Embed Size (px)

Citation preview

CHAPTER NO. 4

CAPITAL BUDGETING

2

Capital and Capital BudgetingCapital and Capital Budgeting

Capital:

is the stock of assets that will generate a flow of income in the future.

Capital budgeting:

is the planning process for allocating all expenditures that will have an expected benefit to the firm for more than one year.

3

Investment AppraisalInvestment Appraisal

Firms normally place projects in the following categories:

1. Replacement and maintenance of old or damaged equipment.

2. Investments to upgrade or replace existing equipment

3. Marketing investments to expand product lines or distribution facilities.

4. Investments for complying with government or insurance-company safety or environmental requirements.

Need of capital budgeting

A. Whether or not funds should be invested in long term projects

B. Analyze the proposal for expansion

C. To decide for the replacement of permanent assets

D. To make financial analysis of various proposals.

IMPORTANCE OF CAPITAL BUDGETING

1. LARGE INVESTMENT

2. LONG TERM COMMITMENT OF FUNDS

3. IRREVERSIBLE NATURE

4. LONG TERM EFFECT ON PROFITABILITY

5. DIFFICULTIES OF INVESTMENT DECISION

6. NATIONAL IMPORTANCE

CAPITAL BUDGETING PROCESS

CAPITAL BUDGETING PROCESS

1. INVESTMENT PROPOSAL

2. SCREEN PROPOSAL

3. EVALUATE VARIOUS

PROPOSALS

4. FIX PRIORITIES

5. FINAL APPROVAL

6. IMPLEMENT

THE PROPOSAL

7. REVIEW PERFORMANCE

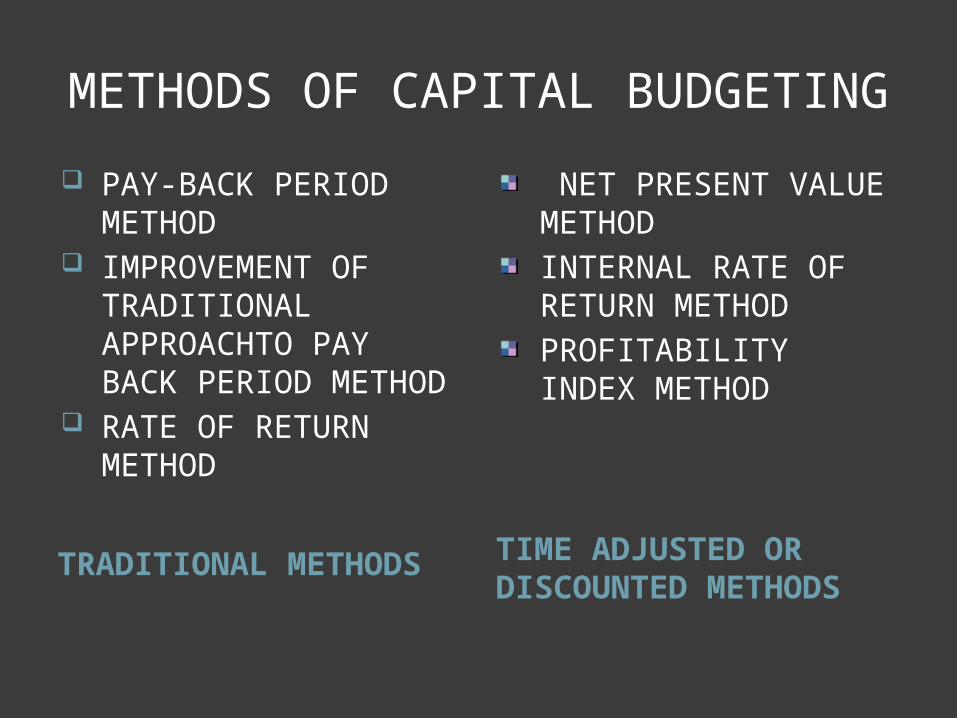

METHODS OF CAPITAL BUDGETING

TRADITIONAL METHODS TIME ADJUSTED OR DISCOUNTED METHODS

PAY-BACK PERIOD METHOD

IMPROVEMENT OF TRADITIONAL APPROACHTO PAY BACK PERIOD METHOD

RATE OF RETURN METHOD

NET PRESENT VALUE METHOD

INTERNAL RATE OF RETURN METHOD

PROFITABILITY INDEX METHOD

8

TRADITIONAL METHOD

Simple Technique for Appraisal of Investment

TRADITIONAL METHOD

Simple Technique for Appraisal of Investment

1. Payback-period criterion:

Payback period is the amount of time sufficient to cover the initial cost of an investment

But it ignores any returns accrue after the pay-back period; ignores the pattern of returns; ignores the time value (time cost) of money.

1. Payback-period criterion:

Payback period is the amount of time sufficient to cover the initial cost of an investment

But it ignores any returns accrue after the pay-back period; ignores the pattern of returns; ignores the time value (time cost) of money.

PAY BACK PERIODIn case of evaluation of a single project, it is adopted if it pays back for itself within a period specified by the management & if the project does not pay back itself within the period specified by the management then it is rejected. Formula to calculate pay back period is-

ADVANTAGES OF PAY BACK PERIOD

DISADVANTAGES OF PAY BACK PERIOD

SIMPLE TO UNDERSTAND SVING IN COST LESSER TIME LESSER LABOUR ACCEPTANCE

&REJECTION DECISION EASY

SHORT TREM APPROACH

NO CONSIDERRATION OF CASH INFLOWS EARNED AFTER PAY BACK PERIOD

NO CONSIDERATION OF COST OF CAPITAL

DIFFICULT TO DETERMINE MINIMUM ACCEPTABLE PAY BACK PERIOD

TREATS EACH ASSET INDIVIDUALLY IN ISOLATION

DOES NOT MEASURE THE TRUE PROFITABILITY

IMPROVEMENT IN TRADITIONAL APPROACH TO PAY BACK PERIOD METHOD

PROFITABILITY METHOD PAY BACK RECIPROCAL METHOD

1. Post pay back profitability method- this method takes in to consideration the returns receivables beyond the pay back period. These returns are called post pay back profits. formula is

PAY BACK RECIPROCAL METHOD

Pay back reciprocal method is employed to estimate the internal rate of return generated by a project. Formula is

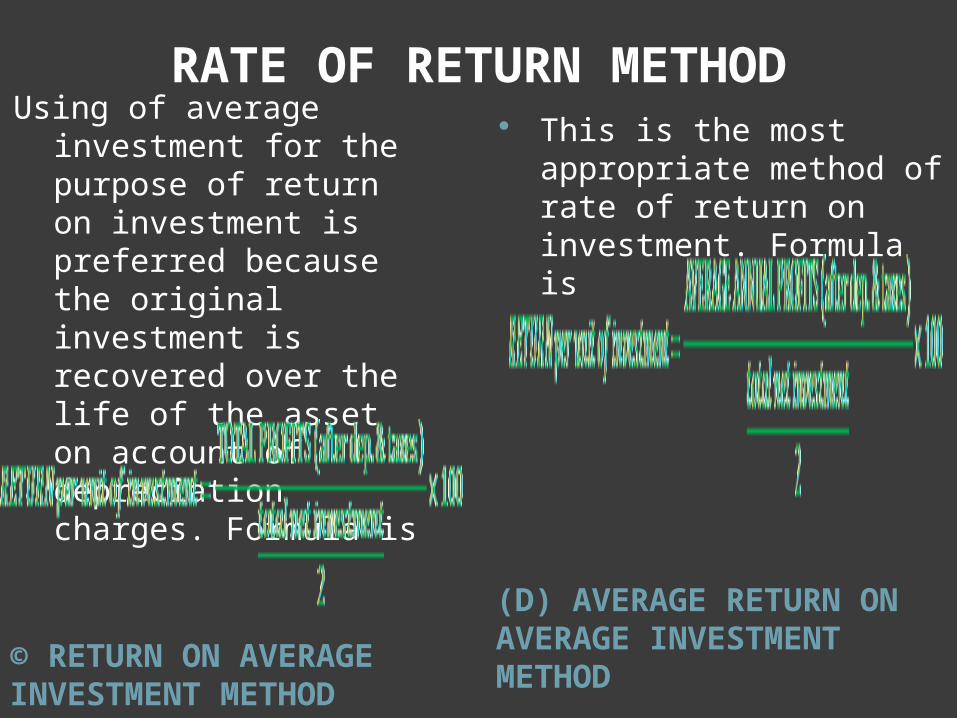

3.RATE OF RETURN METHODThis method takes in to consideration the earnings expected from the investment

over their whole life. It is known as accounting rate of return method for the reason that under this method ,the accounting concept of profit is used rather than cash in

flows.

(A) AVERAGE RATE OF RETURN METHOD

(B) RETURN PER UNIT OF INVESTMENT METHOD

This method establishes the relationship between average annual profits to total investments. Formula is

Under this method small variation of the average rate of return method. formula is

RATE OF RETURN METHOD

© RETURN ON AVERAGE INVESTMENT METHOD

(D) AVERAGE RETURN ON AVERAGE INVESTMENT METHOD

Using of average investment for the purpose of return on investment is preferred because the original investment is recovered over the life of the asset on account of depreciation charges. Formula is

This is the most appropriate method of rate of return on investment. Formula is

13

2. DISCOUNTING METHOD2. DISCOUNTING METHOD

On the other hand, the process of discounting or capitalization is to turn a future stream of services or income into its equivalent present value. When an expected future sum is turned into its equivalent present value, we say that it is discounted or capitalized.

On the other hand, the process of discounting or capitalization is to turn a future stream of services or income into its equivalent present value. When an expected future sum is turned into its equivalent present value, we say that it is discounted or capitalized.

14

The present value of a single future amount

In general, present value (PV) refers to the value now of payments to be received in the future (I). The present value of I after n year at r is:

PV= I

(1+r)n

1.NET PRESENT VALUE TECHNIQUE:

Net present value (NPV) is the difference between the present value of a future cash flow and the initial cost of the investment project; a firm should adopt a project if the expected NPV is positive.

NET PRESENT VALUE

15

NPV = P + I0 +

I1

(1+r)

I2

(1+r)2

+ … ++In

(1+r)n

where:

P: =capital cost, accruing in full at the beginning of the project

I1,2,…n =net cash flows arising from the project in years 1 to n

r =the opportunity cost of capital

NET PRESENT VALUE METHOD

ADVANTAGES DISADVANTAGES

RECOGNISES THE TIME VALUE OF MONEY

TAKES IN TO ACCOUNT THE EARNINGS OVER THE ENTIRE LIFE OF THE PROJECT

CONSIDERATUION OF MAXIMUM PROFITABILITY

THIS METHOD IS DIFFICULT TO UNDERSTAND &OPERATE

DOES NOT PROVIDE GOOD SOLUTION IN CASE PROJECTS WITH UNEQUAL LIVES

DOES NOT PROVIDE GOOD SOLUTION IN CASE PROJECTS WITH UNEQUAL INVESTMENT OF FUNDS

NOT EASY TO DETERMINE AN APPROPRIATE DISCOUNT RATE.

17

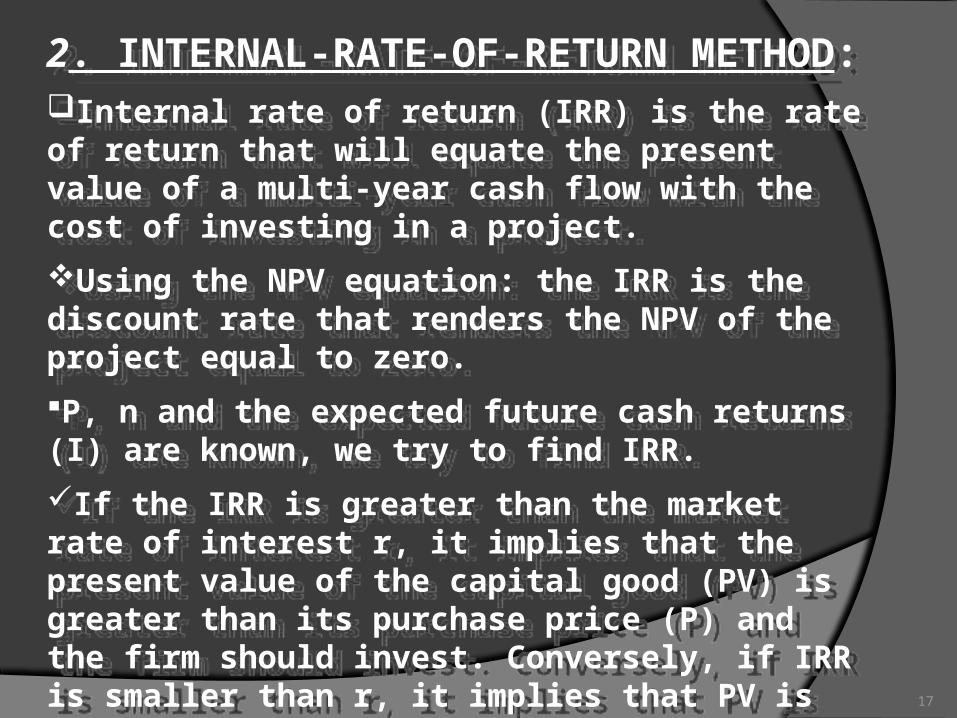

2. INTERNAL-RATE-OF-RETURN METHOD:Internal rate of return (IRR) is the rate of return that will equate the present value of a multi-year cash flow with the cost of investing in a project.

Using the NPV equation: the IRR is the discount rate that renders the NPV of the project equal to zero.

P, n and the expected future cash returns (I) are known, we try to find IRR.

If the IRR is greater than the market rate of interest r, it implies that the present value of the capital good (PV) is greater than its purchase price (P) and the firm should invest. Conversely, if IRR is smaller than r, it implies that PV is smaller than P and the firm should not invest.

2. INTERNAL-RATE-OF-RETURN METHOD:Internal rate of return (IRR) is the rate of return that will equate the present value of a multi-year cash flow with the cost of investing in a project.

Using the NPV equation: the IRR is the discount rate that renders the NPV of the project equal to zero.

P, n and the expected future cash returns (I) are known, we try to find IRR.

If the IRR is greater than the market rate of interest r, it implies that the present value of the capital good (PV) is greater than its purchase price (P) and the firm should invest. Conversely, if IRR is smaller than r, it implies that PV is smaller than P and the firm should not invest.

INTERNAL RATE OF RETURN METHOD

18

IRR =

A1

(1+r)

A2

(1+r)2

+ … ++An

(1+r)n

where:

I1,2,…n =net cash flows arising from the project in years 1 to n

r =RATE OF DISCOUNT OF INTERNAL RATE OF RETURN

The differences between NPV technique and IRR method?

19

In most situations, the IRR method will yield the same results as the NPV method. But:

•there may be more than one value for the IRR that satisfies the NPV equation; if the sign of cash flows changes more than once in the life of the project, there may be multiple solutions

•the NPV rule uses actual opportunity cost of capital as the discount rate; the IRR rule assumes the shareholders can invest at the IRR

•IRR is expressed in terms of a percentage rate of return, it ignores the project’s absolute effect on the wealth of shareholders

In most situations, the IRR method will yield the same results as the NPV method. But:

•there may be more than one value for the IRR that satisfies the NPV equation; if the sign of cash flows changes more than once in the life of the project, there may be multiple solutions

•the NPV rule uses actual opportunity cost of capital as the discount rate; the IRR rule assumes the shareholders can invest at the IRR

•IRR is expressed in terms of a percentage rate of return, it ignores the project’s absolute effect on the wealth of shareholders

DETERMINATION OF INTERNAL RATE OF RETURN

1. WHEN THE ANNUAL NET CASH FLOWS ARE EQUAL OVER THE LIFE OF THE ASSET

. 2. WHEN THE ANNUAL NET CASH FLOWS ARE UNEQUAL OVER THE LIFE OF THE ASSET

THE FORMULA IS STEPS- 1. PREPARE CASH FLOW BY ASSUMING DISCOUNT RATE

2. FIND NPV 3. IF NPV IS POSITIVE APPLY HIGHER RATE 4. IF STILL HIGH APPLY ANOTHER HIGHER

RATE UNTILL NPV BECOME NEGATIVE AFTER NEGATIVE NPV CALCULATE IRR AS

FOLLOWS

INTERNAL RATE OF RETURN

ADVANTAGES DISADVANTAGES

IT TAKES TIME VALUE OF MONEY

CONSIDER THE PROFITABILITY OF THE PROJECT FOR ITS ENTIREECONOMIC LIFE

DERTEMINATION OF COST OF CAPITAL

UNIFORM RANKINGS OF THE PROJECTS

COMPATIBLE WITH THE OBJECT OF MAXIMUM PROFITABILITY.

DIFFICULTY TO UNDERSTAND & OPERATE

BASED ON THE ASSUMPTION THAT EARNING CAN BE REINVESTED

The result of NPV &IRR MAY DIFFER

PROFITABILITY INDEX METHOD

It is also time adjusted method of evaluating the investment proposals. It shows the relationship between present value of cash inflows out flows. Thus

Advantages- slight modification of NPV method. it can significantly rank the various investments.

Disadvantages- difference in ranking of NPV& PI methods.

FACTORS INFLUENCING CAPITAL EXPENDITURE DECISION

1. URGENCY

2. DEGREE OF CERTAINITY

3. INTANGIBLE FACTORS

4. LEGAL FACTORS

5. AVAILABILITY OF FUNDS

6. FUTURE EARNINGS

7. OBSOLESCENCE

8.RESEARCH & DEVELOPMENT PROJECTS

9. COST CONSIDERATION

CAPITAL EXPENDITURE CONTROLCAPITAL EXPENDITURE INVOLVES NON-FLEXIBLE LONG TERM COMMITMENT OF FUNDS. THE SUCCESS OF THE FIRM DEPENDS UPON THAT HOW WE UTILISE OUR CAPITAL EXPENDITURE.

OBJECTIVES STEPS

TO MAKE ESTIMATE OF CAPITAL EXPENDITURE

TO CHECK TOTAL CASH OUTLAY TO ENSURE TIMELY CASH

INFLOWS TO ENSURE THAT ALL CAPITAL

EXPENDITURE PROPERLY SANCTIONED

TO CO-ORDINATE THE PROJECTS OF VARIOUS DEPARTMENT

FIX PRIORITIES AMONG VARIOUS PROJECTS

TO MEASURE THE PERFORMANCE OF THE PROJECT

TO PREVENT OVER- EXPANSION

1. PREPARATION OF CAPITAL

EXPENDITURE BUDGET

2. PROPER AUTHORISATION

OF CAPITAL EXPENDITURE

3. RECORDING &CONTROL OF EXPENDITURE

EVALUATION OF THE

FERFORMANCE OF THE PROJECT