-

8/21/2019 CNBC Fed Survey, Sept 16, 2014

1/29

CNBC Fed Survey September 16, 2014Page 1 of 29

FED SURVEYSeptember 16, 2014

These survey results represent the opinions of 37 of the nations

top money managers, investment

strategists, and professional economists.

They responded to CNBCs invitation to participate in our online

survey. Their responses were collecte

on September 11-13, 2014. Participants were not required to

answer every question.

Results are also shown for identical questions in earlier

surveys.

This is not intended to be a scientific poll and its results

should not be extrapolated beyond those whodid accept our

invitation.

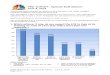

1.By how much do you believe the Fed will, on net, increase

ordecrease the size of its balance sheet in 2015?

-$104

-$146

$24

$60

-$83

-$200

-$150

-$100

-$50

$0

$50

$100

Billions

Mar 18 Apr 28 Jul 29 Aug 20 Sep 16

-

8/21/2019 CNBC Fed Survey, Sept 16, 2014

2/29

CNBC Fed Survey September 16, 2014Page 2 of 29

FED SURVEYSeptember 16, 2014

2.Will the Federal Reserve vote in October to end its QE

program

95%

5%

0%0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Yes No Don't know/unsure

-

8/21/2019 CNBC Fed Survey, Sept 16, 2014

3/29

CNBC Fed Survey September 16, 2014Page 3 of 29

FED SURVEYSeptember 16, 2014

3.What is the probability the Fed will begin a new QE program

in

the 12 months or two years after it concludes the current

QEprogram?(0%=No chance of new QE, 100%=Certainty of new QE)

0%

10%

20%

30%

40%

50%

60%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Chance of new QE

12 months 24 months

Averages:

12 months:10.0%

24 months:14.0%

-

8/21/2019 CNBC Fed Survey, Sept 16, 2014

4/29

CNBC Fed Survey September 16, 2014Page 4 of 29

FED SURVEYSeptember 16, 2014

4.The Fed will remove the phrase considerable time from its

monetary policy statement in ...

41%

24% 24%

11%

0%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

September October December After December Don'tknow/unsure

-

8/21/2019 CNBC Fed Survey, Sept 16, 2014

5/29

CNBC Fed Survey September 16, 2014Page 5 of 29

FED SURVEYSeptember 16, 2014

5.Overall, how do you rate the clarity and credibility of

Fed

communications?

60%61%

63%

68% 64%62%

73%

39% 39%38%

32% 36%

35%

22%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Oct 29 Dec 17 Jan 28 Mar 18 Apr 28 Jul 29 Sep 16

Survey dates

Very/somewhat clear and credible Somewhat not/not very clear and

credible

-

8/21/2019 CNBC Fed Survey, Sept 16, 2014

6/29

CNBC Fed Survey September 16, 2014Page 6 of 29

FED SURVEYSeptember 16, 2014

6.Which of these is the bigger risk to your forecasts for Fed

polic

in 2014?

26% 26%

40%

9%

31%

22%

47%

0%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Fed will be moredovish than I

expect

Fed will be morehawkish than I

expect

Risks are balanced Don't know/unsure

Jul 29 Sep 16

-

8/21/2019 CNBC Fed Survey, Sept 16, 2014

7/29

CNBC Fed Survey September 16, 2014Page 7 of 29

FED SURVEYSeptember 16, 2014

Which of these is the bigger risk to your forecasts for Fed

policy i

2015?

49%

34%

14%

3%

53%

39%

8%

0%

0%

10%

20%

30%

40%

50%

60%

Fed will be moredovish than I

expect

Fed will be morehawkish than I

expect

Risks are balanced Don't know/unsure

Jul 29 Sep 16

-

8/21/2019 CNBC Fed Survey, Sept 16, 2014

8/29

CNBC Fed Survey September 16, 2014Page 8 of 29

FED SURVEYSeptember 16, 2014

7.Relative to an economy operating at full capacity, what

best

describes your view of the amount of resource slack in the

U.S.right now for labor?

48%

36%

4%

8%

4%

0%

34%

40%

6%

11%

9%

0%

20%

60%

3%

6%

9%

3%

0% 10% 20% 30% 40% 50% 60% 70%

Considerably more slack now

Modestly more slack now

No difference

Modestly less slack now

Considerably less slack now

Don't know/unsure

July 29 August 20 Sep 16

-

8/21/2019 CNBC Fed Survey, Sept 16, 2014

9/29

CNBC Fed Survey September 16, 2014Page 9 of 29

FED SURVEYSeptember 16, 2014

Relative to an economy operating at full capacity, what best

describes your view of the amount of resource slack in the

U.S.right now for production capacity?

12%

56%

8%

16%

4%

4%

9%

60%

14%

9%

9%

0%

8%

64%

8%

14%

3%

3%

0% 10% 20% 30% 40% 50% 60% 70%

Considerably more slack now

Modestly more slack now

No difference

Modestly less slack now

Considerably less slack now

Don't know/unsure

July 29 August 20 Sep 16

-

8/21/2019 CNBC Fed Survey, Sept 16, 2014

10/29

CNBC Fed Survey September 16, 2014Page 10 of 29

FED SURVEYSeptember 16, 2014

8.What best describes your view of the most likely outcome

from

the current period of extraordinary monetary policy?

34% 34%

26%

6%

17%

44%

22%

17%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

It will end badlywith one or more of

the following: a

stock market crash,high inflation,

recession

The Fed willnavigate a smooth

transition to more

normal policy

Odds are evenly splitbetween either

outcome

Don't know/unsure

July 29 Sep 16

-

8/21/2019 CNBC Fed Survey, Sept 16, 2014

11/29

CNBC Fed Survey September 16, 2014Page 11 of 29

FED SURVEYSeptember 16, 2014

9.Where do you expect the S&P 500 stock index will be on

?

1857

19131924

1937

1956

2000

20322017

2029

2053

21092075

2149

1,800

1,850

1,900

1,950

2,000

2,050

2,100

2,150

2,200

Dec 17 Jan 28 '14 Mar 18 Apr 28 Jun 4 July 29 Sep 16

Survey Dates

December 31, 2014 June 30, 2015 December 31, 2015

-

8/21/2019 CNBC Fed Survey, Sept 16, 2014

12/29

CNBC Fed Survey September 16, 2014Page 12 of 29

FED SURVEYSeptember 16, 2014

10. What do you expect the yield on the 10-year Treasury

note

will be on ?

3.44%

3.37% 3.32%

3.21%

2.90%

2.83%

2.76%

3.54%

3.24%

3.15% 3.16%

3.43% 3.45%

2.0%

2.5%

3.0%

3.5%

4.0%

Dec 17 Jan 28 '14 Mar 18 Apr 28 Jun 4 Jul 29 Sep 16

Survey Dates

December 31, 2014 June 30, 2015 December 31, 2015

-

8/21/2019 CNBC Fed Survey, Sept 16, 2014

13/29

CNBC Fed Survey September 16, 2014Page 13 of 29

FED SURVEYSeptember 16, 2014

11. What is your forecast for the year-over-year percentage

change in real U.S. GDP for ?

Jan29,'13

Mar19

Apr30

Jun18

Jul30

Sep17

Oct29

Dec17

Jan28,'14

Mar18

Apr28

Jun 4Jul29

Sep16

2014 +2.56 +2.60 +2.62 +2.56 +2.52 +2.63 +2.53 +2.62 +2.77 +2.78

+2.75 +2.33 +1.89 +2.3

2015 +2.90 +3.02 +3.00 +2.81 +2.75 +2.9

+2.56%+2.60% +2.62%

+2.56%+2.52%

+2.63%

+2.53%

+2.62%

+2.77% +2.78% +2.75%

+2.33%

+1.89%

+2.3%

+2.90%

+3.02% +3.00%

+2.81%

+2.75%

+2.9%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

2014 2015

-

8/21/2019 CNBC Fed Survey, Sept 16, 2014

14/29

CNBC Fed Survey September 16, 2014Page 14 of 29

FED SURVEYSeptember 16, 2014

12. What is your forecast for the year-over-year percentage

change in the headline U.S. CPI for ?

1.78%

2.02% 1.99%2.02%

2.29% 2.27%

1.0%

1.2%

1.4%

1.6%

1.8%

2.0%

2.2%

2.4%

Jun 4 Jul 29 Sep 16

Survey Dates

2014 2015

-

8/21/2019 CNBC Fed Survey, Sept 16, 2014

15/29

CNBC Fed Survey September 16, 2014Page 15 of 29

FED SURVEYSeptember 16, 2014

13. When do you expect the Fed to allow its balance sheet to

decline?

Note: In the April survey, the question was phrased as: When do

you believe the Fed will be

reducing the size of its balance sheet?

0%

5%

10%

15%

20%

25%

30%

Oct

Nov

Dec

Jan'15

Feb

Mar

Apr

May

JunJul

Aug

Sep

Oct

Nov

Dec

Jan'16

Feb

Mar

Apr

May

JunJul

Aug

Sep

Oct

Nov

Dec

Jan'17

AfterJan

Apr 28 Jun 4 Jul 29 Sep 16

Averages:April 28 survey:October 2015

June 4 survey:

March 2016

June 29 survey:

December 2015

Sept. 16 survey:

December 2015

-

8/21/2019 CNBC Fed Survey, Sept 16, 2014

16/29

CNBC Fed Survey September 16, 2014Page 16 of 29

FED SURVEYSeptember 16, 2014

14. When do you think the FOMC will first increase the fed

funds

rate?

0%

10%

20%

30%

40%

50%

60%

April 28 Jun 4 Jun 29 Aug 20 Sep 16

Averages:April 28 survey:

July 2015

June 4 survey:August 2015

July 29 survey:

August 2015

Aug 20 survey:

July 2015

Sep 16 survey:

June 2015

-

8/21/2019 CNBC Fed Survey, Sept 16, 2014

17/29

CNBC Fed Survey September 16, 2014Page 17 of 29

FED SURVEYSeptember 16, 2014

15. How would you characterize the Fed's current monetary

policy?

28%

43%

17%

13%

49%

43%

6%

3%

46%

49%

3%

3%

49%

43%

3%

6%

0% 10% 20% 30% 40% 50% 60%

Too accommodative

Just right

Too restrictive

Don't know/unsure

July 31, 2012 July 29, 2014 Aug 20 Sep 16

-

8/21/2019 CNBC Fed Survey, Sept 16, 2014

18/29

CNBC Fed Survey September 16, 2014Page 18 of 29

FED SURVEYSeptember 16, 2014

16. Where do you expect the fed funds target rate will be on

?

Jul 30Sep

17

Oct

29

Dec

17

Jan28

'14

Mar

18

Apr

28Jun 4 Jul 29

Aug

20

Sep

16

Dec 31, 2014

0.28%0.21%0.21%0.20%0.19%0.15%0.27%0.17%0.21%0.16%0.14%

Jun 30, 2015 0.50%0.39%0.40%

Dec 31, 2015

0.97%0.92%0.82%0.70%0.72%0.83%0.99%0.68%1.05%0.89%0.98%

Jun 30, 2016 1.53%1.56%

Dec 31, 2016 1.99%2.13%

0.28%

0.21% 0.21% 0.20% 0.19%0.15%

0.27%

0.17% 0.21% 0.16% 0.14%

0.50%

0.39% 0.40%

0.97%0.92%

0.82%

0.70% 0.72%

0.83%

0.99%

0.68%

1.05%

0.89%

0.98%

1.53%1.56%

1.99%

2.13%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

Dec 2016

June 2016

Dec 2015

June 2015

Dec 2014

-

8/21/2019 CNBC Fed Survey, Sept 16, 2014

19/29

CNBC Fed Survey September 16, 2014Page 19 of 29

FED SURVEYSeptember 16, 2014

17. At what fed funds level WILL/SHOULD the Federal Reserve

stop hiking rates in the current cycle? That is, what

will/shouldbe the terminal rate?

3.16%

3.44%

3.20%3.39%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

Will Should

Aug 20 Sep 16

-

8/21/2019 CNBC Fed Survey, Sept 16, 2014

20/29

CNBC Fed Survey September 16, 2014Page 20 of 29

FED SURVEYSeptember 16, 2014

18. When do you believe fed funds will reach its terminal

rate?

0%

5%

10%

15%

20%

25%

30%

35%

40%

Aug 20 Sep 16

Average:

Aug 20 survey:

Q4 2017

Sep 16 survey

Q3 2017

-

8/21/2019 CNBC Fed Survey, Sept 16, 2014

21/29

CNBC Fed Survey September 16, 2014Page 21 of 29

FED SURVEYSeptember 16, 2014

19. How much concern do you have that each of the following

could create wider global risks? (1=Not concerned at

all,10=Highest level of concern)

5.45.0

4.7

3.1

0

1

2

3

4

5

6

7

8

9

10

Economicweakness in

Europe

Trouble betweenRussia and

Ukraine

ISIS insurgencyand the U.S.

response

Scottishindependence

-

8/21/2019 CNBC Fed Survey, Sept 16, 2014

22/29

CNBC Fed Survey September 16, 2014Page 22 of 29

FED SURVEYSeptember 16, 2014

20. How big a threat to the U.S. economy are "tax inversions,"

in

which a U.S. company merges with a foreign company andmoves its

tax address overseas? (1=No threat at all,10=Enormous threat)

31%

25%

22%

13%

6%

0%

3%

0% 0% 0%0%

5%

10%

15%

20%

25%

30%

35%

1 2 3 4 5 6 7 8 9 10

Level of concern

Average:2.5

-

8/21/2019 CNBC Fed Survey, Sept 16, 2014

23/29

CNBC Fed Survey September 16, 2014Page 23 of 29

FED SURVEYSeptember 16, 2014

21. Whats the best solution for tax inversions?

Other:

Eliminate tax on foreign income for US corporations (and

individuals too!)

Legislation to encourage the return of cash of US corporations

now held abroad

50%

38%

6%

3% 3%

0%0%

10%

20%

30%

40%

50%

60%

Wait forcomprehensiveU.S. corporate

tax reform

Lower top U.S.corporate tax

rate now

Other Raise therequirement for

foreignownership

Don'tknow/unsure

None needed

On average, those selecting this optionthink the top rate should

be lowered to 19%

On average, those selecting this option think

the requirement should be raised to 51%

-

8/21/2019 CNBC Fed Survey, Sept 16, 2014

24/29

CNBC Fed Survey September 16, 2014Page 24 of 29

FED SURVEYSeptember 16, 2014

22. What is the single biggest threat facing the U.S.

economic

recovery?

0% 5% 10% 15% 20% 25% 30% 3

European recession/financial crisis

Tax/regulatory policies

Slow job growth

High gasoline prices

Overall inflationDeflation

Debt ceiling

Too little budget deficit reduction

Too much budget deficit reduction

Rise in interest rates

Geopolitical risks

Other

Don't know/unsure

Europ

reces

/fina

cris

Tax/regul

atory

policies

Slow job

growth

High

gasoline

prices

Overall

inflationDeflation

Debt

ceiling

Too little

budget

deficit

reduction

Too

much

budget

deficit

reduction

Rise in

interest

rates

Geopoliti

cal risksOther

Don't

know/un

sure

Apr 30 2031%20%2%0%2%2%2%9%11%0%

Jun 18 1528%20%2%3%3%0%2%13%13%0%

Jul 30 8%30%22%4%0%2%2%0%4%10%14%4%

Sep 17 4%27%22%7%2%0%4%2%4%18%7%2%

Oct 29 8%29%24%3%3%3%3%3%5%8%13%0%

Dec 17 5%32%29%5%2%0%2%2%2%15%2%2%Jan 28 '14

7%21%30%2%2%0%0%2%2%12%21%0%

Mar 18 1023%26%3%3%5%0%0%8%5%18%0%

Apr 28 3%26%21%0%3%5%0%3%3%8%18%13%0%

Jul 29 1229%12%0%6%3%0%0%0%12%12%12%3%

Sep 16 6%26%29%0%6%3%0%0%0%6%11%11%3%

Apr 30 Jun 18 Jul 30 Sep 17 Oct 29 Dec 17 Jan 28 '14 Mar 18 Apr

28 Jul 29 Sep 16

-

8/21/2019 CNBC Fed Survey, Sept 16, 2014

25/29

CNBC Fed Survey September 16, 2014Page 25 of 29

FED SURVEYSeptember 16, 2014

23. In the next 12 months, what percent probability do you

place on the U.S. entering recession? (0%=No chance ofrecession,

100%=Certainty of recession)

Aug11,

2011

Sep19

Oct31

Jan23,

2012

Mar16

Apr24

Jul31

Sep12

Dec11

Jan29,

2013

Mar19

Apr30

Jun18

Jul30

Sep6

Oct29

Dec17

Jan28

2014

Mar18

Apr28

Jul29

Sep16

Pct. 34.0 36.1 25.5 20.3 19.1 20.6 25.9 26.0 28.5 20.4 17.6 18.2

15.2 16.2 16.9 18.4 17.3 15.3 16.9 14.6 16.2 15.0

34.0%

36.1%

25.5%

20.3%

19.1%

20.6%

25.9%

26.0%

28.5%

20.4%

17.6%

18.2%

15.2%

16.2%16.9%

18.4%

17.3%

15.3%

16.9%

14.6%

16.2%

15.0%

0%

5%

10%

15%

20%

25%

30%

35%

40%

Survey Dates

-

8/21/2019 CNBC Fed Survey, Sept 16, 2014

26/29

CNBC Fed Survey September 16, 2014Page 26 of 29

FED SURVEYSeptember 16, 2014

24. What is your primary area of interest?

Comments:

Tony Crescenzi, PIMCO: The Fed in the months ahead will begin

to

say a long goodbye to its extraordinary monetary

accommodation,keeping its exit more a process than an event, hoping

throughout tokeep markets and the economy stable.

John Donaldson, Haverford Trust Co.: Many people seem toforget

we are at zero interest rates. Which would they prefer; amessage

from the Fed that the economy has improved enough thatthey can

begin the process of raising rates or a message thateverything is

still so weak that we need to stay at zero? We are still

years in time and hundreds of basis points from a restrictive

policythat could hamper the economy.

Dennis Gartman, The Gartman Letter: The concerns over Russiaand

Ukraine are materially over-blown; Russia's army of conscripts

isnot capable of over-running even Ukraine, and the fact that

the

Economics

50%

Equities17%

Fixed Income14%

Currencies3%

Other17%

-

8/21/2019 CNBC Fed Survey, Sept 16, 2014

27/29

CNBC Fed Survey September 16, 2014Page 27 of 29

FED SURVEYSeptember 16, 2014

President of Russia and Ukraine talk far more frequently than

iscommonly understood underscores the fact that this situation is

not

likely to become more severe than it has been thus far and is

farmore likely to become far less severe. Russia and Ukraine

"trade"with one another, and trading partners rarely go to extended

war.

Kevin Giddis, Raymond James/Morgan Keegan: The momentumtrain

towards higher rates is slowly leaving the station. The questionis:

How long are the tracks? The Fed will be the principal character

innext year's market moves.

Stuart Hoffman, PNC Financial Services Group: The"considerable

time" reference in the FOMC statement should bedropped and replaced

with something like "current and anticipatedprogress toward dual

mandate" at the October FOMC meeting whenthe end of QE is

announced.

Hugh Johnson, Hugh Johnson Advisors: Although thegeopolitical

risks are meaningful, they are unlikely to derail thecurrent stock

market-economic cycle. The most substantial risk

(although not imminent) is rising interest rates. We are

currentlywell away from a level that would endanger the current

cyclealthough there will be substantial pressure on the Fed to

raise ratesin Q1-Q3, 2015. This conclusion is consistent with

indicators thattend to lead economic activity. They are not as yet

signaling a turnin economic output.

John Kattar, Ardent Asset Advisors: The message has been loudand

clear that QE ends in October and rate increases are on the

horizon. In recent years, I give the Fed high marks for

transparency- they keep repeating they will do something and then

they do it.Count me as a believer. Rate increases are coming by

March, andthe first step is to remove the calendar guidance from

the statementat this meeting.

-

8/21/2019 CNBC Fed Survey, Sept 16, 2014

28/29

CNBC Fed Survey September 16, 2014Page 28 of 29

FED SURVEYSeptember 16, 2014

David Kotok, Cumberland Advisors: The markets are

notanticipating that energy prices will fall below the marginal

cost of

production in the U.S. The risk of that price decline is rising

asglobal slowing of growth intensifies.

Subodh Kumar, Subodh Kumar & Associates: Geopolitics and

aFederal Reserve in QE exit lead us to expect volatility and to

favorquality across assets, not the financial engineering once more

infavor. From dislocation risk in Britain to tension with Russia to

MiddleEast turmoil to European and U.S. fiscal woes, equity and

bondmarkets have overlooked risk. The Federal Reserve has lacked

clarity

but appears in dial back of the over accommodation resulting

fromQE2, which is likely to be volatile for too-complacent

markets.

Guy LeBas, Janney Montgomery Scott: The one thing that couldsend

the train veering off course on Wednesday is a decision byYellen to

talk up risk premia. Bernanke did the same last summerover concern

for the level of yields and the result was problematicfor all

investors. This time around it isn't about low yields, but

aboutcomplacency in lending markets. With default rates low, we're

far

from a danger zone in the credit markets, but Yellen could

choose topoint out the problem and try to make it go away early by

enforcingloan pricing discipline.

Rob Morgan, V2V Associates: U.S. corporations that are

'taxinverting' themselves out of the country show that the nation

isfacing the same problem that many states in the Northeast

andMidwest are facing - companies are leaving a hostile tax

environmentto go to a friendlier one. Lower the corporate tax rate

now, America!

Joel Naroff, Naroff Economic Advisors: The press have done

theFed's job of preparing the markets for a change in policy so

theFOMC should take advantage of the opening by signaling a

tighteningcould come sooner rather than later.

-

8/21/2019 CNBC Fed Survey, Sept 16, 2014

29/29

FED SURVEYSeptember 16, 2014

Lynn Reaser, Point Loma Nazarene University: The Fed

hascompleted an orderly exit from its bond purchase program,

but

markets are likely to be much less tolerant of rate hikes. The

Fedmight get the timing and amount of rate increases just right,

but donot count on it. Unfortunately, rate increases are likely to

be toosoon and too much or too little and too late.

Allen Sinai, Decision Economics: The U.S. economy finally

has"normalized." In a "normal" business expansion, interest

ratesshould rise. Zero interest rates make little sense in a

normalbusiness expansion.

Hank Smith, Haverford Investments: Even after tapering and

thebeginning of the increasing of the fed funds rate, monetary

policywill still be very accommodative for several more years.

Diane Swonk, Mesirow Financial: The Fed is hedging what it

seesas the greatest downside risk to the economy, which is a

recession.It is unclear there is any way out if we skip into

another recession.

Peter Tanous, Lynx Investment Advisory: Stock market view ofa

world in turmoil: Don't Worry; Be Happy.

Scott Wren, Wells Fargo Advisors: The modest

growth/modestinflation economy we have been living with is unlikely

to change overthe next 12-24 months. Stocks need to be bought on

any pullbacks.This cyclical bull market has more room to run over

the next 2-3years.