Embed Size (px)

Citation preview

CHINA SKY CHEMICAL FIBRE CO., LTD SPECIAL AUDIT REPORT 19 JUNE 2013

Stone Forest Corporate Advisory Pte Ltd 12

EXECUTIVE SUMMARY

Background Information

1. China Sky Chemical Fibre Co., Ltd (“the Company”) was incorporated in Cayman

Islands on 29 March 2005 and was listed on the Mainboard of Singapore Exchange

Limited (“SGX”) on 3 October 2005. The principal activity of the Company is that of an

investment holding company.

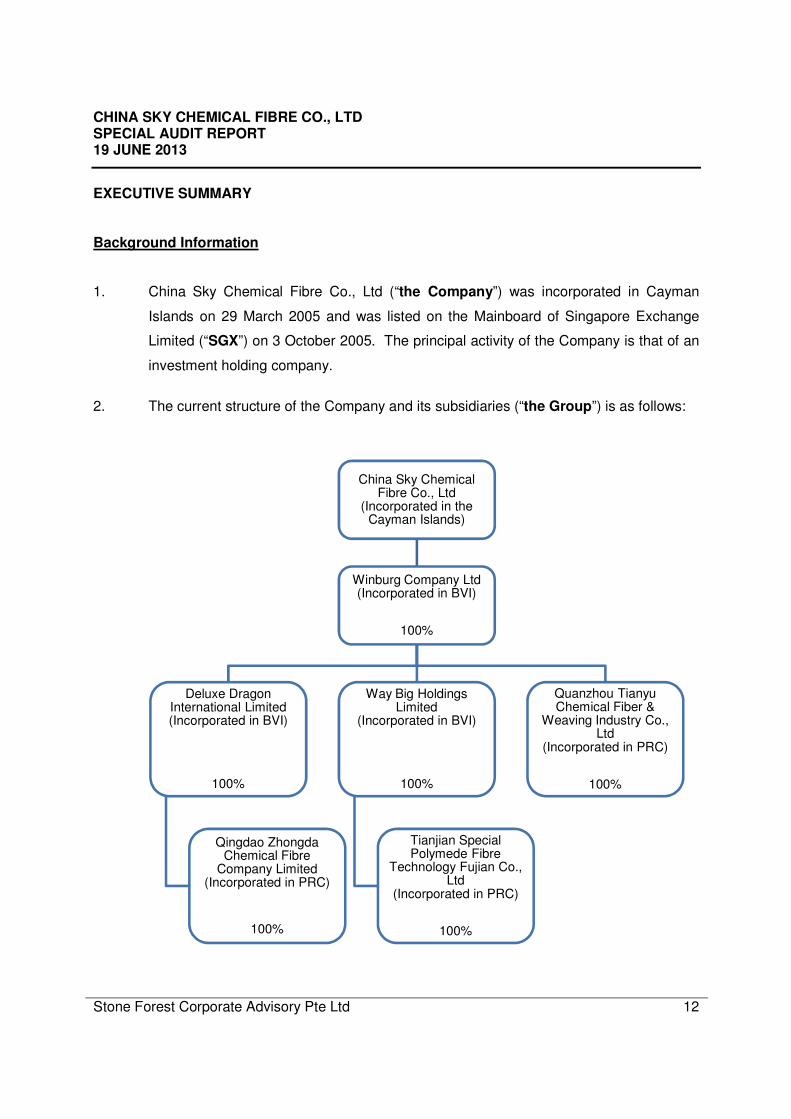

2. The current structure of the Company and its subsidiaries (“the Group”) is as follows:

China Sky Chemical Fibre Co., Ltd

(Incorporated in the Cayman Islands)

Winburg Company Ltd (Incorporated in BVI)

100%

Quanzhou Tianyu Chemical Fiber &

Weaving Industry Co., Ltd

(Incorporated in PRC)

100%

Way Big Holdings Limited

(Incorporated in BVI)

100%

Tianjian Special Polymede Fibre

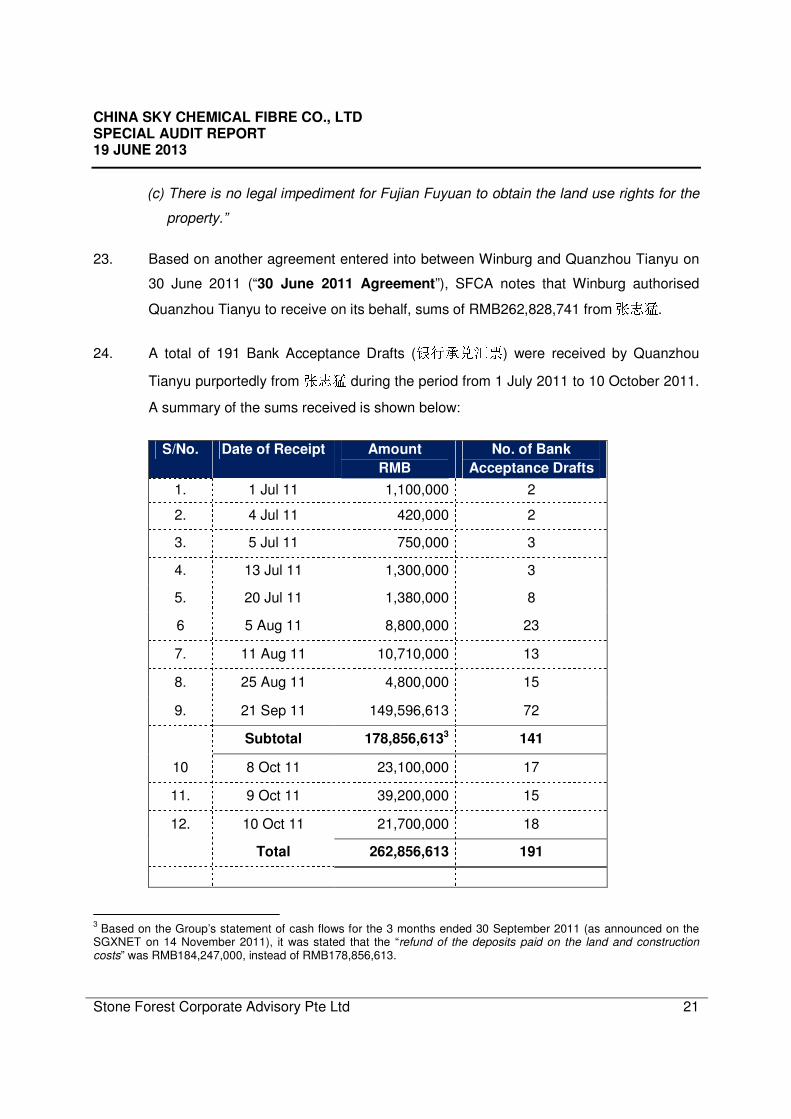

Technology Fujian Co., Ltd

(Incorporated in PRC)

100%

Deluxe Dragon International Limited (Incorporated in BVI)

100%

Qingdao Zhongda Chemical Fibre

Company Limited (Incorporated in PRC)

100%

CHINA SKY CHEMICAL FIBRE CO., LTD SPECIAL AUDIT REPORT 19 JUNE 2013

Stone Forest Corporate Advisory Pte Ltd 13

3. The Company is the ultimate holding company of Quanzhou Tianyu Chemical Fibre &

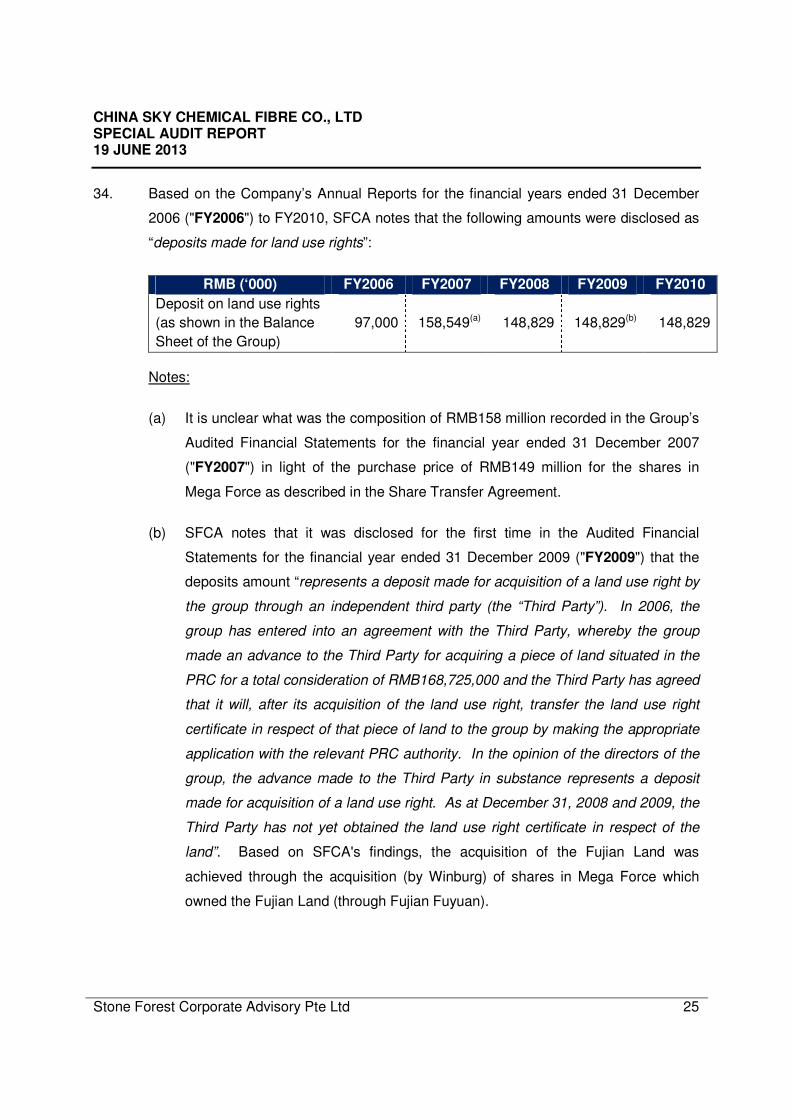

Weaving Industry Co., Ltd (“Quanzhou Tianyu”), Tianjian Special Polymede Fibre

Technology Fujian Co., Ltd (“Tianjian”) and Qingdao Zhongda Chemical Fibre

Company Limited (“Qingdao Zhongda”). Quanzhou Tianyu, Tianjian and Qingdao

Zhongda are incorporated in The People’s Republic of China (“PRC”) (collectively

known as “PRC Operating Subsidiaries”). The PRC Operating Subsidiaries are

principally engaged in the manufacture and sale of chemical fibres (mainly high-end

nylon fibres).

4. Quanzhou Tianyu was previously a wholly-owned subsidiary of Kam Wai Chemical

Fibre Industrial Limited (“Kam Wai”), an investment holding company, which was

incorporated in Hong Kong on 25 January 2002. Kam Wai was in turn wholly-owned

by Winburg Company Ltd ("Winburg"). According to the SGXNET announcement on

30 April 2012, Kam Wai was dissolved on 27 April 2012 and Quanzhou Tianyu

subsequently became a wholly-owned subsidiary of Winburg.

5. On 16 November 2011, pursuant to Mainboard Rule 704(12), SGX issued a directive to

the Company to appoint a special auditor to investigate certain affairs of the Company.

In compliance with the directive, the Audit Committee (“AC”) of the Company appointed

Stone Forest Corporate Advisory Pte Ltd (“SFCA”) on 25 October 2012 as the special

auditor.

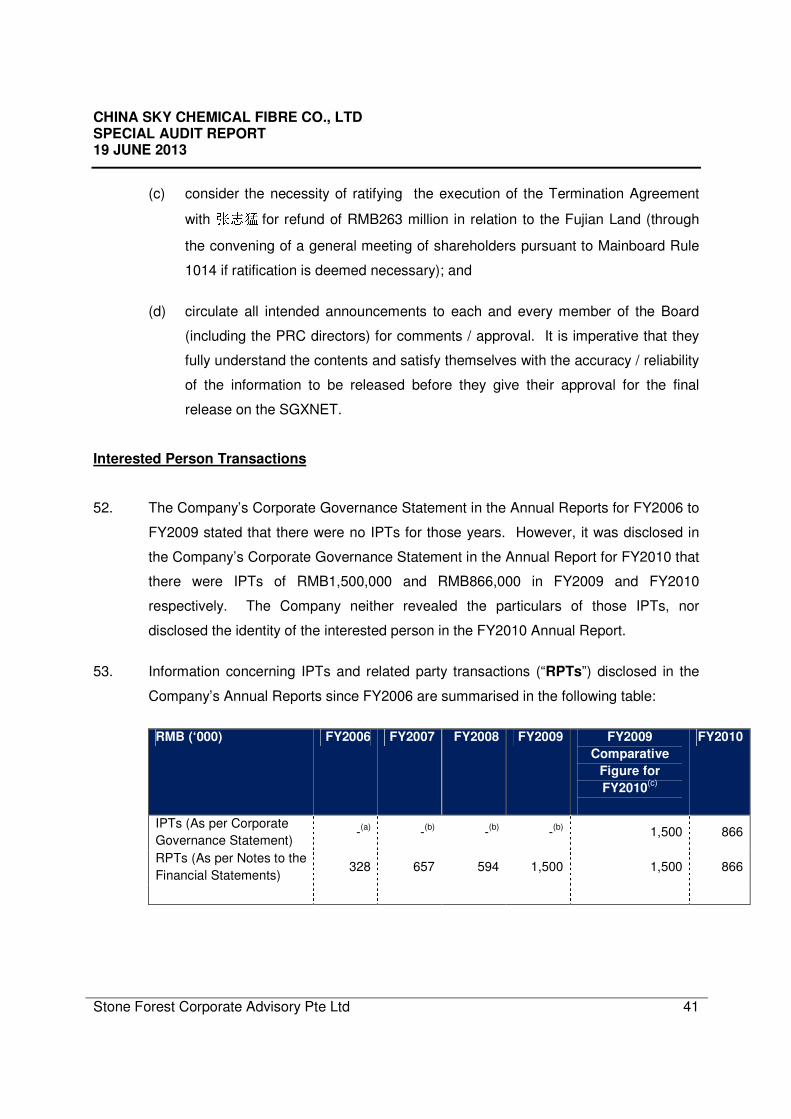

6. The AC of the Company has engaged SFCA to review:-

(a) The circumstances surrounding the major acquisitions related to and in

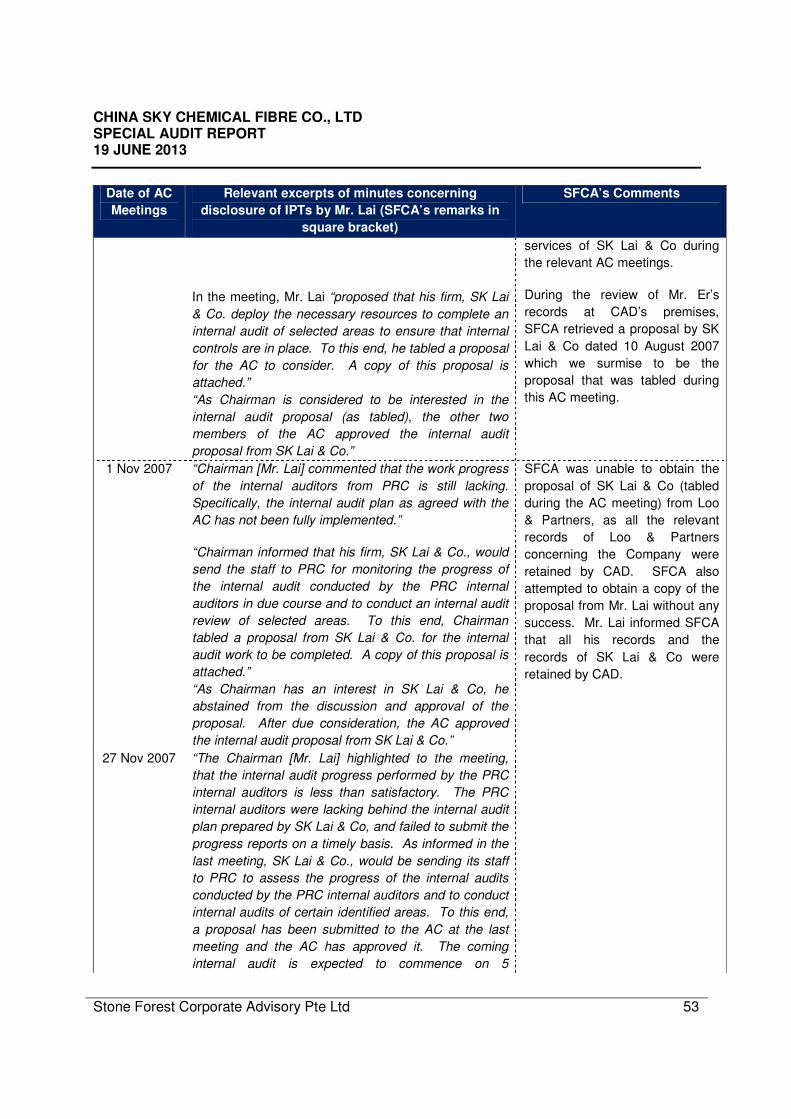

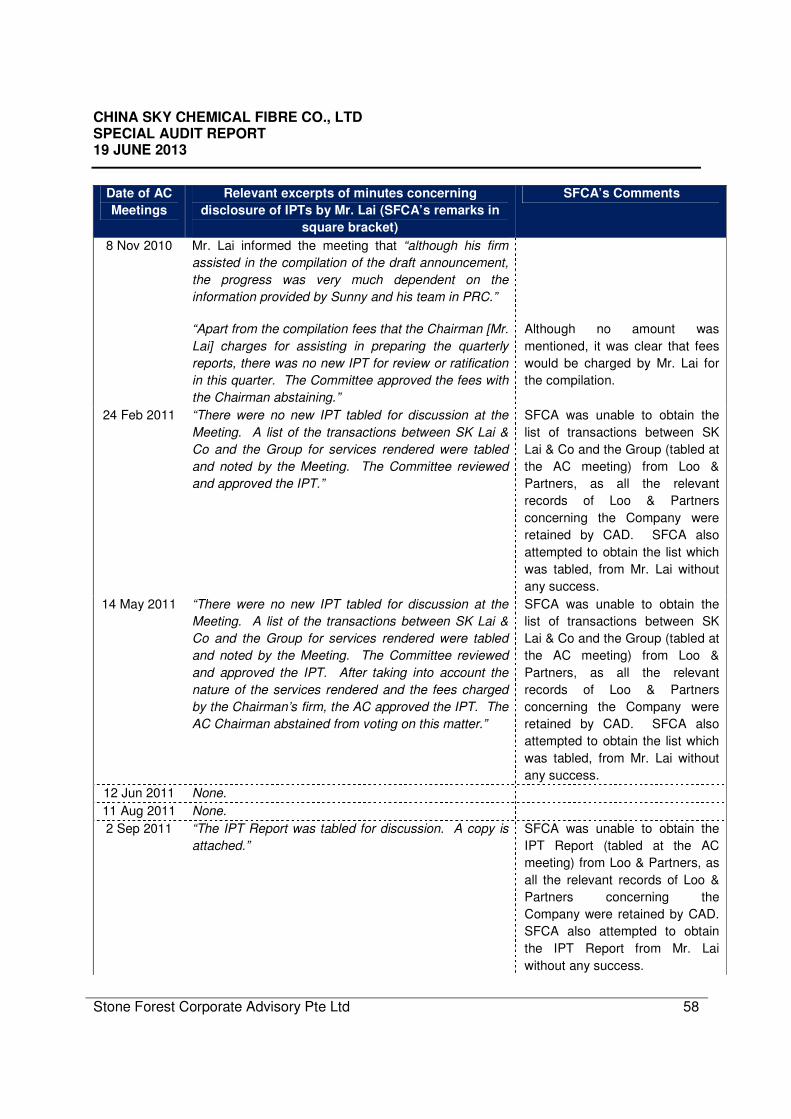

connection with the purchase (and subsequent return) of a piece of land in Fujian

province, PRC. Such ‘major acquisitions’ refer specifically to major acquisitions

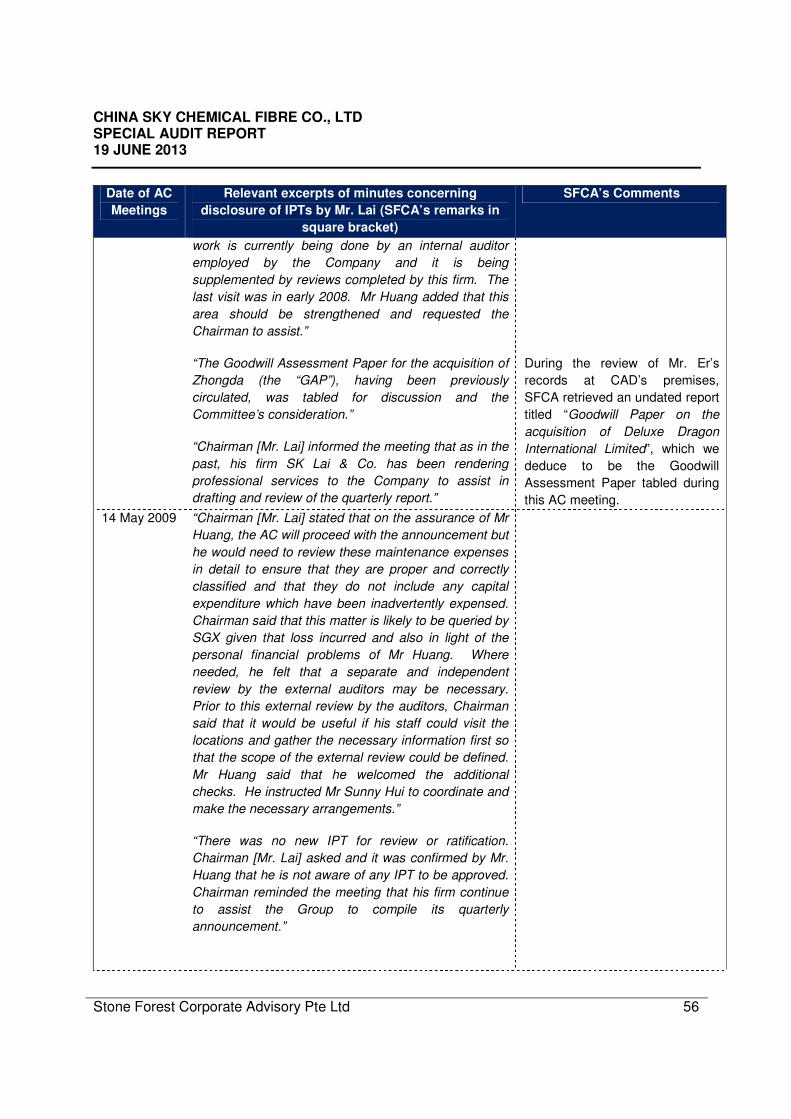

which are related to and in connection with all the circumstances surrounding the

abortive purchase of the Fujian Land;

(b) The nature, circumstances and manner in which interested person transactions

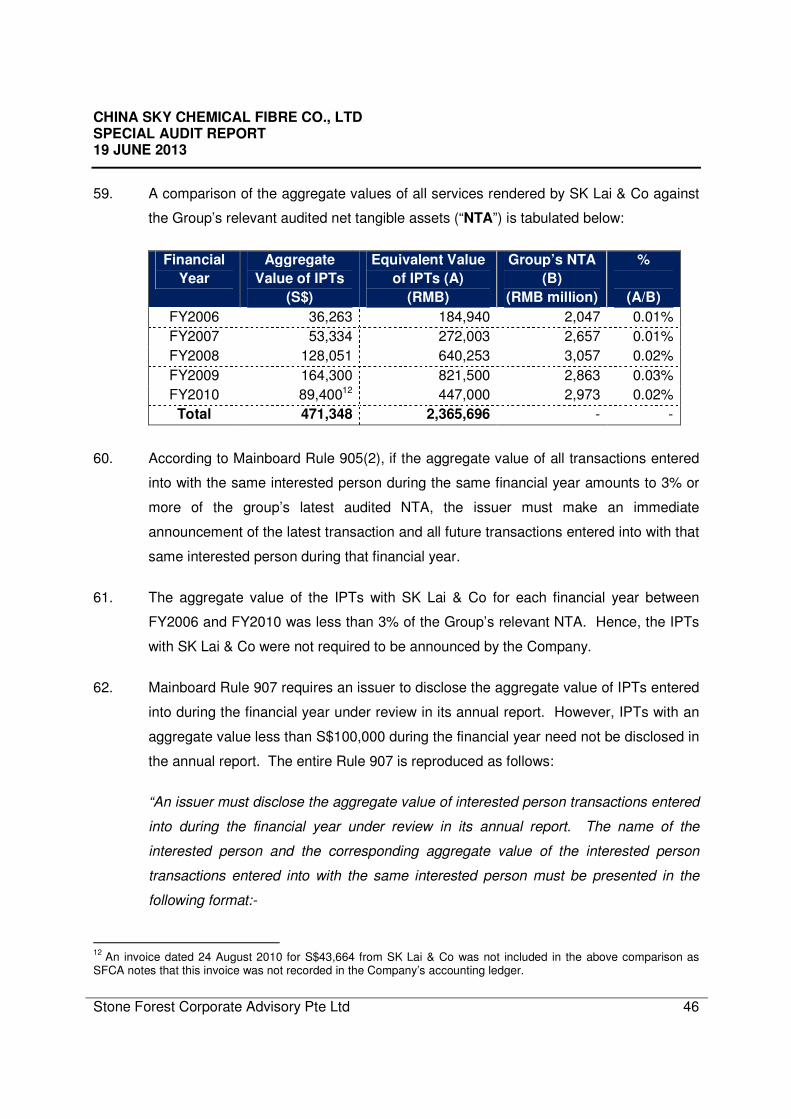

were conducted with a former independent director of the Company; and

CHINA SKY CHEMICAL FIBRE CO., LTD SPECIAL AUDIT REPORT 19 JUNE 2013

Stone Forest Corporate Advisory Pte Ltd 14

(c) The nature and circumstances of the transactions surrounding the repairs and

maintenance costs which were incurred in the first quarter of the financial year

2009.

Fujian Land

7. On 24 November 2006, the Company announced that it had managed to secure a land

in the Fujian province of China (“Fujian Land”). The relevant excerpts of the

announcement are reproduced below:

“The Company has managed to secure an offer of land of around 600 acres in Fujian

province at a very reasonable price. The land will be reserved for future expansion. As

the Company is presently considering venturing into upstream business, part of the

land to be acquired will also be reserved for such purposes.

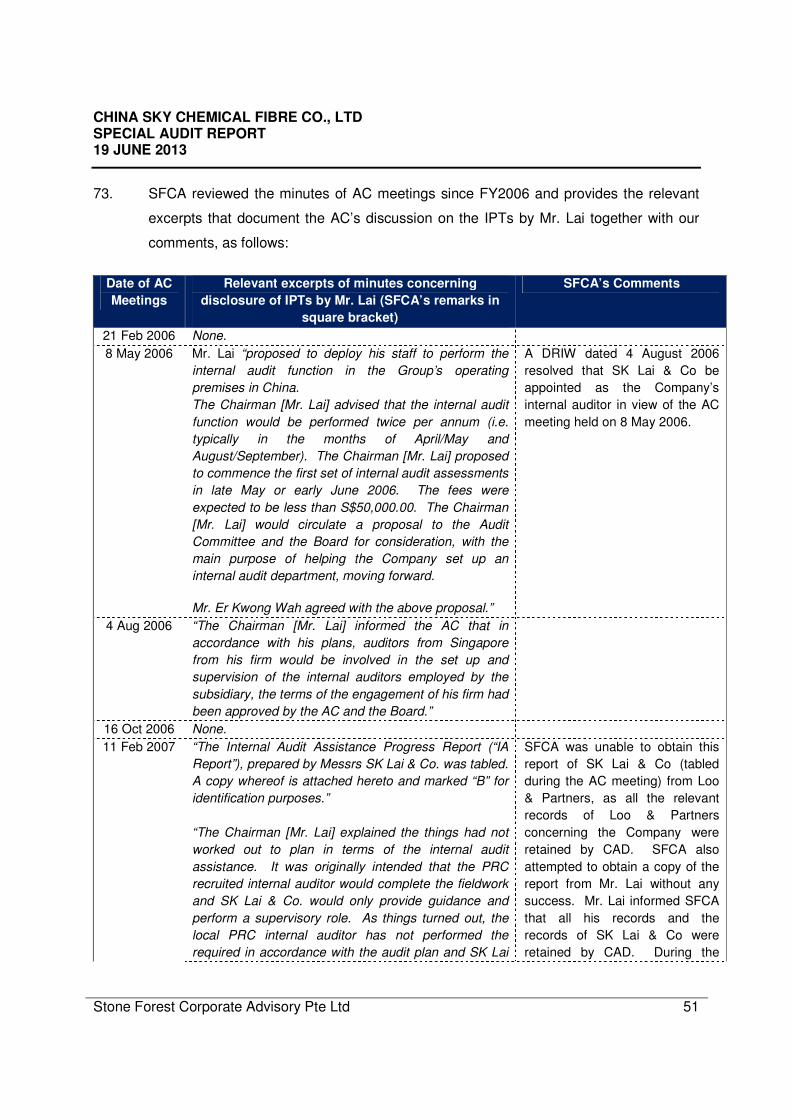

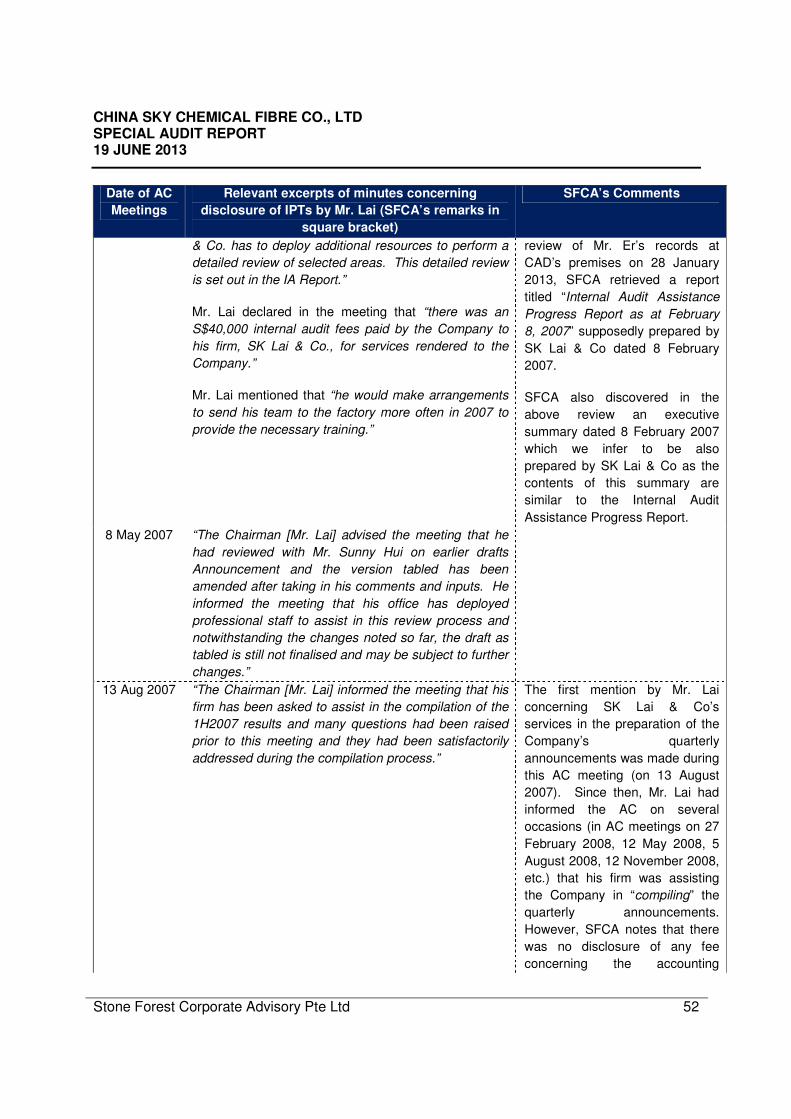

Accordingly, approximately 30% to 40% of the estimated net proceeds from the

Placement (after deducting estimated expenses) of approximately US$68.8 million will

be used for the acquisition of land for future expansion….”

8. On 22 December 2006, the Company made another announcement on the SGXNET

that they had utilised HK$70 million (from the placement of 80 million ordinary shares in

the Company on 1 December 2006) towards the acquisition of the Fujian Land.

According to the same announcement, the acquisition of the Fujian Land was made

through the acquisition of a new wholly-owned subsidiary, Mega Force Investments

Limited (“Mega Force”), by Winburg. Winburg is a wholly-owned subsidiary of the

Company.

9. During the visit to the Company’s office premises in Quanzhou in November 2012,

SFCA was provided with a legal due diligence report prepared by Fujian Qiaosheng

Law Firm (“Fujian Qiaosheng”) dated 25 October 2012 (“Legal Due Diligence

Report”). The Company had appointed Fujian Qiaosheng to perform a legal review of

the transactions relating to the Fujian Land at the request of its current Group CEO, Mr.

Ling Yew Kong. The salient points of the Legal Due Diligence Report (which was

CHINA SKY CHEMICAL FIBRE CO., LTD SPECIAL AUDIT REPORT 19 JUNE 2013

Stone Forest Corporate Advisory Pte Ltd 15

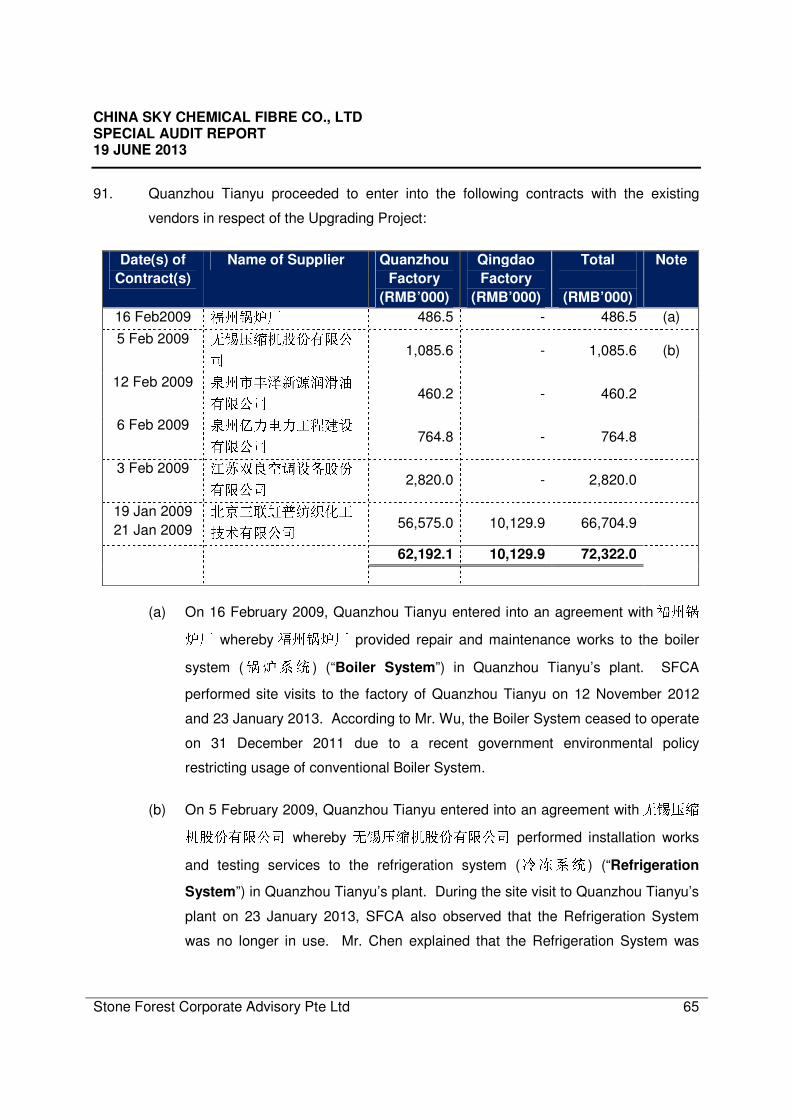

written in Chinese) are translated and reproduced (in English) in the following

paragraphs:

(a) Mega Force was incorporated in the British Virgin Islands on 5 January 2005.

The sole shareholder of Mega Force (during the material time) was as follows:

Name of Sole Shareholder Period ���

Before 18 Dec 2006

Winburg Between 18 Dec 2006 and 17 Oct 2011 ��� From 18 Oct 2011 todate

(b) Fujian Fuyuan Chemical Co., Ltd ("Fujian Fuyuan") was incorporated in PRC on

15 September 2005. The sole shareholder of Fujian Fuyuan was Mega Force.

(c) Fujian Fuyuan and the Quanzhou City Quangang District People’s Government

(��������) (“Local PRC Authority”) entered into an agreement on

20 April 2004 for the purchase of the Fujian Land1.

(d) Subsequently, on 20 October 2006, Fujian Fuyuan and the Local PRC Authority

entered into a supplementary agreement for the purchase of the Fujian Land.

(e) The Fujian Land is located at Quanzhou City Quangang District. It has a land

area of 401,728.68 square metres (approximately 602 acres).

(f) On 2 December 2006, Winburg and

���entered into a share transfer

agreement for the acquisition of 100% interest held by���

in Mega Force

(“Share Transfer Agreement”). The key terms of the Share Transfer

Agreement were as follows:

(i) With the acquisition of Mega Force, Winburg gained full control over Fujian

Fuyuan and the Fujian Land;

1 The 20 April 2004 agreement was entered into between the Local PRC Authority and � � (not Fujian Fuyuan).

While the Legal Due Diligence Report erroneously stated that the agreement was entered between the Local PRC Authority and Fujian Fuyuan on 20 April 2004, SFCA notes that it correctly pointed out that Fujian Fuyuan was only incorporated on 15 September 2005.

CHINA SKY CHEMICAL FIBRE CO., LTD SPECIAL AUDIT REPORT 19 JUNE 2013

Stone Forest Corporate Advisory Pte Ltd 16

(ii) The purchase consideration for the acquisition of Mega Force was RMB149

million. ���

would be responsible for the payment of any outstanding

amount due for the purchase of the Fujian Land; and

(iii)

���would be responsible for obtaining the land use rights certificate for

the Fujian Land, failing which, Winburg could terminate the Share Transfer

Agreement. In the event that the Share Transfer Agreement is terminated

by Winburg, ���

has to refund to Winburg the sum of RMB149 million

paid for the Fujian Land and all costs incurred for the development of the

Fujian Land.

(g) The sum of RMB149 million was paid in full between 19 December 2006 and 24

December 2007.

(h) According to the share register provided by Winburg, Mega Force was a

subsidiary of Winburg during the period from 18 December 2006 to 17 October

2011.

(i) Winburg had entrusted Quanzhou Tianyu to manage the development of the

Fujian Land for RMB114 million.

(j) The Local PRC Authority confirmed that (in the early stages) the progress on the

development of the Fujian Land was smooth. However, there were issues (such

as expropriation of seabed, migration of graves and protests by the locals) which

caused the delay in the development of the Fujian Land. As at 27 June 2011, the

Local PRC Authority could not complete the conversion of the land from

agricultural and forestry purposes to non-agricultural purpose.

(k) As

��� was unable to obtain the land use rights certificate, it was agreed

between Winburg and ���

that the Share Transfer Agreement entered on 2

December 2006 be terminated. On 27 June 2011, both parties signed an

agreement terminating the Share Transfer Agreement (“Termination

Agreement”).

CHINA SKY CHEMICAL FIBRE CO., LTD SPECIAL AUDIT REPORT 19 JUNE 2013

Stone Forest Corporate Advisory Pte Ltd 17

(l) In light of the Termination Agreement, Winburg transferred its 100% shareholding

in Mega Force back to ���

and returned the full rights and control over Fujian

Fuyuan and the Fujian Land to ���

.

(m) Winburg authorised Quanzhou Tianyu to receive on its behalf, funds of RMB263

million from���

. Winburg had received the full refund of RMB263 million from ��� and thus did not suffer any losses on the Fujian Land.

(n) The transactions (i.e. entering of the Share Transfer Agreement and Termination

Agreement) between Winburg and ���

were legitimate and the signing of the

Share Transfer Agreement and the Termination Agreement were not related

party transactions.

(o) According to the land agreement entered into between Fujian Fuyuan and the

Local PRC Authority (in 2006), the red line map (���) of Fujian Land and the

relevant documents, it was confirmed that Fujian Fuyuan had the rights to

develop the Fujian Land.

10. During the interview with

��� on 13 November 2012, he informed SFCA that in April

2004, he signed an agreement (“Letter of Intent”) with the Local PRC Authority to

purchase the Fujian Land for RMB168 million. After the incorporation of Fujian Fuyuan

in September 2005, Fujian Fuyuan formally entered into an agreement with the Local

PRC Authority (in October 2006) for the purchase of the Fujian Land at RMB149 million

(“Land Use Agreement”). SFCA was shown the Letter of Intent and Land Use

Agreement by ���

on 14 November 2012, but was not permitted to retain copies of

these documents.

11. The Share Transfer Agreement was entered into between Winburg and

��� on 2

December 2006 in respect of the acquisition of the Fujian Land. Under the Share

Transfer Agreement, it was agreed that Winburg would purchase the shares fully held

by ���

in Mega Force for a consideration of RMB149 million which was to be paid

before 31 December 2007.

CHINA SKY CHEMICAL FIBRE CO., LTD SPECIAL AUDIT REPORT 19 JUNE 2013

Stone Forest Corporate Advisory Pte Ltd 18

12. Fujian Fuyuan was described in the Share Transfer Agreement as a wholly owned

subsidiary of Mega Force. At the time of the acquisition of Mega Force in late 2006,

Fujian Fuyuan apparently owned the Fujian Land but the land use rights (for non-

agricultural purpose) had yet to be obtained. While the acquisition of Mega Force was

announced by the Company on the SGXNET on 22 December 2006, SFCA notes that

no information was disclosed via announcement or in the Company’s Annual Report

that Fujian Fuyuan was a subsidiary of Mega Force.

13. It was stated in the Share Transfer Agreement that part of the Fujian Land was

reserved for agricultural and forestry purposes. In the event that ���

fails to obtain

the land use rights (for non-agricultural purpose) within a period of time (not specified in

the Share Transfer Agreement), Winburg could terminate the Share Transfer

Agreement and ���

would have to repay the purchase consideration (i.e. RMB149

million) and all the costs incurred on the development of the Fujian Land.

14. SFCA was provided with a copy of an agreement dated 10 January 2008 entered into

between ���������������� !"#$ ! (“%&'(”) and

Quanzhou Tianyu (“Guangxi Jiangong Agreement”). According to the Guangxi

Jiangong Agreement, SFCA notes that ���� was engaged to develop the Fujian

Land and the major works to be carried by them were as follows:

(a) Land excavation ()*+,);

(b) Land refilling ()*-.);

(c) Blasting (/*01); and

(d) Land leveling (2345).

15. On 8 October 2008, Quanzhou Tianyu and ���� entered into a construction

agreement (“Phase One Construction Agreement”) to carry out the land-leveling

works. The construction works were carried out at the site located at ���6789

CHINA SKY CHEMICAL FIBRE CO., LTD SPECIAL AUDIT REPORT 19 JUNE 2013

Stone Forest Corporate Advisory Pte Ltd 19

:;<=> at an agreed sum of RMB58 million. The period of construction was stated

in the agreement to be between 10 October 2008 and 30 April 2009.

16. On 23 February 2009, Quanzhou Tianyu and ���� entered into a second

construction agreement (“Phase Two Construction Agreement”) to carry out further

land-leveling works at an agreed price of RMB56 million. The period of construction

was stated in the agreement to be between 24 February 2009 and 30 September 2009.

17. The Company’s external auditors in their various memoranda / reports to the AC

indicated that they had performed site inspections at the Fujian Land. SFCA also

performed a site visit on 22 January 2013, together with the representative of ����,

to the Fujian Land.

18. The total sum of RMB114 million was first disclosed in an announcement dated 7

March 2011 by the Company in response to SGX's queries on the Group’s full year

results for the financial year ended 31 December 2010 ("FY2010"). SFCA also notes

that the total sum of RMB114 million was disclosed in Note 15 of the Notes to the

Financial Statements at page 57 of the FY2010 Annual Report as “deposit for

construction work on a piece of land to be acquired”.

19. During an AC meeting on 7 January 2010, the former Group Financial Controller, Mr.

Hui San Wing (“Sunny”) informed the meeting that the Fujian Land “is still held by the

original proprietor / vendor company which is a PRC company (“Vendor”). The Vendor

has since run into difficulties in completing the sale or transfer…. Mega Force is now

looking into acquiring the Vendor, in whose name the land is registered in”. At the

material time of the AC meeting, the Fujian Land was owned by Fujian Fuyuan, which

was a subsidiary of Mega Force. SFCA notes that no due diligence was performed by

the Company prior to the acquisition of Fujian Fuyuan (and Mega Force).

20. Based on the Share Transfer Agreement,

���was responsible for completing the

conversion of the land use rights (to non-agricultural purpose). During the interview

with ���

on 13 November 2012, he informed SFCA that he was unable to obtain the

land use rights (for non-agricultural purpose) as required under the Share Transfer

CHINA SKY CHEMICAL FIBRE CO., LTD SPECIAL AUDIT REPORT 19 JUNE 2013

Stone Forest Corporate Advisory Pte Ltd 20

Agreement. Accordingly, at the request of Winburg in 2011, he agreed to terminate the

Share Transfer Agreement with a full refund to Winburg.

21. SFCA was provided with the Termination Agreement entered into between Winburg

and ���

dated 27 June 2011 terminating the Share Transfer Agreement entered on

2 December 20062. The salient points of the Termination Agreement are as follows:

(a) The relevant governmental authority (����) could not convert the land from

agricultural and forestry purposes to non-agricultural purpose and accordingly

both Winburg and ���

agreed to terminate the Share Transfer Agreement;

(b) Winburg had to (within 100 days) transfer its 100% shares in Mega Force to

��� and at the same time, return all documents in relation to Fujian Fuyuan and

the Fujian Land to ���

; and

(c) In return,

��� will (within 100 days) make payment of RMB263 million to the

bank account designated by Winburg.

22. According to a valuation report dated 7 March 2011 prepared by Asset Appraisal

Limited (“Asset Appraisal”) (“Fujian Land Valuation Report”), the Fujian Land,

situated at Xiazhu Village, Jieshan Town, Quangang District, Quanzhou City, was

valued at RMB264 million as at 31 December 2010. It was stated in the Fujian Land

Valuation Report that Asset Appraisal had relied on the legal opinion of Fujian

Qiaosheng issued on 30 January 2011. The legal opinions of Fujian Qiaosheng quoted

in the Fujian Land Valuation Report are reproduced verbatim below:

“ (a) The land use rights of the property were legally held by Fujian Fuyuan;

(b) Fujian Fuyuan has settled the land premium in full; and

2 The former AC Chairman, Mr. Lai and former AC member, Mr. Yeap, in their joint maxwellisation response dated 5

June 2013, informed SFCA that “the Termination Agreement entered between Winburg and [?@A] dated 27 June 2011 was never disclosed to the IDs. The ex-IDs only discovered the existence of all these agreements when they received [SFCA’s] [draft] report”.

CHINA SKY CHEMICAL FIBRE CO., LTD SPECIAL AUDIT REPORT 19 JUNE 2013

Stone Forest Corporate Advisory Pte Ltd 21

(c) There is no legal impediment for Fujian Fuyuan to obtain the land use rights for the

property.”

23. Based on another agreement entered into between Winburg and Quanzhou Tianyu on

30 June 2011 (“30 June 2011 Agreement”), SFCA notes that Winburg authorised

Quanzhou Tianyu to receive on its behalf, sums of RMB262,828,741 from���

.

24. A total of 191 Bank Acceptance Drafts (BCDEFG) were received by Quanzhou

Tianyu purportedly from ���

during the period from 1 July 2011 to 10 October 2011.

A summary of the sums received is shown below:

S/No. Date of Receipt Amount

RMB

No. of Bank

Acceptance Drafts

1. 1 Jul 11 1,100,000 2

2. 4 Jul 11 420,000 2

3. 5 Jul 11 750,000 3

4. 13 Jul 11 1,300,000 3

5. 20 Jul 11 1,380,000 8

6 5 Aug 11 8,800,000 23

7. 11 Aug 11 10,710,000 13

8. 25 Aug 11 4,800,000 15

9. 21 Sep 11 149,596,613 72

Subtotal 178,856,6133 141

10 8 Oct 11 23,100,000 17

11. 9 Oct 11 39,200,000 15

12. 10 Oct 11 21,700,000 18

Total 262,856,613 191

3 Based on the Group’s statement of cash flows for the 3 months ended 30 September 2011 (as announced on the

SGXNET on 14 November 2011), it was stated that the “refund of the deposits paid on the land and construction costs” was RMB184,247,000, instead of RMB178,856,613.

CHINA SKY CHEMICAL FIBRE CO., LTD SPECIAL AUDIT REPORT 19 JUNE 2013

Stone Forest Corporate Advisory Pte Ltd 22

25. SFCA notes that there was a slight discrepancy in the amount received from ���

.

The 30 June 2011 Agreement states that the amount to be received from ���

was

RMB262,828,741 but the actual amount received was RMB262,856,613, giving rise to

a surplus of RMB27,872. SFCA reviewed the accounting ledgers of Quanzhou Tianyu

and noted that the surplus of RMB27,872 was recorded as interest income of

Quanzhou Tianyu.

26. Although the Termination Agreement states that the payments from

��� would be

remitted into the bank account designated by Winburg, SFCA notes that the payments

were made through Bank Acceptance Drafts instead. During his interview on 14

November 2012, Mr. Hu Xiao Jin ("Mr. Hu") confirmed to SFCA that Quanzhou Tianyu

had received the payments of RMB263 million from ���

via Bank Acceptance Drafts,

which are negotiable financial instruments in China.

27. Although SFCA was provided with copies of the Bank Acceptance Drafts amounting to

RMB262,856,613, SFCA notes that Quanzhou Tianyu did not keep copies of the

overleaf of the Bank Acceptance Drafts. In the circumstances, SFCA was unable to

determine:

(a) the original source or the transferor of the Bank Acceptance Drafts was indeed ���

(or parties related to him); and

(b) the bearer or payee of the Bank Acceptance Drafts to be Quanzhou Tianyu.

28. The Bank Acceptance Drafts of RMB263 million were subsequently used to pay a

major supplier of raw materials.

29. In the course of reviewing the current AC Chairman, Mr. Er Kwong Wah's ("Mr. Er")

past emails, SFCA notes that there was an email (dated 29 June 2011) sent by Sunny

to the AC members and Loo & Partners LLP ("Loo & Partners") enclosing an

agreement purportedly entered into between Quanzhou Tianyu and Fujian Fuyuan

dated 27 June 2011 (“Quanzhou Tianyu Agreement”). The Quanzhou Tianyu

Agreement was affixed with the official seals of Quanzhou Tianyu and Fujian Fuyuan.

CHINA SKY CHEMICAL FIBRE CO., LTD SPECIAL AUDIT REPORT 19 JUNE 2013

Stone Forest Corporate Advisory Pte Ltd 23

The subject of the email was “HI)3JKLM”. In the email, Sunny requested Mr.

Teo Boon Hai of Loo & Partners to prepare an announcement for the Fujian Land.

30. On the following day, 30 June 2011, Sunny sent another email to the AC members,

Loo & Partners and Mr. Huang Zhong Xuan ("Mr. Huang"), the former Group CEO,

enclosing an agreement purportedly entered into between Mega Force and Fujian

Fuyuan dated 27 June 2011 (“Mega Force Agreement”). The Mega Force Agreement

was affixed with the official seals of Mega Force and Fujian Fuyuan. The subject of the

email was “Fuyuen Land”. SFCA notes from the email that Sunny advised the parties

to ignore his previous email (presumably the email that was sent by him on 29 June

2011).

31. The salient points of the Mega Force Agreement are as follows:

(a) Both parties, Mega Force and Fujian Fuyuan, agree to terminate the agreement

for the purchase of the Fujian Land;

(b) Fujian Fuyuan will refund the purchase consideration for the Fujian Land of

RMB149 million and the development costs of RMB114 million; and

(c) The sums will be refunded (by way of remittance) to Quanzhou Tianyu

(authorised by Mega Force) as follows:

(i) RMB80 million by 31 July 2011;

(ii) RMB100 million by 31 August 2011; and

(iii) RMB82,828,741 by 30 September 2011.

32. The Termination Agreement was entered into between Winburg and

���, while the

Mega Force Agreement was purportedly entered into between Mega Force and Fujian

Fuyuan. The contents of the Mega Force Agreement were consistent with the

announcement made by the Company on the SGXNET on 1 July 2011. The relevant

excerpts of the announcement are reproduced below:

CHINA SKY CHEMICAL FIBRE CO., LTD SPECIAL AUDIT REPORT 19 JUNE 2013

Stone Forest Corporate Advisory Pte Ltd 24

“In 2006, Mega Force Investment Limited (“Mega Force”), an indirect wholly-owned

subsidiary of the Company, had entered into an agreement (“Agreement”) with the land

owner, Fujian Fuyuan Chemical Fibre Co., Ltd. (“Fujian Fuyuan”) to acquire the

Quanzhou Land. This acquisition has not been completed as the title transfer has not

been executed.

Given the foregoing, Mega Force has initiated negotiations with Fujian Fuyuan to

rescind the Agreement. It has now been agreed with Fujian Fuyuan that the

Agreement be rescinded. As a result, a sum of monies amounting to approximately

RMB263 million shall be paid by Fujian Fuyuan to Mega Force, being the total amount

spent by Mega Force on the Quanzhou Land.”

33. During the interview, Sunny acknowledged that his understanding was incorrect in light

of the Share Transfer Agreement. Sunny clarified that Mr. Huang was directly involved

in the negotiation process with���

on the acquisition and the subsequent return of

the Fujian Land. Sunny said that he was not aware of the existence of the Share

Transfer Agreement and the Termination Agreement at the material time in June 2011

because he was never involved in the negotiation process. The relevant excerpts of

Sunny’s interview transcript (which are translated to English from Chinese) are shown

below:

“I will explain the transaction from the beginning when the Company bought the Fujian

Land. According to my understanding, it was Mega Force which bought the Fujian

Land from Fujian Fuyuan. At the material time, the Company’s management

mentioned that the Fujian Land would be returned to the seller and the seller was

willing to refund the amount paid previously. Accordingly, I was of the view that an

agreement should be entered into with Fujian Fuyuan to document the return of the

Fujian Land. At that time, I informed parties in China to obtain an agreement with

Fujian Fuyuan on the return of the Fujian Land. I realised that the agreement given to

me was wrong as it was an agreement between Quanzhou Tianyu and Fujian Fuyuan.

Subsequently, based on my understanding of the transaction, I informed them that the

agreement should be entered into between Mega Force and Fujian Fuyuan and not

Quanzhou Tianyu and Fujian Fuyuan. That was how the 2 agreements came about.”

CHINA SKY CHEMICAL FIBRE CO., LTD SPECIAL AUDIT REPORT 19 JUNE 2013

Stone Forest Corporate Advisory Pte Ltd 25

34. Based on the Company’s Annual Reports for the financial years ended 31 December

2006 ("FY2006") to FY2010, SFCA notes that the following amounts were disclosed as

“deposits made for land use rights”:

RMB (‘000) FY2006 FY2007 FY2008 FY2009 FY2010

Deposit on land use rights

(as shown in the Balance

Sheet of the Group)

97,000 158,549(a) 148,829 148,829(b) 148,829

Notes:

(a) It is unclear what was the composition of RMB158 million recorded in the Group’s

Audited Financial Statements for the financial year ended 31 December 2007

("FY2007") in light of the purchase price of RMB149 million for the shares in

Mega Force as described in the Share Transfer Agreement.

(b) SFCA notes that it was disclosed for the first time in the Audited Financial

Statements for the financial year ended 31 December 2009 ("FY2009") that the

deposits amount “represents a deposit made for acquisition of a land use right by

the group through an independent third party (the “Third Party”). In 2006, the

group has entered into an agreement with the Third Party, whereby the group

made an advance to the Third Party for acquiring a piece of land situated in the

PRC for a total consideration of RMB168,725,000 and the Third Party has agreed

that it will, after its acquisition of the land use right, transfer the land use right

certificate in respect of that piece of land to the group by making the appropriate

application with the relevant PRC authority. In the opinion of the directors of the

group, the advance made to the Third Party in substance represents a deposit

made for acquisition of a land use right. As at December 31, 2008 and 2009, the

Third Party has not yet obtained the land use right certificate in respect of the

land”. Based on SFCA's findings, the acquisition of the Fujian Land was

achieved through the acquisition (by Winburg) of shares in Mega Force which

owned the Fujian Land (through Fujian Fuyuan).

CHINA SKY CHEMICAL FIBRE CO., LTD SPECIAL AUDIT REPORT 19 JUNE 2013

Stone Forest Corporate Advisory Pte Ltd 26

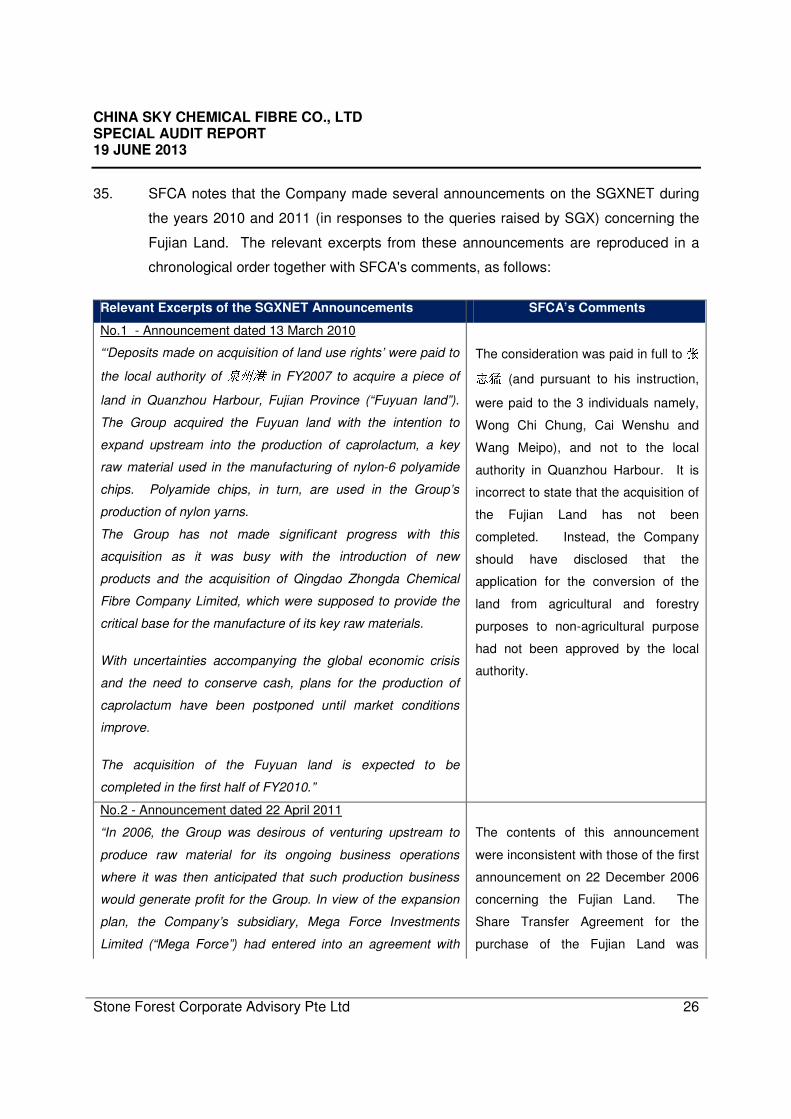

35. SFCA notes that the Company made several announcements on the SGXNET during

the years 2010 and 2011 (in responses to the queries raised by SGX) concerning the

Fujian Land. The relevant excerpts from these announcements are reproduced in a

chronological order together with SFCA's comments, as follows:

Relevant Excerpts of the SGXNET Announcements SFCA’s Comments

No.1 - Announcement dated 13 March 2010

“‘Deposits made on acquisition of land use rights’ were paid to

the local authority of NOP in FY2007 to acquire a piece of

land in Quanzhou Harbour, Fujian Province (“Fuyuan land”).

The Group acquired the Fuyuan land with the intention to

expand upstream into the production of caprolactum, a key

raw material used in the manufacturing of nylon-6 polyamide

chips. Polyamide chips, in turn, are used in the Group’s

production of nylon yarns.

The Group has not made significant progress with this

acquisition as it was busy with the introduction of new

products and the acquisition of Qingdao Zhongda Chemical

Fibre Company Limited, which were supposed to provide the

critical base for the manufacture of its key raw materials.

With uncertainties accompanying the global economic crisis

and the need to conserve cash, plans for the production of

caprolactum have been postponed until market conditions

improve.

The acquisition of the Fuyuan land is expected to be

completed in the first half of FY2010.”

The consideration was paid in full to QRS (and pursuant to his instruction,

were paid to the 3 individuals namely,

Wong Chi Chung, Cai Wenshu and

Wang Meipo), and not to the local

authority in Quanzhou Harbour. It is

incorrect to state that the acquisition of

the Fujian Land has not been

completed. Instead, the Company

should have disclosed that the

application for the conversion of the

land from agricultural and forestry

purposes to non-agricultural purpose

had not been approved by the local

authority.

No.2 - Announcement dated 22 April 2011

“In 2006, the Group was desirous of venturing upstream to

produce raw material for its ongoing business operations

where it was then anticipated that such production business

would generate profit for the Group. In view of the expansion

plan, the Company’s subsidiary, Mega Force Investments

Limited (“Mega Force”) had entered into an agreement with

The contents of this announcement

were inconsistent with those of the first

announcement on 22 December 2006

concerning the Fujian Land. The

Share Transfer Agreement for the

purchase of the Fujian Land was

CHINA SKY CHEMICAL FIBRE CO., LTD SPECIAL AUDIT REPORT 19 JUNE 2013

Stone Forest Corporate Advisory Pte Ltd 27

Relevant Excerpts of the SGXNET Announcements SFCA’s Comments

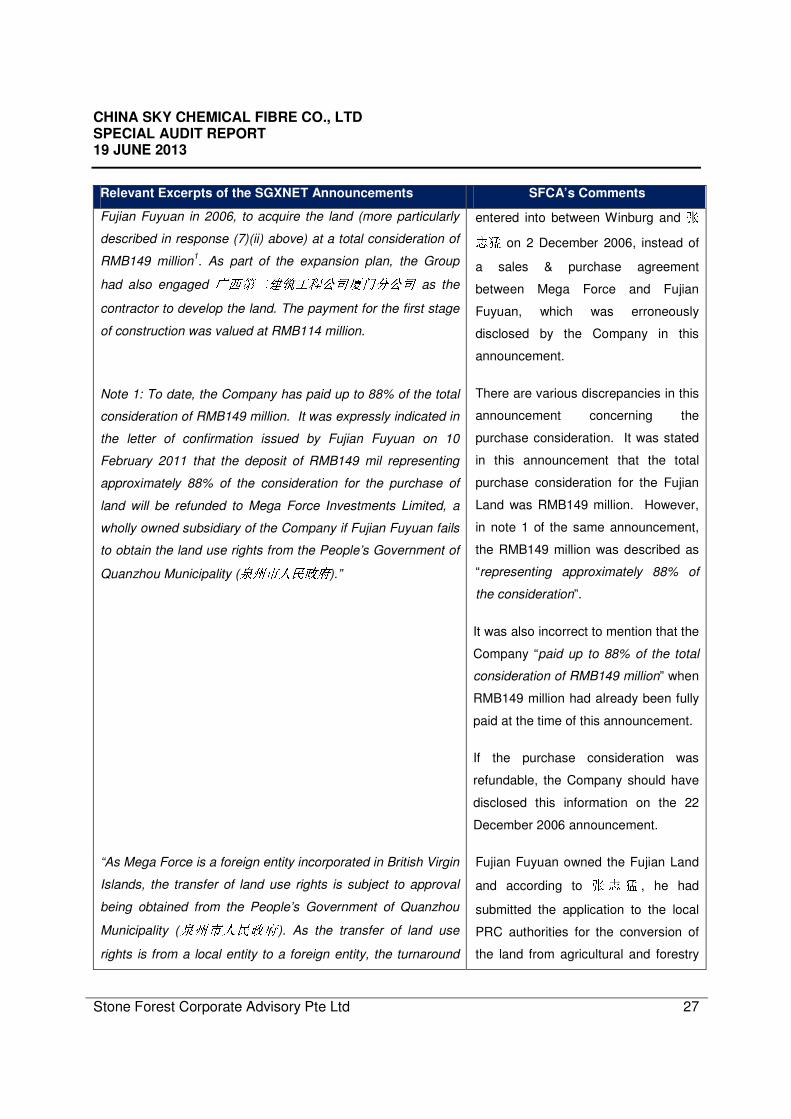

Fujian Fuyuan in 2006, to acquire the land (more particularly

described in response (7)(ii) above) at a total consideration of

RMB149 million1. As part of the expansion plan, the Group

had also engaged TUVWXYZ[\]^_`\] as the

contractor to develop the land. The payment for the first stage

of construction was valued at RMB114 million.

Note 1: To date, the Company has paid up to 88% of the total

consideration of RMB149 million. It was expressly indicated in

the letter of confirmation issued by Fujian Fuyuan on 10

February 2011 that the deposit of RMB149 mil representing

approximately 88% of the consideration for the purchase of

land will be refunded to Mega Force Investments Limited, a

wholly owned subsidiary of the Company if Fujian Fuyuan fails

to obtain the land use rights from the People’s Government of

Quanzhou Municipality (NOabcde).”

entered into between Winburg and QRS on 2 December 2006, instead of

a sales & purchase agreement

between Mega Force and Fujian

Fuyuan, which was erroneously

disclosed by the Company in this

announcement.

There are various discrepancies in this

announcement concerning the

purchase consideration. It was stated

in this announcement that the total

purchase consideration for the Fujian

Land was RMB149 million. However,

in note 1 of the same announcement,

the RMB149 million was described as

“representing approximately 88% of

the consideration”.

It was also incorrect to mention that the

Company “paid up to 88% of the total

consideration of RMB149 million” when

RMB149 million had already been fully

paid at the time of this announcement.

If the purchase consideration was

refundable, the Company should have

disclosed this information on the 22

December 2006 announcement.

“As Mega Force is a foreign entity incorporated in British Virgin

Islands, the transfer of land use rights is subject to approval

being obtained from the People’s Government of Quanzhou

Municipality (NOabcde). As the transfer of land use

rights is from a local entity to a foreign entity, the turnaround

Fujian Fuyuan owned the Fujian Land

and according to QRS , he had

submitted the application to the local

PRC authorities for the conversion of

the land from agricultural and forestry

CHINA SKY CHEMICAL FIBRE CO., LTD SPECIAL AUDIT REPORT 19 JUNE 2013

Stone Forest Corporate Advisory Pte Ltd 28

Relevant Excerpts of the SGXNET Announcements SFCA’s Comments

time in obtaining such approval is very extensive. As such, the

land is still under the name of Fujian Fuyuan.”

purposes to non-agricultural purpose. QRS did not apply to transfer the

land use rights to Mega Force, which

was already a sub-subsidiary of the

Company at the material time of the

announcement. Hence, this

announcement is incorrect and SFCA

is perturbed by the explanation.

“The Third Party referred to is Fujian Fuyuan Chemical Fiber

Co., Ltd. (fXghijklmnop\]) (“Fujian Fuyuan”).

Fujian Fuyuan is a PRC company incorporated in Quanzhou

in 2005 (the shareholder being an individual third party who is

independent and is not related to the Group). Fujian Fuyuan

is presently dormant but solvent.”

Fujian Fuyuan was a subsidiary of

Mega Force since its incorporation on

15 September 2005.

No. 3 - Announcement dated 29 April 2011 “Nevertheless, the Company wishes to confirm that the

individual third party, being the shareholder of Fujian Fuyuan,

is independent and is not related to the Group. The deposit

paid to Fujian Fuyuan is also legally refundable.”

At the time of this announcement,

Fujian Fuyuan was a subsidiary of

Mega Force which is not an individual

third party. This announcement is

erroneous.

“Prior to entering into the sale and purchase agreement with

Fujian Fuyuan Chemical Fibre Co., Ltd (“Fujian Fuyuan”) on 5

December 2006, Mega Force Investments Limited (“Mega

Force”), an indirect wholly owned subsidiary…”

“Upon Mega Force having signed the sale and purchase

agreement with Fujian Fuyuan…”

The Share Transfer Agreement for the

purchase of the Fujian Land was

entered into between Winburg and QRS on 2 December 2006. In light of

the Share Transfer Agreement dated 2

December 2006, SFCA doubts the

existence of the “sale and purchase

agreement dated 5 December 2006”

between Fujian Fuyuan and Mega

Force and would question the validity

of it, if it does exist.

CHINA SKY CHEMICAL FIBRE CO., LTD SPECIAL AUDIT REPORT 19 JUNE 2013

Stone Forest Corporate Advisory Pte Ltd 29

Relevant Excerpts of the SGXNET Announcements SFCA’s Comments

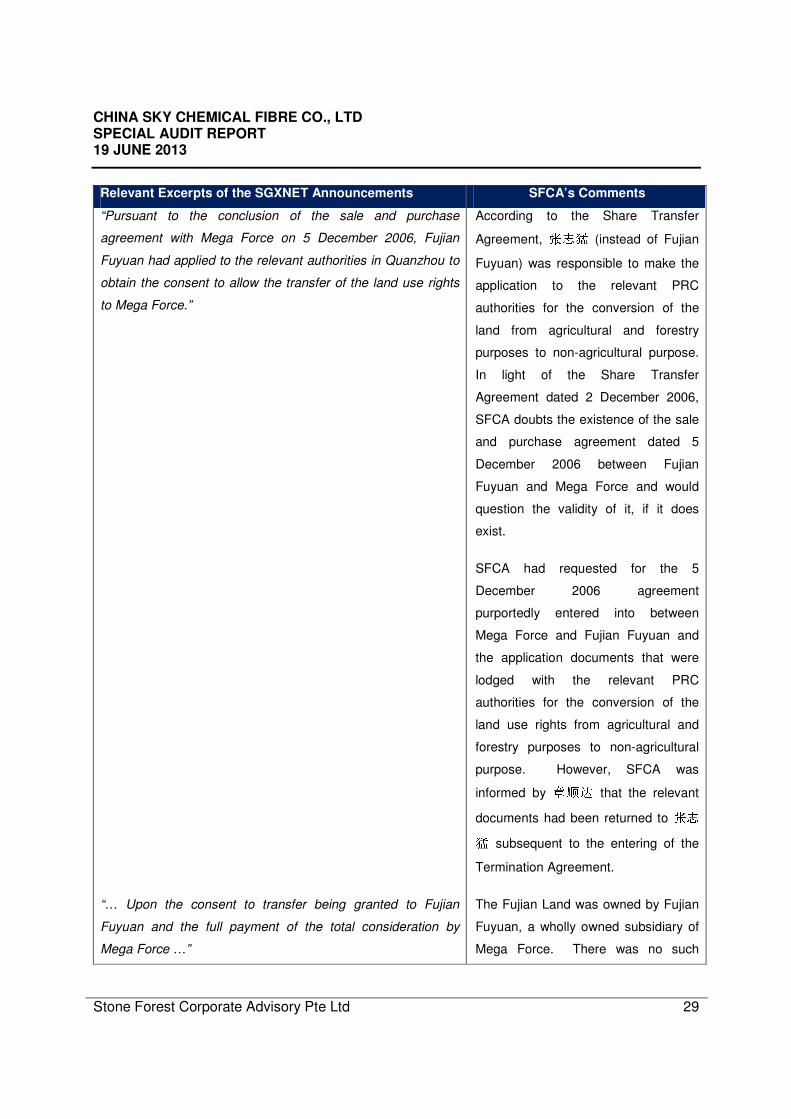

“Pursuant to the conclusion of the sale and purchase

agreement with Mega Force on 5 December 2006, Fujian

Fuyuan had applied to the relevant authorities in Quanzhou to

obtain the consent to allow the transfer of the land use rights

to Mega Force.”

According to the Share Transfer

Agreement, QRS (instead of Fujian

Fuyuan) was responsible to make the

application to the relevant PRC

authorities for the conversion of the

land from agricultural and forestry

purposes to non-agricultural purpose.

In light of the Share Transfer

Agreement dated 2 December 2006,

SFCA doubts the existence of the sale

and purchase agreement dated 5

December 2006 between Fujian

Fuyuan and Mega Force and would

question the validity of it, if it does

exist.

SFCA had requested for the 5

December 2006 agreement

purportedly entered into between

Mega Force and Fujian Fuyuan and

the application documents that were

lodged with the relevant PRC

authorities for the conversion of the

land use rights from agricultural and

forestry purposes to non-agricultural

purpose. However, SFCA was

informed by qrs that the relevant

documents had been returned to QRS subsequent to the entering of the

Termination Agreement.

“… Upon the consent to transfer being granted to Fujian

Fuyuan and the full payment of the total consideration by

Mega Force …”

The Fujian Land was owned by Fujian

Fuyuan, a wholly owned subsidiary of

Mega Force. There was no such

CHINA SKY CHEMICAL FIBRE CO., LTD SPECIAL AUDIT REPORT 19 JUNE 2013

Stone Forest Corporate Advisory Pte Ltd 30

Relevant Excerpts of the SGXNET Announcements SFCA’s Comments

“… Fujian Fuyuan had encountered difficulties in its

application to transfer the land use rights to Mega Force as

Mega Force is a foreign entity.”

application for the land use rights to be

transferred to Mega Force. The total

consideration had been fully paid.

“… In addition, it encountered funding constraints for the

expansion plan by end of 2007. The Group was, however, not

so ready to embark on this expansion in 2007.

As noted from the Company’s annual reports, the Company’s

sales and profitability had decreased substantially from the

second half of 2008 to 2009. Given the uncertain economic

and industry outlook then, and the need for the Company to

integrate its acquisition of Qingdao Zhongda Chemical Fibre

Company Limited during these two years, the Company was

also cautious to embark on the upstream production of raw

materials too expediently.”

Quanzhou Tianyu entered into 2

construction agreements on 8 October

2008 and 23 February 2009 with tuvwto develop the Fujian Land. The

fact that Quanzhou Tianyu proceeded

to perform leveling works on the Fujian

Land in late 2008 and 2009, appears

to be incongruent with this

announcement which states that the

Company was “cautious to embark on

the upstream production of the raw

materials”.

“Going forward, the Company plans to settle the remaining

balance of 12% of the total consideration, which amounts to

RMB19 million, by Q2 FY2011. Barring unforeseen

circumstances, the Company expects that it might be able to

obtain the land use rights certificate from the relevant

authorities in Quanzhou by 1H 2012, and have the title of the

land transferred to Mega Force. It should, however, be noted

that this timetable is based on best estimates provided by

management and the timing is largely beyond the control of

the Company. Nevertheless, the Company will use its best

endeavors to obtain the certificate of land use rights…

The Company intends to complete the acquisition of land.

Based on information available and the management

assessment, there are currently no legal hurdles to overcome

in order for the land to be transferred to Mega Force.”

The purchase consideration had been

paid in full.

The Fujian Land was owned by Fujian

Fuyuan, a wholly owned subsidiary of

Mega Force. There was no such

application for the land use rights to be

transferred to Mega Force.

CHINA SKY CHEMICAL FIBRE CO., LTD SPECIAL AUDIT REPORT 19 JUNE 2013

Stone Forest Corporate Advisory Pte Ltd 31

Relevant Excerpts of the SGXNET Announcements SFCA’s Comments

“The Company is also exploring the prospect of acquiring the

shares of Fujian Fuyuan, if necessary. In the unlikely event

that the Mega Force is unable to complete its transaction with

Fujian Fuyuan, it has the option to require Fujian Fuyuan to

dispose the land in the open market. Based on an

independent valuation commissioned by the Group in March

2011, as at December 31, 2010, the land is valued at RMB

264 million.”

Fujian Fuyuan was already a

subsidiary of Mega Force since its

incorporation on 15 September 2005.

“The initial development plan for the production of upstream

raw materials , includes a number of phases and consists of a

rather extensive construction plan which may eventually cost

approximately RMB5 billion if and when completed. The plan

includes inter alia the construction of the production plant,

outfitting of the plant with highly-advanced technical

equipment and technical know-how and royalties to be paid

out for the utilisation of such technical know-how and the

intellectual properties attached thereto. Insofar as for the

development of the land and construction of basic facilities, it

is estimated to be RMB1 billion.”

The planned expenditures of RMB5

billion or RMB1 billion are material

information which should have been

disclosed at the material time when

the expenditures were contemplated,

rather than in April 2011. During the

period between 2006 and 2010, the

Company’s market capitalisation

ranged from RMB0.8 billion to RMB9

billion. Expenditures of such

magnitude (RMB1 billion and RMB5

billion) would be considered major or

very substantial acquisitions

(depending on the time the

expenditures were contemplated) and

would require the prior approval of the

SGX and the shareholders pursuant to

Mainboard Rule 10154.

4 Mr. Huang, the former Group CEO, in his maxwellisation response dated 25 April 2013, expressed that in light of

the facts that “(1) the conversion of the land use rights had not been obtained by the vendor; and (2) the payment consideration and the development / construction costs had always been categorised as deposits, the Share Transfer Agreement had never been deemed to be completed”. Therefore, according to him, the return of the Fujian Land “could not be construed as a disposal (as defined under listing manual) but rather it was an unwinding of an initial acquisition that was never completed”. Mr. Huang explained that the Share Transfer Agreement was subsequently rescinded “upon the suggestion of SGX”.

CHINA SKY CHEMICAL FIBRE CO., LTD SPECIAL AUDIT REPORT 19 JUNE 2013

Stone Forest Corporate Advisory Pte Ltd 32

Relevant Excerpts of the SGXNET Announcements SFCA’s Comments

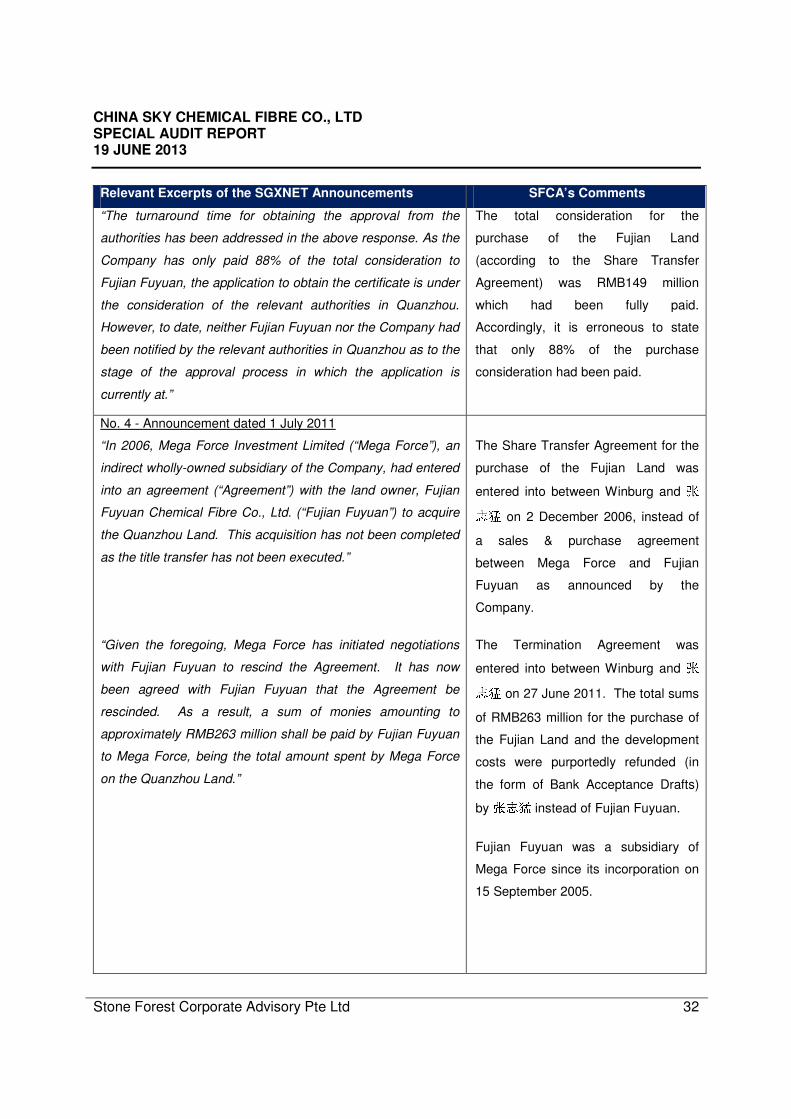

“The turnaround time for obtaining the approval from the

authorities has been addressed in the above response. As the

Company has only paid 88% of the total consideration to

Fujian Fuyuan, the application to obtain the certificate is under

the consideration of the relevant authorities in Quanzhou.

However, to date, neither Fujian Fuyuan nor the Company had

been notified by the relevant authorities in Quanzhou as to the

stage of the approval process in which the application is

currently at.”

The total consideration for the

purchase of the Fujian Land

(according to the Share Transfer

Agreement) was RMB149 million

which had been fully paid.

Accordingly, it is erroneous to state

that only 88% of the purchase

consideration had been paid.

No. 4 - Announcement dated 1 July 2011

“In 2006, Mega Force Investment Limited (“Mega Force”), an

indirect wholly-owned subsidiary of the Company, had entered

into an agreement (“Agreement”) with the land owner, Fujian

Fuyuan Chemical Fibre Co., Ltd. (“Fujian Fuyuan”) to acquire

the Quanzhou Land. This acquisition has not been completed

as the title transfer has not been executed.”

The Share Transfer Agreement for the

purchase of the Fujian Land was

entered into between Winburg and QRS on 2 December 2006, instead of

a sales & purchase agreement

between Mega Force and Fujian

Fuyuan as announced by the

Company.

“Given the foregoing, Mega Force has initiated negotiations

with Fujian Fuyuan to rescind the Agreement. It has now

been agreed with Fujian Fuyuan that the Agreement be

rescinded. As a result, a sum of monies amounting to

approximately RMB263 million shall be paid by Fujian Fuyuan

to Mega Force, being the total amount spent by Mega Force

on the Quanzhou Land.”

The Termination Agreement was

entered into between Winburg and QRS on 27 June 2011. The total sums

of RMB263 million for the purchase of

the Fujian Land and the development

costs were purportedly refunded (in

the form of Bank Acceptance Drafts)

by QRS instead of Fujian Fuyuan.

Fujian Fuyuan was a subsidiary of

Mega Force since its incorporation on

15 September 2005.

CHINA SKY CHEMICAL FIBRE CO., LTD SPECIAL AUDIT REPORT 19 JUNE 2013

Stone Forest Corporate Advisory Pte Ltd 33

Relevant Excerpts of the SGXNET Announcements SFCA’s Comments

No. 5 - Announcement dated 10 October 2011

“Fujian Fuyuan has repaid the sum of monies amounting to

approximately RMB263 million to the Group. As of to date,

the total purchase consideration has been refunded in full to

the Group.”

The Termination Agreement was

entered into between Winburg and QRS on 27 June 2011. The total sums

of RMB263 million for the Fujian Land

and the development costs were

purportedly refunded by QRS instead

of Fujian Fuyuan.

36. During his interview on 23 January 2013, Sunny informed SFCA that the information

required for the preparation of all announcements (including the erroneous

announcements on the Fujian Land) was provided by him. He also described the

announcement preparation and approval process in the following excerpts of his

interview transcript (which are translated to English from Chinese):

“The process is very simple. Loo & Partners drafted the announcements before

sending to everyone for comments. In most instances, Mr. Lai would be the first

person to provide his comments. Based on our past practice, Loo & Partners would

only circulate the revised draft announcement to everyone after receiving comments

from Mr. Lai, as he usually has many comments on the draft announcements. Upon

receiving Mr. Lai’s comments, everyone would look at the revised draft announcement.

When nobody has further comments, Loo & Partners would release the

announcements on the SGXNET.

…Mr. Huang would be informed on the contents of the draft announcements after the

amendments of Mr. Lai and when everyone has no objection to the revised contents.

…There were times where I would call Mr. Huang to inform him on the contents of the

announcements. There were times where his secretary in China would translate

(verbally) the documents to him. Most of the time, I was the one who called him.

There were also occasions where Mr. Lai and CC Loo would call him and explain to

him.

CHINA SKY CHEMICAL FIBRE CO., LTD SPECIAL AUDIT REPORT 19 JUNE 2013

Stone Forest Corporate Advisory Pte Ltd 34

…In most instances, Mr. Huang would give his consent and thereafter I would email

Loo & Partners informing them that the China directors have agreed to the contents of

the announcements.”

37. Based on the search performed by SFCA on Fujian Fuyuan on 18 December 2012,

Mega Force was the sole shareholder of Fujian Fuyuan. However, the search did not

reveal if Mega Force was the shareholder at the date of incorporation of Fujian Fuyuan.

38. On 11 March 2013, SFCA was provided with a copy of the Certificate of Approval on

the incorporation of Fujian Fuyuan by the Company’s Financial Controller, Mr. Lee

Chong Ping. Based on the Certificate of Approval, Mega Force was named as the sole

shareholder of Fujian Fuyuan at the date of its incorporation (i.e. 15 September 2005).

Considering the fact that Mega Force had been the sole shareholder of Fujian Fuyuan

since the time of its incorporation, the information that was furnished to the AC and Loo

& Partners which gave rise to the impression that Fujian Fuyuan was a third party

negotiating with Mega Force on the purchase of the Fujian Land was false5.

39. According to the same search on Fujian Fuyuan, Mr. Huang was still named as the

legal representative (xyz{|��) of Fujian Fuyuan even though Fujian Fuyuan

was no longer a subsidiary of the Company6. The search also revealed that the

directors of Fujian Fuyuan were }~�, ���, ��� and ���. According to Mr.

Huang, all three of them (Mr. Song Jian Sheng ("Mr. Song"), the Executive Director of

the Group, Mr. Wang Zhi Wei, the Non-Executive Director of the Group and himself)

had no further involvement in Fujian Fuyuan after signing the Termination Agreement.

Mr. Huang advised that the necessary documents (e.g. resignation as directors of

Fujian Fuyuan) had been signed and delivered to���

for lodgment with the relevant

PRC authorities at the material time when the shares in Mega Force were transferred

back to ���

(in October 2011, as mentioned in the Legal Due Diligence Report).

5 Mr. Yeap, in his maxwellisation response dated 28 April 2013, informed SFCA that “none of the independent

directors or the external auditor was informed that Fujian Fuyuan was part of the group”. 6 Mr. Lai and Mr. Yeap, in their joint maxwellisation response dated 5 June 2013, informed SFCA that “the fact that

Fujian Fuyuan was a subsidiary of Mega Force was never disclosed to the Board and the ex-IDs only discovered this fact from the draft report compiled by [SFCA]. The fact that Mr. Huang was the legal representative of Fujian Fuyuan and that Fujian Fuyuan was a wholly owned subsidiary of China Sky was only disclosed to the IDs at a meeting held in Hongkong on 30 December 2011”.

CHINA SKY CHEMICAL FIBRE CO., LTD SPECIAL AUDIT REPORT 19 JUNE 2013

Stone Forest Corporate Advisory Pte Ltd 35

40. In the course of the review, SFCA has requested for the following documents from the

Company concerning the Fujian Land but they have not been provided to us:

(a) Documents on transfer of shares in Mega Force from

��� to Winburg (in 2006)

and from Winburg back to���

(in 2011);

(b) Sale and purchase agreement dated 5 December 2006 purportedly entered

between Fujian Fuyuan and Mega Force as disclosed in the announcement

dated 29 April 2011;

(c) Application documents that were purportedly lodged with the relevant PRC

authorities for the conversion of the land from agricultural and forestry purposes

to non-agricultural purpose before the signing of the Termination Agreement;

(d) Copies of the Bank Acceptance Drafts reflecting the name of the transferor(s)

(either���

or companies under his control) and bearer (i.e. Quanzhou Tianyu);

(e) Application documents that were submitted to the relevant PRC authority on the

changes of the legal representative and directors of Fujian Fuyuan;

(f) Documents from the Local PRC Authority confirming that (in the early stages) the

progress on the development of the Fujian Land was smooth as stated in the

Fujian Qiaosheng's Legal Due Diligence Report; and

(g) Letter of confirmation purportedly issued by Fujian Fuyuan to Mega Force on 10

February 2011 (as stated in the SGXNET announcement on 22 April 2011).

In view of the lack of the aforementioned documents (most of which, according to the

Company, had been returned to ���

), SFCA is unable to conclusively verify whether

the transactions concerning the acquisition and subsequent return of the Fujian Land

were in fact implemented in accordance with the Share Transfer Agreement and

Termination Agreement.

41. SFCA has deliberated on all the available evidence gathered from the documents

provided to us and interviews with the relevant persons. Other than the Land Use

CHINA SKY CHEMICAL FIBRE CO., LTD SPECIAL AUDIT REPORT 19 JUNE 2013

Stone Forest Corporate Advisory Pte Ltd 36

Agreement entered into between Fujian Fuyuan and the Local PRC Authority on 20

October 2006, SFCA has not been given any other documents evidencing that Fujian

Fuyuan was the owner of the Fujian Land. However, SFCA understands that the Land

Use Agreement and the red line map (���) will constitute prima facie title to the land

by the authority.

Areas of Concern

42. The planned expenditures of RMB1 billion and RMB5 billion are considered material

information which should have been disclosed at the material time when the

expenditures were contemplated, rather than in April 2011. Expenditures of such

magnitude (RMB1 billion and RMB5 billion) would be considered major or very

substantial acquisitions (depending on the time the expenditures were contemplated)

and also require the prior approval of the SGX and the shareholders pursuant to

Mainboard Rule 1015. Mr. Huang, in his maxwellisation response dated 25 April 2013,

expressed his view that it “was not necessary for the Company to obtain shareholders’

approval because the plan was only conceptual and no details had been finalised. No

contracts relating to the RMB1–5 billion expenditure were awarded”. According to Mr.

Huang, the expansion plan was contingent upon many conditions to be fulfilled. He

explained that it would be premature for the board of directors of the Company

(“Board”) to seek shareholders’ approval when the plan “was still in its stage of infancy

and there were much uncertainty”. SFCA is of the view that even if the expansion plan

was in an infancy stage, the RMB1 billion and RMB5 billion planned expenditures

should have been tabled for discussion by the Board which should then opine whether

an announcement was required at the material time.

43. There was no documentary evidence of the Board’s approval at the material time on

the return of the Fujian Land (through the entering of the Termination Agreement).

44. Mainboard Rule 1014 requires an issuer to seek prior approval of a major transaction

that is not in the ordinary course of business. A transaction is considered major if its

value exceeds 20% of the Company’s market capitalisation. When the Termination

Agreement was entered into on 27 June 2011, the market capitalisation of the

CHINA SKY CHEMICAL FIBRE CO., LTD SPECIAL AUDIT REPORT 19 JUNE 2013

Stone Forest Corporate Advisory Pte Ltd 37

Company was about S$106 million (or RMB552 million based on an exchange rate of

RMB5.21 at the material time). The total refund of RMB263 million forms about 47% of

the Company’s market capitalisation at the material time. The return of the Fujian Land

to ���

(via the transfer of shares in Mega Force) was a major transaction which was

not in the ordinary course of business of the Group. The Company did not convene a

general meeting to approve the return of the Fujian Land to���

and hence

Mainboard Rule 1014 may have been breached7. SFCA has considered a potential

legal argument that the approval of the shareholders may not be required in view of the

fact that the Share Transfer Agreement contained a clause allowing the Fujian Land to

be returned to ���

in the event that the land use rights for non-agricultural purpose

could not be obtained from the relevant PRC authorities. While the directors of the

Company could invoke the contractual rights to return the Fujian Land (via the transfer

of shares in Mega Force), it is imperative under the Mainboard Rules that the

shareholders of the Company be the only ones who should evaluate on the commercial

merits of the return of the land and decide on the best course of action.

45. There were numerous erroneous disclosures made by the Company concerning the

Fujian Land and the refund of the "deposits". Sunny, who had been tasked with

coordinating with Loo & Partners on the preparation of the SGXNET announcements

and obtaining the necessary approval from the directors residing in PRC, did not

exercise reasonable diligence that is expected of a Group Financial Controller. Based

on SFCA's findings, it appears that he had failed to ensure that the contents of the

following announcements (concerning the facts surrounding the acquisition and

subsequent return of the Fujian Land) were correct before obtaining approval for their

release on the SGXNET:

(a) Company’s announcement dated 13 March 2010;

7 Mr. Huang, in his maxwellisation response dated 25 April 2013, expressed that in light of the facts that “(1) the

conversion of the land use rights had not been obtained by the vendor; and (2) the payment consideration and the development / construction costs had always been categorised as deposits, the Share Transfer Agreement had never been deemed to be completed”. Therefore, according to him, the return of the Fujian Land “could not be construed as a disposal (as defined under listing manual) but rather it was an unwinding of an initial acquisition that was never completed”. Mr. Huang explained that the Share Transfer Agreement was subsequently rescinded “upon the suggestion of SGX”.

CHINA SKY CHEMICAL FIBRE CO., LTD SPECIAL AUDIT REPORT 19 JUNE 2013

Stone Forest Corporate Advisory Pte Ltd 38

(b) Company’s announcement dated 22 April 2011;

(c) Company’s announcement dated 29 April 2011;

(d) Company’s announcement dated 1 July 2011; and

(e) Company’s announcement dated 10 October 2011.

46. All the announcements in the preceding paragraph were submitted by Mr. Huang “by

Order of the Board”, as evidenced by his name printed in the announcements. Sunny

said that he would usually translate (verbally) and explain the contents of every

intended announcement to Mr. Huang and obtain Mr. Huang’s approval before

instructing Loo & Partners to release the relevant announcements. Mr. Huang, in his

interview, said that he had placed reliance on Sunny, the former AC Chairman, Mr. Lai

Seng Kwoon ("Mr. Lai")8 and Loo & Partners to draft the necessary announcements

before giving his approval to release them. Given that Mr. Huang had submitted the

erroneous announcements by the order of the Board, the Board9 at the material time

ought to have verified or sought written confirmation from the management that the

contents of the relevant announcements were accurate before their release on the

SGXNET. SFCA is of the view that the Board at the material time did not exercise

8 In his written response dated 2 May 2013, Mr. Lai said that he is incapable of holding “a proper, decent and

meaningful conversation wholly in mandarin”. He explained that “the draft announcements were prepared by the corporate secretarial staff based wholly on information provided by the CFO and that the announcements were only released after the CFO and Mr Huang (through the CFO) confirm that the contents are accurate”. 9 The current AC Chairman, Mr. Er, in his maxwellisation response dated 19 April 2013, said that he had relied “to a

great extent on the information provided by Management and verified by the External Auditor, as well as feedback from the internal auditor at the Audit Committee meetings and further reported at the Board meetings”. Mr. Er also said that the Board acted on the advice from the “Compliance Advisor” (i.e. Loo & Partners) in respect of complying with the SGX listing rules. Mr. Lai, in his letter dated 2 May 2013, said that “there can be no doubt that the management did represent to the Board that the contents were accurate before the release; and there was then no reason to doubt the veracity of such information and confirmation”.

CHINA SKY CHEMICAL FIBRE CO., LTD SPECIAL AUDIT REPORT 19 JUNE 2013

Stone Forest Corporate Advisory Pte Ltd 39

reasonable diligence in ensuring that the contents of the abovementioned

announcements were correct before approving them for release on SGXNET10.

47. SFCA is also perturbed by the existence of the Mega Force Agreement which

apparently formed the basis of the 1 July 2011 announcement by the Company. The

contents of the 1 July 2011 announcement (which had been prepared according to the

terms of the Mega Force Agreement) were incorrect in light of the Termination

Agreement dated 27 June 2011 made between Winburg and ���

. Sunny should

have obtained from Mr. Huang the factual details of the transactions concerning the

Fujian Land before providing the relevant information to Loo & Partners for the purpose

of drafting the necessary announcements. Instead, he caused the 2 agreements

(Quanzhou Tianyu Agreement and Mega Force Agreement) to be prepared11 based on

his erroneous understanding without informing or consulting Mr. Huang, who was

directly involved in the negotiations with���

on the Fujian Land. SFCA is of the

view that Sunny failed to discharge his duties in this aspect as the Group Financial

Controller.

48. Based on the Legal Due Diligence Report and the Certificate of Approval on the

incorporation of Fujian Fuyuan, SFCA notes that Fujian Fuyuan was a subsidiary of

Mega Force since its incorporation on 15 September 2005. Hence, Fujian Fuyuan

became a subsidiary of the Company through the acquisition of Mega Force in

December 2006. However, no disclosure had been made by the Company via

announcements or in its Annual Reports. The Board at the material time and the

former Group Financial Controller ought to have ensured that the acquisition of Fujian

Fuyuan as a subsidiary was disclosed promptly, as required by Mainboard Rule 703.

10

Mr. Lai and Mr. Yeap, in their joint maxwellisation response dated 5 June 2013, informed SFCA that “the IDs had relied on Mr Sunny Hui (CFO) and Mr. Huang (CEO) to provide correct and complete information as a basis for these announcements and there were no reasons to believe that they did not inform the IDs the relevant details. The details as disclosed in these announcements were consistent with the audited financial statements, which the

external auditors had rendered unmodified [sic] opinions for all the relevant years”. Mr. Yeap, in his written response dated 7 June 2013 issued on behalf of the IDs (at the material time), reiterated that “all the announcements were drafted by the corporate secretarial service provider team based on instructions and information from the chief financial officer”.

11

According to Sunny, the former Group Financial Controller, in his maxwellisation response on 25 April 2013, he said that he did not prepare the 2 agreements but merely provided a template to facilitate the preparation of the agreements.

CHINA SKY CHEMICAL FIBRE CO., LTD SPECIAL AUDIT REPORT 19 JUNE 2013

Stone Forest Corporate Advisory Pte Ltd 40

49. No due diligence was performed by the Company prior to the acquisition of Mega

Force and Fujian Fuyuan. SFCA is of the view that the Company should have

performed a proper due diligence to determine if it was legally possible for Fujian

Fuyuan to successfully apply for a conversion of the land use rights prior to the

acquisition of Mega Force. Instead, a legal advice (by Fujian Qiaosheng) was obtained

only in January 2011 (subsequent to the acquisition of Mega Force and Fujian Fuyuan

in 2006), to confirm that the Fujian Land was owned by Fujian Fuyuan and there was

no legal obstacle for Fujian Fuyuan to obtain the land use rights certificate.

50. The Phase One Construction Agreement and the Phase Two Construction Agreement

were entered into on 8 October 2008 and 23 February 2009 respectively. Mainboard

Rule 703 requires an issuer to disclose any information concerning its subsidiary which

is likely to materially affect its share price or value. Mr. Huang, in his maxwellisation

response dated 25 April 2013, said that the contract sum of RMB114 million represents

about 3.7% of the Group’s Net Tangible Assets for the financial year ended 31

December 2008 ("FY2008") and expressed his view that the sum is therefore “deemed

immaterial for announcement purposes”. Nevertheless, SFCA is of the view that the

two construction agreements should have been tabled for discussion and approval by

the Board as a matter of good corporate governance. The Board could then opine on

whether an announcement would be necessary.

Recommendations

51. SFCA recommends the Company to:

(a) issue a clarification announcement on the SGXNET informing its shareholders of

the correct material facts concerning the Fujian Land. The Board should take

steps to ensure that the contents of the announcements are correct before they

are released on the SGXNET;

(b) for good corporate governance practice, put in place a framework and

mechanism to record and document key events (such as the return of the land)

as well as the basis for Board’s decisions in relation to these events;

CHINA SKY CHEMICAL FIBRE CO., LTD SPECIAL AUDIT REPORT 19 JUNE 2013

Stone Forest Corporate Advisory Pte Ltd 41

(c) consider the necessity of ratifying the execution of the Termination Agreement

with ���

for refund of RMB263 million in relation to the Fujian Land (through

the convening of a general meeting of shareholders pursuant to Mainboard Rule

1014 if ratification is deemed necessary); and

(d) circulate all intended announcements to each and every member of the Board

(including the PRC directors) for comments / approval. It is imperative that they

fully understand the contents and satisfy themselves with the accuracy / reliability

of the information to be released before they give their approval for the final

release on the SGXNET.

Interested Person Transactions

52. The Company’s Corporate Governance Statement in the Annual Reports for FY2006 to

FY2009 stated that there were no IPTs for those years. However, it was disclosed in

the Company’s Corporate Governance Statement in the Annual Report for FY2010 that

there were IPTs of RMB1,500,000 and RMB866,000 in FY2009 and FY2010

respectively. The Company neither revealed the particulars of those IPTs, nor

disclosed the identity of the interested person in the FY2010 Annual Report.

53. Information concerning IPTs and related party transactions (“RPTs”) disclosed in the

Company’s Annual Reports since FY2006 are summarised in the following table:

RMB (‘000) FY2006 FY2007 FY2008 FY2009 FY2009

Comparative

Figure for

FY2010(c)

FY2010

IPTs (As per Corporate

Governance Statement) -(a)

-(b)

-(b)

-(b)

1,500 866

RPTs (As per Notes to the

Financial Statements) 328 657 594 1,500 1,500 866

CHINA SKY CHEMICAL FIBRE CO., LTD SPECIAL AUDIT REPORT 19 JUNE 2013

Stone Forest Corporate Advisory Pte Ltd 42

Notes:

(a) It was stated in the Corporate Governance Statement in the Annual Report for

FY2006 that there was no “interested person transactions carried out during

FY2005”. There appears to be a typographical error on “FY2005” as it should

refer to “FY2006”

(b) It was stated in the Corporate Governance Statement in each of the Annual

Reports from FY2007 to FY2009 that there were “no interested person

transactions carried out” during the relevant financial periods.

(c) The RMB1.5 million was disclosed as a FY2009 comparative figure in section F

of the Corporate Governance Statement in the FY2010 Annual Report.

54. In the Company’s announcement on 22 April 2011, SK Lai & Co was revealed as the

interested person in question. Mr. Lai was appointed as independent director ("ID")

and AC Chairman of the Company on 25 August 2005. He resigned as an ID and

Chairman / member of the AC on 5 January 2012. Information concerning the nature

of services rendered by Mr. Lai’s firm, SK Lai & Co, was disclosed in the following

excerpts of the announcement on 22 April 2011:

“SK Lai & Co., a firm of certified public accountants has rendered professional services

to the Company. These services relate to assist in the review and recommendations of

the Company’s internal, accounting and reporting controls, reviewing quarterly financial

statements and the results announcements and providing consultancy and advisory

services for the accounting and consolidation of Qingdao Zhongda Chemical Fibre

Company Limited. Mr. Lai Seng Kwoon who is an Independent Director of the

Company, is a partner of SK Lai & Co. The Board considers Mr Lai Seng Kwoon to be

an independent director, notwithstanding his relationship with the Company, which falls

under Guidance Note 2.1(d) of the Code of Corporate Governance, by virtue of his

position as a partner of SK Lai & Co., which renders professional services to the

Group.”

CHINA SKY CHEMICAL FIBRE CO., LTD SPECIAL AUDIT REPORT 19 JUNE 2013

Stone Forest Corporate Advisory Pte Ltd 43

55. The invoices rendered by SK Lai & Co to the Group since FY2006 are summarised in

the following table:

Nature of Services

Rendered

Relevant

Financial

Years

Fees

S$

Disbursement

S$

GST

S$

Total

S$

Paragraph

Reference

Internal Audit

Services

(including review of

PPE cycle of

Quanzhou Tianyu)

FY2006 to

FY2010

120,500 14,654 - 135,154 56

Accounting Services

(review and

preparation of

quarterly

announcements of

financial results)

FY2007 to

FY2010

315,800 5,400 360 321,560 57

Visit to Qingdao

Zhongda / Goodwill

Assessment Papers /

Due Diligence report

/ Buyback circular

FY2008

and

FY2009

55,000 3,298 - 58,298 58

Total 491,300 23,352 360 515,012

56. Internal Audit Services

(a) The appointment of SK Lai & Co as the Company’s internal auditor was approved

pursuant to a Directors’ Resolution in Writing (“DRIW”) dated 4 August 2006. It

was recorded in this DRIW that the “Audit Committee had in the Audit Committee

meeting held on 8 May 2006, agreed to appoint Messrs SK Lai & Co, a company

owned by Mr. Lai Seng Kwoon, the independent director, to perform internal audit

function in the Group’s operating premises in China”. A proposal of SK Lai & Co

was attached to the DRIW dated 4 August 2006. According to the proposal, the

scope of work of SK Lai & Co was stated as follows:

(i) To identify potential operational, financial and compliance issues that may

adversely affect the Company’s business and its periodic reporting process;

CHINA SKY CHEMICAL FIBRE CO., LTD SPECIAL AUDIT REPORT 19 JUNE 2013

Stone Forest Corporate Advisory Pte Ltd 44

(ii) To formulate internal audit procedures / programs to be carried out for the

review of each identified key risk area and process; and

(iii) To establish a two-year internal audit plan for the performance of internal

audit procedures in accordance with the specific significance of the key risk

areas and processes identified.

The estimated fees (excluding out-of-pocket expenses) quoted by SK Lai & Co

were as follows:

(i) 2006 - $35,000; and

(ii) 2007 - $25,000.

(b) In a letter dated 6 December 2012, SFCA requested Mr. Lai to provide copies of

all proposals and reports previously prepared by SK Lai & Co for the Group.

During his interview on 31 December 2012, Mr. Lai informed SFCA that all the

documents of SK Lai & Co, including the abovementioned proposals and reports,

had been retained by Commercial Affairs Department ("CAD"). During the review

of Mr. Er’s records (that were retained by CAD), SFCA discovered several reports

/ proposals of SK Lai & Co.

57. Accounting Services

(a) Mr. Lai gave a brief description of the accounting work performed by SK Lai & Co

during his interview on 31 December 2012. The relevant excerpts of his interview

transcript describing the accounting services are reproduced below:

“In a broader sense you can say that is accounting services but we do not

meddle with the Chinese accounts. All we do is the consolidation worksheet

comes out, from all the whatever subsidiaries they have. The consolidation, we

help them to do the consolidation, we help them also to align to IFRS, because

their China accounts are using IFRS not FRS. We check for consistency in terms

of the numbers, we ask for breakdown in terms of some of the numbers like

CHINA SKY CHEMICAL FIBRE CO., LTD SPECIAL AUDIT REPORT 19 JUNE 2013

Stone Forest Corporate Advisory Pte Ltd 45

stocks and things like that, how much raw materials, how much WIP, and if there

are other major receivables we will ask for breakdown. We also help them to,

they will normally come out with some explanations on the fluctuation. We would,

you know ask question and elaborate, on the format, and then we calculate the

EPS. So it is reporting not compilation.”

(b) Concerning the SK Lai & Co’s billings for the review and preparation of quarterly

announcements of the Group’s financial results, Mr. Lai informed SFCA during

his interview that there was neither any terms of reference nor any proposal

tabled for approval by the Board or AC.

(c) During his interview, Mr. Lai clarified that the provision of accounting services to

the Company was not premeditated and hence there was no proposal or a letter

of engagement entered between the Company and SK Lai & Co concerning

these services. Mr. Lai explained that the draft quarterly announcements initially

prepared by the Company for his review, as AC Chairman, were not compliant

with the SGX requirements. As a result, he had to deploy the resources of his

firm to assist in preparing the quarterly announcements to meet the SGX

requirements.

58. Other Services

(a) During his interview on 31 December 2012, Mr. Lai added that his firm had

performed the following services to the Group:

(i) Purchase price allocation exercise in 2009 concerning the acquisition of

Deluxe Dragon International Limited (“Deluxe Dragon”); and

(ii) Goodwill impairment assessment of Qingdao Zhongda in 2009.

CHINA SKY CHEMICAL FIBRE CO., LTD SPECIAL AUDIT REPORT 19 JUNE 2013

Stone Forest Corporate Advisory Pte Ltd 46

59. A comparison of the aggregate values of all services rendered by SK Lai & Co against

the Group’s relevant audited net tangible assets (“NTA”) is tabulated below:

Financial

Year

Aggregate

Value of IPTs

(S$)

Equivalent Value

of IPTs (A)

(RMB)

Group’s NTA

(B)

(RMB million)

%

(A/B)

FY2006 36,263 184,940 2,047 0.01%

FY2007 53,334 272,003 2,657 0.01%

FY2008 128,051 640,253 3,057 0.02%

FY2009 164,300 821,500 2,863 0.03%

FY2010 89,40012 447,000 2,973 0.02%

Total 471,348 2,365,696 - -

60. According to Mainboard Rule 905(2), if the aggregate value of all transactions entered

into with the same interested person during the same financial year amounts to 3% or

more of the group’s latest audited NTA, the issuer must make an immediate

announcement of the latest transaction and all future transactions entered into with that

same interested person during that financial year.

61. The aggregate value of the IPTs with SK Lai & Co for each financial year between

FY2006 and FY2010 was less than 3% of the Group’s relevant NTA. Hence, the IPTs

with SK Lai & Co were not required to be announced by the Company.

62. Mainboard Rule 907 requires an issuer to disclose the aggregate value of IPTs entered

into during the financial year under review in its annual report. However, IPTs with an

aggregate value less than S$100,000 during the financial year need not be disclosed in

the annual report. The entire Rule 907 is reproduced as follows:

“An issuer must disclose the aggregate value of interested person transactions entered