Embed Size (px)

Citation preview

88

Chapter 4- Trends in Indian Health Insurance Industry

89

4.1 History and Global Perspective

Under the General Agreement on Trade in Services (GATS) of the World Trade

Organization (WTO) sector classification scheme, health insurance falls under the financial

services sector. Financial services are divided into two sectors: 1) insurance and 2) banking

and other financial services. Within insurance, there are four sub-sectors: a) life, accident

and health insurance, b) non-life insurance, c) reinsurance and retrocession, and, d) services

auxiliary to insurance, including broking and agency services. Despite the appearance of the

term "health insurance" under the first category, many country commitments affecting health

insurance services are in fact covered by the second category (non-life insurance). In India

health insurance is a part of non-life insurance sector. However, life insurance companies are

allowed to sell health insurance products. .

In India insurance is a federal subject and is governed by the Insurance Act 1938 and the

Insurance Regulatory and Development Authority Act, 1999. In India the Insurance business

is divided into four classes namely; a. Life insurance, b. Fire insurance, c. Marine insurance

and d. Miscellaneous insurance. Life insurers transact life insurance business and general

insurance transact the rest. Health insurance falls under the miscellaneous insurance business

but there is no clear demarcation as the same is also offered by the life insurance companies.

Globally, the history of general insurance can be traced back to the early civilization. As the

incidence of losses increased with the advancement of civilization, slowly the idea and

concept of risk pooling and loss sharing started taking roots. Historical facts show that the

Aryans through their cooperatives practiced the loss of profits insurances. The

Mediterranean merchants also practiced insurances from as early as the fourth century BC

through the issue of bottomry bonds, which is an advance of money in a ship during the

period of voyage, repayable on the arrival of the ship. The Code of Manu also indicates the

practice of marine insurance by Indian with their counter parts in Sri-Lanka, Egypt and

Greece23

.

23

The Institute of Chartered Accountants of India, ‗Principle and practice of general insurance‟,

2008.

90

When, talking about the history of health insurance in India, one will find that health

insurance is not of recent origin. One can argue that the concept of health insurance is there

since the beginning of the mankind. In the Vedic literature it‘s stated that people use to

sacrifice animals to Gods and in return expected good health. It is interesting to link this

activity with that of the current concept of health insurance i.e. to pay the premium (animal

sacrifice) to safeguard from ill health. However, in such situation there was no transfer of

risk in contractual terms. The concern for loss resulting from accident and illness can be

traced to ancient civilizations. In fact, one of the earliest forms of health insurance may have

been based on the ancient custom of paying the doctor while in good health and

discontinuing payment during periods of illness. The development of health insurance in

existing form in India is based on pattern followed in Europe and America. Also, health

Insurance or medical insurance schemes had developed in India due to industrial relations

problems between the employer and the employees. The Corporate Houses used to offer core

and non-core benefits to the employees. The insurance policies were granted to large

Corporate Houses purely on an accommodation basis. The cover usually offered to the

employees was in the nature of hospitalization and domiciliary treatment for dental and non-

surgical eye treatment.

Before examining the trends in the Indian health insurance industry, the global insurance

market was looked into. The market size of the global insurance industry which is measured

in terms of premium as a percent of global GDP was first studied, followed by studying the

data on insurance density and insurance penetration. This section is then followed by the

overview of the Indian healthcare system.

4.1.1 Market Share & Segmentation

The market size of the global insurance industry measured in terms of total premium stands

USD 4061bn in year 2007. The life insurance industry accounted for USD 2393bn, Non-life

accounted for USD 1668bn (Table 4.1). In the year 2007 the life insurance industry captures

59 percent of the total global insurance premium and the remaining 41 percent is captured by

the non-life insurance industry. The global premium as a percent of global GDP stands 7.48

91

percent. The total direct premium growth is 3.3 percent. The premium growth in non-life

sector is much less than that of the life insurance sector.

Table 4.1: Global insurance industry overview (market size), 2007

Global Insurance Industry

Amount Units Year Source

Total Gross Insurance Premiums 4061 Billion US$ 2007 Swiss Re

Global Premiums as percent of Global

GDP 7.48 Percent 2007 IMF

Global Life Insurance Premiums 2393 Billion US$ 2007 Swiss Re

Global Non-Life Insurance Premiums 1668 Billion US$ 2007 Swiss Re

Total Direct Premium Growth, 2007-2007 3.3 Percent 2007 Swiss Re

Growth in Life Insurance Premiums 5.4 Percent 2007 Swiss Re

Growth in Non-Life Insurance Premiums 0.7 Percent 2007 Swiss Re

4.1.2 Insurance density and penetration (international market)

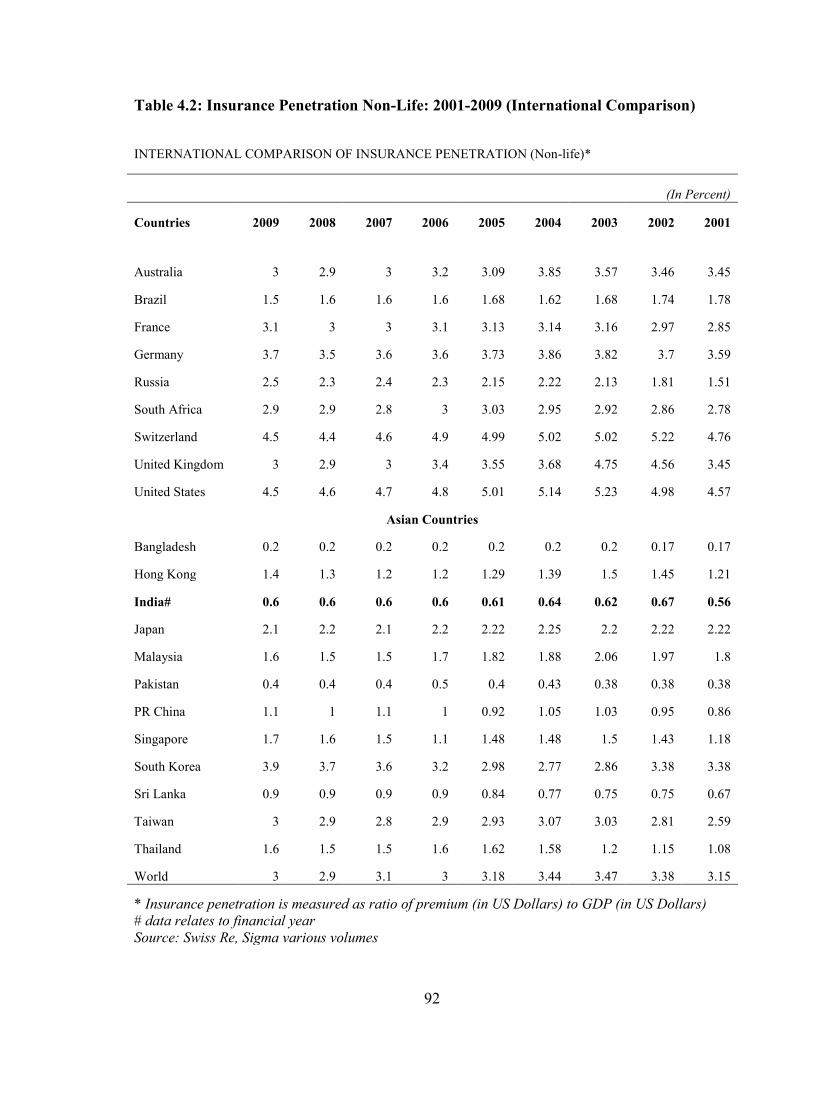

Table 4.2 and Table 4.3 depict the non-life international comparison of insurance penetration

and density24

. The insurance penetration in India has increased to 0.6 percent (2009) from

0.56 percent (2001). In India there had been an increase in insurance density from 2.4 to 6.7

during 2001 to 2009. India is one of the major contributor to the emerging market premium

as could be seen in the Figure 4.1 that reflect the additional premium volume from 2003-

2007 compared with the premium volume of 2002. India occupies seventh rank in the

emerging markets in terms of market share in non life insurance (Table 4.4). In non-life

insurance India‘s share is 3.7 percent and that of China is 17 percent in the year 2007.

24

Insurance penetration is measured in terms of premium as a percent of GDP and insurance density

is measured in terms of per capita premium.

92

Table 4.2: Insurance Penetration Non-Life: 2001-2009 (International Comparison)

INTERNATIONAL COMPARISON OF INSURANCE PENETRATION (Non-life)*

(In Percent)

Countries 2009 2008 2007 2006 2005 2004 2003 2002 2001

Australia 3 2.9 3 3.2 3.09 3.85 3.57 3.46 3.45

Brazil 1.5 1.6 1.6 1.6 1.68 1.62 1.68 1.74 1.78

France 3.1 3 3 3.1 3.13 3.14 3.16 2.97 2.85

Germany 3.7 3.5 3.6 3.6 3.73 3.86 3.82 3.7 3.59

Russia 2.5 2.3 2.4 2.3 2.15 2.22 2.13 1.81 1.51

South Africa 2.9 2.9 2.8 3 3.03 2.95 2.92 2.86 2.78

Switzerland 4.5 4.4 4.6 4.9 4.99 5.02 5.02 5.22 4.76

United Kingdom 3 2.9 3 3.4 3.55 3.68 4.75 4.56 3.45

United States 4.5 4.6 4.7 4.8 5.01 5.14 5.23 4.98 4.57

Asian Countries

Bangladesh 0.2 0.2 0.2 0.2 0.2 0.2 0.2 0.17 0.17

Hong Kong 1.4 1.3 1.2 1.2 1.29 1.39 1.5 1.45 1.21

India# 0.6 0.6 0.6 0.6 0.61 0.64 0.62 0.67 0.56

Japan 2.1 2.2 2.1 2.2 2.22 2.25 2.2 2.22 2.22

Malaysia 1.6 1.5 1.5 1.7 1.82 1.88 2.06 1.97 1.8

Pakistan 0.4 0.4 0.4 0.5 0.4 0.43 0.38 0.38 0.38

PR China 1.1 1 1.1 1 0.92 1.05 1.03 0.95 0.86

Singapore 1.7 1.6 1.5 1.1 1.48 1.48 1.5 1.43 1.18

South Korea 3.9 3.7 3.6 3.2 2.98 2.77 2.86 3.38 3.38

Sri Lanka 0.9 0.9 0.9 0.9 0.84 0.77 0.75 0.75 0.67

Taiwan 3 2.9 2.8 2.9 2.93 3.07 3.03 2.81 2.59

Thailand 1.6 1.5 1.5 1.6 1.62 1.58 1.2 1.15 1.08

World 3 2.9 3.1 3 3.18 3.44 3.47 3.38 3.15

* Insurance penetration is measured as ratio of premium (in US Dollars) to GDP (in US Dollars)

# data relates to financial year

Source: Swiss Re, Sigma various volumes

93

Table 4.3: Insurance Density Non-Life: 2001-2009 (International Comparison)

INTERNATIONAL COMPARISON OF INSURANCE DENSITY (Non-Life)* (In US Dollars)

Countries 2009 2008 2007 2006 2005 2004 2003 2002 2001

Australia 1307.9 1348.6 1326.1 1191.9 1203.2 1186.3 912.1 695.5 628

Brazil 123.8 129.1 106.9 88.4 72.1 55.2 46.8 45 53.2

France 1289.4 1339.2 1219.3 1152.9 1093.9 1057.7 930.4 714.7 630.6

Germany 1518.7 1572.7 1427.9 1300.7 1268.4 1265.3 1120.8 891 809.9

Russia 276.4 268.1 203.3 146.9 116.5 89.6 64.3 43.5 32.6

South Africa 163.9 163.6 159.5 160.2 156.2 141 107.4 64.8 69.1

Switzerland 2852.1 2827.9 2581.7 2450.1 2480.3 2441.3 2228.5 1822.7 1627.1

United Kingdom 1051.2 1275.7 1383.2 1327.1 1311.9 1318 1441.4 1199.7 825.9

United States 2107.3 2177.4 2164.4 2134.2 2122 2062.6 1980.2 1799 1664

Asian Countries

Bangladesh 1.3 1.1 0.9 0.8 0.8 0.8 0.7 0.6 0.6

Hong Kong 417.5 380.8 341.3 331.6 331.7 332.9 348.7 345.1 295.5

India# 6.7 6.2 6.2 5.2 4.4 4 3.5 3 2.4

Japan 840.4 829.2 736 760.4 790.4 830.8 768 714.7 701.1

Malaysia 115 119.5 110.6 103 95.3 89.2 87.2 79.3 68.8

Pakistan 3.6 4 3.9 3.6 2.8 2.2 1.8 1.7 1.5

PR China 40 33.7 25.5 19.4 15.8 12.9 11.2 9.5 7.8

Singapore 645.6 630 531.2 341.2 392 365.4 320.3 300.6 245.8

South Korea 709.7 621 727.3 591.2 495.5 412.5 369.4 337.9 296.7

Sri Lanka 17.7 19.3 14.7 12.8 9.4 7.9 7.2 6.1 5.4

Taiwan 494.8 499.6 462.3 450.3 446.4 414.4 383.2 354.1 327.6

Thailand 62.7 64.9 58.9 50 44.4 41.3 27.6 23.1 19.8

World 253.9 264.2 249.6 224.2 219 220 202.5 175.6 158.3

* Insurance density is measured as ratio of premium (in US Dollar) to total population.

# data relates to financial year.

Source: Swiss Re, Sigma various volumes

94

Figure 4.1: Contribution to emerging market premium (growth 2003-2007)

111

38

24

5.8

5.0

3.4

3.3

3.1

2.0

2.0

21

4.0

0 50 100 150 200 250 300

Emerging Markets

India

Russia

South Africa

Mexico

Indonesia

bn USD (real at 2002 prices)

Premium volume 2002 Additional premium volume 2002-2007

Source: National insurance authorities, Swiss Re Economic Research & Consulting.

Table 4.4: Top 10 countries in non- life insurance (emerging markets)

Non-life insurance

2007 premium volume

(in USD milllion)

Share of emerging

markets

China 33,810 17.00 percent

Russia 28,973 14.60 percent

Brazil 20,501 10.30 percent

Mexico 9,763 4.90 percent

South Africa 8,345 4.20 percent

Poland 7,677 3.90 percent

India 7,402 3.70 percent

Turkey 7,201 3.60 percent

Venezuela 6,977 3.50 percent

Argentina 4,471 2.20 percent

Top 10 129,619 68.00 percent

Source: Insurance Information Bureau, IRDA

95

4.2 Overview of Indian healthcare system

The trends in the health insurance market are governed by multiple factors, one of which is

the nature and type of healthcare system existing in the given geography. For example, if the

healthcare system promotes out of pocket expenditures then there would be a large

percentage of population which would depend on private healthcare providers for their

medical needs. This will lead to higher demands for the private care and thus the cost of care

would increase must faster. A point will come when the healthcare cost would be so high

that it would become difficult for an average individual to afford health care cost. It will be

then that the health insurance companies would come into play and would try to apply the

principle of risk pooling and principle of large numbers. On the other side they would also

make efforts to bring down the cost of healthcare expenditure by contracting with healthcare

providers for better rates and also by monitoring the cost closely. Thus, it is important to

study the overview of the Indian healthcare system in context of the trends in the Indian

health insurance industry.

4.2.1 Determinants of Health

Before looking into the Indian healthcare system let‘s briefly examine the determinants of

health. As per World Health Organization a child born in a developing country is ten to

fifteen times more likely to die before reaching his first birthday than a child born in a

developed country. Similarly, the individual may expect to live up to fifty years compared to

eighty years in some developed countries. There has been this observation that during World

War II fighting in the same area in similar conditions more European soldiers developed

jaundice (Hepatitis A) as compared to Indian soldiers. So what determines whether a person

will fall ill or die? It is just being born or living in a particular geographical area or more

than that? Obviously it‘s more than that. Health is a multifactorial amalgamation of various

determinants. Some of the important determinants of health are examined and then linked

with the cover extended under health insurance policy. This determinant includes genetic,

environmental, socio-cultural, economic, health services, political system and technological

advancements. A brief description of these determinants is presented below.

96

4.2.1.1 Genetic- The positive health advocated by WHO implies that a person should be able

to express as completely as possible the potentialities of his genetic heritage. The

genetic makeup of each individual is unique and cannot be altered after conception.

The genetic constitution determines the health status to a great extent. It is may be

due to this reason that there are specific exclusions with respect to congenital illness

(both internal and external) in most of the health insurance policy. Now, the question

arises if the health insurance firms should be allowed to exclude any genetic

conditions in a person or not? The answer is not an easy one and one need to examine

this on a case to case basis and in lack of any specific regulations the decision

becomes more difficult.

4.2.1.2 Environmental- Environment may be internal or external. Internal environment is

dealt with by internal medicine. The external environment involves all that is external

to the individual. The external environment factors range from housing, water supply,

family structure and occupation. In health insurance the internal environment is

covered quite fairly. The only clause is that of hospitalization i.e. the insured need to

be hospitalized for a minimum of twenty four hours. However, there are few

exceptions where day care surgeries are covered due to advancement in medical

technology.

4.2.1.3 Socio-cultural- Social interactions with parents, peer groups, friends and siblings are

through school and mass media affects the life-style of individuals. Personal habits

like smoking, alcohol intake, drug abuse are developed through social interactions.

Obesity, drug addictions are few examples of medical problems resulting from social

causes. Life style can have a positive effect on health. Reduction of smoking,

avoiding red meat, regular exercise all contribute to a healthy life style. In health

insurance underwriting all these factors are kept in mind to measure the potential risk

of health and based on the life style of the individual necessary discounts or loading

is done in the base premium. Now a day‘s one can find that most of the health insurer

are focusing on the lifestyle of the customers and trying to bring positive health

outcomes by extending memberships to health clubs and exercise centers.

97

4.2.1.4 Economic- Economic performance is the major factor in reducing morbidity,

increasing and improving life expectancy. Economic status determines the

purchasing power, quality of life, family size and disease pattern. It is one of the

crucial factors which determine which determine health seeking behavior. We have

seen in India how the central and state governments fund the health insurance

schemes for the poor who does not have the purchasing power.

4.2.1.5 Health Services- The health services must be equitably distributed, affordable and

socially acceptable. The health services can be offered at the primary, secondary and

tertiary level. It can also be bifurcated in terms of public and private space. From

health insurance perspective it is important to ensure that there is synergy between

the offering of the public and the private healthcare providers i.e. in places where

there is no public infrastructure; health insurance can be used as a mechanism to

deploy funds for the development of private health care services. This could be

practically seen in districts where RSBY policy has been launched.

4.2.1.6 Political System- The percentage of Gross National Product (GNP) spent on health is

a quantitative indicator of political commitment. To achieve the goal of health for all,

WHO has set the target of at least 5 percent expenditure of each country‘s GNP on

health care. India spends 3 percent of its GNP on health care. In addition to this it is

the political system which decides the investment of funds by the foreign players into

insurance sector. Currently, the FDI cap is of 26 percent in any insurance company.

However, the bill to raise the FDI limit to 49 percent is on its way and should be

passed given the current diplomatic pressures from the developed countries like US.

4.2.1.7 Technological advancements- There are many who suggest that improvement in

technology has lead to better health care outcomes. Whether, the health care cost has

risen or not due to technological advancement is not clearly know. In health

insurance this determinant is used to extend benefits to the customer by covering day

care treatments i.e. medical treatment and or surgical procedure which is undertaken

under general or local anesthesia in a hospital or a day care center in less 24 hours

because of technological advancement.

98

Thus we have seen that there are multiple determinants on one‘s health and how each one of

them is linked with the health insurance industry. Now, the overview of the Indian health

care system followed by healthcare financing is presented.

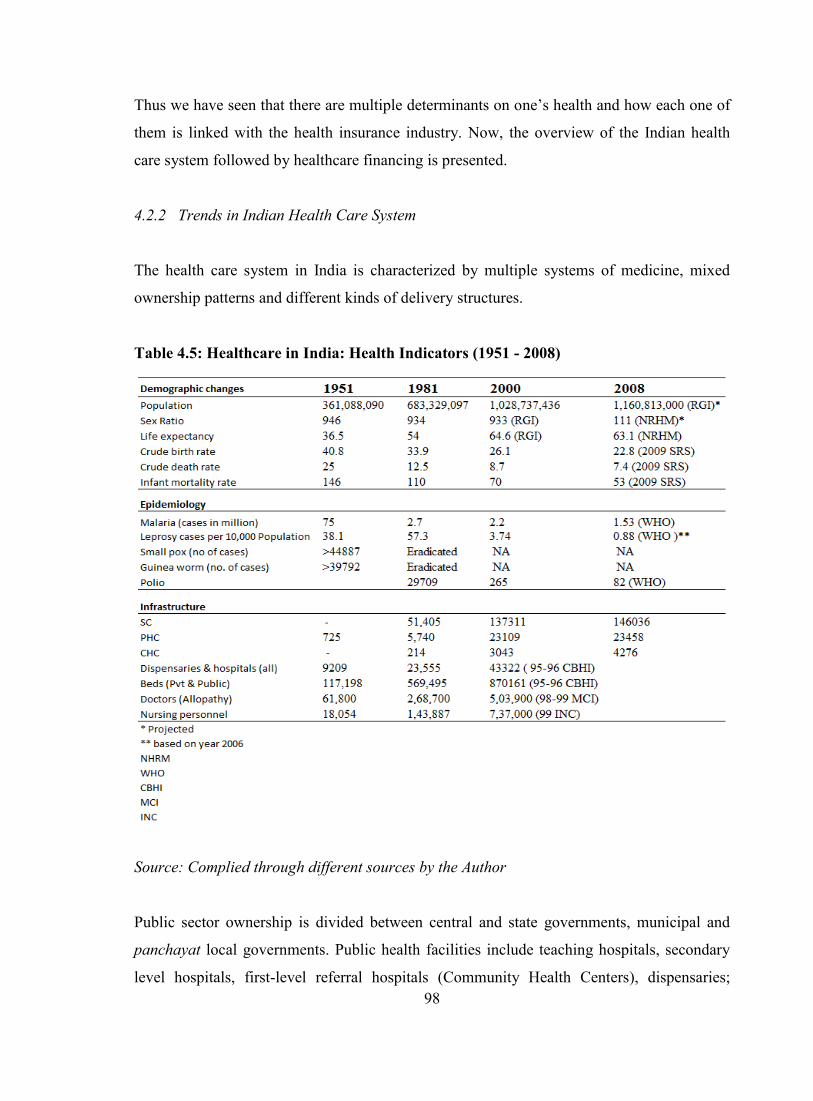

4.2.2 Trends in Indian Health Care System

The health care system in India is characterized by multiple systems of medicine, mixed

ownership patterns and different kinds of delivery structures.

Table 4.5: Healthcare in India: Health Indicators (1951 - 2008)

Source: Complied through different sources by the Author

Public sector ownership is divided between central and state governments, municipal and

panchayat local governments. Public health facilities include teaching hospitals, secondary

level hospitals, first-level referral hospitals (Community Health Centers), dispensaries;

99

Primary Health Centres (PHCs), Sub-Centres, and health posts. Also included are public

facilities for selected occupational groups like organized work force (ESI), defence,

government employees (CGHS), railways, post and telegraph and mines among others. The

private sector (for profit and not for profit) is the dominant sector with 50 percent of people

seeking indoor care and around 60 to 70 percent of those seeking ambulatory care (or

outpatient care) from private health facilities. While India has made significant gains in

terms of health indicators - demographic, infrastructural and epidemiological (see Table 4.5)

it continues to grapple with newer challenges.

The country is now in the midst of a dual disease burden of communicable and non-

communicable diseases. This is coupled with spiraling health costs, high financial burden on

the poor and erosion in their incomes. Around 24 percent of all people hospitalized in India

in a single year fall below the poverty line due to hospitalization. An analysis of financing of

hospitalization shows that large proportion of people; especially those in the bottom four

income quintiles borrow money or sell assets to pay for hospitalization25

. This situation

exists in a scenario where health care is financed through general tax revenue, community

financing, out of pocket payment and social and private health insurance schemes. India

spends about 4.9 percent of GDP on health26

.The total health expenditure in India is around

5 percent of GDP, with breakdown of public expenditure (0.9 percent); private expenditure

(4.0 percent). The private expenditure can be further classified as out-of-pocket (OOP)

expenditure (3.6 percent) and employees/community financing (0.4 percent). It is evident

that public health investment has been comparatively low. In fact as a percentage of GDP it

has declined from 1.3 percent in 1990 to 0.9 percent in 2010. Furthermore, the central

budgetary allocation for health (as a percentage of the total Central budget) has been

stagnant at 1.3 percent while in the states it has declined from 7.0 percent to 5.5 percent. In

light of the fiscal crisis facing the government at both central and state levels, in the form of

shrinking public health budgets, escalating health care costs coupled with demand for health-

care services, and lack of easy access of people from the low-income group to quality health

25

World Bank Report, 2002

26 World Health Report- India, 2002.

100

care, health insurance is emerging as an alternative mechanism for financing of health care in

India.

A population pyramid, also called an age structure diagram, is a graphical illustration that

shows the distribution of various age groups in a human population (typically that of a

country or region of the world), which ideally forms the shape of a pyramid when the region

is healthy. A great deal of information about the population broken down by age and sex can

be read from a population pyramid, and this can shed light on the extent of development and

other aspects of the population. A population pyramid also tells how many people of each

age range live in the area. There tends to be more females than males in the older age groups,

due to females' longer life expectancy. Figure 4.2, 4.3 and 4.4 depicts the population

pyramid by broad age-group, projected population pyramid 2001 and 2026 of India. In India

the demographic transition27

has been relatively slow but steady. As a result the country was

able to avoid adverse effects of too rapid changes in the number and age structure of the

population on social and economic development. In the period between1996 to 2016,

population in the age group greater than 60 yrs will increase from 62.3 to 112.9 million28

.

Figure 4.2: Percentage of population by broad age-groups: India 2001-2026

Source: Office of the Registrar General and Census Commissioner, India.

27 Demographic transition is the transition from a stable population with high mortality and fertility to

a stable population with low mortality and fertility. During the transition population growth and

changes in the age structure of the population are inevitable.

28 Source: Technical Group on Population Projections, Registrar General of India (RGI) 1996

101

Figure 4.3: Projected population Pyramid: India-2001

Source: Office of the Registrar General and Census Commissioner, India.

Figure 4.4: Projected population Pyramid: India-2026

Source: Office of the Registrar General and Census Commissioner, India.

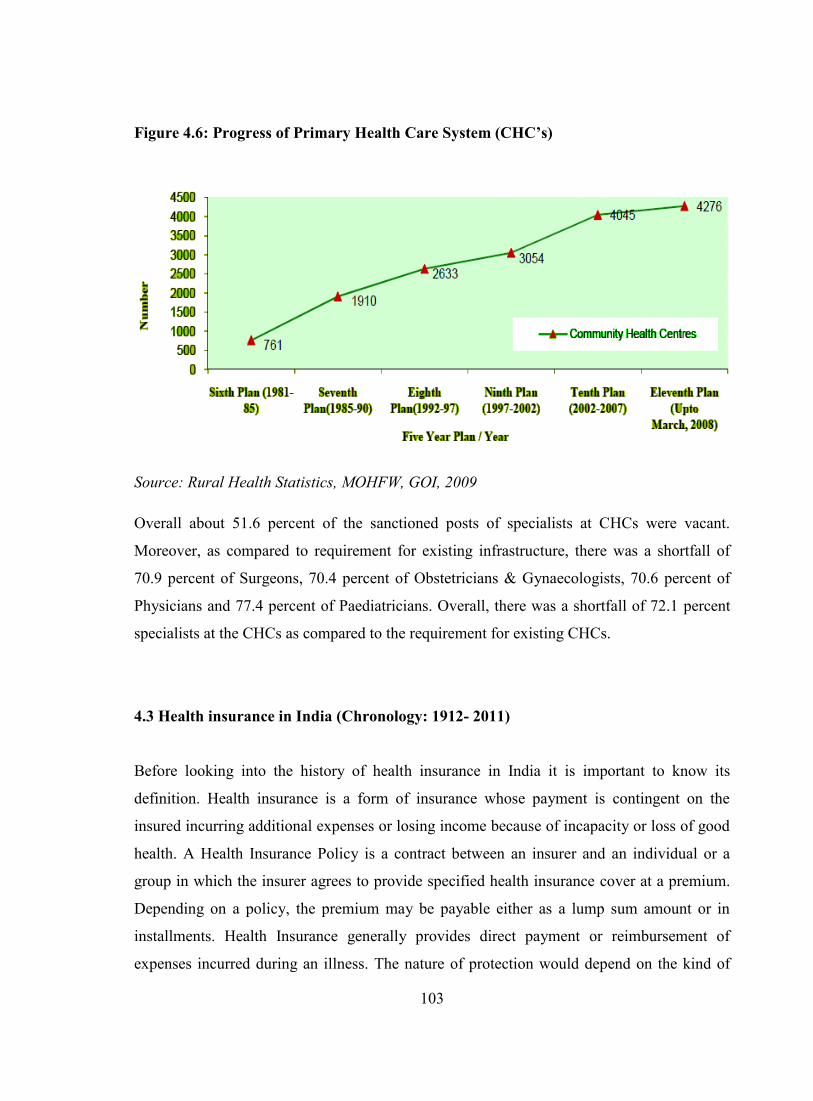

The Primary Health Care Infrastructure has been developed as a three tier system with Sub

Centre, PHC and CHC being the three pillars of Primary Health Care System. Progress of

Sub Centres, which is the most peripheral contact point between the Primary Health Care

102

System and the community, is a prerequisite for the overall progress of the entire system. A

look at the number of Sub Centres functioning over the years reveal that at the end of the

Sixth Plan (1981-85) there were 84,376 Sub Centres. The figure rose to 1, 30,165 at the end

of Seventh Plan (1985-90) and to 1, 45,272 at the end of Tenth Plan (2002-2007). As on

March, 2008 there were 1, 46,036 Sub Centres functioning in the country.

Figure 4.5: Progress of Primary Health Care System (PHC’s)

Source: Rural Health Statistics, MOHFW, GOI, 2009

Similar progress can be seen in the number of PHCs which was 9115 at the end of Sixth plan

(1981-85) and the figure almost doubled to 18671 at the end of Seventh Plan (1985-90) and

rose to 22370 at the end of Tenth Plan (2002-2007). As on March, 2008, there are 23458

PHCs functioning in the country (Figure 4.5). In accordance with the progress in the number

of SCs and PHCs, the number of CHCs has also increased from 761 at the end of Sixth Plan

(1981-85) to 1910 at the end of Seventh Plan (1985-90) and 4045 at the end of Tenth Plan

(2002-2007). As on March, 2008 there were 4276 CHCs functioning (Figure 4.6). According

to the figures of population based on 2001 Population Census, the shortfall in the rural health

infrastructure comes out to be of 20486 Sub Centres, 4477 PHCs and 2337 CHCs, ignoring

surplus in some States / UTs. The current position of specialists manpower at CHCs reveal

that as on March, 2008, out of the sanctioned posts, 55.3 percent of Surgeons, 48.2 percent

of Obstetricians & Gynaecologists, 54.5 percent of Physicians and about 47.2 percent of

Paediatricians were vacant.

103

Figure 4.6: Progress of Primary Health Care System (CHC’s)

Source: Rural Health Statistics, MOHFW, GOI, 2009

Overall about 51.6 percent of the sanctioned posts of specialists at CHCs were vacant.

Moreover, as compared to requirement for existing infrastructure, there was a shortfall of

70.9 percent of Surgeons, 70.4 percent of Obstetricians & Gynaecologists, 70.6 percent of

Physicians and 77.4 percent of Paediatricians. Overall, there was a shortfall of 72.1 percent

specialists at the CHCs as compared to the requirement for existing CHCs.

4.3 Health insurance in India (Chronology: 1912- 2011)

Before looking into the history of health insurance in India it is important to know its

definition. Health insurance is a form of insurance whose payment is contingent on the

insured incurring additional expenses or losing income because of incapacity or loss of good

health. A Health Insurance Policy is a contract between an insurer and an individual or a

group in which the insurer agrees to provide specified health insurance cover at a premium.

Depending on a policy, the premium may be payable either as a lump sum amount or in

installments. Health Insurance generally provides direct payment or reimbursement of

expenses incurred during an illness. The nature of protection would depend on the kind of

104

policy purchased and the cost and range of protection under that policy. Health insurance

could be either a personal scheme or a group scheme sponsored by an employer. Unlike life

insurance where there are only two parties i.e. the insured and the insurer, in the case of

health insurance there are three parties namely the insured, the insurer and the provider

(network hospital). There is also TPA which acts as an extended arm of the insurance

company and helps in claim processing, managing the hospital networks and at times helping

in enrollment of customers.

The generic features of insurance are equally applicable to the concept of health insurance.

Insurance primarily rests on the principle of pooling of risk associated with the same cause

i.e. health to share losses on some equitable basis. Insurance‘ whether it is health or any

other line of insurance, is a concept of sharing financial burden. Insurance follows a simple

statistical principle of ―diversity‖ or ―pooling of resources and sharing of risk‖. This means

that from out of a given population that is Insured, those needing the financial support by

way of a claim for loss is very small. Especially in the case of Health Insurance, it is less

than 5 percent of the total population covered in its current form. This in effect means that

out of the amount contributed by 100percent, financial claims are paid to only 5 percent.

This theory of diversity is an important factor in a country like India.

Thus, health insurance in a narrow sense would be ‗an individual or group purchasing health

care coverage in advance by paying a fee called premium.‘ In its broader sense, it would be

any arrangement that helps to defer, delay, reduce or altogether avoid payment for health

care incurred by individuals and households.

Taking into account various developments in and outside the insurance sector, showcasing

the developments in the field of insurance, including developments specific to health

insurance, with brief summaries are given in chronological order (see Table 4.6).

105

Table 4.6: Health insurance in India (Chronology: 1912- 2011)

YEAR Important Developments (Pre - Privatization)

1912 Insurance Act, 1912 passed, setting down rules and regulations specific to

insurance industry.

1923 Workman‘s Compensation Act passed, aims to provide workmen and/or

dependents some relief in case of accidents arising out of or in the course of

employment, causing death or disablement

1938 Insurance Act, 1938 passed, recognizing two categories, i.e. Life and non-

life (general) insurance. Led to an insurance wing being set-up, attached to

the Ministry of Finance.

1948 Employee‘s State Insurance (ESI) Act passed, providing protection to

workers & dependents in the organized sector for sickness, maternity, death

1954 The Central Government Health Scheme started in 1954, providing health

cover to employees of Central Government, MPs, Judges, Freedom Fighters

and their families.

1956 Life Insurance industry nationalized and Life Insurance Corporation of

India (LIC) set up subsequently.

1959 Mudaliar Committee constituted, recommended provision of long-range

health insurance policy for all and strengthening Primary Health Centers.

1972 General Insurance industry nationalized

1986 General Insurance Corporation of India (GIC) introduced mediclaim

insurance policy

1999 Insurance Regulatory and Development Authority (IRDA) Act passed

2000 W.e.f. Dec 2000, GIC became the National Re-insurer, its earlier role of co-

ordination between the four subsidiaries taken over by a new body, General

Insurance (Public Sector Companies) Association (GIPSA).

106

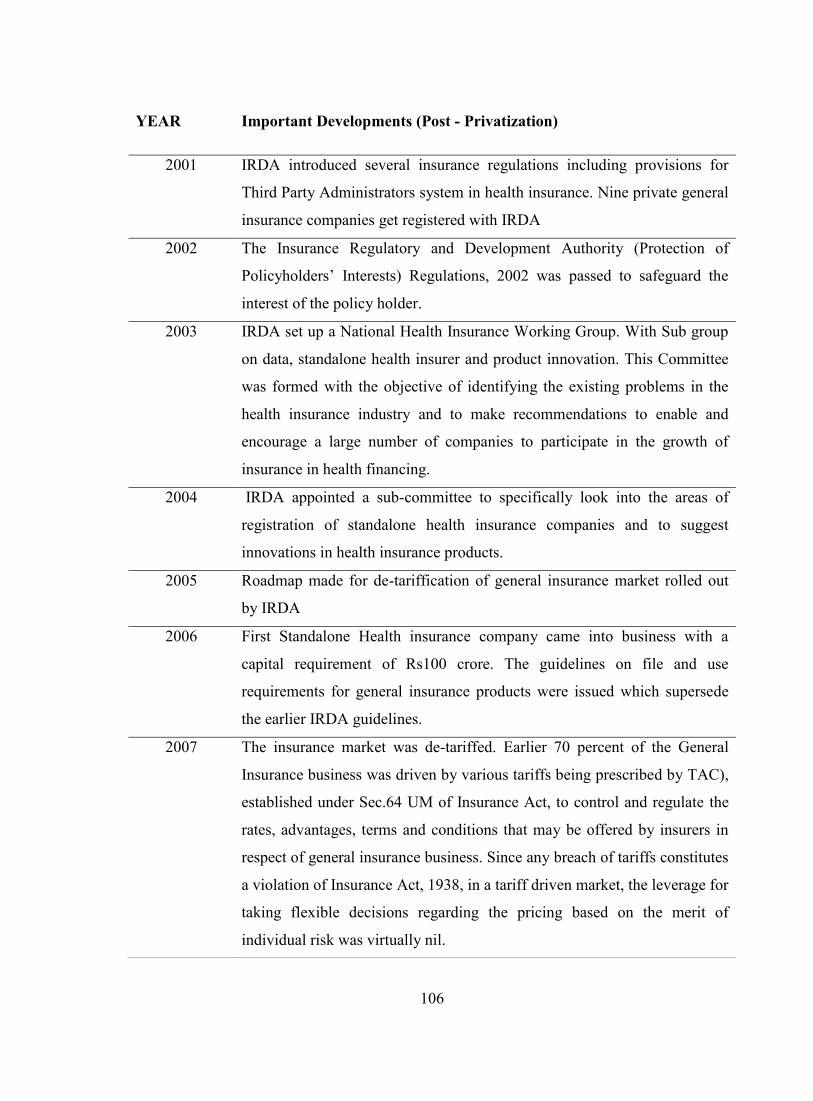

YEAR Important Developments (Post - Privatization)

2001 IRDA introduced several insurance regulations including provisions for

Third Party Administrators system in health insurance. Nine private general

insurance companies get registered with IRDA

2002 The Insurance Regulatory and Development Authority (Protection of

Policyholders‘ Interests) Regulations, 2002 was passed to safeguard the

interest of the policy holder.

2003 IRDA set up a National Health Insurance Working Group. With Sub group

on data, standalone health insurer and product innovation. This Committee

was formed with the objective of identifying the existing problems in the

health insurance industry and to make recommendations to enable and

encourage a large number of companies to participate in the growth of

insurance in health financing.

2004 IRDA appointed a sub-committee to specifically look into the areas of

registration of standalone health insurance companies and to suggest

innovations in health insurance products.

2005 Roadmap made for de-tariffication of general insurance market rolled out

by IRDA

2006 First Standalone Health insurance company came into business with a

capital requirement of Rs100 crore. The guidelines on file and use

requirements for general insurance products were issued which supersede

the earlier IRDA guidelines.

2007 The insurance market was de-tariffed. Earlier 70 percent of the General

Insurance business was driven by various tariffs being prescribed by TAC),

established under Sec.64 UM of Insurance Act, to control and regulate the

rates, advantages, terms and conditions that may be offered by insurers in

respect of general insurance business. Since any breach of tariffs constitutes

a violation of Insurance Act, 1938, in a tariff driven market, the leverage for

taking flexible decisions regarding the pricing based on the merit of

individual risk was virtually nil.

107

General insurance as a whole, developed with the industrial revolution in the West and with

the consequent growth of seafaring trade and commerce in the seventh century. In India too,

evidence of insurance in some form can be traced as early as from the Aryan period. The

British and some of the other foreign insurance companies through their agencies transacted

insurance business in India. The first general insurance company in India was the Triton

Insurance company Ltd., established in Calcutta in 1850 AD, with the British holding major

2008 Insurance Information bureau set up by IRDA (primarily working on Health

and motor data). General insurance Council for the first time defined the

"Pre-existing" clause and made it standard across the industry.

2009 The Renewability of Health insurance policies circular issued on 31st

March 2009 advises non-life insurers not to generally decline renewals

except for certain specified reasons. Detailed instructions on Health

Insurance for Senior Citizens stipulate that all health insurance products

filed on or after 1st July, 2009 must allow entry up to 65 years of age, and

also to make adequate dissemination of product information on websites.

Also, the FICCI report on Health Insurance released in July 2009 includes

Standard Treatment Guidelines for 21 common causes of hospitalization.

2010 The Preferred Provider Network (PPN) of hospitals introduced in July 2010

to offer cashless medical treatment following the initiative taken by the four

pubic insurers to bring discipline on the pricing of hospital services. The

health insurance market continues to be dominated by the four state-owned

general insurers, which together accounted for almost 60 percent of the

premiums.

2011 A key development was the announcement of portability of health

insurance policies by IRDA. The regulator has issued guidelines for the

arrangement to be effective from 1 July 2011, which will allow

policyholders to switch providers on the same policy terms, particularly

without losing the credit gained for pre-existing conditions in terms of

waiting period. Circular on ―De-Listing of Hospitals‖ and guidelines on

―Distance Marketing‖ also rolled out.

108

share. The first general insurance company by Indian promoters was the Indian Mercantile

Insurance company Ltd. started in Bombay in 1906-07.

Following the First World War, several foreign insurance companies started insurance

business in India, capturing about 40 percent of the insurance market in India at the time of

Independence. It was in the year 1912 that the ―insurance Act‖ was passed which was then

revised in the year 1932. This was under the revised Act that the Life and Non-life categories

were recognized. In India the general insurance is also known as ―Non-life‖. The health

insurance was a part of the non-life business; however, there was no clear demarcation then.

Even today both the life and the non-life companies are allowed to have health insurance

products.

The year 1940-1960 has witnessed the launch of the ESI and the CGHS schemes. These

schemes had the elements of health insurance concepts but were not placed with any

insurer29

.

In the year 1971, the government by an ordinance nationalized the general insurance

business, under the General insurance Nationalization Act, 1972 to ensure orderly and

healthy growth of the business. The then existing 107 companies were brought under the

aegis of GIC of India and were merged with the four public general insurance players

namely the National insurance company, the Oriental insurance company, the United

insurance company and the New India assurance company. These four public insurance

companies were distributed geographically and had their head offices at Kolkata, New-Delhi,

Chennai and Mumbai respectively. The primary reason for such division was to have wider

spread with regional focus. It was expected that the subsidiary companies would provide

effective competition to each other with the support from GIC. The GIC facilitated

coordination, competition and laid down standards for market conduct, customer service and

development of the market.

29

The current study excludes these two schemes as it would be a separate independent research area

in itself.

109

In 1973 the general insurance industry was nationalized and with the liberalization of the

market, the four public players became autonomous and were directly answerable to the

Ministry of Finance as their owner. The General Insurance Corporation of India was

designated as the Indian Re-insurer.

In 1981, the Apex Body of Public Sector Insurance Companies i.e. GIC designed a limited

cover for individuals and families for covering their hospitalization needs. This was replaced

by a mediclaim policy in the year 1986 under a market agreement to provide insurance

benefits to individuals and groups under a group mediclaim policy. The then ‗Mediclaim‘

Insurance Policy provided reimbursement of medical expenses for hospitalization and

domiciliary hospitalization, but it does not cover OPD treatment. The sum that is assured

under this policy varies from Rs.15, 000 to Rs.5 lac. It was available to the people from the

age of 5 years to the age of 80 years. The children between the age of 3 months and 5 years

were covered with some additional premium. The minimum premium was Rs. 213 per

annum for the lowest sum assured, that is, Rs. 15,000 (for people below 35 years of age).

The highest premium was Rs. 17,156 per annum for people in the age group between 76

years and 80 years for the maximum sum assured, that is, up to Rs. 5 lac. There was a family

discount of 10 percent and some cumulative bonus if the previous year had been claim-free.

The scheme so introduced was modified in 1991 and 1996 in the light of experience and

suggestions received from the insuring public and medical fraternity. The benefit that was

provided under the mediclaim policy was on reimbursement basis only. Reimbursement of

the expenses was allowed by insurance companies on production of the required bills given

by the hospitals where the treatment was taken. This created the need for cashless payment

facility at hospitals, as it was difficult for an insured person to arrange for funds at the time

of admission in the hospital. Requests were made to GIC for introducing a system whereby,

payment could be made directly by the insurance company to the hospital where the

treatment was taken. Insurance companies entered into tie up with hospitals to provide such

benefit whereby an insured person could collect a certificate of his eligibility from an

insurance company and produce the same to the hospital for taking the treatment. The

settlement of the claims was directly made with the hospitals. This tie up with hospitals

failed in course of time in view of some reported cases wherein the hospital managed to get

110

claims reimbursement of such insured persons who took treatment for pre-existing

ailments30

.

As a part of the financial reforms in the year 1993 the Government of India appointed a

committee know as Malhotra Committee on reforms in the insurance sector. This committee

rightly recommended the opening up of insurance sector to competition stating that

introduction of competition will result in better customer service and new products. As the

insurance market was open in the year 2001, there were nine new entrants. Up to June 2011

there were 48 insurance companies licensed by IRDA and doing business in India (24 life

insurance companies and 24 non-life insurance companies and within non-life, there were

three specialist health insurance companies).

4.4 Major players and Performance

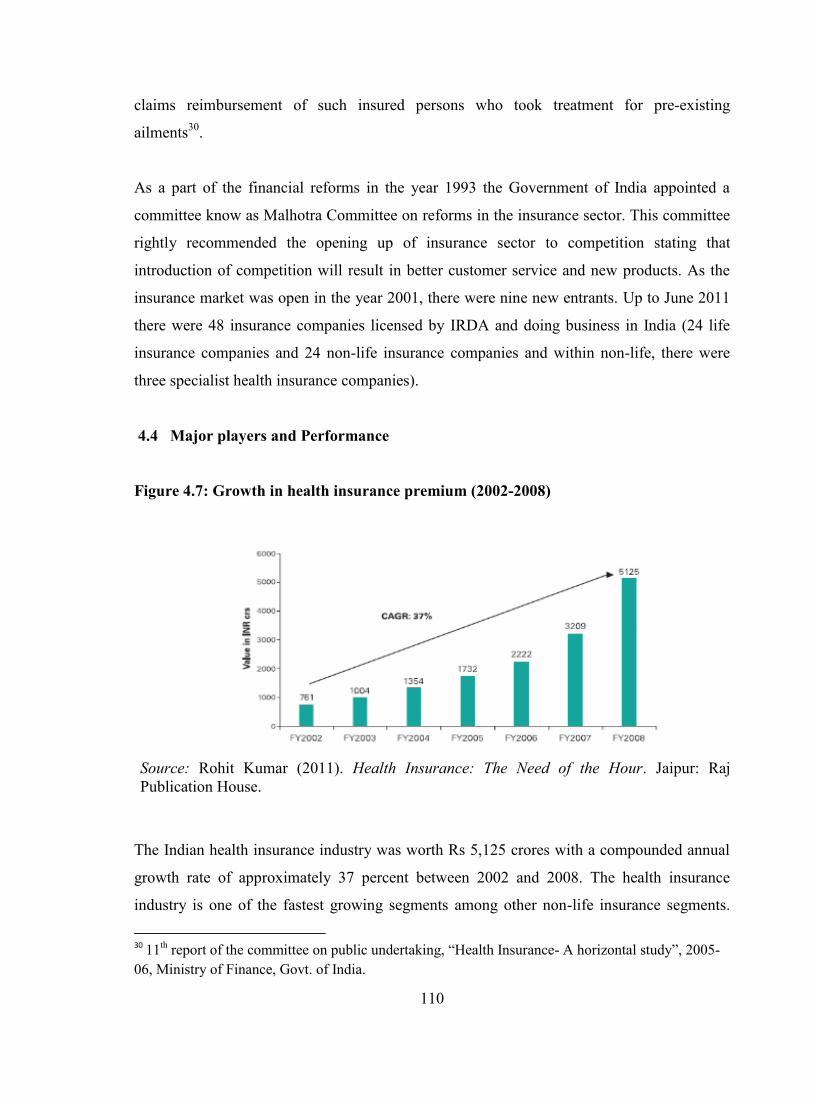

Figure 4.7: Growth in health insurance premium (2002-2008)

Source: Rohit Kumar (2011). Health Insurance: The Need of the Hour. Jaipur: Raj

Publication House.

The Indian health insurance industry was worth Rs 5,125 crores with a compounded annual

growth rate of approximately 37 percent between 2002 and 2008. The health insurance

industry is one of the fastest growing segments among other non-life insurance segments.

30

11th report of the committee on public undertaking, ―Health Insurance- A horizontal study‖, 2005-

06, Ministry of Finance, Govt. of India.

111

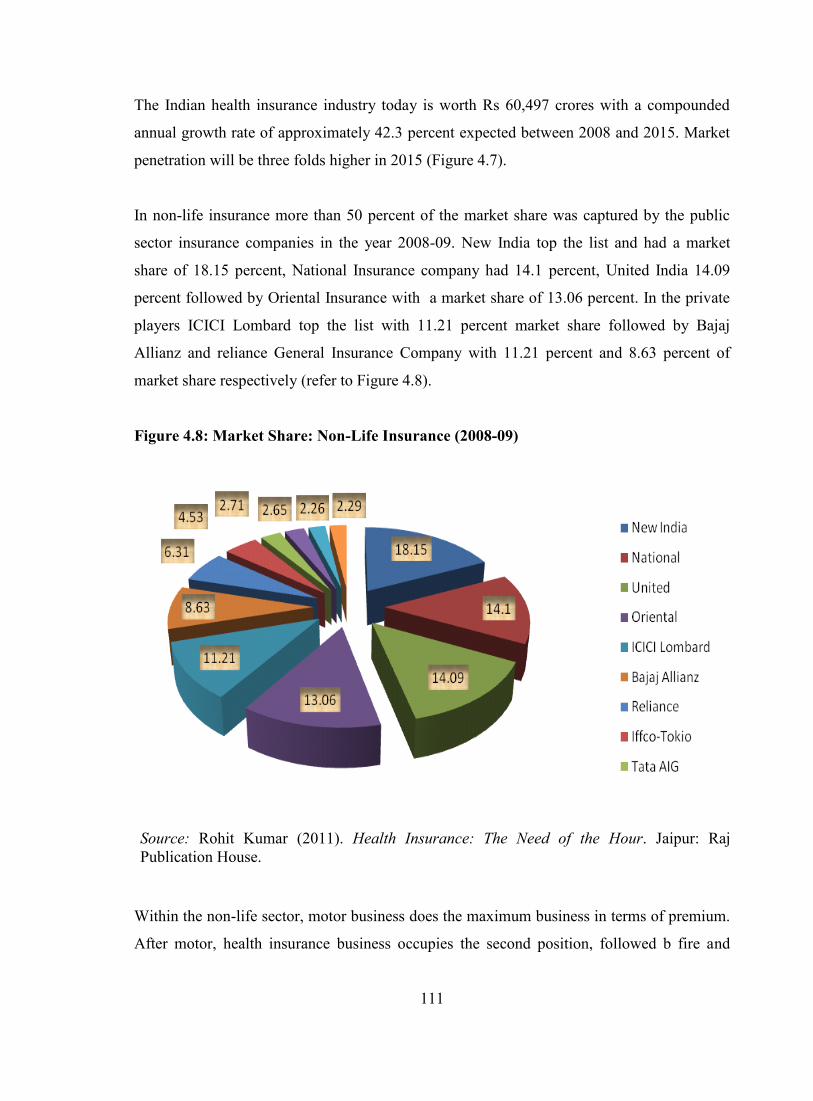

The Indian health insurance industry today is worth Rs 60,497 crores with a compounded

annual growth rate of approximately 42.3 percent expected between 2008 and 2015. Market

penetration will be three folds higher in 2015 (Figure 4.7).

In non-life insurance more than 50 percent of the market share was captured by the public

sector insurance companies in the year 2008-09. New India top the list and had a market

share of 18.15 percent, National Insurance company had 14.1 percent, United India 14.09

percent followed by Oriental Insurance with a market share of 13.06 percent. In the private

players ICICI Lombard top the list with 11.21 percent market share followed by Bajaj

Allianz and reliance General Insurance Company with 11.21 percent and 8.63 percent of

market share respectively (refer to Figure 4.8).

Figure 4.8: Market Share: Non-Life Insurance (2008-09)

Source: Rohit Kumar (2011). Health Insurance: The Need of the Hour. Jaipur: Raj

Publication House.

Within the non-life sector, motor business does the maximum business in terms of premium.

After motor, health insurance business occupies the second position, followed b fire and

112

marine business. Across all these segments from 2007-08 to 2008-09 health insurance has

seen the maximum growth (refer Figure 4.9).

Figure 4.9: Non-Life insurance company- segment wise premium (2007and 2009)

Source: Rohit Kumar (2011). Health Insurance: The Need of the Hour. Jaipur: Raj

Publication House.

Figure 4.10: Market Share- Health Insurance (Earned premium 2008-09)

Source: Rohit Kumar, K. Rangarajan, and Nagarajan Ranganathan (2011). ―Health Insurance

in India—A Study of Provider‘s Perceptions in Delhi & the NCR,‖ Journal of Health

Management 13: 259-277.

113

Again in health insurance business the public sector insurance companies had more than 50

percent of the market share, measured in terms of earned premium (year 2008-09). However,

there was a difference in the ranking of public and private sector companies. The third rank

was occupied by ICICI Lombard. One of the interesting observations was that Star Health

insurance company (the first standalone health insurance company in India) had captured 11

percent of the overall market share (Figure 4.10). Thus, one can argue that standalone health

insurance companies are going to increase the level of competition within the health

insurance market and are here to stay.

On examining the latest data on market share for the period April-May 2011 it was observed

that ICIC Lombard had 29 percent of the market share, Star Health had 23 percent of the

market share followed by HDFC Ergo (9 percent), Royal Subdram (6 percent), Reliance

General (5 percent), IFFICO Tokio and Apollo Munich (4 percent each). Here, it is

interesting to note that the three standalone insurance companies captured some 28 percent

of the market share within the private insurance space (Figure 4.11). The customer segment

wise premium data is currently not available. However, the regulator had asked the insurers

and TPA‘s to start providing the health data on the basis of customer segment i.e retail,

corporate and mass business.

In the area of retail health product it was found that different levels of cover are being

offered by different insurance companies. In most of the cases the pre-existing disease was

not covered before fourth year from policy inception date (see table 4.7). It was also

observed that there were co-payment and sub-limit options being built-in in the product. This

may be primarily because to reduce the claim paid cost and also to offer retail health

insurance policy at a lower price.

The incurred claim ratio for both private and public sector companies for three consecutive

years i.e. 2006-07 to 2008-09 is presented in table 4.8. It was observed that the claim ratio

for public sector insurance companies was 20 to 15 percent higher than that of the private

players. One of the possible reasons for this difference could be because the public sector

insurance companies might be offering the health insurance product at a lower price to

corporate houses. In other words the public sector insurance companies might be subsidizing

the health insurance premium in lieu of premium received on other insurance product like

fire and marine business.

114

Figure 4.11: Market Share (Health Insurance) - Private Players (April -May -2011)

Source: Insurance Information Bureau, IRDA.

Table 4.7: Retail health insurance product- Market Comparison

Market Comparison (Retail policy)

Cover IL Bajaj Chola OIC Ntn'l Star

Hosp √ √ √ √ √ √Pre 30 60 60 30 30 30

Post 60 90 90 60 60

7% of hosp bill

max 7k

PED 5th 5th No NA 4th No

30 day √ √ √ √ √ √Named ailments 2 yrs 2 yrs 1 yr 2 yr 2 yr 1yr/ 2yr

Co-pay

We pay

full claims

10% co-

pay in non-

n/w

hospitals

10% for

Diab/Hyp &

25% if both.

Sub-limits

Only in

case of

cataract

Hernia/pile

s/cataratc

etc 10% of

SI

Room

Rent 1%

of SI, ICU

2% of SI

Room Rent

2% of SI max

4k

Two Year √SI 2L-4L 1L-10L 1L-10L 1L-5L 1L-5L

Entry Age 60 55 55/69 (for dependant parents)60 60 1L-5L

IL- ICICI Lombard, OIC- Oriental Insurance, Ntn‟l- National Insurance

Source: Author‟s compilation based on the study of the retails products (2009-10) offered by

selected insurance companies.

115

Table 4.8: Incurred Claim Ratio (2006-07 to 2009)

INCURRED CLAIMS RATIO (Percent)

YEAR 2008-09 2007-08 2006-07

PUBLIC 116.60 112.36 157.79

NEW INDIA 107.41 89.88 212.81

ORIENTAL 136.96 123.77 132.51

NATIONAL 111.27 118.01 131.47

UNITED 121.27 135.36 160.05

PRIVATE 85.33 94.81 103.42

ROYAL SUNDARAM 43.57 44.78 46.99

BAJAJ ALLIANZ 78.02 85.19 78.64

TATA AIG 46.71 74.93 61.69

RELIANCE 91.74 112.14 113.01

IFFCO TOKIO 122.23 121.14 152.89

ICICI LOMBARD 86.07 98.79 118.70

CHOLAMANDALAM 108.99 93.03 79.51

HDFC CHUBB 100.5 142.46 87.10

FUTURE GENERALI 141.12 Na Na

GRAND TOTAL 105.95 106.99 141.02

Source: Insurance Information Bureau, IRDA

However, subsidizing should get minimized due to de-tariffication of the general insurance

industry recently. The claim ratio for the public sector has shown improvement. From more

than 100 percent in 2006-07 it has come down to 85.33 percent. However, including both

public and private players the claim ratio is still more than 100 percent i.e. for 2008-09 it

was standing at 105.95 percent.

116

4.5 Current opportunities and threats

Insurance company today find themselves surrounded by a variety of challenges as they

work towards profitable growth and to compete in this dynamic industry. Across the industry

the insurance companies faces common challenges. The opportunity and threats includes the

following:

4.5.1 Governance and risk management: The record losses from Hurricanes Katrina,

Wilma and Rita have once again highlighted the scale of the risks faced by insurer‘s

in an increasingly complex and uncertain financial, geopolitical and climatic

environment. Model outputs are clearly critical in monitoring and controlling

aggregations and concentrations of risk. However, the largely unexpected gravity of

the losses and resulting pressure on reinsurance programmes have once again

underlined the importance of quality data, effective validation and calibration of

model outputs and, not least, the sense check of underwriting experience and

intuition. The development of Enterprise Risk Management (ERM)31

capabilities can

help to protect insurers from losses, earnings surprises and name risk and provide a

platform for strengthening governance, decision-making and regulatory compliance.

However, a recent study conducted by PricewaterhouseCoopers32

, revealed that many

insurers are finding it difficult to make headway in implementing and embedding

ERM in the face of continuing data, systems and governance challenges. However,

the study also found many examples of how insightful and effective management are

helping to overcome these technical and organizational hurdles and bring greater

clarity to insurers‘ ERM missions.

4.5.2 The growth imperative: To be succesful in the growth initiatives companies have

tried to design innovative bundles of good products and services. They have tried to

31

ERM programmes can help to safeguard businesses against losses, earnings surprises and name

risk. This includes strengthening the management of credit, market and other financial risks, along

with more effective controls over less quantifiable, though equally hazardous, non-financial risks

such as fraud, systems failure and breaches in compliance with regulatory and corporate guidelines

32 The report is available at:

http://www.pwc.com/extweb/pwcpublications.nsf/docid/2E4B06FB305460138525746C00625848.

117

cross sell by strengthening their relationship with agents and brokers and by

spreading their business in emerging markets like India and China.

4.5.3 Managing the complexities of compliance: In almost all the countries of the world the

insurance market is highly regulated. The degree may vary. Growing regulatory

requirements are bringing increased scrutiny to governance, information security,

monitoring and reporting process in insurance companies. Much of this change is

taking place in Europe by the advent of solvency II33

and in the United States with

the upcoming NIAC revised Model Audit Rule (MAR)34

. The effect of these

regulation are likely to be felt globally, as the evolving regulatory picture set the

canvas for industry best practices. There is an opportunity to use the regulatory

requirements as the catalyst to improve the overall management and build confidence

in the public eye.

4.5.4 Human Capital: Many insurers are facing mounting skills shortages. Yet, investment

in recruitment, training and career development often less than other financial

sectors. The primary focus can often be short-term demands rather than securing the

talent companies need to meet longer term strategic objectives. The effect of

demographic shifts, evolving aspirations and accelerating globalization are set to

transform the shape of the global labour market and could make it even harder for

insurers to attract and retain good people. In this competitive labour market,

33

Solvency II is the updated set of regulatory requirements for insurance firms that operate in the

European Union. It is based on economic principles for the measurement of assets and liabilities. It is

also a risk-based system as risk is measured on consistent principles and capital requirements depend

directly on this.

34 The National Association of Insurance Commissioners (NAIC) Annual Financial Reporting Model

Regulation, also known as the Model Audit Rule (MAR), requires that private insurance companies

with direct premiums written and assumed in excess of $500 million per year adopt corporate

governance and reporting standards. The Model Audit Rule, originally issued to drive consistency

across insurance regulators, was modified in 2006 and will take effect for the year ending 2010. The

new modifications within the Model Audit Rule are very similar to those of the Sarbanes-Oxley Act

of 2002 (SOX or Sarbanes-Oxley), which was issued in response to several high-profile fraudulent

financial reporting scandals at large public corporations. It was these scandals that caused there to be

a much greater emphasis placed on the accuracy of companies‘ financial statements and the method

in which they were assembled.

118

successful companies will need to develop a strategic approach to HR management

capable of anticipating and responding to evolving business needs and workforce

expectations. They will also need to identify and realize opportunities to differentiate

benefits, career development prospects and other key aspects of their employment

brand in both developed and emerging markets.

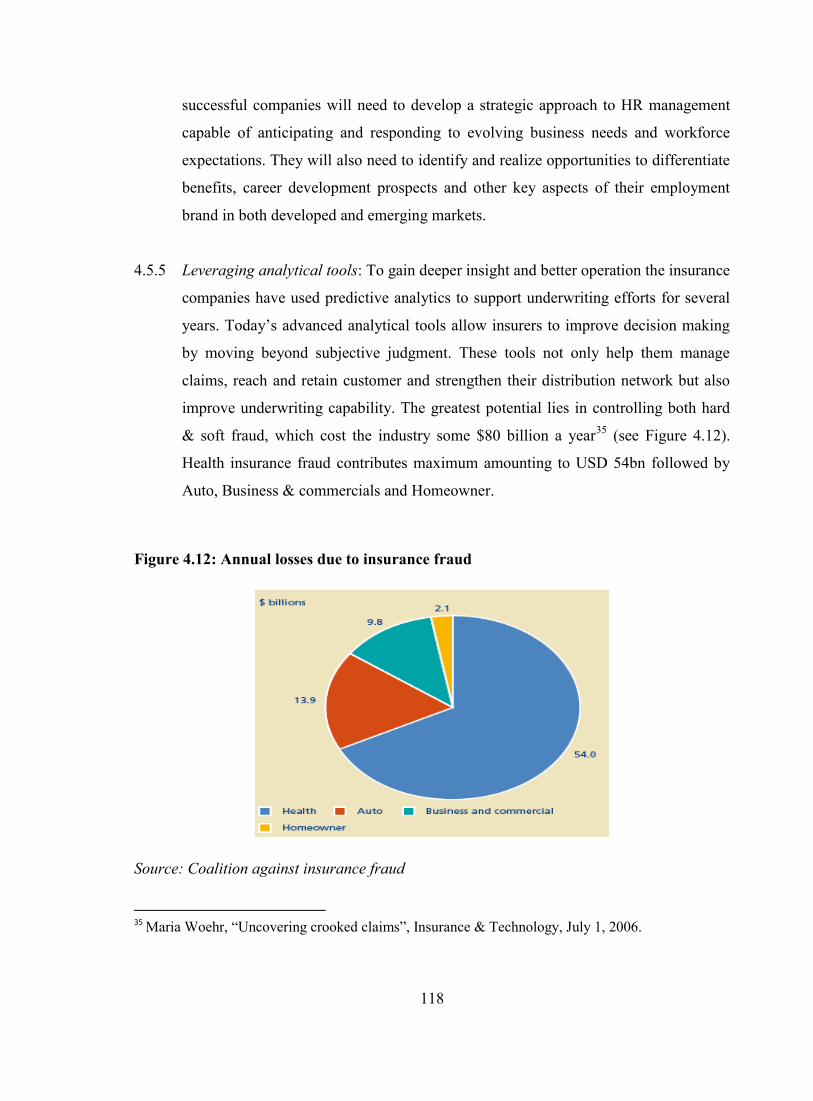

4.5.5 Leveraging analytical tools: To gain deeper insight and better operation the insurance

companies have used predictive analytics to support underwriting efforts for several

years. Today‘s advanced analytical tools allow insurers to improve decision making

by moving beyond subjective judgment. These tools not only help them manage

claims, reach and retain customer and strengthen their distribution network but also

improve underwriting capability. The greatest potential lies in controlling both hard

& soft fraud, which cost the industry some $80 billion a year35

(see Figure 4.12).

Health insurance fraud contributes maximum amounting to USD 54bn followed by

Auto, Business & commercials and Homeowner.

Figure 4.12: Annual losses due to insurance fraud

Source: Coalition against insurance fraud

35

Maria Woehr, ―Uncovering crooked claims‖, Insurance & Technology, July 1, 2006.

119

Given the above opportunities and challenges the top executives of the insurance companies

are quite optimistic about the future growth of insurance industry.

In April 2009, the Economist Intelligence Unit surveyed, on behalf of KPMG International,

315 global insurance executives from around the world. The respondents were split among

life insurance (42 percent), non-life insurance (49 percent) and reinsurance (9 percent)

companies or divisions. The Key findings of the survey were as under:

i. Over half of respondents see positive prospects for growth in the next 12 months.

ii. While respondents believe themselves to be well-capitalized, and rating themselves

highly in terms of effectiveness across most risk management activities, there is a

clear sense that a greater focus on both capital management and risk management

would be warranted.

iii. Two thirds of companies have appointed board level risk committees.

There is limited appetite for incremental spend, with almost half the respondents expecting

to improve performance without increasing resources.

The global insurance industry is bound to contribute towards the growth of world economy

and will keep evolving in the way the other financial markets have done in the past. The

study of the global insurance market reveals that there is a level of saturation reached in the

industrialized countries and the focus has moved to the emerging markets like China and

India.

4.6 Legal & regulatory aspects of health insurance

The Constitution of India has a federal structure i.e. it provides for distribution of powers

between the Union and the States. It enumerates the powers of the Parliament and State

Legislatures in three lists, namely Union list, State list and Concurrent list. As insurance is

included in the Union list, the parliament has the exclusive legislative empowerment to

regulate the insurance industry in India. Thus, the laws with reference to insurance are

uniform throughout the territories of India.

120

As we have seen earlier, the insurance industry (both life and general) has gone through the

complete cycle from being a free market, to nationalization and then again opened for private

players. The common thread connecting this cycle is the legal framework, which has also

undergone a sea change. However, The Insurance Act of 1938 along with various

amendments over the years continues till date to be the definitive piece of legislation on

insurance and controls both life insurance and general insurance.

The general insurance business was nationalized with effect from January 1, 1973, through

the introduction of the General Insurance Business (Nationalisation) Act, 1972 (―GIC Act‖).

Under the provisions of the GIC Act, the shares of the existing Indian general insurance

companies and undertakings of other existing insurers were transferred to the GIC to secure

the development of the general insurance business in India and for t he regulation and control

of such business. The GIC was established by the Central Government in accordance with

the provisions of the Companies Act, 1956 (―Companies Act‖) in November 1972 and it

commenced business on January 1, 1973. Prior to 1973, there were a hundred and seven

companies, including foreign companies, offering general insurance in India. These

companies were amalgamated and grouped into four subsidiary companies of GIC viz. the

National Insurance Company Ltd. (―National Co.‖), the New India Assurance Company Ltd.

(―New India Co.‖), the Oriental Insurance Company Ltd. (―Oriental Co.‖), and the United

India Assurance Company Ltd. (―United Co.‖). GIC undertakes mainly re-insurance

business apart from aviation insurance. The bulk of the general insurance business of fire,

marine, motor and miscellaneous insurance business is under taken by the four subsidiaries.

It was in the year 1993, the Government of India set up an eight-member committee chaired

by Mr. R. N. Malhotra (commonly called as the Malhotra Committee), a former Governor of

India's apex bank, the Reserve Bank of India to review the prevailing structure of regulation

and supervision of the insurance sector and to make recommendations for strengthening and

modernizing the regulatory system. The Committee submitted its report to the Indian

Government in January 1994. Two of the key recommendations of the Committee included

the privatization of the insurance sector by permit ting the entry of private players to enter

the business of life and general insurance and the establishment of an Insurance Regulatory

Authority.

121

The Indian Parliament passed the Insurance Regulator y and Development Act,

1999 (―IRDA Act‖) on December 2, 1999 with the aim ―to provide for the establishment of

an Authority, to protect t he interests of the policy holders, to regulate, promote and ensure

orderly growth of the insurance industry and to amend the Insurance Act, 1938, the Life

Insurance Corporation Act, 1956 and the General Insurance Business (Nationalization) Act,

1972‖.

IRDA has been entrusted with the duty to regulate, promote and ensure the orderly growth of

the insurance and re-insurance business in India. In addition to this, it has been conferred

with numerous powers and functions which include prescribing regulations on the

investments of funds by insurance companies, regulating maintenance of the margin of

solvency, adjudication of disputes between insurers and intermediaries, supervising the

functioning of the Tariff Advisory Committee, specifying the percentage of premium income

of the insurer t o finance schemes for promoting and regulating professional organizations

and specifying the percentage of life insurance business and general insurance business to be

undertaken by the insurer in the rural or social sector.

The broad regulatory framework for health insurance business in India includes: Deposits;

Investments; Valuation of Assets Liabilities and Solvency Margins; Submission of Returns;

Actuary; Insurance Advertisements; Obligations to the Rural and Social Sector; Assignment

and Nomination; Foreign Exchange laws; Taxation laws and Stamp Duty.

In the month of February 2011, IRDA had rolled out the regulation on portability of health

insurance to safeguard the interest of the policyholders. The gist of guidelines is given

below:

All insurers issuing health insurance policies shall allow for credit gained by the

insured for pre existing conditions in terms of waiting period when insured switches

from one insurer to another or from one plan to another, provided the previous policy

has been maintained without break.

122

This credit shall be limited to the sum assured (including bonus) under the previous

policy.

When policyholder is switching from one insurer to other, Insurers shall process the

proposal with speed and efficiency and all decisions thereof shall be communicated

in writing within a reasonable period not exceeding 15 days from receipt of proposal

by the insurer.

If the policy results into discontinuance because of any delay by the insurer in

accepting the proposal, the insurer shall not treat the policy as discontinuance and

shall allow portability.

Insurers shall clearly draw the attention of the policyholder in the policy contract and

the promotional material like prospectus, sales literature etc.

Insurer to share the entire database including the claim details of the policies where

the policyholders has opted for portability with their counterparts where requested.

All applications for the portability shall be acknowledged by the insurers within three

working days.

Having looked into the external environment including the trends in the Indian health

insurance industry it becomes quite evident that the health insurance sector is growing at a

fast pace and so is the level of competition. The key developments in the Indian health

insurance industry had taken place post the privatization. There are multiple initiatives taken

by the regulator to improve the growth and built trust among the minds of the policyholders.

The standalone health insurance companies are here to stay and are increasing their market

share on a year to year basis. The detariffication of the insurance industry will help reduce

the subsidization offered in health insurance However, currently the health insurance

industry has a claim ratio of more than 100 percent and to ensure that the business is

profitable one needs to develop strategies for synergy among insurers and providers, and in

doing so it is important to understand the attitude, interest and concerns of the different

stakeholders. The health insurance industry is highly regulated unlike the healthcare industry

and it is important to meet the needs and expectations of different stakeholders.