Embed Size (px)

Citation preview

Charitable Contributions, Endowments and

Inequality in Higher Education

Damien Capelle

Princeton University

1/28

Introduction

Donations and Endowments...

• ... are extremely unequally distributed across colleges

• ... are subject to special tax treatment

– Income tax deduction for charitable contributions

– Endowments are tax exempt

• ... (increasingly) attracts a lot of public attention

– Tax avoidance for the wealthy

– Income tax deduction is a regressive subsidy

– Strong positive correlation between average parental income of students and

amount of donations/endowment income ⇒ Very local redistribution

– Adversely affects hiring incentives and behaviors of colleges: legacy, sports

– Inefficient hoarding of endowment

2/28

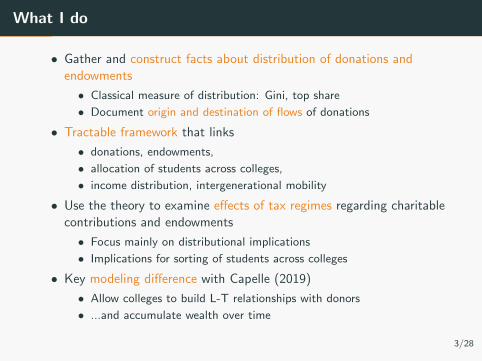

What I do

• Gather and construct facts about distribution of donations and

endowments

• Classical measure of distribution: Gini, top share

• Document origin and destination of flows of donations

• Tractable framework that links

• donations, endowments,

• allocation of students across colleges,

• income distribution, intergenerational mobility

• Use the theory to examine effects of tax regimes regarding charitable

contributions and endowments

• Focus mainly on distributional implications

• Implications for sorting of students across colleges

• Key modeling difference with Capelle (2019)

• Allow colleges to build L-T relationships with donors

• ...and accumulate wealth over time

3/28

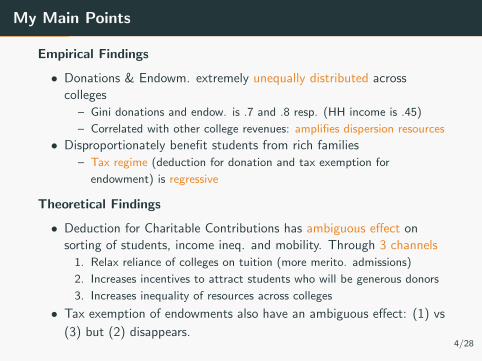

My Main Points

Empirical Findings

• Donations & Endowm. extremely unequally distributed across

colleges

– Gini donations and endow. is .7 and .8 resp. (HH income is .45)

– Correlated with other college revenues: amplifies dispersion resources

• Disproportionately benefit students from rich families

– Tax regime (deduction for donation and tax exemption for

endowment) is regressive

Theoretical Findings

• Deduction for Charitable Contributions has ambiguous effect on

sorting of students, income ineq. and mobility. Through 3 channels

1. Relax reliance of colleges on tuition (more merito. admissions)

2. Increases incentives to attract students who will be generous donors

3. Increases inequality of resources across colleges

• Tax exemption of endowments also have an ambiguous effect: (1) vs

(3) but (2) disappears.4/28

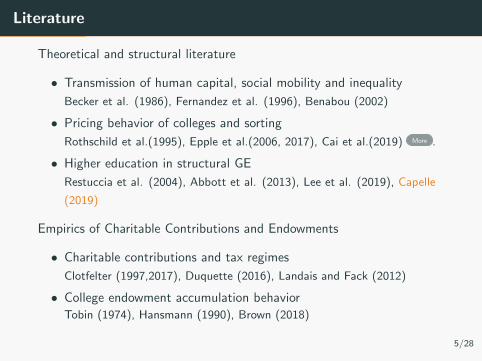

Literature

Theoretical and structural literature

• Transmission of human capital, social mobility and inequality

Becker et al. (1986), Fernandez et al. (1996), Benabou (2002)

• Pricing behavior of colleges and sorting

Rothschild et al.(1995), Epple et al.(2006, 2017), Cai et al.(2019) More .

• Higher education in structural GE

Restuccia et al. (2004), Abbott et al. (2013), Lee et al. (2019), Capelle

(2019)

Empirics of Charitable Contributions and Endowments

• Charitable contributions and tax regimes

Clotfelter (1997,2017), Duquette (2016), Landais and Fack (2012)

• College endowment accumulation behavior

Tobin (1974), Hansmann (1990), Brown (2018)

5/28

Table of Contents

Introduction

Stylized Facts

The Model

Extension with Endowment

Quantitative Analysis (skip today)

Conclusion

6/28

Stylized Facts

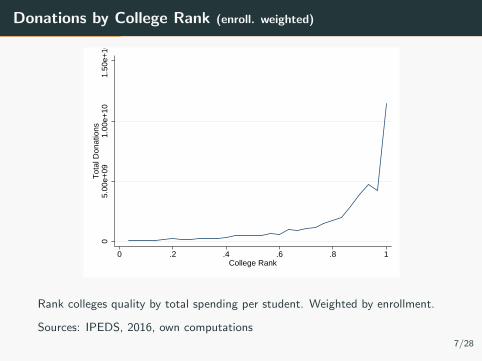

Donations by College Rank (enroll. weighted)

05.

00e+

091.

00e+

101.

50e+

10T

otal

Don

atio

ns

0 .2 .4 .6 .8 1College Rank

Rank colleges quality by total spending per student. Weighted by enrollment.

Sources: IPEDS, 2016, own computations

7/28

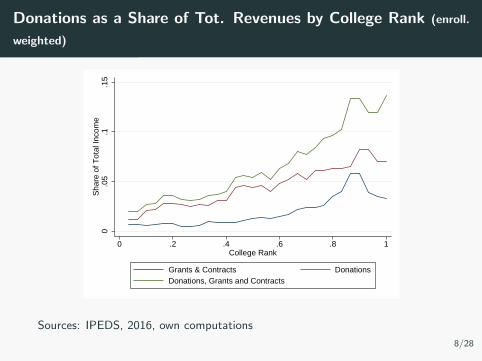

Donations as a Share of Tot. Revenues by College Rank (enroll.

weighted)

0.0

5.1

.15

Sha

re o

f Tot

al In

com

e

0 .2 .4 .6 .8 1College Rank

Grants & Contracts DonationsDonations, Grants and Contracts

Sources: IPEDS, 2016, own computations

8/28

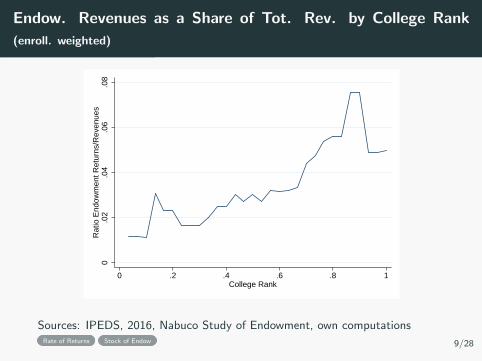

Endow. Revenues as a Share of Tot. Rev. by College Rank

(enroll. weighted)

0.0

2.0

4.0

6.0

8R

atio

End

owm

ent R

etur

ns/R

even

ues

0 .2 .4 .6 .8 1College Rank

Sources: IPEDS, 2016, Nabuco Study of Endowment, own computationsRate of Returns Stock of Endow 9/28

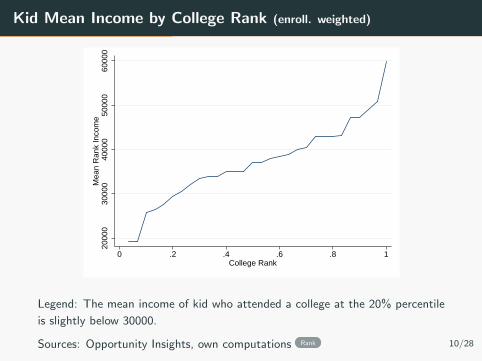

Kid Mean Income by College Rank (enroll. weighted)

2000

030

000

4000

050

000

6000

0M

ean

Ran

k In

com

e

0 .2 .4 .6 .8 1College Rank

Legend: The mean income of kid who attended a college at the 20% percentile

is slightly below 30000.

Sources: Opportunity Insights, own computations Rank 10/28

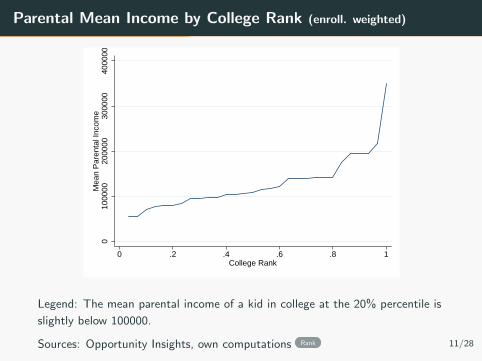

Parental Mean Income by College Rank (enroll. weighted)

010

0000

2000

0030

0000

4000

00M

ean

Par

enta

l Inc

ome

0 .2 .4 .6 .8 1College Rank

Legend: The mean parental income of a kid in college at the 20% percentile is

slightly below 100000.

Sources: Opportunity Insights, own computations Rank 11/28

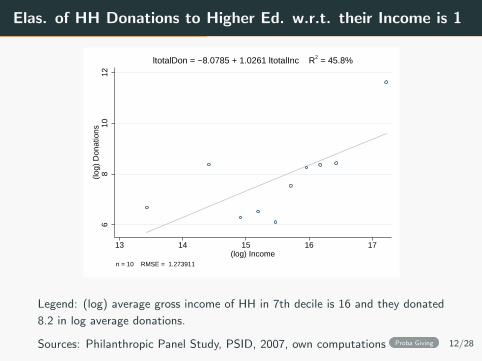

Elas. of HH Donations to Higher Ed. w.r.t. their Income is 1

68

1012

(log)

Don

atio

ns

13 14 15 16 17(log) Income

n = 10 RMSE = 1.273911

ltotalDon = −8.0785 + 1.0261 ltotalInc R2 = 45.8%

Legend: (log) average gross income of HH in 7th decile is 16 and they donated

8.2 in log average donations.

Sources: Philanthropic Panel Study, PSID, 2007, own computations Proba Giving 12/28

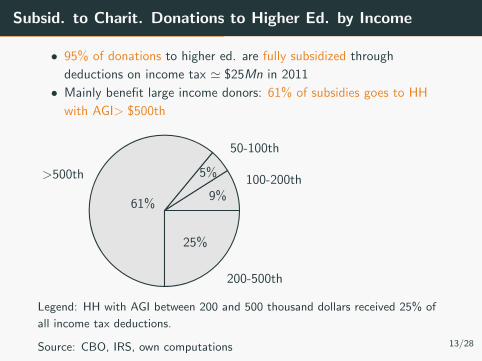

Subsid. to Charit. Donations to Higher Ed. by Income

• 95% of donations to higher ed. are fully subsidized through

deductions on income tax ' $25Mn in 2011

• Mainly benefit large income donors: 61% of subsidies goes to HH

with AGI> $500th

100-200th9%

50-100th

5%>500th

61%

200-500th

25%

Legend: HH with AGI between 200 and 500 thousand dollars received 25% of

all income tax deductions.

Source: CBO, IRS, own computations 13/28

The Model

The Model

Outline

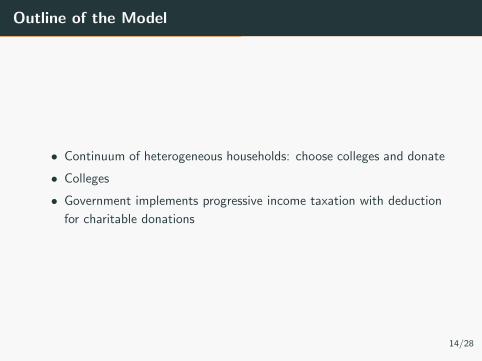

Outline of the Model

• Continuum of heterogeneous households: choose colleges and donate

• Colleges

• Government implements progressive income taxation with deduction

for charitable donations

14/28

The Model

Households

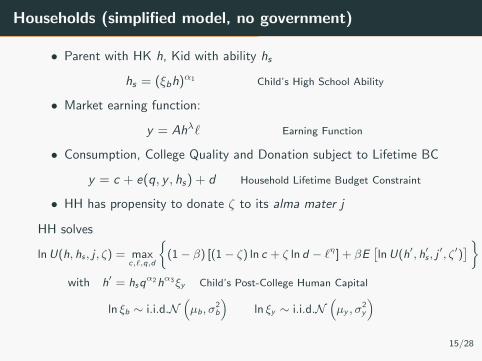

Households (simplified model, no government)

• Parent with HK h, Kid with ability hs

hs = (ξbh)α1 Child’s High School Ability

• Market earning function:

y = Ahλ` Earning Function

• Consumption, College Quality and Donation subject to Lifetime BC

y = c + e(q, y , hs) + d Household Lifetime Budget Constraint

• HH has propensity to donate ζ to its alma mater j

HH solves

lnU(h, hs , j , ζ) = maxc,`,q,d

{(1− β) [(1− ζ) ln c + ζ ln d − `η] + βE

[lnU(h′, h′s , j

′, ζ′)]}

with h′ = hsqα2hα3ξy Child’s Post-College Human Capital

ln ξb ∼ i.i.d.N(µb, σ

2b

)ln ξy ∼ i.i.d.N

(µy , σ

2y

)15/28

The Model

Colleges

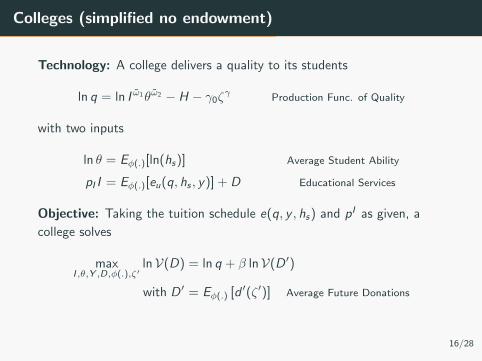

Colleges (simplified no endowment)

Technology: A college delivers a quality to its students

ln q = ln I ω̃1θω̃2 − H − γ0ζγ

Production Func. of Quality

with two inputs

ln θ = Eφ(.)[ln(hs)] Average Student Ability

pI I = Eφ(.)[eu(q, hs , y)] + D Educational Services

Objective: Taking the tuition schedule e(q, y , hs) and pI as given, a

college solves

maxI ,θ,Y ,D,φ(.),ζ′

lnV(D) = ln q + β lnV(D ′)

with D ′ = Eφ(.) [d ′(ζ ′)] Average Future Donations

16/28

The Model

Government

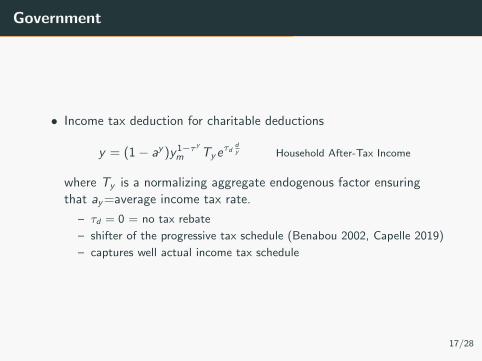

Government

• Income tax deduction for charitable deductions

y = (1− ay )y1−τ y

m Tyeτd

dy Household After-Tax Income

where Ty is a normalizing aggregate endogenous factor ensuring

that ay=average income tax rate.

– τd = 0 = no tax rebate

– shifter of the progressive tax schedule (Benabou 2002, Capelle 2019)

– captures well actual income tax schedule

17/28

The Model

Equilibrium: Tuition Schedule, Sorting Rule and

Law of Motion

Restrictions

– Steady-state

– Distribution of HK is log-normal

– Colleges are indifferent between all student types (interior F.O.C.)

18/28

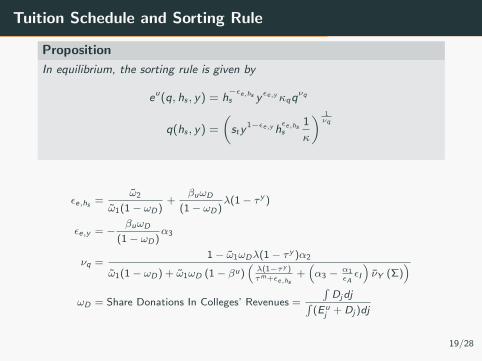

Tuition Schedule and Sorting Rule

Proposition

In equilibrium, the sorting rule is given by

eu(q, hs , y) = h−εe,hss y εe,yκqq

νq

q(hs , y) =

(sty

1−εe,y hεe,hss

1

κ

) 1νq

εe,hs =ω̃2

ω̃1(1 − ωD)+

βuωD

(1 − ωD)λ(1 − τ y )

εe,y = −βuωD

(1 − ωD)α3

νq =1 − ω̃1ωDλ(1 − τ y )α2

ω̃1(1 − ωD) + ω̃1ωD (1 − βu)(λ(1−τy )τm+εe,hs

+(α3 − α1

εAεI

)ν̄Y (Σ)

)ωD = Share Donations In Colleges’ Revenues =

∫Djdj∫

(Euj + Dj )dj

19/28

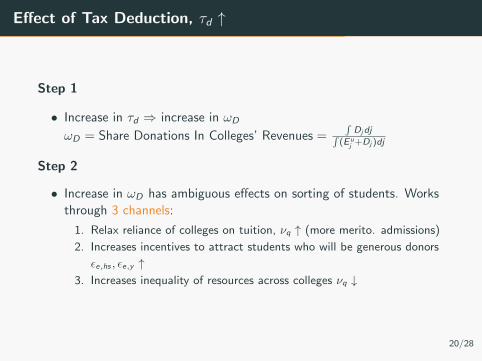

Effect of Tax Deduction, τd ↑

Step 1

• Increase in τd ⇒ increase in ωD

ωD = Share Donations In Colleges’ Revenues =∫Djdj∫

(E uj +Dj )dj

Step 2

• Increase in ωD has ambiguous effects on sorting of students. Works

through 3 channels:

1. Relax reliance of colleges on tuition, νq ↑ (more merito. admissions)

2. Increases incentives to attract students who will be generous donors

εe,hs , εe,y ↑3. Increases inequality of resources across colleges νq ↓

20/28

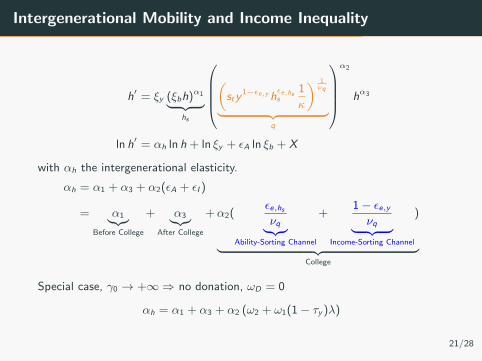

Intergenerational Mobility and Income Inequality

h′ = ξy (ξbh)α1︸ ︷︷ ︸hs

(sty

1−εe,y hεe,hss

1

κ

) 1νq

︸ ︷︷ ︸q

α2

hα3

ln h′ = αh ln h + ln ξy + εA ln ξb + X

with αh the intergenerational elasticity.

αh = α1 + α3 + α2(εA + εI )

= α1︸︷︷︸Before College

+ α3︸︷︷︸After College

+α2(εe,hsνq︸︷︷︸

Ability-Sorting Channel

+1− εe,yνq︸ ︷︷ ︸

Income-Sorting Channel

)

︸ ︷︷ ︸College

Special case, γ0 → +∞⇒ no donation, ωD = 0

αh = α1 + α3 + α2 (ω2 + ω1(1− τy )λ)

21/28

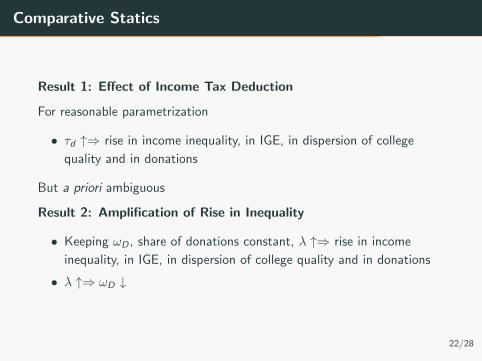

Comparative Statics

Result 1: Effect of Income Tax Deduction

For reasonable parametrization

• τd ↑⇒ rise in income inequality, in IGE, in dispersion of college

quality and in donations

But a priori ambiguous

Result 2: Amplification of Rise in Inequality

• Keeping ωD , share of donations constant, λ ↑⇒ rise in income

inequality, in IGE, in dispersion of college quality and in donations

• λ ↑⇒ ωD ↓

22/28

Extension with Endowment

Endowment (model)

• College objective with love for wealth (Hansmann, 1990) and social

objective

maxI ,θ,Y ,D,φ(.)χ,ζ′,A′

lnV(D,A) = ln q + ω4 lnA− ω̃3 lnY︸ ︷︷ ︸Flow Value

+βu lnV(D ′,A′)

• College Budget Constraint:

pI Ij = Eφ(.)[eu(q, hs , y)] + Dj + χjAj

with χj payout rate out of endowment Aj .

• Law of Motion of Endowment

A′ = erH(1− χ)A

• Progressive Taxation of Endow. (aa is average rate, τa is slope)

A′ = erH(1− aa)Ta [(1− χ)A]1−τa

23/28

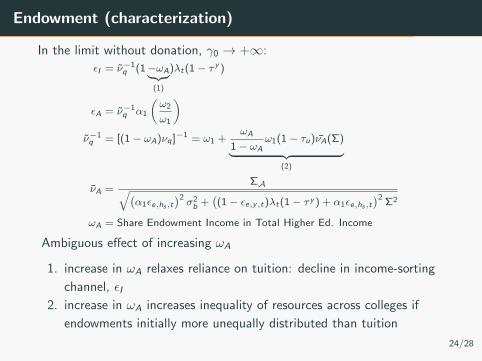

Endowment (characterization)

In the limit without donation, γ0 → +∞:

εI = ν̃−1q (1−ωA︸ ︷︷ ︸

(1)

)λt(1 − τ y )

εA = ν̃−1q α1

(ω2

ω1

)ν̃−1q = [(1 − ωA)νq ]−1 = ω1 +

ωA

1 − ωAω1(1 − τu)ν̄A(Σ)︸ ︷︷ ︸

(2)

ν̄A =ΣA√(

α1εe,hs ,t)2σ2b +

((1 − εe,y,t)λt(1 − τ y ) + α1εe,hs ,t

)2Σ2

ωA = Share Endowment Income in Total Higher Ed. Income

Ambiguous effect of increasing ωA

1. increase in ωA relaxes reliance on tuition: decline in income-sorting

channel, εI2. increase in ωA increases inequality of resources across colleges if

endowments initially more unequally distributed than tuition

24/28

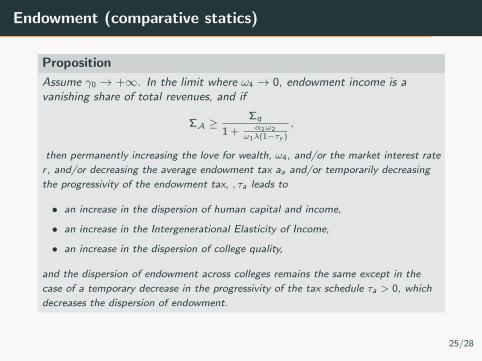

Endowment (comparative statics)

Proposition

Assume γ0 → +∞. In the limit where ω4 → 0, endowment income is avanishing share of total revenues, and if

ΣA ≥Σq

1 + α1ω2ω1λ(1−τy )

,

then permanently increasing the love for wealth, ω4, and/or the market interest rate

r , and/or decreasing the average endowment tax aa and/or temporarily decreasing

the progressivity of the endowment tax, , τa leads to

• an increase in the dispersion of human capital and income,

• an increase in the Intergenerational Elasticity of Income,

• an increase in the dispersion of college quality,

and the dispersion of endowment across colleges remains the same except in the

case of a temporary decrease in the progressivity of the tax schedule τa > 0, which

decreases the dispersion of endowment.

25/28

Conclusion

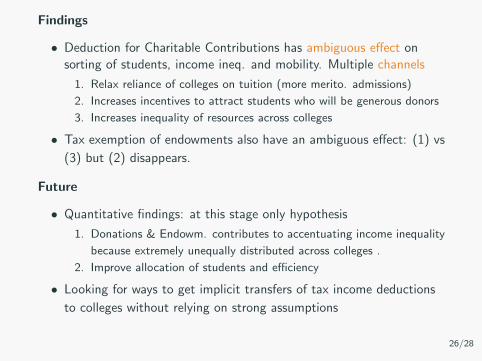

Findings

• Deduction for Charitable Contributions has ambiguous effect on

sorting of students, income ineq. and mobility. Multiple channels

1. Relax reliance of colleges on tuition (more merito. admissions)

2. Increases incentives to attract students who will be generous donors

3. Increases inequality of resources across colleges

• Tax exemption of endowments also have an ambiguous effect: (1) vs

(3) but (2) disappears.

Future

• Quantitative findings: at this stage only hypothesis

1. Donations & Endowm. contributes to accentuating income inequality

because extremely unequally distributed across colleges .

2. Improve allocation of students and efficiency

• Looking for ways to get implicit transfers of tax income deductions

to colleges without relying on strong assumptions

26/28

References

27/28

Appendix

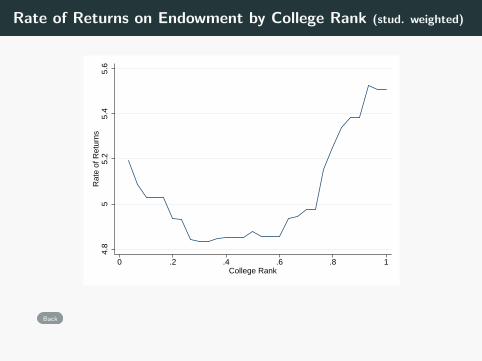

Rate of Returns on Endowment by College Rank (stud. weighted)

4.8

55.

25.

45.

6R

ate

of R

etur

ns

0 .2 .4 .6 .8 1College Rank

Back

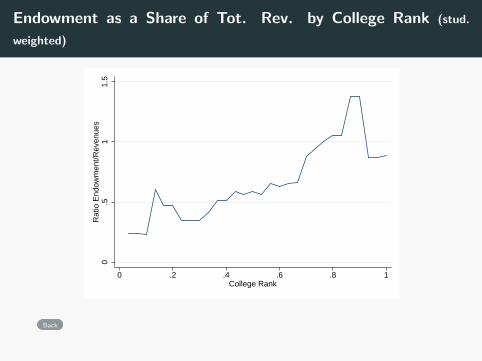

Endowment as a Share of Tot. Rev. by College Rank (stud.

weighted)

0.5

11.

5R

atio

End

owm

ent/R

even

ues

0 .2 .4 .6 .8 1College Rank

Back

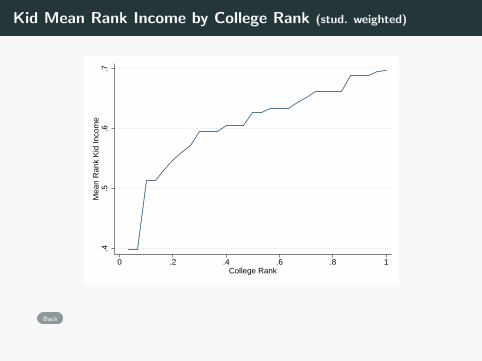

Kid Mean Rank Income by College Rank (stud. weighted)

.4.5

.6.7

Mea

n R

ank

Kid

Inco

me

0 .2 .4 .6 .8 1College Rank

Back

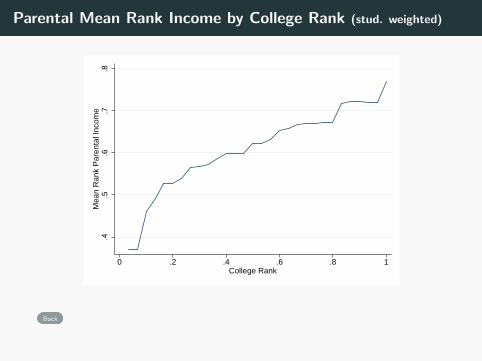

Parental Mean Rank Income by College Rank (stud. weighted)

.4.5

.6.7

.8M

ean

Ran

k P

aren

tal I

ncom

e

0 .2 .4 .6 .8 1College Rank

Back

Proba. Giving by Income Rank

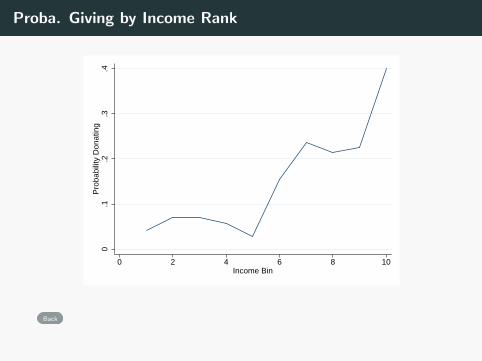

0.1

.2.3

.4P

roba

bilit

y D

onat

ing

0 2 4 6 8 10Income Bin

Back