pe

quintal. While at Rajkot market, prices were in the range of Rs.12400- 15500 per kg. The total arrivals reporte

at Rajkot market were around 180 tonnes. Stock positions at the NCDEX accredited warehouses are 230

tonnes as on 26 Feb 2016.

Caradamom

Cardamom futures resumed its trade in downward direction tracking weak supply and demand factors in the

market.Cardamom March futures closed the trade at Rs. 666.10 per kg, losing 0.93% from its previous clos

while the April futures closed with loss of 0.58% from its previous trade. Expectation of pick up in expor

demand limited the major losses for turmeric futures. During previous auction, cardamom arrivals were a

108300.2 kgs, higher by 87704.8 kgs from previous auction. Prices traded at Rs. 950 per kg, up by Rs. 93 from

its previous price for premium and Rs. 581.68 per kg on an average.Demand is good for cardamom sinc

almost complete daily arrivals are being sold. However, lack of availability of quality material for export i

limiting exporters from active buying in the market. As on 25th Feb 2016, MCX warehouses have 32.700 MT

eligible for delivery.

7/24/2019 Commodity Research Report 29 February 2016 Ways2Capital

http://slidepdf.com/reader/full/commodity-research-report-29-february-2016-ways2capital 9/9

LEGAL DISCLAIMER

This Document has been prepared by Ways2Capital (A Division of High Brow Market Research Investmen

Advisor Pvt Ltd). The information, analysis and estimates contained herein are based on Ways2Capita

Equity/Commodities Research assessment and have been obtained from sources believed to be reliable. Thi

document is meant for the use of the intended recipient only. This document, at best, represents Ways2Capita

Equity/Commodities Research opinion and is meant for general information only. Ways2Capita

Equity/Commodities Research, its directors, officers or employees shall not in any way to be responsible fo

the contents stated herein. Ways2Capital Equity/Commodities Research expressly disclaims any and al

liabilities that may arise from information, errors or omissions in this connection. This document is not to b

considered as an offer to sell or a solicitation to buy any securities or commodities.

All information, levels & recommendations provided above are given on the basis of technical & fundamenta

research done by the panel of expert of Ways2Capital but we do not accept any liability for errors of opinion

People surfing through the website have right to opt the product services of their own choices.

Any investment in commodity market bears risk, company will not be liable for any loss done on theserecommendations. These levels do not necessarily indicate future price moment. Company holds the right to

alter the information without any further notice. Any browsing through website means acceptance o

disclaimer.