Embed Size (px)

Citation preview

1

Chapter Seventeen

Using Accounting Information

Learning Objectives1. Explain why accounting information and audited financial

statements are important.

2 Id tif th l h ti i f ti d2. Identify the people who use accounting information and possible careers in the accounting industry.

3. Discuss the accounting process.

4. Read and interpret a balance sheet.

5. Read and interpret an income statement.

Copyright © Cengage Learning. All rights reserved. 17| 2

6. Describe business activities that affect a firm’s cash flow.

7. Summarize how managers evaluate the financial health of a business.

2

Chapter 17 Outline

– Why Accounting Information Is Important• Recent Accounting Problems for Corporations and Their g p

Auditors• Why Audited Financial Statements Are Important• Reform: The Sarbanes‐Oxley Act of 2002

– Who Uses Accounting Information?• The People Who Use Accounting Information• Different Types of Accounting• Careers in Accounting

– The Accounting Process• The Accounting Equation• The Accounting Cycle

Copyright © Cengage Learning. All rights reserved. 17| 3

Chapter 17 Outline (cont’d)

– The Balance SheetA t• Assets

• Liabilities and Owners’ Equity

– The Income Statement• Revenues

• Cost of Goods Sold

• Operating Expenses• Operating Expenses

• Net Income

– The Statement of Cash Flows

Copyright © Cengage Learning. All rights reserved. 17| 4

3

Chapter 17 Outline (cont’d)

– Evaluating Financial StatementsU i A l R t t C D t f Diff t• Using Annual Reports to Compare Data for Different Accounting Periods

• Comparing Data with Other Firms’ Data

• Profitability Ratios

• Short‐Term Financial Ratios

• Activity Ratiosy

• Debt‐to‐Owners’ Equity Ratio

• Northeast’s Financial Ratios: A Summary

Copyright © Cengage Learning. All rights reserved. 17| 5

Why Accounting Information Is Important

• Recent accounting problems for corporations and their auditors– Pressure on corporate executives to look good

to analysts and investors

• Why audited financial statements are important

B k dit i t d t

Copyright © Cengage Learning. All rights reserved. 17| 6

– Bankers, creditors, investors, and government agencies rely on an auditor’s opinion

4

Why Accounting Information Is Important (cont’d)

• What is an audit?

• Reform: The Sarbanes‐Oxley Act of 2002

Copyright © Cengage Learning. All rights reserved. 17| 7

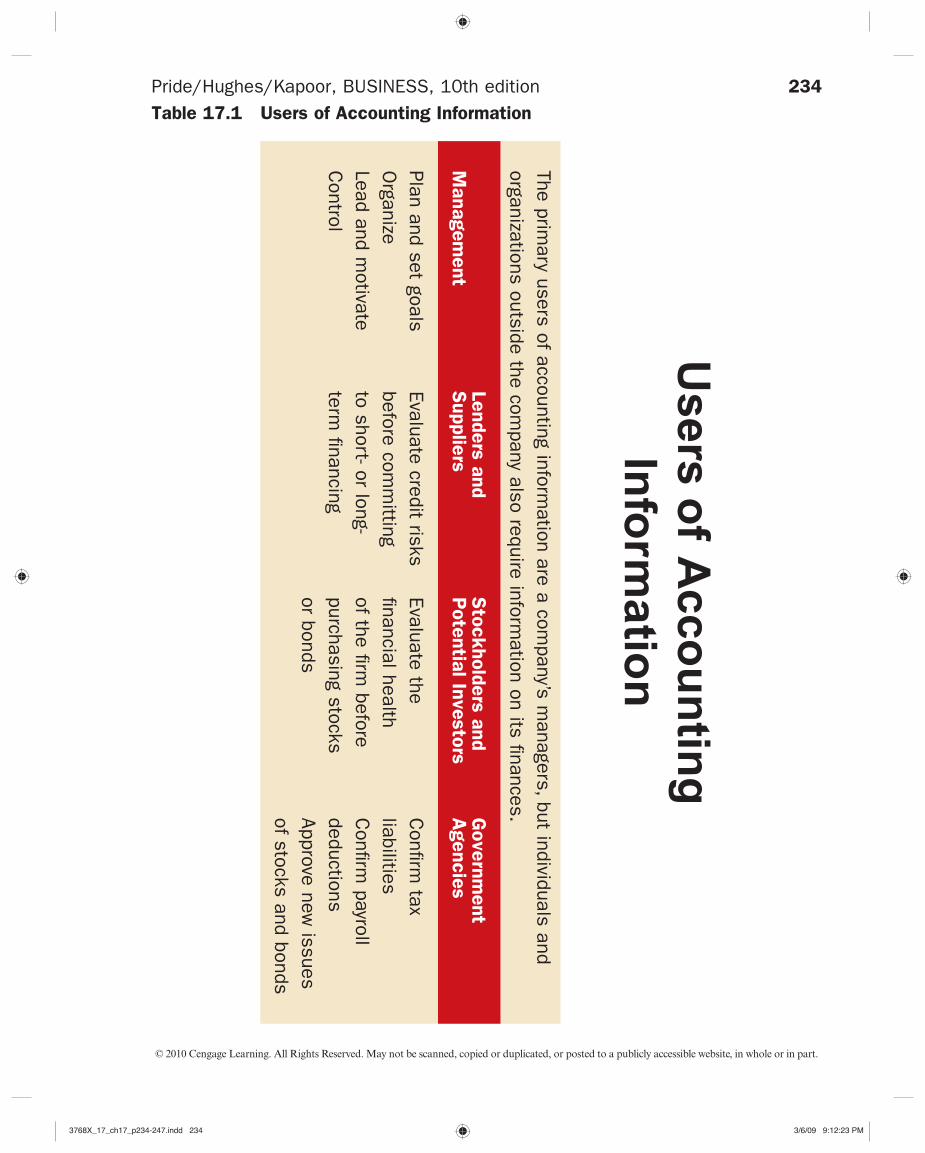

Who Uses Accounting Information • The people who use accounting information

– Managers are primary usersg p y

– Lenders require financial information before lending

– Stockholders want to know whether to invest or how well their investment is doing

– Government agencies require a variety of information

Copyright © Cengage Learning. All rights reserved. 17| 8

information

5

Careers in Accounting• Qualities to be successful in accounting

– Be responsible, honest, ethicalBe responsible, honest, ethical

– Have a strong background in financial management

– Know how to use a computer and accounting software

– Be able to communicate with people who need accounting information

Copyright © Cengage Learning. All rights reserved. 17| 9

accounting information

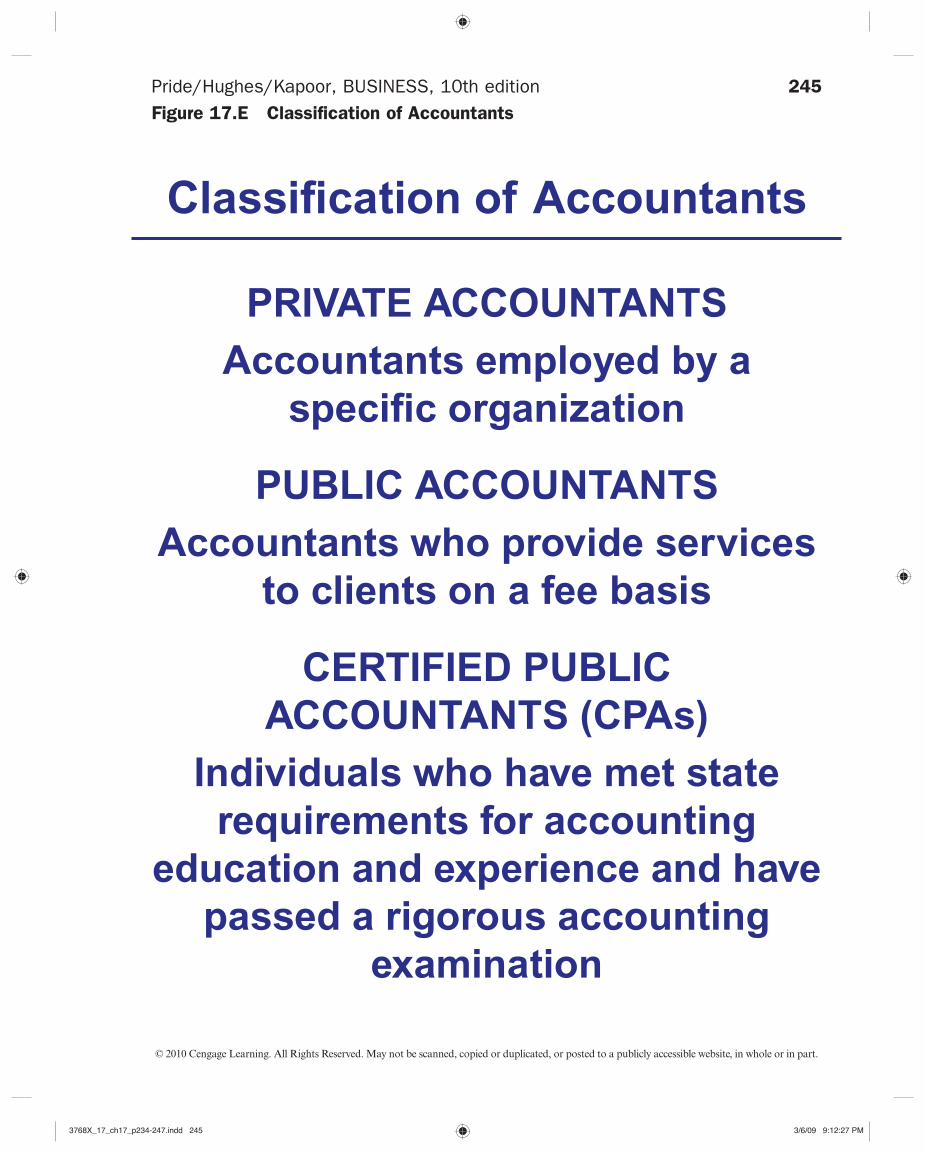

Careers in Accounting (cont’d)

• Private Accountant– Employed by a specific organizationp y y p g– Services performed for the employer

• General accounting (recording transactions and preparing statements)

• Budgeting (for sales and operating expenses)• Cost accounting (determining costs of producing

products and services)

Copyright © Cengage Learning. All rights reserved. 17| 10

products and services)• Tax accounting (planning strategy and preparing

returns)• Internal auditing (reviewing finances and operations

against goals)

6

Careers in Accounting (cont’d)

• Public Accountant– Provides services to clients on a fee basis– Self‐employed or employee of an accounting firm

• Certified Public Accountant (CPA)– Has met state requirements for accounting

education and experience and has passed a rigorous two‐day accounting examination prepared b h AICPA

Copyright © Cengage Learning. All rights reserved. 17| 11

by the AICPA– Participates in continuing‐education programs to

maintain certification

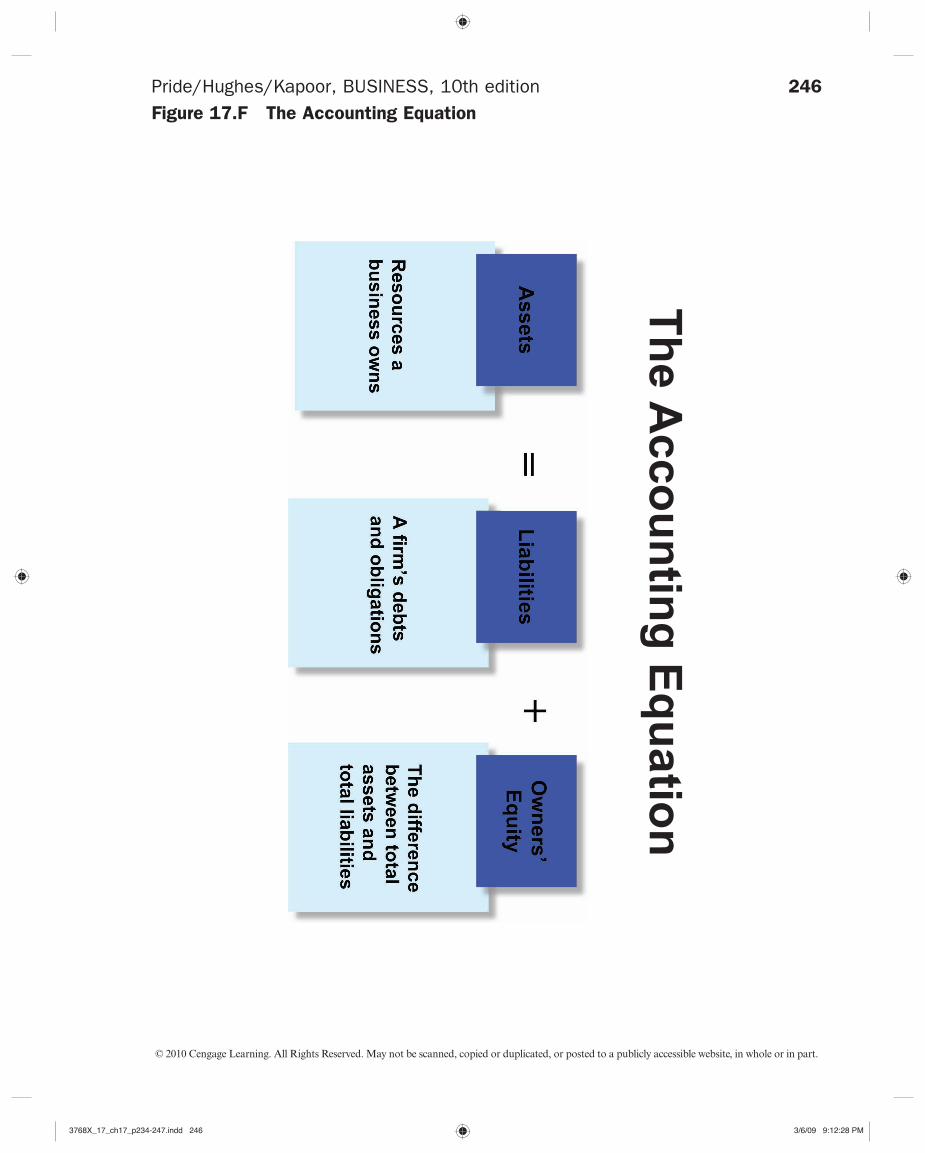

The Accounting Process• The accounting equation

Assets = Liabilities + Owners’ equityh h b ( h– Assets—the resources that a business owns (e.g., cash, inventory,

equipment, and real estate)

– Liabilities—the firm’s debts

– Owners’ equity—the difference between assets and liabilities (what would be left for the owners if the firm’s assets were sold and the money used to pay off its liabilities)

Copyright © Cengage Learning. All rights reserved. 17| 12

Double-entry bookkeeping system: Each financial transaction is recorded as two separate accounting entries to maintain the balance of the accounting equation

7

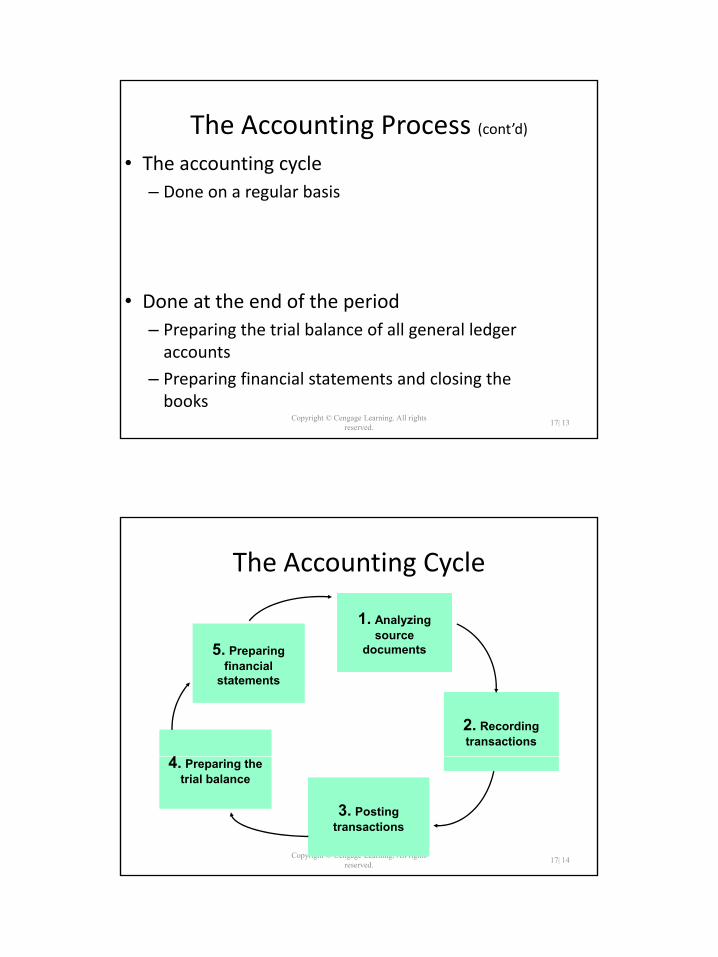

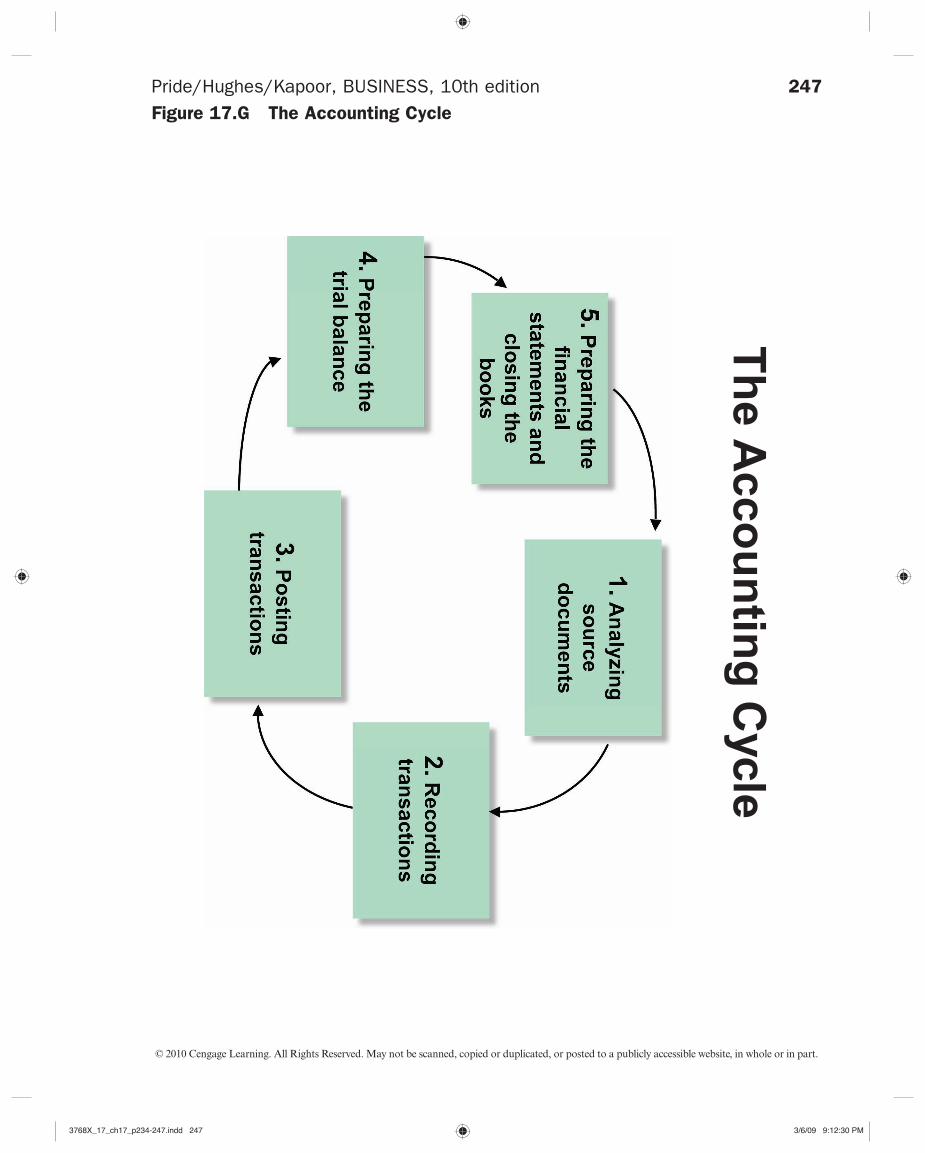

The Accounting Process (cont’d)

• The accounting cycle– Done on a regular basisg

• Done at the end of the period

Copyright © Cengage Learning. All rights reserved. 17| 13

– Preparing the trial balance of all general ledger accounts

– Preparing financial statements and closing the books

The Accounting Cycle

1. Analyzing source

1. Analyzing sourcesource

documentssource

documents

2. Recording transactions2. Recording transactions

44

5. Preparing financial

statements

5. Preparing financial

statements

Copyright © Cengage Learning. All rights reserved. 17| 14

4. Preparing the trial balance

4. Preparing the trial balance

3. Posting transactions3. Posting

transactions

8

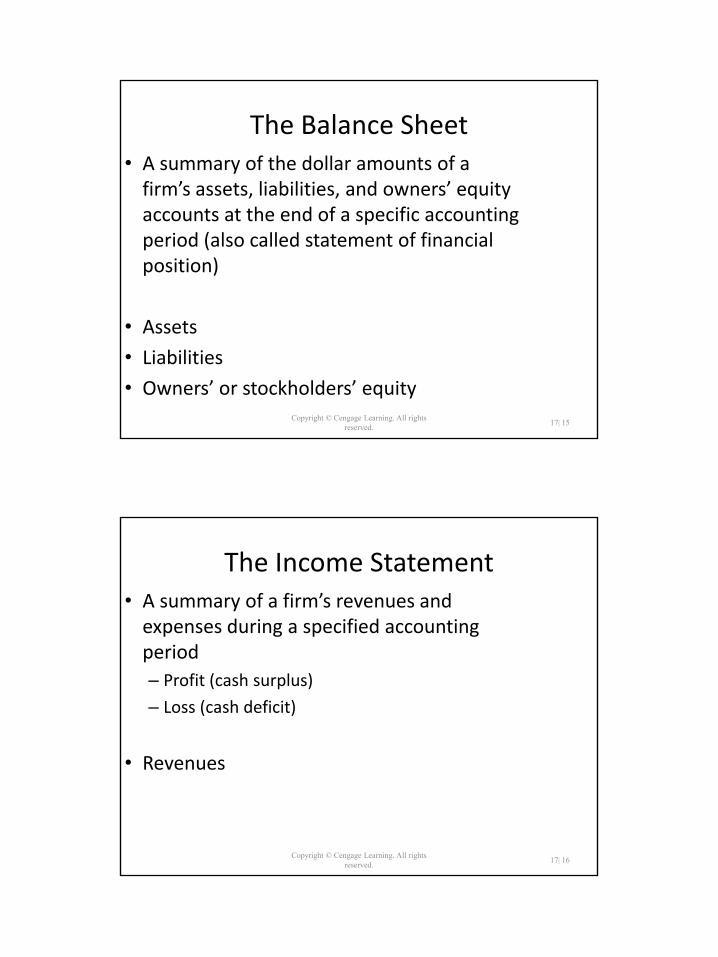

The Balance Sheet• A summary of the dollar amounts of a

firm’s assets, liabilities, and owners’ equity accounts at the end of a specific accounting period (also called statement of financial position)

Copyright © Cengage Learning. All rights reserved. 17| 15

• Assets

• Liabilities

• Owners’ or stockholders’ equity

The Income Statement• A summary of a firm’s revenues and

expenses during a specified accounting period– Profit (cash surplus)

– Loss (cash deficit)

R

Copyright © Cengage Learning. All rights reserved. 17| 16

• Revenues

9

The Income Statement (cont.)

• Cost of goods sold– The dollar amount equal to beginning q g g

inventory plus net purchases less ending inventory

Cost of goods sold

Beginning inventory

Net purchases

Ending inventory

= + –

G fi

Copyright © Cengage Learning. All rights reserved. 17| 17

• Gross profit– A firm’s net sales less the cost of goods

sold

The Income Statement (cont.)

• Operating expenses

• Net income

Copyright © Cengage Learning. All rights reserved. 17| 18

• Net loss

10

The Statement of Cash Flows• Illustrates how the operating, investing, and

financing activities of a company affect cash during an accounting period

Copyright © Cengage Learning. All rights reserved. 17| 19

Evaluating Financial Statements• Identify trends in sales, profits, borrowing,

and other business variables

• Determine whether the firm is on track to meet long‐term goals

Copyright © Cengage Learning. All rights reserved. 17| 20

11

Comparing Data with Other Firms’ Data

• Comparisons are possible because of GAAP

• Managers can get a general idea of a firm’s relative effectiveness and its standing within the industry

• Data are available from annual reports of public corporations

Copyright © Cengage Learning. All rights reserved. 17| 21

p p

• Industry averages are available from Dun & Bradstreet, Standard & Poor’s, industry trade associations

Financial Ratios• Numbers that show the relationship

between two elements of a firm’s financial statements

• Can be compared with– The firm’s own past ratios– Ratios of competitors– Industry averages

Copyright © Cengage Learning. All rights reserved. 17| 22

Industry averages

• Information to calculate ratios is found on a firm’s balance sheet and income statement

234

© 2010 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Pride/Hughes/Kapoor, BUSINESS, 10th editionTable 17.1 Users of Accounting Information

Users

of A

cco

un

ting

Info

rma

tion

The primary users of accounting inform

ation are a company’s m

anagers, but individuals and organizations outside the com

pany also require information on its finances.

Managem

ent

Lenders

and

Supplie

rsS

tockhold

ers

and

Pote

ntia

l Investo

rsG

overn

ment

Agencie

s

Plan and set goals O

rganize Lead and m

otivate C

ontrol

Evaluate credit risks before com

mitting

to shor t- or long-term

financing

Evaluate the financial health of the firm

before purchasing stocks or bonds

Confirm

tax liabilitiesC

onfirm payroll

deductionsApprove new

issues of stocks and bonds

3768X_17_ch17_p234-247.indd 2343768X_17_ch17_p234-247.indd 234 3/6/09 9:12:23 PM3/6/09 9:12:23 PM

235

© 2010 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

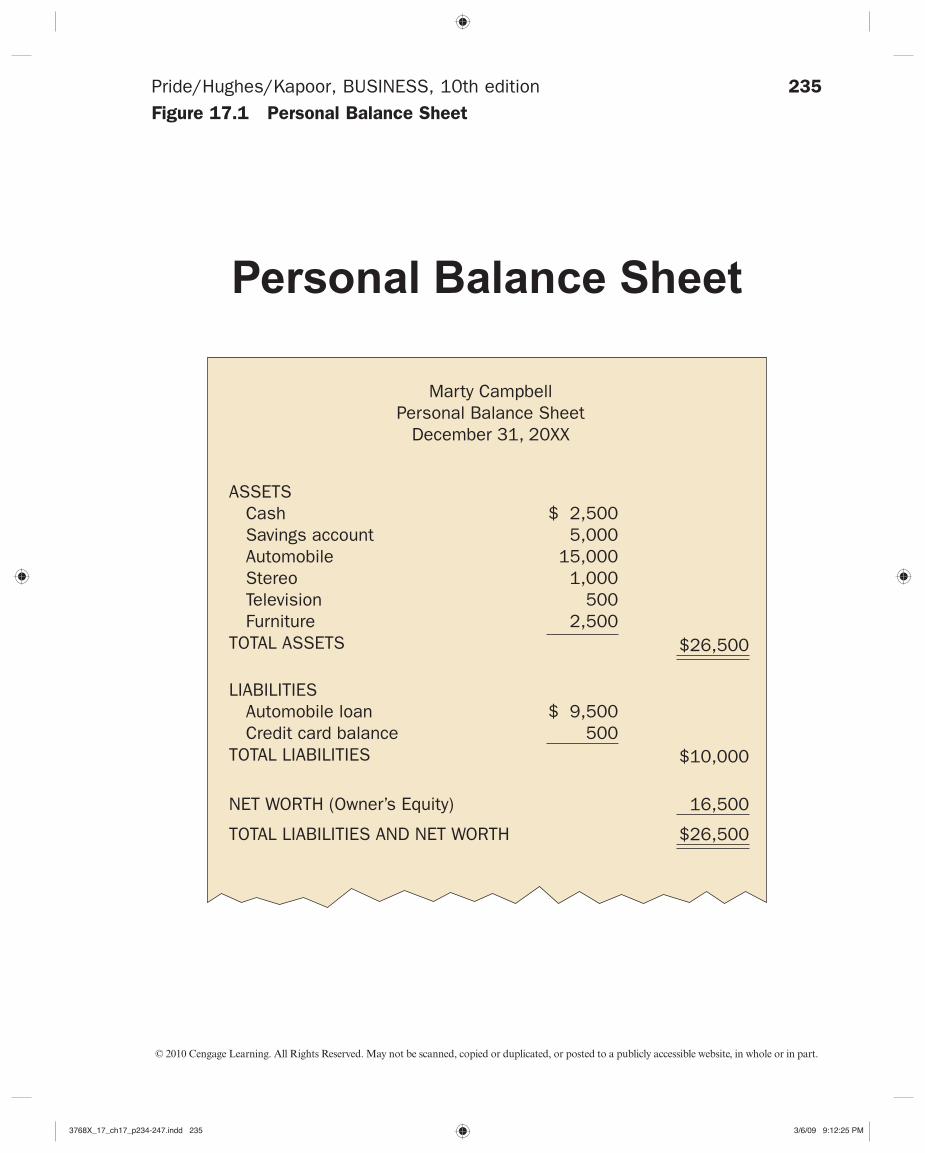

Pride/Hughes/Kapoor, BUSINESS, 10th editionFigure 17.1 Personal Balance Sheet

Personal Balance Sheet

Marty CampbellPersonal Balance Sheet

December 31, 20XX

ASSETS Cash Savings account Automobile Stereo Television FurnitureTOTAL ASSETS

LIABILITIES Automobile loan Credit card balanceTOTAL LIABILITIES

NET WORTH (Owner’s Equity)

TOTAL LIABILITIES AND NET WORTH

$ 9,500500

$ 2,5005,000

15,0001,000

5002,500

$26,500

$10,000

16,500

$26,500

3768X_17_ch17_p234-247.indd 2353768X_17_ch17_p234-247.indd 235 3/6/09 9:12:25 PM3/6/09 9:12:25 PM

236

© 2010 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

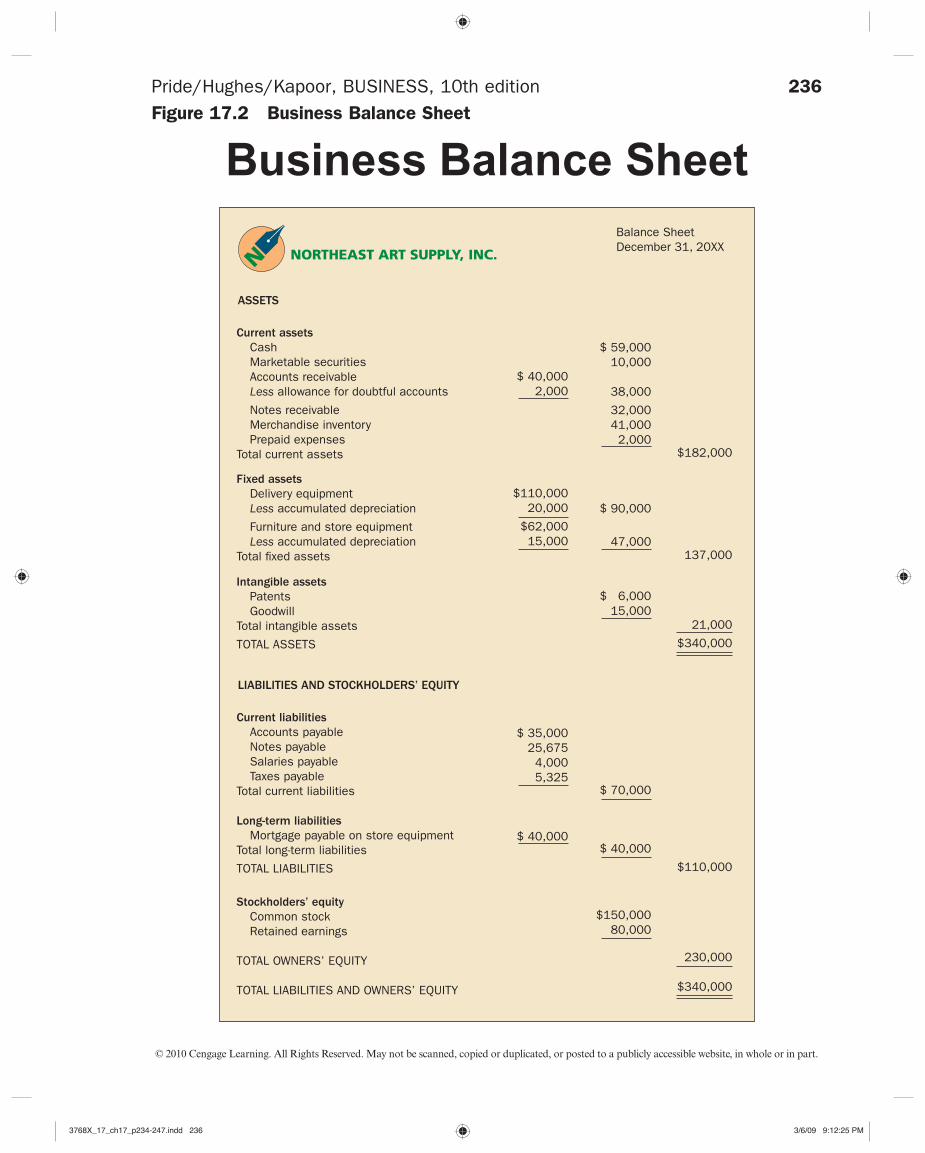

Pride/Hughes/Kapoor, BUSINESS, 10th editionFigure 17.2 Business Balance Sheet

Business Balance Sheet

Balance SheetDecember 31, 20XX

Current assets

Cash Marketable securities Accounts receivable Less allowance for doubtful accounts

Notes receivable Merchandise inventory Prepaid expensesTotal current assets

Fixed assets

Delivery equipment Less accumulated depreciation

Furniture and store equipment Less accumulated depreciationTotal fixed assets

ASSETS

$ 40,0002,000

$182,000

137,000

$110,000

230,000

$340,000

21,000

$340,000

$ 59,00010,000

38,000

32,00041,0002,000

Current liabilities

Accounts payable Notes payable Salaries payable Taxes payableTotal current liabilities

Long-term liabilities

Mortgage payable on store equipmentTotal long-term liabilities

TOTAL LIABILITIES

Stockholders’ equity

Common stock Retained earnings

TOTAL OWNERS’ EQUITY

TOTAL LIABILITIES AND OWNERS’ EQUITY

LIABILITIES AND STOCKHOLDERS’ EQUITY

$ 70,000

$ 90,000

47,000

$110,00020,000

$62,00015,000

$ 35,00025,6754,0005,325

$ 40,000

Intangible assets

Patents GoodwillTotal intangible assets

TOTAL ASSETS

$ 6,00015,000

$ 40,000

$150,00080,000

3768X_17_ch17_p234-247.indd 2363768X_17_ch17_p234-247.indd 236 3/6/09 9:12:25 PM3/6/09 9:12:25 PM

237

© 2010 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

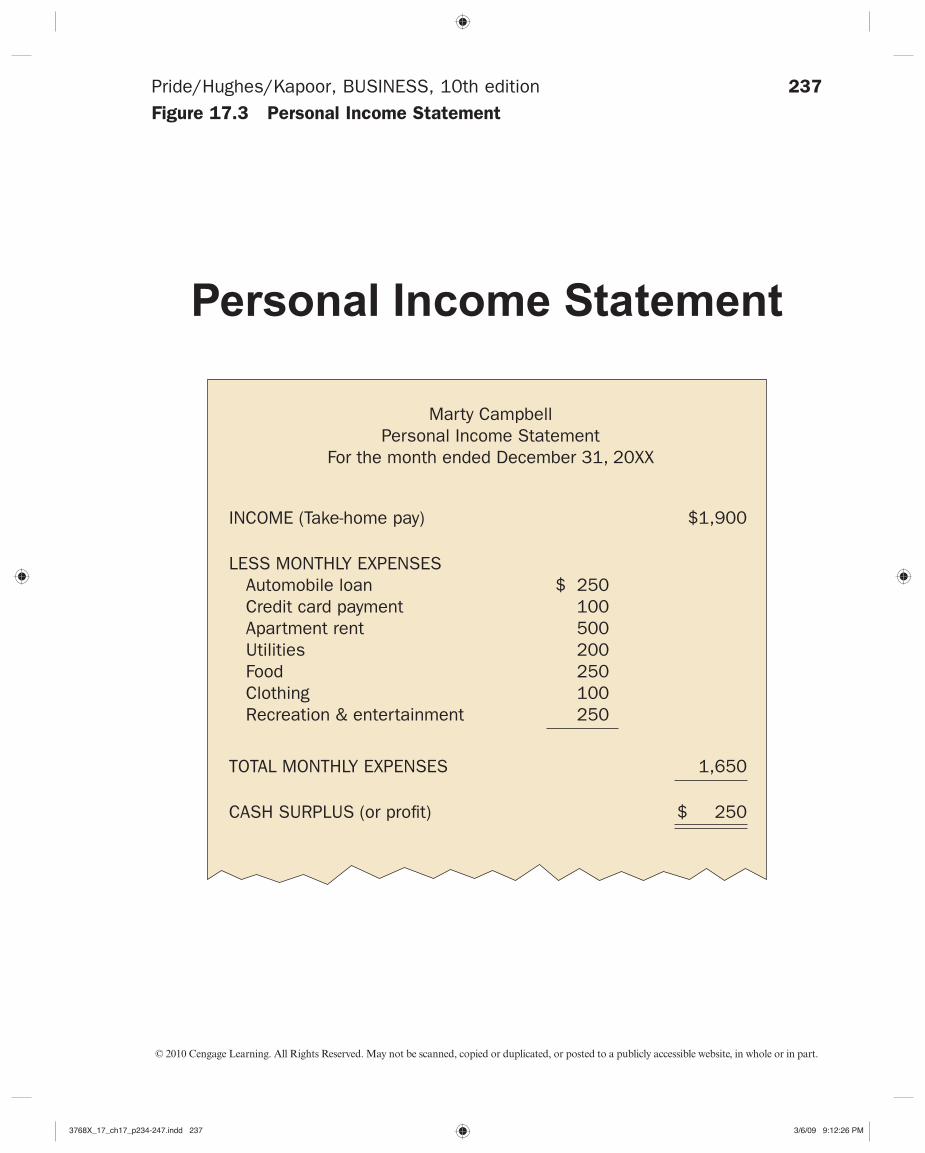

Pride/Hughes/Kapoor, BUSINESS, 10th editionFigure 17.3 Personal Income Statement

Personal Income Statement

Marty CampbellPersonal Income Statement

For the month ended December 31, 20XX

LESS MONTHLY EXPENSES Automobile loan Credit card payment Apartment rent Utilities Food Clothing Recreation & entertainment

INCOME (Take-home pay) $1,900

$ 250100500200250100250

TOTAL MONTHLY EXPENSES 1,650

CASH SURPLUS (or profit) $ 250

3768X_17_ch17_p234-247.indd 2373768X_17_ch17_p234-247.indd 237 3/6/09 9:12:26 PM3/6/09 9:12:26 PM

238

© 2010 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

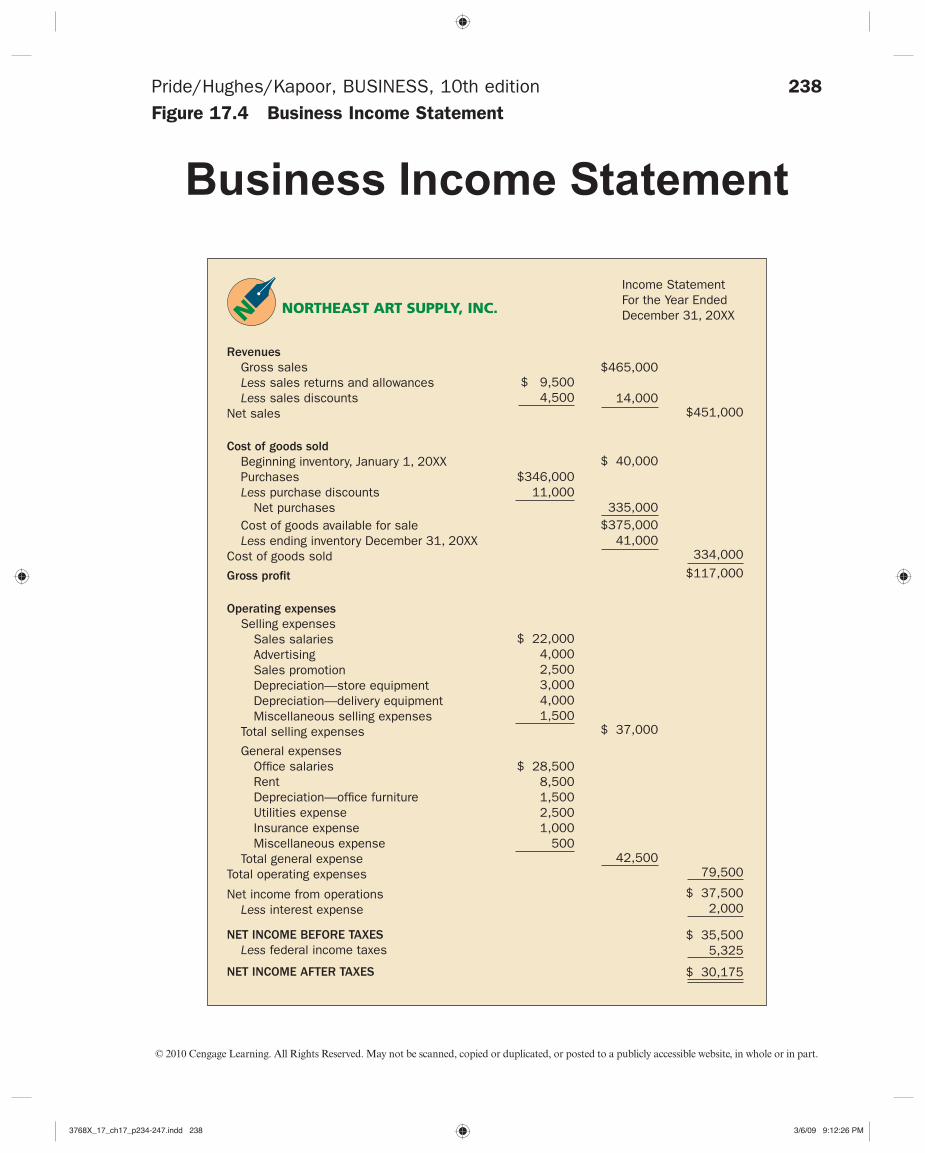

Pride/Hughes/Kapoor, BUSINESS, 10th editionFigure 17.4 Business Income Statement

Business Income Statement

Income StatementFor the Year EndedDecember 31, 20XX

Revenues

Gross sales Less sales returns and allowances Less sales discountsNet sales

$ 9,5004,500

$465,000

14,000

$ 40,000

$375,00041,000

335,000

$451,000

334,000 $117,000

Cost of goods sold

Beginning inventory, January 1, 20XX Purchases Less purchase discounts Net purchases Cost of goods available for sale Less ending inventory December 31, 20XXCost of goods sold

Gross profit

Operating expenses

Selling expenses Sales salaries Advertising Sales promotion Depreciation—store equipment Depreciation—delivery equipment Miscellaneous selling expenses Total selling expenses

General expenses Office salaries Rent Depreciation—office furniture Utilities expense Insurance expense Miscellaneous expense Total general expenseTotal operating expenses

NET INCOME BEFORE TAXES

Less federal income taxes

Net income from operations Less interest expense

NET INCOME AFTER TAXES

42,500

$ 37,000

$ 37,5002,000

79,500

$ 35,5005,325

$ 30,175

$346,00011,000

$ 22,0004,0002,5003,0004,0001,500

$ 28,5008,5001,5002,5001,000

500

3768X_17_ch17_p234-247.indd 2383768X_17_ch17_p234-247.indd 238 3/6/09 9:12:26 PM3/6/09 9:12:26 PM

239

© 2010 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

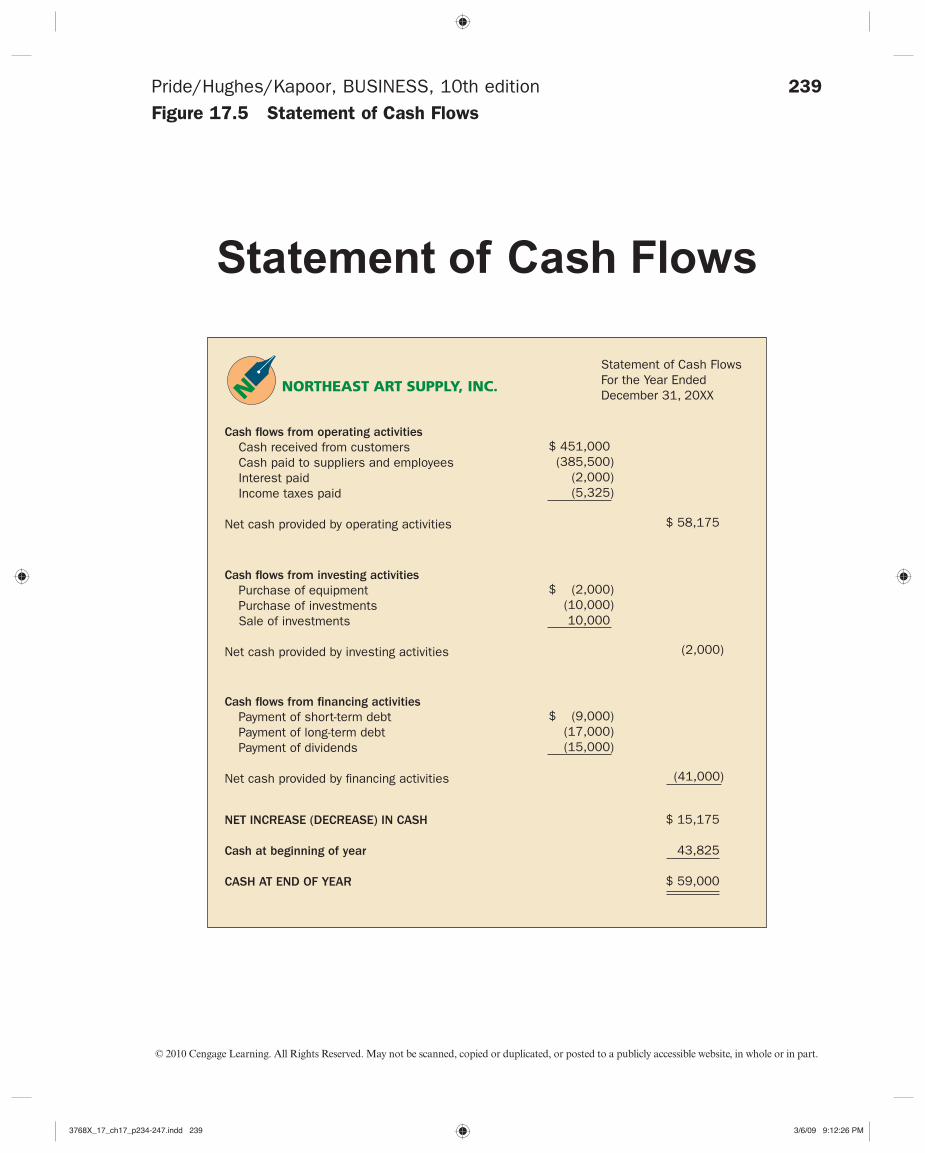

Pride/Hughes/Kapoor, BUSINESS, 10th editionFigure 17.5 Statement of Cash Flows

Statement of Cash Flows

Statement of Cash FlowsFor the Year EndedDecember 31, 20XX

Cash flows from operating activities

Cash received from customers Cash paid to suppliers and employees Interest paid Income taxes paid

Net cash provided by operating activities

$ 451,000 (385,500)

(2,000)(5,325)

$ 58,175

Cash flows from investing activities

Purchase of equipment Purchase of investments Sale of investments

Net cash provided by investing activities

$ (2,000) (10,000)

10,000

(2,000)

Cash flows from financing activities

Payment of short-term debt Payment of long-term debt Payment of dividends

Net cash provided by financing activities

$ (9,000)(17,000)(15,000)

(41,000)

NET INCREASE (DECREASE) IN CASH

Cash at beginning of year

CASH AT END OF YEAR

$ 15,175

43,825

$ 59,000

3768X_17_ch17_p234-247.indd 2393768X_17_ch17_p234-247.indd 239 3/6/09 9:12:26 PM3/6/09 9:12:26 PM

240

© 2010 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

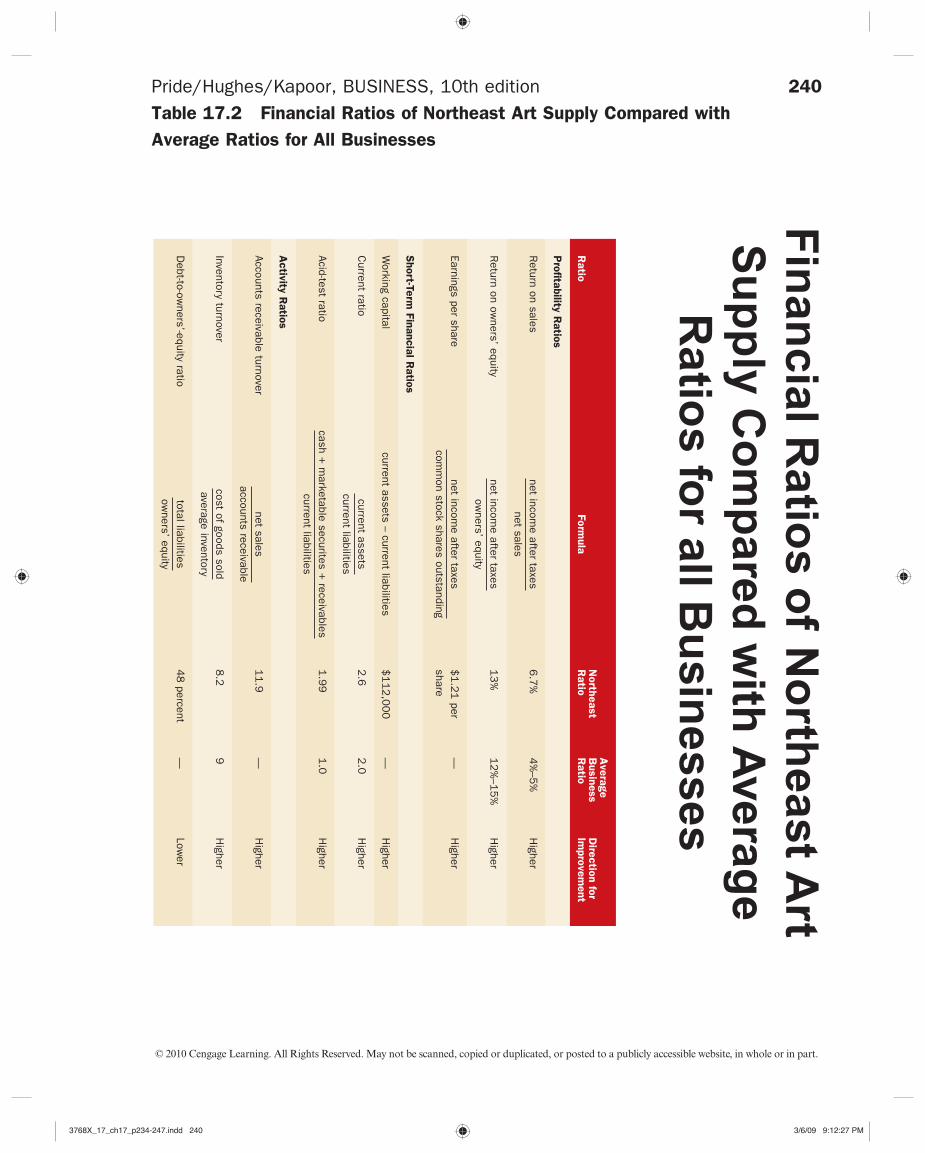

Pride/Hughes/Kapoor, BUSINESS, 10th editionTable 17.2 Financial Ratios of Northeast Art Supply Compared with

Average Ratios for All BusinessesF

inan

cia

l Ra

tios o

f No

rthea

st A

rt

Su

pp

ly C

om

pare

d w

ith A

vera

ge

Ra

tios fo

r all B

usin

ess

es

alu

mro

Foi

ta

RN

orth

east

Ratio

Avera

ge

Busin

ess

Ratio

Dire

ctio

n fo

r Im

pro

vem

ent

Pro

fita

bility

Ratio

s

Return on sales

net income after taxes

net sales6

.7%

4%

–5%

Higher

Return on ow

ners’ equitynet incom

e after taxesow

ners’ equity1

3%

12

%–1

5%

Higher

Earnings per sharenet incom

e after taxescom

mon stock shares outstanding

$1

.21

per share

—H

igher

Short-T

erm

Fin

ancia

l Ratio

s

rehg

iH

—0

00,

21

1$

seiti

liba

il tn

erru

c –

stes

sa t

nerr

ucla

tipa

c gn

ikro

WCurrent ratio

current assetscurrent liabilities

2.6

2.0

Higher

Acid-test ratiocash +

marketable securites +

receivablescurrent liabilities

1.9

91

.0H

igher

Activ

ity R

atio

s

Accounts receivable turnovernet sales

accounts receivable1

1.9

—H

igher

Inventory turnover cost of goods soldaverage inventory

8.2

9H

igher

Debt-to-ow

ners’-equity ratiototal liabilitiesow

ners’ equity4

8 percent

—Low

er

3768X_17_ch17_p234-247.indd 2403768X_17_ch17_p234-247.indd 240 3/6/09 9:12:27 PM3/6/09 9:12:27 PM

241

© 2010 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

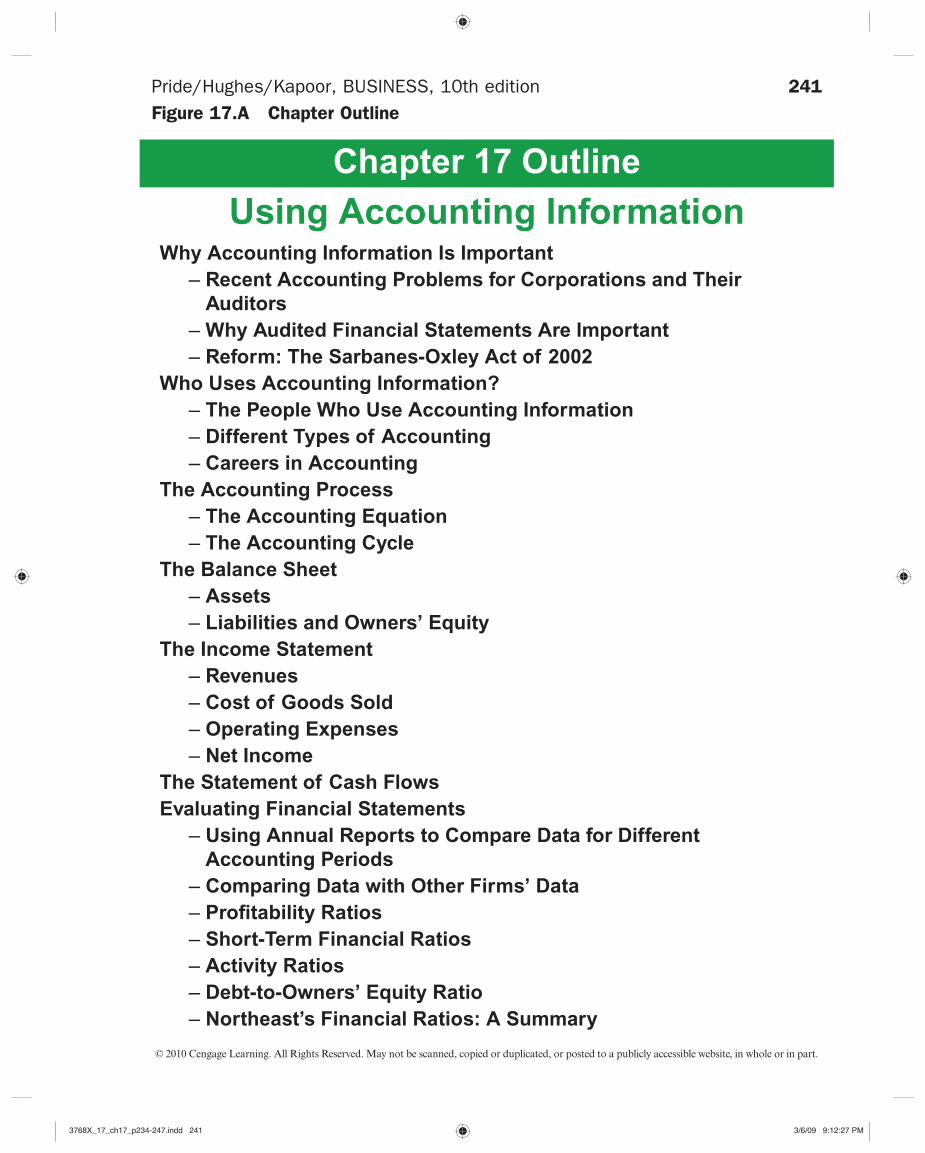

Pride/Hughes/Kapoor, BUSINESS, 10th editionFigure 17.A Chapter Outline

Chapter 17 Outline

Using Accounting InformationWhy Accounting Information Is Important

– Recent Accounting Problems for Corporations and Their

Auditors

– Why Audited Financial Statements Are Important

– Reform: The Sarbanes-Oxley Act of 2002

Who Uses Accounting Information?

– The People Who Use Accounting Information

– Different Types of Accounting

– Careers in Accounting

The Accounting Process

– The Accounting Equation

– The Accounting Cycle

The Balance Sheet

– Assets

– Liabilities and Owners’ Equity

The Income Statement

– Revenues

– Cost of Goods Sold

– Operating Expenses

– Net Income

The Statement of Cash Flows

Evaluating Financial Statements

– Using Annual Reports to Compare Data for Different

Accounting Periods

– Comparing Data with Other Firms’ Data

– Profi tability Ratios

– Short-Term Financial Ratios

– Activity Ratios

– Debt-to-Owners’ Equity Ratio

– Northeast’s Financial Ratios: A Summary

3768X_17_ch17_p234-247.indd 2413768X_17_ch17_p234-247.indd 241 3/6/09 9:12:27 PM3/6/09 9:12:27 PM

242

© 2010 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

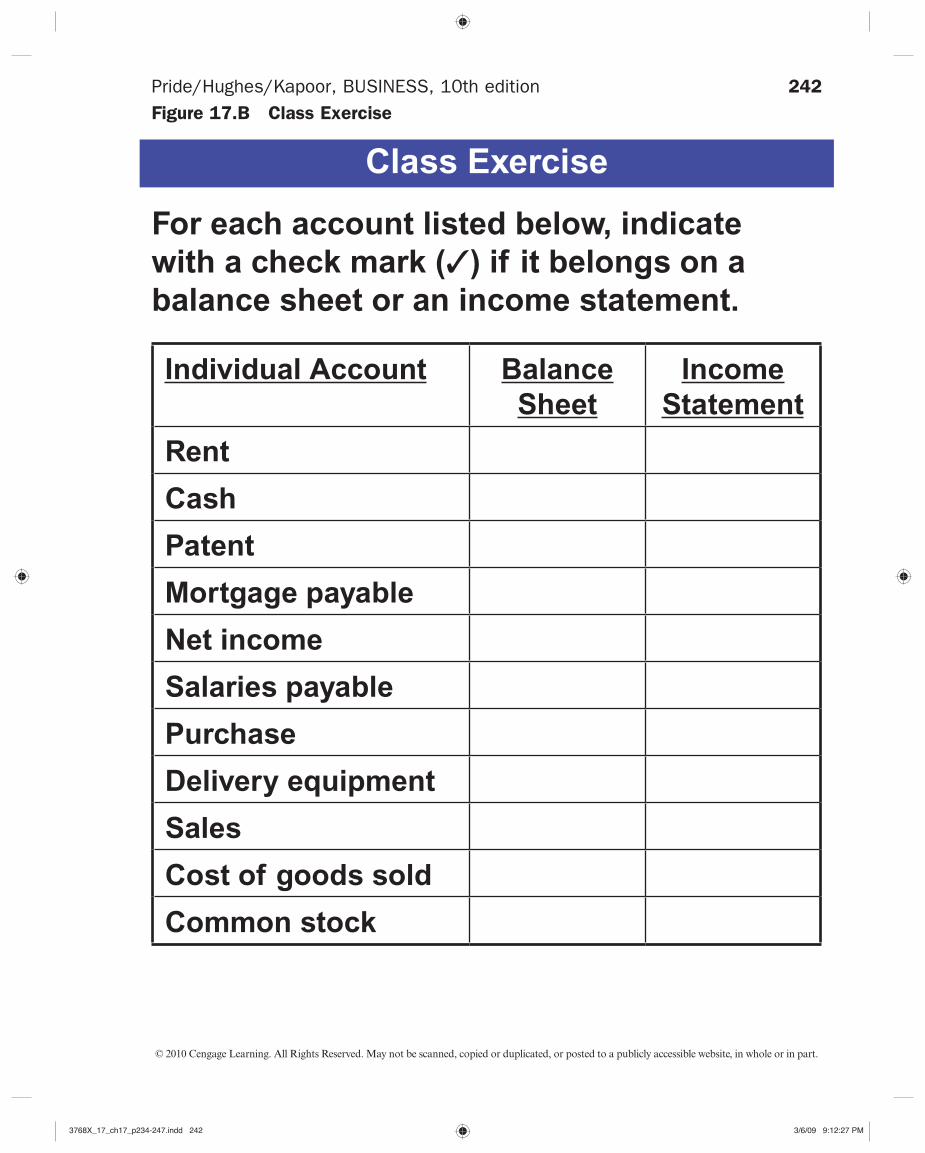

Pride/Hughes/Kapoor, BUSINESS, 10th editionFigure 17.B Class Exercise

Class Exercise

For each account listed below, indicate

with a check mark (✓) if it belongs on a

balance sheet or an income statement.

Individual Account Balance

Sheet

Income

Statement

Rent

Cash

Patent

Mortgage payable

Net income

Salaries payable

Purchase

Delivery equipment

Sales

Cost of goods sold

Common stock

3768X_17_ch17_p234-247.indd 2423768X_17_ch17_p234-247.indd 242 3/6/09 9:12:27 PM3/6/09 9:12:27 PM

243

© 2010 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

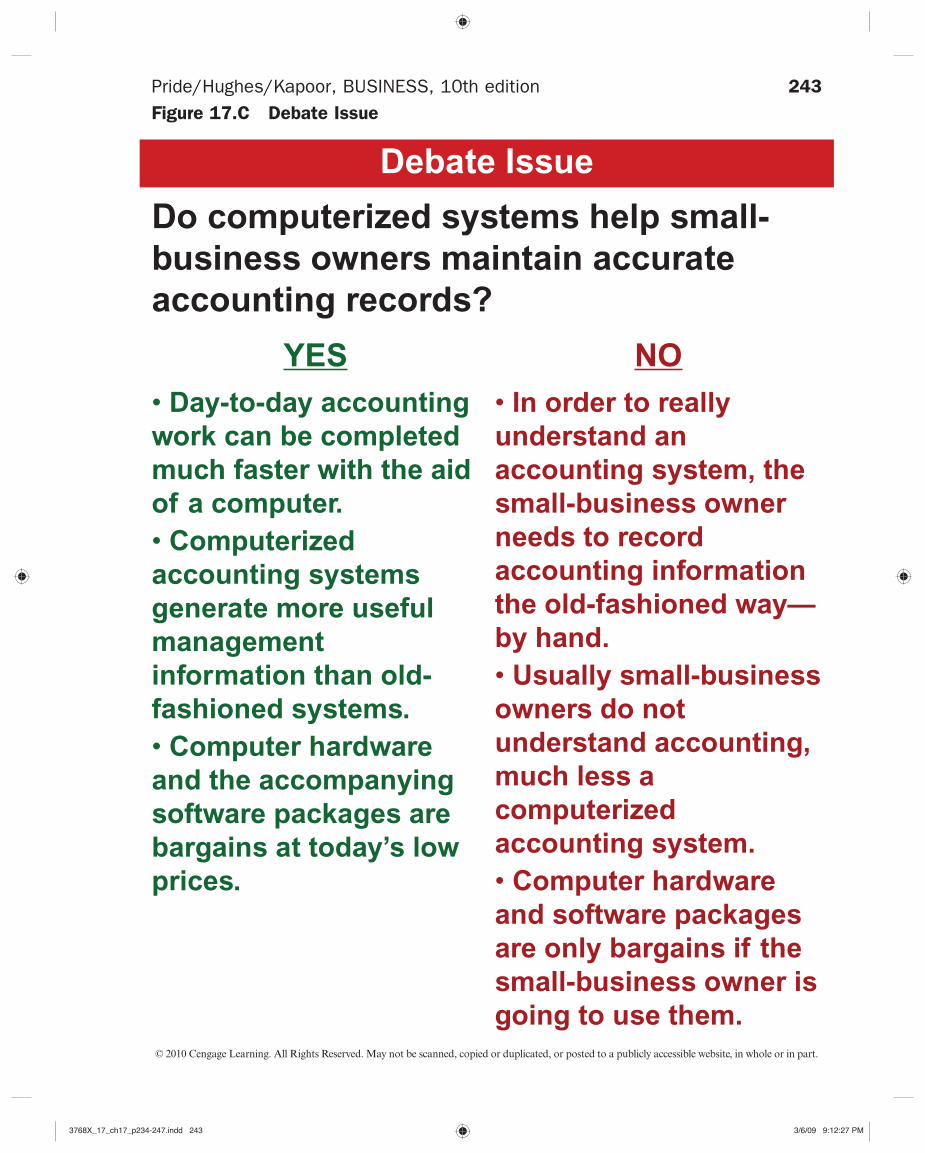

Pride/Hughes/Kapoor, BUSINESS, 10th editionFigure 17.C Debate Issue

Debate Issue

Do computerized systems help small-

business owners maintain accurate

accounting records?

YES

• Day-to-day accounting

work can be completed

much faster with the aid

of a computer.

• Computerized

accounting systems

generate more useful

management

information than old-

fashioned systems.

• Computer hardware

and the accompanying

software packages are

bargains at today’s low

prices.

NO

• In order to really

understand an

accounting system, the

small-business owner

needs to record

accounting information

the old-fashioned way—

by hand.

• Usually small-business

owners do not

understand accounting,

much less a

computerized

accounting system.

• Computer hardware

and software packages

are only bargains if the

small-business owner is

going to use them.

3768X_17_ch17_p234-247.indd 2433768X_17_ch17_p234-247.indd 243 3/6/09 9:12:27 PM3/6/09 9:12:27 PM

244

© 2010 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Pride/Hughes/Kapoor, BUSINESS, 10th editionFigure 17.D Chapter Quiz

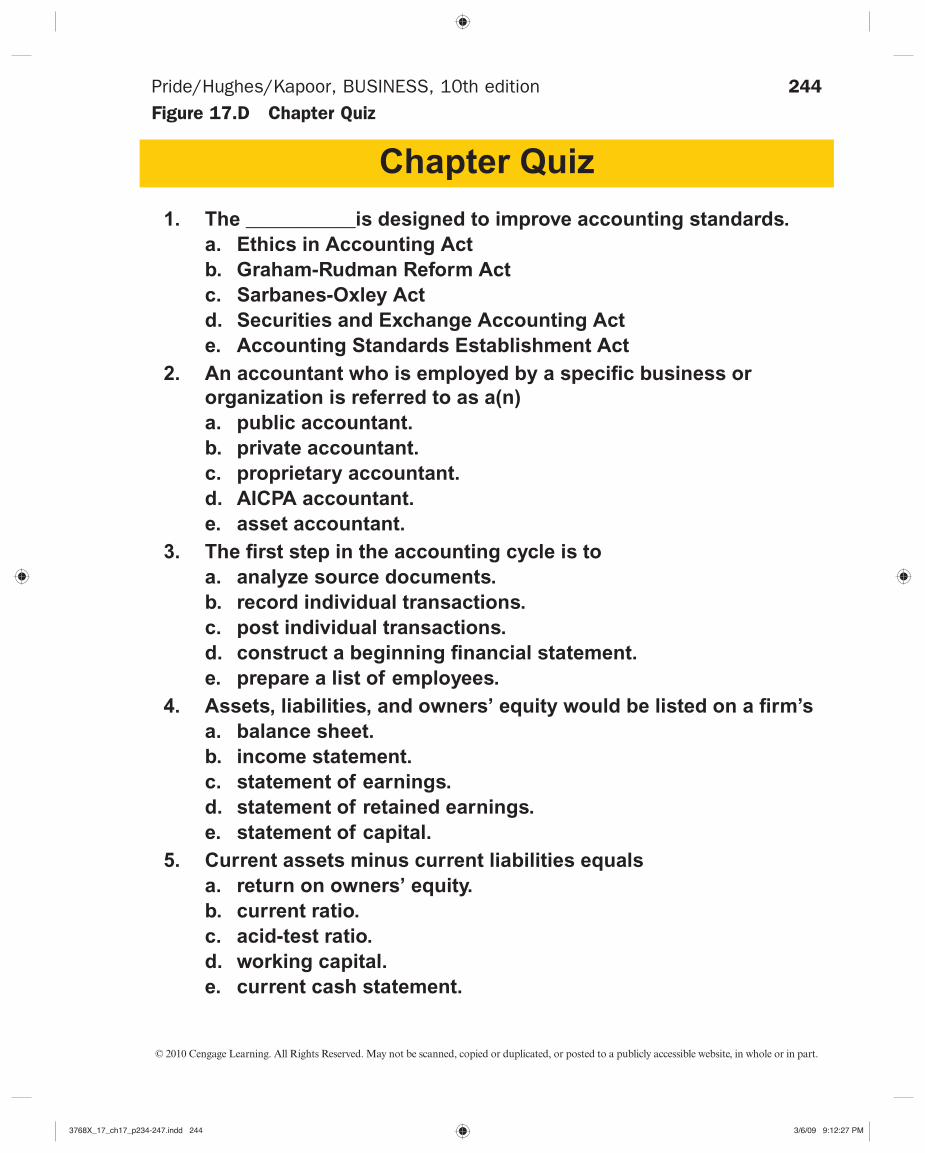

Chapter Quiz

1. The ___________is designed to improve accounting standards.

a. Ethics in Accounting Act

b. Graham-Rudman Reform Act

c. Sarbanes-Oxley Act

d. Securities and Exchange Accounting Act

e. Accounting Standards Establishment Act

2. An accountant who is employed by a specifi c business or

organization is referred to as a(n)

a. public accountant.

b. private accountant.

c. proprietary accountant.

d. AICPA accountant.

e. asset accountant.

3. The fi rst step in the accounting cycle is to

a. analyze source documents.

b. record individual transactions.

c. post individual transactions.

d. construct a beginning fi nancial statement.

e. prepare a list of employees.

4. Assets, liabilities, and owners’ equity would be listed on a fi rm’s

a. balance sheet.

b. income statement.

c. statement of earnings.

d. statement of retained earnings.

e. statement of capital.

5. Current assets minus current liabilities equals

a. return on owners’ equity.

b. current ratio.

c. acid-test ratio.

d. working capital.

e. current cash statement.

3768X_17_ch17_p234-247.indd 2443768X_17_ch17_p234-247.indd 244 3/6/09 9:12:27 PM3/6/09 9:12:27 PM

245

© 2010 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Pride/Hughes/Kapoor, BUSINESS, 10th editionFigure 17.E Classification of Accountants

Classifi cation of Accountants

PRIVATE ACCOUNTANTS

Accountants employed by a

specifi c organization

PUBLIC ACCOUNTANTS

Accountants who provide services

to clients on a fee basis

CERTIFIED PUBLIC

ACCOUNTANTS (CPAs)

Individuals who have met state

requirements for accounting

education and experience and have

passed a rigorous accounting

examination

3768X_17_ch17_p234-247.indd 2453768X_17_ch17_p234-247.indd 245 3/6/09 9:12:27 PM3/6/09 9:12:27 PM

246

© 2010 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Pride/Hughes/Kapoor, BUSINESS, 10th editionFigure 17.F The Accounting Equation

Th

e A

cco

un

ting

Eq

ua

tion

3768X_17_ch17_p234-247.indd 2463768X_17_ch17_p234-247.indd 246 3/6/09 9:12:28 PM3/6/09 9:12:28 PM

247

© 2010 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Pride/Hughes/Kapoor, BUSINESS, 10th editionFigure 17.G The Accounting Cycle

Th

e A

cco

un

ting

Cycle

3768X_17_ch17_p234-247.indd 2473768X_17_ch17_p234-247.indd 247 3/6/09 9:12:30 PM3/6/09 9:12:30 PM