Embed Size (px)

Citation preview

EN Official Journal of the European Communities L 246/14.9.98

II

(Acts whose publication is not obligatory)

COMMISSION

COMMISSION DECISION

of 11 March 1998

relating to a proceeding under Articles 85 and 86 of the EC Treaty

(Case Nos IV/34.073, IV/34.395 and IV/35.436 Van den Bergh Foods Limited)

(notified under document number C(1998) 292)

(Only the English text is authentic)

(98/531/EC)

THE COMMISSION OF THE EUROPEAN COMMUNTIES,

Having regard to the Treaty establishing the EuropeanCommunity,

Having regard to Council Regulation No 17 of6 February 1962, first Regulation implementingArticles 85 and 86 of the Treaty (1), as last amended bythe Act of Accession of Austria, Finland and Sweden, andin particular Article 3(1) thereof,

Having regard to the applications lodged underArticle 3(2) of Regulation No 17 by Masterfoods Limitedand Valley Ice Cream (Ireland) Limited against Van denBergh Foods Limited, formerly HB Ice Cream Limited,alleging that they are being hindered, in restraint ofcompetition, in selling their ice-cream products inIreland,

Having regard to the Commission Decision of 29 July1993 to initiate proceedings in this case,

Having regard to the application for negativeclearance/excemption lodged pursuant to Article 4(1) ofRegulation No 17 by Van den Bergh Foods Ltd on9 March 1995 for its distribution arrangements forimpulse ice-cream products in Ireland,

(1) OJ 13, 21.2.1962, p. 204/62.

Having given the undertaking concerned, pursuant toArticle 19(1) of Regulation No 17 in conjunction withCommission Regulation No 99/63/EEC of 25 July 1963on the hearings provided for in Article 19(1) and (2) ofCouncil Regulation No 17 (2), the opportunity of beingheard on the matters to which the Commission has takenobjection,

Having consulted the Advisory Committee on RestrictivePractices and Dominant Positions,

Whereas:

I. INTRODUCTION

(1) This Decision relates to the arrangements by Vanden Bergh Foods Limited, formerly known as HBIce Cream Limited, (hereinafter ‘HB’) for thedistribution of its impulse ice-cream products inIreland. HB pursues a policy under which it makesfreezer cabinets available to retail outlets stockingits ice-cream products on the basis of cabinetexclusivity.

(2) OJ 127, 20.8.1963, p. 2268/63.

EN Official Journal of the European CommunitiesL 246/2 4.9.98

(2) On 18 September 1991, Master Foods Limited,trading as Mars Ireland, (hereinafter ‘Mars’)lodged with the Commission a complaint (3) underArticle 3 of Regulation No 17 against HB, inrespect of the latter’s provision to a large numberof retailers of freezer cabinets on the basis ofcabinet exclusivity. Mars claims that it is beinghindered, in restraint of competition, from gainingaccess to retail outlets for the sale of its impulseice-cream products in Ireland by reason of thispractice.

(3) Mars entered the Irish ice-cream market in 1989.In April 1990, the Irish High Court granted aninterlocutory injunction to HB which preventedMars products from being placed in HB freezercabinets. In May 1992, the High Court (4) grantedHB a permanent order restraining Mars frominducing retailers to store its ice-cream products inHB’s cabinets. The court further held that HB’spolicy of freezer exclusivity was not caught by theprohibition contained in Article 85(1). It alsofound that Article 86 had not been infringed,either by HB’s exclusivity or by its pricing policies.The court did, however, consider that HB helda dominant position on the Irish impulseice-cream market. Mars has appealed against thesejudgments to the Irish Supreme Court.

(4) On 22 July 1992, Valley Ice Cream (Ireland)Limited (‘Valley’) lodged with the Commission acomplaint (5), against HB similar in terms to theMars complaint. Valley was a manufacturer of icecream in Ireland, but went into liquidation in1997. It had, until shortly before that, been actingas principal distributor for Mars ice-creamproducts in Ireland.

(5) On 29 July 1993, the Commission provisionallyconcluded that the system of distribution at thattime operated by HB infringed both Article 85 andArticle 86, addressing a Statement of Objectionsagainst HB to that effect. HB contested theCommission’s view of the legality of itsdistribution arrangements.

(6) In its Statement of Objections, the Commissiondid accept that HB’s arrangements bring aboutsome improvement in distribution, but found thatthis was outweighed by the harmful effects ofrestricted competition. It was none the less madeclear that HB remained at liberty to proposean alteration to its distribution arrangementsfor impulse ice cream in Ireland which might be

(3) Case No IV/34.073.(4) Masterfoods v. HB Ice Cream, [1992] 3 CMLR 830.(5) Case No IV/34.395.

capable of qualifying for an exemption pursuantto Article 85(3). While maintaining its view asto the legality of its current distributionarrangements, and following discussions with theCommission, HB came forward with suchproposals. On 8 March 1995, these were notifiedto the Commission (6), which then issued astatement (7) expressing the prima facie view thatthe changes would merit exemption.

(7) On the basis of these proposals and in the light ofHB’s expressed expctations regarding their effectsin the market, on 15 August 1995(8) theCommission announced its intention to take afavourable view towards HB’s distributionarrangements as notified. The changes did not,however, achieve the expected results in terms ofopened outlets. In view of this and of the situationas it currently stands in the market, theCommission has revised its expressed intention(see paragraph 247 et seq.). Accordingly, on22 January 1997 the Commission sent a newStatement of Objections to HB. HB submitted itswritten response thereto on 24 April 1997, andput forward its arguments at an oral hearing heldon 11 June 1997.

II. THE FACTS

1. The product

(i) Ice cream generally

(8) The essential raw materials for the production ofice cream include milk (including skimmed milk),fat (milk or vegetable) and sugar. Other additionsmay include, inter alia, emulsifying and stabilisingagents, colouring and flavouring substances, nuts,chocolate, and fruit concentrate. Legislationconcerning product definition, labelling, andpermitted contents (air coefficient etc.) variessomewhat between the different Member States.The contents of frozen yoghurt, ‘water ices’/‘ice

(6) Case No IV/35.436.(7) Commission press release of 8 March 1995 IP/95/229.(8) OJ C 211, 15.8.1995, p. 4; publication pursuant to

Article 19(3) of Regulation No 17, which contained asummary of HB’s distribution arrangements as revised,inviting the comments of interested third parties. Commentswere received from Mars.

EN Official Journal of the European Communities L 246/34.9.98

pops’ (water-based products) and ‘soft’/‘whipped’ice cream (which is made with vegetable fat andhas no dairy content) differ substantially fromice-cream products generally.

(9) Ice-cream products must be kept at a lowtemperature during all stages of production anddistribution before ultimate consumption. Anexception to this is soft ice cream which isdelivered to a retailer in the form of an ambientsoft mix (sold to retailers either as a ‘fresh’ or‘sterile’ product), and is only transformed into afinal product by being processed through specialdispensing equipment on the retailer’s premises.

(10) Ice cream can be categorised according to how itis manufactured and distributed. A distinction isusually made between ‘artisan’ ice cream on theone hand, which is generally produced, distributedand consumed locally on a small scale, andindustrial ice cream on the other, which isproduced for wide-scale distribution. Almost all ofthe ice cream produced and sold in Ireland is ofthe industrial kind.

(11) Ice cream can also be categorised accordingto where it is intended to be consumed. Thisgenerally includes three categories:

— ‘impulse’ ice cream, consisting of single-wrapped items (often stick products), andindividual portions of ‘scooped’ ice cream,designed for immediate consumption at or nearthe place of purchase,

— ‘take-home’ ice cream, including multipacks ofsingle items, blocks, tubs, dessert products andso on, intended for consumption at home,

— catering ice cream, which is sold in bulkto hotels, restaurants, cafés, etc., forconsumption, as part of a catering service,in those places.

(ii) Impulse ice cream

(12) Single-wrapped items of impulse ice cream aregenerally stored in self-service freezer cabinetsinstalled in or just outside the retailer’s premises.The cabinets are usually prominently positioned.As with all products relying on impulse purchasingdecisions, availability and visibility at point of sale

are important factors in the sale of impulse icecream. If the product is not available or visible,that is a sales opportunity which may bepermanently lost (9), consumers of impulse icecream will in general not travel to buy, ordefer a purchasing decision. Access to wide-scale distribution is particularly crucial for thesampling by consumers of new products, therebystimulating demand for those products. Single-wrapped impulse ice-cream products are almostinvariably branded products, supported byconsiderable investment in advertising and otherpromotional activity.

(13) Seasonal factors have a considerable effect on theconsumption of impulse ice cream, with most salesbeing made during the summer months. In 1992,for example, approximately two thirds of HB’simpulse sales were made in the four-month periodfrom May to August. Sales also depend to asubstantial degree on the weather.

(14) While children are particularly important aspurchasers of single item ice-cream products, thetrend in new industrial impulse lines is towards‘premium’ or ‘super premium’ items (termsgenerally denoting products with a high dairy fatcontent and a low proportion of air), whichappeal primarily to adult consumers. These aremore highly priced products aimed at a widermarket which includes adults, and represent thefastest growing segment of the impulse market.

(15) Scooping ice cream is delivered in bulk form tothe retailer, who generally stores it in aspecially-designed freezer cabinet and serves it to acustomer on a cone. In Ireland, scooping ice creamis of only marginal importance in terms of sales.

(16) Soft ice cream is delivered in the form of anambient soft mix to the retailer, who must thenfurther process the mix by the addition of furtheringredients and by the use of special dispensingequipment which transforms it into the low-

(9) Noel McEneaney, HB’s Marketing Manager is quoted in theMarch 1996 issue of the Irish retail magazine ‘Shelflife’ assaying: ‘There is a rule of thumb that for every three peoplewho purchase an impulse product, only one entered the shopwith the intention of buying an ice cream. We try tomaximise this factor by ensuring that the first thing thecustomer sees when he or she enters the shop is an ice-creamcabinet, either inside the entrance or next to the cashregister’.

EN Official Journal of the European CommunitiesL 246/4 4.9.98

temperature product which is served to thecustomer. Soft ice cream is usually served on awafer cone.

(17) From the manufacturer’s point of view, large-scalebusiness in impulse ice cream is capital intensiveand involves considerable business risks due to itsdependence on unpredictable weather conditions.It requires high levels of working capital in orderto finance manufacture in advance of the seasonand to hold stocks. Considerable logistical andplanning demands are imposed on the businessover the annual cycle in order to support therelatively short campaign season.

2. The ice-cream market in the Community

(18) Within the Community, Member States’ ice-creammarkets demonstrate different characteristics. Theannual consumption of ‘artisan’ ice cream, forexample, ranges from over six litres per capita inItaly to less than half a litre per capita in Spain,and even less in Ireland. Industrial supply accountsfor most of the products sold in Europe.Production of industrial ice cream is highest in theUK and, in descending order, in Germany, Italyand France. Sales of impulse ice cream as aproportion of the total ice-cream market also varyconsiderably between Member States.

(19) Companies in the Unilever group are the largestice-cream suppliers in most Member States. In theimpulse sector, Unilever companies are the marketleaders in every Member State with the exceptionof Spain, Greece and Finland. The Nestlé,Artic/Beatrice, Grand Metropolitan and Schöllergroups all sell ice cream in more than one MemberState. Some of these groups of companies.Unilever and Nestlé for example, trade in differentMember States under different names.

(20) National legislation on the content of ice creamis not harmonised in the Community. Thedifferences that exist, especially those relating tothe permitted types of dairy and vegetable fat, maygive rise to material differences in the productsavailable in different Member States and in theircost. Average retail prices for similar and evenidentical ice-cream products can also varysignificantly from one Member State to another.An analysis, however, of the range of products onoffer for sale by suppliers operating in severalmarkets shows that similar or identical productsare often sold under different product or brand

names. There is, moreover, a considerable volumeof trade between Member States in ice-creamproducts.

(21) The practice of supplying freezer cabinets toretailers subject to a condition of exclusivity iswidely employed by ice-cream manufacturers anddistributors throughout Europe, both bycompanies of the Unilever group and by many ofits competitors.

3. The ice-cream market in Ireland

(i) General

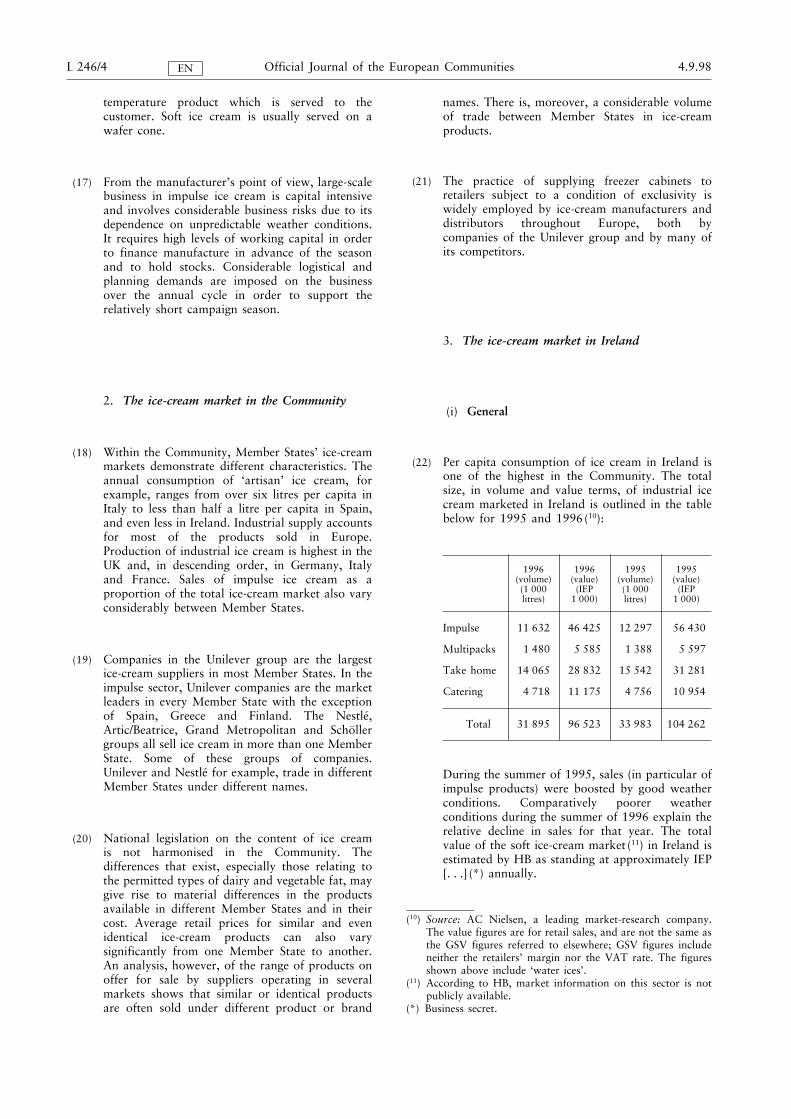

(22) Per capita consumption of ice cream in Ireland isone of the highest in the Community. The totalsize, in volume and value terms, of industrial icecream marketed in Ireland is outlined in the tablebelow for 1995 and 1996(10):

1996(volume)(1 000litres)

1996(value)

(IEP1 000)

1995(volume)(1 000litres)

1995(value)

(IEP1 000)

Impulse 11 632 46 425 12 297 56 430

Multipacks 1 480 5 585 1 388 5 597

Take home 14 065 28 832 15 542 31 281

Catering 4 718 11 175 4 756 10 954

Total 31 895 96 523 33 983 104 262

During the summer of 1995, sales (in particular ofimpulse products) were boosted by good weatherconditions. Comparatively poorer weatherconditions during the summer of 1996 explain therelative decline in sales for that year. The totalvalue of the soft ice-cream market (11) in Ireland isestimated by HB as standing at approximately IEP[. . .] (*) annually.

(10) Source: AC Nielsen, a leading market-research company.The value figures are for retail sales, and are not the same asthe GSV figures referred to elsewhere; GSV figures includeneither the retailers’ margin nor the VAT rate. The figuresshown above include ‘water ices’.

(11) According to HB, market information on this sector is notpublicly available.

(*) Business secret.

EN Official Journal of the European Communities L 246/54.9.98

(ii) HB

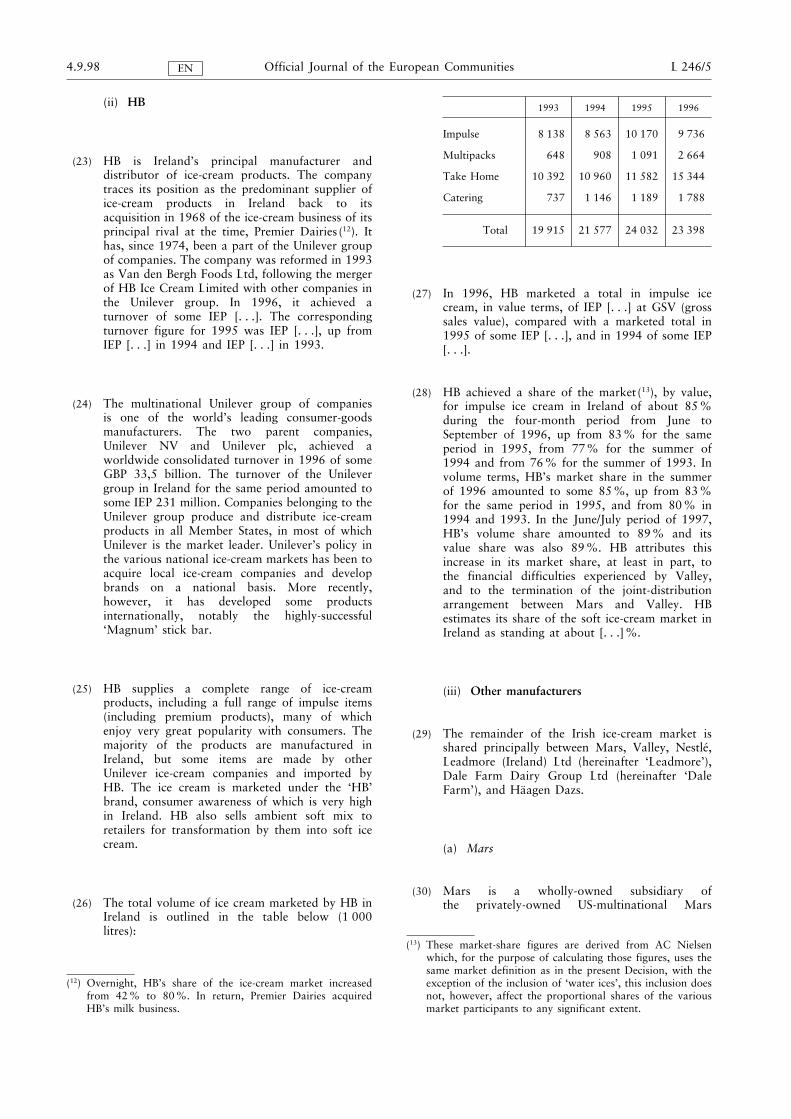

(23) HB is Ireland’s principal manufacturer anddistributor of ice-cream products. The companytraces its position as the predominant supplier ofice-cream products in Ireland back to itsacquisition in 1968 of the ice-cream business of itsprincipal rival at the time, Premier Dairies (12). Ithas, since 1974, been a part of the Unilever groupof companies. The company was reformed in 1993as Van den Bergh Foods Ltd, following the mergerof HB Ice Cream Limited with other companies inthe Unilever group. In 1996, it achieved aturnover of some IEP [. . .]. The correspondingturnover figure for 1995 was IEP [. . .], up fromIEP [. . .] in 1994 and IEP [. . .] in 1993.

(24) The multinational Unilever group of companiesis one of the world’s leading consumer-goodsmanufacturers. The two parent companies,Unilever NV and Unilever plc, achieved aworldwide consolidated turnover in 1996 of someGBP 33,5 billion. The turnover of the Unilevergroup in Ireland for the same period amounted tosome IEP 231 million. Companies belonging to theUnilever group produce and distribute ice-creamproducts in all Member States, in most of whichUnilever is the market leader. Unilever’s policy inthe various national ice-cream markets has been toacquire local ice-cream companies and developbrands on a national basis. More recently,however, it has developed some productsinternationally, notably the highly-successful‘Magnum’ stick bar.

(25) HB supplies a complete range of ice-creamproducts, including a full range of impulse items(including premium products), many of whichenjoy very great popularity with consumers. Themajority of the products are manufactured inIreland, but some items are made by otherUnilever ice-cream companies and imported byHB. The ice cream is marketed under the ‘HB’brand, consumer awareness of which is very highin Ireland. HB also sells ambient soft mix toretailers for transformation by them into soft icecream.

(26) The total volume of ice cream marketed by HB inIreland is outlined in the table below (1 000litres):

(12) Overnight, HB’s share of the ice-cream market increasedfrom 42% to 80%. In return, Premier Dairies acquiredHB’s milk business.

1993 1994 1995 1996

Impulse 8 138 8 563 10 170 9 736

Multipacks 648 908 1 091 2 664

Take Home 10 392 10 960 11 582 15 344

Catering 737 1 146 1 189 1 788

Total 19 915 21 577 24 032 23 398

(27) In 1996, HB marketed a total in impulse icecream, in value terms, of IEP [. . .] at GSV (grosssales value), compared with a marketed total in1995 of some IEP [. . .], and in 1994 of some IEP[. . .].

(28) HB achieved a share of the market (13), by value,for impulse ice cream in Ireland of about 85%during the four-month period from June toSeptember of 1996, up from 83% for the sameperiod in 1995, from 77% for the summer of1994 and from 76% for the summer of 1993. Involume terms, HB’s market share in the summerof 1996 amounted to some 85%, up from 83%for the same period in 1995, and from 80% in1994 and 1993. In the June/July period of 1997,HB’s volume share amounted to 89% and itsvalue share was also 89%. HB attributes thisincrease in its market share, at least in part, tothe financial difficulties experienced by Valley,and to the termination of the joint-distributionarrangement between Mars and Valley. HBestimates its share of the soft ice-cream market inIreland as standing at about [. . .]%.

(iii) Other manufacturers

(29) The remainder of the Irish ice-cream market isshared principally between Mars, Valley, Nestlé,Leadmore (Ireland) Ltd (hereinafter ‘Leadmore’),Dale Farm Dairy Group Ltd (hereinafter ‘DaleFarm’), and Häagen Dazs.

(a) Mars

(30) Mars is a wholly-owned subsidiary ofthe privately-owned US-multinational Mars

(13) These market-share figures are derived from AC Nielsenwhich, for the purpose of calculating those figures, uses thesame market definition as in the present Decision, with theexception of the inclusion of ‘water ices’, this inclusion doesnot, however, affect the proportional shares of the variousmarket participants to any significant extent.

EN Official Journal of the European CommunitiesL 246/6 4.9.98

Incorporated. As such, it is part of aninternational group with subsidiaries in mostMember States. Mars first entered the ice-creammarket when it purchased Dove, a US ice-creamcompany. Building on the renown of its ambientconfectionery brands, Mars developed ice-creamversions of some of those brands, therebyextending them into another product category.Mars manufactures all of its ice cream for theEuropean market at its production facilities inFrance (Doveurope SA) and uses the same productnames in each Member State. It first launched itsice-cream products in Europe in 1988.

(31) Mars began selling its ice cream in Ireland, insingle-item form as well as in multipacks, in 1989.The brands’ already high recognition amongconsumers reduced the costs of market launch.The range of ice-cream products offered by Marsis limited to a relatively small number of items,most of which are in the premium (high-price)segment of the market and appeal primarily toadult consumers.

(32) Mars’ market share in value terms for impulse icecream in Ireland during the period from June toSeptember 1996 was about 6%, down from 7%for the same period in 1995, and down fromabout 10% for the summer of 1994 and 14% for1993. Mars’ shares in volume terms are somewhatlower, reflecting the premium nature of the rangeof products which it offers. In the summers of1995 and 1996, it achieved some 4%, down fromabout 6% in summer 1994, and from 8% in1993. In the June/July period of 1997, Mars’volume share amounted to 4% and its value sharewas 5%.

(b) Valley

(33) Until its liquidation in October 1997, Valleysupplied a wide range of impulse ice-creamproducts, though it did not offer products in thepremium category. Valley had a history offinancial difficulty, including its liquidation andsubsequent reconstitution in 1985. It had a marketshare (value) in the summer of 1996 of about 6%,compared with a share for 1994 and 1995 of 7%,and for 1993 of 5%. Its share in volume termsamounted to about 8% in 1996, compared to 9%the previous year. In the June/July period of 1997,Valley’s volume share amounted to 3% and itsvalue share was 2%. From 1989 until early 1997,Valley was the primary distributor of Mars’impulse ice-cream products.

(c) Nestlé

(34) Nestlé is a multinational company with ice-creamsubsidiaries in most Member States. Nestlé enteredthe Irish market in 1994, and achieved a marketshare by value and volume of about 2% in 1995and 1996, up from about 1% in 1994. In theJune/July period of 1997, Nestlé’s volume andvalue shares both amounted to 2%.

(d) Häagen Dazs

(35) Häagen Dazs (part of the Grand Metropolitangroup of companies) entered the Irish impulseice-cream market in 1993 with a limited range ofpremium-priced luxury ice creams. Its share of theimpulse ice-cream market is very small and is notseparately calculated by Nielsen.

(e) Dale Farm

(36) Dale Farm, a subsidiary of the UK dairy companyNorthern Foods, is a company primarily based inNorthern Ireland and the market leader there; itdistributes its ice-cream products via independentfranchisees and agents. It secured a 1% volumeand value market share in the summers of 1995and 1996, up from 0,5% in 1994. In the June/Julyperiod of 1997, Dale Farm’s volume and valueshares both amounted to 1,5%. Dale Farm alsodistributes Mars’ products, though these aresupplied to it by the UK, rather than the Irish,Mars subsidiary.

(f) Leadmore

(37) Leadmore is a regional producer of ice-creamproducts. In December 1994, Leadmore Ice CreamLtd went into receivership. It was purchased as agoing concern from the receiver in May 1995 andreconstituted as Leadmore (Ireland) Ltd.Leadmore achieved a value market share of about0,5% in the summers of 1995, 1996 and June/July1997, down from 3% in the summer of 1994.Leadmore largely operates within a limitedgeographic area.

(g) Soft-mix suppliers

(38) Apart from HB (see above), the other principalsuppliers of soft mix in Ireland are: R&F Martin(trading under the name ‘Angelito’s’), with anestimated 35% market share; Pritchards, with anestimated 20% share; other suppliers includeLeepatrick Dairies and Dawn Dairies, with evensmaller shares.

EN Official Journal of the European Communities L 246/74.9.98

4. Distribution channels for impulse ice cream inIreland

(i) General

(39) In Ireland, industrial impulse ice cream isdistributed to consumers through a wide array ofretail and other outlets ranging from grocerystores, the ‘traditional’ retail trade (often referredto as TSNs — tobacconists, sweetshops,newsagents), garage forecourts, and kiosks toplaces of entertainment and leisure. By far themost important outlets for impulse sales are thetraditional retail trade, grocery stores (includingsymbol/franchise groups) and garages. This isillustrated by AC Nielsen surveys (14) of theice-cream market in Ireland for the summer of1992 and April/May 1995 which gave thefollowing breakdown (in value terms) of impulseice cream sold through the different retailchannels:

June/July1992

August/September

1992

April/May1995

Multiples 3% 4% 2%

Grocery 60% 59% 55%

TSN/garages 37% 37% 43%

(40) The AC Nielsen retail censuses for 1991 and 1994show the following retail outlet structure forthe food and confectionery trade (numbers ofoutlets):

1991 1994

Multiples 154 160

Symbol groups 999 1 015

Grocery 6 069 5 652

TSNs 1 864 1 863

Garages 1 186 979

Total 10 272 9 669

(14) AC Nielsen’s impulse ice cream audit is the only regularreliable source of market data concerning the distribution ofimpulse ice cream in Ireland. The outlets included inNielsen’s ‘Universe’ are the same as those surveyed for itsambient confectionery audit and excludes some marginal icecream outlets such as cinemas, theatres and ice-creamstands.

(41) As can be seen, the structure has changed littleover the three-year period, except for a decline inthe number of grocery outlets. Most of theseoutlets sell impulse ice cream. In 1994, theproportion was 95%. HB estimates the number ofretail outlets selling impulse ice cream as standing(in 1997) at 9 454, on the basis of the AC Nielsenfigures.

(42) Multiples (a category of outlets essentiallycomprising supermarkets) sell principallytake-home ice cream, including multipacks, andthese are often stored, as are frozen foods, in theretailers’ own freezer cabinets. It should also benoted that in some of the smaller grocery outletsin Ireland, impulse and take-home ice-creamproducts can be sold from the same outlets andeven from the same freezer cabinet.

(43) Normal retail outlets clearly have limited space forthe siting of freezer cabinets. The outlets whichare the most important for the sale of impulse icecream are generally small in area, and areconsequently under particular space constraints.Impulse ice cream is a marginal product for mostretailers, in that it will only account for a limitedpercentage of an outlet’s turnover and profits, andcompetes for sales space with a range of other(impulse and non-impulse) products, many ofwhich have the advantages that their sales are notseasonally variable and so annually may providehigher sales per unit of area (15). According toinformation provided by HB, ice cream amountsto only 8,5% in value of total sales in Ireland of‘impulse’ products (confectionery, soft drinks,savoury snacks and ice cream). Moreover, thespace which is available in an outlet is not all ofequal value for the sale of impulse products:prominence of display is crucial (see footnote 9).

(44) Access to distribution is normally measured interms of: (a) ‘unweighted (numeric) distribution’,namely the percentage of outlets offering impulseice cream, in numeric terms, where amanufacturer’s products are available; and (b)‘weighted distribution’, namely the percentage ofoutlets offering impulse ice cream where amanufacturer’s products are available, weightedfor turnover in impulse ice cream. Althoughweighted distribution is generally considered themore important measure of a company’sdistribution levels, in the case of impulse productsnumeric distribution is of particular importance: itis the most accurate indication of the widespreadavailability (and visibility) of the product toconsumers. The importance of high levels of

(15) The market survey carried out by Lansdowne in the summerof 1996, described in detail below, found that there wasonly minimal freezer movement to satisfy seasonal demandvariation (see paragraph 97).

EN Official Journal of the European CommunitiesL 246/8 4.9.98

numeric distribution is most pronounced whereimpulse products are being launched in the marketfor the first time, thereby increasing the chancethat consumers will try the product at least once.

(ii) HB

(45) HB ice-cream products are available in eachcategory of distribution channel referred to atparagraph 38. HB sells its impulse ice-creamproducts to [. . .] customers in total. [. . .] ([. . .]%) of HB’s customers have an annual turnover inHB impulse ice cream of less than IEP 1 500.

(46) According to AC Nielsen surveys conducted inIreland over the last few years, HB achieved about79% numeric distribution and 94% weighteddistribution for its impulse ice-cream products inthe August/September period of 1995. This meansthat its products were being sold from 79% ofoutlets by number (16), and that HB impulseproducts were being sold from outlets accountingfor 94% of total impulse ice-cream sales inIreland. The figures were almost the same in theJune/July period of that year, when the weightedshare was 95%. In June/July 1994, the numericand weighted distribution figures for HB were78% and 92% respectively. In August/Septemberof that year, the figures were 79% and 93%. Inthe June/July period of 1996, HB’s numericdistribution was 82% and its weighted share96%; in August/September 1996, the figuresremained unchanged, but in June/July 1997, HB’snumeric distribution was 85% and its weightedshare 97%.

(iii) Mars

(47) According to AC Nielsen, Mars achieved about35% numeric distribution and 48% weighteddistribution for its impulse ice-cream products inthe August/September period of 1995. The figureswere the same in the June/July period of that year.

(16) The real figures for unweighted/numeric distribution aresomewhat higher, because not all the outlets surveyed stockimpulse ice cream. For example, only 93% of all the outletssurveyed in this time period were selling impulse ice cream.In this instance, therefore, it is more accurate to adjust thefigure of 79% to 79/93 = 85%. A similar adjustment can bemade for all the time periods, but has not been for thepurposes of this Decision. The same distortion does notexist for the weighted figure.

In June/July 1994, the numeric and weighteddistribution figures for Mars were 36% and 56%respectively. In August/September of that year, thefigures were 34% and 52%. In the June/Julyperiod of 1996, Mars’ numeric distribution was32% and its weighted share 43%; inAugust/September 1996, the numeric figure was31% and the weighted share remained unchanged.In June/July 1997, its numeric distribution was30% and the weighted share 40%.

(48) Mars estimates (on the basis of a survey carriedout by its salesforce at the time) that, prior to thegranting of the interlocutory injunction by theIrish High Court in 1990 (subsequently madepermanent, see paragraph 3), preventing Marsfrom inducing retailers to stock Mars ice-creamproducts in HB cabinets, it had attained a level ofsome 42% numeric distribution in the impulseice-cream market in Ireland. This level wasreached within the first few months of the launchof its products in the Irish market and wasachieved, in large part, by the placing of Marsproducts in HB freezer cabinets. Following theinjunction, Mars estimates that its level ofdistribution fell to below 20%.

(iv) Other manufacturers

(49) Valley achieved numeric distribution in August/September 1995 of 29% and weighteddistribution of 36% in the same period. InJune/July 1995 the figures were 30% and 37%respectively. In June/July 1994, they were 28%and 39% respectively; in August/September 1994,they were 29% and 39% respectively. In theJune/July period of 1996, Valley’s numericdistribution was 26% and its weighted share31%; in August/September 1996, the weightedfigure was 30% and the numeric share remainedunchanged. In June/July 1997, its numericdistribution fell to 20% and its weighted share to19%.

(50) Nestlé achieved numeric distribution in August/September 1995 of 20%, and weighteddistribution of 25% in the same period. InJune/July 1995 the figures were 20% and 26%respectively. In June/July 1994, they were 19%and 18% respectively; in August/September 1994,they were 20% and 19% respectively. Most ofNestlé’s distribution figures in 1994 wereaccounted for by sales of just one of its range ofproducts, ‘Fruit Pastilles’. In the June/July periodof 1996, Nestlés numeric distribution was 19%and its weighted share 24%; in August/September1996, the numeric figure was 18% and the

EN Official Journal of the European Communities L 246/94.9.98

weighted share 25%. In June/July 1997, itsnumeric distribution increased to 20% and itsweighted share declined to 21%.

(51) Dale Farm achieved numeric distribution inAugust/September 1995 of 11%, and weighteddistribution of 12% in the same period. InJune/July 1995 the figures were 11% and 11%respectively. In June/July 1994, they were 5% and6% respectively; in August/September 1994, theywere 4% and 6% respectively. In the June/Julyperiod of 1996, Dale Farm’s numeric distributionwas 9% and its weighted share 8%; inAugust/September 1996, the numeric figure was8% and the weighted share 7%. In June/July1997, the numeric share was 11% and theweighted share 11%.

(52) Prior to going into receivership at the end of1994, Leadmore had secured in June/July 1994 a17% numeric distribution and a 15% weightedfigure. Its numeric distribution figure in the sameperiod of 1995 was some 10%. In the June/Julyperiod of 1996, Leadmore’s numeric distributionwas 7% and its weighted share 6%. In June/July1997, the numeric share was at 4% and theweighted share 7%.

5. Distribution arrangements for impulse icecream in Ireland generally

(53) The wide-scale distribution of industrial ice creamrequires, among other things, frequent deliveryusing refrigerated transport from the factory to thesales outlet or catering establishment, which mustin turn have cold-storage facilities (usually freezercabinets) on the premises. A manufacturer of icecream needs either to build up his owndistribution network for frozen products, or toconclude an agreement allowing him access to thedistribution network of another ice-creammanufacturer or wholesaler. A distributor needs tobe able to ensure frequent ‘drops’ and to respondto orders at short notice, particularly in summer.

(54) The custom in Ireland has been for manufacturerssupplying impulse ice cream to lend freezercabinets to the retailer free on loan (i.e. with nodirect charge) and subject to freezer-cabinetagreements, under which the retailer undertakesthat freezers are to be used exclusively for thestorage of the supplier’s products (cabinetexclusivity); this is illustrated in the marketresearch detailed below (see paragraphs 90 and91). The supplier usually provides a maintenanceservice for the freezer cabinets, also free of charge(with no direct charge). Manufacturers oftensupply most of their products to retailers direct,including via agents, without selling to

independent intermediaries; wholesale business inice cream is small-scale in Ireland.

(55) Until the disposal by HB of a portion of itscabinet fleet in 1996 (see paragraphs 72 and 73),there appear to have been very few retailer-ownedcabinets in place in Ireland for the storage and saleof impulse ice-cream products, as is illustrated bythe market research outlined at paragraph 85 etseq.

6. HB’s distribution arrangements for impulseice cream in Ireland

(i) General

(56) HB operates a direct distribution system to 80%of its ice-cream outlets in Ireland. Delivery is madedirect to the cabinet, whether it is owned by HBor otherwise. HB has regional depots, from whichlocal delivery in its own fleet of refrigerated vansis carried out. The remaining 20% of its outletsreceive deliveries from eight different local agentswho distribute on behalf of HB; the arrangementswith these distributors are long-standing and stemfrom logistical difficulties for HB in otherwiseachieving geographical coverage by directdistribution to all outlets. Within the Irish market,HB alone has a nationwide, vertically integrateddistribution network.

(57) HB provideds turnover-related discounts forpurchases of its ice cream (not applicable tosoft-mix ice cream). These are given in accordancewith a graduated scale ranging from (for 1997) a2% discount for purchases of IEP 1 350 to IEP2 750 to an 11% discount for purchases of IEP26 601 or more. The discounts are made availableto all retailers of HB ice cream irrespective of thequestion of cabinet ownership.

(ii) Cabinet provision

(a) HB-exclusive cabinets

(58) HB has for many years made available to retailersfreezer cabinets for the storage and display ofimpulse ice cream at the point of sale (17). Thecabinet is either loaned to the retailer with nodirect charge (see paragraphs 76 to 79) or leasedfor a nominal annual rent (IEP 1) which is notcollected. The maintenance and repair of thecabinets is also performed by HB. HB does not

(17) The storage of HB’s take-home ice-cream products is alsopermitted.

EN Official Journal of the European CommunitiesL 246/10 4.9.98

provide dispensing machinery to retailers for theprocessing of soft ice cream.

(59) The cabinet is supplied in accordance with astandard form contract concluded between HB onthe one hand and the retailer on the other; themain provisions of the cabinet agreement arethat:

— HB agrees to make a freezer cabinet availableto the retailer; the ownership and property inthe cabinet remains that of HB, and HBundertakes to maintain it at its own cost andexpense (save where damage is due to theretailer’s misuse or neglect of the cabinet),

— the cabinet is to be used exclusively for storingproducts for sale which are supplied by HB;accordingly no product manufactured orsupplied by a third party is to be sold oroffered for sale from the freezer cabinet, orstored therein,

— the agreement is terminable at any time byeither party giving two months’ notice (18),

— the retailer undertakes to keep the cabinet in aprominent position on his premises. Only HBadvertising material may be displayed on topof or on the sides of the cabinet.

(60) The number of retailers which whom HB has suchcabinet agreements (those supplied subject to acondition as to exclusivity) amounts (in 1997) to7 907. HB has given a breakdown of itsfreezer-cabinet agreements as follows:

1995 1996(1) 1997

Grocers 10 224 8 420 8 315

TSNs 1 749 1 440 1 410

Filling stations 1 170 951 925

Other outlets 323 487 500

Total 13 453 11 298 11 150

(1) These figures reflect the position in September 1996, and takeinto account the cabinets disposed of by HB during 1995 and1996 (see paragraphs 72 and 73).

(18) HB has, however, indicated that it does not in practice, seekto enforce the requirement of two months’ notice forretailers wishing to terminate on shorter notice or withoutnotice.

(61) HB has at present (in 1997) [. . .] cabinets installedin outlets in Ireland as ‘front-of-shop’ (19) cabinets.In 1995, HB marketed IEP [. . .] in outlets withHB freezer-cabinet agreements, representing [. . .more than 95% . . .] of the total impulse icecream marketed by HB in Ireland in that year (seeparagraph 27). In 1994, HB marketed IEP [. . .] inoutlets with HB freezer-cabinet agreements, whichalso represented [. . . more than 95% . . .] of thetotal impulse ice cream marketed by HB in Irelandin that year.

(62) It has not been HB’s official policy to provide acabinet to any outlet which offers to stock icecream. Instead, both financial and tradingcriteria (20) are applied. The financial criteria arebased on the marginal cost to HB involved intaking on a new outlet, coupled with anacceptable return on that investment. This includesan assessment therefore of (a) the net cost to HBof the cabinet, and (b) its variable margin on theassociated ice-cream sales through the outlet. Thetrading criteria are expressed as an annual salestarget, based on a minimum estimated turnover inthe outlet in question.

(63) Substantial overall economies are achieved whereHB, as opposed to individual retailers or evenlarge buying groups, bears the cost of purchasingand maintaining freezer cabinets. As part of theUnilever Group (which buys a very large numberof cabinets per year) HB obtains significantdiscounts for such scale purchases. By means ofillustration, HB estimates that the capital cost(including delivery, storage, handling and so on)to a retailer of purchasing a standard 1 m freezercabinet would be very considerably higher thanthe capital cost to HB of providing the samecabinet. HB employs its own refrigerationengineers for cabinet maintenance and repair, andalso uses the services of local refrigerationcompanies. During 1994, 1995 and 1996, HB’sexpenditure on freezer cabinets (includingpurchase, installation, maintenance, cabinet‘control’ and depreciation) amounted to [. . .]%,[. . .]% and [. . .]% of its turnover in impulse icecream, respectively, for each of the three years.

(19) Some cabinets are kept in the rear of the outlet for storagepurposes.

(20) HB has indicated, however, that, in practice, it does notalways insist on strict compliance with these criteria as anecessary precondition for receipt of an HB freezercabinet.

EN Official Journal of the European Communities L 246/114.9.98

(64) The importance attributed by the Unilever groupof companies to the policy of supplying freezercabinets subject to exclusivity became particularlyevident following the entry of Mars on theEuropean market in the late 1980s. The followingextracts (paragraphs 65 to 68) from companydocuments are an illustration of how crucialUnilever saw the maintenance of freezerexclusivity at that time.

(65) In a Unilever group document dated 3 September1990 and entitled ‘Mars’ position in Europe andthe FPC(21) response’, under the heading ‘Strategicapproach’, one of the points made is ‘. . . to makeevery effort to maintain cabinet exclusivity’.

(66) In another FPC document dated April 1989 andentitled ‘European ice cream marketing strategy’,reference is made to the importance of freezerexclusivity retaining ownership of the freezercabinet: ‘We must retain ownership of the cabinet,particularly where distribution is performed bythird parties, in order to retain, as far as possiblethrough exclusivity contracts, sole brand supply tothe fridge, and de facto, to the outlet’.

(67) The ‘Minutes of the marketing managers meeting’held in Rotterdam (an FPC document) inNovember 1989 contain the following statements:‘HB has driven Mars down to 400 HB outlets(4,2%) from their August peak of 1 920 cabinets(29,7%) by establishing a Special Task Force . . .In certain cases, they [HB] have been able to buyMars out of outlets. Diversion to otherrefrigeration in store and very selective cabinetwithdrawal is also being used . . .’; under theheading ‘Mars, What next?’, it is stated that, ‘Toachieve their economies of scale in productionMars needs to achieve significant volumeincreases. They need to break down thedistribution barrier . . . . Denying Marsdistribution is the key immediate response to theirentry . . .’.

(68) In a Unilever internal strategy document entitled‘Frozen products coordination, Sales DirectorsConference, June 1990, Vienna, highlights andfollow-up action’, the importance of freezerexclusivity is underlined. Under the heading

(21) Frozen products coordination.

‘Exlusivity’ it is stated: ‘We are all too aware thatin many countries one of the foundations of oursuccess, EXCLUSIVITY, is now under threat:

— Exclusivity at concessionaire and distributorlevel,

— Exclusivity in the outlets and cabinets’.

(b) Revision of cabinet policy

(69) In the light of the Commission’s Statement ofObjections of 29 July 1993 (see paragraph 5), andfollowing discussion with the Commission, HB hasrevised its distribution arrangements. These havebeen notified to the Commission, as an applicationfor negative clearance or, failing that, exemption(see paragraph 6). The revised arrangementsinclude the standard-form agreement under whichHB continues, on request, to supply HB-exclusivefreezer cabinets to retailers as just described(paragraphs 58 and 59), as well as HB’s standardconditions of sale and discount schedule (seeparagraph 57); these now include a new pricingscheme for its ice-cream products (seeparagraphs 76 to 79) and the introduction of ahire-purchase scheme (see paragraphs 70 and 71)designed to facilitate the acquisition of freezercabinets by retailers.

(70) HB has introduced, as an optional alternative tothe acceptance of an HB cabinet under thestandard-cabinet agreement, a freezer cabinethire-purchase scheme designed to enable retainersto buy their own new cabinet. The cabinets areoffered at the wholesale price at which HBpurchased them, as is evidenced by an invoicefrom the independent cabinet supplier. Under thescheme, retailers are offered a 1 m ‘visi-top’cabinet, available in respect of one cabinet peroutlet at any time. Details of the scheme arepublished on HB price lists and relevantpromotional material. Repayment is made over amaximum period of five years; the terms for earlyrepayment without penalty are made clear to theretailer. The credit rate should be the prevailinghire-purchase rate in Ireland (22). The cabinet is

(22) It should be determined in accordance with objectivecriteria, for example, the Bank of Ireland lending rate tosmall businesses.

EN Official Journal of the European CommunitiesL 246/12 4.9.98

to be exclusively used for the stocking of HBproducts during the period of repayment only.Maintenance is performed by Unilever throughoutthe repayment period, during which period hire-purchasers will qualify for the differential pricinglump sum (see paragraphs 76 to 79), minus themaintenance element (23).

(71) Unilever informed the Commission that it believedthat the scheme would ‘prove attractive to retailersand incentivise them to buy their own cabinets’.Since the introduction of the hire-purchase schemein Ireland in early 1995, not a single retailer hasavailed himself of the offer.

(72) As a means of achieving a substantial freeing up ofoutlets in the short term, Unilever undertook tothe Commission to ensure the sale of an in situ‘front-of-shop’ freezer cabinet with ‘a usefulremaining life’ to retailers in a significant number(some 20%) of the outlets in which its cabinetswere then (December 1994) installed; in total,1 750 cabinets were to be sold. No more than 400of such cabinets were to be sold in outlets with anannual turnover in HB impulse ice cream of belowIEP 650, and none were to be in outlets with aturnover of less than IEP 400 p.a. in thoseproducts. From the moment of sale, a retailer wasto be eligible for an annual lump sum under thedifferential pricing scheme (see paragraphs 76 to79). Sale was to be made to retailers with currentpossession of a sole HB cabinet. The price wasto be pitched at a level which would ensureachievement of these results. Sale was to be carriedout on a ‘one-off’ basis during 1995 and 1996;sale was to take place equally in 1995 and 1996,and a reasonable geographic spread was to beensured. The disposal of cabinets was intended to‘kick start’ a movement towards freezer cabinetownership by retailers. Unilever stated that theeffect of the measure would be ‘to provide, for the1995 season, a visible and material change to therelevant market. This (would) provide a ‘kickstart’ to the process, the future development ofwhich is underwritten by the dual price structureand the hire-purchase scheme’.

(23) The cost of maintenance was calculated as amounting to IEP[. . .] in 1995, and so the sum paid to hire-purchasers wasIEP [. . .] p.a. in that year. HB was to be flexible in relationto payment of the bonus to those who chose tohire-purchase during the course of 1995.

(73) In accordance with this undertaking, HB hasdisposed of [. . .] cabinets in [. . .] outlets since thebeginning of 1995; almost all of these disposalswere carried out during the first half of 1996(24)and [. . .]. According to HB, 1 750 of the disposalscomply with the conditions cited in paragraph 72.Almost all of the cabinets disposed of were modelsand types of cabinet which have not been newlyinstalled by HB in outlets over at least the last[. . .] years. The average age of the cabinetsdisposed of is just under [. . .] years (25). Not all ofthe cabinets disposed of had been installed inretail outlets; some ([. . .], according to HB) wereinstalled in schools, staff canteens, swimmingpools and the like. Over [. . .] customers acquiredmore than one cabinet under the disposal scheme.HB concentrated its disposals in what it describesas the ‘small-shop sector’. According to HB, thetotal turnover in impulse ice cream of all thoseoutlets which have acquired cabinets in this way isapproximately IEP [. . .].

(c) Recent cabinet instalation and productproliferation

(74) In 1994, HB intensified its modernisation of itsfreezer-cabinet stock, replacing many of the oldercabinet models (26). In 1993, [. . .] new cabinetswere installed in outlets; in 1994, [. . .]; in 1995,[. . .]; in 1996 to August, [. . .]. In general, the newcabinets take up more floor space in retail outlets(though they are, in some instances, smaller involume), not only in that they are larger in areabut also in that many are ‘island-type’ cabinetswhich should not adjoin other store fixtures or thewall of the store. HB talks of changing patterns inits cabinet fleet, which it identifies as the‘increasing popularity of the island cabinet model,largely at the expense of visitop and closed topmodels’, ‘a gradual increase in the proportion ofcabinets with a length in excess of 1 m’, and ‘a

(24) Only [. . .] were sold during 1995, and most of these in thelater part of the year.

(25) The average lifetime of a cabinet is estimated by HB to be10 years; cabinets are amortised by HB after eight years.

(26) HB states that it ‘undertook a programme designed tomaintain the image of the HB brand and the visibility of theHB product range by, inter alia, replacing ageing cabinetswith more modern units’; Mars states that ‘Unilever ran anexceptional freezer placement programme in 1994 and1995; a comparison between the two Rosslyn surveys showsthat the 1994/95 replacement rate was over 230% of the1990/91 replacement rate’. Mars goes on to say that ‘thenew Unilever freezers are all larger than the ones that theyreplace (save one type which has not been widely placed)’.

EN Official Journal of the European Communities L 246/134.9.98

gradual reduction in the overall size of cabinetstaking into account length, breadth and height’.According to HB, these patterns are explained by‘two principal factors’: ‘(i) the decline in theproportion of total outlets represented by TSNsand small independent grocers means that theproportion of the total cabinet fleet represented bythe 1 m visitop typical of such outlets has shown acorresponding decrease; and (ii) the introductionby manufacturers of new cabinets designed to bemore user friendly for the self-serving customerand, to that end, longer and shallower’.

(75) Mars points out that ‘Unilever’s general productproliferation, and range expansion has the aim offilling these freezers . . . so that retailers can bepersuaded that they have a ‘full range’ ofice-cream products and therefore have no need tosell competing manufacturers’ products’.

(d) Pricing arrangements

(76) Until March 1995, HB supplied its ice-creamproducts and freezer cabinets at an ‘inclusive’price. This price included the capital costs of thecabinet, its maintenance costs and the value of theice-cream products. All retailers were charged thesame price irrespective of the ownership of thecabinets in which the products are stocked. Thus,a retail outlet with its own freezer cabinet paid thesame price for HB ice cream as a retailer acceptingthe offer of an HB freezer. In the 1993 Statementof Objections (see paragraph 5), the Commissionreached the provisional conclusion that thispricing policy infringed Article 86 of the ECTreaty in that it discriminated against retailerswho had not taken an HB freezer cabinet, butwho none the less purchased HB ice cream. TheCommission provisionally concluded that theinclusive pricing policy not only served as aninducement to grant exclusivity, to the detrimentof competing suppliers of impulse ice cream, butthat it also gave rise to discrimination betweentrading partners, by treating dissimilar situationsin a similar fashion. Retailers with their ownfreezer cabinets effectively paid for a service whichthey did not receive and, in so doing, were forcedto subsidise cabinet provision to those taking HBcabinets; the former retailers thereby placedthemselves at a competitive disadvantage vis-à-visthe latter ones.

(77) In view of the Commission’s objection, HBabandoned the policy of ‘inclusive pricing’ in1995, and introduced a ‘differential’ or ‘dual’pricing scheme. The scheme allows for thepayment of a lump sum to retailers stocking HBice cream but not taking an HB freezer cabinet,provided that retailer achieves a minimum annualturnover in HB ice cream (sales from the outlet) ofIEP 650 GSV (gross sales value). This lump sum iscurrently set at IEP 78 p.a. and reflects thepurchase and maintenance cost savings to HB innot supplying and servicing a standard 1 mcabinet to the retailer. The retail turnoverthreshold is set at a level which, according to HB,allows it to secure a minimum return on the saleof ice cream to a retailer.

(78) Unilever stated that the new scheme was ‘designedto remove any economic incentive on the retailerto take the HB cabinet’. Unilever went on to saythat the scheme would ‘have a significant effect onthe alleged foreclosure of the market, as moreretailers realise that the bonus can fund thepurchase of their own freezer’.

(79) The scheme has been operational since thebeginning of 1995 and its terms are published onHB price lists; for 1995, retailers holding theirown cabinets for a part year were to receive a partbonus. The lump sum can be periodically adjustedto reflect any changes in HB’s costs. Similarly, theturnover threshold may also be varied from timeto time. All variations are to be carried out in atransparent manner. In March/April 1996, [. . .]retailers qualified for, and received, the dualpricing bonus relating to 1995 purchases ofimpulse ice cream from HB. In 1997, [. . .]retailers qualified for, and received, the dualpricing bonus relating to 1996 purchases ofimpulse ice cream from HB.

7. Other manufacturers’ distribution arrangementsfor impulse ice cream in Ireland

(i) Mars and Valley

(80) In 1989, Mars appointed Valley to distribute itsnewly developed ice-cream products. Prior to thegranting of an injunction against Mars by the IrishHigh Court in 1991 (see paragraph 3), Mars

EN Official Journal of the European CommunitiesL 246/14 4.9.98

products had also been placed by some retailers inHB-owned cabinets. Initially, Mars supplied Valleywho then supplied the Mars products into Valleyor Mars-owned freezer cabinets, as well as intocabinets jointly purchased by Mars and Valley.Mars has, however, been doing some directdistribution since 1993. Following the 1992 HighCourt judgment rendering permanent theinjunction against Mars, Mars and Valleyamended their cabinet agreements to make themsupplier-exclusive. Mars states that its ‘totalexpenditure on freezers alone in 1994 was 22% ofits turnover in impulse ice cream’ in that year. InMarch 1997, Mars terminated its distributionarrangement with Valley.

(ii) Nestlé

(81) Since Nestlé entered the Irish impulse ice-creammarket in 1994, it has been installing freezercabinets in retail outlets subject to a condition ofexclusivity. Nestlé distributes its ice cream inIreland solely through distributors. On enteringthe ice-cream market in 1994, Nestlé entered intoa cooperation arrangement with Leadmoreregarding distribution; this was not continuedbeyond the first ice-cream season.

(iii) Dale Farm

(82) Dale Farm provides freezer cabinets to retailoutlets on free-on-loan terms, for the exclusivestorage of Dale Farm ice cream, Mars ice creamand other Northern Foods frozen food products.

(iv) Häagen Dazs

(83) Häagen Dazs installs freezer cabinets in retailoutlets for the storage of its impulse and otherice-cream products; the cabinets are mainly smalland are subject to a condition of exclusivity. Allof its ice-cream products are sold throughdistributors.

(v) Leadmore

(84) Leadmore supplies freezer cabinets to retail outletssubject to a condition of exclusivity.

8. Market research and quantification offoreclosure

(85) A general point should first be made in relation tomarket research: there is always a certain marginof error when data are obtained by surveying onlya sample, however carefully chosen for itsrepresentativeness, of the total market in question.It is, however, the only effective and affordablemeans of obtaining many kinds of marketinformation. The reliability of such data can,moreover, be significantly enhanced where morethan one survey of a particular market tendsubstantially to corroborate each other’s findings,as is the case with the three market researchsurveys described below.

(86) While HB acknowledges a broad correlationbetween the results of the Lansdowne and B&Asurveys, it criticises the representativeness of theRosslyn survey for being ‘based on revisitingoutlets surveyed some five years previously’ in asimilar survey, which original survey was allegedly‘based on a random sample with no attempt atstratification’ according to outlet type and size.The Rosslyn survey, according to HB, is‘disproportionately tilted towards TSNs at theexpense of independent grocers’, in contrast withthe Lansdowne and B&A surveys, which arestratified in accordance with the Nielsen Universeof outlets. It is also the only one of the threesurveys to have been conducted before thedisposal by HB of some of its freezer cabinetsunder the ‘kick-start’ scheme. The Commissionhas taken due note of these criticisms in anyreliance which it has placed on that survey. TheCommission has also noted that the B&A surveyis weighted significantly more toward large outletsthan the other two surveys.

(i) The Lansdowne survey

(87) The survey was carried out on behalf of theCommission by Lansdowne Market ResearchLimited in July/August 1996, the height of the

EN Official Journal of the European Communities L 246/154.9.98

ice-cream season. A random sample of 501 outletswas chosen, and it was ensured that this would berepresentative of the relevant retail trade (27). Ageographical spread, including a clear urban/ruraldivide was ensured. The data was acquired byface-to-face interviews with owners/managers inall outlets. The survey’s principal findings aredetailed below.

(88) Of all cabinets in the outlets surveyed 84% wereowned by an ice-cream manufacturer/supplier:61% of all supplier-provided cabinets wereHB-owned(28); 11% of them were Mars-owned;9% were Valley-owned; 8% were Nestlé-owned;4% Dale Farm-owned(29); 2% Leadmore-owned;1% Häagen Dazs-owned.

(89) Of all cabinets 12% were found to beretailer-owned; 2% were on hire purchase froman ice-cream manufacturer; 1% were owned by aretail group. 38% of retailer-owned cabinets werepurchased from HB or HB agents.

(90) The proportion of outlets with only one freezercabinet for impulse ice cream was 58%; theproportion with two such freezers was 35%; theproportion with three or more was 7%. Theaverage (mean) number of cabinets per outlet was1,50.

(91) Of all outlets selling impulse ice cream 85% hadat least one supplier-provided cabinet; 72%(30)had at least one HB cabinet; 14% had at least oneMars cabinet; 10% Nestlé; 10% Valley; 5%(31)Dale Farm; 2% Leadmore; 1% Häagen Dazs; 5%other suppliers. Of all outlets 17% had at leastone cabinet owned by the retailer himself.

(92) Of all outlets 56% had a cabinet, or cabinets,from one manufacturer/supplier only (and are

(27) 68% of the sample were grocery/convenience stores, 21%were TSNs, 11% were garages. Multiples were not included.92% of the sample were independently owned; a further6% were part of a chain (symbol group).

(28) Includes cabinets owned by HB agents.(29) Includes cabinets owned by Dale Farm agents.(30) Includes 2% (of all outlets) where cabinets are owned by

HB agents.(31) Includes 1% (of all outlets) where cabinets are owned by

Dale Farm agents.

consequently only in a position to sell theice-cream products of that single manufacturer/supplier); 27% had cabinets owned by more thanone manufacturer/supplier (and no retailer-ownedcabinets): consequently, 83% of all outlets haveonly manufacturer/supplier-provided cabinets;17% of all outlets had at least one cabinet ownedby the retailer himself, this 17% being composedof 12% of all outlets which only have a retailer-owned cabinet and 5% of all outlets which havea retailer-owned cabinet/s, as well as amanufacturer/supplier-owned cabinet/s.

(93) This information was also broken down accordingto the turnover of each outlet surveyed in impulseice cream. There were three categories: (i) outletswith a turnover of under IEP 1 000 (22% of theoutlets), (ii) outlets with a turnover of betweenIEP 1 000 and IEP 2 000 (23% of the outlets),and (iii) outlets with a turnover of IEP 2 000 ormore (40% of the outlets) (32). 28% of outlets incategory (i) had at least one cabinet owned by theretailer himself (22% only had a retailer-ownedcabinet/s, 6% had a retailer-owned cabinet/s aswell as a manufacturer-supplier-owned cabinet/s);19% of outlets in category (ii) had at least onecabinet owned by the retailer himself (15% onlyhad a retailer-owned cabinet/s, 4% had a retailer-owned cabinet/s as well as a manufacturer/supplier-owned cabinet/s); however, only 10% ofoutlets in category (iii) had at least one cabinetowned by the retailer himself (4% only had aretailer-owned cabinet/s, 6% had a retailer-ownedcabinet/s as well as a manufacturer/supplier-ownedcabinet/s). 58% of outlets in categories (i) and (ii)had a cabinet/s from one manufacturer/supplieronly (and are consequently only in a position tosell the ice-cream products of that singlemanufacturer/supplier); 53% of outlets incategory (iii) are only in a position to sell theice-cream products of that single manufacturer/supplier.

(32) 15% of the outlets refused to disclose their turnover.

EN Official Journal of the European CommunitiesL 246/16 4.9.98

(94) 95% of HB cabinets are set up in outlets whichhave only got manufacturer-supplied cabinets;58% of HB’s cabinets are in outlets where onlyHB’s cabinets are in place. The level of sales ofimpulse ice cream in outlets in the latter categoryof outlet is almost identical to that in any outletswith HB cabinets.

(95) 47% of all outlets are only in a position to sell theice-cream products of a single manufacturer/supplier, with a single cabinet only in each outlet;8% are only in a position to sell the ice-creamproducts of a single manufacturer/supplier, withonly two cabinets. 41% of all outlets are only in aposition to sell the ice-cream products of HB,35% of all outlets are only in a position to sell theice-cream products of HB, with one HB cabinetonly, 6% with two or more HB cabinets only.15% of outlets are only in a position to sell theice-cream products of a single manufacturer/supplier other than HB. None of these otherbrands is significant in terms of the number ofoutlets tied to the sale of its products alone.

(96) The average age of the cabinets surveyed was 3,02years; for retailer-owned cabinets, the average agewas 4,59 years; for HB cabinets, it was 2,92; forMars cabinets, 2,06; for Valley cabinets, 3,53; forNestlé cabinets, 1,65. Retailers were unable todate one in six of the cabinets surveyed.

(97) When retailers were asked if it would be a ‘viableoption’ for them to use up further space to installanother freezer cabinet for impulse ice cream,87% of all outlets said that it would not; 11%said that it would. Of all outlets 53% consideredthat one freezer cabinet would be the optimalnumber of cabinets to have in the store during thesummer (ice cream) season; 36% said two wouldbe optimal; 8% said three; 1% four or more. Theaverage optimal number was 1,57. Lansdownehave commented that ‘it is evident that thenumber of ice-cream cabinets currently in place inretail outlets around the country is perceived asapproaching the maximum viable’.

(98) Of the cabinets surveyed 97% were permanentlyin place in the store (i.e. they had not just beenbrought in for the summer season). Of all outlets87% said that they never placed additional

cabinets in the store in order to cope with theincreased demand during the summer; 6% saidthey sometimes did; a further 6% said they alwaysdid.

(99) Of all cabinets surveyed 90% are used exclusivelyfor ice-cream storage (50% are only used forstoring impulse products, 40% for storing bothimpulse and non-impulse products); 94% of allmanufacturer-owned cabinets surveyed are usedexclusively for ice-cream storage (54% are onlyused for storing impulse products, 40% forstoring both impulse and non-impulse products);however only 67% of all retailer-owned cabinetssurveyed are used exclusively for ice-cream storage(26% are only used for storing impulse products,41% for storing both impulse and non-impulseproducts, 34% for storing both ice cream andnon-ice-cream products).

(100) Those retailers who did not own a freezer cabinetwere asked for their reasons for not owning suchcabinets: 54% indicated that it did not makecommercial sense; 25% that the cost wasprohibitive; 9% said they only had demandfor one brand of ice cream; 4% said it wasinconvenient.

(101) All retailers who did not own a frezeer cabinet orwere not hire purchasing a freezer from HB wereasked if HB’s hire purchase offer interested them.8% said it did, while 78% were not interested byit. 54% said they were not at all interested; 24%said they were not very interested; 5% wereindifferent; 6% were quite interested; 2% veryinterested. The overwhelming reason cited for thislack of interest was contentment with currentfreezer cabinet arrangements.

(102) All outlets only in a position to sell the ice-creamproducts of HB were asked if there was demandfor brands other than HB: 53% responded thatthere was no demand; 40% that there wasdemand (31% reported a little demand, 9% a bigdemand). The same category of outlets was furtherasked if they were interested in stocking brands

EN Official Journal of the European Communities L 246/174.9.98

other than HB: 62%(33) said they were notinterested (32%(34) not at all interested, 30%(35)not very interested); 9% were indifferent; 25%(36)were interested (17%(37) quite interested, 8%(38)very interested).

(103) Of those interested in stocking brands other thanHB (25% of 41% of all outlets, hence 10% of alloutlets), 53% said they would not be prepared toinstall an additional cabinet for the storage ofsuch brands; 40% said they would be preparedto do so. Almost all of those not prepared citedspace constraints as the main reason. A majorityof those prepared to install a further cabinetexpressed a preference for a supplier-exclusiveone.

(104) Those interested in stocking brands other than HBwere also asked if they would be prepared toreplace or exchange (‘swap’) one of their existingHB cabinets with one from another ice-creamsupplier: 82% said they were not prepared to doso; 11% said they were. The principal reasonscited for this unwillingness to replace HB cabinetswere the popularity and leadership position of HBand contentment with the present arrangement.The same group were further asked if they wouldbe prepared to replace or exchange one of theirexisting HB cabinets with a cabinet hired orpurchased by the retailer himself: 76% said theywould not be prepared to do so; 18% said theywould. Happiness with the current arrangementand cost considerations were the principal reasonsgiven for the lack of preparedness. Finally, thesame group was asked if they would be preparedto exchange an HB cabinet for two smaller ones,one not owned by HB: 49% said no; 44% yes.

(33) In the Statement of Objections, this figure was mistakenlyquoted in the text as 65% (a figure from the preliminarysurvey results); the survey was annexed in full to theStatement of Objections.

(34) Ibid. mistakenly quoted in the Statement of Objections as37%.

(35) Ibid. mistakenly quoted in the Statement of Objections as28%.

(36) Ibid. mistakenly quoted in the Statement of Objections as22%.

(37) Ibid. mistakenly quoted in the Statement of Objections as16%.

(38) Ibid. mistakenly quoted in the Statement of Objections as6%.

(ii) The Rosslyn survey

(105) Mars also commissioned a survey of the Irishimpulse ice-cream market. The survey was carriedout by the London-based firm Rosslyn ResearchLtd (39), though the fieldwork was done bythe locally-based Irish Marketing Surveys. TheRosslyn survey covers 408 outlets spreadgeographcially throughout Ireland, and with aspread of outlet size and type. Some of theRosslyn survey’s main findings are outlined below,together with some comparative figures from theRosslyn survey of 1991. On the basis of theresults yielded by this survey, Mars furthercommissioned an economic analysis to be carriedout, also discussed below.

(106) The proportion of outlets with only one ‘front-ofstore’ freezer cabinet for impulse ice cream was64%(40); the proportion with two such freezerswas 31%(41); the proportion with three or morewas 4%(42). The average (mean) number ofcabinets per outlet was 1,42 (43).

(107) Of the freezer cabinets 92%(44) were owned bythe manufacturer of the product stocked in it.6%(45) of the cabinets were owned by the retailerhimself. 64%(46) of cabinets were owned byHB(47), 14%(48) by Mars, 4% by Valley, 2% byDale Farm, 1% by Leadmore.

(108) 50% of outlets had one HB freezer only; 5% hadtwo HB freezers only; 2% had one Mars freezeronly; 1% each had one Valley, Dale Farm andLeadmore freezer only; 14% had one HB and one

(39) An almost identical survey was carried out for Mars by thesame company in December 1991/January 1992, the resultsof which were cited in the Commission’s Statement ofObjections of 29 July 1993. All but 40 were the sameoutlets as interviewed in 1991.

(40) 79% in 1991.(41) 20% in 1991.(42) 1% in 1991.(43) 1,22 in 1991.(44) 89% in 1991.(45) 11% in 1991.(46) 71% in 1991.(47) 68% of ‘back of shop’ freezers.(48) 1% in 1991.

EN Official Journal of the European CommunitiesL 246/18 4.9.98

Mars freezer; 7% had an HB freezer and onefrom any other manufacturer except Mars.

(109) Of the manufacturer-supplied freezers 97% wereon loan from that manufacturer; of these, 99%were provided free of charge, and 88% wereprovided subject to an exclusivity condition (49).Of retailers supplied with freezers bymanufacturers 27%(50) said they would like tostock other manufacturers’ products in the freezers(68%(51) were not interested).

(110) Of retailers with manufacturer-exclusive cabinets87% would have to install another freezer if theywished to sell another brand of ice cream; ofthese, 67% said they did not ‘have room’ to doso. Of those who said they did have room, 15%said they had chosen not to install one because it‘would not be economical in terms of runningcosts’ and 13% because they had ‘better use forthe space’; 43% of those with room said theywould be prepared to install another cabinet ‘ifthe demand was high for another product’.

(111) Of those freezer cabinets replaced (returned,exchanged or changed) by another freezer fromthe same or different ice-cream manufacturer overthe previous five years, 78% of them belonged toHB; 55% of the freezers were returned, exchangedor changed in order to be replaced by a moremodern freezer; a further 25% of them werereturned, exchanged or changed in order to bereplaced by a larger freezer; 74% of the newfreezers belong to HB; freezers returned,exchanged or changed were almost invariablyreplaced by freezers from the same manufacturer— 214 of the 234 freezers replaced were HBfreezers replacing HB freezers.

(112) Of all outlets 72% said they would not beprepared to install a replacement or additional

(49) As no suppliers appear to supply cabinets on non-exclusiveterms, it is most likely that the remaining 12% were alsosubject to an exclusivity condition of which the retailer wasunaware.

(50) 52% in 1991.(51) 44% in 1991.

freezer; of those who would be prepared to do so(26% of the total sample), 82% would not beprepared to buy a cabinet themselves; 94% ofthem would not be prepared to take a cabinetsubject to exclusivity on a loan reflecting the costsof cabinet provision; 80% would not take anon-exclusive cabinet on rent; 84% would,however, be prepared to take a free on loancabinet on supplier-exclusive terms. When thesame 26% of the sample were asked if they couldinstall a further cabinet (in addition to anothersupplier-exclusive one), 77% said they could not;of these, 51% cited lack of space and better use ofspace as reasons, while a further 22% said itwould not be economical in terms of runningcosts. Of those who said they could (20% of26% of total sample), only 17% were prepared todo so.

(113) The survey was carried out in mid-April 1996.Only 5% of retailers had been offered a freezerunder the ‘kick-start’ disposal (see paragraphs 72and 73). Only 13% of retailers were aware of theexistence of the HB hire-purchase scheme.

(114) The economic analysis was carried out by the firmof economists, Case Associates, and is entitled‘Estimating foreclosure levels in the Irish ice-creammarket’. This analysis has drawn a number ofconclusions from the survey. The analysispurports, inter alia, to calculate what proportionof all outlets are ‘foreclosed’ in the sense that anew cabinet would have to be installed in orderfor a new entrant to be able to sell its ice creamthere. It concludes, by one means of calculation,that at least 89%(52) of all outlets selling impulseice cream are foreclosed in this way. Using analternative means of calculation, the analysisarrives at a foreclosure level (in the sense justdescribed) of 84%(53). Yet another means of

(52) The calculation is based on the fact that, in the 408 outletssampled, no more than 45 cabinets were not supplier-provided (they were retailer-owned, ‘other owner’ or ‘don’tknow’), if any outlet contained more than one such cabinet,the foreclosure level would be even higher.

(53) 234 outlets had only a supplier-provided cabinet, 87 hadone HB cabinet and one other supplier-provided cabinet, 23outlets had two HB cabinets: these 344 outlets represent84% of the total sample.

EN Official Journal of the European Communities L 246/194.9.98

calculation puts foreclosure at the higher level of93%(54).

(iii) The B&A surveys

(115) HB also commissioned a market survey, whichwas conducted in August/September 1996 byBehaviour & Attitudes Limited, a market researchfirm. The results of this survey were containedin HB’s written response to the Statement ofObjections. The sample for the survey comprised507 retail outlets, spread geographicallythroughout Ireland, and with a spread of outletsize and type (55). The survey’s principal findingsare outlined below.

(116) [. . .]% of outlets surveyed had one cabinet infront of the store, [. . .]% two cabinets, and[. . .]% three or more. HB products were soldfrom [. . .]% of the outlets surveyed, Mars from[. . .]%, Valley from [. . .]%, Nestlé from [. . .]%,and Häagen Dazs from [. . .]%. [. . .]% of all theoutlets surveyed stocked HB ice-cream productstogether with the products of no other ice-creammanufacturer. HB faces direct competition fromother ice-cream brands in [. . .]% of the outletssurveyed, less than[. . .]% of the outlets in whichits products are sold.

(117) Of those outlets with only one cabinet, [. . .]% ofthese were HB cabinets, [. . .]% were Marscabinets, [. . .]% Valley cabinets, [. . .]% Nestlécabinets and were [. . .]% retailer cabinets. Ofthose with two or more cabinets, [. . .]% had atleast one HB cabinet, [. . .]% a Mars cabinet,[. . .]% a Valley cabinet, [. . .]% a Nestlé cabinet,[. . .]% a Häagen Dazs cabinet, and [. . .]% a

(54) This was the method of calculation used by William Bishop,an economist who analysed foreclosure levels on the basis ofthe 1991 Rosslyn survey: the method involves dividing thetotal number of outlets sampled by the mean number offreezers present in all these outlets, and then multiplying bythe number of retailer- and ‘other’-owned cabinets. Thismethod assumes that retailer-owned cabinets are likely to bespread across outlets in the same proportion as any othercabinets.

(55) 20% were TSNs; 63% were grocery outlets, of which 10%were ‘symbol’ stores; 10% were garages; others 7%.Multiples were excluded.

retailer cabinet. [. . .]% of all outlets surveyed hada single HB cabinet alone in front of store.

(118) B&A asked retailers how often they were askedfor brands not currently stocked. [. . .]% repliedthat they were never asked, [. . .]% said rarely,[. . .]% occasionally and [. . .]% frequently. Ofthose who were at some stage asked for non-stocked brands, [. . .]% took no action, [. . .]%‘added a manufacturer’, and none ‘changedmanufacturer’. The survey found that, over theprevious seven years, [. . .]% of the outlets had atsome stage stocked new brands of ice cream, andthat [. . .]% of outlets had at some stage de-stocked brands of ice cream; the principal reasonscited for such de-stocking were lack of customerdemand ([. . .]%), poor delivery standards([. . .]%), and poor cabinet maintenance ([. . .]%).

(119) Retailers with only one cabinet in their outlet wereasked if they were prepared to install a secondcabinet, [. . .]% were not, [. . .]% were, and theremainder did not know. The main reason citedfor this absence of preparedness was lack of space.The same outlets were also asked about theirpreparedness to replace the existing cabinet,[. . .]% were not prepared, [. . .]% were andthe remainder did not know. The principal reasonsgiven for such lack of preparedness weresatisfaction with the current supplier’s productrange and cabinet. The same retailers were furtherasked if they would be prepared to replace theexisting freezer with two smaller ones, [. . .]%were not, [. . .]% were and the remainder did notknow.