-

7/27/2019 CNBC Fed Survey results, October 29, 2013

1/33

CNBC Fed Survey October 29, 2013Page 1 of 33

FED SURVEYOctober 29, 2013

These survey results represent the opinions of 40 of the nations

top money managers, investment

strategists, and professional economists.

They responded to CNBCs invitation to participate in our online

survey. Their responses were collecte

on October 25-26, 2013. Participants were not required to answer

every question.

Results are also shown for identical questions in earlier

surveys.

This is not intended to be a scientific poll and its results

should not be extrapolated beyond those who

did accept our invitation.

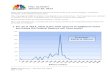

1.For all of 2013 and for all of 2014 (and only in 2014), what

isthe total amount of additional asset purchases the Federal

Reserve will have made?

$858.8$917.0 $936.6

$883.6$921.9 $941.9

$948.5

$1,023.7

$370.6 $367.1 $373.5 $374.8 $381.9

$646.1

$0

$200

$400

$600

$800

$1,000

$1,200

1/29/2013 4/30/2013 7/30/2013 9/17/2013

Billions

2013 2014

-

7/27/2019 CNBC Fed Survey results, October 29, 2013

2/33

CNBC Fed Survey October 29, 2013Page 2 of 33

FED SURVEYOctober 29, 2013

2.In what month do you expect the Fed to begin tapering

itspurchases?

0%

10%

20%

30%

40%

50%

60%

June 18 July 30 Sept 6 Sept 17 Oct 29

Averages

Jan 29: Dec 2013

March 19: Jan 2014

April 30: Feb 2014

June 18: Dec 2013

July 30: November 2013

Sep 6: November 2013

Sept 17: November 2013

Oct 29: April 2014Plurality of 45% said March 2014

-

7/27/2019 CNBC Fed Survey results, October 29, 2013

3/33

CNBC Fed Survey October 29, 2013Page 3 of 33

FED SURVEYOctober 29, 2013

3.By how much do you believe the Fed will reduce its

assetpurchases in that first month?

$22.1

$19.2

$12.6

$14.5 $14.2

$0

$5

$10

$15

$20

$25

July 5 July 30 Sept 6 Sept 17 Oct 29

Billions

On average, respondents

believe the Fed willmaintain its new level ofasset purchases for

3.03months.

-

7/27/2019 CNBC Fed Survey results, October 29, 2013

4/33

CNBC Fed Survey October 29, 2013Page 4 of 33

FED SURVEYOctober 29, 2013

4.What mix of Treasuries vs. mortgage-backed securities do

youexpect in the Federal Reserve's taper?

28% 29%

72% 71%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Sep 17 Oct 29

Treasuries MBS

-

7/27/2019 CNBC Fed Survey results, October 29, 2013

5/33

CNBC Fed Survey October 29, 2013Page 5 of 33

FED SURVEYOctober 29, 2013

5.When do you expect the Federal Reserve will completely

stoppurchasing assets?

0%

5%

10%

15%

20%

25%

30%

June 18 July 30 Sept 6 Sept 17 Oct 29

Averages

Jan 29: Nov 2013

Mar 19: May 2014Apr 30: July 2014Jun 18: July 2014

July 30: Aug 2014

Sept 6: Aug 2014

Sept 17: Aug 2014

Oct 29: Dec 2014

Plurality of 23%saidOct1415% said later than Jun 2015

-

7/27/2019 CNBC Fed Survey results, October 29, 2013

6/33

CNBC Fed Survey October 29, 2013Page 6 of 33

FED SURVEYOctober 29, 2013

6.Based on your expectations for tapering, what percentage ofthe

ultimate impact on each market is already discounted inthe overall

prices of that market?

66%

58%

68%

81%

73%

82%81%

70%

81%

58%

50%

57%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Treasuries Equities Mortgages

July 30 Sept 6 Sept 17 Oct 29

-

7/27/2019 CNBC Fed Survey results, October 29, 2013

7/33

CNBC Fed Survey October 29, 2013Page 7 of 33

FED SURVEYOctober 29, 2013

7.Compared to Ben Bernanke, Fed chair nominee Janet Yellenwill

be:

15%

44%

28%

3%

0%

10%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Much moredovish

Somewhatmore dovish

No different Somewhatmore

hawkish

Much morehawkish

Don'tknow/unsure

-

7/27/2019 CNBC Fed Survey results, October 29, 2013

8/33

CNBC Fed Survey October 29, 2013Page 8 of 33

FED SURVEYOctober 29, 2013

8.Please rate the following four candidates for the Fedchairmans

job on the listed qualities. (On a scale of 1 to 5,where a higher

number means a higher rating.)

Numbers in parentheses to the right of the qualities represent

how essential they are to the job of Fchairman on a scale of 1

(least) to 5 (most), as ranked in the July 30 survey.

4.35

4.22

3.32

3.95

3.35

3.38

4.16

3.97

3.42

3.36

4.05

3.42

3.44

3.54

2.89

3.08

3.65

4.57

3.34

3.31

2.00 2.50 3.00 3.50 4.00 4.50 5.0

Monetary policy expertise (4.52)

Ability to manage a financial crisis (4.30)

Good communication skills (4.22)

Respect from financial markets (4.18)

Concern about inflation (4.08)

Financial market expertise (4.04)

Respect from international financial leaders (3.41)

Concern about unemployment (3.39)

Good political skills (3.27)

Banking regulatory expertise (2.94)

Bernanke Yellen

-

7/27/2019 CNBC Fed Survey results, October 29, 2013

9/33

CNBC Fed Survey October 29, 2013Page 9 of 33

FED SURVEYOctober 29, 2013

Sum of candidate ratings weighted by essentialness of each

quality.

0

20

40

60

80

100

120

140

160

Yellen Bernanke

Banking regulatory expertise (2.94)

Good political skills (3.27)

Concern about unemployment (3.39)

Respect from international financial

leaders (3.41)

Financial market expertise (4.04)

Concern about inflation (4.08)

Respect from financial markets (4.18)

Good communication skills (4.22)

Ability to manage a financial crisis

(4.30)

Monetary policy expertise (4.52)

-

7/27/2019 CNBC Fed Survey results, October 29, 2013

10/33

CNBC Fed Survey October 29, 2013Page 10 of 33

FED SURVEYOctober 29, 2013

9.What grade would you give Fed Chairman Ben Bernanke?

Numerical average based on A=4, B=3, C=2, D=1, F=0

26%

42%

22%

5%

5%

22%

48%

19%

5%

3%

4%

23%

48%

13%

9%

0%

7%

30%

48%

18%

2%

2%

0%

21%

50%

21%

0%

3%

5%

0% 10% 20% 30% 40% 50% 60%

A

B

C

D

F

Don't know/unsure

Dec 22, 2010 July 21, 2011 Jan 23, 2012 Sept 17, 2013 Oct 29,

2013

Average forSept 17 survey:

B (3.00)

Average for

Oct 29survey:

B- (2.77)

-

7/27/2019 CNBC Fed Survey results, October 29, 2013

11/33

CNBC Fed Survey October 29, 2013Page 11 of 33

FED SURVEYOctober 29, 2013

Comments on this question:

Robert Brusca, Fact and Opinion Economics: (B) A for crisis

management andresponse. B/C for policy in the recovery.

John Donaldson, Haverford Trust Co.: (A) If he had not been on

duty, therecession could have been much, much worse.

Mike Dueker, Russell Investments: (B) Bernanke was great at

managing throughfinancial crisis, but not as strong at

understanding what would precipitate a financialcrisis.

Stuart Hoffman, PNC: (A) An A for effort and for results.

Lee Hoskins, Pacific Research Institute: (C) Bernanke

resurrected the discreditePhillips curve with strong support from

Yellen, so expect a weak response to risinginflation in the

future.

Barry Knapp, Barclays PLC: (B) Crisis management is an A, impact

of 5+ years ofZIRP (zero interest rate policy) and UMP is likely to

prove less favorable.

David Kotok, Cumberland Advisors: (B) Before Lehman, results

were based on

academic view. After Lehman failed, he became seasoned and

forceful.

Subodh Kumar, Subodh Kumar & Associates: (C) The total

Bernankeconsideration is pre-2007 miss of bubble; good skills at

QE1 at start of crisis; miss of

QE3 in boosting real growth.

Justin Lederer, Cantor Fitzgerald: (B) Based on 2008

actions.

Lynn Reaser, Point Loma Nazarene University: (B) Mr. Bernanke

handled thefinancial crisis very well. The exit strategy and

implementation strategy from

monetary ease remain to be tested.

John Roberts, Hilliard Lyons: (B) Really a B+. He helped inflate

the bubble in thefirst place, and probably gets a low grade because

of this. However, the response to

the crisis was such to overwhelm those issues. The question,

however, becomeswhether he extends the current accommodation too

long. From that perspective, you

could probably give him an incomplete because the ultimate grade

will not be appare

-

7/27/2019 CNBC Fed Survey results, October 29, 2013

12/33

CNBC Fed Survey October 29, 2013Page 12 of 33

FED SURVEYOctober 29, 2013

for a significant period after he leaves.

John Ryding, RDQ Economics: (C) A+ for handling of financial

crisis, C forcommunication, D for monetary policy.

Diane Swonk, Mesirow Financial: (A) We will look back and

realize he saved usfrom a depression worse than the Great

Depression.

Peter Tanous, Lynx Investment Advisory: (Don't Know/Unsure) We

won't knowthe final grade until we see the effects of the massive

increase in the Fed's balance

sheet and the effect, if any, of "printing" huge amounts of new

money.

Jason Trennert, Strategas: (B) He deserves an A+ for

understanding that he couldincrease the size of the Fed's balance

sheet without creating inflation. If there is a

problem, in my view it's that his munificence has allowed fiscal

policy makers tocompletely shirk their responsibilities to the

American people.

.

-

7/27/2019 CNBC Fed Survey results, October 29, 2013

13/33

CNBC Fed Survey October 29, 2013Page 13 of 33

FED SURVEYOctober 29, 2013

10.Overall, how do you rate the clarity and credibility of

Fedcommunications?

5%

55%

21%

18%

0%0%

10%

20%

30%

40%

50%

60%

Very clear andcredible

Somewhat clearand credible

Somewhat notclear and

credible

Not very clearand credible

Don'tknow/unsure

-

7/27/2019 CNBC Fed Survey results, October 29, 2013

14/33

CNBC Fed Survey October 29, 2013Page 14 of 33

FED SURVEYOctober 29, 2013

11.Since September 2012, market functioning in the governmenbond

market has:

2%

8%

4%3%

19%

11%12%

17%

20%

24%

60%

65%

47%46%

42%

50%

15%

15%

29%

25%27%

16%

2% 2% 2% 2%

3%0%

10%

20%

30%

40%

50%

60%

70%

March 19 April 30 June 18 July 30 Sept 17 Oct 29

Worsened somewhat

Improved somewhat

Improved a lot

Sta ed the same

Worsened a lot

-

7/27/2019 CNBC Fed Survey results, October 29, 2013

15/33

CNBC Fed Survey October 29, 2013Page 15 of 33

FED SURVEYOctober 29, 2013

12.Since September 2012, market functioning in the

mortgage-backed security market market has:

4%

2%

5%4% 5%

3%

31%

22%

21%

31%

23%

29%29%

39%

21%

31%

41%

37%

20% 20%

32%

20%18% 18%

2%

4%5%

6%

5%5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

March 19 April 30 June 18 July 30 Sept 17 Oct 29

Stayed the same

Worsened a lot

Improved a lot

Worsened somewhat

Improved somewhat

-

7/27/2019 CNBC Fed Survey results, October 29, 2013

16/33

CNBC Fed Survey October 29, 2013Page 16 of 33

FED SURVEYOctober 29, 2013

13.Compared with the debate at the beginning of the year,

thenext round of discussions to raise the debt ceiling will be:

19%

44%

35%

2%

24%

49%

27%

0%

10%

23%

67%

0%0%

10%

20%

30%

40%

50%

60%

70%

80%

More contentious About the same Less contentious Don't

know/unsure

July 30 Sept 17 Oct 29

-

7/27/2019 CNBC Fed Survey results, October 29, 2013

17/33

CNBC Fed Survey October 29, 2013Page 17 of 33

FED SURVEYOctober 29, 2013

What is the probability that the United States fails to raise

the

debt ceiling in the coming months and defaults on at least

someof its payments?

0%

10%

20%

30%

40%

50%

60%

70%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Percentage

ofrespondents

Default probability

July 30 Sept 17 Oct 29

AveragesJuly 30: 6.6%

Sept 17: 8.4%Oct 29: 4.6%

-

7/27/2019 CNBC Fed Survey results, October 29, 2013

18/33

CNBC Fed Survey October 29, 2013Page 18 of 33

FED SURVEYOctober 29, 2013

14.When it comes to the budget deficit, the United States:

80%

67%

52%

40% 40%

50%53%

16%

25%

39%

44%

52%

41%40%

4% 4%9%

12%

8% 9%5%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

January 29 March 19 April 30 June 18 July 30 Sept 17 Oct 29

Should urgently enact a plan that puts it on a path toward a

sustainable

budget deficit

Has at least a couple of years before it must enact such a

plan

Does not need to enact a plan that puts it on a path toward a

sustainabl

budget deficit

Don't know/unsure

-

7/27/2019 CNBC Fed Survey results, October 29, 2013

19/33

CNBC Fed Survey October 29, 2013Page 19 of 33

FED SURVEYOctober 29, 2013

15.Where do you expect the S&P 500 stock index will be on

?

1547

1589

1612

1655

1691

1654

1685

1753

1723

1751

1709

1752

1816

1,400

1,450

1,500

1,550

1,600

1,650

1,700

1,750

1,800

1,850

Jan 292013

Mar 19 Apr 30 Jun 18 Jul 30 Sep 6 Sep 30 Oct 29

Survey Dates

December 31, 2013 June 30, 2014

-

7/27/2019 CNBC Fed Survey results, October 29, 2013

20/33

CNBC Fed Survey October 29, 2013Page 20 of 33

FED SURVEYOctober 29, 2013

16.What do you expect the yield on the 10-year Treasury notewill

be on ?

2.31% 2.35%

2.10%

2.41%

2.73%

3.00% 3.02%

2.65%

2.80%

3.10%

3.33%3.39%

3.00%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

Jan 29

2013

Mar 19 Apr 30 Jun 18 Jul 30 Sep 6 Sep 30 Oct 29

Survey Dates

December 31, 2013 June 30, 2014

-

7/27/2019 CNBC Fed Survey results, October 29, 2013

21/33

CNBC Fed Survey October 29, 2013Page 21 of 33

FED SURVEYOctober 29, 2013

17.What is your forecast for the year-over-year percentagechange

in real U.S. GDP for ?

+2.6%

+2.7%

+2.6%

+2.3%

+2.2%

+1.9%

+2.1%+2.1%+2.1%+2.1%

+1.9%

+2.0%+1.9%

+2.6%+2.6%+2.6%

+2.6%+2.5%

+2.6%

+2.5%

1.0%

1.5%

2.0%

2.5%

3.0%

Survey Dates

2013 2014

-

7/27/2019 CNBC Fed Survey results, October 29, 2013

22/33

CNBC Fed Survey October 29, 2013Page 22 of 33

FED SURVEYOctober 29, 2013

18.What effect, if any, did the government shutdown/debtceiling

debate have on your GDP forecast for these quarters?

0%

10%

20%

30%

40%

50%

60%

70%

80%

2013 Q4 2014 Q1 2014 Q2

Averages:

2013 Q4

-0.29%2014 Q1

No change

2014 Q2

+0.04%

-

7/27/2019 CNBC Fed Survey results, October 29, 2013

23/33

CNBC Fed Survey October 29, 2013Page 23 of 33

FED SURVEYOctober 29, 2013

19.(Asked if forecast was lowered) How much of the

negativeimpact came from:

53%

71%81%

44%

26%

19%

3% 3%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2013 Q4 2014 Q1 2014 Q2

Rise in uncertainty Government spending reductions Other

-

7/27/2019 CNBC Fed Survey results, October 29, 2013

24/33

CNBC Fed Survey October 29, 2013Page 24 of 33

FED SURVEYOctober 29, 2013

21.Compared to last year, the holiday shopping season will

be:

8%

23%

35%

31%

0%

4%

0%

5%

10%

15%

20%

25%

30%

35%

40%

A lot better Somewhatbetter

The same Somewhatworse

A lot worse Don'tknow/unsure

-

7/27/2019 CNBC Fed Survey results, October 29, 2013

25/33

CNBC Fed Survey October 29, 2013Page 25 of 33

FED SURVEYOctober 29, 2013

22.When do you think the FOMC will first increase the fed

fundsrate?

Increase fed funds rate

(Average response)

Survey Date

Dec

11,

2012

Jan

29,

2013

Mar

19,

2013

Apr

30,

2013

Jun

18,

2013

Jul

30,

2013

Sept

6,

2013

Sept

17,

2013

Sept

6,

2013

2013 Q2

Q3

Q4

2014 Q1

Q2

Q3

Q4

2015 Q12015

Q12015

Q12015

Q1

Q22015

Q22015

Q22015

Q2

Q32015

Q32015

Q32015

Q3

Q4

2016 Q1

Q2

Q3

Q4

2017 or later

-

7/27/2019 CNBC Fed Survey results, October 29, 2013

26/33

CNBC Fed Survey October 29, 2013Page 26 of 33

FED SURVEYOctober 29, 2013

23.Currently, Fed policy is not to raise interest rates until

theunemployment rate is at least 6.5%. Will the Fed change

thatguidance?

30%

60%

10%

44%

51%

4%

47%

42%

11%

0%

10%

20%

30%

40%

50%

60%

70%

Yes No Don't know/unsure

Jul 30 Sep 17 Oct 29

-

7/27/2019 CNBC Fed Survey results, October 29, 2013

27/33

CNBC Fed Survey October 29, 2013Page 27 of 33

FED SURVEYOctober 29, 2013

24.Where do you expect the fed funds target rate will be on

?

0.33%

0.27%

0.21%

0.17%0.19%0.19%

0.16%0.15%0.13% 0.13%

0.11%

0.20%0.18%

0.16%0.14%0.13%

0.28%

0.21%0.21%

0.97%

0.92%

0.82%

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

Jul 31 Sep12

Dec11

Jan29

2013

Mar19

Apr30

Jun18

Jul 30 Sep 6 Sep17

Oct29

Survey Dates

Dec 31, 2013 June 30, 2014 Dec 31, 2014 Dec 31, 2015

-

7/27/2019 CNBC Fed Survey results, October 29, 2013

28/33

CNBC Fed Survey October 29, 2013Page 28 of 33

FED SURVEYOctober 29, 2013

25.In the next 12 months, what percent probability do you

placeon the U.S. entering recession? (0%=No chance of

recession,100%=Certainty of recession)

34.0%

36.1%

25.5%

20.3%

19.1%

20.6%

25.9%

26.0%

28.5%

20.4%

17.6%

18.2%

15.2%

16.2%

16.9%

18.4%

0%

5%

10%

15%

20%

25%

30%

35%

40%

Survey Dates

-

7/27/2019 CNBC Fed Survey results, October 29, 2013

29/33

CNBC Fed Survey October 29, 2013Page 29 of 33

FED SURVEYOctober 29, 2013

26.What is the single biggest threat facing the U.S.

economicrecovery?

0% 5% 10% 15% 20% 25% 30% 3

European recession/financial crisis

Tax/regulatory policies

Slow job growth

High gasoline prices

Overall inflation

Deflation

Debt ceiling

Too little budget deficit reduction

Too much budget deficit reduction

Rise in interest rates

Other

Don't know/unsure

Europ

reces

/finan

cris

Tax/regul

atory

policies

Slow job

growth

High

gasoline

prices

Overall

inflationDeflation

Debt

ceiling

Too little

budget

deficit

reduction

Too

much

budget

deficit

reduction

Rise in

interest

rates

Other

Don't

know/un

sure

Apr 30 20%31%20%2%0%2%2%2%9%11%0%

Jun 18 15%28%20%2%3%3%0%2%13%13%0%

Jul 30 8%30%22%4%0%2%2%0%4%10%14%4%

Sep 17 4%27%22%7%2%0%4%2%4%18%7%2%

Oct 29 8%29%24%3%3%3%3%3%5%8%13%0%

Apr 30 Jun 18 Jul 30 Sep 17 Oct 29

-

7/27/2019 CNBC Fed Survey results, October 29, 2013

30/33

CNBC Fed Survey October 29, 2013Page 30 of 33

FED SURVEYOctober 29, 2013

27.What is your primary area of interest?

Comments:

Robert Brusca, Fact and Opinion Economics: God Help us.

John Donaldson, Haverford Trust Co.: The criticism of Yellen

asbeing soft on inflation is unfair. She is fully committed to the

Fed'sdual mission. There has been so little inflation during her

tenure asvice-chair, what opportunity has there been for her to

"talk tough"on inflation?

Mike Dueker, Russell Investments: While the increase in

stock

prices in 2013 might provide some optimism to Fed

policymakers,they have to consider whether consumption will respond

as stronglyto stock market wealth as previous estimates suggested.

Manypeople are behind in saving for retirement and they might view

stockmarket gains as more ephemeral than they used to, so

theirwillingness to consume part of recent stock market gains might

be

Economics45%

Equities

21%

Fixed Income

13%

Currencies

0%

Other21%

-

7/27/2019 CNBC Fed Survey results, October 29, 2013

31/33

CNBC Fed Survey October 29, 2013Page 31 of 33

FED SURVEYOctober 29, 2013

limited.

Kevin Giddis, Raymond James/Morgan Keegan: Just about thetime

you think the bond bull market is about to end because of somenewly

found economic strength, the U.S. government goes intoaction, and

makes it all better for bonds. This will likely continue into2014

as well. Thank you Washington!

Stuart Hoffman, PNC: Shorter holiday shopping season will

notprevent a rise in holiday sales of 3.0-3.5% from last year. 2

millionmore employed, high house and stock prices and lower

gasoline

prices drive holiday sales higher.

Lee Hoskins, Pacific Research Institute: Despite all the

forwardguidance, inflation target and employment rate guide,

post-policyaction still rests on next month's data. Effective

policy requires alonger-term perspective.

David Kotok, Cumberland Advisors: Federal government actionshave

ONLY added to slowing. Congress and the White House have

only made things worse than they would otherwise be.

Alan Kral, Trevor Stewart Burton & Jacobsen: With an

electioncoming, the Fed will refrain from tightening monetary

policy

Subodh Kumar, Subodh Kumar & Associates: Fudges on

U.S.budget restructuring, European finance restructuring and

laborrestructuring in Japan are risks for the global economy,

quantitativeeasing (QE) notwithstanding. Another QE collateral risk

is that it is

likely abetting political procrastination. Quality of delivery

and offinancial structure should be emphasized in portfolio

structure alongwith cash reserves and other assets for

diversification.

Rob Morgan, Fulcrum Securities: The weak non-farm payrollreport

on October 22nd virtually guarantees that the Fed won't taper

-

7/27/2019 CNBC Fed Survey results, October 29, 2013

32/33

CNBC Fed Survey October 29, 2013Page 32 of 33

FED SURVEYOctober 29, 2013

QE until 2014.

Chad Morganlander, Stifel Nicolaus (Washington

CrossingAdvisors): Unfortunately, the U.S. economy in 2014 will

look similarto 2013. This will force the Federal Reserve to

continue QE longerthan consensus expectations. Investors should

expect sub-pareconomic growth coupled with modest corporate

earnings and topline growth.

James Paulsen, Wells Capital Management: Could we have a bitof

an inflation scare sometime in 2014? Yellen will come in as

chairman perceived as a dove when the U.S. dollar is already

veryweak and falling, commodity prices bottomed in 2013 and may

beshowing signs of lifting again, emerging world economies

arereaccelerating after 2 years of slowing while both Europe and

Japanare growing again (adding again to global inflation

pressures).Inflation stock sectors like materials have been

outpacing the stockmarket in recent months, the Baltic freight rate

index has recentlyexploded higher, annual wage inflation is close

to breaking to newhighs for the recovery and the unemployment rate

may have a 6

percent-ish handle on it just as Yellen takes the helm.

Perhaps,most importantly, what if monetary velocity finally turns

up in 2014as it has in every post-war recovery. (This would really

change theconversation at the Fed)? I am not suggesting 2014 will

produce amajor inflation problem, but could it produce a "fear" of

inflation forthe first time in this recovery?

Lynn Reaser, Point Loma Nazarene University: The U.S.economy now

faces a crisis in confidence. Monetary policy can now

inflate asset prices but will have little impact on spurring

more jobgrowth and lower unemployment.

John Roberts, Hilliard Lyons: Too much

bullishness/complacencycurrently in the equity markets. While

earnings remain good, weakrevenue growth remains a worry and with

GDP growth as low as it is,

-

7/27/2019 CNBC Fed Survey results, October 29, 2013

33/33

FED SURVEYOctober 29, 2013

valuations are slightly extended in the current

economicenvironment.

John Ryding, RDQ Economics: September seriously hurt

thecredibility of Fed communications and has left the market

focusingexcessively on the latest jobs number.

Richard Steinberg, Steinberg Global Asset Management: Oncewe get

past the Washington noise (and it will be noisy), the focuswill

have to be job growth. Unemployed people don't buy goods

andservices.

Diane Swonk, Mesirow Financial: Brinkmanship has cost us inways

we will not know for years to come, economically

andgeopolitically

f