Embed Size (px)

Citation preview

Chapter One

What is Business?

© 2007 The McGraw-Hill Companies, Inc., All Rights Reserved.

McGraw-Hill/IrwinIntroduction to Business

1 - 3

What is Business?

• Business - goal-directed behavior aimed at getting and

using productive resources to buy, make, trade, and sell goods and services that can be sold at a profit

1 - 4

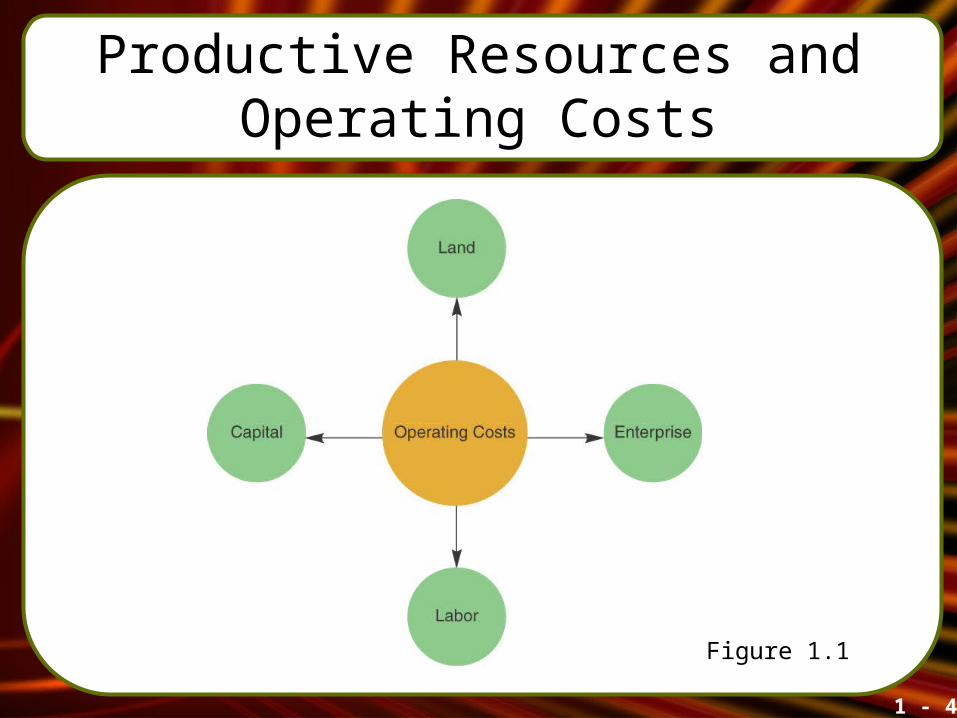

Productive Resources and Operating Costs

Figure 1.1

1 - 5

Key Business Terms

• Business Model - a company’s plan of action to use

resources to create a product that will give it a competitive advantage

• Competitive advantage - a company’s ability to offer customers a

product that has more value to them than similar products offered by other companies

1 - 6

Key Business Terms

• Sales revenue - the amount of money or income that a

company generates from the sale of the product

• Profit - the total amount of money left over after

operating costs have been deducted from sales revenues

1 - 7

Key Business Terms

• Capital - profit that is kept in a company and

invested in its business

• Wealth - the sum total of the resources, assets,

riches, and material possessions owned by people and groups in society

1 - 8

Profit and Profitability

• Profitability - a measurement of how well a company is

making use of its resources relative to its competitors

• Profit - the difference between sales revenues and

operating costs

1 - 9

Business as Commerce

• Trade - the exchange of products through the use

of money

• Barter - the exchange of one product for another

product

1 - 10

Transaction Costs Related to Business

• Transaction Costs - the costs of bargaining, negotiating,

monitoring, and regulating exchanges between people in business

1 - 11

Demand, Supply, and the Market Price

• Diminishing marginal utility - the principle that the value people receive

from an additional unit of a product declines as they obtain more of a product

1 - 12

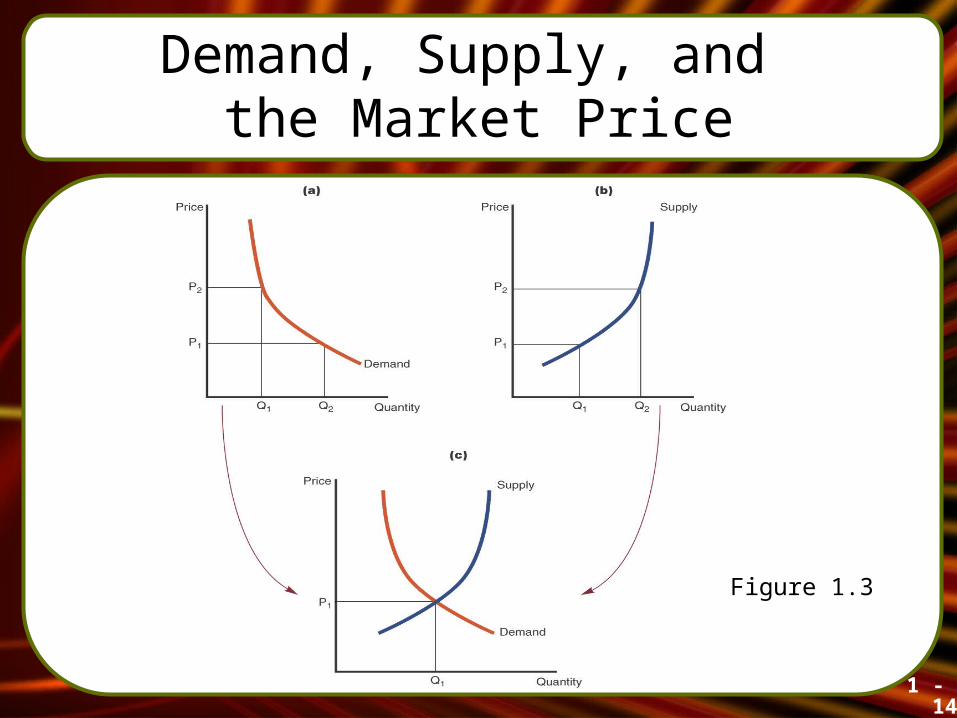

Demand, Supply, and the Market Price

• Law of demand - the principle that states as the price of a

product rises, consumers will buy less of it, and as the price of it falls, consumers will buy more of it

1 - 13

Demand, Supply, and the Market Price

• Law of supply - the principle that states that as the price of

a product rises, producers will supply more of it, and that as the price of it falls, producers will supply less of it

1 - 14

Demand, Supply, and the Market Price

Figure 1.3

1 - 15

Determining the Market Price

• Market - buyers and sellers

for a particular product

1 - 16

The Business Model and Profitability

• Industry - a group of companies that makes similar

products and competes for the same customers

1 - 17

The Invisible Hand of the Market

• Invisible hand - the principle that the pursuit of self-interest

in the marketplace naturally leads to the improved well-being of society in general

1 - 18

The Invisible Hand of the Market

• Monopoly - a situation in which one company controls

the supply of a product and can charge an artificially high price for it

• Human capital - a person’s stock of knowledge, skills,

experience, judgment, personality, and abilities

1 - 19

Business Organizations

• Organizational structure - the framework of task and authority

relationships that coordinates people so they work towards a common goal

• Functional activities - the task-specific operations needed to

convert resources into finished goods and services sold to customers