Embed Size (px)

Citation preview

Chapter

Brealey, Myers, and Allen

Principles of Corporate Finance

11th Global Edition

THE VALUE OF COMMON STOCKS

4

4-4-22

4-1 HOW COMMON STOCKS ARE TRADED

•Primary Market• New securities

•Secondary Market• Previously-issued securities

•Common Stock• Ownership shares in publicly-held corporation

4-4-33

4-1 HOW COMMON STOCKS ARE TRADED

• Electronic Communication Networks (ECNs)• Computer networks that allow electronic trading

• Exchange-Traded Funds (ETFs)• Stock portfolios bought/sold in single trade

4-4-44

4-2 HOW COMMON STOCKS ARE VALUED

• Book Value• Net worth of firm according to balance sheet

• Dividend• Periodic cash distribution from firm to the shareholders

• P/E Ratio• Price per share divided by earnings per share

• Market Value Balance Sheet• Financial statement that uses market value of assets and liabilities

4-4-55

4-2 HOW COMMON STOCKS ARE VALUED

• Discounted Cash Flow (DCF) Formula• Value of a stock = present value of future cash flows

dividends) future dPV(expectePV(stock)

4-4-66

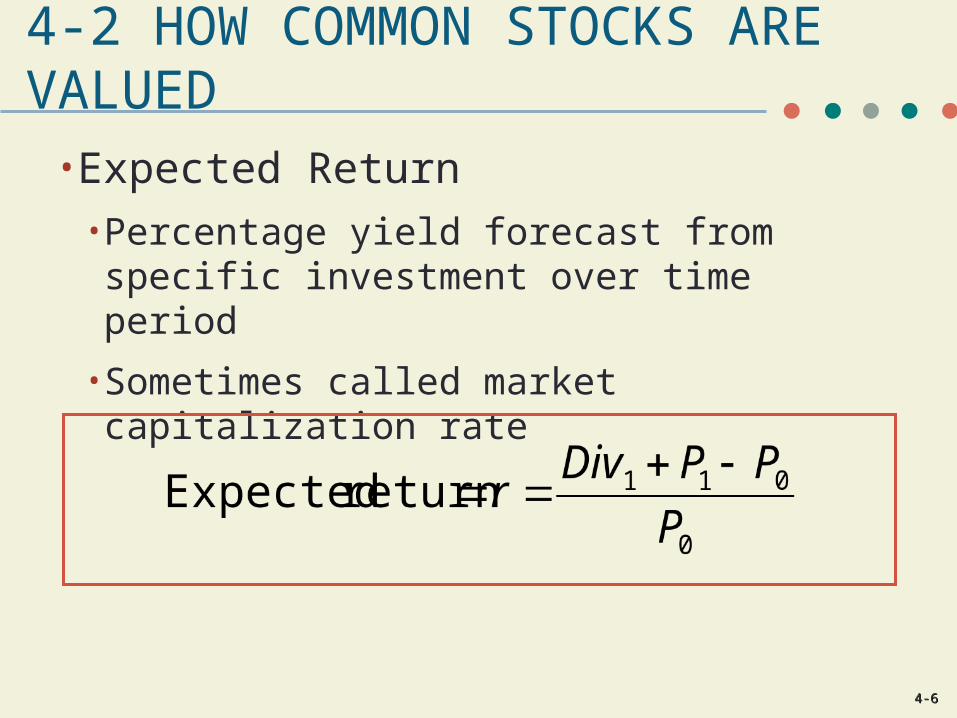

4-2 HOW COMMON STOCKS ARE VALUED

• Expected Return• Percentage yield forecast from specific investment over time period

• Sometimes called market capitalization rate

4-4-77

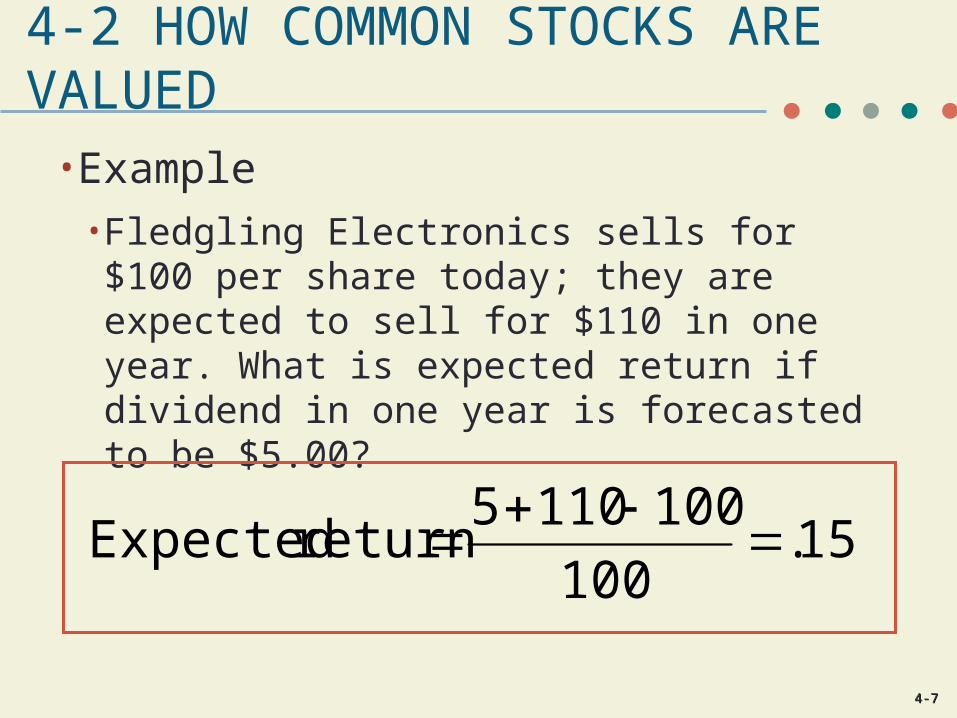

4-2 HOW COMMON STOCKS ARE VALUED

• Example• Fledgling Electronics sells for $100 per share today; they are expected to sell for $110 in one year. What is expected return if dividend in one year is forecasted to be $5.00?

15.100

1001105return Expected

4-4-88

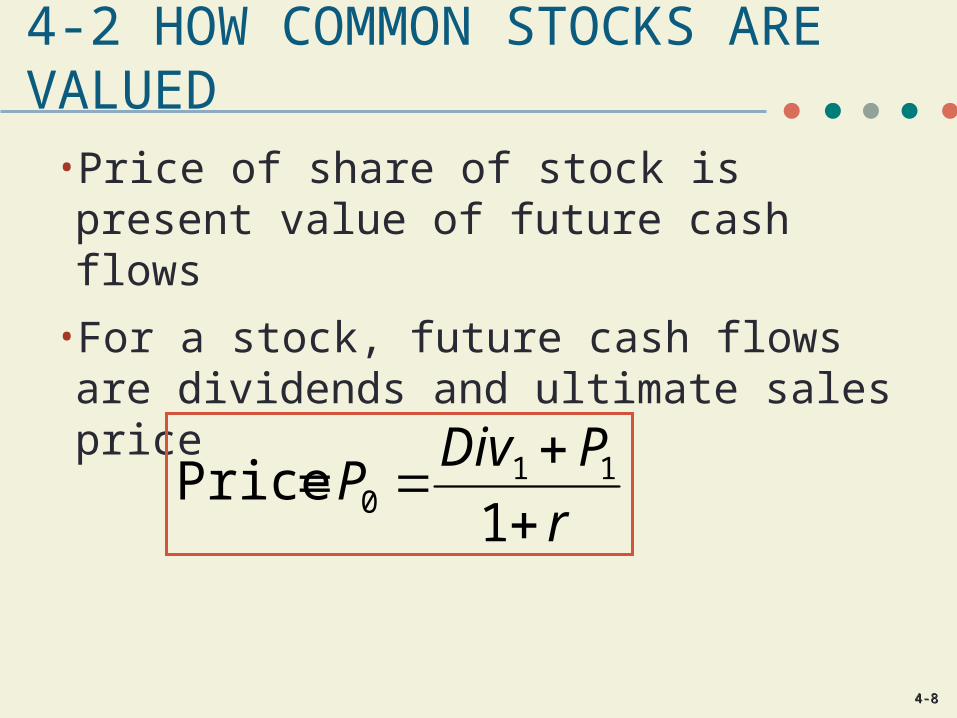

4-2 HOW COMMON STOCKS ARE VALUED

• Price of share of stock is present value of future cash flows

• For a stock, future cash flows are dividends and ultimate sales price

r

PDivP

1

Price 110

4-4-99

4-2 HOW COMMON STOCKS ARE VALUED

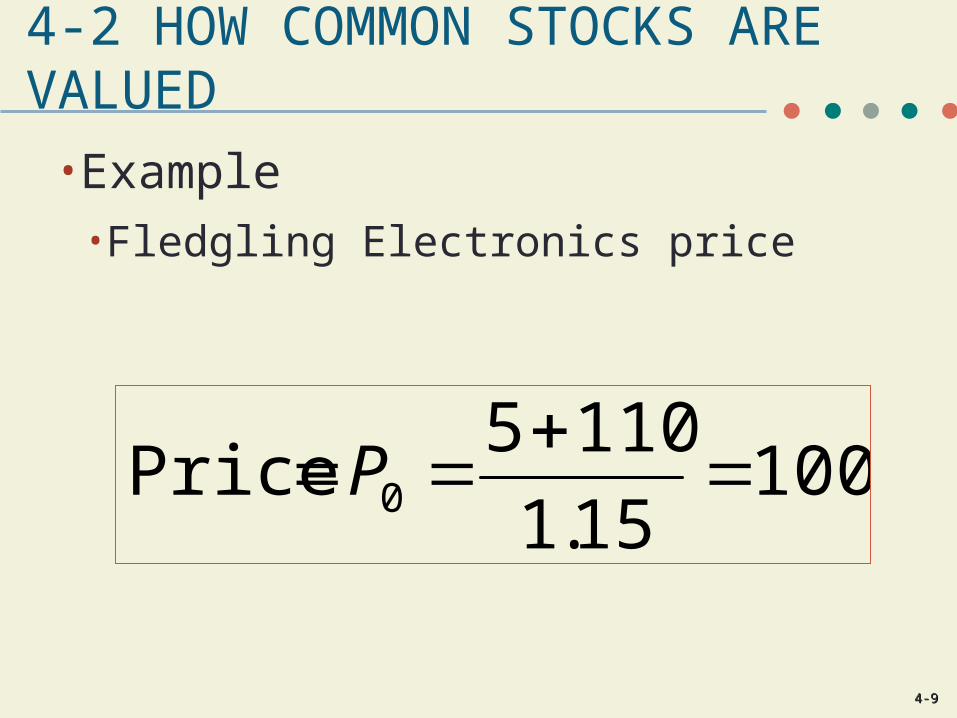

•Example• Fledgling Electronics price

10015.1

1105Price 0

P

4-4-1010

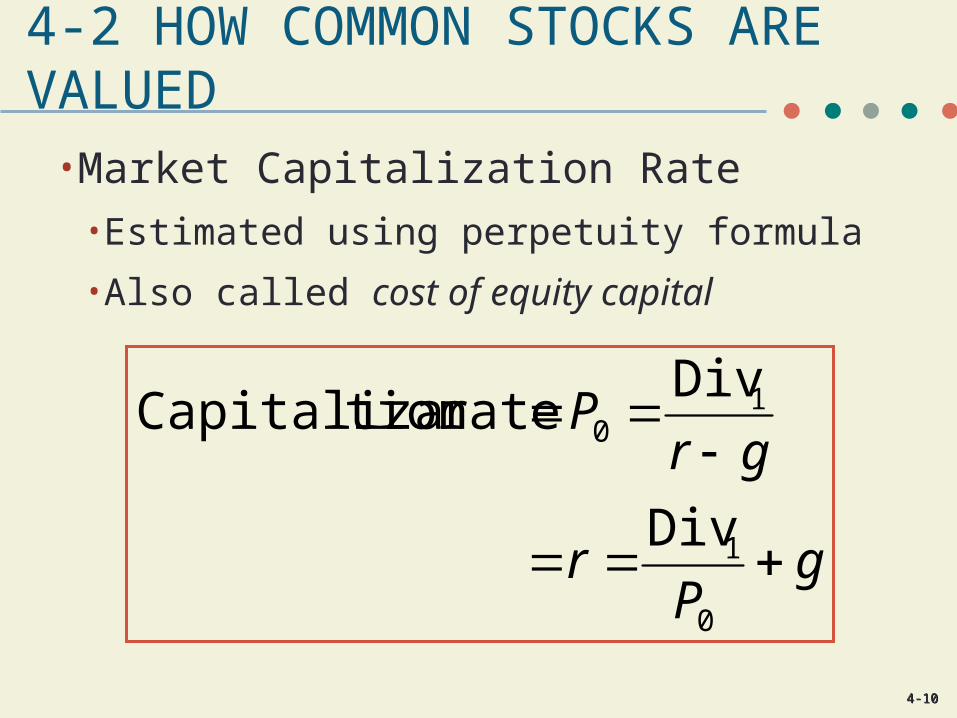

4-2 HOW COMMON STOCKS ARE VALUED

• Market Capitalization Rate• Estimated using perpetuity formula

• Also called cost of equity capital

gP

r

grP

0

1

10

Div

Divratetion Capitaliza

4-4-1111

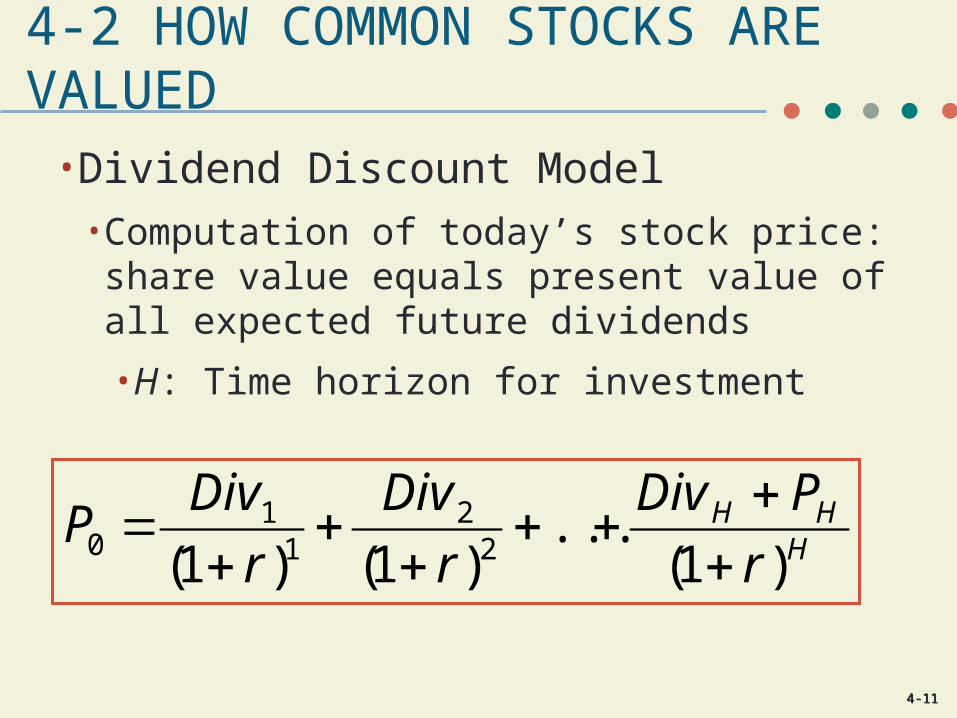

4-2 HOW COMMON STOCKS ARE VALUED

• Dividend Discount Model• Computation of today’s stock price: share value equals present value of all expected future dividends

• H: Time horizon for investment

HHH

r

PDiv

r

Div

r

DivP

)1(...

)1()1( 22

11

0

4-4-1212

4-2 HOW COMMON STOCKS ARE VALUED

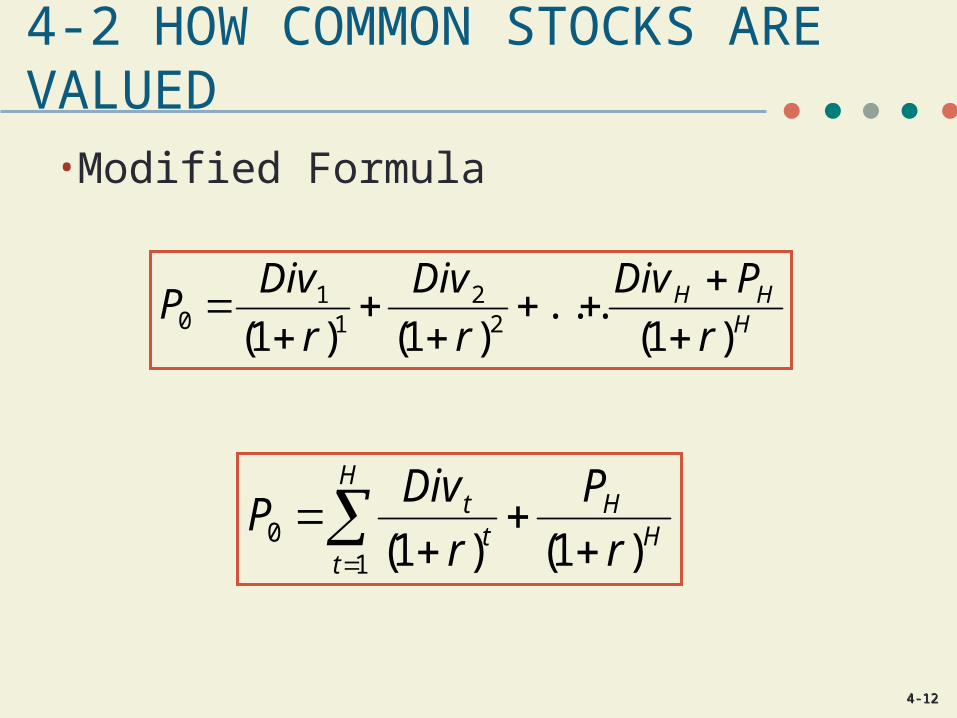

• Modified Formula

HHH

r

PDiv

r

Div

r

DivP

)1(...

)1()1( 22

11

0

HH

H

ttt

r

P

r

DivP

)1()1(10

4-4-1313

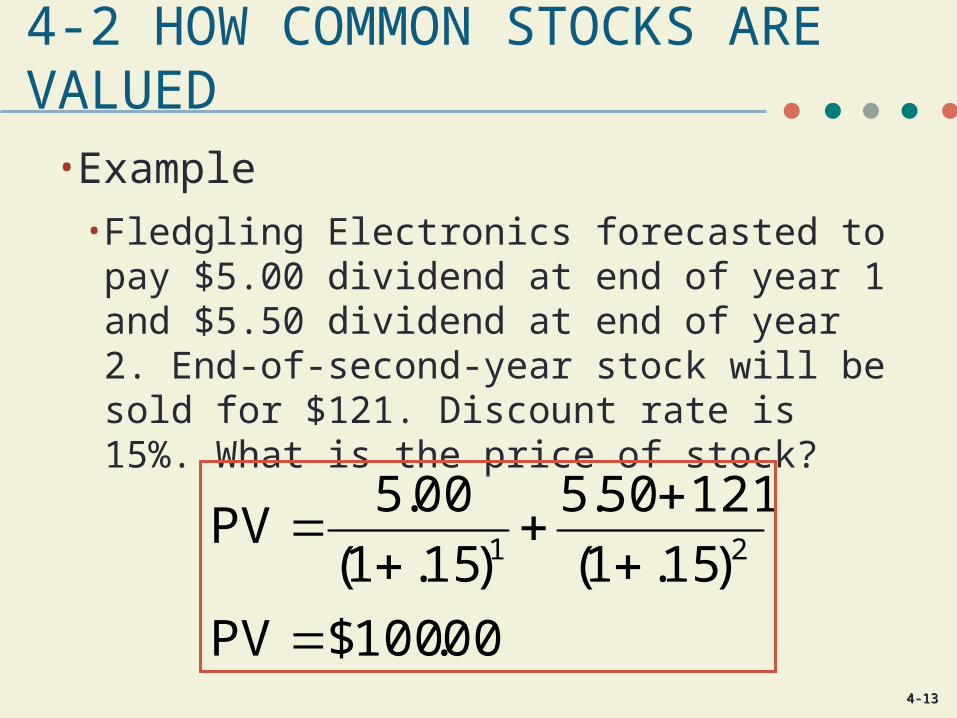

4-2 HOW COMMON STOCKS ARE VALUED

• Example• Fledgling Electronics forecasted to pay $5.00 dividend at end of year 1 and $5.50 dividend at end of year 2. End-of-second-year stock will be sold for $121. Discount rate is 15%. What is the price of stock?

00.100$PV

)15.1(

12150.5

)15.1(

00.5PV

21

4-4-1414

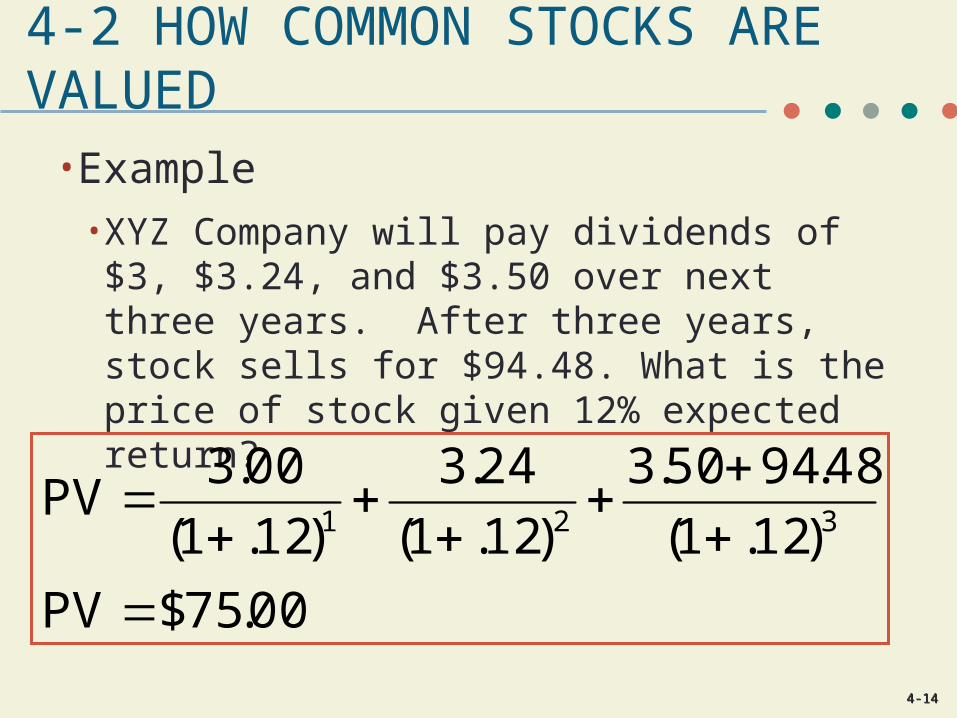

4-2 HOW COMMON STOCKS ARE VALUED

• Example• XYZ Company will pay dividends of $3, $3.24, and $3.50 over next three years. After three years, stock sells for $94.48. What is the price of stock given 12% expected return?

00.75$PV

)12.1(

48.9450.3

)12.1(

24.3

)12.1(

00.3PV

321

4-4-1515

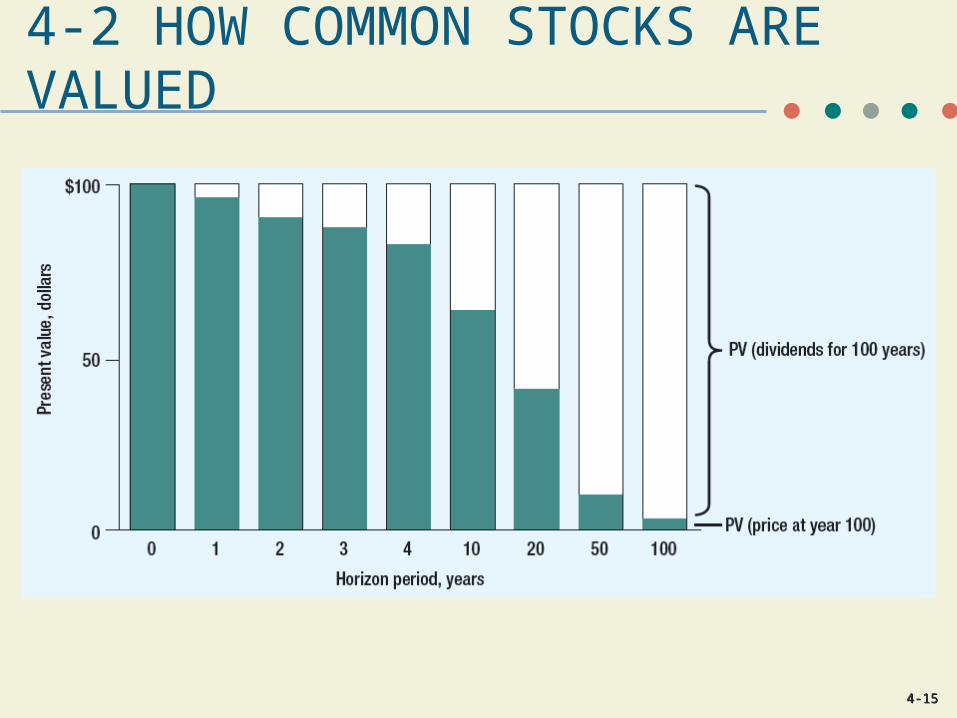

4-2 HOW COMMON STOCKS ARE VALUED

4-4-1616

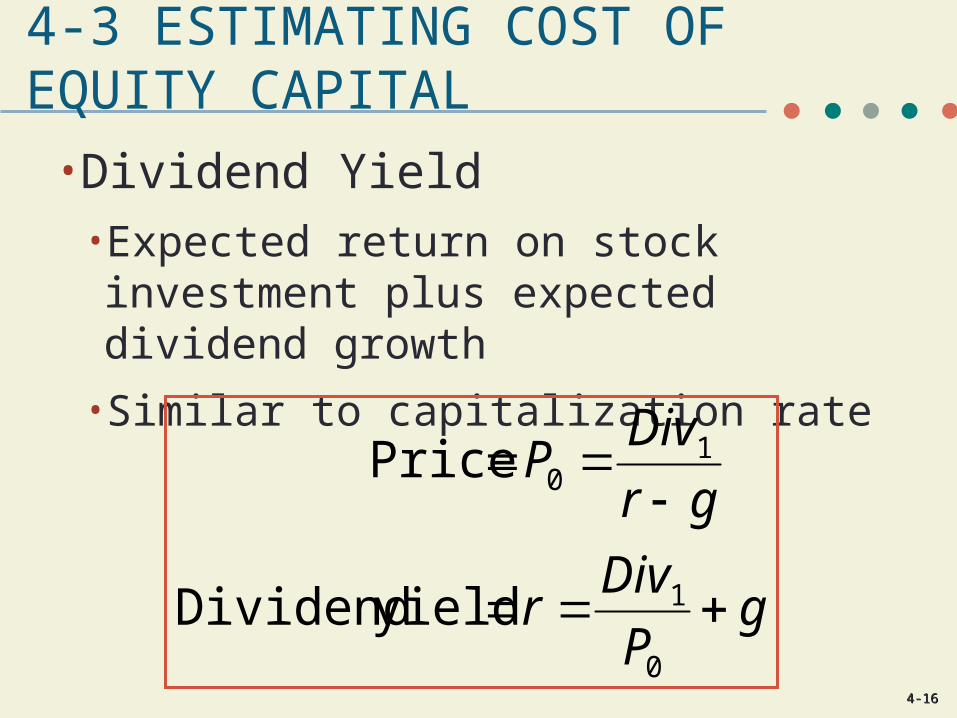

4-3 ESTIMATING COST OF EQUITY CAPITAL

•Dividend Yield• Expected return on stock investment plus expected dividend growth

• Similar to capitalization rate

gP

Divr

gr

DivP

0

1

10

yield Dividend

Price

4-4-1717

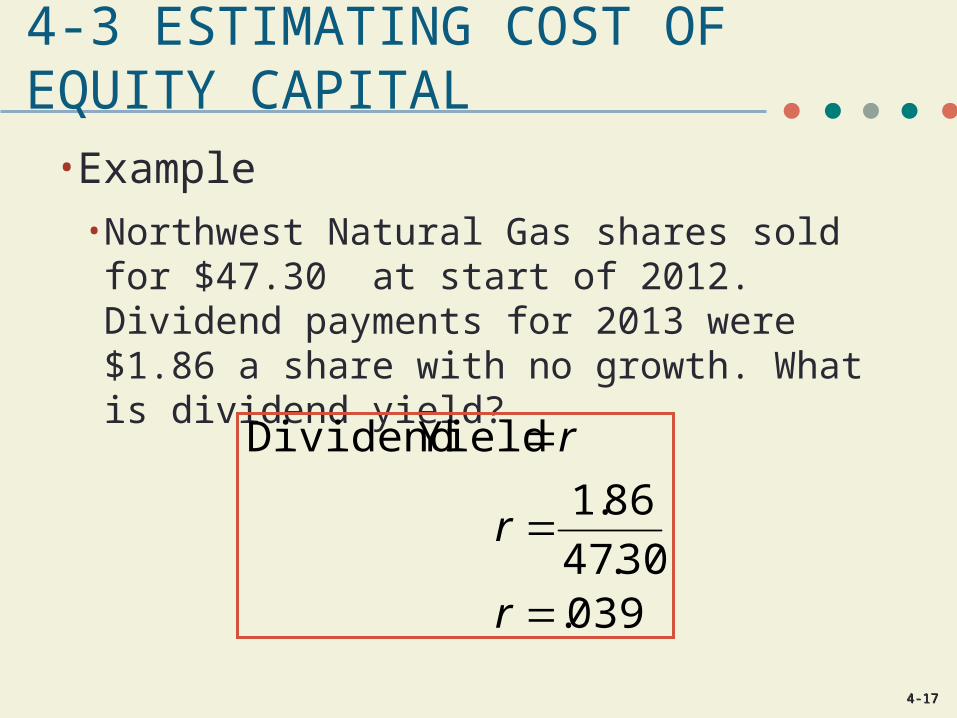

4-3 ESTIMATING COST OF EQUITY CAPITAL

• Example• Northwest Natural Gas shares sold for $47.30 at start of 2012. Dividend payments for 2013 were $1.86 a share with no growth. What is dividend yield?

039.30.47

86.1

Yield Dividend

r

r

r

4-4-1818

4-3 ESTIMATING COST OF EQUITY CAPITAL

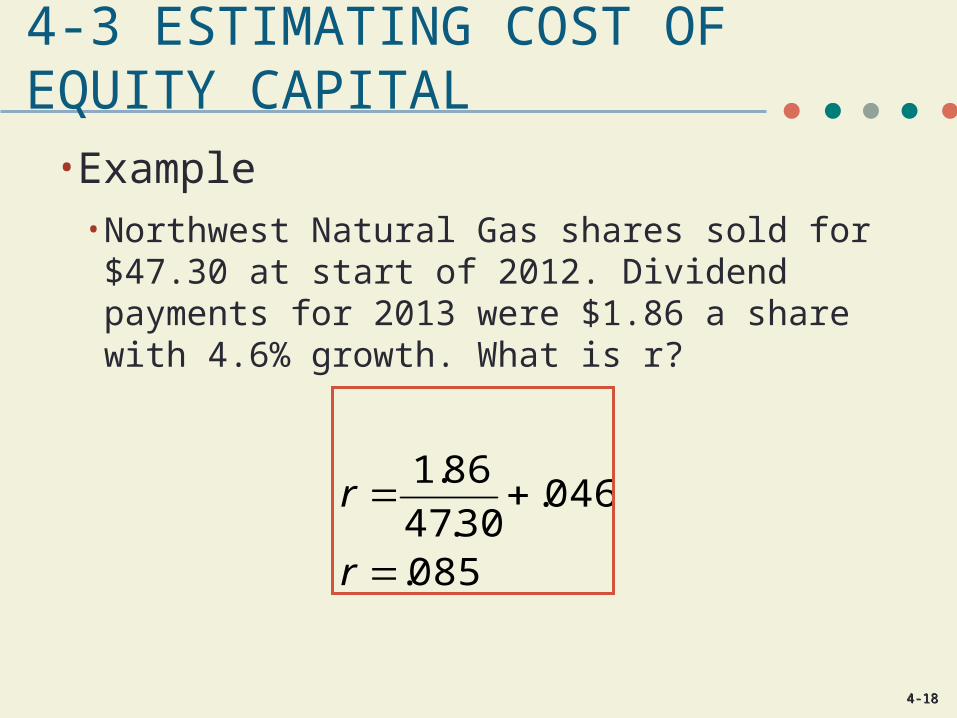

• Example• Northwest Natural Gas shares sold for $47.30 at start of 2012. Dividend payments for 2013 were $1.86 a share with 4.6% growth. What is r?

085.

046.30.47

86.1

r

r

4-4-1919

4-3 ESTIMATING COST OF EQUITY CAPITAL

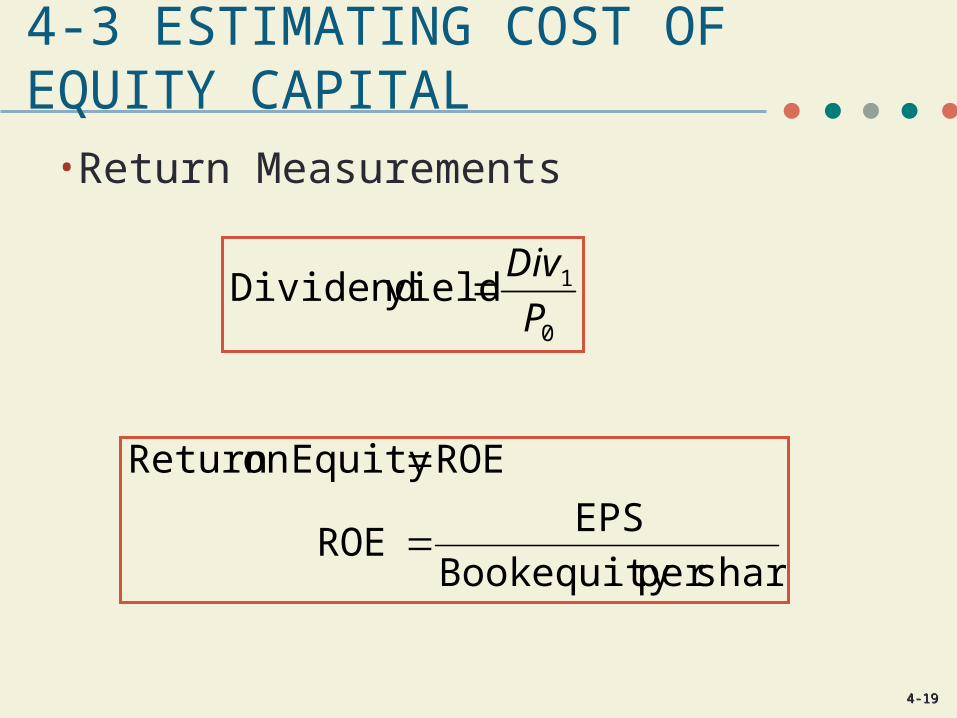

• Return Measurements

0

1yield DividendP

Div

shareper equity Book

EPSROE

ROEEquityon Return

4-4-2020

4-3 ESTIMATING COST OF EQUITY CAPITAL

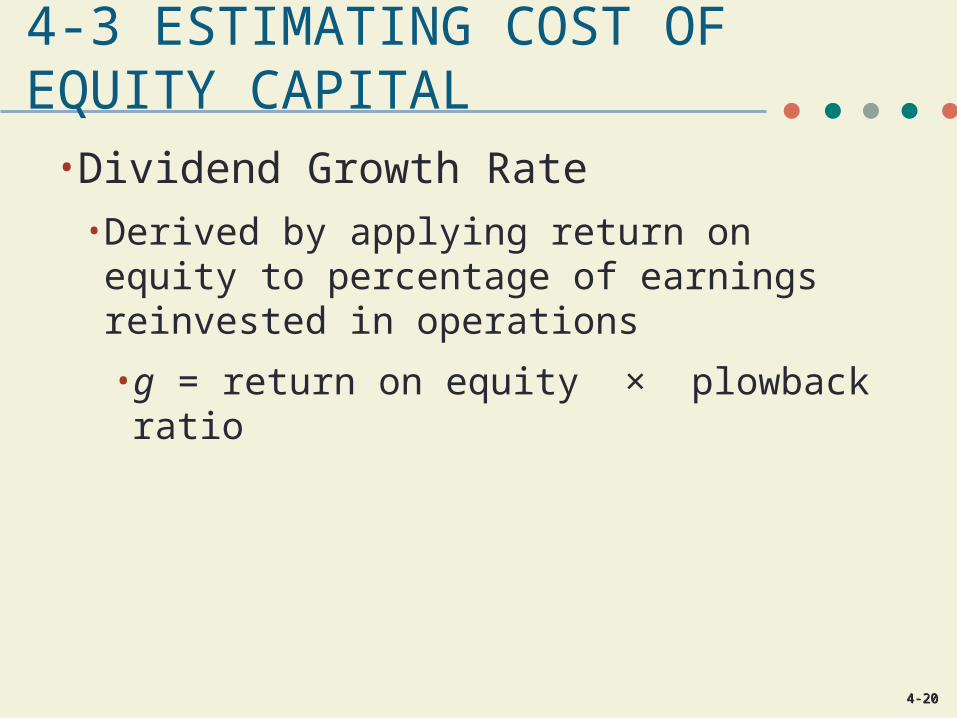

• Dividend Growth Rate• Derived by applying return on equity to percentage of earnings reinvested in operations

• g = return on equity × plowback ratio

4-4-2121

4-3 ESTIMATING COST OF EQUITY CAPITAL

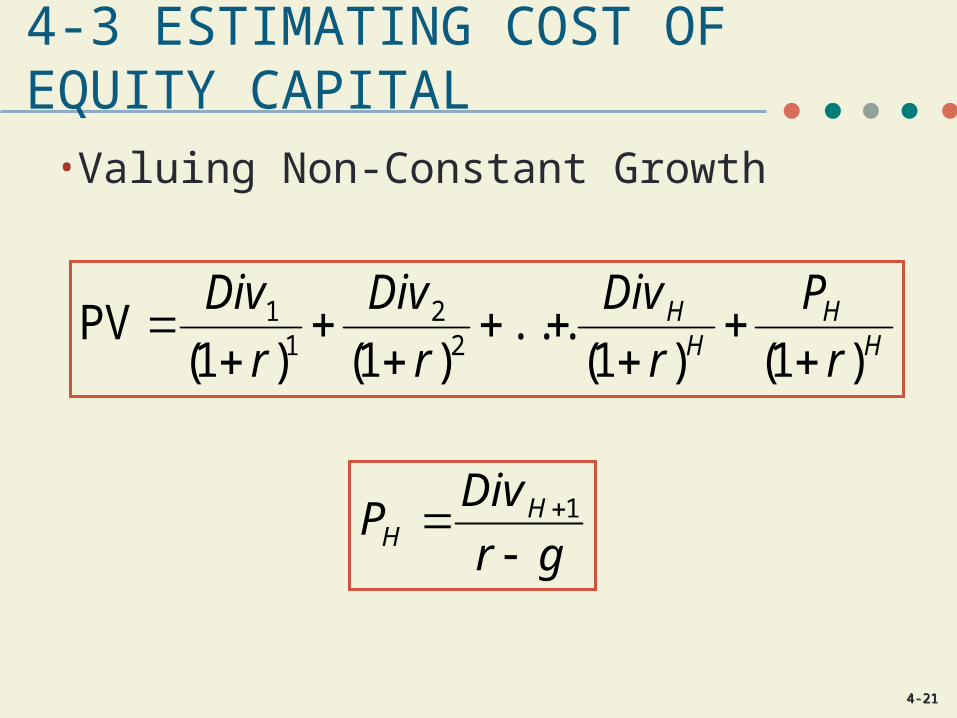

• Valuing Non-Constant Growth

HH

HH

r

P

r

Div

r

Div

r

Div

)1()1(...

)1()1(PV

22

11

gr

DivP HH

1

4-4-2222

4-3 ESTIMATING COST OF EQUITY CAPITAL

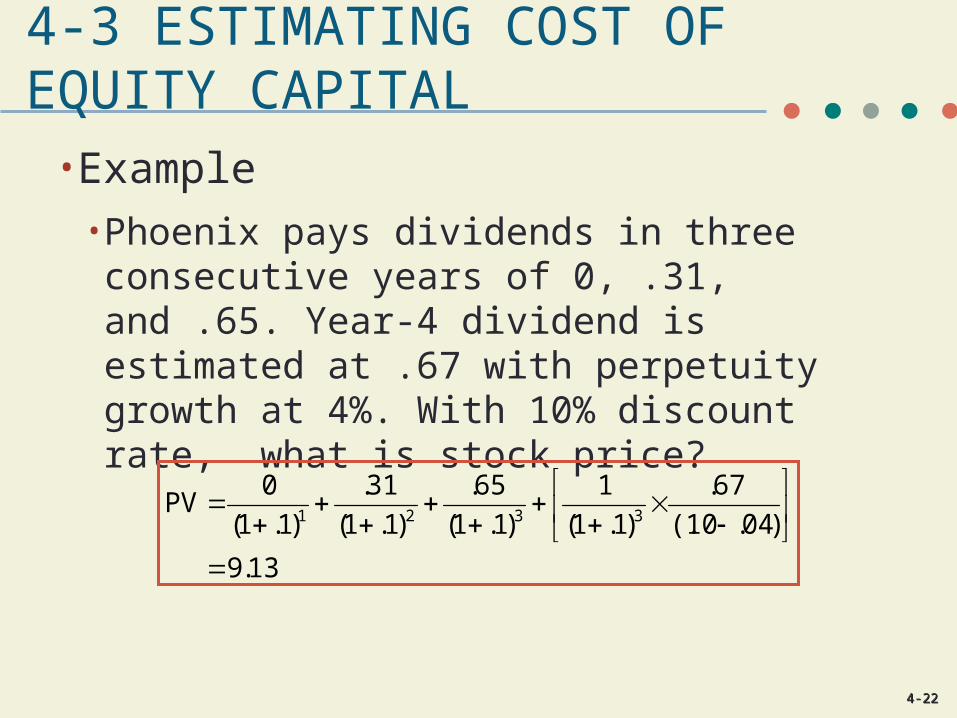

• Example• Phoenix pays dividends in three consecutive years of 0, .31, and .65. Year-4 dividend is estimated at .67 with perpetuity growth at 4%. With 10% discount rate, what is stock price?

13.9

)04.10(.

67.

)1.1(

1

)1.1(

65.

)1.1(

31.

)1.1(

0PV

3321

4-4-2323

4-4 STOCK PRICE AND EARNINGS PER SHARE

• If firm pays lower dividend and reinvests funds, stock price may increase due to higher future dividends

• Payout Ratio• Fraction of earnings paid out as dividends

• Plowback Ratio • Fraction of earnings retained by firm

4-4-2424

4-4 STOCK PRICE AND EARNINGS PER SHARE

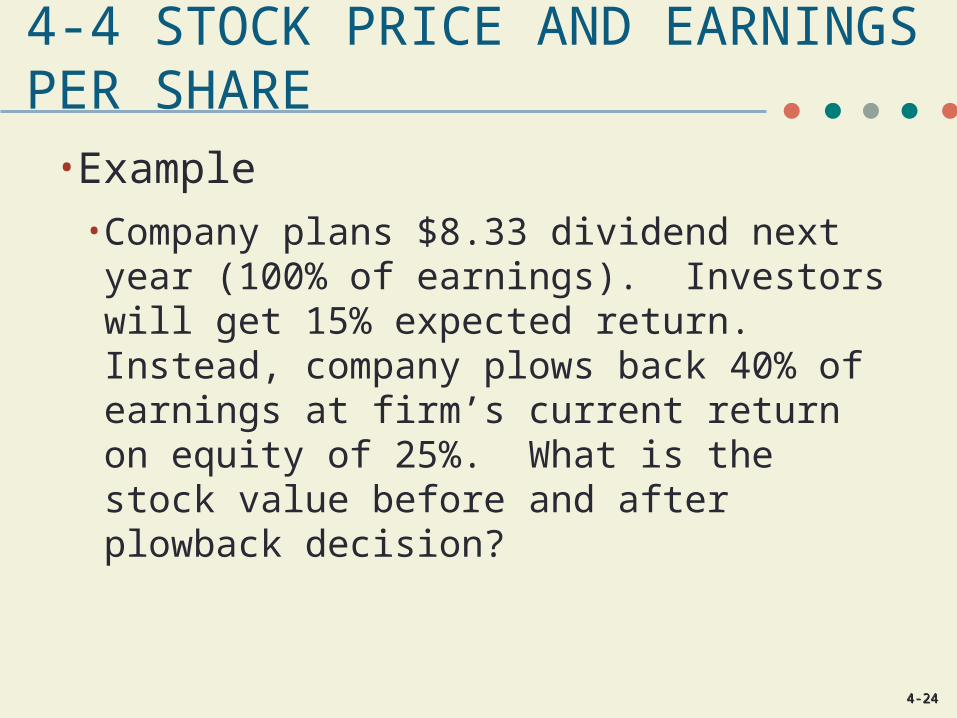

• Example• Company plans $8.33 dividend next year (100% of earnings). Investors will get 15% expected return. Instead, company plows back 40% of earnings at firm’s current return on equity of 25%. What is the stock value before and after plowback decision?

4-4-2525

4-4 STOCK PRICE AND EARNINGS PER SHARE

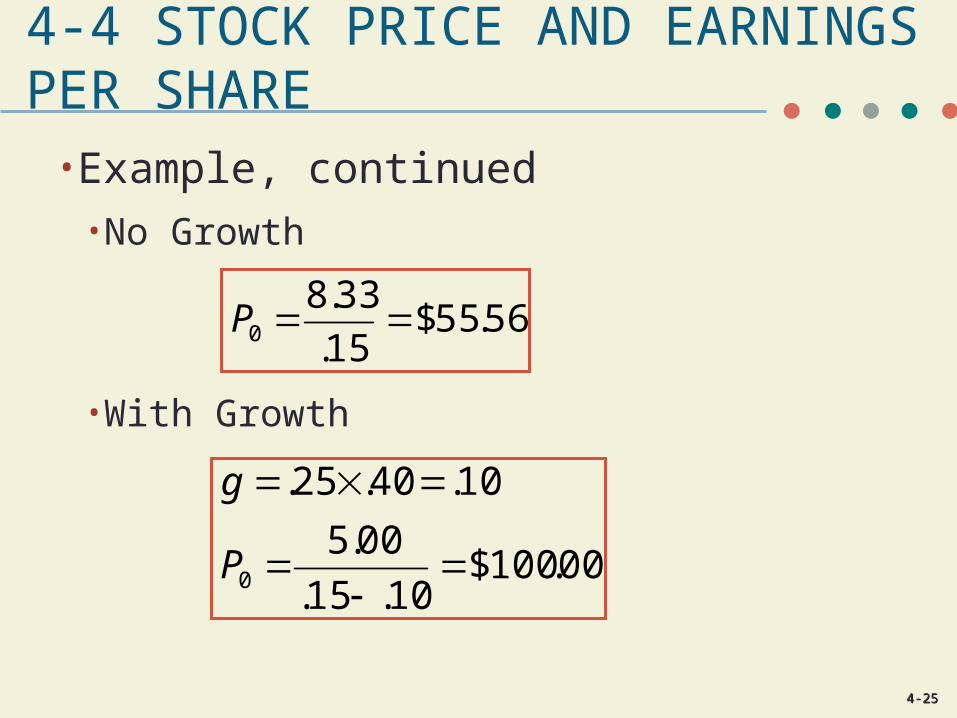

• Example, continued• No Growth

• With Growth

56.55$15.

33.80 P

00.100$10.15.

00.5

10.40.25.

0

P

g

4-4-2626

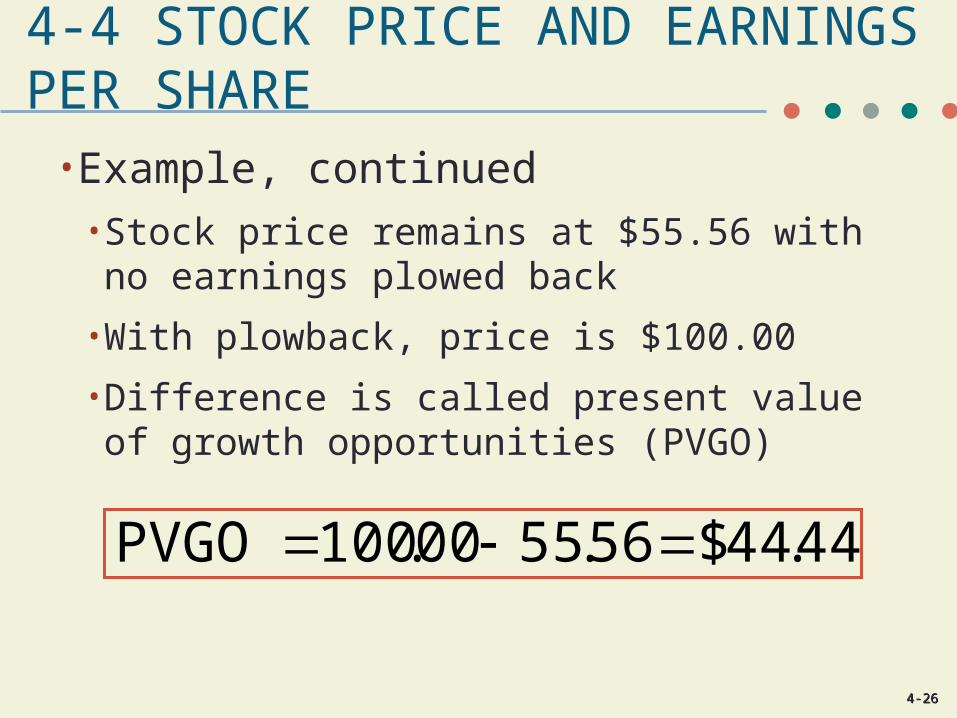

4-4 STOCK PRICE AND EARNINGS PER SHARE

• Example, continued• Stock price remains at $55.56 with no earnings plowed back

• With plowback, price is $100.00

• Difference is called present value of growth opportunities (PVGO)

44.44$56.5500.100PVGO

4-4-2727

4-4 STOCK PRICE AND EARNINGS PER SHARE

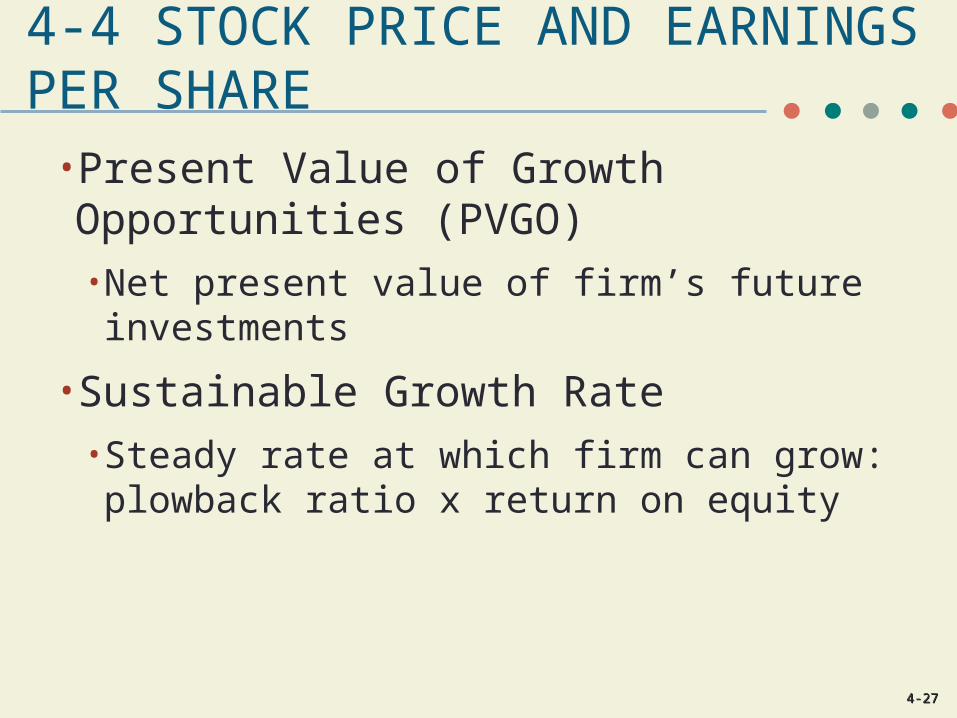

• Present Value of Growth Opportunities (PVGO)• Net present value of firm’s future investments

• Sustainable Growth Rate• Steady rate at which firm can grow: plowback ratio x return on equity

4-4-2828

4-5 VALUING A BUSINESS

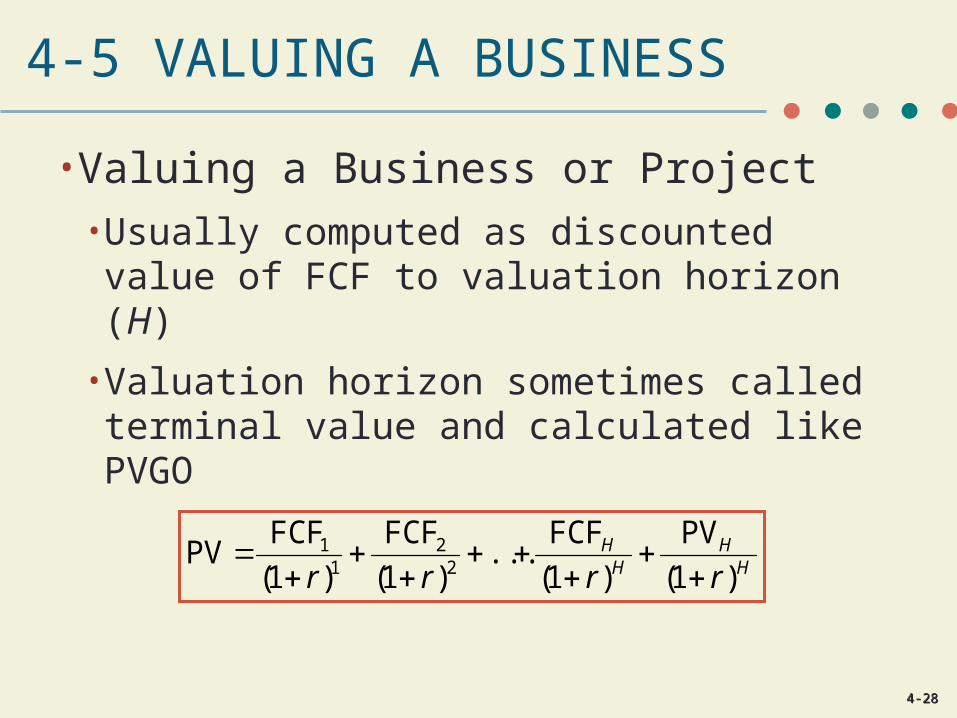

• Valuing a Business or Project• Usually computed as discounted value of FCF to valuation horizon (H)

• Valuation horizon sometimes called terminal value and calculated like PVGO

HH

HH

rrrr )1(

PV

)1(

FCF...

)1(

FCF

)1(

FCFPV

22

11

4-4-2929

4-5 VALUING A BUSINESS

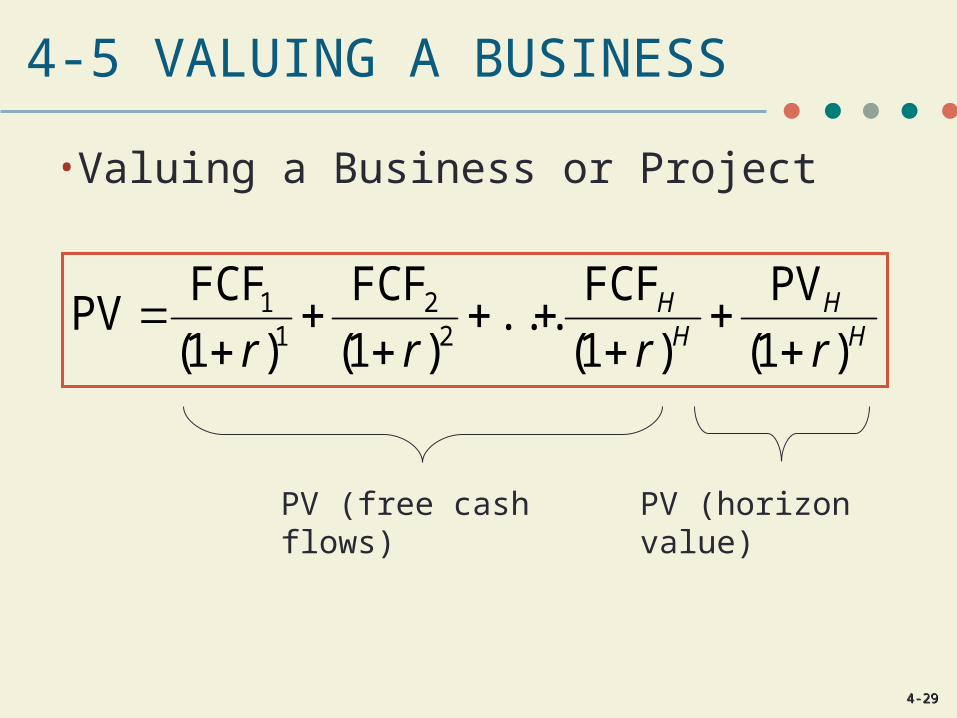

• Valuing a Business or Project

HH

HH

rrrr )1(

PV

)1(

FCF...

)1(

FCF

)1(

FCFPV

22

11

PV (free cash flows) PV (horizon value)

4-4-3030

4-5 VALUING A BUSINESS

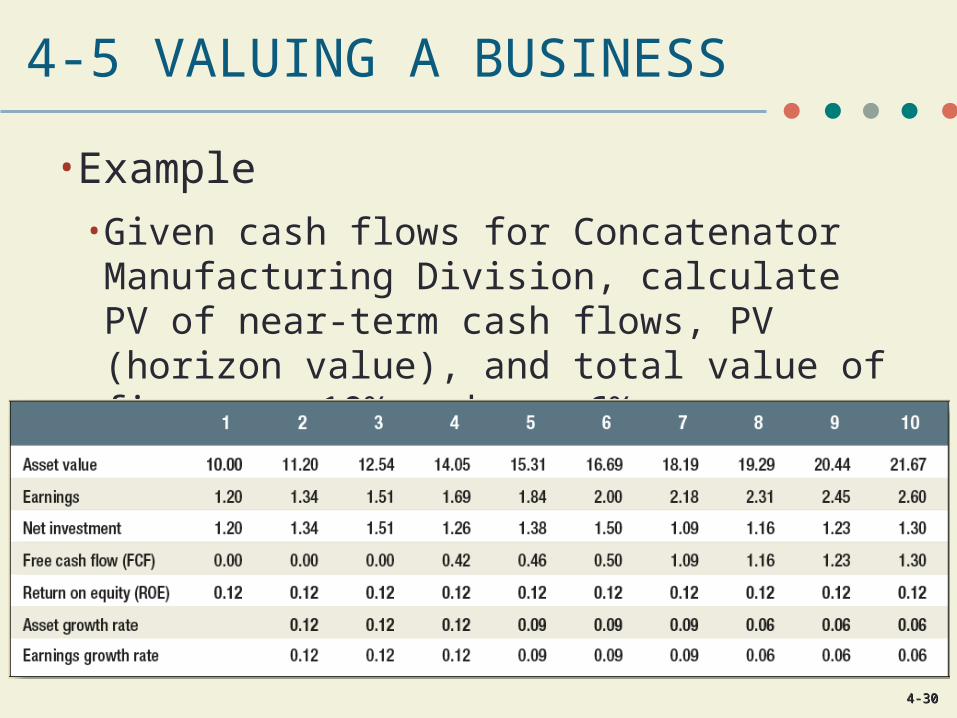

• Example• Given cash flows for Concatenator Manufacturing Division, calculate PV of near-term cash flows, PV (horizon value), and total value of firm; r = 10% and g = 6%

4-4-3131

4-5 VALUING A BUSINESS

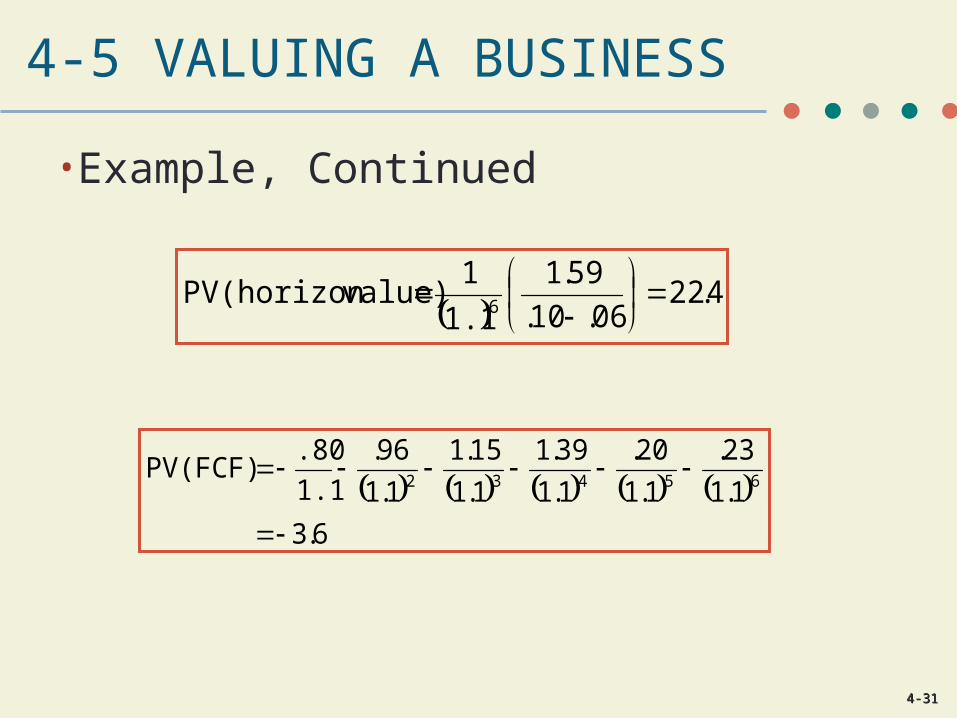

• Example, Continued

4.22

06.10.

59.1

1.1

1 value)PV(horizon 6

6.3

1.1

23.

1.1

20.

1.1

39.1

1.1

15.1

1.1

96.

1.1

.80PV(FCF) 65432

4-4-3232

4-5 VALUING A BUSINESS

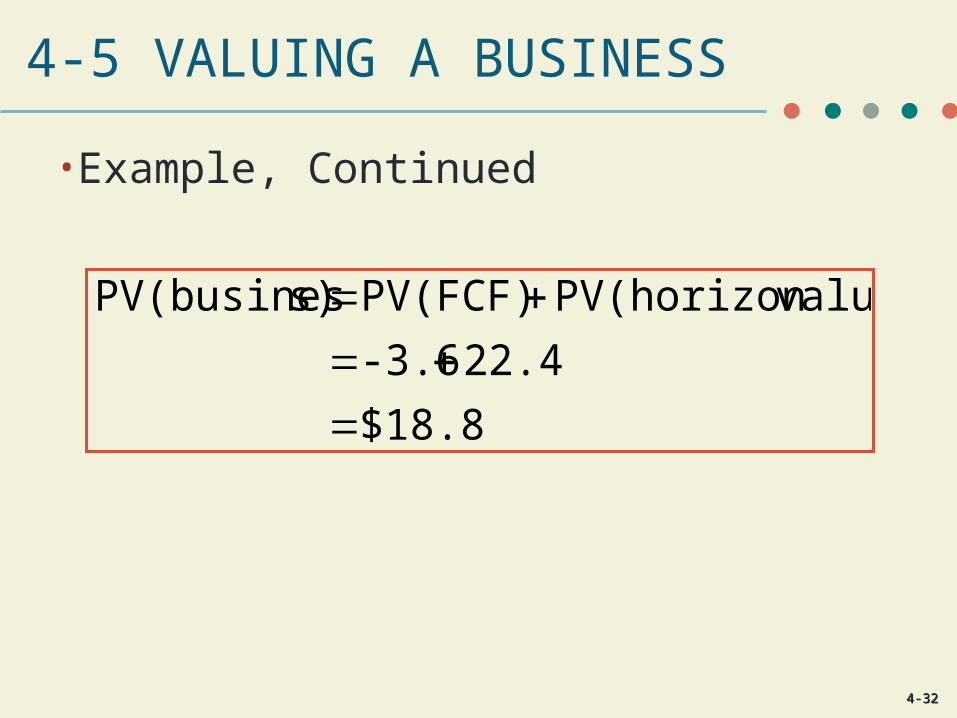

• Example, Continued

$18.8

22.4-3.6

value)PV(horizonPV(FCF)s)PV(busines