Embed Size (px)

Citation preview

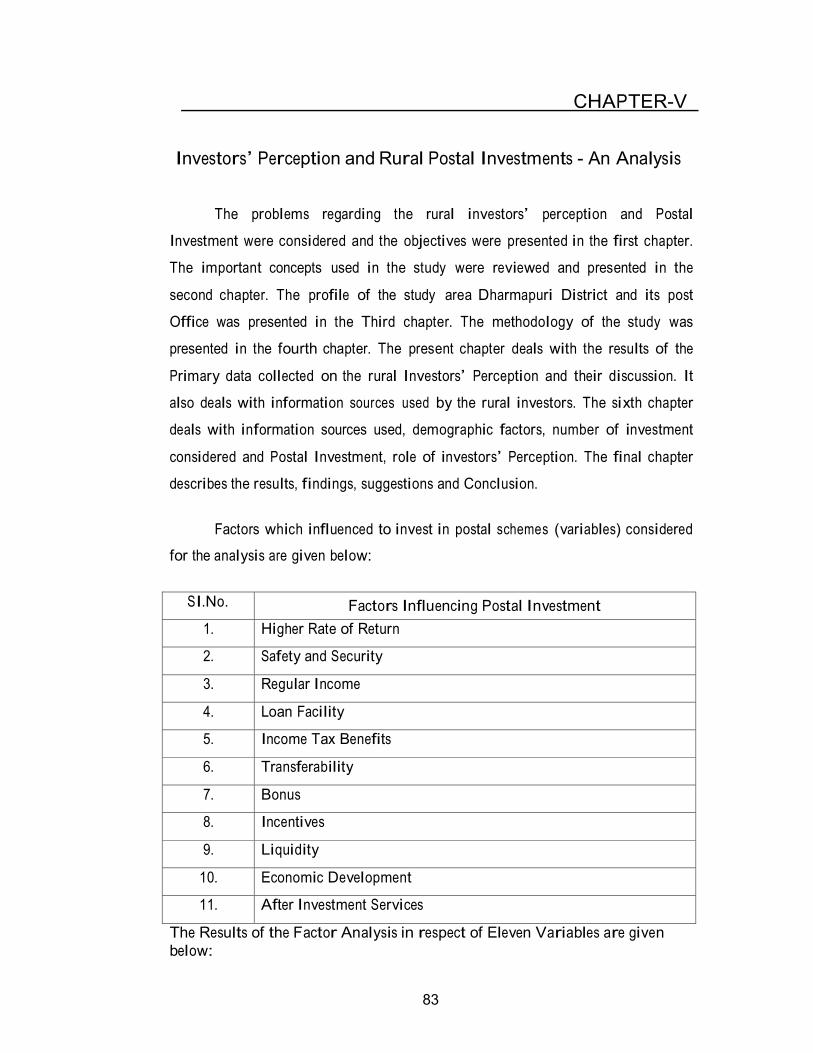

83

CHAPTER-V

Investors’ Perception and Rural Postal Investments - An Analysis

The problems regarding the rural investors’ perception and Postal

Investment were considered and the objectives were presented in the first chapter.

The important concepts used in the study were reviewed and presented in the

second chapter. The profile of the study area Dharmapuri District and its post

Office was presented in the Third chapter. The methodology of the study was

presented in the fourth chapter. The present chapter deals with the results of the

Primary data collected on the rural Investors’ Perception and their discussion. It

also deals with information sources used by the rural investors. The sixth chapter

deals with information sources used, demographic factors, number of investment

considered and Postal Investment, role of investors’ Perception. The final chapter

describes the results, findings, suggestions and Conclusion.

Factors which influenced to invest in postal schemes (variables) considered

for the analysis are given below:

SI.No. Factors Influencing Postal Investment

1. Higher Rate of Return

2. Safety and Security

3. Regular Income

4. Loan Facility

5. Income Tax Benefits

6. Transferability

7. Bonus

8. Incentives

9. Liquidity

10. Economic Development

11. After Investment Services

The Results of the Factor Analysis in respect of Eleven Variables are given

below:

84

Kaiser-Meyer-Olkin Measure of Sampling Adequacy 0.607

Bartlett's Test of Sphericity

Approx. Chi-Square 1665.466

Degree of freedom 55

Significance 0.001

5.1 Post Office Time Deposits

The KMO (Kaiser-Meyer-Olkin) and Barlett’s Test has been used to

find the suitability of the factor analysis for factor reduction. KMO test is a

measure showing the sample adequacy to examine the appropriateness of the

factor analysis. As the KMO (Kaiser-Meyer Olkin) value 0.607 is close to 1 and

Bartlett’s test value is 0.001 which is less than 0.05, it is concluded that the factor

analysis is suitable. The following table shows that the factors suitability test.

Table.5.1.1

Factor Suitability Test

After testing suitability of the Factor Analysis, the explainable variables are

processed to find the principle factors. The results of the analysis are given below

in table 2.12

Table.5.1.2

Total Variance and Factors

C

om

pon

ent

Initial Eigen Values Extraction Sums of

Squared Loadings Rotation Sums of

Squared Loadings

Total

% o

f

Vari

an

ce

Cum

ula

tiv

e

%

Total

% o

f

Vari

an

ce

Cum

ula

tiv

e

%

Total

% o

f

Vari

an

ce

Cum

ula

tiv

e

%

1 3.451 31.376 31.376 3.451 31.376 31.376 3.256 29.604 29.604 2 2.470 22.458 53.834 2.470 22.458 53.834 2.341 21.278 50.882 3 2.049 18.628 72.462 2.049 18.628 72.462 2.063 18.757 69.639 4 1.230 11.179 83.641 1.230 11.179 83.641 1.540 14.002 83.641

5 0.575 5.230 88.871

6 0.395 3.591 92.463 7 0.334 3.034 95.496 8 0.191 1.736 97.232 9 0.167 1.516 98.748

10 0.126 1.147 99.895 11 0.012 0.105 100.000

Extraction Method: Principal Component Analysis.

85

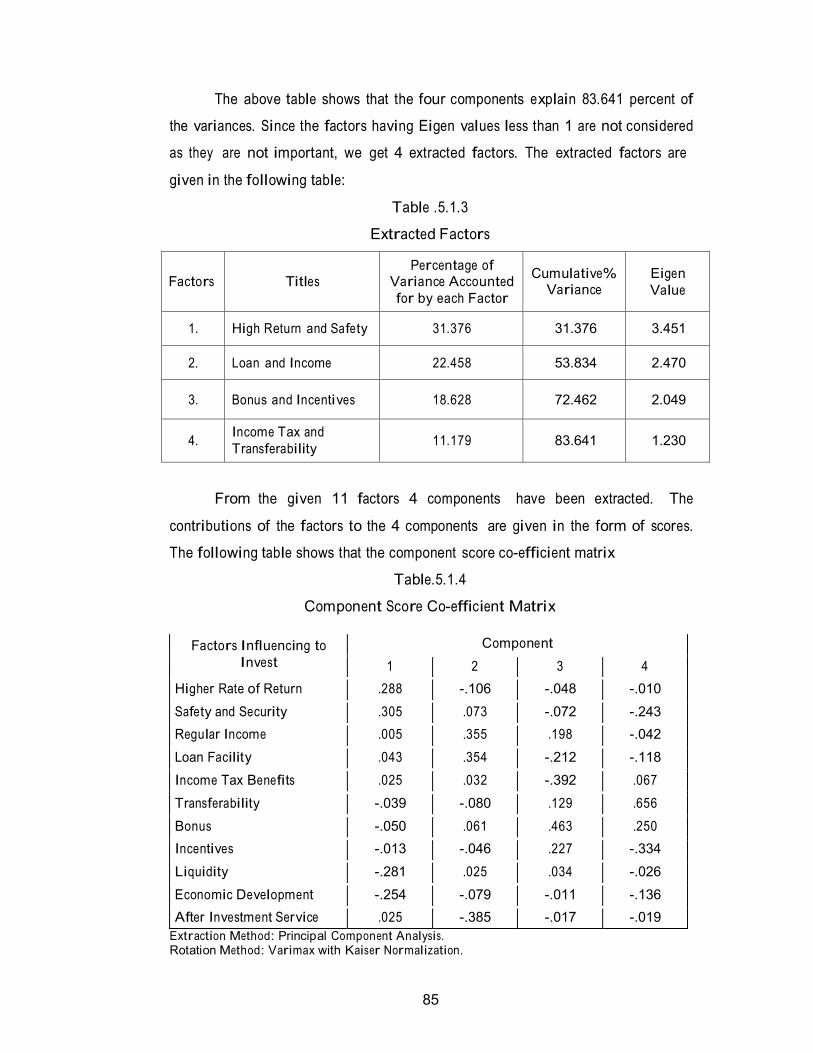

The above table shows that the four components explain 83.641 percent of

the variances. Since the factors having Eigen values less than 1 are not considered

as they are not important, we get 4 extracted factors. The extracted factors are

given in the following table:

Table .5.1.3

Extracted Factors

Factors

Titles Percentage of

Variance Accounted

for by each Factor

Cumulative% Variance

Eigen

Value

1.

High Return and Safety

31.376

31.376

3.451

2.

Loan and Income

22.458

53.834

2.470

3.

Bonus and Incentives

18.628

72.462

2.049

4. Income Tax and

Transferability

11.179

83.641

1.230

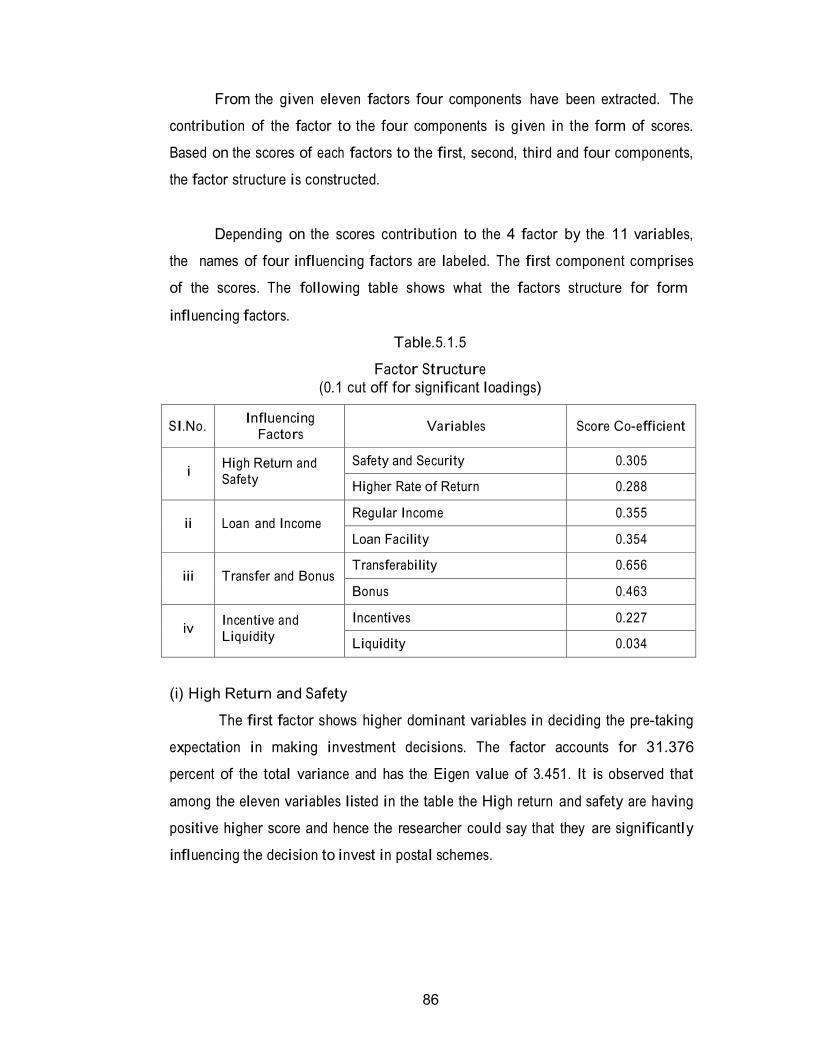

From the given 11 factors 4 components have been extracted. The

contributions of the factors to the 4 components are given in the form of scores.

The following table shows that the component score co-efficient matrix

Table.5.1.4

Component Score Co-efficient Matrix

Factors Influencing to

Invest

Component

1 2 3 4

Higher Rate of Return .288 -.106 -.048 -.010

Safety and Security .305 .073 -.072 -.243

Regular Income .005 .355 .198 -.042

Loan Facility .043 .354 -.212 -.118

Income Tax Benefits .025 .032 -.392 .067

Transferability -.039 -.080 .129 .656

Bonus -.050 .061 .463 .250

Incentives -.013 -.046 .227 -.334

Liquidity -.281 .025 .034 -.026

Economic Development -.254 -.079 -.011 -.136

After Investment Service .025 -.385 -.017 -.019

Extraction Method: Principal Component Analysis. Rotation Method: Varimax with Kaiser Normalization.

86

From the given eleven factors four components have been extracted. The

contribution of the factor to the four components is given in the form of scores.

Based on the scores of each factors to the first, second, third and four components,

the factor structure is constructed.

Depending on the scores contribution to the 4 factor by the 11 variables,

the names of four influencing factors are labeled. The first component comprises

of the scores. The following table shows what the factors structure for form

influencing factors.

Table.5.1.5

Factor Structure

(0.1 cut off for significant loadings)

SI.No. Influencing

Factors

Variables

Score Co-efficient

i

High Return and Safety

Safety and Security 0.305

Higher Rate of Return 0.288

ii

Loan and Income

Regular Income 0.355

Loan Facility 0.354

iii

Transfer and Bonus

Transferability 0.656

Bonus 0.463

iv

Incentive and Liquidity

Incentives 0.227

Liquidity 0.034

(i) High Return and Safety

The first factor shows higher dominant variables in deciding the pre-taking

expectation in making investment decisions. The factor accounts for 31.376

percent of the total variance and has the Eigen value of 3.451. It is observed that

among the eleven variables listed in the table the High return and safety are having

positive higher score and hence the researcher could say that they are significantly

influencing the decision to invest in postal schemes.

87

(ii) Loan and Income

The second factor which influences the decision to invest in postal schemes

is loan and Income. This factor accounts for 22.458 percent of the total variance

and has the Eigen value of 2.470. It is observed that the Loan and income are

having positive higher score and hence the researcher could say that they are

significantly influencing the investment decisions.

(iii) Bonus and Incentives

The third factor which influences decision to invest in postal schemes is

Bonus and Incentives. This factor accounts for 18.628 percent of the total variance

and has the Eigen value of 2.049. It is observed that Incentives and Bonus are

having positive higher score and hence the researcher could say that they are

significantly influencing the investment decisions.

(iv) Income Tax and Transferability

The fourth factor which influences decision to invest in postal Schemes is

Incom Tax and Transferability. This factor accounts for 11.179 percent of the total

variance and has the Eigen value of 1.230. It is observed that Income Tax and

Transferability is having positive higher score and hence the researcher could say

that they are significantly influencing the investment decisions.

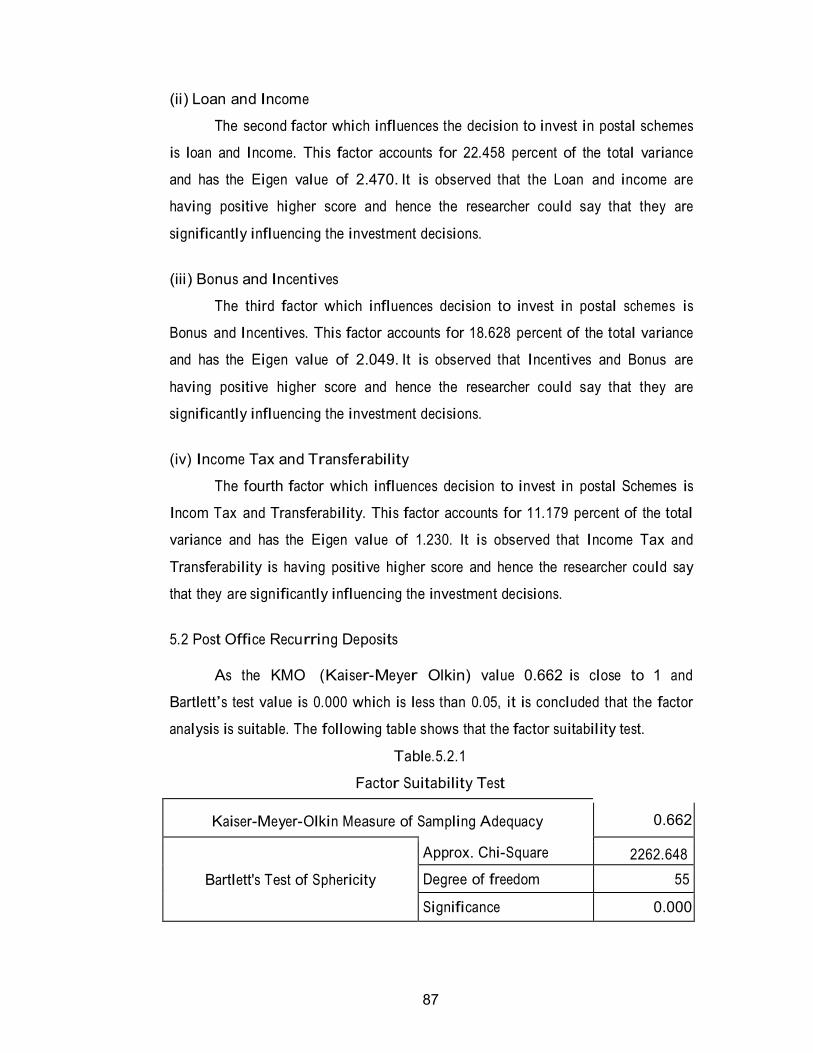

5.2 Post Office Recurring Deposits

As the KMO (Kaiser-Meyer Olkin) value 0.662 is close to 1 and

Bartlett’s test value is 0.000 which is less than 0.05, it is concluded that the factor

analysis is suitable. The following table shows that the factor suitability test.

Table.5.2.1

Factor Suitability Test

Kaiser-Meyer-Olkin Measure of Sampling Adequacy

0.662

Bartlett's Test of Sphericity

Approx. Chi-Square 2262.648

Degree of freedom 55

Significance 0.000

88

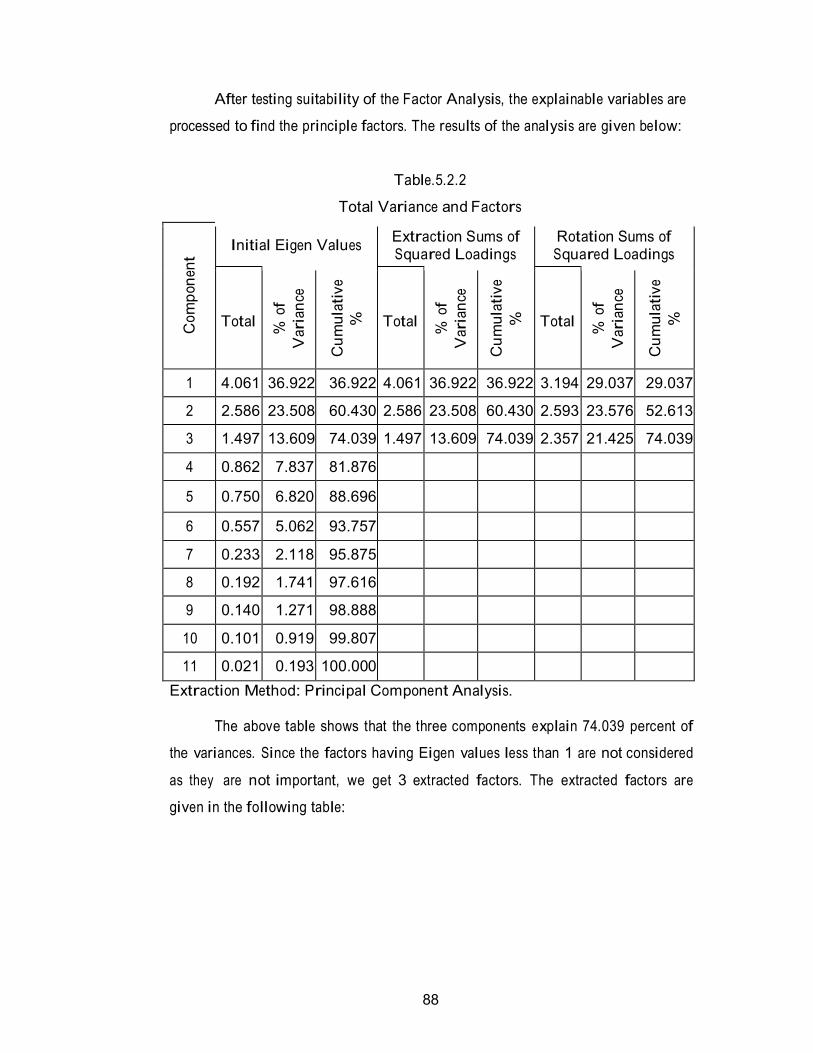

After testing suitability of the Factor Analysis, the explainable variables are

processed to find the principle factors. The results of the analysis are given below:

Table.5.2.2

Total Variance and Factors

C

om

pon

ent

Initial Eigen Values Extraction Sums of Squared Loadings

Rotation Sums of Squared Loadings

Total

% o

f

Var

ian

ce

Cu

mula

tiv

e

%

Total

% o

f

Var

ian

ce

Cu

mula

tiv

e

%

Total

% o

f

Var

ian

ce

Cu

mula

tiv

e

%

1 4.061 36.922 36.922 4.061 36.922 36.922 3.194 29.037 29.037

2 2.586 23.508 60.430 2.586 23.508 60.430 2.593 23.576 52.613

3 1.497 13.609 74.039 1.497 13.609 74.039 2.357 21.425 74.039

4 0.862 7.837 81.876

5 0.750 6.820 88.696

6 0.557 5.062 93.757

7 0.233 2.118 95.875

8 0.192 1.741 97.616

9 0.140 1.271 98.888

10 0.101 0.919 99.807

11 0.021 0.193 100.000

Extraction Method: Principal Component Analysis.

The above table shows that the three components explain 74.039 percent of

the variances. Since the factors having Eigen values less than 1 are not considered

as they are not important, we get 3 extracted factors. The extracted factors are

given in the following table:

89

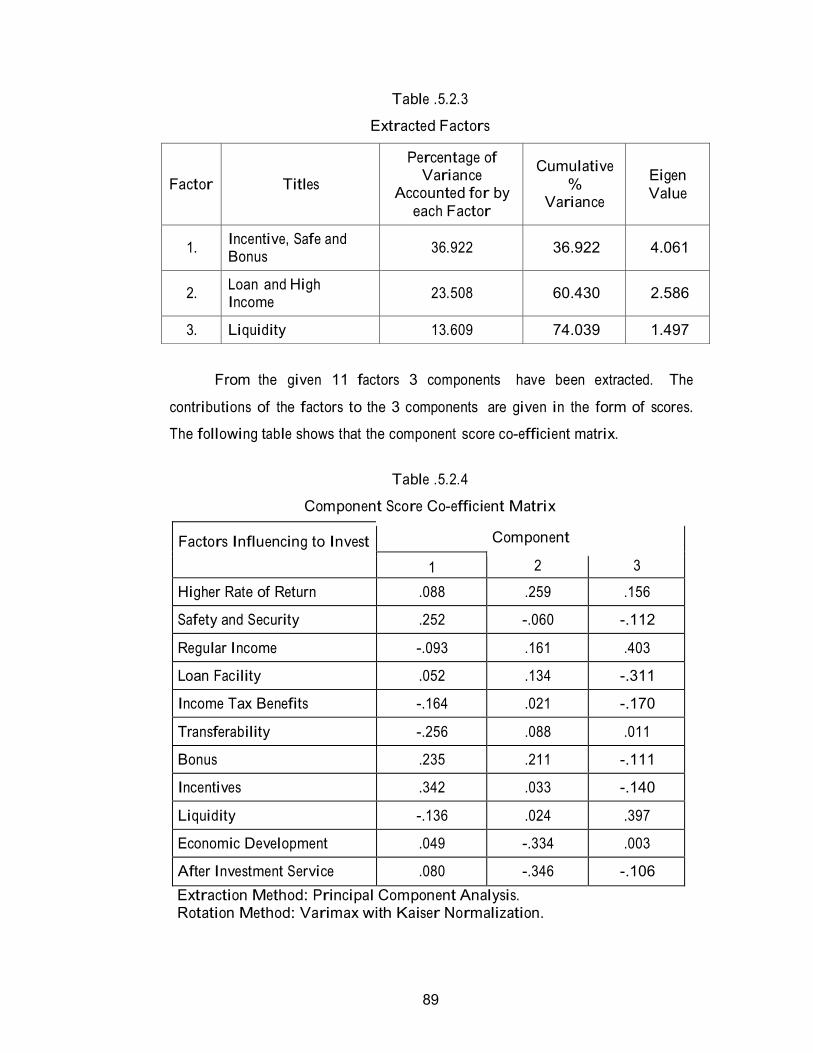

Table .5.2.3

Extracted Factors

Factor

Titles

Percentage of Variance

Accounted for by

each Factor

Cumulative

% Variance

Eigen

Value

1. Incentive, Safe and Bonus

36.922

36.922

4.061

2. Loan and High Income

23.508

60.430

2.586

3. Liquidity 13.609 74.039 1.497

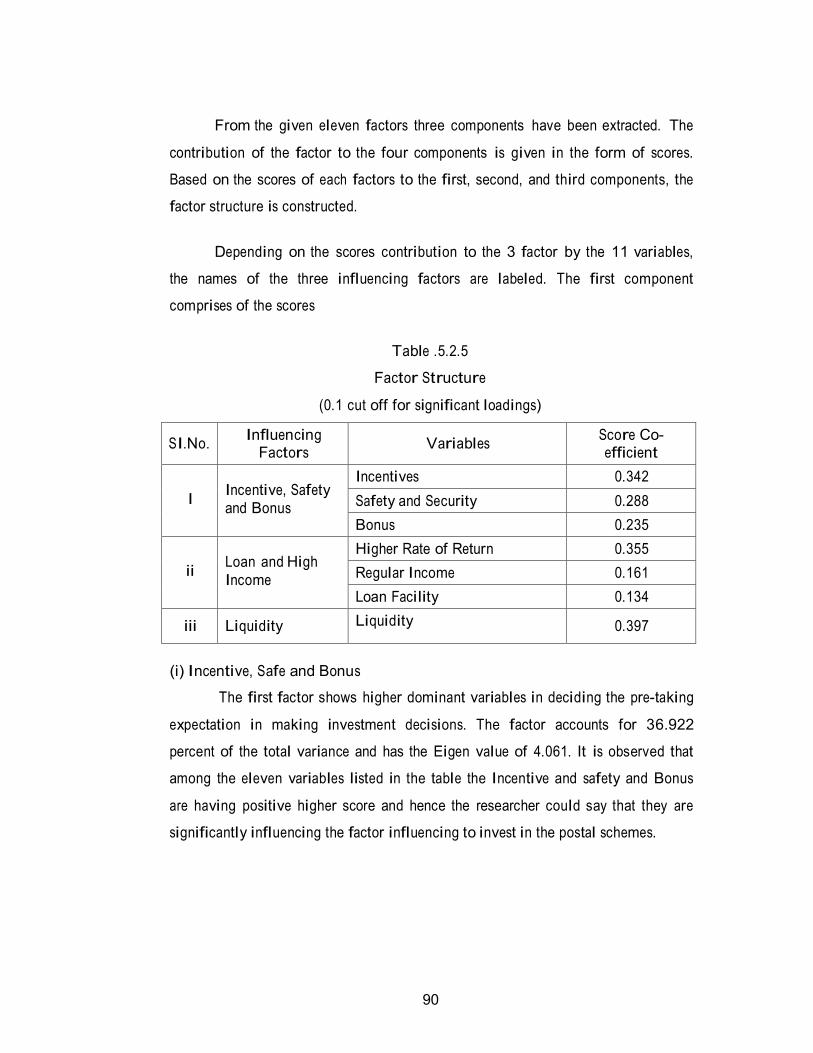

From the given 11 factors 3 components have been extracted. The

contributions of the factors to the 3 components are given in the form of scores.

The following table shows that the component score co-efficient matrix.

Table .5.2.4

Component Score Co-efficient Matrix

Factors Influencing to Invest Component

1 2 3

Higher Rate of Return .088 .259 .156

Safety and Security .252 -.060 -.112

Regular Income -.093 .161 .403

Loan Facility .052 .134 -.311

Income Tax Benefits -.164 .021 -.170

Transferability -.256 .088 .011

Bonus .235 .211 -.111

Incentives .342 .033 -.140

Liquidity -.136 .024 .397

Economic Development .049 -.334 .003

After Investment Service .080 -.346 -.106

Extraction Method: Principal Component Analysis. Rotation Method: Varimax with Kaiser Normalization.

90

From the given eleven factors three components have been extracted. The

contribution of the factor to the four components is given in the form of scores.

Based on the scores of each factors to the first, second, and third components, the

factor structure is constructed.

Depending on the scores contribution to the 3 factor by the 11 variables,

the names of the three influencing factors are labeled. The first component

comprises of the scores

Table .5.2.5

Factor Structure

(0.1 cut off for significant loadings)

SI.No. Influencing

Factors

Variables Score Co- efficient

I

Incentive, Safety

and Bonus

Incentives 0.342

Safety and Security 0.288

Bonus 0.235

ii

Loan and High

Income

Higher Rate of Return 0.355

Regular Income 0.161

Loan Facility 0.134

iii

Liquidity Liquidity

0.397

(i) Incentive, Safe and Bonus

The first factor shows higher dominant variables in deciding the pre-taking

expectation in making investment decisions. The factor accounts for 36.922

percent of the total variance and has the Eigen value of 4.061. It is observed that

among the eleven variables listed in the table the Incentive and safety and Bonus

are having positive higher score and hence the researcher could say that they are

significantly influencing the factor influencing to invest in the postal schemes.

91

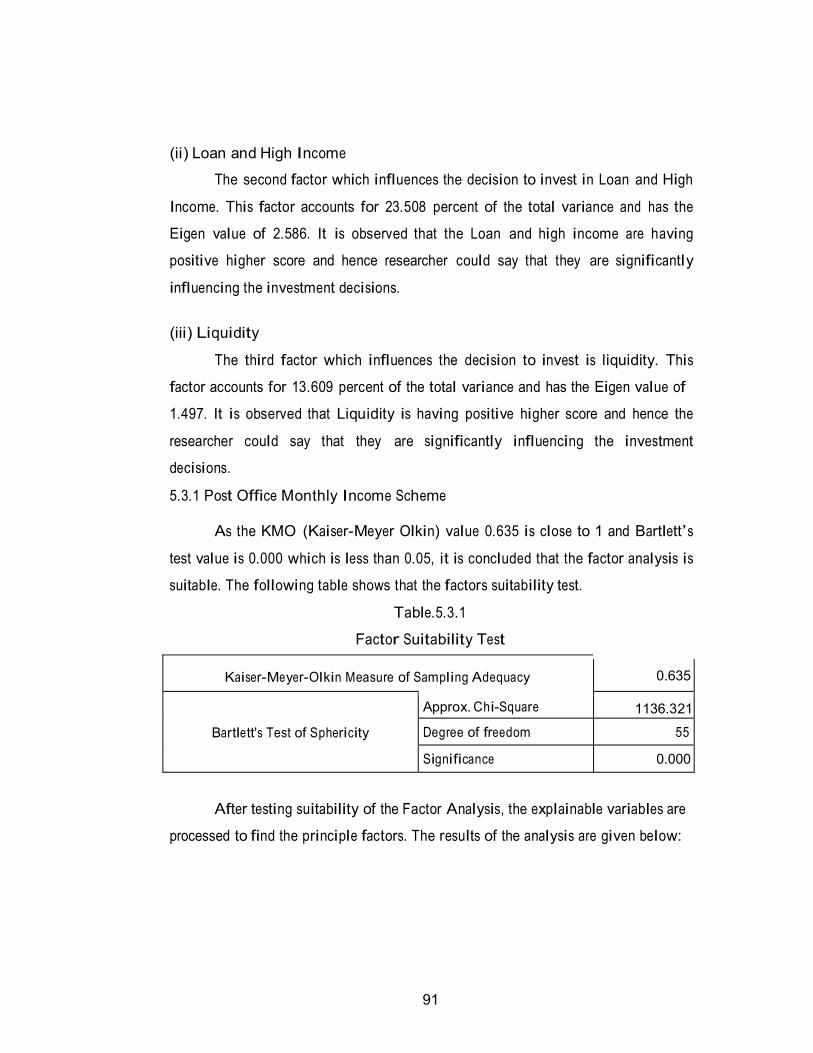

(ii) Loan and High Income

The second factor which influences the decision to invest in Loan and High

Income. This factor accounts for 23.508 percent of the total variance and has the

Eigen value of 2.586. It is observed that the Loan and high income are having

positive higher score and hence researcher could say that they are significantly

influencing the investment decisions.

(iii) Liquidity

The third factor which influences the decision to invest is liquidity. This

factor accounts for 13.609 percent of the total variance and has the Eigen value of

1.497. It is observed that Liquidity is having positive higher score and hence the

researcher could say that they are significantly influencing the investment

decisions.

5.3.1 Post Office Monthly Income Scheme

As the KMO (Kaiser-Meyer Olkin) value 0.635 is close to 1 and Bartlett’s

test value is 0.000 which is less than 0.05, it is concluded that the factor analysis is

suitable. The following table shows that the factors suitability test.

Table.5.3.1

Factor Suitability Test

Kaiser-Meyer-Olkin Measure of Sampling Adequacy

0.635

Bartlett's Test of Sphericity

Approx. Chi-Square 1136.321

Degree of freedom 55

Significance 0.000

After testing suitability of the Factor Analysis, the explainable variables are

processed to find the principle factors. The results of the analysis are given below:

92

Table.5.3.2

Total Variance and Factors

C

om

pon

ent

Initial Eigen Values Extraction Sums of

Squared Loadings Rotation Sums of

Squared Loadings

Total

% o

f

Vari

an

ce

Cum

ula

tiv

e

%

Total

% o

f

Vari

an

ce

Cum

ula

tiv

e

%

Total

% o

f

Vari

an

ce

Cum

ula

tiv

e

%

1 2.849 25.897 25.897 2.849 25.897 25.897 2.312 21.017 21.017

2 2.203 20.024 45.921 2.203 20.024 45.921 2.085 18.957 39.974

3 1.644 14.947 60.868 1.644 14.947 60.868 1.978 17.984 57.959

4 1.405 12.773 73.641 1.405 12.773 73.641 1.574 14.306 72.265

5 1.295 11.777 85.418 1.295 11.777 85.418 1.447 13.153 85.418

6 0.503 4.569 89.987

7 0.461 4.192 94.179

8 0.327 2.974 97.153

9 0.200 1.822 98.975

10 0.085 0.775 99.749

11 0.028 0.251 100.000 Extraction Method: Principal Component Analysis.

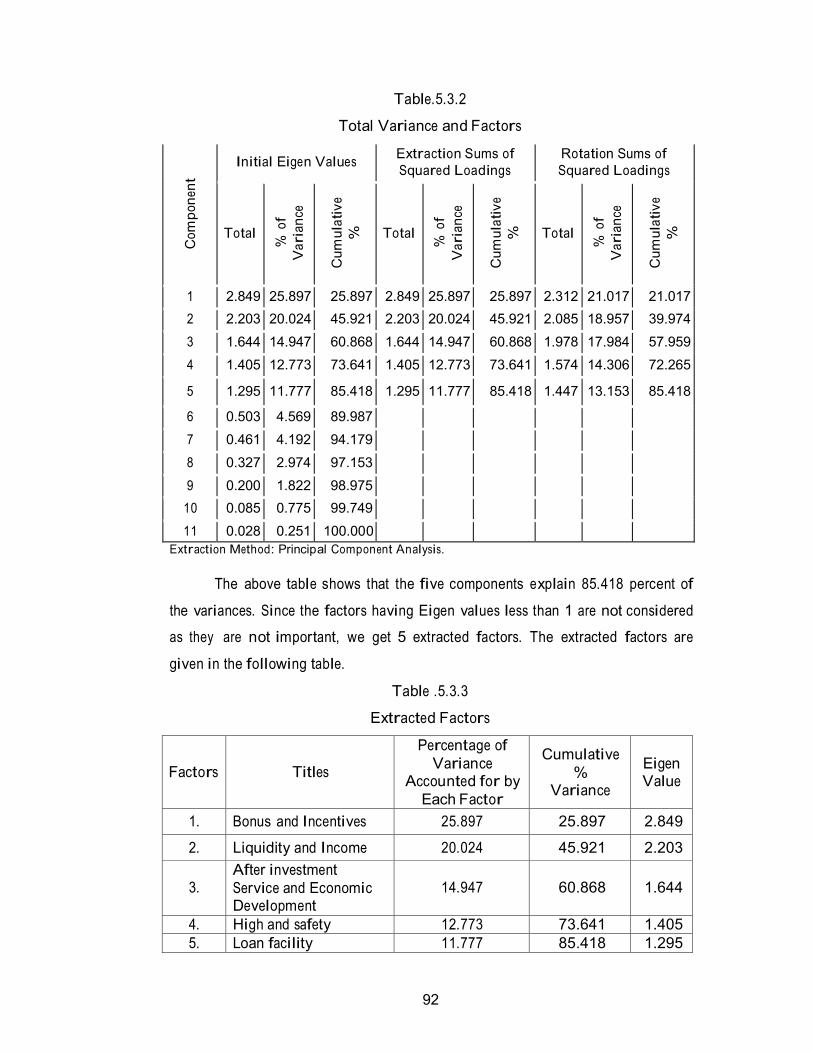

The above table shows that the five components explain 85.418 percent of

the variances. Since the factors having Eigen values less than 1 are not considered

as they are not important, we get 5 extracted factors. The extracted factors are

given in the following table.

Table .5.3.3

Extracted Factors

Factors

Titles

Percentage of

Variance Accounted for by

Each Factor

Cumulative

% Variance

Eigen Value

1. Bonus and Incentives 25.897 25.897 2.849

2. Liquidity and Income 20.024 45.921 2.203

3.

After investment

Service and Economic Development

14.947

60.868

1.644

4. High and safety 12.773 73.641 1.405

5. Loan facility 11.777 85.418 1.295

93

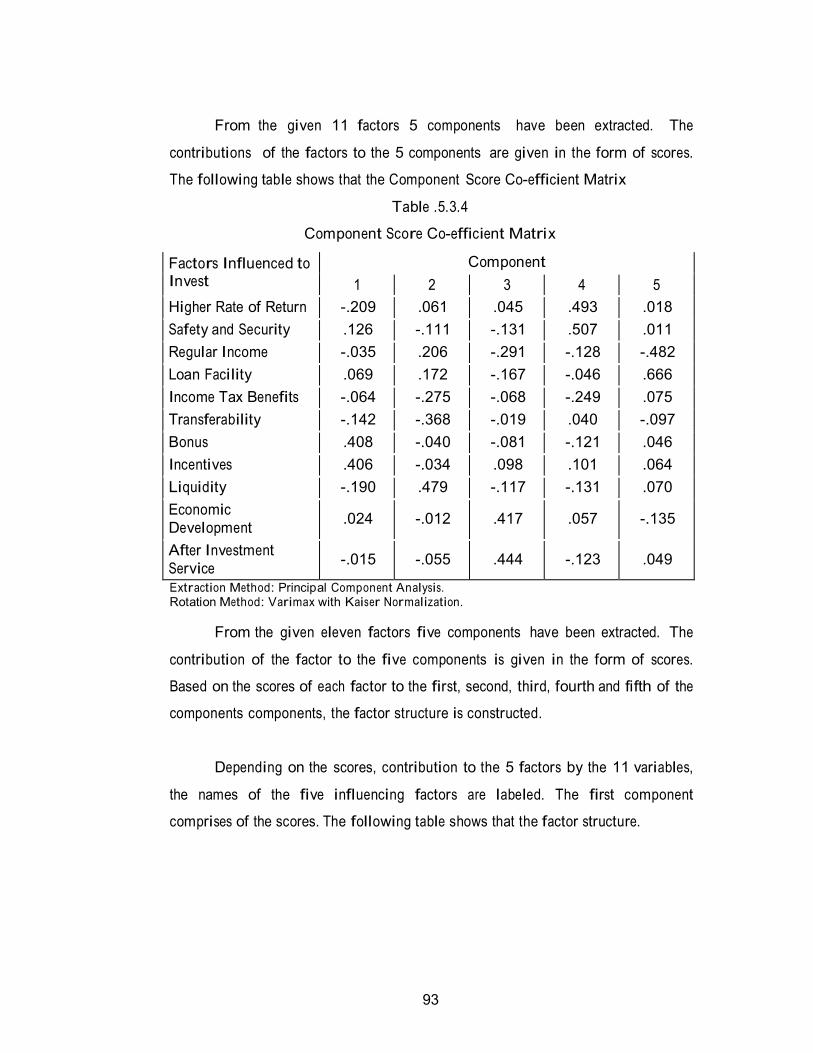

From the given 11 factors 5 components have been extracted. The

contributions of the factors to the 5 components are given in the form of scores.

The following table shows that the Component Score Co-efficient Matrix

Table .5.3.4

Component Score Co-efficient Matrix

Factors Influenced to Invest

Component

1 2 3 4 5

Higher Rate of Return -.209 .061 .045 .493 .018

Safety and Security .126 -.111 -.131 .507 .011

Regular Income -.035 .206 -.291 -.128 -.482

Loan Facility .069 .172 -.167 -.046 .666

Income Tax Benefits -.064 -.275 -.068 -.249 .075

Transferability -.142 -.368 -.019 .040 -.097

Bonus .408 -.040 -.081 -.121 .046

Incentives .406 -.034 .098 .101 .064

Liquidity -.190 .479 -.117 -.131 .070

Economic

Development

.024

-.012

.417

.057

-.135

After Investment

Service

-.015

-.055

.444

-.123

.049

Extraction Method: Principal Component Analysis. Rotation Method: Varimax with Kaiser Normalization.

From the given eleven factors five components have been extracted. The

contribution of the factor to the five components is given in the form of scores.

Based on the scores of each factor to the first, second, third, fourth and fifth of the

components components, the factor structure is constructed.

Depending on the scores, contribution to the 5 factors by the 11 variables,

the names of the five influencing factors are labeled. The first component

comprises of the scores. The following table shows that the factor structure.

94

Table.5.3.5

Factor Structure

(0.1 cut off for significant loadings)

SI.No. Influencing Factors

Variables Score Co- efficient

i

Bonus and

Incentives

Bonus 0.408

Incentives 0.406

ii

Liquidity and

Income

Liquidity 0.479

Regular Income 0.206

iii After Service and Economic

Development

After Investment Service 0.444

Economic Development 0.417

iv

High Rate and

Safety

Safety and Security 0.507

Higher Rate of Return 0.493

v Loan facility Loan Facility 0.666

(i) Bonus and Incentives

The first factor shows higher dominant variables in deciding the pre-taking

expectation in making investment decisions. The factor accounts for 25.897

percent of the total variance and has the Eigen value of 2.849. It is observed that

among the eleven variables listed in the table Bonus and Incentives are having

positive higher score and hence the researcher could say that they are significantly

influencing the decision to invest in the postal schemes.

(ii) Liquidity and Income

The second factor which influences decision to invest in postal schemes is

Liquidity and Income. This factor accounts for 20.024 per cent of the total

variance and has the Eigen value of 2.203. It is observed that the Liquidity and

Income are having positive higher score and hence the researcher could say that

they are significantly influencing the investment decisions.

(iii) After Investment Service and Economic Development

The third factor which influences decision to invest postal schemes is After

investment Service and Economic Development. This factor accounts for 14.947

95

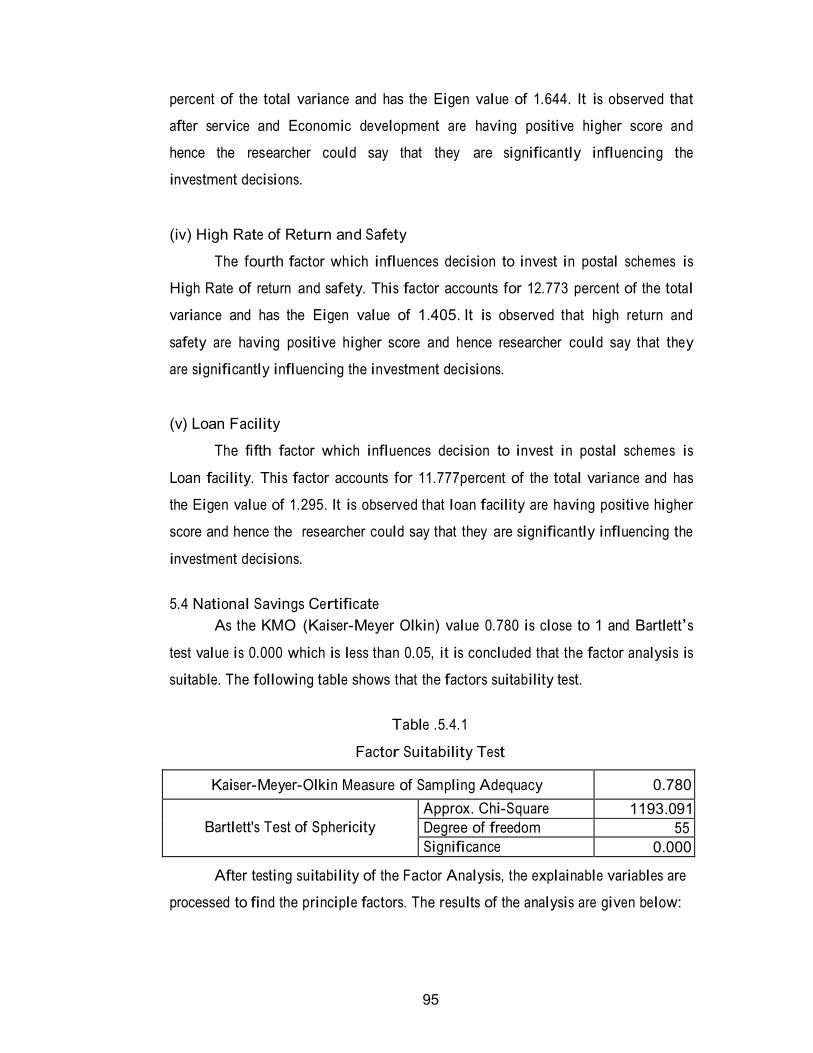

percent of the total variance and has the Eigen value of 1.644. It is observed that

after service and Economic development are having positive higher score and

hence the researcher could say that they are significantly influencing the

investment decisions.

(iv) High Rate of Return and Safety

The fourth factor which influences decision to invest in postal schemes is

High Rate of return and safety. This factor accounts for 12.773 percent of the total

variance and has the Eigen value of 1.405. It is observed that high return and

safety are having positive higher score and hence researcher could say that they

are significantly influencing the investment decisions.

(v) Loan Facility

The fifth factor which influences decision to invest in postal schemes is

Loan facility. This factor accounts for 11.777percent of the total variance and has

the Eigen value of 1.295. It is observed that loan facility are having positive higher

score and hence the researcher could say that they are significantly influencing the

investment decisions.

5.4 National Savings Certificate

As the KMO (Kaiser-Meyer Olkin) value 0.780 is close to 1 and Bartlett’s

test value is 0.000 which is less than 0.05, it is concluded that the factor analysis is

suitable. The following table shows that the factors suitability test.

Table .5.4.1

Factor Suitability Test

Kaiser-Meyer-Olkin Measure of Sampling Adequacy 0.780

Bartlett's Test of Sphericity

Approx. Chi-Square 1193.091

Degree of freedom 55

Significance 0.000

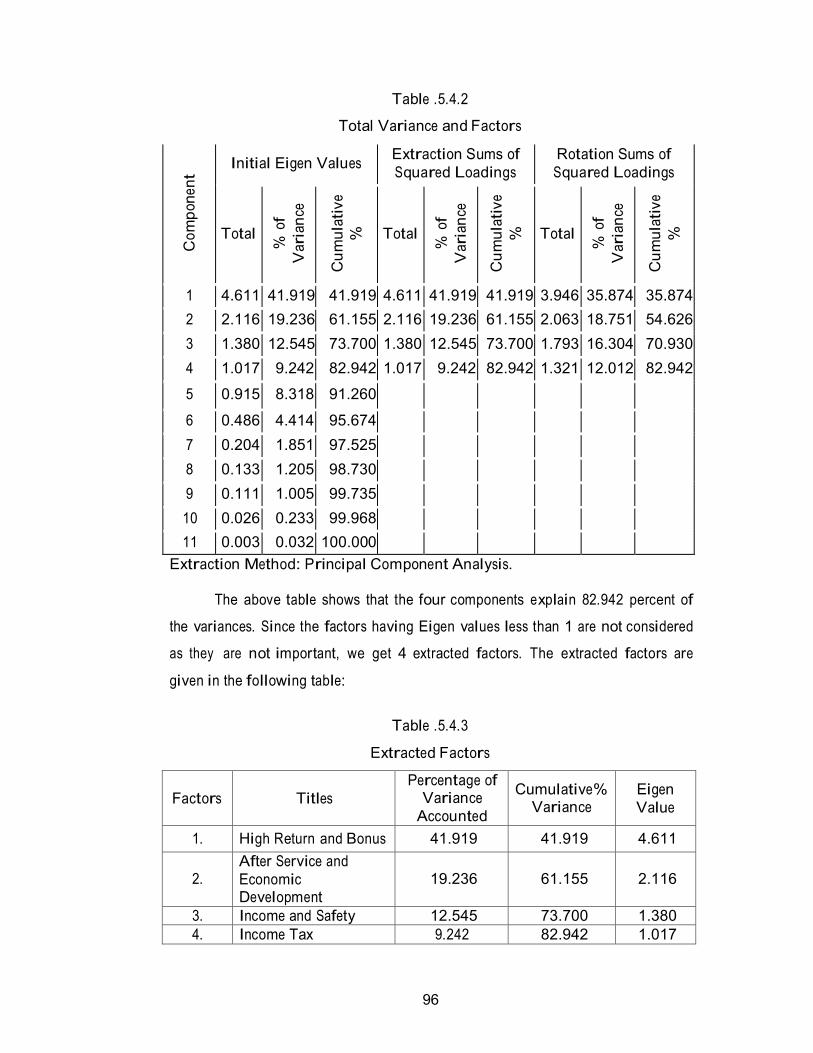

After testing suitability of the Factor Analysis, the explainable variables are

processed to find the principle factors. The results of the analysis are given below:

96

Table .5.4.2

Total Variance and Factors

C

om

pon

ent

Initial Eigen Values Extraction Sums of

Squared Loadings

Rotation Sums of

Squared Loadings

Total

% o

f

Var

ian

ce

Cu

mula

tiv

e

%

Total

% o

f

Var

ian

ce

Cu

mula

tiv

e

%

Total

% o

f

Var

ian

ce

Cu

mula

tiv

e

%

1 4.611 41.919 41.919 4.611 41.919 41.919 3.946 35.874 35.874

2 2.116 19.236 61.155 2.116 19.236 61.155 2.063 18.751 54.626

3 1.380 12.545 73.700 1.380 12.545 73.700 1.793 16.304 70.930

4 1.017 9.242 82.942 1.017 9.242 82.942 1.321 12.012 82.942

5 0.915 8.318 91.260

6 0.486 4.414 95.674

7 0.204 1.851 97.525

8 0.133 1.205 98.730

9 0.111 1.005 99.735

10 0.026 0.233 99.968

11 0.003 0.032 100.000

Extraction Method: Principal Component Analysis.

The above table shows that the four components explain 82.942 percent of

the variances. Since the factors having Eigen values less than 1 are not considered

as they are not important, we get 4 extracted factors. The extracted factors are

given in the following table:

Table .5.4.3

Extracted Factors

Factors

Titles

Percentage of Variance

Accounted

Cumulative% Variance

Eigen

Value

1. High Return and Bonus 41.919 41.919 4.611

2.

After Service and

Economic Development

19.236

61.155

2.116

3. Income and Safety 12.545 73.700 1.380

4. Income Tax 9.242 82.942 1.017

97

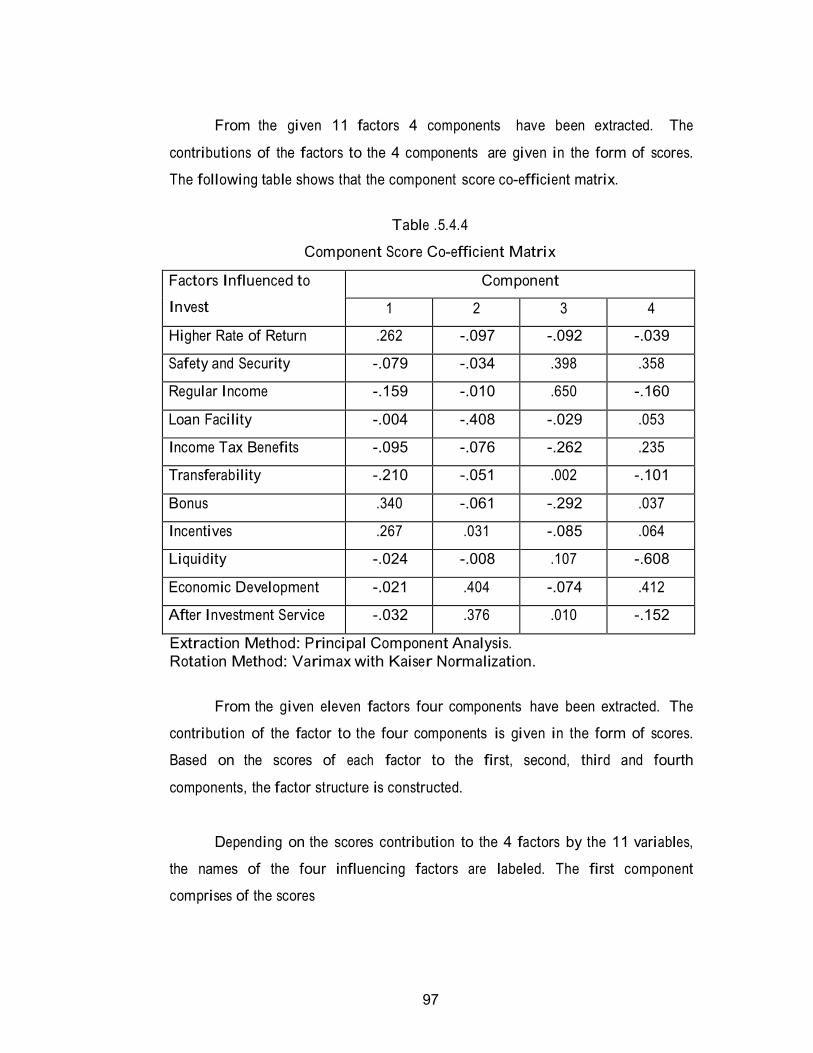

From the given 11 factors 4 components have been extracted. The

contributions of the factors to the 4 components are given in the form of scores.

The following table shows that the component score co-efficient matrix.

Table .5.4.4

Component Score Co-efficient Matrix

Factors Influenced to

Invest

Component

1 2 3 4

Higher Rate of Return .262 -.097 -.092 -.039

Safety and Security -.079 -.034 .398 .358

Regular Income -.159 -.010 .650 -.160

Loan Facility -.004 -.408 -.029 .053

Income Tax Benefits -.095 -.076 -.262 .235

Transferability -.210 -.051 .002 -.101

Bonus .340 -.061 -.292 .037

Incentives .267 .031 -.085 .064

Liquidity -.024 -.008 .107 -.608

Economic Development -.021 .404 -.074 .412

After Investment Service -.032 .376 .010 -.152

Extraction Method: Principal Component Analysis.

Rotation Method: Varimax with Kaiser Normalization.

From the given eleven factors four components have been extracted. The

contribution of the factor to the four components is given in the form of scores.

Based on the scores of each factor to the first, second, third and fourth

components, the factor structure is constructed.

Depending on the scores contribution to the 4 factors by the 11 variables,

the names of the four influencing factors are labeled. The first component

comprises of the scores

98

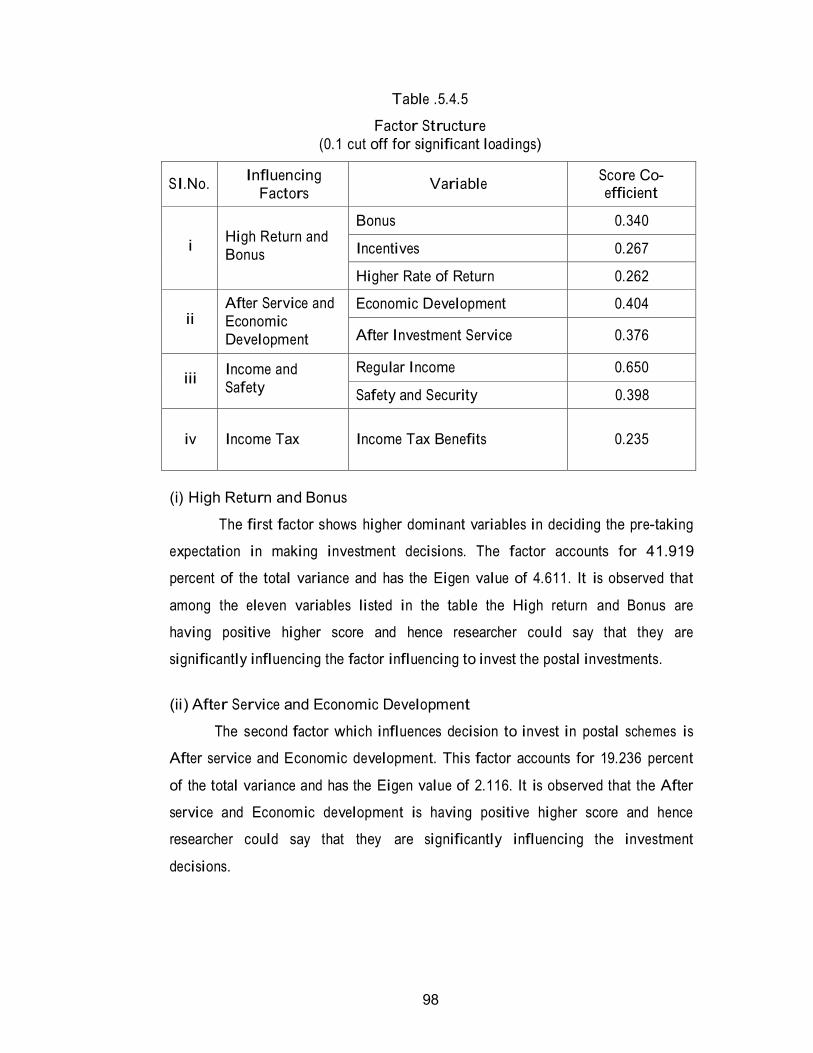

Table .5.4.5

Factor Structure

(0.1 cut off for significant loadings)

SI.No. Influencing

Factors

Variable Score Co- efficient

i

High Return and

Bonus

Bonus 0.340

Incentives 0.267

Higher Rate of Return 0.262

ii

After Service and

Economic

Development

Economic Development 0.404

After Investment Service

0.376

iii

Income and

Safety

Regular Income 0.650

Safety and Security 0.398

iv

Income Tax

Income Tax Benefits

0.235

(i) High Return and Bonus

The first factor shows higher dominant variables in deciding the pre-taking

expectation in making investment decisions. The factor accounts for 41.919

percent of the total variance and has the Eigen value of 4.611. It is observed that

among the eleven variables listed in the table the High return and Bonus are

having positive higher score and hence researcher could say that they are

significantly influencing the factor influencing to invest the postal investments.

(ii) After Service and Economic Development

The second factor which influences decision to invest in postal schemes is

After service and Economic development. This factor accounts for 19.236 percent

of the total variance and has the Eigen value of 2.116. It is observed that the After

service and Economic development is having positive higher score and hence

researcher could say that they are significantly influencing the investment

decisions.

99

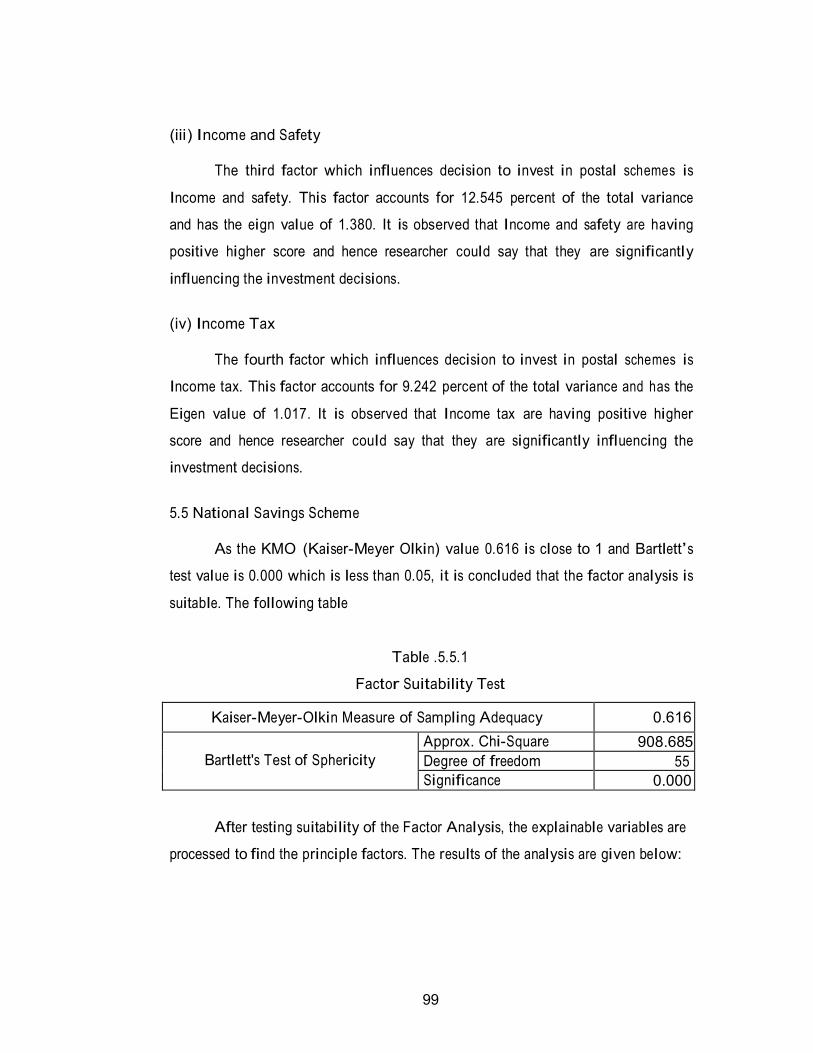

(iii) Income and Safety

The third factor which influences decision to invest in postal schemes is

Income and safety. This factor accounts for 12.545 percent of the total variance

and has the eign value of 1.380. It is observed that Income and safety are having

positive higher score and hence researcher could say that they are significantly

influencing the investment decisions.

(iv) Income Tax

The fourth factor which influences decision to invest in postal schemes is

Income tax. This factor accounts for 9.242 percent of the total variance and has the

Eigen value of 1.017. It is observed that Income tax are having positive higher

score and hence researcher could say that they are significantly influencing the

investment decisions.

5.5 National Savings Scheme

As the KMO (Kaiser-Meyer Olkin) value 0.616 is close to 1 and Bartlett’s

test value is 0.000 which is less than 0.05, it is concluded that the factor analysis is

suitable. The following table

Table .5.5.1

Factor Suitability Test

Kaiser-Meyer-Olkin Measure of Sampling Adequacy 0.616

Bartlett's Test of Sphericity

Approx. Chi-Square 908.685

Degree of freedom 55

Significance 0.000

After testing suitability of the Factor Analysis, the explainable variables are

processed to find the principle factors. The results of the analysis are given below:

100

Table .5.5.2

Total Variance and Factors

C

om

pon

ent

Initial Eigen Values Extraction Sums of Squared Loadings

Rotation Sums of Squared Loadings

Total

% o

f

Var

ian

ce

Cu

mula

tiv

e

%

Total

% o

f

Var

ian

ce

Cu

mula

tiv

e

%

Total

% o

f

Var

ian

ce

Cu

mula

tiv

e

%

1 3.996 36.326 36.326 3.996 36.326 36.326 2.655 24.137 24.137

2 2.417 21.969 58.294 2.417 21.969 58.294 2.514 22.855 46.992

3 1.609 14.625 72.919 1.609 14.625 72.919 2.388 21.706 68.698

4 1.291 11.736 84.655 1.291 11.736 84.655 1.755 15.958 84.655

5 0.791 7.194 91.849

6 0.431 3.917 95.766

7 0.250 2.272 98.039

8 0.141 1.283 99.321

9 0.052 0.475 99.796

10 0.019 0.176 99.972

11 0.003 0.028 100.000

Extraction Method: Principal Component Analysis.

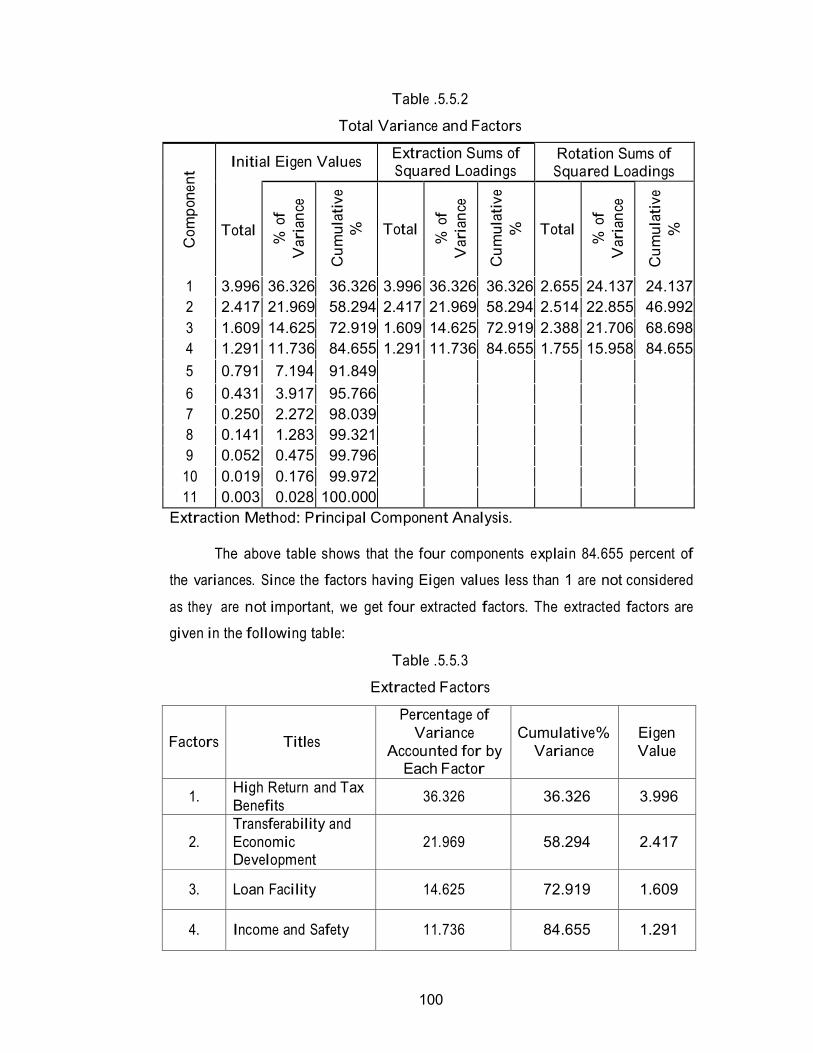

The above table shows that the four components explain 84.655 percent of

the variances. Since the factors having Eigen values less than 1 are not considered

as they are not important, we get four extracted factors. The extracted factors are

given in the following table:

Table .5.5.3

Extracted Factors

Factors

Titles

Percentage of

Variance

Accounted for by Each Factor

Cumulative%

Variance

Eigen

Value

1. High Return and Tax

Benefits

36.326

36.326

3.996

2.

Transferability and

Economic Development

21.969

58.294

2.417

3.

Loan Facility

14.625

72.919

1.609

4.

Income and Safety

11.736

84.655

1.291

101

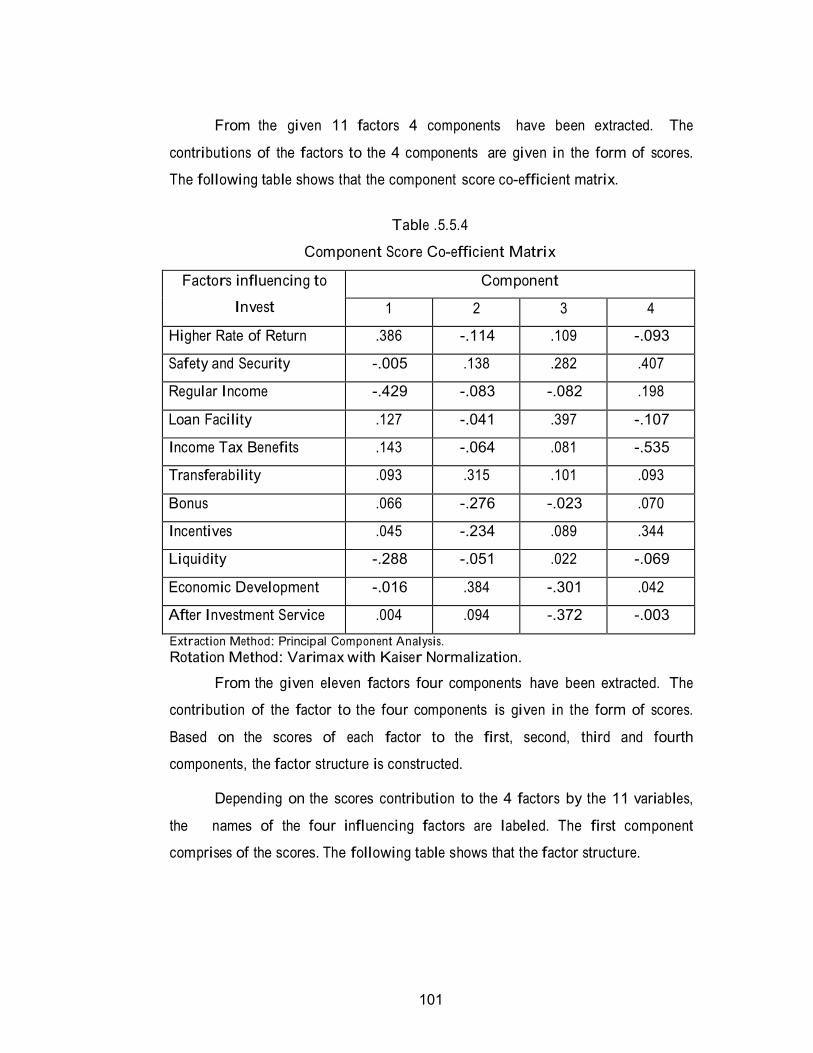

From the given 11 factors 4 components have been extracted. The

contributions of the factors to the 4 components are given in the form of scores.

The following table shows that the component score co-efficient matrix.

Table .5.5.4

Component Score Co-efficient Matrix

Factors influencing to

Invest

Component

1 2 3 4

Higher Rate of Return .386 -.114 .109 -.093

Safety and Security -.005 .138 .282 .407

Regular Income -.429 -.083 -.082 .198

Loan Facility .127 -.041 .397 -.107

Income Tax Benefits .143 -.064 .081 -.535

Transferability .093 .315 .101 .093

Bonus .066 -.276 -.023 .070

Incentives .045 -.234 .089 .344

Liquidity -.288 -.051 .022 -.069

Economic Development -.016 .384 -.301 .042

After Investment Service .004 .094 -.372 -.003

Extraction Method: Principal Component Analysis.

Rotation Method: Varimax with Kaiser Normalization.

From the given eleven factors four components have been extracted. The

contribution of the factor to the four components is given in the form of scores.

Based on the scores of each factor to the first, second, third and fourth

components, the factor structure is constructed.

Depending on the scores contribution to the 4 factors by the 11 variables,

the names of the four influencing factors are labeled. The first component

comprises of the scores. The following table shows that the factor structure.

102

Table .5.5.5

Factor Structure

(0.1 cut off for significant loadings)

SI.No. Influencing

Factors

Variables Score Co- efficient

i

High Return and

Tax Benefits

Higher Rate of Return 0.386

Income Tax Benefits 0.143

ii

Transferability

and Economic Development

Economic Development 0.384

Transferability

0.315

iii Loan Facility Loan Facility 0.397

iv

Income and

Safety

Safety and Security 0.407

Incentives 0.344

Regular Income 0.198

(i) High Return and Tax Benefits

The first factor shows higher dominant variables in deciding the pre-taking

expectation in making investment decisions. The factor accounts for 36.326

percent of the total variance and has the Eigen value of 3.996. It is observed that

among the eleven variables listed in the table the High return and tax benefits are

having positive higher score and hence researcher could say that they are

significantly influencing the factor influencing to invest the postal investments.

(ii) Transferability and Economic Development

The second factor which influences decision to invest in postal schemes is

Transferability and Economic development. This factor accounts for 21.969

percent of the total variance and has the Eigen value of 2.417. It is observed that

the Transferability and Economic development is having positive higher score and

hence the researcher could say that they are significantly influencing the

investment decisions.

103

(iii) Loan Facility

The third factor which influences decision to invest in postal schemes is

Loan facility. This factor accounts for 14.625 percent of the total variance and has

the eign value of 1.609. It is observed that loan facility are having positive higher

score and hence researcher could say that they are significantly influencing the

investment decisions.

(iv) Income and Safety

The fourth factor which influences decision to invest in postal schemes is

Oncom and Safety. This factor accounts for 11.736 percent of the total variance

and has the eign value of 1.291. It is observed that Income and safety are having

positive higher score and hence researcher could say that they are significantly

influencing the investment decisions.

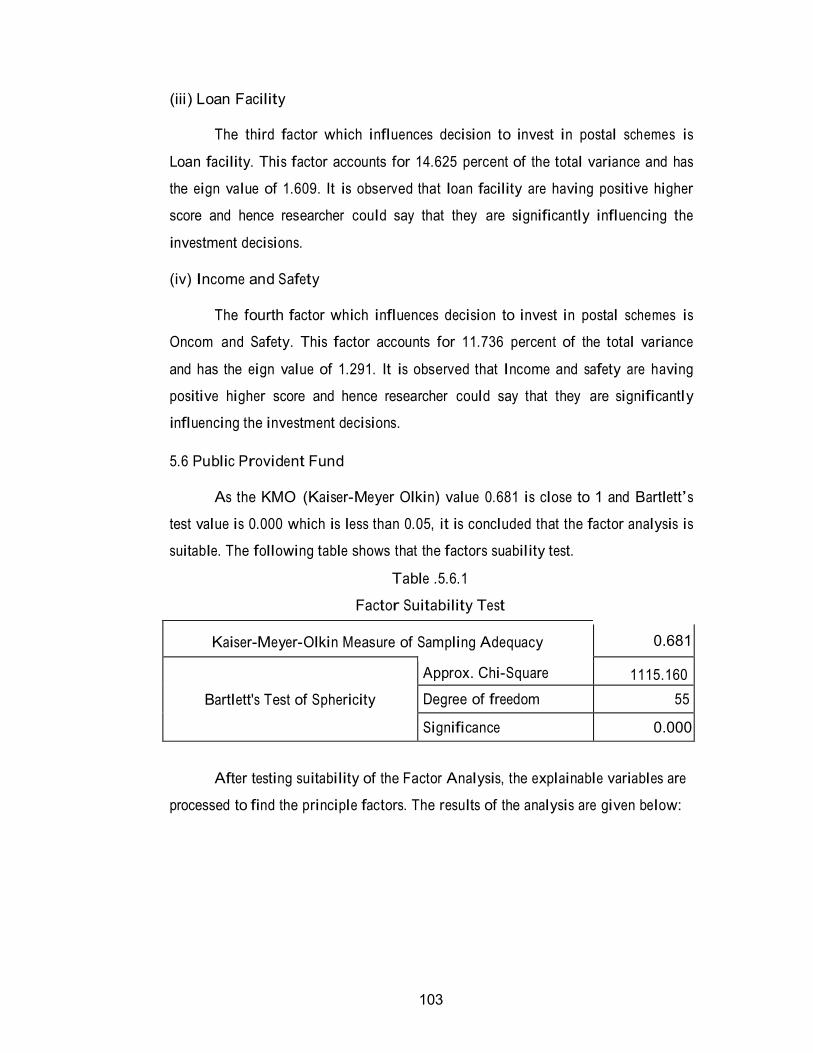

5.6 Public Provident Fund

As the KMO (Kaiser-Meyer Olkin) value 0.681 is close to 1 and Bartlett’s

test value is 0.000 which is less than 0.05, it is concluded that the factor analysis is

suitable. The following table shows that the factors suability test.

Table .5.6.1

Factor Suitability Test

Kaiser-Meyer-Olkin Measure of Sampling Adequacy

0.681

Bartlett's Test of Sphericity

Approx. Chi-Square 1115.160

Degree of freedom 55

Significance 0.000

After testing suitability of the Factor Analysis, the explainable variables are

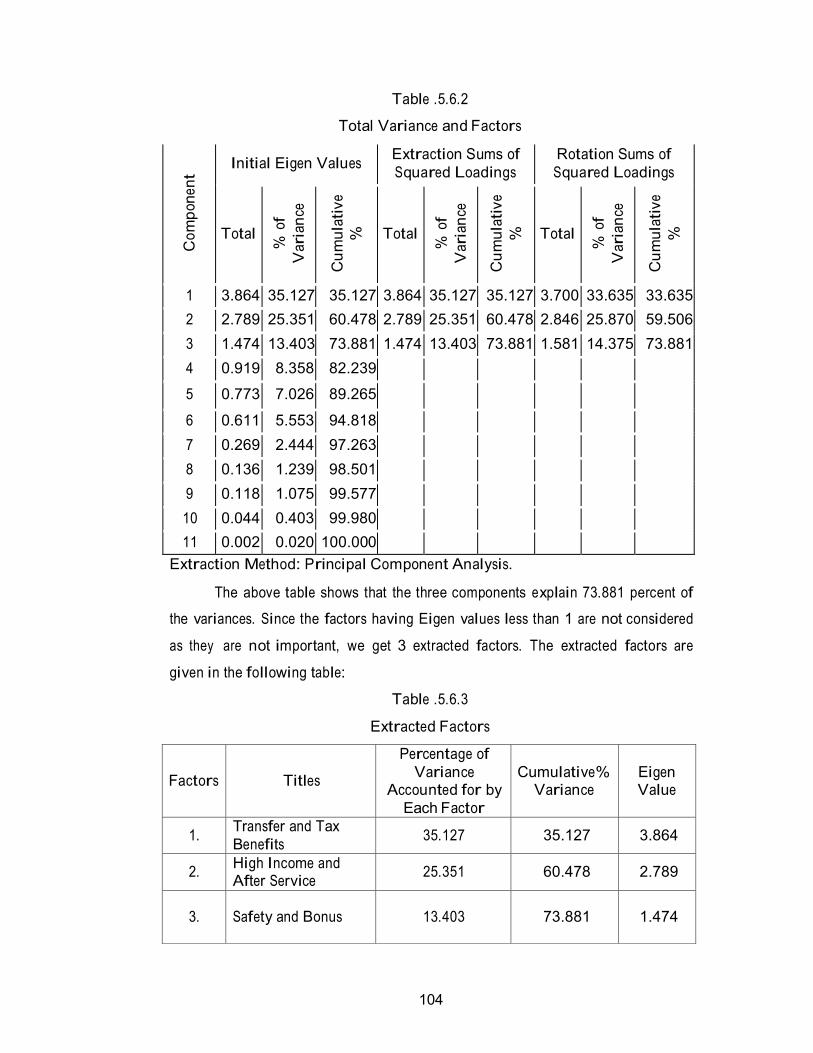

processed to find the principle factors. The results of the analysis are given below:

104

Table .5.6.2

Total Variance and Factors

C

om

pon

ent

Initial Eigen Values Extraction Sums of

Squared Loadings

Rotation Sums of

Squared Loadings

Total

% o

f

Var

ian

ce

Cu

mula

tiv

e

%

Total

% o

f

Var

ian

ce

Cu

mula

tiv

e

%

Total

% o

f

Var

ian

ce

Cu

mula

tiv

e

%

1 3.864 35.127 35.127 3.864 35.127 35.127 3.700 33.635 33.635

2 2.789 25.351 60.478 2.789 25.351 60.478 2.846 25.870 59.506

3 1.474 13.403 73.881 1.474 13.403 73.881 1.581 14.375 73.881

4 0.919 8.358 82.239

5 0.773 7.026 89.265

6 0.611 5.553 94.818

7 0.269 2.444 97.263

8 0.136 1.239 98.501

9 0.118 1.075 99.577

10 0.044 0.403 99.980

11 0.002 0.020 100.000

Extraction Method: Principal Component Analysis.

The above table shows that the three components explain 73.881 percent of

the variances. Since the factors having Eigen values less than 1 are not considered

as they are not important, we get 3 extracted factors. The extracted factors are

given in the following table:

Table .5.6.3

Extracted Factors

Factors

Titles

Percentage of

Variance Accounted for by

Each Factor

Cumulative%

Variance

Eigen Value

1. Transfer and Tax

Benefits

35.127

35.127

3.864

2. High Income and After Service

25.351

60.478

2.789

3.

Safety and Bonus

13.403

73.881

1.474

105

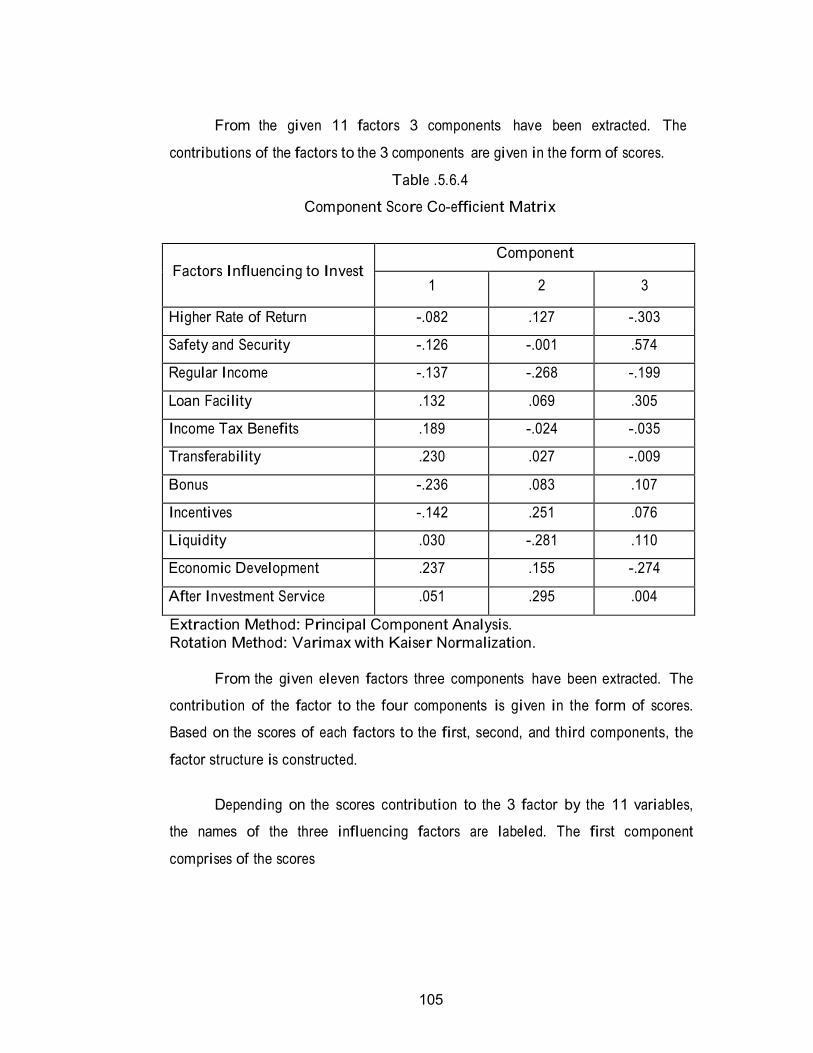

From the given 11 factors 3 components have been extracted. The

contributions of the factors to the 3 components are given in the form of scores.

Table .5.6.4

Component Score Co-efficient Matrix

Factors Influencing to Invest

Component

1 2 3

Higher Rate of Return -.082 .127 -.303

Safety and Security -.126 -.001 .574

Regular Income -.137 -.268 -.199

Loan Facility .132 .069 .305

Income Tax Benefits .189 -.024 -.035

Transferability .230 .027 -.009

Bonus -.236 .083 .107

Incentives -.142 .251 .076

Liquidity .030 -.281 .110

Economic Development .237 .155 -.274

After Investment Service .051 .295 .004

Extraction Method: Principal Component Analysis.

Rotation Method: Varimax with Kaiser Normalization.

From the given eleven factors three components have been extracted. The

contribution of the factor to the four components is given in the form of scores.

Based on the scores of each factors to the first, second, and third components, the

factor structure is constructed.

Depending on the scores contribution to the 3 factor by the 11 variables,

the names of the three influencing factors are labeled. The first component

comprises of the scores

106

Table .5.6.5

Factor Structure (0.1 cut off for significant loadings)

SI.No. Influencing

Factors

Variables

Score Co-efficient

i

Transfer and Tax Benefits

Economic Development 0.237

Transferability 0.230

Income tax benefits 0.189

ii

High Income and After Service

After investment Service 0.295

Incentives 0.251

Higher Rate of Return 0.127

iii

Safety and Bonus

Safety and Security 0.397

Loan Facility 0.305

Liquidity 0.110

Bonus 0.107

(i) Transfer and Tax Benefits

The first factor shows higher dominant variables in deciding the pre-taking

expectation in making investment decisions. The factor accounts for 35.127

percent of the total variance and has the Eigen value of 3.864. It is observed that

among the eleven variables listed in the table the transfer and tax benefits are

having positive higher score and hence researcher could say that they are

significantly influencing the decision to invest.

(ii) High Income and After Service

The second factor which influences decision to invest in postal Schemes is

High income and after service. This factor accounts for 25.351 percent of the total

variance and has the Eigen value of 2.789. It is observed that the high income and

after service are having positive higher score and hence researcher could say that

they are significantly influencing the investment decisions.

(iii) Safety and Bonus

The third factor which influences decision to invest in postal Schemes is

safety and Bonus. This factor accounts for 13.403 percent of the total variance and

has the Eigen value of 1.474. It is observed that safety and bonus are having

107

positive higher score and hence researcher could say that they are significantly

influencing the investment decisions.

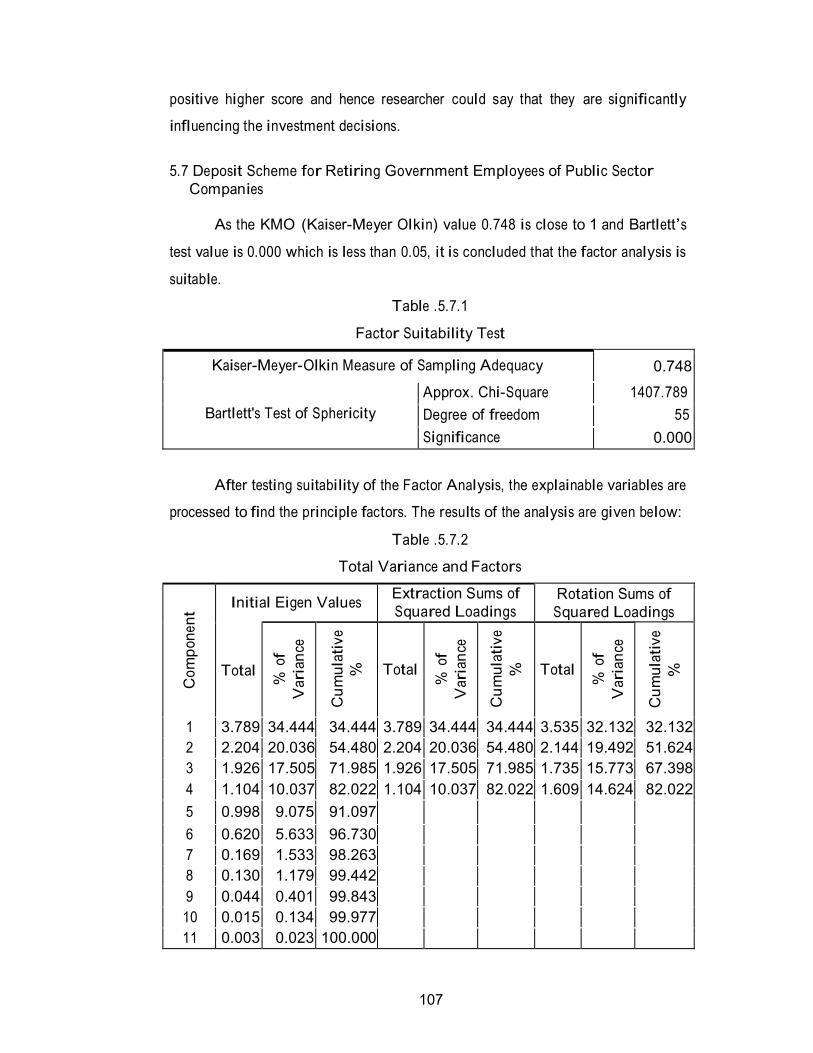

5.7 Deposit Scheme for Retiring Government Employees of Public Sector

Companies

As the KMO (Kaiser-Meyer Olkin) value 0.748 is close to 1 and Bartlett’s

test value is 0.000 which is less than 0.05, it is concluded that the factor analysis is

suitable.

Table .5.7.1

Factor Suitability Test

Kaiser-Meyer-Olkin Measure of Sampling Adequacy 0.748

Bartlett's Test of Sphericity

Approx. Chi-Square 1407.789

Degree of freedom 55

Significance 0.000

After testing suitability of the Factor Analysis, the explainable variables are

processed to find the principle factors. The results of the analysis are given below:

Table .5.7.2

Total Variance and Factors

C

om

pon

ent

Initial Eigen Values Extraction Sums of

Squared Loadings Rotation Sums of

Squared Loadings

Total

% o

f

Var

ian

ce

Cu

mula

tiv

e

%

Total

% o

f

Var

ian

ce

Cu

mula

tiv

e

%

Total

% o

f

Var

ian

ce

Cu

mula

tiv

e

%

1 3.789 34.444 34.444 3.789 34.444 34.444 3.535 32.132 32.132

2 2.204 20.036 54.480 2.204 20.036 54.480 2.144 19.492 51.624

3 1.926 17.505 71.985 1.926 17.505 71.985 1.735 15.773 67.398

4 1.104 10.037 82.022 1.104 10.037 82.022 1.609 14.624 82.022

5 0.998 9.075 91.097

6 0.620 5.633 96.730

7 0.169 1.533 98.263

8 0.130 1.179 99.442

9 0.044 0.401 99.843

10 0.015 0.134 99.977

11 0.003 0.023 100.000

108

Extraction Method: Principal Component Analysis.

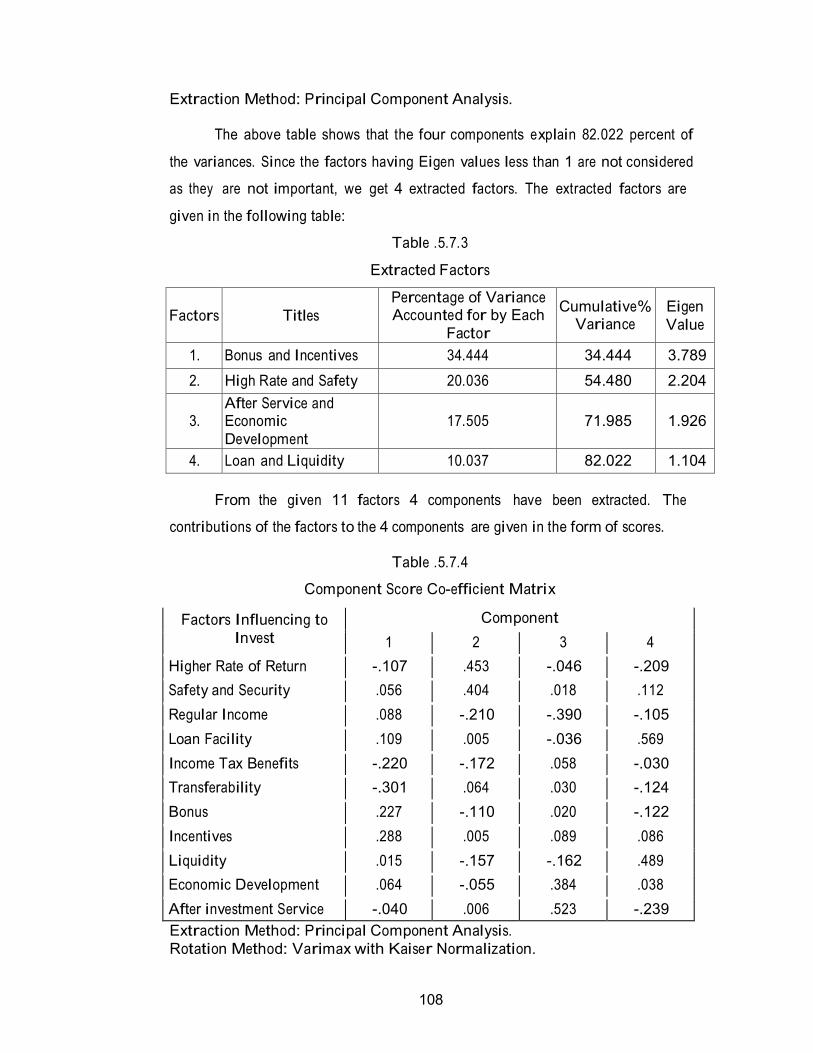

The above table shows that the four components explain 82.022 percent of

the variances. Since the factors having Eigen values less than 1 are not considered

as they are not important, we get 4 extracted factors. The extracted factors are

given in the following table:

Table .5.7.3

Extracted Factors

Factors

Titles

Percentage of Variance Accounted for by Each

Factor

Cumulative% Variance

Eigen

Value

1. Bonus and Incentives 34.444 34.444 3.789

2. High Rate and Safety 20.036 54.480 2.204

3.

After Service and Economic

Development

17.505

71.985

1.926

4. Loan and Liquidity 10.037 82.022 1.104

From the given 11 factors 4 components have been extracted. The

contributions of the factors to the 4 components are given in the form of scores.

Table .5.7.4

Component Score Co-efficient Matrix

Factors Influencing to

Invest

Component

1 2 3 4

Higher Rate of Return -.107 .453 -.046 -.209

Safety and Security .056 .404 .018 .112

Regular Income .088 -.210 -.390 -.105

Loan Facility .109 .005 -.036 .569

Income Tax Benefits -.220 -.172 .058 -.030

Transferability -.301 .064 .030 -.124

Bonus .227 -.110 .020 -.122

Incentives .288 .005 .089 .086

Liquidity .015 -.157 -.162 .489

Economic Development .064 -.055 .384 .038

After investment Service -.040 .006 .523 -.239

Extraction Method: Principal Component Analysis.

Rotation Method: Varimax with Kaiser Normalization.

109

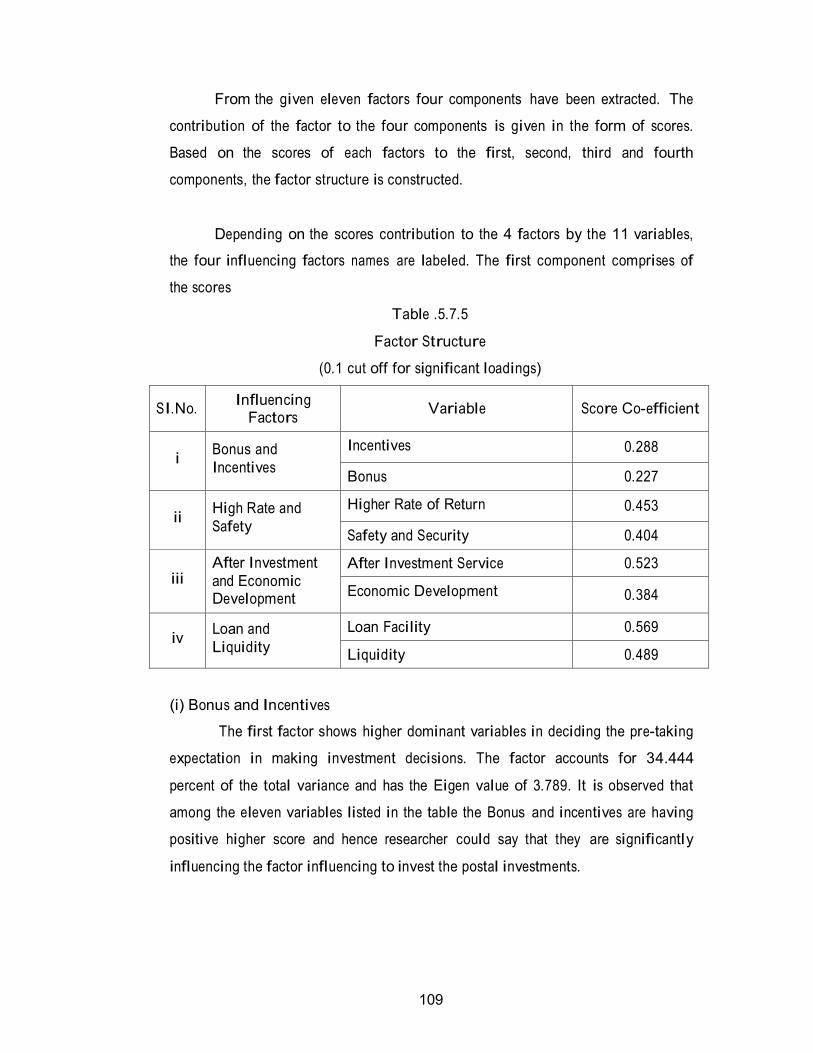

From the given eleven factors four components have been extracted. The

contribution of the factor to the four components is given in the form of scores.

Based on the scores of each factors to the first, second, third and fourth

components, the factor structure is constructed.

Depending on the scores contribution to the 4 factors by the 11 variables,

the four influencing factors names are labeled. The first component comprises of

the scores

Table .5.7.5

Factor Structure

(0.1 cut off for significant loadings)

SI.No. Influencing

Factors

Variable

Score Co-efficient

i

Bonus and

Incentives

Incentives 0.288

Bonus 0.227

ii

High Rate and

Safety

Higher Rate of Return 0.453

Safety and Security 0.404

iii

After Investment

and Economic Development

After Investment Service 0.523

Economic Development

0.384

iv

Loan and

Liquidity

Loan Facility 0.569

Liquidity 0.489

(i) Bonus and Incentives

The first factor shows higher dominant variables in deciding the pre-taking

expectation in making investment decisions. The factor accounts for 34.444

percent of the total variance and has the Eigen value of 3.789. It is observed that

among the eleven variables listed in the table the Bonus and incentives are having

positive higher score and hence researcher could say that they are significantly

influencing the factor influencing to invest the postal investments.

110

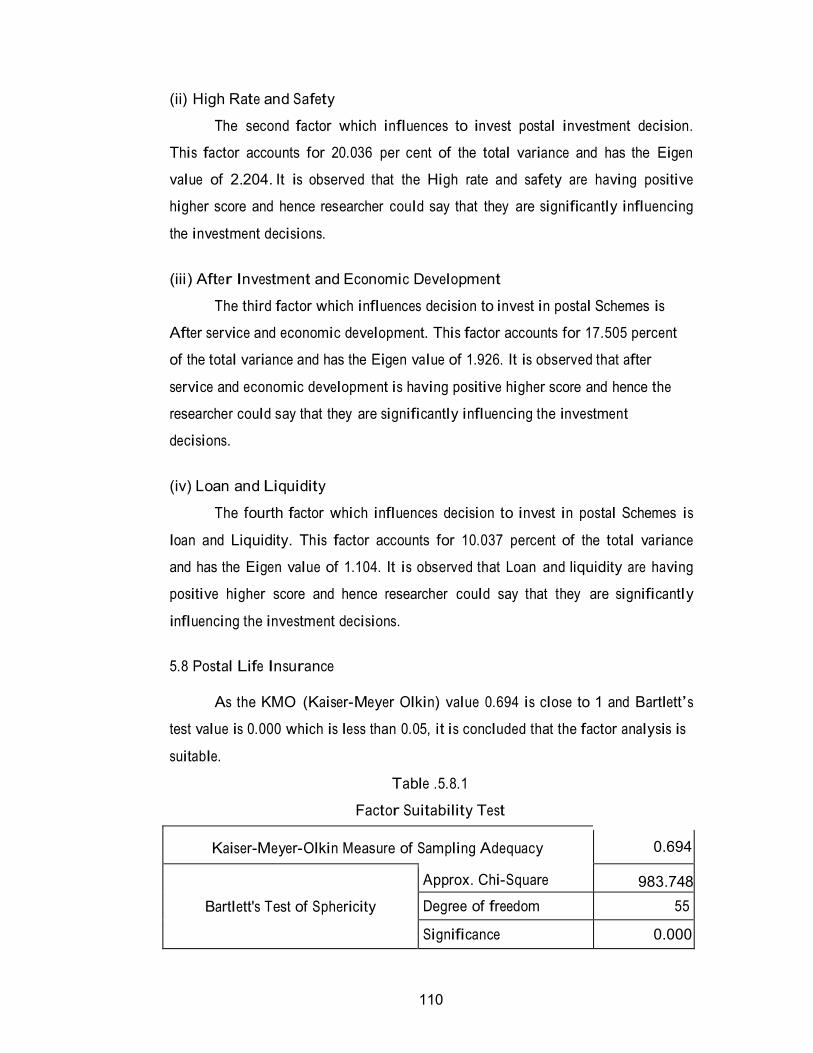

(ii) High Rate and Safety

The second factor which influences to invest postal investment decision.

This factor accounts for 20.036 per cent of the total variance and has the Eigen

value of 2.204. It is observed that the High rate and safety are having positive

higher score and hence researcher could say that they are significantly influencing

the investment decisions.

(iii) After Investment and Economic Development

The third factor which influences decision to invest in postal Schemes is

After service and economic development. This factor accounts for 17.505 percent

of the total variance and has the Eigen value of 1.926. It is observed that after

service and economic development is having positive higher score and hence the

researcher could say that they are significantly influencing the investment

decisions.

(iv) Loan and Liquidity

The fourth factor which influences decision to invest in postal Schemes is

loan and Liquidity. This factor accounts for 10.037 percent of the total variance

and has the Eigen value of 1.104. It is observed that Loan and liquidity are having

positive higher score and hence researcher could say that they are significantly

influencing the investment decisions.

5.8 Postal Life Insurance

As the KMO (Kaiser-Meyer Olkin) value 0.694 is close to 1 and Bartlett’s

test value is 0.000 which is less than 0.05, it is concluded that the factor analysis is

suitable.

Table .5.8.1

Factor Suitability Test

Kaiser-Meyer-Olkin Measure of Sampling Adequacy

0.694

Bartlett's Test of Sphericity

Approx. Chi-Square 983.748

Degree of freedom 55

Significance 0.000

111

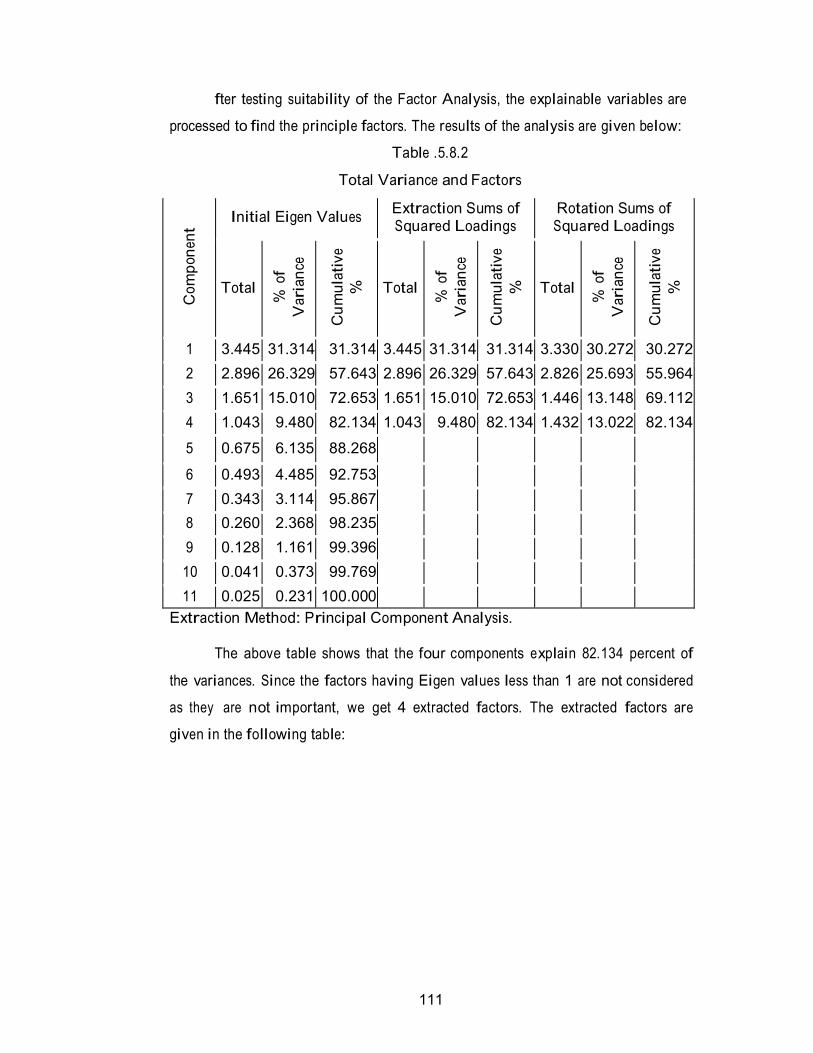

fter testing suitability of the Factor Analysis, the explainable variables are

processed to find the principle factors. The results of the analysis are given below:

Table .5.8.2

Total Variance and Factors

C

om

pon

ent

Initial Eigen Values Extraction Sums of Squared Loadings

Rotation Sums of Squared Loadings

Total

% o

f

Var

ian

ce

Cu

mula

tiv

e

%

Total

% o

f

Var

ian

ce

Cu

mula

tiv

e

%

Total

% o

f

Var

ian

ce

Cu

mula

tiv

e

%

1 3.445 31.314 31.314 3.445 31.314 31.314 3.330 30.272 30.272

2 2.896 26.329 57.643 2.896 26.329 57.643 2.826 25.693 55.964

3 1.651 15.010 72.653 1.651 15.010 72.653 1.446 13.148 69.112

4 1.043 9.480 82.134 1.043 9.480 82.134 1.432 13.022 82.134

5 0.675 6.135 88.268

6 0.493 4.485 92.753

7 0.343 3.114 95.867

8 0.260 2.368 98.235

9 0.128 1.161 99.396

10 0.041 0.373 99.769

11 0.025 0.231 100.000

Extraction Method: Principal Component Analysis.

The above table shows that the four components explain 82.134 percent of

the variances. Since the factors having Eigen values less than 1 are not considered

as they are not important, we get 4 extracted factors. The extracted factors are

given in the following table:

112

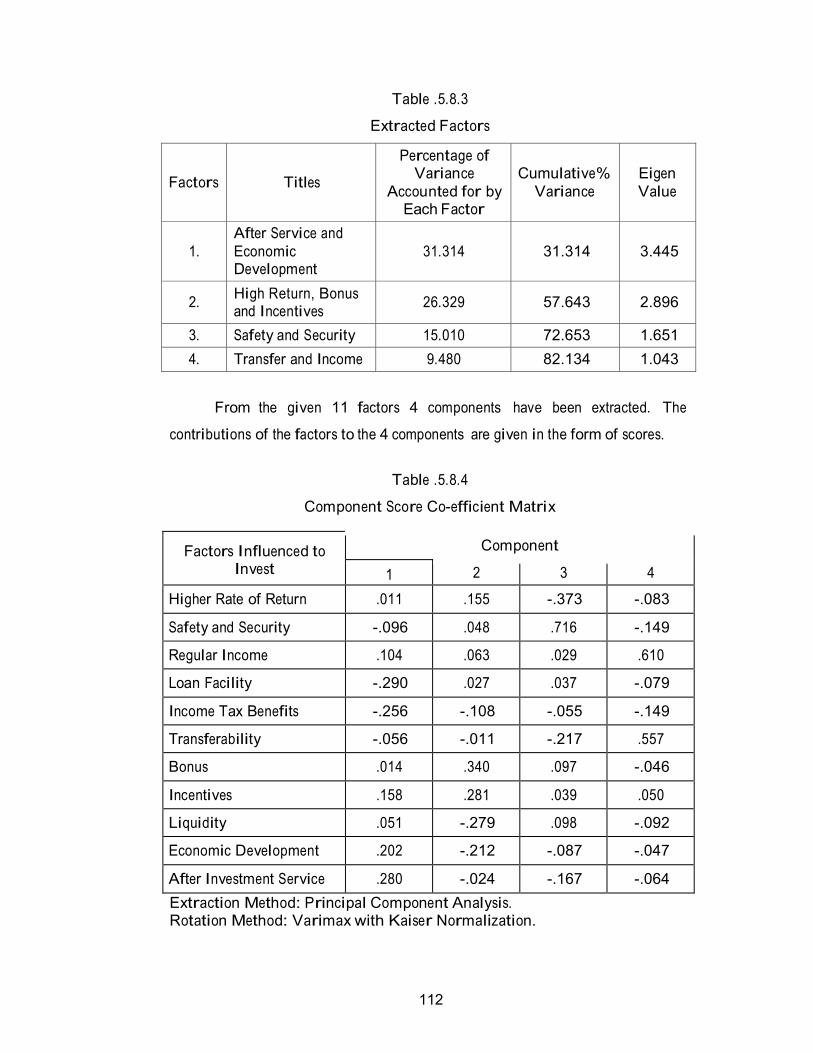

Table .5.8.3

Extracted Factors

Factors

Titles

Percentage of Variance

Accounted for by Each Factor

Cumulative%

Variance

Eigen

Value

1.

After Service and

Economic Development

31.314

31.314

3.445

2. High Return, Bonus and Incentives

26.329

57.643

2.896

3. Safety and Security 15.010 72.653 1.651

4. Transfer and Income 9.480 82.134 1.043

From the given 11 factors 4 components have been extracted. The

contributions of the factors to the 4 components are given in the form of scores.

Table .5.8.4

Component Score Co-efficient Matrix

Factors Influenced to Invest

Component

1 2 3 4

Higher Rate of Return .011 .155 -.373 -.083

Safety and Security -.096 .048 .716 -.149

Regular Income .104 .063 .029 .610

Loan Facility -.290 .027 .037 -.079

Income Tax Benefits -.256 -.108 -.055 -.149

Transferability -.056 -.011 -.217 .557

Bonus .014 .340 .097 -.046

Incentives .158 .281 .039 .050

Liquidity .051 -.279 .098 -.092

Economic Development .202 -.212 -.087 -.047

After Investment Service .280 -.024 -.167 -.064

Extraction Method: Principal Component Analysis. Rotation Method: Varimax with Kaiser Normalization.

113

From the given eleven factors four components have been extracted. The

contribution of the factor to the four components is given in the form of scores.

Based on the scores of each factors to the first, second, third and fourth

components, the factor structure is constructed.

Depending on the scores contribution to the 4 factors by the 11 variables,

the names of the four influencing factors are labeled. The first component

comprises of the scores.

Table .5.8.5

Factor Structure

(0.1 cut off for significant loadings)

SI.No. Influencing

Factors

Variable Score Co-

efficient

i

After Service and

Economic Development

After Investment Service 0.280

Economic Development

0.202

ii

High Return,

Bonus and Incentives

Bonus 0.340

Incentives 0.281

Higher Rate of Return 0.155

iii Safety and Security

Safety and Security

0.716

iv

Transfer and

Income

Regular Income

0.610

Transferability 0.557

(i) After Service and Economic Development

The first factor shows higher dominant variables in deciding the pre-taking

expectation in making investment decisions. The factor accounts for 31.314

percent of the total variance and has the Eigen value of 3.445. It is observed that

among the eleven variables listed in the table the after service and economic

development are having positive higher score and hence researcher could say that

they are significantly influencing the factor influencing to invest the postal

investments.

114

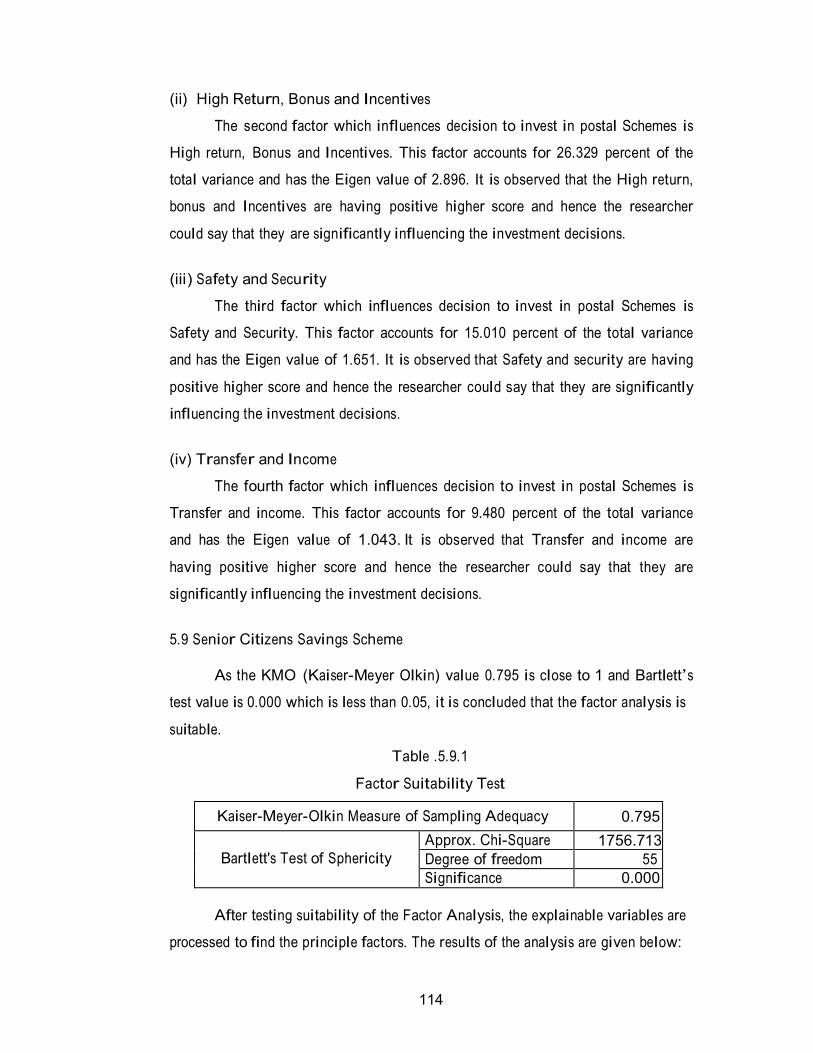

(ii) High Return, Bonus and Incentives

The second factor which influences decision to invest in postal Schemes is

High return, Bonus and Incentives. This factor accounts for 26.329 percent of the

total variance and has the Eigen value of 2.896. It is observed that the High return,

bonus and Incentives are having positive higher score and hence the researcher

could say that they are significantly influencing the investment decisions.

(iii) Safety and Security

The third factor which influences decision to invest in postal Schemes is

Safety and Security. This factor accounts for 15.010 percent of the total variance

and has the Eigen value of 1.651. It is observed that Safety and security are having

positive higher score and hence the researcher could say that they are significantly

influencing the investment decisions.

(iv) Transfer and Income

The fourth factor which influences decision to invest in postal Schemes is

Transfer and income. This factor accounts for 9.480 percent of the total variance

and has the Eigen value of 1.043. It is observed that Transfer and income are

having positive higher score and hence the researcher could say that they are

significantly influencing the investment decisions.

5.9 Senior Citizens Savings Scheme

As the KMO (Kaiser-Meyer Olkin) value 0.795 is close to 1 and Bartlett’s

test value is 0.000 which is less than 0.05, it is concluded that the factor analysis is

suitable.

Table .5.9.1

Factor Suitability Test

Kaiser-Meyer-Olkin Measure of Sampling Adequacy 0.795

Bartlett's Test of Sphericity

Approx. Chi-Square 1756.713

Degree of freedom 55

Significance 0.000

After testing suitability of the Factor Analysis, the explainable variables are

processed to find the principle factors. The results of the analysis are given below:

115

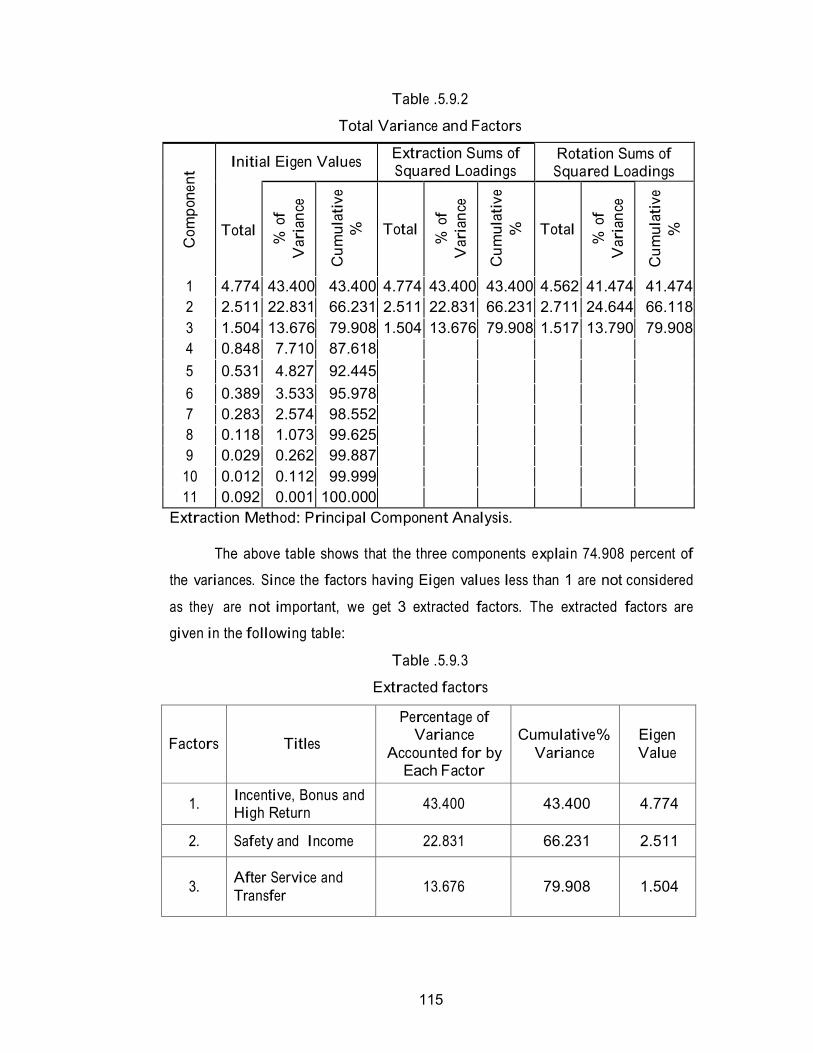

Table .5.9.2

Total Variance and Factors

C

om

pon

ent

Initial Eigen Values Extraction Sums of Squared Loadings

Rotation Sums of Squared Loadings

Total

% o

f

Var

ian

ce

Cu

mula

tiv

e

%

Total

% o

f

Var

ian

ce

Cu

mula

tiv

e

%

Total

% o

f

Var

ian

ce

Cu

mula

tiv

e

%

1 4.774 43.400 43.400 4.774 43.400 43.400 4.562 41.474 41.474

2 2.511 22.831 66.231 2.511 22.831 66.231 2.711 24.644 66.118

3 1.504 13.676 79.908 1.504 13.676 79.908 1.517 13.790 79.908

4 0.848 7.710 87.618

5 0.531 4.827 92.445

6 0.389 3.533 95.978

7 0.283 2.574 98.552

8 0.118 1.073 99.625

9 0.029 0.262 99.887

10 0.012 0.112 99.999

11 0.092 0.001 100.000

Extraction Method: Principal Component Analysis.

The above table shows that the three components explain 74.908 percent of

the variances. Since the factors having Eigen values less than 1 are not considered

as they are not important, we get 3 extracted factors. The extracted factors are

given in the following table:

Table .5.9.3

Extracted factors

Factors

Titles

Percentage of Variance

Accounted for by Each Factor

Cumulative%

Variance

Eigen

Value

1. Incentive, Bonus and High Return

43.400

43.400

4.774

2.

Safety and Income

22.831

66.231

2.511

3.

After Service and

Transfer

13.676

79.908

1.504

116

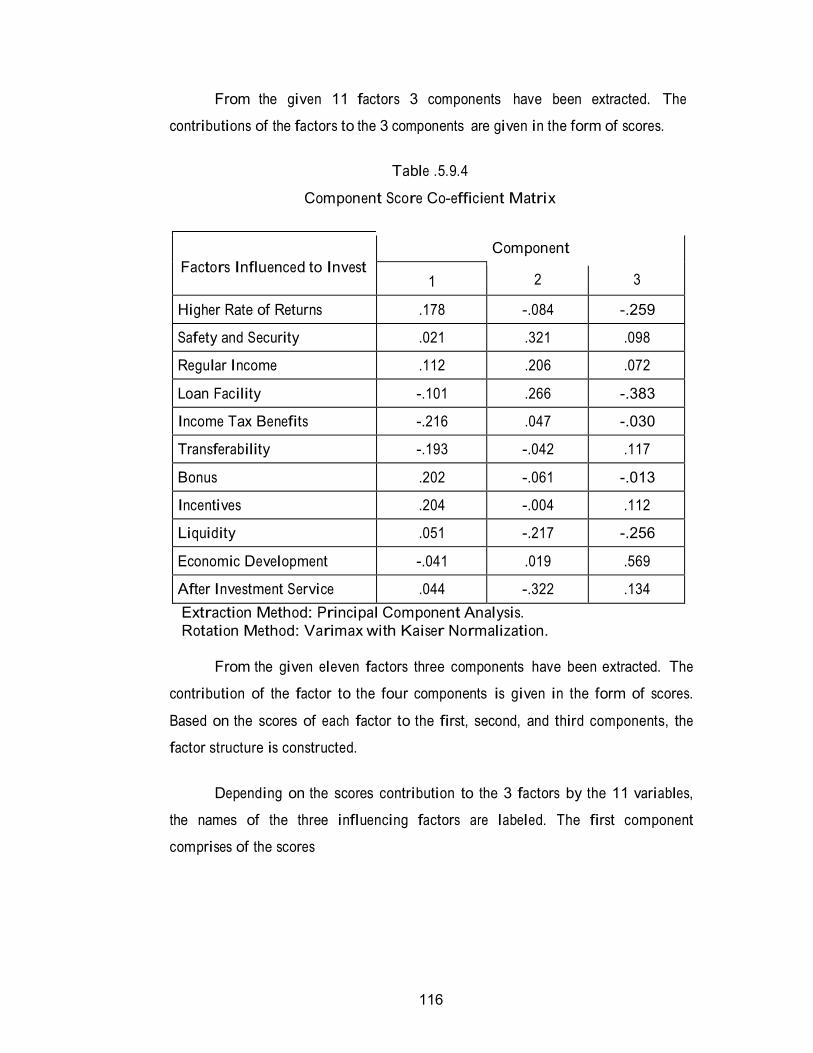

From the given 11 factors 3 components have been extracted. The

contributions of the factors to the 3 components are given in the form of scores.

Table .5.9.4

Component Score Co-efficient Matrix

Factors Influenced to Invest

Component

1 2 3

Higher Rate of Returns .178 -.084 -.259

Safety and Security .021 .321 .098

Regular Income .112 .206 .072

Loan Facility -.101 .266 -.383

Income Tax Benefits -.216 .047 -.030

Transferability -.193 -.042 .117

Bonus .202 -.061 -.013

Incentives .204 -.004 .112

Liquidity .051 -.217 -.256

Economic Development -.041 .019 .569

After Investment Service .044 -.322 .134

Extraction Method: Principal Component Analysis.

Rotation Method: Varimax with Kaiser Normalization.

From the given eleven factors three components have been extracted. The

contribution of the factor to the four components is given in the form of scores.

Based on the scores of each factor to the first, second, and third components, the

factor structure is constructed.

Depending on the scores contribution to the 3 factors by the 11 variables,

the names of the three influencing factors are labeled. The first component

comprises of the scores

117

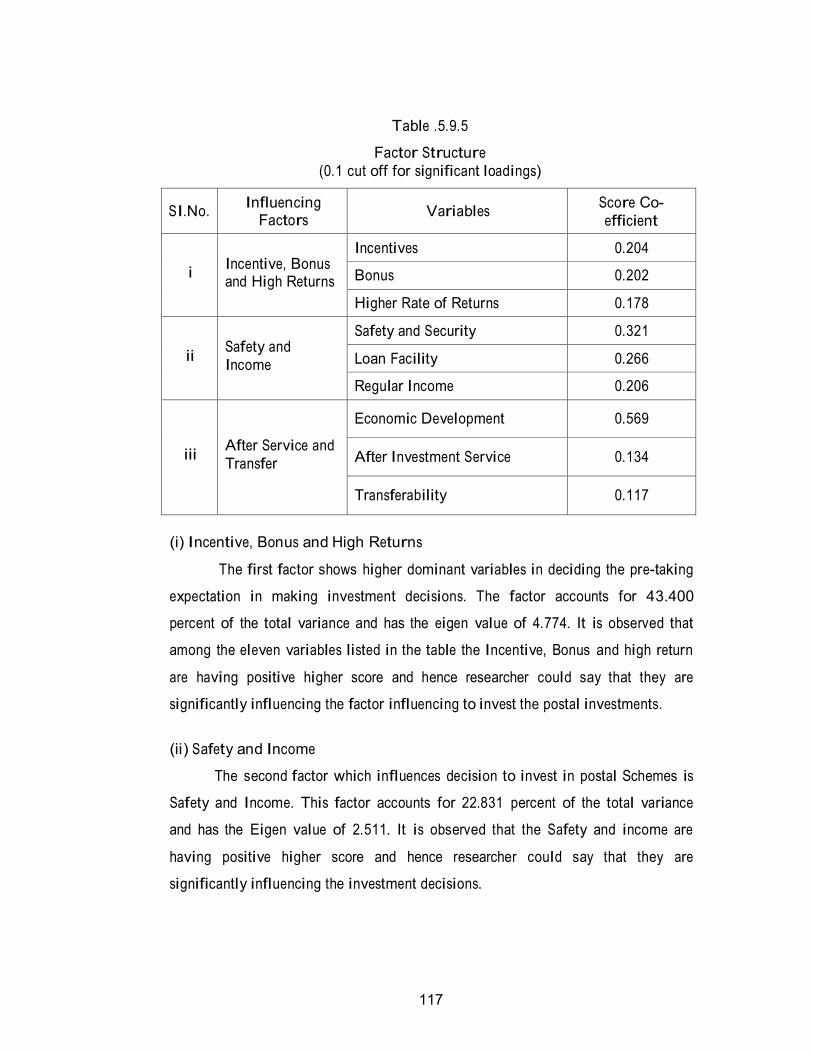

Table .5.9.5

Factor Structure

(0.1 cut off for significant loadings)

SI.No. Influencing

Factors

Variables Score Co-

efficient

i

Incentive, Bonus and High Returns

Incentives 0.204

Bonus 0.202

Higher Rate of Returns 0.178

ii

Safety and

Income

Safety and Security 0.321

Loan Facility 0.266

Regular Income 0.206

iii

After Service and

Transfer

Economic Development

0.569

After Investment Service

0.134

Transferability

0.117

(i) Incentive, Bonus and High Returns

The first factor shows higher dominant variables in deciding the pre-taking

expectation in making investment decisions. The factor accounts for 43.400

percent of the total variance and has the eigen value of 4.774. It is observed that

among the eleven variables listed in the table the Incentive, Bonus and high return

are having positive higher score and hence researcher could say that they are

significantly influencing the factor influencing to invest the postal investments.

(ii) Safety and Income

The second factor which influences decision to invest in postal Schemes is

Safety and Income. This factor accounts for 22.831 percent of the total variance

and has the Eigen value of 2.511. It is observed that the Safety and income are

having positive higher score and hence researcher could say that they are

significantly influencing the investment decisions.

118

(iii) After Service and Transfer

The third factor which influences decision to invest in postal Schemes is

After service and transfer. This factor accounts for 13.676 percent of the total

variance and has the Eigen value of 1.504. It is observed that after service and

transfer are having positive higher score and hence researcher could say that they

are significantly influencing the investment decisions.

5.10 Analysis of Variance (ANOVA)

5.10.1 Age and Maturity Period of Postal Investments

Null Hypothesis Ho: There is no significant difference among mean scores

of the maturity period of postal investments and different age group of

respondents. The following table shows that the Age Group of Respondents and

Maturity period Postal Investment.

Table .5.10.1 Panel (a)

Test of Hypothesis: Age Group of Respondents and Maturity Period Postal

Investment

Sl.No.

Age

N

Mean Std.

Deviation

1. Up to 30 206 2.17 1.141

2. 31-45 156 1.94 0.759

3. 46-55 126 2.92 1.269

4. 56 and above 112 1.94 1.180

Total 600 2.22 1.153

Panel (a)

Sl.No. Source of

Variation

Sum of

Squares

df Mean

Square

F Value Level of

Significance

1. Between Groups

83.892

3

27.964

23.402

0.000

2. Within Groups

712.181

596

1.195

Total 796.073 599

119

The Null Hypothesis is rejected as ‘P’ value is less than 0.05. The maturity

period postal investments and different age group of respondents. Therefore it is

concluded that there is significant difference among mean scores of the maturity

period postal investments and different age group of respondents.

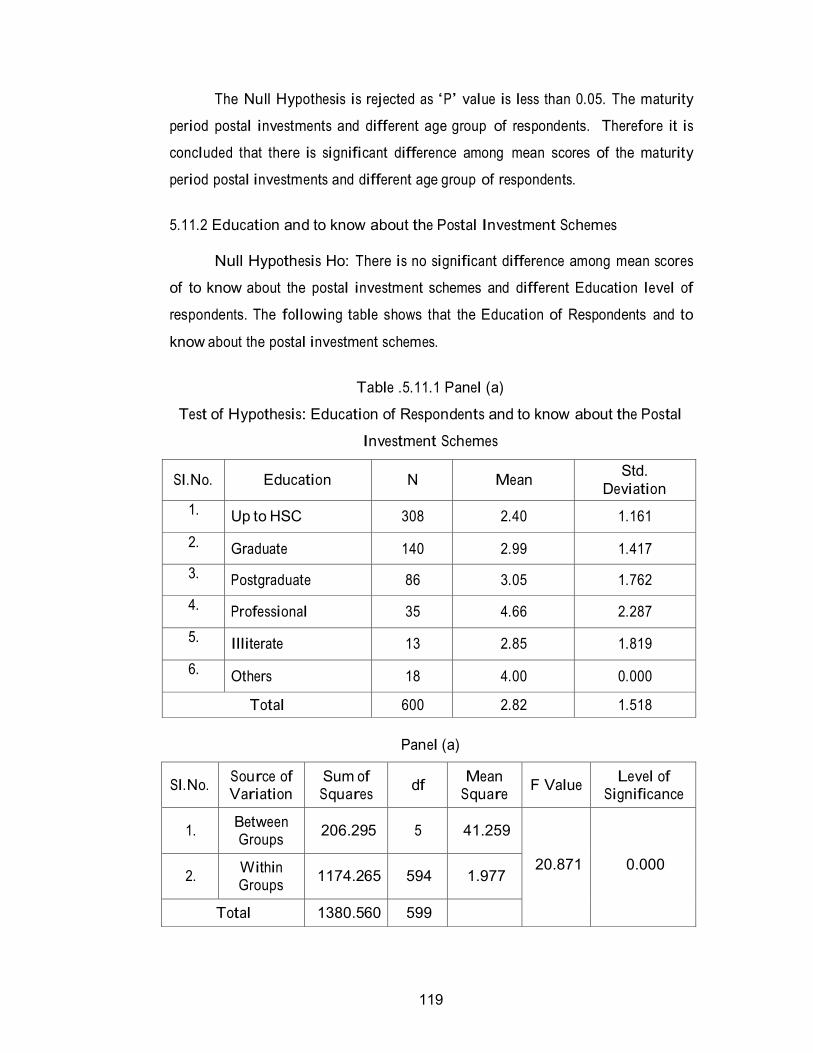

5.11.2 Education and to know about the Postal Investment Schemes

Null Hypothesis Ho: There is no significant difference among mean scores

of to know about the postal investment schemes and different Education level of

respondents. The following table shows that the Education of Respondents and to

know about the postal investment schemes.

Table .5.11.1 Panel (a)

Test of Hypothesis: Education of Respondents and to know about the Postal

Investment Schemes

Sl.No.

Education

N

Mean Std.

Deviation

1.

Up to HSC

308

2.40

1.161

2. Graduate 140 2.99 1.417

3. Postgraduate 86 3.05 1.762

4.

Professional

35

4.66

2.287

5.

Illiterate

13

2.85

1.819

6.

Others

18

4.00

0.000

Total 600 2.82 1.518

Panel (a)

Sl.No. Source of Variation

Sum of Squares

df Mean

Square

F Value Level of

Significance

1. Between Groups

206.295

5

41.259

20.871

0.000

2. Within Groups

1174.265

594

1.977

Total 1380.560 599

120

The Null Hypothesis is rejected as ‘P’ value is less than 0.05. Know about

the postal investment schemes and different Education level of respondents.

Therefore it is concluded that there is significant difference among mean scores of

know about the postal investment schemes and different Education level of

respondents.

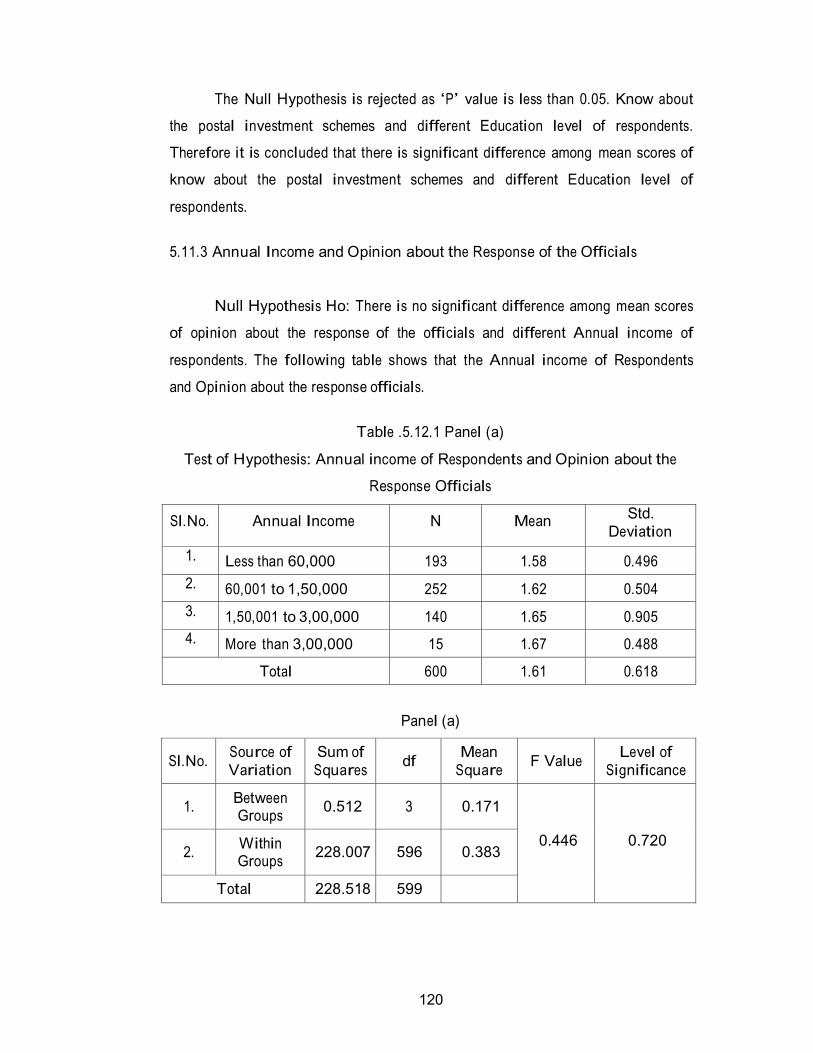

5.11.3 Annual Income and Opinion about the Response of the Officials

Null Hypothesis Ho: There is no significant difference among mean scores

of opinion about the response of the officials and different Annual income of

respondents. The following table shows that the Annual income of Respondents

and Opinion about the response officials.

Table .5.12.1 Panel (a)

Test of Hypothesis: Annual income of Respondents and Opinion about the

Response Officials

Sl.No.

Annual Income

N

Mean Std.

Deviation

1. Less than 60,000 193 1.58 0.496

2. 60,001 to 1,50,000 252 1.62 0.504

3. 1,50,001 to 3,00,000 140 1.65 0.905

4. More than 3,00,000 15 1.67 0.488

Total 600 1.61 0.618

Panel (a)

Sl.No. Source of

Variation

Sum of

Squares

df Mean

Square

F Value Level of

Significance

1. Between Groups

0.512

3

0.171

0.446

0.720

2. Within Groups

228.007

596

0.383

Total 228.518 599

121

The Null Hypothesis is accepted as ‘P’ value is greater than 0.05. Opinion

about the response of the officials and Income level of respondents. Therefore it is

concluded that there is significant difference among mean scores of Opinion about

the response of the officials and Income level of respondents.

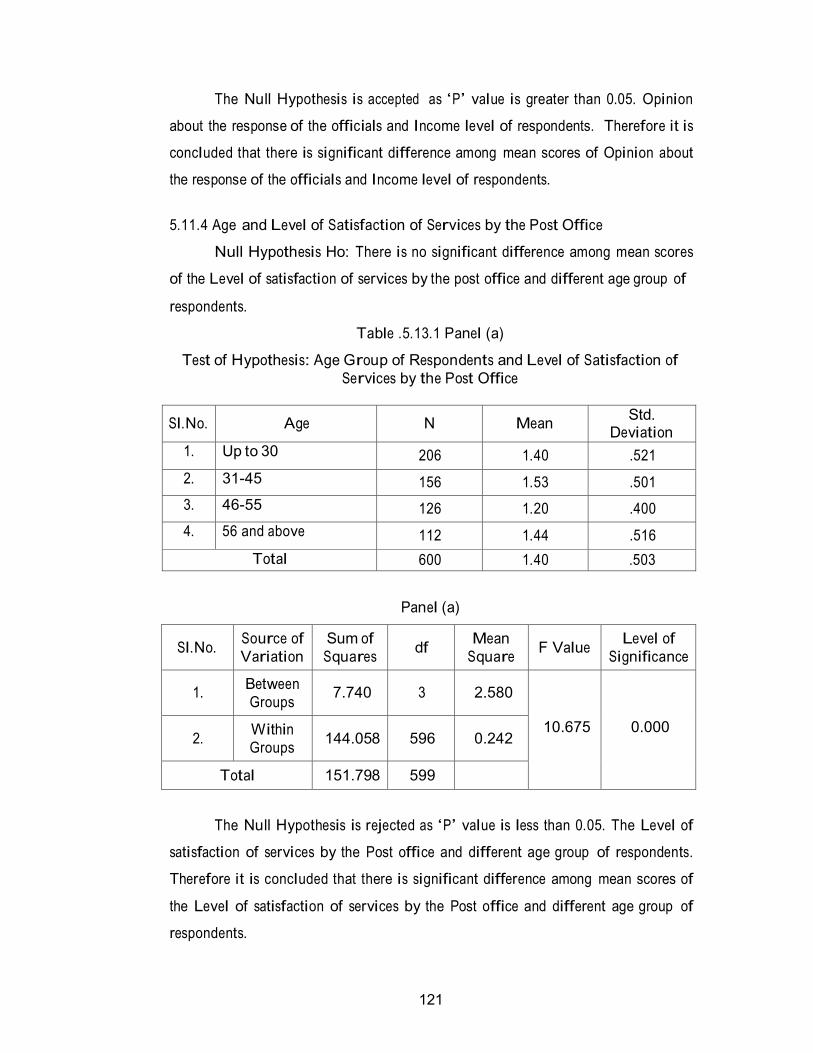

5.11.4 Age and Level of Satisfaction of Services by the Post Office

Null Hypothesis Ho: There is no significant difference among mean scores

of the Level of satisfaction of services by the post office and different age group of

respondents.

Table .5.13.1 Panel (a)

Test of Hypothesis: Age Group of Respondents and Level of Satisfaction of

Services by the Post Office

Sl.No.

Age

N

Mean Std.

Deviation

1. Up to 30 206 1.40 .521

2. 31-45 156 1.53 .501

3. 46-55 126 1.20 .400

4. 56 and above 112 1.44 .516

Total 600 1.40 .503

Panel (a)

Sl.No. Source of

Variation

Sum of

Squares

df Mean

Square

F Value Level of

Significance

1. Between

Groups

7.740

3

2.580

10.675

0.000

2. Within

Groups

144.058

596

0.242

Total 151.798 599

The Null Hypothesis is rejected as ‘P’ value is less than 0.05. The Level of

satisfaction of services by the Post office and different age group of respondents.

Therefore it is concluded that there is significant difference among mean scores of

the Level of satisfaction of services by the Post office and different age group of

respondents.

122

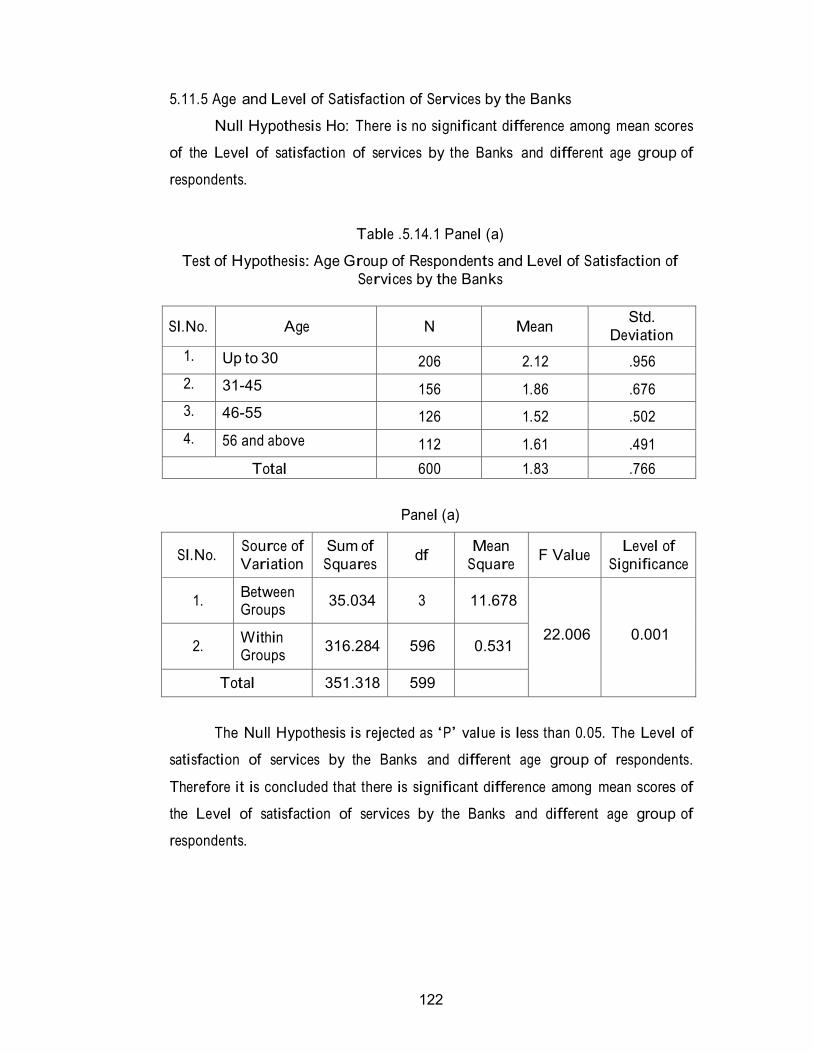

5.11.5 Age and Level of Satisfaction of Services by the Banks

Null Hypothesis Ho: There is no significant difference among mean scores

of the Level of satisfaction of services by the Banks and different age group of

respondents.

Table .5.14.1 Panel (a)

Test of Hypothesis: Age Group of Respondents and Level of Satisfaction of

Services by the Banks

Sl.No.

Age

N

Mean Std.

Deviation

1. Up to 30 206 2.12 .956

2. 31-45 156 1.86 .676

3. 46-55 126 1.52 .502

4. 56 and above 112 1.61 .491

Total 600 1.83 .766

Panel (a)

Sl.No. Source of

Variation

Sum of

Squares

df Mean

Square

F Value Level of

Significance

1. Between Groups

35.034

3

11.678

22.006

0.001

2. Within Groups

316.284

596

0.531

Total 351.318 599

The Null Hypothesis is rejected as ‘P’ value is less than 0.05. The Level of

satisfaction of services by the Banks and different age group of respondents.

Therefore it is concluded that there is significant difference among mean scores of

the Level of satisfaction of services by the Banks and different age group of

respondents.

123

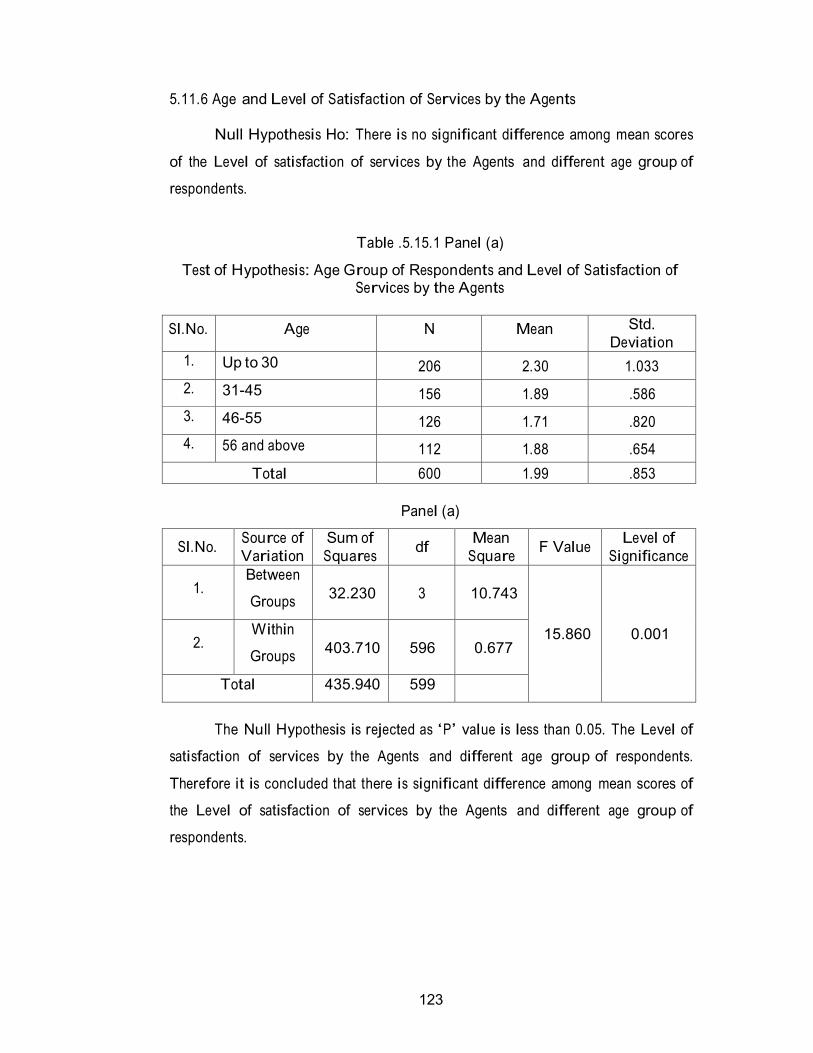

5.11.6 Age and Level of Satisfaction of Services by the Agents

Null Hypothesis Ho: There is no significant difference among mean scores

of the Level of satisfaction of services by the Agents and different age group of

respondents.

Table .5.15.1 Panel (a)

Test of Hypothesis: Age Group of Respondents and Level of Satisfaction of Services by the Agents

Sl.No. Age N Mean Std.

Deviation

1. Up to 30 206 2.30 1.033

2. 31-45 156 1.89 .586

3. 46-55 126 1.71 .820

4. 56 and above 112 1.88 .654

Total 600 1.99 .853

Panel (a)

Sl.No. Source of

Variation

Sum of

Squares

df Mean

Square

F Value Level of

Significance

1. Between

Groups

32.230

3

10.743

15.860

0.001

2. Within

Groups

403.710

596

0.677

Total 435.940 599

The Null Hypothesis is rejected as ‘P’ value is less than 0.05. The Level of

satisfaction of services by the Agents and different age group of respondents.

Therefore it is concluded that there is significant difference among mean scores of

the Level of satisfaction of services by the Agents and different age group of

respondents.

124

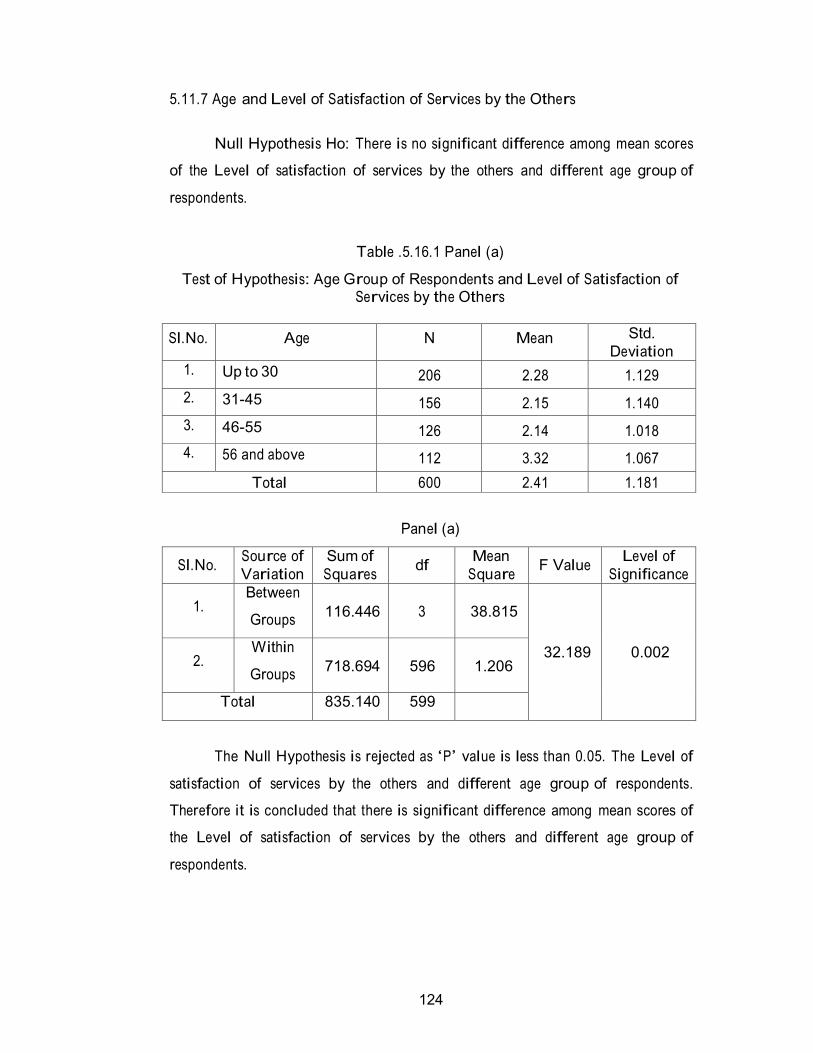

5.11.7 Age and Level of Satisfaction of Services by the Others

Null Hypothesis Ho: There is no significant difference among mean scores

of the Level of satisfaction of services by the others and different age group of

respondents.

Table .5.16.1 Panel (a)

Test of Hypothesis: Age Group of Respondents and Level of Satisfaction of Services by the Others

Sl.No. Age N Mean Std.

Deviation

1. Up to 30 206 2.28 1.129

2. 31-45 156 2.15 1.140

3. 46-55 126 2.14 1.018

4. 56 and above 112 3.32 1.067

Total 600 2.41 1.181

Panel (a)

Sl.No. Source of

Variation

Sum of

Squares

df Mean

Square

F Value Level of

Significance

1. Between

Groups

116.446

3

38.815

32.189

0.002

2. Within

Groups

718.694

596

1.206

Total 835.140 599

The Null Hypothesis is rejected as ‘P’ value is less than 0.05. The Level of

satisfaction of services by the others and different age group of respondents.

Therefore it is concluded that there is significant difference among mean scores of

the Level of satisfaction of services by the others and different age group of

respondents.

125

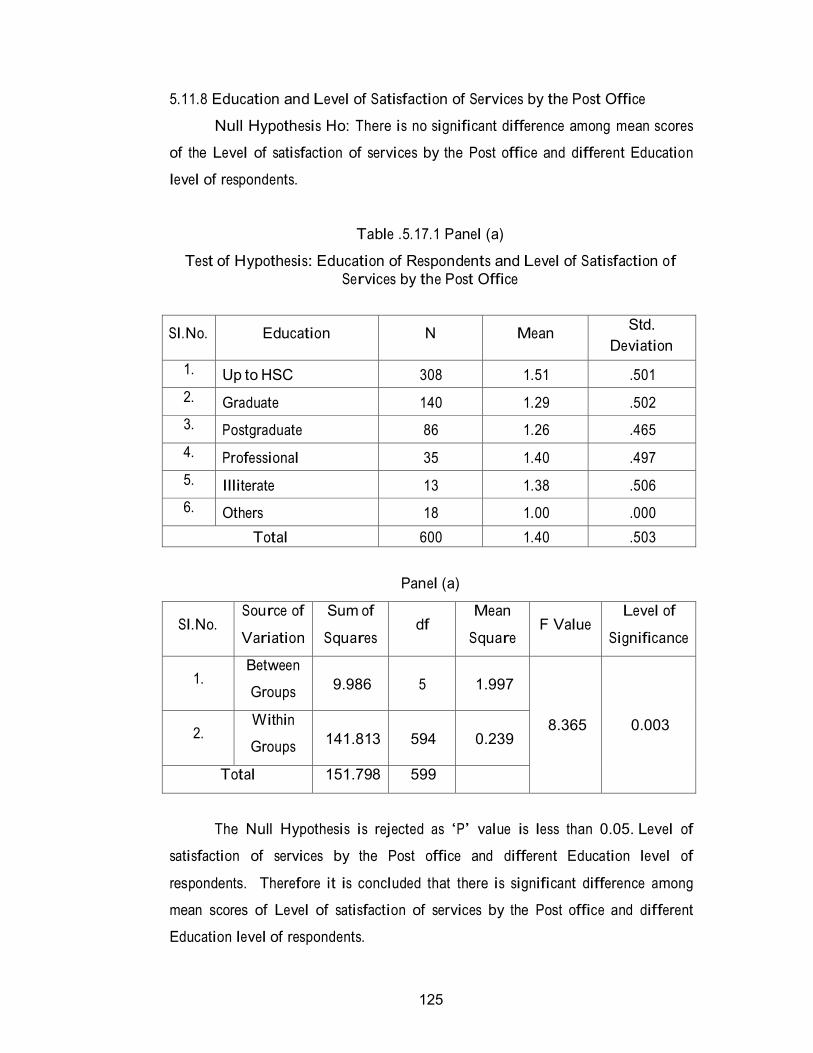

5.11.8 Education and Level of Satisfaction of Services by the Post Office

Null Hypothesis Ho: There is no significant difference among mean scores

of the Level of satisfaction of services by the Post office and different Education

level of respondents.

Table .5.17.1 Panel (a)

Test of Hypothesis: Education of Respondents and Level of Satisfaction of

Services by the Post Office

Sl.No.

Education

N

Mean Std.

Deviation

1. Up to HSC 308 1.51 .501

2. Graduate 140 1.29 .502

3. Postgraduate 86 1.26 .465

4. Professional 35 1.40 .497

5. Illiterate 13 1.38 .506

6. Others 18 1.00 .000

Total 600 1.40 .503

Panel (a)

Sl.No. Source of

Variation

Sum of

Squares

df Mean

Square

F Value Level of

Significance

1. Between

Groups

9.986

5

1.997

8.365

0.003

2. Within

Groups

141.813

594

0.239

Total 151.798 599

The Null Hypothesis is rejected as ‘P’ value is less than 0.05. Level of

satisfaction of services by the Post office and different Education level of

respondents. Therefore it is concluded that there is significant difference among

mean scores of Level of satisfaction of services by the Post office and different

Education level of respondents.

126

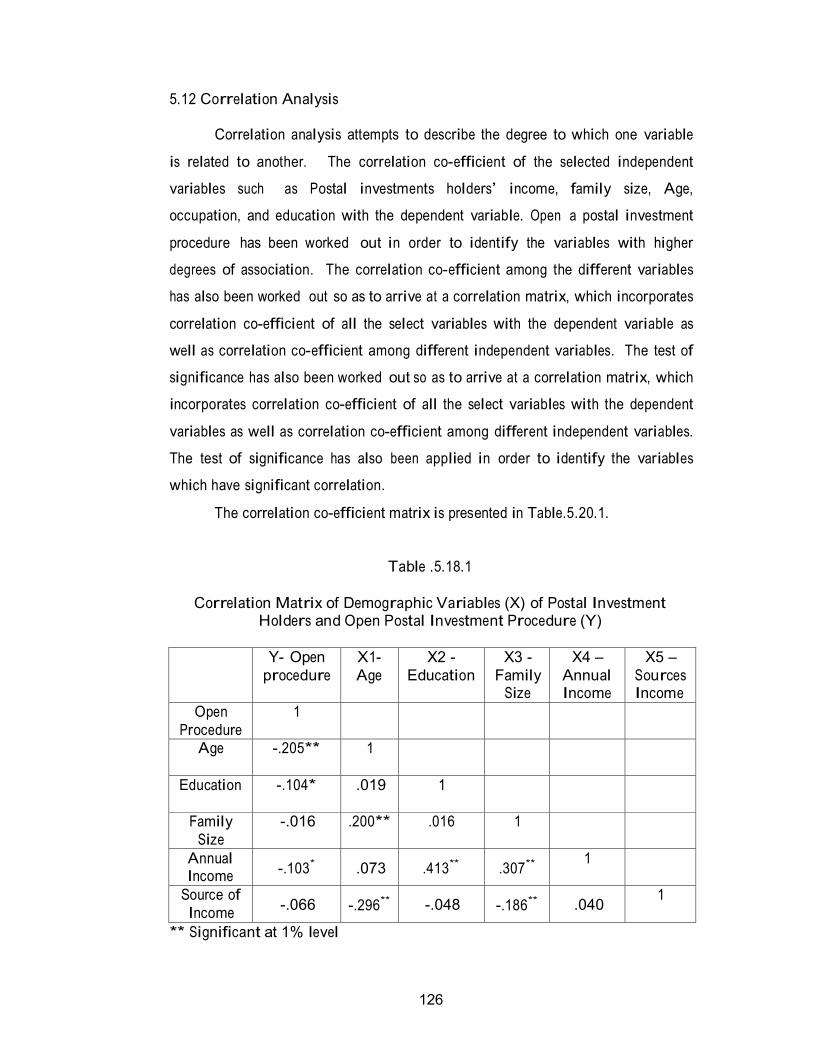

5.12 Correlation Analysis

Correlation analysis attempts to describe the degree to which one variable

is related to another. The correlation co-efficient of the selected independent

variables such as Postal investments holders’ income, family size, Age,

occupation, and education with the dependent variable. Open a postal investment

procedure has been worked out in order to identify the variables with higher

degrees of association. The correlation co-efficient among the different variables

has also been worked out so as to arrive at a correlation matrix, which incorporates

correlation co-efficient of all the select variables with the dependent variable as

well as correlation co-efficient among different independent variables. The test of

significance has also been worked out so as to arrive at a correlation matrix, which

incorporates correlation co-efficient of all the select variables with the dependent

variables as well as correlation co-efficient among different independent variables.

The test of significance has also been applied in order to identify the variables

which have significant correlation.

The correlation co-efficient matrix is presented in Table.5.20.1.

Table .5.18.1

Correlation Matrix of Demographic Variables (X) of Postal Investment

Holders and Open Postal Investment Procedure (Y)

Y- Open

procedure

X1-

Age

X2 -

Education

X3 -

Family Size

X4 –

Annual Income

X5 –

Sources Income

Open

Procedure

1

Age -.205** 1

Education -.104* .019 1

Family

Size

-.016 .200** .016 1

Annual Income

-.103*

.073

.413**

.307** 1

Source of

Income

-.066

-.296**

-.048

-.186**

.040 1

** Significant at 1% level

127

Table.5.20.1 shows the inter-correlation between demographic

characteristics of postal investment holders and open postal investment procedure.

The open postal investment is significantly and positively correlated with Annual

income of the Postal investment holders, their family size, and Source of income.

This in turn indicates that higher the income, the family size, and the Source

income, the open postal investment procedure is independent of the postal

investment holders’ occupation as well as education since the correlation

coefficient between them is non-significant. A few independent variables are

significantly correlated with each other. Family income has significant correlation

with family size and source of income. Family size and occupation of postal

investment holder and education have significant positive correlation.

Section Summary

An overview of the details presented in this chapter shows that most of the

sample investors in any category expect to have safety and security on their

investment.

This chapter has presented an analysis of the several factors that motivated

and influenced the investors in their investment and their expected safety and

security on their investment. The next chapter deals with the attitude of the

investors towards postal investment.