Embed Size (px)

Citation preview

China Power Market Outlook to 2030 - Business Propensity Indicator (BPI), Market Trends, Regulation and Competitive Landscape

GDPE0513ICR / Published JUL 2011 Page 1

© GlobalData. This report is a licensed product and is not to be photocopied

China Power Market Outlook to 2030 - Business Propensity Indicator (BPI), Market Trends, Regulation and Competitive

Landscape Reference Code: GDPE0513ICR Publication Date: July 2011

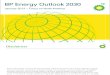

Thermal Fuel is the Dominant Source in the Power Mix

The cumulative installed capacity for power in China was

977,019 MW (Megawatts) in 2010, and the thermal installed

capacity accounted for over 72% of installed capacity, that is,

705,779 MW. China has good domestic production of coal and

gas, which helps cater to the country‟s power requirements.

Coal plants are the dominating source of power generation in

the country. However, the government is trying to incorporate

clean coal technologies to its power production to reduce

carbon emissions from coal-fired plants.

Power Market, China, Cumulative Thermal Installed Capacity (MW), 2000-2010

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

2000 2005 2010

Therm

al In

sta

lled C

apa

city (

MW

)

Source: GlobalData, National Bureau of Statistics of China, China Electricity Council

Continued Growth in Power Generation

Since the liberalization of the economy in China from the early

1990s, power generation in the country has been increasing at

a very fast pace to fulfill the industrial and commercial power

requirements of the country. During the forecast period,

electricity generation is expected to increase at a Compound

Annual Growth Rate (CAGR) of 11.3% from 1,377,891 GWh

(Gigawatt-hours) in 2000 to 4,011,219 GWh in 2010.

Power Market, China, Total Power Generation (GWh), 2000-2010

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

2000 2005 2010T

ota

l G

enera

tion (

GW

h)

Source: GlobalData, National Bureau of Statistics of China, China Electricity Council

Clean Energy in the Country

China has a lot of thermal installed capacity, especially in the

form of coal-fired plants, and as a result they have high carbon

emissions as well. Prior to 2005, there were very few renewable

energy power plants in the country; however, since then the

government has been encouraging the installation of a higher

percentage of non-thermal power plants in the country.

There is a lot of government support to increase the utilization

of non- thermal resources in the country. The new 12th Five

Year Plan (2011- 2015) draft was relased earlier this year, and

this plan includes a new target for cutting energy consumption

per unit of GDP (Gross Domestic Product) and also targets for

reducing carbon dioxide emissions per unit of GDP. The

government aims to increase energy consumption from non-

fossil fuel sources to 15% by 2020. There are compulsory

targets for generating utilities to generate power from non-

thermal resources as well. In April 2010, the new renewable

energy law took effect which included more detailed planning

and co-ordination of renewable energy with the country‟s

transmission grid planning as well. Such policies ensure that

there will be high growth in clean technology and renewable

energy in the coming years.

China Power Market Outlook to 2030 - Business Propensity Indicator (BPI), Market Trends, Regulation and Competitive Landscape

GDPE0513ICR / Published JUL 2011 Page 2

© GlobalData. This report is a licensed product and is not to be photocopied

1 Table of Contents

1 Table of Contents .................................................................................................................................. 2 1.1 List of Tables .................................................................................................................................. 4 1.2 List of Figures ................................................................................................................................. 5

2 Introduction ........................................................................................................................................... 6 2.1 GlobalData Report Guidance .......................................................................................................... 7

3 Business Propensity Indicator Methodology .......................................................................................... 8 3.1 Methodology Adopted For Evaluating the Business Propensity Indicator for the Asia Pacific region

8 3.1.1 Capacity and Reserve Potential ............................................................................................ 8 3.1.2 Regulatory Scenario .............................................................................................................. 9 3.1.3 Investment Scenario .............................................................................................................. 9 3.1.4 Transmission and Distribution (T&D) Infrastructure ..............................................................11 3.1.5 Macro Economic Scenario ....................................................................................................12 3.1.6 Competitive Scenario ...........................................................................................................13

3.2 Methodology Adopted to Arrive at a Final Rank.............................................................................14 4 Power Market, China, Business Propensity Indicator ...........................................................................17

4.1 Capacity and Reserve Potential .....................................................................................................18 4.2 Regulatory Scenario ......................................................................................................................18 4.3 Investment Scenario ......................................................................................................................19 4.4 Transmission and Distribution Infrastructure .................................................................................19 4.5 Macroeconomic Factors ................................................................................................................20 4.6 Competitive Scenario .....................................................................................................................20 4.7 Conclusion .....................................................................................................................................21 4.8 Power Market, China, Business Propensity Indicator Ranking ......................................................22

4.8.1 Present Ranking ...................................................................................................................22 4.8.2 Future Ranking .....................................................................................................................23

5 China Power Market Analysis, 2000-2030 ...........................................................................................24 5.1 Demand and Consumption Scenario .............................................................................................24 5.2 Import and Export Scenario ...........................................................................................................25 5.3 Power Consumption, 2000-2030 ...................................................................................................26 5.4 Cumulative Installed Capacity, 2000-2030 ....................................................................................28

5.4.1 Cumulative Installed Capacity by Type of Power Plant: Percentage ....................................28 5.4.2 Cumulative Installed Capacity: Total Value, 2000-2030 .......................................................29 5.4.3 Cumulative Thermal Installed Capacity, 2000-2030 .............................................................32 5.4.4 Cumulative Hydro Installed Capacity, 2000-2030 .................................................................34 5.4.5 Cumulative Nuclear Installed Capacity, 2000-2020 ..............................................................36 5.4.6 Cumulative Renewable Installed Capacity, 2000-2030 ........................................................38

5.5 Power Generation, 2000-2030 .......................................................................................................40 5.5.1 Thermal Power Generation, 2000-2030 ...............................................................................43 5.5.2 Hydropower Generation, 2000-2030 ....................................................................................45 5.5.3 Nuclear Power Generation, 2000-2030 ................................................................................47 5.5.4 Renewable Power Generation, 2000-2030 ...........................................................................49

6 Power Market, China, Top Active and Upcoming Projects ...................................................................51 6.1 Active Power Projects ....................................................................................................................51

6.1.1 Top 10 Active Thermal Power Projects ................................................................................51 6.1.2 Top 10 Active Hydropower Plants ........................................................................................52 6.1.3 Top 10 Active Nuclear Commercial Reactors .......................................................................53 6.1.4 Top 10 Renewable Power Projects ......................................................................................54

6.2 Upcoming Power Projects .............................................................................................................55 6.2.1 Top 10 Upcoming Thermal Power Projects ..........................................................................55 6.2.2 Top 10 Upcoming Hydropower Projects ...............................................................................56 6.2.3 Top 10 Upcoming Nuclear Commercial Reactors .................................................................57 6.2.4 Top 10 Upcoming Renewable Power Projects .....................................................................58

7 Power Market, China, Regulatory Structure .........................................................................................59 7.1 Regulatory Structure, Overview .....................................................................................................59 7.2 Restructuring of Power Market ......................................................................................................59 7.3 Latest Reforms Aim at Increasing Competition ..............................................................................59 7.4 Policies to Support Lower Carbon Technologies ...........................................................................60

China Power Market Outlook to 2030 - Business Propensity Indicator (BPI), Market Trends, Regulation and Competitive Landscape

GDPE0513ICR / Published JUL 2011 Page 3

© GlobalData. This report is a licensed product and is not to be photocopied

7.5 Proposals between China and European Union to Strengthen the Carbon Capture and Storage (CCS) Projects ...............................................................................................................................60

7.6 Development Plan for Renewable Energy .....................................................................................60 8 Power Market, China, Infrastructure .....................................................................................................61

8.1 Infrastructure Overview ..................................................................................................................61 8.1.1 Infrastructure Overview, Grid Interconnection ......................................................................61 8.1.2 Infrastructure Overview, Infrastructure Development ...........................................................61 8.1.3 Infrastructure Overview, Transmission Line Lengths, 2000-2020 .........................................62 8.1.4 Infrastructure Overview, Distribution Line Lengths (Ckm), 2000-2020 .................................63

9 Power Market, China, Competitive Landscape: Snapshot of Top Five Power Companies ..................64 9.1 Market Share of Major Power Generating Companies ..................................................................64 9.2 Key Companies in the Chinese Power Market, China HuaNeng Group ........................................65

9.2.1 China HuaNeng Group, Company Overview ........................................................................65 9.2.2 China HuaNeng Group, Business Description ......................................................................65 9.2.3 China HuaNeng Group, SWOT Analysis ..............................................................................66

9.3 Key Companies in the Chinese Power Market, China Datang Corporation ...................................69 9.3.1 China Datang Corporation, Company Overview ...................................................................69 9.3.2 China Datang Corporation, Business Description .................................................................69 9.3.3 China Datang Corporation, SWOT Analysis .........................................................................71

9.4 Key Companies in the Chinese Power Market, China Guodian Corporation .................................74 9.4.1 China Guodian Corporation, Company Overview .................................................................74 9.4.2 China Guodian Corporation, Business Description ...............................................................74 9.4.3 China Guodian Corporation, SWOT Analysis .......................................................................75

9.5 Key Companies in the Chinese Power Market, China Huadian Corporation .................................77 9.5.1 China Huadian Corporation, Company Overview .................................................................77 9.5.2 China Huadian Corporation, Business Description ...............................................................77 9.5.3 China Huadian Corporation, SWOT Analysis .......................................................................78

9.6 Key Companies in the Chinese Power Market, China Power Investment Corporation ..................82 9.6.1 China Power Investment Corporation, Company Overview ..................................................82 9.6.2 China Power Investment Corporation, Business Description................................................82 9.6.3 China Power Investment Corporation, SWOT Analysis ........................................................83

10 Appendix ..............................................................................................................................................86 10.1 Market Definitions ..........................................................................................................................86

10.1.1 Power ...................................................................................................................................86 10.1.2 Installed Capacity .................................................................................................................86 10.1.3 Active Installed Capacity.......................................................................................................86 10.1.4 Electricity Generation ...........................................................................................................86 10.1.5 Thermal Power .....................................................................................................................86 10.1.6 Hydro Power .........................................................................................................................86 10.1.7 Nuclear Power ......................................................................................................................86 10.1.8 Renewable Energy Resources .............................................................................................86 10.1.9 Generation Company ...........................................................................................................86 10.1.10 Electricity Consumption ........................................................................................................86 10.1.11 Transmission Network ..........................................................................................................86 10.1.12 Interconnector .......................................................................................................................86 10.1.13 Transmission and Distribution Loss ......................................................................................87

10.2 Abbreviations .................................................................................................................................87 10.2.1 Coverage ..............................................................................................................................88 10.2.2 Secondary Research ............................................................................................................88 10.2.3 Primary Research .................................................................................................................88

10.3 Contact Us .....................................................................................................................................89 10.4 Disclaimer ......................................................................................................................................89

China Power Market Outlook to 2030 - Business Propensity Indicator (BPI), Market Trends, Regulation and Competitive Landscape

GDPE0513ICR / Published JUL 2011 Page 4

© GlobalData. This report is a licensed product and is not to be photocopied

1.1 List of Tables

Table 1: Ease of Doing Business-Categories and Subcategories ...........................................................10 Table 2: Scoring Methodology for the Parameters ..................................................................................15 Table 3: Best Score for Present and Future Scenario ............................................................................16 Table 4: Power Market, China, Breakdown of Electricity Consumption, By Sector (%), 2009 ................24 Table 5: Power Market, China, Total Annual Imports and Exports (GWh), 2000-2009 ...........................25 Table 6: Power Market, China, Power Consumption (GWh), 2000-2030 ................................................27 Table 7: Power Market, China, Cumulative Installed Capacity (MW), 2000-2030 ...................................30 Table 8: Power Market, China, Cumulative Thermal Installed Capacity (MW), 2000-2030 ....................33 Table 9: Power Market, China, Cumulative Hydro Installed Capacity (MW), 2000-2030 ........................35 Table 10: Power Market, China, Cumulative Nuclear Installed Capacity (MW), 2000-2030 .....................37 Table 11: Power Market, China, Cumulative Renewable Installed Capacity (MW), 2000-2030 ................39 Table 12: Power Market, China, Power Generation (GWh), 2000-2030 ...................................................41 Table 13: Power Market, China, Thermal Power Generation (GWh), 2000-2030 .....................................44 Table 14: Power Market, China, Hydropower Generation (GWh), 2000-2030 ..........................................46 Table 15: Power Market, China, Nuclear Power Generation (GWh), 2000-2030 ......................................48 Table 16: Power Market, China, Renewable Power Generation (GWh), 2000-2030 ................................50 Table 17: Power Market, China, Active Thermal Power Plants.................................................................51 Table 18: Power Market, China, Top 10 Active Hydropower Plants .........................................................52 Table 19: Power Market, China, Top 10 Active Nuclear Commercial Reactors ........................................53 Table 20: Power Market, China, Top 10 Active Renewable Power Plants ................................................54 Table 21: Power Market, China, Top 10 Upcoming Thermal Power Plants ..............................................55 Table 22: Power Market, China, Top 10 Upcoming Hydropower Plants ...................................................56 Table 23: Power Market, China, Top 10 Upcoming Nuclear Commercial Reactors ..................................57 Table 24: Power Market, China, Top 10 Upcoming Renewable Power Plants .........................................58 Table 25: Power Market, China, Transmission Line Lengths (Ckm), 2000-2020 ......................................62 Table 26: Power Market, China, Distribution Line Lengths (Ckm), 2000-2020 .........................................63 Table 27: Power Market, China, Installed Capacity Share of Major Power Generating Companies (%),

2009 ..........................................................................................................................................64 Table 28: China HuaNeng Group, SWOT Analysis, 2010 ........................................................................66 Table 29: China Datang Corporation, SWOT Analysis, 2010 ...................................................................71 Table 30: China Guodian Corporation, SWOT Analysis, 2010 .................................................................75 Table 31: China Huadian Corporation, SWOT Analysis, 2010 .................................................................78 Table 32: China Power Investment Corporation, SWOT Analysis, 2010 ..................................................83 Table 33: Abbreviations, ...........................................................................................................................87

China Power Market Outlook to 2030 - Business Propensity Indicator (BPI), Market Trends, Regulation and Competitive Landscape

GDPE0513ICR / Published JUL 2011 Page 5

© GlobalData. This report is a licensed product and is not to be photocopied

1.2 List of Figures

Figure 1: Weightage Assigned to the Six Factors (%),2000-2020 ...........................................................14 Figure 2: Power Market, China, Business Propensity Indicator ...............................................................17 Figure 3: Power Market, China, Business Propensity Indicator Ranking .................................................22 Figure 4: Power Market, China, Breakdown of Electricity Consumption, By Sector (%), 2009 ................24 Figure 5: Power Market, China, Total Annual Imports and Exports (GWh), 2000-2009 ...........................25 Figure 6: Power Market, China, Annual Power Consumption (GWh), 2000-2030 ....................................26 Figure 7: Power Market, China, Cumulative Installed Capacity (MW), 2010 ............................................28 Figure 8: Power Market, China, Cumulative Installed Capacity (MW), 2000-2030 ...................................29 Figure 9: Power Market, China, Installed Capacity Comparison of 10 Asia Pacific Countries(MW), 2010-

2020 ..........................................................................................................................................31 Figure 10: Power Market, China, Cumulative Thermal Installed Capacity (MW), 2000-2030 ....................32 Figure 11: Power Market, China, Cumulative Hydro Installed Capacity (MW), 2000-2030 ........................34 Figure 12: Power Market, China, Cumulative Nuclear Installed Capacity (MW), 2000-2030 .....................36 Figure 13: Power Market, China, Cumulative Renewable Installed Capacity (MW), 2000-2030 ................38 Figure 14: Power Market, China, Power Generation (GWh), 2000-2030 ...................................................40 Figure 15: Power Market Outlook, China, Annual Generation Comparison of 10 Asia Pacific

Countries(MW), 2010-2020 .......................................................................................................42 Figure 16: Power Market, China, Thermal Power Generation (GWh), 2000-2030 .....................................43 Figure 17: Power Market, China, Hydropower Generation (GWh), 2000-2030 ..........................................45 Figure 18: Power Market, China, Nuclear Power Generation (GWh), 2000-2030 ......................................47 Figure 19: Power Market, China, Renewable Power Generation (GWh), 2000-2030 ................................49 Figure 20: Power Market, China, Installed Capacity Share of Major Power Generating Companies (%),

2009 ..........................................................................................................................................64

China Power Market Outlook to 2030 - Business Propensity Indicator (BPI), Market Trends, Regulation and Competitive Landscape

GDPE0513ICR / Published JUL 2011 Page 6

© GlobalData. This report is a licensed product and is not to be photocopied

2 Introduction

Since 1979, China has reformed and opened its economy to the world. The liberalization of the country‟s

markets occurred in the 1990s and 2000s. Historically, the country has averaged a growth rate of 10%

and all the industries have been booming in the country. China presents as the most promising Asia-

Pacific market for majority of the power generation and equipment market along with other industries. The

country‟s rapid industrialization has increased the demand for power from energy-intensive industries.

In 2002, in line with the power reform plan, China‟s electricity generation was separated from grid

operations and separate entities were created to govern each. The generation assets of the State Power

Corporation were split into five newly created generating companies known as the Big Five, namely, the

China Datang Corporation, the China Guodian Corporation, the China Huadian Corporation, the China

HuaNeng Group and the China Power Investment Corporation. The transmission and distribution assets

were separated into two major grid companies, namely, the State Grid Corporation of China (SGCC) and

China Southern Power Grid Company Limited. In 2003, the State Electricity Regulatory Commission

(SERC) was established by the State Council, which is responsible for developing laws and regulations

and performing administrative and regulatory duties for the national power industry. The National

Development and Reform Commission (NDRC), under the State Council, is a macroeconomic

management agency. Its major functions include approving major power projects and formulating plans

for the development of the energy sector.

The accelerated development of China‟s renewable energy industry has been promoted by a combination

of government encouragement and market guidance. The government of China has developed various

financial and regulatory initiatives to promote renewable energy sources. The main regulatory policy

framework for renewable energy in China is based on the national development plan and the Renewable

Energy Law. The Law, effective from January 1, 2006, set an obligatory target that 10% of China‟s power

capacity should be generated from renewable energy sources by 2010.

The SGCC, a state-owned corporation, is the largest electricity transmission and distribution company in

China. It operates with five subsidiaries, namely, North China Grid Company Ltd, Northwest China Grid

Company Ltd, Northeast China Grid Company Ltd, East China Grid Company Ltd and Central China Grid

Company Ltd. China Southern Power Grid Company Limited is the state-owned enterprise for power

transmission, covering China's five southern provinces of Guangdong, Guangxi, Yunnan, Guizhou and

Hainan. China has wide-ranging cross-regional interconnections and is moving towards a nationwide

interconnected grid system. There are seven inter-provincial power networks, namely, Northwest China,

Northeast China, East China, Central China, North China, South China and Sichuan and Chongqing.

There are also five independent provincial-level power networks, namely, Xinjiang, Hainan, Shandong,

Fujian and Tibet.

The demand from the industrial sector has witnessed the highest growth in recent years in China.

Increased demand from energy-intensive industries, along with increases in the standard of living,

progress in rural electrification and a decline in rural electricity prices, and an increase in consumption in

the residential sector, have rapidly increased power consumption in the country. The cumulative installed

capacity of China was 977,019 Megawatts (MW) in 2010, with thermal sources accounting for over 72%

of installed capacity. The increasing demand is being met by the installation of new generating capacity.

China Power Market Outlook to 2030 - Business Propensity Indicator (BPI), Market Trends, Regulation and Competitive Landscape

GDPE0513ICR / Published JUL 2011 Page 7

© GlobalData. This report is a licensed product and is not to be photocopied

2.1 GlobalData Report Guidance

The report comprises an executive summary capturing the key growth trends in the China power

market.

The next chapter covers the methodology to Business Propensity Indicator for the country.

The next chapter covers the Business Propensity Indicator analysis of the country from 2000-2020

The next chapter covers the demand and consumption scenario of the market, import and export

scenario, and the power consumption patterns from 2000-2010 with forecasts to 2030.

This is followed by cumulative capacity and power generation information and the segmentation by

source of energy from 2000–2010, with forecasts to 2030.

The following chapter provides information on the top active and planned power plants, segmented

by the source of energy.

The chapter on regulatory structure describes in brief the power regulatory structure, prominent

policies and policies influencing the future of the power market.

The chapter on infrastructure shows data on the electricity transmission infrastructure and future

development plans.

The last chapter describes the competitive landscape of the country‟s power market, with a complete

description and SWOT analysis of the top companies in the market.

China Power Market Outlook to 2030 - Business Propensity Indicator (BPI), Market Trends, Regulation and Competitive Landscape

GDPE0513ICR / Published JUL 2011 Page 8

© GlobalData. This report is a licensed product and is not to be photocopied

3 Business Propensity Indicator Methodology

3.1 Methodology Adopted For Evaluating the Business Propensity Indicator for the Asia Pacific region

The business propensity indicator is evaluated for 17 countries in the Asia Pacific region. This indicator is

arrived at based on detailed analysis of each of the countries on six key factors, which are likely to have

a huge impact on the growth of the power industry in that country. This analysis is further scaled down

wherein a series of parameters under each factor are analyzed. These parameters have been identified

on the basis of GlobalData‟s understanding of the power market and discussions with industry experts

across a broad spectrum of the power supply chain.

The seventeen countries are evaluated on factors such capacity and reserve potential, the regulatory,

economic, investment and competitive scenarios, and the transmission and distribution infrastructure for

both the current and future, thereby identifying investment potential in the power sector in each country.

Each of the seventeen countries in the region are ranked from 1 to 17 based on the scores for the future

scenario. The current scenario scores help in understanding the prevalent power market in that country.

The six key factors identified to arrive at the business propensity indicator for a country are as follows:

3.1.1 Capacity and Reserve Potential

The capacity and reserve potential as a factor evaluates the country on certain key parameters such as

energy security and its reliance on a number of technologies to meet its power requirements. The final

outcome attempts to analyze the country‟s energy and power independence.

There are four key parameters that are evaluated in order to arrive at a final score of this factor. These

are as follows:

3.1.1.1 Total Installed Capacity

Installed capacity in a country is an indicator of the total size of the power sector.

Current Scenario (2010)

This parameter evaluates the current installed capacity in the country.

Future Scenario (2020)

This parameter evaluates the forecasted installed capacity in the country.

3.1.1.2 Compound Annual Growth Rate (CAGR) of Installed Capacity

The CAGR of the installed capacity is an indicator of the rate of development and investment in the power

generating capacity of the country. A higher CAGR of installed capacity indicates strong investments in

the generating capacity of the country.

Current Scenario (2000-2010)

This parameter evaluates the growth of installed capacity in the country over the last decade.

Future Scenario (2011-2020)

The parameter is an indicator of the likely rate of growth in the generating capacity foreseen for the

country over the coming decade.

China Power Market Outlook to 2030 - Business Propensity Indicator (BPI), Market Trends, Regulation and Competitive Landscape

GDPE0513ICR / Published JUL 2011 Page 9

© GlobalData. This report is a licensed product and is not to be photocopied

3.1.1.3 Power Diversity Mix (2010)

This parameter evaluates the level of power diversity mix in the country. It looks at the number of

technologies used for power generation in the country and the total percentage of the highest technology

in the total capacity mix in order to evaluate this parameter. Strength of power diversity mix indicates the

countries reliance on a number of technologies and fuels to meet its power needs.

Current Scenario (2010)

In the current scenario this parameter looks at the number of technologies used in the country to generate

power and it also evaluates the percentage of reliance on the largest technology as of 2010.

Future Scenario (2020)

This parameter looks at the technology dependence on various fuel sources for power generation in the

future. A country‟s dependence on a single technology to meet its future needs is also considered while

evaluating this parameter.

3.1.1.4 Reserve Potential

Setting up of power plants in a country depends, to a large extent, on the fuel reserves that the country

possesses. The fuel reserves in a country help in evaluating whether the country has the current and the

potential resources to be able to meet its power needs. The final outcome helps in evaluating the

country‟s self sustainability to meet its power needs.

Current Scenario (2010)

In the present scenario this parameter evaluates the present fuel reserve potential in the country as of

2010.

Future Scenario (2020)

In the future scenario this parameter evaluates the future fuel reserve potential in the country as is

expected in 2020.

3.1.2 Regulatory Scenario

The regulatory scenario of the countries is evaluated on the basis of two parameters, namely the

regulations pertaining to power generation and transmission and emission specific regulations. In the

future, the intentions of the government on these two parameters have been analyzed.

3.1.3 Investment Scenario

The investment scenario in a country looks at the investment opportunity available in the power sector. In

order to arrive at this, the investments made by both the government and private sector are considered.

The parameters evaluated to arrive at a score for this factor are as follows:

3.1.3.1 Foreign Direct Investment (FDI) in Power

The percentage of FDI allowed in a country‟s power sector is an indicator of the investment scope for

foreign players. The higher the allowed percentage of FDI the better is the investment scenario for foreign

players in the country‟s power sector.

Present Scenario (2010)

The parameter evaluates the FDI allowed in the power sector as of 2010

Future Scenario (2020)

This parameter evaluates the intent for FDI in the power sector for the country in the future

3.1.3.2 Governmental and private investments in the power sector

This parameter evaluates the investments made by the government and the private players in the

country‟s power sector. For the future scenario, any plans or intentions to invest in the power sector are

captured to evaluate this parameter.

China Power Market Outlook to 2030 - Business Propensity Indicator (BPI), Market Trends, Regulation and Competitive Landscape

GDPE0513ICR / Published JUL 2011 Page 10

© GlobalData. This report is a licensed product and is not to be photocopied

3.1.3.3 Ease of Doing Business

The ease of doing business is a global ranking exercise on 183 countries conducted by the World Bank.

This parameter averages the country's percentile rankings on 10 topics, made up of a variety of

indicators, giving equal weights to each topic. 1 is the highest rank (highest ease of doing business) and

183 is the lowest rank (Ranked lowest on ease of doing business). The various categories considered for

ranking the countries are:

Present Scenario (2009) (Pre recession Scenario)

This ranking indicates the pre recession ranking of the countries.

Future scenario (2011) (Post recession Scenario)

This ranking indicates the post recession ranking of the countries. These rankings are also a good

indicator of the country‟s future ease of doing business.

Table 1: Ease of Doing Business-Categories and Subcategories

Categories Subcategories

Starting a business Procedures, time, cost and paid-in minimum capital to open a new business

Protecting investors Strength of investor protection index , extent of disclosure index , extent of director liability index and ease of shareholder suits index

Dealing with construction permits

Procedures, time and cost to obtain construction permits, inspections and utility connections

Paying taxes Number of tax payments, time to prepare and file tax returns and to pay taxes, total taxes as a share of profit before all taxes are paid

Employing workers Trading across borders

Registering property Procedures, time and cost to transfer commercial real estate

Enforcing contracts Procedures, time and cost to resolve a commercial dispute

Getting Credit Strength of legal rights index, depth of credit information index

Closing of business Recovery rate in bankruptcy

Starting a business Procedures, time, cost and paid-in minimum capital to open a new business

Protecting investors Strength of investor protection index, extent of disclosure index, extent of director liability index and ease of shareholder suits index

Dealing with construction permits

Procedures, time and cost to obtain construction permits, inspections and utility connections

Paying taxes Number of tax payments, time to prepare and file tax returns and to pay taxes, total taxes as a share of profit before all taxes are paid

Employing workers Trading across borders

Registering property Procedures, time and cost to transfer commercial real estate

Enforcing contracts Procedures, time and cost to resolve a commercial dispute

Getting Credit Strength of legal rights index, depth of credit information index

Source: GlobalData, Doingbusiness.com

China Power Market Outlook to 2030 - Business Propensity Indicator (BPI), Market Trends, Regulation and Competitive Landscape

GDPE0513ICR / Published JUL 2011 Page 11

© GlobalData. This report is a licensed product and is not to be photocopied

3.1.4 Transmission and Distribution (T&D) Infrastructure

The robustness of a country‟s transmission and distribution infrastructure is a strong indicator of the

strength of the power sector in that country. A strong infrastructure indicates a stable market for

investment in the generation side of the power sector.

This factor evaluates the following parameters to arrive at a final score for the factor.

3.1.4.1 Existing Transmission and Distribution Infrastructure

This parameter evaluates the existing T&D infrastructure in the country. It takes into account whether the

country‟s available infrastructure is able to meet its present requirements. It is indicative of the robustness

of the T&D infrastructure.

Present Scenario (2010)

It evaluates the robustness of the existing T&D infrastructure in the country.

Future Scenario (2020)

The parameter evaluates the upcoming T&D infrastructure in the country and its impact on the power

sector.

3.1.4.2 Transmission and Distribution Interconnections

Interconnections are a strong indicator of the country‟s ability to meet its electricity demand, either peak or

normal load through imports. The existence of a strong network of interconnections also allows the

country to participate in inter-regional power pools, thereby generating additional revenues.

3.1.4.3 Electrification Ratio

The electrification ratio is the ratio of households with an electricity connection to total households in the

country. The countries are compared on the electrification ratio and ranked in descending order. A high

electrification ratio indicates high electricity penetration levels, made possible by the existence of robust

transmission and distribution networks. A country with a better transmission and distribution infrastructure

will have a higher probability of generating more electricity in the future, if other needs such as fuel

resources and financial requirements are met. Hence, for the purpose of this study the countries with

higher electrification rates are ranked higher.

3.1.4.4 T&D Losses

The transmission and distribution losses are the amount of power lost while getting transmitted from one

point to another. These include losses in transmission between sources of generation and points of

distribution and in the distribution to consumers, including pilferage.

High transmission losses in a country signify a poor transmission infrastructure and loss of revenue to the

utilities and other entities operating in sale of electricity. Hence for this study, countries with greater

transmission and distribution losses have been ranked lower.

China Power Market Outlook to 2030 - Business Propensity Indicator (BPI), Market Trends, Regulation and Competitive Landscape

GDPE0513ICR / Published JUL 2011 Page 12

© GlobalData. This report is a licensed product and is not to be photocopied

3.1.5 Macro Economic Scenario

Macro economic factors are indicative of the behavior of the economy as a whole which in turn will

determine the growth of the power sector in the country. As such, certain parameters including population

growth, Gross Domestic Product (GDP) growth, and political scenario are analyzed to understand the

performance of the economy.

3.1.5.1 Actual Consumption and CAGR of Consumption

This parameter is indicative of the actual consumption and the rate at which electricity consumption is

growing in the country. This helps in understanding the consumption pattern in the country and how it is

going to change in the future. A high rate of growth indicates that the necessary steps may be taken by

the governments of the respective countries to increase electricity generation. This makes countries with

higher consumption and high growth rates more attractive.

Present Scenario (2010)

The electricity consumption in the country as of 2010 is evaluated along with the CAGR of electricity

consumption over the last decade.

Future Scenario (2020)

The electricity consumption expected in the country as of 2020 is evaluated along with the CAGR of

electricity consumption forecasted over the coming decade.

3.1.5.2 CAGR of GDP

GDP, which is the most accurate snapshot of the economy as a whole, will determine the pace of

development in the power sector.

Present Scenario (2005-2010)

CAGR of GDP for the last five years is calculated

Future Scenario (2011-2015)

CAGR of GDP forecasted for the next five years is calculated

3.1.5.3 Actual population and CAGR of Population

This parameter is indicative of the actual population per square km in the country and the rate at which

the population is growing. Growth in the population is indicative of the growth of the power sector in the

country.

Present Scenario (2000-2010)

Actual population per square km in the country as of 2010 and population growth over the last decade.

Future Scenario (2011-2020)

Actual population per square km expected in the country as of 2020 and population growth foreseen for

the next decade.

3.1.5.4 Political Risk

It is indicative of the stability of the government and policies favoring the country‟s economic

development. A stable government will result in cohesive policy which in turn will spur developments in

the power sector.

Present Scenario (2010)

It indicates the stability of the government at present by underlying key policies favoring the development

of the power industry.

Future Scenario (2020)

It indicates the forecasted stability of the government by considering likely policies that will influence the

development of the market.

China Power Market Outlook to 2030 - Business Propensity Indicator (BPI), Market Trends, Regulation and Competitive Landscape

GDPE0513ICR / Published JUL 2011 Page 13

© GlobalData. This report is a licensed product and is not to be photocopied

3.1.6 Competitive Scenario

The competitive scenario factor evaluates the competition in the power sector of a country. This

parameter is important to understand the level of competition and hence the growth available in the power

sector of the country. This factor is evaluated keeping in mind the following parameters:

3.1.6.1 Entry Barrier

This parameter evaluates the barriers of entry in the power sector of the country. The higher the entry

barrier the more difficult it is for a new entrant to enter the market.

Present Scenario (2010)

This parameter evaluates the barrier of entry in the power sector in the present scenario.

Future Scenario (2020)

This parameter evaluates the barrier of entry that may impact on the market in the future.

3.1.6.2 Degree of Competition

This parameter evaluates the market structure in the power market of a country, such as the number of

competitors operating in the market and their installed capacity. It also evaluates the level of competition

in the power retail sector in the country.

Present Scenario (2010)

The parameter evaluates the degree of competition and the retail power market in the present scenario in

the country‟s power sector.

Future Scenario (2020)

The parameter evaluates the degree of competition foreseen in the future and the expected retail power

activity in the future in the county.

3.1.6.3 Power Equipment Market Competition

This parameter evaluates the competition in the country‟s equipment market. A higher level of competition

indicates a lower degree of monopoly and a low barrier to entry in the equipments market. It is an

indicator of the growth potential in the equipment market.

Present Scenario (2010)

The parameter evaluates the degree of competition in the present equipment market in the power sector.

Future Scenario (2020)

The parameter evaluates the foreseen degree of competition in the equipment market in the power sector

in the future.

China Power Market Outlook to 2030 - Business Propensity Indicator (BPI), Market Trends, Regulation and Competitive Landscape

GDPE0513ICR / Published JUL 2011 Page 14

© GlobalData. This report is a licensed product and is not to be photocopied

3.2 Methodology Adopted to Arrive at a Final Rank

In order to rank the seventeen countries in the Asia Pacific region the following methodology has been

adopted:

Each of the factors has been assigned a weightage based on the level of impact each factor has on the

business propensity indicator of the country. These weightages have been arrived at based on a series of

discussions with industry experts across the supply chain. The weightages assigned are as follows:

Figure 1: Weightage Assigned to the Six Factors (%),2000-2020

0%

5%

10%

15%

20%

25%

Capacity and Reserve Potential

Regulatory Scenario

Investment Scenario

Transmission and DistributionInfrastructure

Macroeconomic Scenario

Competitive Scenario

Source: GlobalData

The factor, capacity and reserve potential of a country, has been assigned a strong weightage of 25%, as

it evaluates the existing and future growth in the country‟s installed generating capacity, which is expected

to have the biggest impact on the country‟s business propensity indicator. The reserve potential in the

country for the present and future scenarios is also evaluated. The growth of the power sector is largely

dependent on the reserve potential in the country as well as the growth of the existing generating

infrastructure and hence this factor will have a strong impact on the business propensity indicator of the

country.

The regulatory infrastructure factor in a country is assigned a weightage of 15%. This is because the

present regulatory reforms in the country as well as in the future are expected to drive the growth of the

power sector. Governmental regulations and incentives are expected to be one of the biggest drivers for

power sector investment.

The investment scenario factor in a country is assigned a weightage of 15%.This factor is evaluated on

the basis of investments allowed and driven by the government and the private sector in the country.

Larger investments will drive the growth in the country‟s power sector.

The transmission and distribution infrastructure factor is also assigned a weightage of 15%.This factor

evaluates the robustness of the transmission and distribution infrastructure to facilitate growth in the

power sector.

China Power Market Outlook to 2030 - Business Propensity Indicator (BPI), Market Trends, Regulation and Competitive Landscape

GDPE0513ICR / Published JUL 2011 Page 15

© GlobalData. This report is a licensed product and is not to be photocopied

The macro economic factor is assigned a weightage of 15%. This factor evaluates the economic growth of

the country. Economic development of a country largely impacts on the growth of the power sector and

hence this factor has been assigned a strong weightage.

The competitive scenario factor has been assigned a weightage of 15%.This factor evaluates the level of

competition in the country‟s power sector and is an indicator of the growth opportunity in the power

industry.

Each parameter in the above mentioned factors has been evaluated from a scale of 1 to 6 with 1 been the

lowest score and 6 indicating the highest growth.

Table 2: Scoring Methodology for the Parameters

Score

1 Lowest

2

3

4

5

6 Highest

Source: GlobalData

China Power Market Outlook to 2030 - Business Propensity Indicator (BPI), Market Trends, Regulation and Competitive Landscape

GDPE0513ICR / Published JUL 2011 Page 16

© GlobalData. This report is a licensed product and is not to be photocopied

The Best Case Scenario is as follows:

The final score for the present as well as the future scenario will be out of a total score of 20.

Table 3: Best Score for Present and Future Scenario

Factor Weightage Parameter Best

Score

Capacity and Reserve Potential 25%

Existing Installed Capacity 6

Power Diversity Mix 6

Resource Reserve Potential 6

CAGR of Installed Capacity 6

Regulatory Scenario 15% Regulatory for generation and transmission 6

Regulatory for emissions 6

Investment Scenario 15%

FDI in Power 6

Government and Private Investments 6

Doing Business Rank 6

Transmission and Distribution Infrastructure

15%

Existing T&D 6

Existing Interconnection 6

T&D Losses 6

Electrification Ratio 6

Macro Economic 15%

GDP CAGR 6

Population per sq. km, CAGR of population 6

Actual Consumption, CAGR of consumption 6

Political Risk 6

Competitive Scenario 15%

Entry Barrier 6

Degree of Competition in power generation, retail sector competition

6

Equipment Market 6

Total 20

Source: GlobalData

China Power Market Outlook to 2030 - Business Propensity Indicator (BPI), Market Trends, Regulation and Competitive Landscape

GDPE0513ICR / Published JUL 2011 Page 17

© GlobalData. This report is a licensed product and is not to be photocopied

4 Power Market, China, Business Propensity Indicator

The following section analyses China on the basis of six factors in order to analyze the power market of

the country. The analysis focuses on both the present scenario of the market as well as the expected

future scenario. The factors which have been considered in the analysis are the capacity and resource

potential in the country, the regulatory mechanism in power sector, the investment scenario in the power

sector, transmission and distribution infrastructure, macroeconomic conditions and the competitive

scenario in the country‟s power sector.

Figure 2: Power Market, China, Business Propensity Indicator

1

0

1

2

3

4

5

6

Future Scenario

Bu

sin

ess P

rop

en

sit

y S

co

re

Present Scenario

Capacity and Reserve Potential

Regulatory Environment

Investment Scenario

T&D Infrastructure

Macroeconomic Scenario

Competitive Scenario

High Propensity Indicator

Medium Propensity

Indicator

Low Propensity Indicator

Low

Score

High

Score

Source: GlobalData

*The scores of individual factors cannot be compared among themselves as the final score for each factor

differs. This chart is indicative of the change in the factors in present and future scenario

China Power Market Outlook to 2030 - Business Propensity Indicator (BPI), Market Trends, Regulation and Competitive Landscape

GDPE0513ICR / Published JUL 2011 Page 18

© GlobalData. This report is a licensed product and is not to be photocopied

4.1 Capacity and Reserve Potential

China is the main driver for the Asia-Pacific power market, with an installed capacity base of 977,019 MW

in 2010. During the period of 2000 to 2010, the installed capacity has been increasing at a Compound

Annual Growth Rate (CAGR) of 11.8% and as a result presenting various opportunities for huge

investments in the power sector. In the future, the country is expected to increase its installed capacity to

2,248,180 MW at a very high CAGR of 8.5%. The country employs all four technologies (thermal, hydro,

nuclear and renewable) with thermal sources accounting for over 72% of the total installed capacity. The

share of renewable and nuclear energy in the country‟s power mix has been relatively low. However, the

country is expected to increase the share of other technologies to diversify its portfolio. By 2020, thermal

installations are expected to account for just 64.8% of total installed capacity. The government has set

huge targets for increasing installation capacities for all types of power plants. The country aims to

increase the use of non-fossil fuel to 15% by 2020. This includes hydro, renewable and nuclear power

generated from domestic sources.

The majority of fuel requirements in china are met by domestic fuel production. Coal is completely met by

domestic production and most gas demand is met through domestic production as well. The country has

very small amounts of liquified natural gas (LNG) imports that are required to meet the gas requirements

in the country. The uranium for nuclear reactors is imported. With the level of supply required by its

energy demand, however, there is a good chance that China will be a net importer of coal by 2020. This is

one of the main reasons for the country‟s focus on diversifying its energy portfolio and increasing the

share of other technologies in its power mix. Natural gas imports in the country will also increase in future

and so China is collaborating with Iran and other countries for a guaranteed LNG supply. China, being a

vast country, has a lot of potential in renewable energy, in terms of solar, biomass, wind, hydro and

geothermal power, which is expected to be capitalized on in order to maximize its renewable installed

capacity in future.

4.2 Regulatory Scenario

China has been undergoing market reforms in its power market since the early 1990s. Since then, China

has been trying to open the power market up to foreign players, increase investments and foster

capitalism in their economy. During the 2000s capacity installation increases were encouraged by the

government and as a result they have increased at a fast pace as well. Since 2003, the government has

looked into increasing the use of renewable energy in the country and has started setting targets for

increasing non-thermal resources. The government has also grown concerned over the level of carbon

emissions produced in the country. They have been shutting down inefficient, small power plants and

banned the construction of thermal power plants with capacity lower than 600 MW. The Chinese

government has also recently passed a regulation through which a part of electricity tariff would be

determined by the cost of generation. They have also introduced a system, where the country would be

divided into regions and the cost of each renewable energy installation would be different according to the

potential of each technology in each region. In March 2009, China opened 20% of its power market to

industries with high power consumption. These companies have been directly allowed to purchase power

from power generation companies.

The country is setting more stringent emission standards to reduce the emissions as well. At the end of

2009, China announced that it would reduce the carbon intensity of its GDP by 40-45% relative to 2005

levels by 2020. By 2020, utilities will be required to have 8% of their capacity and 3% of their power

generation from non-hydro renewable sources. In September 2007, the NDRC published a long-term

renewable goal report according to which, 30,000 MW of wind power, 30,000 MW of biomass and 1,800

MW of solar power were to be developed by 2020. The new renewable energy law took effect in 2010 and

this law included detailed plans for renewable energy and also addressed the issue of co-ordination of

renewable energy with the country‟s transmission grid planning. Various provisions like a guarantee of

renewable power purchase along with deadlines and penalties for non-compliance are included in the law.

China Power Market Outlook to 2030 - Business Propensity Indicator (BPI), Market Trends, Regulation and Competitive Landscape

GDPE0513ICR / Published JUL 2011 Page 19

© GlobalData. This report is a licensed product and is not to be photocopied

4.3 Investment Scenario

China is a communist country with a closed economy, which makes it difficult prospect for investment.

However, due to the huge opportunities in the country and the amount of investment required there, it has

a very good investment scenario. In 2010 alone, the country recorded investment of $106 billion

(excluding investments in the stock market). The country has a 100% FDI allowance in certain types of

power generation projects and restriction in some other types. Traditional coal power plant installations

are restricted to FDI, however, renewable, hydro and gas- fired plants are open to foreign investments. In

2010, the country ranked 78 on the ease of doing business list. There is a high amount of investment from

the private as well as public sector in the country. In 2009, the country invested $34.6 billion in clean

energy, which was the highest investment for clean energy that year. There was an investment of $12.11

billion for Ultra high voltage (UHV) transmission lines during 2009 and 2010 as well.

Power equipment manufacturers are being encouraged in the country and research grants are available

for these companies. The government has also encouraged the foreign transfer of knowledge in the

power sector when building new technologies in the country. China is expected to be one of the major

markets for smart grid investments in the future. The government is also encouraging investment in green

grids and smart grids in the country. The government has finalized a proposal for a huge amount of

money for solar farms and rooftop panels in the country. Other than this, there are a number of carbon

capture and storage projects and other power projects that are being promoted in the country, and private

companies are investing in each of these.

4.4 Transmission and Distribution Infrastructure

China is 92% electrified and the government is concentrating on improving the country‟s infrastructure

and increasing power line lengths to fully electrify the country. The main power grids cover all the cities

and most of the rural areas. Recently, 500 kilo-volt (kV) grids have begun to replace 220kV grids. China

aims to have a strong smart grid in place by 2020. Between 2000 and 2020, the country‟s transmission

line length increased at a CAGR of 7.6%. In the future, between 2011 and 2020, the transmission line

length is expected to increase at a CAGR of 9.2%. The total distribution line length is expected to grow at

a CAGR of 8.6% between 2011 and 2020 from 18,738,429 circuit kilometer (Ckm) in 2011 to 39,501,312

Ckm in 2020.

The national transmission and distribution body recently commercially deployed a 1000kV ultra high

voltage line for a length of 640km. The target is to build 17,600 km of UHV lines by 2012. The extra-high

voltage technology of smart grids will facilitate smaller losses and long distance and high capacity

networks. According to the Chinese Electricity Council‟s investment plan around $390 billion would be

spent on grid construction by 2015. The target is to build three west-east and three north-south long

distance lines in the country. With the government‟s focus on increasing the number renewable energy

projects, the state transmission body has combined the aims in order to increase the number of

transmission grid connections with increasing the renewable installed capacity in the country as well. The

government aims to build an ultra high voltage transmission network that could fully absorb the non-fossil

fuel generated electricity available, and these plans would also help bring down the current transmission

loss level of 5- 6%.

China Power Market Outlook to 2030 - Business Propensity Indicator (BPI), Market Trends, Regulation and Competitive Landscape

GDPE0513ICR / Published JUL 2011 Page 20

© GlobalData. This report is a licensed product and is not to be photocopied

4.5 Macroeconomic Factors

The GDP of China has been growing at a CAGR of 11.2% from 2005-2010, which is the highest GDP

growth in Asia-Pacific and one of the best worldwide. The population has experienced a CAGR of 0.67%

from 2000-2010. The growth of demand for electricity, along with GDP and population growth drove the

increase of electricity consumption in the country at a CAGR of 11.3% during 2000-2010.

In the future, the country‟s GDP is expected to increase at a CAGR of 9.5% from 2011-2015 and the

population at a CAGR of 0.6% from 2010-2020. Electricity consumption is forecast to increase at a CAGR

of 9.6% from 2011-2020, mainly to fulfill the country‟s internal demand and close the gap between

electricity demand and consumption in China.

The political risk in the country is high due to the communist leadership. The companies have to deal with

a closed government and with non-transparent policies and bureaucracy. The government has been

opening the country‟s markets up rapidly; but the required framework for healthy and stable foreign

investment does not exist. In the future, however, the political risk is expected to reduce once the country

is more open to capitalist markets and investment. Increased transparency in laws and policies, coupled

with acceptance of foreign establishment as part of the country is expected to happen over a period of

team.

4.6 Competitive Scenario

China is a communist economy and even though the power market is liberalized, the Chinese government

companies control most of the power generation assets in the country. The single power company was

liberalized into five big generation companies, which continued to own most of the generating capacity in

2010. Foreign investment in the country in terms of generating capacity is fairly limited. There is no retail-

level open market, and the prices are determined by the state and central bodies. However, in 2009, 20%

of the market was opened to retail where the companies could sell their power directly to the big power-

consuming companies in order to promote a retail market. The major entry barrier to the power market is

the weak enforcement of contract laws and other laws. This is a huge entry barrier for the foreign investor

especially, as the favoritism towards the local is high and there is a huge information barrier. But with

better contract laws and strengthening of other laws, this issue would be less of a barrier to entry into the

power market.

In terms of the power equipment market, the country has high levels of competition. The local competition

is very high and as a result international penetration is very low. Chinese suppliers, especially for boilers

and turbines, provide parts at cheaper prices and as a result dominate the market. The Chinese wind

turbine market is encouraged by the government‟s regulatory and policy framework. The government

encourages exports and has subsidies and other policies in place to encourage exports and research to

improve equipment technologies. Since 2006, it is estimated that the Chinese domestic wind turbine

market has increased by 100% every year. With the government‟s encouragement and further opening of

the markets, the competitive scenario in the country is very good in both scenarios.

China Power Market Outlook to 2030 - Business Propensity Indicator (BPI), Market Trends, Regulation and Competitive Landscape

GDPE0513ICR / Published JUL 2011 Page 21

© GlobalData. This report is a licensed product and is not to be photocopied

4.7 Conclusion

It can be concluded on the basis of the above analysis that the power market in China is expected to

witness improvements in the future. Major driving factors for the Chinese power market are

macroeconomic factors and the competitive structure in the country as explained in the sections above.

The political scenario is expected to be better in the future due to country‟s increasing acceptance of

foreign investment and increasing number of policies aimed towards establishing foreign players in the

country.

The competitive scenario is expected to grow stronger in the country as well. This is mainly due the

country‟s encouragement of competition within the country. The various government support programs

that are available, along with the intent to establish more competitive pricing in each state to promote

renewable energy. Transmission and distribution in China scored slightly lower than the present scenario

in the future, because, even though there is huge investment in the future scenario to improve the

country‟s transmission and distribution lines, increase its electrification ratio and raise the number of ultra

high voltage lines, there are no concrete plans for developing new interconnections with other countries.

China has a strong power mix in the present scenario, with the presence of four technologies, a high

amount of domestic fuel resources and a very high capacity installed base. In the future, this is expected

to grow even further and with the diversification of its energy portfolio and lower dependence on thermal

installed capacity that is expected by 2020, the power mix in the future scenario is rated slightly better.

The regulations in place support improving the country‟s installed capacity, generation, energy efficiency,

renewable energy sources and reducing carbon emissions in the present scenario. This strong support is

expected to continue in the future as well, and as a result they score relatively similar on the scale.

China currently has a high level of competition, especially among local players, and is going to experience

a huge increase in terms of generating capacity and investment requirements in the future. This presents

huge potential for anyone looking to invest in the country. The country‟s power sector strongly affects the

world market and China is expected to continue to be the best economy for investment among the Asian

countries.

China Power Market Outlook to 2030 - Business Propensity Indicator (BPI), Market Trends, Regulation and Competitive Landscape

GDPE0513ICR / Published JUL 2011 Page 22

© GlobalData. This report is a licensed product and is not to be photocopied

4.8 Power Market, China, Business Propensity Indicator Ranking

Figure 3: Power Market, China, Business Propensity Indicator Ranking

2

Bar Chart - Dual Back to Back

10.4

12.3

13.3

13.4

13.5

13.6

13.7

13.8

13.9

14.1

14.1

14.2

14.5

14.9

16.3

16.4

17.1

0 5 10 15 20

Afghanistan

Sri Lanka

New Zealand

Philipines

Kazakhstan

Pakistan

Malaysia

Thailand

Taiwan

Vietnam

Indonesia

Japan

Singapore

South Korea

Australia

India

China

Business Propensity Indicator– Future Scenario

8.3

10.2

10.8

11.2

11.3

11.4

11.7

12.4

13.1

13.1

13.2

13.3

13.5

13.8

14.9

15.6

16.3

0 5 10 15 20

Afghanistan

Sri Lanka

Philipines

New Zealand

Kazakhstan

Vietnam

Pakistan

Indonesia

Malaysia

Thailand

Taiwan

Japan

South Korea

Singapore

Australia

India

China

Business Propensity Indicator– Present Scenario

Country Scores Country Scores

The rating adjacent to each country are indicative of the total scores

for the country against the maximum score of 20

Source: GlobalData

4.8.1 Present Ranking

When compared with 17 other countries in the Asia-Pacific region, China ranks as the first in the present

scenario, followed by India and Australia. China has the largest capacity base in the region and the other

countries lag way behind in terms of their power mix. The country has an installed capacity of 978,742

MW in 2010, whereas India has an installed capacity of only 179, 037 MW and Japan with an installed

capacity of 240,923 MW. China has grown at a CAGR of 11.8% and it is the world‟s most populous

country. In terms of investments they significantly outperform other Asian countries.

China is ahead of the other Asia-Pacific countries in terms of GDP growth as well. They have invested

heavily in infrastructure, and like many other developed countries, they are investing in smart grid

technology and clean energy as well. China‟s investments in clean energy surpassed the USA‟s in 2010.

China is the strongest economy among the Asian countries, and their power market is bigger than any

other, which explains their being ranked first.

China Power Market Outlook to 2030 - Business Propensity Indicator (BPI), Market Trends, Regulation and Competitive Landscape

GDPE0513ICR / Published JUL 2011 Page 23

© GlobalData. This report is a licensed product and is not to be photocopied

4.8.2 Future Ranking

In the future, China is expected to remain ranked number one. They will still have a huge population, high

GDP and a huge consumption CAGR. The country is expected to increase its generating capacity by

8.5% to meet its demand. The government‟s strong investment in clean energy and transmission is

expected to continue as well. Market competition is expected to be encouraged and improve. China‟s

transmission and distribution (T&D) is expected to increase at a CAGR of 9.1% in the next 10 years, and

due to the sheer size of the country the line length base growth is expected to be higher than in other

Asian countries like India and Australia. Compared to India, its closest rival, China ranks better in

transmission losses and electrification ratio as well. Compared with India, which is also rich in domestic

fuel resources, China is expected to import a much lower percentage of coal and natural gas in the future.

China scores higher than India on power mix, infrastructure and competitive scenario in the terms of

future opportunity. Compared with Australia, its other, second-closest rival, China scores higher on its

power mix, infrastructure and macroeconomic factors.

China Power Market Outlook to 2030 - Business Propensity Indicator (BPI), Market Trends, Regulation and Competitive Landscape

GDPE0513ICR / Published JUL 2011 Page 24

© GlobalData. This report is a licensed product and is not to be photocopied

5 China Power Market Analysis, 2000-2030

5.1 Demand and Consumption Scenario

In 2010, China recorded electricity consumption of 3,446,451 GWh. The majority of the electricity was

consumed by secondary industry users, who accounted for 74.7% of electricity consumption. Secondary

industries include areas like mining and quarrying, manufacturing, production and the supply of electricity,

water and gas and construction. The power consumed by the residential sector accounted for 12.2% of

the total power consumed. Tertiary industries accounted for 10.7% of the total electricity consumption,

which includes service sectors like consumer services (like the hotel and leisure sector), producer

services (like finance and real estate), distribution services (logistic, storage, wholesale) and public

services. The primary industries, which include agriculture, forestry, animal husbandry, fishery and

services that support these industries, accounted for the remaining 2.4% of the power consumed.

Figure 4: Power Market, China, Breakdown of Electricity Consumption, By Sector (%), 2009

Secondary industry,

74.7%

Total power

consumption of urban

and rural residents,

12.2%

Tertiary Industry,

10.7%

Primary Industry,

2.4%

Source: GlobalData, China Electricity Council

Table 4: Power Market, China, Breakdown of Electricity Consumption, By Sector (%), 2009

Sector Percentage (%)

Secondary Industry 74.7%

Total Power Consumption of Urban and Rural Residents 12.2%

Tertiary Industry 10.7%

Total Power Consumption of Urban and Rural Residents 12.2%

Primary Industry 2.4%

Source: GlobalData, China Electricity Council

China Power Market Outlook to 2030 - Business Propensity Indicator (BPI), Market Trends, Regulation and Competitive Landscape

GDPE0513ICR / Published JUL 2011 Page 25

© GlobalData. This report is a licensed product and is not to be photocopied

5.2 Import and Export Scenario

China is a net exporter of electricity. China‟s total power exports stood at 10,300 GWh in 2000 whereas

imports were a mere 1,546 GWh in the same year. In 2009, China‟s total electricity exports increased to

17,386 GWh. On the other hand, imports stood at 6,006 GWh. China has signed two contracts with