Embed Size (px)

Citation preview

COMMITTEE OF THE WHOLE AGENDA REPORT

TO: Mayor Furniss and Members of Committee of the Whole

MEETING DATE: April 12, 2017

SUBJECT: ACCOUNTS RECEIVABLE POLICY C-FS-12

RECOMMENDATION: 1. That Committee of the Whole recommend to Township Council that Township Policy C-FS-12 (Accounts Receivable) be adopted as presented in the April 12, 2017 staff report.

APPROVALS: Date Signature

Submitted By: Shannon Johnson, Treasurer 30/03/17 Original signed by S. Johnson

Acknowledged: Steve McDonald, CAO 30/03/17 Original signed by S. McDonald

ORIGIN: Each year, the Township of Muskoka Lakes issues invoices to recover costs incurred in providing certain services. Some of these invoices become uncollectible during the course of the year for a variety of reasons. Staff recommends that the Treasurer be delegated authority to establish procedures and processes in order to write-off from the financial records of the Township amounts up to $10,000.00 that are deemed uncollectible. This delegation would allow the Township to increase efficiencies, comply with best practices of other area municipalities and to insure that the Township’s accounts receivable balance better reflects what is owed and is reasonably expected to be collected.

The write-off of accounts receivable does not prevent the Township from further pursing collection activity against an outstanding account as written in Township Policy C-FS-12, section 3 – Collection Process for Overdue Accounts

This policy does not apply to outstanding property taxes or Provincial Offences Act (POA) fines, which are governed by different By-laws, policies and procedures.

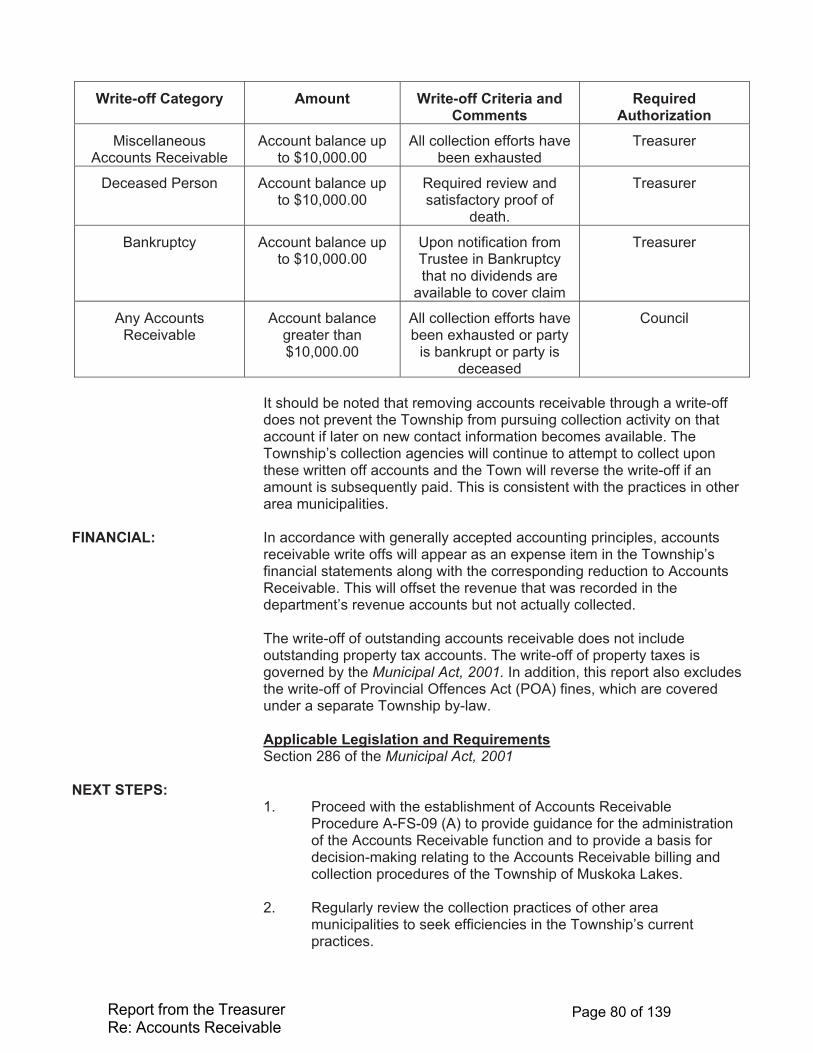

PURPOSE: To delegate authority to the Treasurer to deem accounts receivable as uncollectible and eligible for write-off in accordance with the associated policy. Under the Township’s approved policy C-FS-12, the Treasurer can write-off an account receivable, when all reasonable steps to collect the amount owing have been unsuccessful. Accounts Receivable items are subject to write-off procedures as outlined below:

Report from the Treasurer Re: Accounts Receivable

Page 79 of 139

Write-off Category Amount Write-off Criteria and Comments

RequiredAuthorization

Miscellaneous Accounts Receivable

Account balance up to $10,000.00

All collection efforts have been exhausted

Treasurer

Deceased Person Account balance up to $10,000.00

Required review and satisfactory proof of

death.

Treasurer

Bankruptcy Account balance up to $10,000.00

Upon notification from Trustee in Bankruptcy that no dividends are

available to cover claim

Treasurer

Any Accounts Receivable

Account balance greater than $10,000.00

All collection efforts have been exhausted or party

is bankrupt or party is deceased

Council

It should be noted that removing accounts receivable through a write-off does not prevent the Township from pursuing collection activity on that account if later on new contact information becomes available. The Township’s collection agencies will continue to attempt to collect upon these written off accounts and the Town will reverse the write-off if an amount is subsequently paid. This is consistent with the practices in other area municipalities.

FINANCIAL: In accordance with generally accepted accounting principles, accounts receivable write offs will appear as an expense item in the Township’s financial statements along with the corresponding reduction to Accounts Receivable. This will offset the revenue that was recorded in the department’s revenue accounts but not actually collected.

The write-off of outstanding accounts receivable does not include outstanding property tax accounts. The write-off of property taxes is governed by the Municipal Act, 2001. In addition, this report also excludes the write-off of Provincial Offences Act (POA) fines, which are covered under a separate Township by-law.

Applicable Legislation and Requirements Section 286 of the Municipal Act, 2001

NEXT STEPS: 1. Proceed with the establishment of Accounts Receivable

Procedure A-FS-09 (A) to provide guidance for the administration of the Accounts Receivable function and to provide a basis for decision-making relating to the Accounts Receivable billing and collection procedures of the Township of Muskoka Lakes.

2. Regularly review the collection practices of other area municipalities to seek efficiencies in the Township’s current practices.

Report from the Treasurer Re: Accounts Receivable

Page 80 of 139

C-FS-12

THE CORPORATION OF THE TOWNSHIP OF MUSKOKA LAKES

TOWNSHIP COUNCIL POLICY Accounts Receivable

AUTHORITY: APPROVED: REVISED: Township Council Res. No: Res. No:

Date: Date:

The Corporation of the Township of Muskoka LakesTOWNSHIP POLICY C-FS-12

Page 1 of 3

PURPOSE: The purpose of this policy is to ensure the Township’s accounts receivable practices meet the goal of a responsible, cost effective and accountable local government as it promotes consistency and accountability with respect to the treatment of revenue owed to the Township for Township services.

POLICY: To ensure efficiency, consistency and accountability with respect to the following areas within Accounts Receivable:

1. Billing & Payment Terms2. Collection Process3. Write-offs4. Payment Methods5. Credit Balances

STANDARDS:

1. Billing & Payment Terms

The Township issues invoices on a timely basis upon receipt of an invoice request that has been approved by the invoicing Department’s Supervisor/Manager as well as sufficient documentation supporting the request.

The Township has the authority to charge interest on accounts in arrears as allowed by provincial legislation. If an account is outstanding greater than thirty days, this receivable is considered to be in arrears. A monthly interest rate, consistent with the interest rate charged on outstanding property taxes, will be applied to all overdue balances unless different payment terms have been stipulated in an official agreement with the Township.

The payments shall be applied first against all accrued interest with the remaining being applied to principal of the first outstanding account noted on the payment remittance. The remaining amount of the payment will be applied in order of the oldest to the most recent arrears.

Report from the Treasurer Re: Accounts Receivable

Page 81 of 139

The Corporation of the Township of Muskoka LakesTOWNSHIP POLICY C-FS-12

Page 2 of 3

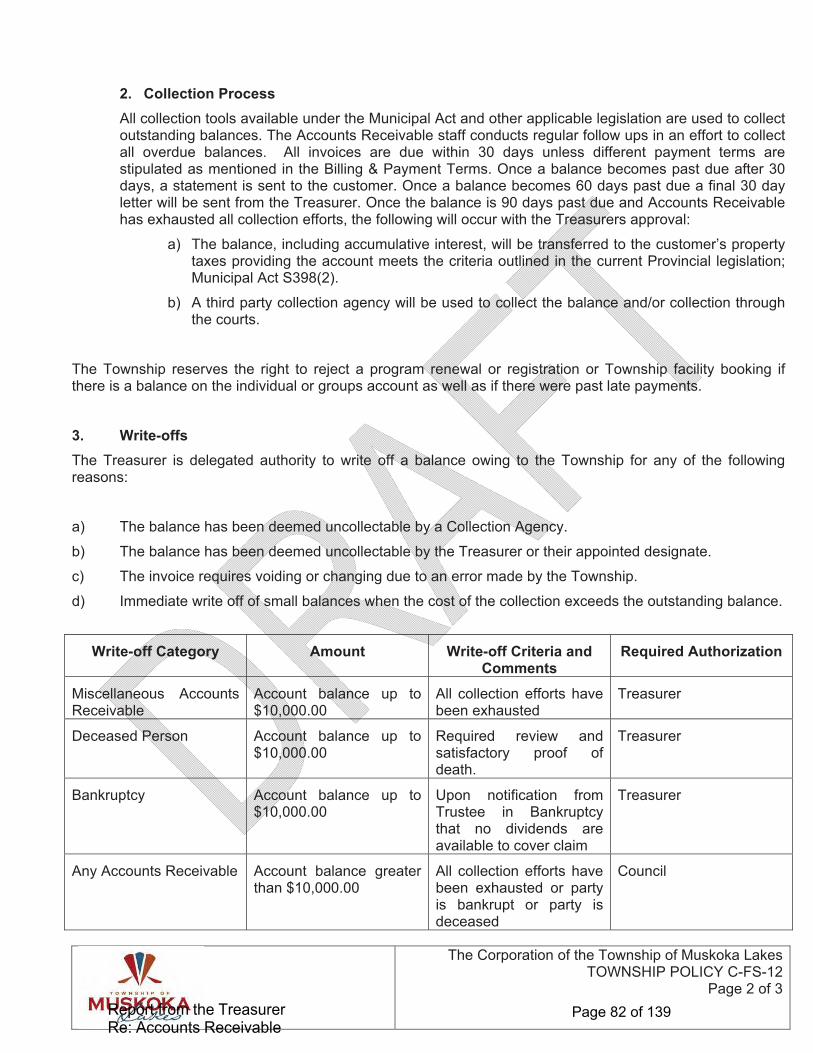

2. Collection Process

All collection tools available under the Municipal Act and other applicable legislation are used to collect outstanding balances. The Accounts Receivable staff conducts regular follow ups in an effort to collect all overdue balances. All invoices are due within 30 days unless different payment terms are stipulated as mentioned in the Billing & Payment Terms. Once a balance becomes past due after 30 days, a statement is sent to the customer. Once a balance becomes 60 days past due a final 30 day letter will be sent from the Treasurer. Once the balance is 90 days past due and Accounts Receivable has exhausted all collection efforts, the following will occur with the Treasurers approval:

a) The balance, including accumulative interest, will be transferred to the customer’s propertytaxes providing the account meets the criteria outlined in the current Provincial legislation;Municipal Act S398(2).

b) A third party collection agency will be used to collect the balance and/or collection throughthe courts.

The Township reserves the right to reject a program renewal or registration or Township facility booking if there is a balance on the individual or groups account as well as if there were past late payments.

3. Write-offs

The Treasurer is delegated authority to write off a balance owing to the Township for any of the following reasons:

a) The balance has been deemed uncollectable by a Collection Agency.

b) The balance has been deemed uncollectable by the Treasurer or their appointed designate.

c) The invoice requires voiding or changing due to an error made by the Township.

d) Immediate write off of small balances when the cost of the collection exceeds the outstanding balance.

Write-off Category Amount Write-off Criteria and Comments

Required Authorization

Miscellaneous Accounts Receivable

Account balance up to $10,000.00

All collection efforts have been exhausted

Treasurer

Deceased Person Account balance up to $10,000.00

Required review and satisfactory proof of death.

Treasurer

Bankruptcy Account balance up to $10,000.00

Upon notification from Trustee in Bankruptcy that no dividends are available to cover claim

Treasurer

Any Accounts Receivable Account balance greater than $10,000.00

All collection efforts have been exhausted or party is bankrupt or party is deceased

Council

Report from the Treasurer Re: Accounts Receivable

Page 82 of 139

The Corporation of the Township of Muskoka Lakes TOWNSHIP POLICY C-FS-12

Page 3 of 3

4. Payment Methods

The following methods of payment are accepted by Accounts Receivable for balances due:

a) Cash (*)

b) Debit

c) Cheque (*)

* Canadian currency only

Certified funds are required when replacing a payment that was returned by a financial institution.

5. Credit Balances

Any credit balance will be applied as a reduction to any outstanding invoices on the account. In the absence of such, the credit balance should be refunded to the payer by cheque. No refunds will be made by cash or debit cards.

ADMINISTRATIVE PROCEDURES:

Forms and instructions for their completion, signature and submission will be contained in a detailed Administrative Procedure.

1

CROSS REFERENCES:

Report from the Treasurer Re: Accounts Receivable

Page 83 of 139