Embed Size (px)

Citation preview

CHAPTER –I

2

INTRODUCTION The accounting information remains the primary source of information to the

management in any organizations, irrespective its operation i.e., either

manufacturing or service industry. However, as Johnson and Kaplan (1987)

observed, today’s management accounting information system is driven by

procedures and cycles of the organization and its financial reporting system.

This becomes essential for managers to make planning and control decisions.

The reason is that traditional costing systems focused on managing costs by

means of cost-based budgets, standards, and variances, established at the

departmental or in other words unit level. In such a system, many of the

volume-sensitive cost drivers are attached to the overhead costs as an

economical means of ensuring a proper match between organizational

revenues and expenses. This approach tends to shows that the over- or

underestimates the costs of products or services based on misleading

measures, thus resulting in erroneous financial including accounting decisions

(Cokins, 1986). Today, organizations including confectionary industry need to

focus on processes and activities’ costs, as well as performance measurements

for quality attributes such as customer satisfaction, reliability, cycle time,

flexibility, and productivity of the organization. The critical success factor of

any organization require continuous involvement in managing all activities to

ensure that a high quality service is provided in the most efficient and

effective manner by observing sound cost accounting system. Hence, the role

3

and application of ABC system of accounting assumes greater importance in

cost and management accounting.

Activity-Based Cost Accounting

Cost accounting and process accounting are difficult for companies with

complex processes and manufacturing practices such as a company where

many raw goods are used to create many different items. ABC was created out

of the need to overcome these difficulties by dividing production into its core

activities. After this division, the costs for these activities are calculated and

allocated to products based on how much of a particular activity is needed to

produce a product.

Origin of Activity-Based Cost Accounting

Activity-Based Costing (ABC) arose in the 1980s from the increasing lack of

relevance of traditional cost accounting methods. The traditional cost

accounting methods were designed around 1870 - 1920 and in those days

industry was labour intensive, there was no automation, the product variety

was small and the overhead costs in companies were generally very low

compared to today. However, from the 1960s - particularly 1980s - this

changed rapidly. For these reasons, traditional cost accounting has been called

everything from 'number 1 enemy of production' and questions whether it is

'an asset or a liability' have been raised. Cost accounting worked well for item

or service-based businesses to generate the true cost of the production of an

4

item or completion of a service. The direct costs of completing a project were

added in with the indirect costs of overhead to arrive at the true cost. Over the

years, many methods of cost accounting developed because of the

inadequacies of the simple cost method.

Rationale for Adopting of ABC System

The rationale for adopting the ABC system of accounting is as follows:

1. The first and most important reason is that it gives accuracy in the

process of costing with regard to the product line, the end-users of the

product, the stock-keeping units employed by the management and the

channel and category which streamline the flow of the product from the

producer to the end user.

2. This system better assists in the process of understanding the concept of

overhead costs i.e. the allocation of common business resources as they

are used by specific product lines and their relation to specific cost

driver.

3. The system is easy to understand and interpret as it is accessible,

useable and practically implement able across all norms of business set-

ups.

4. This process uses cost per unit or marginal cost as the computation base

in contrast to the traditional cost accounting methods which employ

total cost.

5

5. The system works exceptionally well will quality improvement and up

gradation programs e.g. Six Sigma.

6. This system is particularly helpful in identifying and ear-marking some

of the matters business activities which are a burden or stress on the

business i.e. wasteful or non value adding services, etc.

Limitations of Traditional Costing Systems

The absorption costing method could distort product costs because it allocates

overhead costs proportionally to the portion of direct costs. Glad and Becker

(1996) identified a number of fundamental limitations in traditional costing

systems:

• Labour, as a basis for assigning manufacturing overhead, is irrelevant as

it is significantly less than an overhead and many overheads do not bear

any relationship to labour costs of labour hours;

• The cost of technology is not assigned to products based on usage.

Moreover, direct (labour) cost is replaced by indirect (machine) cost(s);

• Service-related costs have increased considerably in the last few decades.

Costing for these services was previously non-existent;

• Customer-related costs (finance, discounts, distribution, sales, after-sales

service, etc.) are not related to the product’s cost objects;

• Customer profitability has become as crucial as product profitability.

6

In some instances, especially when a company has a very homogenous output,

few departments with overheads and customers are very similar in nature, the

simple absorption costing method should provide very accurate outputs,

despite its limitations. The absorption costing method boasts one very

important advantage - it is very simple to put into utilization. All the

information the user has to gather together can be found in accounting books

or product material and labour sheets.

The logical solution of registered disadvantages of traditional absorption

costing systems was to develop a costing method which would be able to

incorporate and utilize cause-and-effect instead of widely applied arbitrary

allocation principles into the company costing system (Drury, 2001), (Lucas,

1997). In situation, when the portion of overheads exceeds 50% of total

company costs and the company is using single measures for allocation of

overhead costs to the cost objects, the risk of an incorrect product or customer

costs calculation becomes significant. Following the 1970s, there was a general

realization of the limitations in traditional costing systems. Greater

competition and further inaccuracies in costing products effectively

encouraged businesses to seek out alternative methods, ones offering far more

transparency and enabling accurate and causal cost allocation. It was then, at

the dawn of the 1980s that the Activity-Based Costing (ABC) method came

about, being quickly adopted by enterprises of many and various types. The

spread of ABC owed a significant debt to advances in computing and IT

thereby permitting practical utilization of ABC principles.

7

Role of Activity-Based Costing

There is a growing body of literature over the last decade, which argues that,

compared with traditional costing systems; ABC offers important advantages

to many organizations in general and service industry in particular. Despite its

slow diffusion rate, ABC method is now an accepted element of the

accounting and control systems of industrial and service firms, and it has been

employed in both Governmental and not-for-profit organizations. ABC is a

methodology that is designed to provide managers with more accurate

product and service costs, clearer insights into what causes costs to exist and

what drives costs and more relevant information for strategic decision-

making. ABC information reflects the activities performed in the institution,

the resources consumed, and the purpose of those activities. It provides a

focus on activities of those not visible through traditional accounting system.

With this information system, managers can make better decisions about what

happens in the business?, who does what in the business?, and what do

activities cost?. This redesign process may sometimes lead to higher levels of

productivity by either maintaining or minimising the overall costs.

ABM, on the other hand, refers to the use of ABC information to understand

and to bring significant changes in the way that the organizations do their

business. ABC system therefore is considered to be a strategic tool that allows

managers to quantify the value of products or services; use a common

language for base lining and benchmarking process; look at their activities

8

with a process view; and choose courses of actions based on ABC information.

Other management initiatives such as balanced scorecard and performance

management also draw upon the knowledge created by ABC (Maiga and

Jacobs, 2003). Strategic ABM information can provide vital support to the

management accountants about financial and non-financial measures of

performance to support the four perspectives (financial, customer relationship,

internal business process, and learning and growth) of the balance scorecard

project. In brief, ABM is a discipline- a modern accounting tool that focuses on

the management of activities as the route to improving organizational

performance and the value received by its customers. Therefore, the

management must now how to determine the cost of resources used, and then

trace these costs to the activity costs. The activity costs will ultimately arrive at

the product costs.

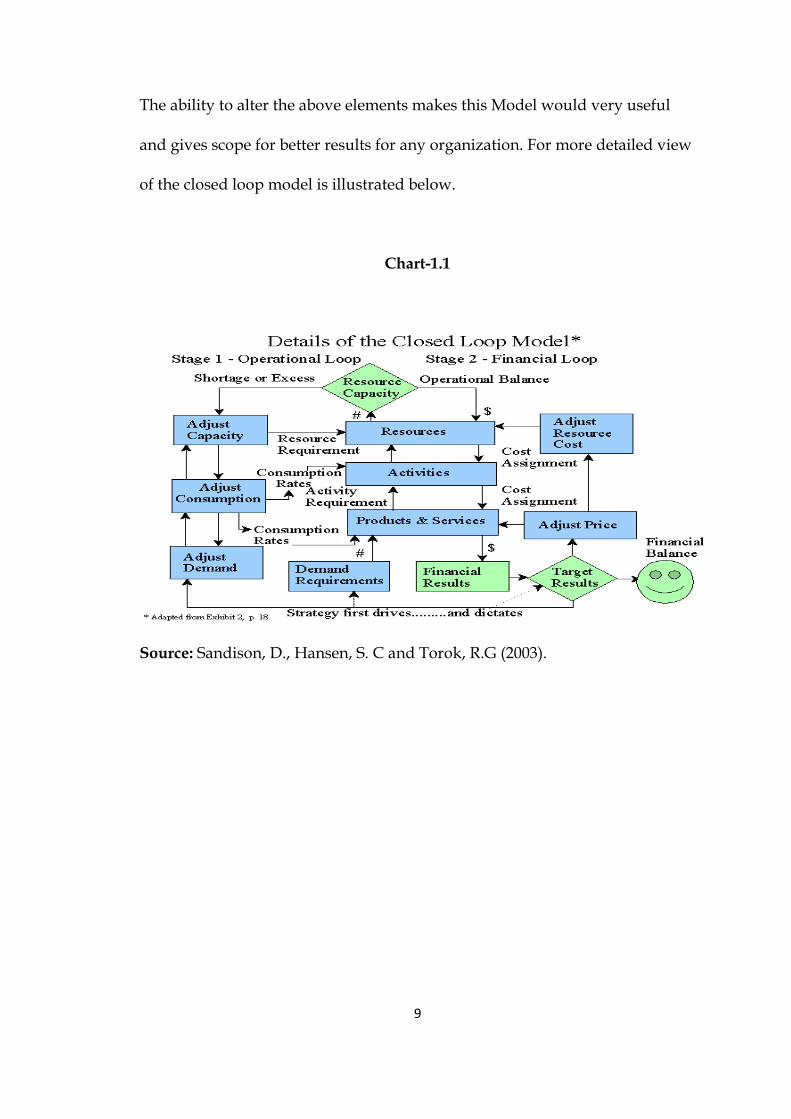

If any of these phases were to become imbalanced, the Closed Loop Model

allows for an adjustment with regard to the following five elements to reach

the target budget:

1. Product demand quality;

2. Activity and resource consumption;

3. Resource capacity;

4. Resource cost;

5. Product/service price.

9

The ability to alter the above elements makes this Model would very useful

and gives scope for better results for any organization. For more detailed view

of the closed loop model is illustrated below.

Chart-1.1

Source: Sandison, D., Hansen, S. C and Torok, R.G (2003).

10

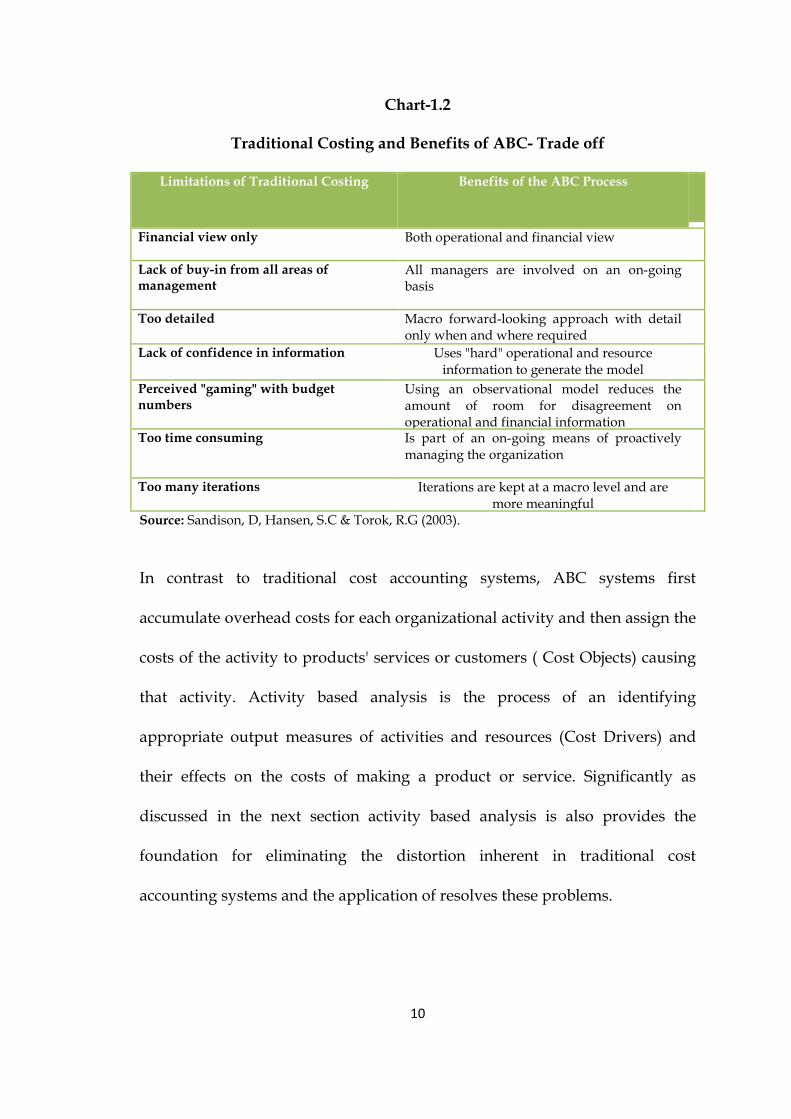

Chart-1.2

Traditional Costing and Benefits of ABC- Trade off

Limitations of Traditional Costing Benefits of the ABC Process

Financial view only Both operational and financial view

Lack of buy-in from all areas of management

All managers are involved on an on-going basis

Too detailed Macro forward-looking approach with detail only when and where required

Lack of confidence in information Uses "hard" operational and resource information to generate the model

Perceived "gaming" with budget numbers

Using an observational model reduces the amount of room for disagreement on operational and financial information

Too time consuming Is part of an on-going means of proactively managing the organization

Too many iterations Iterations are kept at a macro level and are more meaningful

Source: Sandison, D, Hansen, S.C & Torok, R.G (2003).

In contrast to traditional cost accounting systems, ABC systems first

accumulate overhead costs for each organizational activity and then assign the

costs of the activity to products' services or customers ( Cost Objects) causing

that activity. Activity based analysis is the process of an identifying

appropriate output measures of activities and resources (Cost Drivers) and

their effects on the costs of making a product or service. Significantly as

discussed in the next section activity based analysis is also provides the

foundation for eliminating the distortion inherent in traditional cost

accounting systems and the application of resolves these problems.

11

Purpose of ABC Methodology

Overall aim of this method of costing was to increase transparency of cost-

consumption. In the following are the resulting features of the implementation

of ABC model:

1. Capacity utilization and planning

2. Internal cost allocation

3. Customer profitability

4. Product posting and pricing

5. The controlling process-rolling with shorter cycles

6. Reporting- standard reports and Online Analytical Processing (OLAP).

Although our case study was taken place in the Iran context, the proposed

application of ABC model is not a modified from the German version of

ABC/M, as such “Prozesskostenrechnung” (process cost calculation). It is not

the purpose of this attempt to consider from the Anglo-American original

ABC (Cooper & Kaplan, 1998).

Review of Literature

In this section, an attempt has been made to present a broad review of the

work done by earlier researchers on the application of ABC system, its

implementation, ABC as a method for assessing the economics of

modularization, activity based performance management, cost control and

quality measures, integrating ABC and traditional costing and financial

reporting, ABC as a management tool for improving cost effectiveness of the

organizations across countries i.e., at national and international level.

12

1. Ildikó Réka Ştefan (2011), emphasized in the Romanian Journal of

Economics that new cost systems such as ABC and ABM could be a strong

couple that assures competitiveness and efficiency for each company. Another

objective is to present that, besides its disadvantages, firms implement the

ABC/ABM system because it permits better tracing of costs to objects,

superior allocation of overheads to cost objects, financial and non-financial

analysis and measures useful to managers and management accountants in

the decision making process.

2. Devinaga Rasiah (2011) in the paper titled ‘Why ABC is still lagging

behind the traditional costing in Malaysia? (Journal of Applied Finance &

Banking, International Scientific Press), made an attempt to compare activity-

based costing (ABC) model and traditional costing method as a comparative

study on a manufacturing and a service sector organization in Malaysia. He

calculated the cost and performance of activities, resources and cost objects

and revealed that ABC is as an alternative model to traditional cost-based

accounting systems. According to this study, the results indicated that most of

the operations managers have believed that their present costing systems

were adequate for decision making. In certain circumstances, operations

managers evaluated their cost systems as more effective than those using

other costing systems are as more effective than those using other costing

systems. Activity-based costing systems were evaluated as somewhat more

useful, but no relevant literature was found to indicate that either the external

13

or internal environment of the firm was correlated with the choice of costing

system.

3. Dorota Kuchta and Aleksandra Niedzielska (2011) at the 8th International

Conference on Enterprise Systems, Accounting and Logistics focused on the

main problems associated with the construction of Activity Based Costing

model for research projects. In large scale research projects huge sums of

money are spent and the donator wanted to know more about it. What is

more, in such projects a part of money has to be “lost” – because a part of

experiments do not succeed and a part of hypotheses turn out to be false.

Hence, it should be possible one to assess whether these losses are reasonable

and justified. Further, in large scale projects may results in which may not be

expected – e.g. applications of the invented technology in other domains. It

would also be useful to identify the cost of “byproducts”. Further, they

concluded that, it would also be extremely useful to know the cost not only of

final products, but also of activities - as similar activities may later be repeated

in other products. In short, as large scale projects cost is more than much, it

seems normal to expect that their cost is adequately planned and controlled.

Activity Based Costing is a tool which may help in anticipating probable costs

to be incurred.

4. Oleg Dejnega (2011) in his article ‘method time driven ABC as a literature

review’ and examines the implementation of this method in the condition of

manufacturing companies, distribution centres, agriculture, but also in the

field of services, especially in hospitality. This study aimed at finding out the

14

base principles of method time driven activity based costing in its right

application.

5. Abuthakeer, S.S, Mohanram, P.V and Mohan Kumar, G (2010) in

International Journal of Lean Thinking Volume 1 (2) with a title Activity Based

Costing Value Stream Mapping, attempted to integrate Value Stream Map

(VSM) with the cost aspects. A value stream map provides a blueprint for

implementing the principles of ABC and the manufacturing concepts by

illustrating information and materials flow in a value stream. The objective of

their study was to integrate various cost aspects. The idea is to introduce a cost

line, which enhances the clarity in decision making. The redesigned map

proves to be effective in highlighting the improvement in the cost accounting

areas, in terms of quantitative data. TAKT time calculation is carried out to set

the pace of production.

6. Boris Popesko (2010) made an attempt in International Review of Business

Research Papers, an article titled Utilization of Activity-Based Costing System

in Manufacturing Industries – Methodology, Benefits and Limitations, to

identify the detailed consequences of putting in place an ABC system and its

structure within the manufacturing industry. He analyzed the input and

output information and data required for an effective utilization of the system.

The close bond between cost allocation methodology and application

procedures are also necessary for effective ABC implementation, ABC system

resultant in not only efficiency of manufacturing businesses but also data

utilizable for decision making. He concluded that the effective implementation

15

of ABC system can provide accurate product costing and proves a useful aid

for manufacturing business operations.

7. Roztocki, Narcyz & Sally, M (2010) in their article adoption and

implementation of Activity Based Costing: A Web-based Survey, gathered

evidence about the current status of ABC adoption and implementation. They

observed that this method was introduced way back in 1980’s but this study

indicated that the rate of adopting ABC are now similar for service firms too.

They concluded that the larger firms are more likely to have adoption than

smaller firms, this is because (i) ABC is more beneficial in larger firms that

have a diverse mix of products or services; (ii) larger firms are also more likely

to have specialized staff familiar with this method.

8. Feras Alsamawi (2010) in their paper Activity Based Performance

Management – state-of-the-art and not time driven and he examine which

costing method -Activity Based Costing /Management (ABC/M) or Time-

Driven Activity Based Costing (TD-ABC) - fits best in the frame of

performance management. A literature review on both costing methods and

qualitative observations from a case study, where ABC/M was implemented

in a German logistics company, provide the basis for our research. TD-ABC

comes along with a variety of alleged improvements compared to existing

ABC/M, which is assumed to struggle with conceptual problems and low

diffusion rates (ABC-paradox). We can find that TD-ABC is only appropriate

for simple company models, because of its limited expressiveness and

accuracy. Our findings show shortcomings connected to the concept of TD-

16

ABC concerning data gathering and the myopic view on time to reflect all

business activities. Furthermore there is significant evidence that a part of the

academic world missed to capture ABC/M in its state-of-the-art; for them it

still exist in the conceived version from the mid-80�s. ABC/M provides all

features necessary to function within the frame of Performance Management.

We develop a framework which is based on ABC/M and name this Activity

Based Performance Management (ABPM). We show how ABPM supports to

align operational and financial decisions to a company’s strategy.

9. Fawzi, A (2008) in his Doctoral Thesis submitted to Dublin Institute of

Technology on barriers to adopting ABC Systems as an empirical investigation

using Cluster Analysis and the researcher seeks to establish why ABC

adoption rates are low given the claimed benefits of the system. The view is

taken that there are likely to be two sets of interacting variables influencing

ABC adoption, contingent variables and the company’s ability or willingness

to address implementation barriers. He argued that ABC system adoption and

success will depend upon specific contingent factors such as product diversity,

cost structure, firm size, competition, and business unit culture. A contingency

model of ABC adoption has been developed in order to examine and

investigate the reasons why the take up or adoption of ABC systems remains

low.

The survey undertaken comprised all firms listed in Business and Finance (2004)

Irelands Top 1000 Companies (the total number of companies included in the list

were only 925 companies). 218 questionnaires were returned, generates a

17

23.6% response rate through mail survey. The quantitative data were

processed using a SPSS program, leading to appropriate descriptive and

inferential statistical analysis, including frequencies, means, standard

deviations, chi-square, t-test, Mann-Whitney and ANOVA tests. Cluster

analysis was used to profile the companies according to the individually

significant contingent factors. Seven contingent variables were identified from

the literature, six of which were found to be statistically significantly

associated with ABC adoption. Companies were “clustered” using these

variables into three groups, and reasons for non-adoption were identified.

He suggests that (a) in the adoption of ABC; two distinct sets of variables are

at work. The ‘Contingent Variables’ which likely render it appropriate or

useful for the company to adopt ABC, and the company’s ability, or

willingness to address the ‘Barriers’ and difficulties associated with ABC

adoption. The results show a strong significant association between contingent

variables and the adoption of ABC; (b) the contingent variables alone may not

of themselves adequately explain the actual take up of ABC systems.

Moreover, it suggests that two companies which have similar profiles with

regard to contingent variables (with higher overheads, more product diversity

etc.) may yet reach different decision with regards to ABC adoption, due to

their differing abilities or willingness to address and overcome the issues

relating to ABC implementation, the results completely support this

suggestion. It is concluded that ‘Technical Issues’ are the most common factor

militating against ABC adoption within companies who are rejecting and

18

actively considering its adoption within the cluster whose profile most closely

matches the prime factors.

10. Katja Antikainen, Tarja Roivainen, Mirva Hyvärinen, Juhani Toivonen

& Timo Kärri(2005) at Frontiers of E-Business Research, Studied the evolution

of ABC to ABM and states that there were two phases also helped the

employees to see how the ABC works and how the ABC becomes ABM. It was

thought to be quite natural that at first they built a model to get the cost

information and at the second phase the planning and control point.

11. Jesper Thyssen, Poul Israelsen & Brian Jørgensen (2004) in their paper an

attempt has been made to examine the ABC as a method for assessing the

economics of modularization – a case study and beyond. The paper accounts

for an ABC analysis performed in a case company – Martin Group A/S –

where the object was to support decision-making concerning product

modularity. ABC was chosen because it is a costing method that in principle

takes a total cost perspective which as it is argued in the paper is a necessary

perspective when evaluating modularity. The ABC-analysis is structured in

such a way that it shows how much higher the materials cost of the over-

specified modularised component can be compared to the average materials

cost for the product-unique components that it substitutes. This procedure

provides case-specific insights to the designers. Moreover, it provides the

platform for stating three general rules of the cost efficiency of

modularization, which in combination points to the highest profit potential of

product modularization to be where (i) commonality between otherwise

19

product-unique modules are high, and where (ii) volume and (iii) difference

between unit-level cost of otherwise unique modules are low. The cost

analysis presented makes use of the activity and cost object hierarchies of

ABC. Two problems applying these are identified and discussed: (i) theory

provides only vague recommendations concerning the placement of the initial

design costs in the ABC model, and (ii) the product-profitability hierarchies

resulting from extended modular structures are more complex than described

in literature.

12. Carlos Manuel & Ferreira Lima (2004) studied the growing relevance of

costs assessment model, influenced by the activity-based costing (ABC) and

applicable to higher education institutions (An International Journal of

Economics and Management Research, 1(1), pp.57-65.). Therefore, based on

the procedures used by the services of a faculty belonging to a large

Portuguese university, they tried to create a model which allows the

attribution of each department’s expenditure to the various cost objects –

courses, research projects, services. In this way, they tried to present a model

which, without being too complex, has a level of detail sufficient enough to

enable the production of reliable information and which can be applied in the

context of higher education institutions.

13. Hughes, S. B & Gjerde, K. A. P (2003) highlighted in their study titled ‘Do

different cost systems make a difference’? (Management Accounting

Quarterly), that the dimensions of ABC, traditional and variable costing

system and they noticed that though the survey results indicate that “there are

20

few differences in the internal and external environments of ABC, traditional

and variable-cost system users”, they indicated that ABC and variable-cost

systems better serve users and that “the best system may integrate ABC and

variable-cost system attributes”. The results also found that industry pressures

did not influence the cost system used and that ABC systems were able to

present cost of unused capacity more clearly than the other systems. Further,

the authors concluded by stating that some of the reasons for the lack of

statistically significant environmental differences are due to the fact that “the

survey does not consider measuring the appropriate internal or external

dimensions”. The survey results reported that out of the 130 companies

surveyed, 46 companies have been using traditional cost systems, 11 use ABC

systems, 39 use both traditional and ABC cost systems (for result reporting

purposes, the ABC users were combined with the traditional and ABC users),

and 34 use variable-cost and TOC systems. From that group 29 use traditional

variables costing and 5 of them used TOC based costing.

14. Sandison, D., Hansen, S. C & Torok, R.G (2003) Activity-based planning and

budgeting: A new approach (Journal of Cost Management (March/April), pp.

16-22) developed a new approach to budgeting and planning is related to the

flexibility and dynamic aspect of the model. This aspect allows for a better link to

performance management and accountability. This approach is not too much time

consuming because of the proactive and flexible planning involved. Finally, authors

concluded that the ABPB approach accommodates the dynamic business

environment that the majority of organizations operate in today business setting.

21

15. Jones, T. C. & Dugdale, D (2002) developed that the idea of ABC is that

systems are built through the interactions of humans (actors) and non-humans

(networks) where actors or system builders fight with others in the network,

with competing networks, with consumers, with non-human actors and with

economic forces in the development and translation of theory into practice and

practice into theory. In order to study this phenomenon, the authors follow

actors (people and organizations) as they circulate and associate

intermediaries, i.e., literary inscriptions, technical artifacts, human beings and

money. ABC should be studied as a socio-technical system where the actors

and networks interact in waves or cycles.

16. Cokins, G. (2002) studied that the ABC data can be used to provide feed-

forward data that can be used for target costing. Further, ABC provides data

on cost centers, which product-related costs are traced to. ABC uses activity-

driver quantity measures to transmit a component’s usage on the equipment

costs. ABC data can be used to cost the components that comprise a product.

This is known as feature-based costing. In feature-based costing, the driver is

now thought of as a feature equivalent, rather than based on another measure

such as time. He concluded that it is a conversion of the time measure to make

the component into the types of features that require the time. These feature-

based costs can be used to project costs of a proposed new product, hence

making it useful for target costing.

17. Trond Bjornenak & Falconer Mitchell (2002) studied a comparative

analysis on ABC system accumulated in the UK and USA accounting journals

22

over the fourteen year period since the ABC emerged. This evidence is used

both longitudinally and cross sectional to gain insights into how ABC started,

how it has been communicated, how it has been researched, how it is

constituted, how it has generated attention and how it has developed and

changed.

18. Baxendale, S. J & Dornbusch, V (2000) analyzed the theory of constraints

(TOC) and found that tracing of resource costs to activities is the major

difference between ABC and TOC. ABC advocates tracing costs to obtain

product costs, whereas TOC adamantly discourages attempts to determine

product costs. However, both ABC and TOC are concerned about the unused

capacities of activities. When the constraint is an internal one, TOC is sufficient

to support short-term decision making. However, when the constraint is

external, TOC information by itself is not sufficient to support marketing

decision makers. They concluded that in order to make strategic judgments

concerning the development and promotion of new products? The answer is

to use TOC information in conjunction with ABC information.

19. Fayek (2000) linked the job-costing model with activity-based costing. He

conceived a schedule activity as an activity in ABC. He proposed that costing

each schedule activity and job is activity-based costing. However, a schedule

activity in construction differs from an activity in activity-based costing

because each schedule activity is a task or service that a contractor or crew is

supposed to provide, as opposed one of several process steps involved in its

execution or production. The ‘activity’ in ABC refers to the production

23

process. The ‘activity’ in ‘schedule activity’ refers to the product of production

processes, but neglects the processes themselves. Therefore, assigning costs to

schedule activities in construction projects is not equivalent to activity-based

costing.

20. Back et al. (2000) and Maxwell et al. (1998) linked process modelling and

simulation with activity-based costing. They expanded the concept of activity

following that of process modelling. However, their model uses only one

resource driver such as time and does not recognize activity cost drivers. The

model does not recognize a cost hierarchy either. Moreover, their model

concentrates on field operations neglecting other elements in the value chain

such as procurement, material handling, production, and hand-over.

21. Coate, C. J & Frey, K.J (1999) made an attempt to integrate both ABC and

TOC into the traditional cost accounting system and presented a brief

discussion about the two most popular cost accounting and production

theories, ABC and the Theory of Constraints (TOC), and to determine if ABC

and TOC are complimentary or competing concepts. Further, the article

focuses on whether both theories can be integrated with financial reporting.

By integrating ABC and TOC into the traditional cost accounting system, the

resulting system combines variance analysis with three key elements of TOC:

(i) constraint identification,(ii) constraint exploitation and (iii)

interdependencies of resources. “Considering system constraints in an ABC-

based variance analysis is an excellent way to coordinate cost system, TOC

24

and Financial Reporting”. Thus, ABC and TOC are complementary to each

other and not incompatible with financial reporting.

22. Cokins, G (1999) in the Journal of Cost Management (July/August),

attempted to help management to clear up confusion about Activity Based

Costing (ABC) and Activity Based Management (ABM) and how these

concepts should be applied to help solve operational and strategic problems

with the data that is produced by these systems. He noted that in order to

sustain an ABC/ABM system, management accountants and employees who

intend to use the data must have an understanding of the system and be sold

on the idea. ABC/ABM should not be seen as an improvement program, but

as an enabler for other improvement programs. He concluded that the output

of ABC/ABM is always the input for some other system. Once the appropriate

level of aggregation is achieved then the connection of ABC/ABM data to the

analysis of business problems will become obvious.

23. Huang, L (1999) in Journal of Cost Management (Nov/Dec), developed a

model managing costs and its integration of ABC and the theory of constraints

(TOC) as opposing views of the nature of product costing. Product costing

from an ABC perspective assumes all costs are traceable to products and vary

in proportion to certain cost drivers. From a TOC perspective, costs are fixed

and sunk relative to the product choices and production-level decisions. Thus,

ABC cost information is inputted into the TOC for product-mix decisions. In

conclusion, Huang makes a point that by taking advantage of integrating the

TOC and ABC a firm will attain quality decision-making. The study concluded

25

that in order to gain a complete understanding of the integration between

ABC and the TOC, Huang first defines ABC and TOC from various cost

accounting analysts/theorists’ ABC was first developed in 1971 and became

popular in the 1980’s. In 1971 an ABC framework was provided that included

five fundamental ideas.

24. Brimson, J. A (1998) in the paper titled Feature costing: Beyond ABC

(Journal of Cost Management (January/February)) highlighted several

advantages of cost accounting systems over the conventional overhead

allocation method and activity based costing method. One advantage is that

feature costing uses the process management model, and this model allows for

a better understanding of product costing. Another advantage of feature

costing is the ease of use over previous methods. This is due to the fact that

less data is needed to calculate the product cost. The last advantage is that

feature costing determines the factors that cause a variation to happen. This

allows for improvements to be made to the product process.

25. Kaplan, R. S (1998) in his book Cost & Effect – Using Integrated cost

systems to drive profitability and performance, (Harvard Business School

press), believes that compensation is critical for successful innovation in action

research. Companies should not view the involvement of action researchers

with implementations (or their consulting alliance partners) as a favor they are

doing for the researchers, granting them permission to do research on their

sites. The study found in Kaplan’s case, the compensation was a small, but

26

important, hurdle to improve the likelihood that the project had strong

support within the company.

26. Kee, R. (1998) suggested in his paper- Integrating ABC and the theory of

constraints to evaluate outsourcing decisions that the companies adopting

ABC system must produce the component over the short- term and make a

series of short-term decisions that could lead to producing the component

over an extended time period. Using ABC alone could lead to outsourcing the

component immediately, even though it is more economical for the company

to continue producing the component in the short- run. Therefore, ABC and

TOC are more beneficial if used together than alone in making outsourcing,

resource-allocation decisions.

27. Krumwiede, K. R. (1998) revealed in his article ‘ABC: why its tried and

how it succeeds’ that of the companies who have tried ABC and found that

there are 54 percent of the companies to the extent of somewhat using for

decision-making and 89 percent of those companies using ABC as it was

worth only in case of cost implementation. However, not all the companies

implementing ABC have proven to be beneficial. Many users commented that

ABC is not the single answer to all of their needs, but it is one of many tools to

be used in order to attain the organization’s long-term goals.

28. Brausch, J. M & Taylor, T.C (1997) in their article they focused to address

the failure of companies to use the full capacity of committed resources, and to

explore the costing and managing problems of production capacity for unused

material. The authors found that mostly manufacturing (or operations)

27

personnel (with informal communication with production, marketing, and

other areas) are responsible for managing capacity, while in some cases a CEO,

or a joint effort by manufacturing, marketing, and finance individuals, exists.

Various plans, reports, and systems exist that could provide accurate

information about capacity utilization. However, the companies lacked a

proactive view of production potential other than meeting the expectations of

sales or marketing. For instance utilization rate reports can measure (true)

unused capacity, if the measurement base used is (full) output potential,

seldom if ever the case. It is noticed from this study the conditions of unused

or excess capacity are and have been reported by cost accounting as

unfavorable volume variances. The volumes used ranging from theoretical to

concept of capacity. It is concluded that methods used, except possibly

theoretical capacity, result in volume variances that reflect the failure to reach

production levels built into the overhead rate formula, not unused capacity.

29. Ittner, C. D., Larcker, D.F & Randall, T (1997) in their article “ABC

hierarchy, production policies and its impact on firm’s profitability” indicates

that the operational measures used by the organization correspond to the cost

hierarchy classifications, though inconsistent with some prior findings.

Additional findings of relationships between particular cost drivers and the

organization’s production and inventory policies indicate that the cost driver

analysis should be tailored to the production environment. The authors

identify several areas for further research.

28

30. Gaiser, B. (1997) German cost management systems narrated an integrated

approach to ABC in German context of cost control system and he explains

that there is no perfect way or magical formula to calculate cost. It all depends

among other things, nature of the company, manufacturing product or service,

the ratio of direct costs to indirect costs and the information needed by

management. Another important development in German cost management is

Prozesskostenrechnung (process costing or German version of ABC). Which

was created in 1987, it integrates concepts of ABC into German control

systems. Process costing, as defined by the author, makes a distinction

between processes and sub processes. It is concluded that the cost accountants

usually pays more attention to main processes in order to plan and monitor

improvement in productivity. Indirect costs from main processes are assigned

to the outcome using a single cost driver. According to him, the German

concept of process costing mainly emphasizes on indirect activities, whereas

GPK is still used to provide cost data for control in production activities.

31. Gosselin, M. (1997) examined in his article the effect of strategy and

organizational structure on the adoption and implementation of ABC

innovations. He found adoption of ABC is associated with more vertical

integration; whereas implementation is associated with more centralized and

formal structures of firm. The author proposes that once a firm decides to

adopt ABC, a higher degree of centralization and formalization make it harder

for management to stop the implementation of the system. Additionally, once

committed to putting the system in place, mechanistic firms provide the

29

needed support for full implementation. This study explored the “ABC paradox” via a

diffusion of innovation perspective. Further, ABC is treated as an innovation, and

organizational strategy and structure are examined as possible factors as

associated with ABC implementation.

32. Caltrider, J, Pattison,D & Richardson, P (1995) described the challenges

that a hospital faces in improving quality and reducing costs in the paper Can

cost control and quality care coexist?. They found that the Children's Hospital

in San Diego California experienced pressure from its accrediting body to

improve quality and reduce costs in 1992. The hospital achieved almost

immediate results from the pilot teams. The Orthopedics Unit achieved a 20

percent reduction in costs of treating femur fractures. Patient Registration and

Billing reduced billing errors by 50% to insurance companies. The Neonatal

unit achieved a 20 percent reduction in cost per case.

33. Hammer, B & Stinson, C.H (1995) in their article they opined that by

modifying both the accounting of environmental cost to better trace cost to

processes that cause them and proper management incentives can lead

companies to better manage and control cost associated with environmental

compliance and waste management. It is noticed from their attempt that some

of the larger costs are often traced to actual activities, but many other costs

such as compliance and oversight cost are often assigned to general overhead

and then allocated with a generic driver across the company. It is also

examined that, if a company actually produces hazardous waste another cost

is produced. This cost is often a step function based on the volume of materials

30

produced that triggers different levels of Resource Conservation and Recovery

Act (RCRA) compliance. Plants that are considered “small-quantity

generators” are exempt from RCRA reporting. Those that produce more are

faced with increasing reporting requirements, while those that are considered

“treatment, storage, and disposal” (TSD) face the most extreme reporting

requirements.

34. Holmen, J. S (1995) in his doctoral study “ABC Versus TOC and their

relevance of time” and he developed a scheduling approach known as

optimized production technology (OPT) that used TOC principles. This

method was coined "synchronous manufacturing" in 1984 and became the

theory of constraints in 1987. When comparing ABC with the TOC it becomes

clear that the cost paradigms are based on different time horizons—ABC has a

long run horizon, while the TOC has a short-run horizon. The concept of

short-run versus long- run looks at whether the capacity of the production

facility can be expanded or contracted. It is assumed that in the short-run

production capacity is fixed and cannot be readily changed. This creates

bottlenecks and brings the assumptions of the TOC to life. In the long run,

however, more costs become variable, especially when spending and

consumption are brought into alignment. This reinforces the assumptions

underlying ABC. These methods are based on different sets of assumptions

with separate time horizons; thus, claims that one approach is superior over

the other should be abandoned. There is room for both approaches when they

are used appropriately. He suggested that the accountants need to understand

31

each tool and how they work in order to know when one is appropriate and

the other is not.

35. Boer, G & Jeter, D (1993) in their study they examined various modern

manufacturing methods the material cost and labour cost data for a variety of

manufacturing industries for the years 1899 through 1987. Specifically, he

reviews assertions made by accounting thinkers and empirical data related to

the validity and generality of these claims. Moreover, the emphasis in their

paper was to provide evidence of the extent to which manufacturing has

changed over time and to examine the nature of these changes. Additionally, it

is the authors purpose to provide similar data for as many industries as

possible.

36. Johnson, H. T (1987) studied the declining role of cost management in 20th

century cost accounting and he concluded by pointing out that cost

management information needs to benefit managers, not accountants. Cost

management systems should produce information that will help management

“identify and evaluate the resources needed to deliver value to the customer.”

Further, the cost accounting information is not just relevant to management

decision-making but also everything for the firm and its shareholders. Author

believes that manufacturers stopped gathering cost management information

early in the 1900s because the costs to gather and process the information

outweighed the benefits that it provided. Manufacturers found other ways to

maintain profitability and did not focus on cost management from the 1920s to

32

the 1950s. The author believes that defenders of, as well as critics of cost

accounting do not understand its purpose.

Research Gap

From the review of previous studies, this section highlights the gaps that are

given scope for present study. First, a majority of research still was done

mostly in developed countries and very little work has been done in

developing countries, especially Asian context. Thus, it is necessary to identify

whether the Asian culture and way of doing business may have a different

impact of ABC adoption and implementation. Second, a majority if ABC

research reviewed adopted the behavioral and organizational variables and

factors influencing ABC success. Third, a majority of work done is on the

development of ABC; distinguish between both traditional costing methods

and ABC from their relative merits and demerits; ABC as a method for

assessing the economies of modularization; an integration of ABC and the

theory of constraints, etc. Fourth, few researches have examined the effects of

corporate culture on ABC success empirically. Finally, the review literature

shows most of the studies on ABC implementation researches were conducted

using quantitative method such questionnaire survey and there are very few

research used qualitative methods. The next research gap is that no previous

research done on the application of ABC in Iran general and KSFIC

(Khootka) of Iran in particular.

This study focuses on the experiences of users and non-users of ABC

system within the food and beverage industry with special reference to Komaz

33

Sabah Food Industrial Complex (Khootka) of Iran. The food and beverage

market in Iran is very competitive; many large retail organizations stimulate

competition in terms of price and on-time delivery, while consumers demand

a larger array of differentiated products. Use of advanced technology could

provide food production process and the producers could offer a wider array

of products and attractive packages. This in turn leads to more complex

production and distribution systems. Complexity of production and logistic

systems, combined with a large number of differentiated products are

considered suitable situations for the application of Activity-Based Costing.

Having reviewed the previous research studies listed above and keeping in

view of statement of the problem, and there is no studies of similar kind was

done so far with regard to application of ABC in food industry and hence, an

attempt has been made here in this study “a study on application of ABC in

Komaz Sabah Food Industrial Complex (Khootka) of Iran’ is undertaken to fill

the research gap.

Significance of the study

Increased liberalization and globalization of economies have not only

intensified the competition to be faced by the Iranian business enterprises in

both international and domestic market but also put a demand on them to

produce products of different quality to suit the diverse customer groups

located all over the world. Higher business risk owing to dynamism in

customers’ taste, innovative strategies by the competitors and other micro

34

level changes demand the contemporary managers to be strategic with regard

to product and process design, pricing,, product mix and distribution

decisions. In this context, the four important factors that have influenced the

Iranian business environment which include: (i) market dynamism; (ii)

production dynamism; (iii) management innovation and (iv) cost dynamism.

To equip with the above dynamisms and to reduce the cost of production, it is

essential to renovate the cost systems is more essential for the emerging

competitive environment. On the other hand, the problem of traditional cost

systems is not only confine to manufacturing costs but also overheads

including marketing costs are hidden under the traditional cost system. In

most of the traditional costing promotional overheads being allocated on the

basis of sales which create further typical problems of over allocation or under

allocation; while some old established brands are over supported, the new

upcoming brands are under supported. Because of the facts that some

important items of cost remain hidden under conventional system, the

rationality of cost allocation tends to disappear. To get rid of such problem

they advocate for using an accurate activity based costing system combined

with an annual zero-based appraisal that would ensure a focused product line

optimally use manufacturing capacity, advertising and promotion budget,

sales force time and available retail space.

Activity-Based Costing (ABC) arose in the 1980s from the increasing

lack of relevance of traditional cost accounting methods. The traditional

35

costing methods were designed around 1870 - 1920 and in those days industry

was labour intensive, there was no automation, the product variety was small

and the overhead costs in companies were generally very low compared to

today. However, from the 1960s - particularly 1980s - this changed rapidly. For

these reasons, and more, traditional cost accounting system has been called

everything from 'number one enemy of production' and questions whether it

is 'an asset or a liability' have been raised. The question of course is whether

ABC has overcome these deficiencies or not? In fact, ABC has been called one

of the most important management innovations- modern accounting systems.

In view of this and the studies listed above, a modest attempt is made to study

the differences in ABC system and VBC system of accounting in a

manufacturing industry of Iran in general and KSFIC in particular.

Objectives of the Study

The main objective of the study is to analyze the application of ABC system

of accounting for Komaj Saba Food Industrial Complex (Khootka), Iran by

identifying and grouping the activities involved in resources consumed and to

study the cost accumulation procedures and practices under traditional

costing system and cost accumulation under ABC in KSFIC in order to know

whether there is any significance difference between cost per product by ABC

and VBC techniques of cost accounting.

36

The specific objectives of the present study are as follows:

1. To present an overview of Activity Based Costing and Profile of KSFIC;

2. To study the cost accumulation procedures and practices under Volume

Based Costing (VBC) at KSFIC of Iran;

3. To assess the application of ABC system of cost accounting and its

impact on the profitability of KSFIC; and

4. To make a comparative analysis of ABC system and VBC system of

accounting and their effectiveness in terms of profitability and cost

reduction along with some measures for effective implementation of

ABC system in KSFIC, Iran.

Hypotheses

It is proposed:

1. H0: there is no significance difference in indirect cost allocation by ABC

and VBC technique for different products, viz; Biscuit, Wafer, Chocolate,

Candy, Cake and Spaghetti.

2. H1: there is a significance difference in indirect cost allocation by ABC

and VBC technique for different products under study.

Research Methodology

The present study is an applied research in nature. The study mainly relies on

secondary data for which secondary data has been collected from annual

reports of the company. The study is confined to six products of KSFIC Viz;

37

Biscuits, Wafers, Chocolates, Candies, Cakes and Spaghettis. Currently the

EBIT is arrived using volume based costing.

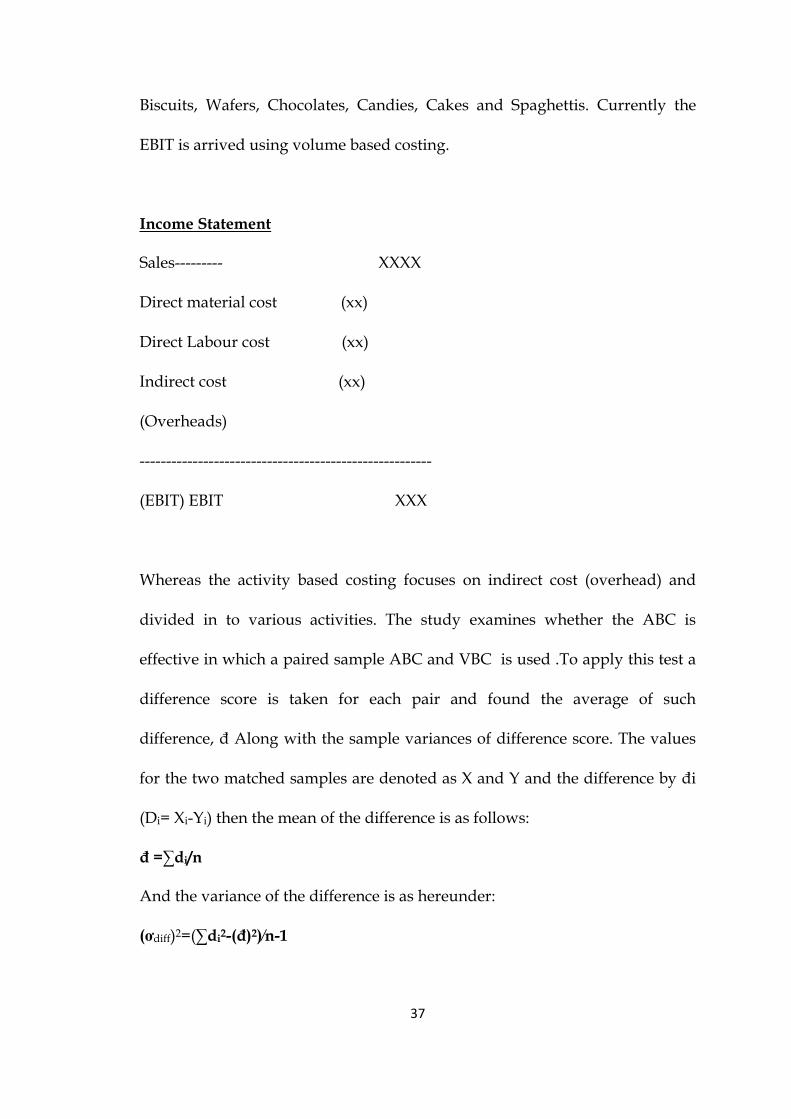

Income Statement

Sales--------- XXXX

Direct material cost (xx)

Direct Labour cost (xx)

Indirect cost (xx)

(Overheads)

-------------------------------------------------------

(EBIT) EBIT XXX

Whereas the activity based costing focuses on indirect cost (overhead) and

divided in to various activities. The study examines whether the ABC is

effective in which a paired sample ABC and VBC is used .To apply this test a

difference score is taken for each pair and found the average of such

difference, đ Along with the sample variances of difference score. The values

for the two matched samples are denoted as X and Y and the difference by đi

(Di= Xi-Yi) then the mean of the difference is as follows:

đ =∑di/n

And the variance of the difference is as hereunder:

(ơdiff)2=(∑di2-(đ)2)⁄n-1

38

Assuming the said difference to be usually distributed and independent, we

have applied pair t-test for judging the significant differences and work out

the test statistic t as under:

t = (đ– 0) ⁄ (ơdiff ÷ √n) with n degree of freedom

đ=Mean of difference

Ơdiff = standard deviation of differences

n = number of matched pairs

An identification of non-value added cost further determined by the following

procedure:

• Identify the factors which influence the cost of each activity – the cost

drivers.

• Collect accurate data on direct labour, material and overhead costs.

• Establish the demands made by particular activities, using the cost

drivers as a measure of demand.

• Trace the cost of activities products according to a services demand for

each activity.

The rules developed by Kaplan and Cooper (1998) for these processes are:

1. Focus on expensive resources, this directing attention to resource

categories where the new costing process has the potential to make big

differences on product costs,

2. Emphasis resources whose demand patterns are un-correlated with

traditional measures.

39

Thus, ABC is the process of tracing costs first from resources to activities and

then from activities to specific services. The technique of ABC lays the

importance of different costs for different services and the identification of just

those costs which are relevant to a particular decision. However, it does not

challenge the conventional accounting methods and theory; instead, it refines

the ideas and concepts of conventional methods.

ABC system require implementation of the following cost concepts:

• Multiple cost component names.

• User defined cost component names.

• Segregation of direct and indirect costs.

• Use of charge codes and other user – defined cost drivers.

• User defined activity measures and statistics.

Scope and Period of the Study

The present study confined to the existing VBC accounting system and it is

compared with ABC which is proposed accounting system in Komaj Sabah

Food Industrial Complex of Iran as a case study and which covers a period of

six years from 2005-06 to 2010-11.

40

Limitations of the Study

The study is mainly based on secondary data though at some places primary

data has also been used. The data has been collected from more than one

source and there may be discrepancies in the data on account of their

reporting. While computing the percentages and averages the figures are

approximated. Therefore, sometimes the totals may not exactly tally. Another

limitation may be pertaining to the limited period of the study i.e., only five

years regarding an application of ABC system of accounting at KSFIC may

not be reflecting on the firms’ profitability and even in the future.

Plan of the Study

The present study has been organized into seven chapters. The chapter details

are as under.

Chapter –I Introduction

This chapter deals with the backdrop of the study. Limitations of traditional

costing systems, it also presents origin of ABC, Rationale for adopting ABC as

an accounting system, role and importance of ABC system of accounting.

Further, it is also reviews the relevant literature on the subject, need for and

significance of the study, objectives of the study, research methodology, scope

and limitations of the study and organization of the study.

Chapter – II An Overview of Activity Based Costing

This chapter highlights an application of ABC system of costing an overview.

It also covers the conceptual framework of ABC analysis, process of activity

based costing, logic and assumptions, models of ABC, traditional approaches

41

of costing. Further, this chapter also presents a brief picture of costing

procedures and the usage of ABC costing system across the globe and in Iran

in particular.

Chapter - III Profile of Komaj Saba Food Industrial Complex

In this chapter, the genesis and a brief profile of Komaj Sabah Food Industrial

Complex (Khootka) of Iran were covered including their broad spectrum of

operations over a period of five years and also since its inception.

Chapter – IVVBC Cost Accumulation Practice in Komaj Saba Food

Industrial Complex

This chapter presents a description of cost accumulation procedures and

practices in Komaj Saba Food Industrial Complex of Iran under volume based

costing (VBC).

Chapter – V Application of ABC and its Impact on Profitability

The chapter covers in-depth analysis of cost allocation procedures and

practices to various activities of the company high lighting the cost

accumulation at each cost centre.

Chapter - VI Comparative Analyze of ABC and VBC Systems in Komaj Saba

Food Industrial Complex

The chapter makes a comparative analysis of cost allocation practices of KSFIC

with regard to Activity Based Costing and Volume Based Costing system of

accounting of KSFIC.

42

Chapter - VI Summary, Conclusion and Findings

This is the last chapter which presents summary of conclusions and findings

that emerged from the study. Further, this chapter also highlights the scope

for further research to be done in the area.

43

References

1. Ildikó Réka Ştefan (2011). ABC and Activity based Management (ABM)

Implementation – Is This the Solution for Organizations to Gain

Profitability?, Romanian Journal of Economics, pp. 151-168.

2. Devinaga Rasiah (2011). Why ABC is still tagging behind the traditional

costing in Malaysia? Journal of Applied Finance & Banking, International

Scientific Press, Vol.1 (1), Pp. 83-106.

3. Dorota Kuchta & Aleksandra, N (2011). Activity Based Costing in large

scale research projects, 8thInternational Conference on Enterprise Systems,

Accounting and Logistics (8Th ICESAL 2011), pp. 11-12.

4. Dejnega, O (2010). Methods of ABC and Time- driven ABC and their

application in practice by measuring processing costs. Paper presented at

the 12th international conference MEKON, Ostrava, Czech Republic,

February 3-4, 2010.

5. Abuthakeer,S.S., Mohanram, P.V & Mohan Kumar, G (2010). Activity

Based Costing Value Stream Mapping, International Journal of Lean

Thinking Volume 1 (2).

6. Boris Popesko (2010). Utilization of Activity-Based Costing System in

Manufacturing Industries – Methodology, Benefits and Limitations,

International Review of Business Research Papers, Vol.6 (1), Pp. 1-17.

7. Roztocki, Narcyz & Sally, M (2010). Adoption and implementation of

Activity Based Costing: A Web-based Survey. Paper presented at

international conference, state university of New York, 2010.

44

8. Feras Alsamawi (2010). Activity Based Performance Management – state-

of-the-art and not time driven. Unpublished thesis submitted for the

degree in Finance and International Business, University of Aarhus,

October, 2010.

9. Fawzi, A (2008). Barriers to Adopting Activity-based Costing Systems

(ABC): An Empirical Investigation Using Cluster Analysis, Unpublished

Doctoral Thesis submitted to Dublin Institute of Technology, 2008.

10. Katja, A,, Tarja, R., Mirva, H., Juhani Toivonen & Timo Kärri(2005).

Activity-Based Costing Process of a Day-Surgery Unit – from Cost

Accounting to Comprehensive Management, Frontiers of E-Business

Research.

11. Jesper Thyssen, Poul Israelsen & Brian Jørgensen (2004). Activity Based

Costing as a method for assessing the economics of modularization – a

case study and beyond. Working paper 09-04, September 2004.

12. Carlos Manuel Ferreira Lima (2004). The Applicability of the Principles of

Activity Based Costing System in a Higher Education Institution. An

International Journal of Economics and Management Research, 1(1), pp.57-

65.

13. Hughes, S. B & Gjerde, K.A.P (2003). Do different cost systems make a

difference? Management Accounting Quarterly, pp. 22-30.

14. Sandison, D, Hansen, S.C & Torok, R.G (2003). Activity-based planning

and budgeting: A new approach. Journal of Cost

Management (March/April), pp. 16-22.

45

15. Jones, T. C & Dugdale, D (2002). The ABC bandwagon and the juggernaut

of modernity. Accounting, Organizations and Society 27(1-2), pp. 121-163.

16. Cokins, G (2002). Integrating target costing and ABC. Journal of Cost

Management (July/August), pp. 13-22.

17. Trond Bjornenak & Falconer Mitchell (2002) The Development of Activity

Based Costing Journal Literature 1987-2000, European Accounting Review,

Vol. 11 (3), 2002.

18. Baxendale, S. J & Dornbusch, V (2000). Activity-based costing for a

hospice. Strategic Finance (March), pp. 60-70.

19. Fayek, A.R., (2000). An Activity-Based Data Acquisition and Job Costing

Modelling, Proceedings of the Construction Congress IV: building

together for a better tomorrow in an increasingly complex world, Walsh,

K.D.(editor), ASCE, Orlando, FL, 30-35.

20. Back, W.E., D.A., Maxwell, & L.J., Isidore, (2000). Activity-Based Costing

as a Tool for Process Improvement Evaluation, Journal of Management in

Engineering, ASCE, March/April, 48-59.

21. Coate, C. J & Frey, K.J (1999). Integrating ABC, TOC, and financial

reporting. Journal of Cost Management (July/August), pp. 22-27.

22. Cokins, G (1999). Using ABC to become ABM. Journal of Cost

Management (January/February), pp. 29-35.

23. Huang, L (1999). The integration of activity-based costing and the theory

of constraints. Journal of Cost Management (Nov/Dec), pp. 21-27.

46

24. Brimson, J. A (1998). Feature costing: Beyond ABC. Journal of Cost

Management (January/February), pp. 6-12.

25. Kaplan, R & Cooper, R (1998). Cost & Effect – Using Integrated cost

systems to drive profitability and performance, Harward Business School

press, ISBN: 978-0-87584-788-7.

26. Kee, R (1998). Integrating ABC and the theory of constraints to evaluate

outsourcing decisions. Journal of Cost Management.pp.24-36.

27. Krumwiede, K. R (1998). ABC: Why it's tried and how it succeeds.

Management Accounting (April), pp. 32-34, 36 & 38.

28. Brausch, J. M & Taylor, T.C (1997). Who is accounting for the cost of

capacity? Management Accounting: pp. 44-46, 48-50

29. Ittner, C. D., Larcker, D.F & Randall, T (1997). The activity-based cost

hierarchy, production policies and firm profitability. Journal of

Management Accounting Research (9), pp. 143-162.

30. Gaiser, B (1997). German cost management systems. Journal of Cost

Management (September/October), pp. 35-41.

31. Gosselin, M (1997). The effect of strategy and organizational structure on

the adoption and implementation of ABC. Accounting, Organizations and

Society 22(2), pp. 105-122.

32. Caltrider, J., Pattison, D & Richardson,P (1995). Can cost control and

quality care coexist? Management Accounting (August), pp. 38-42.

33. Hammer, B & Stinson, C.H (1995). Managerial accounting and

environmental compliance costs. Journal of Cost Management. Pp. 4-10.

47

34. Holmen, J. S (1995). ABC vs. TOC- It’s a matter of time. Management

Accounting (January), pp. 37-40.

35. Boer, G & Jeter, D (1993). What's new about modern manufacturing?

Empirical evidence of manufacturing changes. Journal of Management

Accounting Research (5):pp. 61-83.

36. Johnson, H. T (1987). The decline of cost management: A reinterpretation

of 20th-century cost accounting. Journal of Cost Management (Spring), pp.

5-12.