Embed Size (px)

Citation preview

Chemtech: A Showcase forCommon Law PartnershipDoctrines

By Andy Howlett and Lisandra Ortiz

Reprinted from Tax Notes, June 15, 2015, p. 1285

tax notesVolume 147, Number 11 June 15, 2015

®

(C)

TaxA

nalysts2015.A

llrightsreserved.

TaxA

nalystsdoes

notclaim

copyrightin

anypublic

domain

orthird

partycontent.

Chemtech: A Showcase forCommon Law Partnership Doctrines

By Andy Howlett and Lisandra Ortiz

Table of Contents

I. Facts . . . . . . . . . . . . . . . . . . . . . . . . . . . 1285A. Chemtech I . . . . . . . . . . . . . . . . . . . . 1285B. Chemtech II . . . . . . . . . . . . . . . . . . . . 1288

II. District Court Decision . . . . . . . . . . . . . . 1289A. Economic Substance . . . . . . . . . . . . . . 1290B. Sham Partnership . . . . . . . . . . . . . . . . 1290C. Bona Fide Partners . . . . . . . . . . . . . . . 1291

III. Fifth Circuit Decision . . . . . . . . . . . . . . . 1292A. Dow and the Government State Their

Cases . . . . . . . . . . . . . . . . . . . . . . . . 1292B. Fifth Circuit Opinion . . . . . . . . . . . . . . 1293C. Petition for Rehearing En Banc . . . . . . . 1295

IV. Chemtech’s Significance . . . . . . . . . . . . . 1295V. Conclusion . . . . . . . . . . . . . . . . . . . . . . . 1297

On September 10, 2014, the Fifth Circuit an-nounced its decision in Chemtech,1 giving the gov-ernment a win in its years-long battle againstallegedly abusive tax shelters. The case is significantfor the courts’ use of common law doctrines todisregard two partnerships formed by Dow Chemi-cal Co. The district court broadly invoked the shampartnership doctrine, the economic substance doc-trine, and the bona fide partner doctrine, whereasthe Fifth Circuit focused solely on the sham part-nership issue.

This report examines Chemtech in depth, analyz-ing its implications for partnership arrangements. Itconcludes that in light of the district court and FifthCircuit opinions, practitioners must consider theallocation of upside potential and downside riskwhen forming partnerships that involve priorityreturns, guarantees, and other protections againstlimited partners’ risk of loss.

I. Facts

A. Chemtech I

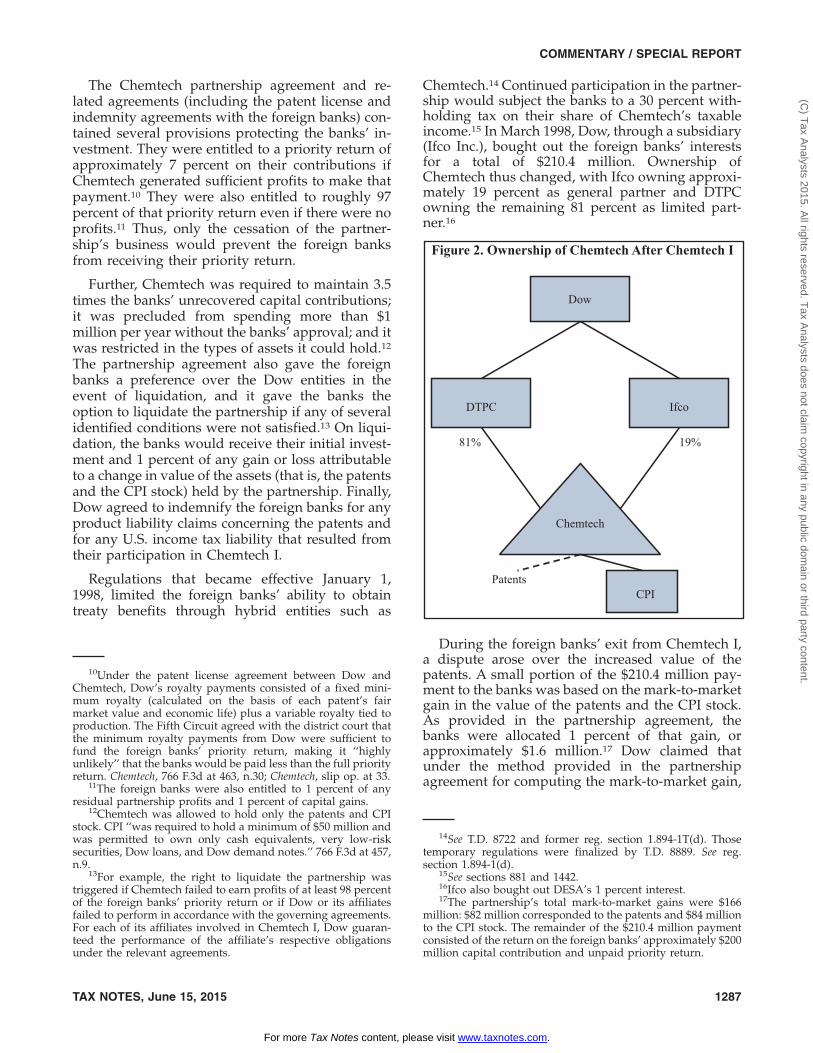

Goldman Sachs, Dow’s principal investmentbank since the 1950s, proposed in 1992 that thecompany use a special limited investment partner-ship structure.2 Dow implemented the transaction(Chemtech I) from 1993 until 1998 by formingChemtech Royalty Associates LP (Chemtech), aDelaware limited partnership.

Several Dow entities were involved in theChemtech I transaction. A foreign subsidiary, DowEurope SA (DESA), contributed approximately $10million to Chemtech and received a 1 percentinterest as the general partner. Diamond Technol-ogy Partnership Co. (DTPC), another Dow subsid-iary, initially became an 88 percent limited partnerby contributing to Chemtech 73 patents created and

1Chemtech Royalty Associates LP v. United States, 766 F.3d 453(5th Cir. 2014), aff’g in part and rev’g and vacating in part, No.3:05-cv-00944 (M.D. La. 2013) (slip op.).

2See Plaintiff’s Pretrial Brief at 11, Chemtech Royalty AssociatesLP v. United States, Nos. 05-944, 06-258, 07-405 (M.D. La. 2011).Throughout this report, uncontested facts are generally takenfrom the Fifth Circuit’s opinion, the district court’s opinion,Dow’s briefs, or some combination thereof.

Lisandra Ortiz

Andy Howlett

Andy Howlett is a seniorassociate and Lisandra Ortiz isan associate with Miller & Che-valier Chtd. The authors thankLinda Carlisle and PatriciaSweeney for their assistancewith this report.

Howlett and Ortiz examineChemtech and the issues itraises for tax practitioners informing partnership transac-tions. They analyze the lowercourt’s broad decision, whichdisregarded the partnerships atissue using three separate com-mon law doctrines, and theycompare it with the Fifth Cir-cuit’s narrower opinion, whichaddressed only the sham part-nership issue.

tax notes™

SPECIAL REPORT

TAX NOTES, June 15, 2015 1285

For more Tax Notes content, please visit www.taxnotes.com.

(C) T

ax Analysts 2015. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

used by Dow in its business operations.3 In anothertransaction, DESA and DTPC formed ChemtechPortfolio Inc. (CPI), a Texas corporation, and DTPCtransferred all its CPI stock to Chemtech as a capitalcontribution.4 Chemtech took an initial basis ofapproximately $2.5 million in the CPI stock, thesame as DTPC’s basis.

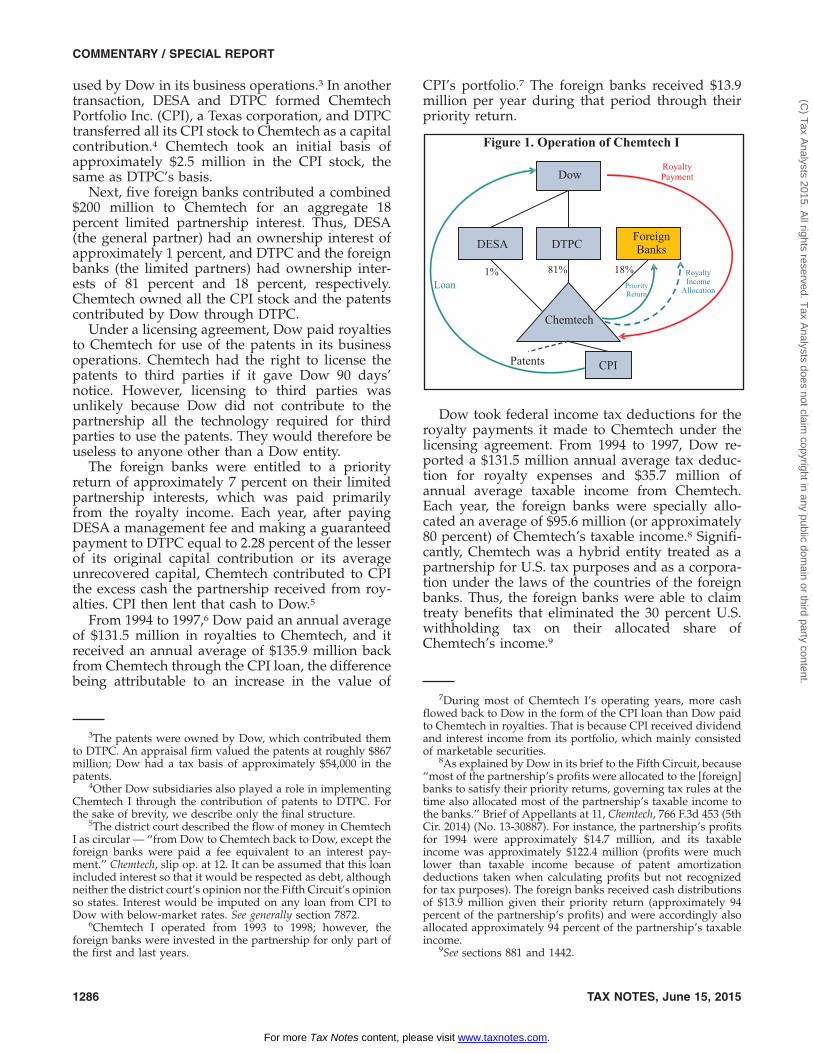

Next, five foreign banks contributed a combined$200 million to Chemtech for an aggregate 18percent limited partnership interest. Thus, DESA(the general partner) had an ownership interest ofapproximately 1 percent, and DTPC and the foreignbanks (the limited partners) had ownership inter-ests of 81 percent and 18 percent, respectively.Chemtech owned all the CPI stock and the patentscontributed by Dow through DTPC.

Under a licensing agreement, Dow paid royaltiesto Chemtech for use of the patents in its businessoperations. Chemtech had the right to license thepatents to third parties if it gave Dow 90 days’notice. However, licensing to third parties wasunlikely because Dow did not contribute to thepartnership all the technology required for thirdparties to use the patents. They would therefore beuseless to anyone other than a Dow entity.

The foreign banks were entitled to a priorityreturn of approximately 7 percent on their limitedpartnership interests, which was paid primarilyfrom the royalty income. Each year, after payingDESA a management fee and making a guaranteedpayment to DTPC equal to 2.28 percent of the lesserof its original capital contribution or its averageunrecovered capital, Chemtech contributed to CPIthe excess cash the partnership received from roy-alties. CPI then lent that cash to Dow.5

From 1994 to 1997,6 Dow paid an annual averageof $131.5 million in royalties to Chemtech, and itreceived an annual average of $135.9 million backfrom Chemtech through the CPI loan, the differencebeing attributable to an increase in the value of

CPI’s portfolio.7 The foreign banks received $13.9million per year during that period through theirpriority return.

Dow took federal income tax deductions for theroyalty payments it made to Chemtech under thelicensing agreement. From 1994 to 1997, Dow re-ported a $131.5 million annual average tax deduc-tion for royalty expenses and $35.7 million ofannual average taxable income from Chemtech.Each year, the foreign banks were specially allo-cated an average of $95.6 million (or approximately80 percent) of Chemtech’s taxable income.8 Signifi-cantly, Chemtech was a hybrid entity treated as apartnership for U.S. tax purposes and as a corpora-tion under the laws of the countries of the foreignbanks. Thus, the foreign banks were able to claimtreaty benefits that eliminated the 30 percent U.S.withholding tax on their allocated share ofChemtech’s income.9

3The patents were owned by Dow, which contributed themto DTPC. An appraisal firm valued the patents at roughly $867million; Dow had a tax basis of approximately $54,000 in thepatents.

4Other Dow subsidiaries also played a role in implementingChemtech I through the contribution of patents to DTPC. Forthe sake of brevity, we describe only the final structure.

5The district court described the flow of money in ChemtechI as circular — ‘‘from Dow to Chemtech back to Dow, except theforeign banks were paid a fee equivalent to an interest pay-ment.’’ Chemtech, slip op. at 12. It can be assumed that this loanincluded interest so that it would be respected as debt, althoughneither the district court’s opinion nor the Fifth Circuit’s opinionso states. Interest would be imputed on any loan from CPI toDow with below-market rates. See generally section 7872.

6Chemtech I operated from 1993 to 1998; however, theforeign banks were invested in the partnership for only part ofthe first and last years.

7During most of Chemtech I’s operating years, more cashflowed back to Dow in the form of the CPI loan than Dow paidto Chemtech in royalties. That is because CPI received dividendand interest income from its portfolio, which mainly consistedof marketable securities.

8As explained by Dow in its brief to the Fifth Circuit, because‘‘most of the partnership’s profits were allocated to the [foreign]banks to satisfy their priority returns, governing tax rules at thetime also allocated most of the partnership’s taxable income tothe banks.’’ Brief of Appellants at 11, Chemtech, 766 F.3d 453 (5thCir. 2014) (No. 13-30887). For instance, the partnership’s profitsfor 1994 were approximately $14.7 million, and its taxableincome was approximately $122.4 million (profits were muchlower than taxable income because of patent amortizationdeductions taken when calculating profits but not recognizedfor tax purposes). The foreign banks received cash distributionsof $13.9 million given their priority return (approximately 94percent of the partnership’s profits) and were accordingly alsoallocated approximately 94 percent of the partnership’s taxableincome.

9See sections 881 and 1442.

Dow

ForeignBanksDTPCDESA

CPI

Chemtech

Patents

1% 18%81%

RoyaltyPayment

Loan PriorityReturn

RoyaltyIncome

Allocation

Figure 1. Operation of Chemtech I

COMMENTARY / SPECIAL REPORT

1286 TAX NOTES, June 15, 2015

For more Tax Notes content, please visit www.taxnotes.com.

(C) T

ax Analysts 2015. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

The Chemtech partnership agreement and re-lated agreements (including the patent license andindemnity agreements with the foreign banks) con-tained several provisions protecting the banks’ in-vestment. They were entitled to a priority return ofapproximately 7 percent on their contributions ifChemtech generated sufficient profits to make thatpayment.10 They were also entitled to roughly 97percent of that priority return even if there were noprofits.11 Thus, only the cessation of the partner-ship’s business would prevent the foreign banksfrom receiving their priority return.

Further, Chemtech was required to maintain 3.5times the banks’ unrecovered capital contributions;it was precluded from spending more than $1million per year without the banks’ approval; and itwas restricted in the types of assets it could hold.12

The partnership agreement also gave the foreignbanks a preference over the Dow entities in theevent of liquidation, and it gave the banks theoption to liquidate the partnership if any of severalidentified conditions were not satisfied.13 On liqui-dation, the banks would receive their initial invest-ment and 1 percent of any gain or loss attributableto a change in value of the assets (that is, the patentsand the CPI stock) held by the partnership. Finally,Dow agreed to indemnify the foreign banks for anyproduct liability claims concerning the patents andfor any U.S. income tax liability that resulted fromtheir participation in Chemtech I.

Regulations that became effective January 1,1998, limited the foreign banks’ ability to obtaintreaty benefits through hybrid entities such as

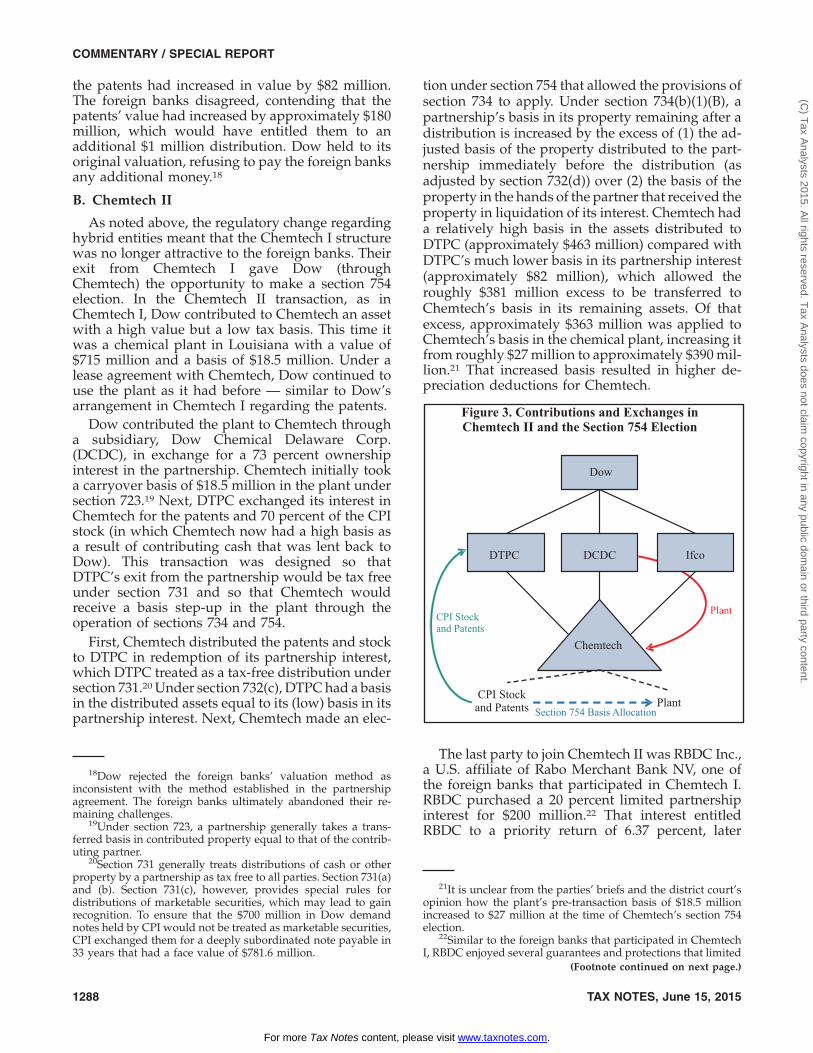

Chemtech.14 Continued participation in the partner-ship would subject the banks to a 30 percent with-holding tax on their share of Chemtech’s taxableincome.15 In March 1998, Dow, through a subsidiary(Ifco Inc.), bought out the foreign banks’ interestsfor a total of $210.4 million. Ownership ofChemtech thus changed, with Ifco owning approxi-mately 19 percent as general partner and DTPCowning the remaining 81 percent as limited part-ner.16

During the foreign banks’ exit from Chemtech I,a dispute arose over the increased value of thepatents. A small portion of the $210.4 million pay-ment to the banks was based on the mark-to-marketgain in the value of the patents and the CPI stock.As provided in the partnership agreement, thebanks were allocated 1 percent of that gain, orapproximately $1.6 million.17 Dow claimed thatunder the method provided in the partnershipagreement for computing the mark-to-market gain,

10Under the patent license agreement between Dow andChemtech, Dow’s royalty payments consisted of a fixed mini-mum royalty (calculated on the basis of each patent’s fairmarket value and economic life) plus a variable royalty tied toproduction. The Fifth Circuit agreed with the district court thatthe minimum royalty payments from Dow were sufficient tofund the foreign banks’ priority return, making it ‘‘highlyunlikely’’ that the banks would be paid less than the full priorityreturn. Chemtech, 766 F.3d at 463, n.30; Chemtech, slip op. at 33.

11The foreign banks were also entitled to 1 percent of anyresidual partnership profits and 1 percent of capital gains.

12Chemtech was allowed to hold only the patents and CPIstock. CPI ‘‘was required to hold a minimum of $50 million andwas permitted to own only cash equivalents, very low-risksecurities, Dow loans, and Dow demand notes.’’ 766 F.3d at 457,n.9.

13For example, the right to liquidate the partnership wastriggered if Chemtech failed to earn profits of at least 98 percentof the foreign banks’ priority return or if Dow or its affiliatesfailed to perform in accordance with the governing agreements.For each of its affiliates involved in Chemtech I, Dow guaran-teed the performance of the affiliate’s respective obligationsunder the relevant agreements.

14See T.D. 8722 and former reg. section 1.894-1T(d). Thosetemporary regulations were finalized by T.D. 8889. See reg.section 1.894-1(d).

15See sections 881 and 1442.16Ifco also bought out DESA’s 1 percent interest.17The partnership’s total mark-to-market gains were $166

million: $82 million corresponded to the patents and $84 millionto the CPI stock. The remainder of the $210.4 million paymentconsisted of the return on the foreign banks’ approximately $200million capital contribution and unpaid priority return.

Dow

IfcoDTPC

CPI

Chemtech

Patents

19%81%

Figure 2. Ownership of Chemtech After Chemtech I

COMMENTARY / SPECIAL REPORT

TAX NOTES, June 15, 2015 1287

For more Tax Notes content, please visit www.taxnotes.com.

(C) T

ax Analysts 2015. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

the patents had increased in value by $82 million.The foreign banks disagreed, contending that thepatents’ value had increased by approximately $180million, which would have entitled them to anadditional $1 million distribution. Dow held to itsoriginal valuation, refusing to pay the foreign banksany additional money.18

B. Chemtech II

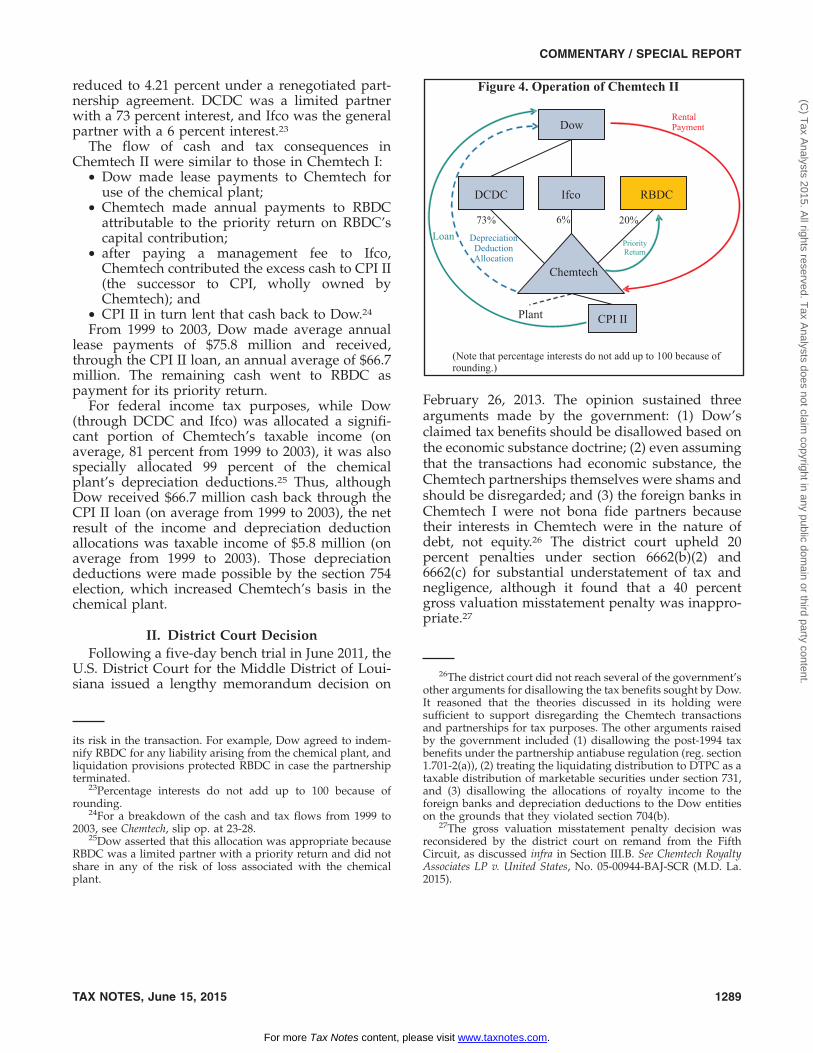

As noted above, the regulatory change regardinghybrid entities meant that the Chemtech I structurewas no longer attractive to the foreign banks. Theirexit from Chemtech I gave Dow (throughChemtech) the opportunity to make a section 754election. In the Chemtech II transaction, as inChemtech I, Dow contributed to Chemtech an assetwith a high value but a low tax basis. This time itwas a chemical plant in Louisiana with a value of$715 million and a basis of $18.5 million. Under alease agreement with Chemtech, Dow continued touse the plant as it had before — similar to Dow’sarrangement in Chemtech I regarding the patents.

Dow contributed the plant to Chemtech througha subsidiary, Dow Chemical Delaware Corp.(DCDC), in exchange for a 73 percent ownershipinterest in the partnership. Chemtech initially tooka carryover basis of $18.5 million in the plant undersection 723.19 Next, DTPC exchanged its interest inChemtech for the patents and 70 percent of the CPIstock (in which Chemtech now had a high basis asa result of contributing cash that was lent back toDow). This transaction was designed so thatDTPC’s exit from the partnership would be tax freeunder section 731 and so that Chemtech wouldreceive a basis step-up in the plant through theoperation of sections 734 and 754.

First, Chemtech distributed the patents and stockto DTPC in redemption of its partnership interest,which DTPC treated as a tax-free distribution undersection 731.20 Under section 732(c), DTPC had a basisin the distributed assets equal to its (low) basis in itspartnership interest. Next, Chemtech made an elec-

tion under section 754 that allowed the provisions ofsection 734 to apply. Under section 734(b)(1)(B), apartnership’s basis in its property remaining after adistribution is increased by the excess of (1) the ad-justed basis of the property distributed to the part-nership immediately before the distribution (asadjusted by section 732(d)) over (2) the basis of theproperty in the hands of the partner that received theproperty in liquidation of its interest. Chemtech hada relatively high basis in the assets distributed toDTPC (approximately $463 million) compared withDTPC’s much lower basis in its partnership interest(approximately $82 million), which allowed theroughly $381 million excess to be transferred toChemtech’s basis in its remaining assets. Of thatexcess, approximately $363 million was applied toChemtech’s basis in the chemical plant, increasing itfrom roughly $27 million to approximately $390 mil-lion.21 That increased basis resulted in higher de-preciation deductions for Chemtech.

The last party to join Chemtech II was RBDC Inc.,a U.S. affiliate of Rabo Merchant Bank NV, one ofthe foreign banks that participated in Chemtech I.RBDC purchased a 20 percent limited partnershipinterest for $200 million.22 That interest entitledRBDC to a priority return of 6.37 percent, later

18Dow rejected the foreign banks’ valuation method asinconsistent with the method established in the partnershipagreement. The foreign banks ultimately abandoned their re-maining challenges.

19Under section 723, a partnership generally takes a trans-ferred basis in contributed property equal to that of the contrib-uting partner.

20Section 731 generally treats distributions of cash or otherproperty by a partnership as tax free to all parties. Section 731(a)and (b). Section 731(c), however, provides special rules fordistributions of marketable securities, which may lead to gainrecognition. To ensure that the $700 million in Dow demandnotes held by CPI would not be treated as marketable securities,CPI exchanged them for a deeply subordinated note payable in33 years that had a face value of $781.6 million.

21It is unclear from the parties’ briefs and the district court’sopinion how the plant’s pre-transaction basis of $18.5 millionincreased to $27 million at the time of Chemtech’s section 754election.

22Similar to the foreign banks that participated in ChemtechI, RBDC enjoyed several guarantees and protections that limited

Dow

IfcoDCDCDTPC

Chemtech

CPI Stockand Patents Plant

CPI Stockand Patents

Section 754 Basis Allocation

Figure 3. Contributions and Exchanges inChemtech II and the Section 754 Election

Plant

COMMENTARY / SPECIAL REPORT

(Footnote continued on next page.)

1288 TAX NOTES, June 15, 2015

For more Tax Notes content, please visit www.taxnotes.com.

(C) T

ax Analysts 2015. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

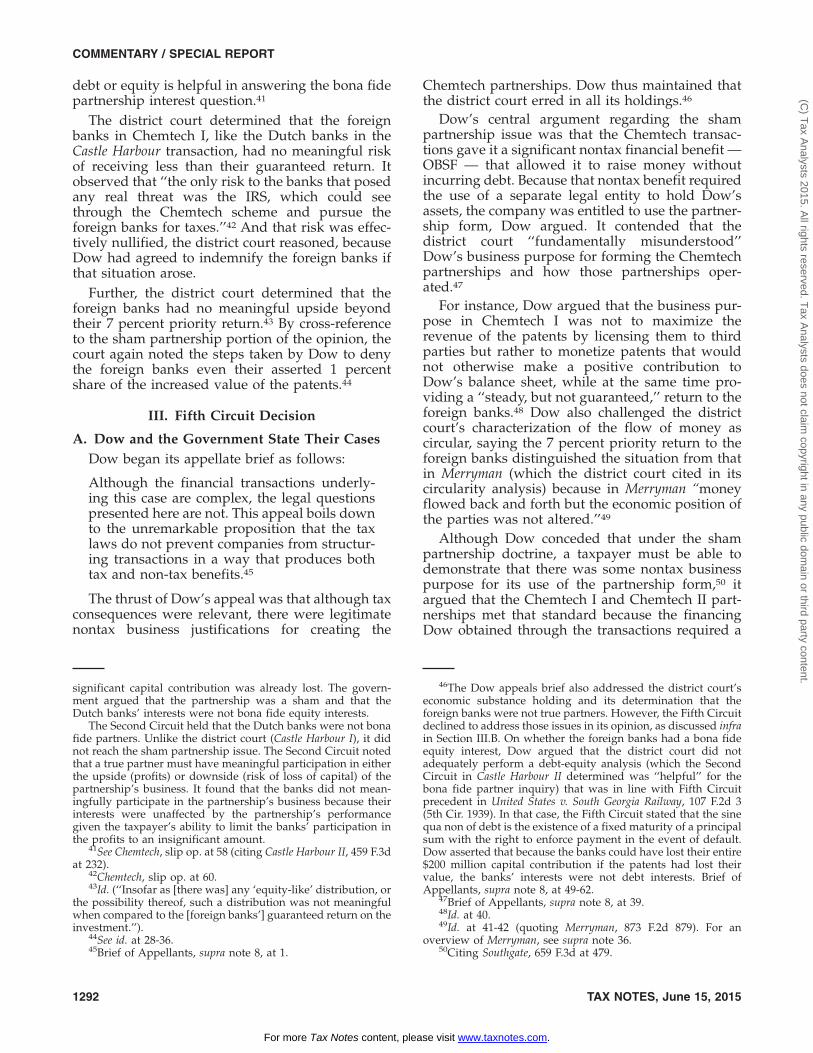

reduced to 4.21 percent under a renegotiated part-nership agreement. DCDC was a limited partnerwith a 73 percent interest, and Ifco was the generalpartner with a 6 percent interest.23

The flow of cash and tax consequences inChemtech II were similar to those in Chemtech I:

• Dow made lease payments to Chemtech foruse of the chemical plant;

• Chemtech made annual payments to RBDCattributable to the priority return on RBDC’scapital contribution;

• after paying a management fee to Ifco,Chemtech contributed the excess cash to CPI II(the successor to CPI, wholly owned byChemtech); and

• CPI II in turn lent that cash back to Dow.24

From 1999 to 2003, Dow made average annuallease payments of $75.8 million and received,through the CPI II loan, an annual average of $66.7million. The remaining cash went to RBDC aspayment for its priority return.

For federal income tax purposes, while Dow(through DCDC and Ifco) was allocated a signifi-cant portion of Chemtech’s taxable income (onaverage, 81 percent from 1999 to 2003), it was alsospecially allocated 99 percent of the chemicalplant’s depreciation deductions.25 Thus, althoughDow received $66.7 million cash back through theCPI II loan (on average from 1999 to 2003), the netresult of the income and depreciation deductionallocations was taxable income of $5.8 million (onaverage from 1999 to 2003). Those depreciationdeductions were made possible by the section 754election, which increased Chemtech’s basis in thechemical plant.

II. District Court DecisionFollowing a five-day bench trial in June 2011, the

U.S. District Court for the Middle District of Loui-siana issued a lengthy memorandum decision on

February 26, 2013. The opinion sustained threearguments made by the government: (1) Dow’sclaimed tax benefits should be disallowed based onthe economic substance doctrine; (2) even assumingthat the transactions had economic substance, theChemtech partnerships themselves were shams andshould be disregarded; and (3) the foreign banks inChemtech I were not bona fide partners becausetheir interests in Chemtech were in the nature ofdebt, not equity.26 The district court upheld 20percent penalties under section 6662(b)(2) and6662(c) for substantial understatement of tax andnegligence, although it found that a 40 percentgross valuation misstatement penalty was inappro-priate.27

its risk in the transaction. For example, Dow agreed to indem-nify RBDC for any liability arising from the chemical plant, andliquidation provisions protected RBDC in case the partnershipterminated.

23Percentage interests do not add up to 100 because ofrounding.

24For a breakdown of the cash and tax flows from 1999 to2003, see Chemtech, slip op. at 23-28.

25Dow asserted that this allocation was appropriate becauseRBDC was a limited partner with a priority return and did notshare in any of the risk of loss associated with the chemicalplant.

26The district court did not reach several of the government’sother arguments for disallowing the tax benefits sought by Dow.It reasoned that the theories discussed in its holding weresufficient to support disregarding the Chemtech transactionsand partnerships for tax purposes. The other arguments raisedby the government included (1) disallowing the post-1994 taxbenefits under the partnership antiabuse regulation (reg. section1.701-2(a)), (2) treating the liquidating distribution to DTPC as ataxable distribution of marketable securities under section 731,and (3) disallowing the allocations of royalty income to theforeign banks and depreciation deductions to the Dow entitieson the grounds that they violated section 704(b).

27The gross valuation misstatement penalty decision wasreconsidered by the district court on remand from the FifthCircuit, as discussed infra in Section III.B. See Chemtech RoyaltyAssociates LP v. United States, No. 05-00944-BAJ-SCR (M.D. La.2015).

Dow

RBDCIfcoDCDC

CPI II

Chemtech

Plant

73% 20%6%

RentalPayment

LoanPriorityReturn

DepreciationDeductionAllocation

Figure 4. Operation of Chemtech II

(Note that percentage interests do not add up to 100 because ofrounding.)

COMMENTARY / SPECIAL REPORT

TAX NOTES, June 15, 2015 1289

For more Tax Notes content, please visit www.taxnotes.com.

(C) T

ax Analysts 2015. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

A. Economic Substance

Relying on Frank Lyon28 and Klamath,29 the dis-trict court stated that in the Fifth Circuit, a transac-tion is respected for tax purposes under theeconomic substance doctrine if it ‘‘(1) has economicsubstance compelled by business or regulatory re-alities, (2) is imbued with tax-independent consid-erations, and (3) is not shaped totally by taxavoidance features.’’30 The district court also ob-served that in the Fifth Circuit, Klamath has beenread as establishing a two-part economic substancetest: an objective prong (the taxpayer must establishthat the transaction had a reasonable possibility ofprofit) and a subjective prong (the taxpayer mustestablish that it was motivated to enter into thetransaction for a legitimate nontax business pur-pose).31 The district court found that the Chemtechtransactions satisfied neither of those prongs.

On the objective prong, the district court said thatthere was in fact no income generated by formingChemtech. The circular cash flows ultimately re-sulted in no economic advantage — a findingsupported by the testimony of both sides’ experts —

according to the district court.32 Thus, the districtcourt concluded that the transaction in no wayaffected Dow’s financial position.

Analyzing the subjective prong, the district courtlooked to Dow’s asserted business purpose in en-tering the Chemtech transactions: its desire to ob-tain off-balance-sheet financing (OBSF). Dowargued that its primary business purpose in enter-ing the transaction was to raise capital withoutissuing debt, which would hurt its balance sheet. Itasserted that OBSF was a useful tool to maintain ahigh credit rating, which was significantly affectedby the company’s ratio of debt to total capital.

The district court rejected Dow’s OBSF argu-ment. It believed that the Chemtech transactionshad no genuine business purpose and were moti-vated solely by tax avoidance considerations. Thedistrict court noted that when the purpose of thetransaction is to make a profit, a ‘‘reasonable possi-bility of profit that is substantial in relation to thetax benefits generated’’ is required.33 Dow did notassert that the purpose of the Chemtech transac-tions was to make a profit but rather said it was toobtain OBSF. For the district court, Dow’s need forOBSF did not satisfy the requisite business purposebecause there were cheaper and simpler alterna-tives that could have achieved the company’s ob-jective of raising capital while maintaining a strongcredit rating. Accordingly, the district court con-cluded that whatever benefits OBSF would haveprovided paled in comparison with the expectedtax benefits of the Chemtech transactions.

B. Sham Partnership

The district court applied the sham partnershipdoctrine to Chemtech I and Chemtech II and deter-mined that the partnerships should be disregardedfor federal tax purposes. At the core of the shampartnership doctrine is Culbertson, in which theSupreme Court in 1949 held that a partnership willbe respected for federal tax purposes only if ‘‘thepartners really and truly intended to join togetherfor the purpose of carrying on the business andsharing in the profits and losses or both.’’34 Thatassessment of the taxpayer’s subjective intent is

28Frank Lyon Co. v. United States, 435 U.S. 561, 583-584 (1978)(When ‘‘there is a genuine multiple-party transaction witheconomic substance which is compelled or encouraged bybusiness or regulatory realities, is imbued with tax-independentconsiderations, and is not shaped solely by tax avoidancefeatures that have meaningless labels attached, the Governmentshould honor the allocation of rights and duties effectuated bythe parties.’’).

29Klamath Strategic Investment Fund v. United States, 568 F.3d537 (5th Cir. 2009).

30Chemtech, slip op. at 47 (quoting Klamath, 568 F.3d at 544).31Id. (citing Southgate Master Fund LLC v. United States, 651 F.

Supp.2d 596, 654 (N.D. Tex. 2009), aff’d, 659 F.3d 466 (5th Cir.2011)). In Southgate, the taxpayer formed a partnership with aChinese government bank. The bank contributed a high-basis,low-value package of nonperforming loans to the partnership.The taxpayer contributed marketable low-risk securities to thepartnership and retained effective control over them. The part-nership then sold a portion of the nonperforming loans, whichgenerated a loss to the partnership because of its high basis inthe loans. The Fifth Circuit held that the partnership’s acquisi-tion of the nonperforming loans had economic substance be-cause (1) under the objective inquiry, the partnership and itsmembers entered into the transaction ‘‘with a reasonable possi-bility of making a profit’’; and (2) subjectively, the loans wereacquired for ‘‘legitimate purposes,’’ with the parties believingthat they could earn a profit and some of the partners agreeingto the deal ‘‘regardless of whether it had any tax benefits.’’Southgate, 659 F.3d at 480-483. The court determined, however,that the partnership was a sham because the partners and thebank did not intend to join together in the conduct of a business,did not intend to share the profits and losses of the venture, anddid not have a valid business purpose. Id. at 483-491; see infraSection II.B (discussing the Chemtech district court’s sham part-nership holding).

32‘‘Both Dr. Hubbard and Dow’s economic expert, AndrewCarron, agree that ‘the net present value of the financingtransactions is at most zero.’’’ Chemtech, slip op. at 48.

33Id. at 51.34Commissioner v. Culbertson, 337 U.S. 733, 741 (1949) (citation

and internal quotation marks omitted). The sham partnershipdoctrine has also been the subject of several recent decisions,and its contours continue to evolve. See, e.g., Southgate, 659 F.3d466.

COMMENTARY / SPECIAL REPORT

1290 TAX NOTES, June 15, 2015

For more Tax Notes content, please visit www.taxnotes.com.

(C) T

ax Analysts 2015. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

made in light of all relevant facts and circum-stances.35 The district court characterized the test aswhether the formation of the partnership (as distin-guished from its business operations) has economicsubstance.36

The district court determined that Dow had nointent to derive additional revenue through its useof the partnership form, a finding that contributedto the court’s conclusion that Chemtech was not atrue partnership.37 Regarding the patents Dow con-tributed to the partnership in Chemtech I, thedistrict court found it significant that Dow chosepatents it would be able to continue to use after thetransfer and that the company had no intention oflicensing the patents to third parties. Moreover, inthe district court’s view, the circular flow of funds— with no real opportunity for anything resem-

bling an economic profit — further suggested thatthe partnership was a sham.38

The final factor considered by the district court inits sham partnership analysis was the allocation ofrisks and losses between the partners. It found thatthe foreign banks in Chemtech I and RBDC inChemtech II did not bear the risks of a true partneror entrepreneur but rather, as a result of the guar-antees provided by Dow, essentially had securedloan interests. Moreover, it determined that becausethe partnership agreement in Chemtech I allocated99 percent of any growth in the value of the patentsto Dow, the foreign banks’ potential upside wasconsiderably limited as well. The district court alsofound the dispute concerning the banks’ 1 percentinterest in the growth of the patents significant,stating that Dow’s success in preventing the foreignbanks from collecting an additional $1 million ofasserted appreciation in the patents underscoredthe limited nature of the banks’ interest in theupside of the partnership’s business. In light ofthose findings, the district court held that theChemtech partnerships should be disregarded fortax purposes under the sham partnership doctrine.

C. Bona Fide PartnersFinally, the district court held that the foreign

banks in Chemtech I were not true partners. In theopinion, this is phrased as a separate inquiry, al-though the ‘‘true partner’’ analysis was, in thedistrict court’s view, significant in reaching theconclusion that the partnership itself was a sham.39

Regarding whether the foreign banks in Chemtech Iwere bona fide partners, the district court relied onthe Second Circuit’s opinion in Castle Harbour II,40

stating that the inquiry of whether an interest is

35Culbertson, 337 U.S. at 742. The district court in Chemtechrejected Dow’s argument that the test in Moline Properties v.Commissioner, 319 U.S. 436 (1943), should apply. Under Dow’sinterpretation of the Moline Properties test, a partnership will berespected if it was formed for a business purpose or it actuallycarried on a business activity. The district court found that thetest as formulated by Dow conflicted with Fifth Circuit prec-edent. It added that the Moline Properties test is ‘‘a unitary testunder which ‘the existence of a formal business activity is agiven but the inquiry turns on the existence of a nontax businessmotive.’’’ Chemtech, slip op. at 55 (quoting ASA InvesteringsPartnership v. Commissioner, 201 F.3d 505, 512 (D.C. Cir. 2000)).

36Chemtech, slip op. at 54-55 (citing Merryman v. Commis-sioner, 873 F.2d 879, 881 (5th Cir. 1989)). In Merryman, thetaxpayer had an interest in a partnership formed by an oildrilling company, along with the company’s key officers andemployees. The company sold the partnership an oil rig forinstallment payments over seven years, with the companymanaging all aspects of the rig’s operation. Approximately sixmonths after executing the sale agreement, in a purportedsection 351 exchange, the partners transferred their partnershipinterests into a corporation they owned. The partnershipclaimed depreciation deductions and an investment tax creditfor the oil rig.

The Tax Court determined that although operation of the oilrig had economic substance and was entered into for profit, theformation and role of the partnership had no nontax purpose.The Fifth Circuit agreed that the partnership should be disre-garded for tax purposes because its formation and functionlacked economic purpose and profit motive. Some of the factsfound significant by the court were the sale of the oil rig to thepartnership on ‘‘exceedingly favorable terms’’ (no down pay-ment required, and the partnership waived all warranties), thecircular flow of funds among the parties without altering theireconomic positions, and the ‘‘pattern of interconnected owner-ship of [the partnership] and related entities.’’ See Merryman, 873F.2d at 882-883.

37Chemtech, slip op. at 56. As the district court stated in itssham partnership analysis, ‘‘selection of the partnership formmust have been driven by a genuine business purpose.’’ Id. at 54(quoting Southgate, 659 F.3d at 484).

38Chemtech, slip op. at 56-57 (comparing the circular flow offunds in the Chemtech transactions to the cash flow in Merry-man).

39See Chemtech, slip op. at 57 (‘‘A partner whose risks are allinsured at the expense of another partner ‘hardly fits within thetraditional notion of a partnership.’ A valid partnership is notformed where, among other things, one partner receives aguaranteed, specific return’’ (citations omitted).).

40TIFD III-E Inc. v. United States, 459 F.3d 220 (2d Cir. 2006).In Castle Harbour II, two Dutch banks formed a partnership withthe taxpayer, a U.S. corporation. The banks contributed cash tothe partnership, entitling them to a guaranteed return and apreferred return in addition to an annual return of principal.The taxpayer contributed cash and aircraft that had been fullydepreciated for tax purposes. The banks were allocated 98percent of the partnership’s taxable income or loss. However,the Second Circuit concluded that the banks realistically could(and did) receive only their fixed return because the amountthey would receive depended on the partnership’s book oper-ating income, which was much lower than its taxable income,given depreciation deductions taken on the aircraft for bookpurposes only. The banks were protected against losses becausetheir investment would not be at risk until the taxpayer’s

COMMENTARY / SPECIAL REPORT

(Footnote continued on next page.)

TAX NOTES, June 15, 2015 1291

For more Tax Notes content, please visit www.taxnotes.com.

(C) T

ax Analysts 2015. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

debt or equity is helpful in answering the bona fidepartnership interest question.41

The district court determined that the foreignbanks in Chemtech I, like the Dutch banks in theCastle Harbour transaction, had no meaningful riskof receiving less than their guaranteed return. Itobserved that ‘‘the only risk to the banks that posedany real threat was the IRS, which could seethrough the Chemtech scheme and pursue theforeign banks for taxes.’’42 And that risk was effec-tively nullified, the district court reasoned, becauseDow had agreed to indemnify the foreign banks ifthat situation arose.

Further, the district court determined that theforeign banks had no meaningful upside beyondtheir 7 percent priority return.43 By cross-referenceto the sham partnership portion of the opinion, thecourt again noted the steps taken by Dow to denythe foreign banks even their asserted 1 percentshare of the increased value of the patents.44

III. Fifth Circuit Decision

A. Dow and the Government State Their CasesDow began its appellate brief as follows:

Although the financial transactions underly-ing this case are complex, the legal questionspresented here are not. This appeal boils downto the unremarkable proposition that the taxlaws do not prevent companies from structur-ing transactions in a way that produces bothtax and non-tax benefits.45

The thrust of Dow’s appeal was that although taxconsequences were relevant, there were legitimatenontax business justifications for creating the

Chemtech partnerships. Dow thus maintained thatthe district court erred in all its holdings.46

Dow’s central argument regarding the shampartnership issue was that the Chemtech transac-tions gave it a significant nontax financial benefit —OBSF — that allowed it to raise money withoutincurring debt. Because that nontax benefit requiredthe use of a separate legal entity to hold Dow’sassets, the company was entitled to use the partner-ship form, Dow argued. It contended that thedistrict court ‘‘fundamentally misunderstood’’Dow’s business purpose for forming the Chemtechpartnerships and how those partnerships oper-ated.47

For instance, Dow argued that the business pur-pose in Chemtech I was not to maximize therevenue of the patents by licensing them to thirdparties but rather to monetize patents that wouldnot otherwise make a positive contribution toDow’s balance sheet, while at the same time pro-viding a ‘‘steady, but not guaranteed,’’ return to theforeign banks.48 Dow also challenged the districtcourt’s characterization of the flow of money ascircular, saying the 7 percent priority return to theforeign banks distinguished the situation from thatin Merryman (which the district court cited in itscircularity analysis) because in Merryman ‘‘moneyflowed back and forth but the economic position ofthe parties was not altered.’’49

Although Dow conceded that under the shampartnership doctrine, a taxpayer must be able todemonstrate that there was some nontax businesspurpose for its use of the partnership form,50 itargued that the Chemtech I and Chemtech II part-nerships met that standard because the financingDow obtained through the transactions required a

significant capital contribution was already lost. The govern-ment argued that the partnership was a sham and that theDutch banks’ interests were not bona fide equity interests.

The Second Circuit held that the Dutch banks were not bonafide partners. Unlike the district court (Castle Harbour I), it didnot reach the sham partnership issue. The Second Circuit notedthat a true partner must have meaningful participation in eitherthe upside (profits) or downside (risk of loss of capital) of thepartnership’s business. It found that the banks did not mean-ingfully participate in the partnership’s business because theirinterests were unaffected by the partnership’s performancegiven the taxpayer’s ability to limit the banks’ participation inthe profits to an insignificant amount.

41See Chemtech, slip op. at 58 (citing Castle Harbour II, 459 F.3dat 232).

42Chemtech, slip op. at 60.43Id. (‘‘Insofar as [there was] any ‘equity-like’ distribution, or

the possibility thereof, such a distribution was not meaningfulwhen compared to the [foreign banks’] guaranteed return on theinvestment.’’).

44See id. at 28-36.45Brief of Appellants, supra note 8, at 1.

46The Dow appeals brief also addressed the district court’seconomic substance holding and its determination that theforeign banks were not true partners. However, the Fifth Circuitdeclined to address those issues in its opinion, as discussed infrain Section III.B. On whether the foreign banks had a bona fideequity interest, Dow argued that the district court did notadequately perform a debt-equity analysis (which the SecondCircuit in Castle Harbour II determined was ‘‘helpful’’ for thebona fide partner inquiry) that was in line with Fifth Circuitprecedent in United States v. South Georgia Railway, 107 F.2d 3(5th Cir. 1939). In that case, the Fifth Circuit stated that the sinequa non of debt is the existence of a fixed maturity of a principalsum with the right to enforce payment in the event of default.Dow asserted that because the banks could have lost their entire$200 million capital contribution if the patents had lost theirvalue, the banks’ interests were not debt interests. Brief ofAppellants, supra note 8, at 49-62.

47Brief of Appellants, supra note 8, at 39.48Id. at 40.49Id. at 41-42 (quoting Merryman, 873 F.2d 879). For an

overview of Merryman, see supra note 36.50Citing Southgate, 659 F.3d at 479.

COMMENTARY / SPECIAL REPORT

1292 TAX NOTES, June 15, 2015

For more Tax Notes content, please visit www.taxnotes.com.

(C) T

ax Analysts 2015. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

separate business entity.51 Dow distinguished theChemtech partnerships from the partnership inSouthgate, partially on the grounds that theChemtech partners strictly adhered to the terms ofthe partnership agreement, whereas in Southgate theforeign partner effectively reneged on its obligationto service a portfolio of loans owned by the part-nership.52 Dow noted that unlike in Southgate, allthe parties in the Chemtech transactions respectedthe partnership form.

In its reply brief,53 the government argued thatthe district court was correct in determining that theChemtech partnerships were shams. The patentsand the chemical plant that were nominally ownedby the Chemtech partnerships were never reallyavailable for use in any partnership business, thegovernment asserted, pointing to the fact that thepartnerships’ sole source of income was the Dowroyalty payments (Chemtech I) and rental pay-ments (Chemtech II). Accordingly, the governmentcontended that the banks never saw themselves asmanaging the partnerships’ underlying assets or asoccupying a position from which they would profitfrom the partnerships’ asserted business purpose,which reflected the limited upside, non-equity na-ture of the banks’ interests. Similarly, the govern-ment maintained that the banks knew that theywere effectively insulated from risk because theywere protected from any tax or liability risk regard-ing the patents and they would receive their prior-ity return unless the patents or the plant decreasedsignificantly in value, an unlikely scenario.

The government asserted that Dow never an-swered the critical business purpose inquiry re-quired under Culbertson and Southgate:

Dow’s brief does not even address the criticalquestion of what business was being con-ducted by the Chemtech partnerships. Theanswer is supplied, however, by the record:none. Although Dow argues on appeal, as itdid below, that its purpose for forming theChemtech partnerships was to achieve [OBSF](an assertion the court rejected), that allegedpurpose still does not explain what businessthe partnerships were formed to conduct, and,

in fact, actually conducted. Dow’s assertionthat its purpose was to obtain [OBSF] onlybolsters the conclusion that the partnershipswere not intended to conduct any business.54

Thus, the government argued that even if Dowhad a business purpose for forming the partner-ships as separate entities (OBSF), the partnershipsthemselves were required to have a business pur-pose as well because the relevant test required allthe partners to act with a business purpose, not justone of them.55 The government claimed that theChemtech partnerships were merely vehiclesthrough which Dow could obtain tax benefits andthat the assets contributed to the partnerships ‘‘onlymattered insofar as their value secured the banks’contributions and generated tax deductions.’’56

Further, the government maintained that even ifthe partnerships engaged in a legitimate businessactivity, there was no real intent for Dow and thebanks to share in the profits and losses of thebusiness. Although the partnership agreements ontheir face gave the banks a share of the profits andlosses, their actual participation in the business wasnot meaningful, according to the government. Itasserted that similar to the Dutch banks in CastleHarbour, the banks in the Chemtech partnershipswere virtually guaranteed to receive a fixed returnon their investment. Because of the structure of theagreements and Dow’s active management andvaluation of the patents, the government argued,the banks were unlikely to receive anything signifi-cantly more or less than the guaranteed return,given the unlikelihood that the patents and chemi-cal plant would lose their value and given theindemnities and guarantees provided by Dow.57

B. Fifth Circuit Opinion

The Fifth Circuit released its opinion just over amonth after hearing oral arguments. The court ofappeals addressed only the sham partnership hold-ing, which it affirmed. It did not consider whetherthe district court erred in determining that thetransactions lacked economic substance or in clas-sifying the transactions as debt.

51Dow acknowledged that the separate business entity couldhave been formed as a corporation rather than a partnership. Itargued, however, that ‘‘the sham partnership doctrine does notrequire a taxpayer to justify why it elected to use a partnershipentity as opposed to a corporate entity’’ and that ‘‘a businessentity is free to choose its tax status for tax-motivated reasons.’’Brief of Appellants, supra note 8, at 44-45 (citation omitted).

52See Southgate, 659 F.3d at 475-476.53Government’s Combined Answering and Opening Brief,

Chemtech, 766 F.3d 453 (5th Cir. 2014) (No. 13-30887) (govern-ment’s brief).

54Id. at 44 (emphasis in original).55Id. at 40 (quoting Southgate, 659 F.3d at 483-484) (citing

Culbertson, 337 U.S. 733). The government further argued thattax benefits, not OBSF, were driving the Chemtech transactionsand that this fact (with which the district court agreed) furthersupported characterizing the Chemtech partnerships as shams.Id. at 53-57.

56Id. at 44.57The government argued that ‘‘Chemtech could only suffer

a loss through a series of highly unlikely and catastrophicevents: Dow declaring bankruptcy, and the patents and chemi-cal plant losing all of their value.’’ Id. at 51.

COMMENTARY / SPECIAL REPORT

TAX NOTES, June 15, 2015 1293

For more Tax Notes content, please visit www.taxnotes.com.

(C) T

ax Analysts 2015. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

Relying on Culbertson and Southgate, the FifthCircuit affirmed that a partnership is required tohave ‘‘(1) the intent to act in good faith for somegenuine business purpose and (2) the intent to bepartners, demonstrated by an intent to share ‘theprofits and losses.’’’58 Focusing on the second prongof that test, the Fifth Circuit concluded that theChemtech partnership was a sham.

In its analysis, the Fifth Circuit referenced CastleHarbour II even though in identifying meaningfulupside potential and downside risk in that case, theSecond Circuit focused on whether the Dutch bankswere bona fide partners, not on whether the part-nership itself was a sham.59 The Fifth Circuit tiedthe bona fide partner inquiry of Castle Harbour II tothe sham partnership test of Culbertson by notingthat a partnership requires, in addition to a businesspurpose, the partners’ intent to share the profits andlosses of the partnership’s business.

Before applying the Castle Harbour II approach toexamine the Chemtech transactions, the Fifth Cir-cuit rejected Dow’s argument that the banks’ inter-ests could not be classified as debt under debt-equity principles and that they were therefore bonafide equity interests in the partnership — whichDow argued necessarily led to the conclusion thatthe partnership itself was valid.60 The Fifth Circuitheld that a pure debt-equity analysis did not controlthe inquiry since Castle Harbour II had describedthat analysis as helpful but not necessary.61 Such anapproach, the Fifth Circuit stated, ran ‘‘afoul ofCulbertson and Southgate’’ and would elevate formover substance.62 In sum, the Fifth Circuit deter-mined that simply finding that the foreign banks’interests were not debt would be insufficient toreach the conclusion that the partnership was not asham.

The Fifth Circuit then listed three reasons sup-porting its holding that Dow and the foreign banksdid not truly intend to share in the profits andlosses of the Chemtech partnership. First, in the

court’s view, the banks’ annual priority return ontheir investment, independent of the partnership’ssuccess, did not suggest an intent to share profitsand losses. The Fifth Circuit characterized thechance of the banks receiving anything significantlymore or less than their fixed return as highlyunlikely because they would be compensated re-gardless of the partnership’s profitability.

Second, the Fifth Circuit determined that anyintent to share in the downside of the partnership’sactivities was negated by Dow bearing all signifi-cant risks arising from the Chemtech transactions.Here, the Fifth Circuit identified several ‘‘ironcladassurances’’ protecting the banks’ investment, suchas Dow’s agreement to indemnify them for anyliability arising from the patents and chemical plantand for any tax liability. Thus, the Fifth Circuitagreed with the district court that the banks facedeffectively no risk that they would lose their initialinvestment or not get their priority return.

Third, the Fifth Circuit found that the absence ofmeaningful upside potential for the foreign bankswas strong evidence that they did not intend toenter into a legitimate partnership with the Dowentities. Whether the foreign banks in Chemtech Iwould share in residual profits of the partnershipand receive anything beyond their priority returndepended on whether the patents increased invalue. The Fifth Circuit noted that (1) neither Downor the banks contended that they expected thepatents to increase in value; and (2) Dow did notargue that the Chemtech partnership was createdfor purposes of managing and profiting from thepatents. The Fifth Circuit said there was no way theparties could have intended to share in the profits ofChemtech I if the business of the partnership (man-aging the patents) was not expected to be profitable.

The Fifth Circuit expressed no opinion on thedistrict court’s imposition of the 20 percent penal-ties for negligence and substantial understatementunder section 6662(b)(1) and (2), but it instructedthe lower court generally to consider whether im-posing those penalties would be consistent with theappellate opinion. It also instructed the districtcourt to consider both the substantial valuation (20percent) and gross valuation (40 percent) misstate-ment penalties under section 6662(b)(3) and (h).63

58Chemtech, 766 F.3d at 461.59See Castle Harbour II, 459 F.3d at 231, n.11. The partnership

in Castle Harbour II was formed by two Dutch banks and a U.S.corporation. Given the Second Circuit’s holding that the Dutchbanks were not true partners under a bona fide partner inquiry,there was no partnership left and it therefore may have beenunnecessary for the court to reach a sham partnership inquiry.

60Chemtech, 766 F.3d at 462-463. Dow relied on South GeorgiaRailway, 107 F.2d 3, to argue that debt required (1) a fixedmaturity date requiring payment of a fixed amount, and (2) thelegal right of enforcement in case of default. Chemtech, 766 F.3dat 462. Dow reasoned that because the foreign banks’ invest-ment did not satisfy those requirements, their interests wereequity and the banks were thus valid partners. Id.

61See Castle Harbour II, 459 F.3d at 232.62Chemtech, 766 F.3d at 463.

63Id. at 465. Penalties under section 6662 are not stacked,even if more than one penalty applies. Thus, the significance ofthe Fifth Circuit’s instruction was to allow the imposition of a 40percent penalty as opposed to a 20 percent penalty. The FifthCircuit noted that the Supreme Court recently held in UnitedStates v. Woods, 134 S. Ct. 557, 566 (2013), that the valuationpenalty could apply even if the transaction were disallowedentirely.

COMMENTARY / SPECIAL REPORT

1294 TAX NOTES, June 15, 2015

For more Tax Notes content, please visit www.taxnotes.com.

(C) T

ax Analysts 2015. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

The district court, relying on Heasley,64 had con-cluded that it could not impose a valuation mis-statement penalty in cases in which the entiretransaction had been disregarded. The Fifth Circuitremanded the case on this point in light of theSupreme Court’s intervening opinion in Woods,65

which suggested that valuation misstatement pen-alties were potentially applicable.

On remand, the district court determined that itcould impose the substantial and gross valuationpenalties as a result of the Supreme Court decisionin Woods.66 The district court held that because theplant’s basis was increased from approximately $27million to more than $400 million in Chemtech II(exceeding the 400 percent threshold required un-der section 6662(h)(2)(A)(ii)(I)), the 40 percent grossvaluation penalty applied.67

C. Petition for Rehearing En Banc

On October 27, 2014, Dow filed a petition forrehearing en banc, presenting the issue as whether acourt may disregard a partnership as a sham for taxpurposes ‘‘based solely on the allocation of profitsand losses among its equity investors.’’68 Dow ar-gued that the appellate decision was inconsistentwith Culbertson, Fifth Circuit precedent, and deci-sions by other courts of appeals because it requiredthat ‘‘a partner’s return be risky or subject tosignificant variability’’ to satisfy Culbertson’s re-quirement that the partners come together to sharethe profits and losses of the partnership. Dow alsoasserted that the Fifth Circuit’s view of the ‘‘sharingof profits and losses’’ requirement would disruptestablished financing arrangements. On November17, 2014, the Fifth Circuit denied the petition.69

IV. Chemtech’s Significance

The district court struck down the Chemtechpartnerships broadly, determining that they werevoid under the economic substance, sham partner-ship, and bona fide partner doctrines. On the shampartnership doctrine, the district court concludedthat there was no genuine business purpose. Thecourt did not respect Dow’s asserted business pur-pose of obtaining OBSF, and it found that there wasno intent to share the partnership’s profits andlosses.

By contrast, the Fifth Circuit accomplished with ascalpel what the district court did with a sledge-hammer: It disregarded the Chemtech partnershipsbased solely on one prong of the sham partnershipdoctrine, concluding that Dow had no intent toshare either the profits or the losses of Chemtechwith the foreign banks.

The district court’s decision is nonetheless rel-evant to practitioners as an example of how ajudicial fact-finder may invoke the sham partner-ship, economic substance, and bona fide partnerdoctrines to disregard a partnership arrangement,particularly when it is a marketed transaction.Perhaps most significant to practitioners is thedistrict court’s application of its own judgmentregarding whether the taxpayer’s asserted businesspurpose in entering into the transaction could havebeen attained by ‘‘cheaper and less complex alter-natives.’’70 Practitioners therefore should be pre-pared to justify the profit potential of theirpartnership transactions while also being cognizantthat a large difference between potential or actualprofits and federal income tax benefits likely willinvite greater judicial scrutiny, a concept reaffirmedby the district court’s decision.71

The Fifth Circuit’s decision lays out importantprinciples regarding the sham partnership doctrine.Chemtech is particularly significant for future part-nership arrangements given the Fifth Circuit’s treat-ment of guarantees and preferred returns asimportant considerations when determiningwhether there are impermissible protections of apartner’s investment that will prevent a partnershipfrom being respected.

64Heasley v. Commissioner, 902 F.2d 380 (5th Cir. 1990).65See supra note 63.66See Chemtech Royalty Associates LP, supra note 27.67Id.68Petition for Rehearing En Banc at 4, Chemtech, 766 F.3d 453

(5th Cir. 2014) (No. 13-30887) (Oct. 27, 2014).69Denial of Petition for Rehearing En Banc, Chemtech, 766 F.3d

453 (5th Cir. 2014) (No. 13-30887) (Nov. 17, 2014).

70Chemtech, slip op. at 52. The district court scrutinizedDow’s asserted business purpose of obtaining OBSF by engag-ing in a business-type analysis. Despite Dow’s explanation of itsbusiness conditions at the time of the Chemtech transactionsand of the company’s need for a strong credit rating, the districtcourt found that the evidence did not show that Dow had acritical need for cash at that time, and did not ‘‘support theconclusion that Dow had a need for financial flexibility orcapital expenditures.’’ Id. at 39. Further, the district court notedthat ‘‘no evidence shows that Dow evaluated less costly alter-natives to the Chemtech transaction when, in fact, other formsof financing existed that would have allowed Dow to achieveOBSF.’’ Id. Critical to those findings, however, is the fact thatChemtech I was marketed by Goldman Sachs to Dow. See, e.g.,id. at 2-3, 40, and 51.

71In determining that under the subjective prong of theeconomic substance doctrine, Dow lacked a business purposefor entering into the Chemtech transactions, the district courtfound significant the difference between the transactions’ po-tential nontax benefits and tax benefits, stating that ‘‘if thepurported purpose of a transaction is to make a profit, courtsrequire that there be a reasonable possibility of profit that issubstantial in relation to the tax benefits generated.’’ Id. at 51(citing Nevada Partners Fund LLC v. United States, 714 F. Supp.2d598, 632 (S.D. Miss. 2010)); see supra Section II.A.

COMMENTARY / SPECIAL REPORT

TAX NOTES, June 15, 2015 1295

For more Tax Notes content, please visit www.taxnotes.com.

(C) T

ax Analysts 2015. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

Like the district court, the Fifth Circuit focusedon whether the upside and downside risk taken onby the foreign banks indicated an intent to share theprofits and losses of the partnership, as required bythe second prong of the sham partnership inquiry.72

Even though the Fifth Circuit did not directlyanalyze the business purpose requirement of thesham partnership doctrine, which was discussed bythe district court,73 it implied that having a partner-ship business purpose (as opposed to the individualbusiness purposes of the partners for using thepartnership form, such as OBSF) was a prerequisiteto meeting the meaningful participation require-ment because the parties had to intend to share theprofits of some joint enterprise.

In the Fifth Circuit’s view, meaningful participa-tion in the upside and downside of the partnershiprequires more than simple possession of an interestthat was not debt.74 The Fifth Circuit thus reaf-firmed that the relevant inquiry into whether thepartnership should be respected is controlled byCulbertson and its progeny, not by inquiries concern-ing whether an interest is bona fide debt for taxpurposes, even though a true debt interest wouldalways fail the Culbertson test in the Fifth Circuit’sview because the holder would lack the intent to bea partner of the obligor.75

In assessing Dow’s intent to be a partner with theforeign banks, the Fifth Circuit attached great sig-nificance to the guarantees offered by Dow, whichthe court had examined in determining whether thebanks had any meaningful risk in entering into thetransaction. Those guarantees, or ‘‘ironclad assur-ances’’ as the Fifth Circuit described them, in-cluded:

• the requirement that Chemtech maintain assetsequivalent to 3.5 times the foreign banks’ un-recovered capital contributions;

• the limitations on the types of assets Chemtechcould hold;

• the preference given to the foreign banks incase of liquidation of the partnership, whichpermitted the banks to receive their full invest-ment upon liquidation so long as the partner-ship had sufficient assets (which would bebacked by Dow’s guarantees); and

• Dow’s guarantees that its subsidiaries wouldperform their obligations as required by thecontrolling agreements.76

Despite the lack of a sinking fund or other moneyset aside to actually guarantee payment of theforeign banks’ priority return,77 the Fifth Circuitfound that Dow’s guarantees had the same effect:protecting the banks’ investments and insulatingthem from all the significant risks arising out of thetransaction. Further, the Fifth Circuit found impor-tant that the banks were entitled to a priority return,which in its view was independent of the partner-ship’s success because of the aforementioned pro-tections. Even though Dow itself could havebecome insolvent, which would have rendered itsguarantees meaningless, the Fifth Circuit did notconsider that possibility and thus essentially con-cluded that the Dow guarantees fully protected thebanks against any meaningful risk.

The Fifth Circuit’s determination that the foreignbanks had no meaningful upside was partiallybased on its view that Dow did not contend that thecontributed patents would increase in value be-cause, in the court’s words, ‘‘the parties could nothave intended to share profits through a means noone expected or designed to be profitable.’’78 TheFifth Circuit was apparently unimpressed by thebanks’ attempt to get more money from the increasein the patents’ value (that value did in fact in-crease).79 It simply said that the district court wasnot in error on this point because the foreign bankscollectively had only a 1 percent interest in thevalue increase, which was not enough to be mean-ingful. The Fifth Circuit found significant (1) thelack of assertion by Dow and the foreign banks thatthe patents were expected to increase in value, (2)

72The district court’s characterization of the transactionunder the sham partnership doctrine is a question of law subjectto de novo review, while ‘‘the particular facts from which thatcharacterization is made are reviewed for clear error.’’ Chemtech,766 F.3d at 460.

73The first prong under the sham partnership doctrine con-siders whether the parties had ‘‘the intent to act in good faith forsome genuine business purpose.’’ Id. at 461. The Fifth Circuitdid not evaluate that prong.

74As discussed supra in Section III.B, the Fifth Circuit rejectedDow’s argument that before applying the sham partnershipdoctrine under Culbertson, the court had to first determinewhether the banks’ interests qualified as debt or equity. SeeChemtech, 766 F.3d at 462-463. Instead, the Fifth Circuit believedthat there was no precedent requiring it to ‘‘find a validpartnership solely because the parties did not have a legal rightto demand repayment of their principal investment on any fixedfuture date,’’ which Dow argued was a feature of a debt interest.Id. at 462. And the court ultimately expressed no opinion onwhether the banks’ interests should be classified as debt.

75Id. at 463 (‘‘We limit our inquiry to whether Dow possessedthe intent to be partners with the foreign banks, focusing onwhether Dow had the intent to share the profits and losses withthe foreign banks.’’).

76See supra Section I.A.77In fact, ‘‘Dow did not [guarantee] the return of the [foreign

banks’] initial investment in Chemtech or the financial perfor-mance of the Partnership.’’ Plaintiff’s Pretrial Brief, supra note 2,Appendix I, at 4.

78Chemtech, 766 F.3d at 464.79Over the duration of Chemtech I, the patents increased in

value by $82 million (under Dow’s calculations). See supraSection I.A.

COMMENTARY / SPECIAL REPORT

1296 TAX NOTES, June 15, 2015

For more Tax Notes content, please visit www.taxnotes.com.

(C) T

ax Analysts 2015. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

Dow’s ability to remove patents that were profit-able, and (3) the foreign banks’ limited (1 percent)participation in any increase in the value of thepatents.

Accordingly, to the extent that a limited partner’sreturn is subject to protections or guarantees, theparties should consider how they will establish thatthe limited partner has a real risk of not receivingthe return. A court following Chemtech may not takeinto account the possibility that the guarantor couldbecome insolvent. Similarly, the parties should con-sider the limited partner’s share of any potentialupside beyond its priority return and how it wouldprove meaningful participation in that potentialupside. That analysis should take into account theother partners’ ability to control profitability by, forexample, removing the partnership assets they con-tributed. Unfortunately, the Fifth Circuit did notprovide clear guidance on how much downside riskor upside participation is required to rise to thelevel of meaningful, although it identified the for-eign banks’ 1 percent participation in the increase invalue of the patents as insufficient.

The Fifth Circuit’s reliance on authority regard-ing the bona fide partner inquiry for its holding thatChemtech was a sham partnership is also notewor-thy. Both Castle Harbour II and Historic Boardwalk80

applied the meaningful upside/downside test todetermine if an asserted interest in a partnershipwas in fact a partnership interest. The Fifth Circuitstated that ‘‘in Castle Harbour II, in conducting thesham-partnership inquiry, the Second Circuit con-sidered it helpful first to address whether an interesthas ‘the prevailing character of debt or equity.’’’81

However, in the section of the Castle Harbour IIopinion cited by the Fifth Circuit, the Second Circuitwas examining whether the Dutch banks’ ‘‘interestshould be deemed a bona fide equity participation in apartnership,’’ not whether the partnership itself wasa sham.82 Since the partnership in Castle Harbour IIhad only three partners (the two Dutch banks andthe U.S. corporation), the Second Circuit’s holdingthat the two Dutch banks were not legitimatepartners effectively disregarded the partnershipanyway (just as a sham partnership holding wouldhave); however, the two doctrines are typicallyframed as separate analyses, as the district court’sopinion in Chemtech demonstrates.

Following the Fifth Circuit’s decision in Chemtech,the principles of Castle Harbour II are relevant to both

inquiries. It is questionable how substantively dis-tinct the bona fide partner inquiry is from the shampartnership inquiry when both determinations relyon an analysis of a partner’s meaningful upside anddownside regarding its partnership interest. Onedifference is that while Castle Harbour II83 and His-toric Boardwalk84 provide that either meaningful up-side potential or meaningful downside risk wouldbe sufficient for an investor to be treated as a bonafide partner, Chemtech states that both are required tosurvive the sham partnership inquiry.85 That is inline with the Fifth Circuit’s sham partnership prec-edent in Southgate, which invoked the sham part-nership doctrine based in part on ‘‘the lack of intentto share profits and losses.’’86

V. ConclusionThe Fifth Circuit’s decision in Chemtech represents

the latest development of the sham partnership doc-trine. Case law will no doubt evolve in this area asthe IRS continues to challenge partnerships it be-lieves are motivated solely or primarily by federaltax benefits, regardless of whether those structuresare the product of marketed transactions. Practitio-ners should carefully consider the concepts andframework of the Chemtech decisions in evaluatingpotential judicial challenges to partnership struc-tures. The allocation of potential profits beyond aguaranteed or priority return (upside) and risks(downside) must be considered when forming part-nerships that involve priority returns, guarantees,and other protections against limited partners’ riskof loss. Although Chemtech does not provide specificbenchmarks for that inquiry, it gives practitioners anindication of the factors that the Fifth Circuit con-siders significant, which should be taken into ac-count when planning partnership transactions.

80Historic Boardwalk Hall LLC v. Commissioner, 694 F.3d 425(3d Cir. 2012).

81Chemtech, 766 F.3d at 462 (emphasis in original) (citingCastle Harbour II, 459 F.3d at 232).

82Castle Harbour II, 459 F.3d at 232 (emphasis added).

83Id. at 224 (‘‘While the government raises several argumentson appeal, we focus primarily on its contention that the Dutchbanks should not be treated as equity partners in the CastleHarbour partnership because they had no meaningful stake inthe success or failure of the partnership.’’); id. at 241 (‘‘Werecognize that if the Dutch banks had a sufficiently sizable sharein the profit potential of the partnership, they might appropri-ately be deemed equity participants for tax purposes, notwith-standing the guaranteed repayment of their initial investment atan agreed rate of return.’’).

84Historic Boardwalk, 694 F.3d at 463 (‘‘We conclude thatbecause [the investor] lacked a meaningful stake in either thesuccess or failure of [the partnership], it was not a bona fidepartner.’’).

85See Chemtech, 766 F.3d at 463 (‘‘In assessing whether thedistrict court erred in its sham-partnership holding . . . we limitour inquiry to whether Dow possessed the intent to be partnerswith the foreign banks, focusing on whether Dow had the intentto share the profits and losses with the foreign banks’’ (emphasisadded).).

86Southgate, 659 F.3d at 486 (emphasis added).

COMMENTARY / SPECIAL REPORT

TAX NOTES, June 15, 2015 1297

For more Tax Notes content, please visit www.taxnotes.com.

(C) T

ax Analysts 2015. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.