Embed Size (px)

DESCRIPTION

Chapter 17. Estate Planning: Saving Your Heirs Money and Headaches. Learning Objectives. Understand the importance and the process of estate planning. Calculate and avoid estate taxes. Draft a will and understand its purpose in estate planning. Avoid probate. The Estate Planning Process. - PowerPoint PPT Presentation

Citation preview

PART 5:LIFE CYCLE ISSUES

Chapter 17

Estate Planning: Saving Your Heirs Money and Headaches

17-2

Learning Objectives

Understand the importance and the process of estate planning.

Calculate and avoid estate taxes. Draft a will and understand its purpose in

estate planning. Avoid probate.

17-3

The Estate Planning Process

Step 1: Determine the Value of Your Estate Determine the value of your assets. Use the death benefit, not cash value, to

determine value of life insurance. Include employer-sponsored death benefits. In 2006, the first $2 million of an estate can

be passed tax-free.

17-4

The Estate Planning Process

Step 2: Choose Your Heirs andDecide What They Receive

Once you know what you have, you can decide who’s going to get it.

In addition to a spouse, consider the special needs of your dependents.

17-5

The Estate Planning Process

Step 3: Determine the CashNeeds of the Estate

Before distributing property to heirs, must pay medical costs, funeral expenses, legal fees, outstanding debt, and taxes.

Use liquid funds to cover tax needs.

17-6

The Estate Planning Process

Step 4: Select and Implement YourEstate Planning Techniques

Decide which estate planning tools are most appropriate to achieve your goals.

You may need a will, a durable power of attorney, joint ownership, trusts, life insurance, and gifts.

17-7

Understanding and Avoiding Estate Taxes

The IRS charges estate taxes, then issues an estate tax credit.

Unified tax credit – nullifies the taxes on the first $2 million of an individual’s estate.

Above the $2 million threshold, the taxes in 2006 are 46%. – 45% tax on estate above the threshold from 2007-

2009.

17-8

Understanding and Avoiding Estate Taxes

One goal of the Tax Relief Act of 2001 was to repeal estate taxes.– Since 2002, estate taxes began to disappear.– By 2010, estate taxes will be gone.– Without action by lawmakers, estate taxes will

reappear in 2011. Move towards estate tax planning as net worth

climbs above the tax-free transfer threshold.

17-9

Gift Taxes

Gifts transfer wealth prior to death, reducing the taxable value of the estate.– The recipient is not taxed, either!

Give away $11,000 annually, per recipient,tax-free.

The gift tax and the estate tax work together with a total lifetime tax-exempt ($2 million) limit on gifts over the $11,000.

17-10

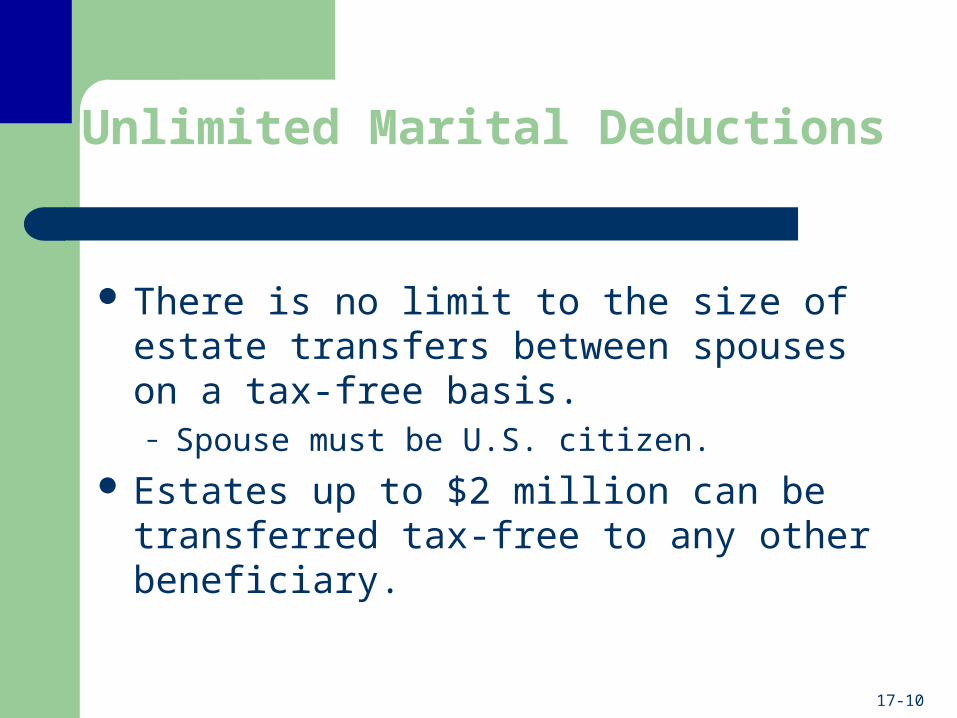

Unlimited Marital Deductions

There is no limit to the size of estate transfers between spouses on a tax-free basis. – Spouse must be U.S. citizen.

Estates up to $2 million can be transferred tax-free to any other beneficiary.

17-11

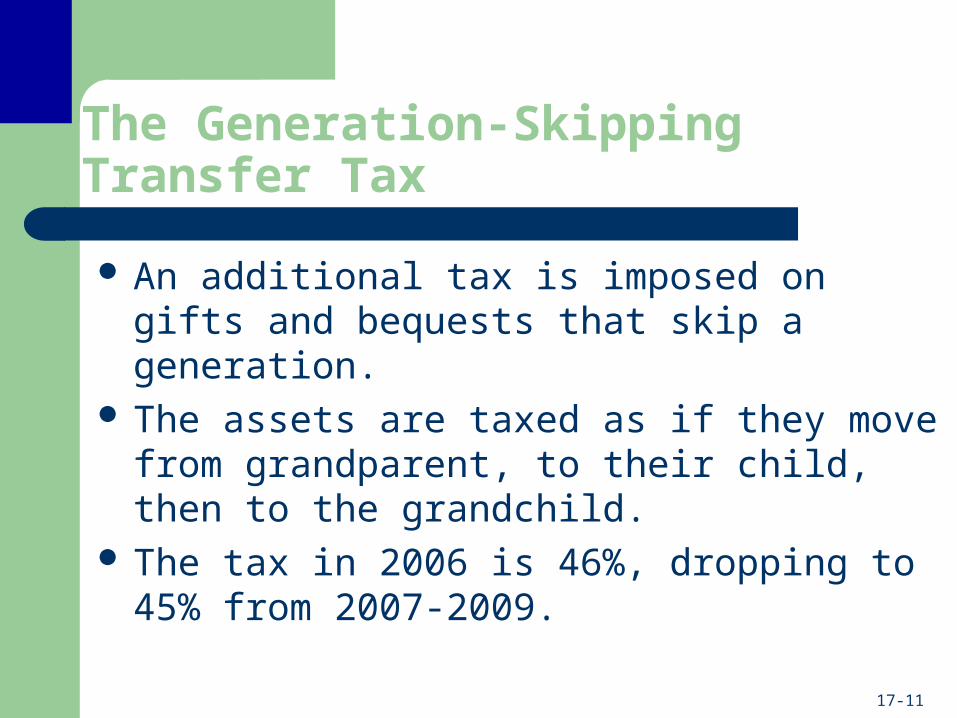

The Generation-Skipping Transfer Tax

An additional tax is imposed on gifts and bequests that skip a generation.

The assets are taxed as if they move from grandparent, to their child, then to the grandchild.

The tax in 2006 is 46%, dropping to 45% from 2007-2009.

17-12

Calculating Estate Taxes

Start by calculating your gross estate. Next calculate your taxable estate.

– Subtract funeral and estate expenses, debts, taxes, and allowable deductions from the gross estate.

Then calculate the gift-adjusted taxable estate.

17-13

Wills

A legal document that describes how to transfer your property to others.

Designate:– Beneficiaries – those who are willed property.– An executor – personal representative who will

carry out the will’s provisions.– A guardian – who will care for children under the

age of 18.

17-14

Wills and Probate

Probate is the legal process of distributing an estate’s assets.

Probate validates the will. Probate court appoints an executor, generally the

one designated in the will. Once the assets have been distributed and the taxes

paid, a report is filed with the court, and the estate is closed.

17-15

Wills and Probate

Advantage Validate the will – allow for

challenges and make sure it is the last will and testament of the deceased.

Disadvantages– Numerous expenses –

legal fees, executor fees, court costs.

– Slow, time consuming process, especially if there are challenges or tax problems.

17-16

Wills and Estate Planning

Why do you need a will?

A Will Can – Assure that a child with special

needs is taken care of.– Make sure property that isn’t co-

owned or in trusts is transferred according to your wishes.

– Make special gifts or bequeaths.

Without a Will– The court will appoint a

guardian for any children.

– The court appoints an administrator to distribute your assets.

17-17

Writing a Will

Although handwritten and oral wills are accepted in some states, this is not a good idea.

Have a lawyer draw up your will or review it. Wills need to be signed and witnessed. Be sure to update it and store in a safe

place.

17-18

Writing a Will

A will should contain:– Introductory statement.– Payment of debt and taxes clause.– Disposition of property clause.– Appointment clause.– Common disaster clause.– Attestation and witness clause.

17-19

Updating or Changing a Will – The Codicil

A codicil is an attachment to a will that alters or amends a portion of the will. – Make sure your will conforms to your present situation.– Substantial changes warrant a new will.

A codicil should be drawn up by a lawyer, witnessed, and attached to the will.

17-20

Letter of Last Instructions

A letter of last instructions is generally written to the surviving spouse.

It is not a legally binding document. It provides information and directions with

respect to the execution of the will.

17-21

Letter of Last Instructions

The letter of last instructions may contain:– Location of the will, legal documents– Location of financial assets– Names of those to notify of the death– Listing of personal property– Funeral and burial instructions– Organ donations

17-22

Selecting an Executor

An executor has a dual role:– Making sure your wishes are carried out.– Managing your property until the estate is passed

on to your heirs.

17-23

Selecting an Executor

The executor will:– Deal with personal matters– Pay taxes – Manage the financial matters of the estate– Distribute assets– Make a final accounting to the courts

17-24

Other Estate Planning Documents

A durable power of attorney provides for someone to act in your place should you become mentally incapacitated.

A living will allows you to state your wishes regarding medical treatment in the event of terminal illness or injury.– The health care proxy designates someone to

make health care decisions for you.

17-25

Avoiding Probate

Probate is essential to validate your will and ensure your provisions are carried out. It can also be time consuming and expensive.

It is a good idea to avoid probate, and the simplest ways to do so include:– Joint ownership– Gifts– Trusts

17-26

Joint Ownership

Jointly-owned assets transfer to the surviving owner without probate.

3 forms of joint ownership:– Joint tenancy with rights of survivorship –

ownership passes to survivor, bypasses the will.– Tenancy on common – deceased owner’s shares

go to estate.– Community property – surviving spouse receives ½

of all property acquired during the marriage.

17-27

Gifts

Do not go through probate. Reduce taxable value of estate, allow you to help

heirs while you are alive. Are a good way to transfer property that grows in

value. Disadvantages include the fact that you may need

the assets or that they are squandered. No limits on gifts to a charity.

17-28

Trusts

A legal entity that holds and manages an asset for another person.

Is created when an individual, a grantor, transfers property to a trustee for the benefit of one or more beneficiaries.

– The trustee can be an individual, an investment firm, or a bank.

Any asset can be placed in a trust.

17-29

Trusts

Why use a trust?– Trusts avoid probate.– Trusts are more difficult to challenge in court.– Trusts can reduce estate taxes.– Trusts allow for professional management.– Trusts can hold money for a child with special needs or

until a child reaches maturity.– Trusts can ensure that children from a previous

marriage will receive an inheritance.

17-30

Living Trusts

Revocable Living Trusts Place assets in trust

while alive, withdraw them later if you wish.

You retain title and have control over assets.

No tax advantages.

Irrevocable Living Trusts Trust is permanent. It becomes a legal

entity, paying taxes on gains produced.

Not part of estate, bypasses probate, no estate taxes.

17-31

Testamentary Trusts

A testamentary trust is created by a will. – It exists once probate has been completed.

Common types:– Standard Family Trusts – also known as A-B Trusts,

Credit-Shelter Trusts and Unified Credit Trusts– Qualified Terminable Interest Property Trust

(Q-TIP)– Sprinkling Trusts

annual income over $100,000

70% completed college

4 times more likely to hold postgraduate degrees

married couples head 85% of wealthy households

17-32

Testamentary Trusts

Standard Family Trusts – reduce estate taxes when one spouse dies before the other. – Assets go directly into the trust, no taxes are

imposed.– Remaining spouse uses the assets, and upon

death, the assets go to the children tax-free.

17-33

Testamentary Trusts

Qualified Terminable Interest Property Trust – ability to direct income from the trust to spouse, then upon spouse’s death, to whomever is selected.– This trust keeps the estate from getting into the

hands of your spouse’s future husband or wife, assets go to the children.

annual income over $100,000

70% completed college

4 times more likely to hold postgraduate degrees

married couples head 85% of wealthy households

17-34

Testamentary Trusts

Sprinkling Trusts – distributes income according to need rather than a pre-set formula.– Trustee uses discretion to distribute the income.– Trustee “sprinkles” income to those who need

it.

annual income over $100,000

70% completed college

4 times more likely to hold postgraduate degrees

married couples head 85% of wealthy households

17-35

Estate Planning

Checklist 17.1 Do you and your family know…

– Location of your will, power of attorney, and living will?– The name of your attorney and accountant?– Where to find your letter of last instructions?– Location of safety deposit box?– Whereabouts of deeds and titles to property?– Site of your investments?– All account numbers?– Last year’s income tax return?– Pension and retirement benefits?

17-36

A Last Word on Estate Planning

Many put off estate planning because it is complex and deals with death.

Go to a professional – don’t do your own estate planning.

Make sure your family knows where your estate planning documents are.

![[PPT]Microbiology Chapter 17 - Austin Community College … ppt/ch 17 ppt.ppt · Web viewMicrobiology Chapter 17 Chapter 17 (Cowan): Diagnosing infections This is wrap up chapter](https://img.pdfslide.us/doc/110x75/5aee76d27f8b9a572b8cc178/pptmicrobiology-chapter-17-austin-community-college-pptch-17-pptpptweb.jpg)