Embed Size (px)

Citation preview

Columbus Association of Health Underwriters

Legislative Update

September 14, 2010

2010 Ohio Election 2010 is a key election year with all major statewide offices

including the Governor up for election. Also, all 99 Ohio House seats and 17 of the 33 Ohio Senate seats are up for election. Which party controls the Ohio House of Representatives is at stake. A change of 4 seats from the Democrats to the Republicans would give Republicans control of the House. In the Senate, the Republican majority will likely stay close to its current 21-12 margin.

The 2010 elections also determine which party controls the State Apportionment Board, the entity that draws the Ohio Legislative district lines. Whichever party wins at least 2 of the 3 races for Governor, Secretary of State and Auditor will have a majority of the Apportionment Board members. History has shown that whichever party draws the district lines greatly increases their chances of winning a majority of seats in the Ohio Legislature.

Recap on PPACA

President signed Patient Protection and Affordable Care Act (PPACA) on March 23, 2010

Reconciliation bill signed on March 30 Interpretation of legislation now requires examining multiple

sources: Senate-passed bill, H.R. 3590 (now P.L. 111-148) Manager’s amendment to the Senate bill Reconciliation bill, H.R. 4872 Very important: Check all three sources when

considering how the bill works

PPACA Overview

Makes significant statutory changes affecting the regulation of and payment for many types of private health insurance – many insurance market reforms

Will require almost all private sector employers to evaluate the health benefits they currently offer and consider whether they are compliant

For those without access to employer coverage, new individual mandate to purchase and maintain minimum coverage in 2014

Grandfathered Plans

Essentially all plans in effect on date of PPACA enactment (March 23, 2010) are “grandfathered”

Very few changes are permitted if a plan wants to retain grandfathered status Plans must provide a statement to participant that it

believes it is a “grandfathered” plan Plans that made changes between March 23 and June 14 have

an opportunity to reverse any significant changes made without losing grandfathering status. This must be done by the plan year following

September 23, 2010

The “Why” of Grandfathered Plans

PPACA requirements that are waived if a plan remains “grandfathered” The requirement that emergency services must be provided without pre-

authorization and treated as in-network The rating limits, guaranteed issue, guaranteed renewability, and

essential benefits packages that begin in 2014 The cost-sharing and deductible limits, non-discrimination for clinical trial

participants, non-discrimination on providers acting within scope of license

Cost sharing for preventive care The non-discrimination rules for fully insured plans The requirement that pediatricians must be an allowable primary care

physician choice The requirement that females can go to an OB/GYN without a referral The requirement that plans must provide an internal and external

appeals process

What Grandfathered Plans Can’t Do

Can’t raise co-insurance charges i.e. if insured is required to pay 20% of hospital bill, this percentage can’t increase

Can’t increase co-pay more than the greater of $5 (adjusted annually for medical inflation) or medical inflation plus 15 percentage points

Can’t reduce employer contribution more than 5 percentage points

Can’t increase deductible more than medical inflation plus 15 percentage points

Can’t reduce any insurer annual dollar limit in place as of

March 23, 2010

What Grandfathered Plans Can’t Do

Can’t use a merger, acquisition or business restructuring for the purpose of covering new individuals under a grandfathered plan

Can’t change carriers if you are fully insured Can’t move employees to a grandfathered plan with

lower benefits Can’t make a significant cut to benefits such as

eliminating benefits for a particular condition

What Grandfathered Plans Can Do

Add family members or new employees Disenrollment of employees Make changes as a result of state or federal regulations Make changes to voluntarily adopt some or all of the

law’s requirements Change third party administrator if you are self-funded Increase premiums

Other 2010 Issues

Temporary High Risk Pool Small business tax credit Medicare Part D subsides are not taxable Early retiree reinsurance program New federal insurance plan requirements

Temporary High Risk Pool Implementation for Uninsurable Ohioans in Individual Market

Medical Mutual selected to operate pool Applications started August 1st with coverage effective

date of September 1st

Completed applications received after August 15th will be effective October 1st

Approximately $152 million for Ohio out of $5 billion total

Eligible persons will pay a standard market rate As of September 1st approximately 330 enrolled in

program Agents that have an MMO appointment will be paid a

$50 fee per enrolled individual

Temporary High Risk Pool Eligibility Requirements

Must be a citizen or national of the U.S. or lawfully present in the U.S. and an Ohio resident

Must be uninsured for six (6) months prior to the date you apply for coverage

Cannot be eligible for coverage under the federal Medicare program, the Ohio Medical Assistance Program, the Ohio Children’s Health Insurance Program or an employer-sponsored group health plan, unless you are subject to a mandatory initial waiting period

Must have a qualifying pre-existing condition as evidenced by a denial of coverage by two insurers or documentation from a health professional of a qualifying pre-existing condition

High Risk Pool Questions

Go to www.ohiohighriskpool.com Call 1-877-730-1117 Go to Ohio Department of Insurance website

www.insurance.ohio.gov and click on

High Risk Pool FAQs

PPACA in 2010

Certain small businesses are eligible for phase one of the small business premium tax credit. Small employers with fewer than 25 employees may receive a

maximum credit, based on number of employees, of up to 35% of premiums until 2014.

Employer must contribute at least 50% of the total premium cost.

Businesses do not have to have a tax liability to be eligible Non-profits are eligible up to 25% of premiums Average salary must be $50,000 or less (owner income

exempted) Note: This may or may not be helpful, the credit reduces amount of

premiums that can be deducted by the employer

www.bcbsnc.com/taxcredit

PPACA in 2010

Owner’s benefits and income generally not included in the credit calculation.

IRS has a Q and A section and helpful information on its website.

Not all questions are answered at this point.

Go to www.irs.gov for more information.

PPACA in 2010

Employer deductibility for retiree Medicare Part D subsidies is eliminated in 2013, but this results in an immediate accounting impact. Large employers will be most effected by this change. Organizations like AT&T,

Caterpillar, Verizon and other large corporations reported the fiscal impact immediately

$250 Medicare beneficiary rebate for Part D coverage gap In 2011 50% discount on prescriptions filled in Part D coverage gap; also begin

phase-in of subsidies of 75% of generics for prescriptions in Part D coverage gap

PPACA in 2010

Establishes federal review of health insurance premium rates. Secretary of HHS, in conjunction with the states, will have new

authority to monitor health insurance carrier premium increases beginning in 2010 to prevent unreasonable increases and publicly disclose such information.

Ohio is one of 45 states that was just approved to receive $1 million each to help improve the oversight of proposed health insurance increases.

PPACA in 2010

2010 Reinsurance Program for employer “early retiree” health benefits (age 55-64) provides for subsidies up to 80 percent of the insurance costs (claim corridor of $15-90K) IF they invest the difference in wellness and chronic care management programs, among other things The program became effective June 23, 2010. Self-funded and fully insured plans eligible.

Effective Plan Years on/after Sept. 23, 2010 All Plans, Including Grandfathered

Restrictions on annual limits Plans may impose only “restricted annual limits” on the

dollar value of “essential benefits.” HHS to establish annual limits on the dollar value of essential benefits. On and after January 1, 2014, no annual limits will be permitted

No lifetime limits Plans may not impose lifetime limits on dollar value of

“essential benefits”

Effective Plan Years on/after Sept. 23, 2010All Plans, Including Grandfathered

New restrictions on “rescissions” Plans may not rescind coverage unless person

commits fraud or makes a material misrepresentation prohibited under the terms of the plan

Pre-Ex Restrictions Plans may not impose any preexisting condition

restriction on children under the age of 19. After January 1, 2014, plans may not impose preexisting condition restrictions on anyone

Effective Plan Years on/after Sept. 23, 2010All Plans, Including Grandfathered

Coverage for dependents to age 26 If a plan offers dependent coverage of children, such

coverage must extend to a child until the child reaches age 26

Some carriers are implementing this change early For grandfathered plans, this requirement applies

before January 1, 2014 only if the adult child is not eligible to enroll in another plan

Ohio Dependent Age Law

Coverage up to age 28 – For new or renewed policies effective on or after July 1, 2010

Law applies to group policies for dependents including COBRA and state continuation, and individual policies that include coverage for dependents including conversion, open enrollment basic and standard plans

The employer is not required to pay for any part of the dependent cost

Effective for Plan Years on/after Sept. 23, 2010 (Grandfathered Exempt)

For all group and individual plans, including self-insured plans, emergency services covered at in-network rate regardless of provider

Preventive care without cost sharing an “A” or “B” rating from the US Preventive Services Task Force on services that receive

New appeals process rules for coverage determinations and claims

Non-discrimination provisions Applies to fully insured plans (previously only applied to self-

insured plans) Prohibits employers from discriminating in favor of highly

compensated individuals relative to rank-and-file employees with respect to eligibility to participate in a group health plan

Penalties of $100 per day for each employee whose benefits not incompliance, up to 10% of cost of the group health plan or $500,000, whichever is less

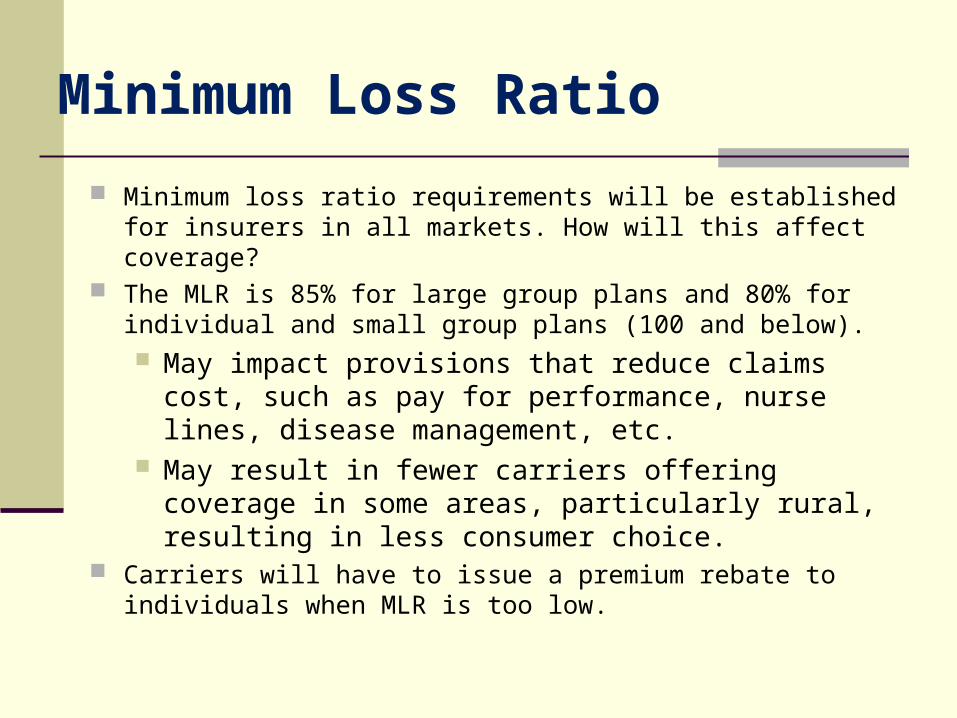

Minimum Loss Ratio

Minimum loss ratio requirements will be established for insurers in all markets. How will this affect coverage?

The MLR is 85% for large group plans and 80% for individual and small group plans (100 and below). May impact provisions that reduce claims cost, such as

pay for performance, nurse lines, disease management, etc.

May result in fewer carriers offering coverage in some areas, particularly rural, resulting in less consumer choice.

Carriers will have to issue a premium rebate to individuals when MLR is too low.

MLR and NAIC

PPACA stated that the National Association of Insurance Commissioners (NAIC) will be responsible for drafting the MLR calculation and submitting the formula proposal to HHS by fall 2010

The organization has been working to establish a formula for the past few months. The NAIC held their national convention in Seattle a couple weeks ago and hopes to have a draft of the calculation available for comment in the near future

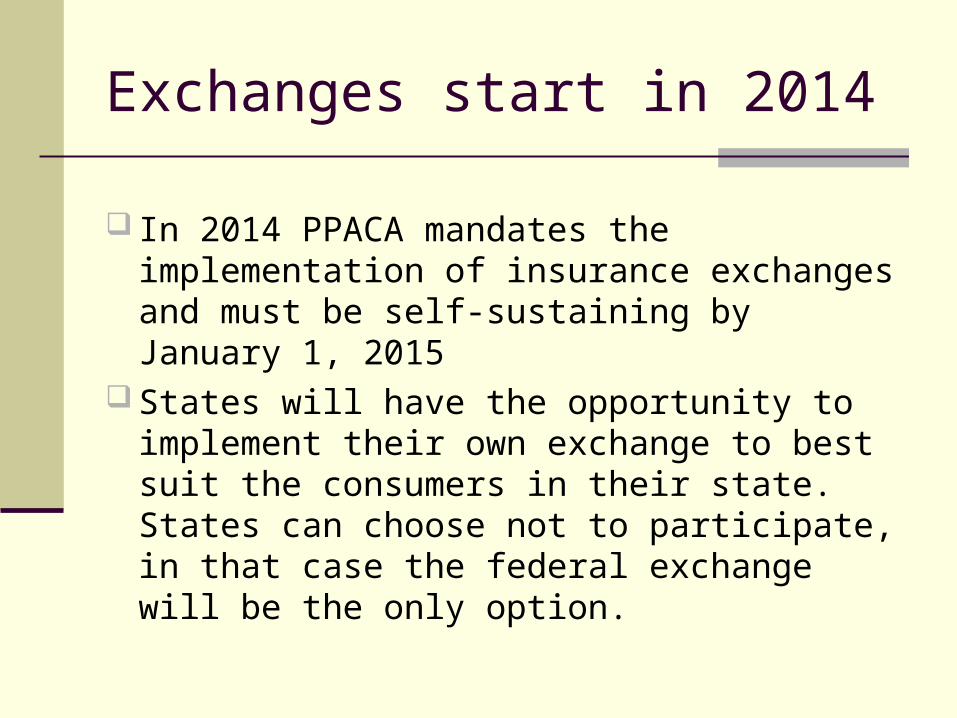

Exchanges start in 2014

In 2014 PPACA mandates the implementation of insurance exchanges and must be self-sustaining by January 1, 2015

States will have the opportunity to implement their own exchange to best suit the consumers in their state. States can choose not to participate, in that case the federal exchange will be the only option.

Exchanges

Two Exchanges – Non-group-market and a Small Business Health Options Program; however, state can choose to operate one exchange for both groups

Small businesses are defined as less than 100 employees although states can limit Exchange to 50 employees through 2016, but then are permitted to allow businesses with more than 100 employees beginning in 2017

Ohio Exchange Activities

Governor and ODI Establishing Health Benefits Exchange Task Force now

Representatives of employers, insurers, providers, consumers and agents will participate on the Task Force

OAHU has been chosen as a member of the Task Force

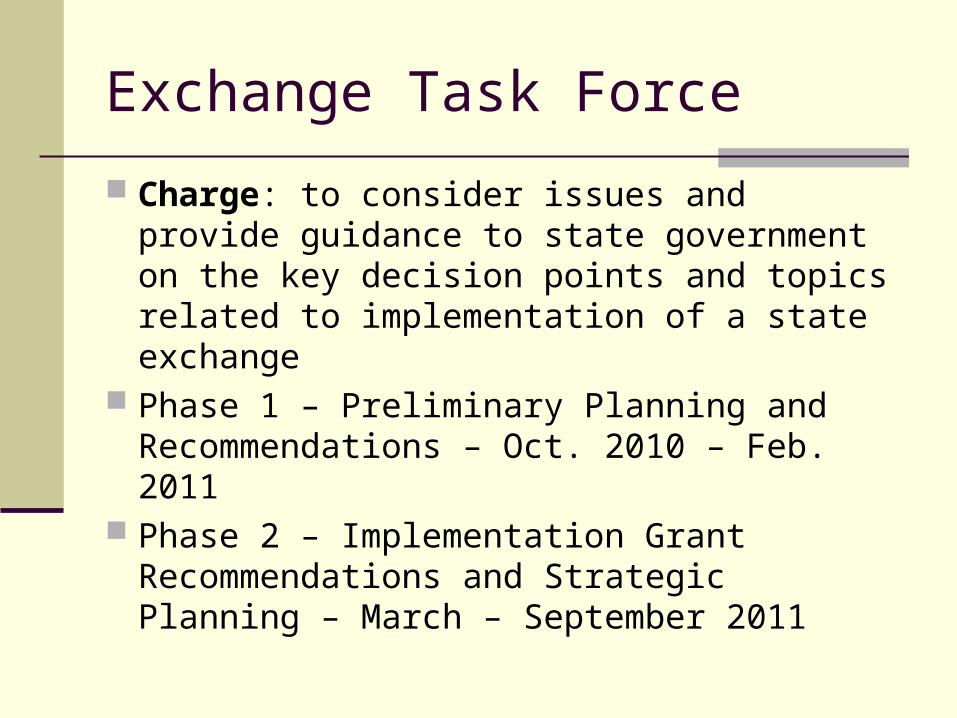

Exchange Task Force

Charge: to consider issues and provide guidance to state government on the key decision points and topics related to implementation of a state exchange

Phase 1 – Preliminary Planning and Recommendations – Oct. 2010 – Feb. 2011

Phase 2 – Implementation Grant Recommendations and Strategic Planning – March – September 2011