Embed Size (px)

Citation preview

Chequers: the Single Market by another name

WhytheChequersplanonlycompoundstheUK’stradedisadvantage

EwenStewartandBrianMonteith

WithaforewordbyTheRtHontheLordLilley

2

Chequers:theSingleMarketbyanothernameWhytheChequersPlanonlycompounds

theUK’stradedisadvantage

EwenStewartandBrianMonteith

22October2018

CONTENTS

Foreword 3

ExecutiveSummary 5

Introduction 6

TheproblemwithChequers 6

TheUKhasatradeproblem 8

Towardsfreetrade–amuchbetterideathanChequers 17

WhyChequersshouldbechucked 22

Conclusions 23

3

FOREWORD

byTheRtHonTheLordLilley

ThispapershatterstheillusionthatSingleMarketmembershiphasbeenanirreplaceableboontoBritishmanufacturing.ThatillusionliesbehindtheChequersplantokeeptheUKsubjecttoSingleMarketruesongoods.

IconfessthatIbearsomeresponsibilityfornurturingthisillusion.AstheTradeandIndustrySecretarywhoimplementedtheoriginalSingleMarketprogrammeIfrequentlylaudeditsputativebenefits.Indeed,theinitialideawassensible.Itinvolvedmutualrecognitionofeachmember’sproductstandardsandremovingthosethatwereanti-competitive.So,companiesneedmakeonlyonerangefortheentireSingleMarketinsteadof28variantstoconformtoeachmemberstate’srules.

ButthatbenefittedAmericanorJapanesemanufacturersexportingtoEuropeasmuchasBritishorGermanfirmsexportingwithinEurope.Europeanconsumersbenefittedthroughlowercosts.European(andcertainlyBritish)firmsgainedlittleadvantage.UKgoodsexportstooriginalSingleMarketcountriesgrewatunder1.0%pabetween1993-2015whereasourexportstocountrieswetradeonWTOtermswithgrewthreetimesasmuchatalmost3%.

Sadly,theSingleMarketchangedfrommutualrecognitiontocentralised,uniformanddetailedregulation.Thishelpedestablishedfirmsconsolidatetheirgriponthemarketbymakingitharderfornew-comerstoenter–andburdenedcompaniesthatonlytradewithintheirhomemarketsinadditiontothosewhichexport.

Thatmayexplainwhycontinentalindustry,whichstartedwithacomparativeadvantageinmanufacturing,capturedsuchastrongshareoftheUKmarketthatisnowtheEU27’sbiggestexportmarket.

Asthepapermakesclear,BritishmanufacturersdorelativelymuchbetterexportingoutsidetheSingleMarket.Butourgreatestcomparativeadvantageliesinservices.OverhalfthevalueaddedthatBritainexportsisinserviceswherewehaveasubstantialsurplusworld-wide.ButagainourperformanceintheSingleMarketisdisappointing.AlowerproportionofUKserviceexportsthanofgoodsgoestoEurope,whereoursurplusismodestcomparedtothatwithAmerica.

BecauseservicesaremuchlessimportanttoothermembersthantotheUK,theEUhasmadelittleprogressinremovingrestrictivepractices,despiteendlesspromises.Oneexceptionisthecreationof‘passports’forfinancialservicesfirms.AsFinancialSecretarytotheTreasuryInegotiatedthefirstDirectivecreatingapassportforbanksenablingthemtooperateviaabranchregulatedbytheirhomecountryregulatorratherthansettinguplocalsubsidiaries.IwasdisappointedafewyearslaterwhenmyDepartmentcouldnotfindanyBritishbankmakinguseofpassporting.However,sincepassportingwasextendedtoawiderrangeoffinancialactivitiestheirusehasbecomeextensive.

Immediatelyfollowingthereferendum,concernsabouttheimpactofthelossofpassportingonfinancialservicesdominatedthemedia.Interestingly,thathassubsided.BanksdidnotprotestwhenthePrimeMinisteracknowledgedthatpassportswouldcease.AndtheyscarcelyutteredawhimperwhenChequersofferedtokeepSingleMarketrulesforproductsbutsoughtnocontinuingaccessforfinancialservices.Cityfirmshavefound‘workarounds’forlossofpassportsand

4

equivalence.Moreimportant,theyandtheBankofEnglandhaveconcludedthattheCitywillbebetteroffmakingitsownrulesthanremaininga‘ruletaker’.

Thatraisesthequestion:wouldwenotbebetteroffbeingfreetomakeourownrulesongoodsaswell,ratherthanbearuletaker?Wewouldnotusesuchfreedomtoscrapruleswholesale.Butmanycouldbestreamlinedandaboveallmadelessofabarriertonewentrants.

ThemostfrighteningaspectofChequersisthatitcommitsBritaintoacceptallfuturerules.YetBritainisparticularlystronginemergingindustrieslikebio-tech,fintech,AIandgeneticengineering–whereruleshaveyettobeset.Itwouldbeanactofself-harmtoallowthoserulestobemadebycountriesthatlacksuchindustriesandoftenapplyextremeversionsoftheprecautionaryprinciplethatthrottlenewdevelopments.

5

EXECUTIVESUMMARY

• ThereisanillusionattheheartofGovernmentthattheSingleMarketissocriticaltoUKtradingandeconomicintereststhattheEUreferendumresultandConservativeandLabourPartymanifestopledgestoleaveitshouldbeover-ruledbytheruseofadoptingacommonrulebookforgoodsandmostfoodsundertheChequersproposal.

• ThispapershowsthatmembershipoftheSingleMarket,orsimilar,viatheChequersproposalofacommonrulebookiseffectivelyremainingintheEUinallbutname.MoreoveritriskspermanentlylockingtheUKintotheworld’sslowestgrowing,mostregulatoryburdensomeandunderperformingbloc.

• TheUKtradeswiththeworld.ShehasasurpluswiththeUS,theworld’smostcompetitivemarket,andabroadlyneutralpositionwiththerestoftheworldexcludingtheEU.IncontrasttheUKhasa£96bndeficitwiththeEU.IsitnotoddthattheUKcantradewellwithcountieswhereithasnotradedealyethasamassivedeficitwhereithasacommonrulebookandsocalledfrictionlesstrade?

• ThispaperdemonstratesthatbeingamemberoftheEU‘commonrulebook’orSingleMarketharmsBritishtradinginterests.TheSingleMarketdoesnotplaytoUKcomparativeadvantageinservicesbutbindsusinongoods,wherewerunalargedeficit.

• ItdemonstratestheclearunderperformanceoftheEurozoneeconomicallywhichhasresultedinUKbusinessvotingwithitsfeetbydivestingoutoftheEUintofastergrowthareas–notablyAsiaandAustralasia.

• Itoutlineswhyvestedinterestssupportregulationasananti-competitivetooltothedetrimentofsmallandmediumsizedcompaniesandtheconsumer.

• WeshowthemajorUKtradingopportunityisincreasinglyinfastgrowingservicesareasthatareoftenhighmargin,moreimmunetodevelopedmarketunder-cuttingandenjoyingstructuralgrowth.

• WedemonstratethatwhiletheChequersproposaliswrappedupinadifferentlanguageusinginnocuoussoundingwords,likethecommonrulebook,thelegaltextisveryclear.ChequersmeanstheUKisboundbycommonrulesthatexclusivelyemanatefromtheEUwiththeUKhavingnosaywhatsoeverintheirframing.Itisnotapartnershipofequals.

• ChequersisthereforetheequivalentofremainingintheSingleMarketinallbutnamewhileabandoninganypretencetotakebackcontrolofresettinganyregulations–thusbreakingthespiritofthereferendumresultandthemanifestopledgesofbothConservativeandLabourparties.

• TheEUhasalreadyofferedGreatBritainasimilardealtoCanada.Weshouldbiteitshandoff.

• ThisdealmustbeforthewholeUKbyincludingNorthernIreland.Therequirementofafrictionlessborderisanotherrouse.NorthernIrelandalreadyhasaborderincurrency,tax,VAT,certainagriculturalstandards,socialprovision,pensionsandthelike.CanadaPlusoffersanearfrictionlessopportunitythatisawin-winforbothparties.

6

INTRODUCTION

ItisaclichébutBritainisatradingnation.LastyeartheUKexported£615bnofgoodsandservicestotheworld.TradeisthelifebloodofthenationandthehistoricUKreferendumvotetoleavetheEuropeanUnionofJune2016providesthefirstopportunity,sincetheUKjoinedtheCommonMarketin1973,tooperateanindependenttradepolicydesignedtomaximiseBritishopportunities.Toputitanotherway,thisisalikelyonce-in-a-lifetimeopportunitytogetitright.

BREXITprovidesauniqueopportunitytore-bootUKtradeandtheUK’sopportunitiesforfutureprosperitybyre-takingcontroloftradepolicy.Whatwedowiththosetoolswillbeamajordeterminantofgrowthgoingforward.Brexitisnotapanaceainitself.Itwillbeasuccessifwecanadopttherightmicro-andmacro-economicpoliciesandtradingrelationships.Historywilljudgeitafailureifwedonot.

Thispaperisdesigned,usingofficialdataprovidedbytheONSPinkBookontradeandEuroStat,toprovidearoutemaptosecuringtherighttradedealforBritainandindeedtheEU.

Todothiswehighlightthecurrenttradingandassetbalancesheetpatterns,thebalanceofUKtradeandcomparativeadvantage,coupledwithananalysisofwheretheopportunitylies.WeexaminethereasonsforthecontinuingandgrowingasymmetryintradingwiththeEUandtherestoftheworldandwedrawconclusionsastowhatagoodtradedealmightlooklike.

THEPROBLEMWITHCHEQUERS

TheRemaincamp,includingourthenPrimeMinster,DavidCameron,wasveryclear.AvotetoleavewouldmeanleavingtheentireEUstructurethattheysaidincludedtheSingleMarketandCustomsUnion.Thisinitselfwasanobviousconsequence,astoremainintheSingleMarketwouldnotreallybetoleaveatall,asthevastmajorityofEUregulationsareSingleMarketrelated.ToremaininacommonrulebookwouldinflictontheUKascenariowhereshetookvirtuallyalltheruleswithoutasay,hardlywhatwaspromisedandsurelythecompleteantithesisof“takingbackcontrol”.

ItisthusdisingenuousoftheremainleadershipnowtoclaimthatvotersdidnotknowwhattheywerevotingforanditwasnotclearthatBrexitwouldmeanleavingtheCustomsUnion.ThereisaverylargebodyofwrittenandverbalevidencefromtheremaincampaignandindeedsubsequentmanifestocommitmentsfromboththeLabourandConservativepartiesthattheUKwouldleavetheEUSingleMarketandCustomsUnion.SadlytheChequersproposaldoesnotremotelymeetthereferendumormanifestocommitmentsgivenbyeitherthecurrentPrimeMinister,orLeaderoftheOpposition.

TheChequersproposalmaybewrappedupinadifferentlanguageusinginnocuoussoundingwords,likethecommonrulebook,butthelegaltextisveryclear.ChequersmeanstheUKisboundbycommonrulesthatexclusivelyemanateformtheEUwiththeUKhavingnosaywhatsoeverintheirframing.Itisnotapartnershipofequals.

Shoulditbeagreed,Parliamentwouldeffectivelybeforcedtoaccept,applyandobeywhatevertheEUproposedanddefactoboundwithanyrulingsbytheEuropeanCourtsofJustice(ECJ).WhilethecurrentUKinfluenceinagreeingregulationisminimal(theUKhasan8.4%shareofthevoteintheCouncilofMinisters)Chequersreducesthattozero.ThusChequersiseffectivelyremaininginthe

7

SingleMarketinallbutnamewhileabandoninganypretencetotakebackcontrolofanysettingofregulations–thusbreakingthespirtofthereferendumresultandthesolemnelectionmanifestopromises.

Moreover,underChequersthereisnoabilityfortheUKtorepealanyexistingEUlawinthefieldsoftheSingleMarket,agricultural,environment,climatechange,socialwelfare,employmentandconsumerprotection.

TheproposalmakescleartheUKwouldnotbeallowedtoreduceregulationbelowtheEUlevelasaminimum,thusnegatingoneoftheprinciplebenefitsofBrexit–theabilitytofameourownlawsandreduceburdensomeandanti-competitiveregulation.GiventhattheseareasaccountforvirtuallyallEUstatutelawitishardtoseehowChequersinanywaymeansleavingtheEUinanymeaningfulwayatall.

TheproposaldoessayParliamentcouldchosenottoincorporatenewEUlawintoUKlaw,butthattheUK‘recognisesthiswouldhaveconsequences.’GiventheUKwouldhavepromisedtomaintainacommonrulebook,andaso-calledfrictionlessborderwiththeIrishRepublic,itisveryhardtoenvisageanyscenariowheretheUKcouldlegallytakesuchanactionaswebelievetheauthorsoftheproposalwellknow.

TheoreticallytheUKcouldsigntradeagreementswiththirdpartiesbutwhowouldwishtodothatwithacountryboundbytherulesofBrussel’s?Negotiationswouldhavelittlemeaningandthereisalmostnoscopetodeliver.

IfChequersformsthebasisforanagreementwiththeEUwebelievetheUK’sbodyoflawwillbebarelyonejotdifferentfromtheEUacquisinfiveyears’time.Moreover,asitisproposedChequerswillbeenshrinedininternationallaw,futureParliamentswillhavevirtuallynorealisticlegalabilitytorevisitthis.

WhatmakestheChequersproposalworseisthatitscompromisesaresoneedless.TheUK’sgovernmentiscaughtintheheadlightsofcontinuingestablishmentcampaigningthatacceptsmembershipoftheSingleMarketissocriticalitmustbepreserveddespitethereferendumandmanifestooutcome.ThispaperwillclearlydemonstratethisisamajorfallacythatneedschallengingasunderthecurrentarrangementstheUK’stradeisbeingmateriallyhamstrung.TheSingleMarketanditscommonrulebookarenotblessingsbutformacurse.

LockedintothefailingEU‘SingleMarket’anditscommonrulebooktheUKhasrunupahugeandgrowingdeficitwiththeEU.Despitethisweareabletorunasurpluswiththerestoftheworld.Thisseemsparadoxical–wearefailingwherewearetiedintotheEUstructure,currentlylegally–andyetsucceedingwiththerestoftheworldwherewearenot.

TheSingleMarketistheworld’sslowestgrowingbloc.Thathasbeenthecaseforagenerationnow.ItishighlyregulatedandhasfailedtoplaytotheUK’sstrategicadvantage–services.ThishascementedaperpetualandgrowingUKtradedeficitwiththeEU.

TheEU’seconomicunderperformanceisduetomanyfactorsbutoneofthemistheextraordinaryburdensomeandbureaucraticregulatoryframeworkEUcompaniesandconsumersareforcedtoadopt.Remaininginthatstructurewillmakeitalmostimpossibletostrikebeneficialtradedealswhilemaintainingsignificantadditionalcoststoconsumers.Moreover,regulatorycreepgoeswellbeyondsmoothingfrictionlesstradeintoareasliketheenvironment,employmentlawandsocialprotection,allareastheUKParliamentwouldbemuchabletolegislateforeffectively.

8

ItiscriticaltounderstandthatonedoesnotneedtobeinsideorpartoftheSingleMarkettotradewithit.ItisanenduringfallacythatSingleMarketmembershipenhancestrade–itdoesnot.Allcountries,withatinynumberofexceptionsofthoseundersanction(likeSyriaorNorthKorea)havefullaccesstotheSingleMarket.

TakeChinaforexample,itisnotamemberbutenjoysgrowingtradewiththeEU,asdoestheUSandAustralia.IndeednoneofthoseexampleshaveanyspecialtradedealswiththeEUbuttradeflowsfreelyunderWorldTradeOrganisation(WTO)guidance.AllofthemcantradefreelywithanyEUnations.Yes,allcountiesneedtocomplywithSingleMarketregulation,justasallcountries,exportingtoChinahavetoacceptitslocalstandards,butitisabsolutelythecasethatthereisopenaccesstotradeforallnationsoutsidetheEU,orEuropeanEconomicArea(EEA)structures.

THEUKHASATRADEPROBLEM

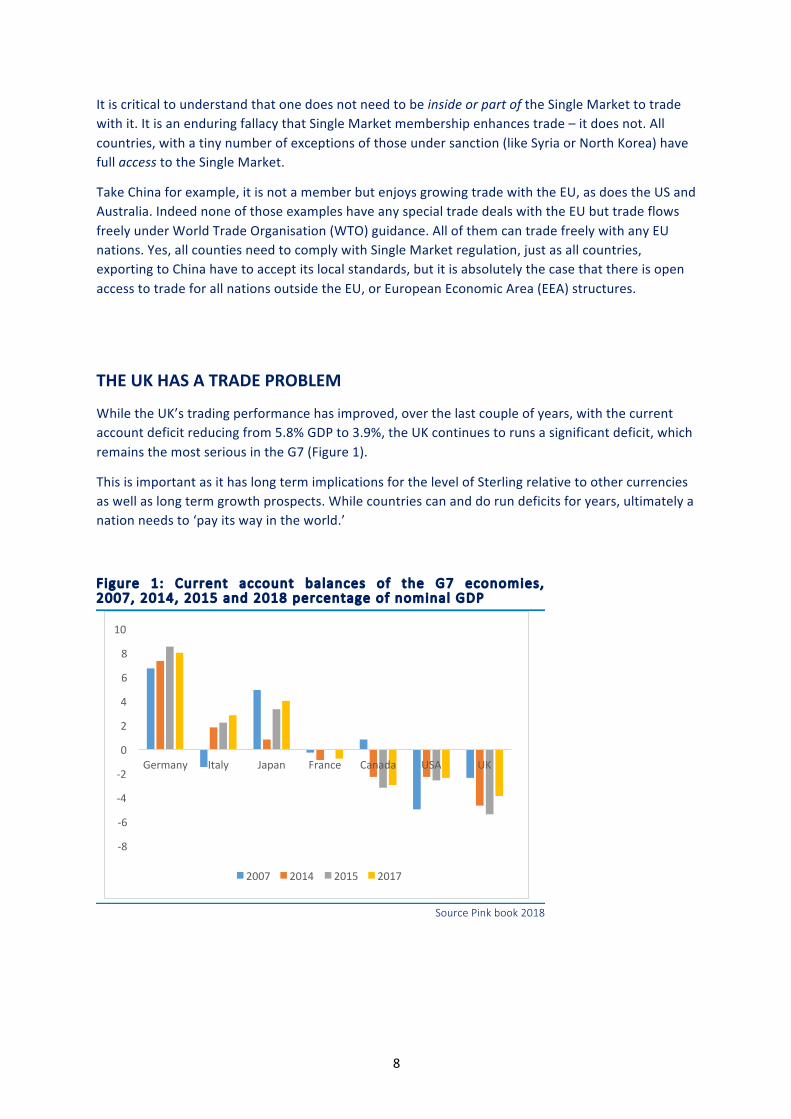

WhiletheUK’stradingperformancehasimproved,overthelastcoupleofyears,withthecurrentaccountdeficitreducingfrom5.8%GDPto3.9%,theUKcontinuestorunsasignificantdeficit,whichremainsthemostseriousintheG7(Figure1).

ThisisimportantasithaslongtermimplicationsforthelevelofSterlingrelativetoothercurrenciesaswellaslongtermgrowthprospects.Whilecountriescananddorundeficitsforyears,ultimatelyanationneedsto‘payitswayintheworld.’

Figure 1: Current account balances of the G7 economies, 2007, 2014, 2015 and 2018 percentage of nominal GDP

Source Pink book 2018

-8

-6

-4

-2

0

2

4

6

8

10

Germany Italy Japan France Canada USA UK

2007 2014 2015 2017

9

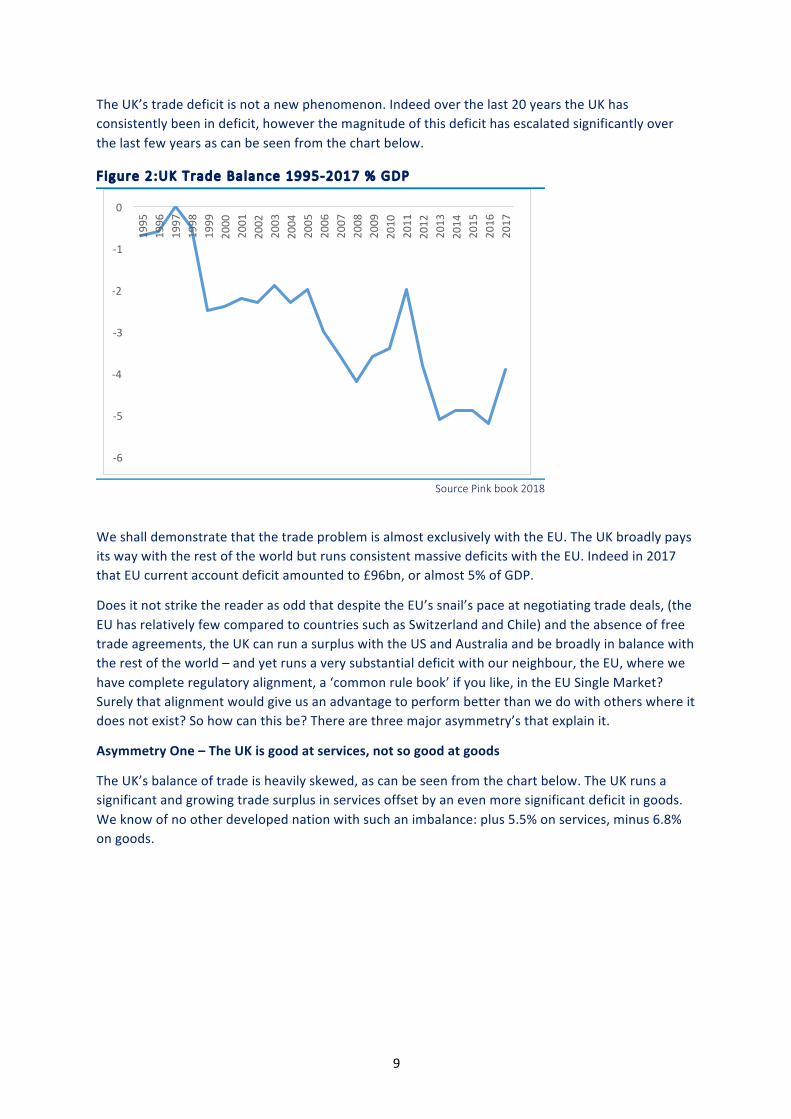

TheUK’stradedeficitisnotanewphenomenon.Indeedoverthelast20yearstheUKhasconsistentlybeenindeficit,howeverthemagnitudeofthisdeficithasescalatedsignificantlyoverthelastfewyearsascanbeseenfromthechartbelow.

Figure 2:UK Trade Balance 1995-2017 % GDP

Source Pink book 2018

WeshalldemonstratethatthetradeproblemisalmostexclusivelywiththeEU.TheUKbroadlypaysitswaywiththerestoftheworldbutrunsconsistentmassivedeficitswiththeEU.Indeedin2017thatEUcurrentaccountdeficitamountedto£96bn,oralmost5%ofGDP.

DoesitnotstrikethereaderasoddthatdespitetheEU’ssnail’spaceatnegotiatingtradedeals,(theEUhasrelativelyfewcomparedtocountriessuchasSwitzerlandandChile)andtheabsenceoffreetradeagreements,theUKcanrunasurpluswiththeUSandAustraliaandbebroadlyinbalancewiththerestoftheworld–andyetrunsaverysubstantialdeficitwithourneighbour,theEU,wherewehavecompleteregulatoryalignment,a‘commonrulebook’ifyoulike,intheEUSingleMarket?Surelythatalignmentwouldgiveusanadvantagetoperformbetterthanwedowithotherswhereitdoesnotexist?Sohowcanthisbe?Therearethreemajorasymmetry’sthatexplainit.

AsymmetryOne–TheUKisgoodatservices,notsogoodatgoods

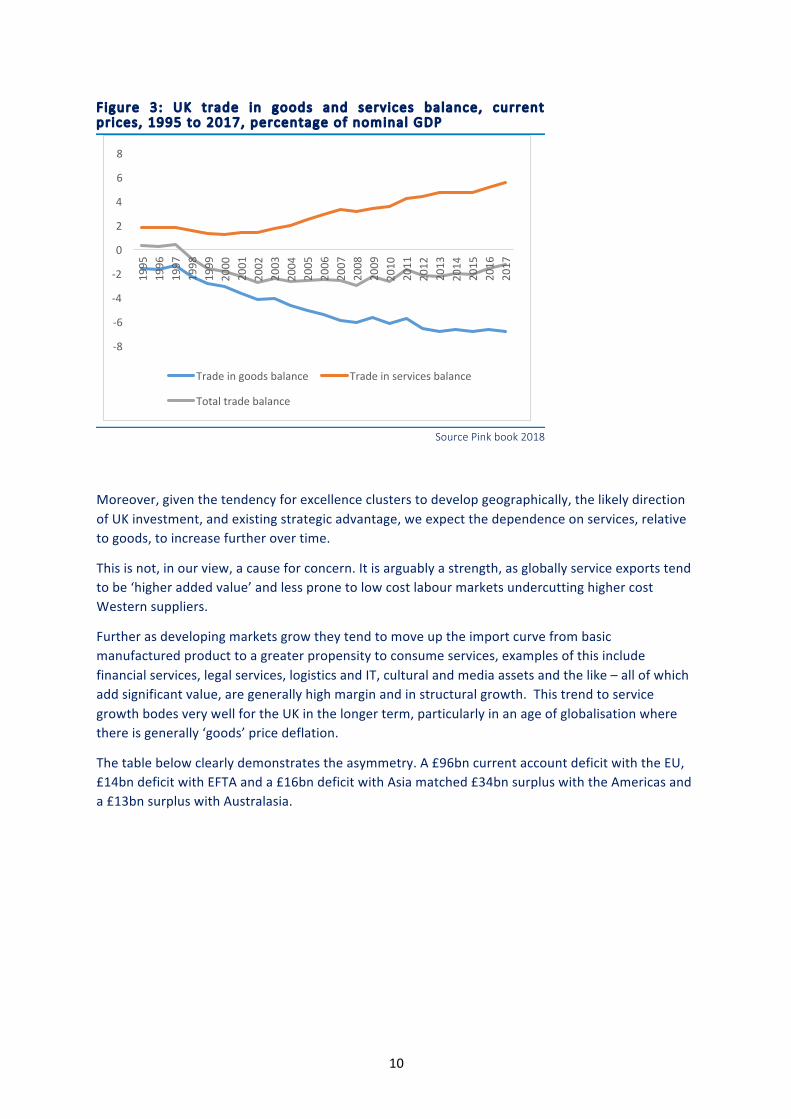

TheUK’sbalanceoftradeisheavilyskewed,ascanbeseenfromthechartbelow.TheUKrunsasignificantandgrowingtradesurplusinservicesoffsetbyanevenmoresignificantdeficitingoods.Weknowofnootherdevelopednationwithsuchanimbalance:plus5.5%onservices,minus6.8%ongoods.

-6

-5

-4

-3

-2

-1

0

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

10

Figure 3: UK trade in goods and services balance, current pr ices, 1995 to 2017, percentage of nominal GDP

Source Pink book 2018

Moreover,giventhetendencyforexcellenceclusterstodevelopgeographically,thelikelydirectionofUKinvestment,andexistingstrategicadvantage,weexpectthedependenceonservices,relativetogoods,toincreasefurtherovertime.

Thisisnot,inourview,acauseforconcern.Itisarguablyastrength,asgloballyserviceexportstendtobe‘higheraddedvalue’andlesspronetolowcostlabourmarketsundercuttinghighercostWesternsuppliers.

Furtherasdevelopingmarketsgrowtheytendtomoveuptheimportcurvefrombasicmanufacturedproducttoagreaterpropensitytoconsumeservices,examplesofthisincludefinancialservices,legalservices,logisticsandIT,culturalandmediaassetsandthelike–allofwhichaddsignificantvalue,aregenerallyhighmarginandinstructuralgrowth.ThistrendtoservicegrowthbodesverywellfortheUKinthelongerterm,particularlyinanageofglobalisationwherethereisgenerally‘goods’pricedeflation.

Thetablebelowclearlydemonstratestheasymmetry.A£96bncurrentaccountdeficitwiththeEU,£14bndeficitwithEFTAanda£16bndeficitwithAsiamatched£34bnsurpluswiththeAmericasanda£13bnsurpluswithAustralasia.

-8

-6

-4

-2

0

2

4

6

81995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

Tradeingoodsbalance Tradeinservicesbalance

Totaltradebalance

11

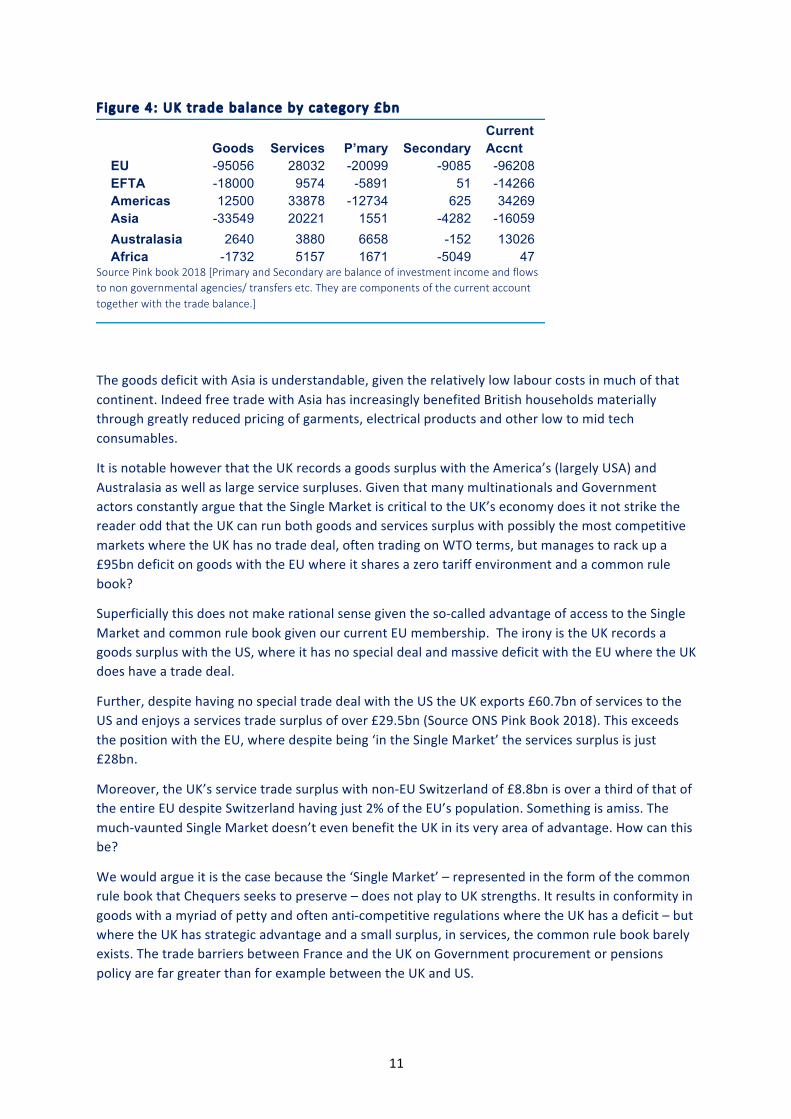

Figure 4: UK trade balance by category £bn

Current

Goods Services P’mary Secondary Accnt

EU -95056 28032 -20099 -9085 -96208 EFTA -18000 9574 -5891 51 -14266 Americas 12500 33878 -12734 625 34269 Asia -33549 20221 1551 -4282 -16059 Australasia 2640 3880 6658 -152 13026 Africa -1732 5157 1671 -5049 47

Source Pink book 2018 [Primary and Secondary are balance of investment income and flows to non governmental agencies/ transfers etc. They are components of the current account together with the trade balance.]

ThegoodsdeficitwithAsiaisunderstandable,giventherelativelylowlabourcostsinmuchofthatcontinent.IndeedfreetradewithAsiahasincreasinglybenefitedBritishhouseholdsmateriallythroughgreatlyreducedpricingofgarments,electricalproductsandotherlowtomidtechconsumables.

ItisnotablehoweverthattheUKrecordsagoodssurpluswiththeAmerica’s(largelyUSA)andAustralasiaaswellaslargeservicesurpluses.GiventhatmanymultinationalsandGovernmentactorsconstantlyarguethattheSingleMarketiscriticaltotheUK’seconomydoesitnotstrikethereaderoddthattheUKcanrunbothgoodsandservicessurpluswithpossiblythemostcompetitivemarketswheretheUKhasnotradedeal,oftentradingonWTOterms,butmanagestorackupa£95bndeficitongoodswiththeEUwhereitsharesazerotariffenvironmentandacommonrulebook?

Superficiallythisdoesnotmakerationalsensegiventheso-calledadvantageofaccesstotheSingleMarketandcommonrulebookgivenourcurrentEUmembership.TheironyistheUKrecordsagoodssurpluswiththeUS,whereithasnospecialdealandmassivedeficitwiththeEUwheretheUKdoeshaveatradedeal.

Further,despitehavingnospecialtradedealwiththeUStheUKexports£60.7bnofservicestotheUSandenjoysaservicestradesurplusofover£29.5bn(SourceONSPinkBook2018).ThisexceedsthepositionwiththeEU,wheredespitebeing‘intheSingleMarket’theservicessurplusisjust£28bn.

Moreover,theUK’sservicetradesurpluswithnon-EUSwitzerlandof£8.8bnisoverathirdofthatoftheentireEUdespiteSwitzerlandhavingjust2%oftheEU’spopulation.Somethingisamiss.Themuch-vauntedSingleMarketdoesn’tevenbenefittheUKinitsveryareaofadvantage.Howcanthisbe?

Wewouldargueitisthecasebecausethe‘SingleMarket’–representedintheformofthecommonrulebookthatChequersseekstopreserve–doesnotplaytoUKstrengths.Itresultsinconformityingoodswithamyriadofpettyandoftenanti-competitiveregulationswheretheUKhasadeficit–butwheretheUKhasstrategicadvantageandasmallsurplus,inservices,thecommonrulebookbarelyexists.ThetradebarriersbetweenFranceandtheUKonGovernmentprocurementorpensionspolicyarefargreaterthanforexamplebetweentheUKandUS.

12

TheevidencesuggeststhattheproblemoftheUK’stradedeficitwiththeEUisacommonrulebookthatweakensourabilitytotradeeffectivelyandwhereitisnon-existentorhardlydevelopedwetrademoreeffectively.ThiswouldexplainwhytheUKcanbemoresuccessfulintradingservicestotheUS,thanwiththeentireEU.TheSingleMarkethasbeendesignedtolargelybenefitthestrategicadvantageofFranceandGermanyinparticular,greatlytothedetrimentoftheUK.Thenumbersarestarkandtheyspeakforthemselves.

AsymmetryTwo–wedowellwiththerestoftheworldandverybadlywiththeEU

Britaincompeteswellwiththeworld.WeareabletorunconsistentsubstantialsurpluseswiththeAmericas(includingarguablytheworld’smostcompetitivemarket–theUS),surpluseswithAustralasiaandabroadbalancewithAfrica.ThedeficitwithAsiaisfairlysmall,at£16bn,whenoneconsidersthelabourcostcompetitiveadvantagetheregionenjoys.

BycomparisontheUK’stradingperformancewiththeEUisextremelyweakwitha£96bndeficitin2015.TheUK’stradepositionhasbeenconstantlynegativewiththeEU.However,since2010thepositionhassharplydeteriorated.ThechartbelowhighlightsUKtradeperformance,since2004,byregion.

Figure 6:UK Current Account trade balance by region £bn

Source Pink Book 2018

ThekeyreasontheChequersproposal,withitsruletakingapproach,willbesodamagingtoUKexports,inthelongtermisitlockstheUKpermanentlyintoanover-regulatedsystemthatfavoursgoodsoverservices.

ThesystemisnotdesignedforUKstrategicadvantage.ItneverhasbeeninthefortyyearsofUKmembershipandgiventhestrengthsandweaknessesofFranceandGermany,thetwoprincipleEUpartners,itneverwillbe.ThusitistrulybizarretotossawayoneofthecriticalopportunitiesfromBrexitbylockingUKtradeintopermanentunderperformanceintheEuropeanarena.

Further,theUK’stradingbalancewiththeEUisconstantlypooracrosstheboard,thenotableexceptionbeingtheRepublicofIrelandwheretheUKpostsconsistentsurpluses.Figure7includes

-140000-120000-100000-80000-60000-40000-20000

0200004000060000

20042005200620072008200920102011201220132014201520162017

EU28 Americas Asia Australasia Africa

13

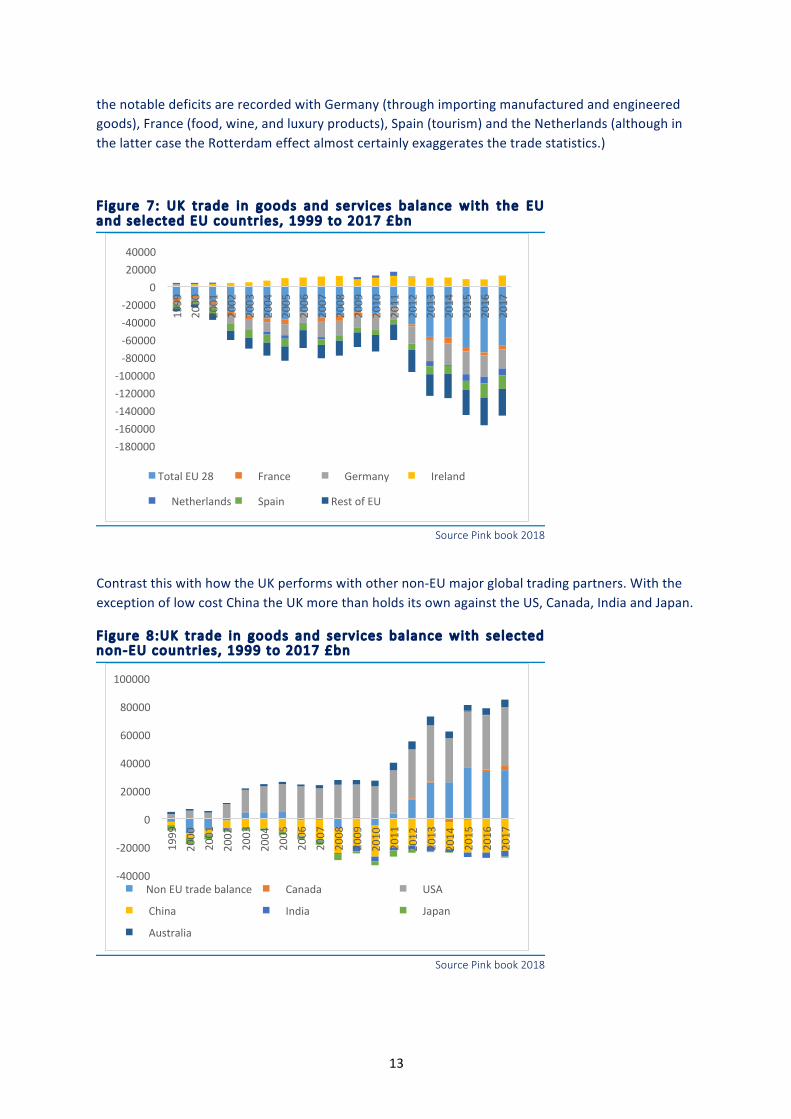

thenotabledeficitsarerecordedwithGermany(throughimportingmanufacturedandengineeredgoods),France(food,wine,andluxuryproducts),Spain(tourism)andtheNetherlands(althoughinthelattercasetheRotterdameffectalmostcertainlyexaggeratesthetradestatistics.)

Figure 7: UK trade in goods and services balance with the EU and selected EU countr ies, 1999 to 2017 £bn

Source Pink book 2018

ContrastthiswithhowtheUKperformswithothernon-EUmajorglobaltradingpartners.WiththeexceptionoflowcostChinatheUKmorethanholdsitsownagainsttheUS,Canada,IndiaandJapan.

Figure 8:UK trade in goods and services balance with selected non-EU countr ies, 1999 to 2017 £bn

Source Pink book 2018

-180000-160000-140000-120000-100000-80000-60000-40000-20000

02000040000

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

TotalEU28 France Germany Ireland

Netherlands Spain RestofEU

-40000

-20000

0

20000

40000

60000

80000

100000

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

NonEUtradebalance Canada USA

China India Japan

Australia

14

ThegreatfallacyoftradeisthatacountryneedstobeinaSingleMarkettotradewithit.TheUK’sbalanceoftradeshowsthisismanifestlynottrue.TheUKdoesnothavetobe“inside”theUStotradewithit,whythenshouldtheUKhavetobe“inside”theEU’sSingleMarkettotradewithit?

Itistruethatonehastocomplywithlocalrulesandregulation–andrightlyso–butthatisnotaproblemforUKcompaniestradinggoodsandserviceswithChina,USandAustralia,threecountrieswheretheEUhasnoformaltradeagreement,sowhyshoulditbeaproblemwiththeEU?

Manypoliticianshavefallenintothetrapofbelievingthatmembershipandproximityareespeciallyimportant.Theyarenotnearlyasimportantasisoftensupposed.Whatgeneratestradeiscomparativeadvantage,innovationanddevisingproductsandservicesthataredesired,notreamsofregulation,conformityandmercantilismthattheEUissospecialisedin.Thisregulatorybehaviouronlyprotectsexistingvestedinterests,whichinthelongtermstiflethetradeandinnovation.

Moreover,theEU,byfirefightingtopreservetheEurozoneincreasinglyhasitselfavestedinterestthatdifferentiatesitfromtheUKandotherEurozonemembers.Thishasbegatfurtherregulation,notablyinthefinancialandmonetaryfielddirectlyharmingUKinterestsandproductivity.

Theironyisthat,despiteanoisylobby,theUKtradesveryeffectivelyglobally–justnotintheEU–provingthattheEUsystemoftradehasnotworkedtoUKadvantage.

AsymmetryThree–theglobalsizeoftheEUisininexorablestructuraldecline

In1991theUSandEuropeanUnioncombinedaccountedfor51.6%ofglobalGDP.China’sweightwasjust1.8%.TodaytheUSandEUaccountfor39.8%globalGDP.Chinanowaccountsfor15.5%oftheworldtotal,slightlysurpassingtheEurozonecombined.

AsisdemonstratedbelowtheUShasbroadlyheldglobalshareaccountingforjustunderaquarterofglobalGDP.TheEurozone,aftermanyyearoflargelyself-inflictedveryweakGDPperformance,hasseenitssharedeclinefrom22.1%10yearsagotojust14.8%today.Currentprojectionsareforthistodeclinetounder10%by2028.

Figure 15: Share of Global GDP %

Source World Bank

0.0%5.0%10.0%15.0%20.0%25.0%30.0%35.0%40.0%

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

China India UnitedKingdom

UnitedStates Russia Euroarea

15

Europeisourneighbourandallyanditwillalwaysremainavitaltrading,culturalandsecuritypartnerbut,thedeclineinitsimportanceoverthelastdecadeisstructural.FortheUK,themajorityofexportgrowthopportunitywillcomefromoutsidetheEU.Thisisanearinevitableconsequenceofdemographicchange,aGDPcatch-upfromalowbasebydevelopingmarketswithemergingdomesticwealth,andconsequentsalesopportunities,technologytransferandEUpolicyfailure,notablythroughthedysfunctionalandasymmetricperformanceoftheEuro.

ThatisnottosaythatEuropeannationscannotprosper,theycaniftheyadoptreasonablyopenfreemarketpolicies,butgrowthwilllargelycomefromelsewhereandUKplchasindeedbeenfollowingthatinexorabletrend.

InourviewmuchofthelacklustreperformanceoftheEurozoneis,however,self-inflicted.WhilethispaperisdesignedtolookatUKtradeopportunitiesandnotthesub-optimalstructureoftheEuro,therealityforthecurrencyistheinherentcontradictionwithintheEurozonefromlockingthemoreuncompetitivenationsintoperpetuallowgrowthasthesafetyvalveofdevaluationisremoved.ThisremainsunresolvedandinourviewwillcontinuetoresultinunacceptablyhighlevelsofunemploymentattheEUperipheryinthemediumterm,andcontinuinglongtermGDPunder-performance.ThisfailuredirectlyimpactsUKtradebyreducingopportunitygiventhelackoflongtermgrowth.

ThetablebelowshowsGDPgrowth,forselectedmajornations,since2009.EurozonecountriesareinredandgenerallyhavelaggedUK,emergingmarketandG7developedmarketgrowth.ThisunderperformancehasledtolacklustreUKexportgrowthtotheEurozone.

Figure 9: Cumulat ive GDP 2009-2017 (2009= 100) Eurozone member in red

Source ONS

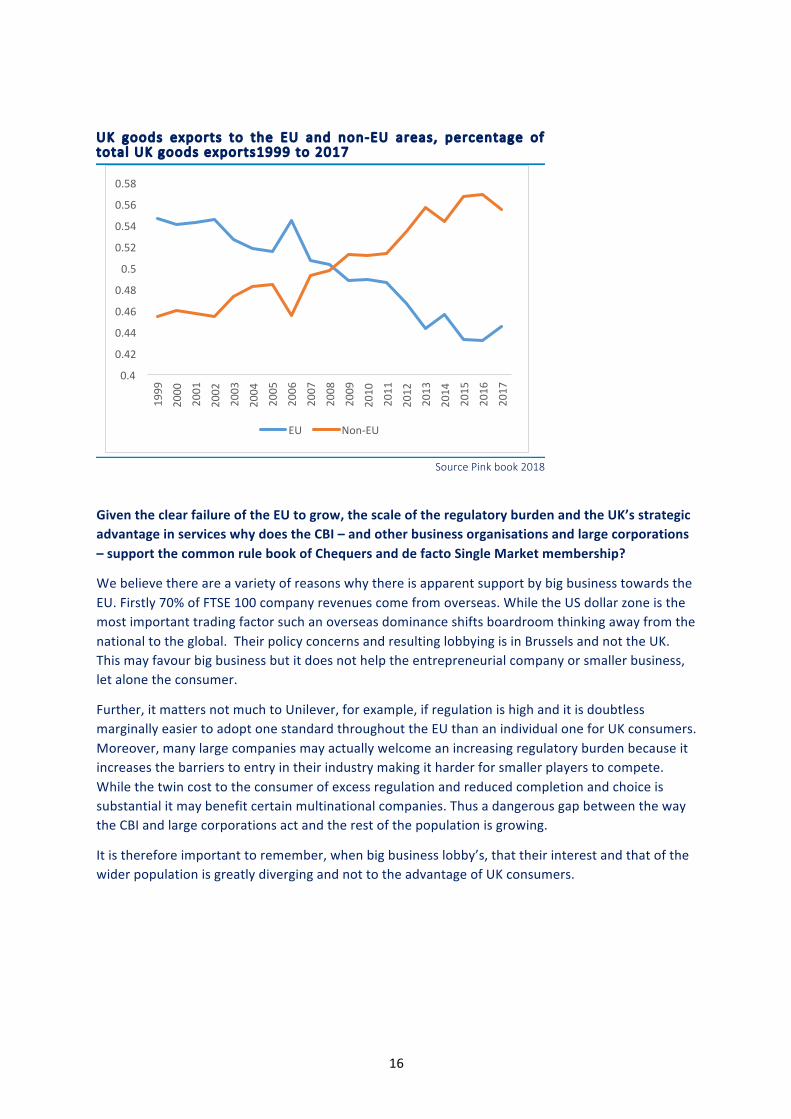

ShiftingglobalweightsandgrowthopportunityinevitablyhashadaprofoundimpactontheUK’stradingpatternsandhasresultedinthelongdriftawayfromtradingwiththeEU,asourprimarypartner,ascanbeseenfromthechartbelow.In1999over55%ofUKtradewaswiththeEU.Todaythatfigurehasfallento43%–ascanbeseenfromthechartbelow.UKplcisvotingwithitsfeet.

0

50

100

150

200

250

300

China

India

Australia

SouthKo

rea

Ireland

USA

Sw

eden

Sw

itzerland

Norway

UK

Germ

any

Austria

Be

lgium

Japan

France

Nethe

rland

sEu

roArea

Spain

Denm

ark

Finland

Portugal

Italy

Greece

16

UK goods exports to the EU and non-EU areas, percentage of total UK goods exports1999 to 2017

Source Pink book 2018

GiventheclearfailureoftheEUtogrow,thescaleoftheregulatoryburdenandtheUK’sstrategicadvantageinserviceswhydoestheCBI–andotherbusinessorganisationsandlargecorporations–supportthecommonrulebookofChequersanddefactoSingleMarketmembership?

WebelievethereareavarietyofreasonswhythereisapparentsupportbybigbusinesstowardstheEU.Firstly70%ofFTSE100companyrevenuescomefromoverseas.WhiletheUSdollarzoneisthemostimportanttradingfactorsuchanoverseasdominanceshiftsboardroomthinkingawayfromthenationaltotheglobal.TheirpolicyconcernsandresultinglobbyingisinBrusselsandnottheUK.Thismayfavourbigbusinessbutitdoesnothelptheentrepreneurialcompanyorsmallerbusiness,letalonetheconsumer.

Further,itmattersnotmuchtoUnilever,forexample,ifregulationishighanditisdoubtlessmarginallyeasiertoadoptonestandardthroughouttheEUthananindividualoneforUKconsumers.Moreover,manylargecompaniesmayactuallywelcomeanincreasingregulatoryburdenbecauseitincreasesthebarrierstoentryintheirindustrymakingitharderforsmallerplayerstocompete.Whilethetwincosttotheconsumerofexcessregulationandreducedcompletionandchoiceissubstantialitmaybenefitcertainmultinationalcompanies.ThusadangerousgapbetweenthewaytheCBIandlargecorporationsactandtherestofthepopulationisgrowing.

Itisthereforeimportanttoremember,whenbigbusinesslobby’s,thattheirinterestandthatofthewiderpopulationisgreatlydivergingandnottotheadvantageofUKconsumers.

0.4

0.42

0.44

0.46

0.48

0.5

0.52

0.54

0.56

0.58

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

EU Non-EU

17

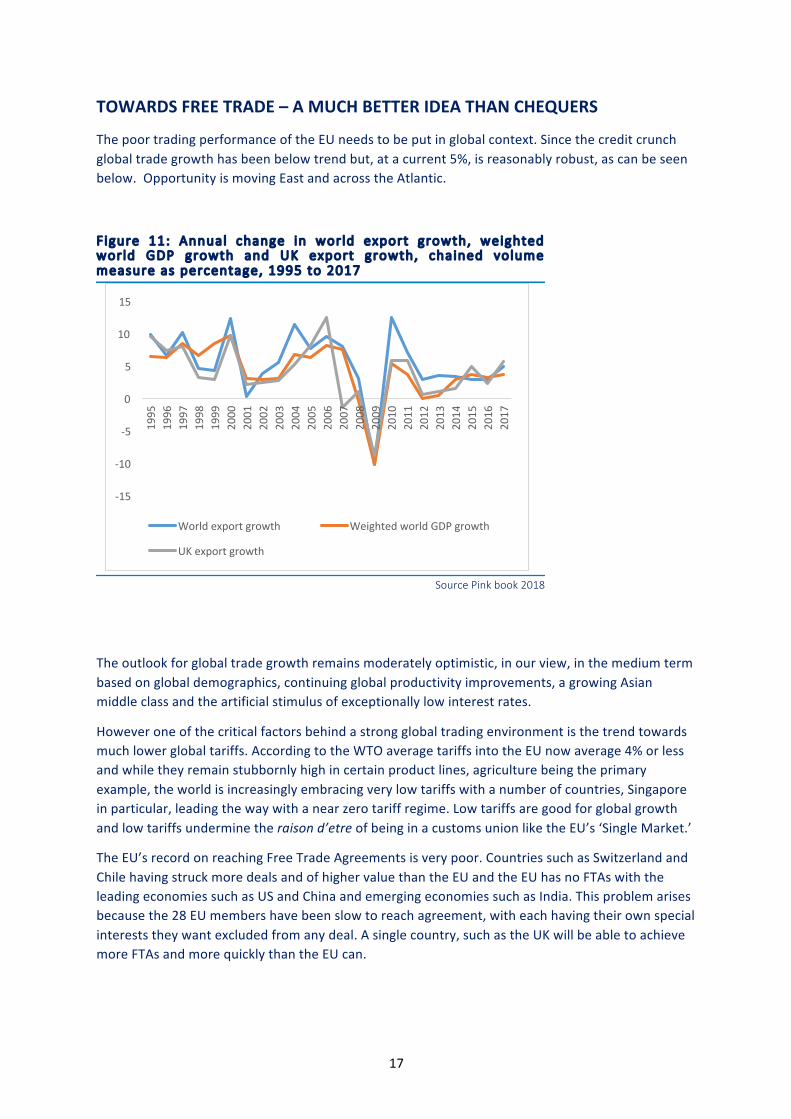

TOWARDSFREETRADE–AMUCHBETTERIDEATHANCHEQUERS

ThepoortradingperformanceoftheEUneedstobeputinglobalcontext.Sincethecreditcrunchglobaltradegrowthhasbeenbelowtrendbut,atacurrent5%,isreasonablyrobust,ascanbeseenbelow.OpportunityismovingEastandacrosstheAtlantic.

Figure 11: Annual change in world export growth, weighted world GDP growth and UK export growth, chained volume measure as percentage, 1995 to 2017

Source Pink book 2018

Theoutlookforglobaltradegrowthremainsmoderatelyoptimistic,inourview,inthemediumtermbasedonglobaldemographics,continuingglobalproductivityimprovements,agrowingAsianmiddleclassandtheartificialstimulusofexceptionallylowinterestrates.

Howeveroneofthecriticalfactorsbehindastrongglobaltradingenvironmentisthetrendtowardsmuchlowerglobaltariffs.AccordingtotheWTOaveragetariffsintotheEUnowaverage4%orlessandwhiletheyremainstubbornlyhighincertainproductlines,agriculturebeingtheprimaryexample,theworldisincreasinglyembracingverylowtariffswithanumberofcountries,Singaporeinparticular,leadingthewaywithanearzerotariffregime.Lowtariffsaregoodforglobalgrowthandlowtariffsunderminetheraisond’etreofbeinginacustomsunionliketheEU’s‘SingleMarket.’

TheEU’srecordonreachingFreeTradeAgreementsisverypoor.CountriessuchasSwitzerlandandChilehavingstruckmoredealsandofhighervaluethantheEUandtheEUhasnoFTAswiththeleadingeconomiessuchasUSandChinaandemergingeconomiessuchasIndia.Thisproblemarisesbecausethe28EUmembershavebeenslowtoreachagreement,witheachhavingtheirownspecialintereststheywantexcludedfromanydeal.Asinglecountry,suchastheUKwillbeabletoachievemoreFTAsandmorequicklythantheEUcan.

-15

-10

-5

0

5

10

15

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

Worldexportgrowth WeightedworldGDPgrowth

UKexportgrowth

18

Figure 15: Average Global tar if fs

Source WTO

AfarbetterideathanChequersistoridetheglobalshiftintariffsdownwardsandstrikeoutandseektradedealswiththeUS,China,Australia–andindeedtheEU.Thesedealsshouldplaytoourstrengthsinservicesaswellaszerotariffsingoods.FarfrombeingatthebackofthequeuemanycountriesrelishtheregulatorycompetitionthatanunshackledUKcouldoffer.

WhereareEUtariffsnow?

ThechartbelowshowstheEU’scurrentexternaltariffstructurewherenotradedealhasbeenstruck.InotherwordsthisistheWTOoption.Outsidecertainagriculturalproductstariffsareverylow.

Figure 15: EU external tar if f structure

Source Eurostat

0

0.5

1

1.5

2

2.5

3

3.5

Canada Switzerland EuropeanUnion

Singapore UnitedStates

05

10152025303540

19

IndeeditshouldbenotedthatagriculturalproductsimportedfromAfricaandotherdevelopingmarketsaresubjecttothesetariffscurrentlydirectlycostingtheUKconsumerandtheAfricanfarmerdearly.TheUK,withinthecustomsunionhasnoabilitytovarythesetariffs.UnderChequers,orsimilarderivativethatwillcontinuetobethecase.

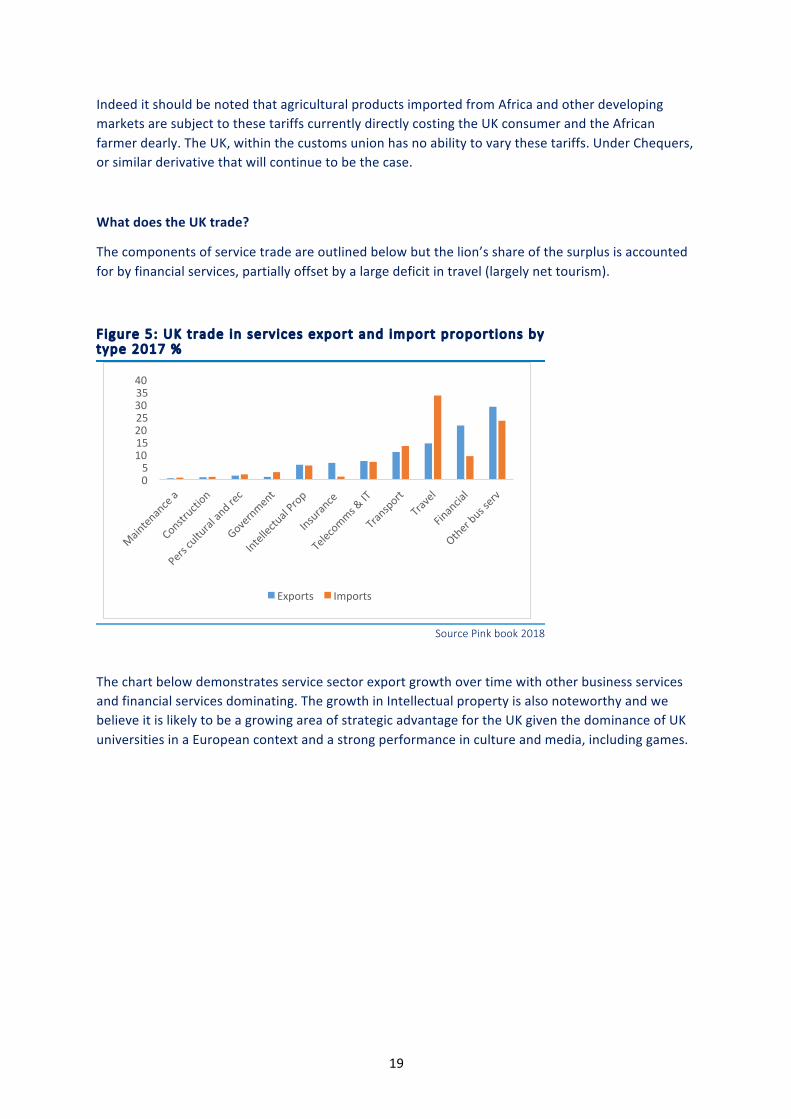

WhatdoestheUKtrade?

Thecomponentsofservicetradeareoutlinedbelowbutthelion’sshareofthesurplusisaccountedforbyfinancialservices,partiallyoffsetbyalargedeficitintravel(largelynettourism).

Figure 5: UK trade in services export and import proport ions by type 2017 %

Source Pink book 2018

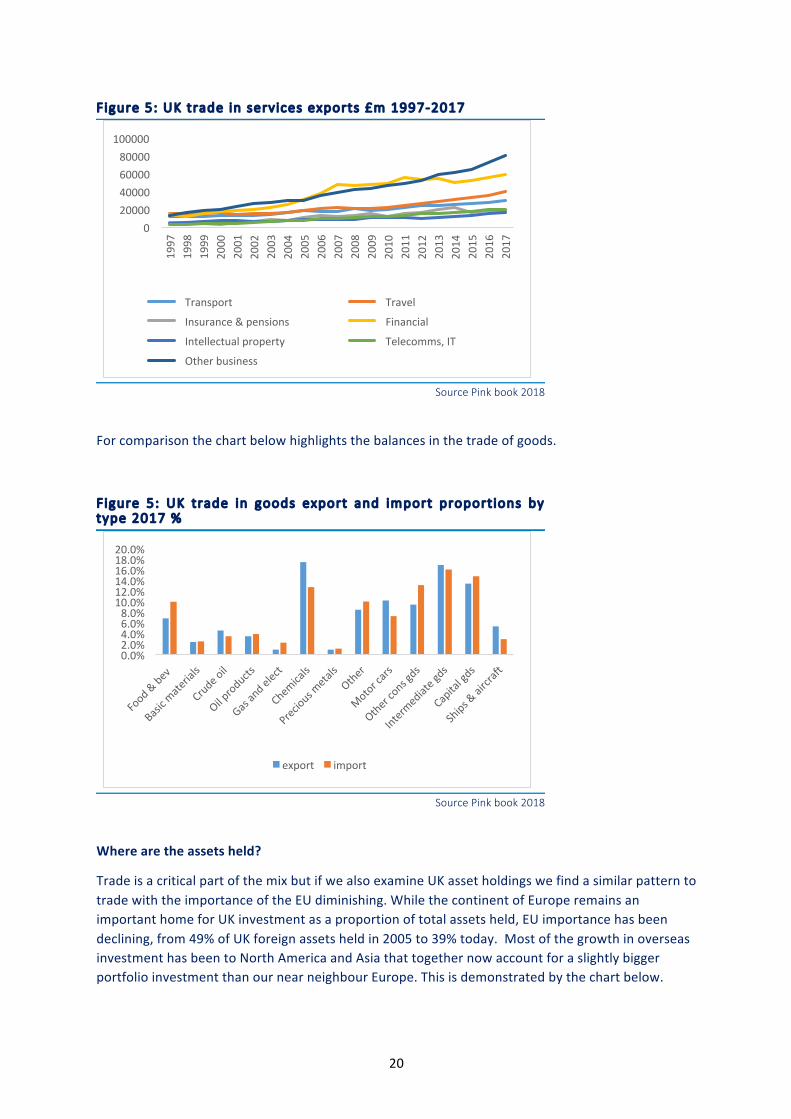

Thechartbelowdemonstratesservicesectorexportgrowthovertimewithotherbusinessservicesandfinancialservicesdominating.ThegrowthinIntellectualpropertyisalsonoteworthyandwebelieveitislikelytobeagrowingareaofstrategicadvantagefortheUKgiventhedominanceofUKuniversitiesinaEuropeancontextandastrongperformanceincultureandmedia,includinggames.

05

10152025303540

Exports Imports

20

Figure 5: UK trade in services exports £m 1997-2017

Source Pink book 2018

Forcomparisonthechartbelowhighlightsthebalancesinthetradeofgoods.

Figure 5: UK trade in goods export and import proport ions by type 2017 %

Source Pink book 2018

Wherearetheassetsheld?

TradeisacriticalpartofthemixbutifwealsoexamineUKassetholdingswefindasimilarpatterntotradewiththeimportanceoftheEUdiminishing.WhilethecontinentofEuroperemainsanimportanthomeforUKinvestmentasaproportionoftotalassetsheld,EUimportancehasbeendeclining,from49%ofUKforeignassetsheldin2005to39%today.MostofthegrowthinoverseasinvestmenthasbeentoNorthAmericaandAsiathattogethernowaccountforaslightlybiggerportfolioinvestmentthanournearneighbourEurope.Thisisdemonstratedbythechartbelow.

020000400006000080000

100000

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

Transport Travel

Insurance&pensions Financial

Intellectualproperty Telecomms,IT

Otherbusiness

0.0%2.0%4.0%6.0%8.0%10.0%12.0%14.0%16.0%18.0%20.0%

export import

21

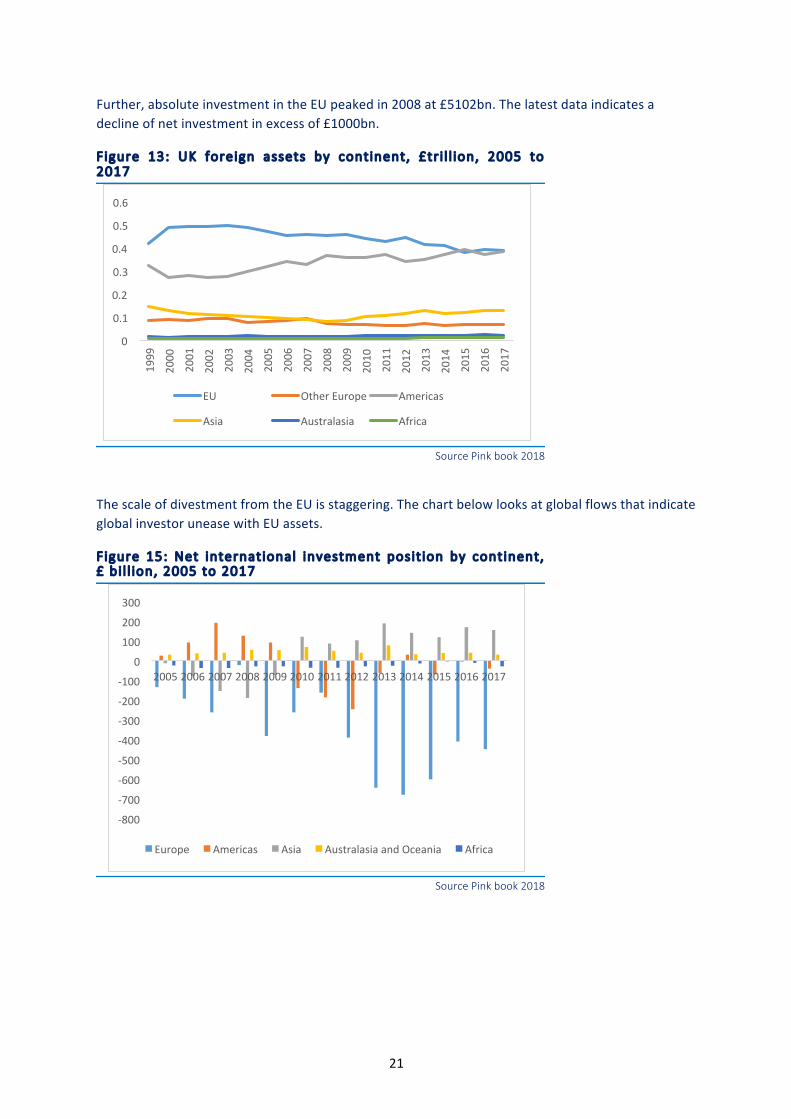

Further,absoluteinvestmentintheEUpeakedin2008at£5102bn.Thelatestdataindicatesadeclineofnetinvestmentinexcessof£1000bn.

Figure 13: UK foreign assets by continent, £tr i l l ion, 2005 to 2017

Source Pink book 2018

ThescaleofdivestmentfromtheEUisstaggering.ThechartbelowlooksatglobalflowsthatindicateglobalinvestoruneasewithEUassets.

Figure 15: Net international investment posit ion by continent, £ bi l l ion, 2005 to 2017

Source Pink book 2018

0

0.1

0.2

0.3

0.4

0.5

0.6

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

EU OtherEurope Americas

Asia Australasia Africa

-800

-700

-600

-500

-400

-300

-200

-100

0

100

200

300

2005200620072008200920102011201220132014201520162017

Europe Americas Asia AustralasiaandOceania Africa

22

WHYCHEQUERSSHOULDBECHUCKED

WehavedemonstratedthattheChequersProposalseffectivelymeanremainingintheEUSingleMarketdefactoandwillresultintheUKbeingobligedtoincorporatenewacquisinalllawrelatingtotheSingleMarket,environment,climatechange,socialandemploymentlawandconsumerprotection–leavinglittlescopetoadoptanymeaningfulindependentpolicy.Worsestill,itwillallbesignedintointernationaltreatymakingitverydifficulttounwind.

WehavedemonstratedthatwhilemaintainingfriendlyandconstructiverelationswiththeEUismanifestlyinbothparties’intereststheEUhasbeenforageneration,andislikelytocontinuetobefortheforeseeablefuture,theworld’sslowestgrowingbloc.Moreoverwehave,shownthattheUKtradesinsurpluswiththeUSandbroadlyneutrallywiththerestoftheworldbutrecordsa£96bncurrentaccountdeficitwiththeEU.ItissuperficiallyoddthatwecantradejustfinewherewehavenospecialdealandmassivelyindeficitwiththeEUwherewedo.Whatsortofnegotiatorswouldwishtolockusintothatsortofrelationshipinperpetuity?

TheUKGovernmentneedstoraiseitsgameandquickly.TheUKhasauniqueopportunitytotradefreelywiththeEUandexpandourlinksglobally.TheoftenarguedobjectiontoadealsimilartoCanada–thesocalledCanadaPlus–isthatittheEUsaysitrequiresaborderdowntheIrishSeagiventheUKgovernment’ssomewhatmisguidedbackstopagreementwiththeEU.

WeconsiderthistobeafabricatedrusetokeeptheUKintheSingleMarket.Sadly,thereareclearlythosewithintheBritishgovernmentmachinewhohavelatchedontothissupposedprobleminordertojustifyremaininginsideacustomsunionandsinglemarket.YetaborderbetweentheUKandtheIrishRepublicalreadyexistsatmanylevels(includingcurrency,VAT,tax,duties,welfare,justice)andensuringsmoothacceptanceofstandardsshouldnotbeaproblem.Theirony,however,istheIrishRepublichasfarmoretolosethantheUKiftalksfail,givenhowdependenttheRepublicisontheUKfortradewith44%ofIrishexportsgoingtotheUK.

ThereisaclearroutemapforadealandindeedoneDonaldTusk,PresidentoftheEUCouncilhasregularlyofferedtoGreatBritain–itnowneedstobeofferedtothewholeoftheUK.WithgoodwillonbothsidestheIrishissuecansensiblyberesolvedastheEUwellknows.

Moreover,theBritishpopulationisnotimpressed.GlobalBritaindemonstratedwithoneofthebiggestopinionpollsevercarriedout,withover22,000votersquestionedinthetop44Conservativemarginalconstituencies,thatChequersisnotonlyunlovedbutthepopulationhasseenthroughitaswell.TheclearpollingevidenceisthepopulationknowsChequersisBrexitinnameonlyandbelievesitwillbebadforthemandbadforthecountry.ItcouldwellcosttheConservativePartypoweraswehavedemonstratedthatatinyswinginsupportshiftsthebalancetoaCorbyn/SNPcoalitionoraCorbynvictoryoutright.

Thelinkhttps://globalbritain.co.uk/brexit-polling/providesthefullpollingdatasetbutChequersisplayingwithfire.IttiestheUKtoafailingbloc,makestheUKaruletakerwithnosayonnewlaw,severelyhamperstheUK’sabilitytostrikenewtradedealsandwithnearcertaintyensuresthattheUKislockedintoasystemthatharmsourtradingrelationshipsinthelongtermgivenitwouldbeenshrinedininternationallaw.

OntopofthistheChequersproposalisinbadfaithasitclearlycontravenesthereferendumresultthatwassubsequentlybackedupbysolemnmanifestopledges.Ignoringthestatedandimplicitpromisestoacceptthepublic’sdecisionanddeliveraBrexitthatmeantleavingtheSingleMarketandCustomsUnionwoulddountolddamagetothedemocraticprocess.

23

Putsimply,CanadaPlusformsthebasisofanoffer.Itisadealthatwouldworkforbusinessandplaystoourpotential.TheEUisusingtheIrishbackstopasanmethodtokeeptheUKintheSingleMarketandCustomsUniontoitsadvantage–itsbluffmustbecalled.

CONCLUSIONS

ThekeymythpropagatedinfavouroftheSingleMarketisthatitiscentraltoUKprosperity.Itisnot.WehavedemonstratedthattheUKtradeswellwiththeworldbutpoorlywiththeEU.ThisisoddastheUKhasnospecialtradearrangementswiththeUS,ChinaorAustraliabutrunsasmalltradesurpluswiththerestoftheworld,butaverylargedeficitwiththeveryregionwehaveacustomsunionwith–theEU.

TheEUisinstructuraldecline.Ithasunderperformedeveryotherregionintheworldforageneration.ThisisnotacoincidenceasotheradvancedeconomiesincludingtheUS,CanadaandAustraliahavepoweredahead.ItistheinstitutionalarrangementsoftheEUandthesinglecurrencyinparticularthathasresultedinrapideconomicdeclineandsociallyunacceptablelevelsofunemploymentinmuchoftheEU.TheEU’strendtowardscentralisedregulationunderminescompetitionandincreasesregulatoryburden.WithintheSingleMarketframeworktheUKwillcontinuetobebeholdentoneedlessregulationandlegalcreepasEUlawyersinterpretadefinitionofEUcompetencewellbeyondmerelytradingstandardsandintotomanyotherareasofnationallife.

TheEUhasalsofailedtosignglobalfreetradedealswiththeworld’smostimportantpartnersincludingtheUS,ChinaorAustralia.InsidetheEUtheUKcannotstrikeitsowndealswiththemanymuchfastergrowingnations.BecausetheEUisadiversegroupof28nationsagreementishighlyproblematicandcumbersome,hencethefailuretoreachagreement.OutsidetheEUtheUKcanmuchmorereadilystrikefreetradedeals.

ItisnowapparentfromcommentsfromtheUS,ChinaandAustraliaandothersthatfarfrombeing’atthebackofthequeue’othercountriesareverykeentostrikemutuallybeneficialfreetradedealswiththeUK.ThiswillallowtheUKtorebuilditshistoricmissionofencouragingglobalfreetradethathasgoneofftrackoverthelast40yearsastheUKhassurrendereditstradepolicy,sounsuccessfullytotheEU.

ItisalsoamyththattheUKneedstobepartoftheSingleMarkettotradewithit.Thisisclearlynotthecase.Allnationshaveaccess,outsideatinynumberundersanction(NorthKoreaandSyriaforexample)solongastheycomplywithlocalregulations.Thisisthecasetheworldover.OnedoesnotneedtojoinChinatotradewithitanymorethanoneneedstojointheEU.

ItisclearlyintheEU’sintereststoagreeazerotariffdealwiththeUK.TherearemanyreasonsforthisbuttheprimaryoneissimplybecausetheEUsellsmoretotheUKthantheUKsellstotheEU.ItwouldbenonsensicaltoundermineitsowntradeparticularlyatatimewhenEUgrowthissoweak.

If,however,theEUrefusestodosowithinreasonabletimeframe,theUKshouldleavetheEUwithoutaformalagreementon29thMarch2019,relyingonWTOrulesandstrikingfreetradedealswithourglobalpartners.ThisoutcomewouldbefarbetterthanwhattheChequersPlanoffersbecausetheUKwouldotherwisebesaddledwithacurrentmarginalinfluenceonSingleMarket

24

regulation(12%voteintheCouncilofMinisters)fornosayinregulatoryframeworkatallwhilehavingtoacceptfreemovementofpeople.

Toremainunderthejurisdictionofthecommonrulebook,effectivelystillunderEUjurisdiction,havinglefttheEU,istheremainoptionthatdeliversasovereigntyillusion–withnosay,lowgrowthandahighregulatoryburdenthatwouldlockinperpetualtradedeficits.ThatiswhyChequersmustbechuckedandCanadaPlususedasthetemplateforanewrelationship.

Abouttheauthors…EwenStewartEwenisaneconomicconsultanthavingpreviouslybeenworkedformajorinvestmentbanksinTheCityasaStrategist.EwenjoinedGlobalBritainasdirectorin2012whenBrexitwasstillaconceptandhassincehelpedmakeitareality.BrianMonteithBrianworkedinfinancialPRinTheCityfromtheearly80sbeforeestablishinghisowncommunicationconsultanciesinScotland.HelaterservedeightyearsasanelectedmemberoftheScottishParliamentincludingfouryearsasConvenerofthePublicAuditCommittee.Hereturnedtopoliticalandstrategiccommunicationsin2007andworksinternationallyinEurope,AfricaandtheCaribbean.

Disclaimer

GlobalBritainLimitedresearchandcommunicationsareintendedtoaddtotheunderstandingofeconomicandpoliticalpolicyandenhanceandinformpublicdebate.Althoughtheinformationcompiledinourresearchisproducedtothebestofourability,itsaccuracyisnotguaranteed.AnypersonsusingGlobalBritain’sresearchorcommunicationmaterialdoessosolelyattheirownriskandGlobalBritainLimitedshallbeundernoliabilitywhatsoeverinrespectthereof.

Usersacceptthatallintellectualpropertyrights(includingcopyright,patents,trademarks)whetherregistered,ornot,onthecommunicationshallremainthepropertyofGlobalBritainLimitedandnocustomer,orotherpersonshall,orshallattempttoobtainanytitletosuchrights.InformationappearingonthiscommunicationisthecopyrightofGlobalBritainLimitedhoweverusersarepermittedtocopysomematerialfortheirpersonalusesolongasGlobalBritainiscreditedastheinformationsource.

NeitherGlobalBritainLimited,noranyofitssuppliers,makeanywarrantiesexpressedorimplied,astotheaccuracy,adequacy,qualityorfitnessforanyparticularpurposeoftheinformationortheservicesforaparticularpurposeoruseandallsuchwarrantiesareexpresslyexcludedtothefullestextentthatsuchwarrantiesmaybeexcludedbylaw.Youbearallrisksfromanyusesorresultsofusinganyinformation.Youareresponsibleforvalidatingtheintegrityofanyinformationreceivedovertheinternet.

DuetothenumberofsourcesfromwhichGlobalBritainLimitedobtainscontentGlobalBritainLimitedshallnothaveanyliability(whetherincontractortort)foranylosses,costsordamagesresultingfromorrelatedtouseoforinabilitytouseanyinformationcontainedintheSiteortheprovisionoftheSitetothefullestextenttowhichsuchliabilitymaybeexcludedoravoidedbylawandinnoeventshallGlobalBritainLimitedbeliabletoyouforlostprofitsorforindirect,incidental,special,punitiveorconsequentialdamagesarisingoutoforinrelationtotheprovisionofinformationontheSite.

COMPANYDETAILS

GlobalBritainLimitedRegisteredoffice:LyntonHouse,7-12TavistockSquare,LondonWC1H9BQRegisteredinEnglandNo03502745