Embed Size (px)

Citation preview

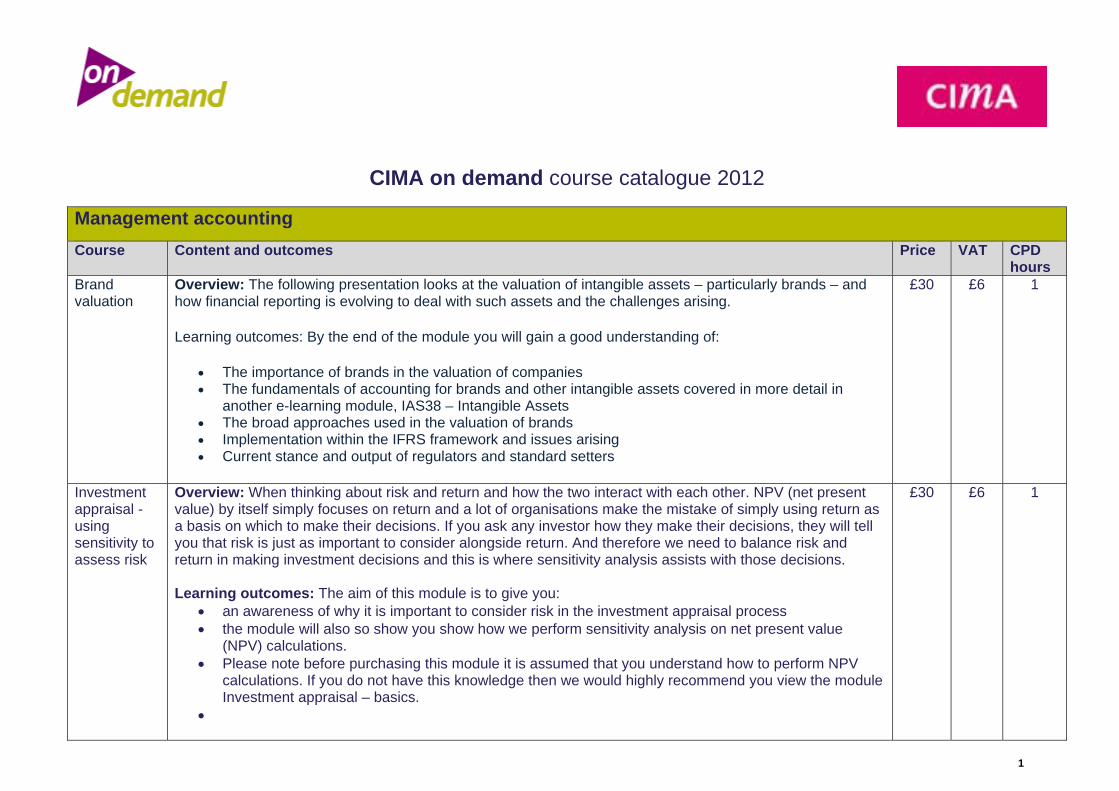

1

CIMA on demand course catalogue 2012

Management accounting

Course Content and outcomes Price VAT CPD

hours Brand valuation

Overview: The following presentation looks at the valuation of intangible assets – particularly brands – and how financial reporting is evolving to deal with such assets and the challenges arising.

Learning outcomes: By the end of the module you will gain a good understanding of:

• The importance of brands in the valuation of companies • The fundamentals of accounting for brands and other intangible assets covered in more detail in

another e-learning module, IAS38 – Intangible Assets • The broad approaches used in the valuation of brands • Implementation within the IFRS framework and issues arising • Current stance and output of regulators and standard setters

£30 £6 1

Investment appraisal - using sensitivity to assess risk

Overview: When thinking about risk and return and how the two interact with each other. NPV (net present value) by itself simply focuses on return and a lot of organisations make the mistake of simply using return as a basis on which to make their decisions. If you ask any investor how they make their decisions, they will tell you that risk is just as important to consider alongside return. And therefore we need to balance risk and return in making investment decisions and this is where sensitivity analysis assists with those decisions. Learning outcomes: The aim of this module is to give you:

• an awareness of why it is important to consider risk in the investment appraisal process • the module will also so show you show how we perform sensitivity analysis on net present value

(NPV) calculations. • Please note before purchasing this module it is assumed that you understand how to perform NPV

calculations. If you do not have this knowledge then we would highly recommend you view the module Investment appraisal – basics.

•

£30 £6 1

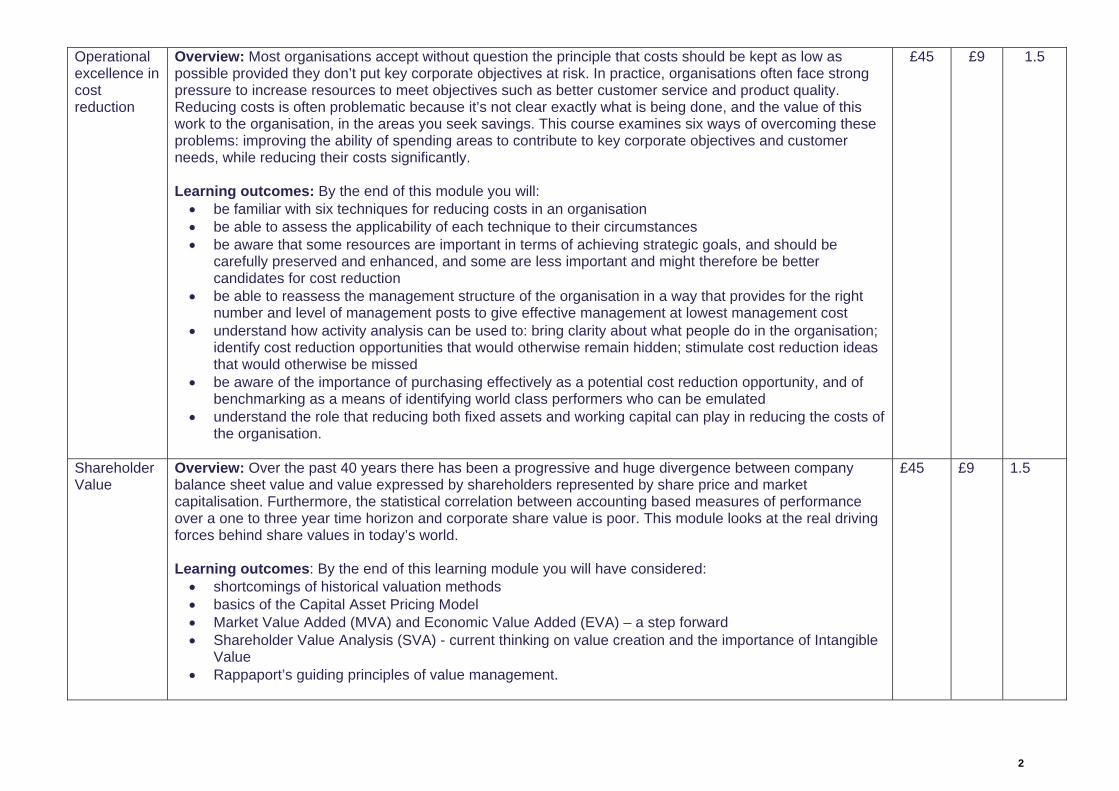

2

Operational excellence in cost reduction

Overview: Most organisations accept without question the principle that costs should be kept as low as possible provided they don’t put key corporate objectives at risk. In practice, organisations often face strong pressure to increase resources to meet objectives such as better customer service and product quality. Reducing costs is often problematic because it’s not clear exactly what is being done, and the value of this work to the organisation, in the areas you seek savings. This course examines six ways of overcoming these problems: improving the ability of spending areas to contribute to key corporate objectives and customer needs, while reducing their costs significantly. Learning outcomes: By the end of this module you will: • be familiar with six techniques for reducing costs in an organisation • be able to assess the applicability of each technique to their circumstances • be aware that some resources are important in terms of achieving strategic goals, and should be

carefully preserved and enhanced, and some are less important and might therefore be better candidates for cost reduction

• be able to reassess the management structure of the organisation in a way that provides for the right number and level of management posts to give effective management at lowest management cost

• understand how activity analysis can be used to: bring clarity about what people do in the organisation; identify cost reduction opportunities that would otherwise remain hidden; stimulate cost reduction ideas that would otherwise be missed

• be aware of the importance of purchasing effectively as a potential cost reduction opportunity, and of benchmarking as a means of identifying world class performers who can be emulated

• understand the role that reducing both fixed assets and working capital can play in reducing the costs of the organisation.

£45 £9 1.5

Shareholder Value

Overview: Over the past 40 years there has been a progressive and huge divergence between company balance sheet value and value expressed by shareholders represented by share price and market capitalisation. Furthermore, the statistical correlation between accounting based measures of performance over a one to three year time horizon and corporate share value is poor. This module looks at the real driving forces behind share values in today’s world. Learning outcomes: By the end of this learning module you will have considered: • shortcomings of historical valuation methods • basics of the Capital Asset Pricing Model • Market Value Added (MVA) and Economic Value Added (EVA) – a step forward • Shareholder Value Analysis (SVA) - current thinking on value creation and the importance of Intangible

Value • Rappaport’s guiding principles of value management.

£45 £9 1.5

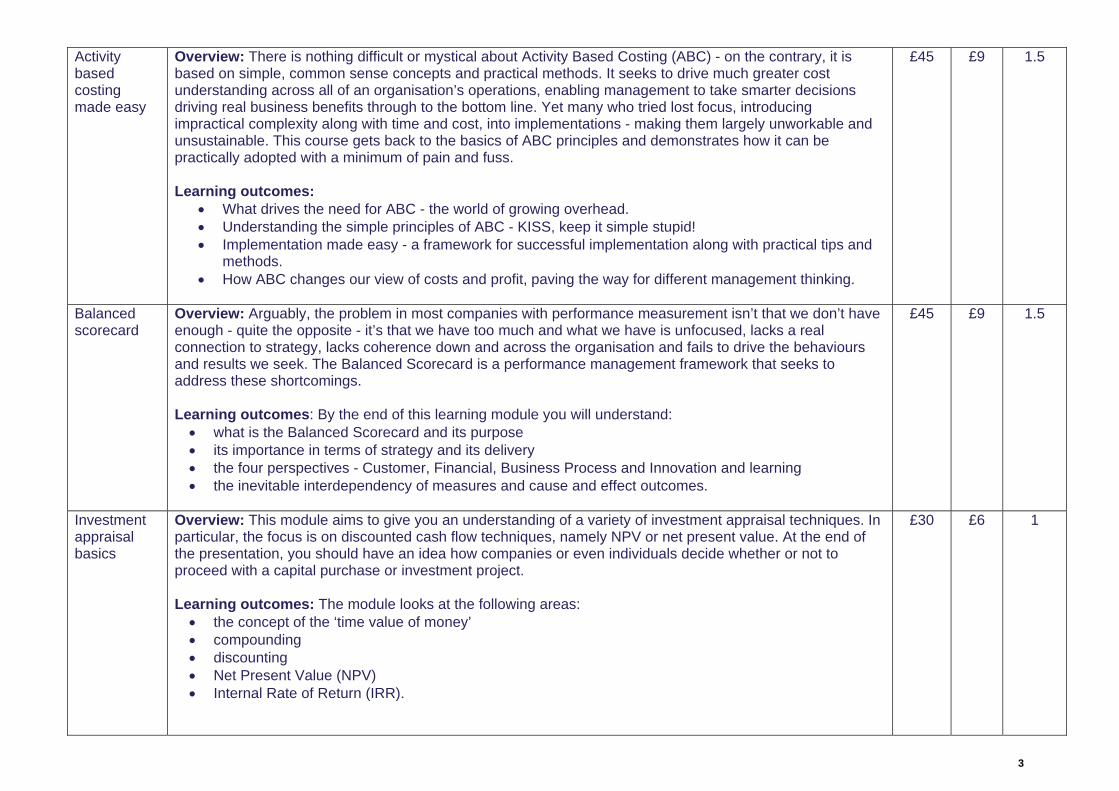

3

Activity based costing made easy

Overview: There is nothing difficult or mystical about Activity Based Costing (ABC) - on the contrary, it is based on simple, common sense concepts and practical methods. It seeks to drive much greater cost understanding across all of an organisation’s operations, enabling management to take smarter decisions driving real business benefits through to the bottom line. Yet many who tried lost focus, introducing impractical complexity along with time and cost, into implementations - making them largely unworkable and unsustainable. This course gets back to the basics of ABC principles and demonstrates how it can be practically adopted with a minimum of pain and fuss. Learning outcomes:

• What drives the need for ABC - the world of growing overhead. • Understanding the simple principles of ABC - KISS, keep it simple stupid! • Implementation made easy - a framework for successful implementation along with practical tips and

methods. • How ABC changes our view of costs and profit, paving the way for different management thinking.

£45 £9 1.5

Balanced scorecard

Overview: Arguably, the problem in most companies with performance measurement isn’t that we don’t have enough - quite the opposite - it’s that we have too much and what we have is unfocused, lacks a real connection to strategy, lacks coherence down and across the organisation and fails to drive the behaviours and results we seek. The Balanced Scorecard is a performance management framework that seeks to address these shortcomings. Learning outcomes: By the end of this learning module you will understand: • what is the Balanced Scorecard and its purpose • its importance in terms of strategy and its delivery • the four perspectives - Customer, Financial, Business Process and Innovation and learning • the inevitable interdependency of measures and cause and effect outcomes.

£45 £9 1.5

Investment appraisal basics

Overview: This module aims to give you an understanding of a variety of investment appraisal techniques. In particular, the focus is on discounted cash flow techniques, namely NPV or net present value. At the end of the presentation, you should have an idea how companies or even individuals decide whether or not to proceed with a capital purchase or investment project. Learning outcomes: The module looks at the following areas: • the concept of the ‘time value of money’ • compounding • discounting • Net Present Value (NPV) • Internal Rate of Return (IRR).

£30 £6 1

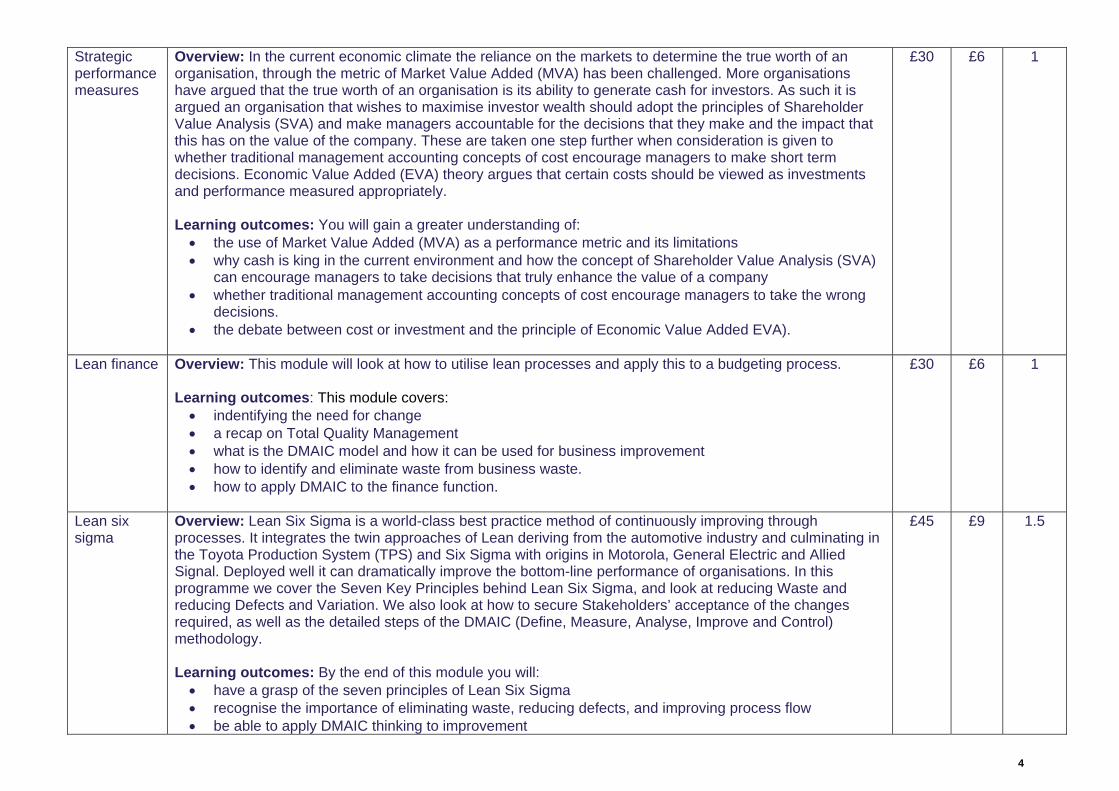

4

Strategic performance measures

Overview: In the current economic climate the reliance on the markets to determine the true worth of an organisation, through the metric of Market Value Added (MVA) has been challenged. More organisations have argued that the true worth of an organisation is its ability to generate cash for investors. As such it is argued an organisation that wishes to maximise investor wealth should adopt the principles of Shareholder Value Analysis (SVA) and make managers accountable for the decisions that they make and the impact that this has on the value of the company. These are taken one step further when consideration is given to whether traditional management accounting concepts of cost encourage managers to make short term decisions. Economic Value Added (EVA) theory argues that certain costs should be viewed as investments and performance measured appropriately. Learning outcomes: You will gain a greater understanding of: • the use of Market Value Added (MVA) as a performance metric and its limitations • why cash is king in the current environment and how the concept of Shareholder Value Analysis (SVA)

can encourage managers to take decisions that truly enhance the value of a company • whether traditional management accounting concepts of cost encourage managers to take the wrong

decisions. • the debate between cost or investment and the principle of Economic Value Added EVA).

£30 £6 1

Lean finance Overview: This module will look at how to utilise lean processes and apply this to a budgeting process. Learning outcomes: This module covers: • indentifying the need for change • a recap on Total Quality Management • what is the DMAIC model and how it can be used for business improvement • how to identify and eliminate waste from business waste. • how to apply DMAIC to the finance function.

£30 £6 1

Lean six sigma

Overview: Lean Six Sigma is a world-class best practice method of continuously improving through processes. It integrates the twin approaches of Lean deriving from the automotive industry and culminating in the Toyota Production System (TPS) and Six Sigma with origins in Motorola, General Electric and Allied Signal. Deployed well it can dramatically improve the bottom-line performance of organisations. In this programme we cover the Seven Key Principles behind Lean Six Sigma, and look at reducing Waste and reducing Defects and Variation. We also look at how to secure Stakeholders’ acceptance of the changes required, as well as the detailed steps of the DMAIC (Define, Measure, Analyse, Improve and Control) methodology. Learning outcomes: By the end of this module you will: • have a grasp of the seven principles of Lean Six Sigma • recognise the importance of eliminating waste, reducing defects, and improving process flow • be able to apply DMAIC thinking to improvement

£45 £9 1.5

5

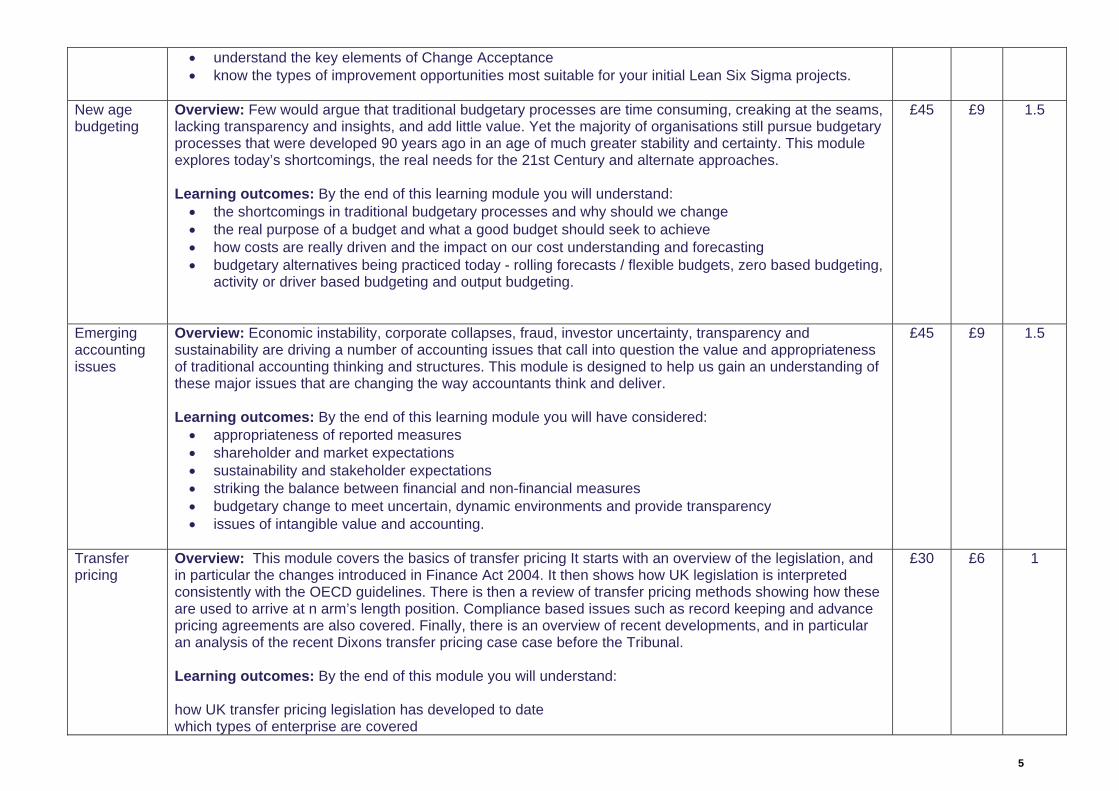

• understand the key elements of Change Acceptance • know the types of improvement opportunities most suitable for your initial Lean Six Sigma projects.

New age budgeting

Overview: Few would argue that traditional budgetary processes are time consuming, creaking at the seams, lacking transparency and insights, and add little value. Yet the majority of organisations still pursue budgetary processes that were developed 90 years ago in an age of much greater stability and certainty. This module explores today’s shortcomings, the real needs for the 21st Century and alternate approaches. Learning outcomes: By the end of this learning module you will understand: • the shortcomings in traditional budgetary processes and why should we change • the real purpose of a budget and what a good budget should seek to achieve • how costs are really driven and the impact on our cost understanding and forecasting • budgetary alternatives being practiced today - rolling forecasts / flexible budgets, zero based budgeting,

activity or driver based budgeting and output budgeting.

£45 £9 1.5

Emerging accounting issues

Overview: Economic instability, corporate collapses, fraud, investor uncertainty, transparency and sustainability are driving a number of accounting issues that call into question the value and appropriateness of traditional accounting thinking and structures. This module is designed to help us gain an understanding of these major issues that are changing the way accountants think and deliver. Learning outcomes: By the end of this learning module you will have considered: • appropriateness of reported measures • shareholder and market expectations • sustainability and stakeholder expectations • striking the balance between financial and non-financial measures • budgetary change to meet uncertain, dynamic environments and provide transparency • issues of intangible value and accounting.

£45 £9 1.5

Transfer pricing

Overview: This module covers the basics of transfer pricing It starts with an overview of the legislation, and in particular the changes introduced in Finance Act 2004. It then shows how UK legislation is interpreted consistently with the OECD guidelines. There is then a review of transfer pricing methods showing how these are used to arrive at n arm’s length position. Compliance based issues such as record keeping and advance pricing agreements are also covered. Finally, there is an overview of recent developments, and in particular an analysis of the recent Dixons transfer pricing case case before the Tribunal. Learning outcomes: By the end of this module you will understand: how UK transfer pricing legislation has developed to date which types of enterprise are covered

£30 £6 1

6

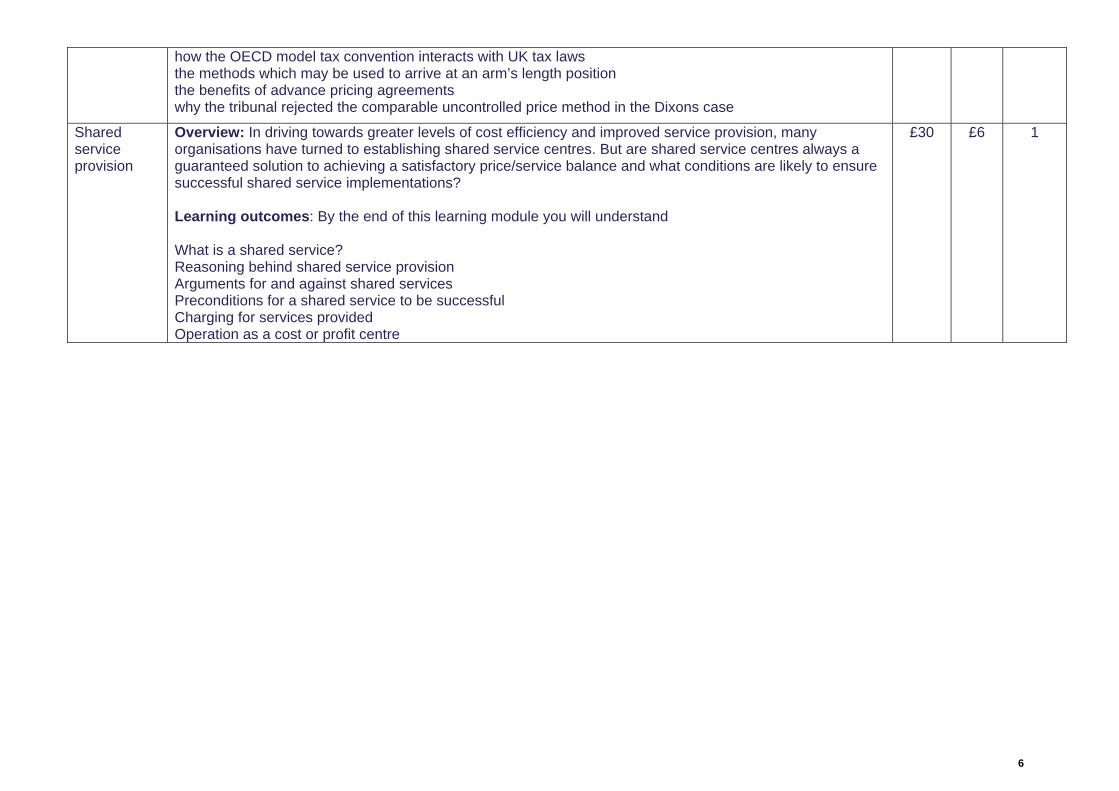

how the OECD model tax convention interacts with UK tax laws the methods which may be used to arrive at an arm’s length position the benefits of advance pricing agreements why the tribunal rejected the comparable uncontrolled price method in the Dixons case

Shared service provision

Overview: In driving towards greater levels of cost efficiency and improved service provision, many organisations have turned to establishing shared service centres. But are shared service centres always a guaranteed solution to achieving a satisfactory price/service balance and what conditions are likely to ensure successful shared service implementations? Learning outcomes: By the end of this learning module you will understand What is a shared service? Reasoning behind shared service provision Arguments for and against shared services Preconditions for a shared service to be successful Charging for services provided Operation as a cost or profit centre

£30 £6 1

7

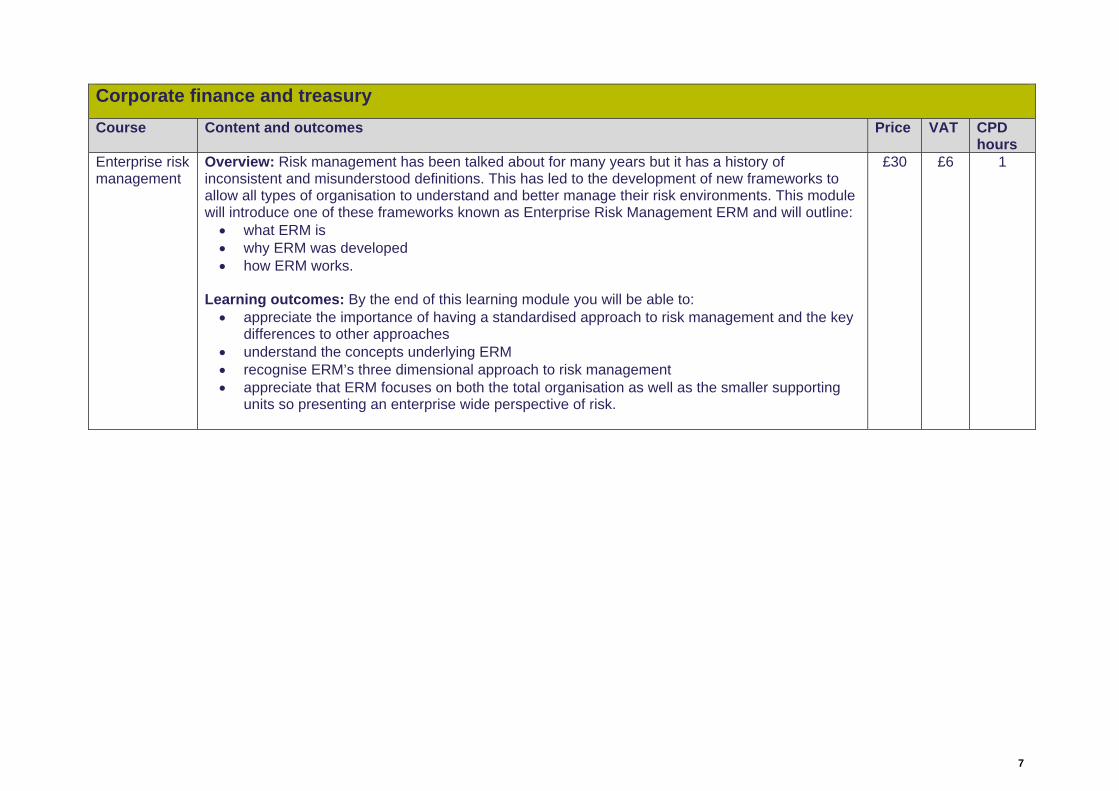

Corporate finance and treasury

Course Content and outcomes Price VAT CPD hours

Enterprise risk management

Overview: Risk management has been talked about for many years but it has a history of inconsistent and misunderstood definitions. This has led to the development of new frameworks to allow all types of organisation to understand and better manage their risk environments. This module will introduce one of these frameworks known as Enterprise Risk Management ERM and will outline: • what ERM is • why ERM was developed • how ERM works.

Learning outcomes: By the end of this learning module you will be able to: • appreciate the importance of having a standardised approach to risk management and the key

differences to other approaches • understand the concepts underlying ERM • recognise ERM’s three dimensional approach to risk management • appreciate that ERM focuses on both the total organisation as well as the smaller supporting

units so presenting an enterprise wide perspective of risk.

£30 £6 1

8

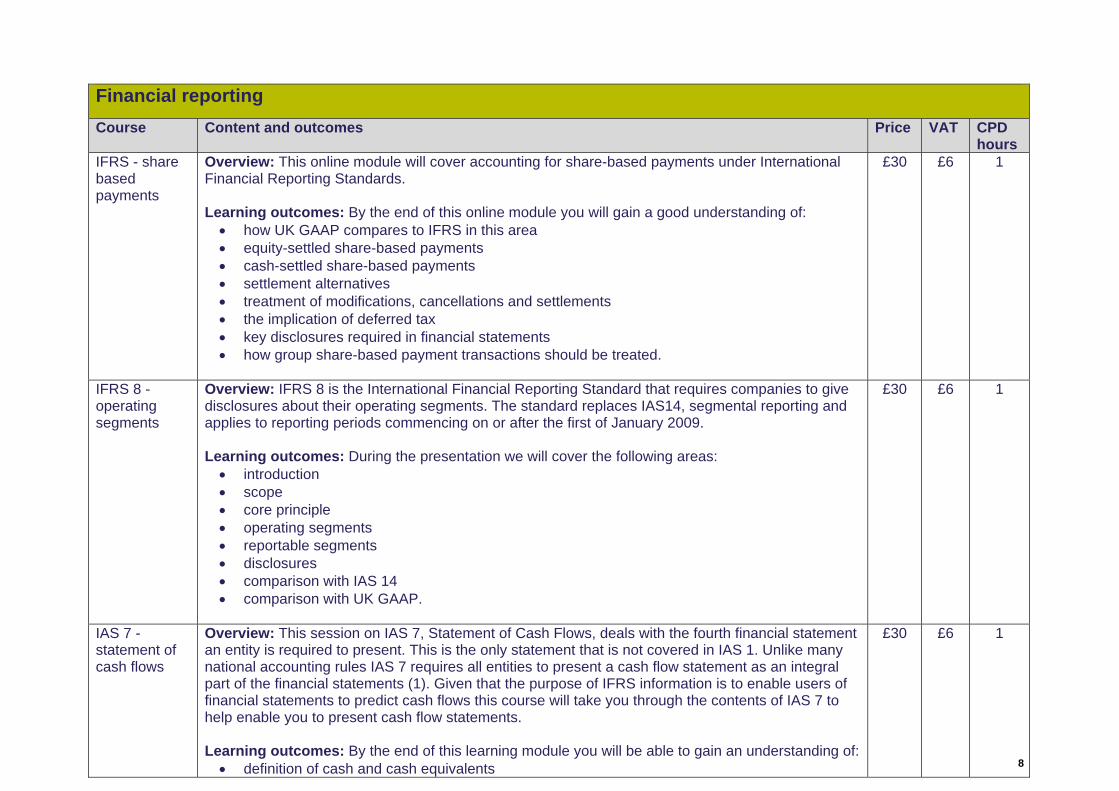

Financial reporting

Course Content and outcomes Price VAT CPD hours

IFRS - share based payments

Overview: This online module will cover accounting for share-based payments under International Financial Reporting Standards. Learning outcomes: By the end of this online module you will gain a good understanding of: • how UK GAAP compares to IFRS in this area • equity-settled share-based payments • cash-settled share-based payments • settlement alternatives • treatment of modifications, cancellations and settlements • the implication of deferred tax • key disclosures required in financial statements • how group share-based payment transactions should be treated.

£30 £6 1

IFRS 8 - operating segments

Overview: IFRS 8 is the International Financial Reporting Standard that requires companies to give disclosures about their operating segments. The standard replaces IAS14, segmental reporting and applies to reporting periods commencing on or after the first of January 2009. Learning outcomes: During the presentation we will cover the following areas: • introduction • scope • core principle • operating segments • reportable segments • disclosures • comparison with IAS 14 • comparison with UK GAAP.

£30 £6 1

IAS 7 - statement of cash flows

Overview: This session on IAS 7, Statement of Cash Flows, deals with the fourth financial statement an entity is required to present. This is the only statement that is not covered in IAS 1. Unlike many national accounting rules IAS 7 requires all entities to present a cash flow statement as an integral part of the financial statements (1). Given that the purpose of IFRS information is to enable users of financial statements to predict cash flows this course will take you through the contents of IAS 7 to help enable you to present cash flow statements. Learning outcomes: By the end of this learning module you will be able to gain an understanding of: • definition of cash and cash equivalents

£30 £6 1

9

• three main headings: operating, investing and financing • direct or indirect method • some netting allowed • actual or average exchange rates • interest and dividends can be classified in any way • disclosures.

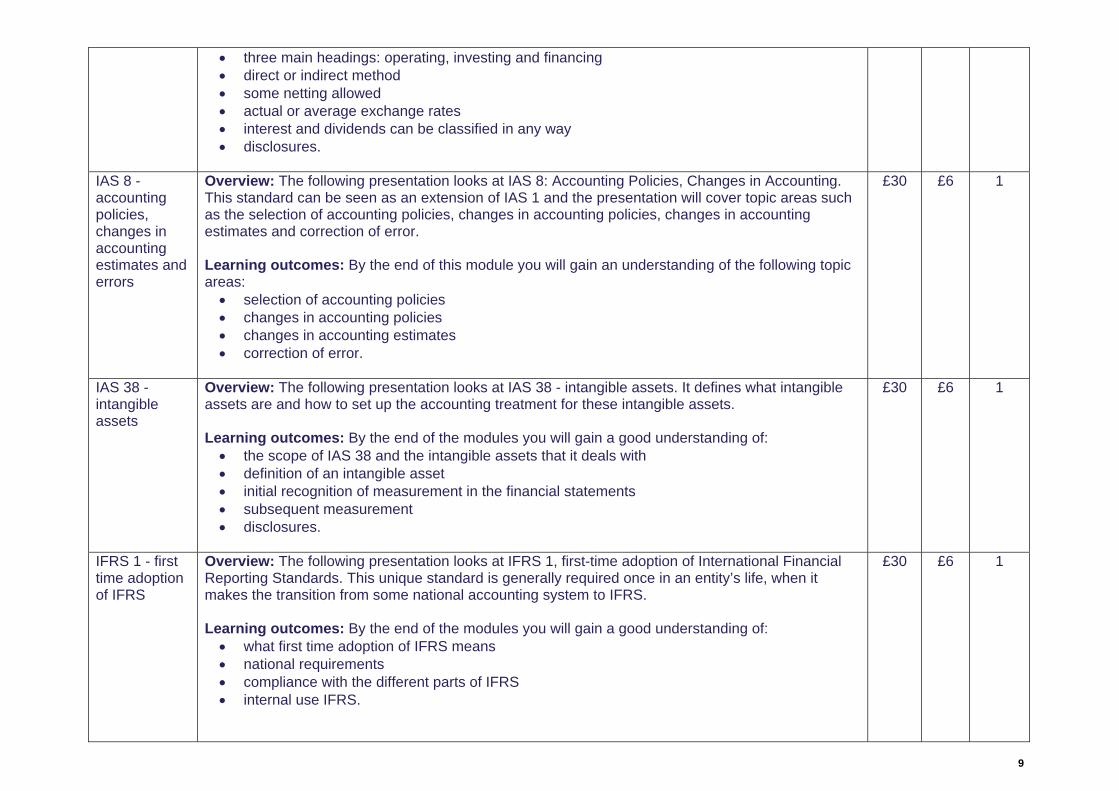

IAS 8 - accounting policies, changes in accounting estimates and errors

Overview: The following presentation looks at IAS 8: Accounting Policies, Changes in Accounting. This standard can be seen as an extension of IAS 1 and the presentation will cover topic areas such as the selection of accounting policies, changes in accounting policies, changes in accounting estimates and correction of error. Learning outcomes: By the end of this module you will gain an understanding of the following topic areas: • selection of accounting policies • changes in accounting policies • changes in accounting estimates • correction of error.

£30 £6 1

IAS 38 - intangible assets

Overview: The following presentation looks at IAS 38 - intangible assets. It defines what intangible assets are and how to set up the accounting treatment for these intangible assets. Learning outcomes: By the end of the modules you will gain a good understanding of: • the scope of IAS 38 and the intangible assets that it deals with • definition of an intangible asset • initial recognition of measurement in the financial statements • subsequent measurement • disclosures.

£30 £6 1

IFRS 1 - first time adoption of IFRS

Overview: The following presentation looks at IFRS 1, first-time adoption of International Financial Reporting Standards. This unique standard is generally required once in an entity’s life, when it makes the transition from some national accounting system to IFRS. Learning outcomes: By the end of the modules you will gain a good understanding of: • what first time adoption of IFRS means • national requirements • compliance with the different parts of IFRS • internal use IFRS.

£30 £6 1

10

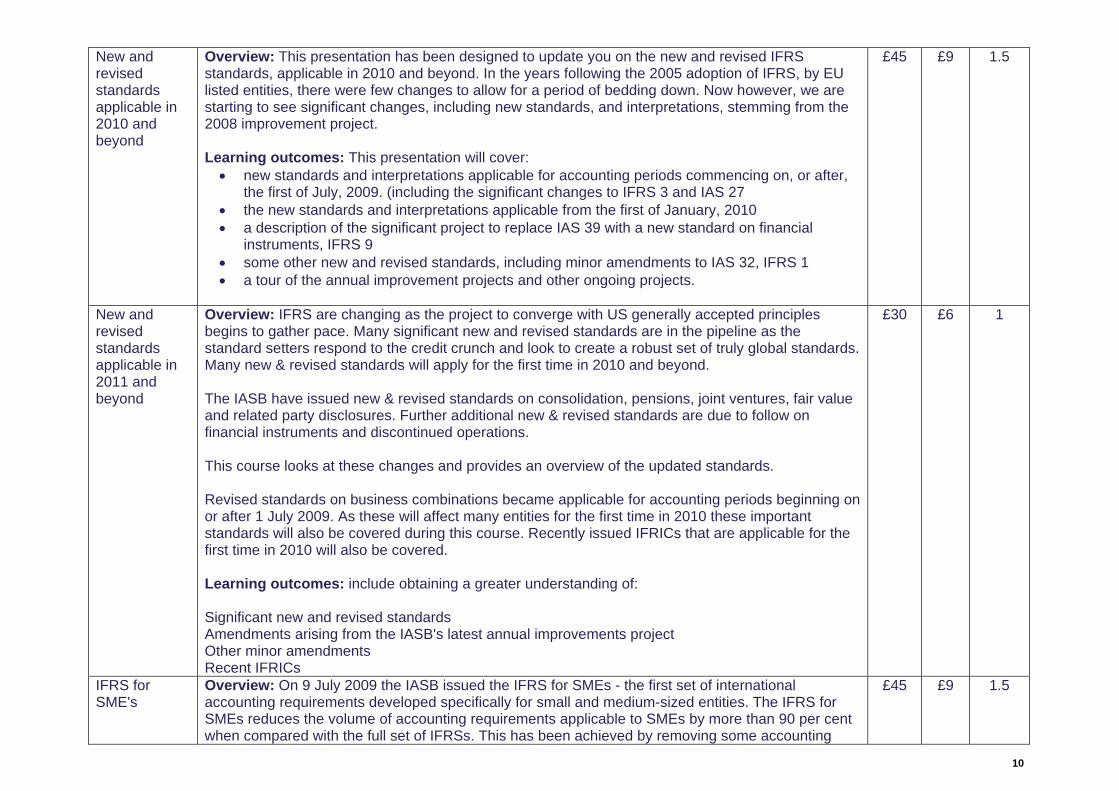

New and revised standards applicable in 2010 and beyond

Overview: This presentation has been designed to update you on the new and revised IFRS standards, applicable in 2010 and beyond. In the years following the 2005 adoption of IFRS, by EU listed entities, there were few changes to allow for a period of bedding down. Now however, we are starting to see significant changes, including new standards, and interpretations, stemming from the 2008 improvement project. Learning outcomes: This presentation will cover: • new standards and interpretations applicable for accounting periods commencing on, or after,

the first of July, 2009. (including the significant changes to IFRS 3 and IAS 27 • the new standards and interpretations applicable from the first of January, 2010 • a description of the significant project to replace IAS 39 with a new standard on financial

instruments, IFRS 9 • some other new and revised standards, including minor amendments to IAS 32, IFRS 1 • a tour of the annual improvement projects and other ongoing projects.

£45 £9 1.5

New and revised standards applicable in 2011 and beyond

Overview: IFRS are changing as the project to converge with US generally accepted principles begins to gather pace. Many significant new and revised standards are in the pipeline as the standard setters respond to the credit crunch and look to create a robust set of truly global standards. Many new & revised standards will apply for the first time in 2010 and beyond. The IASB have issued new & revised standards on consolidation, pensions, joint ventures, fair value and related party disclosures. Further additional new & revised standards are due to follow on financial instruments and discontinued operations. This course looks at these changes and provides an overview of the updated standards. Revised standards on business combinations became applicable for accounting periods beginning on or after 1 July 2009. As these will affect many entities for the first time in 2010 these important standards will also be covered during this course. Recently issued IFRICs that are applicable for the first time in 2010 will also be covered. Learning outcomes: include obtaining a greater understanding of: Significant new and revised standards Amendments arising from the IASB's latest annual improvements project Other minor amendments Recent IFRICs

£30 £6 1

IFRS for SME's

Overview: On 9 July 2009 the IASB issued the IFRS for SMEs - the first set of international accounting requirements developed specifically for small and medium-sized entities. The IFRS for SMEs reduces the volume of accounting requirements applicable to SMEs by more than 90 per cent when compared with the full set of IFRSs. This has been achieved by removing some accounting

£45 £9 1.5

11

treatments permitted under full IFRSs, eliminating topics and disclosure requirements that are not generally relevant to SMEs and simplifying requirements for recognition and measurement, Here in the UK, the ASB has indicated that it is likely to require the use of the IFRS for SMEs for large and medium-sized private entities - meaning that more companies than ever will be required to bid farewell to UK GAAP and adopt international standards. It is likely that full implementation will take place after a transition period running from 2010 to 2012. This course provides an overview of the content of the IFRS for SMEs. Learning outcomes: By the end of this course you will obtain a greater understanding of:

• which entities can use the IFRS for SMEs • what adopting the IFRS for SMEs means for a UK company • who previously followed the FRSSE or full UK GAAP • which topics are excluded • which topics have been simplified • what disclosures are required.

12

Law and tax matters

Course Content and outcomes Price VAT CPD hours

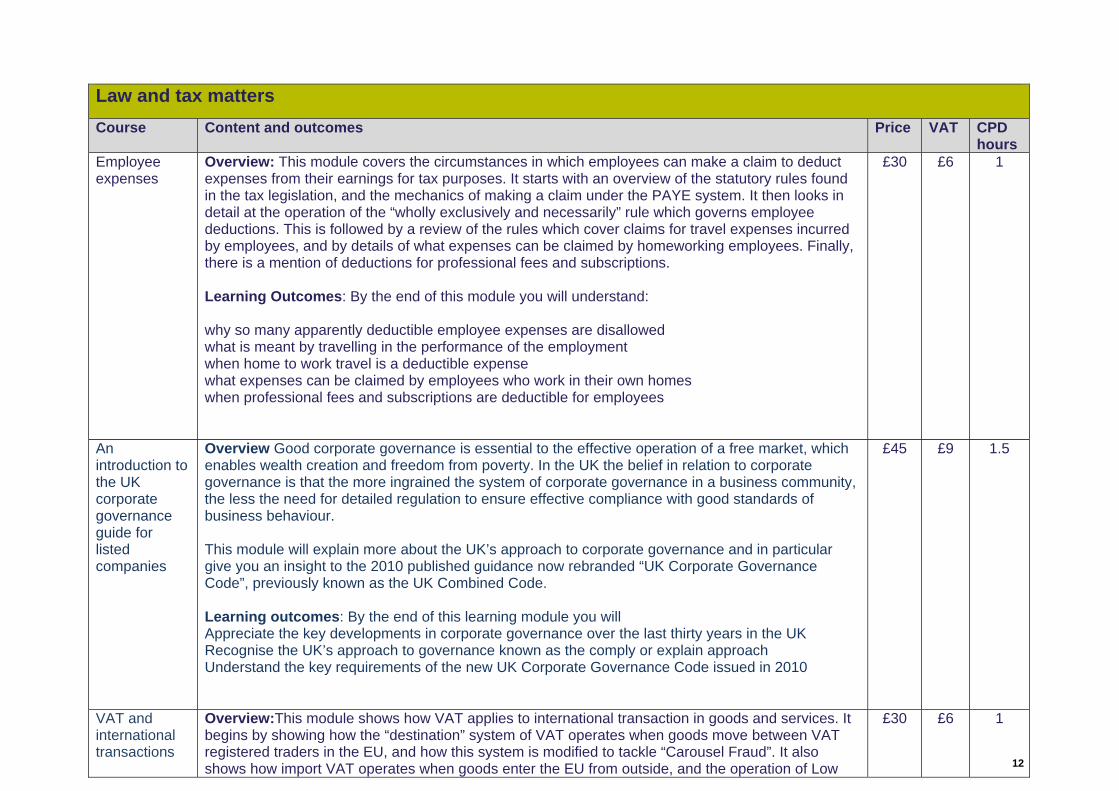

Employee expenses

Overview: This module covers the circumstances in which employees can make a claim to deduct expenses from their earnings for tax purposes. It starts with an overview of the statutory rules found in the tax legislation, and the mechanics of making a claim under the PAYE system. It then looks in detail at the operation of the “wholly exclusively and necessarily” rule which governs employee deductions. This is followed by a review of the rules which cover claims for travel expenses incurred by employees, and by details of what expenses can be claimed by homeworking employees. Finally, there is a mention of deductions for professional fees and subscriptions. Learning Outcomes: By the end of this module you will understand: why so many apparently deductible employee expenses are disallowed what is meant by travelling in the performance of the employment when home to work travel is a deductible expense what expenses can be claimed by employees who work in their own homes when professional fees and subscriptions are deductible for employees

£30 £6 1

An introduction to the UK corporate governance guide for listed companies

Overview Good corporate governance is essential to the effective operation of a free market, which enables wealth creation and freedom from poverty. In the UK the belief in relation to corporate governance is that the more ingrained the system of corporate governance in a business community, the less the need for detailed regulation to ensure effective compliance with good standards of business behaviour. This module will explain more about the UK’s approach to corporate governance and in particular give you an insight to the 2010 published guidance now rebranded “UK Corporate Governance Code”, previously known as the UK Combined Code. Learning outcomes: By the end of this learning module you will Appreciate the key developments in corporate governance over the last thirty years in the UK Recognise the UK’s approach to governance known as the comply or explain approach Understand the key requirements of the new UK Corporate Governance Code issued in 2010

£45 £9 1.5

VAT and international transactions

Overview:This module shows how VAT applies to international transaction in goods and services. It begins by showing how the “destination” system of VAT operates when goods move between VAT registered traders in the EU, and how this system is modified to tackle “Carousel Fraud”. It also shows how import VAT operates when goods enter the EU from outside, and the operation of Low

£30 £6 1

13

Value Consignment Relief. It then shows how the rules apply to cross border supplies of services both before and after the changes which came into force on 1 January 2010 and 2011. Finally, the rules on claiming refunds of “out of state” VAT are covered. Learning outcomes: By the end of this module you will understand: how VAT operates on cross border supplies of goods in the EU how the “reverse charge” is accounted for by the customer the measures taken by the UK government to counter carousel fraud how VAT applies to imports the rules on cross border supplies of services how refunds are claimed for “out of state” VAT

Corporation tax what an accountant needs to know - Loss relief, capital gains and groups

Overview: This module begins by covering the various claims a single company can make to obtain relief for trading losses. Where losses are carried forward, the restrictions resulting from a change in ownership are covered. The loss relief available where a company is a member of a group is dealt with next. The module then looks at corporation tax on chargeable gains, covering indexation allowance and roll over relief on the replacement of business assets, together with the substantial shareholding exemption. Finally, the ways in which membership of a group can impact on corporation tax on capital gains is dealt with. Learning outcomes: By the end of this module you will understand: How companies obtain relief for trading losses The effect of a change of ownership on the carry forward of losses When group relief can be claimed for losses The operation of corporation tax on capital gains The relief from tax on capital gains where business assets are replaced How to obtain the benefit of the substantial shareholding exemption How membership of a group can affect corporation tax on chargeable gains

£30 £6 1

Corporation tax what an accountant needs to know - Capital allowances

Overview: This module covers the calculation of capital allowances for corporation tax. It begins by reviewing the important distinction between buildings, plant fixed to buildings, and other plant. The module then covers the many recent changes in the rates of annual investment allowance, first year allowance and writing down allowance. The new extended period for short life assets treatment is dealt with, as is the effect of the recent change to a CO2 emissions basis for capital allowances on cars. Finally, the phasing out of industrial buildings and agricultural buildings allowance is covered. Learning outcomes: By the end of this module you will understand:

£30 £6 1

14

The distinction between plant and buildings The operation of the annual investment allowance The rules governing the first year allowance Writing down allowance rates, and how they are changing How higher allowances can be claimed on short life assets The new rules on capital allowances on cars How industrial buildings allowances have been withdrawn

Corporation tax what an accountant needs to know - Computation of profits

Overview: This module covers the computation of profits for corporation tax purposes. It starts by showing how profits may need to be adjusted to comply with the “wholly and exclusively” rule and the prohibition on the deduction of capital expenditure. It then shows how the tax treatment of investment and property businesses differs from that of a trading business. The way in which companies deal with interest paid or received under the loan relationships rules is looked at, and the module concludes with a summary of the rules on intangible fixed assets. Learning outcomes: By the end of this module you will understand: The importance of accounting treatment on the computation of taxable profits The rules which may make expenses disallowable for tax purposes The importance of the distinction between capital and revenue expenditure How an investment business carried on by a company is taxed How property business carried on by a company is taxed The loan relationships rules and their impact on companies The treatment of Intangible fixed assets acquired before or after 1 April 2002

£30 £6 1

Corporation tax what an accountant needs to know - the basics

Overview: This module covers the basics of corporation tax. It begins by showing which types of body are liable to corporation tax and the question of when companies are resident in the UK. After looking at an outline computation, the rules governing the beginning and end of a corporation tax accounting period are considered. Next, the rates of corporation tax are reviewed, showing how the small profits rate operates. The effect of associated companies on entitlement to the small profits rate, where the rules have recently changed, is considered next. Finally, the module shows how filing of tax returns and payment of tax is governed by the rules of self assessment. Learning outcomes: By the end of this module you will understand: Which types of entity pay Corporation Tax The structure of an outline tax computation When accounting periods begin and end The importance of total and augmented profits in relation to CT rates The existing and new rules on associated companies The operation of corporation tax self assessment

£30 £6 1

15

Compliance with anti-money laundering requirements

Overview: The following compliance presentation looks at anti-money laundering requirements. It will introduce anti-money laundering requirements and explain how it will affect you. Learning outcomes: By the end of this course you will be able to: • define what money laundering is • understand the legislation and how to apply it in practice • apply and understand CDD • report any money laundering activity through the correct channels.

£30 £6 1

Directors duties under the CA 2006

Overview: This course takes a detailed look at the statutory directors’ duties under the Companies Act 2006 and gives practical guidance on compliance with them. This course would benefit anyone engaged with managing or advising companies. Learning outcomes: By the end of this presentation, delegates will gain:

• an overview of the statutory directors’ duties regime and its interaction with fiduciary and common law duties

• an understanding of how the seven statutory duties apply including practical guidance and best practice tips on compliance; in particular, the course will take a detailed look at:

o the practical implications of the S.172 duty to promote the success of the company o the S.175 duty to avoid situational conflicts and the new independent board

authorisation exemption.

£30 £6 1

Generation hangover

Overview: Recent research has found that 77% of employers believe alcohol is the biggest threat to employee well being. A survey by Knowledge Union Health Care showed that 33% of employees admitted to going to work with a hangover. This course looks to identify the impact of alcohol in the workplace and what are some of the issues faced by both the employee and employer. Learning outcomes: By the end of this module you will: • understand the impact on employers, and the legal implications for employers, of such use • recognise the signs of alcohol and drug misuse in the workplace • be aware of the different courses of action an employer may take to address the problem.

£30 £6 1

Generation Facebook

Overview: The social networking revolution. Indications are that the fastest growing membership to social networking sites is amongst the workforce population. With the ease of accessibility to the internet in the workplace, this growth has had a considerable impact on behaviour of employees. The opportunities to now be online and socialising, rather than online and working, are at their highest, and the phenomenon does not look set to slow. This course considers not only the negative, but also the positive impacts of social networking technology for employers, the rights of employees, and how these 21st Century workplace issues can be managed.

£30 £6 1

16

Learning outcomes: By the end of this learning module you will be able to: • understand the terminology associated with social networking • consider the legal background applicable to the use of such technology in the workplace • understand the risks in the workplace from use and misuse of social networking • gain practical hints for dealing with problems caused by the use of social networking by

employees.

Introduction to Sarbanes Oxley

Overview: The Sarbanes Oxley Act was introduced in 2002 in response to many corporate scandals in the U.S.A. Since then many U.S. listed companies, including their overseas subsidiaries, have taken action to ensure that they are compliant with the relevant provisions in the legislation. This one hour e-learning course will give you an insight into the Sarbanes Oxley Act providing you with an appreciation of why it has emerged, the key provisions and the key practical areas that companies need to appreciate to ensure compliance. Learning outcomes: By the end of this learning module you will: • understand the drivers and rationale for the act • appreciate the key provisions of the act • recognise the jargon • appreciate the key issues to consider when implementing practically.

£30 £6 1

Employment law basics

Overview: The aim of this presentation is to introduce delegates to some of the basic elements, practices and procedures within employment law and to provide foundation knowledge of the subject. Learning outcomes: By the end of this presentation, delegates will understand the following: • sources of employment law • forum for resolving employment dispute • dispute resolutions procedures within employment law • employment tribunal rules of procedure • methods of settling claims.

£30 £6 1

17

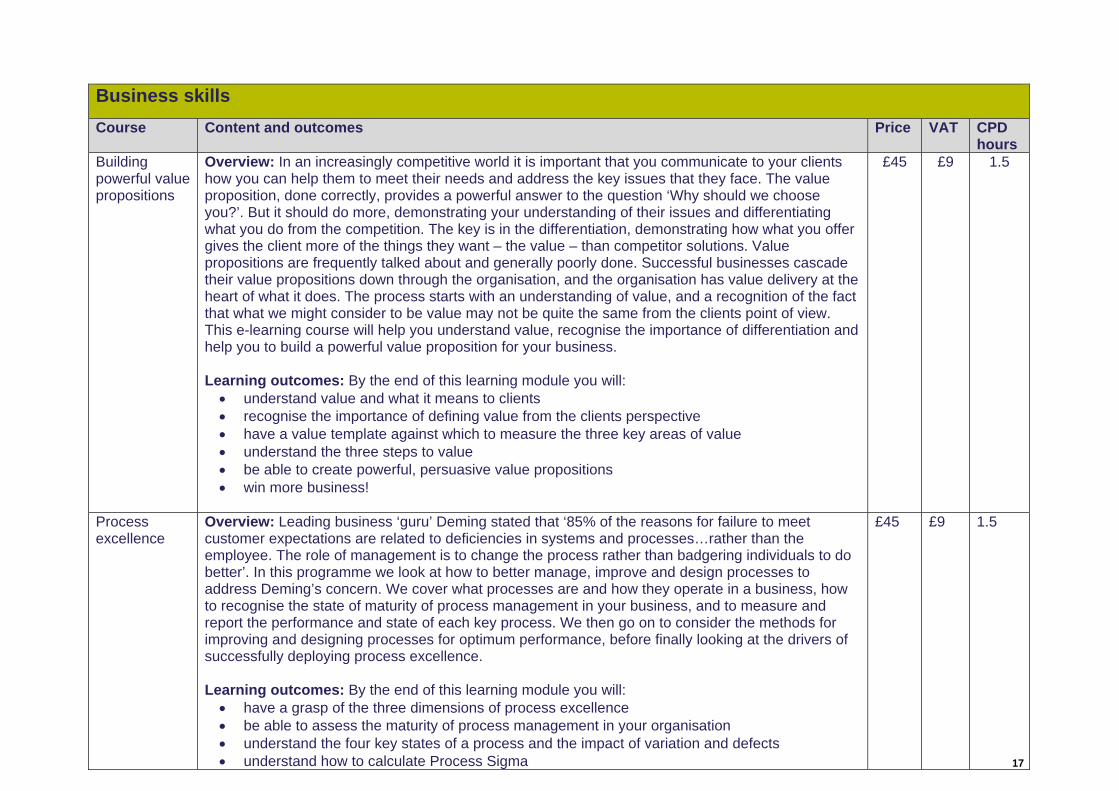

Business skills

Course Content and outcomes Price VAT CPD hours

Building powerful value propositions

Overview: In an increasingly competitive world it is important that you communicate to your clients how you can help them to meet their needs and address the key issues that they face. The value proposition, done correctly, provides a powerful answer to the question ‘Why should we choose you?’. But it should do more, demonstrating your understanding of their issues and differentiating what you do from the competition. The key is in the differentiation, demonstrating how what you offer gives the client more of the things they want – the value – than competitor solutions. Value propositions are frequently talked about and generally poorly done. Successful businesses cascade their value propositions down through the organisation, and the organisation has value delivery at the heart of what it does. The process starts with an understanding of value, and a recognition of the fact that what we might consider to be value may not be quite the same from the clients point of view. This e-learning course will help you understand value, recognise the importance of differentiation and help you to build a powerful value proposition for your business. Learning outcomes: By the end of this learning module you will: • understand value and what it means to clients • recognise the importance of defining value from the clients perspective • have a value template against which to measure the three key areas of value • understand the three steps to value • be able to create powerful, persuasive value propositions • win more business!

£45 £9 1.5

Process excellence

Overview: Leading business ‘guru’ Deming stated that ‘85% of the reasons for failure to meet customer expectations are related to deficiencies in systems and processes…rather than the employee. The role of management is to change the process rather than badgering individuals to do better’. In this programme we look at how to better manage, improve and design processes to address Deming’s concern. We cover what processes are and how they operate in a business, how to recognise the state of maturity of process management in your business, and to measure and report the performance and state of each key process. We then go on to consider the methods for improving and designing processes for optimum performance, before finally looking at the drivers of successfully deploying process excellence. Learning outcomes: By the end of this learning module you will: • have a grasp of the three dimensions of process excellence • be able to assess the maturity of process management in your organisation • understand the four key states of a process and the impact of variation and defects • understand how to calculate Process Sigma

£45 £9 1.5

18

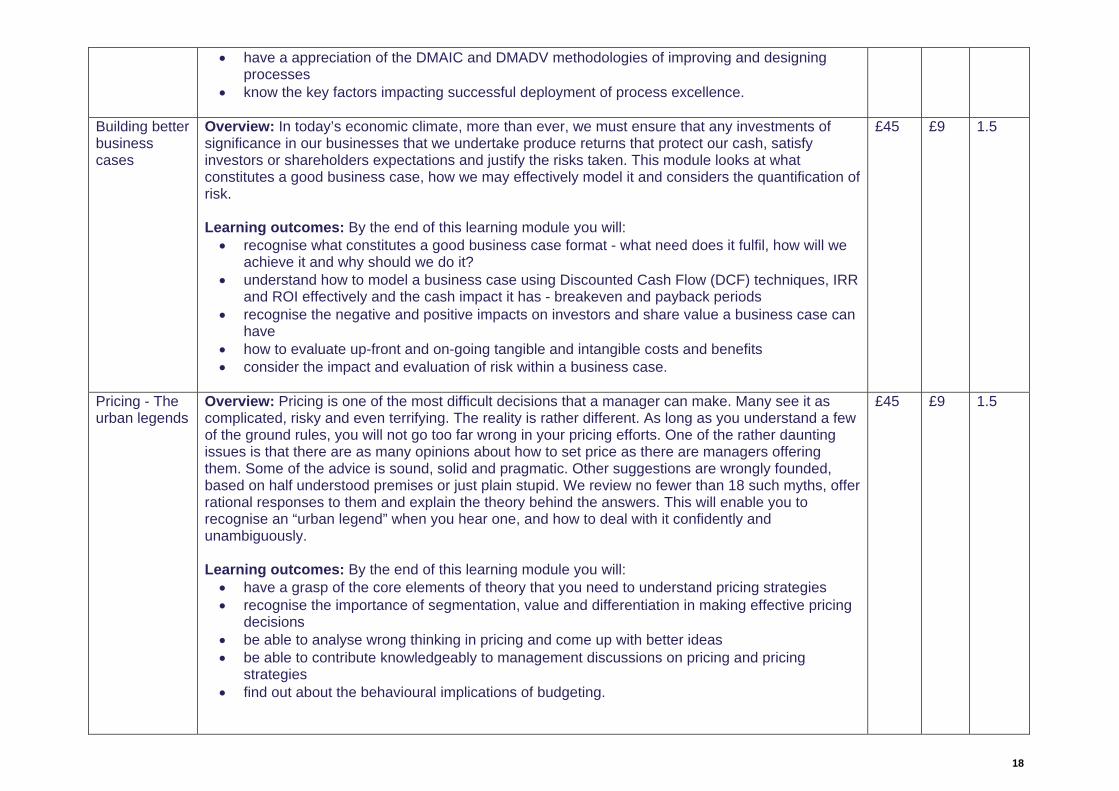

• have a appreciation of the DMAIC and DMADV methodologies of improving and designing processes

• know the key factors impacting successful deployment of process excellence.

Building better business cases

Overview: In today’s economic climate, more than ever, we must ensure that any investments of significance in our businesses that we undertake produce returns that protect our cash, satisfy investors or shareholders expectations and justify the risks taken. This module looks at what constitutes a good business case, how we may effectively model it and considers the quantification of risk. Learning outcomes: By the end of this learning module you will: • recognise what constitutes a good business case format - what need does it fulfil, how will we

achieve it and why should we do it? • understand how to model a business case using Discounted Cash Flow (DCF) techniques, IRR

and ROI effectively and the cash impact it has - breakeven and payback periods • recognise the negative and positive impacts on investors and share value a business case can

have • how to evaluate up-front and on-going tangible and intangible costs and benefits • consider the impact and evaluation of risk within a business case.

£45 £9 1.5

Pricing - The urban legends

Overview: Pricing is one of the most difficult decisions that a manager can make. Many see it as complicated, risky and even terrifying. The reality is rather different. As long as you understand a few of the ground rules, you will not go too far wrong in your pricing efforts. One of the rather daunting issues is that there are as many opinions about how to set price as there are managers offering them. Some of the advice is sound, solid and pragmatic. Other suggestions are wrongly founded, based on half understood premises or just plain stupid. We review no fewer than 18 such myths, offer rational responses to them and explain the theory behind the answers. This will enable you to recognise an “urban legend” when you hear one, and how to deal with it confidently and unambiguously. Learning outcomes: By the end of this learning module you will: • have a grasp of the core elements of theory that you need to understand pricing strategies • recognise the importance of segmentation, value and differentiation in making effective pricing

decisions • be able to analyse wrong thinking in pricing and come up with better ideas • be able to contribute knowledgeably to management discussions on pricing and pricing

strategies • find out about the behavioural implications of budgeting.

£45 £9 1.5

19

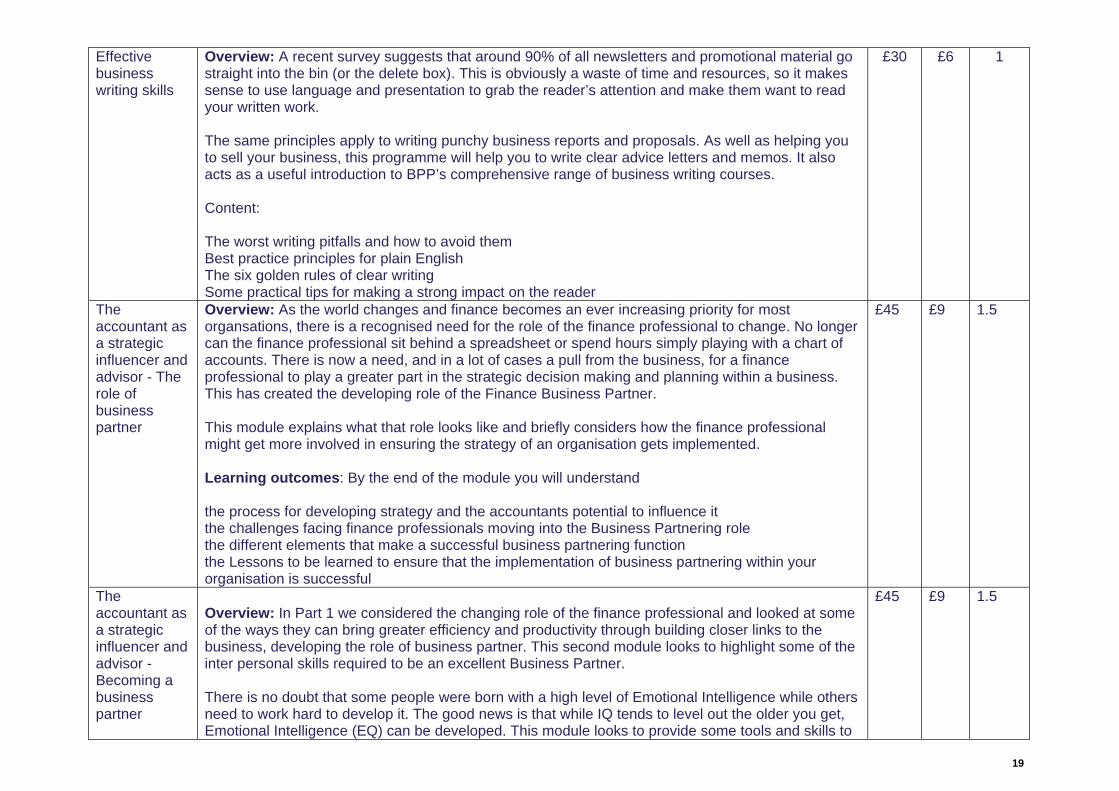

Effective business writing skills

Overview: A recent survey suggests that around 90% of all newsletters and promotional material go straight into the bin (or the delete box). This is obviously a waste of time and resources, so it makes sense to use language and presentation to grab the reader’s attention and make them want to read your written work. The same principles apply to writing punchy business reports and proposals. As well as helping you to sell your business, this programme will help you to write clear advice letters and memos. It also acts as a useful introduction to BPP’s comprehensive range of business writing courses. Content: The worst writing pitfalls and how to avoid them Best practice principles for plain English The six golden rules of clear writing Some practical tips for making a strong impact on the reader

£30 £6 1

The accountant as a strategic influencer and advisor - The role of business partner

Overview: As the world changes and finance becomes an ever increasing priority for most organsations, there is a recognised need for the role of the finance professional to change. No longer can the finance professional sit behind a spreadsheet or spend hours simply playing with a chart of accounts. There is now a need, and in a lot of cases a pull from the business, for a finance professional to play a greater part in the strategic decision making and planning within a business. This has created the developing role of the Finance Business Partner. This module explains what that role looks like and briefly considers how the finance professional might get more involved in ensuring the strategy of an organisation gets implemented. Learning outcomes: By the end of the module you will understand the process for developing strategy and the accountants potential to influence it the challenges facing finance professionals moving into the Business Partnering role the different elements that make a successful business partnering function the Lessons to be learned to ensure that the implementation of business partnering within your organisation is successful

£45 £9 1.5

The accountant as a strategic influencer and advisor - Becoming a business partner

Overview: In Part 1 we considered the changing role of the finance professional and looked at some of the ways they can bring greater efficiency and productivity through building closer links to the business, developing the role of business partner. This second module looks to highlight some of the inter personal skills required to be an excellent Business Partner. There is no doubt that some people were born with a high level of Emotional Intelligence while others need to work hard to develop it. The good news is that while IQ tends to level out the older you get, Emotional Intelligence (EQ) can be developed. This module looks to provide some tools and skills to

£45 £9 1.5

20

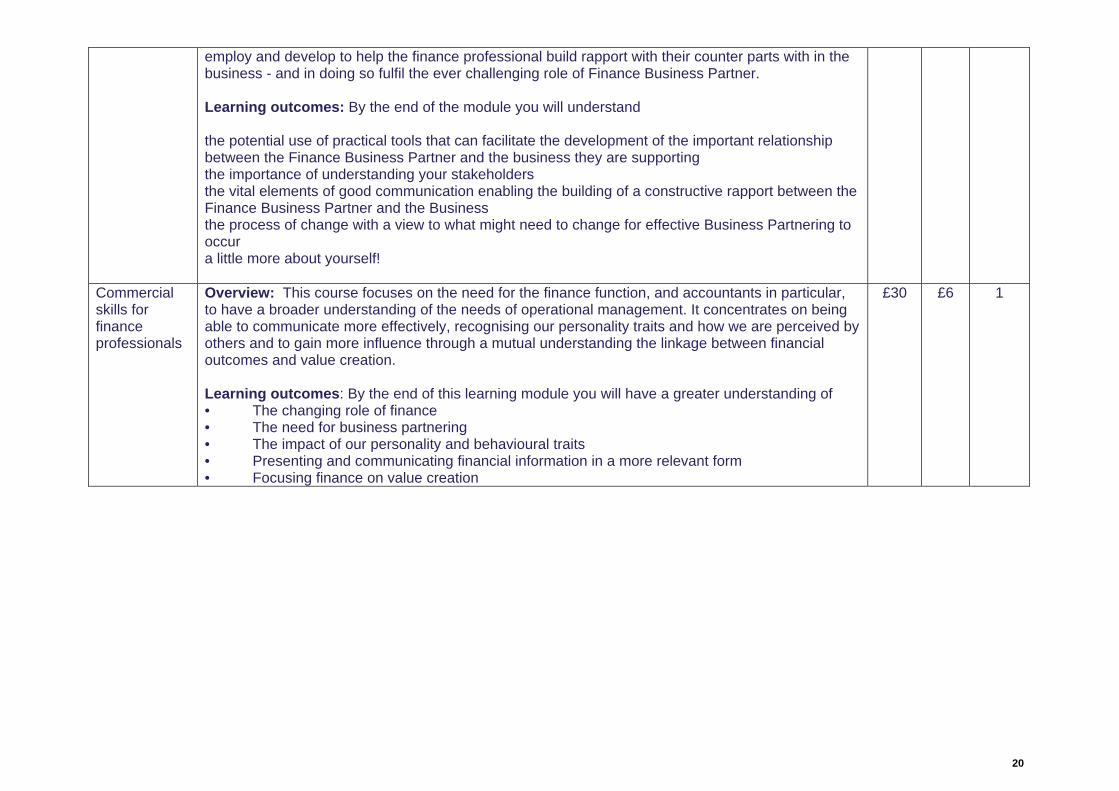

employ and develop to help the finance professional build rapport with their counter parts with in the business - and in doing so fulfil the ever challenging role of Finance Business Partner. Learning outcomes: By the end of the module you will understand the potential use of practical tools that can facilitate the development of the important relationship between the Finance Business Partner and the business they are supporting the importance of understanding your stakeholders the vital elements of good communication enabling the building of a constructive rapport between the Finance Business Partner and the Business the process of change with a view to what might need to change for effective Business Partnering to occur a little more about yourself!

Commercial skills for finance professionals

Overview: This course focuses on the need for the finance function, and accountants in particular, to have a broader understanding of the needs of operational management. It concentrates on being able to communicate more effectively, recognising our personality traits and how we are perceived by others and to gain more influence through a mutual understanding the linkage between financial outcomes and value creation. Learning outcomes: By the end of this learning module you will have a greater understanding of • The changing role of finance • The need for business partnering • The impact of our personality and behavioural traits • Presenting and communicating financial information in a more relevant form • Focusing finance on value creation

£30 £6 1

21

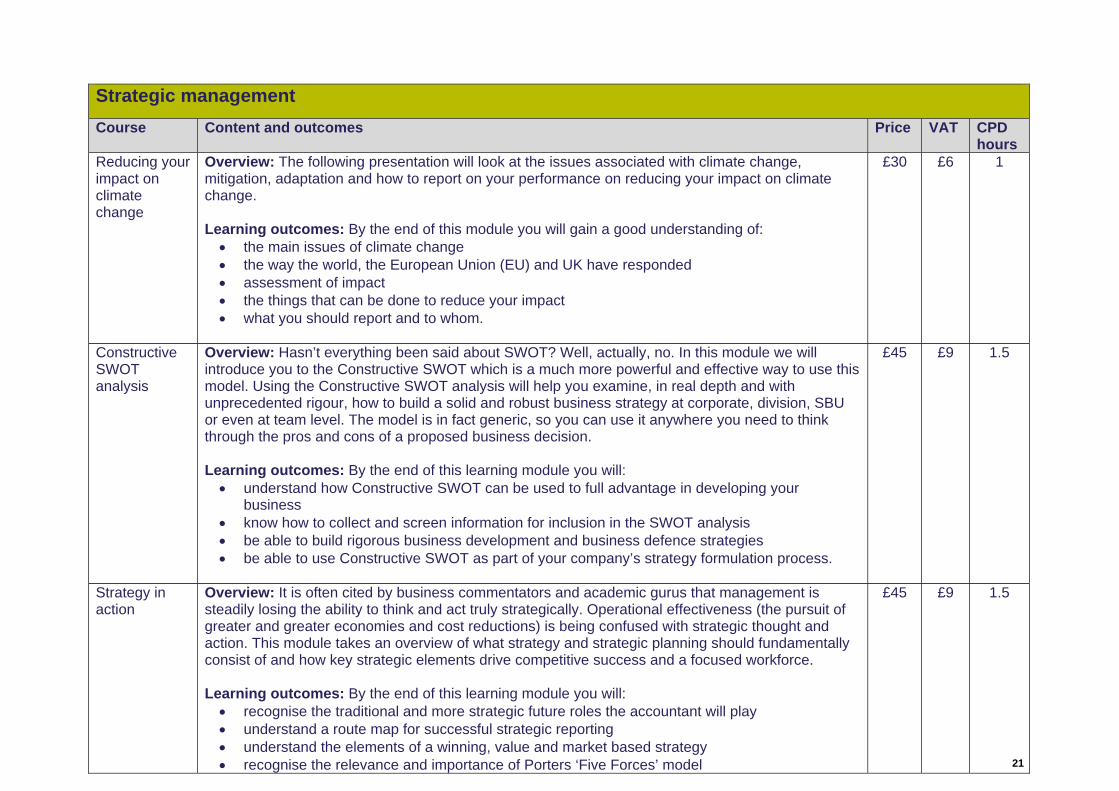

Strategic management

Course Content and outcomes Price VAT CPD hours

Reducing your impact on climate change

Overview: The following presentation will look at the issues associated with climate change, mitigation, adaptation and how to report on your performance on reducing your impact on climate change. Learning outcomes: By the end of this module you will gain a good understanding of: • the main issues of climate change • the way the world, the European Union (EU) and UK have responded • assessment of impact • the things that can be done to reduce your impact • what you should report and to whom.

£30 £6 1

Constructive SWOT analysis

Overview: Hasn’t everything been said about SWOT? Well, actually, no. In this module we will introduce you to the Constructive SWOT which is a much more powerful and effective way to use this model. Using the Constructive SWOT analysis will help you examine, in real depth and with unprecedented rigour, how to build a solid and robust business strategy at corporate, division, SBU or even at team level. The model is in fact generic, so you can use it anywhere you need to think through the pros and cons of a proposed business decision. Learning outcomes: By the end of this learning module you will: • understand how Constructive SWOT can be used to full advantage in developing your

business • know how to collect and screen information for inclusion in the SWOT analysis • be able to build rigorous business development and business defence strategies • be able to use Constructive SWOT as part of your company’s strategy formulation process.

£45 £9 1.5

Strategy in action

Overview: It is often cited by business commentators and academic gurus that management is steadily losing the ability to think and act truly strategically. Operational effectiveness (the pursuit of greater and greater economies and cost reductions) is being confused with strategic thought and action. This module takes an overview of what strategy and strategic planning should fundamentally consist of and how key strategic elements drive competitive success and a focused workforce. Learning outcomes: By the end of this learning module you will: • recognise the traditional and more strategic future roles the accountant will play • understand a route map for successful strategic reporting • understand the elements of a winning, value and market based strategy • recognise the relevance and importance of Porters ‘Five Forces’ model

£45 £9 1.5

22

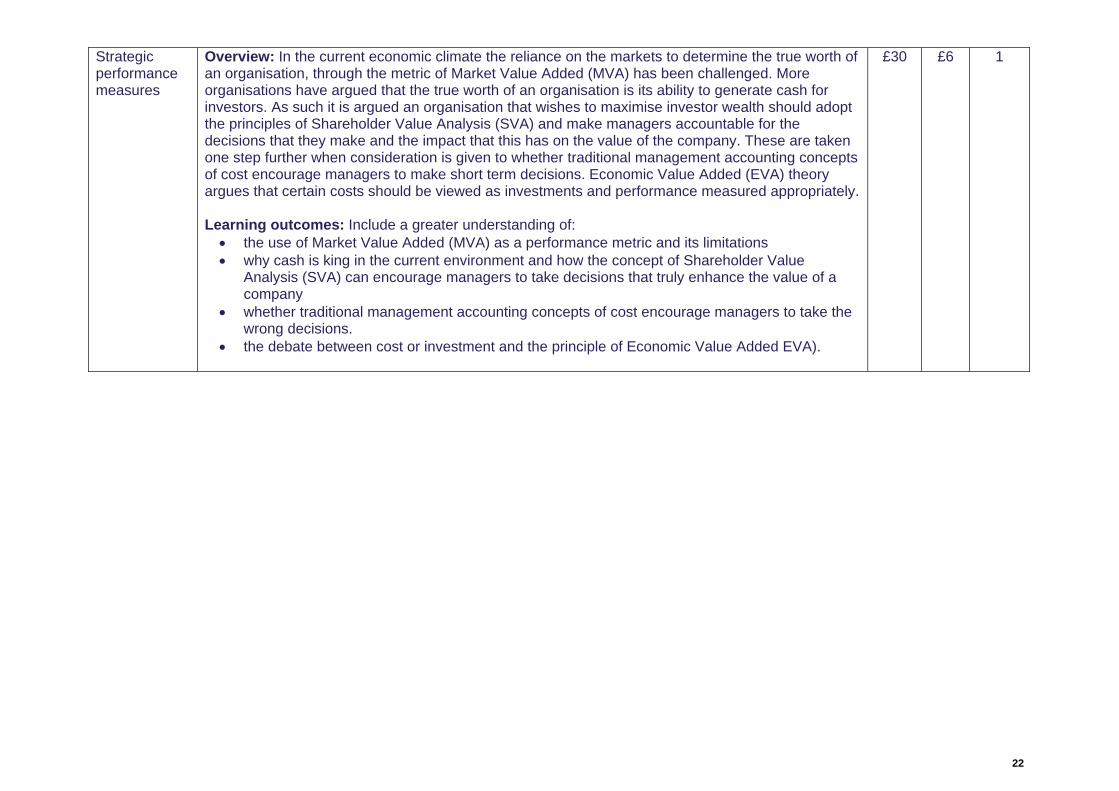

Strategic performance measures

Overview: In the current economic climate the reliance on the markets to determine the true worth of an organisation, through the metric of Market Value Added (MVA) has been challenged. More organisations have argued that the true worth of an organisation is its ability to generate cash for investors. As such it is argued an organisation that wishes to maximise investor wealth should adopt the principles of Shareholder Value Analysis (SVA) and make managers accountable for the decisions that they make and the impact that this has on the value of the company. These are taken one step further when consideration is given to whether traditional management accounting concepts of cost encourage managers to make short term decisions. Economic Value Added (EVA) theory argues that certain costs should be viewed as investments and performance measured appropriately. Learning outcomes: Include a greater understanding of: • the use of Market Value Added (MVA) as a performance metric and its limitations • why cash is king in the current environment and how the concept of Shareholder Value

Analysis (SVA) can encourage managers to take decisions that truly enhance the value of a company

• whether traditional management accounting concepts of cost encourage managers to take the wrong decisions.

• the debate between cost or investment and the principle of Economic Value Added EVA).

£30 £6 1

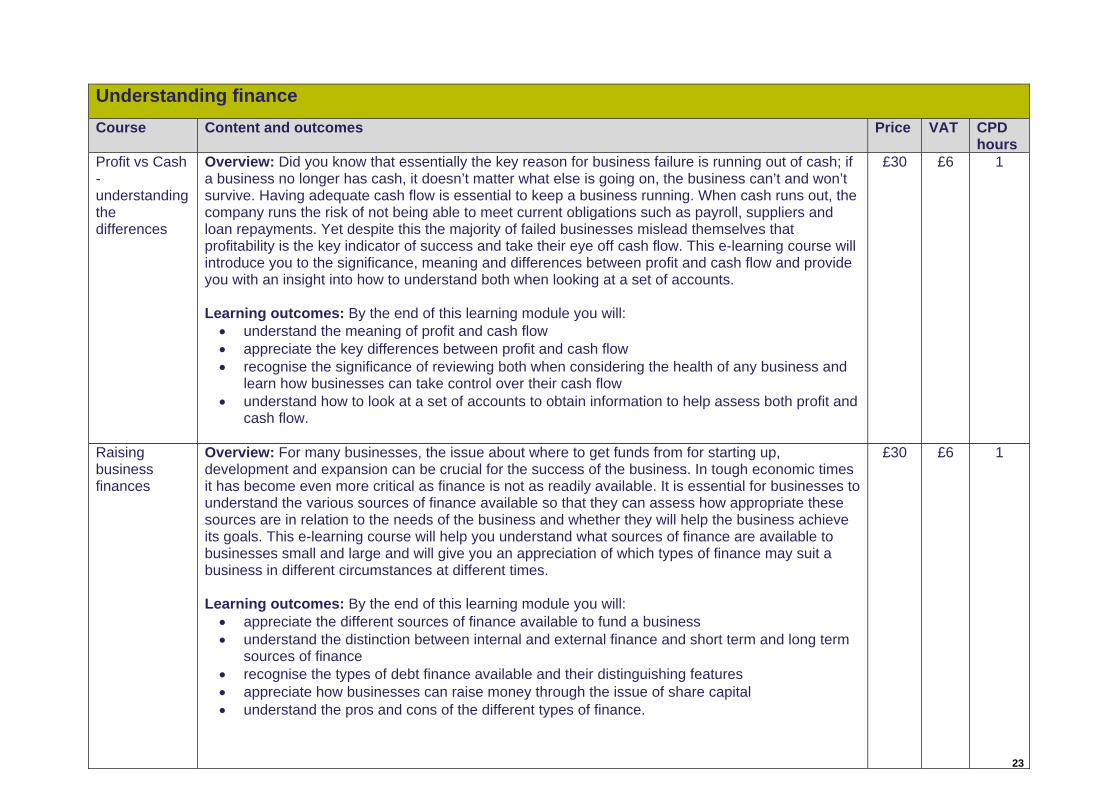

23

Understanding finance Course Content and outcomes Price VAT CPD

hours Profit vs Cash - understanding the differences

Overview: Did you know that essentially the key reason for business failure is running out of cash; if a business no longer has cash, it doesn’t matter what else is going on, the business can’t and won’t survive. Having adequate cash flow is essential to keep a business running. When cash runs out, the company runs the risk of not being able to meet current obligations such as payroll, suppliers and loan repayments. Yet despite this the majority of failed businesses mislead themselves that profitability is the key indicator of success and take their eye off cash flow. This e-learning course will introduce you to the significance, meaning and differences between profit and cash flow and provide you with an insight into how to understand both when looking at a set of accounts. Learning outcomes: By the end of this learning module you will: • understand the meaning of profit and cash flow • appreciate the key differences between profit and cash flow • recognise the significance of reviewing both when considering the health of any business and

learn how businesses can take control over their cash flow • understand how to look at a set of accounts to obtain information to help assess both profit and

cash flow.

£30 £6 1

Raising business finances

Overview: For many businesses, the issue about where to get funds from for starting up, development and expansion can be crucial for the success of the business. In tough economic times it has become even more critical as finance is not as readily available. It is essential for businesses to understand the various sources of finance available so that they can assess how appropriate these sources are in relation to the needs of the business and whether they will help the business achieve its goals. This e-learning course will help you understand what sources of finance are available to businesses small and large and will give you an appreciation of which types of finance may suit a business in different circumstances at different times. Learning outcomes: By the end of this learning module you will: • appreciate the different sources of finance available to fund a business • understand the distinction between internal and external finance and short term and long term

sources of finance • recognise the types of debt finance available and their distinguishing features • appreciate how businesses can raise money through the issue of share capital • understand the pros and cons of the different types of finance.

£30 £6 1

24

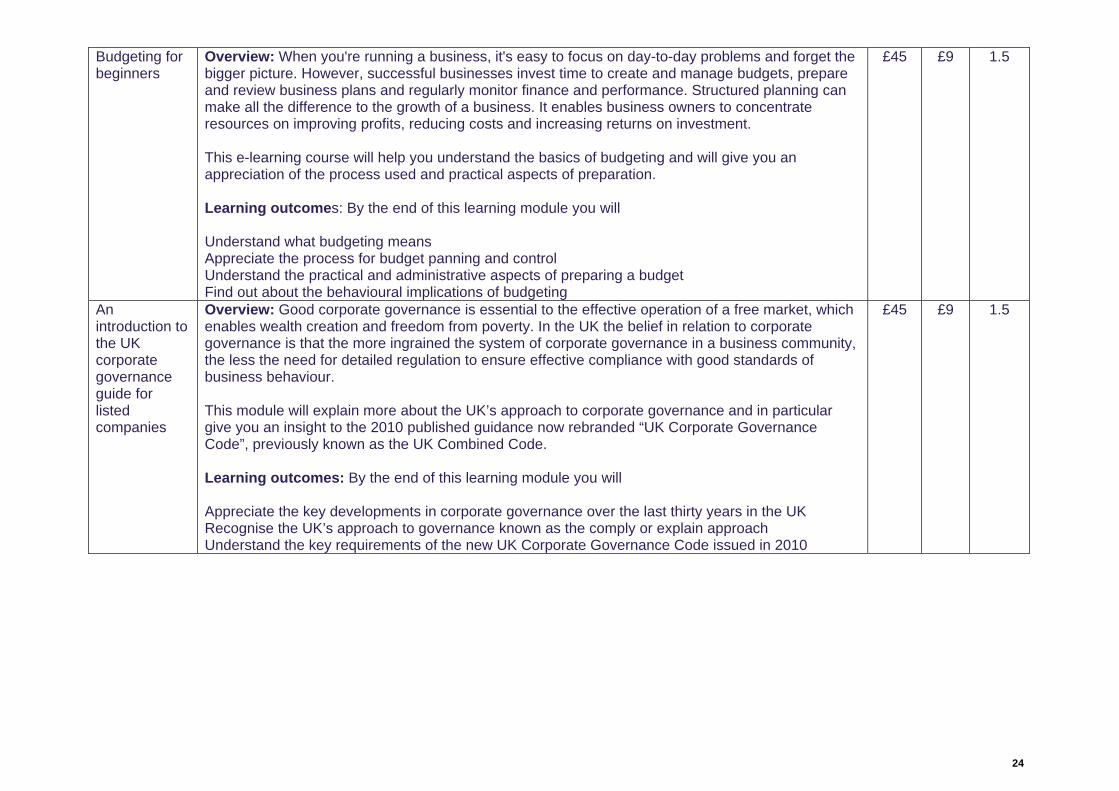

Budgeting for beginners

Overview: When you're running a business, it's easy to focus on day-to-day problems and forget the bigger picture. However, successful businesses invest time to create and manage budgets, prepare and review business plans and regularly monitor finance and performance. Structured planning can make all the difference to the growth of a business. It enables business owners to concentrate resources on improving profits, reducing costs and increasing returns on investment. This e-learning course will help you understand the basics of budgeting and will give you an appreciation of the process used and practical aspects of preparation. Learning outcomes: By the end of this learning module you will Understand what budgeting means Appreciate the process for budget panning and control Understand the practical and administrative aspects of preparing a budget Find out about the behavioural implications of budgeting

£45 £9 1.5

An introduction to the UK corporate governance guide for listed companies

Overview: Good corporate governance is essential to the effective operation of a free market, which enables wealth creation and freedom from poverty. In the UK the belief in relation to corporate governance is that the more ingrained the system of corporate governance in a business community, the less the need for detailed regulation to ensure effective compliance with good standards of business behaviour. This module will explain more about the UK’s approach to corporate governance and in particular give you an insight to the 2010 published guidance now rebranded “UK Corporate Governance Code”, previously known as the UK Combined Code. Learning outcomes: By the end of this learning module you will Appreciate the key developments in corporate governance over the last thirty years in the UK Recognise the UK’s approach to governance known as the comply or explain approach Understand the key requirements of the new UK Corporate Governance Code issued in 2010

£45 £9 1.5

25

Working capital management

Overview: Every business needs adequate liquid resources in order to maintain day-to-day cash flow. It needs enough cash to pay wages and salaries as they fall due and to pay creditors if it is to keep its workforce and ensure its supplies. Maintaining adequate working capital is not just important in the short-term. Sufficient liquidity must be maintained in order to ensure the survival of the business in the long-term as well. Even a profitable business may fail if it doesn’t have adequate cash flow to meet its liabilities as they fall due . Learning outcomes: By the end of this learning module you will Understand the meaning of working capital Appreciate what Working capital management relates to Learn about some key liquidity ratios used to understand more about a business’ working capital position Understand various techniques used to manage working capital

£45 £9 1.5

![CIMA C1 Quiz Wk 8 2012 [Read-Only]](https://img.pdfslide.us/doc/110x75/563db87c550346aa9a942427/cima-c1-quiz-wk-8-2012-read-only.jpg)