Embed Size (px)

Citation preview

CHAPTER 9 – LIABILITIES PROBLEM SOLUTIONS

Assessing Your Recall

9.1 The three essential characteristics of a liability are:a) The liability represents a duty or responsibility to transfer assets or services at a future date.b) The entity that is obligated has little or no discretion to avoid the future transfer.c) The transaction or event that gives rise to the obligation has already occurred.

9.2 A mutually unexecuted contract is a contract between two parties in which neither party has performed its part of the agreement. A purchase commitment would be an example of such a contract. The goods have not been delivered and no cash has been paid to the seller. Under GAAP mutually unexecuted contracts are not recorded in the financial statements. Under some circumstances a loss on a mutually unexecuted contract must be recognized prior to performance but gains are never recognized before performance.

9.3 Under GAAP, liabilities are valued at the net present value of the obligation. In the case of current liabilities the difference between the gross amount and the net present value is so small that the gross amount is used. This makes the accounting entries easier and does not produce materially different amounts.

9.4 Warranty expense is an estimate of cost to be incurred in the future related to current period sales. The actual costs are incurred when the product sold in the current period requires repairs at a later date, and the company is obligated to perform these repairs at no charge. Because the revenues from product sales are recognized in the current period, the estimated warranty costs must be estimated and matched to these revenues in order to determine profit.

9.5 Unearned revenues are those revenues that have not yet met the

criteria for revenue recognition. Payments received by a magazine publisher for future copies of the magazine would be an example. The unearned revenues are recognized as liabilities on the books of the seller until the revenue recognition criteria are met, at which time the liability is reduced and revenue is recognized.

9.6 Employers often object when the government changes CPP/QPP or EI rates because such changes increase current labour costs, and make it more expensive for companies to hire additional employees. It is more expensive because the employer is required to make a separate

1

contribution to CPP/QPP and EI on behalf of each employee, in addition to the amount that is deducted from each pay cheque.

9.7 The current portion of long-term debt is that portion of long-term debt

that is within one year of being due. It is recorded with the current liabilities because this portion of long-term debt must be paid off in the upcoming year. In order to present users of financial statements with a fair picture of all cash outflows that are expected to occur within one year of the balance sheet date, the current portion of long-term debt must be classified within current liabilities.

9.8 Commitments are not recognized in the financial statements under GAAP since they represent mutually unexecuted contracts. To the extent that one party has performed part of the contract, such as when a deposit is made, that portion of the contract is accounted for. The other circumstance under which a commitment should be recognized is if there is a probable loss on the commitment. This type of loss should be recognized in the financial statements.

9.9 Loss contingencies may be recognized in the financial statements if two criteria are met. They are:a) Information available prior to the issuance of the financial statements indicates that it is likely that an asset has been impaired or that a liability has been incurred.b) The amount of the loss can be reasonably estimated.

9.10 In the liability method, deferred taxes are calculated through estimating the liability to pay taxes in the future based on the temporary differences that exist in the current period. For example, although warranty expense hits the income statement in the current period, the related tax savings occur in future periods as the actual warranty costs are incurred. Thus, a future tax asset is established in order to reflect the anticipated future tax benefit that arises from a temporary difference existing in the current period.

9.11 In the liability method deferred taxes represents an estimate of the

actual liability to pay taxes in the future that arises because of current period temporary differences. In the deferral method, deferred taxes is the difference between the tax expense that is reported to shareholders (based on the recognized revenues and expenses and the current tax rate) and actual tax payable to Revenue Canada. Thus, the liability method focuses on the balance sheet because it estimates the actual future tax asset or liability, while the deferral method focuses on the income statement because it estimates the tax expense that is reported to shareholders. Another important difference between the liability and deferral methods is the effect of

2

changes in tax rates. Under the liability method, the existing future tax asset or liability must be recalculated to reflect the change in rates, while no such changes are made under the deferral method. A final difference is that under the liability method, the future tax assets and liabilities must be reviewed to ensure that the future tax impact is accurate.

9.12 Temporary differences: This term refers to differences in the carrying values of assets / liabilities as recorded in the accounting records versus those recorded in the tax records. Permanent differences: This term refers to the difference that arises when a revenue or expense is recognized for book or tax purposes but not the other. This results in a permanent difference in the recognized revenues and expenses between the tax books and the accounting reporting books. Under GAAP no future income taxes are recognized for these types of differences.Originating / Reversing Differences: Originating and reversing differences arise in the context of timing differences. Because the issue is one of timing, a difference between book and tax originates in one period but is reversed in a subsequent period. For example, in the amortization of an asset the amortization expense for tax purposes is typically higher than the amortization for book purposes in the first few years of the asset’s life. This would result in an originating difference. In the last half of the asset’s life the amortization for book purposes will be higher than for tax purposes resulting in a reversing difference.

Applying Your Knowledge

9.13 a) The liability represents a duty or responsibility to transfer assets or services at a future date.An argument that could be suggested in support of this is: future tax liabilities represent an estimate of the future tax

obligation that arises from current period temporary differences. An argument that could be suggested against this is: changes in tax rules or rates are difficult to anticipate, so the future tax liability might not be an accurate measure of the assets that must be transferred in the future.b) The entity that is obligated has little or no discretion to avoid the

futuretransfer.An argument that could be suggested in support of this is: the items that cause temporary differences will reverse themselves in the future and the tax will become payable.An argument that could be suggested against this is:

3

the company may use tax minimization opportunities such as continuing to buy plant and equipment that is subject to CCA.c) The transaction or event that gives rise to the obligation has already occurred.An argument that could be suggested in support of this is: the obligation to pay taxes in the future occurs because of a temporary difference that arose in the current period.An argument that could be suggested against this is: because the income or expense that has caused the deferred taxes in the future may indeed not be realized in the future, the argument can be made that the transaction or event that will cause the future payment of tax has not occurred yet.

4

9.14 a)1. A-Inventory 65,300

L-Accounts payable 65,300L-Accounts payable 74,600

A-Cash 74,6002. L-Unearned revenue 1,900

SE-Sales revenue 1,900A-Cash 6,500

L-Unearned revenue 6,5003. L-Bank indebtedness 5,000

A-Cash 5,000SE-Interest expense 46

A-Cash 46($12,300 - $5,000) x .075/12 = 46

4. L-Wages payable 3,500A-Cash 3,500

SE-Wage expense 18,000L-Wages payable 12,438L-Person income tax payable 4,500L-CPP payable 576L-EI payable 486

SE-Wages expense 1,256L-CPP payable 576L-EI payable 680

5. L-Personal income tax payable 2,100L-CPP payable 1,100L-EI payable 1,230

A-Cash 4,4306. SE-Interest expense 67

L-Interest payable 67$10,000 x .08 / 12 = $67

7. A-Cash 4,000L-Bank indebtedness 4,000

5

b)Current liabilities

Bank indebtedness $11,300Accounts payable 36,400Interest payable 67Unearned revenue 6,500Wages payable 12,438Personal income tax payable 4,500CPP payable 1,152EI payable 1,166Short-term note payable 10,000

$83,523

6

9.15 a) 1. A-Computer system 26,500

L-Accounts payable 23,000 A-Cash 3,500

2. A-Inventory 96,000 L-Accounts payable 96,000

L-Accounts payable 89,000 A-Cash 89,000

3. A-Cash 35,000 L-Short-term loan 35,000

SE-Interest expense 117 L-Interest payable($35,000 x .08 x .5/12)

117

4. L-Rent payable 24,000SE-Rent expense 12,000 A-Cash 36,000

5. L-Unearned revenue 2,250 SE-Revenue 2,250

6. SE-Warranty expense 18,000 L-Obligations under warranties 18,000

L-Obligations under warranties 1,100 A-Cash 1,100

7. SE-Wages expense 4,200 L-Wages payable 4,200

8. SE-Interest expense 1,900 A-Cash 1,900

9. L-Bank loan 4,000 L-Current portion of LT debt 4,000

b) Current Liabilities:Accounts payable $112,300Wages payable 4,200Interest payable 117Obligations under warranties 49,900Short-term loan 35,000

7

Current portion of long-term debt 4,000$205,517

c) $4,000 of the 5 year bank loan represents the current-portion oflong-term debt because it requires the use of current assets and must be paid during the upcoming year. The remaining $16,000 does not require the use of current assets, and is thus classified as part of long-term liabilities.

9.16 a)

1. A-Inventory 556,400 L-Accounts payable 556,400

L-Accounts payable 521,500 A-Cash 521,500

2. SE-Warranty expense 43,764 L-Estimated warranty obligation 43,764

L-Estimated warranty obligation 39,040 A-Cash 39,040

3. L-Wages expense 142,000 L-Income tax payable 38,340 L-CPP payable 4,544 L-EI payable 3,834 A-Cash 95,282

SE-Wages expense 9,912 L-CPP payable 4,544 L-EI payable 5,368

b) Current liabilities:

Accounts payable $34,900Income tax payable 38,340CPP payable 9,088EI payable 9,202Estimated warranty obligation 4,724

$96,254

8

9.17 a) Journal entries

Aug. A-Cash 18,000 L-Unearned advertising revenue 18,000

Sept. A-Cash 90,000 L-Unearned subscription revenue 90,000

To Dec.

A-Cash SE-Magazine revenue

77,00077,000

SE-Printing expense 66,000 A-Cash 66,000

b) Adjusting journal entriesL-Unearned advertising revenue 9,000 SE-Advertising revenue 9,000

L-Unearned subscription revenue 45,000 SE-Subscription revenue 45,000

c)University Survival Magazine

Income StatementFor the Year ended December 31, 20xx

Revenue:Subscription revenue $ 45,000Magazine revenue 77,000Advertising revenue 9,000

Total revenue $131,000

Printing expense 66,000

Net income $ 65,000

9

d) Cash balance = $18,000 + $90,000 + $77,000 - $66,000 = $119,000

To: University Survival Magazine OwnersFrom: You name, AccountantRe: Results of operations to December 31, 20xx

The results of operations to December 31, 20xx are a net income of $65,000. This is substantially less than the current bank balance of $119,000. The reason for this difference is that revenues are recorded only when they are earned. The cash from both the subscriptions and the advertising was put in the bank when it was received but the revenue recognized from these two items needs to be spread out over the eight months for which the company has an obligation to print the magazine. Therefore, the revenue from the subscriptions and advertising represents only half of the cash that was received.

9.18 a) Computers Galore should classify the one year warranty obligation as

current liabilities, because these obligations may require the use of current assets and expire within one year. Regarding the two year warranties, part of this obligation is current and part is long-term, depending upon when the computers tend to require repairs. Based on past experience, Computer Galore might be able to estimate the portion of the extended warranty obligation that requires current funds, and the portion of that will not be claimed within the upcoming year. If such an estimate cannot be made, the principle of conservatism indicates that the entire obligation should be classified as current.

b) Computers Galore should record a warranty expense with its computers because the failure to do so would result in an overstatement of revenues. Thus, the estimated cost of fulfilling the standard one- month warranty is the amount of warranty expense that Computer Galore should recognize. The cost of fulfilling the extended warranty obligations is not built into the sale price of the computer, so no warranty expense need be recognized. The additional warranty coverage has been paid for by the customers thus creating an obligation rather than an expense.

c) A-Cash 110,600

L-Estimated warranty obligation 110,600A-Cash 114,750

10

L-Estimated warranty obligation 114,750L-Estimated warranty obligation 64,200

A-Cash 64,200L-Estimated warranty obligation 79,100

A-Cash 79,100

d) If the actual warranty costs incurred by Computer Galore are less than the amount collected from customers for the warranty coverage, then once the warranties expire, the remaining warranty obligation is eliminated, and the difference is a current period revenue. If the actual warranty costs are greater than expected, than the difference is recognized as an additional warranty expense of the current period.

9.19 Cool Air Conditioning Company: Journal Entries

Period Transaction Debit CreditQ1 A-Cash

L-Contract fees rec’d in advance1125,000

125,000

SE-Contract expenses 80,000 A-Cash 80,000

L-Contract fees received in advance 125,000 SE-Contract revenue 2 125,000

Q2 A-Cash 200,000 L-Contract fees rec’d in advance3 200,000

SE-Contract expenses 66,000 A-Cash 66,000

L-Contract fees received in advance 150,000 SE-Contract revenue4 150,000

Q3 A-Cash 225,000 L-Contract fees rec’d in advance5 225,000

SE-Contract expenses 98,000 A-Cash 98,000

L-Contract fees received in advance 175,000 SE-Contract revenue6 175,000

11

Q4 A-Cash 100,000 L-Contract fees rec’d in advance7 100,000

SE-Contract expenses 115,000 A-Cash 115,000

L-Contract fees received in advance 175,000 SE-Contract revenue8 175,000

Notes:1 $125,000 = 250 x $5002 750 Contract outstanding on Jan. 1

+250 New contracts in Q1 1,000 Total contracts in Q1 x $125/quarter = $125,000

3 $200,000 = 400 x $5004 1,000 Total contracts from Q1 - 200 Contracts that expire at end of Q1 800 Existing contracts that continue into Q2 + 400 New contracts in Q2 1,200 Total contracts in Q2 x $125/quarter = $150,0005 $225,000 = 450 x $5006 1,200 Total contracts from Q2

- 250 Contracts that expire at end of Q2 950 Existing contracts that continue into Q3 + 450 New contracts in Q3 1,400 Total contracts in Q3 x $125 / quarter = $175,000

7 $100,000 = 200 x $5008 1,400 Total contracts from Q3

- 200 Contracts that expire at end of Q3 1,200 Existing contracts that continue into Q4 + 200 New contracts in Q4 1,400 Total contracts in Q4 x $125 / quarter = $175,000

b) At the end of the year, 1,050 contracts were outstanding, at a value of $237,500.

Quarter in which contract initiated

Quarters left in contract

Number of contracts

Value

2 1 400 $ 50,000

3 2 450 $112,5004 3 200 $

12

75,000Totals 1,050 $237,500

13

c) Partial Balance SheetCurrent Liabilities:

Contract fees received in advance $237,500Partial Income StatementContract revenue $625,000Contract expense 359,000

$266,000

9.20 The first date at which the furniture company should mention anything about the situation with Mia Thorn is at the date the suit is filed (June 10, 20x2). At this date the liability would be considered a contingent liability and the company would have to evaluate whether it is likely that the suit will be lost and would have to estimate the potential losses. It is unlikely that the company will judge it to be likely that it will lose the suit so it would seem that only a footnote disclosure would be required at this point. In fact, if the company judges the chances of losing as remote even footnote disclosure would not be required, although most companies would report a suit such as this if the consequences are material. On December 13, 20x2, even though the jury ruled against the company there is still some doubt as to whether it will have to pay the claim because the company still has the opportunity to appeal the decision. At this date, footnote disclosure would be required and recognition of the loss could be recognized if legal counsel thought that the appeal would not be successful. By the end of 20x3 it is clear that the company has lost and at this point a liability and associated loss would be recognized in the financial statements if it had not been recognized earlier. Even if it had been recognized earlier there would need to be an incremental entry for the additional amount awarded.

14

9.21 a) Liability methodStraight-line:Annual book amortization = $38,000 / 8 = $4,750 per yearYear 20x1:

Book TaxIncome before amortization and tax

$80,000 $80,000

Amortization / CCA 4,750 3,800 1 Income before taxes 75,250 76,200Taxes @ 25% 19,050Tax expense: CurrentFuture

19,050 (238) 2

Tax expense 18,812 Net Income $56,438

1 $3,800 = $38,000 x 20% x ½2 $238 = [($38,000 - $4,750) – ($38,000 - $3,800)] x 25%SE-Current tax expense 19,050

L-Tax payable 19,050A-Future income tax asset 238

SE-Future tax expense 238

15

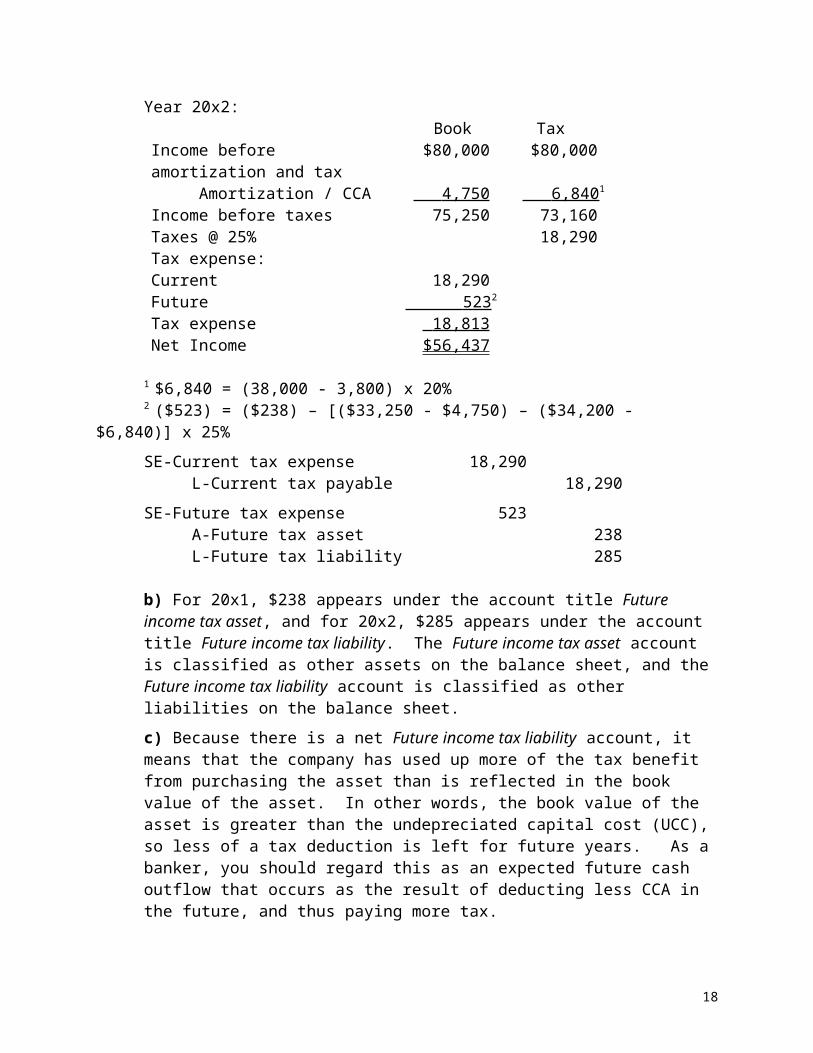

Year 20x2:Book Tax

Income before amortization and tax

$80,000 $80,000

Amortization / CCA 4,750 6,840 1

Income before taxes 75,250 73,160Taxes @ 25% 18,290Tax expense: CurrentFuture

18,290 523 2

Tax expense 18,813 Net Income $56,437

1 $6,840 = (38,000 - 3,800) x 20%2 ($523) = ($238) – [($33,250 - $4,750) – ($34,200 - $6,840)] x 25%SE-Current tax expense 18,290

L-Current tax payable 18,290SE-Future tax expense 523

A-Future tax asset 238L-Future tax liability 285

b) For 20x1, $238 appears under the account title Future income tax asset, and for 20x2, $285 appears under the account title Future income tax liability. The Future income tax asset account is classified as other assets on the balance sheet, and the Future income tax liability account is classified as other liabilities on the balance sheet. c) Because there is a net Future income tax liability account, it means that the company has used up more of the tax benefit from purchasing the asset than is reflected in the book value of the asset. In other words, the book value of the asset is greater than the undepreciated capital cost (UCC), so less of a tax deduction is left for future years. As a banker, you should regard this as an expected future cash outflow that occurs as the result of deducting less CCA in the future, and thus paying more tax.

16

9.22 a) Liability method

Straight-line:Annual book amortization = ($18,000 - $3,000) / 5

= $3,000 per year

Year 20x1:Book Tax

Income before amortization and tax

$75,000 $75,000

Amortization / CCA 3,000 2,700 1 Income before taxes 72,000 72,300Taxes @ 40% 28,920Tax expense: Current (Payable)Future

28,920 (120) 2

Tax expense 28,800 Net Income $43,200

1 $2,700 = $18,000 x 30% x ½2 $120 = [($18,000 - $3,000) – ($18,000 - $2,700)] x 40%SE-Income tax expense 28,800A-Future income tax asset 120

L-Income tax payable 28,920

b)UCC Book Value Temporary

differenceFuture tax liability (asset)

20x1 15,300 15,000 (300) (120)20x2 10,710 12,000 1,590 636Total 1,290 51620x3 7,497 9,000 213 85Total 1,503 601

17

c) The future tax liability (asset) account changed from 20x1 to 20x2 because of the half year rule for capital cost allowance. Thus, the tax book value (UCC) exceeded the accounting book value in 20x1, creating a future tax asset. In 20x2, because the half year rule is no longer in effect, UCC drops below the accounting book vaue resulting in a taxable temporary difference that eliminates the future tax asset and creates a future tax liability. In 20x3, accounting book value continues to exceed UCC, increasing the future tax liability.

9.23 a)Warranty liability = 4% x $2,590,000 = $103,600Warranty costs incurred = 25,000Deductible temporary difference = $ 78,600

Future tax asset = 32% x $78,600 = $ 25,152b) The future tax asset would likely be reported as Other Assets (long-term) on the balance sheet because the warranty covers a period of 5 years. c) If the tax rate in 20x5 changed to 40%, then the future tax asset at that date would need to be recalculated using the 40% tax rate. Since the tax rate used to be 32%, the future tax asset would increase as a result of the higher rate. In other words, a larger tax deduction would be available to the company when the actual warranty costs were incurred.

Management Perspective Problems

9.24 As a stock analyst, you should look at a future tax liability as a real future obligation of the company to pay taxes in excess of the tax rate applied to accounting income. In other words, because of temporary differences that originated in the past, taxable income is going to exceed accounting income in the future and the company is going to pay more income taxes to Revenue Canada. However, a future tax liability is different than a long-term bank loan because there is more uncertainty regarding both the amount and the timing of the obligation. For example, if a company continues to invest in fixed assets, then the undepreciated capital cost is going to be less than the accounting book value year after year, so that the future tax liability continues to increase.

9.25 In terms of financial statement disclosure, you might find a footnote

that explains the risks associated with the manufacture and transportation of chemicals, and outlines any contingent liabilities currently pending. In assessing the company’s liabilities, you would

18

be interested in the nature and extent of such contingent liabilities, and the details of litigation that the company faces.

9.26 a) The sweeteners create a legal obligation of the company even

though they may not be recorded at the time of signing of the agreement since they could be viewed as mutually unexecuted contracts. They have the potential, however, to result in losses to the company if economic conditions change and the company finds itself in a situation where it must deliver raw materials at a fixed price.b) As long as the current market price of the raw materials is at or below the contract price that is fixed there is little to record relative to these contracts as they would be viewed as mutually unexecuted.c) Our answer to b) would change if the market price exceeded the contract price. With each delivery the company would suffer a loss and the company should accrue a loss on all of the contracts when it can reasonably estimate the amount.d) Shareholders should probably have some awareness of the existence of these contracts since they have the potential to create losses for the company. As mutually unexecuted contracts they are typically not recorded but footnote disclosures could clearly be given.

9.27 a) Financial impact of rate changesCPP EI

Old rates 3.2% of $10,000 = $320

3.78% of $10,000 = $378

Changed rates 3.6% of $10,000 = $360

3.7% of $10,000 = $370

Effect $ 40

$ (8)

Net effect = $ 32 x 20$640

b) Memo

To: President of CompanyFrom: Your Name, AccountantRe: Financial impact of change in CPP and EI ratesThe change in CPP and EI rates increases the cost of maintaining the existing labor force in the amount of $640 per period. In addition, employee contributions are also increasing, so that the net cheque that each employee receives falls. The company might want to consider increasing wages in order that employees not suffer

19

decreases in income, and to ensure that the company is able to attract employees. Any considerations of this nature will result in additional labour costs for the company.c) In order to reduce the impact of these rate changes, the company could reduce its labor force, decrease the hours its employees work, or consider moving to another country.

20

Reading and Interpreting Published Financial Statements

9.28 a) For producing properties, the estimated costs for reclamation are estimated and expensed over the life of the estimated reserves. The costs of reclamation are part of the cost associated with generating the revenue from the producing properties and therefore it is appropriate that these costs be matched against the revenue as it is generated. For non-producing properties, the accrued as liabilities when the costs are likely to be incurred and can be reasonably estimated. Actual site reclamation costs are deducted from the liability. The non-producing properties are not generating revenue and therefore it is not possible to match these costs to anything. It is therefore appropriate that they be expensed as soon as they are known.

b) Part of the cost associated with the revenue generated from producing properties is the cost of cleaning up and restoring the property after the revenue generation is complete. It is therefore appropriate to match these costs against the revenue as it occurs. It is not appropriate to wait until the actual costs are incurred because at that time there is no revenue against which to generate these costs.

9.29 a) A line of credit is an agreement with a lending institution in which the institution allows the company to access cash beyond the balance in its account. As soon as this extra cash is accessed, the amount is owed to the financial institution and interest is charged against the amount accessed. It is a short-term loan. CAE would want to have lines of credit in various currencies if it was buying from suppliers outside of Canada and repaying those amounts in currencies other than the Canadian dollar.

b) A prime rate is the rate of interest charged by financial institutions to its best customers, those with the best credit rating. It is usually the lowest borrowing rate charged by the financial institution. The closer the interest rate on the line of credit is to the prime rate, the greater the confidence that the financial institution has in the company’s ability to repay the debt.

c) Unsecured means that there are no specific assets that are tied to the debt. If the company fails to repay the debt, the financial institution would have to sue the company for repayment and could not claim specific assets as payment for the debt. If specific assets are tied to the debt and if the value of those assets is sufficient to cover the outstanding debt, it is likely that CAE could get a reduced rate of interest. When debt is secured, the risk on non-payment is

21

reduced and financial institutions are often willing to accept reduced interest.

9.30 a) Customer deposits represent the amounts that clients have given to Mackenzie to be invested. b) Customer deposits are likely long-term because most clients would be interested in leaving their funds with Mackenzie to manage over an extended period of time. Customers could, however, withdraw there funds within a short period of time which gives the assets a short-term aspect.c) This asset implies that Mackenzie is involved in loaning out mortgage money. In fact, Mackenzie has a subsidiary operation called M.R.S. Trust Company that manages residential and commercial mortgage portfolios. It is listed with the assets because it represents the future mortgage payments that will be made to the company in repayment of mortgage money borrowed. To Mackenzie this is an asset.

9.31 a) A commercial paper program is a program whereby a company that has a high credit rating borrows from another through the issuance of unsecured promissory notes. The bank does not consider Xerox to be a particularly good credit risk, however, because the interest rates on its long-term debt instruments are much higher.b) The short-term borrowing rate is much lower than the long-term borrowing rate because the risk of Xerox defaulting on its short-term debt has been assessed at much less than the risk of it defaulting on long-term debt. In general, the interest rate on long-term borrowings is higher due to expected inflation, and greater uncertainties associated with the long-term. c) A secured debt means that the lender has claims against specific assets of the borrowing company in the event of default. A company might choose to issue secured debt in order to obtain a lower interest rate on the debt.

9.32 a) Dofasco’s statutory rate for income tax in 1998 is 42.98% ($120.4/$280.1).

b) The actual tax rate is 37.38% ($104.7/$280.1).

c) Permanent differences are differences between accounting and tax reporting that never reverse themselves. An accounting item will never become a tax item or a tax item will never become an accounting item. The manufacturing and processing credit is a deduction allowed for tax purposes but it is not an expense in the accounting records. The resource allowance is a also a deduction

22

allowed for tax purposes which is not an expense for accounting purposes.

d) In 1998Dofasco actually paid $108.2 million in income tax to Revenue Canada. This amount is shown as the current amount in the first table in Exhibit 9-14.

9.33 a) Laidlaw likely included this note because there exists the distinct possibility of a significant loss if the court rules against the subsidiary. Although the company does not think that the courts will rule against it, the company feels that this information is relevant for shareholders and other decision-makers. b) Laidlaw will likely continue to provide a note about this matter in its financial statements until the court has ruled either in favor or against its subsidiary. At this time, Laidlaw can remove the note and accrue an actual loss if necessary.

c) The 1998 financial statements do not include a note on this contingency any more. An examination of the financial statements does not reveal how this issue was resolved. The lack of information probably means that the resolution of the issue did not materially affect the company.

9.34 a) A line of credit is an agreement with a lending institution in which the institution allows the company to access cash beyond the balance in its account. As soon as this extra cash is accessed, the amount is owed to the financial institution and interest is charged against the amount accessed.b) The bank would raise the interest rate if it considered the risk of collection higher than it was before. Also, the level of debt increased significantly over the last year and this may have affected the bank’s decision as well. Chai-Na-Ta may be able to convince the bank to lower the rate the next time it renews the line of credit, if it pays off the current outstanding debt within the given time frame.c) When a debt is secured, it means that certain assets are pledged against default of the debt. If the company cannot repay the debt, the bank can force the company to sell the secured assets in order to recover the amount of the debt. If the debt was not secured, it is probably that the interest rate would increase because the bank’s ability to collect the amount owed in case of default is less certain.

9.35 a) The “guaranteeing of indebtedness of third parties” means that the company has agreed to act as a guarantor for other companies. If those companies default on outstanding commitments, the creditor can come to Alcan to collect the amount owed.

23

b) It was important for Alcan to include a note about the guarantees because there is a possibility that Alcan could be required to pay these amounts in the future if the third parties default. Users need to know about this possibility.c) These commitments for the supplies of goods and services represent mutually unexecuted contracts. As either side acts on the conditions of these contracts – delivers goods, performs services, pays in advance or amounts owed – the actions are recorded in the accounting system. Prior to such actions nothing is recorded unless there is a likelihood of future losses associated with these contracts. The fact that they are described in the commitment sections of the notes indicates that they have not been recorded in the accounting system.

Beyond the Book

9.36 Answers to this question will be depend on the company selected.

9.37 Answers to this question will be depend on the company selected.

24

CASE

9.38 The Bigger Motor Companya) 1. Line of credit

If Bigger borrowed $60,000 in January, it would need to repay the money in four montly instalments of $15,000 starting in February. If we assume that the amount was borrowed on January 1 and repayments started February 1, the cost of borrowing would be:

$60,000 x .09 x 1/12 = $450; repayment amount, $15,450$45,000 x .09 x 1/12 = $338; repayment amount, $15,338$30,000 x .09 x 1/12 = $225; repayment amount, $15,225$15,000 x .09 x 1/12 = $113; repayment amount, $15,113Total cost of borrowing is $1,126.

2. Accounts payableIf Bigger purchases $50,000 per month and does not pay in 30 days it forfeits a $1,000 discount each month. This costs the company 12.2% (.02 / (60/365)). As well, the delay of the $50,000 does not provide enough working capital if the company needs $60,000.

3. Short-term bank loanCash balance that must be maintained = .15 x $75,000 = $11,250.Cash balance available to be used = $63,750 which is enough to cover the $60,000 need for working capital.Assuming that the monthly payments are made at the end of each month, the interest payments would be calculated as:$75,000 x .07 x 1/12 = $438; repayment amount, $7,938$67,500 x .07 x 1/12 = $394; repayment amount, $7,894$60,000 x .07 x 1/12 = $350; repayment amount, $7,850$52,500 x .07 x 1/12 = $306; repayment amount, $7,806$45,000 x .07 x 1/12 = $263; repayment amount, $7,763$37,500 x .07 x 1/12 = $219; repayment amount, $7,719$30,000 x .07 x 1/12 = $175; repayment amount, $7,675$22,500 x .07 x 1/12 = $131; repayment amount, $7,631$15,000 x .07 x 1/12 = $88; repayment amount, $7,588$7,500 x .07 x 1/12 = $44; repayment amount, $7,544Total interest payments = $2,408

b) Students’ recommendations may vary. They should not choose the accounts payable alternative. This alternative does not generate enough working capital. If the student chooses the line of credit, the reason should be that the total amount paid in interest is the least. However, the company may not be able to make payments as high as $15,000 over four consecutive months. If the student chooses the short-term loan, the reason should be that this spreads the payments over a longer period of time and may make it easier for the company

25

to manage. Although the total interest paid over the ten months is higher, the interest rate is lower. If the company has excess cash it may be able to pay off the debt in a shorter period of time than the ten months. This would save some interest costs.

Critical Thinking Question

9.39 a) The criteria for evaluating a contingency are 1) it is likely that some future event will result in the company incurring an obligation which will require the use of assets or the performance of a service and 2) the amount of the loss can be reasonably estimated.In the case of a resource company, these criteria would have to be applied to their specific circumstance. If the company knew that it had an obligation to clean up or restore the site to its original condition, it would meet the first criteria and a contingency would be present. If it was not required to clean up or restore the site and it had no intention of doing so, it could argue that no contingency was present.With respect to measurement of the future obligation, a more difficult problem arises. If the company had not incurred these cost before, it would have a difficult time arriving at a reasonable estimation of those future costs. If it had cleaned up or restored previous sites, it would likely be able to reasonably estimate these future costs. Another source of this information would be the costs incurred by other companies that have cleaned up or restored sites.In general, the following criteria would determine what the company would do: If it is likely that it will be involved in a future clean-up or restoration and it can reasonably estimate the future cost of this activity, it should record a portion of that future cost in each year that it recognized revenue from the site. If it is likely that it will be involved in a future clean-up or restoration but it is not possible to reasonably estimate the future cost of this activity, it should disclose information about this contingency in the note to the financial statements. As soon as it can reasonably estimate the future costs, it should start recording them. If it is likely that it will clean up or restore the site, it does not need to record or disclose any information about it.b) Present (discounted) value of future cash flows is one of four different measurement attributes of assets and liabilities used in practice (the others are historical cost, replacement cost, and net realizable value). Recognition is dependent upon an element having a relevant attribute, which in itself is a function of the nature of the item and the relevance and reliability of the attribute measure. For

26

example, equipment is most often reported using the historical cost measurement attribute. The selection of this attribute probably reflects the concern that other attributes are less reliable measures, although many would question the relevance of the historical cost attribute, especially for decisions such as determining the collateral value of an asset. However, the accounting literature recognized that decision makers must often trade off the relevance of information and the reliability of the measure.This question addresses the reliability of present value measures. The most common reason for viewing present value as a second choice for measurement is that it is highly subjective and would need to be amended or modified over time. In contrast, the direct measures described above generally are more reliable because they can be objectively determined.One of the primary characteristics of contingencies, such as lawsuits, is the extended length of time over which the event will occur. Not only is the litigation process time consuming (e.g., from the point in time in which litigation is begun through initial settlement, appeals, and final verdict or settlement), but the payment of damages may occur over an extended period of time. In such cases, accountants may consider using present value to measure litigation settlements although the CICA Handbook does not specifically make this recommendation.

27

![v } ( ] r À v ] W l ] v > ] u ]Exchange loss incurred on foreign currency payments and liabilities during the six months period amounted to Rs. 236 million due to continuous devaluation](https://img.pdfslide.us/doc/110x75/604be4a55dfc51102e114626/v-r-v-w-l-v-u-exchange-loss-incurred-on-foreign-currency-payments.jpg)