Embed Size (px)

Citation preview

COLLIERS INTERNATIONAL2011 SERBIA REAL ESTATE REVIEWAlbania Bulgaria Croatia Czech Republic Greece Hungary Poland Romania Russia Serbia Slovakia Ukraine

Accelerating success.

Research: [email protected]. 130 | CollieRS inteRnAtionAl

2011 CollIERS REAl EStAtE REvIEw » CoUNtRY

Serbia

Dear Friends and Partners,

the last year has proven to be challenging for all of us. All of the real estate market segments suffered, each in their own manner. Although the messages we receive from banks, investors as well as the government are encouraging, 2011 will continue to be a year of caution but a slow and definite recovery.

As a result of all this change, the one thing we can say is that the market is a lot more sophisticated than it was 2 – 3 years ago. Some difficult lessons were learned, and among them the most important one would be that the market has shifted towards tenants and buyers.

it will continue to take an innovative and sophisticated approach to achieve successful and sustainable real estate solutions, tapping into local and global experience.

We hope to continue to accelerate your success.

Best regards, Maja Sahbaz

Maja Sahbaz general manager colliers international serbia

Address 115D Mihajla Pupina Blvd. 11070 New Belgrade, Serbia

Phone +381 11 313 99 55

Email [email protected]

P. 130 | CollieRS inteRnAtionAl

CollieRS inteRnAtionAl | P. 131Research: [email protected]

2011 CollIERS REAl EStAtE REvIEw » SERBIA

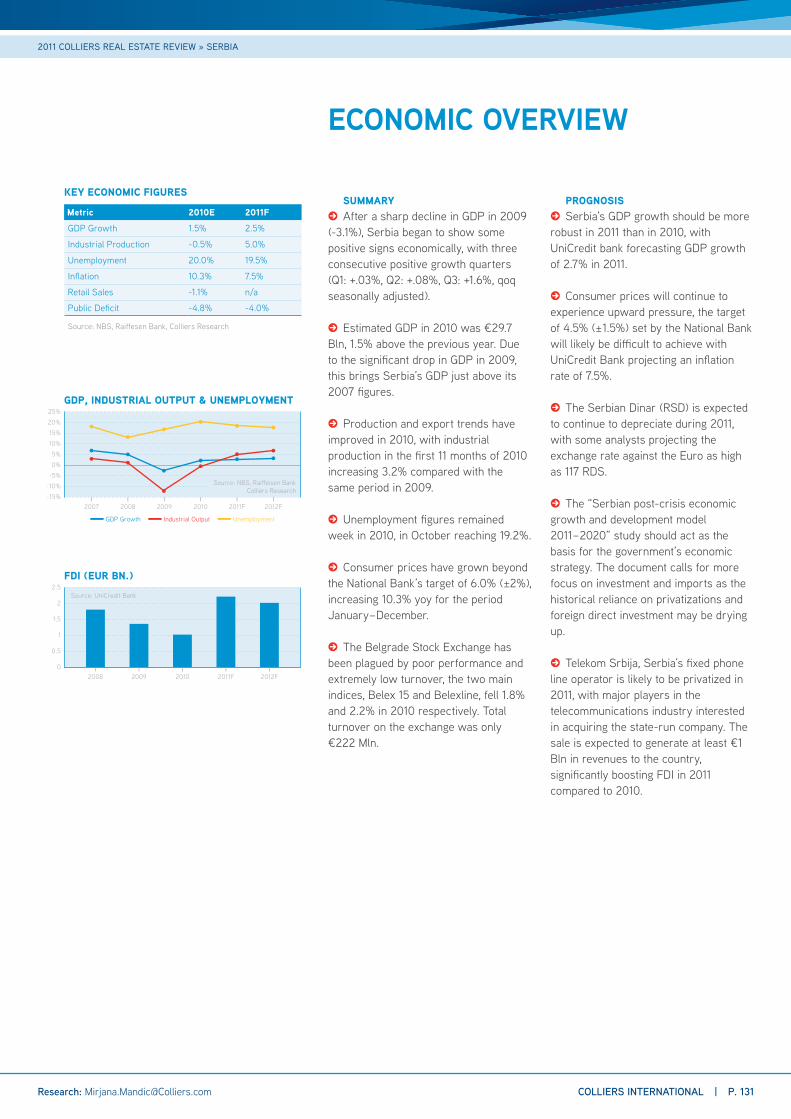

SUMMARY � After a sharp decline in GDP in 2009

(-3.1%), Serbia began to show some positive signs economically, with three consecutive positive growth quarters (Q1: +.03%, Q2: +.08%, Q3: +1.6%, qoq seasonally adjusted).

� Estimated GDP in 2010 was €29.7 Bln, 1.5% above the previous year. Due to the significant drop in GDP in 2009, this brings Serbia’s GDP just above its 2007 figures.

� Production and export trends have improved in 2010, with industrial production in the first 11 months of 2010 increasing 3.2% compared with the same period in 2009.

� Unemployment figures remained week in 2010, in October reaching 19.2%.

� Consumer prices have grown beyond the National Bank’s target of 6.0% (±2%), increasing 10.3% yoy for the period January – December.

� The Belgrade Stock Exchange has been plagued by poor performance and extremely low turnover, the two main indices, Belex 15 and Belexline, fell 1.8% and 2.2% in 2010 respectively. Total turnover on the exchange was only €222 Mln.

PROGNOSIS � Serbia’s GDP growth should be more

robust in 2011 than in 2010, with UniCredit bank forecasting GDP growth of 2.7% in 2011.

� Consumer prices will continue to experience upward pressure, the target of 4.5% (± 1.5%) set by the National Bank will likely be difficult to achieve with UniCredit Bank projecting an inflation rate of 7.5%.

� The Serbian Dinar (RSD) is expected to continue to depreciate during 2011, with some analysts projecting the exchange rate against the Euro as high as 117 RDS.

� The “Serbian post-crisis economic growth and development model 2011 – 2020” study should act as the basis for the government’s economic strategy. The document calls for more focus on investment and imports as the historical reliance on privatizations and foreign direct investment may be drying up.

� Telekom Srbija, Serbia’s fixed phone line operator is likely to be privatized in 2011, with major players in the telecommunications industry interested in acquiring the state-run company. The sale is expected to generate at least €1 Bln in revenues to the country, significantly boosting FDI in 2011 compared to 2010.

ECONOMIC OVERVIEW

KEY ECONOMIC FIGURES

Metric 2010E 2011FGDP Growth 1.5% 2.5%

Industrial Production -0.5% 5.0%

Unemployment 20.0% 19.5%

Inflation 10.3% 7.5%

Retail Sales -1.1% n/a

Public Deficit -4.8% -4.0%

Source: NBS, Raiffesen Bank, Colliers Research

|

2007|

2008|

2009|

2012F|

2011F|

2010

25%

20%

15%

10%

5%

0%

-5%

-10%

-15%

GDP, INDUSTRIAL OUTPUT & UNEMPLOYMENT

▬ GDP Growth ▬ Industrial Output ▬ Unemployment

Source: NBS, Raiffeisen BankColliers Research

2.5

2

1.5

1

0.5

0

FDI (EUR BN.)

|

2008|

2010|

2012F|

2011F|

2009

Source: UniCredit Bank

P. 132 | CollieRS inteRnAtionAl Research: [email protected]

2011 CollIERS REAl EStAtE REvIEw » SERBIA

SUPPLY � Despite the construction slowdown

experienced by the Belgrade office market during 2010, the total stock of Class A and B office space increased by 76,100 Sqm. By year-end it stood at 658,419 Sqm.

� Of this, Class A stock comprises 414,503 Sqm GLA an increase of 22.5% compared to 2009. The total stock of Class B space remained the same as in 2009 – at 243,916 Sqm.

� New Class A buildings delivered to the market in the second half 2010 included the Dexy Co office building of 9,056 Sqm, located in New Belgrade. Other significant additions to stock included two buildings (Belville Office Building 1 – 8,089 Sqm GLA and Belville Office Building 2 – 15,302 Sqm GLA) which opened within the University village on Jurija Gagarina Street, in New Belgrade.

DEMAND � Encouraged by somewhat lower

rental levels, numerous companies started their search for new business premises in 2010. These tenants came from a range of business sectors including finance and insurance, engineering, architecture and construction; IT, media and publishing and retaling. Among the companies seeking space were Findomestic Bank, KBC Securities, Meridian Balkans, SunGard, Reuters, Beneton, and others.

� Local and foreign government institutions and embassies were also active players in the market. The Australian Embassy took 800 Sqm in the “19th Avenue” office building in New Belgrade, and the Flight Control Agency of Serbia took up 1,200 Sqm in the “M Invest” building also in New Belgrade.

� In terms of deal size, the majority of demand (70% of requests) was for premises up to 500 Sqm. The remaining 30% of requests were for larger footplates of 1,000 Sqm and above.

VACANCY / AVAILABILITY � The vacancy rate increased to

24,24% by end 2010, which equates to 159,633 Sqm. Class A vacancy increased compared to the previous year, driven in large part by additions to stock, while Class B vacancy decreased.

� By type, there was 105,222 Sqm of vacant Class A – a vacancy rate of 25.4%. Class B vacant space account for 54,111 Sqm – a vacancy rate of 22.3%.

RENTS � Although rents for all types of office

space experienced a decrease, there was a greater fall in Class A rents, due to the higher level of new additions. Prime headline rents by year-end fell to €16 per Sqm. In general, headline rents for Class A space vary from €13 to €16 Sqm/pcm. Class B rents remained steady at ca. €13.5 Sqm/pcm.

� In cases where the whole building is offered for rent, with sizes ranging from 1,000 to 2,500 Sqm, prime headline rents range from €10 to €12 Sqm/pcm.

PROGNOSIS � Over 50,000 Sqm of space is on

track to be delivered to the market in 2011. This comprises of primarly Class A stock, delivered by a few key developments. The buildings expected to have a big impact on the market are the B23 office building by Verano, comprising 35,000 Sqm including state of the art systems. Another interesting new project is Tri lista Duvana by MPC Holding (8,200 Sqm GLA) in one of the top business location in Belgrade’s CBD.

� This will create significant competition amongst developers/owners for grade A tenants, putting further downward pressure on class A rents.

OFFICE MARKET

KEY OFFICE FIGURES

Metric MeasureTotal Stock (A and B) 658,419 Sqm GLA

Vacancy (A and B) 24.24%

Prime Headline Rent €16/Sqm/month

Source: Colliers International

KEY LEASE TRANSACTIONS

Tenant Size (Sqm) Project LocationFindomestic bank 2,500 Napred Block 26 New

Belgrade

Medico Uno 1,000 BelgradeWarehouse Pancevo

Cardiovasular Hospital 1,250 Block 24 New

BelgradeNumanovic Furniture 1,950 Garden Center Zemun

|

H2 2009|

H1 2009|

H2 2008|

H1 2010|

H2 2010

70,000

60,000

50,000

40,000

30,000

20,000

10,000

0

ADDITIONS TO OFFICE STOCK IN BELGRADE

Source: Colliers International

|

Q1 2008|

Q1 2009|

Q2 2008|

Q1 2010|

Q2 2009|

Q2 2010

180,000

160,000

140,000

120,000

100,000

80,000

60,000

40,000

20,000

0

VACANT SPACE IN BELGRADE

▬ Class A ▬ Class B ▬ Overall

Source: Colliers International

CollieRS inteRnAtionAl | P. 133Research: [email protected]

2011 CollIERS REAl EStAtE REvIEw » SERBIA

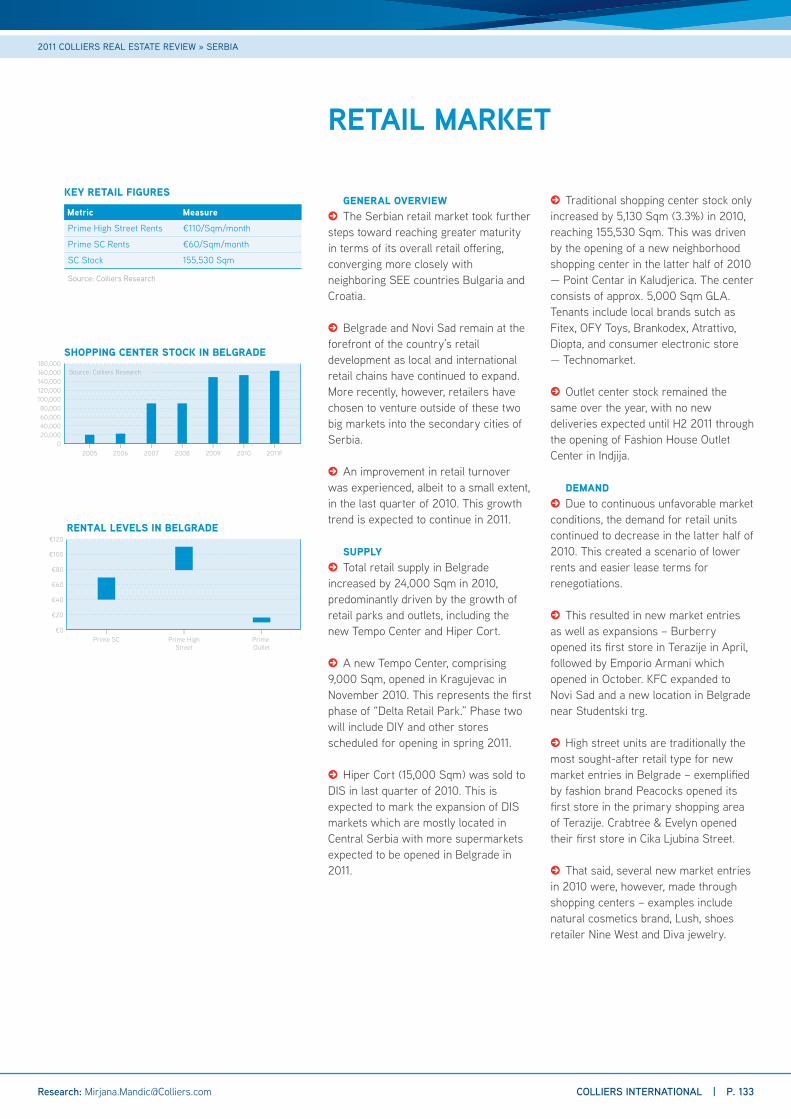

GENERAL OVERVIEW � The Serbian retail market took further

steps toward reaching greater maturity in terms of its overall retail offering, converging more closely with neighboring SEE countries Bulgaria and Croatia.

� Belgrade and Novi Sad remain at the forefront of the country’s retail development as local and international retail chains have continued to expand. More recently, however, retailers have chosen to venture outside of these two big markets into the secondary cities of Serbia.

� An improvement in retail turnover was experienced, albeit to a small extent, in the last quarter of 2010. This growth trend is expected to continue in 2011.

SUPPLY � Total retail supply in Belgrade

increased by 24,000 Sqm in 2010, predominantly driven by the growth of retail parks and outlets, including the new Tempo Center and Hiper Cort.

� A new Tempo Center, comprising 9,000 Sqm, opened in Kragujevac in November 2010. This represents the first phase of “Delta Retail Park.” Phase two will include DIY and other stores scheduled for opening in spring 2011.

� Hiper Cort (15,000 Sqm) was sold to DIS in last quarter of 2010. This is expected to mark the expansion of DIS markets which are mostly located in Central Serbia with more supermarkets expected to be opened in Belgrade in 2011.

� Traditional shopping center stock only increased by 5,130 Sqm (3.3%) in 2010, reaching 155,530 Sqm. This was driven by the opening of a new neighborhood shopping center in the latter half of 2010 — Point Centar in Kaludjerica. The center consists of approx. 5,000 Sqm GLA. Tenants include local brands sutch as Fitex, OFY Toys, Brankodex, Atrattivo, Diopta, and consumer electronic store — Technomarket.

� Outlet center stock remained the same over the year, with no new deliveries expected until H2 2011 through the opening of Fashion House Outlet Center in Indjija.

DEMAND � Due to continuous unfavorable market

conditions, the demand for retail units continued to decrease in the latter half of 2010. This created a scenario of lower rents and easier lease terms for renegotiations.

� This resulted in new market entries as well as expansions – Burberry opened its first store in Terazije in April, followed by Emporio Armani which opened in October. KFC expanded to Novi Sad and a new location in Belgrade near Studentski trg.

� High street units are traditionally the most sought-after retail type for new market entries in Belgrade – exemplified by fashion brand Peacocks opened its first store in the primary shopping area of Terazije. Crabtree & Evelyn opened their first store in Cika Ljubina Street.

� That said, several new market entries in 2010 were, however, made through shopping centers – examples include natural cosmetics brand, Lush, shoes retailer Nine West and Diva jewelry.

RETAIL MARKET

KEY RETAIL FIGURES

Metric MeasurePrime High Street Rents €110/Sqm/month

Prime SC Rents €60/Sqm/month

SC Stock 155,530 Sqm

Source: Colliers Research

|

2009|

2008|

2007|

2006|

2005|

2010|

2011F

180,000160,000140,000120,000100,00080,00060,00040,00020,000

0

SHOPPING CENTER STOCK IN BELGRADESource: Colliers Research

|

Prime SC|

Prime HighStreet

|

Prime Outlet

€120

€100

€80

€60

€40

€20

€0

RENTAL LEVELS IN BELGRADE

P. 134 | CollieRS inteRnAtionAl

RETAIL MARKET

VACANCY & RENTS � The vacancy rate in the large, existing

modern international-style shopping centers – Delta and Usce – remained at 0%. Such shopping centers maintained high asking rents although some retailers did renegotiate terms to reflect difficult conditions.

� Prime High street rents continued to be strong at €110 per Sqm. Asking rents at the lower end of the scale, for larger units can be €40 – 50 per Sqm lower.

� Peripheral retail areas experienced an increase in the vacancy rate. Interest in these locations is mostly generated by local retailers, service providers and banks interested in expanding their network. Rental levels in these areas range from €15 – 25 per Sqm.

PIPELINE � The retail market in Belgrade will

feature several new, large shopping center commencements and completions in 2011.

� The Pasino brdo neighborhood shopping center, anchored by Roda market, is expected to have their big opening in the beginning of 2011. The second phase of Pancevo Retail Park featuring 8,000 Sqm GLA, as well as the second phase of Delta Park in Kragujevac are both expected for delivery during 2011.

� Fashion House Outlet Center Belgrade, located between Belgrade and Novi Sad in Indjija Retail Park; will feature 15,000 Sqm in phase one and is scheduled for completion in 2011.

� In terms of commencements, Rajiceva shopping center — the first shopping center development in the downtown area comprising 18,500 Sqm GLA is expected to start in Q1 2011. Completion is scheduled for 2012.

� Big CEE, an Israeli company, plans to develop a new retail park in the vicinity of Novi Sad – some 4 km away from the city. This project will feature 30,000 Sqm of GLA and 1,500 parking spaces. The building process is expected to commence during 2011 with completion set for 2012.

PROGNOSIS � The Serbian retail market experienced

its biggest expansion during 2007 – 2009, although it still lags behind more developed regional capitals on a Sqm per capita basis. While the potential is there, this depends on Serbia’s ability to generate economic growth and stability, which is looking ever more promising.

� Based on planned and committed developments, the retail offer in Serbia is clearly growing and improving. With this change comes more choice for retailers considering Serbia/Belgrade as their market entry point. Although most retailers choose Belgrade to start building their network, Mr. Bricolage and TKC opted for other cities and are planning their Belgrade expansion in 2011.

� A continued improvement in retail turnover, albeit it moderate in 2011, will help bring more retailers to the market.

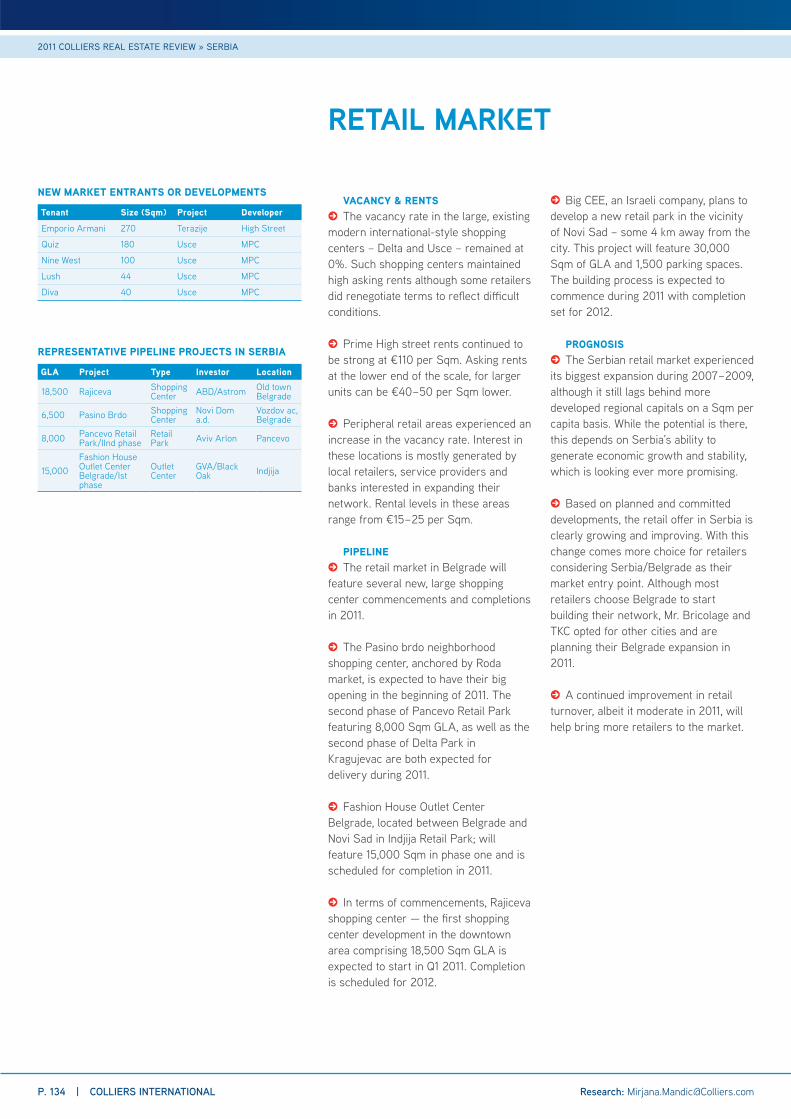

NEW MARKET ENTRANTS OR DEVELOPMENTS

Tenant Size (Sqm) Project DeveloperEmporio Armani 270 Terazije High Street

Quiz 180 Usce MPC

Nine West 100 Usce MPC

Lush 44 Usce MPC

Diva 40 Usce MPC

REPRESENTATIVE PIPELINE PROJECTS IN SERBIA

GLA Project Type Investor Location

18,500 Rajiceva Shopping Center ABD/Astrom Old town

Belgrade

6,500 Pasino Brdo Shopping Center

Novi Dom a.d.

Vozdov ac, Belgrade

8,000 Pancevo Retail Park/IInd phase

Retail Park Aviv Arlon Pancevo

15,000Fashion House Outlet Center Belgrade/Ist phase

Outlet Center

GVA/Black Oak Indjija

2011 CollIERS REAl EStAtE REvIEw » SERBIA

Research: [email protected]

CollieRS inteRnAtionAl | P. 135

2011 CollIERS REAl EStAtE REvIEw » SERBIA

RESIDENTIAL MARKET

OVERVIEW � The Serbian residential market

activity continued on a downward trend in 2010. In particular, average sales prices decreased and construction activity was lower significantly than in previous years. This is most prevalent in Belgrade, which is traditionally the most active residential market.

SUPPLY � The Serbian market witnessed a

continued decrease in the number of building permits issued in 2010. On average there was a 20% decreased in building permits issued in 2010 when compared to 2009. In Belgrade, this is a continuation of the trend set in 2009 when the market experienced a 21.1% decrease in the delivery residential units compared to 2008.

PIPELINE � Several major developments have

been announced to be delivered through the phasing of developments over the next 3 years. The most notable developments include large scale complexes such as West 65 (GBA: 47,500 Sqm) in New Belgrade, Golf 8 (GBA: 15,172 Sqm) in Banovo brdo, Basal complex (GBA: 7,500 M2) and 4. Juli Government complex (GBA: 271,252 Sqm) in New Belgrade. Besides New Belgrade, which traditionally offers the largest possibilities for development, major developments will also take place in other major municipalities.

DEMAND AND SALES PRICE � Sales prices dropped a further 5% in

the second half of 2010, meaning prices have dropped by some 15 – 20% in the last two years as demand remains muted.

� In the last 12 months the largest decreases occured in the municipality of Cukarica (cca. 10%), followed by Stari Grad (cca. 8.25%), Savski Venac (cca. 7.25%), New Belgrade (cca. 6.85%), Vozdovac (cca. 6.75%), Vracar (cca. 6.15%), Palilula (cca. 5.55%), Zemun (cca. 5.35%) and Zvezdara (cca. 3.75%).

The highest sales prices of new developments are still achieved in the municipalities of Stari Grad, then Savski Venac, New Belgrade and Vracar.

RENTS � In the second half of 2010, net rental

levels remained similar to the first half of 2010. Traditionally the most attractive area for renting is Senjak, followed by Dedinje and Stari Grad. In the second half of 2010 demand for apartments in Stari Grad (old town) increased considerably. There was also an increase in demand for apartments in Vracar. Demand for New Belgrade showed a marked decrease.

� Average rental levels Sqm/pcm in Belgrade’s most popular municipalities range from €6–12. Rents differ by location – from the top of the market, such as Senjak (€9 – 12), to the lower end of the market such as Banovo Brdo (€6 – 8).

FORECAST � Sales prices are expected to decline

in the short term, before stabilising in the second half of 2011. It is expected that the apartments constructed by the Government will have influence on the mid- to low-class market. This should result in a slight price reduction of similarly targeted projects in order to be more competitive.

� At present a discrepancy in prices among similar projects in similar locations still exists. Colliers expects greater transparency and sophistication on the market to emerge in future so prices are more closely correlated to location, size and the quality of a given project.

RESIDENTIAL SUPPLY IN SERBIA (No. of units)

Tenant 2008 2009 IndexSerbia 17,967 17,408 -3.1%

Belgrade 7,306 5,759 -21.1%

Novi Sad 1,946 2,186 +12.3%

Nis 1,000 1,016 +1.6%

Kragujevac 419 532 +26.9%

Subotica 472 409 -13.3%

Source: Statistical Office of Republic of Serbia

AVG. RANGE OF PRICES FOR NEW DEVELOPMENTS

Municipality BelgradeVoždovac €1,500 – 1,700 (VAT included)

Vračar €2,300 – 2,500 (VAT included)

Zvezdara €1,650 – 1,850 (VAT included)

Zemun €1,200 – 1,400 (VAT included)

New Belgrade €2,300 – 2,600 (VAT included)

Palilula €1,700 – 1,900 (VAT included)

Stari Grad €3,000 – 3,300 (VAT included)

Čukarica €2,000 – 2,300 (VAT included)

Savski Venac €2,300 – 2,700 (VAT included)

Source: Colliers International

RENTAL LEVELS

Area Average Rent (€/Sqm/pcm)Savski Venac (Senjak) 9 – 12

Savski Venac (Dedinje) 9 – 11

Vracar 8 – 12

Stari Grad 8 – 11

New Belgrade 7 – 10

Vozdovac 7 – 9

Cukarica (Banovo Brdo) 6 – 8

Source: Colliers International

-0.12

-0.10

-0.08

-0.06

-0.04

-0.02

0

PRICE DECREASE TREND IN BELGRADE

| | | | | | | | |

Cukari

ca

Stari G

rad

Savsk

i Ven

ac

New B

elgrad

e

Vozd

ovac

Vrac

ar

Palilul

a

Zemun

Zvez

dara

Source: Colliers International

Research: [email protected]

P. 136 | CollieRS inteRnAtionAl Contact: [email protected]

SERBIA TAX SUMMARY

CORPORATE INCOME TAX AND CAPITAL GAINS

� Corporate income tax is levied at a 10% flat rate on resident and non-resident entities. A resident entity is a legal entity which is incorporated or has a place of effective management and control on the territory of Serbia. Resident legal entities are liable for payment of tax on their worldwide income in the country. Non-resident entities pay tax on the income generated through a permanent establishment on the territory of Serbia (branches).

� The tax period is the calendar year. A corporate tax return has to be submitted by 10 March of the following year for the then previous year, whereas corporate income tax is to be paid during the year through monthly advanced payments (by 15th in the month for the previous month).

� Taxable income is established on the basis of accounting profit disclosed in the annual income statement, in accordance with International Financial Reporting Standards, and is subject to further adjustments in the tax balance.

� Capital gains are disclosed separately in the tax balance and are subject to a 10% tax. The capital gain is the difference between the sale and purchase price of assets (real estate, securities, intellectual property rights, investment units). If such difference is negative, a capital loss is reported.

LOSSES � Losses generated from business, financial

and non-business transactions, excluding capital losses, may be carried forward for up to five subsequent tax periods and can be offset against future taxable income. Losses carried forward into the future are not cancelled by mergers, acquisitions, spin-offs and other organizational changes.

� Capital losses may be carried forward for five years and offset only against capital gains.

TAX DEPRECIATION � For corporate income tax purposes, fixed

assets are divided into five groups, with depreciation rates prescribed for each group:

Group Depreciation rate

I 2.5%

II 10%

III 15%

IV 20%

V 30%

� Fixed assets classified under the first group are depreciated using the straight-line method, while a declining method is prescribed for fixed assets in the other groups. A depreciation rate of 2.5% is applied to the purchase value of a first group fixed asset where the real estate is classified.

THIN CAPITALIZATION � Interest and related expenses towards

related entities are deductible up to four times the value of the taxpayer’s equity (limit for banks is 10 times the bank’s equity). The non-deductible amount of interest expense may not be carried forward any longer and represents a permanent difference.

WITHHOLDING TAXES � Withholding tax at the rate of 20% is

deducted from dividends, share in profits, royalties, interest, capital gains and lease payments for real estate and other assets derived by non-residents on the territory of Serbia. Withholding tax may be reduced by double taxation treaties.

� If a non-resident taxpayer receives capital gains from a Serbian resident, other non-resident, resident or non-resident individual or open investment fund on the territory of Serbia, 20% withholding tax has to be paid if not provided otherwise by a respective double taxation treaty. The non-resident taxpayer has to submit a special tax return within 15 days of generating the capital gains via proxy, based on which the Tax Authorities assess the tax liability.

DOUBLE TAXATION CONVENTIONS � As at 1 January 2011 Serbia has 47

effective double taxation conventions on income and capital. Agreements with Egypt, France, Great Britain and Malaysia cover the avoidance of double taxation of income only.

VAT � VAT is levied on the following: — supply of goods and services by a taxpayer on the territory of Serbia in the course of doing business and.

— import of goods into Serbia.

� A taxpayer is any entity that independently supplies goods and services in the course of doing business.

� Each entity whose turnover in the previous 12 months (sales of goods and services excluding sales of real estate and equipment used in performing business activity) exceeds RSD 4 Mln is obliged to register for VAT. An entity whose turnover in the previous 12 months or forecasted turnover in the following 12 months is between RSD 2 and 4 Mln may opt to be registered for VAT (small undertakings).

� Only the first transfer of newly built buildings (i.e. buildings built as of 1 January 2005) is subject to VAT at the rate of 8% (residential building) or 18%. Supply of land, as well as renting of land is exempt from VAT without credit.

PROPERTY TAX � In Serbia tax on property is paid by the

title holder of property rights (ownership, right of use, etc.). Companies pay property tax at the maximum rate of 0.4% per year on the net book value of land and completed development property as at 31 December.

REAL ESTATE TRANSFER TAX � Second and all future transfers of

real-estate property, as well as the first transfer of real-estate property built before 1 January 2005, are subject to transfer tax at the rate of 2.5%. The taxpayer is the seller. However, the buyer may assume liability of paying this tax, but this has to be stipulated in the sales and purchase agreement.

2011 CollIERS REAl EStAtE REvIEw » SERBIA

www.colliers.com