Embed Size (px)

Citation preview

CIMA BA1: BA1 Fundamentals of Business Economics

Module: 02

Stakeholders and Stakeholders’ Wealth

15

STAKEHOLDERS

1. Stakeholders

Do you have shares in Google? Well, you might have, but you probably don't!

That means you are not a shareholder and as such you do not stand to gain

financially from Google's business activities.

However, you still have an interest, or a stake, in how they do. This is

because you use the service every day. If Google went out of business, it

would make your life more difficult as you'd have to find another source for all

those services of theirs you use. This makes you, as a customer, a

stakeholder in Google.

The best way to think of a profit seeking organisation is to think of its

primary responsibility as being to maximise wealth for its shareholders e.g.

provide them with the largest income that they can. However, though the shareholders are the primary focus, there are still a number of groups

which have an interest in how an organisation operates. These groups

are called stakeholders.

Stakeholders can affect, or be affected by, an organisation's strategy and

policies. Therefore, it is important for all organisations to understand

their stakeholders and the stakeholders’ interests. General examples of

stakeholders include: customers, employees, suppliers, creditors,

debtors, the community, government and unions.

OK, let’s have a quick check that we’re with it so far …

Example

Which of the following would not be a stakeholder for a state provided

school?

a) Pupils

b) Teachers

c) Parents

d) Shareholders

Answer

d) shareholders – a school provided by the state would not have

shareholders. It’s owned and provided by the state.

Pupils, teachers and parents would all be affected by, and can affect, the

decisions being made by the school. They are therefore, all stakeholders of

the school.

16

Example

Which of the following are not stakeholders for a company?

a) Shareholders

b) Employees

c) Customers

d) Those living in the surrounding area

Answer

It's a bit of a trick this one... The company’s activities could affect all these people:

Shareholders – by affecting the level of profit that they receive in dividends

Employees – any decisions regarding roles, hours, salaries, bonuses etc. will

affect employees

Customers – will be affected by any decisions regarding availability of

products, pricing, provision of customer support etc.

Those living in the surrounding area – affected by decisions regarding time

and number of any deliveries, any expansion plans, parking arrangements for

staff e.g. poor provision could lead to congestion in an area etc.

… and therefore, they are all stakeholders.

Each stakeholder will exert a different level of influence over how an

organisation operates. This influence can be positive (either by supporting

or contributing to the organisation), or negative (which would be blocking or

opposing).

17

2. Classifying stakeholders

To make informed decisions and policies regarding all the business's

stakeholders, it is crucial that an organisation classifies its stakeholders

into various groups. This can be done in a number of ways; to begin with,

the organisation can determine whether the stakeholder is internal,

external or connected.

Internal stakeholders

What sort of influence would these different stakeholders have? Well that is

related to their own objectives – let's take a look at the objectives of a

variety of different stakeholders:

Let’s take a look at an example:

18

Example

ABC Ltd runs a bonus scheme for its managers based on profits. The

directors have decided that the company’s focus should be growth in order to

remain competitive. If the directors take the needs of all stakeholders into

consideration, what would be the best approach for achieving this objective?

a) Ignore the managers’ bonus scheme and focus on growth

b) Construct the objective to ensure both profitability and growth is

achieved

c) Look to remove the bonus scheme

Answer

b) - This will satisfy both objectives and ensure that the managers’ needs as

stakeholders are being addressed. This scenario demonstrates how

stakeholders influence company decision making.

Why not a) – This ignores the manager’s needs as stakeholders and c) -

again, if the bonus scheme is something that the managers consider part of

their remuneration package (how they are paid), removing it will not be

taking their needs as stakeholders into consideration.

Connected stakeholders

Connected stakeholders are external to the business, but closely related –

usually with business relationships with the company.

The areas of concern for connected stakeholders are as follows:

19

Example

Which of the below are not a connected stakeholder for ABC Ltd?

a) Shareholders

b) Mr Smith, an entrepreneur who loaned the company £100,000

c) The company who provides internal fixtures and fittings for the

company’s outlets

d) Mrs Smith who buys the company’s products on a regular basis

e) Bob Jones who works in the local outlet

Answer

e) – Bob is an employee and therefore an internal stakeholder.

External stakeholders

External stakeholders cover any stakeholders of the business which do not

have close working relationships with the business.

The areas of concern from external stakeholders are as follows:

Example

ABC Ltd now decide to open a new depot, they have chosen a site which is

just beyond a residential estate. It is currently woodland. The company will

need to undergo an employment campaign. The area is strategically key for

transportation but has a reasonably high employment level. The company is

therefore thinking that they will have to offer higher wages than they currently

20

pay to existing staff amongst whom trade union representation is high. Which

external stakeholder groups will try to exert influence over the decision being

made by the company?

a) Environmental pressure groups

b) Residents of the nearby estate

c) Local and central government

d) Trade unions

e) All of the above

Answer

e) – all of the above.

Environmental pressure groups – due to the destruction of the woodland.

Residents – potential noise and light pollution and increased congestion but

also, employment opportunities.

Local and central government – adherence to all relevant laws e.g. planning,

employment and health and safety. Also, potentially due to the increase in

employment and tax revenue.

Trade Unions – potential conflict with existing terms of work for current staff.

Primary and secondary stakeholders

Stakeholders can also be defined in categories as primary and secondary.

Primary stakeholders

These are stakeholders which have a direct interest in the business

e.g. employees, investors, shareholders, customers and suppliers. They are

the internal and connected stakeholders.

Secondary stakeholders

These are therefore, unsurprisingly, those with an indirect interest in the

business e.g. pressure groups, local community, governments. They are the

external stakeholders.

21

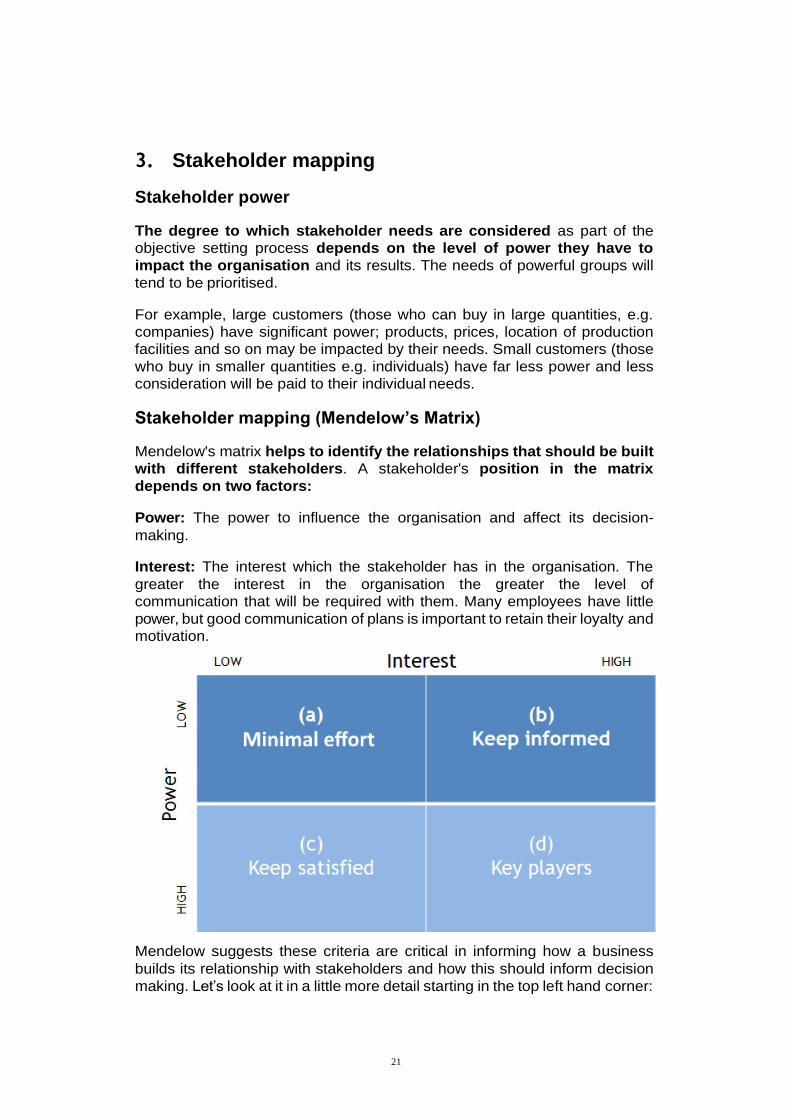

3. Stakeholder mapping

Stakeholder power

The degree to which stakeholder needs are considered as part of the

objective setting process depends on the level of power they have to

impact the organisation and its results. The needs of powerful groups will

tend to be prioritised.

For example, large customers (those who can buy in large quantities, e.g.

companies) have significant power; products, prices, location of production

facilities and so on may be impacted by their needs. Small customers (those

who buy in smaller quantities e.g. individuals) have far less power and less

consideration will be paid to their individual needs.

Stakeholder mapping (Mendelow’s Matrix)

Mendelow's matrix helps to identify the relationships that should be built

with different stakeholders. A stakeholder's position in the matrix

depends on two factors:

Power: The power to influence the organisation and affect its decision-

making.

Interest: The interest which the stakeholder has in the organisation. The

greater the interest in the organisation the greater the level of

communication that will be required with them. Many employees have little

power, but good communication of plans is important to retain their loyalty and

motivation.

Mendelow suggests these criteria are critical in informing how a business

builds its relationship with stakeholders and how this should inform decision

making. Let’s look at it in a little more detail starting in the top left hand corner:

22

a) Minimal effort

Stakeholders with a low level of interest and low power require the least

consideration when making business decisions. These stakeholders

should be monitored but require minimal effort.

For example, a small supplier hired intermittently for non-core supplies,

such as paper clips, or a temporary employee. Give them basic information to

meet their needs but pay little attention to them in decision making and

strategy.

b) Keep informed

Stakeholders with a high level of interest and low power need to be kept

informed when making business decisions. An example is the local

community, or community representatives. They have no great influence on

business decision making, but may influence other more powerful

stakeholder groups, by protesting or lobbying etc. A full-time employee

would be in a similar position with respect to power, but could join with

others, in say a union, if they felt they needed to increase power.

Therefore, they should be kept informed of relevant decisions and involved

in the decision-making process where necessary.

For example, if ABC Ltd want to go ahead with their new depot, they may

wish to hold community meetings, undergo outreach work and/or keep the

community informed about the details of this development through leafleting

and newsletters.

c) Keep satisfied

Stakeholders with a low level of interest and high power should be kept

satisfied during business decision making. Such groups may have no direct

interest but have the potential to move to (d) if the business activity

concerns or involves them e.g. relevant government departments.

Stakeholders in this sector should be monitored and provided with any

relevant information e.g. the tax authorities need to be provided with

necessary accounting information and receive any taxes due on time.

In our example, ABC Ltd may wish to consult with the government on health

and safety issues and ensure that they comply with regulations with respect

to their new depot, providing any necessary paperwork.

d) Key players

Stakeholders with a high level of interest and high power must be

consulted with throughout the decision-making process. (e.g. keep close).

For example, for a profit seeking, private sector organisation, key players

would be major shareholders. It is critical to keep this group informed and

involve them in decision making.

For example, conducting regular board meetings where shareholders views can influence decision making and updating shareholders regularly with

strategic plans.

23

Example

Polly's Purrfect Pets

Polly owns a small chain of five pet shops called Polly's Purrfect Pets. When

you place Polly's Purrfect Pets on Mendelow's matrix, it looks like this:

a) Minimal effort – An independent contractor who occasionally carries out

work. They have very little power and interest in the day to day running of

Polly's Purrfect Pets and little effort will be put into the relationship.

b) Keep informed – Polly's employees have a high interest as they rely on

Polly's for employment, but low power. Regular customers have a high

interest as they rely on Polly's for their pet supplies but again, low power.

Polly should inform them of any business decisions that may affect them.

This could be done via regular updates for employees and messages on

social media for regular customers.

c) Keep satisfied – In the UK, pet shop licences must be issued by the local

council. The local council will not have a high interest in Polly's, however, if

Polly's was found to be selling unsafe pet food then the council could revoke

the pet shop licence, which means they have high power. Therefore, Polly

should discuss any changes that may affect her licence with the council

before implementing them.

A major supplier of the leading cat food brand has high power as Polly's

would lose custom if they were to stop stocking the food. However, the cat

food brand has low interest in Polly's as this is a relatively small company.

Polly should ensure that the supplier's needs are always met, which is most

likely to mean always paying them promptly.

24

d) Key players – As shown above, it is possible for a “keep satisfied” to

become a “key player” under particular circumstances. Current key players

are Polly herself, Polly's brother who co-owns the company and a local cats

home who buy all of their cat food through a contract with Polly's. If the cats

home were to switch suppliers, then Polly's would lose a significant income.

Polly should keep a good working relationship with her brother and keep him

involved in business decisions. Polly should also keep the cats home

involved in any big decisions such as relocation, a change in suppliers or a

significant change in prices as this might affect them.

25

4. Stakeholder conflicts

Keeping on with our Purrfect Pets example, Polly (the owner) and her brother

have been having managerial discussions. Polly's brother is concerned that

they might be overstaffed in one of the shops. He is proposing to make one

full time employee redundant. The employees are all outraged. They don't

want to be the one who is made redundant and feel that with one less

employee the shop will be understaffed. This is a stakeholder conflict.

It is crucial that an organisation realises its stakeholders have different

sets of needs and expectations. These may result in conflict. It is critical

to understand the needs of varying stakeholders and to resolve conflicts

wherever possible.

Resolving stakeholder conflict

Cyert and March proposed four ways in which a company can look to resolve

stakeholder conflict:

Satisficing

This word, coined by Cyert and March, is a mash-up of "satisfying" and

"sacrificing". It means holding negotiations between key stakeholder groups and arriving at an accepted compromise. For example, Polly's brother and

the employees meet and decide to reduce all employees’ hours, instead of

making one of them redundant.

Sequential attention

This involves taking turns focusing on the needs of different stakeholder

groups. For example, the employee is not made redundant, but the

agreement is that next time redundancies need to be made, it will be from this

shop. The idea is that the needs of the employees are met this time, but

next time, a different stakeholder's needs will be met, namely Polly's brother.

Side payments

When a stakeholder's needs cannot be met initially, they are compensated

in some way as a compromise. For example, one employee is made

redundant, but is given a larger than expected redundancy package.

Exercise of power

When a compromise or action cannot be agreed upon it is resolved by a senior figure who exercises their power to force through a decision. For

example, Polly decides that the redundancy is the best option and pushes

through the decision.

26

5. Stakeholders and not for profit organisations

In a profit seeking organisation, the shareholders will be the key

stakeholders. However, in a not for profit organisation, other stakeholders will be more important. Due to the competing demands of a variety of

stakeholders, the organisation must manage expectations and balance

demands.

Example

White Valley local council, a not-for profit organisation, has a slogan,

“Understanding the needs of the community”. It decided that it should have a

new external market place. The only available site was a car park which also

included a small garden area with some benches. The impacts that this

decision would have on the local area include:

• Potential loss of trade for local shops due to new competition from the market traders.

• Potential increased trade for some local shops due to increased footfall caused by the new market.

• Less parking for shoppers which may affect footfall for all traders.

• Loss of a green space affecting the quality of life for those who used it.

• Increased trading opportunities for local trades people thereby increasing income, tax revenue etc.

• Congestion due to the new attraction bringing in increased numbers of shoppers and the presence of lorries and vans belonging to the

trades people on market day.

So, whose needs should take precedence?

How do we quantify all of these impacts in order to compare them? e.g. how

much extra congestion is offset by the increase in trade seen by some local

shop keepers? How do we put a value on quality of life; that lost relaxing

lunch spot?

The answer is that it's very hard and there is no right approach. That that is

the challenge in not-for-profit businesses – lots of stakeholders with different

needs all of whom are important. The goal should be to try to balance

everyone's needs as best possible realising that there will inevitably need to

be some compromise from most groups!

27

6. The agency problem

Margaret has bought shares in GP PLC, a retailer. She believes that they are

going to do well, make huge profits and therefore pay out large dividends,

which she can then use to pay for her holiday!

Sheila has just been made one of the Directors in the company. She is so

excited and has spent the morning walking around her office making a list of

all the things she will need to support her new-found status; large leather

chair, sturdy wooden desk, original artwork, large wool rug, coffee maker and

of course a personal assistant. When it comes to her strategy for the

business, as her bonus is based on sales, she's decided to raise prices,

spend money on a big marketing campaign and then have a big sale at the

end of the season!

Will Margaret be happy with Sheila’s spending and business strategy? Are

they working towards the same goals? The answer to both these questions is

of course – no!

This is another example of stakeholder conflict. Sometimes also known as

the principal – agent problem, it arises because we have the shareholders,

(Margaret) who are the principals or legal owners of the business, and they

are in charge of employing the management (e.g. directors, Sheila) – the 'agent'. So, the shareholders employ the directors to run the business on

their behalf.

28

Why does this cause a problem? Well, although the managers should be

running the business in the shareholders' interests - they have a

responsibility to do so (called a fiduciary duty), it is inevitable that their

own personal interests will be considered too. This conflict is the

agency problem. For instance, when it comes to deciding salaries, the

managers are going to be pushing for as high a salary as possible (because

this determines what they get in their pay packets to spend!), whilst the

shareholders will want to set appropriate salaries that don't incur enormous

costs for the business (because they want profits to be as high as possible to

increase the dividends that they receive).

There are a couple of other models which may help explain further why

those managing the company can have different motivations from owners

causing the agency problem:

Baumol’s theory of sales maximisation - Baumol was a consultant and as

part of his work he observed that management are often more concerned

with maximising sales as opposed to profit. Why? Well, because

bonuses are more likely to be related to sales rather than profits. In addition,

higher sales give the perception of company growth which looks good, helps

raise funds from banks, and secures more jobs. However, more sales do not

necessarily mean greater profits if costs are not controlled. Cue potentially

unhappy shareholders who ultimately want higher profits not sales.

Williamson's “Model of Managerial discretion” suggests that in satisfying

their own needs management may incur costs e.g. bonuses, elaborate

offices, or increasing staff levels so they are managing more people (more

people can be seen as more importance!). As long as profits are supporting

these costs they will have little motivation to improve company performance

beyond this.

One general cause of the agency problem is information asymmetry. What

does that mean? Well, it means that the information available to each

party isn’t equal. The directors will have more information about the

company available to them than the shareholders (see example below) and

as a result the shareholders are not always able to fully hold directors

accountable for decisions made.

For example, the Chief Executive Officer (in charge of running the company)

will have access to lots of internal information and specific data relating to the

performance of the company in their internal reports and systems.

Shareholders have only what is given to them by the directors – often just

the annual reports. They have a limited view of what's really going on and so

may find it hard to criticise the directors. Compare this with a football

manager – fans are easily able to hold the manager to account because the

results and performances can be seen every week on the pitch – there is far

less information asymmetry in football.

29

The agency problem in the non-profit sector

As discussed earlier, whilst these are not set up to maximise profits and will

probably not have shareholder owners, they can still suffer from a variant of

the agency problem. For example, in the public sector, some workers may

still be more concerned with swish offices, gaining power, or earning higher

salaries or bonuses, than concentrating on the needs of the organisation and

the people it serves.

Solutions to the agency problem

The overall issue here is therefore how to align these potential two different

sets of goals and the only way to do that … is to make them the same! Some

example of how to make this work would be:

• Link bonus payments to the achieving of targets relating to profit levels.

• Put employee profit sharing schemes in place. This will focus

everyone’s attention on the level of profits being achieved, as higher profits will mean higher rewards!

• Give management company shares as part of their remuneration

package. Through these managers therefore also become owners and, hence interests are aligned. Apple put this policy in place in 2013 for their executives.

• Ensure that management is shared by a number of directors. If

there are several people that have to agree on a strategy and

direction, it is less likely that objectives will be dominated by the

interests of one party.

• Corporate Governance (see below); put in place the rules and regulations which determine how a company is run.

30

7. Corporate governance

Corporate Governance is one of those subjects which will keep coming back

within your studies, so it’s good to take a little time here to look at it a little

more closely.

Corporate Governance concerns the set of rules and procedures which are

put in place to determine how an organisation is controlled and

managed. Its main objective is to balance the demands of all its

stakeholders, internal, external and connected (see earlier) including legal

requirements set out by the Government. It therefore helps to overcome

many of the issues surrounding the principal-agent problem. The way it

achieves this is through:

• Setting levels of reporting and disclosure so shareholders are

given relevant information.

• Setting rules for how the board of directors is run and managed and how decisions are made.

• Making regular communication with shareholders compulsory.

• Having independent directors on the board (non-executive directors)

to look after the shareholder needs.

Thereby:

• Ensuring a level of transparency so that all stakeholders can

clearly see how their needs are being met e.g. directors’ pay and

bonuses etc. have to be publicly disclosed.

• Ensuring that there is adequate knowledge and experience within a

company’s management such that required duties can be successfully completed.

• Providing timely, clear information delivered to shareholders

regarding the business’s activities and achievement of its stated financial aims. Ensuring that the business is operating in a legal and ethical way.

32

SSTAKEHOLDERS WEALTH

1. Introduction

UK based law firm, Slater and Gordon experienced a share price fall by

around 95% between April 2015 and February 2016. By October 2016, legal

action by the shareholders affected was looming with an estimated cost of

around $250m. The grievance concerned disclosures made to the financial

markets surrounding the company’s performance and predictions which

shareholders felt were unrealistic and meant they had invested based on

false information and promises.

This is a great example of a loss of shareholder wealth (and shareholders not

being happy about this). In this chapter we’re going to look in more detail at

what shareholder wealth is, the factors that affect it, how we measure it

in the short and long term and how all this affects management

decision making.

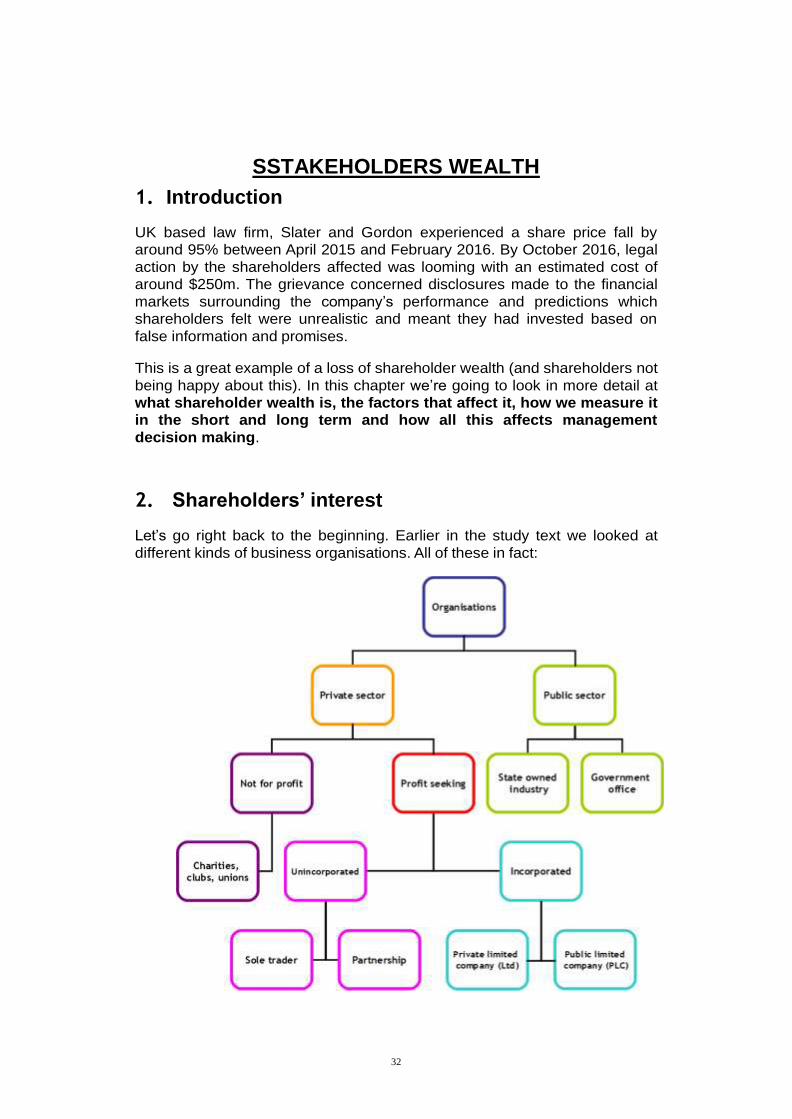

2. Shareholders’ interest

Let’s go right back to the beginning. Earlier in the study text we looked at

different kinds of business organisations. All of these in fact:

33

If this doesn’t look familiar, it may be time to go back and have another read

through! In this chapter, we’re only concerned with these:

Why only these? Well, these are the ones that sell shares and which

therefore have shareholder owners. If you remember, the difference

between them is that the shares of public limited companies are traded on the

stock market and are therefore available to any potential investor to buy and

sell, those of private limited companies aren’t. The shares in private limited

companies will have been purchased by those specifically approached for

investment in the business e.g. like the Dragons in the Dragon’s Den

programme in the UK. So, I guess we need to start by thinking about what

shares are?

Shares and share prices

Time to get our heads around lots of definitions.

Finance is raised by a company through selling equal part shares in the company which are bought by investors. What exactly does this mean? Well,

a company is split into a number of shares and an investor’s shares

represent the proportion of the company they own. For example, if the

company issues 1,000 shares and one investor purchases 100, they own

10% of the company:

100

1,000

= 10%

The investor is said to own 10% equity of the company, or 10% of the

equities of the company. Equity also being another name for a share.

34

A shareholder is an investor who has bought shares (equity) in a

company. Their level of share ownership represents their proportion of

ownership of the profits, losses and assets of the company. In return,

shareholders expect to receive dividends. These are payments made by

the company out of the profits of the company. Also known as a

distribution of profits. The shareholder will receive an amount equal in

proportion to the shareholding that they own. Let's say the company paid out

£1m in dividends, our shareholder with 10% of the shares would get

£100,000.

Types of shares

There are two main types of share an investor can buy, these are:

Ordinary shares – the most common type of share. Ordinary shares entitle

the holder to voting rights on decisions made by the company at

shareholder meetings and a dividend distribution.

Preference shares – a special class of share that not all companies offer.

The holders of these shares get their dividends paid first out of the profits

of the business. Only when these individuals have been paid, do ordinary

shareholders receive any payments. However, they do not have any voting

rights at shareholder meetings.

Objectives of shareholders

There are a variety of objectives a company works towards. However, for a

private company, the main objective will be to maximise the wealth of

its investors. In order to achieve this, a company aims to maximise its

profits which can then be paid in the form of dividends to its shareholders or

re-invested in the company in order to increase the share price.

Shareholders have a direct interest in how a company performs financially

and will make decisions on whether to buy more shares, or sell the ones

they own, based on financial statements and any other disclosures

made about the financial performance, actual or predicted, of the company.

These disclosures are known as short and medium-term measures.

35

Summary

36

3. Calculating shareholder wealth in the short-term

So how do we measure shareholders’ wealth? Well that depends if you’re

taking a short or a long term view!

Let’s start by looking at short term measures. Short term measures include

those that give an indication of likely returns over the course of the next

financial year.

Return on capital employed

A key short term measure is return on capital employed (ROCE). This

establishes how efficient a company is in generating profits from the

amount invested in the company.

ROCE is calculated as follows:

ROCE =

Profit before interest and tax (PBIT)

Total assets less current liabilities

X 100%

37

If you haven't heard of the term ’current liability' before, this is something

which the company owes and expects to pay back within a year. e.g. a

short-term loan from a bank.

The figure generated will be compared to shareholders’ expectations and will

inform their investment decisions e.g. whether to buy or sell.

Example

In 20X2, Fox plc earned profit before tax of £425,200 and paid back interest of

£38,010. Total assets less current liabilities were £1,560,000. Calculate

ROCE for 20X2.

In 20X3 the corresponding figures were £468,000; £41,000 and £1,670,000,

what was the ROCE for 20X3?

38

Answer

OK, we’re doing the same thing for both years, so the easiest thing to do is to

put both in the same table. We have been given the profit before tax, so to

get to the profit before interest and tax, we need to add the interest back.

20X2 20X3

£ £

Profit before tax 425,200 468,000

Interest 38,010 41,000

Profit before interest

and tax (PBIT) 463,210 509,000

Total assets less

current liabilities 1,560,000 1,670,000

Right, so now we have all the figures that we need, time to put them into the

formula:

So what is this calculation doing? Well, it’s showing us how effectively the

company is utilising its assets to generate profit. Back to our shareholder,

let’s say they were hoping for a ROCE of 29%, are they happy and will they

make an investment? Well, yes, the ROCE of the company has turned out to be

higher than they wanted in order to invest, they are definitely going to buy!

Now, say another company, Hare PLC, had a ROCE of 42%, which company is

doing better? Well, it’s Hare PLC. They have a higher ROCE and are therefore

gaining a greater return (level of profit) on their assets than Fox PLC.

How will this affect our shareholder? Well, both companies have a ROCE above

the level that they were looking for, but Hare PLC is doing even better so,

assuming there are no other factors to sway their decision, our shareholder will

be looking to put their money here!

39

However, whilst ROCE is a useful calculation it does fail to take into account

where the profits go. For example, the calculated percentage may be high, but

what if the level oftax and interest payable are also high? After that is taken off,

there may be no profit left for shareholders! Our potential shareholder would be

very upset!

This is where Earnings per share or EPS comes in.

Earnings per share

ROCE enables investors to work out the return generated to all investors.

Calculating earnings per share (EPS) enables investors to see the

profit earned for each share they own.

The amount calculated using this formula is the potential dividend that could

be paid out per share. However, it is up to the directors to decide the actual

value of the dividend to be distributed which may be much lower if they decide

to retain profits in the business to invest in business growth.

Note: This formula includes only equity shares issued, (those that have

actually been sold). Take care that there is another number this could be

confused with and that is equity shares authorised, which is the total

number of shares which the board are authorised to sell in total – some of

which may not have been put up for sale yet.

Example

Using the income statement below for Demo Company plc, calculate the EPS

for 20X2.

Profit before interest and tax

£

250,000

Interest (35,000)

Profit before tax 215,000

Tax (60,000)

Profit after tax 155,000

Preference dividend (6,000)

Profit available for ordinary shareholders (earnings) 149,000

Ordinary dividend (89,000)

Retained profit 60,000

The company has issued 100,000 ordinary shares and 25,000 preference

shares.

40

Answer

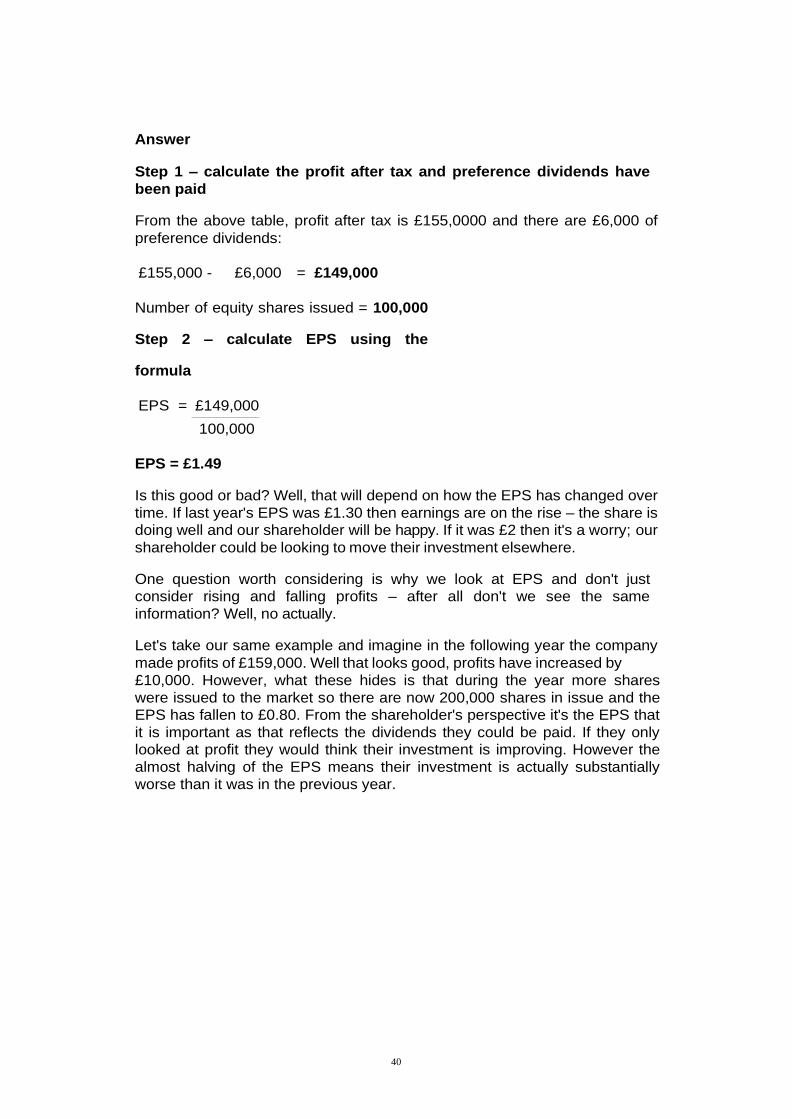

Step 1 – calculate the profit after tax and preference dividends have

been paid

From the above table, profit after tax is £155,0000 and there are £6,000 of

preference dividends:

£155,000 - £6,000 = £149,000

Number of equity shares issued = 100,000

Step 2 – calculate EPS using the

formula

EPS = £149,000

100,000

EPS = £1.49

Is this good or bad? Well, that will depend on how the EPS has changed over

time. If last year's EPS was £1.30 then earnings are on the rise – the share is

doing well and our shareholder will be happy. If it was £2 then it's a worry; our

shareholder could be looking to move their investment elsewhere.

One question worth considering is why we look at EPS and don't just

consider rising and falling profits – after all don't we see the same

information? Well, no actually.

Let's take our same example and imagine in the following year the company

made profits of £159,000. Well that looks good, profits have increased by

£10,000. However, what these hides is that during the year more shares

were issued to the market so there are now 200,000 shares in issue and the

EPS has fallen to £0.80. From the shareholder's perspective it's the EPS that

it is important as that reflects the dividends they could be paid. If they only

looked at profit they would think their investment is improving. However the

almost halving of the EPS means their investment is actually substantially

worse than it was in the previous year.

41

4. Long term shareholder wealth

Measuring long term financial performance

So, we’ve seen how a shareholder can work out how wealthy they’re going to

be in the short term (in the next year) using measures such as Return on

Capital Employed (ROCE) and Earning Per Share (EPS), but what if they’re

looking several years ahead, how can longer term financial performance be

measured?

Let's use an example to demonstrate this point.

Stephanie has just inherited £100 from her great aunt, she has decided to invest it for five years in Doing Well Plc. Over the long term, the returns

that she can expect to receive will be in the form of:

• The dividends received – a payment from the company which represents her share in the company's profits, and;

• Any increase in the price of the share when she sells.

If Stephanie was looking ahead, over five years she could add up all the

dividends expected and the expected share price to see how much her

investment would be worth at the end of the period. Let's say Doing Well Plc

expect to pay her a dividend of £10 per year (£50 in total) and anticipate the

value of the shares rising by £20 then her total return is £70.

However there are some issues with this approach:

• Estimated values may not be the same as actual results – in fact they're highly likely to be very different as much can change in the real world e.g. the economy, customer trends, competitors release new products.

• It does not take into account her cost of capital – the amount of return she wants to make given the risk taken.

Let's say she considers Doing Well PLC a risky investment she may

want a 30% return each year to cover the risk. £70 over 5 years is not

enough to cover this return and so it is not an investment she should

make.

• Stephanie may not know her cost of capital – after all how much

return does she really expect to achieve given the risk she is taking and how does she work this out?

• It ignores the time value of money - the fact that returns now are

more valuable than those received later.

i.e. Stephanie would rather have £70 today than £70 in 5 years' time.

42

Why is that?

It is likely to be worth more today than in 5 years as costs are likely to

have gone up in that 5 year period.

She is also not guaranteed to get the money, after all Doing Well might

not be doing quite so well in 5 years' time and may not be able to afford

to pay her!

In our earlier calculation of her returns, we ignored the timings of when

she would receive them (the time value of money) and we shouldn't

ignore that.

Valuing a company

In theory the value of a company should be higher if it will have higher

returns in the future and lower if it will have lower returns. A company with

£2m of net cash inflows each year should have a higher valuation than one

with £1m of net cash inflows each year.

If a company is expected to improve its cash inflows in the future, say by

launching a new product, then the share price should rise.

Later on, in this study text we will learn a technique known as Net Present

Value which can be used to estimate the value of a company using

cash flows. Using this approach, the greater the net cash inflows the greater

the value of the company. This technique does take into account the cost

of capital and the time value of money, so it's very useful. However, it's also

quite complicated, so don't worry any more about this now, but do be aware

that it exists.

Factors affecting the future value of shares

So, we have seen that the value of a company depends on the value of

future cash inflows – the more the better.

Those inflows can be affected by 3 main factors:

• Internal factors

• External factors

• Financial influences

Let's examine each of these in more detail.

Internal factors – these are factors which come from within a company

e.g. management policies, strategy, product releases, union influence etc.

These factors exert either a positive or negative influence on cash flows and

hence share prices.

For example, news of the release of the latest Apple iPhone is likely to cause

43

the share price to increase. Conversely, news that Apple had been exploiting

workers in a less economically developed country may attract negative

publicity and cause share prices to decrease.

External factors – are factors which lie outside of the company, e.g.

competitor action, the economy, government regulation etc.

For example, news of Samsung releasing a new Smartphone with more

advanced features and functionality than the current Apple iPhone may

cause Apple’s share price to decrease, as people perceive that Samsung may

gain a greater market share and Apple’s profit could therefore fall.

Conversely, an improvement in the economic position of countries which are

in its key markets will be likely to increase Apple’s share price as people will

have more money to spend on the latest and best gadgets.

Financial influences - If a company releases statements indicating earnings

are higher than expected share prices are likely to increase. The opposite is

true if a company reports its financial year is less profitable than expected.

Market expectations

Share prices often react as much as a result of people's expectations

about future profitability as to actual results. Here's an example to

demonstrate the point.

Mobile Mania Ltd, a mobile phone manufacturer, has announced a new

investment project in super-efficient mini transmission masts. Even though the

company has not actually released projected cash flow information, the

market makes its best assumption of what this means for the business.

Commentators within the market have devoured all the information

provided about the project and their protections suggest that the future cash

44

flow will increase significantly as a result of this project. As a result the share

price has soared.

Six months down the line, information is released by the company that the

technology required is proving temperamental and the market believes costs

will rise significantly. The market now expects the project to be less profitable

than previously expected and so the share price drops.

Positive information and estimations will therefore lead to increases in

share price and help to persuade shareholders to invest, whilst negative

information will have the opposite effect.

45

5. Risk and return – the required rate

Returning to Stephanie’s decision earlier of whether to invest £100 in shares

of Doing Well PLC, another option she has is to invest it in a bank. One key

consideration in this decision is that of risk.

For investors, investing in shares is riskier than investing money in the

bank. This is due to a number of factors, such as:

Annual dividends from shares will vary year-on-year depending

on the annual profits achieved by the company. The bank's interest

will be consistent and guaranteed and so putting money in bank

accounts is considered less risky.

We saw earlier that the market value of shares varies due to market

perceptions about the company and the economy. Share values can

therefore rise and fall over time, whereas the investment in the

bank stays the same; the initial deposit plus any interest earned.

Investors will lose the investment if the company becomes

insolvent i.e. hasn’t got enough money to pay everybody it owes, and

therefore gets closed down. Investments in banks are often

guaranteed by governments, so even if the bank goes bust the

investment is usually safe.

There are two main categories of risk associated with investing in shares of a

company, these are:

Systematic risks – the uncertainty inherent in a particular market.

For example, during difficult times in the economy of a country the

property market is often hit badly and profits in property companies

often fall significantly. Building companies have a high systematic risk.

Contrast this with supermarkets where profits tend to stay high even

during difficult economic times as people still need to buy food.

Supermarkets have low systematic risk.

Unsystematic risks - the uncertainty inherent in a particular

company due to factors unique to it

For example, Steel PLC has a highly unionised workforce who often

strike. Also, skilled labour is in shortage near their factory and so

there is a risk that costs will be high. These are specific risks that are

not necessarily relevant to all steel companies, but are specific to

Steel PLC. They are therefore unsystematic risks.

46

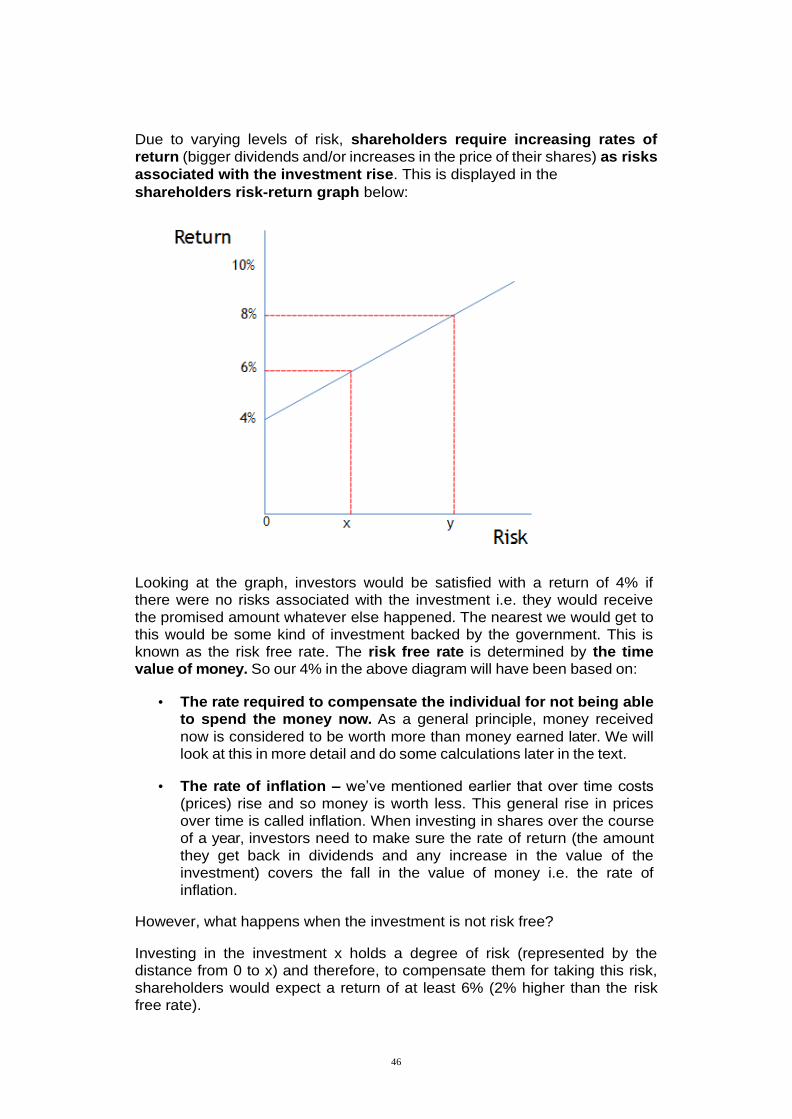

Due to varying levels of risk, shareholders require increasing rates of

return (bigger dividends and/or increases in the price of their shares) as risks

associated with the investment rise. This is displayed in the

shareholders risk-return graph below:

Looking at the graph, investors would be satisfied with a return of 4% if

there were no risks associated with the investment i.e. they would receive

the promised amount whatever else happened. The nearest we would get to

this would be some kind of investment backed by the government. This is

known as the risk free rate. The risk free rate is determined by the time

value of money. So our 4% in the above diagram will have been based on:

• The rate required to compensate the individual for not being able

to spend the money now. As a general principle, money received

now is considered to be worth more than money earned later. We will

look at this in more detail and do some calculations later in the text.

• The rate of inflation – we’ve mentioned earlier that over time costs

(prices) rise and so money is worth less. This general rise in prices

over time is called inflation. When investing in shares over the course

of a year, investors need to make sure the rate of return (the amount

they get back in dividends and any increase in the value of the

investment) covers the fall in the value of money i.e. the rate of

inflation.

However, what happens when the investment is not risk free?

Investing in the investment x holds a degree of risk (represented by the

distance from 0 to x) and therefore, to compensate them for taking this risk,

shareholders would expect a return of at least 6% (2% higher than the risk

free rate).

47

Investing in y is riskier still than x, therefore shareholders would expect a

return of at least 8% (4% higher than the risk free rate).

Other factors which affect risk and return

There are a number of other issues which impact risk and return.

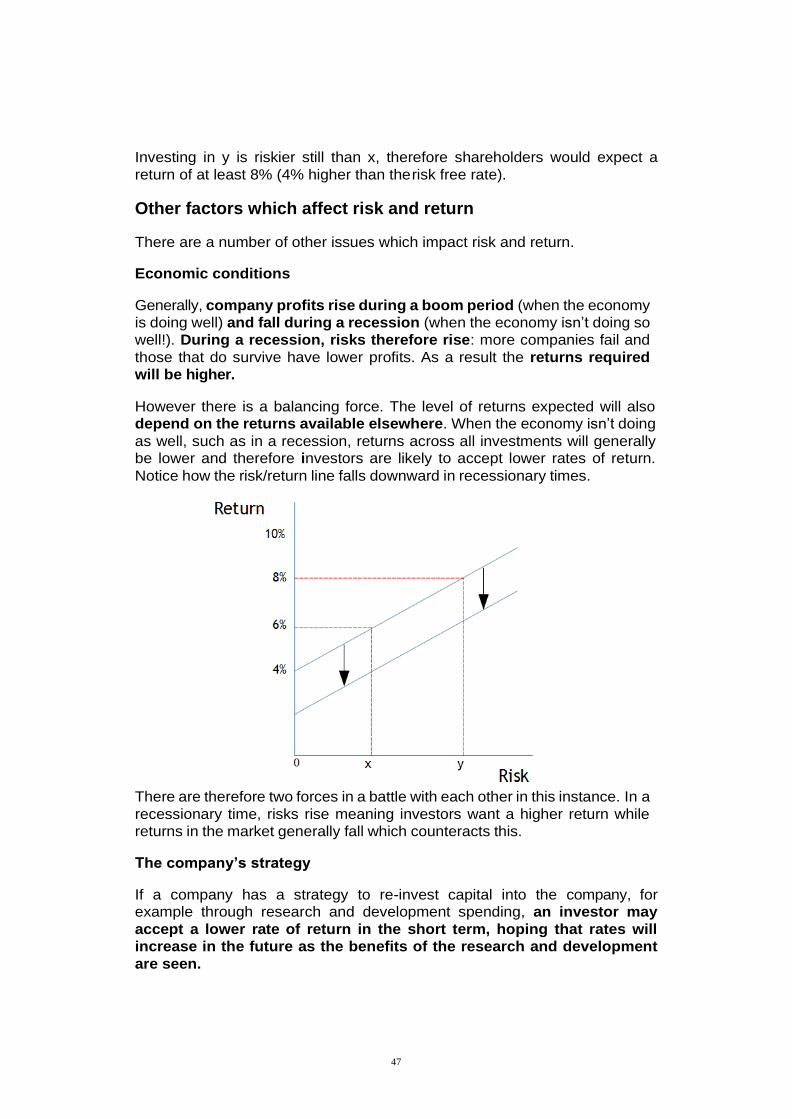

Economic conditions

Generally, company profits rise during a boom period (when the economy

is doing well) and fall during a recession (when the economy isn’t doing so

well!). During a recession, risks therefore rise: more companies fail and

those that do survive have lower profits. As a result the returns required

will be higher.

However there is a balancing force. The level of returns expected will also depend on the returns available elsewhere. When the economy isn’t doing

as well, such as in a recession, returns across all investments will generally be lower and therefore investors are likely to accept lower rates of return.

Notice how the risk/return line falls downward in recessionary times.

There are therefore two forces in a battle with each other in this instance. In a

recessionary time, risks rise meaning investors want a higher return while

returns in the market generally fall which counteracts this.

The company’s strategy

If a company has a strategy to re-invest capital into the company, for example through research and development spending, an investor may

accept a lower rate of return in the short term, hoping that rates will

increase in the future as the benefits of the research and development

are seen.

48

Expectations about the industry

If a particular market segment/industry is performing well, the required

rate of return is likely to be higher on investments in that particular

industry, due to increased expectations across the whole sector and

investors move their funds into companies in that sector causing the share

price to rise. The opposite is true if the market segment is performing badly

when investors will move their money out of one industry and into another.

Summary

So, where does that leave Stephanie? Well to be sure that she’s making the

right long term decision on her investment, she must make sure that the

rate of return that she is expecting to get takes into account a number of

key factors:

If the return isn’t sufficient enough after taking these factors into account, she’s

going to have to look elsewhere!

49

6. Shareholders’ impact on management decisions

So, Stephanie has decided to go ahead and invest her £100 in shares in

Doing Well PLC and has therefore become a shareholder. Does this affect

Doing Well PLC at all? Why would they be concerned who their shareholders

are?

Well basically, if the management want to keep the investment these

shareholders bring, they need to keep them happy!

How do they do this?

Dividend policy

A dividend policy is the determination of how much and how frequently

cash is paid out of profits to shareholders in the form dividends. It is

published by the business so that potential shareholders like Stephanie can

take it into consideration when they are deciding where to put their money.

For example, if Stephanie had been planning on using the dividend every

year to buy a holiday, there would be no point in buying shares in a company

who’s dividend policy stated that they weren’t going to be paying one

because they were going to reinvest it all back in the business!

In coming up with this policy the company has to consider the other

financial needs of the business. For example, research and development

costs, funds for expansion of manufacturing etc. They can’t set out a

dividend policy stating that they will pay out 5% of net profits every year if they

need 10% to pay for the new manufacturing facility that they are planning.

By stating their dividend policy, the business then needs to make sure that

every project that it takes on fits in with it. Effectively therefore, every

decision taken has to take into account:

• Their shareholders’ cost of capital (return level they want to see) -

For example, if the business has large pension funds investing in its

shares, these will generally be looking for high, consistent returns to

boost their clients’ funds. Their cost of capital will therefore be quite

high and therefore, to keep them happy, so must the returns on any

projects taken on by the business.

• The level of risk their shareholders want to take. Shareholders

investing in a company which has stated in its dividend policy that it will consistently pay out 25% of its net profit in dividends every year

e.g. a low risk, consistent return, won’t be happy if the management

announce a high-risk project which may or may not bring about a

return and could even lead to a fall in profits should it all go wrong!

50

Signalling

Dividend announcements convey information, intended or sometimes

unintended, to the market e.g. a lower dividend this year than last year

could lead to the assumption that the company’s performance is worse. As a

result, the price of their shares could drop as people either react by selling

their shares or choosing not to buy. Management will therefore be looking to

avoid the negative consequences of this by only choosing those projects

which allow them to make positive announcements!

Shareholder communication

So, we’re generally saying that the business needs to stay close to their

shareholders and understand their needs. How do they do this? This

involves arranging shareholder meetings (some of which are compulsory at

certain times but you’ll find out about those in another subject!) and taking

advantage of these meetings to get to know those present and their views. At

other times, it will involve communicating the details of all project

decisions or dividend announcements to avoid those disadvantageous

assumptions!