Embed Size (px)

Citation preview

A presentation by Prof. Thomas Plenborg, Jens Overgaard Knudsen and Simon Vesterby Kold

Choice of comparable firms for multiple valuation

1

Agenda

2

1 Comparable firm selection for multiple valuation

2 Our idea

3 How did we test it and how does it work?

4 Questions

Who are we and what is the background of our project?

Professor at Department of Accounting and Auditing, CBS

Global Finance Graduate at Novo Nordisk A/S

Cand.merc.fir from CBS in 2015

Financial Analyst at Novo A/S

Cand.merc.fir from CBS in 2015

Thomas Plenborg Jens Overgaard Knudsen Simon Kold

Desired outcome:

₊ Help analysts and investors in improving valuation accuracy

3

Derivation of multiples from the present value relation

For simplicity, consider a firm which has a constant growth rate and discount factor forever.

FCFFWACCt gr

FCFFEV−

=

De grD

MVE−

=

P/E

P/B

EV/EBIT

EV/EBITDA

EV/SALES inEBITDAmRTRROICgr

gROICDEPR

FCFFWACC

FCFF arg)%1()1(1×−×−××

−

−

)%1()1(1DEPR

FCFFWACC

FCFF RTRROICgr

gROIC−×−××

−

−

)1(1 TRROICgr

gROIC

FCFFWACC

FCFF −××−

−

ROEgrgROE

De

D 1×

−−

De

D

grgROE

−−

Ideal peer-group companies for multiple valuation purposes should be truly identical on the basis of these properties - But how can we identify such firms?

4

5

Two obvious approaches for comparable firm selection: Industry affiliation and fundamentals

Industry Affiliation Fundamentals

Rat

iona

le fo

r the

ap

proa

ch

Theoretical difficulties in defining “an industry”

Industry classes are subjectively defined and subjectively chosen

Companies within the same industry class can be very different from each other

Dra

wba

cks

Companies within the same industry are subject to similar market characteristics

Companies within the same industry tend to produce similar products, leading to similarities of their supply and demand curves

Easy to use and widely applied in practice

Current fundamentals can be used to approximate future profitability, growth and risk

Independent of subjectively defined industry classes

Can incorporate, in principle, an infinite amount of peers

Used for comparable firm selection in a range of empirical studies , including combinations with industry

Which fundamentals are best at projecting future levels of profitability, growth and risk?

Gathering fundamental data for a lot of companies can be a cumbersome process

Most fundamental approaches are only capable of using 2-3 proxies

Illustration of the issue All firms in the sample

Previous attempts at the fundamental approach

We know that the levels of multiples are determined by profitability, growth and risk

Previous studies show that identifying comparable firms based on fundamentals may be a useful alternative to industry classification

However, in these studies, peers are selected in the intersection of the most similar firms in terms of proxies for profitability, growth and risk

This creates an issue

6

The 14% closest firms in terms of ROE

Of these firms, the 14% closest firms in terms of size

Adding a third or fourth variable would further reduce the number of peers

In effect, this restrains the approach to only being able to use two proxies for profitability, growth and risk

Consequence

The intersection of the two (leaving only 2% of the sample)

Agenda

7

1 Comparable firm selection for multiple valuation

2 Our idea

3 How did we test it and how does it work?

4 Questions

The Idea: -Sum of Rank Differences (SARD)

8

SARD proposition

Characteristics of the SARD model

Our method selects comparable firms based on the least sum of absolute rank differences across a range of variables which are

expected to affect multiples

If a potential peer has a low SARD value, the approach suggests that the potential peer and the target firm share similarities with respect to the chosen variables.

If these variables are useful proxies of the drivers of the multiple, then the identified peers and the target firm should also be traded at similar prices.

We propose a method where peers are selected on the basis of fundamentals and which allow for more than just one or two fundamental value drivers

𝑆𝑆𝑆𝑆𝑆𝑆𝐷𝐷𝑖𝑖,𝑗𝑗 = |𝑟𝑟𝑋𝑋,𝑖𝑖 − 𝑟𝑟𝑋𝑋,𝑗𝑗| + |𝑟𝑟𝑌𝑌,𝑖𝑖 − 𝑟𝑟𝑌𝑌,𝑗𝑗| + ⋯+ |𝑟𝑟𝑍𝑍,𝑖𝑖 − 𝑟𝑟𝑍𝑍,𝑗𝑗|

where SARD is the sum of absolute rank difference between firm i and firm j, rx,i is the rank of firm i in terms of variable x, rx,j is the rank of firm j in terms of variable x … and so forth.

9

A 5-step implementation guide to the SARD approach

Select base sample

1

Estimate relevant value drivers

2

Convert into ranks

3

Calculate rank difference (“Penalty points”)

4

Find the firms with the lowest SARD

5

A 5-step implementation guide to the SARD approach

• Construct a sample from which to select peer-group from. Could be:

- A large sample (like our empirical study where we use S&P 1500)

- A qualitative selected sample (e.g. subjective perception of industry affiliation)

• Select and calculate relevant value drivers. Our tests include: - Return on equity (profitability) - Net debt/EBIT (risk) - Size (risk and different levels of multiples) - Forecasted EPS growth t+2 (growth) - EBIT-margin (relevant for EV/sales

multiples)

• Practitioner implementation: Consider manuel adjustments, NTM ratios, industry-specific ratios etc ?

10

Select base sample

Estimate relevant value drivers

2

1

ROE Size

(bn. $) rROE rsize

Abbott Labs 10% 67 9 6 Coca-Cola 22% 185 6 3 Estee Lauder 34% 31 1 9

General Mills 24% 35 4 8 Johnson & Johnson

23% 280 5 1 Kellogg Co 20% 24 7 10 Mondelez 7% 69 10 5 Pepsico 31% 146 2 4 Procter & Gamble

17% 204 8 2 Reynolds America

30% 66 3 7

• Transform all value drivers into ranks • Enables you to combine value drivers regardless of scale • Possibility of assigning weights to value drivers

11

Implementation tip

Convert into ranks

3 A 5-step implementation guide to the SARD approach

• Calculate the difference in ranks between each firm in the base sample and the firm subject to the valuation

• Repeat for each

value driver

• The rank differences in the table is based on ROE

Calculate rank difference (“Penalty points”)

4 A 5-step implementation guide to the SARD approach

Abbott Labs Coca-Cola Estee Lauder General

Mills Abbott Labs n/a |9-6|+|6-3|=6 |9-1|+|6-9|=11

Coca-Cola n/a |6-1|+|3-9|=11

Estee Lauder n/a

General Mills

Johnson & Johnson

Kellogg Co Mondelez Pepsico

Procter & Gamble

Reynolds America

• Calculate the sum of absolute rank differences across the value drivers

• Identify the firms with the least sum of absolute rank differences

• Decide on a cut-off (i.e. number of firms to include as peers). In the example below we use six as cut-off (i.e. select six peers)

Peer

Abbott Labs

Coca-Cola

Estee Lauder

General M

ills

Johnson &

Johnson

Kellogg Co

Mondelez

Pepsico

Procter &

Gam

ble

Reynolds Am

erica

1

Mondelez (2)

Procter & Gamble

(3)

General Mills (4)

Reynolds America

(2) Coca-Cola (3) General

Mills (5) Abbott Labs

(2) Reynolds

America (4) Coca-

Cola (3) General Mills

(2)

2

Procter & Gamble

(5)

Johnson & Johnson

(3)

Reynolds America

(4)

Estee Lauder

(4)

Procter & Gamble

(4)

Abbott Labs (6)

Procter & Gamble

(5) Coca-Cola (5)

Johnson &

Johnson (4)

Pepsico (4)

3 Kellogg Co (6)

Pepsico (5) Pepsico

(6) Kellogg Co (5)

Pepsico (6)

Reynolds America

(7) Coca-Cola (6) General Mills

(6) Mondelez

(5) Estee Lauder

(4)

4 Coca-Cola

(6) Abbott Labs (6)

Kellogg Co (7)

Pepsico (6)

General Mills (8)

Estee Lauder (7)

Kellogg Co (8)

Estee Lauder (6)

Abbott Labs (5)

Coca-Cola (7)

5 General

Mills (7)

Mondelez (6)

Abbott Labs (11)

Abbott Labs (7)

Reynolds America (8)

Mondelez (8)

Reynolds America (9)

Johnson & Johnson (6)

Pepsico (8) Abbott Labs (7)

6 Reynolds America

(7)

Reynolds America

(7)

Coca-Cola (11)

Coca-Cola (7)

Abbott Labs (9)

Coca-Cola (8)

Pepsico (9)

Procter & Gamble

(8)

Kellogg Co (9) Kellogg Co (7)

Find the firms with the lowest SARD

5 A 5-step implementation guide to the SARD approach

Agenda

14

1 Comparable firm selection for multiple valuation

2 Our idea

3 How did we test it and how does it work?

4 Questions

Random example from S&P 1500: Six peers selected for IFF on the basis of SARD

Peers Industry EV/EBIT ROE Debt/EBIT Size

KB Home Consumer Durables & Apparel 7.3 23% 2.3 3,175

Beckman Coulter Inc Health Care Equip. & Services 13.2 23% 2.0 3,354

Pioneer Natural Resources Co Energy 12.6 22% 3.6 3,878

McCormick & Co Inc Food, Beverage & Tobacco 16.9 24% 2.0 4,593

TCF Financial Corp Banks 12.4 23% 4.5 3,601

Knight-Ridder Inc. Media 12.8 20% 2.6 5,777

15

Firm being valued Industry EV/EBIT ROE Debt/EBIT Size International Flavors & Fragrances (IFF)

Materials 12.9 23% 2.7 3,356

11.8 12.9

Actual EV/EBIT of IIF

Prediction of the EV/EBIT multiple (harmonic mean

of peers)

8%

Valuation error │(11.8-12.9)/12.9│

A distinct pattern: Combining fundamentals seems to work

Absolute percentage errors and ranks (brackets) of valuations based on each selection method

Industry ROE ROE Debt/EBIT

ROE Debt/EBIT Size

ROE Debt/EBIT Size Growth

ROE Debt/EBIT Size Growth EBIT-margin

Median 0.255 (4) 0.292 (6) 0.260 (5) 0.250 (3) 0.228 (2) 0.222 (1) Mean 0.341 (3) 0.390 (6) 0.351 (5) 0.343 (4) 0.309 (2) 0.307 (1) IQ 0.330 (3) 0.364 (6) 0.335 (5) 0.330 (4) 0.297 (2) 0.291 (1)

Median 0.407 (2) 0.531 (6) 0.504 (5) 0.477 (4) 0.470 (3) 0.254 (1) Mean 0.576 (2) 0.761 (6) 0.720 (5) 0.693 (4) 0.671 (3) 0.360 (1) IQ 0.463 (2) 0.499 (6) 0.483 (5) 0.480 (3) 0.481 (4) 0.332 (1)

Median 0.349 (6) 0.298 (5) 0.283 (4) 0.275 (3) 0.241 (2) 0.240 (1) Mean 0.444 (6) 0.377 (5) 0.360 (4) 0.348 (3) 0.316 (2) 0.313 (1) IQ 0.416 (6) 0.352 (5) 0.347 (4) 0.335 (3) 0.312 (1) 0.313 (2)

Median 0.286 (5) 0.297 (6) 0.286 (4) 0.279 (3) 0.244 (2) 0.240 (1) Mean 0.382 (6) 0.375 (5) 0.363 (4) 0.354 (3) 0.325 (2) 0.325 (1) IQ 0.380 (6) 0.352 (5) 0.347 (4) 0.340 (3) 0.321 (1) 0.321 (2)

16

EV/EBIT

EV/Sales

P/B

P/E

The pattern remains intra-industry

Absolute percentage errors and ranks (brackets) of valuations based on each selection method

Industry ROE (same industry)

ROE Debt/EBIT (s.industry)

ROE Debt/EBIT Size (s.industry)

ROE Debt/EBIT Size Growth (s.industry)

ROE Debt/EBIT Size Growth EBIT-% (s.industry)

Median 0.255 (6) 0.244 (5) 0.219 (4) 0.215 (3) 0.206 (2) 0.203 (1) Mean 0.341 (6) 0.321 (5) 0.295 (4) 0.290 (3) 0.279 (2) 0.275 (1) IQ 0.330 (6) 0.311 (5) 0.296 (4) 0.292 (3) 0.280 (2) 0.279 (1)

Median 0.407 (6) 0.380 (5) 0.364 (4) 0.344 (3) 0.338 (2) 0.271 (1) Mean 0.576 (6) 0.537 (5) 0.514 (4) 0.492 (3) 0.483 (2) 0.369 (1) IQ 0.463 (6) 0.452 (5) 0.439 (4) 0.426 (3) 0.423 (2) 0.357 (1)

Median 0.349 (6) 0.247 (4) 0.249 (5) 0.243 (3) 0.240 (1) 0.241 (2) Mean 0.444 (6) 0.318 (4) 0.322 (5) 0.312 (3) 0.310 (2) 0.307 (1) IQ 0.416 (6) 0.317 (4) 0.319 (5) 0.311 (3) 0.310 (2) 0.304 (1)

Median 0.286 (6) 0.247 (5) 0.244 (4) 0.241 (3) 0.228 (2) 0.225 (1) Mean 0.382 (6) 0.322 (5) 0.322 (4) 0.320 (3) 0.307 (2) 0.306 (1) IQ 0.380 (6) 0.319 (3) 0.327 (4) 0.331 (5) 0.316 (2) 0.311 (1)

17

EV/EBIT

EV/Sales

P/B

P/E

Robustness checks

Robustness checks performed in this study

18

Number of firms in peer group

Across time

Across size

Number of firms in peer group

EV/Sales

19

• The ranking of selection methods remain stable across various numbers of peers • Incrementally increasing accuracy when peers are added • Similar results for all evaluated multiples

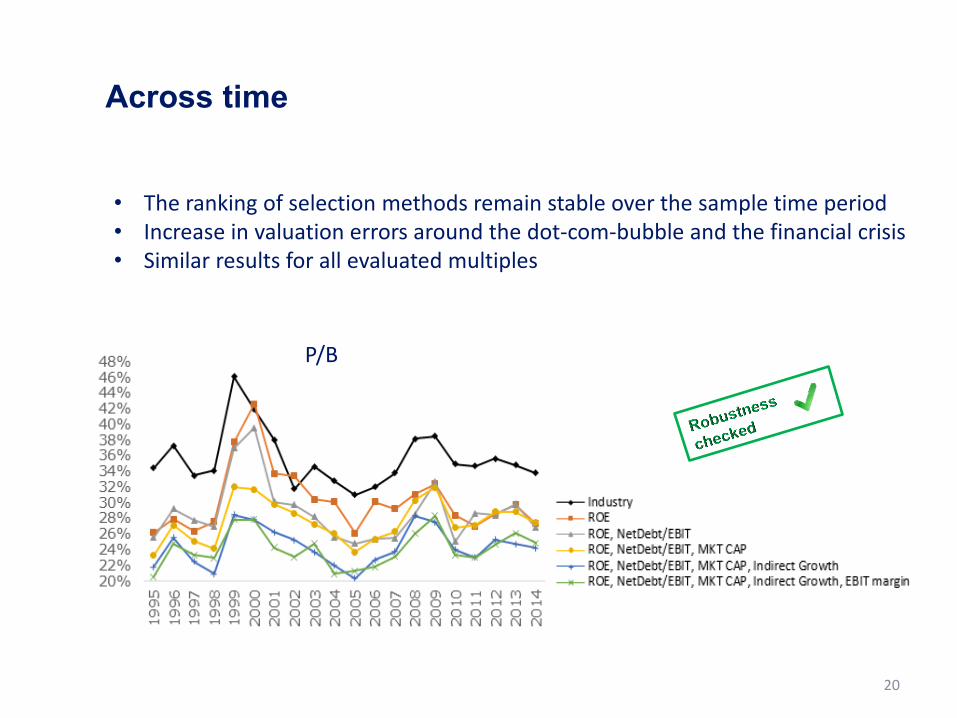

Across time

P/B

20

• The ranking of selection methods remain stable over the sample time period • Increase in valuation errors around the dot-com-bubble and the financial crisis • Similar results for all evaluated multiples

Industry ROE ROE Debt/EBIT

ROE Debt/EBIT Size

ROE Debt/EBIT Size Growth

ROE Debt/EBIT Size Growth EBIT-margin

P/B:

S&P 500 0.326 (6) 0.256 (4) 0.273 (5) 0.222 (3) 0.221 (2) 0.210 (1)

S&P 400 0.367 (6) 0.256 (5) 0.234 (4) 0.204 (2) 0.217 (3) 0.199 (1)

S&P 600 0.343 (6) 0.278 (5) 0.260 (4) 0.259 (3) 0.213 (2) 0.200 (1)

21

Across size

• The ranking of selection methods remain stable over the sample time period • Seems to be less estimation error in S&P 500 compared to the other two indices • Similar results for all evaluated multiples

Conclusions

22

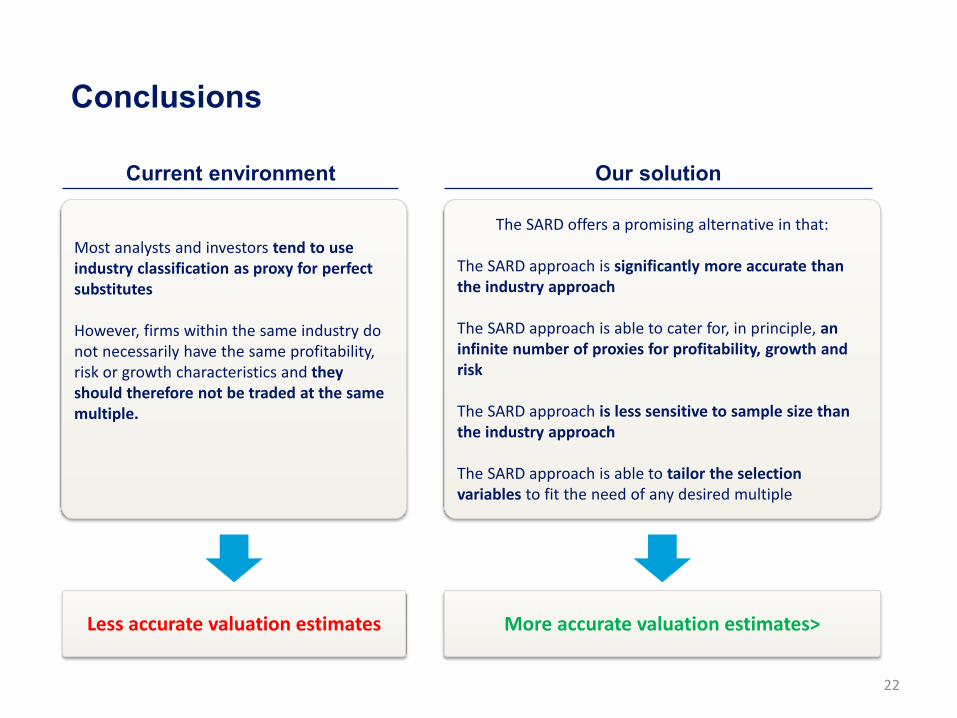

Most analysts and investors tend to use industry classification as proxy for perfect substitutes However, firms within the same industry do not necessarily have the same profitability, risk or growth characteristics and they should therefore not be traded at the same multiple.

Current environment

Less accurate valuation estimates

The SARD offers a promising alternative in that: The SARD approach is significantly more accurate than the industry approach The SARD approach is able to cater for, in principle, an infinite number of proxies for profitability, growth and risk The SARD approach is less sensitive to sample size than the industry approach The SARD approach is able to tailor the selection variables to fit the need of any desired multiple

Our solution

More accurate valuation estimates>

Agenda

23

1 Comparable firm selection for multiple valuation

2 Our idea

3 How did we test it and how does it work?

4 Questions