Embed Size (px)

Citation preview

December 06,2010

Phillips Carbon Black Ltd

On a ambitious growth plan.

SKP Securities Ltd www.skpmoneywise.com Page 1 of 14

Outlook & Recommendation

We have valued the company by applying the Discounted Cash Flow

Method and have arrived a fair value of Rs 254 implying an upside of

40% from current levels to be reached in 15 months time. While

calculating, we taken a WACC of 12.45% from FY11E to FY15E and a

terminal growth rate of 2% thereafter and hence initiate a BUY

recommendation.

CMP Rs. 180 Target Rs 254 Buy

Key Share Data Face Value (Rs.) 10.00

Equity Capital (Rs. Crs) 33.22

Market. Capitalization (Rs. Crs) 597

52-wk High / Low (Rs.) 242/134

Average Yearly Volume 57057

BSE code 506590

NSE code PHILIIPCARB

Reuters code PHIL.BO

Bloomberg code PHCB IN

Shareholding Pattern – 30

th September, 2010

Financials (Rs. Crs)

FY09 FY10 FY11E FY12E

Net Sales 1200 1344 1407 1783 Sales Gr 4% 15% 14% 27%

Operating Profit 9 204 224 332 PAT -65 123 106 179 PAT Gr -178% 289% -14% 69% EPS (Rs.) 0 43 32 52

Key Financial Ratios

FY09 FY10 FY11E FY12E

P/E 0.00 4.51 5.62 3.46 P/BV 0.42 1.69 1.11 0.86 MCap/Sales 0.08 0.41 0.42 0.33 EV/EBIDTA 56.76 5.25 4.78 3.22 ROCE -1.81% 22.73% 18.00% 28.00% RONW -28.13% 45.22% 20.00% 24.00% OPM(%) 0.84% 16.57% 15.95% 18.63% NPM (%) 0.00% 9.90% 7.53% 10.03% Debt-Equity 1.55 1.81 0.96 0.63

Performance comparison PCBL Vs BSE MidlCap

Analyst: Pinaki Banerjee

Tel No.: +91 33 4007 7416; Mobile: +919674040602

Email: [email protected]

Company profile:- Philips Carbon Black (PCBL), a member of RP Goenka

Group was incorporated on March 30, 1960 and is a leading

manufacturer of various grades of carbon black in India. Columbian

Chemical Corporation, US, a leading international producer of rubber

blacks is the Technical Collaborator of the company.

Investment Rationale

Largest Carbon Black company in India and eighth in the world.

� The company is the largest carbon black producer in the country

with a production capacity of 360,000 MT at present which is

expected to go upto 410,000 by end of FY11. Along with that, it

has also got co-generation power plants which, after meeting

their own requirements are sold to the grid.

� Apollo, MRF, CEAT, Bridgestone, JK etc are some of the

renowned clients of the company who have now embarked on a

massive expansion plan.

Connected to the automobile growth story

The Indian automobile industry has been on a strong growth path since

last year, and is expected to continue its growth momentum in future.

The growth in the automobile industry shall drive up the demand for

tyres also which in turn will drive the growth of the company.

Revenues from power also to add significantly to the topline.

The company is also increasing its power generation capacity from

60.5MW at present to 76 MW by Sep 2012. The revenues from power

which stood at 4% of the topline in FY10 is expected to go upto 7%-8% in

the next two years time. Since the company sources its own power from

the plants, the power cost is significantly low, thereby easing the operating

margins to a significant extent.

Foray into Vietnam to be another feather in the cap

The company has embarked upon ambitious expansion plans in India

and abroad. It is setting up two plants in Vietnam with a capacity of

about 100,000 MT in 80:20 joint venture with some local companies. The

first phase of about 60,000 MT is expected to become operational by

Sep 2012.

Phillips Carbon Black Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 2 of 14

Global Industry Overview:-

Carbon Black is well recognized to be the best reinforcing material in rubber compounds. The tyre industry

consumes about 80% of the total carbon black production around the world. As per estimates about nine million

metric tons of Carbon Black are manufactured annually worldwide.

Key Points:-

Global demand expected to rise by about 4.30% through 2013

Source:- SKP Research

Special Blacks expected to be a key item in the future

The market for special blacks is expected to grow by 5.90% every year to 1.20 million metric tons which at

present they constitute about 10% of the overall global carbon black market on a tonnage basis. This segment,

apart from offering higher margins provides the suppliers with a shield against the cyclic nature of the tyre and

motor vehicles industries. Apart from the regular users like plastics, inks and paint industry, other users as

conductive fillers are expected to hold out good growth prospects till 2013 and thereafter.

Asia/Pacific region to be the key players

]

Source:- SKP Research

• A healthy global rubber market is

expected to help raise the demand for

world carbon black by 4.30% every year

to 2013 to about 11.60 million metric

tons .

• Majority of carbon black find use as a

reinforcement material in vulcanized

rubber goods, including over 60% in

motor vehicles tyres alone.

• It is estimated that the demand for

carbon black from the tyre industry is

expected to increase from 3.70% every

year to 6.90 million metric tons through

2013. The non tyre carbon black market

is estimated to increase by 4.80% every

year to 3.60 million metric tons to 2013.

Phillips Carbon Black Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 3 of 14

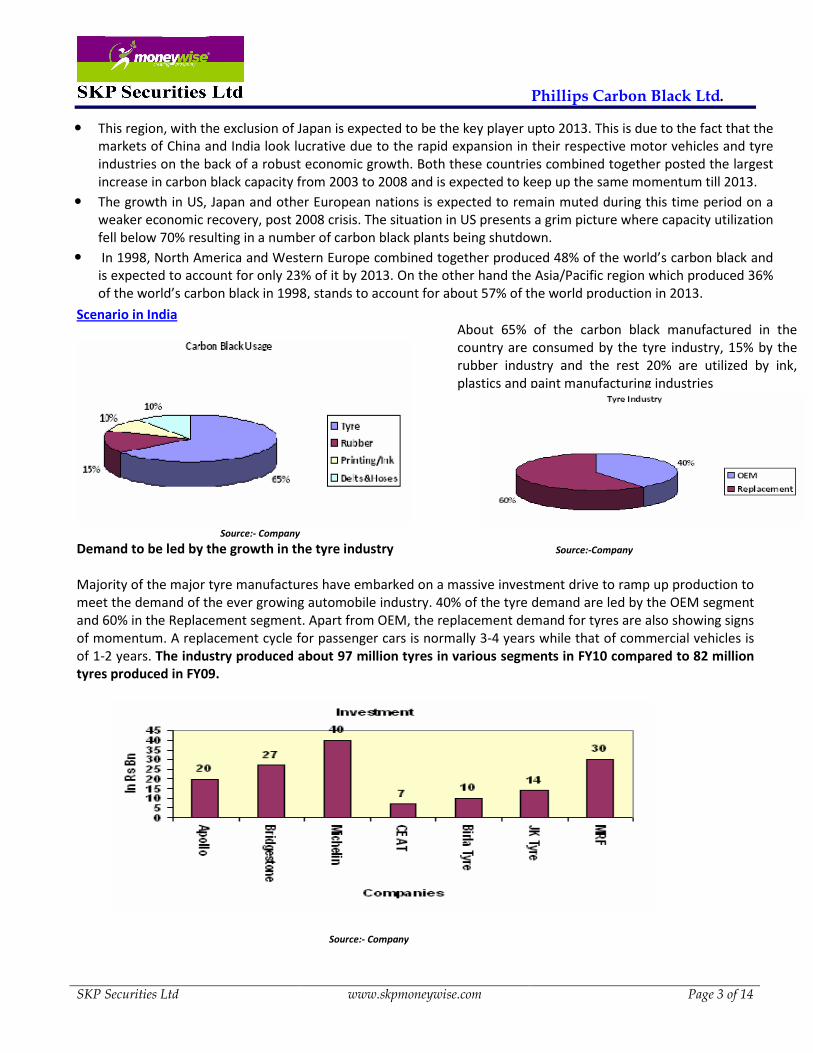

Scenario in India

Source:- Company

Demand to be led by the growth in the tyre industry Source:-Company

Majority of the major tyre manufactures have embarked on a massive investment drive to ramp up production to

meet the demand of the ever growing automobile industry. 40% of the tyre demand are led by the OEM segment

and 60% in the Replacement segment. Apart from OEM, the replacement demand for tyres are also showing signs

of momentum. A replacement cycle for passenger cars is normally 3-4 years while that of commercial vehicles is

of 1-2 years. The industry produced about 97 million tyres in various segments in FY10 compared to 82 million

tyres produced in FY09.

Source:- Company

About 65% of the carbon black manufactured in the

country are consumed by the tyre industry, 15% by the

rubber industry and the rest 20% are utilized by ink,

plastics and paint manufacturing industries

• This region, with the exclusion of Japan is expected to be the key player upto 2013. This is due to the fact that the

markets of China and India look lucrative due to the rapid expansion in their respective motor vehicles and tyre

industries on the back of a robust economic growth. Both these countries combined together posted the largest

increase in carbon black capacity from 2003 to 2008 and is expected to keep up the same momentum till 2013.

• The growth in US, Japan and other European nations is expected to remain muted during this time period on a

weaker economic recovery, post 2008 crisis. The situation in US presents a grim picture where capacity utilization

fell below 70% resulting in a number of carbon black plants being shutdown.

• In 1998, North America and Western Europe combined together produced 48% of the world’s carbon black and

is expected to account for only 23% of it by 2013. On the other hand the Asia/Pacific region which produced 36%

of the world’s carbon black in 1998, stands to account for about 57% of the world production in 2013.

Phillips Carbon Black Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 4 of 14

India emerging to be a major hub for automobile manufacturers

Major international car makers as Hyundai, Toyota, Nissan have set up shops in the country to ride the ever

increasing auto demand in the country in the passenger cars segment. Apart from this, a rise in industrial activity,

strong rural demand and availability of credit at attractive rates will drive up the demand for commercial vehicles

also.

Other segments also hold out a good promise

As mentioned before, apart from the tyre industry, ink, plastics and the paint manufacturing industry also hold

out a good promise for growth in the future.

• Ink- The Indian Printing Ink Industry is currently valued at about Rs 1800 crore- Rs 2000 crore with an

average growth rate of about 12%-15% annually. In terms of tonnage of ink manufactured in India, it is

estimated to be about 110 million tons annually.

• Plastics- The historical growth of the Indian plastic industry has been quite impressive at about 12%-14%

annually. The consumption level which at present is about 8 million tons is expected to reach a projected

level of 12 million tons by 2012.

• Paints- The phenomenal growth of the housing sector in India, rapid urbanization along with the

availability of easy to secure housing loans have been the prime drivers of the decorative paints industry

which comprises about 70% of $2 billion paint industry in India. Industrial paints add up to 30% of the

revenues of the industry. The size of the Indian Paint Industry is about 940 million liters. The organized

sector comprises about 54% of the total volume and 65% of the value. In the last 10 years, the industry

has shown a CAGR growth of about 10%-12% annually.

• Rubber- The production of rubber in the country varies between 7-8 Lakh tons annually amounting to

about Rs 4000 crore. It is estimated that about 6000 rubber manufacturing units are present comprising

of large, medium and small scale industry. The industry contributes about Rs 50 billion to the National

Exchequer in the form of various taxes. The per capital consumption of rubber in the country is only

about 800 grams compared to 12 to 14 kilos in Japan, USA and Europe. Thus, the country is still far from

attaining saturation levels and hence provides the industry with tremendous growth prospects in the

times of come.

Company Overview:-

Source:- Company

Source:- Company

Philips Carbon Black (PCBL), a member of RP Goenka

Group was incorporated on March 30, 1960 and is a

leading manufacturer of various grades of carbon black in

India. Columbian Chemical Corporation, US, a leading

international producer of rubber blacks is the Technical

Collaborator of the company.

Phillips Carbon Black Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 5 of 14

Year Milestones

1960 Incorporated in Kolkata

1962 Production begins with its collaborator Phillips Petroleum Company, USA

1978 Collaboration with Phillips Petroleum Company, USA ends

1988 Signs Technical agreement with Columbian Chemicals Company, USA

2003 Sets up a 12MW co-generation power plant in Baroda

2005 Sets up a 12MW CPP in Palej

2007 Signs MOU for setting up a plant in Vietnam

2008 Sets up a 30 MW CPP in Durgapur

2009 90000 MT facility in Mundra commences production taking total capacity to 360000 MT

2009 Sets up a 16MW CPP in Mundra

2010 Has plans to add another 50000MT in Mundra Source:-Company

Largest producer of carbon black in India and ninth in the world

Rank Name Origin Country Capacity(MT)

1 Cabot USA 2010000

2 Evonik Germany 1450000

3 Columbian USA 1130000

4 Birla India 790000

5 CSRC Taiwan 740000

6 Sid Rich USA 450000

7 Tokai Japan 370000

8 PCBL India 360000

9 Omsk Russia 350000

10 Black Cat China 290000 Source:- SKP Research

Source:- Company

Phillips Carbon Black Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 6 of 14

Clientele:- Renowned clients of the company include some of the world’s renowned as well as the leading

domestic tyre manufacturers of the country. These are Apollo, MRF, CEAT, Bridgestone, JK etc.

Last 5 Years Revenues

825

1123 1165 12001344

0

500

1000

1500

FY06 FY07 FY08 FY09 FY10

Financial Years

In R

s C

r

Projects Under Implementation Source:- Company

Growth In power revenues

Revenue:- At present about 96% of the total revenues

accrue from sale of carbon black while the rest is come

sale of surplus power to the grid. Of the total revenues

85% comes through domestic sales while 15% is through

exports.

The company took full advantage of the Electricity

Act of 2003 and began to generate power through

the waste gases produced from the production of

carbon black. After meeting its internal

requirements, the surplus power is sold to the

grid. Power revenues of the company have grown

at a CAGR of 85% through FY06-10 since the

commissioning of its power plants

Growth in Power Revenues

46106

149 155

545

0

100

200

300

400

500

600

FY06 FY07 FY08 FY09 FY10

Financial Years

In M

n

Phillips Carbon Black Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 7 of 14

Source:- Company

Vietnam Joint Venture:- The company has began work on its Vietnam project in a JV with 3 local companies

where it would be having 80% share. The project is to be funded through a debt equity ratio of 2:1. The total cost

of the project is estimated to be about Rs 450 Cr.

Source:- Company

Investment Rationale

Growth in the tyre segment to be the main growth driver

Source:- SKP Research

Strategic locations of all its plants

Particulars Phase-I Phase-II

Carbon Black(MT) 60000 55000

CPP(MW) 12 6

Investment($Mn) 63 21

Commissioning 2012 2013

Revenue at 90% capacity utilization($Mn) 60 53

• The auto industry in India is one of the largest

in the world. It produces about 11 million 2

and 4 wheeled vehicles and exports about 1.50

million vehicles every year.

• By 2050 the country is expected to top the

world in car volumes with approximately 611

million vehicles on the roads. This in turn is

expected to drive the tyre industry forward

thus paving the way for the company to grow

at a CAGR growth of about 10%-12% anually.

• Since the company holds a dominant position

in the carbon black market, it is expected to

gain significantly with the growth in the

automobile segment and subsequently an

increase in the demand for tyres.

• The company’s 4 plants are strategically

located to cater to the tyre demands of the

respective regions, thereby reducing the

cost of freight.

• It is also on the look out to buy further land

to set up a new carbon black facility in

southern India to cater to the upcoming auto

hub. The company is in talks with the

governments of Tamil Nadu and Andhra

Pradesh for this and the deal is expected to

be finalized soon.

Plant Tyre Companies

Kochi Apollo,JK,Michelin,MRF

Palej Bridgestone

Mundra Ceat

Automobile Production

12641473

17131846

2166

363547 540 486 466

0

500

1000

1500

2000

2500

2005 2006 2007 2008 2009

Years

In '

00

0

Passenger Cars

Commercial Vehicles

Phillips Carbon Black Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 8 of 14

Vietnam venture to enhance the fortunes of the company

Exports to be stronger in the times to come Source:- SKP Research

Currently the exports constitute about 16%-17% of the top line growth. Now with the various capacity expansions

in place and the foray into Vietnam the exports are likely to go up to 20%-22% of the total sales of the company.

Power segment to increase revenues and improve margins

At present about 5% of the revenues accrue from the sale of power. With the increase in the power generation

capacity from 60.5 MW to 76 MW by Sep 2011, the share of revenues from power sale is expected to increase to

6%-7% over the next 2 years. At present about 15%-20% of the power produced are used for their own captive

consumption and about 35%-40% of it is sold to the grid. The cost incurred to generate power is about 70p/unit

while it can be sold to the grid at about Rs2-3/unit. In the absence of raw material cost the power business has

got EBIDTA margins of about 90%.

Power Projects lead to carbon credits

The Palej power plant of the company has been registered with UNCDM(Clean Development Mechanism) board

and have subsequently sold the same and added to the topline. The company plans to register other power plants

too with UNCDM, but the process is a lengthy one and can take at least a couple of years. However, the Palej

power plant is expected to generate carbon credits till FY15.

Backward integration in the form of Coal Tar Distillation

Carbon Black Feed stock is the main raw materials used by the company at present which has to be imported. The

price of these is directly linked to the international crude oil prices. An increase in those can put some severe

pressure on the operating margins of the company. To mitigate the risk the company plans to start using coal tar

in future as its raw material. Coal Tar is a by product generated through the processing of coal into coke for use in

steel manufacturing. The process of putting the plans into action has started and this can take effect in another 2-

3 years. The company plans to go into long term contracts with domestic steel manufacturers in this regard.

The country is known to be the fourth largest producer of

rubber but unfortunately does not have a single carbon

black facility. All the demands are met through imports. It

is estimated that the current demand for carbon black ,

which at present stands around 60,000 MT is expected to

reach at least 100,000 MT in two years time. Apart from

the expansion of local tyre companies many foreign

players are also looking to set up shop there. The company

presently has a 40% market share in Vietnam.

Phillips Carbon Black Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 9 of 14

Financial Performance

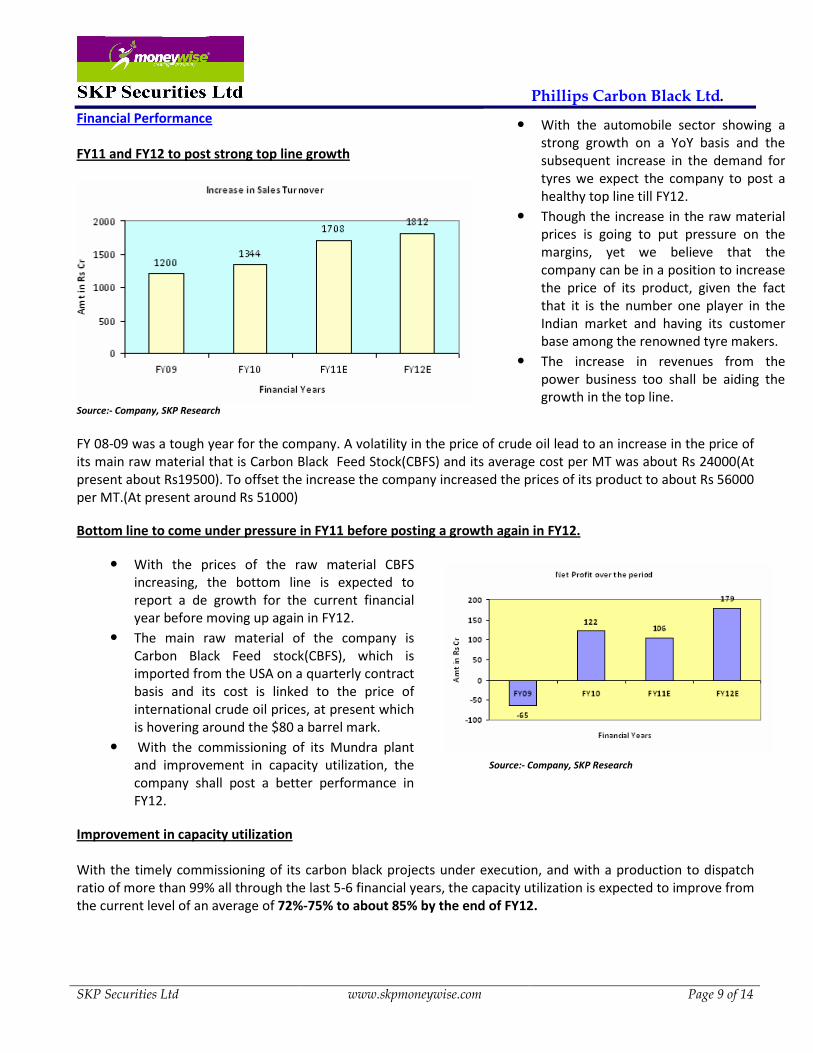

FY11 and FY12 to post strong top line growth

Source:- Company, SKP Research

FY 08-09 was a tough year for the company. A volatility in the price of crude oil lead to an increase in the price of

its main raw material that is Carbon Black Feed Stock(CBFS) and its average cost per MT was about Rs 24000(At

present about Rs19500). To offset the increase the company increased the prices of its product to about Rs 56000

per MT.(At present around Rs 51000)

Bottom line to come under pressure in FY11 before posting a growth again in FY12.

Source:- Company, SKP Research

Improvement in capacity utilization

With the timely commissioning of its carbon black projects under execution, and with a production to dispatch

ratio of more than 99% all through the last 5-6 financial years, the capacity utilization is expected to improve from

the current level of an average of 72%-75% to about 85% by the end of FY12.

• With the automobile sector showing a

strong growth on a YoY basis and the

subsequent increase in the demand for

tyres we expect the company to post a

healthy top line till FY12.

• Though the increase in the raw material

prices is going to put pressure on the

margins, yet we believe that the

company can be in a position to increase

the price of its product, given the fact

that it is the number one player in the

Indian market and having its customer

base among the renowned tyre makers.

• The increase in revenues from the

power business too shall be aiding the

growth in the top line.

• With the prices of the raw material CBFS

increasing, the bottom line is expected to

report a de growth for the current financial

year before moving up again in FY12.

• The main raw material of the company is

Carbon Black Feed stock(CBFS), which is

imported from the USA on a quarterly contract

basis and its cost is linked to the price of

international crude oil prices, at present which

is hovering around the $80 a barrel mark.

• With the commissioning of its Mundra plant

and improvement in capacity utilization, the

company shall post a better performance in

FY12.

Phillips Carbon Black Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 10 of 14

Increase in capacity utlization

270000

360000

410000 410000

212150

258000295200

348500

0

50000

100000

150000

200000

250000

300000

350000

400000

450000

FY09 FY10 FY11E FY12E

Financial Years

Am

t in

MT

Capacity

Production

Source:- Company, SKP Research

Increase in realization price

Source:- Company, SKP Research

Operating margins expected to increase

Source:- Company, SKP Research

Sales Quantity and Realization Price

215

256

326345

56

51

50.550.5

0

50

100

150

200

250

300

350

400

FY09 FY10 FY11E FY12E

Financial Years

Sa

les

In M

T i

n '

00

0'

47

48

49

50

51

52

53

54

55

56

57

Re

ali

zati

on

Pri

ce M

T i

n

'00

0'

Sales

RealizationThe company is expected to increase its

realization price gradually over the next few

years with increase in sales quantity. With the

price of the raw material and other

manufacturing expenses expected to increase

over a period of time, the company will be

bound to increase the realization price to

offset the increase in manufacturing costs.

With the increase in the realization

price along with an increase in the

sales volume, the operating margins

are expected to show an increase from

the current levels of about 16% in

FY11 to about 18% in FY12. An

increase in contribution from power

sales too shall aid the growth as it has

got higher margins.

Operating Profit

0

50

100

150

200

250

300

350

Am

t In

Rs

Cr

0

5

10

15

20

In %

Operating Profit

OPM(%)

Phillips Carbon Black Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 11 of 14

ROCE and RONW to show a decrease in FY11

Source:- Company, SKP Research

Risks and Concerns

Highly dependent on the performance of the tyre industry

The company derives its maximum revenues from the tyre industry which in turn is dependent on the fortunes of

the auto sector. Any adverse happening in the auto industry is going to have a negative effect on the company. It

had faced a similar situation in FY09 due to the effect of the global financial crisis.

Volatility in the prices of its raw materials

Carbon Black Feed Stock(CBFS), the main raw material of the company is imported from the USA and is

dependent on the prices of international oil prices. An increase in that is going to put pressure on the margins of

the company. To mitigate this risk, the company has initiated the process of replacing CBFS with coal tar pitch

which is a byproduct from the steel manufacturing process. It has already started discussions with some major

steel manufacturers in this regard. However, it shall take another 2 years time to actually put that into practice.

Delay in project execution will increase cost and hamper earnings

The company is at present executing a 50000MT carbon black facility in Mundra along with a 10MW power

project and a 8MW power facility in Kochi. A delay in executing these projects could affect company’s earnings.

The Vietnam project also has not yet achieved financial closure. Any delay in that is also going to be prove

detrimental to the company.

Threat of cheap imports

Though an anti dumping duty is in place, yet a threat of cheap imports always remain high which may prove

detrimental to the interest of the company.

Due to the ongoing capacity expansion

plans the RONW and ROCE shall decline in

FY11, after which they are expected to

stabilize in FY12.

Phillips Carbon Black Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 12 of 14

Valuations and Outlook

We have valued the company by applying the Discounted Cash Flow method by taking a WACC of 12.45% from

FY11E to FY15E and a terminal growth rate of 2% thereafter and have arrived at a fair value price of Rs 254

implying a upside of 40% from current levels to be achieved in 15 months time. However, we have not factored

in the Vietnam Project as of now, since it is in a preliminary stage and yet to achieve financial closure.

PV of Projected Cash Flows 307

PV of Terminal Value 537

Fair Value 844

No of Shares Outstanding 3.32

Fair Value Per Share 254

• We firmly believe that the company is going to reap the benefits of the automobile growth story as

depicted in the YoY sales increases of all the auto majors which includes two wheelers, four wheelers and

commercial vehicles.

• Being the No1 choice of all the major tyre manufacturers of the country as well as some renowned ones

outside, it is going to put up a good performance in the times to come. This shall further be aided by the

timely and successful commissioning of the projects under implementation.

• The Vietnam project is expected to be completed fully by the end of FY14 and this shall be the focal point

of supplying its products to the South East Asian region thereby decreasing the shipping and

transportation costs of the company which till now is being sent from India.

• The company is expected to sell all its surplus power after meeting all its own requirements which till now

is just about 20%-25% of the total power generated.

• Volatility of raw materials mainly the CBFS remains a key concern of dragging the margins down.

However, the company has already started to look at using coal tar pitch instead and is in talks with some

major steel producers. Though things are still on paper, yet it is expected to start taking effect slowly

after 2 years time. This shall reduce the company’s dependency on CBFS gradually.

• FY13 to FY15 shall be the consolidation phase for the company. On the domestic side, it is expected to

achieve 100% capacity utilization and the Vietnam project is also expected to become operational by

then.

• New capacity expansions in the form of a new carbon black facility in South India along with

diversification into carbon chemicals manufacturing are in the pipeline.

Phillips Carbon Black Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 13 of 14

Income Statement

Particulars FY09 FY10 FY11E FY12E

Net sales 1076 1233 1407 1783

Growth (%) 4% 15% 14% 27%

Other Income 14 24 28 45

Stock Adjustments 10 15 17 255

Total Income 1100 1272 1452 1849

Raw Material Consumed 940 884 1016 1231

Power and Fuel Cost 6 14 15 18

Employee Cost 33 35 40 50

Other Mfg Expenses 38 49 56 78

Selling and Admn Expenses 43 50 58 79

Misc Expenses 32 36 42 62

Total Expenditure 1091 1068 1228 1517

Operating Profit 9 204 224 332

OPM(%) 0.84% 16.57% 15.95% 18.63%

Interest 87 43 45 50

Depreciation 20 31 38 44

PBT -97 131 142 238

Tax 33 8 35 60

PAT -65 123 106 179

Growth in PAT -173% 289% -14% 69%

EPS 0.00 43 32 52

NPM(%) 0.00 9.90% 7.53% 10.03%

Dividend Per Sh. (Rs.) 0.00 5.00 5.00 5.00

Balance Sheet

Particulars FY09 FY10 FY11E FY12E

Equity Capital 28 28 33 35

Reserves 190 296 485 719

Share Warrants 0.00 0.00 0.12 0.00

Net worth 218 324 519 754

Secured Loan 413 496 447 405

Unsecured Loan 13 60 50 45

Total Liabilities 644 880 1016 1204

Net Fixed Assets 228 593 661 717

Capital WIP 383 92 112 135

Investments 38 38 46 40

Inventories 121 197 225 357

Accounts receivable 181 295 338 446

Cash & Bank 7 33 32 28

Loan & Advances 84 149 86 40

Current Assets 393 674 681 871

Current Liab. 395 448 457 517

Provisions 2 20 17 21

Total Curr. liab. & prov. 397 508 474 538

Net Current Assets -4 166 207 332

Net Deferred Tax -2 -10 -10 -20

Total Assets 644 880 1016 1204

Cash Flow Statement

Particulars FY09 FY10 FY11E FY12E

Profit before Tax -97 131 142 238

Add: Depreciation, Int. & Other

Expenses 41 57 75 84

Net changes in WC, tax interest 169 -139 -63 -120

Cash flow from operating activities 113 49 153 202

Cash flow from investing activities -232 -97 -133 -117

Cash flow from financing activities 111 74 -21 -89

Net Increase/Decrease in Cash &

Cash Equivalents -8 26 -1 -4

Opening Cash Balance 15 7 33 32

Closing Cash Balance 7 33 32 28

Key Ratios

Particulars FY09 FY10 FY11E FY12E

Valuation Ratios

P/E 0.00 4.51 5.62 3.46

P/BV 0.42 1.69 1.11 0.86

EV/EBIDTA 56.76 5.25 4.78 3.22

Mkp/Sales 0.08 0.41 0.42 0.33

Earnings Ratios

OPM 0.84% 16.57% 15.95% 18.63%

NPM 0.00% 9.95% 7.55% 10.02%

ROCE -1.81% 22.73% 18.00% 28.00%

RONW -28.13% 45.22% 20.00% 24.00%

Balance Sheet Ratios

Current Ratio 0.97 0.93 1.43 1.62

Debt/Equity 1.55 1.81 0.96 0.63

Debtor days 67 69 81 79

Inventory Days 49 58 62 69

Consolidated Financials in Rs. Crores

Phillips Carbon Black Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 14 of 14

Consolidated Financials (in Rs. Crores)

Member: NSE BSE NSDL CDSL NCDEX* MCX* MCX-SX FPSB *Group Entities

INB/INF: 230707532, BSE INB: 010707538, CDSL IN-DP-CDSL-132-2000, DPID: 021800, NSDL IN-DP-NSDL: 222-2001, DP ID: IN302646, ARN: 0006, NCDEX: 00715, MCX: 31705, MCX-SX: INE 260707532

The above analysis and data are based on last available prices and not official closing rates.

SKP Research is also available on Bloomberg, Thomson First Call & Investext Myiris, Moneycontrol, Tickerplant and ISI Securities

.

DISCLAIMER: This document has been issued by SKP Securities Ltd (SKP), a stock broker registered with and regulated by Securities & Exchange Board of India,

for the information of its clients/potential clients and business associates/affiliates only and is for private circulation only, disseminated and available electronically

and in printed form. Additional information on recommended securities may be made available on request. This document is supplied to you solely for your

information and no matter contained herein may be reproduced, reprinted, sold, copied in whole or in part, redistributed or passed on, directly or indirectly, to any

other person for any purpose, in India or into any other country without prior written consent of SKP. The distribution of this document in other jurisdictions may be

strictly restricted and/ or prohibited by law, and persons into whose possession this document comes should inform themselves about such restriction and/ or

prohibition, and observe any such restrictions and/ or prohibition. If you are dissatisfied with the contents of this complimentary document or with the terms of this

Disclaimer, your sole and exclusive remedy is to stop using the document and SKP shall not be responsible and/ or liable in any manner. Neither this document nor

the information or any opinion expressed therein should be construed as an investment advice or offer to anybody to acquire, subscribe, purchase, sell, dispose of,

retain any securities or derivatives related to such securities or an offer to sell or the solicitation of an offer to purchase or subscribe for any investment or as an

official endorsement of any investment. Any recommendation or view or opinion expressed on investments in this document is not intended to constitute investment

advice and should not be intended or treated as a substitute for necessary review or validation or any professional advice. The views expressed in this document are

those of the analyst which are subject to change and do not represent to be an authority on the subject. SKP may or may not subscribe to any and/ or all the views

expressed herein. It is the endeavor of SKP to ensure that the analyst(s) use current, reliable, comprehensive information and obtain such information from sources,

which the analyst(s) believes to be reliable. However, such information may not have been independently verified by SKP or the analyst(s). The information, opinions

and views contained within this document are based upon publicly available information, considered reliable at the time of publication, which are subject to change

from time to time without any prior notice. The Document may be updated anytime without any prior notice to anybody. SKP makes no guarantee, representation or

warranty, express or implied; and accepts no responsibility or liability as to the accuracy or completeness or correctness of the information in this Report. SKP, its

Directors, affiliates and employees do not accept any liability whatsoever, direct or indirect, that may arise from the use of the information or recommendations

herein. Please note that past performance is not necessarily a guide to evaluate future performance. SKP or its affiliates, may, from time to time render advisory and

other services to companies being referred to in this document and receive compensation for the same. SKP and/or its affiliates, directors and employees may trade for

their own account or may also perform or seek to perform investment banking or underwriting services for or relating to those companies and may also be represented

in the supervisory board or on any other committee of those companies or may sell or buy any securities or make any investment, which may be contrary to or

inconsistent with this document. This document should be read and relied upon at the sole discretion and risk of the reader. The value of any investment made at your

discretion based on this document or income there from may be affected by changes in economic, financial and/ or political factors and may go down as well as up

and you may not get back the full or the expected amount invested. Some securities and/ or investments involve substantial risk and are not suitable for all investors.

Neither SKP nor its affiliates or their directors, employees, agents or representatives/associates, shall be responsible or liable in any manner, directly or indirectly, for

information, views or opinions expressed in this document or the contents or any errors or discrepancies herein or for any decisions or actions taken in reliance on the

document or inability to use or access our service or this document or for any loss or damages whether direct or indirect, incidental, special or consequential including

without limitation loss of revenue or profits or any loss or damage that may arise from or in connection with the use of or reliance on this document or inability to use

or access our service or this document.

SKP Securities Ltd Contacts Research Sales

Mumbai Kolkata Mumbai Kolkata

Phone 022 2281 9012 033 4007 7000 022 2281 1015 033 4007 7400

Fax 022 2283 0932 033 4007 7007 022 2283 0932 033 4007 7007

E-mail [email protected] [email protected] [email protected]