Embed Size (px)

Citation preview

CITY OF ROCHESTER Economic Development Authority Agenda

Council/Board Chambers 151 4th Street SE

Special Meeting July 22, 2019

07:30 PM

A. CALL TO ORDER

B. CONSENT AGENDA/ORGANIZATIONAL BUSINESS

B.1. Economic Development Authority - Special Meeting - Apr 15, 2019 7:30 PM

C. HEARINGS

C.1. Request to Establish Development District # 72 and Tax Increment Financing District # 72-1 by Rochester Hotel Partners LLC

D. REPORTS AND RECOMMENDATIONS

E. RESOLUTIONS AND ORDINANCES

F. TABLED ITEMS

G. OTHER BUSINESS

H. ADJOURN

Special Meeting - April 15, 2019

Draft

CITY OF ROCHESTER, MINNESOTA

Economic Development Authority MINUTES

A. CALL TO ORDER

Attendee Name Title Status Arrived

Randy Staver President Present

Patrick Keane Commissioner Present

Michael Wojcik Commissioner Present

Nick Campion Commissioner Present

Mark Bilderback Commissioner Present

Shaun C. Palmer Commissioner Present

Annalissa Johnson Commissioner Present

Kim Norton Mayor Present

B. CONSENT AGENDA/ORGANIZATIONAL BUSINESS

B.1. Approve EDA Meeting Minutes from March 18, 2019

RESULT: APPROVED [UNANIMOUS] MOVER: Nick Campion, Commissioner SECONDER: Mark Bilderback, Commissioner AYES: Staver, Keane, Wojcik, Campion, Bilderback, Palmer, Johnson

C. HEARINGS

C.1. Request to Establish Development District # 70 and Tax Increment Financing District # 70-1 by Harvestview Place II and Approval of Development Assistance Agreement between City of Rochester and Harvestview Place II President Staver opened the public hearing. Ryan Schwickert came forward representing Joseph Development. There being no one further to speak, the public hearing was closed. Adopted Resolution No. EDA19-006 establishing Development District #70 and Tax Increment Financing District #70-0.

RESULT: ADOPTED [UNANIMOUS] MOVER: Nick Campion, Commissioner SECONDER: Mark Bilderback, Commissioner AYES: Staver, Keane, Wojcik, Campion, Bilderback, Palmer, Johnson

C.2. Request to Establish Development District # 73 and Tax Increment Financing District # 73-1 by Village Capital Corporation and Approval of Development Assistance Agreement between City of Rochester and Village Capital Corporation President Staver opened the public hearing. Abby Frans came forward representing the developer Village Capital.

B.1

Packet Pg. 2

Special Meeting - April 15, 2019

There being no one further to speak, the public hearing was closed. Adopted Resolution No. EDA19-007 establishing Development District #73 and Tax Increment Financing District #73-1.

RESULT: ADOPTED [UNANIMOUS] MOVER: Nick Campion, Commissioner SECONDER: Annalissa Johnson, Commissioner AYES: Staver, Keane, Wojcik, Campion, Bilderback, Palmer, Johnson

D. REPORTS AND RECOMMENDATIONS

E. RESOLUTIONS AND ORDINANCES

F. TABLED ITEMS

G. OTHER BUSINESS

H. ADJOURN

There being no further business before the EDA, the meeting was adjourned at 10:04 p.m.

_____________________ Anissa N. Hollingshead Secretary, Economic Development Authority

RESULT: APPROVED [UNANIMOUS] MOVER: Nick Campion, Commissioner SECONDER: Annalissa Johnson, Commissioner AYES: Staver, Keane, Wojcik, Campion, Bilderback, Palmer, Johnson

B.1

Packet Pg. 3

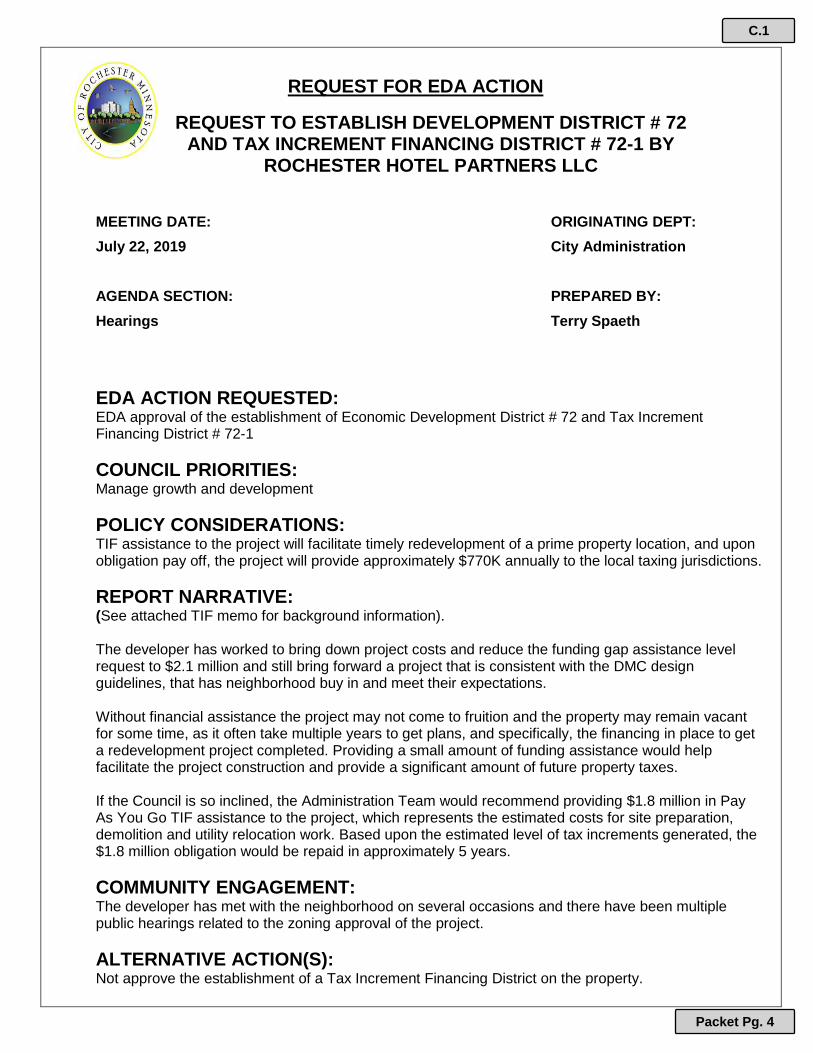

REQUEST FOR EDA ACTION

REQUEST TO ESTABLISH DEVELOPMENT DISTRICT # 72 AND TAX INCREMENT FINANCING DISTRICT # 72-1 BY

ROCHESTER HOTEL PARTNERS LLC

MEETING DATE: ORIGINATING DEPT:

July 22, 2019 City Administration

AGENDA SECTION: PREPARED BY:

Hearings Terry Spaeth

EDA ACTION REQUESTED: EDA approval of the establishment of Economic Development District # 72 and Tax Increment Financing District # 72-1

COUNCIL PRIORITIES: Manage growth and development

POLICY CONSIDERATIONS: TIF assistance to the project will facilitate timely redevelopment of a prime property location, and upon obligation pay off, the project will provide approximately $770K annually to the local taxing jurisdictions.

REPORT NARRATIVE: (See attached TIF memo for background information). The developer has worked to bring down project costs and reduce the funding gap assistance level request to $2.1 million and still bring forward a project that is consistent with the DMC design guidelines, that has neighborhood buy in and meet their expectations. Without financial assistance the project may not come to fruition and the property may remain vacant for some time, as it often take multiple years to get plans, and specifically, the financing in place to get a redevelopment project completed. Providing a small amount of funding assistance would help facilitate the project construction and provide a significant amount of future property taxes. If the Council is so inclined, the Administration Team would recommend providing $1.8 million in Pay As You Go TIF assistance to the project, which represents the estimated costs for site preparation, demolition and utility relocation work. Based upon the estimated level of tax increments generated, the $1.8 million obligation would be repaid in approximately 5 years.

COMMUNITY ENGAGEMENT: The developer has met with the neighborhood on several occasions and there have been multiple public hearings related to the zoning approval of the project.

ALTERNATIVE ACTION(S): Not approve the establishment of a Tax Increment Financing District on the property.

C.1

Packet Pg. 4

PRIOR EDA ACTION: None

FISCAL AND RESOURCE IMPACT: If a Tax Increment Financing District is established, it is with the understanding that a subsequent TIF Development Assistance Agreement providing $ 1.8 million in TIF assistance is forthcoming. It is estimated this obligation would be paid off in approximately 5 years, and thence forward, would provide approximately $770K annually in property tax revenues to the local taxing jurisdictions.

ATTACHMENTS:

Location Map

Rochester Hotel Partners -- City TIF application -- Letter_7_16_2019

EKN TIF memo

DOCSOPEN-#563693-v7-Rochester_TIF_72-1_Eleven_02_Hotel_TIF_PLAN_(Redevelopment)

DOCSOPEN-#563696-v2-Rochester_TIF_72-1_Eleven_02_Hotel_EDA_APPROVING_RESOLUTION

DOCSOPEN-#563697-v2-Rochester_TIF_72-1_Eleven_02_Hotel_CITY_APPROVING_RESOLUTION

C.1

Packet Pg. 5

/

Proposed TIF District # 72-1 Location Map

ext

2nd St. SW

11th

Aven

ue S

W

C.1.a

Packet Pg. 6

pg. i

January 22, 2019

City of Rochester 201 4th Street SE Rochester, MN 55904 ATTN: Administration – Terry Spaeth Dear Mr. Spaeth, EKN Development Group, Western States Lodging and Napean Capital, collectively operating as Rochester Hotel Partners, LLC, (“RHP”), are pleased to have submitted an application for TIF financing to the City of Rochester in support of RHP’s proposed 250 room, dual-branded, Staybridge Suites and EVEN Hotel (Hotel) at the former site of Virgil’s Auto Clinic & Towing at 1102 Second Street, SW in Rochester (northwest corner of 2nd Street SW and 11th Avenue NW) – “1102 Project”. By this time, you have received our application fee of $5,000 and a blight study for the project site prepared by TSP Architects. We are looking forward to the Staff’s formal recommendations to the City Council regarding our application and on Monday the 22nd of July, the City Council’s associated deliberation and vote. The financially viability of the 1102 Project is contingent on the outcome of RHP’s TIF request, which is approximately $2.1 million. (I include with this letter our most up-to-date spreadsheet financial and Gap analysis for the project along with the most current bid from Weis our contractor covering the project’s hard construction costs. The former accounts for the current 250 room plan, the debt financing we currently have available to us and the anticipated development costs including the hard costs shown in the Weis budget). The 1102 Project will be transformative to the St. Mary’s corridor and represent an important building block for realizing the City’s ambitious development vision for Rochester’s downtown. As you know, some highlights of the proposed Hotel include:

• An extraordinary level of coordination between the development team and community and public stakeholders.

• Expected transient occupancy tax, net sales tax and net property tax generation from the Hotel once operational (net of estimated Virgil sales taxes absent the business’ closure and property tax rebates associated with the requested TIF award) of almost $129 million over thirty-five years.

• Over 260 jobs made available by the project during the Hotel’s construction. • Nearly 70 post construction jobs to be created to operate the Hotel. • A design that on its 1st Street, SW frontage has a distinctly residential feel that seamlessly

integrates with the adjacent residential neighborhood. (This design element was the direct result of a close collaboration between the development team and the area’s neighborhood association representatives).

• A design fronting 11th Avenue NW and 2nd Street SW that is timelessly modern and textured in style, which through glazing and other elements, along with envisioned landscaping, will connect the Hotel to the adjacent streetscape.

• Along the Hotel’s Second Street SW frontage wrapping around the corner on 11th Avenue NW, approximately 4,000 square feet of rentable retail space and deep setbacks that will allow for

C.1.b

Packet Pg. 7

pg. ii

outdoor seating and public congregation to activate the area – no such street-side experience currently exists along Second Street SW across from St. Mary’s Hospital.

• Parking facilities that are completely hidden within the Hotel structure helping to achieve the community’s objective of removing cars from the street and creating a pedestrian-centric experience.

• Provide an upscale, lifestyle and health/wellness-oriented hotel product, which is currently not available, within the St. Mary’s subdistrict or the broader Rochester lodging marketplace.

With the above noted, it is important to understand that while we have closed on the purchase of the site our investors are looking to the outcome of our City TIF application to decide how they want to, and if they will at all, proceed with the project. Given where we are late in the economic cycle, it has been challenging, to say the least, in keeping our investors committed to the project. If we receive the TIF award, I am certain we will be able to move forward and, in fact, will be able to quickly break ground. We have worked diligently to value engineer the design of the building to bring costs down (and benefited from cost reductions with the exclusion of prevailing wage) but all of the extras pushed by the City, DMCC and neighborhood association, which we agree enhance the building, such as those mentioned above and others have driven the project’s costs much higher than under our original designs first discussed with the City. Outside of current public sentiment and confusion around TIF, which we understand is difficult to gauge and maneuver, we have been offered a number of reasons why there has been a reluctance to award the project TIF that I would like to quickly cover here below (bolded and in italics) and that I may also discuss during my presentation to the City Council on the 22nd.

o EKN paid too much for the property. As a premiere commercial site in Rochester and one that had an operating and profitable business on it up until very recently, we feel the negotiated price was right in line with the comps (of which there were few), the market and the site’s income-based value. The original underwriting of the project based on our initial designs for the hotel that all conformed to City’s requirements indicated the pricing for the land to be reasonable. Also, on a dollars-per-hotel-room basis we bought the property for about $24,000 per room. This is actually on the very low end of the typical per-room site costs for EVEN and Staybridge hotels. So, land price is not why we are faced with a financial gap.

o To reduce or eliminate the financial gap, EKN should simply increase its projected occupancy and

rate or lower its operating expenses. This solution was actually proffered in Springsted’s report that the City commissioned to evaluate our TIF application (the same consultants that reviewed EKN Development Group’s TIF applications for its Indigo and Hyatt House projects in Rochester). Frankly, I was taken aback when I saw this recommendation. We very carefully underwrote the project taking full account of the operational economies of a dual-branded hotel of 250 keys and even Springsted determined those projections to be reasonable and in line with market. The projected occupancy and rate that the hotel will realize, which support our investment underwriting, reflect a premium to the market in which the hotel competes consistent with the positioning of the EVEN and Staybridge brands, that our hotel will be brand new and that it will provide a superior lodging experience to any other property in the St. Mary’s sub-district. We were aggressive as possible with our revenue projections but to arbitrarily suggest increasing those assumptions just to make the numbers work is, in truth,

C.1.b

Packet Pg. 8

pg. iii

misguided and would undermine our credibility with our investors resulting in serious backlash. The same is true for operating expenses. We very carefully worked up our projections of the hotel’s operating expenses assuming best practices in management and efficiencies. Currently our projected profit percentages are materially higher (and thus, our operating expense ratios materially lower) than those percentages shown in published statistics for select service and extended stay hotels such as we propose to build. To push those expense ratios lower would be a fiction and unrealizable.

o The City already gave EKN a much higher density of rooms than were originally permitted for the

site. The higher density on the site was necessary to even approach financial feasibility for the project. The whole objective is to design a project that meets brand standards and that will be financially successful. The project was dead out the gate absent the increase in density. The challenge in the present case is that all the design upgrades/changes we have had to incorporate as noted above drove the costs up too much even with scale economies and revenue increases that came with the higher density.

o There is other hotel investing going on in the City that is not requiring public assistance. I believe this was specifically in reference to updating planned at the Marriott and the Kahler as well as the construction of a new luxury hotel on top of the Gonda Building. To start, a property improvement program to an existing, going concern, stabilized hotel like the Marriott or Kahler is not only a standard cyclic activity that any hotel operator will perform to keep their hotel competitive but even if more substantial a renovation, it requires a much lower incremental investment return than a new-build hotel development like the 1102 Project. Simply put, the investment risks associated with a property improvement program are relatively low because the hotel is already established, there is no entitlement, financing, construction and any of the myriad of other risks associated with new development. Also, a branded property like the Marriott, due to brand requirements, obligatorily sets aside reserves every month to cover these improvement programs; I would assume that the Kahler (an independent) also systematically sets aside reserves for this purpose as is common practice in hotel operations. We will be doing the same as per IHG’s requirements for the EVEN and Staybridge franchising.

With respect to the luxury hotel on top of Gonda. First, investment return requirements for luxury hotels are generally lower than for other hotel segments because the investment is often driven in part by vanity and other non-financial considerations, especially with capital coming from Asia or the Middle East. Second, and very importantly, the investors in that project will benefit from the fact that they are in partnership with Mayo and building on top of an existing structure (no going into the ground). Mayo’s massive balance sheet and ability to get what it wants (little entitlement risk) are large risk mitigators, thereby reducing the project’s investment return requirements, all else being equal. Building on top of an existing building avoids much of the construction risk that comes with most new build development. For example, with our Hyatt House project we have already experienced some cost and timing overruns due to the discovery of old piping in the ground

C.1.b

Packet Pg. 9

pg. iv

at a range of depths and a deposit of quartz that was extremely difficult to bore into. What is in the ground is much more difficult to control than what is going to be built on it.

o The equity investment return that EKN is requiring is more than necessary (above market). We have applied an investment return hurdle of 16% in our gap analysis and after much effort were able to convince our investors in all our projects in Rochester to accept that return hurdle. Absent the ~$2 million of TIF that the City staff has indicated it would recommend for our St. Mary’s project, we do not reach that hurdle; a hurdle, which is extremely low for new development or substantial redevelopment. Publications from a range of sources such as PKF Consulting and Realtyrates.com generally show greenfield development equity return requirements for hotels are above 20%. Hotels are one of the riskiest real estate asset classes. 20% is typically the return hurdle that we need to offer investors in our projects. In addition, how is it that that return hurdle was accepted without comment for our two other TIF applications but has now become an issue? This question begs highlighting since current market risk concerns for new hotel development are substantially higher than they were when we submitted our TIF applications for the other two of EKN’s Rochester projects.

With all the above noted, I want to make sure that you understand it has been a real pleasure working with the City on all our developments, particularly you, Steve Rymer and the rest of the City Administration’s staff. You have made the development process substantially easier than our experience in most other markets and I commend you for that. I also appreciate your collective efforts and support as it relates to our TIF request. We are excited to be continued members of the Rochester community.

Please let me know if you have any questions or concerns regarding our application or require any additional information from us. Thank you for your consideration.

Best regards,

Jason Bass, CPA, CFA Director of Finance – EKN Development Group 602-430-2485

C.1.b

Packet Pg. 10

C.1.c

Packet Pg. 11

C.1.c

Packet Pg. 12

C.1.c

Packet Pg. 13

C.1.c

Packet Pg. 14

C.1.c

Packet Pg. 15

C.1.c

Packet Pg. 16

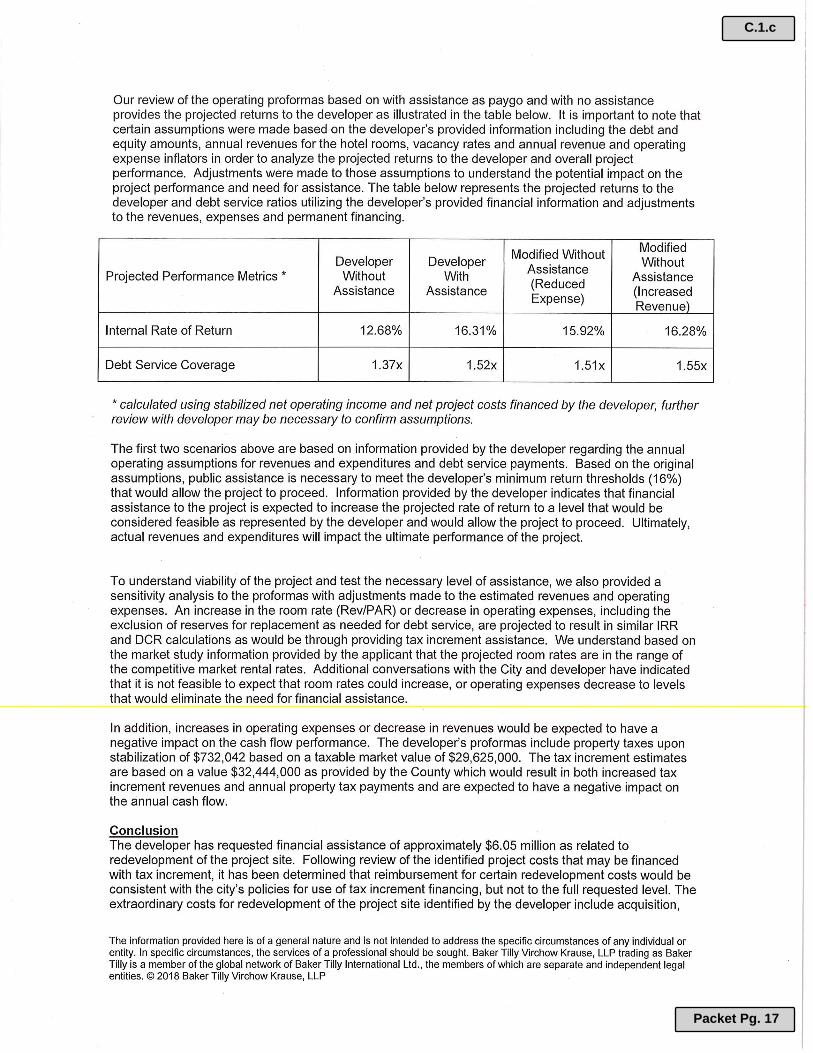

C.1.c

Packet Pg. 17

C.1.c

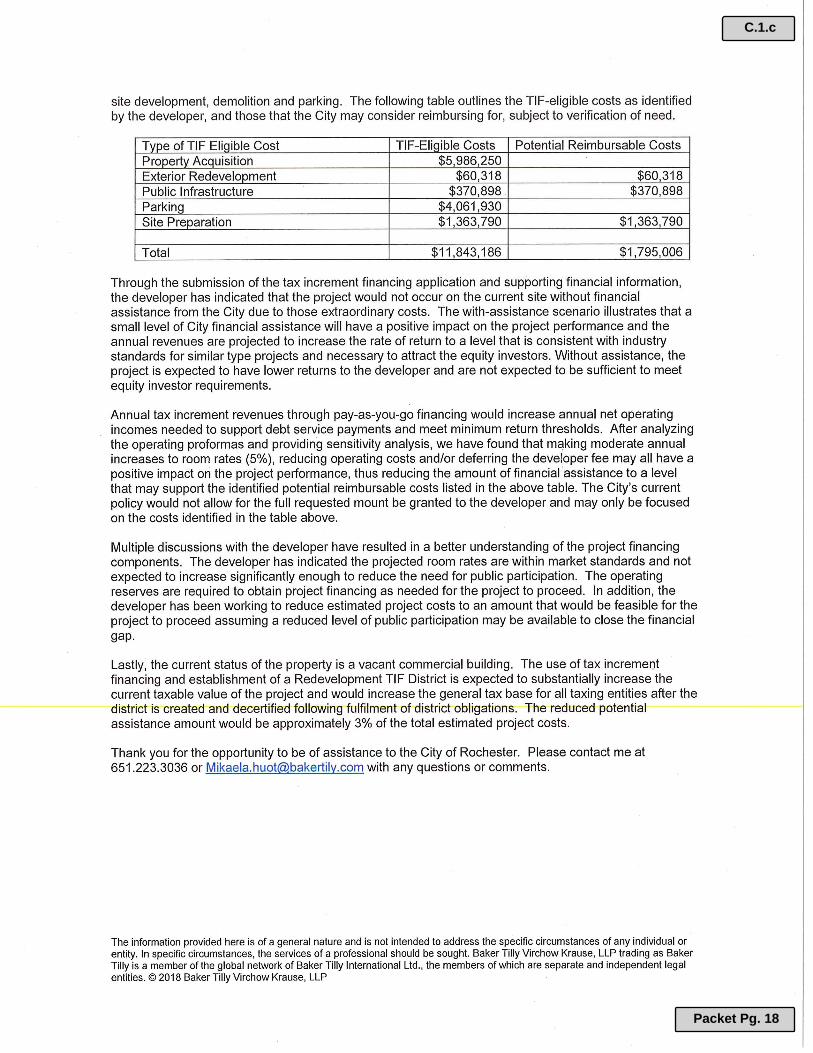

Packet Pg. 18

C.1.c

Packet Pg. 19

563693v7RC110-110

Economic Development Plan for Economic Development District No. 72

of the

Rochester Economic Development Authority

and

Tax Increment Financing Plan for

Redevelopment Tax Increment Financing District No. 72-1

(Eleven 02 Hotel Project)

July 22, 2019

This document was drafted by:

Kennedy & Graven, Chartered (JSB)

470 U.S. Bank Plaza

200 South Sixth Street

Minneapolis, MN 55402

Tel: (612) 337-9300

Fax: (612) 337-9310

C.1.d

Packet Pg. 20

1-1 563693v7RC110-110

Section I.

Economic Development Plan for

Economic Development District No. 72

Section 1.1. Definitions. The terms defined below, for purposes of this Economic

Development District and Economic Development Plan and for purposes of any Tax Increment

Financing Districts and Plans which may be now or hereafter established and approved within

the Economic Development District, shall have the following respective meanings, unless the

context specifically requires otherwise. The term “development” includes redevelopment, and

the term “developing” includes redeveloping.

“City” means the City of Rochester, Minnesota.

“Council” means the Common Council of the City, its governing body.

“Company” means Rochester Hotel Partners, LLC, a Delaware limited liability company,

or an affiliate thereof, and any successor or assigns.

“County” means Olmsted County, Minnesota.

“Development” means the acquisition of property located at 1101 2nd St. SW, Rochester,

MN 55902, the demolition the existing one-story structure thereon, and the construction of a

five-story, 237-room hotel and related parking ramp.

“Development District” means Economic Development District No. 72 of the EDA

established hereby, as the same may be amended.

“Development Plan” means the Development Plan, set forth herein, for the Development

District, as the same may be amended.

“EDA” means the Rochester Economic Development Authority.

“Enabling Act” means Minnesota Statutes, Sections 469.090 through 469.1082, as the

same may be amended or supplemented.

“State” means the State of Minnesota.

“Tax Increment District” means TIF District No. 72-1 and any tax increment financing

district established pursuant to the TIF Act now or in the future within the Development District,

and as the same may be amended.

“Tax Increment Plan” means the TIF Plan and any other respective tax increment

financing plans adopted pursuant to the TIF Act for any other Tax Increment Districts,

respectively, as the same may be amended.

“Tax Increments” means increments, as defined in Minnesota Statutes, Section 469.174

subdivision 25, clause (1), as the same may be amended, from the Tax Increment District.

C.1.d

Packet Pg. 21

1-2 563693v7RC110-110

“TIF Act” means Minnesota Statutes, Sections 469.174 through 469.1794, as the same

may be amended.

“TIF District No. 72-1” means Redevelopment Tax Increment Financing District No. 72-

1 (Eleven 02 Hotel Project) established within the Development District.

“TIF Plan” means this Tax Increment Financing Plan for TIF District No. 72-1, as

amended.

Section 1.2. Enabling Act; Statutory Authority. Pursuant to the Enabling Act, the EDA

is authorized to exercise the powers of an economic development authority and the powers of a

municipal housing and redevelopment authority established under Minnesota Statutes, Sections

469.001 to 469.047. It is the intention of the EDA, notwithstanding the enumeration of specific

goals and objectives in the TIF Plan, that the EDA shall have and enjoy with respect to the

Development District the full range of powers and duties conferred upon the EDA pursuant to

the Enabling Act, the TIF Act and such other legal authority as the EDA may have or enjoy from

time to time.

Section 1.3. Statement and Finding of Public Purpose. The EDA finds that there is a

need for development within the City and the Development District to provide employment

opportunities, to improve the local tax base, to provide housing, and to improve the general

economy of the City and the State. The sound development of the economic security of the

residents of the City depends upon proper development of marginal and other property, which

includes property that meets any one of a number of conditions, including properties whose

values are too low to pay for the public services required or rendered and properties whose lack

of use or improper use has resulted in stagnant or unproductive land that could otherwise

contribute to the public health, safety, and welfare.

The EDA finds that in many cases such property cannot be developed without public

participation and assistance in forms including property acquisition and/or write-down, proper

planning, the financing of land assembly in the work of clearance or development, and the

making or financing of various other public and private improvements necessary for

development. In cases where the development of property cannot be done by private enterprise

alone, the EDA believes it to be in the public interest to consider the exercise of its powers, to

advance and spend public money, and to provide the means and impetus for such development.

The EDA finds that in certain cases, property within the Development District would or

may not be available for development without the specific financial aid to be sought, that the

Development Plan and the Tax Increment Plan will afford maximum opportunity, consistent with

the needs of the City as a whole, for the development of the Development District by private

enterprise, and that the Development Plan conforms to the general plan for the development of

the City as a whole.

The EDA also finds that the welfare of the City and the State requires the active

promotion, retention, attraction, encouragement, and development of economically sound

industry and commerce through governmental action for the purpose of preventing the

emergence of blighted lands and areas of chronic unemployment. It shall also be the policy of

C.1.d

Packet Pg. 22

1-3 563693v7RC110-110

the EDA to facilitate and encourage such action as may be necessary to prevent the economic

deterioration of such areas to the point where the process can be reversed only by total

redevelopment. Through the use of the powers conferred on the EDA pursuant to the Enabling

Act, promoting economic development may prevent the occurrence of conditions requiring

redevelopment and prevent the emergence of blight, marginal land, and substantial and persistent

unemployment.

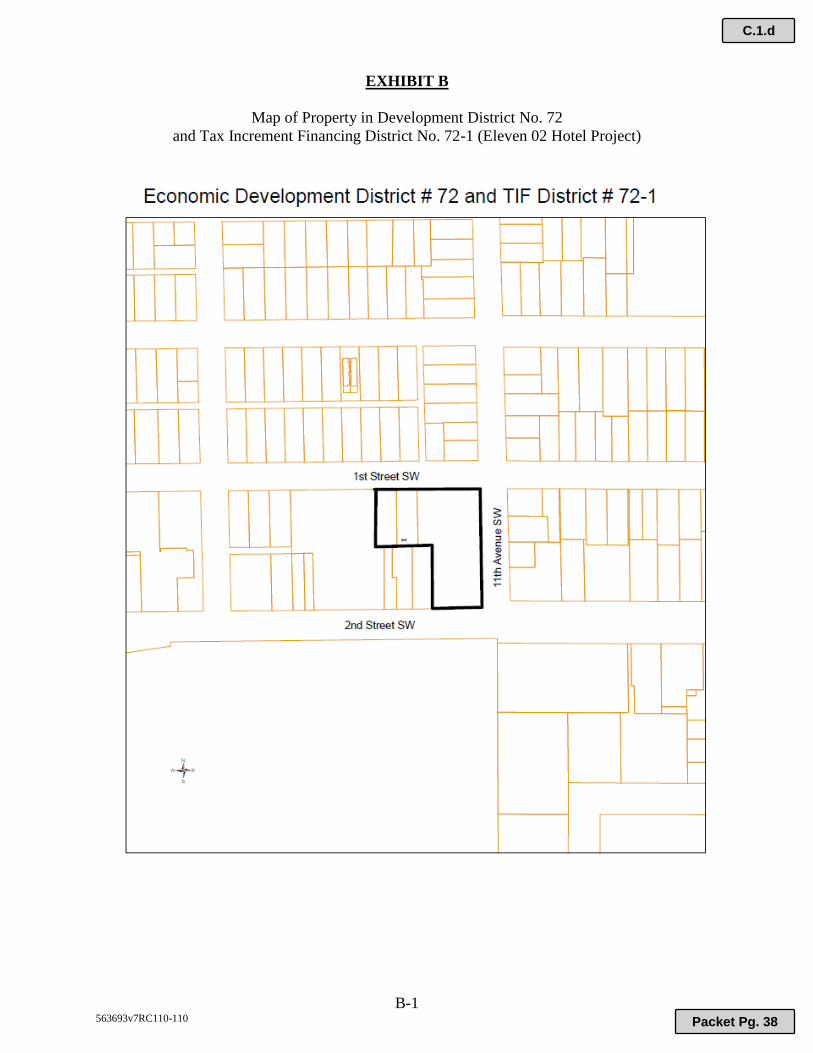

Section 1.4. Boundaries of the Development District. The property within the City

which is hereby designated as, and which shall initially constitute the Development District, is

the property described on Exhibit A attached hereto and as depicted on the map attached as

Exhibit B hereto. The EDA finds that the Development District, together with the objectives

which the EDA seeks to accomplish or encourage with respect to such property, constitutes an

“economic development district” within the meaning of Minnesota Statutes, Section 469.101.

The Development District shall also include all adjacent roadways, skyways, rights-of-way and

other areas wherein will be installed or upgraded the various public improvements necessary for

and part of the overall project.

Section 1.5. Development Activities. The EDA will perform or cause to be performed, to

the extent permitted by law, all project activities pursuant to the Enabling Act and the TIF Act

and other applicable state laws, and in doing so anticipates that the following may, but are not

required, to be undertaken by the EDA:

(a) The making of studies, planning, and other formal and informal activities

relating to the Development Plan.

(b) The implementation and administration of the Development Plan.

(c) The rezoning of land within the Development District.

(d) The acquisition of property, or interests in property when such acquisition

is consistent with the objectives of the Development Plan.

(e) The preparation of property for use and development in accordance with

applicable Land Use Regulations and a Development Agreement, including abatement of

hazardous materials, demolition of structures, clearance of sites, placement of fill and

grading.

(f) The resale of property to private parties.

(g) The construction or reconstruction of improvements described in Section

2.7 hereof.

(h) Provide for the construction of a range of housing options within the

Development District, including affordable housing.

(i) The issuance of tax increment bonds to finance the Public Costs of the

Development Plan, and the use of Tax Increments or other funds available to the City or

C.1.d

Packet Pg. 23

1-4 563693v7RC110-110

the EDA to pay or finance the Public Costs of the Development Plan incurred or to be

incurred by it pursuant to a Development Agreement.

(j) The use of Tax Increments to pay debt service on tax increment bonds or

otherwise pay or reimburse with interest the Public Costs of the Development Plan.

Section 1.6. Amendments. The EDA reserves the right to alter and amend the

Development Plan and the TIF Plan, subject to the provisions of state law regulating such action.

The EDA specifically reserves the right to enlarge or reduce the size of the Development District

and the Tax Increment District, the Development Plan and the Public Costs of the Development

Plan and the amount of tax increment bonds to be issued to finance such cost by following the

procedures specified in Minnesota Statutes, Section 469.175, Subdivision 4.

C.1.d

Packet Pg. 24

2-1 563693v7RC110-110

Section II.

Tax Increment Financing Plan for Redevelopment Tax Increment

Financing District No. 72-1

(Eleven 02 Hotel Project)

Section 2.1. Statement of Objectives. The establishment of the Development District in

the City pursuant to the Enabling Act is necessary and in the best interests of the City and its

residents and is necessary to give the EDA the ability to meet certain public purpose objectives

that would not be obtainable in the foreseeable future without intervention by the EDA in the

normal development process. The EDA seeks to achieve one or more of the following objectives

and the objectives set forth in the foregoing Development Plan with respect to such property

within the Development District as the EDA may determine and in such circumstances and upon

such terms as the EDA may deem appropriate or necessary:

(a) To provide for the acquisition of land and construction and financing of

site improvements in the Development District which are necessary for the orderly and

beneficial development of the Development District, and adjacent areas of the City.

(b) To promote and secure the prompt and cohesive development of property

within the Development District in a manner consistent with the Land Use Plan for the

Rochester Urban Service Area.

(c) To secure the prompt development of property in the Development

District in order to (i) realize return on presently existing public investment in public

utilities, streets, and other infrastructures; (ii) prevent the emergence of blight or blighting

factors; (iii) promote retention and expansion of the property tax base of the City and

other taxing jurisdictions in order to better enable such entities to pay for governmental

services and programs that they are required to provide; and (iv) increase the supply of

rental housing facilities.

(d) To assist such prompt development through the acquisition or write-down

of certain interests in property within the Development District which is not now in

productive use or in its highest and best use, to make or defray the cost of soil corrections

or other site improvements on said property, and to construct or reimburse for the

construction of public improvements and other facilities on or for the benefit of said

property, thereby promoting and securing the development of other land within the

Development District.

(e) Through the implementation of this Tax Increment Plan, to provide an

impetus for commercial, residential and other appropriate development in the

Development District or necessary to accommodate increased population within the City.

(f) To promote and secure additional employment opportunities within the

City, and the diversification thereof, and to prevent the loss of existing employment

opportunities, thereby improving living standards, reducing unemployment and

preventing the loss of valuable human resources.

C.1.d

Packet Pg. 25

2-2 563693v7RC110-110

(g) To provide funding for an ongoing development strategy and to prioritize

the use of available resources.

(h) To implement and revise from time to time, as may be deemed necessary

or desirable, a consolidated and unified plan and to finance the associated development

costs on an area-wide basis.

(i) To employ any of the powers of the EDA for the benefit of the

Development District in such cases and upon such terms as the EDA may deem

appropriate.

(j) To construct or acquire facilities deemed desirable for the development of

the Development District.

(k) To promote redevelopment of blighted or marginal property.

(l) To encourage the expansion and improvement of local business, economic

activity and development, whenever possible.

(m) To create a desirable and unique character within the Development

District through quality land use alternatives and design quality in new buildings.

(n) To provide for the construction of a range of housing options, including

affordable housing, within the Development District and elsewhere in the City as

permitted by applicable laws.

Section 2.2. Property Acquisition. The EDA does not currently intend to acquire any

property within TIF District No. 72-1 but reserves the right to acquire and convey (for full value

or a discount) such property, or appropriate interests therein, within the Development District as

the EDA may deem to be necessary or desirable to assist in the implementation of the TIF Plan.

The Company has site control of the property in TIF District No. 72-1 in connection with the

construction of the Development. The City and the EDA will not exercise eminent domain

powers in the TIF District with respect to property for the Development.

Section 2.3. Parcels to be Included in TIF District No. 72-1. TIF District No. 72-1 shall

consist of the property described on Exhibit A and depicted (together with the depiction of the

Development District) on the map attached as Exhibit B hereto. TIF District No. 72-1 shall also

include all adjacent roadways, rights-of-way and other area wherein will be installed or upgraded

the various public improvements necessary for and part of the overall project.

Section 2.4. Development Activity Anticipated for TIF District No. 72-1. The EDA

anticipates entering into a development agreement with the Company for the construction of the

Development. The EDA anticipates assisting the Company with certain costs associated with the

Development as described in Section 2.7 herein. The total development costs of the

Development are anticipated to be approximately $58,234,984. Construction of the

Development is expected to commence by approximately August 31, 2019 and be completed by

approximately December 31, 2020.

C.1.d

Packet Pg. 26

2-3 563693v7RC110-110

Section 2.5. Estimated Public Improvement Costs. The estimated public improvement

costs and the amount of bonded indebtedness (including interest thereon) to be incurred within

and for the benefit of the Tax Increment District are set forth herein, including without limitation

Section 2.7 herein. General obligation and/or tax increment revenue obligations, including pay

as you go tax increment revenue notes, interfund loans, and any other “bonds” as defined in the

TIF Act with interest in the 3% to 8% range, in addition to the direct use of tax increments, or

other borrowing or available funds (including without limitation interest-bearing EDA loans and

other assistance) may be used as required to finance such costs.

Section 2.6. Estimated Tax Capacity and Retention of Tax Increment. The base

estimated market value of taxable property in TIF District No. 72-1 is approximately

$2,323,500. The most recent net tax capacity of TIF District No. 72-1 is estimated to be

approximately $45,720 as of 2019. The net tax capacity of TIF District No. 72-1, at the

completion of development, which is estimated to occur by approximately December 31, 2020, is

estimated to be approximately $647,690; therefore the captured net tax capacity at the

completion of the development is estimated to be approximately $601,970.

The market value upon completion of the Development is estimated to be approximately

$32,422,000. The Tax Increments will be captured for up to 25 years after receipt of the first

Tax Increments or until the Public Costs described herein have been paid. The EDA determines

that 100% of the available increase in net tax capacity from TIF District No. 72-1 shall be used

for the repayment of bonds and the payment of Public Costs in accordance with the Development

Plan and this Tax Increment Plan.

Section 2.7. Estimated Development Costs. The development costs shall include the

estimated public improvement and development costs described in this Section (the “Public

Costs”). These costs are anticipated to be made or incurred within the Development District and

financed in whole or in part by tax increment or other available revenues of the EDA.

The total of these Public Costs is estimated at 100% of the Tax Increments to be

generated by TIF District No. 72-1 during its existence. These Tax Increments are expected to

be applied in direct or indirect aid of the development activities described in this Section and in

Sections 2.4 and 2.5 for such costs as site acquisition, improvement and/or other preparation and

development of building facilities.

The total development costs of the Development are anticipated to be approximately

$58,234,984. The budget for the Development Plan for the Development District and the TIF

Plan for TIF District No. 72-1 to be financed from Tax Increments, which is also part of the

budget for the portion of the Development to be financed from Tax Increments, is presently

estimated as follows:

C.1.d

Packet Pg. 27

2-4 563693v7RC110-110

Real Property Acquisition $0

Other Public Redevelopment Costs (including parking, streets, pedestrian

pathways and landscaping)

$10,361,819

Affordable Housing $964,546

Administrative Expenses $964,546

Interest on Indebtedness $7,000,000

Total $19,290,911

Bonding authorized by this Tax Increment Plan in an amount up to $19,290,911 may

include traditional general obligation or revenue bonding, including interest-bearing “pay-as-

you-go” financing, interest bearing internal EDA-financed borrowing, and any other “bonds” as

defined in the TIF Act. If bonding is required to finance the foregoing costs, the reasonable and

customary expenses for that bonding, such as capitalized interest, interest on the debt in the 3%

to 8% range, bond discount, and fiscal and legal fees, would be added to the estimates listed

above; subject to the requirements of the TIF Act. The EDA intends to issue a combination of a

“pay-as-you-go” note to the Company and internal, interfund loans in an aggregate amount up to

the total amount set forth above but does not currently expect to issue any other bonds payable

from TIF District No. 72-1.

The EDA intends to pay from available tax increment such qualifying administrative

costs as may be permitted by, but subject to the applicable limitations provided in, the TIF Act,

which is 10% of the total tax increments, as defined in section 469.174, subdivision 25, clause

(1).

Section 2.8. Type of Tax Increment District. The EDA, in determining the need to create

a tax increment financing district in accordance with the TIF Act, finds that TIF District No. 72-1

is a “redevelopment district” pursuant to Minnesota Statutes, Section 469.174, Subd. 10 as

described below.

TIF District No. 72-1 currently contains one parcel. The parcel is occupied because it

meets the requirements of Section 469.174, Subd. 10(a)(1) in that 100% (which is greater than

the required 15%) of the area of the parcel is occupied by buildings, streets, utilities, paved or

gravel parking lots or similar structures. The occupied parcel consists of 100% of the area of TIF

District No. 72-1 (which is greater than the required 70%). In addition, there is one building

located in TIF District No. 72-1. The sole building, which is 100% (i.e. greater than the required

50%) of the buildings within TIF District No. 72-1, is “structurally substandard” to a degree

requiring substantial renovation or clearance. The “structurally substandard” building was not in

compliance with the building code applicable to new buildings, and the costs of modifying the

building to satisfy the building code would be more than 15% of the cost of constructing a new

structure of the same square footage and type on the site. The reasons and supporting facts for

these determinations are set forth in the Blight Assessment for Hotel Rochester Partners, LLC

Rochester, Minnesota dated July 10, 2019, prepared by TSP, Inc. These findings are based in

part upon on-site examination and written reports substantiating the structurally substandard

nature of the buildings. All of the reasons and supporting facts and data for the determination

that TIF District No. 72-1 is a redevelopment district under the statute referenced in this Section

2.8 shall be kept on file in the offices of the City and be available to the public throughout the

life of TIF District No. 72-1.

C.1.d

Packet Pg. 28

2-5 563693v7RC110-110

Section 2.9. Duration of Tax Increment District. The duration of TIF District No. 72-1

will be 25 years from the receipt of the first tax increment. In accordance with Minnesota

Statutes, Section 469.175, Subd. 1(b), the EDA elects to first receive increment in 2022, resulting

in an estimated final year of 2047. The EDA may terminate TIF District No. 72-1 before the

end of the 26 year term if all costs of the project have been paid or provided for.

Section 2.10. Impact on Taxing Jurisdictions; Captured Net Tax Capacity; Estimated Tax

Increment. The impact of TIF District No. 72-1 on the affected taxing jurisdictions is reflected

in the EDA’s anticipated need to utilize the Tax Increments generated from TIF District No. 72-1

during the period described in Section 2.9 above for the purposes of financing the Public Costs

referenced in Section 2.7 above, as the same may be amended, following which period the

increased assessed valuations will inure to the benefit of such taxing jurisdictions.

For the payable 2019 property taxes, the respective tax capacity rates and net tax

capacities of these taxing jurisdictions are set out in the following table.

Taxing Jurisdiction Tax Capacity Rate Tax Capacity

City of Rochester 52.723 $141,631,536

Olmsted County 53.562 $199,131,753

I.S.D. No. 535 15.684 $164,529,334

Olmsted County HRA 1.286 $194,546,403

TOTAL 123.255 $699,839,026

On the assumption that the estimated captured tax capacity of TIF District No. 72-1

would be available to the above taxing jurisdictions without creation of TIF District No. 72-1,

the impact of this tax increment financing on the tax capacities of those taxing jurisdictions is

relatively small, as shown by comparing on a percentage basis the marginal effect on tax

capacity rates and by comparing the estimated $601,970 of captured net tax capacity upon

completion of the Development to the foregoing tax capacities of each of those jurisdictions,

respectively.

On the alternate assumption, which has been found to be the case, that none of the

estimated captured tax capacity would be available to these taxing jurisdictions without the

creation of TIF District No. 72-1, during the period of the existence of TIF District No. 72-1,

there would be no effect on the above tax capacities, but upon the expiration or earlier

termination of TIF District No. 72-1, each taxing jurisdiction’s tax capacity would be increased

by the captured tax capacity, as it may be adjusted over that time period.

The estimated amount of tax increment that will be generated over the life of TIF District

No. 72-1 is approximately $19,290,911 less the deduction by the Office of the State Auditor. The

estimated amount of tax increment attributable to the County, School District, and County HRA

levies is estimated to be approximately $8,383,106, $2,454,737 and $201,275, respectively. It is

C.1.d

Packet Pg. 29

2-6 563693v7RC110-110

not expected that the Development will have any impact on the need for new or improved public

infrastructure other than the infrastructure paid for by Tax Increments or private funds including

improvements to adjacent streets, sidewalks and utility systems. The City’s police and fire

departments currently serve the area so the City’s budget for services such as police and fire

protection is anticipated not to increase and the probable impact of TIF District No. 72-1 on such

services is expected to be minimal. The EDA anticipates that it will issue a pay as you go tax

increment revenue note to the Company for a portion of the Public Costs but such note or other

obligations will not affect the City’s or the EDA’s ability to issue other debt for general fund

purposes.

Section 2.11. Reasonable Expectations. The EDA has determined that the proposed

development of TIF District No. 72-1 would not reasonably be expected to occur solely through

private investment within the reasonably foreseeable future and that the increased market value

of the site that could reasonably be expected to occur without the use of tax increment financing

is approximately $0, which is less than $20,381,238, which is the increase in the market value

estimated to result from the proposed development (approximately $30,098,500, assuming no

annual inflation) after subtracting the present value of the projected tax increments for the

maximum duration of TIF District No. 72-1 (approximately $9,717,262).

Redevelopment of the site and construction of the Development would not move forward

without a variety of funding sources, including tax increment financing, due to the condition of

the site and the buildings thereon and the higher cost of redevelopment compared to development

of bare land.

Section 2.12. Tax Increment Accounts. Consistent with Minnesota Statutes, Section

469.177, Subdivision 5, requiring that “tax increment received with respect to any district shall

be segregated by the authority in a special account or accounts on its official books and records

or as otherwise established by resolution of the authority to be held by a trustee or trustees for the

benefit of the holders of the bonds,” the EDA and/or the City will account for all increment from

TIF District No. 72-1 in one or more City or EDA accounts and subaccounts, including the

ability where deemed appropriate to establish one or more accounts for the proper accounting

and implementation of the Tax Increment Plan and the Development Plan and the portion of the

development costs to be financed directly or indirectly with tax increment. The right to make

appropriate transfers in and out of such accounts is hereby reserved, along with the right to make

both external and internal interest-bearing borrowings, whether long-term or short-term,

including transfers from other City or EDA funds and interfund loans to cash flow tax increment

obligations and other legitimate expenditures.

The Council and EDA resolutions initially approving this Tax Increment Plan contain a

policy regarding “interfund loans and advances,” within the meaning of Minnesota Statutes,

Section 469.174, Subdivision 3.

Section 2.13. Modifications to Tax Increment District. In accordance with Minnesota

Statutes, Section 469.175, Subd. 4, any:

1. reduction or enlargement of the geographic area of the Tax Increment District;

C.1.d

Packet Pg. 30

2-7 563693v7RC110-110

2. increase in amount of bonded indebtedness to be incurred, including a

determination to capitalize interest on debt if that determination was not a part of

the original plan, or to increase or decrease the amount of interest on the debt to

be capitalized;

3. increase in the portion of the captured net tax capacity to be retained by the EDA;

4. increase in total estimated tax increment expenditures; or

5. designation of additional property to be acquired by the EDA,

shall be approved upon notice and after the discussion, public hearing and findings required for

approval of the original Tax Increment Plan.

The geographic area of the Tax Increment District may be reduced, but shall not be

enlarged after 5 years following the date of certification of the original net tax capacity by the

County Auditor. The requirements of this paragraph do not apply if (1) the only modification is

elimination of parcel(s) from the Tax Increment District, and (2)(A) the current net tax capacity

of the parcel(s) eliminated from the Tax Increment District equals or exceeds the net tax capacity

of those parcel(s) in the Tax Increment District’s original net tax capacity, or (B) the EDA agrees

that, notwithstanding Minnesota Statutes, Section 469.177, Subd. 1, the original net tax capacity

will be reduced by no more than the current net tax capacity of the parcel(s) eliminated from the

Tax Increment District.

The EDA must notify the County Auditor of any modification that reduces or enlarges

the geographic area of the Tax Increment District or the Development District. Modifications to

the Tax Increment District in the form of a budget modification or an expansion of the

boundaries will be recorded in the Tax Increment Plan.

No modifications to TIF District No. 72-1 or the TIF Plan have been made as of the date

hereof.

Section 2.14. Administrative Expenses. In accordance with Minnesota Statutes, Section

469.174, Subd. 14, and Minnesota Statutes, Section 469.176, Subd. 3, administrative expenses

means all expenditures of the EDA, other than:

1. amounts paid for the purchase of land or amounts paid to contractors or others

providing materials and services, including architectural and engineering services,

directly connected with the physical development of the real property in the

Development District;

2. relocation benefits paid to or services provided for persons residing or businesses

located in the Development District; or

3. amounts used to pay interest on, fund a reserve for, or sell at a discount bonds

issued pursuant to Minnesota Statutes, Section 469.178.

C.1.d

Packet Pg. 31

2-8 563693v7RC110-110

Administrative expenses also include amounts paid for services provided by bond

counsel, fiscal consultants, and planning or economic development consultants. Tax increment

may be used to pay any authorized and documented administrative expenses for the Tax

Increment District up to but not to exceed 10% of the total tax increment expenditures authorized

by this TIF Plan or the total tax increments, as defined in section 469.174, subdivision 25, clause

(1), whichever is less.

Pursuant to Minnesota Statutes, Section 469.176, Subd. 4h, tax increments may be used

to pay for the county’s actual administrative expenses incurred in connection with the Tax

Increment District. The county may require payment of those expenses by February l5 of the

year following the year the expenses were incurred. Increments used to pay the county’s

administrative expenses under subdivision 4h are not subject to the 10% limit.

Pursuant to Minnesota Statutes, Section 469.177, Subd. 11, the county treasurer shall

deduct an amount equal to approximately .36% of any Tax Increments distributed to the EDA

and the county treasurer shall pay the amount deducted to the state treasurer for deposit in the

state general fund to be appropriated to the State Auditor for the cost of financial reporting of tax

increment financing information and the cost of examining and auditing authorities’ use of tax

increment financing.

Section 2.15. Limitation on Property Not Subject to Improvement; Four-Year Rule. If

after 4 years from the date of certification of the original net tax capacity of the tax increment

financing district pursuant to Minnesota Statutes, Section 469.177, no demolition, rehabilitation

or renovation of property or other site preparation, including qualified improvement of a street

adjacent to a parcel but not installation of utility service including sewer or water systems, has

been commenced on a parcel located within a tax increment financing district by the authority or

by the owner of the parcel in accordance with the tax increment financing plan, no additional tax

increment may be taken from that parcel and the original net tax capacity of that parcel shall be

excluded from the original net tax capacity of the tax increment financing district. If the

authority or the owner of the parcel subsequently commences demolition, rehabilitation or

renovation or other site preparation on that parcel including qualified improvement of a street

adjacent to that parcel, in accordance with the tax increment financing plan, the authority shall

certify to the county auditor that the activity has commenced and the county auditor shall certify

the net tax capacity thereof as most recently certified by the commissioner of revenue and add it

to the original net tax capacity of the tax increment financing district. The county auditor must

enforce the provisions of this subdivision. For purposes of this subdivision, qualified

improvements of a street are limited to (1) construction or opening of a new street, (2) relocation

of a street, and (3) substantial reconstruction or rebuilding of an existing street.

Section 2.16. Use of Tax Increment. The EDA hereby determines that it will use 100%

of the captured net tax capacity of taxable property located in the Tax Increment District for the

following purposes:

1. to pay the principal of and interest on bonds used to finance a project;

C.1.d

Packet Pg. 32

2-9 563693v7RC110-110

2. to finance, or otherwise pay the capital and administration costs of a project

pursuant to Minnesota Statutes, Sections 469.001 to 469.047, and of the

Development District in accordance with the Enabling Act;

3. to pay for project costs as identified in the budget;

4. to finance, or otherwise pay for other purposes as provided in Minnesota Statutes,

Section 469.176, Subd. 4;

5. to pay principal and interest on any loans, advances or other payments made to

the EDA or for the benefit of a developer;

6. to finance or otherwise pay premiums and other costs for insurance, credit

enhancement, or other security guaranteeing the payment when due of principal

and interest on tax increment bonds or bonds issued pursuant to the Tax

Increment Plan, Minnesota Statutes, Chapter 462C and Minnesota Statutes,

Sections 469.152 to 469.1655, or any combination thereof; and

7. to accumulate or maintain a reserve securing the payment when due of the

principal and interest on the tax increment bonds or bonds issued pursuant to

Minnesota Statutes, Chapter 462C and Minnesota Statutes, Sections 469.152 to

469.1655, or both.

These revenues shall not be used to circumvent any levy limitations applicable to the

EDA nor for other purposes prohibited by Minnesota Statutes, Section 469.176, Subd. 4. In

accordance with Minnesota Statutes, Section 469.176, Subd. 4j, at least 90% of the Tax

Increments will be used to finance the cost of correcting the conditions that allow designation of

a tax increment financing district as a redevelopment district. These costs include, but are not

limited to, acquiring properties containing structurally substandard buildings or improvements or

hazardous substances, pollution, or contaminants, acquiring adjacent parcels necessary to

provide a site of sufficient size to permit development, demolition and rehabilitation of

structures, clearing of the land, the removal of hazardous substances or remediation necessary to

development of the land, and installation of utilities, roads, sidewalks, and parking facilities for

the site. The allocated administrative expenses of the authority, including the cost of preparation

of the development action response plan, may be included in the qualifying costs.

Section 2.17. Notification of Prior Planned Improvements. The EDA shall, after due and

diligent search, accompany its request for certification to the County Auditor or its notice of the

Tax Increment District enlargement with a listing of all properties within the Tax Increment

District or area of enlargement for which building permits have been issued during the 18

months immediately preceding approval of the Tax Increment Plan by the municipality pursuant

to Minnesota Statutes, Section 469.175, Subd. 3. The County Auditor shall increase the original

value of the Tax Increment District by the value of improvements for which a building permit

was issued.

Section 2.18. Excess Tax Increments. Pursuant to Minnesota Statutes, Section 469.176,

Subd 2, in any year in which the tax increment exceeds the amount necessary to pay the costs

authorized by the Tax Increment Plan, including the amount necessary to cancel any tax levy as

C.1.d

Packet Pg. 33

2-10 563693v7RC110-110

provided in Minnesota Statutes, Section 475.61, Subd. 3, the EDA shall use the excess amount to

do any of the following:

1. prepay any outstanding bonds;

2. discharge the pledge of tax increment therefor;

3. pay into an escrow account dedicated to the payment of such bond; or

4. return the excess to the County Auditor for redistribution to the respective taxing

jurisdictions in proportion to their local tax rates.

In addition, the EDA may, subject to the limitations set forth herein, choose to modify the

Tax Increment Plan in order to finance additional public costs in the Tax Increment District and

the Development District or terminate the Tax Increment District in advance of its legally

required termination date.

Section 2.19. Requirements for Agreements with Developers. The EDA will review any

proposal for private development to determine its conformance with the Tax Increment Plan and

with applicable municipal ordinances and codes. To facilitate this effort, the following

documents may be requested for review and approval: site plan, construction, mechanical, and

electrical system drawings, landscaping plan, grading and storm drainage plan, signage system

plan, and any other drawings or narrative deemed necessary by the EDA to demonstrate the

conformance of the development with City plans and ordinances. The EDA may also use the

agreements to address other issues related to the development.

Pursuant to Minnesota Statutes, Section 469.176, Subd. 5, no more than 25%, by acreage,

of the property to be acquired in the Tax Increment District as set forth in the Tax Increment Plan

shall at any time be owned by the EDA as a result of acquisition with the proceeds of bonds

issued pursuant to Minnesota Statutes, Section 469.178, without the EDA having, prior to

acquisition in excess of 25% of the acreage, concluded an agreement for the development or

redevelopment of the property acquired and which provides recourse for the EDA should the

development or redevelopment not be completed.

Section 2.20. Other Limitations on the Use of Tax Increment.

1. General Limitations. All revenue derived from Tax Increments shall be used in

accordance with the Tax Increment Plan. The revenues shall be used to finance, or

otherwise pay the capital and administration costs of the Development District

pursuant to the Enabling Act;

These revenues shall not be used to circumvent existing levy limit law. No

revenues derived from Tax Increments shall be used for the acquisition,

construction, renovation, operation or maintenance of a building to be used

primarily and regularly for conducting the business of a municipality, county,

school district, or any other local unit of government or the state or federal

government, or for a commons area used as a public park, or a facility used for

social, recreation or conference purposes. This provision shall not prohibit the

C.1.d

Packet Pg. 34

2-11 563693v7RC110-110

use of revenues derived from Tax Increments for the construction or renovation of

a parking structure.

2. Pooling Limitations. Except as otherwise provided in paragraph 4 below, at least

75% of Tax Increments from the Tax Increment District must be expended on

activities in the Tax Increment District or to pay bonds, to the extent that the

proceeds of the bonds were used to finance activities within said district or to pay,

or secure payment of, debt service on credit enhanced bonds. Not more than 25%

of said Tax Increments may be expended, through a development fund or

otherwise, on activities outside of the Tax Increment District except to pay, or

secure payment of, debt service on credit enhanced bonds. For purposes of

applying this restriction, all administrative expenses must be treated as if they

were solely for activities outside of the Tax Increment District.

3. Five Year Limitation on Commitment of Tax Increments. Tax Increments derived

from the Tax Increment District shall be deemed to have satisfied the 75% test set

forth in paragraph (2) above only if the 5-year rule set forth in Minnesota Statutes,

Section 469.1763, Subd. 3, has been satisfied; and beginning with the 6th year

following certification of the Tax Increment District, Minnesota Statutes, Section

469.1763, Subd. 4 applies.

4. Expenditures for Tax Credit Eligible Housing. The EDA hereby elects to

authorize spending up to an additional 10% of the tax increments on activities

located outside the Tax Increment District as permitted by Minnesota Statutes,

Section 469.1763, Subd. 2(d) provided that the expenditures meet the following

requirements:

(1) they are used exclusively to assist housing that meets the

requirements for a qualified low-income building as defined in Section 42 of the

Internal Revenue Code of 1986, as amended (the “Code”);

(2) they do not exceed the qualified basis of housing as defined under

Section 42(c) of the Code less the amount of any credit allowed under Section 42

of the Code, and

(3) they are used to (i) acquire and prepare the site for housing, (ii)

acquire, construct or rehabilitate the housing or (iii) make public improvements

directly related to the housing.

Section 2.21. County Road Costs. Pursuant to Minnesota Statutes, Section 469.175,

Subd. 1a, the County board may require the EDA to pay for all or part of the cost of County road

improvements if, the proposed development to be assisted by tax increment will, in the judgment

of the County, substantially increase the use of County roads requiring construction of road

improvements or other road costs and if the road improvements are not scheduled within the next

five years under a capital improvement plan or other County plan.

C.1.d

Packet Pg. 35

2-12 563693v7RC110-110

In the opinion of the EDA and consultants, the proposed development outlined in this

Plan will have little or no impact upon County roads. If the County elects to use increments to

improve County roads, it must notify the EDA within 30 days of receipt of this Plan.

Section 2.22. Assessment Agreements. Pursuant to Minnesota Statutes, Section 469.177,

Subd. 8, the EDA may enter into an agreement in recordable form with the developer of property

within the Tax Increment District which establishes a minimum market value of the land and

completed improvements for the duration of the Tax Increment District. The assessment

agreement shall be presented to the assessor who shall review the plans and specifications for the

improvements constructed, review the market value previously assigned to the land upon which

the improvements are to be constructed and, so long as the minimum market value contained in

the assessment agreement appear, in the judgment of the assessor, to be a reasonable estimate,

the assessor may certify the minimum market value agreement. The EDA anticipates it may

enter into an assessment agreement with the Company.

Section 2.23. Administration of the Tax Increment District. Administration of the Tax

Increment District will be handled by the Executive Director of the EDA.

Section 2.24. Financial Reporting Requirements. The EDA will comply with all

reporting requirements of Minnesota Statutes, Section 469.175, Subd. 5 and 6.

Section 2.25. Environmental Controls; Land Use Regulations. All municipal actions,

public improvements and private development shall be carried out in a manner consistent with

existing environmental controls and all applicable Land Use Regulations.

Section 2.26. Park and Open Space to be Created. Park and open space within the

Development District if created will be created in accordance with the zoning and platting

ordinances of the City.

Section 2.27. Development Program. The development program which the EDA seeks

to further through the implementation of this Tax Increment District and TIF Plan is the

Development Plan, as provided in Section I above.

C.1.d

Packet Pg. 36

A-1 563693v7RC110-110

EXHIBIT A

Description of Property in Development District No. 72 and Redevelopment Tax Increment

Financing District No. 72-1 (Eleven 02 Hotel Project)

Lot 1, Block 1, RHP Hotel Subdivision

All in Olmsted County, Minnesota. The land is Abstract property.

C.1.d

Packet Pg. 37

B-1 563693v7RC110-110

EXHIBIT B

Map of Property in Development District No. 72

and Tax Increment Financing District No. 72-1 (Eleven 02 Hotel Project)

C.1.d

Packet Pg. 38

563696v2RC110-110

EDA RESOLUTION NO. ______

COUNCIL RESOLUTION NO. ______

ROCHESTER ECONOMIC DEVELOPMENT AUTHORITY

COUNTY OF OLMSTED

STATE OF MINNESOTA

RESOLUTION APPROVING AN ECONOMIC DEVELOPMENT DISTRICT AND

ECONOMIC DEVELOPMENT PLAN THEREFOR, APPROVING A REDEVELOPMENT

TAX INCREMENT FINANCING DISTRICT AND A TAX INCREMENT FINANCING

PLAN THEREFOR

BE IT RESOLVED by the Board of Commissioners (the “Board”) of the Rochester

Economic Development Authority (the “EDA”), as follows:

Section 1. Recitals.

1.01. It has been proposed that the EDA establish Economic Development District No.

72 (the “Development District”), adopt the Economic Development Plan for the Development

District (the “Development Plan”), establish Redevelopment Tax Increment Financing District

No. 72-1 (Eleven 02 Hotel Project) within the Development District (the “TIF District”) and

adopt a Tax Increment Financing Plan therefor (the “TIF Plan” and, together with the

Development Plan, the “Plans”), all pursuant to and in conformity with applicable law, including

Minnesota Statutes, Sections 469.174 through 469.1794 (the “TIF Act”), and Sections 469.001

through 469.047 and Sections 469.090 through 469.1082, all as amended (collectively, the

“Act”); all as reflected in that certain document entitled in part “Economic Development Plan for

Economic Development District No. 72 of the Rochester Economic Development Authority and

Tax Increment Financing Plan for Redevelopment Tax Increment Financing District No. 72-1

(Eleven 02 Hotel Project),” dated July 22, 2019, and presented for the Board’s consideration.

1.02. The Board has investigated the facts relating to the establishment of the

Development District, the adoption of the Development Plan, the establishment of the TIF

District and the adoption of the TIF Plan.

1.03. The TIF District is being established to facilitate the acquisition of property

located at 1101 2nd St. SW, Rochester, MN 55902, the demolition the existing one-story

structure thereon, and the construction of a five-story, 237-room hotel and related parking ramp,

all within the Development District (the “Development”) to be undertaken by Rochester Hotel

Partners, LLC, a Delaware limited liability company or an affiliate thereof (the “Developer”).

1.04. Certain written reports and other documentation (collectively, the “Reports”)

relating to the Plans, including the tax increment application made and other information

supplied by the Developer as to the activities contemplated therein and the Blight Assessment for

Hotel Rochester Partners, LLC Rochester, Minnesota dated July 10, 2019, prepared by TSP, Inc.

(the “Redevelopment TIF Assessment”) have heretofore been assembled or prepared by staff or

C.1.e

Packet Pg. 39

2 563696v2RC110-110

others and submitted to the Board and/or made a part of the City of Rochester (the “City”) and

EDA files and proceedings on the Plans. The Reports include data, information and/or

substantiation constituting or relating to (1) the “studies and analyses” on why the TIF District

meets the requirements to be a redevelopment tax increment financing district, (2) why the

assistance satisfies the so-called “but for” test and (3) the bases for the other findings and

determinations made in this resolution. The Board hereby confirms, ratifies and adopts the

Reports, which are hereby incorporated into and made as fully a part of this resolution to the

same extent as if set forth in full herein.

1.05. The EDA or the City has performed all actions required by law to be performed

prior to the adoption and approval of the TIF Plan, including but not limited to notice to the

County Commissioner representing the area of the County to be included in the TIF District,

delivery of the TIF Plan to the County and School Board and the holding of a joint public

hearing thereon by the City and the EDA following notice thereof published in the City’s official

newspaper at least 10 but not more than 30 days prior to the public hearing.

Section 2. Findings for the Adoption and Approval of the Plans.

2.01. The Board hereby finds that the Development District is proper and desirable to

establish in the City and the Development Plan will afford maximum opportunity, consistent

with the needs of the City as a whole, for the development of the Development District by

private enterprise.

2.02. The Board hereby finds that the TIF District is in the public interest and is a

“redevelopment tax increment financing district” within the meaning of Minnesota Statutes,

Section 469.174, Subdivision 10, because the TIF District consists of a project or portions of a

project within which the following conditions, reasonably distributed throughout the TIF

District, exist: (1) parcels consisting of at least 70% of the area of the TIF District are occupied

by buildings, streets, utilities, paved or gravel parking lots, or other similar structures; and (2)

more than 50% of the buildings located within the TIF District are deemed “structurally

substandard” (within the meaning of Minnesota Statutes, Section 469.174, Subd. 10(b)), to a

degree requiring substantial renovation or clearance. The TIF District consists of one parcel

which is “occupied” as defined in Minnesota Statutes, Section 469.174, Subd. 10(a)(1) in that at

least 15% of the area of the parcel is occupied by buildings, streets, utilities, paved or gravel

parking lots, or other similar structures. Based on the Redevelopment TIF Assessment, the sole

building in the TIF District (100%, which is more than 50% of the buildings within the TIF

District), is found to be structurally substandard, not in compliance with applicable building

codes, and the building could not be brought into such compliance at a cost of less than 15% of

the cost of constructing a new structure of the same size and type on the subject site. These

findings are based in part upon on-site examination and a written report substantiating the

structurally substandard nature of the buildings. The reasons and supporting facts for the

determination that the TIF District is a redevelopment district under the statute are set forth in the

Redevelopment TIF Assessment, which is incorporated herein by reference, and a copy of which

is on file with the City Administrator.

2.03. The Board hereby makes the following additional findings in connection with the

TIF District:

C.1.e

Packet Pg. 40

3 563696v2RC110-110

(a) The Board further finds that the proposed Development, in the opinion of

the Board, would not occur solely through private investment within the reasonably

foreseeable future and, therefore, the use of tax increment financing is deemed necessary.

(b) The Board further finds that the TIF Plan conforms to the general plan for

the development or redevelopment of the City as a whole.

(c) The Board further finds that the TIF Plan will afford maximum

opportunity consistent with the sound needs of the City as a whole for the development of

the TIF District by private enterprise.

(d) For purposes of compliance with Minnesota Statutes, Section 469.175,

Subdivision 3(b)(2)(ii), the Board hereby finds that the increased market value of the site

that could reasonably be expected to occur without the use of tax increment financing is

approximately $0, which is less than $$20,381,238, which is the increase in the market

value estimated to result from the proposed development (approximately $30,098,500,

assuming no annual inflation) after subtracting the present value of the projected tax

increments for the maximum duration of the TIF District (approximately $9,717,262).

Thus, the use of tax increment financing will be a positive net gain to the City, the School

District, and the County, and the tax increment assistance does not exceed the benefit

which will be derived therefrom.

2.04. The EDA elects to retain all of the captured tax capacity to finance the costs of the

TIF District and the Development District.

2.05. The provisions of this Section 2 are hereby incorporated by reference into and

made a part of the TIF Plan.

2.06. The Board further finds that the Plans are intended and in the judgment of the

Board its effect will be to promote the public purposes and accomplish the objectives specified

therein.

2.07. The Development District and the TIF District are hereby established and the

Plans, as presented to the Board on this date, including without limitation the findings and

statements of objectives contained therein, are hereby approved, ratified, established, and

adopted and shall be placed on file in the office of the Executive Director of the EDA. City or

EDA staff shall, in writing, request the Olmsted County Auditor to certify the new TIF District

and file the Plans with the Commissioner of Revenue and the Office of the State Auditor.

Section 3. Interfund Loans.

3.01. The Board hereby approves a policy on interfund loans or advances (“Loans”) for

the TIF District, as follows:

(a) The authorized tax increment eligible costs (including without limitation

out-of-pocket administrative expenses in an amount up to $964,546, interest in an amount

up to $7,000,000 and other project costs in an amount up to $11,326,365) payable from

the TIF District, as its TIF Plan is originally adopted or may be amended, may need to be

C.1.e

Packet Pg. 41

4 563696v2RC110-110

financed on a short-term and/or long-term basis via one or more Loans, as may be

determined by the City Finance Director from time to time.

(b) The Loans may be advanced if and as needed from available monies in the

City’s or EDA’s general fund or other City or EDA fund designated by the City Finance

Director. Loans may be structured as draw-down or “line of credit” obligations of the

lending fund(s).

(c) Neither the maximum principal amount of any one Loan nor the aggregate

principal amount of all Loans may exceed $19,290,911 outstanding at any time.

(d) All Loans shall mature not later than February 1, 2048 or such earlier date

as the City Finance Director may specify in writing. All Loans may be pre-paid, in whole

or in part, whether from tax increment revenue, tax increment revenue bond proceeds or

other eligible sources.