Embed Size (px)

Citation preview

Chapter 5 The Operating Cycle and

Merchandising Operations

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Financial Accounting, 11e

Learning Objectives Identify the management issues related to merchandising businesses.

Describe the terms of sale related to merchandising transactions.

Prepare an income statement and record merchandising transactions under the perpetual inventory system.

Prepare an income statement and record merchandising transactions under the periodic inventory system.

Describe the components of internal control, control activities, and limitations on internal control.

Apply internal control activities to common merchandising transactions.

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Managing Merchandising Businesses

Merchandising business: Earns income by buying and selling goods.

Merchandise inventory: Goods for sale.Evaluation of Liquidity

Sufficient money on hand to pay bills when due and cash for unexpected needs.

Working capital: Measure of liquidity; the amount by which current assets exceed current liabilities.

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Current Ratiofor Best Buy

Current ratio: The ratio of current assets to current liabilities.

If Best Buy’s current assets are $10,566 and current liabilities are $8,978:

$10,566Current Ratio =

$8,978

= 1.18

Current AssetsCurrent Ratio

Current Liabilities

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Operating Cycle Operating cycle: A series of transactions a business

engages in for an amount of time.Common transactions:

Purchase of merchandise inventory for cash or on credit Payment for purchases made on credit Sales of merchandise inventory for cash or on credit Collection of cash from credit sales

Financing period: Period between the time the supplier must be paid and the end of the operating cycle.

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Cash Flows in the Operating Cycle

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

The Financing Period

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Choice of Inventory System

Perpetual inventory system: Continuous records kept of the quantity and cost of individual items bought and sold.

Periodic inventory system: Unsold inventory is counted periodically.Physical count is usually taken at the end of

the accounting period.

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Foreign Business Transactions

If a domestic company bills a foreign company in a foreign currency and accepts payment in that foreign currency, it will incur an exchange gain or loss if the exchange rate between the domestic and foreign currencies changes between the date of sale and the date of payment.

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

The Need for Internal Controls

Internal controls: Accounting systems and control procedures to protect a company’s assets.

Physical inventory: An actual count of all merchandise on hand. Includes all goods intended for sale. Includes goods in transit from suppliers if title to the

goods has passed to the merchandiser. Does not include merchandise that a company has

sold but not yet delivered to customers.

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Management’s Responsibility for Internal Control

Safeguard the firm’s assetsEnsure the reliability of the accounting

recordsSee that employees comply with all legal

requirements and operate the firm to the best advantage of its owners

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

The management of SavRite Corporation made the following decisions. Indicate whether each decision pertains primarily to (a) cash flow management, (b) choice of inventory system, or (c) foreign transactions.

1. Decided to decrease the credit terms offered to customers from 30 days to 20 days to speed up collection of accounts.

2. Decided to purchase goods made by a supplier in India.

3. Decided to measure working capital monthly to ensure that there is an adequate reserve to maintain liquidity.

4. Decided that sales would increase if salespeople knew how much inventory was on hand at any one time.

5. Decided to try to negotiate a longer time to pay suppliers than had been previously granted.

SOLUTION 1. a; 2. c; 3. a; 4. b; 5. a © 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Terms of Sale

Trade discount: Percentage (usually 30 percent or more) off list or catalogue prices.

Sales discount: Discounts a buyer takes when paying an invoice within a set number of days from the invoice date.

Purchases discount: Discounts a buyer takes for early pa.yment of merchandise

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Transportation Costs FOB shipping point: “Free on board” for the seller; the

buyer bears the shipping costs. Freight-in: When the buyer pays transportation charge.

FOB destination: The seller bears the transportation costs. Delivery expense (or freight-out): When the seller pays the

transportation charge.

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Terms of Debit and Credit Card Sales

Debit cards deduct directly from a person’s bank account.

Credit cards allow for payment later. Seller does not have to establish the customer’s

credit, collect from the customer, or tie up money in accounts receivable.

Lender does not pay the total amount of the credit card sales, but discounts 2 to 6 percent. The discount is a selling expense for the merchandiser.

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

A local company sells refrigerators that it buys from the manufacturer.

a. The manufacturer sets a list or catalogue price of $1,200 for a refrigerator. The manufacturer offers its dealers a 40 percent trade discount and terms of FOB destination.

b. Assume the same terms as a, except the manufacturer sells the refrigerator under terms of FOB shipping point. The cost of shipping is $120.

c. Assume the same terms as b, except the manufacturer offers a sales discount of 2/10, n/30. Sales discounts do not apply to shipping costs.

What is the net cost of the refrigerator to the dealer in each case, assuming payment is made within 10 days of purchase?

SOLUTION a. $1,200 – ($1,200 × 0.40) = $720 b. $720 + $120= $840c. $840 – ($720 × 0.02) = $825.60

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Perpetual Inventory System

Under the perpetual inventory system, the Merchandise Inventory and Cost of Goods Sold accounts are continually updated during the accounting period as purchases, sales, and other inventory transactions that affect these accounts occur.

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Income Statement Under the Perpetual Inventory System

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

EXAMPLE: Purchases on Credit (slide 1 of 2)

Aug. 3: Received merchandise purchased on credit, invoice dated August 1, terms n/10, $4,890.

Analysis: Under the perpetual inventory system, the cost of merchandise is recorded in the Merchandise Inventory account at the time of purchase, which

▲ increases the Merchandise Inventory account and

▲ increases the Accounts Payable account.

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

EXAMPLE: Purchases on Credit (slide 2 of 2)

Comment: In the transaction described here, payment is due 10 days from the invoice date. If an invoice includes a charge for shipping or if shipping is billed separately, it should be debited to Freight-In.

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

EXAMPLE: Purchases Returns and Allowances

Aug. 6: Returned part of merchandise received on August 3 for credit, $480.

Analysis: Under the perpetual inventory system, purchases returns and allowances▼ decrease the Accounts Payable account and

▼ decrease the Merchandise Inventory account.

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

EXAMPLE: Payments on Account

Aug. 10: Paid amount due in full for the purchase of August 3, part of which was returned on August 6, $4,410.

Analysis: Payment is made for the net amount due of $4,410 ($4,890 – $480), which ▼ decreases the Accounts Payable account and

▼ decreases the Cash account.

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Recording Purchase Transactions Under the Perpetual Inventory System

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

EXAMPLE: Sales on Credit (slide 1 of 2)

Aug. 7: Sold merchandise on credit, terms n/30, FOB destination, $1,200; the cost of the merchandise was $720.

Analysis: Under the perpetual inventory system, sales always require two entries. First, the sale is recorded, which

▲ increases the Accounts Receivable account and

▲ increases the Sales account. Second, Cost of Goods Sold is updated by a transfer from

Merchandise Inventory, which

▲ increases the Cost of Goods Sold account and

▼ decreases the Merchandise Inventory account.

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

EXAMPLE: Sales on Credit (slide 2 of 2)

Comment: In the case of cash sales, Cash rather than Accounts Receivable is debited for the amount of the sale. If the seller pays for the shipping, the shipping cost should be debited to Delivery Expense.

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Sales Returns and Allowances

The Sales Returns and Allowances account gives management a readily available measure of unsatisfactory products and dissatisfied customers.

This account is a contra-revenue account with a normal debit balance, and it is deducted from sales on the income statement.

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

EXAMPLE: Sales Returns and Allowances (slide 1 of 3)

Aug. 9: Accepted return of part of merchandise sold on August 7 for full credit and returned it to merchandise inventory, $300; the cost of the merchandise was $180.

Analysis: Under the perpetual inventory system, when a seller allows the buyer to return all or part of a sale or gives an allowance—a reduction in amount—two entries are necessary.

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

EXAMPLE: Sales Returns and Allowances (slide 2 of 3)

First, the original sale is reversed, which ▲ increases the Sales Returns and Allowances

account and ▼ decreases the Accounts Receivable account.

Second, the cost of the merchandise must also be transferred from the Cost of Goods Sold account back into the Merchandise Inventory account, which

▲ increases the Merchandise Inventory account and ▼ decreases the Cost of Goods Sold account.

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

EXAMPLE: Sales Returns and Allowances (slide 3 of 3)

Comment: If the company makes an allowance instead of accepting a return or if the merchandise cannot be returned to inventory and resold, this transfer is not made.

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

EXAMPLE: Receipts on Account

Sept. 5: Collected in full for sale of merchandise on August 7, less the return on August 9, $900.

Analysis: Collection is made for the net amount due of $900 ($1,200 – $300), which ▲ increases the Cash account and

▼ decreases the Accounts Receivable account.

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Recording Sales Transactions Under the Perpetual Inventory System

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

The numbered items below are account titles, and the lettered items that follow are types of merchandising transactions. For each transaction, indicate which accounts are debited or credited by placing the account numbers in the appropriate columns, assuming use of a perpetual inventory system.

1. Cash 2. Accounts Receivable 3. Merchandise Inventory

Account Account

Debited Credited

a. Purchase on credit _________________

b. Purchase return for credit _________________

c. Purchase for cash ________ _________

d. Sale on credit ________ _________

e. Sale for cash ________ _________

f. Sales return for credit ________ _________

g. Payment on account ________ _________

h. Receipt on account ________ _________

4. Accounts Payable 5. Sales

6. Sales Returns and Allowances 7. Cost of Goods Sold

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

SOLUTION

Account Account

Debited Credited

a. Purchase on credit 3 4

b. Purchase return for credit 4 3

c. Purchase for cash 3 1

d. Sale on credit 2, 7 5, 3

e. Sale for cash 1, 7 5, 3

f. Sales return for credit 6, 3 2, 7

g. Payment on account 4 1

h. Receipt on account 1 2

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Periodic Inventory System Under the periodic inventory system, Cost of Goods Sold

is computed on the income statement because it is not updated for purchases, sales, and other transactions as it is under the perpetual inventory system.

Cost of goods available for sale: Total cost of merchandise that could be sold in the accounting period. The difference between the cost of goods sold and cost of

goods available for sale is the amount not sold, or ending merchandise inventory.

Net purchases: Total purchases plus any freight-in less any deductions such as purchases returns and allowances and discounts from suppliers for early payment.

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Income Statement Under the Periodic Inventory System

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

The Components of Cost of Goods Sold

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

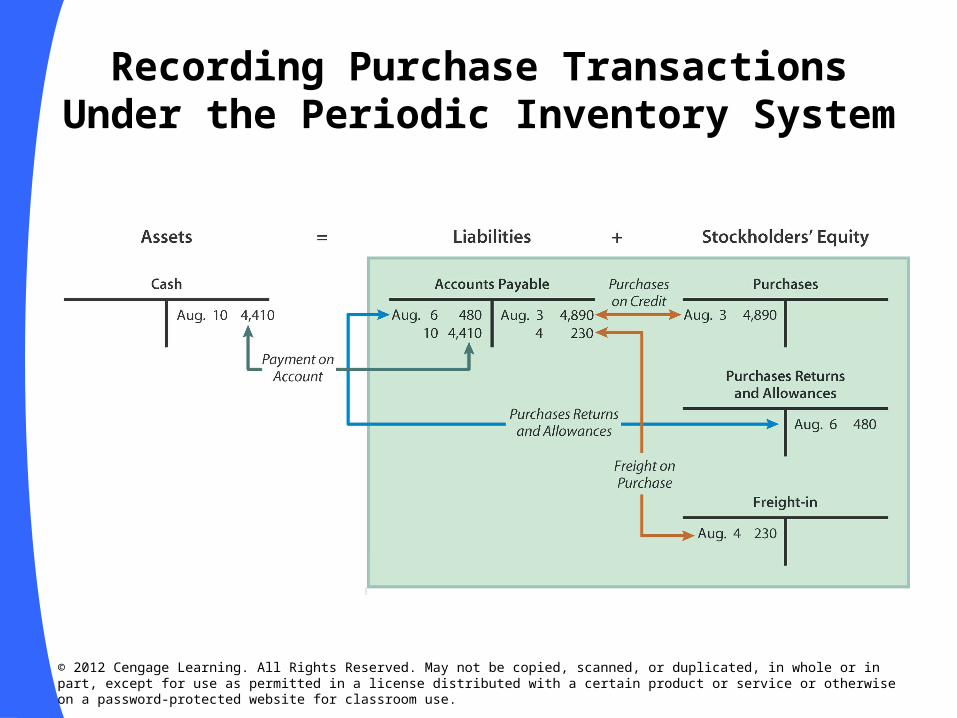

EXAMPLE: Purchases on Credit (slide 1 of 2)

Aug. 3: Received merchandise purchased on credit, invoice dated August 1, terms n/10, $4,890.

Analysis: Under the periodic inventory system, the cost of merchandise is recorded in the Purchases account at the time of purchase. This account is a temporary one used only with the periodic inventory system. The Purchases account does not indicate whether merchandise has been sold or is still on hand. Purchases made by a company ▲ increase the Purchases account and

▲ increase the Accounts Payable account.

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

EXAMPLE: Purchases on Credit (slide 2 of 2)

Comment: Its sole purpose is to accumulate the total cost of merchandise purchased for resale during an accounting period. (Purchases of other assets, such as equipment, are recorded in the appropriate asset account, not in the Purchases account.)

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

EXAMPLE: Purchases Returns and Allowances (slide 1 of 2)

Aug. 6: Returned part of merchandise received on August 3 for credit, $480.

Analysis: This is a contra-purchases account with a normal credit balance, and it is deducted from purchases on the income statement to arrive at net purchases, which ▼ decreases the Accounts Payable account and ▲ increases the Purchases Returns and

Allowances account.

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

EXAMPLE: Purchases Returns and Allowances (slide 2 of 2)

Comment: Under the periodic inventory system, the amount of a return or an allowance is recorded in the Purchases Returns and Allowances account.

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

EXAMPLE: Freight-in (slide 1 of 2)

Aug. 7: Received a bill for freight costs of the purchases on Aug. 3, $230.

Analysis: Freight costs on purchases ▲ increase the Freight-in account

▲ increase the Accounts Payable account.

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

EXAMPLE: Freight-in (slide 2 of 2)

Comment: Freight-in is added on the income statement to net purchases to arrive at net cost of purchases under the periodic method.

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

EXAMPLE:Payments on Account

Aug. 10: Paid amount in full due for the purchase of August 3, part of which was returned on August 6, $4,410.

Analysis: Payment is made for the net amount due of $4,410 ($4,890 - $480), which ▼ decreases the Accounts Payable account and

▼ decreases the Cash account.

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Recording Purchase Transactions Under the Periodic Inventory System

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

EXAMPLE: Sales on Credit (slide 1 of 2)

Aug. 7: Sold merchandise on credit, terms n/30, FOB destination, $1,200; the cost of the merchandise was $720.

Analysis: Under the periodic inventory system, sales require only one entry, which ▲ increases the Accounts Receivable account

and

▲ increases the Sales account. © 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

EXAMPLE: Sales on Credit (slide 2 of 2)

Comment: In the case of cash sales, Cash rather than Accounts Receivable is debited for the amount of the sale. If the seller pays for the shipping, the amount should be debited to Delivery Expense.

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

EXAMPLE: Sales Returns and Allowances (slide 1 of 2)

Aug. 9: Accepted return of part of merchandise sold on August 7 for full credit and returned it to merchandise inventory, $300; the cost of the merchandise was $180.

Analysis: Under the periodic inventory system, when a seller allows the buyer to return all or part of a sale or gives an allowance, only one entry is needed, which ▲ increases the Sales Returns and Allowances account and

▼ decreases the Accounts Receivable account.

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

EXAMPLE: Sales Returns and Allowances (slide 2 of 2)

Comment: The Sales Returns and Allowances account is a contra-revenue account with a normal debit balance and is deducted from sales on the income statement.

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

EXAMPLE: Receipts on Account (slide 1 of 2)

Sept. 5: Collected in full for sale of merchandise on August 7, less the return on August 9, $900.

Analysis: Collection is made for the net amount due of $900 ($1,200 – $300), which ▲ increases the Cash account and

▼ decreases the Accounts Receivable account.

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Recording Sales Transactions Under the Periodic Inventory

System

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

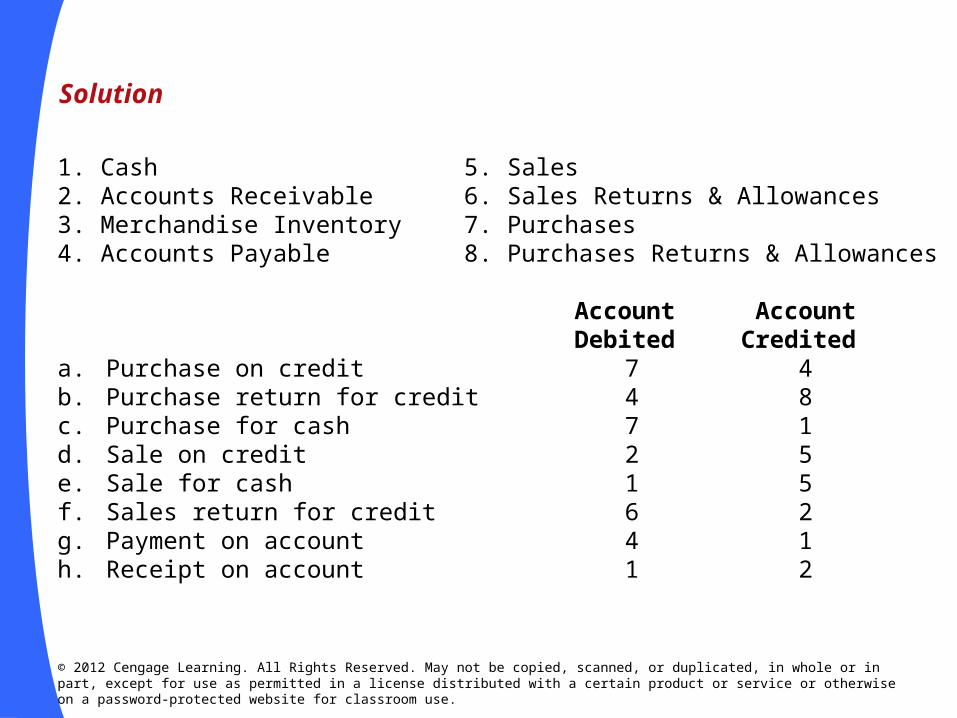

The numbered items below are account titles, and the lettered items that follow are types of merchandising transactions. For each transaction, indicate which accounts are debited or credited by placing the account numbers in the appropriate columns, assuming use of a periodic inventory system.

1. Cash 5. Sales2. Accounts Receivable 6. Sales Returns & Allowances 3. Merchandise Inventory 7. Purchases 4. Accounts Payable 8. Purchases Returns & Allowances

Account AccountDebited Credited

a. Purchase on credit _______ _______b. Purchase return for credit _______ _______c. Purchase for cash _______ _______d. Sale on credit _______ _______e. Sale for cash _______ _______f. Sales return for credit _______ _______g. Payment on account _______ _______h. Receipt on account _______ _______© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

1. Cash 5. Sales2. Accounts Receivable 6. Sales Returns & Allowances 3. Merchandise Inventory 7. Purchases 4. Accounts Payable 8. Purchases Returns & Allowances

Account AccountDebited Credited

a. Purchase on credit 7 4b. Purchase return for credit 4 8c. Purchase for cash 7 1d. Sale on credit 2 5e. Sale for cash 1 5f. Sales return for credit 6 2g. Payment on account 4 1h. Receipt on account 1 2

Solution

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Components of Internal Control (slide 1 of 2)

Control environment: Environment created by management’s overall attitude, awareness, and actions.

Risk assessment: Identifying areas in which risks are high so adequate controls can be implemented.

Information and communication: The accounting system established by management.

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Components of Internal Control (slide 2 of 2)

Control activities: Policies and procedures put in place to see that directives are carried out.

Monitoring: Management’s regular assessment of the quality of internal control, including periodic review of compliance with all policies and procedures.

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Control Activities (1 of 2)

Authorization: Approval of certain transactions and activities.

Recording transactions: Establish accountability for assets by recording them.

Documents and records: Well-designed documents help ensure that transactions are properly recorded.

Physical controls: Controls to limit access to assets.Periodic independent verification: Independent person

should periodically check the records against the assets.

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

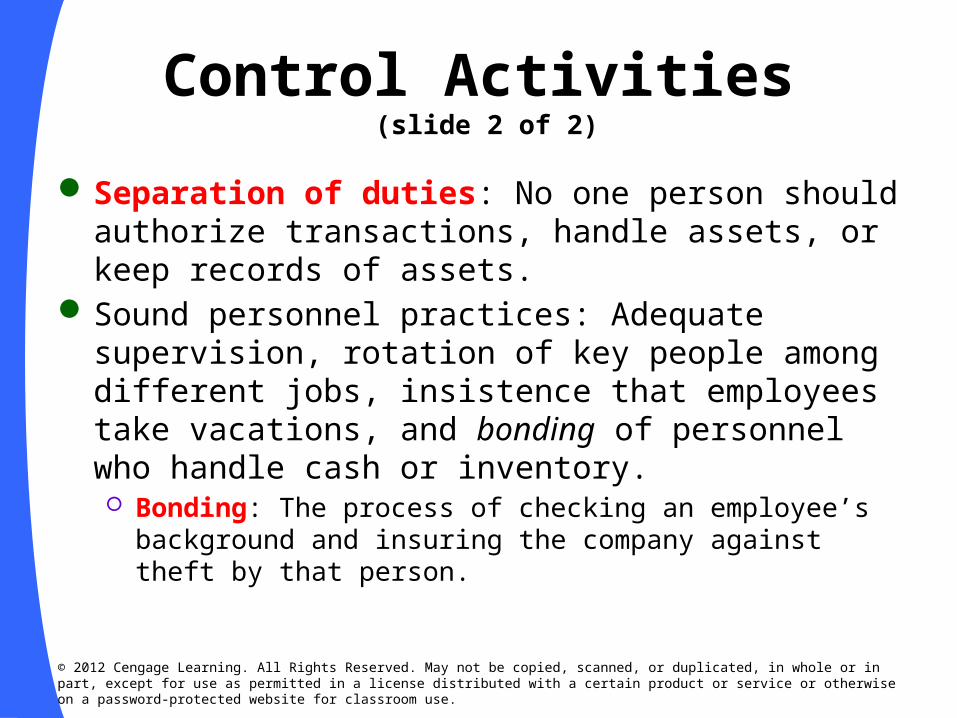

Control Activities (slide 2 of 2)

Separation of duties: No one person should authorize transactions, handle assets, or keep records of assets.

Sound personnel practices: Adequate supervision, rotation of key people among different jobs, insistence that employees take vacations, and bonding of personnel who handle cash or inventory. Bonding: The process of checking an employee’s background

and insuring the company against theft by that person.

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Limitations on Internal Control

As long as people perform control procedures, an internal control system will be vulnerable to human error.

Errors can arise from misunderstandings, mistakes in judgment, carelessness, distraction, or fatigue.

Separation of duties can be defeated through collusion by employees who secretly agree to deceive a company.

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Match the internal control components on the right with the related statements on the left.

____ 1. Establishes separation of duties ____ 2. Communicates appropriate

information to employees ____ 3. Has an internal audit department ____ 4. Performs periodic independent

verification of employees’ work ____ 5. Assesses the possibility of losses ____ 6. Instructs and trains employees ____ 7. Has well-designed documents and

records ____ 8. Limits physical access to

authorized personnel

a. Control environmentb. Risk assessmentc. Information and communicationd. Control activitiese. Monitoring

SOLUTION 1. d; 2. c; 3. e; 4. d; 5. b; 6. a; 7. d; 8. d

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Internal Control Over Merchandising Transactions

Internal Control and Management Goals Keep sufficient inventory on hand to sell without overstocking Keep enough cash on hand to pay in time to receive discounts Keep credit losses as low as possible by selling on credit to

customers who pay in time

Control of Cash Receipts Control of Cash Received by Mail Control of Cash Received over the Counter

Control of Purchases and Cash Disbursements

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Internal Controls in a Large Company: Separation of Duties and Documentation

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Internal Control Plan

for Purchases and Cash

Disbursements

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Items (a)–(e) below are a company’s departments. Items (f) and (g) are firms with which the company has transactions.

a. Requesting department d. Accounting department g. Bank

b. Purchasing department e. Treasurer

c. Receiving department f. Vendor

Use the letter of the department or firm to indicate which one prepares and sends the following business documents:

Prepared by Received by

1. Receiving report _________ _________

2. Purchase order _________ _________

3. Purchase requisition _________ _________

4. Check _________ _________

5. Invoice _________ _________

6. Check authorization _________ _________

7. Bank statement _________ _________

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

SOLUTION

Prepared by Received by

1. Receiving report c d

2. Purchase order b f

3. Purchase requisition a b

4. Check e f

5. Invoice f d

6. Check authorization d e

7. Bank statement g d

© 2012 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.