Embed Size (px)

Citation preview

China Forum

SEMICON Europa

Nov 17,2017

2

China Forum Agenda

• 10:15-10:30 Registration

• 10:30-10:50 Introduction – Laith Altimime, President of SEMI Europe

• 10:50-11:20 The Rise of China IC Industry, Overview – Lung Chu,

President of SEMI China

• 11:20-11:30 SEMI innovation Investment Platform (SIIP) – EU/China

Collaboration

• 11:30-12:00 China Opportunity in an AI Era – Emon Wang, GM of

Techcode Germany

• 12:00-12:30 Q&A Session

The Rise of China IC Industry

- As A Global Ecosystem Partner

Lung Chu 居龙

President, SEMI China

Nov 17,2017 ITPC

4

Outline: Why? What? Where?

• China’s IC Development – Why?

• What?

– Government Initiatives vs Market Forces, Investments

– Opportunities and Challenges

• IC Design

• Manufacturing

• Assembly & Test

• Equipment & Material

• Future Directions. Where?

• Summary

– China as a Global IC Ecosystem Partner

CHINA330

Companie

s

EUROPE255

Companies

INDIA25

Companies

JAPAN414

CompaniesKOREA203

CompaniesAMERICA

S476

Companies

SINGAPORE33 Companies

TAIWAN215

Companies

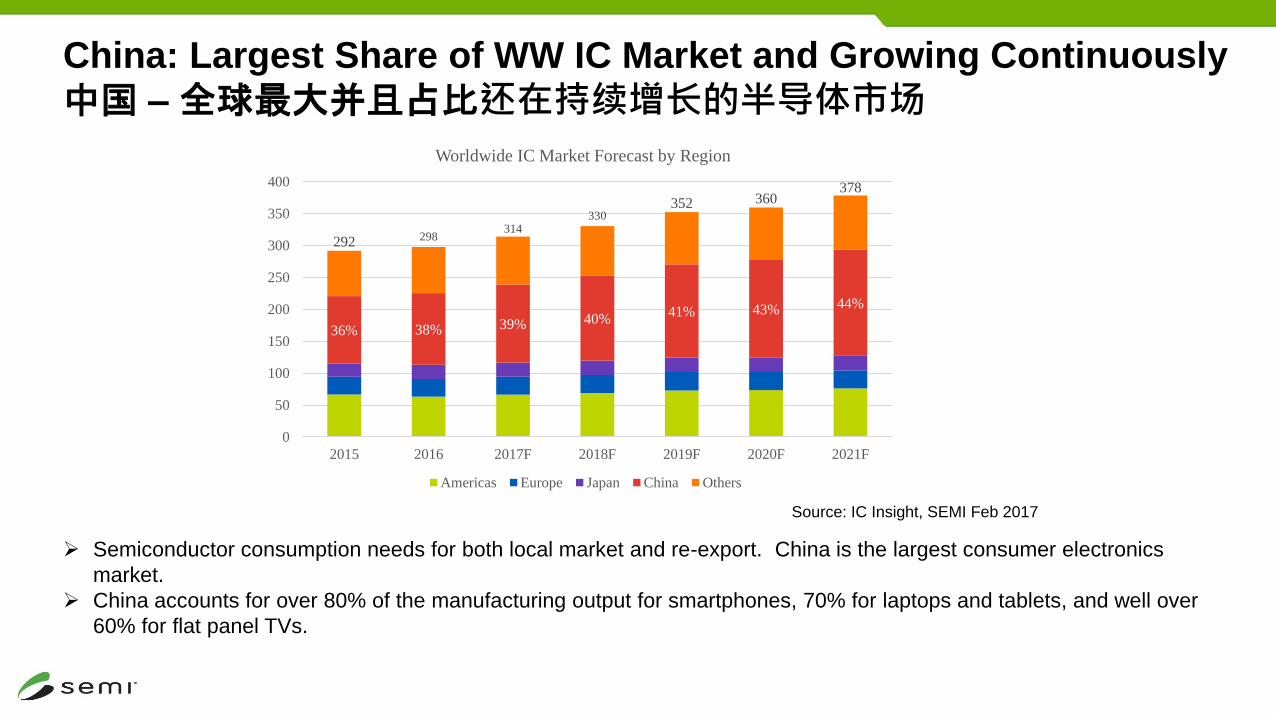

China: Largest Share of WW IC Market and Growing Continuously

中国 – 全球最大并且占比还在持续增长的半导体市场

Semiconductor consumption needs for both local market and re-export. China is the largest consumer electronics

market.

China accounts for over 80% of the manufacturing output for smartphones, 70% for laptops and tablets, and well over

60% for flat panel TVs.

Source: IC Insight, SEMI Feb 2017

36% 38% 39% 40%41% 43% 44%

292 298314

330352 360

378

0

50

100

150

200

250

300

350

400

2015 2016 2017F 2018F 2019F 2020F 2021F

Worldwide IC Market Forecast by Region

Americas Europe Japan China Others

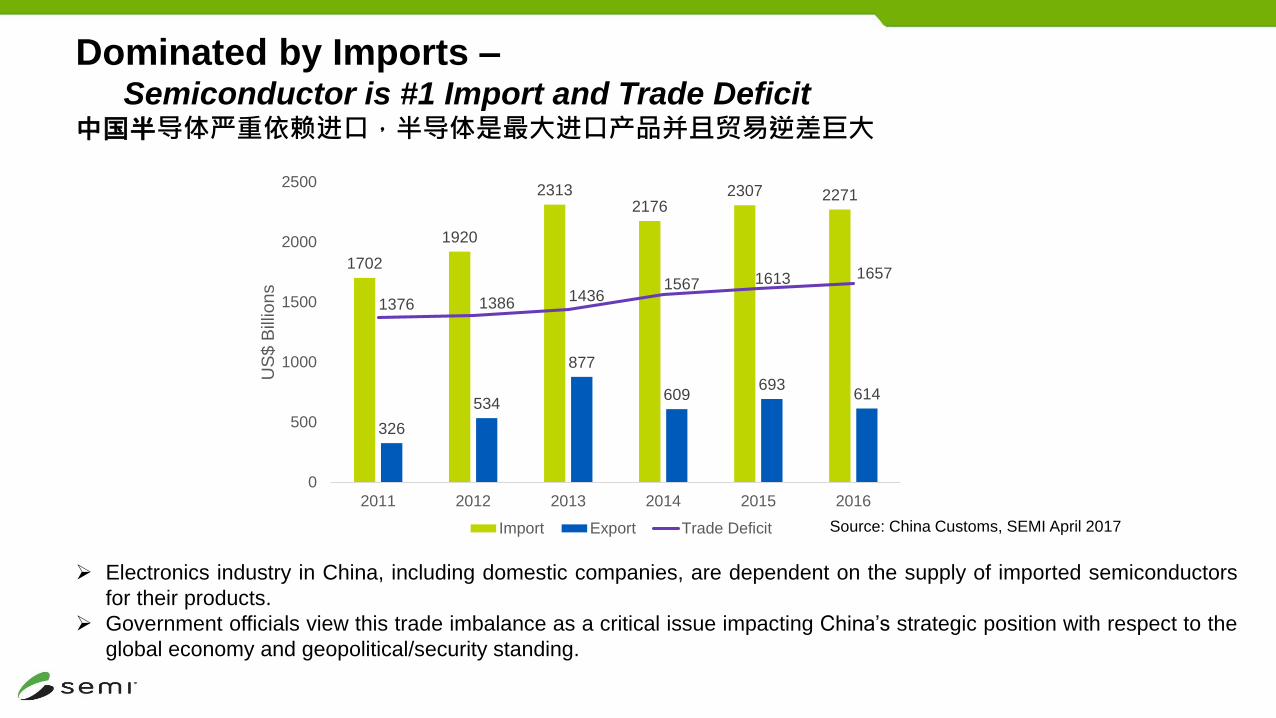

Dominated by Imports –Semiconductor is #1 Import and Trade Deficit

中国半导体严重依赖进口,半导体是最大进口产品并且贸易逆差巨大

Source: China Customs, SEMI April 2017

Electronics industry in China, including domestic companies, are dependent on the supply of imported semiconductors

for their products.

Government officials view this trade imbalance as a critical issue impacting China’s strategic position with respect to the

global economy and geopolitical/security standing.

1702

1920

23132176

2307 2271

326

534

877

609693

614

1376 1386 14361567 1613 1657

0

500

1000

1500

2000

2500

2011 2012 2013 2014 2015 2016

US

$ B

illio

ns

Import Export Trade Deficit

7

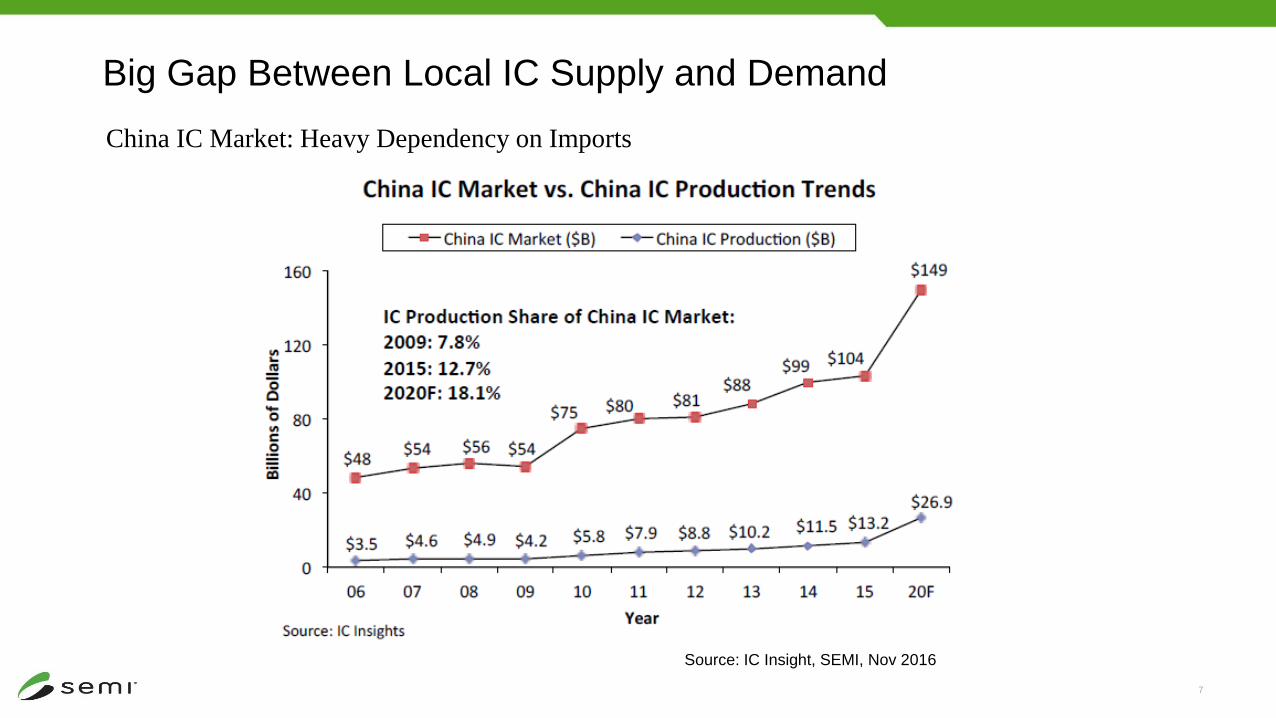

Big Gap Between Local IC Supply and Demand

China IC Market: Heavy Dependency on Imports

Source: IC Insight, SEMI, Nov 2016

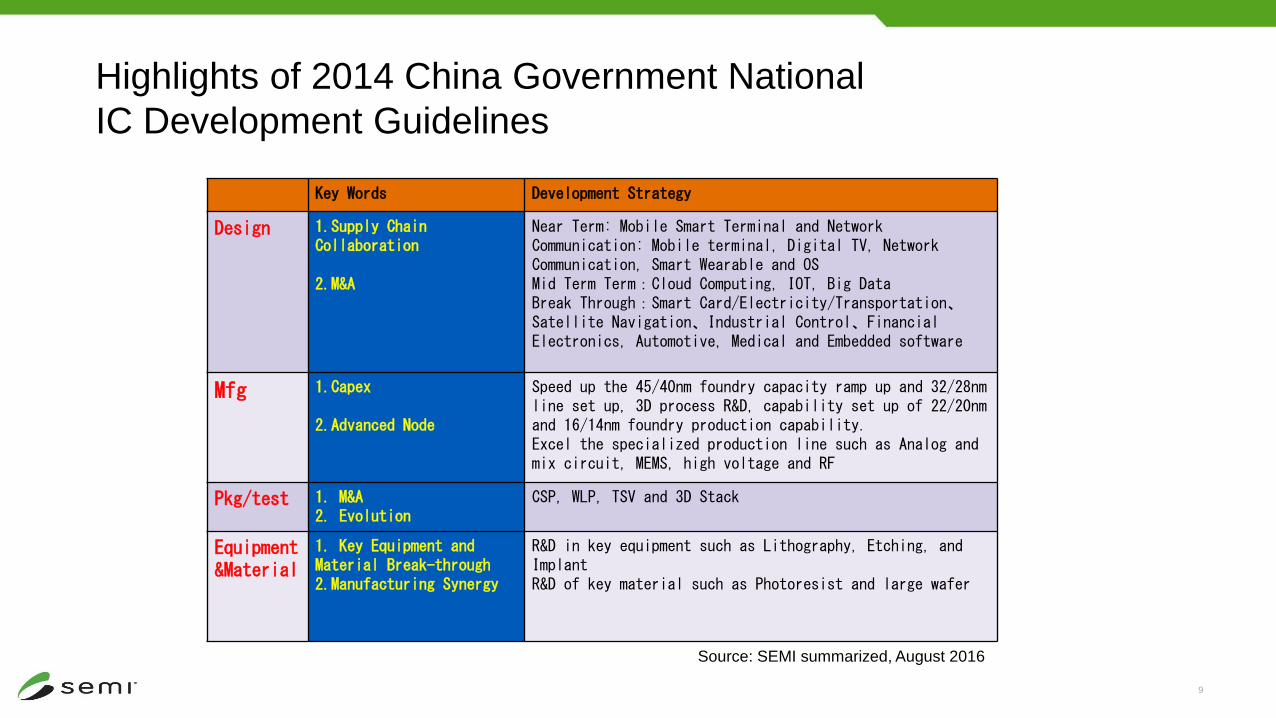

9

Key Words Development Strategy

Design 1.Supply Chain Collaboration

2.M&A

Near Term: Mobile Smart Terminal and Network Communication: Mobile terminal, Digital TV, Network Communication, Smart Wearable and OSMid Term Term:Cloud Computing, IOT, Big DataBreak Through:Smart Card/Electricity/Transportation、Satellite Navigation、Industrial Control、FinancialElectronics, Automotive, Medical and Embedded software

Mfg 1.Capex

2.Advanced Node

Speed up the 45/40nm foundry capacity ramp up and 32/28nmline set up, 3D process R&D, capability set up of 22/20nmand 16/14nm foundry production capability.Excel the specialized production line such as Analog and mix circuit, MEMS, high voltage and RF

Pkg/test 1. M&A2. Evolution

CSP, WLP, TSV and 3D Stack

Equipment &Material

1. Key Equipment and Material Break-through2.Manufacturing Synergy

R&D in key equipment such as Lithography, Etching, and ImplantR&D of key material such as Photoresist and large wafer

Highlights of 2014 China Government National

IC Development Guidelines

Source: SEMI summarized, August 2016

10

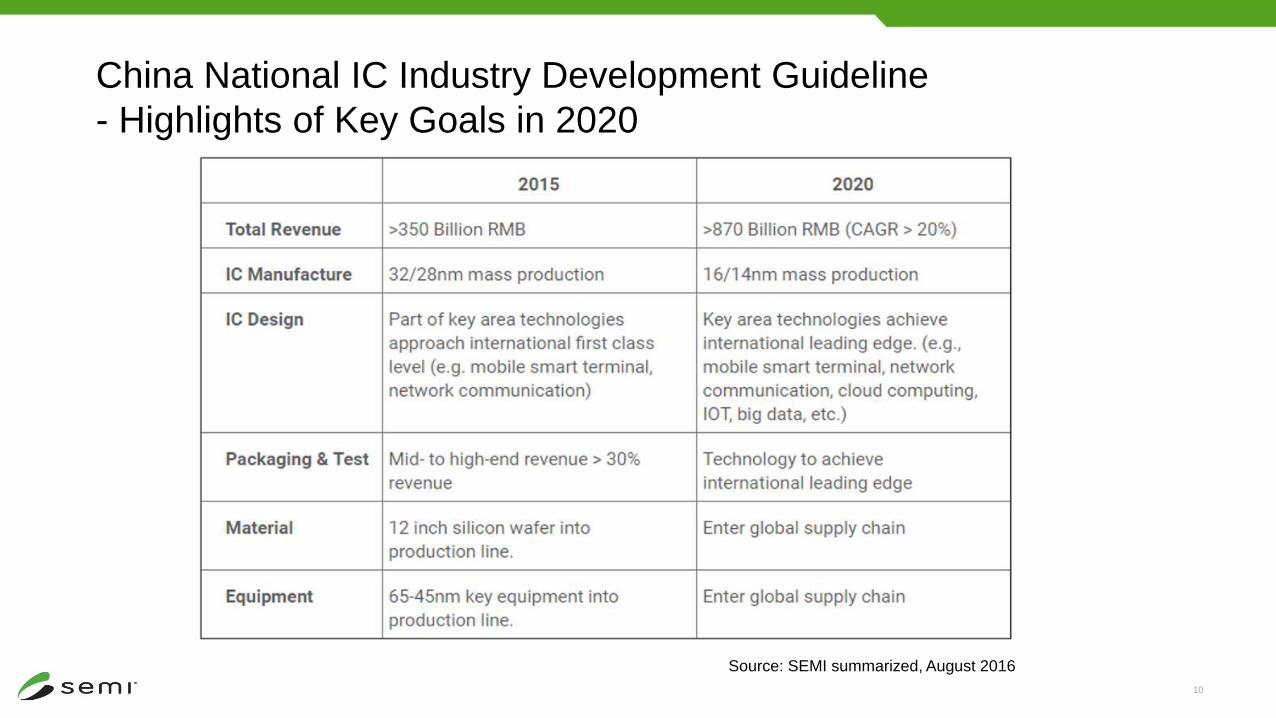

China National IC Industry Development Guideline

- Highlights of Key Goals in 2020

Source: SEMI summarized, August 2016

11

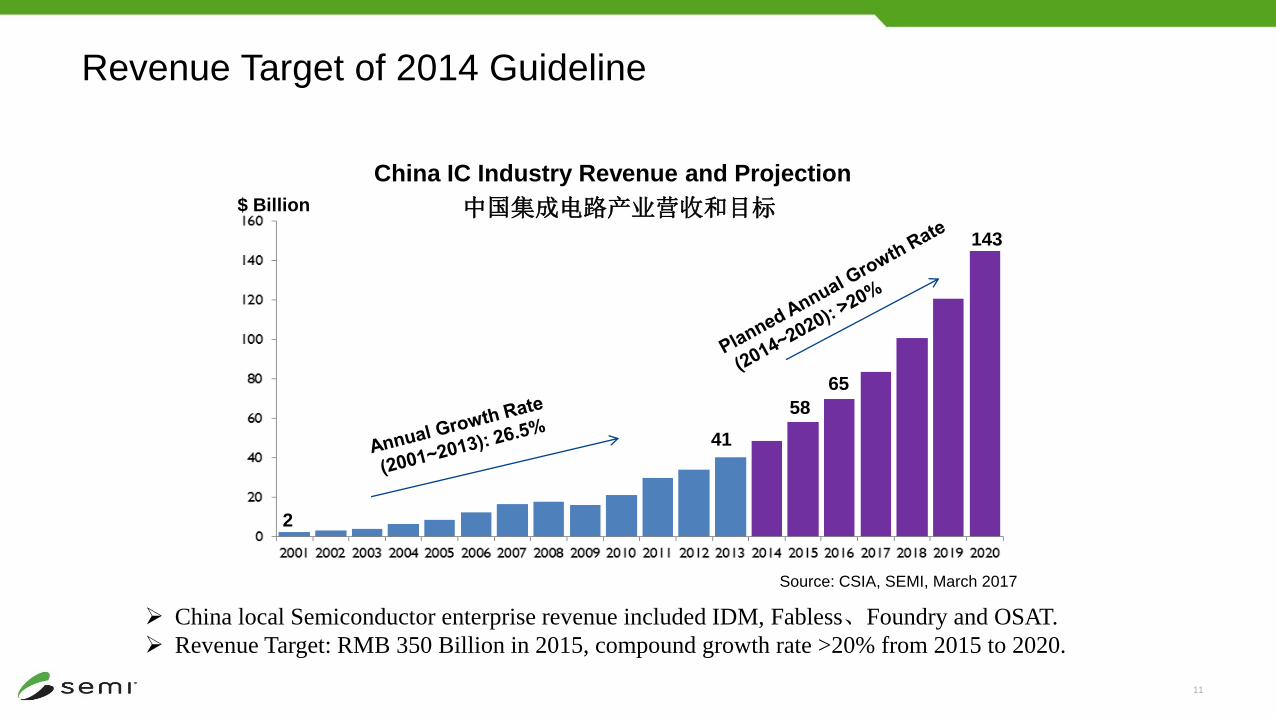

Revenue Target of 2014 Guideline

China IC Industry Revenue and Projection

41

65

143

$ Billion

2

58

Source: CSIA, SEMI, March 2017

中国集成电路产业营收和目标

China local Semiconductor enterprise revenue included IDM, Fabless、Foundry and OSAT.

Revenue Target: RMB 350 Billion in 2015, compound growth rate >20% from 2015 to 2020.

12

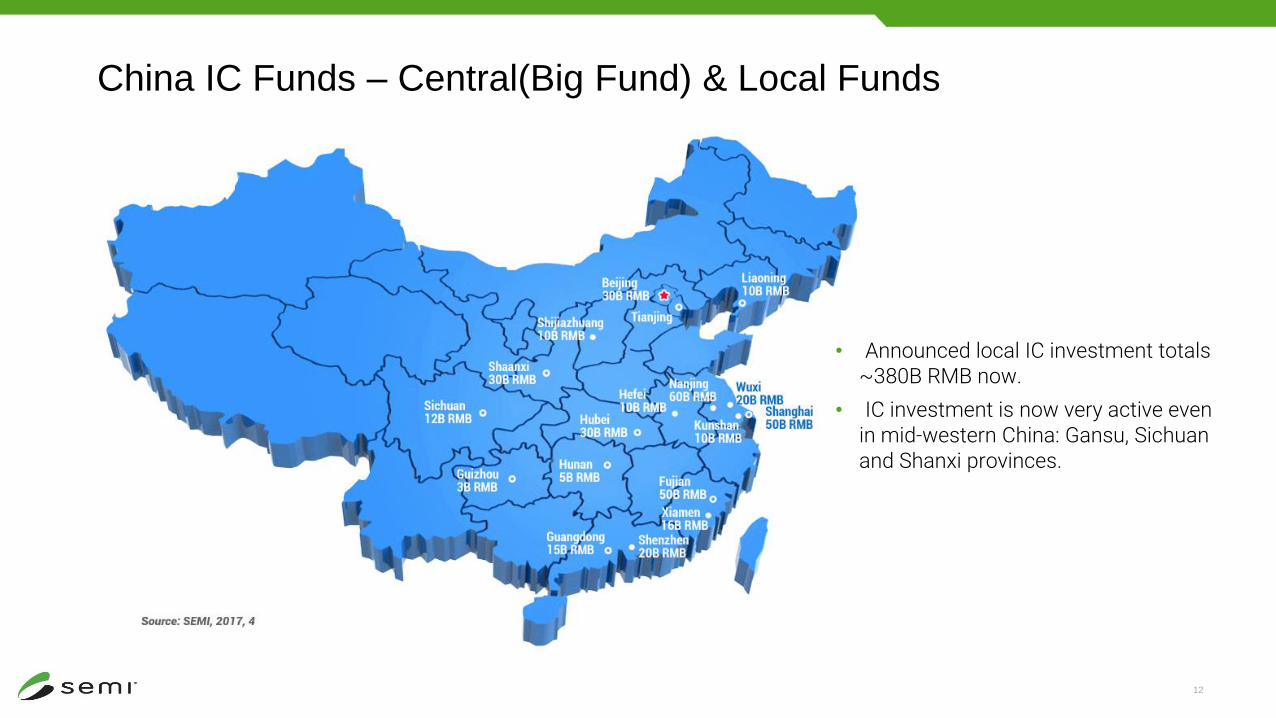

China IC Funds – Central(Big Fund) & Local Funds

About• Announced local IC investment totals

~380B RMB now.

• IC investment is now very active even in mid-western China: Gansu, Sichuan and Shanxi provinces.

14

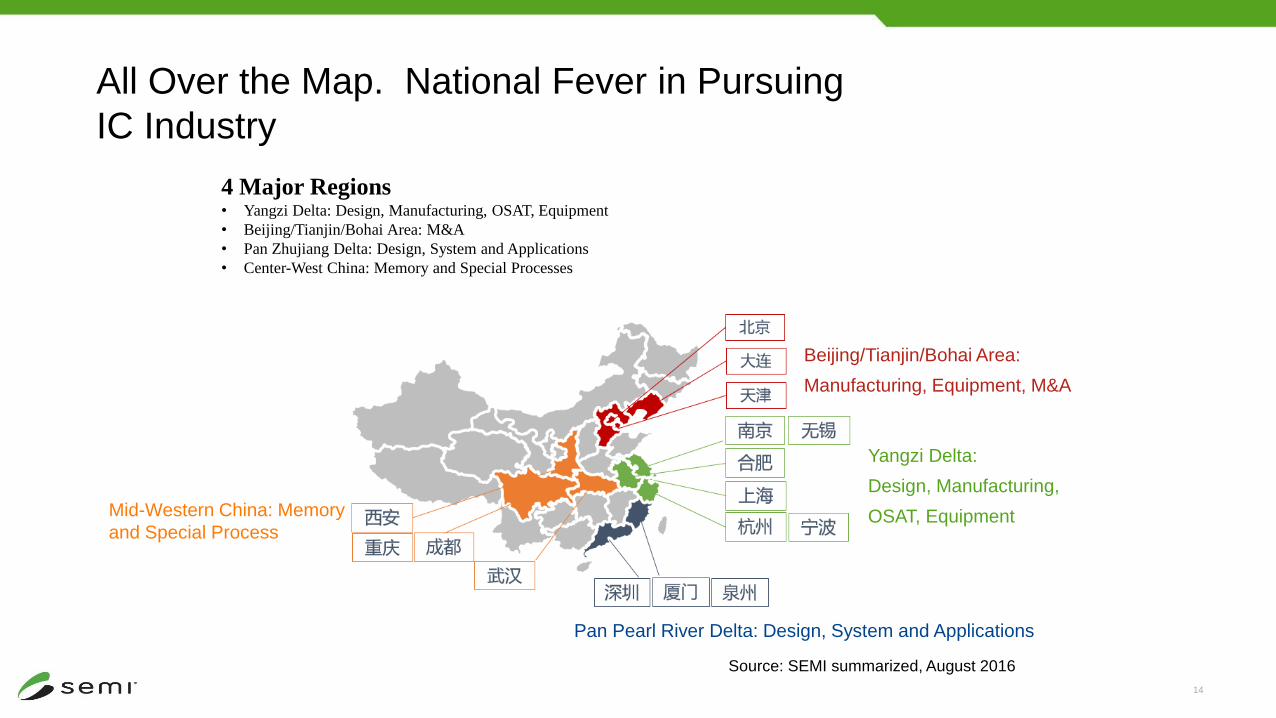

All Over the Map. National Fever in Pursuing

IC Industry

4 Major Regions• Yangzi Delta: Design, Manufacturing, OSAT, Equipment

• Beijing/Tianjin/Bohai Area: M&A

• Pan Zhujiang Delta: Design, System and Applications

• Center-West China: Memory and Special Processes

Beijing/Tianjin/Bohai Area:

Manufacturing, Equipment, M&A

Yangzi Delta:

Design, Manufacturing,

OSAT, EquipmentMid-Western China: Memory

and Special Process

Pan Pearl River Delta: Design, System and Applications

Source: SEMI summarized, August 2016

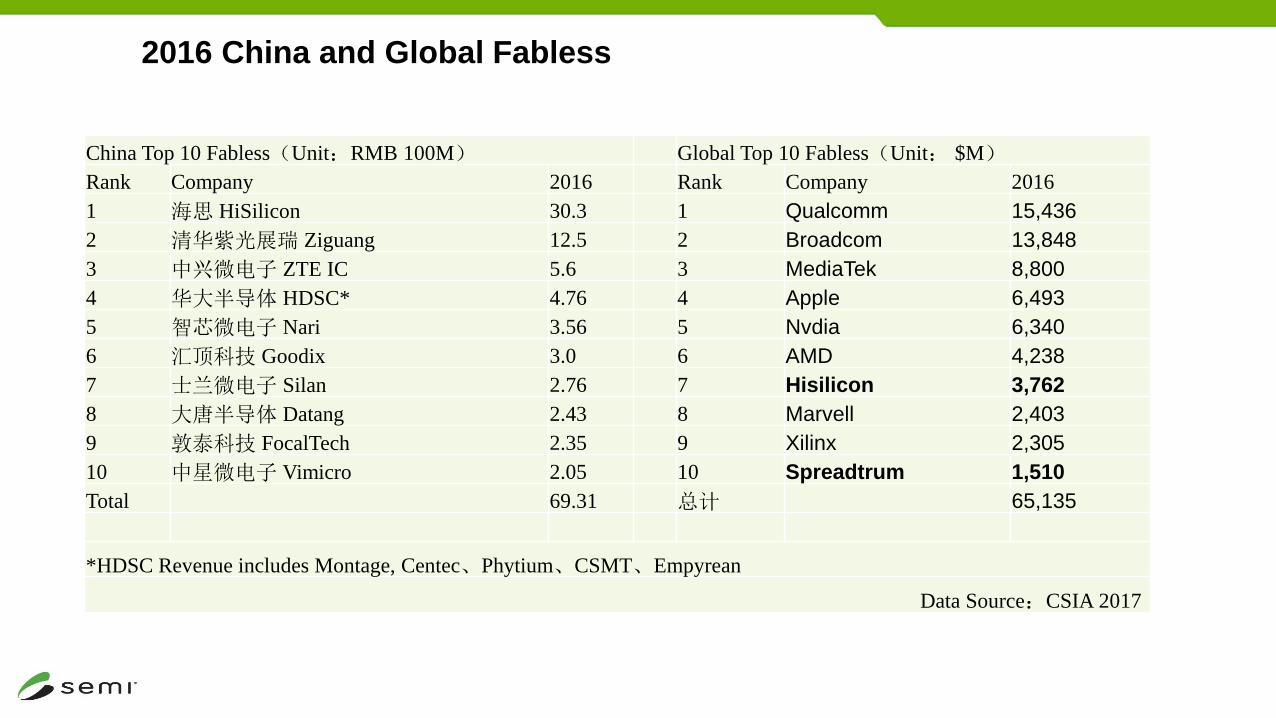

2016 China and Global Fabless

China Top 10 Fabless(Unit:RMB 100M) Global Top 10 Fabless(Unit: $M)

Rank Company 2016 Rank Company 2016

1 海思 HiSilicon 30.3 1 Qualcomm 15,436

2 清华紫光展瑞 Ziguang 12.5 2 Broadcom 13,848

3 中兴微电子 ZTE IC 5.6 3 MediaTek 8,800

4 华大半导体 HDSC* 4.76 4 Apple 6,493

5 智芯微电子 Nari 3.56 5 Nvdia 6,340

6 汇顶科技 Goodix 3.0 6 AMD 4,238

7 士兰微电子 Silan 2.76 7 Hisilicon 3,762

8 大唐半导体 Datang 2.43 8 Marvell 2,403

9 敦泰科技 FocalTech 2.35 9 Xilinx 2,305

10 中星微电子 Vimicro 2.05 10 Spreadtrum 1,510

Total 69.31 总计 65,135

*HDSC Revenue includes Montage, Centec、Phytium、CSMT、Empyrean

Data Source:CSIA 2017

16

99 97 125 134 143 161

534 569632 681

736

1362

0

200

400

600

800

1000

1200

1400

1600

2011 2012 2013 2014 2015 2016

Nu

mb

er

of C

om

pa

nie

s

Sales >100M RMB Other Fabless

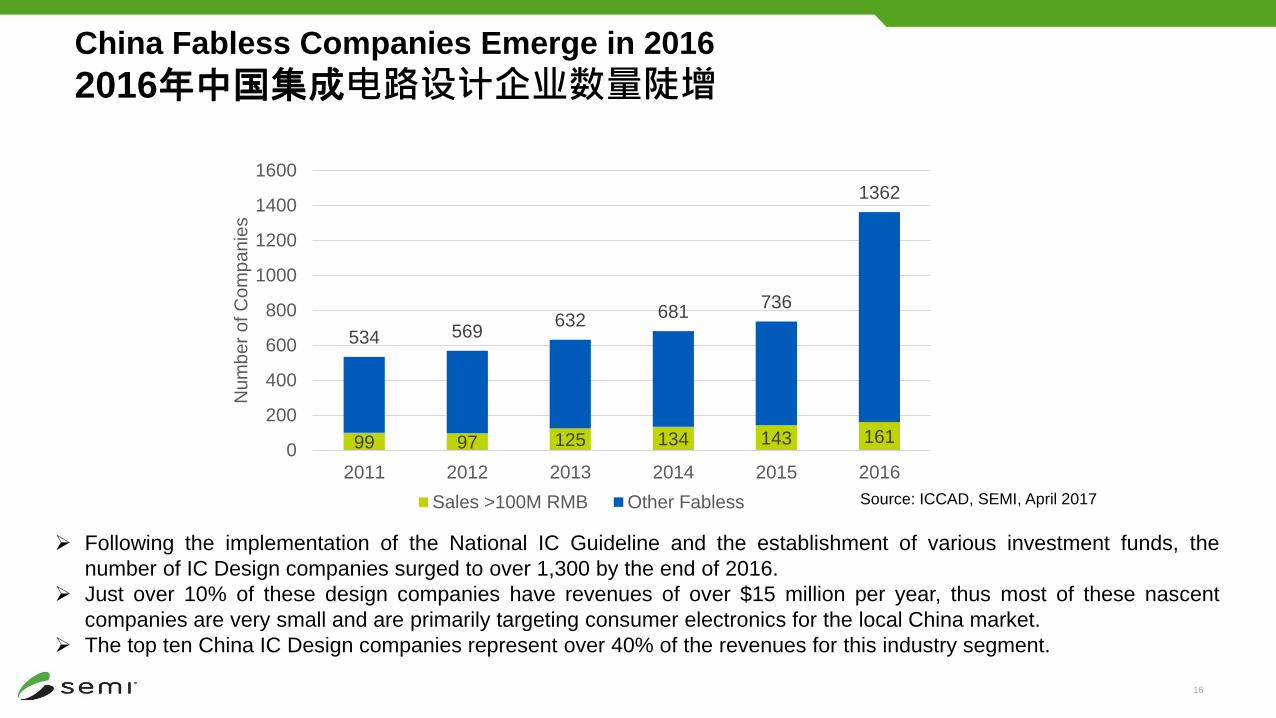

China Fabless Companies Emerge in 2016

2016年中国集成电路设计企业数量陡增

Source: ICCAD, SEMI, April 2017

Following the implementation of the National IC Guideline and the establishment of various investment funds, the

number of IC Design companies surged to over 1,300 by the end of 2016.

Just over 10% of these design companies have revenues of over $15 million per year, thus most of these nascent

companies are very small and are primarily targeting consumer electronics for the local China market.

The top ten China IC Design companies represent over 40% of the revenues for this industry segment.

17

18

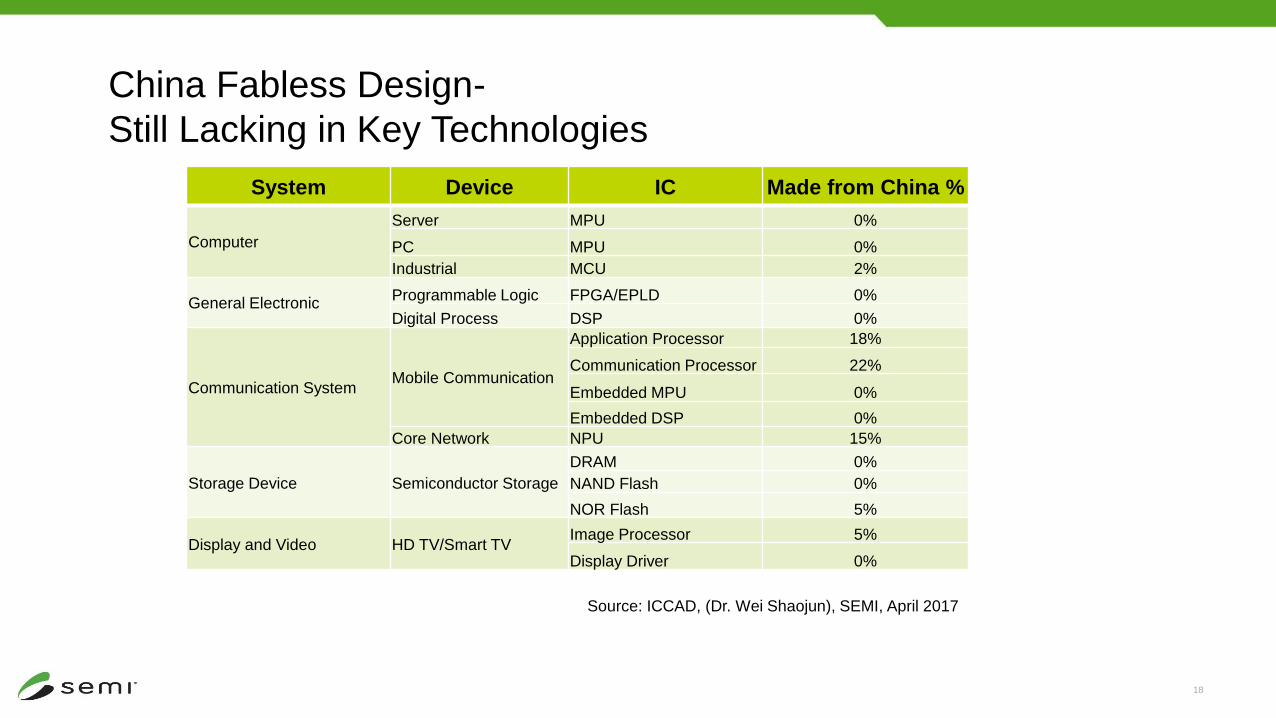

China Fabless Design-

Still Lacking in Key Technologies

System Device IC Made from China %

Computer

Server MPU 0%

PC MPU 0%

Industrial MCU 2%

General ElectronicProgrammable Logic FPGA/EPLD 0%

Digital Process DSP 0%

Communication SystemMobile Communication

Application Processor 18%

Communication Processor 22%

Embedded MPU 0%

Embedded DSP 0%

Core Network NPU 15%

Storage Device Semiconductor Storage

DRAM 0%

NAND Flash 0%

NOR Flash 5%

Display and Video HD TV/Smart TVImage Processor 5%

Display Driver 0%

Source: ICCAD, (Dr. Wei Shaojun), SEMI, April 2017

0

500.000

1.000.000

1.500.000

2.000.000

2.500.000

3.000.000

3.500.000

4.000.000

4.500.000

Americas China Europe &Mideast

Japan Korea SE Asia Taiwan

<= 150mm 200mm 300mm

27%

19

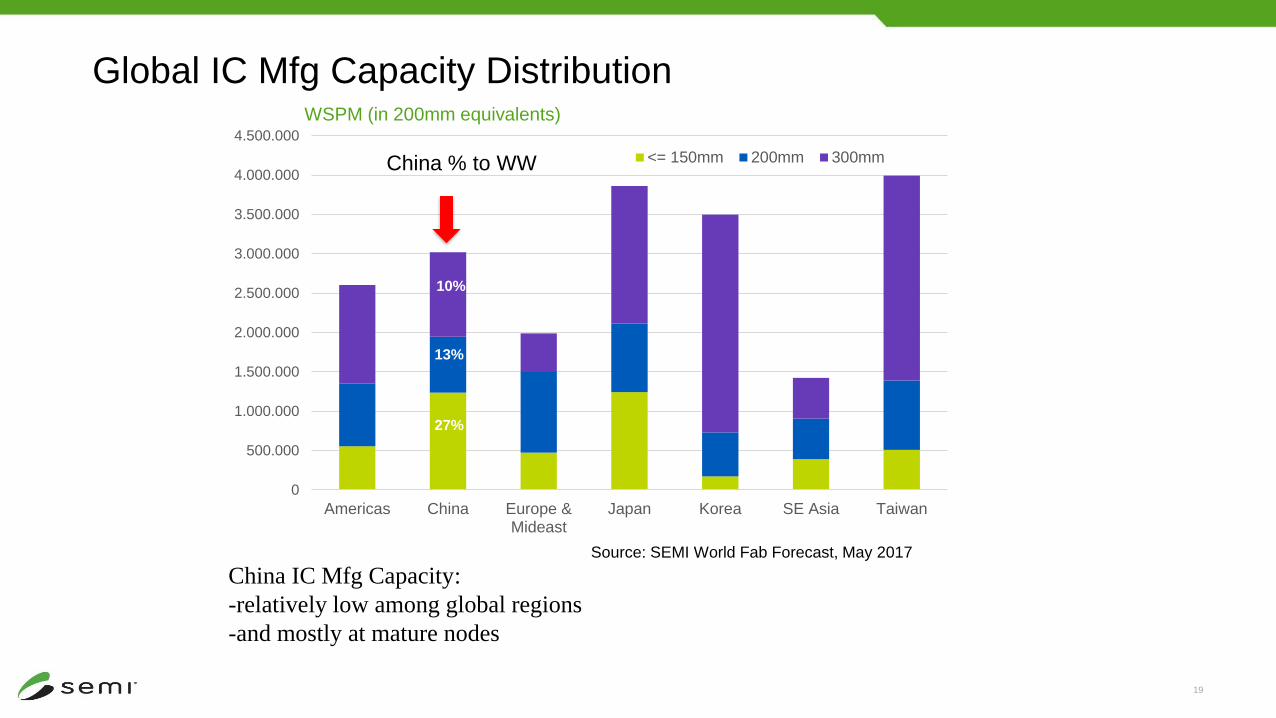

Global IC Mfg Capacity Distribution

Source: SEMI World Fab Forecast, May 2017

China IC Mfg Capacity:

-relatively low among global regions

-and mostly at mature nodes

WSPM (in 200mm equivalents)

China % to WW

10%

13%

New Fab Projects - China Leads the Way

• Since 2015, new fab projects starting production in China have outpaced other semiconductor regions.

• Of the 24 new fab projects underway, or expected to begin construction, 19 are owned by China companies.

The remainder are from investments by overseas companies.

50

21

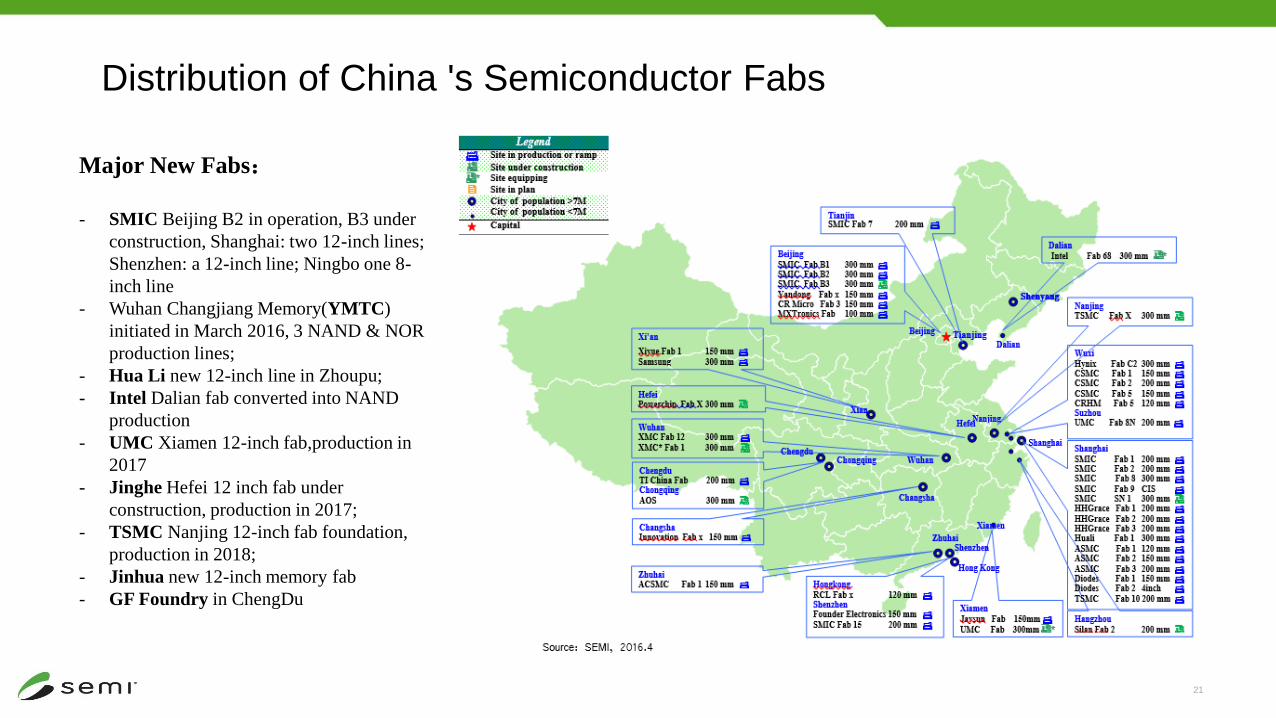

Distribution of China 's Semiconductor Fabs

Major New Fabs:

- SMIC Beijing B2 in operation, B3 under

construction, Shanghai: two 12-inch lines;

Shenzhen: a 12-inch line; Ningbo one 8-

inch line

- Wuhan Changjiang Memory(YMTC)

initiated in March 2016, 3 NAND & NOR

production lines;

- Hua Li new 12-inch line in Zhoupu;

- Intel Dalian fab converted into NAND

production

- UMC Xiamen 12-inch fab,production in

2017

- Jinghe Hefei 12 inch fab under

construction, production in 2017;

- TSMC Nanjing 12-inch fab foundation,

production in 2018;

- Jinhua new 12-inch memory fab

- GF Foundry in ChengDu

22

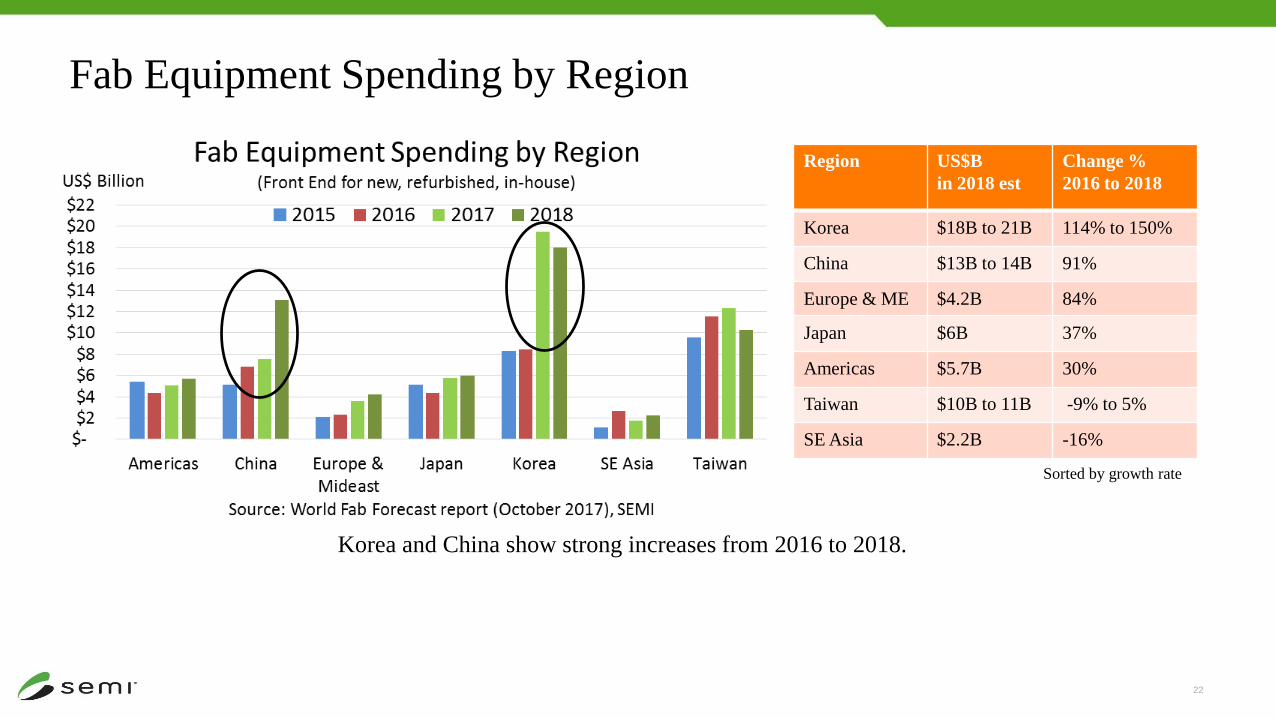

Fab Equipment Spending by Region

Region US$B

in 2018 est

Change %

2016 to 2018

Korea $18B to 21B 114% to 150%

China $13B to 14B 91%

Europe & ME $4.2B 84%

Japan $6B 37%

Americas $5.7B 30%

Taiwan $10B to 11B -9% to 5%

SE Asia $2.2B -16%

Korea and China show strong increases from 2016 to 2018.

Sorted by growth rate

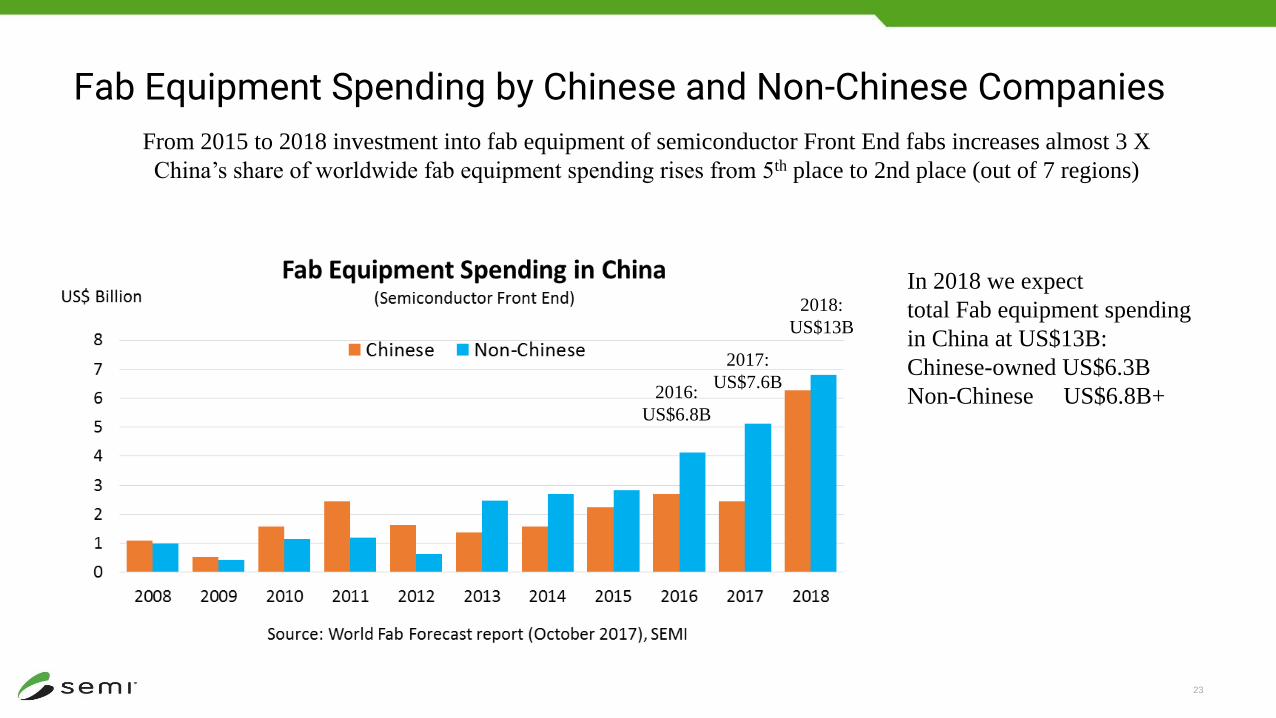

Fab Equipment Spending by Chinese and Non-Chinese Companies

23

From 2015 to 2018 investment into fab equipment of semiconductor Front End fabs increases almost 3 X

China’s share of worldwide fab equipment spending rises from 5th place to 2nd place (out of 7 regions)

In 2018 we expect

total Fab equipment spending

in China at US$13B:

Chinese-owned US$6.3B

Non-Chinese US$6.8B+2016:

US$6.8B

2017:

US$7.6B

2018:

US$13B

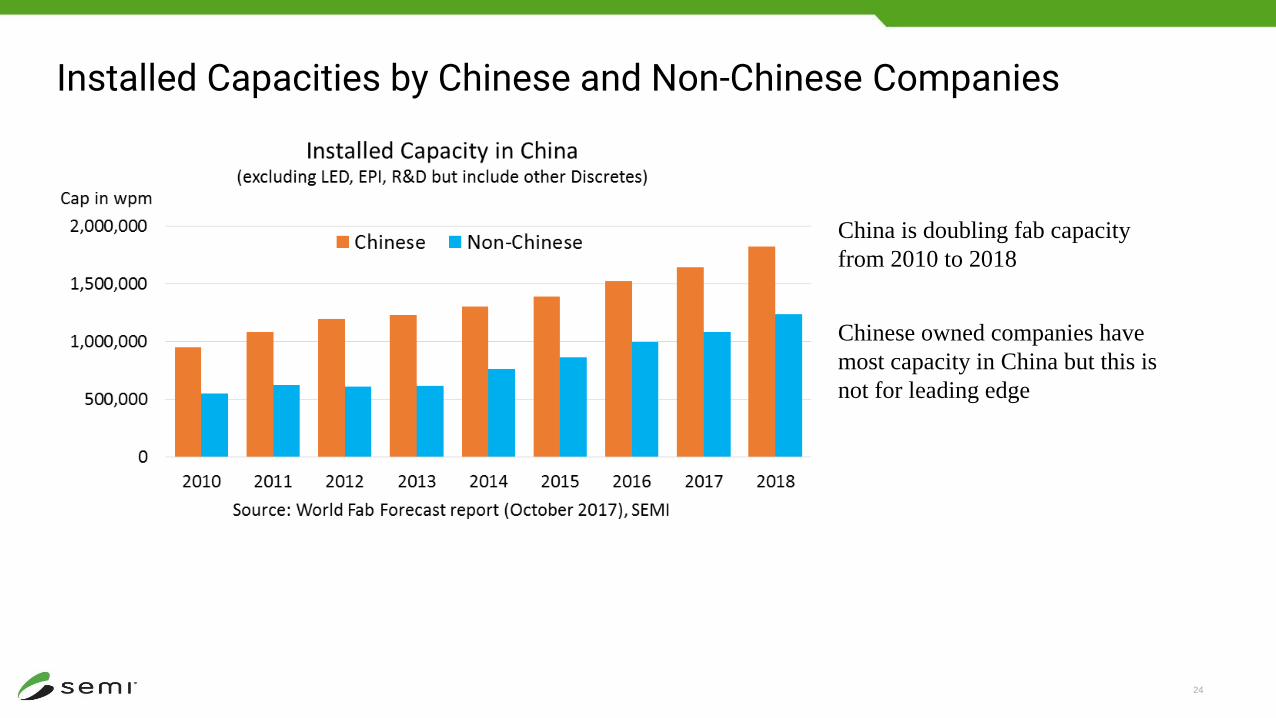

Installed Capacities by Chinese and Non-Chinese Companies

24

Chinese owned companies have

most capacity in China but this is

not for leading edge

China is doubling fab capacity

from 2010 to 2018

25

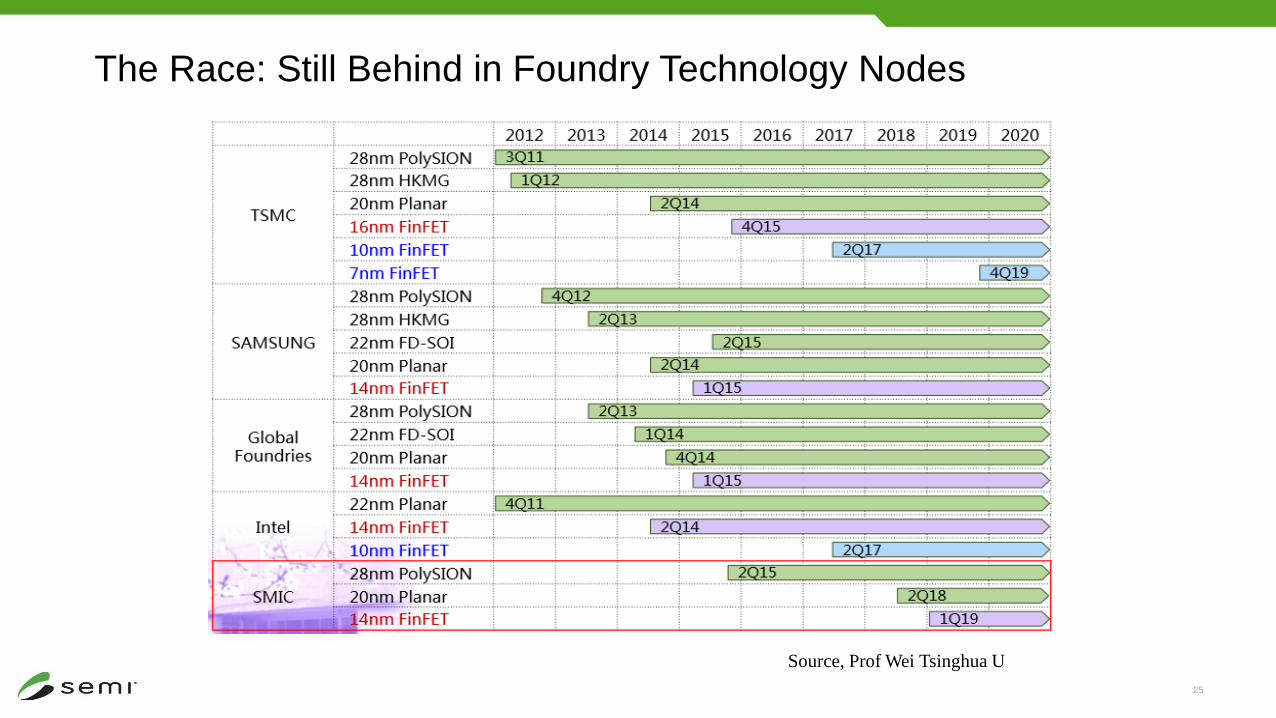

The Race: Still Behind in Foundry Technology Nodes

Source, Prof Wei Tsinghua U

Global Top 10 Packaging & Test Companies

• Three China OSAT companies are ranked in the top 10 global OSAT manufactures.

2016

Rank

2015

RankCompany HQ Location

2015

Revenues ($M)

2016

Revenues ($M)

Percent

Change

1 1 ASE 日月光 台湾地区 4748 4861 2%

2 2 Amkor 安靠 北美 2885 3902 35%

3 3 SPIL 矽品 台湾地区 2607 2638 1%

4 4 JCET 长电科技* 中国 1655 2280 38%

5 6 Powertech 力成 台湾地区 1291 1506 17%

6 5 STATS ChipPAC 星科金鹏* 新加坡 1339 1078 -19%

7 9 Tianshui Huatian 华天科技 中国 597 811 36%

8 13 TFME 通富微电 中国 357 764 114%

9 10 KYEC 京元电子 台湾地区 520 743 43%

10 8 ChipMOS 南茂 台湾地区 606 583 -4%

Total 总和 16605 19166 15%

Source: IC Insights, SEMI, March 2017*JCET acquired STATS ChipPAC (excluding Taiwan site)

65

27

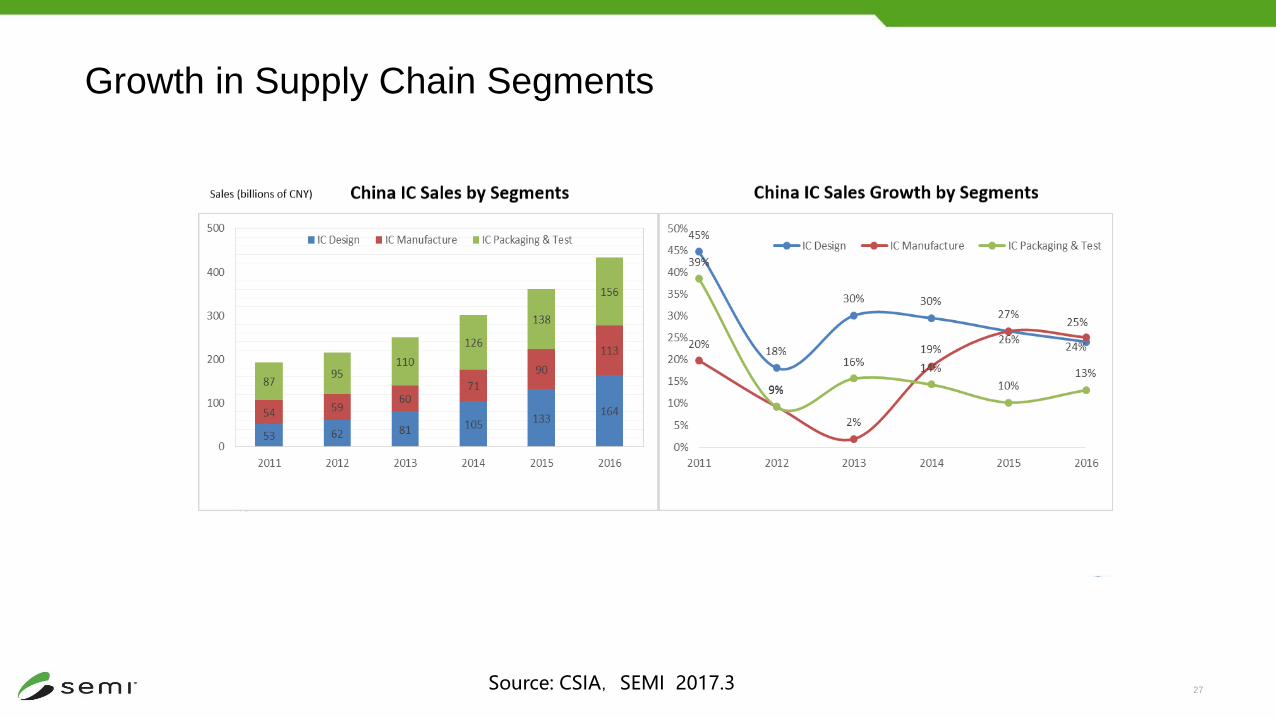

Growth in Supply Chain Segments

Source: CSIA,SEMI 2017.3

$0

$10

$20

$30

$40

$50

$60

2013 2014 2015 2016 2017F 2018F

Europe Japan North America Korea Taiwan China Rest of World

$31.79

$36.53$41.24

$54.33

$37.50

$56.18

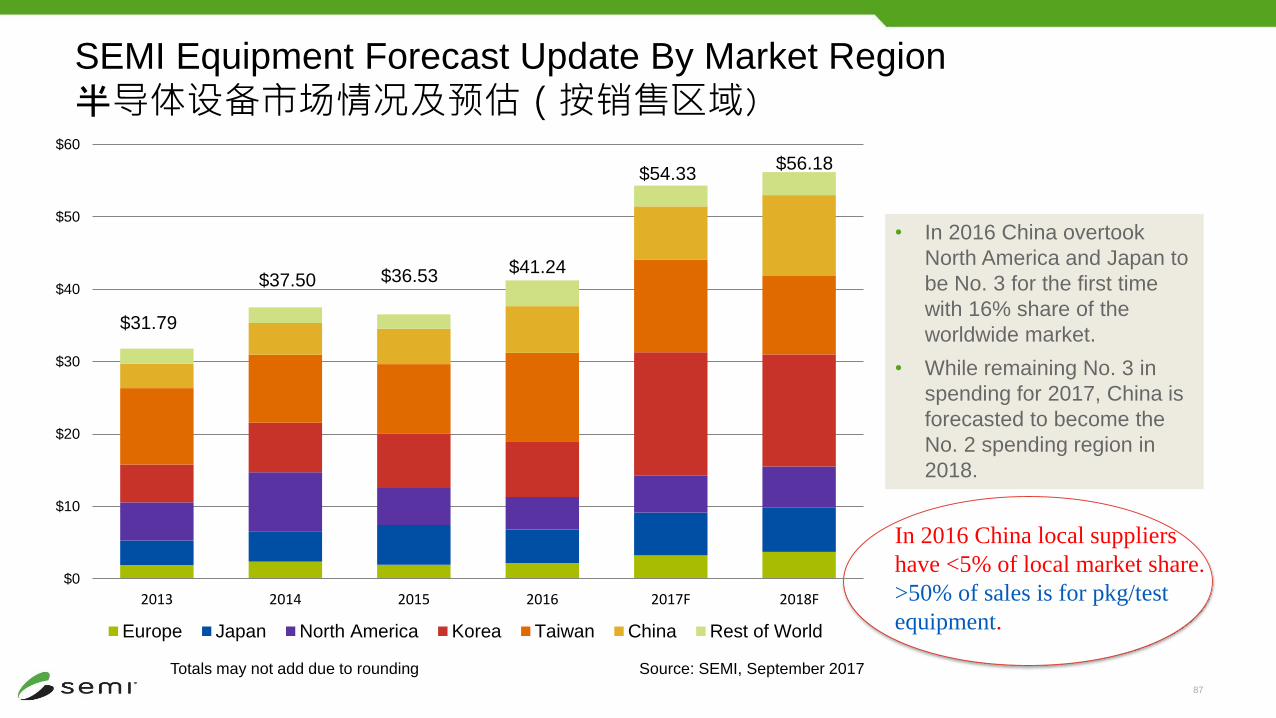

SEMI Equipment Forecast Update By Market Region

半导体设备市场情况及预估(按销售区域)

Source: SEMI, September 2017Totals may not add due to rounding

• In 2016 China overtook

North America and Japan to

be No. 3 for the first time

with 16% share of the

worldwide market.

• While remaining No. 3 in

spending for 2017, China is

forecasted to become the

No. 2 spending region in

2018.

87

In 2016 China local suppliers

have <5% of local market share.

>50% of sales is for pkg/test

equipment.

29

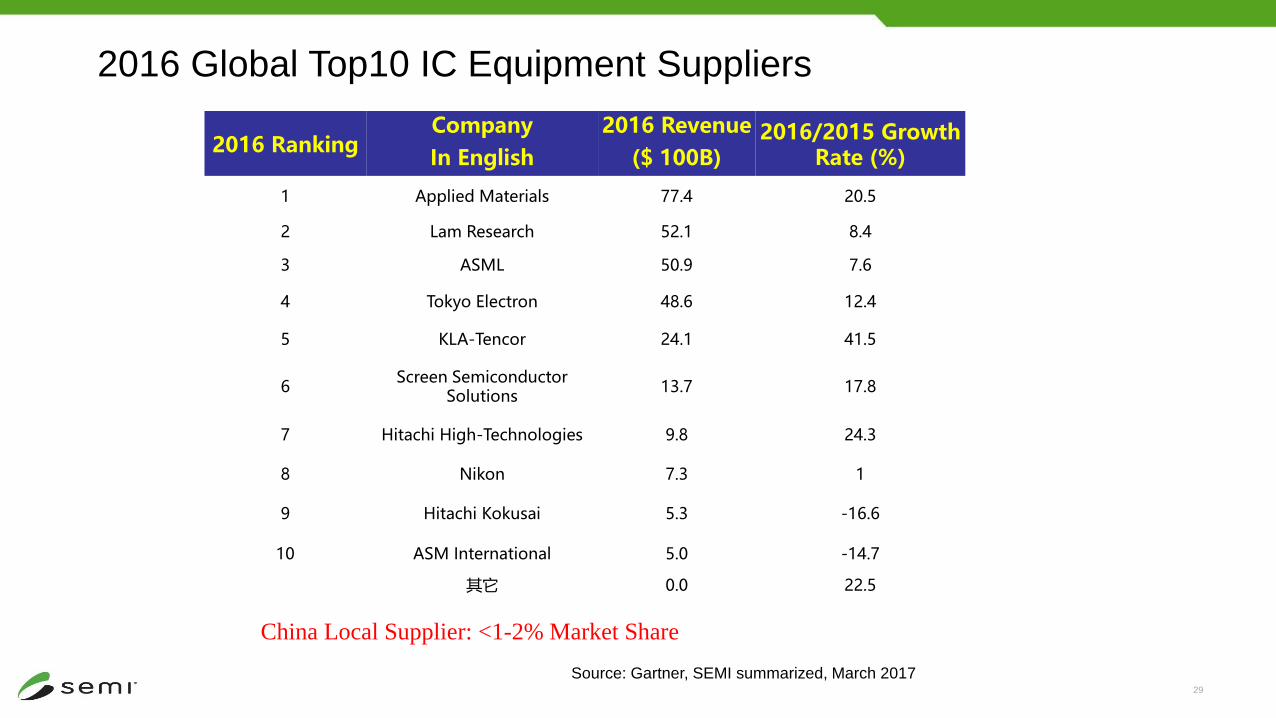

2016 Global Top10 IC Equipment Suppliers

China Local Supplier: <1-2% Market Share

2016 RankingCompany 2016 Revenue 2016/2015 Growth

Rate (%)In English ($ 100B)

1 Applied Materials 77.4 20.5

2 Lam Research 52.1 8.4

3 ASML 50.9 7.6

4 Tokyo Electron 48.6 12.4

5 KLA-Tencor 24.1 41.5

6Screen Semiconductor

Solutions13.7 17.8

7 Hitachi High-Technologies 9.8 24.3

8 Nikon 7.3 1

9 Hitachi Kokusai 5.3 -16.6

10 ASM International 5.0 -14.7

其它 0.0 22.5

Source: Gartner, SEMI summarized, March 2017

72

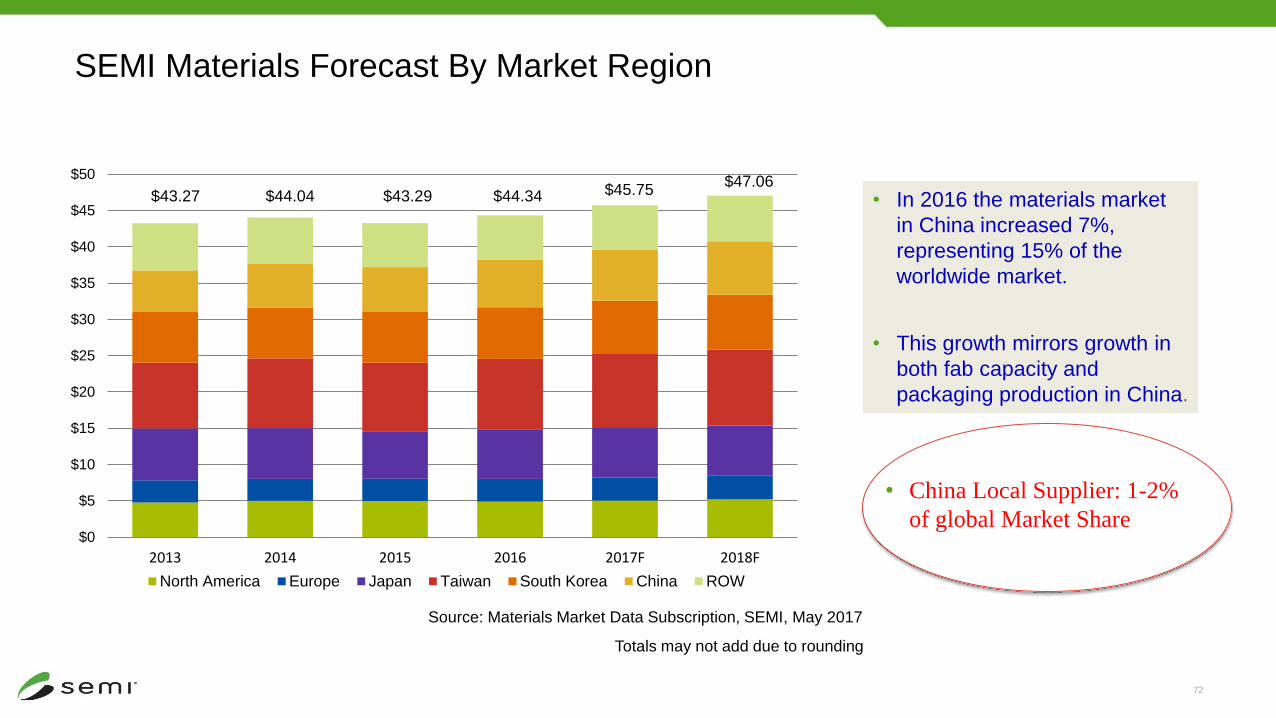

SEMI Materials Forecast By Market Region

Source: Materials Market Data Subscription, SEMI, May 2017

Totals may not add due to rounding

• In 2016 the materials market

in China increased 7%,

representing 15% of the

worldwide market.

• This growth mirrors growth in

both fab capacity and

packaging production in China.

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

$50

2013 2014 2015 2016 2017F 2018F

North America Europe Japan Taiwan South Korea China ROW

$43.27 $43.29 $44.34 $45.75$44.04$47.06

• China Local Supplier: 1-2%

of global Market Share

31

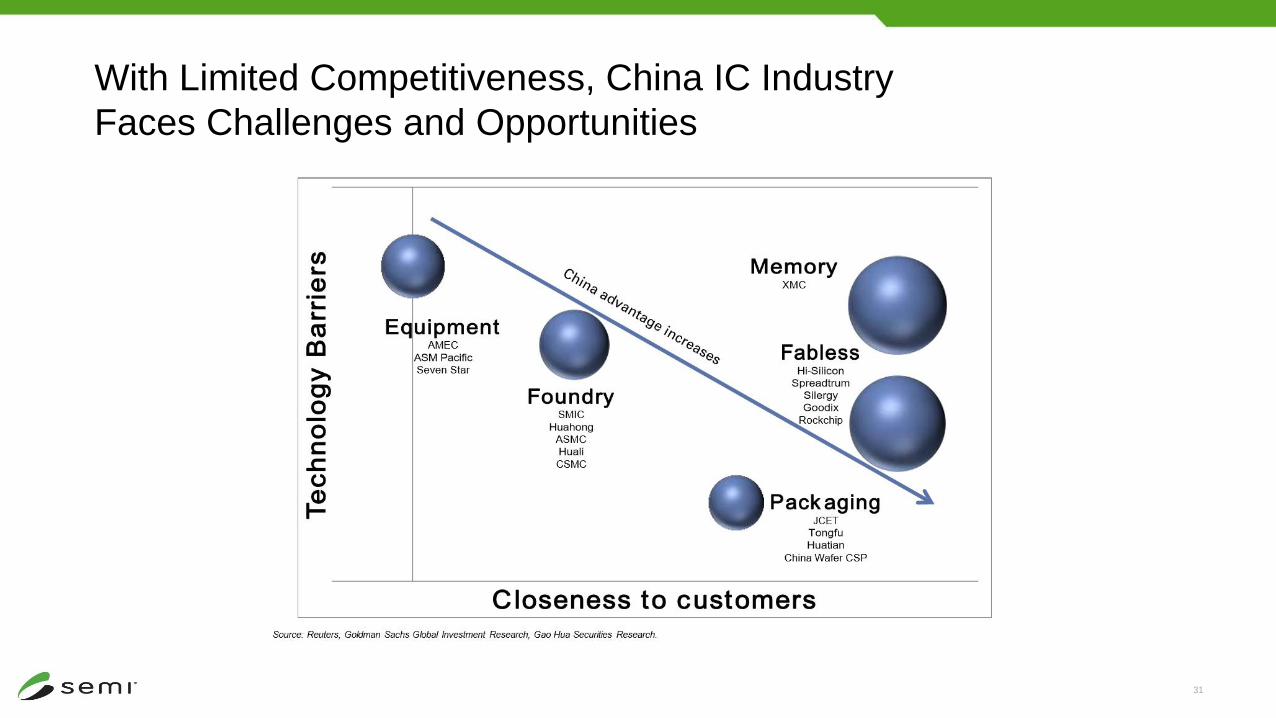

With Limited Competitiveness, China IC Industry

Faces Challenges and Opportunities

32

What’s Ahead? China Semiconductor Industry

• The largest electronics product market

• Fast Growing Application Market Opportunities

– Mobile Computing + 5G (Huawei)

– AI, AR/VR, IoT, Cloud Computing, Big Data (BAT)(WeChat)

– Smart Mfg 2025, Industry 4.0, Industrial Iot

– New Energy, Smart (electric) Automotive

– Smart City, Smart Grid, Smart Medical

• Long term perspective: China’s Transition from Low-cost manufacturing to solution provider, then to innovation.

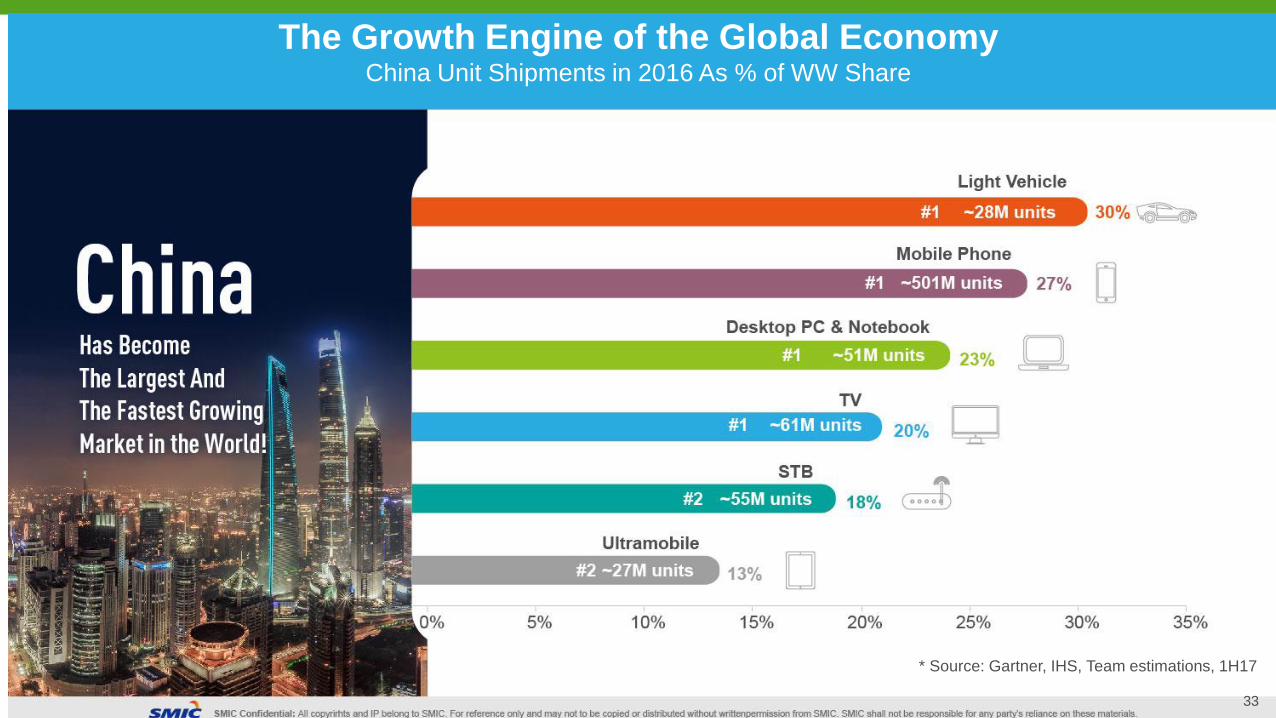

The Growth Engine of the Global EconomyChina Unit Shipments in 2016 As % of WW Share

* Source: Gartner, IHS, Team estimations, 1H17

33

34

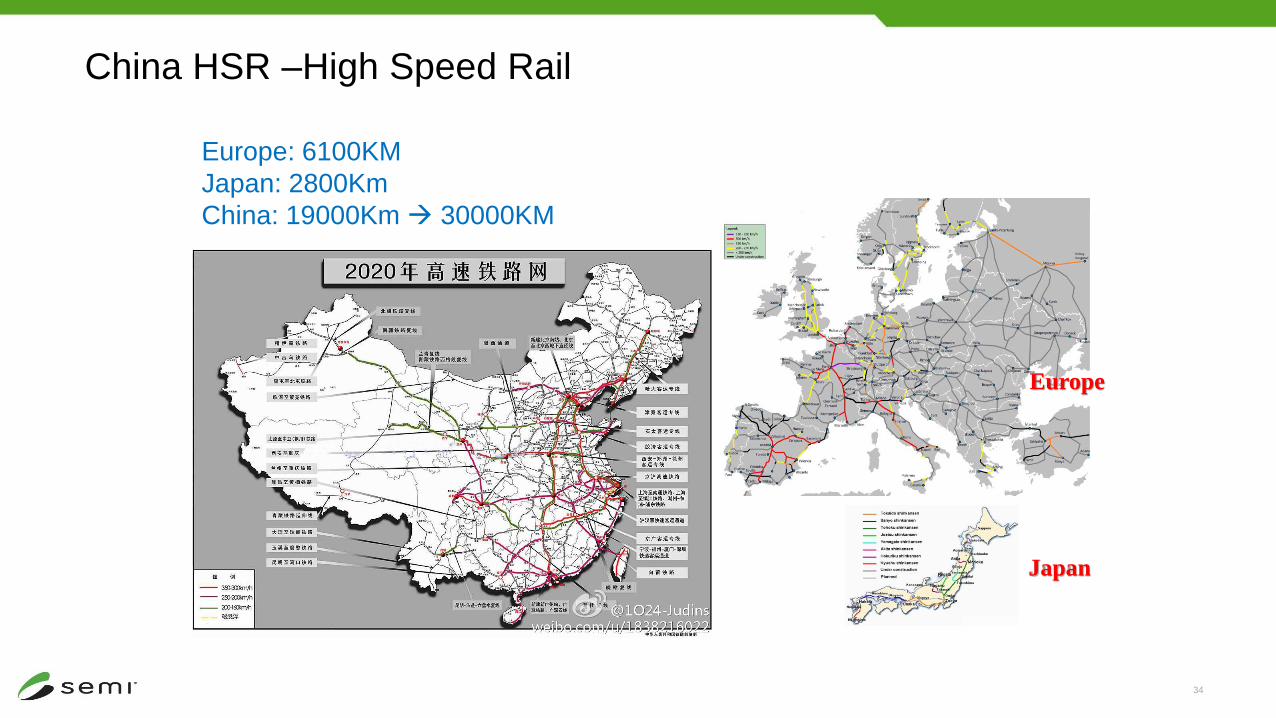

China HSR –High Speed Rail

Japan

Europe

Europe: 6100KM

Japan: 2800Km

China: 19000Km 30000KM

35

Completed

Construction

Planned, 2020

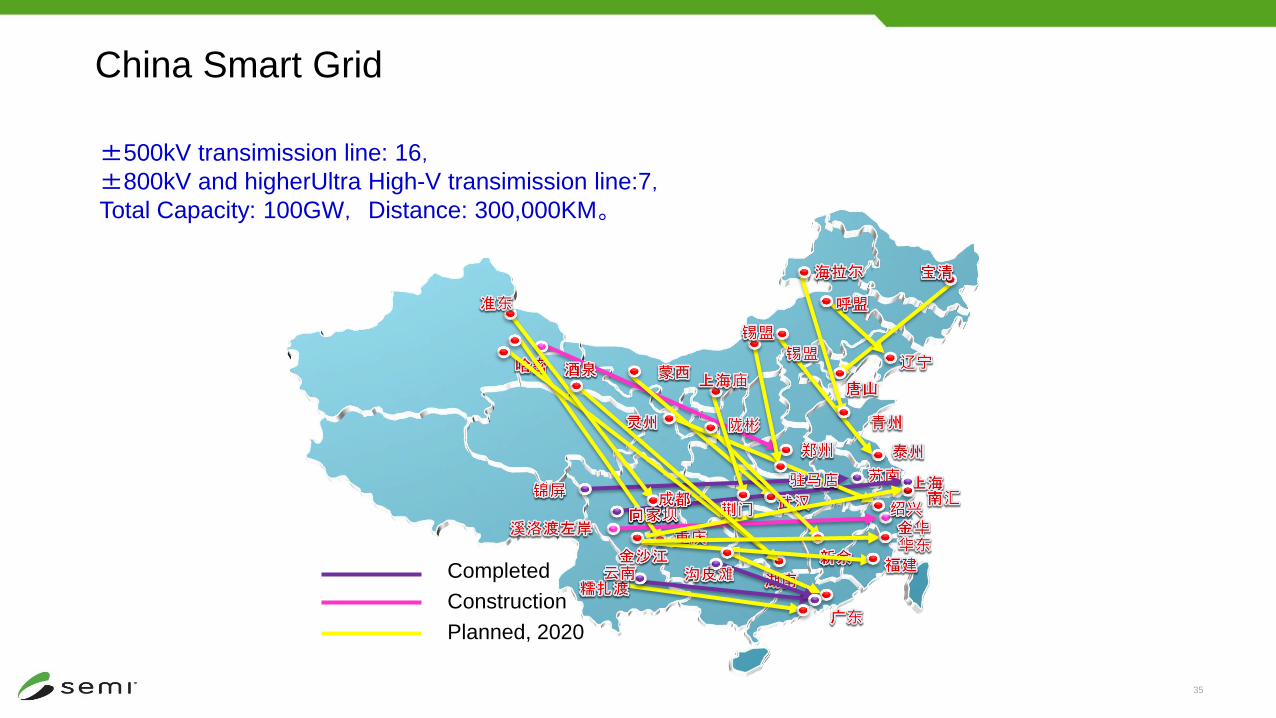

±500kV transimission line: 16,±800kV and higherUltra High-V transimission line:7,Total Capacity: 100GW,Distance: 300,000KM。

China Smart Grid

36

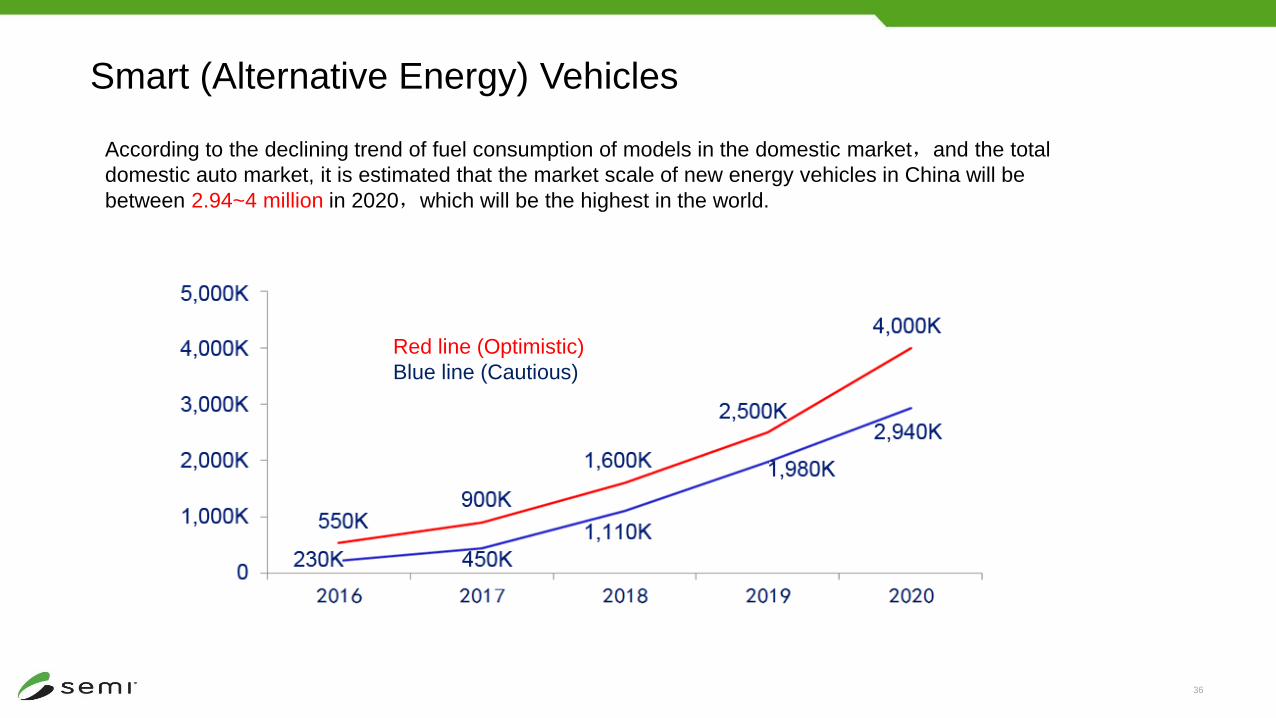

Smart (Alternative Energy) Vehicles

According to the declining trend of fuel consumption of models in the domestic market,and the total

domestic auto market, it is estimated that the market scale of new energy vehicles in China will be

between 2.94~4 million in 2020,which will be the highest in the world.

Red line (Optimistic)

Blue line (Cautious)

37

Summary

• Why?

– Market Driven

– Concerns of Trade Deficit and National Security

• China National IC Development Guideline and Big Fund

– Necessary, Just Timely, or Maybe too late?

• IC Industry Status and Challenges. Good progress….but

– Design/Fabless: Mostly in Low-Margin Consumer Segments

– Mfg: 2-3 Generations Behind. Over capacity? Sustainability?

– Assembly/Test: Improving competitiveness thru R&D and M&A

– Equipment/Material: Dominated by US/JP/EU.

– Not a “threat” yet. => opportunity

38

Summary

• Looking Forward

– China Market: Opportunities for EU/German players.

– Win-win Collaboration: EU/Germany and China

– China as a Global Ecosystem Partner

– Low-Cost Mfg -> Solution -> Innovation

• 3C’s: competition, collaboration, communications.

• SEMI’s Role: Global Supply Chain Collaboration Platform

– Connect, Collaborate, Innovate, Grow, Prosper

39

Latest Updates: 19th National(Party) Congress, 10/18-24

• New Leadership Team, with President Xi in full control

• New Era - While Continuing China Dream, One-Belt-One-Road Push

• No major change in national policy of high-tech & semiconductor development is expected

• Increasing emphasis on innovation besides fab investment

• Phase II of Sino IC (Big) Fund

SEMICON China 2018

March 14-16, 2018

![SEMI CAST TEMS Overview 2017Mayprod7.semi.org/en/sites/semi.org/files/data17/docs... · 7(06 0hvvdjh 7\shv 0hvvdjh 1dph 0hvvdjh 1dph &rpphqw 7&6 ,qlwldol]dwlrq 7&6 6kxwgrzq 6\vwhp](https://img.pdfslide.us/doc/110x75/5e7c1dbaa1720b189f44faf7/semi-cast-tems-overview-706-0hvvdjh-7shv-0hvvdjh-1dph-0hvvdjh-1dph-rpphqw.jpg)