Embed Size (px)

Citation preview

4-1© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

1. The end-of-period spreadsheet illustrates the flow of accounting information from the unadjusted trial balance into the adjusted trial balance and into the financial statements. In doing so, the spreadsheet illustrates the impact of the adjustments on the financial statements.

2. a. Current assets are composed of cash and other assets that may reasonably be expectedto be realized in cash or sold or used up, usually within one year or less, through the normaloperations of the business.

b. Property, plant, and equipment is composed of assets that are used in the business and that are of a permanent or relatively fixed nature.

3. Current liabilities are liabilities that will be due within a short time (usually one year or less) and that are to be paid out of current assets. Liabilities that will not be due for a comparatively long time (usually more than one year) are called non-current liabilities.

4. Revenue, expense, and dividends accounts are generally referred to as temporary accounts.

5. Closing entries are necessary at the end of an accounting period (1) to transfer the balances intemporary accounts to permanent accounts and (2) to prepare the temporary accounts for use inrecording transactions for the next accounting period.

6. Adjusting entries bring the accounts up to date, while closing entries reduce the revenue, expense, and dividends accounts to zero balances for use in recording transactions for the next accounting period.

7. The purpose of the post-closing trial balance is to make sure that the ledger is in balance at thebeginning of the next period.

8. a. The financial statements are the most important output of the accounting cycle.

b. Yes, all companies have an accounting cycle that begins with analyzing and journalizing transactions and ends with a post-closing trial balance. However, companies may differ in how they implement the steps in the accounting cycle. For example, while most companies use computerized accounting systems, some companies may use manual systems.

9. The natural business year is the fiscal year that ends when business activities have reached the lowest point in the annual operating cycle.

10. All the companies listed are general merchandisers whose busiest time of the year is during the holiday season, which extends through most of December. Traditionally, the lowest point of business activity for general merchandisers will be near the end of January and the beginning of February. Thus, these companies have chosen their natural business year for their fiscal year.

CHAPTER 4COMPLETING THE ACCOUNTING CYCLE

DISCUSSION QUESTIONS

CHAPTER 4 Completing the Accounting Cycle

4-2© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

11. The presentation of financial statements started from IAS 1 Accounting Disclosure Policy (1975), IAS 5Information to Be Disclosed in Financial Statements (1976), IAS 13 Presentation of Current Assets andCurrent Liabilities (1979). Subsequently, IAS 1, IAS 5, and IAS 13 were reformatted in 1994 andsuperseded by IAS 1 Presentation of Financial Statements superseded in 1997. In subsequent years,numerous amendments were made to IAS 1, including new disclosure requirements for puttable instruments and obligations arising on liquidation, classification of derivatives as current or non-current, classification of liabilities as current and presentation of comprehensive income.

12. The IFRS Framework describes the basic concepts underlying the preparation and presentation of financialstatements for external users. Its purpose is to provide guidance for developing future IFRSs andresolv-ing accounting issues that are not addressed directly in IFRSs. When developing and applyingaccounting policies, management should follow the framework and use its judgment to provide relevantand reliable information. In making the judgment, management must refer to, and consider theapplicability of the following sources in descending order:

• the requirements and guidance in IASB standards and interpretations dealing with similar and relatedissues; and• the definitions, recognition criteria and measurement concepts for assets, liabilities, income, and expensesin the Framework. [IAS 8.11]Management may also consider the most recent pronouncements of other standard-setting bodies thatuse a similar conceptual framework to develop accounting standards, other accounting literature, and acceptedindustry practices, to the extent that these do not conflict with the sources in paragraph 11. [IAS8.12]

13. In June 2011, the FASB and IASB issued separate amendments to their respective guidance on the presentationof comprehensive income that were convergent in many, but not all respects—Accounting StandardsUpdate No. 2011-05, Comprehensive Income (Topic 220): Presentation of Comprehensive Income (the FASB)and Presentation of Items of Other Comprehensive Income (Amendments to IAS 1, the IASB). Both boardsagreed that items of other comprehensive income need to be more prominently presented and decided topermit the option to present the components of comprehensive income in one or two statements.To increase the prominence of items reported in OCI and to facilitate convergence of U.S. GAAP andIFRS, the FASB decided to eliminate the option to present components of other comprehensive income aspart of the statement of changes in equity in this update.

14. Under IFRS, a complete set of financial statements comprises includes:1. a statement of financial position as of the end of the period;2. a statement of comprehensive income for the period;3. a statement of changes in equity for the period;4. a statement of cash flows for the period;5. a statement of financial position as at the beginning of the earliest comparative periodwhen an entity applies an accounting policy retrospectively or makes a retrospectiverestatement of items in its financial statements, or when it reclassifies items in itsfinancial statements; and6. notes, comprising a summary of significant accounting policies and other explanatoryinformation.

CHAPTER 4 Completing the Accounting Cycle

4-3© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Ex. 4–11. Statement of comprehensive income: 5, 8, 92. Retained earnings statement: 43. Statement of financial position: 1, 2, 3, 6, 7, 10

Ex. 4–2a. Asset: 1, 2, 5, 6, 10b. Liability: 9, 12c. Revenue: 3, 7d. Expense: 4, 8, 11

EXERCISES

CHAPTER 4 Completing the Accounting Cycle

4-4© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Ex. 4–3

Fees earned $175,200Expenses:

Salary expense $70,500Supplies expense 6,000Depreciation expense 4,800Miscellaneous expense 7,400

Total expenses 88,700Net profit $ 86,500

Retained earnings, June 1, 2013 $ 80,400Net profit $86,500Less dividends 12,000Increase in retained earnings 74,500Retained earnings, May 31, 2014 $154,900

Non-current assets: Equity: Property, plant, and equipment: Share capital-ordinary $ 10,000

Office equipment $74,000 Retained earnings 154,900 Less accum. depr. 14,800 Total equity $164,900

Total non-current assets $59,200 Current assets: Current liabilities:

Supplies $ 3,600 Accounts payable $ 24,400 Accounts receivable 90,000 Salaries payable 1,500 Cash 38,000 Total liabilities 25,900

Total current assets 131,600 Total equity and liabilities $190,800 Total assets $190,800

For the Year Ended May 31, 2014

HOLISM CONSULTINGStatement of Financial Position

May 31, 2014Assets Equity and Liabilities

HOLISM CONSULTINGStatement of Comprehensive Income

For the Year Ended May 31, 2014

HOLISM CONSULTINGRetained Earnings Statement

CHAPTER 4 Completing the Accounting Cycle

4-5© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Ex. 4–4

Fees earned $60,000Expenses:

Salary expense $32,450Supplies expense 1,800Depreciation expense 750Miscellaneous expense 1,500

Total expenses 36,500Net profit $23,500

Retained earnings, capital, May 1, 2013 $52,200Net profit $23,500Less dividends 2,000Increase in retained earnings 21,500Retained earnings, April 30, 2014 $73,700

Non-current assets: Equity: Property, plant, and equipment: Share capital-ordinary $30,000

Office equipment $30,500 Retained earnings 73,700 Less accum. depr. 5,250 Total equity $103,700

Total non-current assets $25,250 Current assets: Current liabilities:

Supplies $ 1,200 Accounts payable $ 3,300 Accounts receivable 53,500 Salaries payable 450 Cash 27,500 Total liabilities 3,750

Total current assets 82,200 Total equity and libilities $107,450 Total assets $107,450

OLYMPIA CONSULTINGStatement of Financial Position

April 30, 2014Assets Equity and Liabilities

OLYMPIA CONSULTINGStatement of Comprehensive Income

For the Year Ended April 30, 2014

OLYMPIA CONSULTINGRetained Earnings Statement

For the Year Ended April 30, 2014

CHAPTER 4 Completing the Accounting Cycle

4-6© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Ex. 4–5

Fees earned $440,000Expenses:

Salaries expense $265,150Rent expense 36,000Utilities expense 28,500Depreciation expense 7,250Supplies expense 2,200Insurance expense 1,200Miscellaneous expense 7,100

Total expenses 347,400Net profit $ 92,600

Ex. 4–6

Service revenue $270,900Expenses:

Wages expense $213,100Rent expense 42,000Utilities expense 17,600Depreciation expense 9,000Insurance expense 4,000Supplies expense 3,000Miscellaneous expense 6,000

Total expenses 294,700Net loss $ (23,800)

Statement of Comprehensive IncomeFor the Year Ended February 28, 2014

SHANGHAI MESSENGER SERVICEStatement of Comprehensive Income

For the Year Ended September 30, 2014

VEGGIE HEALTH SERVICES CO.

CHAPTER 4 Completing the Accounting Cycle

4-7© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Ex. 4–7

a.

Revenues $39,304Expenses:

Salaries and employee benefits $15,276Purchased transportation 5,674Fuel 4,151Rentals and landing fees 2,462Maintenance and repairs 1,979Depreciation 1,973Provision for income taxes 813Other expense (income) net 5,524

Total expenses 37,852Net profit $ 1,452

b. The statement of comprehensive incomes are very similar. The actual statementincludes some additional expense and income classifications. For example,the actual statement reports Income Before Income Taxes and Provision forIncome Taxes separately. In addition, the "Other expense (income) net" in thetext is a summary of several items from the Web site, includingIntercompany charges, Interest expense, and Interest income.

Ex. 4–8

Retained earnings, November 1, 2013 $475,000Net profit $90,000Less dividends 48,000Increase in retained earnings 42,000Retained earnings, October 31, 2014 $517,000

WELL SYSTEMS CO.Retained Earnings Statement

For the Year Ended October 31, 2014

FEDEX CORPORATIONStatement of Comprehensive Income

(in millions)For the Year Ended May 31, 2011

CHAPTER 4 Completing the Accounting Cycle

4-8© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Ex. 4–9

Retained earnings, July 1, 2013 $115,800Net loss $20,900Plus dividends 24,000Decrease in retained earnings 44,900Retained earnings, June 30, 2014 $ 70,900

Ex. 4–10a. Current asset: 1, 3, 5, 6b. Property, plant, and equipment: 2, 4

Ex. 4–11Since current liabilities are usually due within one year, $15,000 ($1,250 × 12 months) would be reported as a current liability on the statement of financial position.The remainder of $360,000 ($375,000 – $15,000) would be reported as a non-current liability on the statement of financial position.

WEIRD SPORTSRetained Earnings Statement

For the Year Ended June 30, 2014

CHAPTER 4 Completing the Accounting Cycle

4-9© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Ex. 4–12

Non-current assets: Equity: Property, plant, and equipment: Share capital—ordinary $100,000

Land $290,000 Retained earnings 509,000Equipment $300,000 Total equity $609,000Less accumulated depreciation 103,300 196,700

Total non-current assets $486,700 Current liabilities:Current assets: Accounts payable $ 18,500

Prepaid rent $ 18,000 Salaries payable 8,500Prepaid insurance 19,200 Unearned fees 9,000Supplies 5,350 Total liabilities 36,000Accounts receivable 78,250 Total equity and liabilities $645,000Cash* 37,500

Total current assets 158,300 Total assets $645,000

*$37,500 = $645,000 – $486,700 – $18,000 – $19,200 – $5,350 – $78,250

LABRADOR WEIGHT LOSS CO.Statement of Financial Position

June 30, 2014Assets Equity and Liabilities

CHAPTER 4 Completing the Accounting Cycle

4-10© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Ex. 4–131. The date of the statement should be "August 31, 2014" and not "For the Year

Ended August 31, 2014."

2. Accounts payable should be a current liability.

3. Land should be classified as property, plant, and equipment.

4. "Accumulated depreciation" should be deducted from the related property, plant, and equipment.

5. An adding error was made in determining the amount of the total property, plant, and equipment.

6. Accounts receivable should be a current asset.7. Net profit should be reported on the statement of comprehensive income

and retained earnings statement.

8. Wages payable should be a current liability.

A corrected statement of financial position would be as follows:

CHAPTER 4 Completing the Accounting Cycle

4-11© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Ex. 4–13 (Concluded)

Non-current assets: Equity: Property, plant, and equipment: Share capital—ordinary $ 75,000

Land $225,000 Retained earnings 512,200Building $400,000 Total equity $587,200Less accumulated depreciation 155,000 245,000Equipment $ 97,000 Current liabilities:Less accumulated depreciation 25,000 72,000 Accounts payable $ 31,300

Total non-current assets 542,000$ Wages payable 6,500Current assets: Total liabilities 37,800

Prepaid insurance $16,600 Total equity and liabilities $625,000Supplies 6,500Accounts receivable 41,400Cash 18,500

Total current assets 83,000 Total assets $625,000

LABYRINTH SERVICES CO.Statement of Financial Position

August 31, 2014Assets Equity and Liabilities

CHAPTER 4 Completing the Accounting Cycle

4-12© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Ex. 4–14d. Depreciation Expense—Equipment

g. Fees Earned

j. Supplies Expense

k. Wages Expense

Note: Dividends is closed to Retained Earnings rather than to Income Summary.

Ex. 4–15The income summary account is used to close the revenue and expense accounts, and it aids in detecting and correcting errors. The $1,190,500 represents expenseaccount balances, and the $1,476,300 represents revenue account balances thathave been closed. In this case, the company had net profit of $285,800 ($1,476,300 – $1,190,500).

Ex. 4–16

a. Income Summary 122,650Retained Earnings 122,650

($613,400 – $490,750).

Retained Earnings 55,000Dividends 55,000

b. $901,250 ($833,600 + $122,650 – $55,000)

Ex. 4–17

July 31 Fees Earned 337,900Income Summary 337,900

31 Income Summary 362,000Wages Expense 277,500Rent Expense 54,000Supplies Expense 14,300Miscellaneous Expense 16,200

31 Retained Earnings 24,100Income Summary 24,100

31 Retained Earnings 45,000Dividends 45,000

Closing Entries

CHAPTER 4 Completing the Accounting Cycle

4-13© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Ex. 4–18a. Accounts Payableb. Accumulated Depreciationc. Share capital—ordinaryd. Cashh. Office Equipmentj. Salaries Payablek. Supplies

Ex. 4–19

Debit CreditBalances Balances

Cash 21,350Accounts Receivable 56,700Supplies 7,500Equipment 74,450Accumulated Depreciation—Equipment 12,400Accounts Payable 29,600Salaries Payable 3,200Unearned Rent 11,000Share capital—ordinary 25,000Retained Earnings 78,800

160,000 160,000

Ex. 4–201. h 6. d2. g 7. b3. f 8. a4. c 9. e5. i 10. j

IGLOO TREASURES CO.Post-Closing Trial Balance

January 31, 2014

CHAPTER 4 Completing the Accounting Cycle

4-14© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Ex. 4–21a.

Current assets……………Current liabilitites…………Working capital……………

Current ratio………………

b. Under Armour’s working capital increased by $78,865 ($406,703 – $327,838)during Year 2. The current ratio remained the same at 3.73 in Year 1 and Year 2. A current ratio of 3.73 indicates a strong solvency position. Thus, short-term creditors should not be concerned about receiving payment from Under Armour.

Ex. 4–22a.

Current assets……………Current liabilitites…………Working capital……………

Current ratio………………

b. Starbucks' working capital improved (increased) from Year 1 to Year 2 by $522,500 ($977,300 – $454,800). Starbucks' current ratio also improved(increased) from 1.29 in Year 1 to 1.55 in Year 2. The improved working capitaland current ratio indicate that short-term creditors should not be concernedabout receiving payment from Starbucks.

Appendix Ex. 4–231. i 6. f2. a 7. j3. g 8. e4. d 9. h5. c 10. b

($2,035,800 ÷ $1,581,000)

$ 977,300 $ 454,800

1.55 1.29

December 31

Year 2 Year 1

3.73($555,850 ÷ $149,147)

Year 1Year 2$555,850149,147

$406,703

$2,756,400 $2,035,800

$448,000120,162

1,779,100 1,581,000

($2,756,400 ÷ $1,779,100)

$327,838

3.73($448,000 ÷ $120,162)

CHAPTER 4 Completing the Accounting Cycle

4-15© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Appendix Ex. 4–24

Account Title Debit Credit Debit Credit Cash 12 12 Accounts Receivable 90 (a) 13 103 Supplies 8 (b) 4 4 Prepaid Insurance 12 (c) 10 2 Land 190 190 Equipment 50 50 Accum. Depr.—Equipment 4 (d) 3 7 Accounts Payable 36 36 Wages Payable 0 (e) 1 1 Share Capital—Ordinary 50 50 Retained Earnings 210 210 Dividends 8 8 Fees Earned 200 (a) 13 213 Wages Expense 110 (e) 1 111 Rent Expense 12 12 Insurance Expense 0 (c) 10 10 Utilities Expense 6 6 Supplies Expense 0 (b) 4 4 Depreciation Expense 0 (d) 3 3 Miscellaneous Expense 2 2 Totals 500 500 31 31 517 517

Debit CreditTrial Balance Adjustments Trial Balance

ALERT SECURITY SERVICES CO.End-of-Period Spreadsheet (Work Sheet)

For the Year Ended October 31, 2014Unadjusted Adjusted

CHAPTER 4 Completing the Accounting Cycle

4-16© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Appendix Ex. 4–25

Account Title Debit Credit Debit Credit Cash 12 12 Accounts Receivable 103 103 Supplies 4 4 Prepaid Insurance 2 2 Land 190 190 Equipment 50 50 Accum. Depr.—Equipment 7 7 Accounts Payable 36 36 Wages Payable 1 1 Share Capital—Ordinary 50 50 Retained Earnings 210 210 Dividends 8 8 Fees Earned 213 213 Wages Expense 111 111 Rent Expense 12 12 Insurance Expense 10 10 Utilities Expense 6 6 Supplies Expense 4 4 Depreciation Expense 3 3 Miscellaneous Expense 2 2 Totals 517 517 148 213 369 304 Net profit (loss) 65 65

213 213 369 369

Statement of

Debit CreditTrial Balance Comprehensive Income Financial Position

ALERT SECURITY SERVICES CO.End-of-Period Spreadsheet (Work Sheet)

For the Year Ended October 31, 2014Adjusted Statement of

CHAPTER 4 Completing the Accounting Cycle

4-17© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Appendix Ex. 4–26

Fees earned $213Expenses:

Wages expense $111Rent expense 12Insurance expense 10Utilities expense 6Supplies expense 4Depreciation expense 3Miscellaneous expense 2

Total expenses 148Net profit $ 65

Retained earnings, November 1, 2013 $210Net profit $65Less dividends 8Increase in retained earnings 57Retained earnings, October 31, 2014 $267

Retained Earnings StatementFor the Year Ended October 31, 2014

ALERT SECURITY SERVICES CO.Statement of Comprehensive IncomeFor the Year Ended October 31, 2014

ALERT SECURITY SERVICES CO.

CHAPTER 4 Completing the Accounting Cycle

4-18© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Appendix Ex. 4–26 (Concluded)

Non-current assets: Equity: Property, plant, and equipment: Share capital-ordinary $ 50

Land $190 Retained earnings 267Equipment $50 Total equity $317Less accumulated depreciation 7 43

Total non-current assets $233 Current liabilities:Current assets: Accounts payable $ 36

Prepaid insurance $2 Wages payable 1Supplies 4 Total liabilities 37 Accounts receivable 103 Total equity and liabilities $354Cash 12

Total current assets 121 Total assets $354

ALERT SECURITY SERVICES CO.Statement of Financial Position

October 31, 2014Assets Equity and Liabilities

CHAPTER 4 Completing the Accounting Cycle

4-19© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Appendix Ex. 4–27

2014 Oct. 31 Accounts Receivable 13

Fees Earned 13Accrued fees.

31 Supplies Expense 4Supplies 4

Supplies used ($8 – $4).

31 Insurance Expense 10Prepaid Insurance 10

Insurance expired.

31 Depreciation Expense 3Accumulated Depreciation—Equipment 3

Equipment depreciation.

31 Wages Expense 1Wages Payable 1

Accrued wages.

Appendix Ex. 4–28

2014 Oct. 31 Fees Earned 213

Income Summary 213

31 Income Summary 148Wages Expense 111Rent Expense 12Insurance Expense 10Utilities Expense 6Supplies Expense 4Depreciation Expense 3Miscellaneous Expense 2

31 Income Summary 65Retained Earnings 65

31 Retained Earnings 8Dividends 8

Adjusting Entries

Closing Entries

CHAPTER 4 Completing the Accounting Cycle

4-20© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Prob. 4–1A

1.

Fees earned $368,100Rent revenue 1,000

Total revenues $369,100Expenses:

Salaries and wages expense $164,900Advertising expense 21,700Utilities expense 11,400Repairs expense 8,850Depreciation expense—equipment 4,200Insurance expense 2,500Supplies expense 1,830Depreciation expense—building 1,600Miscellaneous expense 4,320

Total expenses 221,300Net profit $147,800

2.

Retained earnings, August 1, 2013 $128,100Net profit for the year $147,800Less dividends 10,000Increase in retained earnings 137,800Retained earnings, July 31, 2014 $265,900

PROBLEMS

WATCHDOG COMPANYRetained Earnings Statement

For the Year Ended July 31, 2014

WATCHDOG COMPANYStatement of Comprehensive Income

For the Year Ended July 31, 2014

CHAPTER 4 Completing the Accounting Cycle

4-21© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Prob. 4–1A (Continued)

3.

Non-current assets: Equity:Property, plant, and equipment: Share capital-ordinary $ 75,000

Land $ 98,000 Retained earnings 265,900Building $400,000 Total equity $340,900Less accumulated depreciation 206,900 193,100Equipment $101,000 Current liabilities:Less accumulated depreciation 89,300 11,700 Accounts payable $ 15,700

Total non-current assets $ 302,800 Salaries and wages payable 1,800Current assets: Unearned rent 1,100

Prepaid insurance $ 1,700 Total liabilities 18,600 Supplies 900 Total equity and liabilites $359,500Accounts receivable 43,300Cash 10,800

Total current assets 56,700 Total assets $359,500

WATCHDOG COMPANYStatement of Financial Position

July 31, 2014Assets Equity and Liabilities

CHAPTER 4 Completing the Accounting Cycle

4-22© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Prob. 4–1A (Concluded)

4. 2014 July 31 Fees Earned 368,100

Rent Revenue 1,000Income Summary 369,100

31 Income Summary 221,300Salaries and Wages Expense 164,900Advertising Expense 21,700Utilities Expense 11,400Repairs Expense 8,850Depreciation Expense—Equipment 4,200Insurance Expense 2,500Supplies Expense 1,830Depreciation Expense—Building 1,600Miscellaneous Expense 4,320

31 Income Summary 147,800Retained Earnings 147,800

31 Retained Earnings 10,000Dividends 10,000

5.

Debit CreditBalances Balances

Cash 10,800Accounts Receivable 43,300Prepaid Insurance 1,700Supplies 900Land 98,000Building 400,000Accumulated Depreciation—Building 206,900Equipment 101,000Accumulated Depreciation—Equipment 89,300Accounts Payable 15,700Salaries and Wages Payable 1,800Unearned Rent 1,100Share Capital—Ordinary 75,000Retained Earnings 265,900

655,700 655,700

WATCHDOG COMPANYPost-Closing Trial Balance

July 31, 2014

Closing Entries

CHAPTER 4 Completing the Accounting Cycle

4-23© 2012 4 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Prob. 4–2A

1.

Revenues:Service fees $480,000Rent revenue 25,000

Total revenues $505,000Expenses:

Salaries expense $336,000Rent expense 62,500Supplies expense 12,000Depreciation expense—building 6,000Utilities expense 4,400Repairs expense 3,200Insurance expense 2,800Miscellaneous expense 5,100

Total expenses 432,000Net profit $ 73,000

Retained earnings, May 1, 2013 $144,300Net profit for the year $73,000Less dividends 10,000Increase in retained earnings 63,000Retained earnings, April 30, 2014 $207,300

IRONSIDE SECURITY SERVICESRetained Earnings Statement

For the Year Ended April 30, 2014

IRONSIDE SECURITY SERVICESStatement of Comprehensive Income

For the Year Ended April 30, 2014

CHAPTER 4 Completing the Accounting Cycle

4-24© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Prob. 4–2A (Continued)

Non-current assets: Equity:Property, plant, and equipment: Share capital-ordinary $ 35,000

Building $240,500 Retained earnings 207,300Less accum. depreciation 55,200 Total equity 242,300$

Total non-current assets $185,300Current assets: Current liabilities:

Prepaid insurance $ 4,800 Accounts payable $ 6,000Supplies 7,500 Salaries payable 1,500Accounts receivable 37,200 Unearned rent 3,000Cash 18,000 Total liabilities 10,500

Total current assets 67,500 Total assets $252,800 Total equity and liabilities $252,800

IRONSIDE SECURITY SERVICESStatement of Financial Position

April 30, 2014Assets Equity and Liabilities

CHAPTER 4 Completing the Accounting Cycle

4-25© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Prob. 4–2A (Concluded)

2. 2014 Apr. 30 Service Fees 480,000

Rent Revenue 25,000Income Summary 505,000

30 Income Summary 432,000Salaries Expense 336,000Rent Expense 62,500Supplies Expense 12,000Depreciation Expense—Building 6,000Utilities Expense 4,400Repairs Expense 3,200Insurance Expense 2,800Miscellaneous Expense 5,100

30 Income Summary 73,000Retained Earnings 73,000

30 Retained Earnings 10,000Dividends 10,000

3. $37,500 ($47,500 – $10,000) net loss. The $47,500 decrease is caused by the $10,000 dividends and a $37,500 net loss.

Closing Entries

CHAPTER 4 Completing the Accounting Cycle

4-26© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Prob. 4–3A 1., 3., and 6.

June 30 Bal. 11,000

June 30 Bal. 21,500 June 30 Adj. 17,90030 Adj. Bal. 3,600

June 30 Bal. 9,600 June 30 Adj. 5,70030 Adj. Bal. 3,900

June 30 Bal. 232,600

June 30 Bal. 125,40030 Adj. 6,50030 Adj. Bal. 131,900

June 30 Bal. 11,800

June 30 Adj. 1,100

June 30 Bal. 40,000

June 30 Clos. 10,000 June 30 Bal. 65,60030 Clos. 10,70030 Bal. 66,300

June 30 Bal. 10,000 June 30 Clos. 10,000

Cash

Laundry Supplies

Prepaid Insurance

Laundry Equipment

Dividends

Accumulated Depreciation

Accounts Payable

Share Capital—Ordinary

Retained Earnings

Wages Payable

CHAPTER 4 Completing the Accounting Cycle

4-27© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Prob. 4–3A (Continued)

June 30 Clos. 221,500 June 30 Clos. 232,200Clos. 10,700

June 30 Clos. 232,200 June 30 Bal. 232,200

June 30 Bal. 125,200 June 30 Clos. 126,30030 Adj. 1,10030 Adj. Bal. 126,300

June 30 Bal. 40,000 June 30 Clos. 40,000

June 30 Bal. 19,700 June 30 Clos. 19,700

June 30 Adj. 17,900 June 30 Clos. 17,900

June 30 Adj. 6,500 June 30 Clos. 6,500

June 30 Adj. 5,700 June 30 Clos. 5,700

June 30 Bal. 5,400 June 30 Clos. 5,400

Wages Expense

Rent Expense

Utilities Expense

Income Summary

Laundry Revenue

Laundry Supplies Expense

Depreciation Expense

Insurance Expense

Miscellaneous Expense

CHAPTER 4 Completing the Accounting Cycle

4-28© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Prob. 4–3A (Continued)2. Optional (Appendix)

Account Title Debit Credit Debit Credit Debit Credit Debit CreditCash 11,000 11,000 11,000Laundry Supplies 21,500 (a) 17,900 3,600 3,600Prepaid Insurance 9,600 (b) 5,700 3,900 3,900Laundry Equipment 232,600 232,600 232,600Accum. Depreciation 125,400 (c) 6,500 131,900 131,900Accounts Payable 11,800 11,800 11,800Wages Payable (d) 1,100 1,100 1,100Share Capital—Ordinary 40,000 40,000 40,000Retained Earnings 65,600 65,600 65,600Dividends 10,000 10,000 10,000Laundry Revenue 232,200 232,200 232,200Wages Expense 125,200 (d) 1,100 126,300 126,300Rent Expense 40,000 40,000 40,000Utilities Expense 19,700 19,700 19,700Laundry Supplies Exp. (a) 17,900 17,900 17,900Depreciation Expense (c) 6,500 6,500 6,500Insurance Expense (b) 5,700 5,700 5,700Miscellaneous Expense 5,400 5,400 5,400

475,000 475,000 31,200 31,200 482,600 482,600 221,500 232,200 261,100 250,400Net profit 10,700 10,700

232,200 232,200 261,100 261,100

EPICENTER LAUNDRYEnd-of-Period Spreadsheet (Work Sheet)

For the Year Ended June 30, 2014Statement ofUnadjusted Adjusted

Financial PositionTrial BalanceDebit Credit

Trial BalanceStatement of

Comprehensive IncomeAdjustments

CHAPTER 4 Completing the Accounting Cycle

4-29© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Prob. 4–3A (Continued)

3. 2014 June 30 Laundry Supplies Expense 17,900

Laundry Supplies 17,900Supplies used ($21,500 – $3,600).

30 Insurance Expense 5,700Prepaid Insurance 5,700

Insurance expired.

30 Depreciation Expense 6,500Accumulated Depreciation 6,500

Equipment depreciation.

30 Wages Expense 1,100Wages Payable 1,100

Accrued wages.

4.

Debit CreditBalances Balances

Cash 11,000Laundry Supplies 3,600Prepaid Insurance 3,900Laundry Equipment 232,600Accumulated Depreciation 131,900Accounts Payable 11,800Wages Payable 1,100Share Capital—Ordinary 40,000Retained Earnings 65,600Dividends 10,000Laundry Revenue 232,200Wages Expense 126,300Rent Expense 40,000Utilities Expense 19,700Laundry Supplies Expense 17,900Depreciation Expense 6,500Insurance Expense 5,700Miscellaneous Expense 5,400

482,600 482,600

EPICENTER LAUNDRYAdjusted Trial Balance

June 30, 2014

Adjusting Entries

CHAPTER 4 Completing the Accounting Cycle

4-30© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Prob. 4–3A (Continued)

5.

Laundry revenue $232,200Expenses:

Wages expense $126,300Rent expense 40,000Utilities expense 19,700Laundry supplies expense 17,900Depreciation expense 6,500Insurance expense 5,700Miscellaneous expense 5,400

Total expenses 221,500Net profit $ 10,700

Retained earnings, July 1, 2013 $65,600Net profit for the year $10,700Less dividends 10,000Increase in retained earnings 700Retained earnings, June 30, 2014 $66,300

Retained Earnings StatementFor the Year Ended June 30, 2014

EPICENTER LAUNDRYStatement of Comprehensive Income

For the Year Ended June 30, 2014

EPICENTER LAUNDRY

CHAPTER 4 Completing the Accounting Cycle

4-31© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Prob. 4–3A (Continued)

Non-current assets: Equity: Property, plant, and equipment: Share capital—ordinary $40,000

Laundry equipment $232,600 Retained earnings 66,300Less accum. depreciation 131,900 Total equity $106,300

Total non-current assets $100,700Current assets: Current liabilities:

Prepaid insurance $ 3,900 Accounts payable $11,800Laundry supplies 3,600 Wages payable 1,100Cash 11,000 Total liabilities 12,900

Total current assets 18,500 Total assets $119,200 Total equity and liabilities $119,200

EPICENTER LAUNDRYStatement of Financial Position

June 30, 2014Assets Equity and Liabilities

CHAPTER 4 Completing the Accounting Cycle

4-32© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Prob. 4–3A (Concluded)

6. 2014 June 30 Laundry Revenue 232,200

Income Summary 232,200

30 Income Summary 221,500Wages Expense 126,300Rent Expense 40,000Utilities Expense 19,700Laundry Supplies Expense 17,900Depreciation Expense 6,500Insurance Expense 5,700Miscellaneous Expense 5,400

30 Income Summary 10,700Retained Earnings 10,700

30 Retained Earnings 10,000Dividends 10,000

7.

Debit CreditBalances Balances

Cash 11,000Laundry Supplies 3,600Prepaid Insurance 3,900Laundry Equipment 232,600Accumulated Depreciation 131,900Accounts Payable 11,800Wages Payable 1,100Share Capital—Ordinary 40,000Retained Earnings 66,300

251,100 251,100

EPICENTER LAUNDRYPost-Closing Trial Balance

June 30, 2014

Closing Entries

CHAPTER 4 Completing the Accounting Cycle

4-33© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Prob. 4–4A1., 3., and 6.

Account No. 11

Post.Item Ref. Debit Credit Debit Credit

2014 Mar. 31 Balance 12,000

Account No. 13

Post.Item Ref. Debit Credit Debit Credit

2014 Mar. 31 Balance 30,000

31 Adjusting 26 22,500 7,500

Account No. 14

Post.Item Ref. Debit Credit Debit Credit

2014 Mar. 31 Balance 3,600

31 Adjusting 26 1,800 1,800

Account No. 16

Post.Item Ref. Debit Credit Debit Credit

2014 Mar. 31 Balance 110,000

Account No. 17

Post.Item Ref. Debit Credit Debit Credit

2014 Mar. 31 Balance 25,000

31 Adjusting 26 8,350 33,350

Account No. 18

Post.Item Ref. Debit Credit Debit Credit

2014 Mar. 31 Balance 60,000

Account: Equipment

BalanceDate

CashAccount:

Account: Supplies

BalanceDate

DateBalance

BalanceDate

BalanceDate

Account: Prepaid Insurance

Account: Accumulated Depreciation—Equipment

BalanceDate

Account: Trucks

CHAPTER 4 Completing the Accounting Cycle

4-34© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Prob. 4–4A (Continued)

Account No. 19

Post.Item Ref. Debit Credit Debit Credit

2014 Mar. 31 Balance 15,000

31 Adjusting 26 6,200 21,200

Account No. 21

Post.Item Ref. Debit Credit Debit Credit

2014 Mar. 31 Balance 4,000

Account No. 22

Post.Item Ref. Debit Credit Debit Credit

2014 Mar. 31 Adjusting 26 600 600

Account No. 31

Post.Item Ref. Debit Credit Debit Credit

2014 Mar. 31 Balance 26,000

Account No. 32

Post.Item Ref. Debit Credit Debit Credit

2014 Mar. 31 Balance 70,000

31 Closing 27 51,150 121,15031 Closing 27 15,000 106,150

Account No. 33

Post.Item Ref. Debit Credit Debit Credit

2014 Mar. 31 Balance 15,000

31 Closing 27 15,000 — —

BalanceDate

Accumulated Depreciation—TrucksAccount:

Account: Accounts Payable

BalanceDate

DateBalance

BalanceDate

Account: Wages Payable

Account: Share Capital—Ordinary

BalanceDate

Account: Retained Earnings

BalanceDate

Account: Dividends

CHAPTER 4 Completing the Accounting Cycle

4-35© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Prob. 4–4A (Continued)

Account No. 34

Post.Item Ref. Debit Credit Debit Credit

2014 Mar. 31 Closing 27 160,000 160,000

31 Closing 27 108,850 51,15031 Closing 27 51,150 — —

Account No. 41

Post.Item Ref. Debit Credit Debit Credit

2014 Mar. 31 Balance 160,000

31 Closing 27 160,000 — —

Account No. 51

Post.Item Ref. Debit Credit Debit Credit

2014 Mar. 31 Balance 45,000

31 Adjusting 26 600 45,60031 Closing 27 45,600 — —

Account No. 52

Post.Item Ref. Debit Credit Debit Credit

2014 Mar. 31 Adjusting 26 22,500 22,500

31 Closing 27 22,500 — —

Account No. 53

Post.Item Ref. Debit Credit Debit Credit

2014 Mar. 31 Balance 10,600

31 Closing 27 10,600 — —

BalanceDate

Account: Rent Expense

Account: Wages Expense

BalanceDate

Account: Supplies Expense

DateBalance

Income SummaryAccount:

BalanceDate

Account: Service Revenue

BalanceDate

CHAPTER 4 Completing the Accounting Cycle

4-36© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Prob. 4–4A (Continued)

Account No. 54

Post.Item Ref. Debit Credit Debit Credit

2014 Mar. 31 Balance 9,000

31 Closing 27 9,000 — —

Account No. 55

Post.Item Ref. Debit Credit Debit Credit

2014 Mar. 31 Adjusting 26 8,350 8,350

31 Closing 27 8,350 — —

Account No. 56

Post.Item Ref. Debit Credit Debit Credit

2014 Mar. 31 Adjusting 26 6,200 6,200

31 Closing 27 6,200 — —

Account No. 57

Post.Item Ref. Debit Credit Debit Credit

2014 Mar. 31 Adjusting 26 1,800 1,800

31 Closing 27 1,800 — —

Account No. 59

Post.Item Ref. Debit Credit Debit Credit

2014 Mar. 31 Balance 4,800

31 Closing 27 4,800 — —

BalanceDate

Account: Miscellaneous Expense

BalanceDate

Truck ExpenseAccount:

Account: Depreciation Expense—Trucks

Account: Depreciation Expense—Equipment

Date

Account: Insurance Expense

DateBalance

Balance

BalanceDate

CHAPTER 4 Completing the Accounting Cycle

4-37© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Prob. 4–4A (Continued)2. Optional (Appendix)

Account Title Debit Credit Debit Credit Debit Credit Debit CreditCash 12,000 12,000 12,000Supplies 30,000 (a) 22,500 7,500 7,500Prepaid Insurance 3,600 (b) 1,800 1,800 1,800Equipment 110,000 110,000 110,000Accum. Depr.—Equip. 25,000 (c) 8,350 33,350 33,350Trucks 60,000 60,000 60,000Accum. Depr.—Trucks 15,000 (d) 6,200 21,200 21,200Accounts Payable 4,000 4,000 4,000Wages Payable (e) 600 600 600Share Capital—Ordinary 26,000 26,000 26,000Retained Earnings 70,000 70,000 70,000Dividends 15,000 15,000 15,000Service Revenue 160,000 160,000 160,000Wages Expense 45,000 (e) 600 45,600 45,600Supplies Expense (a) 22,500 22,500 22,500Rent Expense 10,600 10,600 10,600Truck Expense 9,000 9,000 9,000Depr. Exp.—Equipment (c) 8,350 8,350 8,350Depr. Exp.—Trucks (d) 6,200 6,200 6,200Insurance Expense (b) 1,800 1,800 1,800Miscellaneous Expense 4,800 4,800 4,800

300,000 300,000 39,450 39,450 315,150 315,150 108,850 160,000 206,300 155,150Net profit 51,150 51,150

160,000 160,000 206,300 206,300

LAKOTA FREIGHT CO.End-of-Period Spreadsheet (Work Sheet)

For the Year Ended March 31, 2014Statement ofUnadjusted Adjusted

Financail PositionTrial BalanceDebit Credit

Trial BalanceStatement of

Comprehensive IncomeAdjustments

CHAPTER 4 Completing the Accounting Cycle

4-38© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Prob. 4–4A (Continued)3. Page 26

Post.Ref. Debit Credit

2014 Mar. 31 Supplies Expense 52 22,500

Supplies 13 22,500Supplies used ($30,000 – $7,500).

31 Insurance Expense 57 1,800Prepaid Insurance 14 1,800

Insurance expired.

31 Depreciation Expense—Equipment 55 8,350Accumulated Depr.—Equipment 17 8,350

Equipment depreciation.

31 Depreciation Expense—Trucks 56 6,200Accumulated Depr.—Trucks 19 6,200

Truck depreciation.

31 Wages Expense 51 600Wages Payable 22 600

Accrued wages.

DateAdjusting Entries

JOURNAL

CHAPTER 4 Completing the Accounting Cycle

4-39© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Prob. 4–4A (Continued)

4.

Debit CreditBalances Balances

Cash 12,000Supplies 7,500Prepaid Insurance 1,800Equipment 110,000Accumulated Depreciation—Equipment 33,350Trucks 60,000Accumulated Depreciation—Trucks 21,200Accounts Payable 4,000Wages Payable 600Share Capital—Ordinary 26,000Retained Earnings 70,000Dividends 15,000Service Revenue 160,000Wages Expense 45,600Supplies Expense 22,500Rent Expense 10,600Truck Expense 9,000Depreciation Expense—Equipment 8,350Depreciation Expense—Trucks 6,200Insurance Expense 1,800Miscellaneous Expense 4,800

315,150 315,150

Adjusted Trial BalanceMarch 31, 2014

LAKOTA FREIGHT CO.

CHAPTER 4 Completing the Accounting Cycle

4-40© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Prob. 4–4A (Continued)

5.

Service revenue $160,000Expenses:

Wages expense $45,600Supplies expense 22,500Rent expense 10,600Truck expense 9,000Depreciation expense—equipment 8,350Depreciation expense—trucks 6,200Insurance expense 1,800Miscellaneous expense 4,800

Total expenses 108,850Net profit $ 51,150

Retained earnings, April 1, 2013 $ 70,000Net profit for the year $51,150Less dividends 15,000Increase in retained earnings 36,150Retained earnings, March 31, 2014 $106,150

LAKOTA FREIGHT CO.Statement of Comprehensive IncomeFor the Year Ended March 31, 2014

LAKOTA FREIGHT CO.Retained Earnings Statement

For the Year Ended March 31, 2014

CHAPTER 4 Completing the Accounting Cycle

4-41© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Prob. 4–4A (Continued)

Non-current assets: Equity: Property, plant, and equipment: Share capital—ordinary $ 26,000

Equipment $110,000 Retained earnings 106,150Less accum. depreciation 33,350 $76,650 Total equity $132,150Trucks $ 60,000Less accum. depreciation 21,200 38,800 Current liabilities:

Total non-current assets $115,450 Accounts payable $ 4,000Current assets: Wages payable 600

Prepaid insurance $1,800 Total liabilities 4,600 Supplies 7,500Cash 12,000

Total current assets 21,300 Total assets $136,750 Total equity and liabilities $136,750

LAKOTA FREIGHT CO.Statement of Financial Position

March 31, 2014Assets Equity and Liabilities

CHAPTER 4 Completing the Accounting Cycle

4-42© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Prob. 4–4A (Concluded)6. Page 27

Post.Ref. Debit Credit

2014 Mar. 31 Service Revenue 41 160,000

Income Summary 34 160,000

31 Income Summary 34 108,850Wages Expense 51 45,600Supplies Expense 52 22,500Rent Expense 53 10,600Truck Expense 54 9,000Depreciation Expense—Equipment 55 8,350Depreciation Expense—Trucks 56 6,200Insurance Expense 57 1,800Miscellaneous Expense 59 4,800

31 Income Summary 34 51,150Retained Earnings 32 51,150

31 Retained Earnings 32 15,000Dividends 33 15,000

7.

Debit CreditBalances Balances

Cash 12,000Supplies 7,500Prepaid Insurance 1,800Equipment 110,000Accumulated Depreciation—Equipment 33,350Trucks 60,000Accumulated Depreciation—Trucks 21,200Accounts Payable 4,000Wages Payable 600Share Capital—Ordinary 26,000Retained Earnings 106,150

191,300 191,300

JOURNAL

March 31, 2014

Closing EntriesDate

LAKOTA FREIGHT CO.Post-Closing Trial Balance

CHAPTER 4 Completing the Accounting Cycle

4-43© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Prob. 4–5A1. and 2.

Page 1

Post.Ref. Debit Credit

2014 July 1 Cash 11 13,500

Accounts Receivable 12 20,800Supplies 14 3,200Office Equipment 18 7,500

Share Capital—Ordinary 31 45,000

1 Prepaid Rent 15 4,800Cash 11 4,800

2 Prepaid Insurance 16 4,500Cash 11 4,500

4 Cash 11 5,500Unearned Fees 23 5,500

5 Office Equipment 18 6,500Accounts Payable 21 6,500

6 Cash 11 15,300Accounts Receivable 12 15,300

10 Miscellaneous Expense 59 400Cash 11 400

12 Accounts Payable 21 5,200Cash 11 5,200

12 Accounts Receivable 12 13,300Fees Earned 41 13,300

14 Salary Expense 51 1,750Cash 11 1,750

Date

JOURNAL

CHAPTER 4 Completing the Accounting Cycle

4-44© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Prob. 4–5A (Continued)Page 2

Post.Ref. Debit Credit

2014 July 17 Cash 11 9,450

Fees Earned 41 9,450

18 Supplies 14 600Cash 11 600

20 Accounts Receivable 12 6,650Fees Earned 41 6,650

24 Cash 11 4,000Fees Earned 41 4,000

26 Cash 11 12,000Accounts Receivable 12 12,000

27 Salary Expense 51 1,750Cash 11 1,750

29 Miscellaneous Expense 59 325Cash 11 325

31 Miscellaneous Expense 59 675Cash 11 675

31 Cash 11 5,200Fees Earned 41 5,200

31 Accounts Receivable 12 3,000Fees Earned 41 3,000

31 Dividends 33 12,500Cash 11 12,500

Date

JOURNAL

CHAPTER 4 Completing the Accounting Cycle

4-45© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Prob. 4–5A (Continued)2., 6., and 9.

Account No. 11

Post.Item Ref. Debit Credit Debit Credit

2014 July 1 1 13,500 13,500

1 1 4,800 8,7002 1 4,500 4,2004 1 5,500 9,7006 1 15,300 25,000

10 1 400 24,60012 1 5,200 19,40014 1 1,750 17,65017 2 9,450 27,10018 2 600 26,50024 2 4,000 30,50026 2 12,000 42,50027 2 1,750 40,75029 2 325 40,42531 2 675 39,75031 2 5,200 44,95031 2 12,500 32,450

Account No. 12

Post.Item Ref. Debit Credit Debit Credit

2014 July 1 1 20,800 20,800

6 1 15,300 5,50012 1 13,300 18,80020 2 6,650 25,45026 2 12,000 13,45031 2 3,000 16,450

Account No. 14

Post.Item Ref. Debit Credit Debit Credit

2014 July 1 1 3,200 3,200

18 2 600 3,80031 Adjusting 3 2,275 1,525

Account: Supplies

CashAccount:

Account: Accounts Receivable

BalanceDate

DateBalance

BalanceDate

CHAPTER 4 Completing the Accounting Cycle

4-46© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Prob. 4–5A (Continued)

Account No. 15

Post.Item Ref. Debit Credit Debit Credit

2014 July 1 1 4,800 4,800

31 Adjusting 3 2,400 2,400

Account No. 16

Post.Item Ref. Debit Credit Debit Credit

2014 July 2 1 4,500 4,500

31 Adjusting 3 375 4,125

Account No. 18

Post.Item Ref. Debit Credit Debit Credit

2014 July 1 1 7,500 7,500

5 1 6,500 14,000

Account No. 19

Post.Item Ref. Debit Credit Debit Credit

2014 July 31 Adjusting 3 750 750

Account No. 21

Post.Item Ref. Debit Credit Debit Credit

2014 July 5 1 6,500 6,500

12 1 5,200 1,300

Account No. 22

Post.Item Ref. Debit Credit Debit Credit

2014 July 31 Adjusting 3 175 175

Account: Accounts Payable

BalanceDate

Account: Salaries Payable

BalanceDate

Account: Office Equipment

BalanceDate

Account: Accumulated Depreciation

BalanceDate

BalanceDate

DateBalance

Prepaid RentAccount:

Account: Prepaid Insurance

CHAPTER 4 Completing the Accounting Cycle

4-47© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Prob. 4–5A (Continued)

Account No. 23

Post.Item Ref. Debit Credit Debit Credit

2014 July 4 1 5,500 5,500

31 Adjusting 3 2,750 2,750

Account No. 31

Post.Item Ref. Debit Credit Debit Credit

20141 1 45,000 45,000

Account No. 32

Post.Item Ref. Debit Credit Debit Credit

2014 July 1 1 — —

31 Adjusting 3 33,475 33,47531 Closing 4 12,500 20,975

Account No. 33

Post.Item Ref. Debit Credit Debit Credit

2014 July 31 2 12,500 12,500

31 Closing 4 12,500 — —

Account No. 34

Post.Item Ref. Debit Credit Debit Credit

2014 July 31 Closing 4 44,350 44,350

31 Closing 4 10,875 33,47531 Closing 4 33,475 — —

Balance

July

Unearned FeesAccount:

Account: Share Capital—Ordinary

Account: Income Summary

Date

Date

Account: Retained Earnings

BalanceDate

Balance

BalanceDate

Account: Dividends

Balance

Date

CHAPTER 4 Completing the Accounting Cycle

4-48© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Prob. 4–5A (Continued)

Account No. 41

Post.Item Ref. Debit Credit Debit Credit

2014 July 12 1 13,300 13,300

17 2 9,450 22,75020 2 6,650 29,40024 2 4,000 33,40031 2 5,200 38,60031 2 3,000 41,60031 Adjusting 3 2,750 44,35031 Closing 4 44,350 — —

Account No. 51

Post.Item Ref. Debit Credit Debit Credit

2014 July 14 1 1,750 1,750

27 2 1,750 3,50031 Adjusting 3 175 3,67531 Closing 4 3,675 — —

Account No. 52

Post.Item Ref. Debit Credit Debit Credit

2014 July 31 Adjusting 3 2,400 2,400

31 Closing 4 2,400 — —

Account No. 53

Post.Item Ref. Debit Credit Debit Credit

2014 July 31 Adjusting 3 2,275 2,275

31 Closing 4 2,275 — —

DateBalance

Salary ExpenseAccount:

Account: Fees Earned

BalanceDate

BalanceDate

Account: Rent Expense

BalanceDate

Account: Supplies Expense

CHAPTER 4 Completing the Accounting Cycle

4-49© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Prob. 4–5A (Continued)

Account No. 54

Post.Item Ref. Debit Credit Debit Credit

2014 July 31 Adjusting 3 750 750

31 Closing 4 750 — —

Account No. 55

Post.Item Ref. Debit Credit Debit Credit

2014 July 31 Adjusting 3 375 375

31 Closing 4 375 — —

Account No. 59

Post.Item Ref. Debit Credit Debit Credit

2014 July 10 1 400 400

29 2 325 72531 2 675 1,40031 Closing 4 1,400 — —

Account: Depreciation Expense

BalanceDate

Account: Insurance Expense

BalanceDate

Account: Miscellaneous Expense

BalanceDate

CHAPTER 4 Completing the Accounting Cycle

4-50© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Prob. 4–5A (Continued)

3.

Debit CreditBalances Balances

Cash 32,450Accounts Receivable 16,450Supplies 3,800Prepaid Rent 4,800Prepaid Insurance 4,500Office Equipment 14,000Accumulated Depreciation 0Accounts Payable 1,300Salaries Payable 0Unearned Fees 5,500Share Capital—Ordinary 45,000Dividends 12,500Fees Earned 41,600Salary Expense 3,500Rent Expense 0Supplies Expense 0Depreciation Expense 0Insurance Expense 0Miscellaneous Expense 1,400

93,400 93,400

Unadjusted Trial BalanceJuly 31, 2014

DIAMOND CONSULTING

CHAPTER 4 Completing the Accounting Cycle

4-51© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Prob. 4–5A (Continued)5. Optional (Appendix)

Account Title Debit Credit Debit Credit Debit Credit Debit CreditCash 32,450 32,450 32,450Accounts Receivable 16,450 16,450 16,450Supplies 3,800 (b) 2,275 1,525 1,525Prepaid Rent 4,800 (e) 2,400 2,400 2,400Prepaid Insurance 4,500 (a) 375 4,125 4,125Office Equipment 14,000 14,000 14,000Accum. Depreciation (c) 750 750 750Accounts Payable 1,300 1,300 1,300Salaries Payable (d) 175 175 175Unearned Fees 5,500 (f) 2,750 2,750 2,750Share Capital—Ordinary 45,000 45,000 45,000Dividends 12,500 12,500 12,500Fees Earned 41,600 (f) 2,750 44,350 44,350Salary Expense 3,500 (d) 175 3,675 3,675Rent Expense (e) 2,400 2,400 2,400Supplies Expense (b) 2,275 2,275 2,275Depreciation Expense (c) 750 750 750Insurance Expense (a) 375 375 375Miscellaneous Expense 1,400 1,400 1,400

93,400 93,400 8,725 8,725 94,325 94,325 10,875 44,350 83,450 49,975Net profit 33,475 33,475

44,350 44,350 83,450 83,450

Financial PositionTrial BalanceDebit Credit

Trial Balance Comprehensive IncomeAdjustments

DIAMOND CONSULTINGEnd-of-Period Spreadsheet (Work Sheet)

For the Month Ended July 31, 2014Statement ofUnadjusted Adjusted Statement of

CHAPTER 4 Completing the Accounting Cycle

4-52© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Prob. 4–5A (Continued)

6. Page 3

Post.Ref. Debit Credit

2014 July 31 Insurance Expense 55 375

Prepaid Insurance 16 375Insurance expired.

31 Supplies Expense 53 2,275Supplies 14 2,275

Supplies used ($3,800 – $1,525).

31 Depreciation Expense 54 750Accumulated Depreciation 19 750

Equipment depreciation.

31 Salary Expense 51 175Salaries Payable 22 175

Accrued salaries.

31 Rent Expense 52 2,400Prepaid Rent 15 2,400

Rent expired.

31 Unearned Fees 23 2,750Fees Earned 41 2,750

Unearned fees earned ($5,500 – $2,750).

DateAdjusting Entries

JOURNAL

CHAPTER 4 Completing the Accounting Cycle

4-53© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Prob. 4–5A (Continued)

7.

Debit CreditBalances Balances

Cash 32,450Accounts Receivable 16,450Supplies 1,525Prepaid Rent 2,400Prepaid Insurance 4,125Office Equipment 14,000Accumulated Depreciation 750Accounts Payable 1,300Salaries Payable 175Unearned Fees 2,750Share Capital—Ordinary 45,000Dividends 12,500Fees Earned 44,350Salary Expense 3,675Rent Expense 2,400Supplies Expense 2,275Depreciation Expense 750Insurance Expense 375Miscellaneous Expense 1,400

94,325 94,325

Adjusted Trial BalanceJuly 31, 2014

DIAMOND CONSULTING

CHAPTER 4 Completing the Accounting Cycle

4-54© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Prob. 4–5A (Continued)

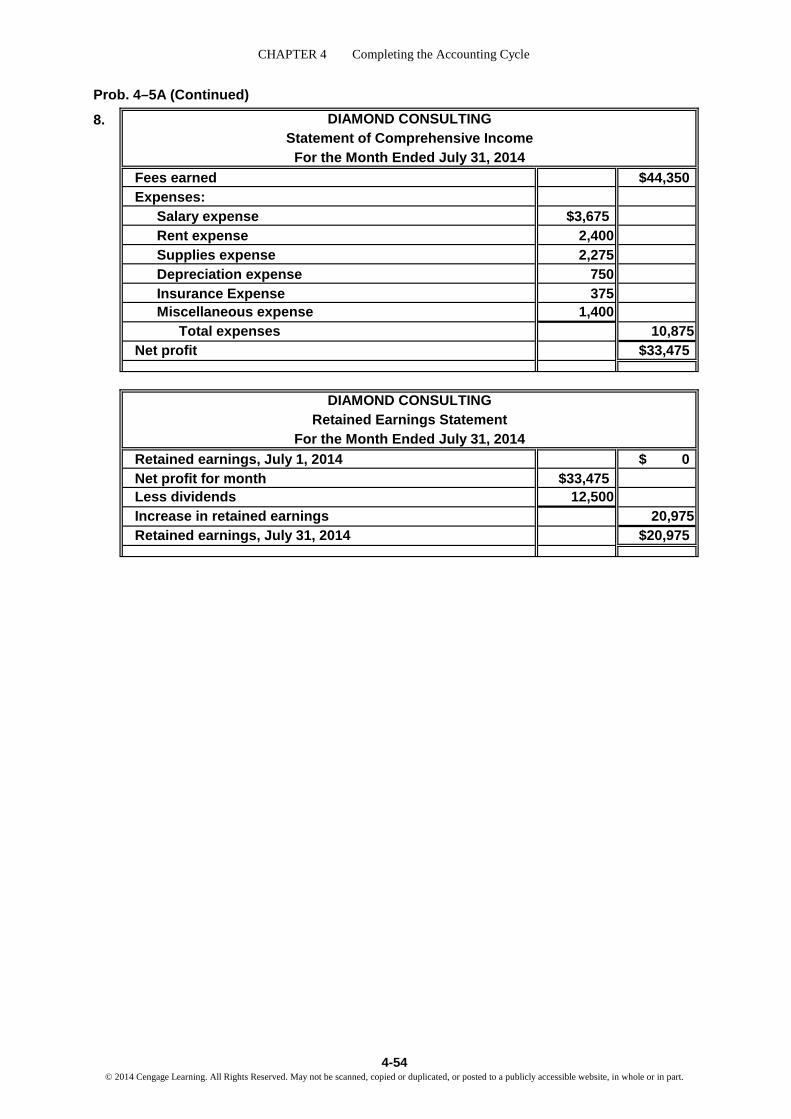

8.

Fees earned $44,350Expenses:

Salary expense $3,675Rent expense 2,400Supplies expense 2,275Depreciation expense 750Insurance Expense 375Miscellaneous expense 1,400

Total expenses 10,875Net profit $33,475

Retained earnings, July 1, 2014 $ 0Net profit for month $33,475Less dividends 12,500Increase in retained earnings 20,975Retained earnings, July 31, 2014 $20,975

DIAMOND CONSULTINGRetained Earnings Statement

For the Month Ended July 31, 2014

DIAMOND CONSULTINGStatement of Comprehensive Income

For the Month Ended July 31, 2014

CHAPTER 4 Completing the Accounting Cycle

4-55© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Prob. 4–5A (Continued)

Non-current assets: Equity:Property, plant, and equipment: Share capital—ordinary $45,000

Office equipment $14,000 Retained earnings 20,975Less accum. depreciation 750 Total equity $ 65,975

Total non-current assets $13,250Current assets: Current liabilities:

Prepaid insurance $4,125 Accounts payable $ 1,300Prepaid rent 2,400 Salaries payable 175Supplies 1,525 Unearned fees 2,750Accounts receivable 16,450 Total liabilities 4,225 Cash 32,450

Total current assets 56,950 Total assets $70,200 Total equity and liabilities $70,200

DIAMOND CONSULTINGStatement of Financial Position

July 31, 2014Assets Equity and Liabilities

CHAPTER 4 Completing the Accounting Cycle

4-56© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Prob. 4–5A (Concluded) 9. Page 4

Post.Ref. Debit Credit

2014 July 31 Fees Earned 41 44,350

Income Summary 34 44,350

31 Income Summary 34 10,875Salary Expense 51 3,675Rent Expense 52 2,400Supplies Expense 53 2,275Depreciation Expense 54 750Insurance Expense 55 375Miscellaneous Expense 59 1,400

31 Income Summary 34 33,475Retained Earnings 32 33,475

31 Retained Earnings 32 12,500Dividends 33 12,500

10.

Debit CreditBalances Balances

Cash 32,450Accounts Receivable 16,450Supplies 1,525Prepaid Rent 2,400Prepaid Insurance 4,125Office Equipment 14,000Accumulated Depreciation 750Accounts Payable 1,300Salaries Payable 175Unearned Fees 2,750Share Capital—Ordinary 45,000Retained Earnings 20,975

70,950 70,950

JOURNAL

July 31, 2014

Closing EntriesDate

DIAMOND CONSULTINGPost-Closing Trial Balance

CHAPTER 4 Completing the Accounting Cycle

4-57© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Prob. 4–1B

1.

Revenues:Fees earned $283,750Rent revenue 3,000

Total revenues $286,750Expenses:

Salaries and wages expense $147,000Advertising expense 86,800Utilities expense 30,000Travel expense 18,750Depreciation expense—equipment 4,550Depreciation expense—building 3,000Supplies expense 1,500Insurance expense 1,300Miscellaneous expense 5,875

Total expenses 298,775Net loss $ 12,025

2.

Retained earnings, July 1, 2013 $271,300Net loss for the year $12,025Add dividends 20,000Decrease in retained earnings 32,025Retained earnings, June 30, 2014 $239,275

LAST CHANCE COMPANYRetained Earnings Statement

For the Year Ended June 30, 2014

LAST CHANCE COMPANYStatement of Comprehensive Income

For the Year Ended June 30, 2014

CHAPTER 4 Completing the Accounting Cycle

4-58© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Prob. 4–1B (Continued)

3.

Non-current assets: Equity:Property, plant, and equipment: Share capital—ordinary $ 90,000

Land $ 80,000 Retained earnings 239,275Building $340,000 Total equity $ 329,275Less accum. depreciation 193,000 147,000Equipment $140,000 Current liabilities:Less accum. depreciation 59,000 81,000 Accounts payable $ 9,750

Total non-current assets $ 308,000 Salaries and wages payable 1,900Current assets: Unearned rent 1,500

Prepaid insurance $ 2,300 Total liabilities 13,150 Supplies 525Accounts receivable 26,500 Total equity and liabilities $342,425Cash 5,100

Total current assets 34,425 Total assets $342,425

LAST CHANCE COMPANYStatement of Financial Position

June 30, 2014Assets Equity and Liabilities

CHAPTER 4 Completing the Accounting Cycle

4-59© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Prob. 4–1B (Concluded)

4. 2014 June 30 Fees Earned 283,750

Rent Revenue 3,000Income Summary 286,750

30 Income Summary 298,775Salaries and Wages Expense 147,000Advertising Expense 86,800Utilities Expense 30,000Travel Expense 18,750Depreciation Expense—Equipment 4,550Depreciation Expense—Building 3,000Supplies Expense 1,500Insurance Expense 1,300Miscellaneous Expense 5,875

30 Retained Earnings 12,025Income Summary 12,025

30 Retained Earnings 20,000Dividends 20,000

5.

Debit CreditBalances Balances

Cash 5,100Accounts Receivable 26,500Prepaid Insurance 2,300Supplies 525Land 80,000Building 340,000Accumulated Depreciation—Building 193,000Equipment 140,000Accumulated Depreciation—Equipment 59,000Accounts Payable 9,750Salaries and Wages Payable 1,900Unearned Rent 1,500Share Capital—Ordinary 90,000Retained Earnings 239,275

594,425 594,425

LAST CHANCE COMPANYPost-Closing Trial Balance

June 30, 2014

CHAPTER 4 Completing the Accounting Cycle

4-60© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Prob. 4–2B1.

Revenues:Service fees $468,000Rent revenue 5,000

Total revenues $473,000Expenses:

Salaries expense $291,000Depreciation expense—equipment 17,500Rent expense 15,500Supplies expense 9,000Utilities expense 8,500Depreciation expense—buildings 6,600Repairs expense 3,450Insurance expense 3,000Miscellaneous expense 5,450

Total expenses 360,000Net profit $113,000

Retained earnings, November 1, 2013 $195,000Net profit for the year $113,000Less dividends 20,000Increase in retained earnings 93,000Retained earnings, October 31, 2014 $288,000

THE GORMAN GROUPRetained Earnings Statement

For the Year Ended October 31, 2014

THE GORMAN GROUPStatement of Comprehensive IncomeFor the Year Ended October 31, 2014

CHAPTER 4 Completing the Accounting Cycle

4-61© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Prob. 4–2B (Continued)

Non-current assets: Equity:Property, plant, and equipment: Share capital—ordinary $ 25,000

Land $ 75,000 Retained earnings 288,000Buildings $250,000 Total equity 313,000$ Less accum. depreciation 117,200 132,800Equipment $240,000 Current liabilities:Less accum. depreciation 151,700 88,300 Accounts payable $ 33,300

Total non-current assets 296,100$ Salaries payable 3,300Current assets: Unearned rent 1,500

Prepaid insurance $ 9,500 Total liabilities 38,100 Supplies 6,350Accounts receivable 28,150 Total equity and liabilities $351,100Cash 11,000

Total current assets 55,000 Total assets $351,100

THE GORMAN GROUPStatement of Financial Position

October 31, 2014Assets Equity and Liabilities

CHAPTER 4 Completing the Accounting Cycle

4-62© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Prob. 4–2B (Concluded)

2. 2014 Oct. 31 Service Fees 468,000

Rent Revenue 5,000Income Summary 473,000

31 Income Summary 360,000Salaries Expense 291,000Depreciation Expense—Equipment 17,500Rent Expense 15,500Supplies Expense 9,000Utilities Expense 8,500Depreciation Expense—Buildings 6,600Repairs Expense 3,450Insurance Expense 3,000Miscellaneous Expense 5,450

31 Income Summary 113,000Retained Earnings 113,000

31 Retained Earnings 20,000Dividends 20,000

3. $135,000 ($115,000 + $20,000) net profit. The $115,000 increase is caused by the Net profit of $135,000 less the $20,000 dividends.

Closing Entries

CHAPTER 4 Completing the Accounting Cycle

4-63© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

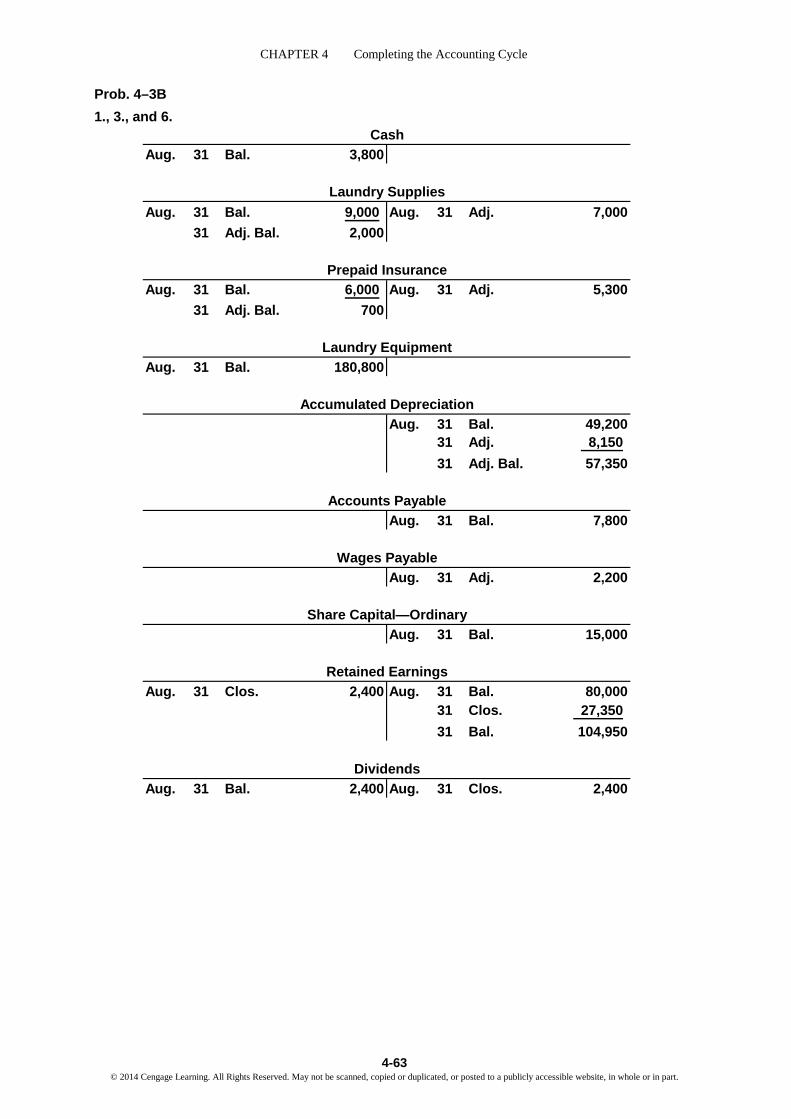

Prob. 4–3B 1., 3., and 6.

Aug. 31 Bal. 3,800

Aug. 31 Bal. 9,000 Aug. 31 Adj. 7,00031 Adj. Bal. 2,000

Aug. 31 Bal. 6,000 Aug. 31 Adj. 5,30031 Adj. Bal. 700

Aug. 31 Bal. 180,800

Aug. 31 Bal. 49,20031 Adj. 8,15031 Adj. Bal. 57,350

Aug. 31 Bal. 7,800

Aug. 31 Adj. 2,200

Aug. 31 Bal. 15,000

Aug. 31 Clos. 2,400 Aug. 31 Bal. 80,00031 Clos. 27,35031 Bal. 104,950

Aug. 31 Bal. 2,400 Aug. 31 Clos. 2,400

Cash

Laundry Supplies

Prepaid Insurance

Laundry Equipment

Dividends

Accumulated Depreciation

Accounts Payable

Share Capital—Ordinary

Retained Earnings

Wages Payable

CHAPTER 4 Completing the Accounting Cycle

4-64© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Prob. 4–3B (Continued)

Aug. 31 Clos. 220,650 Aug. 31 Clos. 248,000Clos. 27,350

Aug. 31 Clos. 248,000 Aug. 31 Bal. 248,000

Aug. 31 Bal. 135,800 Aug. 31 Clos. 138,00031 Adj. 2,20031 Adj. Bal. 138,000

Aug. 31 Bal. 43,200 Aug. 31 Clos. 43,200

Aug. 31 Bal. 16,000 Aug. 31 Clos. 16,000

Aug. 31 Adj. 8,150 Aug. 31 Clos. 8,150

Aug. 31 Adj. 7,000 Aug. 31 Clos. 7,000

Aug. 31 Adj. 5,300 Aug. 31 Clos. 5,300

Aug. 31 Bal. 3,000 Aug. 31 Clos. 3,000Miscellaneous Expense

Income Summary

Laundry Revenue

Laundry Supplies Expense

Wages Expense

Rent Expense

Utilities Expense

Depreciation Expense

Insurance Expense

CHAPTER 4 Completing the Accounting Cycle

4-65© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Prob. 4–3B (Continued)2. Optional (Appendix)

Account Title Debit Credit Debit Credit Debit Credit Debit CreditCash 3,800 3,800 3,800Laundry Supplies 9,000 (c) 7,000 2,000 2,000Prepaid Insurance 6,000 (d) 5,300 700 700Laundry Equipment 180,800 180,800 180,800Accum. Depreciation 49,200 (b) 8,150 57,350 57,350Accounts Payable 7,800 7,800 7,800Wages Payable (a) 2,200 2,200 2,200Share Capital—Ordinary 15,000 15,000 15,000Retained Earnings 80,000 80,000 80,000Dividends 2,400 2,400 2,400Laundry Revenue 248,000 248,000 248,000Wages Expense 135,800 (a) 2,200 138,000 138,000Rent Expense 43,200 43,200 43,200Utilities Expense 16,000 16,000 16,000Depreciation Expense (b) 8,150 8,150 8,150Laundry Supplies Exp. (c) 7,000 7,000 7,000Insurance Expense (b) 5,300 5,300 5,300Miscellaneous Expense 3,000 3,000 3,000

400,000 400,000 22,650 22,650 410,350 410,350 220,650 248,000 189,700 162,350Net profit 27,350 27,350

248,000 248,000 189,700 189,700

Financial PositionTrial BalanceDebit Credit

Trial Balance Comprehensive IncomeAdjustments

LA MESA LAUNDRYEnd-of-Period Spreadsheet (Work Sheet)

For the Year Ended August 31, 2014Statement ofUnadjusted Adjusted Statement of

CHAPTER 4 Completing the Accounting Cycle

4-66© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Prob. 4–3B (Continued)

3. 2014 Aug. 31 Wages Expense 2,200

Wages Payable 2,200Accrued wages.

31 Depreciation Expense 8,150Accumulated Depreciation 8,150

Equipment depreciation.

31 Laundry Supplies Expense 7,000Laundry Supplies 7,000

Supplies used ($9,000 – $2,000).

31 Insurance Expense 5,300Prepaid Insurance 5,300

Insurance expired.

4.

Debit CreditBalances Balances

Cash 3,800Laundry Supplies 2,000Prepaid Insurance 700Laundry Equipment 180,800Accumulated Depreciation 57,350Accounts Payable 7,800Wages Payable 2,200Share Capital—Ordinary 15,000Retained Earnings 80,000Dividends 2,400Laundry Revenue 248,000Wages Expense 138,000Rent Expense 43,200Utilities Expense 16,000Depreciation Expense 8,150Laundry Supplies Expense 7,000Insurance Expense 5,300Miscellaneous Expense 3,000

410,350 410,350

LA MESA LAUNDRYAdjusted Trial Balance

August 31, 2014

Adjusting Entries

CHAPTER 4 Completing the Accounting Cycle

4-67© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Prob. 4–3B (Continued)

5.

Laundry revenue $248,000Expenses:

Wages expense $138,000Rent expense 43,200Utilities expense 16,000Depreciation expense 8,150Laundry supplies expense 7,000Insurance expense 5,300Miscellaneous expense 3,000

Total expenses 220,650Net profit $ 27,350

Retained earnings, September 1, 2013 $ 80,000Net profit for the year $27,350Less dividends 2,400Increase in retained earnings 24,950Retained earnings, August 31, 2014 $104,950

Retained Earnings StatementFor the Year Ended August 31, 2014

LA MESA LAUNDRYStatement of Comprehensive IncomeFor the Year Ended August 31, 2014

LA MESA LAUNDRY

CHAPTER 4 Completing the Accounting Cycle

4-68© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Prob. 4–3B (Continued)

Non-current assets: Equity:Property, plant, and equipment: Share capital—ordinary $ 15,000

Laundry equipment $180,800 Retained earnings 104,950Less accum. depreciation 57,350 Total equity 119,950$

Total non-current assets 123,450$ Current assets: Current liabilities:

Prepaid insurance $ 700 Accounts payable $ 7,800Laundry supplies 2,000 Wages payable 2,200Cash 3,800 Total liabilities 10,000

Total current assets 6,500 Total assets $129,950 Total equity and liabilities $129,950

LA MESA LAUNDRYStatement of Financial Position

August 31, 2014Assets Equity and Liabilities

CHAPTER 4 Completing the Accounting Cycle

4-69© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Prob. 4–3B (Concluded)

6. 2014 Aug. 31 Laundry Revenue 248,000

Income Summary 248,000

31 Income Summary 220,650Wages Expense 138,000Rent Expense 43,200Utilities Expense 16,000Depreciation Expense 8,150Laundry Supplies Expense 7,000Insurance Expense 5,300Miscellaneous Expense 3,000

31 Income Summary 27,350Retained Earnings 27,350

31 Retained Earnings 2,400Dividends 2,400

7.

Debit CreditBalances Balances

Cash 3,800Laundry Supplies 2,000Prepaid Insurance 700Laundry Equipment 180,800Accumulated Depreciation 57,350Accounts Payable 7,800Wages Payable 2,200Share Capital—Ordinary 15,000Retained Earnings 104,950

187,300 187,300

LA MESA LAUNDRYPost-Closing Trial Balance

August 31, 2014

Closing Entries

CHAPTER 4 Completing the Accounting Cycle

4-70© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

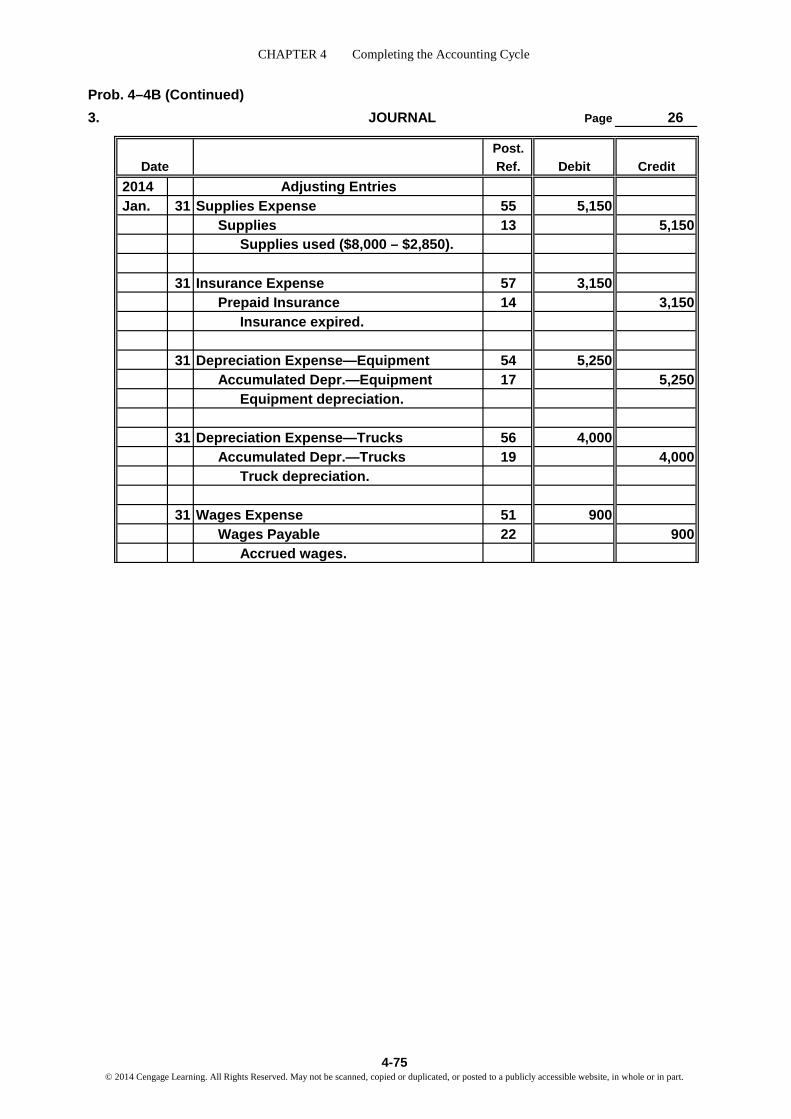

Prob. 4–4B1., 3., and 6.

Account No. 11

Post.Item Ref. Debit Credit Debit Credit

2014 Jan. 31 Balance 13,100

Account No. 13

Post.Item Ref. Debit Credit Debit Credit

2014 Jan. 31 Balance 8,000

31 Adjusting 26 5,150 2,850

Account No. 14

Post.Item Ref. Debit Credit Debit Credit

2014 Jan. 31 Balance 7,500

31 Adjusting 26 3,150 4,350

Account No. 16

Post.Item Ref. Debit Credit Debit Credit

2014 Jan. 31 Balance 113,000

Account No. 17

Post.Item Ref. Debit Credit Debit Credit

2014 Jan. 31 Balance 12,000

31 Adjusting 26 5,250 17,250

Account No. 18

Post.Item Ref. Debit Credit Debit Credit

2014 Jan. 31 Balance 90,000

Account: Accumulated Depreciation—Equipment

BalanceDate

Account: Trucks

BalanceDate

Account: Prepaid Insurance

BalanceDate

Account: Equipment

BalanceDate

BalanceDate

DateBalance

CashAccount:

Account: Supplies

CHAPTER 4 Completing the Accounting Cycle

4-71© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Prob. 4–4B (Continued)

Account No. 19

Post.Item Ref. Debit Credit Debit Credit

2014 Jan. 31 Balance 27,100

31 Adjusting 26 4,000 31,100

Account No. 21

Post.Item Ref. Debit Credit Debit Credit

2014 Jan. 31 Balance 4,500

Account No. 22

Post.Item Ref. Debit Credit Debit Credit

2014 Jan. 31 Adjusting 26 900 900

Account No. 31

Post.Item Ref. Debit Credit Debit Credit

2014 Jan. 31 Balance 30,000 30,000

Account No. 32

Post.Item Ref. Debit Credit Debit Credit

2014 Jan. 31 Balance 96,400

31 Closing 27 46,150 142,55031 Closing 27 3,000 139,550

Account No. 33

Post.Item Ref. Debit Credit Debit Credit

2014 Jan. 31 Balance 3,000

31 Closing 27 3,000 — —

BalanceDate

Account: Share Capital—Ordinary

BalanceDate

Account: Retained Earnings

Account: Wages Payable

BalanceDate

Account: Dividends

BalanceDate

BalanceDate

DateBalance

Accumulated Depreciation—TrucksAccount:

Account: Accounts Payable

CHAPTER 4 Completing the Accounting Cycle

4-72© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Prob. 4–4B (Continued)

Account No. 34

Post.Item Ref. Debit Credit Debit Credit

2014 Jan. 31 Closing 27 155,000 155,000

31 Closing 27 108,850 46,15031 Closing 27 46,150 — —

Account No. 41

Post.Item Ref. Debit Credit Debit Credit

2014 Jan. 31 Balance 155,000

31 Closing 27 155,000 — —

Account No. 51

Post.Item Ref. Debit Credit Debit Credit

2014 Jan. 31 Balance 72,000

31 Adjusting 26 900 72,90031 Closing 27 72,900 — —

Account No. 52

Post.Item Ref. Debit Credit Debit Credit

2014 Jan. 31 Balance 7,600

31 Closing 27 7,600 — —

Account No. 53

Post.Item Ref. Debit Credit Debit Credit

2014 Jan. 31 Balance 5,350

31 Closing 27 5,350 — —

Income SummaryAccount:

Account: Service Revenue

BalanceDate

DateBalance

BalanceDate

Account: Wages Expense

BalanceDate

Account: Rent Expense

BalanceDate

Account: Truck Expense

CHAPTER 4 Completing the Accounting Cycle

4-73© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Prob. 4–4B (Continued)

Account No. 54

Post.Item Ref. Debit Credit Debit Credit

2014 Jan. 31 Adjusting 26 5,250 5,250

31 Closing 27 5,250 — —

Account No. 55

Post.Item Ref. Debit Credit Debit Credit

2014 Jan. 31 Adjusting 26 5,150 5,150

31 Closing 27 5,150 — —

Account No. 56

Post.Item Ref. Debit Credit Debit Credit

2014 Jan. 31 Adjusting 26 4,000 4,000

31 Closing 27 4,000 — —

Account No. 57

Post.Item Ref. Debit Credit Debit Credit

2014 Jan. 31 Adjusting 26 3,150 3,150

31 Closing 27 3,150 — —

Account No. 59

Post.Item Ref. Debit Credit Debit Credit