Embed Size (px)

Citation preview

Delivering transformational growthDelivering transformational growth

Charlie SartainChief ExecutiveChief Executive4 October 2012

1

Disclaimer

This document and the presentation are being made only to and directed only at (A) persons who have professional experience in matters relating to investments falling within Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (the “Order”) or (B) other persons to whom it may otherwise be lawfully communicated (each a “relevant person”). This presentation and its contents are confidential and may not be reproduced, redistributed or y ( p ) p y ppassed on, directly or indirectly, to any other person or published, in whole or in part, for any purpose without the written consent of Xstrata plc (“Xstrata”). This presentation does not constitute or form part of any offer or invitation to sell or issue, or any solicitation of any offer to purchase or subscribe for any securities, or a proposal to make a takeover bid in any jurisdiction. Neither this document nor the fact of its distribution nor the making of the presentation constitutes a recommendation regarding any securities. This presentation is being provided to you for information purposes only.Certain statements, beliefs and opinions contained in this presentation, particularly those regarding the possible or assumed future financial or other performance of Xstrata, industry growth or other trend projections are or may be forward looking statements. Forward-looking statements can be identified by the use of forward-looking terminology, including the terms “believes”, “estimates”, “anticipates”, “expects”, “intends”, “plans”, “goal”, “target”, “aim”, “may”, “will”, “would”, “could” or “should” or in each case their negative or other variations or comparable terminology These forward looking statements include all matters that are not could or should or, in each case, their negative or other variations or comparable terminology. These forward-looking statements include all matters that are not historical facts. By their nature, forward-looking statements involve risks and uncertainties because they relate to events and depend on circumstances that may or may not occur in the future and may be beyond Xstrata’s ability to control or predict. Forward-looking statements are not guarantees of future performance. No representation is made that any of these statements or forecasts will come to pass or that any forecast result will be achieved.Neither Xstrata, nor any of its associates or directors, officers or advisers, provides any representation, assurance or guarantee that the occurrence of the events expressed or implied in any forward-looking statements in this presentation will actually occur. You are cautioned not to place undue reliance on these forward-looking statements.Other than in accordance with its legal or regulatory obligations (including under the UK Listing Rules and the Disclosure and Transparency Rules g g y g g g p yof the Financial Services Authority), Xstrata is not under any obligation and Xstrata expressly disclaims any intention or obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.This presentation may contain references to “cost curves”. A cost curve is a graphic representation in which the total production volume of a given commodity across the relevant industry is arranged on the basis of average unit costs of production from lowest to highest to permit comparisons of the relative cost positions of particular production sites, individual producers or groups of producers across the world or within a given country or region. Generally, a producer’s position on a cost curve is described in terms of the particular percentile or quartile in which the production of a given plant or producer or group of producers appears. To construct cost curves, industry analysts compile information from a variety of sources, including reports made available by producers site visits personal contacts and trade publications. Although producers may participate to some extent in the process through which cost curves are by producers, site visits, personal contacts and trade publications. Although producers may participate to some extent in the process through which cost curves are constructed, they are typically unwilling to validate cost analyses directly because of commercial sensitivities. Inevitably, assumptions must be made by the analyst with respect to data that such analyst is unable to obtain and judgment must be brought to bear in the case of virtually all data, however obtained. Moreover, all cost curves embody a number of significant assumptions with respect to exchange rates and other variables. In summary, the manner in which cost curves are constructed means that they have a number of significant inherent limitations. Notwithstanding their shortcomings, independently produced cost curves are widely used in the industries in which Xstrata operate. No statement in this presentation is intended as a profit forecast or a profit estimate and no statement in this presentation should be interpreted to mean that earnings per Xstrata share for the current or future financial years would necessarily match or exceed the historical published earnings per Xstrata share.Th di ib i f hi i i f i i d i i b i d b l i i j i di i d i h i

2

The distribution of this presentation or any information contained in it may be restricted by law in certain jurisdictions, and any person into whose possession any document containing this presentation or any part of it comes should inform themselves about, and observe, any such restrictions.By attending the presentation and/or accepting or accessing this document you agree to be bound by the foregoing limitations and conditions and, in particular, will be taken to have represented, warranted and undertaken that you have read and agree to comply with the contents of this notice including, without limitation, the obligation to keep this document and its contents confidential and that you are a relevant person (as defined above).

The team presenting today

Charlie Sartain CEO

José Marún Executive General Manager South America Operations

Bob Drabik Executive General Manager Project Development, South America

M C b P j Di AMax Combes Project Director Antapaccay

Joseph Albright Project Director Las Bambas

3

Agenda

• Introduction

• Copper market update

• Xstrata Copper : delivering transformational growth

– North Queensland operations

– Antamina Joint Venture

• South American operations

Coffee break

• Project Development

• Antapaccay Project

• Las Bambas ProjectLas Bambas Project

• Wrap up

4

C k tCopper market

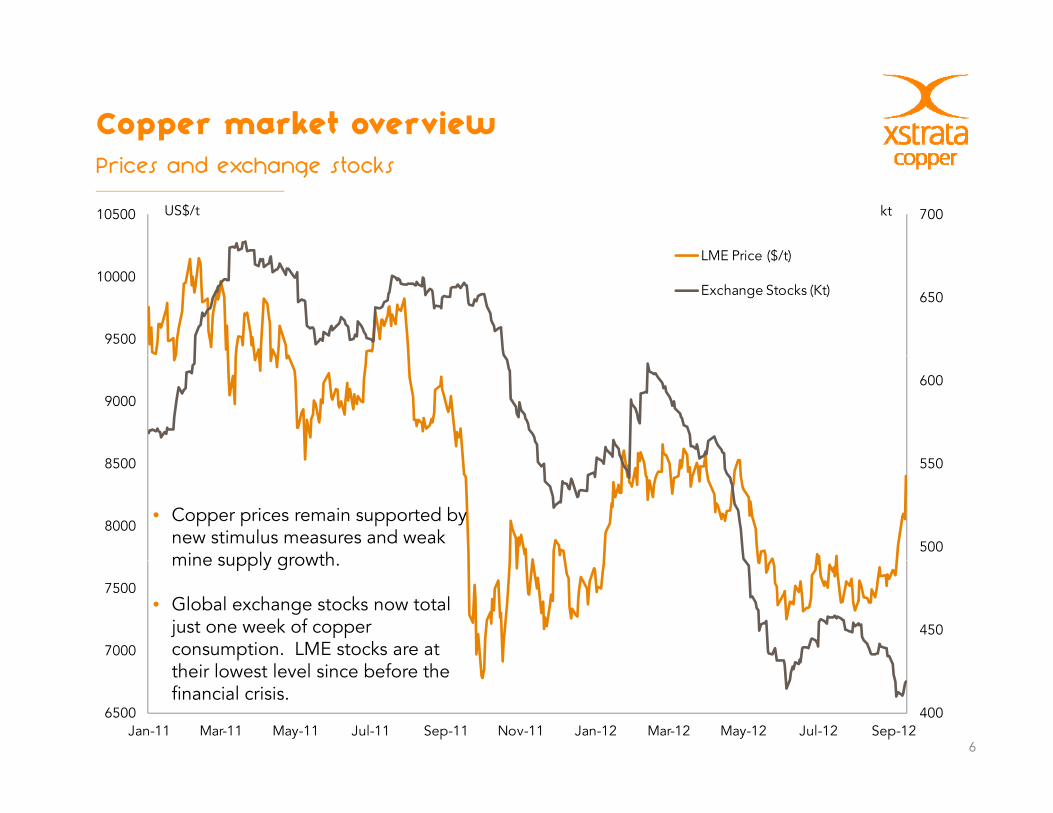

Copper market overviewPrices and exchange stocks

70010500

LME P i ($/t)

US$/t kt

650

9500

10000LME Price ($/t)

Exchange Stocks (Kt)

6009000

500

550

8000

8500

• Copper prices remain supported by new stimulus measures and weak mine supply growth

4507000

7500

mine supply growth.

• Global exchange stocks now total just one week of copper consumption. LME stocks are at

f

6

400Jan-11 Mar-11 May-11 Jul-11 Sep-11 Nov-11 Jan-12 Mar-12 May-12 Jul-12 Sep-12

6500

their lowest level since before the financial crisis.

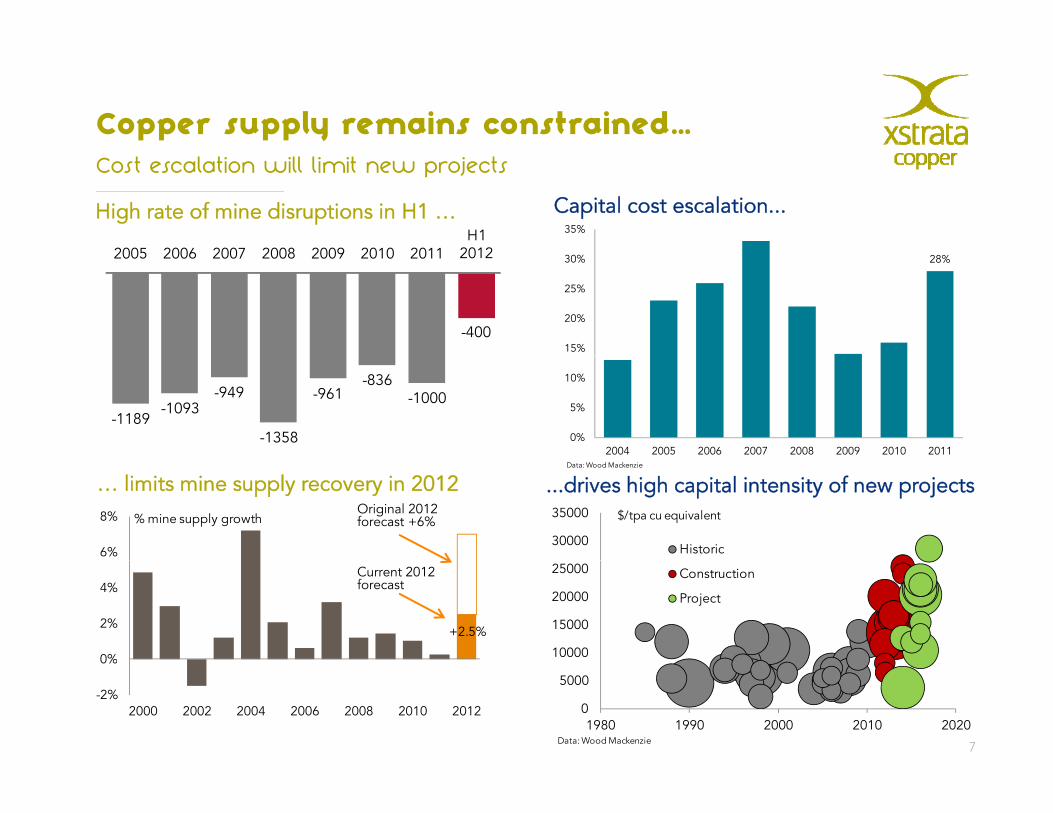

Copper supply remains constrained…

35%

Cost escalation will limit new projects

High rate of mine disruptions in H1 … Capital cost escalation...

2005 2006 2007 2008 2009 2010 2011H1

2012

15%

20%

25%

30% 28%

-400

2005 2006 2007 2008 2009 2010 2011 2012

0%

5%

10%

2004 2005 2006 2007 2008 2009 2010 2011

-1189-1093

-949

-1358

-961-836

-1000

6%

8% % mine supply growth

Data: Wood Mackenzie

… limits mine supply recovery in 2012 ...drives high capital intensity of new projects

30000

35000

Historic

$/tpa cu equivalentOriginal 2012 forecast +6%

0%

2%

4%

+2.5%

10000

15000

20000

25000 Construction

Project

Current 2012 forecast

-2%

0%

2000 2002 2004 2006 2008 2010 2012

7

0

5000

1980 1990 2000 2010 2020Data: Wood Mackenzie

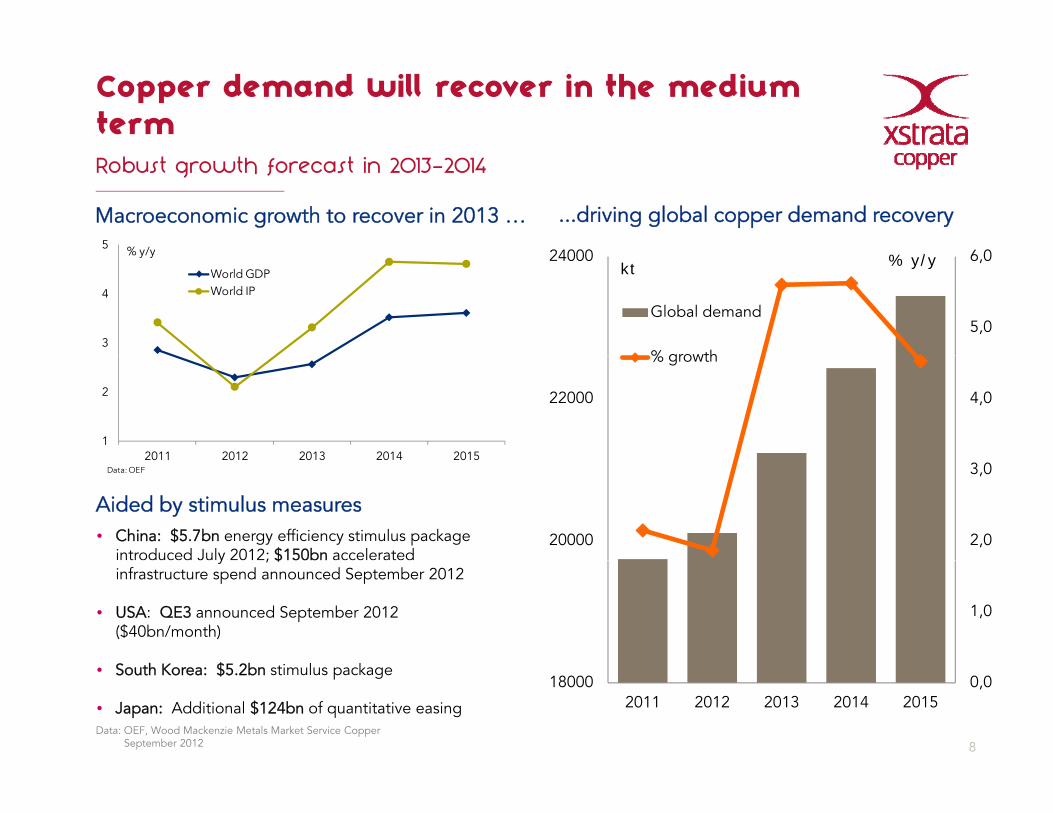

Copper demand will recover in the mediumtermRobust growth forecast in 2013-2014

Macroeconomic growth to recover in 2013 … ...driving global copper demand recovery5 % y/y 6 024000

3

4

World GDPWorld IP

% y/y

5,0

6,024000

Global demand

% growth

kt % y/y

1

2

2011 2012 2013 2014 2015

4,022000

% growth

Aided by stimulus measures• China: $5.7bn energy efficiency stimulus package

introduced July 2012; $150bn accelerated

2011 2012 2013 2014 2015Data: OEF

2,0

3,0

20000y ; $

infrastructure spend announced September 2012

• USA: QE3 announced September 2012 ($40bn/month)

h $ b l k

1,0

8Data: OEF, Wood Mackenzie Metals Market Service Copper

September 2012

• South Korea: $5.2bn stimulus package

• Japan: Additional $124bn of quantitative easing

0,0180002011 2012 2013 2014 2015

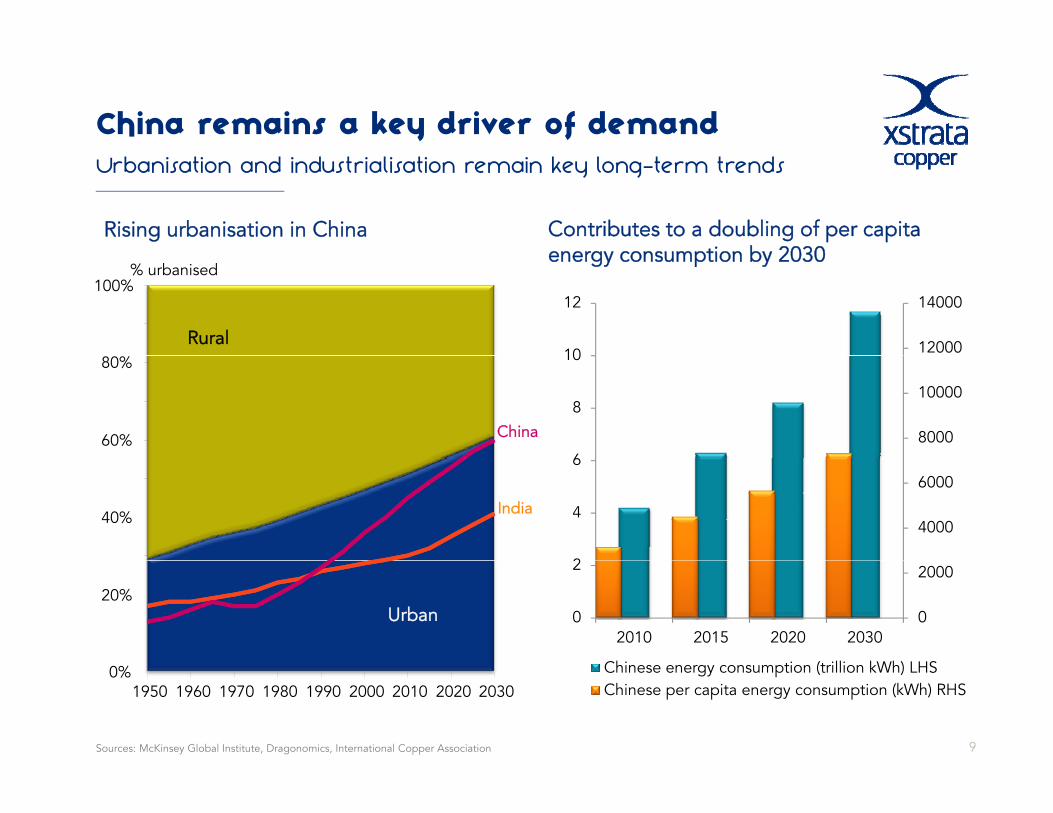

China remains a key driver of demandUrbanisation and industrialisation remain key long-term trends

Rising urbanisation in China Contributes to a doubling of per capita energy consumption by 2030

Rural

100%% urbanised

energy consumption by 2030

12000

14000

10

12

China60%

80%

8000

10000

6

8

10

India40% 4000

6000

2

4

6

Urban 20%

0

2000

0

2

2010 2015 2020 2030

Chi ti (t illi kWh) LHS

9Sources: McKinsey Global Institute, Dragonomics, International Copper Association

0%1950 1960 1970 1980 1990 2000 2010 2020 2030

Chinese energy consumption (trillion kWh) LHSChinese per capita energy consumption (kWh) RHS

Operating Operating excellenceexcellence

Strong geographically diverse portfolioF th l t d ith th 20 000 l Fourth largest copper producer with more than 20,000 employees, 15 assets and 7 major projects in eight countries

11

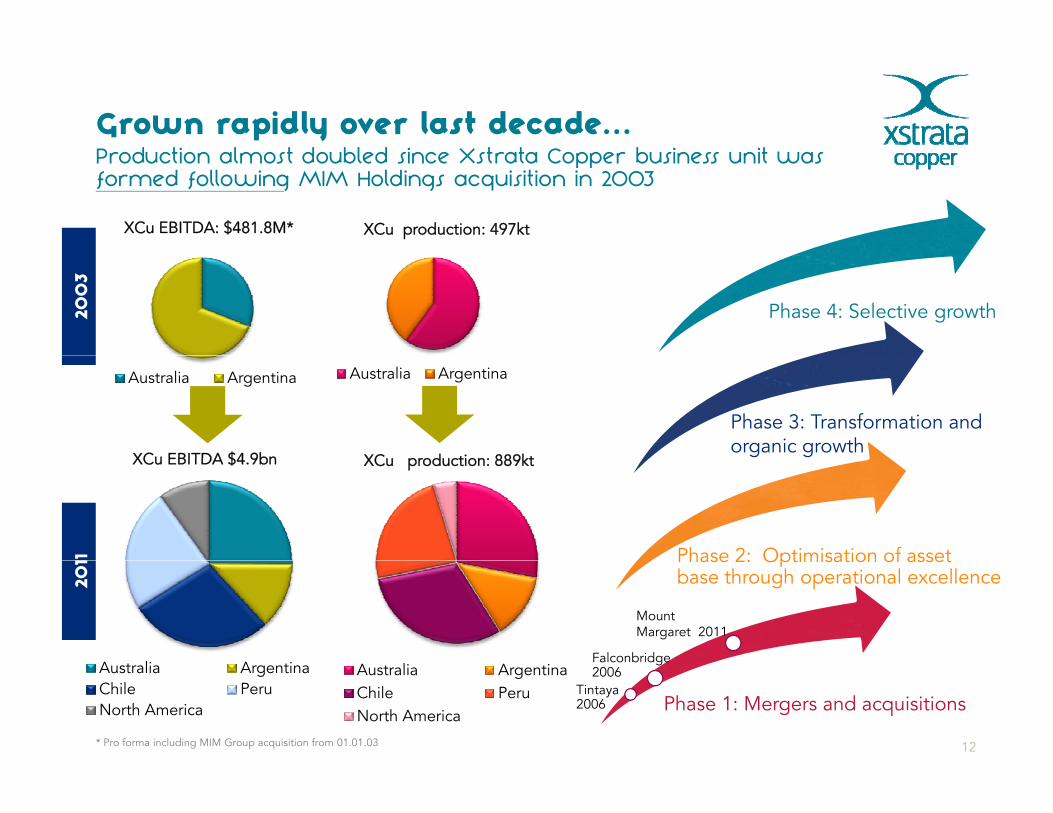

P d ti l t d bl d i X t t C b i it Grown rapidly over last decade... Production almost doubled since Xstrata Copper business unit was formed following MIM Holdings acquisition in 2003

XCu EBITDA: $481.8M* XCu production: 497kt

Phase 4: Selective growth 200

3

Phase 3: Transformation and organic growth

Australia Argentina

XCu EBITDA $4 9bn

Australia Argentina

XC d ti 889kt

Phase 2: Optimisation of asset 11

XCu EBITDA $4.9bn XCu production: 889kt

A li A i

Phase 2: Optimisation of asset base through operational excellence20

1

lFalconbridge

Mount Margaret 2011

Australia ArgentinaChile PeruNorth America

12* Pro forma including MIM Group acquisition from 01.01.03

Phase 1: Mergers and acquisitions

Australia ArgentinaChile PeruNorth America

Tintaya 2006

g2006

… to become the world’s fourth largest copperproducerStrong platform for further growth

• Top five global mined and refined copper producer with copper output of

Mined Copper Production (kt) in 2011

copper producer with copper output of 889,000 tonnes in 2011

• Diversified geographic exposure

b h d

889

• Robust cost position in the second quartile

• 2012 is a transformational year as oldermines are replaced by new lower cost

Codelco Freeport BHPB Xstrata Anglo

mines are replaced by new lower-costproduction from H2

• Projects under construction to further transform business and increase

2011 C1 Normal cash costs (c/lb)

Xstrata transform business and increase production by more than 50% to c.1.5Mtpa in 2015

• Future growth options provide

Xstrata Copper

13

significant optionality

0% 50% 100%

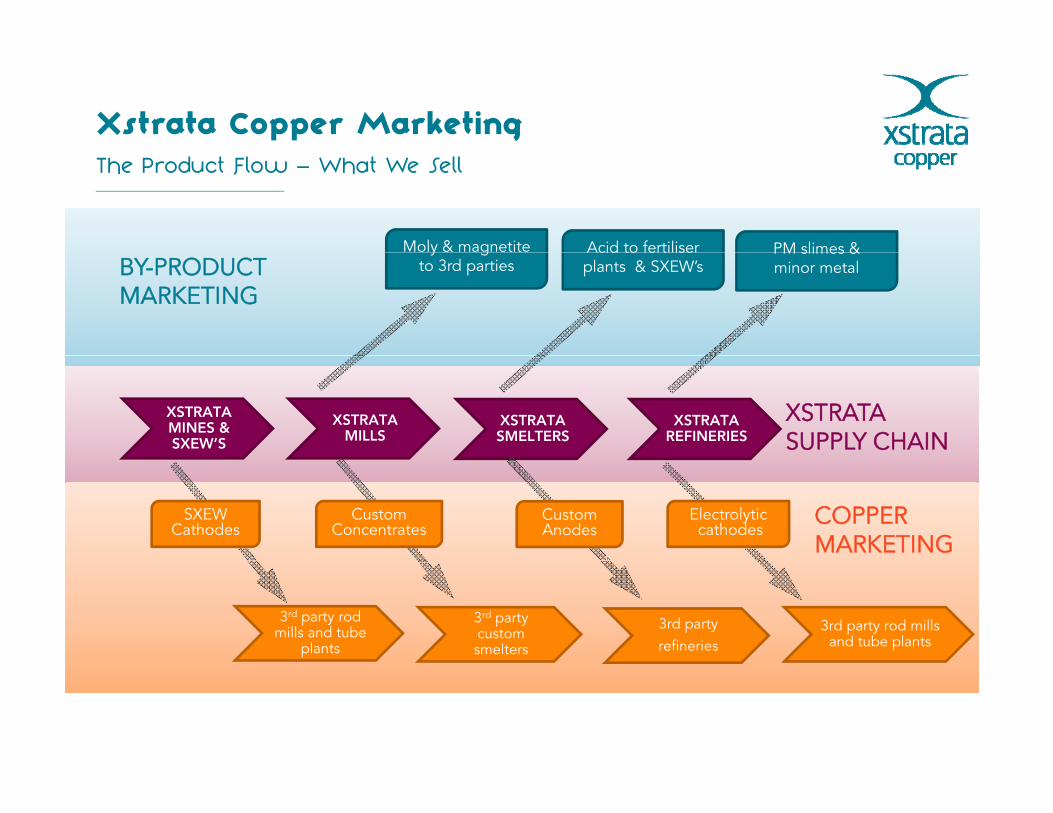

Xstrata Copper MarketingThe Product Flow – What We Sell

Acid to fertiliser Moly & magnetite PM slimes & plants & SXEW’s

y gto 3rd parties

PM slimes & minor metalBY-PRODUCT

MARKETING

XSTRATA MINES & SXEW’S

XSTRATA MILLS

XSTRATA SMELTERS

XSTRATA REFINERIES

XSTRATA SUPPLY CHAIN

CustomAnodes

CustomConcentrates

COPPER MARKETING

Electrolyticcathodes

SXEW Cathodes

3rd party custom smelters

3rd partyrefineries

3rd party rod mills and tube plants

3rd party rod mills and tube

plants

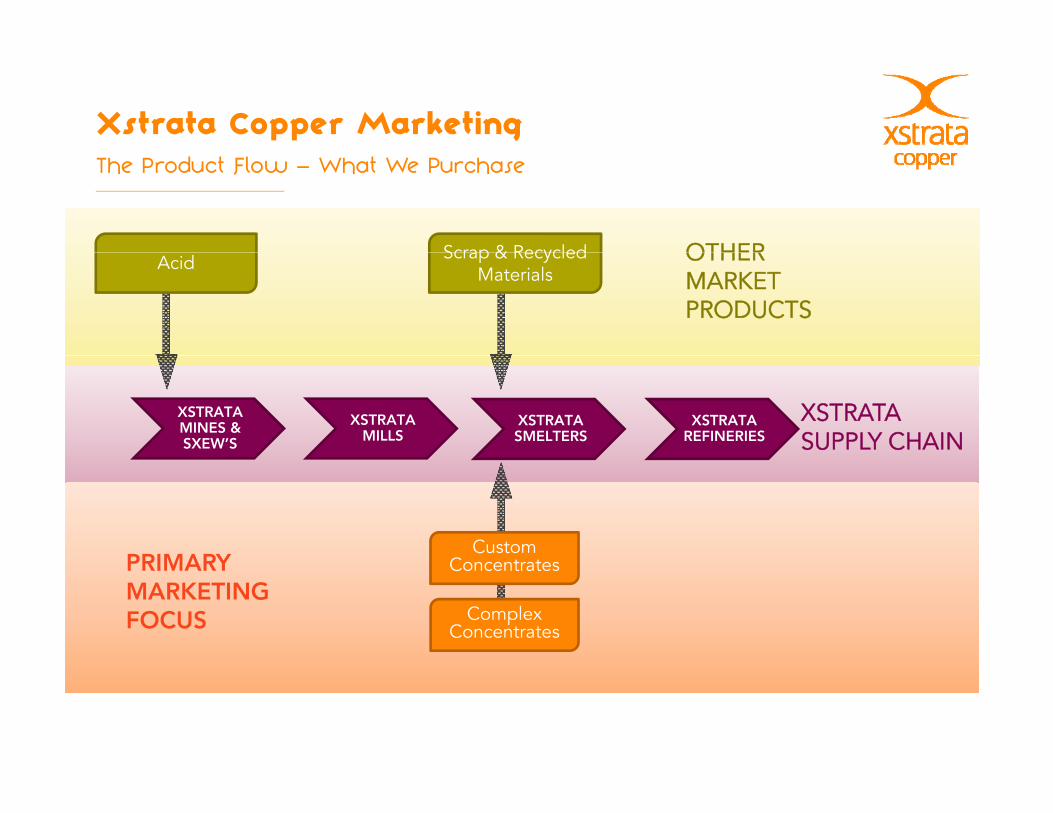

Xstrata Copper MarketingThe Product Flow – What We Purchase

Scrap & Recycled OTHER Scrap & Recycled Materials

Acid OTHER MARKET PRODUCTS

XSTRATA MINES & SXEW’S

XSTRATA MILLS

XSTRATA SMELTERS

XSTRATA REFINERIES

XSTRATA SUPPLY CHAIN

CustomC t tPRIMARY

Complex Concentrates

ConcentratesPRIMARY MARKETING FOCUS

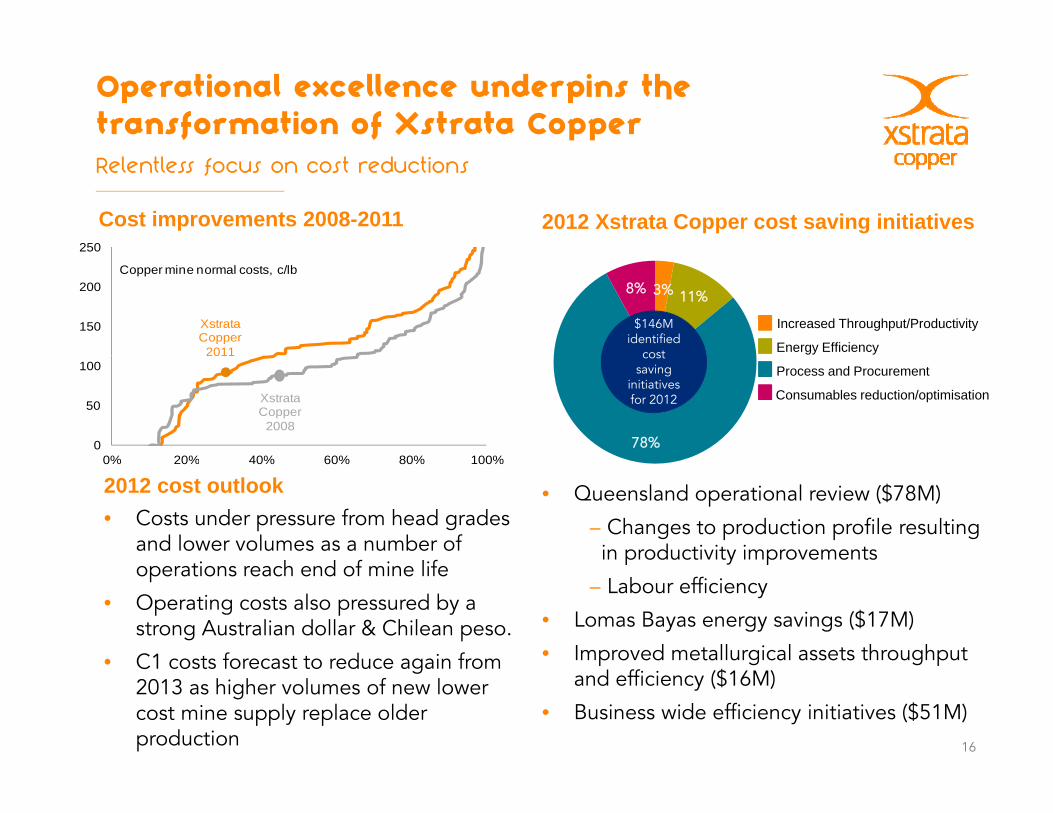

Operational excellence underpins the transformation of Xstrata CopperRelentless focus on cost reductions

2012 Xstrata Copper cost saving initiativesCost improvements 2008-2011250

3% 11%8%

$146M identified

cost

Increased Throughput/Productivity

Energy Efficiency150

200Copper mine normal costs, c/lb

XstrataCopper

2011

78%

cost saving

initiatives for 2012

Process and Procurement

Consumables reduction/optimisation

0

50

100

0% 20% 40% 60% 80% 100%

XstrataCopper

2008

2011

• Queensland operational review ($78M)

– Changes to production profile resulting in productivity improvements

2012 cost outlook • Costs under pressure from head grades

and lower volumes as a number of h d f l f

0% 20% 40% 60% 80% 100%

p y p

– Labour efficiency

• Lomas Bayas energy savings ($17M)

• Improved metallurgical assets throughput

operations reach end of mine life

• Operating costs also pressured by a strong Australian dollar & Chilean peso.

• C1 costs forecast to reduce again from

16

p g g pand efficiency ($16M)

• Business wide efficiency initiatives ($51M)

• C1 costs forecast to reduce again from 2013 as higher volumes of new lower cost mine supply replace older production

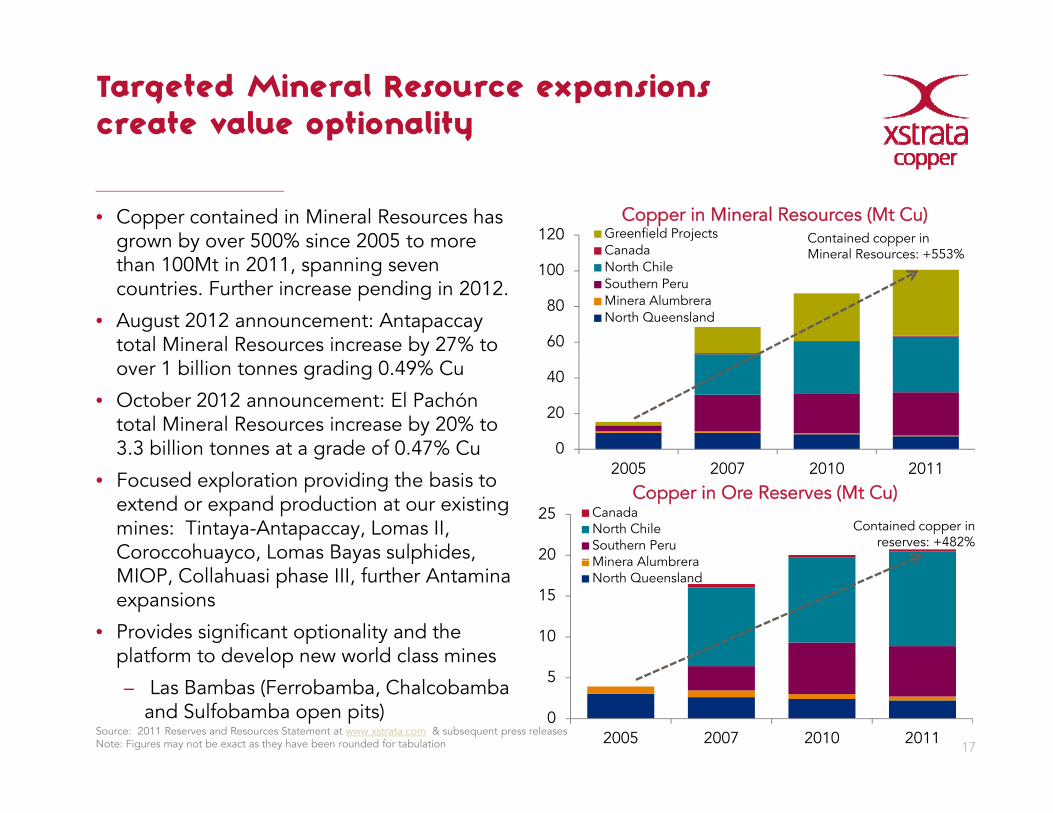

Targeted Mineral Resource expansionscreate value optionality

• Copper contained in Mineral Resources has grown by over 500% since 2005 to more

Copper in Mineral Resources (Mt Cu)120 Greenfield Projects

CanadaContained copper in Mineral Resources: +553%

than 100Mt in 2011, spanning seven countries. Further increase pending in 2012.

• August 2012 announcement: Antapaccay total Mineral Resources increase by 27% to 60

80

100CanadaNorth ChileSouthern PeruMinera AlumbreraNorth Queensland

Mineral Resources: +553%

yover 1 billion tonnes grading 0.49% Cu

• October 2012 announcement: El Pachóntotal Mineral Resources increase by 20% to 3.3 billion tonnes at a grade of 0.47% Cu 0

20

40

g

• Focused exploration providing the basis to extend or expand production at our existing mines: Tintaya-Antapaccay, Lomas II, Coroccohuayco, Lomas Bayas sulphides,

Copper in Ore Reserves (Mt Cu)

20

25 CanadaNorth ChileSouthern PeruMinera Alumbrera

Contained copper in reserves: +482%

2005 2007 2010 2011

y , y p ,MIOP, Collahuasi phase III, further Antamina expansions

• Provides significant optionality and the platform to develop new world class mines

10

15

Minera AlumbreraNorth Queensland

17

p p

– Las Bambas (Ferrobamba, Chalcobambaand Sulfobamba open pits)

Source: 2011 Reserves and Resources Statement at www.xstrata.com & subsequent press releasesNote: Figures may not be exact as they have been rounded for tabulation

0

5

2005 2007 2010 2011

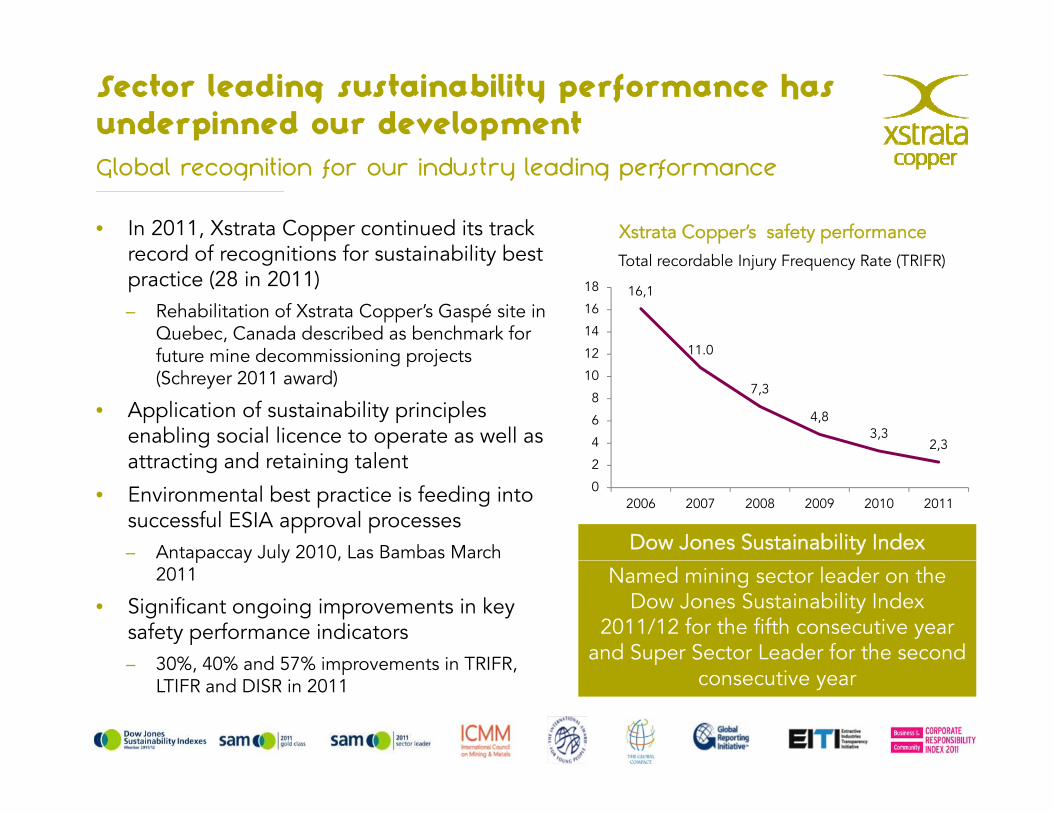

Sector leading sustainability performance has underpinned our development

• In 2011, Xstrata Copper continued its track record of recognitions for sustainability best

Global recognition for our industry leading performance

Xstrata Copper’s safety performancerecord of recognitions for sustainability best practice (28 in 2011)– Rehabilitation of Xstrata Copper’s Gaspé site in

Quebec, Canada described as benchmark for future mine decommissioning projects

Total recordable Injury Frequency Rate (TRIFR)

16,1

11.012

14

16

18

future mine decommissioning projects (Schreyer 2011 award)

• Application of sustainability principles enabling social licence to operate as well as attracting and retaining talent

7,3

4,83,3

2,34

6

8

10

12

attracting and retaining talent

• Environmental best practice is feeding into successful ESIA approval processes– Antapaccay July 2010, Las Bambas March Dow Jones Sustainability Index

0

2

2006 2007 2008 2009 2010 2011

p y y ,2011

• Significant ongoing improvements in key safety performance indicators

30% 40% and 57% improvements in TRIFR

Named mining sector leader on the Dow Jones Sustainability Index

2011/12 for the fifth consecutive year and Super Sector Leader for the second

18

– 30%, 40% and 57% improvements in TRIFR, LTIFR and DISR in 2011

pconsecutive year

DeliveringDeliveringt f ti ltransformational

growthg

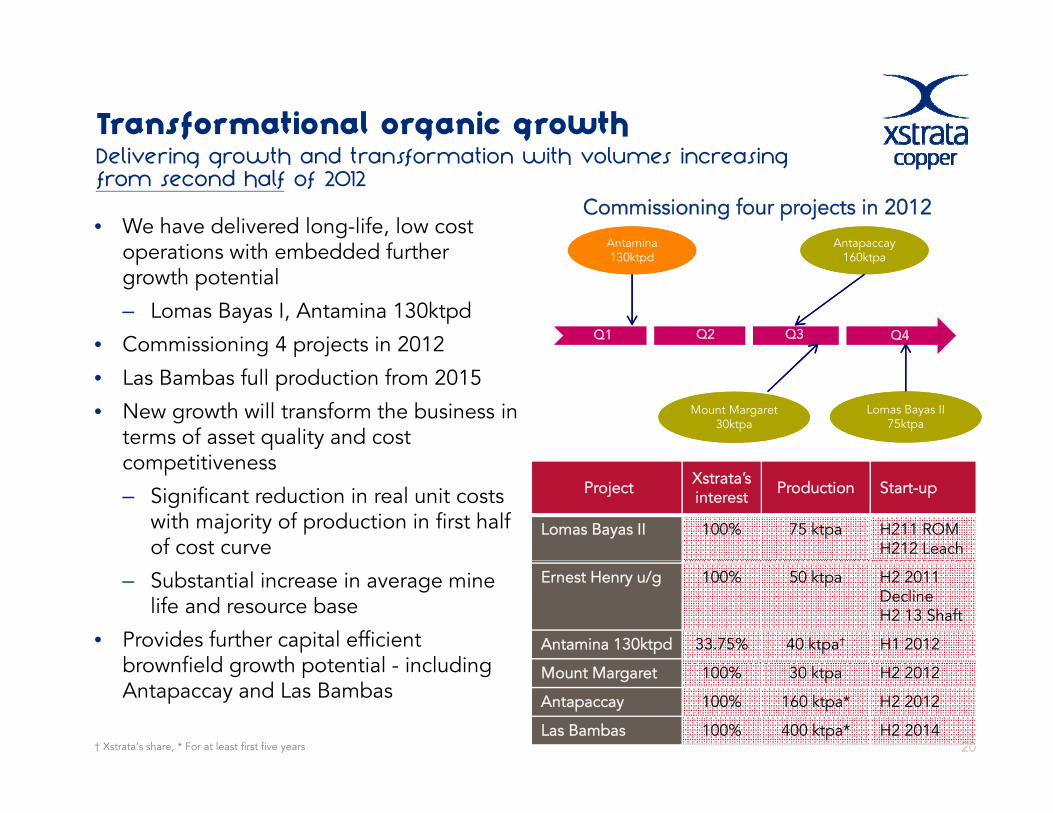

D li i th d t f ti ith l i i Transformational organic growth

• We have delivered long-life, low cost operations with embedded further

Delivering growth and transformation with volumes increasing from second half of 2012

Antapaccay160k

Antapaccay160k

Antamina 130k dAntamina 130k d

Commissioning four projects in 2012

operations with embedded further growth potential

– Lomas Bayas I, Antamina 130ktpd

• Commissioning 4 projects in 2012 Q1 Q2 Q3 Q4

160ktpa160ktpa130ktpd130ktpd

g p j

• Las Bambas full production from 2015

• New growth will transform the business in terms of asset quality and cost

titi

Lomas Bayas II 75ktpa

Lomas Bayas II 75ktpa

Mount Margaret30ktpa

Mount Margaret30ktpa

competitiveness

– Significant reduction in real unit costs with majority of production in first half of cost curve

Project Xstrata’sinterest Production Start-up

Lomas Bayas II 100% 75 ktpa H211 ROMH212 Leach

– Substantial increase in average mine life and resource base

• Provides further capital efficient brownfield growth potential including

Ernest Henry u/g 100% 50 ktpa H2 2011 DeclineH2 13 Shaft

Antamina 130ktpd 33.75% 40 ktpa† H1 2012brownfield growth potential - including Antapaccay and Las Bambas

20† Xstrata’s share, * For at least first five years

Mount Margaret 100% 30 ktpa H2 2012

Antapaccay 100% 160 ktpa* H2 2012

Las Bambas 100% 400 ktpa* H2 2014

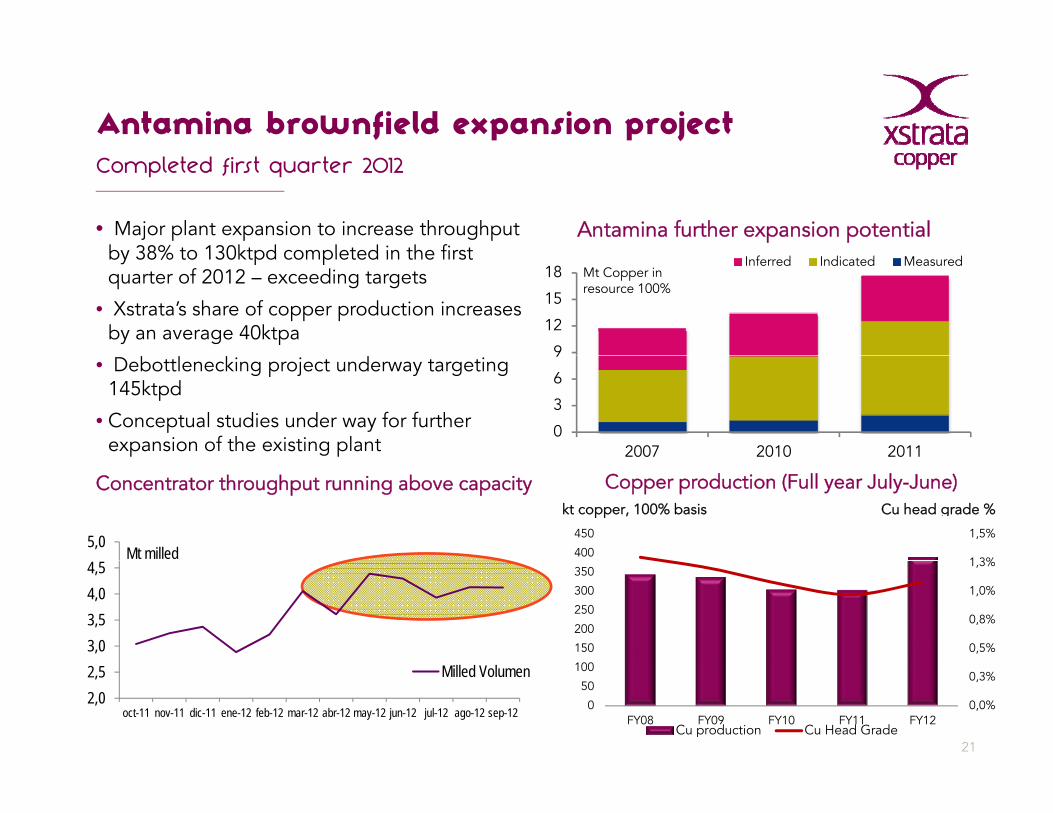

Antamina brownfield expansion projectCompleted first quarter 2012

• Major plant expansion to increase throughput by 38% to 130ktpd completed in the first

Antamina further expansion potential by 38% to 130ktpd completed in the first quarter of 2012 – exceeding targets

• Xstrata’s share of copper production increases by an average 40ktpa

9

12

15

18Inferred Indicated Measured

Mt Copper in resource 100%

• Debottlenecking project underway targeting 145ktpd

• Conceptual studies under way for further expansion of the existing plant

0

3

6

9

2007 2010 2011

Concentrator throughput running above capacity

5,0Mt milled

Copper production (Full year July-June)

1 3%

1,5%

400

450

kt copper, 100% basis Cu head grade %

3,03,54,04,5

0,5%

0,8%

1,0%

1,3%

100

150

200

250

300

350

21

2,02,5

oct-11 nov-11 dic-11 ene-12 feb-12 mar-12 abr-12 may-12 jun-12 jul-12 ago-12 sep-12

Milled Volumen

0,0%

0,3%

0

50

100

FY08 FY09 FY10 FY11 FY12Cu production Cu Head Grade

Antamina 130ktpd expansionRunning above nameplate capacity

Please do not use shadowing or 3D effects on photos or captions

Truck shop

22Ball mill 4 New conveyor beltElectrical control room

2

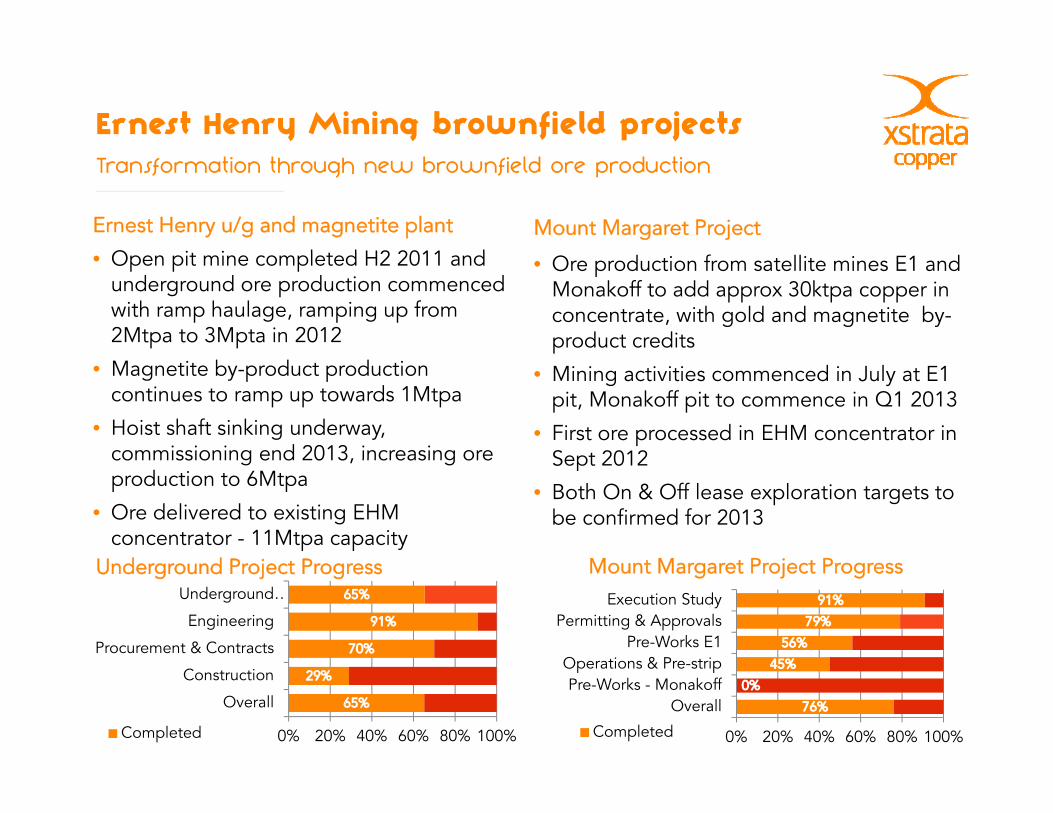

Ernest Henry Mining brownfield projects Transformation through new brownfield ore production

Ernest Henry u/g and magnetite plant

O it i l t d H2 2011 d Mount Margaret Project

• Open pit mine completed H2 2011 and underground ore production commenced with ramp haulage, ramping up from 2Mtpa to 3Mpta in 2012

• Ore production from satellite mines E1 and Monakoff to add approx 30ktpa copper in concentrate, with gold and magnetite by-product credits

• Magnetite by-product production continues to ramp up towards 1Mtpa

• Hoist shaft sinking underway, commissioning end 2013 increasing ore

• Mining activities commenced in July at E1 pit, Monakoff pit to commence in Q1 2013

• First ore processed in EHM concentrator in Sept 2012commissioning end 2013, increasing ore

production to 6Mtpa

• Ore delivered to existing EHM concentrator - 11Mtpa capacity

Sept 2012

• Both On & Off lease exploration targets to be confirmed for 2013

M t M t P j t PU d d P j P

Operations & Pre stripPre-Works E1

Permitting & ApprovalsExecution Study

Mount Margaret Project Progress

Procurement & Contracts

Engineering

Underground …

Underground Project Progress

0% 20% 40% 60% 80% 100%

OverallPre-Works - Monakoff

Operations & Pre-strip

Completed0% 20% 40% 60% 80% 100%

Overall

Construction

Completed

Ernest Henry undergroundShaft development in parallel with ramp u/g production

Please do not use shadowing or 3D effects on photos or captionsShaft Area – Preparing to lift Sheave DeckSheave Deck

24

Shaft SinkingUnderground Development Underground Pump Station

Mount Margaret Project Ore production and processing has commenced

Please do not use shadowing or 3D effects on photos

25

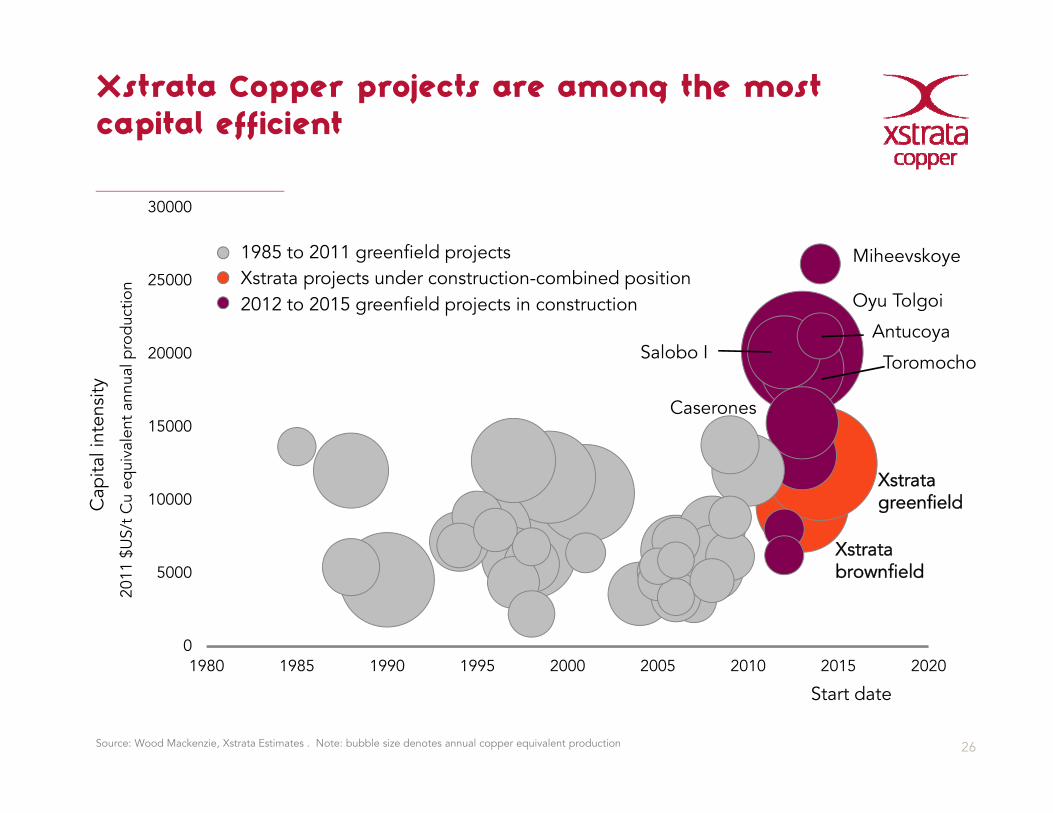

Xstrata Copper projects are among the most capital efficient

30000

Mih k1985 to 2011 greenfield projects

20000

25000Miheevskoye

prod

uctio

n

Salobo I

Oyu Tolgoi

T h

1985 to 2011 greenfield projects

2012 to 2015 greenfield projects in constructionXstrata projects under construction-combined position

Antucoya

15000

20000

l int

ensi

tyva

lent

ann

ual p Salobo I Toromocho

Caserones

10000

Xstrata

XstratagreenfieldC

apita

$U

S/t

Cu

equi

0

5000

1980 1985 1990 1995 2000 2005 2010 2015 2020

brownfield

2011

1980 1985 1990 1995 2000 2005 2010 2015 2020

26

Start date

Source: Wood Mackenzie, Xstrata Estimates . Note: bubble size denotes annual copper equivalent production

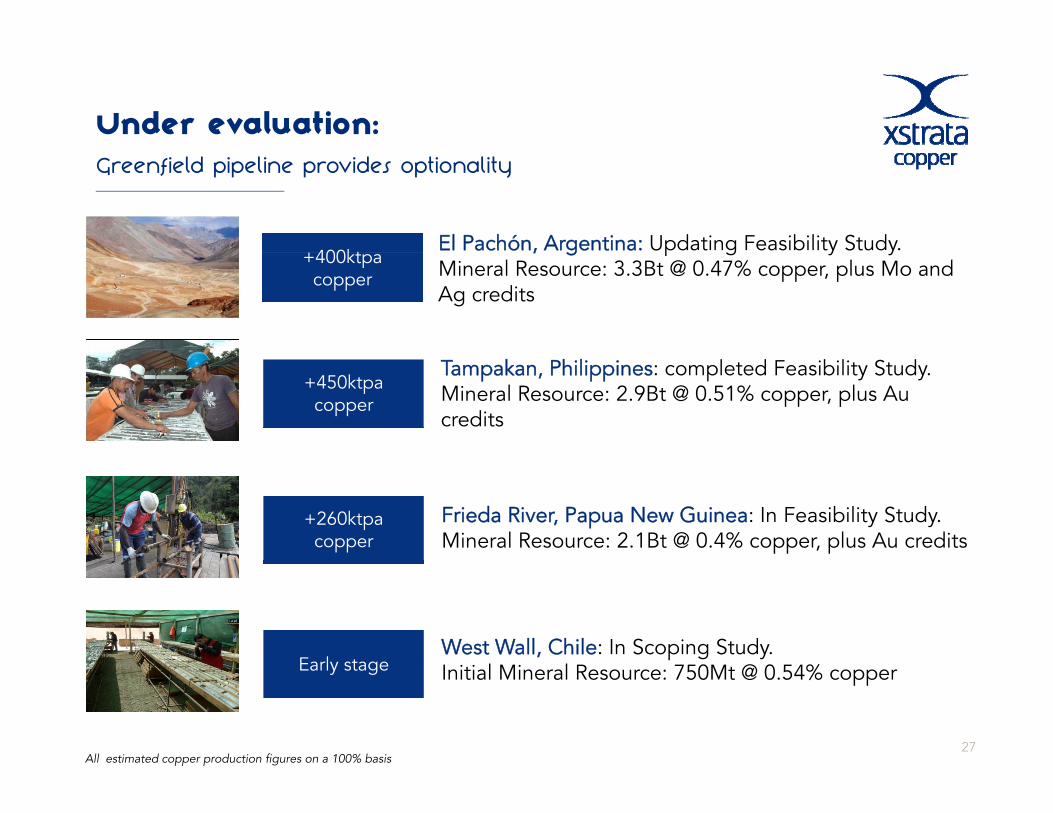

Under evaluation:Greenfield pipeline provides optionality

+400ktEl Pachón, Argentina: Updating Feasibility Study.

+400ktpacopper

, g p g y yMineral Resource: 3.3Bt @ 0.47% copper, plus Mo and Ag credits

+450ktpa copper

Tampakan, Philippines: completed Feasibility Study.Mineral Resource: 2.9Bt @ 0.51% copper, plus Au credits

+260ktpacopper

Frieda River, Papua New Guinea: In Feasibility Study. Mineral Resource: 2.1Bt @ 0.4% copper, plus Au credits

Early stage West Wall, Chile: In Scoping Study.

27

Early stage Initial Mineral Resource: 750Mt @ 0.54% copper

All estimated copper production figures on a 100% basis

Under evaluation:Brownfield pipeline provides value leverage

+300-500ktpaCopper

Collahuasi phase 3 expansion, Chile: In Pre-F ibili S d

+250ktpa

Copper Feasibility Study

Agua Rica, Argentina (MAA): In Feasibility Study

+50kt

copper

h ( ) b l d

g g y y

+50ktpa copper

Coroccohuayco , Peru (Tintaya): In Pre-Feasibility Study

+90ktpacopper

Lomas Bayas Sulphides, Chile: In Pre-Feasibility Study

28

Early stage Antamina expansion, Peru: In Scoping Study

All estimated copper production figures on a 100% basis

Conclusions

• 2012 is a transformational year for Xstrata Copper

f ld d b f ld h f h l f f l• Organic greenfield and brownfield growth transforms the quality of our asset portfolio in terms of volume and cost. By 2015:

– 50% copper growth

– More than 80% of production in the first half of the cost curve – More than 80% of production in the first half of the cost curve

• Growth timed for a cyclical recovery

• Strong platform to deliver further growth

– Las Bambas targeted to start commissioning end 2014Las Bambas targeted to start commissioning end 2014

– Further brownfield and greenfield optionality

29Tintaya concentrator Ernest Henry new underground

mine Horne Smelter recycling

Questions?Questions?

30