Embed Size (px)

Citation preview

cima OFFICIAL REVISION CARDS

CertifiCate LeveL

SUBJECT BA1

fundamentals of Business economics

2

FUNDAMENTALS OF BUSINESS ECONOMICS

Published by: Kaplan Publishing UK

Unit 2 The Business Centre, Molly Millars Lane, Wokingham, Berkshire RG41 2QZ

Copyright © 2017 Kaplan Financial Limited. All rights reserved.

No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form or by any means electronic, mechanical, photocopying, recording or otherwise without the prior written permission of the publisher.

AcknowledgementsThe CIMA Publishing trademark is reproduced with kind permission of CIMA.

Notice The text in this material and any others made available by any Kaplan Group company does not amount to advice on a particular matter and should not be taken as such. No reliance should be placed on the content as the basis for any investment or other decision or in connection with any advice given to third parties. Please consult your appropriate professional adviser as necessary. Kaplan Publishing Limited and all other Kaplan group companies expressly disclaim all liability to any person in respect of any losses or other claims, whether direct, indirect, incidental, consequential or otherwise arising in relation to the use of such materials.

British Library Cataloguing in Publication Data

A catalogue record for this book is available from the British Library

ISBN 978-1-78415-908-5

Printed and bound in Great Britain

3

FUNDAMENTALS OF BUSINESS ECONOMICS

How to use Revision Cards

The concept

• Revision Cards are a new and different way of learning, based upon research into learning styles and effective recall.

• The cards are in full colour and have text supported by a range of images, making them far more effective for visual learners and easier to remember.

• Unlike a bound text, Revision Cards can be rearranged and reorganised to appeal to kinaesthetic learners who prefer to learn by doing.

• Being small enough to carry around means that you can take them anywhere. This gives the opportunity to keep going over what you need to learn and so helps with recall.

• The content has been reduced down to the most important areas, making it far easier to digest and identify the relationships between key topics.

• Revision Cards, however you learn, whoever you are, wherever you are.........

4

FUNDAMENTALS OF BUSINESS ECONOMICS

How to use them

Revision Cards are a pack of approximately 52 cards, slightly bigger than traditional playing cards but still very easy to carry and so convenient to use when travelling or moving around. They can be used during the tuition period or at revision.

They are broken up into 4 sections. • An overview of the entire subject in a

mind map form (orange). • A mind map of each specific topic (blue). • Content for each topic presented so that

it is memorable (green). • Exam tips with references to past

questions on each topic (purple).

Each one is a different colour, allowing you to sort them in many ways.

• Perhaps you want to get a more detailed feel for each topic, why not take all the green cards out of the pack and use those.

• You could create your own mind maps using the blue cards to explore how different topics fit together.

• If at the revision phase why not take all the purple cards and work through the past questions identified.

• And if there are some topics that you understand, take those out of the pack, leaving yourself only the ones you need to concentrate on.

There are just so many ways you can use them.

5

FUNDAMENTALS OF BUSINESS ECONOMICS

Contents

• Microeconomic and Organisational Context I: The Goals and Decisions of Organisations

• Microeconomic and Organisational Context II: The Market System • Financial Context of Business I • Macroeconomic and Institutional Context I: The Domestic Economy • Macroeconomic and Institutional Context II: The International Economy • Financial Context of Business II: International Aspects • Financial Context of Business III: Discounting and Investment Appraisal • Informational Context of Business I: Summarising and Analysing Data • Informational Context of Business II: Index Numbers • Informational Context of Business III: Inter-relationships between variables • Informational Context of Business IV: Forecasting

6

FUNDAMENTALS OF BUSINESS ECONOMICS

Exam guidanceFormat of exam

The assessment for Fundamentals of Business Economics (BA1) is a two hour computer based exam consisting of 60 compulsory questions.

A variety of objective test question styles and types will be used within the assessment, such as:

Multiple choice, multiple response, number entry, drag and drop, drop down and hot spot.

Core areas of the syllabus

The syllabus comprises of

A Macroeconomic and institutional context of business 25%

B Microeconomic and organisational context of business 30%

C Informational context of business 20%

D Financial context of business 25%

7

FUNDAMENTALS OF BUSINESS ECONOMICS

Quality and accuracy are of the utmost importance to us so if you spot an error in any of our products, please send an email to [email protected] with full details.

Our Quality Co-ordinator will work with our technical team to verify the error and take action to ensure it is corrected in future editions.

RevisionCards

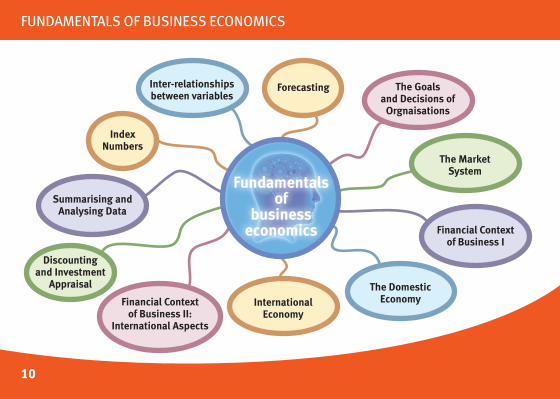

overviewfundamentals of business economics

RevisionCards

10

FUNDAMENTALS OF BUSINESS ECONOMICS

10

Financial Context of Business II:

International Aspects

The Market System

Fundamentalsof

business economics

Summarising and Analysing Data

Discounting and Investment

Appraisal

Financial Context of Business I

The Goals and Decisions of

Orgnaisations

Index Numbers

The Domestic EconomyInternational

Economy

Inter-relationships between variables

Forecasting

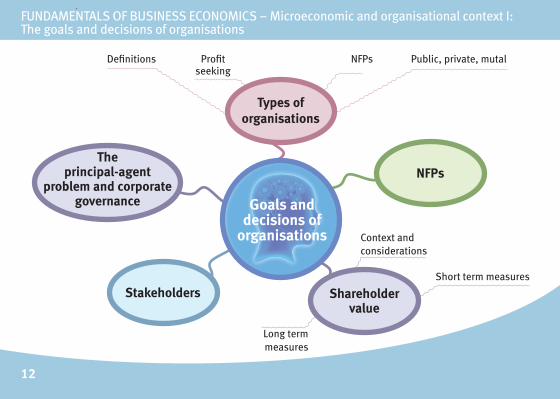

microeconomic and organisational context I:

the goals and decisions of organisations

fundamentals of business economics

RevisionCards

12

FUNDAMENTALS OF BUSINESS ECONOMICS – Microeconomic and organisational context I: The goals and decisions of organisations

The principal-agent

problem and corporate governance

Short term measures

Types of organisations

Context and considerations

NFPs

Stakeholders

Long term measures

Shareholder value

Goals and decisions of

organisations

Definitions Profitseeking

NFPs Public, private, mutal

13

FUNDAMENTALS OF BUSINESS ECONOMICS – Microeconomic and organisational context I: The goals and decisions of organisations

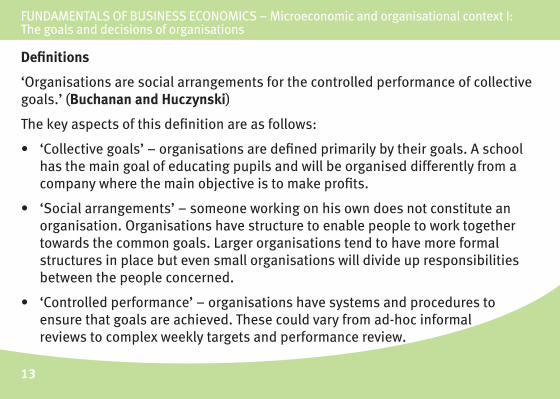

Definitions

‘Organisations are social arrangements for the controlled performance of collective goals.’ (Buchanan and Huczynski)

The key aspects of this definition are as follows:

• ‘Collective goals’ – organisations are defined primarily by their goals. A school has the main goal of educating pupils and will be organised differently from a company where the main objective is to make profits.

• ‘Social arrangements’ – someone working on his own does not constitute an organisation. Organisations have structure to enable people to work together towards the common goals. Larger organisations tend to have more formal structures in place but even small organisations will divide up responsibilities between the people concerned.

• ‘Controlled performance’ – organisations have systems and procedures to ensure that goals are achieved. These could vary from ad-hoc informal reviews to complex weekly targets and performance review.

14

FUNDAMENTALS OF BUSINESS ECONOMICS – Microeconomic and organisational context I: The goals and decisions of organisations

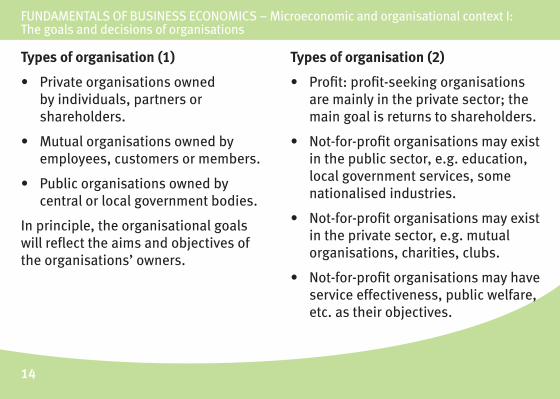

Types of organisation (1)

• Private organisations owned by individuals, partners or shareholders.

• Mutual organisations owned by employees, customers or members.

• Public organisations owned by central or local government bodies.

In principle, the organisational goals will reflect the aims and objectives of the organisations’ owners.

Types of organisation (2)

• Profit: profit-seeking organisations are mainly in the private sector; the main goal is returns to shareholders.

• Not-for-profit organisations may exist in the public sector, e.g. education, local government services, some nationalised industries.

• Not-for-profit organisations may exist in the private sector, e.g. mutual organisations, charities, clubs.

• Not-for-profit organisations may have service effectiveness, public welfare, etc. as their objectives.

15

FUNDAMENTALS OF BUSINESS ECONOMICS – Microeconomic and organisational context I: The goals and decisions of organisations

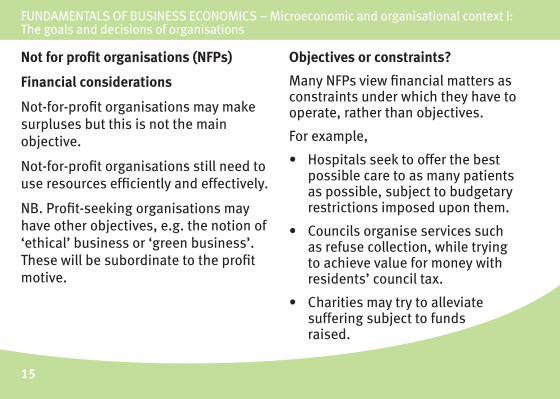

Not for profit organisations (NFPs)

Financial considerations

Not-for-profit organisations may make surpluses but this is not the main objective.

Not-for-profit organisations still need to use resources efficiently and effectively.

NB. Profit-seeking organisations may have other objectives, e.g. the notion of ‘ethical’ business or ‘green business’. These will be subordinate to the profit motive.

Objectives or constraints?

Many NFPs view financial matters as constraints under which they have to operate, rather than objectives.

For example,

• Hospitals seek to offer the best possible care to as many patients as possible, subject to budgetary restrictions imposed upon them.

• Councils organise services such as refuse collection, while trying to achieve value for money with residents’ council tax.

• Charities may try to alleviate suffering subject to funds raised.

16

FUNDAMENTALS OF BUSINESS ECONOMICS – Microeconomic and organisational context I: The goals and decisions of organisations

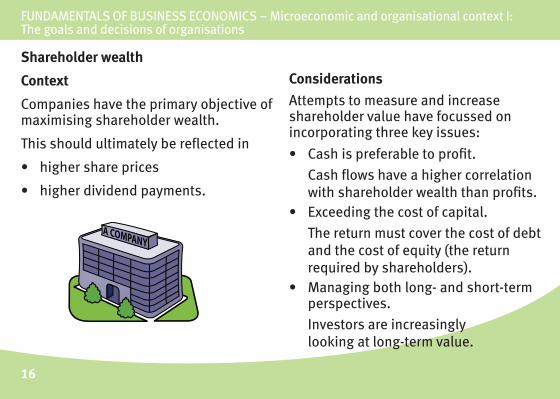

Shareholder wealth

Context

Companies have the primary objective of maximising shareholder wealth.

This should ultimately be reflected in

• higher share prices

• higher dividend payments.

ConsiderationsAttempts to measure and increase shareholder value have focussed on incorporating three key issues:

• Cash is preferable to profit.Cash flows have a higher correlation with shareholder wealth than profits.

• Exceeding the cost of capital.The return must cover the cost of debt and the cost of equity (the return required by shareholders).

• Managing both long- and short-term perspectives.Investors are increasingly looking at long-term value.

17

FUNDAMENTALS OF BUSINESS ECONOMICS – Microeconomic and organisational context I: The goals and decisions of organisations

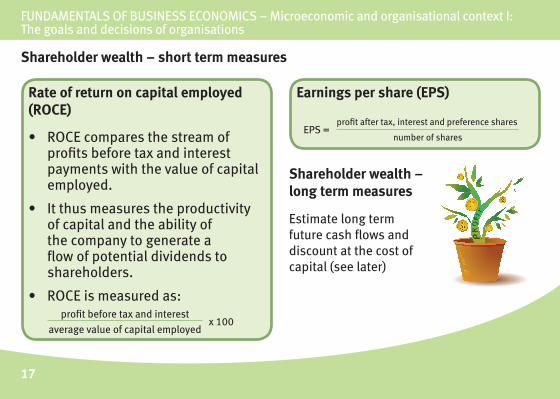

Shareholder wealth – short term measures

Rate of return on capital employed (ROCE)

• ROCE compares the stream of profits before tax and interest payments with the value of capital employed.

• It thus measures the productivity of capital and the ability of the company to generate a flow of potential dividends to shareholders.

• ROCE is measured as:profit before tax and interest

x 100average value of capital employed

Earnings per share (EPS)

EPS =profit after tax, interest and preference shares

number of shares

Shareholder wealth – long term measures

Estimate long term future cash flows and discount at the cost of capital (see later)

18

FUNDAMENTALS OF BUSINESS ECONOMICS – Microeconomic and organisational context I: The goals and decisions of organisations

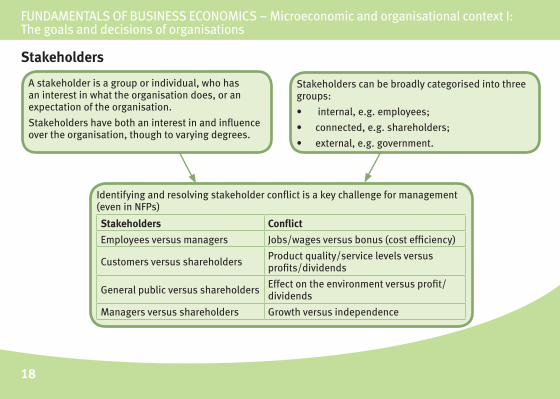

Stakeholders

Identifying and resolving stakeholder conflict is a key challenge for management (even in NFPs)

Stakeholders ConflictEmployees versus managers Jobs/wages versus bonus (cost efficiency)

Customers versus shareholders Product quality/service levels versus profits/dividends

General public versus shareholders Effect on the environment versus profit/dividends

Managers versus shareholders Growth versus independence

Stakeholders can be broadly categorised into three groups:

• internal, e.g. employees; • connected, e.g. shareholders; • external, e.g. government.

A stakeholder is a group or individual, who has an interest in what the organisation does, or an expectation of the organisation.Stakeholders have both an interest in and influence over the organisation, though to varying degrees.

19

FUNDAMENTALS OF BUSINESS ECONOMICS – Microeconomic and organisational context I: The goals and decisions of organisations

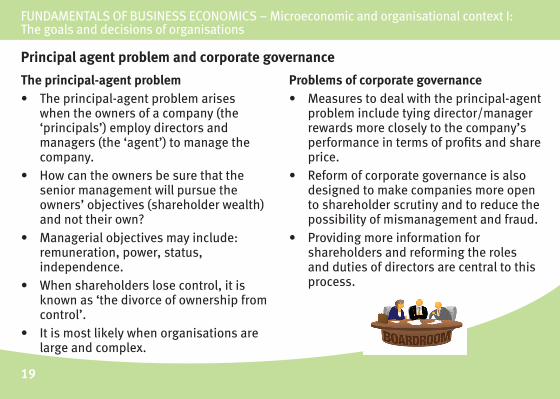

Principal agent problem and corporate governance

The principal-agent problem • The principal-agent problem arises

when the owners of a company (the ‘principals’) employ directors and managers (the ‘agent’) to manage the company.

• How can the owners be sure that the senior management will pursue the owners’ objectives (shareholder wealth) and not their own?

• Managerial objectives may include: remuneration, power, status, independence.

• When shareholders lose control, it is known as ‘the divorce of ownership from control’.

• It is most likely when organisations are large and complex.

Problems of corporate governance • Measures to deal with the principal-agent

problem include tying director/manager rewards more closely to the company’s performance in terms of profits and share price.

• Reform of corporate governance is also designed to make companies more open to shareholder scrutiny and to reduce the possibility of mismanagement and fraud.

• Providing more information for shareholders and reforming the roles and duties of directors are central to this process.

RevisionCards

21

FUNDAMENTALS OF BUSINESS ECONOMICS – Microeconomic and organisational context I: The goals and decisions of organisations

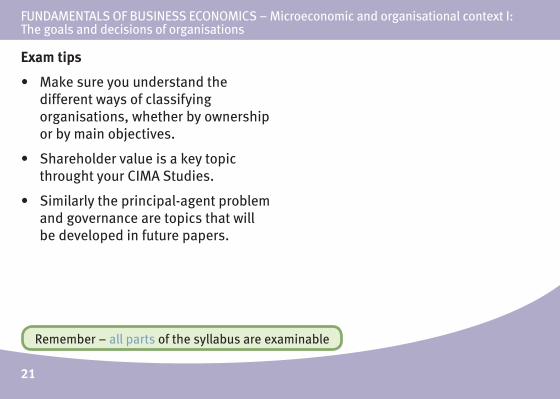

Exam tips

• Make sure you understand the different ways of classifying organisations, whether by ownership or by main objectives.

• Shareholder value is a key topic throught your CIMA Studies.

• Similarly the principal-agent problem and governance are topics that will be developed in future papers.

Remember – all parts of the syllabus are examinable

22

FUNDAMENTALS OF BUSINESS ECONOMICS – Microeconomic and organisational context I: The goals and decisions of organisations

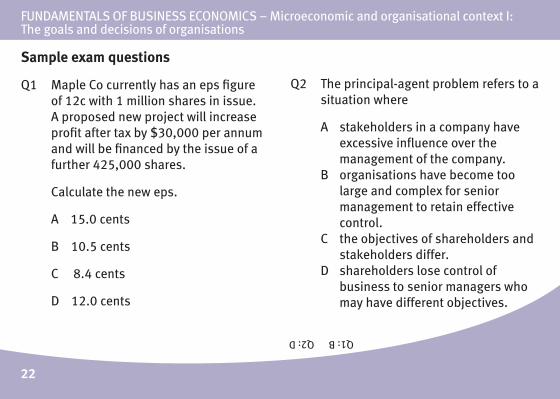

Sample exam questions

Q1 Maple Co currently has an eps figure of 12c with 1 million shares in issue. A proposed new project will increase profit after tax by $30,000 per annum and will be financed by the issue of a further 425,000 shares.

Calculate the new eps.

A 15.0 cents

B 10.5 cents

C 8.4 cents

D 12.0 cents

Q2 The principal-agent problem refers to a situation where

A stakeholders in a company have excessive influence over the management of the company.

B organisations have become too large and complex for senior management to retain effective control.

C the objectives of shareholders and stakeholders differ.

D shareholders lose control of business to senior managers who may have different objectives.

Q1: B Q2: D